about a theoretical framework for analyzing the … · i. financial dualism under this heading, we...

TRANSCRIPT

1

ABOUT A THEORETICAL FRAMEWORK FOR ANALYZING THE DEMAND FOR INFORMAL

FINANCE: A NECESSITY FOR MICROFINANCE INSTITUTIONS

Umuhire Pierre-Germain∗

Paper presented at the Second European Research Conference on Microfinance Groningen, the Netherlands

June 16 – 18, 2011

Université Catholique de Louvain IMMAQ - IRES - Place Montesquieu, 3

1348 Louvain-la-Neuve

∗PhD. Candidate at UCL (IMMAQ-IRES) and member of the CIRTES. E-mail: [email protected]

2

Abstract

Even though the emergence of microcredit in the mid-seventies with the objective of fighting

against financial exclusion could have raised expectations about the probable demise of the

informal finance, recent empirical evidence suggests that this scenario has not been taking place.

Informal finance tends to persist in the city of developing countries despite the rise of

microfinance services. Therefore, the objective of this paper is to look into the toolbox of

economics in order to identify analytical tools that can help microfinance institutions obtaining a

better understanding of the financial behavior of people in informal finance. Drawing from the

development economics literature, this paper highlights a number of theoretical arguments that

may explain the resilience of informal finance. These include the information asymmetry argument,

the transactions costs argument and the contractual risks argument. While these theoretical arguments

focus exclusively on credit, empirical evidence tends to show that people in informal finance are

also looking for saving mechanisms, insurance … All these elements need to be accounted for

while analyzing the demand for informal finance. In this paper, it is especially argued that social

relations do also play a non-negligible role in explaining the demand for informal finance. Putting

together all these analytical tools, we obtain a theoretical framework allowing microfinance

institutions to comprehend the rationale of demand for financial services of the people in

informal finance in order to serve them appropriately.

Key words: Informal finance, microfinance, information asymmetry, transaction costs, contractual risks, social effects

JEL classification: D12, D14, O17, O16, O55,

3

Introduction

In a survey conducted with 398 micro-entrepreneurs operating in Ouagadougou, the capital city

of Burkina Faso (West Africa), I found that enrollment in banks and microfinance (cooperatives)

was respectively about 20% and 34% while at least 85% of the respondents declared to be

involved in informal finance. More surprisingly 41% of the respondents reported to be active in

both informal and formal finance.1 This finding is challenging for, at least, two reasons. First, it

suggests that the use of informal finance is not necessarily triggered by the lack of access to formal markets;

an idea that prevailed in economic literature till recently. Second the persistence of informal

finance constitutes a challenge for microfinance institutions whose prime objective is to fight

against financial exclusion by serving, among others, people in informal finance (Brau & Woller,

2004). Hence, microfinance institutions should wonder whether the resilience of informal finance

reflects their own failure to meet the needs of people in informal finance or if there are

alternative explanations. The objective of this paper is, therefore, to search in the toolbox of

economics in order to identify analytical tools that can help us understanding the rationale of the

demand for informal finance in the cities of developing countries despite the rise of formal

microfinance services. Such a research effort is important for microfinance institutions which

ought to understand why people resort to informal finance if they are to serve them

appropriately.

To begin with, let us note that the economic analysis of financial informality has been influenced

to a great extent by the debates around informal employment. The first studies on informality

were initiated by the pioneers of development economics such as Lewis (Lewis, 1954; 1955; 1972;

1979), Fei and Ranis (1964) Harris and Todaro (1970) to name just a few. These studies laid

down a theoretical framework based on dualistic models aimed at showing how labor markets in

developing countries are segmented in two non-competing sectors; namely the formal (modern) sector

and the informal (traditional) sector. A common feature of these studies lies in the fact that they

present informality as being made of workers (self-employed) rationed out of good jobs in the

more desirable formal sector. Therefore, informality is seen as an option last resort. Besides these

dualistic approaches, there are approaches that depict the informal sector in a positive manner (De

Soto , 1989; Maloney W. F., 2003; 2004). These approaches consider informality as a desirable

alternative to the formal sector.

1 Other recent field studies have also revealed the fact that individuals in informal financial markets may also be active in formal financial markets (Chamlee-Wright, 2002; Collins , Morduch, Rutherford, & Ruthven, 2009; Guérin, Venkatasubramanian, & Héliès, 2009; Guérin, Morvant-Roux , & Servet , 2010)

4

As mentioned above, the economic theories of informal financial markets draw largely from

these initial debates around the informal labor market. Like in the above debates, two concurrent

views can be highlighted. On one side, some theories present informal finance as a makeshift or a

solution of last resort for those excluded formal markets. Theoretical arguments raised by the

proponents of this view include the financial repression argument (McKinnon, 1973 ; 1976;

Shaw, 1973) and the information asymmetry argument (Stiglitz & Weiss, 1981). On the other

side, there are theoretical arguments that put forward the attractiveness of the informal finance in

terms of transaction costs (Chung, 1995; Barham, Boucher, & Carter, 1996) or lower contractual

risks (Boucher, Carter, & Guirkinger, 2008; Guirkinger, 2008). It is also contended that some

informal financial practices offer more effective commitment mechanism for individual with

time-inconsistent preferences (Gugerty, 2007). However, it can be shown that these two views

are not necessarily mutually exclusive given that the transaction costs argument can also be

consistent with financial exclusion. Moreover, we extend the above theoretical framework by

suggesting another argument that is susceptible of explaining the demand for financial services,

and therefore, to shed more light on the conditions underlying the persistence of informal

financial practices. The argument suggested in this section is in terms of social effect.

The remaining of this paper is organized in five sections. The next section presents a discussion

of the economic theories of informal finance and show how these theories have been largely

influenced by the initial debates around the models of market segmentation. The second section

highlights the lessons and the limits of these theoretical approaches with respect to the rationale

of the persistence of the demand for informal finance. The third section introduces the social

effect argument while the fourth section discusses some descriptive statistics which show the

importance of social effects in informal finance. The last section summarizes the main

conclusions of the paper and indicates venues for future research.

I. Theoretical foundations of financial informality

As mentioned above, economic theories on informal finance were largely influenced by the initial

debates around informal employment in developing countries. However, while the early theories

of informality tried to understand why people go to eke out a living in informal activities, the

economic theories of financial informality focused on the analysis the demand for informal

finance. The main focus is no longer the rationale of the supply of labor in informal sector, but

5

on the rationale of the demand for informal financial services. Nevertheless, despite this shift in

focus, the theories on informal finance follow exactly the same analytical framework as the initial

economic theories on informal labor.

i. Financial dualism

Under this heading, we regroup theoretical arguments that present informal finance as a residual

market or a makeshift for those who are unable to access formal financial markets. Two dualistic

arguments are highlighted; namely the financial repression argument and the information

asymmetry argument.

(a) The financial repression argument

The first argument draws from the financial repression theory (McKinnon, 1973 ; 1976; Shaw,

1973) which views informal finance as a result of State intervention in financial markets through

a set of regulations, laws, as well as non-market restrictions.2 Financial repression include policies

such as interest rate ceilings, high liquidity ratio requirements, high bank reserve requirements,

capital controls, restrictions on market entry, credits controls as well as nationalization of banks

(government ownership or domination of banks). All these policies result in an inefficient

allocation of capital as they discourage savings while reducing the supply of credit by banks. As a

consequence, some people are prevented from accessing credit, even though without these

restrictions they would qualify for obtaining bank loans. The resulting unsatisfied demand for

loans is absorbed by the unorganized informal money market which acts as a residual market

such as to allow financial markets to clear (Van Wijnbergen, 1983). Ultimately, financial

repression affects adversely economic growth due to its inefficient resources allocation.3

(b) The information asymmetry argument

While the financial repression theory insists on the exogenous origin of credit restrictions and puts

the blame on State interventions, Stiglitz and Weiss (1981) point the finger to endogenous markets

2 It is often argued that financial repression constitutes an implicit fiscal policy through which the Government can easily get access to cheap financial resources. For instance, a system of high liquidity ratios (or high bank reserves) increases the base money and, thereby, the seigniorage revenue. In the same way, interest rates ceiling help reducing the fiscal burden for highly indebted Government while direct control of credit allocation allows Government to ensure stable provision of capital to strategic economic sectors. 3 Financial repression may have some similarities with the De Soto legalist argument but the two arguments are quite different. Indeed, both arguments point to the existence of unnecessarily and excessive regulations interfering with the smooth running of the competitive markets to justify the rise of informality. However, while De Soto views informality as a deliberate choice, the financial repression theory views the decision to resort to informal finance as a solution of last resort in the absence of anything better. It is rather a lack of choice than a deliberate choice.

