abbott’s xience, a small medical device used to prop open ......abbott’s xience, a small medical...

TRANSCRIPT

Thesis/Key Points

Abbott Laboratories is a shareholder-friendly company poised to make strong gains throughout its various life-science businesses and across multiple geographies, particularly within high growth markets where Abbott is strategically capturing a leadership position. I believe that Abbott Laboratories is an attractive long because the market is grossly underestimating Abbott’s potential market share gains, leading to an unjustifiably low valuation. The following thesis points, derived from fundamental research and VAR, support the conclusion that the company’s stock remains largely undervalued.

Abbott Laboratories possesses a highly-diversified portfolio of popular pharmaceutical and other health care products. Abbott’s strongest feature is that it’s highly diversified — the company sells everything from pharmaceuticals to medical devices to nutritional products — allowing it to have a very wide customer base that can withstand some volatility in the macro economy. The company’s two strongest products are its rheumatoid arthritis drug Humira and its drug-eluting stent Xience, a small medical device used to prop open arteries. As of the end of the third quarter, Xience had more than 30% of the market share for the worldwide stent market. Meanwhile, Humira had sales of $2.1 billion in the third quarter. Abbott Laboratories also makes pharmaceuticals for HIV infection, oncology medicines, anesthesia products, anti-infectives, immunoassay systems, various products for people with diabetes, and medical devices for the eye.

Abbott Laboratories has monopolistic characteristics to its product offerings. Abbott Laboratories faces minimal threats to its dominance in certain product categories where Abbott Laboratories sells its most widely used drugs. The company’s products are also protected from intellectual property infringements for the life of their respective patents, ensuring a predictable stream of steady income for the foreseeable future. Drugs also exhibit recession-proof demand, as health care is considered of vital importance to end-users, and government is consistently a major contributor in paying for the cost of pharmaceutical products such as those sold by Abbott Laboratories. Barriers to entry are enormous and existing companies like Abbott Laboratories tend to marginalize new entrants through more advanced research and development, a broader product offering, more extensive legal and regulatory resources, and superior marketing and distribution capabilities.

Abbott Laboratories is using smart acquisitions to boost its dominance in key growth markets. Abbott Laboratories has a long-established history of completing numerous successful acquisitions each year in order to complement its product offering, create new business segments, and enter entirely new geographic markets. One example of this strategy was executed in 2010 as Abbott purchased the Indian drug maker Piramal Healthcare for $3.7 billion, increasing its presence in the fast-growing emerging markets and expanding its portfolio of low-priced drugs. Piramal, based in Mumbai, makes generic and branded drugs in nine plants in India, Britain, and Canada, and has the largest sales force in India with more than 6,000 representatives. With the addition of Piramal’s operations to Abbott’s existing business in India, Abbott will become the largest drug company in India with 7 percent of the market. In the same year, Abbott acquired Solvay Pharmaceuticals of Belgium, which has a substantial emerging market presence, for $6.6 billion.

Abbott Laboratories should continue to grow on account of a robust product pipeline. ABT has continued to make progress advancing its internal pipeline and adding late-stage pipeline opportunities through licensing and acquisitions. Abbott currently has more than 30 devices across its cardiovascular, vision care, and diabetes pipelines, including next-generation lens technologies and game-changing innovations, such as a bioresorbable vascular scaffold. Abbott is also developing leading-edge, science-based nutrition products and improving formulations of its brands to better serve the needs of consumers.

Abbott Laboratories will benefit from embracing opportunities in emerging markets. Helping to further insulate Abbott from any sort of severe market volatility is its expansive international business. During the second quarter of 2011, more than half of its $4.9 billion in pharmaceutical sales came from outside of the US, while international sales for its diagnostic tools were more than double domestic sales. “Emerging markets represent one of the greatest opportunities in health care,” the chairman and chief executive of Abbott, Miles D. White, said. Emerging markets already make up more than 20 percent of Abbott’s overall business. Drug sales are growing quickly in emerging markets in part because of better diagnosis and an increase in diseases associated with a sedentary lifestyle, like diabetes. Emerging markets will account for 30 to 40 percent of pharmaceutical sales growth in the next 10 years, according to estimates by PricewaterhouseCoopers.

1

Ryan Rechkemmer (rhr2fk) • Manager • CLAS 2014

November 20, 2011

Abbott Laboratories (NYSE: ABT) Memo

EBITDA: $11.03B

EPS: 4.51

Beta: 0.34

Short Ratio: 1.60

20 Nov. 2011 Share Price: $53.52

Market Cap: $83.49B

52-Week Range: $45.07 – 55.61

2010 Revenue: $35.17B

Company Description

Abbott Laboratories is a global, broad-based health care company

devoted to the discovery, development, manufacture, and marketing of

pharmaceuticals and medical products, including nutritionals, devices,

and diagnostics. The company employs approximately 90,000 people

and markets its products in more than 130 countries.