6

failures. These authors show how – in a context of limited liability4- information asymmetries

between the borrower and the lender can lead to credit rationing i.e. situations where no feasible

loan contract is offered to the borrower. Such situations arise when (1) some borrowers receive loans

while others who appear to be identical do not; even if they offer to pay a higher interest rate; (2)

borrowers receive loans of less value than they applied for and lastly, (3) identifiable groups of

borrowers are unable to obtain loans at any interest rate.5 The information asymmetry argument

is explained below.

In a world without information asymmetries, the bank or the lender would be able to identify the

risk profile of every borrower. The figure 1 below depicts such a situation. If there is no risk of

default, all borrowers would face a horizontal supply curve (S0) and would, therefore, be able to

secure any amount of loan at the prevailing contract (market) rate (rc). However, it is often the

case that the probability of default is not zero. Considering a market with two types of perfectly

observable risk profiles, it is possible for lenders to establish contracts tailored to each borrower

by charging higher rates to the riskier borrowers. The result is the existence of different supply

schedules (S1 and S2) for each risk profile. At the end of day two equilibrium rates (r1 and r2) will

prevail on the market. In this case, we have separating equilibria and the interest rate is used to

discriminate between high risk and low risk borrowers.

Figure 1: Individual loan supply curves6

Adapted by the Author from Barham et al. (1996)

4 Limited liability implies that the borrower bears no responsibility to pay out of his pocket in case the returns generated by his project are not enough to meet his debt obligations. 5 This is a rather a broad approach to the concept of credit rationing. A narrow approach would consider as rationed only those borrowers who are not offered a contract at all even if they are willing to accept the prevailing rate. In the broad approach adopted in this paper, the borrower may be offered a contract that is not feasible. There is even a broader approach whereby the borrower may be offered a feasible loan contract but decides to turn it down. This is the approach adopted in Boucher et al (2008; 2007). 6 We assume that all the borrowers can put up strictly equivalent collaterals, let us say “C”. The figure �� �

�

����

represents the fully collateralized loan i.e. the amount of loan for which the lenders are fully protected against the risk of default thanks to the available collaterals regardless the risk profile of the borrowers. Above that amount, the lenders start discriminating between high risk and low risk borrowers

7

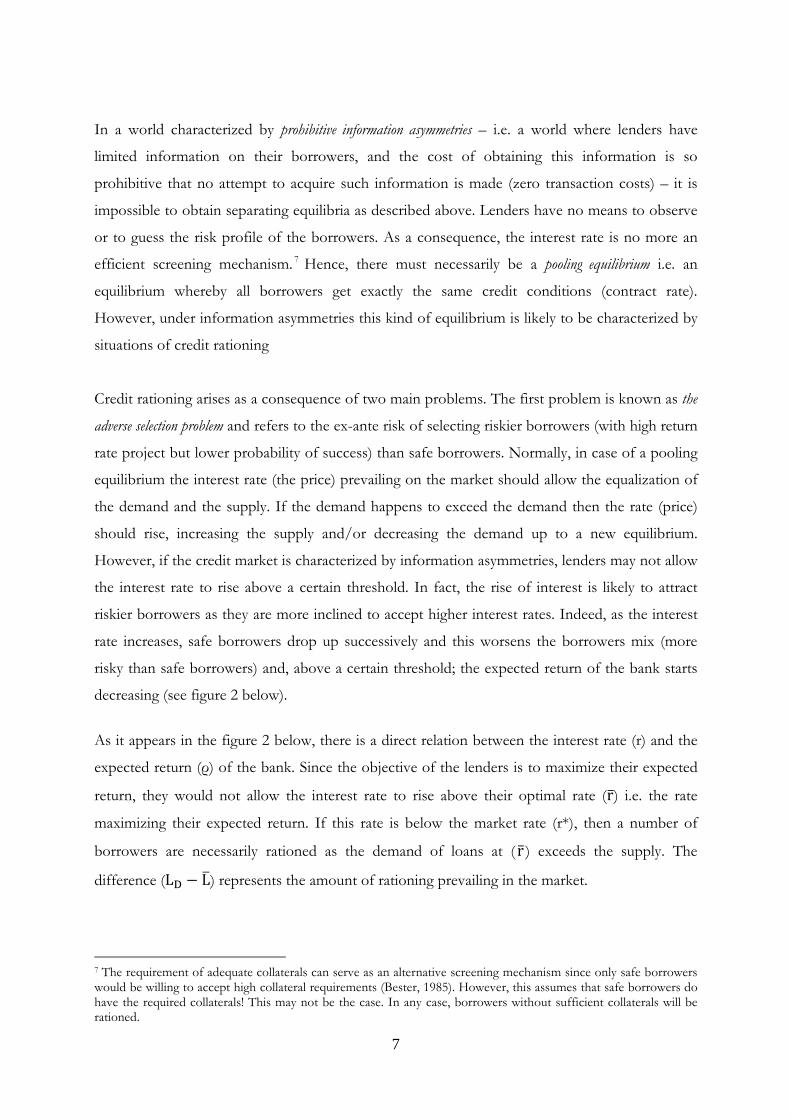

In a world characterized by prohibitive information asymmetries – i.e. a world where lenders have

limited information on their borrowers, and the cost of obtaining this information is so

prohibitive that no attempt to acquire such information is made (zero transaction costs) – it is

impossible to obtain separating equilibria as described above. Lenders have no means to observe

or to guess the risk profile of the borrowers. As a consequence, the interest rate is no more an

efficient screening mechanism. 7 Hence, there must necessarily be a pooling equilibrium i.e. an

equilibrium whereby all borrowers get exactly the same credit conditions (contract rate).

However, under information asymmetries this kind of equilibrium is likely to be characterized by

situations of credit rationing

Credit rationing arises as a consequence of two main problems. The first problem is known as the

adverse selection problem and refers to the ex-ante risk of selecting riskier borrowers (with high return

rate project but lower probability of success) than safe borrowers. Normally, in case of a pooling

equilibrium the interest rate (the price) prevailing on the market should allow the equalization of

the demand and the supply. If the demand happens to exceed the demand then the rate (price)

should rise, increasing the supply and/or decreasing the demand up to a new equilibrium.

However, if the credit market is characterized by information asymmetries, lenders may not allow

the interest rate to rise above a certain threshold. In fact, the rise of interest is likely to attract

riskier borrowers as they are more inclined to accept higher interest rates. Indeed, as the interest

rate increases, safe borrowers drop up successively and this worsens the borrowers mix (more

risky than safe borrowers) and, above a certain threshold; the expected return of the bank starts

decreasing (see figure 2 below).

As it appears in the figure 2 below, there is a direct relation between the interest rate (r) and the

expected return (ρ) of the bank. Since the objective of the lenders is to maximize their expected

return, they would not allow the interest rate to rise above their optimal rate (r̅) i.e. the rate

maximizing their expected return. If this rate is below the market rate (r*), then a number of

borrowers are necessarily rationed as the demand of loans at ( r̅ ) exceeds the supply. The

difference (L� − L�) represents the amount of rationing prevailing in the market.

7 The requirement of adequate collaterals can serve as an alternative screening mechanism since only safe borrowers would be willing to accept high collateral requirements (Bester, 1985). However, this assumes that safe borrowers do have the required collaterals! This may not be the case. In any case, borrowers without sufficient collaterals will be rationed.

8

Figure 2: Non-price credit rationing

Adapted by the Author from Stiglitz and Weis (1981)

The second problem arising from information asymmetry is known as the moral hazard problem and

refers to the ex-post risk of default. In other words, events happening after the establishment of

the loan contract may lead the borrower to default. For instance, high repayment costs can push

safe borrowers to deviate from their initial projects and to replace them by riskier projects (with

high return but low probability of success) once they receive the loan. Once again, high interest

rates are likely to lower banks’ expected return. Finally, borrowers who are rationed out in the

formal sector have no other option than resorting to informal financial practices (Hoff & &

Stiglitz, 1990; 1993). Therefore, informal finance is never a first choice but a makeshift until

something better.

Before concluding this subsection, it is worth noting that credit rationing arising from

asymmetrical information is likely to be wealth biased. Indeed, one of the solutions to the

problem of information asymmetries is to write highly collateralized loan contracts in order to

enhance the lender expected return (Bester, 1985). High collateral requirements are meant to

mitigate the borrowers’ incentive problems. It is quite evident that those without sufficient wealth

to put up as collateral would not be offered any feasible loan contract. Moreover, lenders who are

unable to observe actual risk profiles of the borrowers can associate poverty with high risk

profile. In this case, they are likely to offer loan contracts only to rich borrowers who are

assumed to have expected low-risk profiles while snubbing (rationing partially or totally) poor

borrowers who are assumed to have expected high-risk profiles.

9

ii. The transactions cost argument

Some scholars challenged financial dualism approaches by suggesting that informal finance can

sometimes be the first choice even for individuals with access to formal markets. The

explanations put forward to support this view include the fact that transactions costs are, sometimes,

lower in informal financial markets than in formal markets (Barham, Boucher, & Carter, 1996;

Chung, 1995). However, it is important to note that the existence of transactions costs can lead

to situations of credit rationing (financial dualism) as well. In the next paragraphs, both situations

are highlighted.

Following Gui-Abiad (1993), we define transactions costs as “all non-interest rates expenses incurred by

the borrower in applying for, getting the approval and repaying their loans as well as the costs incurred by the

lenders in evaluating, disbursing and collecting loans”. At least, two situations giving rise to transaction

costs can be readily identified. First, transaction costs can arise due to information asymmetries.

Indeed, one way of overcoming asymmetrical information problems is to engage in information

seeking procedures which are likely to push upward the transaction costs. Such costs include the

costs of securing information about the borrowers’ risk profiles as well as costs of monitoring the

use credit. Second, there are transactions costs which arise even in a perfect information

environment. They include the costs incurred by the lender in preparing loan applications,

evaluating the project viability and the collateral…, the costs incurred directly by the borrower

such as documentation costs, application fees as well as costs of trips to the lender’s premises

(Chung, 1995; Barham, Boucher, & Carter, 1996). We can also include in these costs, the

opportunity cost of time spent on loan application. Such an opportunity cost hinges on a number

of factors such as the distance to be covered by the borrower in order to reach the lender’s

premises, the time span between the application and the lender’s reply… In any case, the

existence of transactions cost of any sort will result in an increase of the effective rate above the

contract (perfect competition) rate. It is should be noted that that the lenders charge to the

borrower whatever cost they incurred in preparing the loan contract.

The figure 3 below depicts two possible outcomes of transactions costs. The first possible

outcome depicts a situation of credit rationing while the second outcome depicts a situation

where transactions render the informal sector more desirable the formal. For the sake of

simplicity, we consider only fixed transactions costs arising in a perfect information environment

10

as in Barham et al. (1996).8 However, the conclusions obtained can be readily extended to

situations where transaction costs arise from asymmetrical information. As it appears in the

figure 3, transaction costs affect the shape of the individual-specific loan supply curve (SF) by

raising the effective rate of interest (re) above the nominal or contract rate (rc).9 Small size loans

are associated with high effective interest rates. The rate decreases as the size of the loan

increases, it hits its minimum when re=rc. Hence, borrowers looking for small loans are likely to

find it costly to borrow from the formal market. Considering a borrower with a demand curve

D0, it appears that no feasible contract is offered to him by the lender as D0 never cuts the

individual supply curve.10 He is transaction cost rationed. Contrariwise, borrowers looking for

bigger size loans – see the demand curve (D1) – are likely to be offered a feasible loan contract.

However, it is cheaper for him to use an informal loan. Contrary to the previous case, the

decision not to apply for a formal loan is not imposed by the lender but is the borrower who

decides not to apply for a formal loan, though he is offered a feasible loan contract. Once again,

it appears that transaction cost rationing is likely to be wealth biased since it affects low amount

loans. We assume that low-income borrowers would be looking for small size loans.

Figure 3: Transaction costs and financial markets

Adapted by the Author from Barham et al. (1996)

8 For the analysis of both fixed and variable transactions costs the reader is referred to Chung (1995). 9 The effective interest rate can be written as �� �

����������

� where “L” stands for the loan size and “TC” for the

transactions cost 10 In the absence of transaction, he would have obtained a loan contract (LT) at the rate (rc). Given the presence of the transaction costs, the lender is ready to offer him a loan contract of equivalent amount but at a higher rate (r1). However, such a loan contract is outside the borrower’s feasible set.

11

iii. Contractual risks argument

Another explanation put forward in order to explain participation to informal finance is the level

of risk attached to formal loan contract (Boucher, Carter, & Guirkinger, 2008; Guirkinger, 2008).

As indicated previously, one way to protect lenders from the borrowers’ risk of default is to write

collateralized loan contracts. However, requiring the borrower to provide collateral (security)

involves extra risks for the borrower as, in case of default; the lender is likely to engage in security

realization procedures and, therefore, the borrower is likely to lose ownership of assets pledged

as collateral.

The contractual risks implied by collateral requirements can push some borrowers, who are able

to meet the collateral requirements, to decide to withdraw voluntarily from the credit market as they do

not want to carry the burden of the contractual risks implied by such collateralized contracts

(Boucher, Carter, & Guirkinger, 2008). In a related study, Boucher and Guirkinger (2007) showed

that collateral requirements are lower in informal sector making it possible for informal lenders to

write more attractive loan contracts. It follows that, borrowers who rejected the highly

collateralized formal loans are likely to resort to informal finance. Unlike the previous cases, the

wealth effects of the contractual risks are complex and will depend on the type of wealth

(financial vs. productive wealth) as well as on the risk status of the borrower (Boucher, Carter, &

Guirkinger, 2008).

iv. The commitment argument

While the above arguments focus exclusively on credit, a number of scholars have highlighted the

importance of saving for people in informal finance (Besley , Coate, & Loury, 1993; Baland &

Siwan, 2002; Ambec & Treich, 2003). Indeed, some individuals report to enroll in specific

informal financial practices in order to bind themselves to a strict saving discipline. This is the

case for Roscas members in Kenya who declare to find it difficult to save alone (Gugerty, 2007).11

Individuals with such commitment problems are said to have time inconsistent or hyperbolic

preferences. Time inconsistency refers to situations whereby preferences between two delayed

rewards reverse in favor of the more proximate reward (Frederick, George , & Ted , 2002). In

other words, even if an individual would prefer to save than spending, once he has money he

11 Roscas are associations whereby individuals agree to meet on a regular basis and convene to contribute periodically a given sum of money to a common pot. The pot is allocated to one of them each time they meet and whoever receives the pot is excluded from receiving it again before each member has had his turn.

12

can’t refrain himself from spending it. In this case he requires an outside commitment

mechanism such as Roscas which “provide a collective mechanism for individual self-control in the presence of

time- inconsistent preferences” (Gugerty, 2007).

Stressing the importance of commitment problems, Morduch (2010) shows how low income

people with hyperbolic preferences, choose to lock down their savings and accept – in case of

liquidity emergency – loans that bear high interest rates. One explanations of this behavior is that,

due to time inconsistency, individuals find it easier to pay back a loan than rebuilding one’s

savings. The cost of credit represents the cost the individual is ready to bear in order to benefit

from the commitment mechanism offered by the credit.

II. Lessons and limits to be learnt from the economic theories of informality

This section discusses the lessons to be learnt from the economic theories of informality as well

as their limits with respect to the rationale of existence of informal finance.

i. So what do we learn from the above theories?

As far as the rationale of the demand for informal finance is concerned, there at least two

important elements that can be learnt from the economic theories of informality reviewed so far.

First, the identified theoretical arguments help explaining why people exhibit demand for

informal finance. Two main opposing views are brought up. Informal finance is either seen as a

makeshift for individuals without access to formal markets or a desirable alternative to formality. Five

theoretical arguments have been identified; (1) financial repression, (2) information asymmetries,

(3) transaction costs, (4) contractual risks and (5) the commitment argument. However, we

restrict our discussion to the four last arguments as the outcomes of financial repression – in

terms of credit rationing – are similar to those of information asymmetries. For microfinance

institutions, these are tools which can help them obtaining a sound knowledge of the financial

needs and constraints of their potential customers.

Second, some of these theoretical arguments are consistent with situations where individuals mix

informal and formal financial practices. Indeed, existing empirical evidence tends to attest the

existence of what is referred to hereafter as the mixed strategies financial behavior and which consists

in the simultaneous use of both types of financial services. Such cases have been identified,

among others, in Zimbabwe where 76% of market traders participate in saving associations

13

known as Roscas while about 77% acknowledge owning a bank account (Chamlee-Wright,

2002). 12 While the information asymmetry argument seems to be inconsistent with mixed

strategies, the arguments in terms of transaction costs, contractual risks and commitment are

consistent with such strategies. Once again, it is very important for microfinance institutions to

understand why people use both informal and formal finance. Such an understanding is likely to

provide microfinance institutions with fine-grained insights in the ways their own products

interact with pre-existing informal financial products. It is evident that a market-oriented design

of microfinance products would benefit immensely from such knowledge. New opportunities of

articulating microfinance products to existing financial practices can be identified etc.13

ii. Informality: an elusive concept

The most evoked limit of economic theories on informality is their lack of consensus of what is

informality. Indeed, despite the intuitive appeal of the concept of informality in analyzing the

inner-heterogeneity of developing countries’ economies, economic theories describe the

mechanisms leading to market segmentation without indicating clearly how the resulting market

segments should be identified.14 To overcome this challenge, a number of scholars suggested

definitions of informal activities based on a certain number of criteria (multi-criteria definitions).

The most popular definition was provided by the International Labor Organization which

defined the Informal sector as: “the non-structured sector that has emerged in the urban centers as a result of

the incapacity of the modern sector to absorb new entrants… it is the sum of all income earning activities outside

legally regulated enterprises and employment relationship” (ILO, 1972; 2002). Seven criteria characterizing

informal activities are identified. These are: (1) ease of entry; (2) reliance on indigenous

resources; (3) family ownership; (4) small scale operations; (5) labor intensive and adaptive

technology; (6) skills acquired outside of the formal sector; (7) unregulated and competitive

markets.

12 We can also mention the cases of International Monetary Fund employees (Ardener & Burman , 1995)bank employees in Bolivia (Adams & Canavesi, 1992) and in Ghana (Bortei-Doku & Aryeetey, 1995) who declared to be engaged in informal financial practices despite having access to formal financial markets. A more recent study carried in Bangladesh, India, and South Africa, revealed also that low Income people use a mixture of informal and formal financial devices in order to manage their daily budget (Collins , Morduch, Rutherford, & Ruthven, 2009) 13 In a recent field study, Guérin et al. (2009; 2010) identified a possible leverage effect between the use of microfinance and informal finance whereby the access to microcredit increases the use of informal loans. 14 For instance, dual models posit the existence of a wage differential as well as some mobility limitation between the segments but they remain silent as to how big should be the wage differential or how strong should be the mobility limitations.

14

However, this definition of informal economy (sector) is nothing but controversial. Each of the

above criteria is subject to critics. Let us consider two main criticisms against the concept of

informal sector as highlighted by Lautier (2004). First, it is claimed that the term of “sector”

refers to a homogeneous industry or economic activity and, therefore, cannot be appropriate for

the so-called informal activities which are extremely heteroclites. As he puts it, it is not because

there is a formal sector that there should necessarily be an informal sector. Against this criticism

it could be said that a sector need not be homogeneous in all respects. What matters is to find a

number of appropriate characteristics shared by the activities to be included in the same sector.

In any case, any economic sector – be it industrial or whatever – displays some level of

heterogeneity (in terms of stakeholders, practices...) and the so-called formal sector is far from

being homogeneous.

Second, it is contended that legality criterion cannot help discriminating between informal and

formal activities as most of human activity is characterized by some legality and some illegality.

No one can be totally illegal – i.e. violating all the laws – and some legally registered organizations

do, from times to times, adopt illegal practices. Such a mixture of legality and illegality makes it

difficult to use the legality as discriminating criterion between the formal and informal sectors.

This situation has led scholars such as Servet (2006) to use the term of (financial) informalities as

he considers that there exist a continuum set of levels of formalities and informalities.

Recognizing the validity of these critics, I would like, however, to argue that the legal criterion

remains a powerful element in discriminating informal and formal sectors particularly for activities

governed by a set of specific regulations such as financial activities. Indeed, the usual framework of applying

the legality criterion is to consider the adherence to labor and taxation regulations which are the

most likely to be violated even by officially registered firms. However, if one considers specific

regulations for specific activities it becomes easier to discriminate between activities adhering to

official regulations and those occurring outside the officially regulated framework. For instance,

in most of the cases, financial activities are submitted to specific regulations with a unique

regulatory authority. Hence, it is easy to distinguish those engaged in financial activities without

recognition of the regulatory authority from those operating under the supervision of the

regulatory authority. In the following, the term of informal financial activities is used to depict

activities that are not submitted to the specific official laws governing activities of similar nature without being

necessarily illegal. It should be noted that informal activities defined according to “the specific law

criterion” can adhere to other regulations (like paying taxes …).

15

iii. An exclusive focus on financial considerations

Another limit of the economic theories on informal finance comes from their exclusive focus

mainly on credit and to a lesser extent on saving products.15 Such an exclusive focus on financial

considerations prevents the economic approaches from getting the entire picture of informal

financial landscape as well as the multiplicity of the needs that are met by informal financial

markets. Indeed, besides saving and credit, there are other reasons which may justify the use of

financial services. In the next section, we introduce a new theoretical argument highlighting the

importance – for the analysis of the demand for informal finance – of motivations that are not

necessarily financial in nature such as motives related to social relations.

III. The argument in terms of social effects

The analysis of the effects of social relations on economic behavior and/or outcomes is not a

new topic in the literature. Empirical studies have shown that differences in the strength of the

social relations (networks) have led to different economic outcomes in Italy (Putnam, Leonardi,

& Nanetti, 1993),16 in Germany (Burchardi & Hassan, 2010). With respect to financial behavior, it

appeared that increased social interactions between members of a microfinance group lending

program has led to more cooperation and lower level of default in India (Feigenberg , Erica , &

Rohini, 2010) while the information received through reputable social groups proved to affect the

saving behavior of low-income households in rural Vietnam (Newman, Finn, & Katleen, 2011).

From a theoretical perspective, the effect of social relations on economic outcomes can be traced

back to the concept of “social embeddedness” that was first coined by Polanyi in his famous book

“the Great transformation” (Polanyi, 1944). 17 This concept indicates that economic action

depends on actions or institutions which are non-economic in content. Following Polanyi,

Granovetter (2005) asserts that the influence of social relations on economic decisions is such

15 The focus on credit has put informal lenders – who are known for charging extremely high interests – on a pedestal by considering them as the representative figure of informal finance. It is quite common to reduce informal financial practices to these money dealers or “loans sharks”. Such a standpoint has, in the best case, led policy makers to ignore informal financial practices, and in the worst case, to adopt repressive policies against any financial practice labeled as informal. 16 Putnam considers social relations (networks) as a component of what he calls the social capital. He defines social capital as a set of features of social organization such as moral obligations and norms, social values (especially trust, reciprocity..) and social networks.... that can improve the efficiency of society by facilitating coordinated action (Feigenberg , Erica , & Rohini, 2010). However, Fafchamps (2006)(2006) suggested that social networks are important only at intermediate level of development and become unnecessary when generalized trust has emerged in the society. 17 The Great Transformation is a historical analysis of the transformation through which has gone the western economies in the late eighteenth and early nineteenth centuries. It describes the emergence, the blossoming and the demise of the self-regulating market.

16

that any attempt to isolate economic behavior from the social relations would lead necessarily to

a partial or a misrepresentation of the reality.18

It is possible to identify at least four types of social effects depending on the channels through

which social relations affect economic behavior. First there are informational effects which identify

effects of social relations on the flow and the quality of information available to the individuals (Easley &

Kleinberg, 2010). Informational aspects can be split into two different effects: (1) the social opinion

effect and the bandwagon effect (Leibenstein, 1950; Granovetter, 1978). Second, there is a reciprocity

effect when economic decisions are motivated by the need of creating or enhancing social

relations. Third, there are network or direct-benefit effects which depict situations where the

consumption of a good or service is directly influenced by the number of other people

consuming it (Easley & Kleinberg, 2010). This is the case of the use of fax machines or

telephone. In fact, a fax machine or a telephone would be useless if owned by one single

individual. Finally, there are reputation effects whereby the threat of terminating social relations or

to damage one’s social reputation may act as social collateral allowing the sustainability of a large

number of arrangements that would not otherwise be feasible (Burchardi & Hassan, 2010; Besley

& Coate , Group lending, Repayment Incentives and Social collateral, 1995; Baland , Moene, &

Siwan, 2003). In the following, we focus on the informational and reciprocity effects.

i. The social opinion effect

The social opinion effect seeks to capture how individuals are influenced in their decision by the

opinions of their friends and acquaintances. As documented by Granovetter (2005), “much

information is subtle, nuanced and difficult to verify, so actors do not believe impersonal sources and instead rely on

people they know”. 19 In fact, opinions of friends and acquaintances increase or decrease the

perceived value of the product/service in the eyes of the individual receiving it. Newman et al.

(2011) showed that the perceived return of using a given financial product is a function of the

information available to the decision maker. Hence, the social opinion effect can be analyzed as

having a positive/negative effect on the utility function of the decision maker. Consider the

following additively separable utility function:

18Social network are defined as a collection of interconnected dyadic social relations that influence economic behavior (Granovetter, 2005). 19 Illustrating how social relations affect the quality of information available to an individual, Granovetter insists on the superiority of the weak ties. Indeed, an individual obtains more diverse and new information from his acquaintances (weak ties) rather than from his closest friends (strong ties). This phenomenon is referred to as “the strength of the weak ties”. Indeed, since an individual’s acquaintances are prone to move in different circles, they are likely to have information that the individual does not already have. In contrary, closest friends will tend to have the same information as they move in similar circles (Granovetter, 1974; 1983).

17

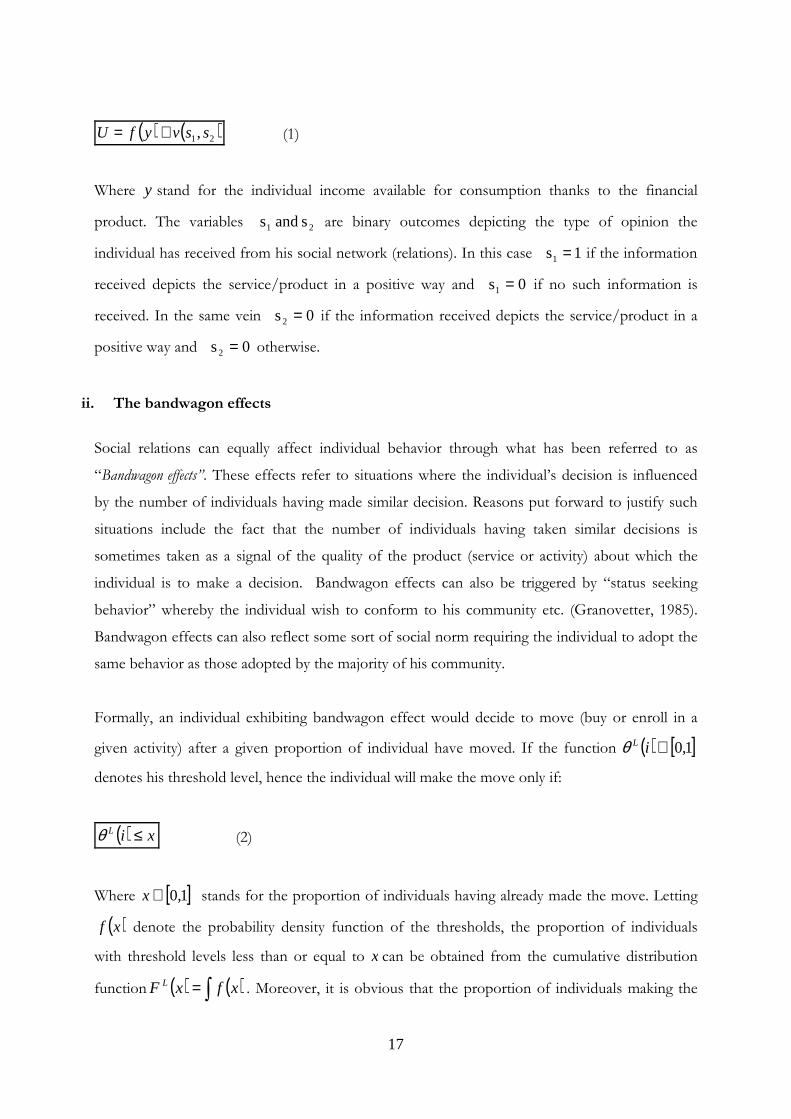

( ) ( )21,ssvyfU += (1)

Where y stand for the individual income available for consumption thanks to the financial

product. The variables s and s 21 are binary outcomes depicting the type of opinion the

individual has received from his social network (relations). In this case 1s 1 = if the information

received depicts the service/product in a positive way and 0s 1 = if no such information is

received. In the same vein 0s 2 = if the information received depicts the service/product in a

positive way and 0s 2 = otherwise.

ii. The bandwagon effects

Social relations can equally affect individual behavior through what has been referred to as

“Bandwagon effects”. These effects refer to situations where the individual’s decision is influenced

by the number of individuals having made similar decision. Reasons put forward to justify such

situations include the fact that the number of individuals having taken similar decisions is

sometimes taken as a signal of the quality of the product (service or activity) about which the

individual is to make a decision. Bandwagon effects can also be triggered by “status seeking

behavior” whereby the individual wish to conform to his community etc. (Granovetter, 1985).

Bandwagon effects can also reflect some sort of social norm requiring the individual to adopt the

same behavior as those adopted by the majority of his community.

Formally, an individual exhibiting bandwagon effect would decide to move (buy or enroll in a

given activity) after a given proportion of individual have moved. If the function ( ) [ ]1,0∈iLθ

denotes his threshold level, hence the individual will make the move only if:

( ) xiL ≤θ (2)

Where [ ]1,0∈x stands for the proportion of individuals having already made the move. Letting

( )xf denote the probability density function of the thresholds, the proportion of individuals

with threshold levels less than or equal to x can be obtained from the cumulative distribution

function ( ) ( )∫= xfxF L . Moreover, it is obvious that the proportion of individuals making the

18

move at time (t+1) is equal to the proportion of individuals who reached their threshold levels at

time (t). We obtain the following difference equation which describes the dynamics of the

threshold model:

( )tL

t xFx =+1 (3)

Combining equations (2) and (3), it is easy to see that a given individual will make the move at

time t, only if the proportion of individuals who reached their threshold levels at time (t-1) is

larger than or equal to his own threshold level. Formally, we get:

( ) ( )1−≤ tLL xFiθ (4)

There exist also situations where an individual may decide not to use a product if a given

threshold is reached. In fact, some people prefer to avoid overly popular products or activities.

This effect is known as the “reverse bandwagon” or “snob effect” (Leibenstein, 1950). In these

situations, individuals have upper threshold and would move only if:

( ) ( )1−≥ tUU xFiθ (5)

Where UU F and θ stand respectively for the individual upper threshold and the cumulative

distribution function of these upper thresholds.

iii. The reciprocity effect

The reciprocity effect refers to situations where the decision to enter into a financial transaction

is motivated not only by the economic benefits but also by the need of social relations. Put

differently, an individual may decide to enter into a loan contract or another type of financial

contract with the objective to create or enhance existing social relations. Note that it does not

matter whether the need for social relations is driven by the search of personal benefit, by

kindness or even imposed by some social norms.

Just as the concept of embeddedness, the concept of reciprocity draws from Polanyi and refers to

a mechanism of exchange whereby individuals get involved in exchange of gifts with the objective of

19

enhancing their social/community relations. 20 There are three main features characterizing a system of

economic exchanges based on a mechanism of reciprocity. First, the reciprocity principle

involves an exchange of gifts in the form of the famous Potlatch triadic cycle: give, receive and give

back. Second, while a price mechanism based on the rule of cost equivalence prevails on the

market, the gifts exchanged under the reciprocity principle may happen to be of totally different

values and forms (Mauss, 1923-1924).21 Third, under the reciprocity mechanism, the exchanges

are not only intended to allow the transfer of goods and services but also to create or enhance the

social ties between the stakeholders. It may even be the case that a gift exchange under the

reciprocity principle is solely intended to create or consolidate social relations.

The reciprocity effect is intended to capture the last feature of the reciprocity mechanism. It is

expected to measure the importance of the need of enhancing social relations or enforcing social

inclusion in economic decisions. Considering that some informal financial practices are highly

embedded in reciprocity mechanisms with a high potential of generating/enhancing social

relations, it is quite important to account for the effect of such social relations while analyzing the

determinants of the financial behavior of individuals involved in those practices.

The reciprocity effect is an inherent characteristic of the (financial) product being exchanged. In

other words, some financial products have a potential of generating valuable social relations while

other do not. Formally, the reciprocity effect has a direct impact on the individual’s utility.

Considering the additively separable utility function indicated in equation (1), we can extend it to

account for the reciprocity effect as follows:

( ) ( ) )(, 321 shssvyfU ++= (6)

20 Polanyi identified three different but non-mutually exclusive forms of economic integration or systems of economic exchange; namely (1) the market exchange based on a price mechanism, (2) the Reciprocity and (3) the Redistribution systems. Under the market principle, the production and the coordination of exchanges are based on a price mechanism whereby prices are freely determined by market forces. The rule of cost equivalence prevails in the market where the price is expected to reflect the value of the good or the service being exchanged. Under the redistribution principle, the exchanges rely on a mechanism which requires the existence of both a Central authority and a set of rules or laws allowing the central authority to collect and redistribute resources. 21The cost-equivalence rule stems from the fact that on competitive markets the cost of production equals the price of output, provided that a rate of return on investment is included in cost. “In neoclassical ethics, prices that exceed cost are unfair to consumers and imply the exploitation of monopolistic advantage, while prices that are below cost represent unfair competition – in the form of a – dumping”. Under the reciprocity principle, the counter gift – in the form of a foreseeable physical benefit for the gift giver – may even not be expected in which case the gift process reduces to two stages: giving and receiving. Note that the forms taken by gifts can range from material objects such as physical goods or services to immaterial objects such as social recognition.

20

To conclude this subsection, let us note that social effects constitute an additional argument

susceptible of explaining the demand for informal finance. This assertion has far reaching

consequences as it suggests that some individuals would still enroll in informal financial practices

even in the absence of information asymmetry, transactions or contractual risks.. Moreover,

social effects are consistent with mixed strategies, and as such, they allow throwing more light on

the rationale of such strategies. Indeed, we can easily figure out that individuals motivated by the

need of creating enhancing social relations may decide to join (informal) financial practices with a

high potential of creating social relations even though they may have access to formal market.

IV. Social effect and informal finance: some empirical evidence

In a recent empirical study carried, Guirkinger (2008) have shown that the information

asymmetries argument, the transaction argument as well as the contractual risks arguments do

contribute significantly to the explanation of the demand for informal loan in rural Peru. In this

section will focus exclusively on the importance of social relations as far as the rationale for

demand for informal finance is concerned. These results presented here were obtained from a

random sample of 398 micro-entrepreneurs operating in three markets located in Ouagadougou,

the Capital City of Burkina. The total population in these markets amounted to 6,500 micro-

entrepreneurs.

The selected micro-entrepreneurs were surveyed using a questionnaire containing among others a

module designed to collect information about the participation of the respondents to the various

financial practices as well as a module made of qualitative questions aimed at identifying the

rationale (self-reported motives) behind the decision to use each of the identified financial

practice. The methodology adopted in this module draws from the Direct Elicitation method

which consists in asking directly the respondents to indicate which elements have motivated their

financial choices (Boucher, Guirkinger, & Trivelli, 2009). Six financial practices were identified.

These include financial transactions with traditional banks and/or microfinance institutions

(cooperatives). There are also transactions with informal practices such Roscas, Informal funds

collectors known as Cauri d’or, loans between friends as well as informal suppliers’ loans.22

22 Roscas and Cauri d’or are popular financial practices. First, Roscas are associations whereby individuals agree to meet on a regular basis and convene to contribute periodically a given sum of money to a common pot. The pot is allocated to one of them each time they meet and whoever receives the pot is excluded from receiving it again before each member has had his turn. Second, the cauri d’or is a financial practice in which an individual called “tontinier” takes the responsibility of collecting and keeping the savings of several other people. Each member of the cauri d’or

21

Figure 4 below shows the rates of enrollment to each of the identified practice. The global

enrollment rate indicates the proportion of respondents who declare to have used a particular

financial practice even though this may no longer be the case while the actual enrollment rate

indicates the actual proportion of respondents who are still using a particular financial practice.

Figure 4: Financial participation

The next figure (figure 5) depicts the proportion of micro-entrepreneurs who declared that social

relations have played an important role in their decision to engage in financial practices.

Figure 5: Social effects

decides to save a given amount of money every day. At the end of 31 payments, the “tontinier” refunds the equivalent of 30 day-payments and keep one day-payment for his remuneration.

0%

10%

20%

30%

40%

50%

60%

70%

Bank

account

Coopec

account

Supplier

credit

Cauri Roscas Friends None

24

%

41

%

63

% 56

%

33

% 23

%

6%

20

%

34

%

63

%

44

%

19

%

21

%

10

%

global actual

0%

10%

20%

30%

40%

50%

Bank Coop Roscas Cauri Friends Sup Cr.

2% 3%

26%

13%

31%

26%

7% 8% 9% 9%11%

3%3%7%

30%

36%

43%

15%

social enhancement social opinion bandwagon

22

Considering each social effect individually, we observe that individuals declaring to engage in a

practice because the majority of their community do so (bandwagon effects) constitute the most

important social related motives for micro-entrepreneurs involved in informal finance. The need

to create or enhance social relations (reciprocity effects) is the next most evoked social related

motive while the social opinion effect is the least evoked. However, the most striking finding is

the net difference between informal and formal practices. Indeed, all the three social effects are

seemingly weaker in the case of formal financial practices. In other words, we can confidently

assume that social effects play a role in explaining the persistence of informal practices. They can

also explain why some people do adopt mixed strategies.

Concluding remarks

In this paper, five theoretical arguments explaining the rationale of the demand for informal

finance have been highlighted and analyzed. They include the argument in terms of information

asymmetries, the argument in terms of transaction costs, the argument in terms of contractual

risks, the argument in terms of commitment mechanism and the argument in terms of social

relations. These theories help understanding the rationale of the existence of informal finance by

highlighting the main elements susceptible of determining the demand for informal finance. They

also open the gate to a broader analysis of the conditions underlying the coexistence of informal

financial practices and formal microfinance. It goes without saying that such an analysis would

involve questioning some of the predictions of the above theories as well inputting new elements

in order to get the whole picture.

As far as venues for future research is concerned, three research questions can be highlighted.

The first question that follows naturally from the analysis in terms of the above four arguments

consists in enquiring how each of these arguments contribute to the empirical explanation of the

demand for informal finance. Put differently, we need to know whether these theories allow

understanding how would-be borrowers and savers, make their choice between informal and

formal microfinance.

The second question, which is, indeed a corollary to the above question consists in enquiring

about the articulation between informal and formal microfinance. Indeed, the analysis of the

sectorial choice – between informal and formal – should allow for the possibility of articulation

between formal and informal practices. The emphasis should then be put on the identification of

23

the practices that are most likely to be articulated as well as on the rationale of such an

articulation.

Last but not least, it is important to analyze the lessons to be learnt from this study by

microfinance institutions. The objective here is, on the one side, to scrutinize the offer of

microfinance services in order to check whether there is some awareness of what is going on in

informal finance and how this is taken into account while designing microfinance products. On

the other side, some suggestions need to be laid down as to how microfinance could better take

advantage of the possible complementarities it can establish with informal finance.

24

REFERENCES Adams, D., & Canavesi, M. (1992). Rotating Savings and Credit Associations in Bolivia.

Dans D. Adams, & D. Fitchett, Informal Finance in Low-Income countries. Washington D.C.: BERG.

Ambec, S., & Treich, N. (2003). Roscas as financial agreements to cope with social pressure. Working Papers 200301, 1-22.

Ardener, S., & Burman , S. (1995). Money-go Rounds: The importance of Rotating Saving and Credit Associations for women. Washington, D.C. : BERG.

Baland , J.-M., & Siwan, A. (2002). The economics of ROSCAs and intrahousehold allocation. Quarterly Journal of Economics, 117(3), 983-995.

Baland , J.-M., Moene, K. O., & Siwan, A. (2003). Sustainability and organizational design in Roscas: Some evidence from Kenya. Working paper, University of British Columbia, University of Namur and University of Oslo.

Barham, B., Boucher, S., & Carter, M. (1996). Credit Constraints, Credit Unions, and Small Scale Producers In Guatemala. World Development, 24(5), 792–805.

Besley , T., & Coate , S. (1995). Group lending, Repayment Incentives and Social collateral. Journal of Development Economics(46).

Besley , T., Coate, S., & Loury, G. (1993). The economics of Rotating and credit associations. American Economic Review(83), 792-810.

Bester, H. (1985). Screening vs Rationing in Credit Markets with Imperfect Informationn. American Economic Review, 75(4), 850-855.

Bortei-Doku, E., & Aryeetey, E. (1995). Mobilizing Cash for Business: Women in Rotating Susu Clubs in Ghana. Dans S. Ardener, & S. Burman, Money-go-Rounds: The Importance of rotating savings and credit associations for women. Washington D.C.: BERG.

Boucher, S., & Guirkinger, C. (2007, November). Risk, Wealth, and Sectoral Choice in Rural Credit Markets. American Journal of Agricultural Economics. 89(4), 991-1004.

Boucher, S., Carter, M., & Guirkinger, C. (2008). Risk rationing and wealth effects in credit markets: Theory and implications for agricultural development. American Journal of Agricultural Economics, 90(2), 409–423.

Boucher, S., Guirkinger, C., & Trivelli, C. (2009). Direct elicitation of credit constraints: Conceptual and practical issues with an empirical application to Peruvian Agriculture. Journal of Economic Development and Cultural Change, 57(4).

Brau, C. J., & Woller, G. M. (2004). Microfinance: A Comprehensive Review of the Existing Literature. Journal of Entrepreneurial Finance and Business Ventures, 9(1), 1-26.

Burchardi, K., & Hassan, T. A. (2010, August 24). The Economic Impact of Social Ties: Evidence from German Reunification. Chicago Booth Research Paper No. 10-27, CRSP Working.

Chamlee-Wright, E. (2002, July). Saving and Accumulation Strategies of Urban Market Women in Harare, Zimbabwe. (U. o. Press, Éd.) Economic Development and Cultural Change, 50(4), 979-1005.

Chung, I. (1995). Market Choice and Effective Demand for Credit: The Roles of Borrower Transaction Costs and Rationing Constraints. Journal of Economic Development, 20(2), 23-44.

Collins , D., Morduch, J., Rutherford, S., & Ruthven, O. (2009). Portfolios of the Poor. Princiton, New Jersey: Princeton University Press.

De Soto , H. (1989). The Other Path: The Invisible Revolution in the Third World. HarperCollins.

25

Easley, D., & Kleinberg, J. (2010). Networks, Crowds, and Markets: Reasoning about a Highly Connected World. Cambridge University Press.

Fafchamps, M. (2006). Development and social capital. Journal of Development Studies, 42(7), 1180 - 1198 .

Fei, J., & Ranis, G. (1964). Development of the Labor Surplus Economy. Homewood IL: Irwin.

Feigenberg , B., Erica , M. F., & Rohini, P. (2010). Building Social Capital Through Microfinance. NBER Working Paper Series, WP 16018.

Fields, G. S. (2009). Segmented Labor Market Models in Developing Countries. In H. K. (Eds.), The Oxford handbook of philosophy of economics (pp. 476-510). Oxford: Oxford University Press.

Frederick, S., George , L., & Ted , O. (2002). Time Discounting and Time Preference: A Critical Review. Journal of Economic Literature, 40(2), 351-401.

Granovetter, M. (1974). Getting a job: a study of contacts and carrers. Cambridge, Harvard University Press.

Granovetter, M. (1978). Threshold Models of Collective Behavio. The American Journal of Sociology, 83(6), 1420-1443.

Granovetter, M. (1983). The Strength of Weak Ties: A Network Theory Revisited. Sociological Theory(1), 201–33.

Granovetter, M. (1985). Economic Action And Social Structure: The Problem Of Embeddedness. The American Journal Of Sociology, 91(3), 481-510.

Granovetter, M. (2005). The Impact of Social Structure On Economic Outcomes. Journal of Economic Perspectives, 19 (1), 33-50.

Guérin, I., Morvant-Roux , S., & Servet , J. M. (2010). Understanding the Diversity and Complexity of Demand for Microfinance Services: Lessons from Informal finance. Rume Working Paper 2009-7.

Guérin, I., Venkatasubramanian, R., & Héliès, O. (2009). Microfinance, Endettement Et Surendettement. Revue Tiers Monde(197), 131–146.

Gugerty, M. K. (2007, January). You Can’t Save Alone: Commitment and Rotating Savings and Credit Associations in Kenya. (U. o. Press, Éd.) Economic Development and Cultural Change, 55(2), 251-82.

Guia-Abiad, V. (1993). Borrower Transaction Costs and Credit Rationing in Rural Financial Markets: The Philllipine Case. The Developing Economies(31), 208–219.

Guirkinger, C. (2008). Understanding the Coexistence of Formal and Informal Credit Markets in Piura, Peru. World Development World Development Vol. 36, No. 8, pp. 1436–1452,, 36(8), 1436–1452,.

Harris, J., & Todaro, M. (1970). Migration Unemployement and Developement : A Two Sectors Analysis. American Economic Review, 60(1), 126-42.

Hoff, K., & & Stiglitz, J. (1990). Imperfect information and rural credit markets: Puzzles and policy perspectives. World Bank Economic Review(5), 235–250.

Hoff, K., & Stiglitz, J. (1993, June). A theory of imperfect competition in rural credit markets in developing countries: Towards a theory of segmented credit markets. Working Paper No. 58.

Hudson, K. (2007, March 1). The new labor market segmentation: Labor market dualism in the new economy . Social Science Research, 36(1), 286-312.

ILO. (1972). Employment, Incomes and Equality: A Strategy for Increasing Productive Employment in Kenya. Geneva: International Labour Office.

ILO. (2002). Women And Men in The Informal Economy : A statistical picture. Geneva: International Labour Office.

26

ILO. (2007). Report IV on Decent Work and the Informal economy: Sixth item on the agenda. Geneva: International Labour Office .

Johnson, R. S. (2004). Market Segmentation Theory: A Pedagogical Model for Explaining the Term Structure of Interest Rates. Journal of Academy of Business Education, 5.

Kirkpatrick, C. &. (2004, December ). The Lewis Model After Fifty Years. Manchester School, 72(6), 679-690.

Lautier, B. (2004). L’économie Informelle Dans Le Tiers Monde. Paris: La Découverte. Leibenstein, H. (1950). Bandwagon, Snob, and Veblen Effects in the theory of consumers'

demand. Quarterly Journal of Economics(64 ), 183‐207. Lewis, W. A. (1954). Economic Development with Unlimited Supplies of Labour.

Manchester School(22), 139–91. Lewis, W. A. (1955). The Theory of Economic Growth. London: George Allen & Unwin. Lewis, W. A. (1972). Reflections on Unlimited Labour. In E. L. DiMarco, International

Economics and Development (Essays in Honour of Raoul Prebisch) (pp. 75-96). New York: Academic Press.

Lewis, W. A. (1979). The Dual Economy Revisited. The Manchester School, 47(3), 211- 229. Maloney, W. F. (2003). Informal Self-Employment: Poverty Trap or Decent Alternative.

Dans G. S. Fields , & G. Pfeffermann, Pathways Out of Poverty. Boston: Kluwer. Maloney, W. F. (2004, July). Informality Revisited. World Development, 32(7), 1159-1178. Mauss, M. (1923-1924). Essai sur le don. Forme et raison de l’échange dans les sociétés

primitives. (C. 2. Edition électronique a été réalisée par Jean-Marie Tremblay, Éd.) l'Année Sociologique, seconde série.

McKinnon, R. I. ( 1973 ). Money and Capital in Economic Development. Washington, DC: Brookings Institution.

McKinnon, R. I. (1976). Money and finance in economic growth and development: essays in honour of Edward S. Shaw. New York (N.Y.): Dekker.

Morduch, J. (2010, August). Borrowing to Save: Perspectives from Portfolios of the Poor. The Financial Access Initiative (mimeo), 1-12.

Morvant–Roux, S. (2009). Access to microcredit and continuity of indebtedness dynamics in rural Mexico: combining anthropology with econometrics. Rume Working Paper(3).

Newman, C., Finn, T., & Katleen, V. D. (2011). Social Capital and Savings Behavior: Evidence from Vietnam. IIIS Discussion Paper No. 351, 1-32.

Nyssens, M. (2000). Les approches économiques du tiers secteur Apports et limites des analyses anglo-saxonnes d’inspiration néo-classique. Sociologie du Travail, 42(4).

Olaya, C. D. (2007). Towards a System Dynamics Model of De Soto’s Theory on Informal Economy. Proceedings of the 25th International Conference of the System Dynamics Society, 1-20.

Polanyi, K. (1944). The Great Transformation. New-York: Holt, Rinehart. Portes, A. a.-K. (1987). Making It Underground: Comparative Material on the Urban Informal

Sector in Western Market Economies. American Journal of Sociology(93), 30-61. Putnam, R., Leonardi, R., & Nanetti, R. (1993). Making Democracy Work: Civic Traditions in

Modern Italy. Princeton: Princeton University Press. Quijano, A. (1974). The marginal pole of the economy and the marginalized labour force.

Economy and Society, 3(4), 393-428. Ranis, G. (2004, December). Arthul Lewis’ Contribution to the Development Thinking and

Policy. Manchester school , 72(6), 712-723. Ranis, G., & Frances, S. (1999). V-Goods and the Role of the Urban Informal Sector in

Development. Economic Development and Cultural Change, 47(2), 88-259. Servet, J. M. (2006). Banquiers aux pieds nus, par Jean-Michel Servet. Paris: Ed. Odile

Jacob.

27

Servet, J. M. (2007). Le principe de réciprocité chez Karl Polanyi, contribution à une définition de l'économie solidaire. Revue Tiers Monde , 2(190), 255-273.

Shaw, E. (1973). Financial Deepening in Economic Development. New York: Oxford University Press.

Stiglitz, J., & Weiss, A. (1981). Credit rationing in Markets with imperfect information. American Economic Review, 71(3), 393-410.

Van Wijnbergen, S. (1983, August-October). Credit policy, inflation and growth in a financially repressed economy. Journal of Development Economic, 13(1-2), 45-65.

Williams, C. C. (2010). Re-theorizing the Informal Economy in Western. The Open Area Studies Journal(3), 1-11.

Williams, C., & Round, J. (2008). A critical evaluation of romantic depictions of the informal economy. Review of Social Economy, 66(3), 297 – 323.

Zukin, S., & DiMaggio , P. (1990). Structures of Capital: The Social Organization of the Economy. New York: Cambridge University Press.

28

APPENDICES

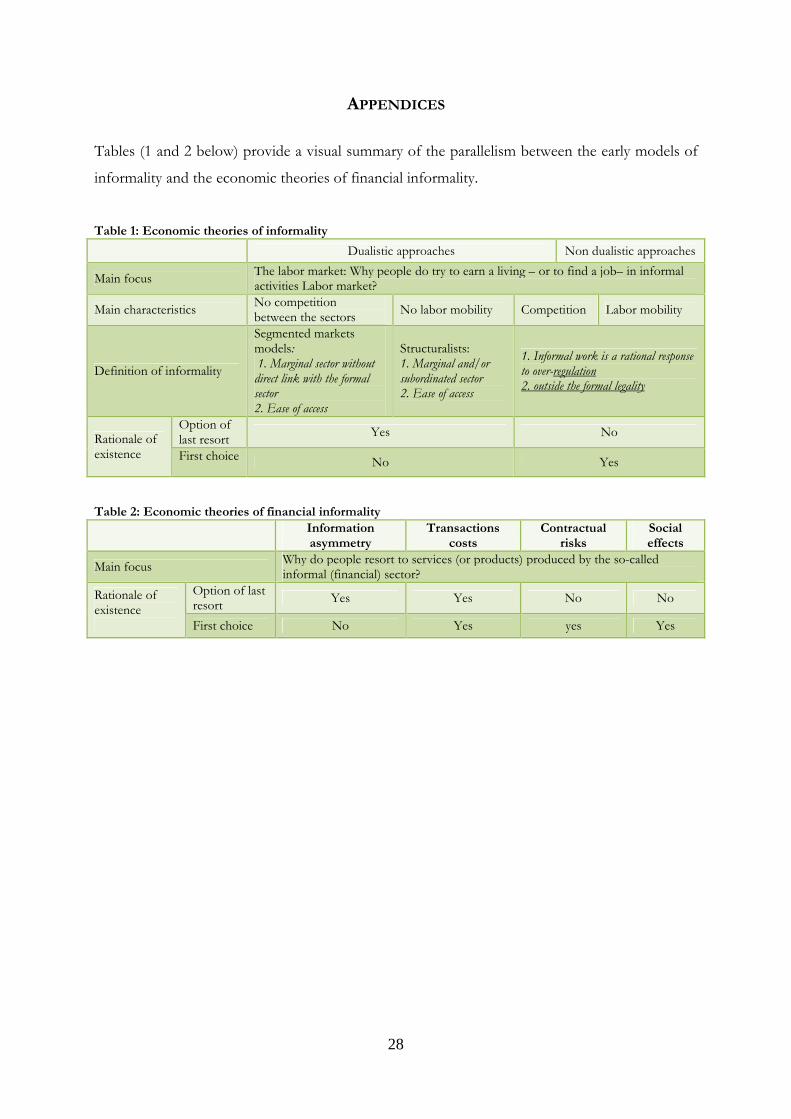

Tables (1 and 2 below) provide a visual summary of the parallelism between the early models of

informality and the economic theories of financial informality.

Table 1: Economic theories of informality

Dualistic approaches Non dualistic approaches

Main focus The labor market: Why people do try to earn a living – or to find a job– in informal activities Labor market?

Main characteristics No competition between the sectors

No labor mobility Competition Labor mobility

Definition of informality

Segmented markets models: 1. Marginal sector without direct link with the formal sector 2. Ease of access

Structuralists: 1. Marginal and/or subordinated sector 2. Ease of access

1. Informal work is a rational response to over-regulation 2. outside the formal legality

Rationale of existence

Option of last resort

Yes No

First choice No Yes

Table 2: Economic theories of financial informality

Information asymmetry

Transactions costs

Contractual risks

Social effects

Main focus Why do people resort to services (or products) produced by the so-called informal (financial) sector?

Rationale of existence

Option of last resort

Yes Yes No No

First choice No Yes yes Yes