Misperception

Investors are often either overly wary of pharmaceutical companies on account of an impending patent cliff or are mesmerized by high dividend yields and disregard longer-term fundamentals. However, Abbott is overlooked despite its fairly attractive dividend, solid earnings growth, and stable product offering. Even amid a drastically changing political climate and occasionally volatile health care market, Abbott Laboratories' wide moat, large size, non-cyclicality, and high levels of cash make the company exceptionally solvent through most any economic conditions, as evidenced by Abbott’s superior AA corporate credit rating. The market has exaggerated the competitive threats to Abbott’s largest source of revenue, Humira, which has patent protection until 2016.

As of September, the company had about $8.0 billion in cash and short-term investments on its books, and unlike most of its peers, Abbott isn’t facing any sort of major patent cliff in the next few years that would make it susceptible to competition from generics. Abbott Chief Executive Miles White said that diversity is key to the company’s success: “In a world where you have to balance quarterly performance with long-term R&D that can be anywhere from 4 to 12 years, depending on whether you're in devices or diagnostics or pharmaceuticals, diversity is a lot better for us. That's how we manage sustainable, stable returns that investors seem to look for and expect, while protecting those long-term investments in R&D.”

Rather than act as a liability for the company, Abbott’s dividend, which has been paid to shareholders continuously since 1926 and which has been increased for the past 38 consecutive years, is instead evidence of management’s commitment to rewarding shareholders and serves as a stabilizing factor for the stock. Furthermore, while Abbott is trading at a much-deserved premium to its pharmaceutical peers, the stock is undervalued relative to its own historical averages. Given Abbott’s attractive long-term fundamentals, shares are even more attractively valued at current levels.

How It Plays Out Over the past few years, Abbott has increased its focus on the higher-margin pharmaceutical and medical device divisions by making

numerous acquisitions to improve its business mix. Abbott can be expected to continue pursuing strategic acquisitions, as well as partnerships and alliances, as a means to broaden the business and enhance growth.

Abbott Laboratories going forward can still be anticipated to prosper in a changing regulatory and political landscape. Recent landmark health care reform legislation will expand access to insurance coverage, and this carries both positive and negative consequences. Positive outcomes include higher volumes of drugs and medical procedures as more people would have health coverage. Negative outcomes, however, include the potential for downward pressure on medical product pricing and additional taxation across the sector. The Supreme Court is scheduled to review the constitutionality of key passages in the law by June of 2012, thus politics will continue to impact Abbott.

Demographic trends provide a tailwind for the health care industry in general. The over-60 age group will be one of the fastest-growing age groups over the next couple of decades, and utilization of health care products such as prescription drugs and devices increases with age. Continued innovation and new treatment options for unmet medical diseases such as diabetes and cancer favor sustained growth in demand for Abbott Laboratories’ health care products. The company is actively seeking to increase the size of its addressable market, as evidenced by Abbott’s efforts to expand its distribution channels abroad, particularly in high growth markets such as India.

Risks / What Signs Would Indicate We Are Wrong?

Generic competition for ABT’s pharmaceutical products is likely to arise at various times in the future, due in part to patent expirations, which could depress revenue for certain products. This would have a larger effect when applicable to such blockbuster drugs as Humira, which accounted for nearly 18% of ABT’s total revenue in 2010 and is expected to be a major engine for medium-term growth.

While the company remains dedicated to expanding research and development, with new pharmaceutical drugs and medical devices currently in its pipeline, regulatory approval from the FDA and profitable commercialization of these products is uncertain.

Impending federal healthcare legislation could adversely affect the pharmaceutical industry, especially through potential changes in Medicare and Medicaid spending and adverse negotiated pricing terms that would exert negative pressures on the profitability of companies such as Abbott. Regulatory oversight could also prove burdensome in the process of new product development and pricing.

The pace of recent acquisitions could be interpreted as an attempt by the company to artificially boost earnings through inorganic growth, and could result in operating inefficiencies, reorganizational and integration costs, or a failure to realize anticipated synergies.

Pharmaceutical companies are susceptible to litigation from competitors over patent rights and customers concerning product safety. Abbott has been implicated in fraudulent drug pricing and marketing conduct and engaging in other questionable practices in the past.

Signposts / Follow-Up

Abbott Laboratories has a solid record of revenue growth, yet the company has a more volatile history with controlling costs. It will be important to observe changes in ABT’s profit margins, R&D expenses as a percentage of revenue, and free cash flow figures.

The effects of U.S. health care reform and new R&D venture costs, as well as the pace of future acquisitions and revenue growth in emerging markets, should be followed.

It will be vital to track the progress of the company’s product pipeline, especially the strength of results from late stage clinical trials for prospective blockbuster pharmaceuticals and medical devices, as Abbott’s continued profitability hinges on its ability to successfully gain regulatory approval for highly demanded new products.

2

Ryan Rechkemmer (rhr2fk) • Manager • CLAS 2014

November 20, 2011

3

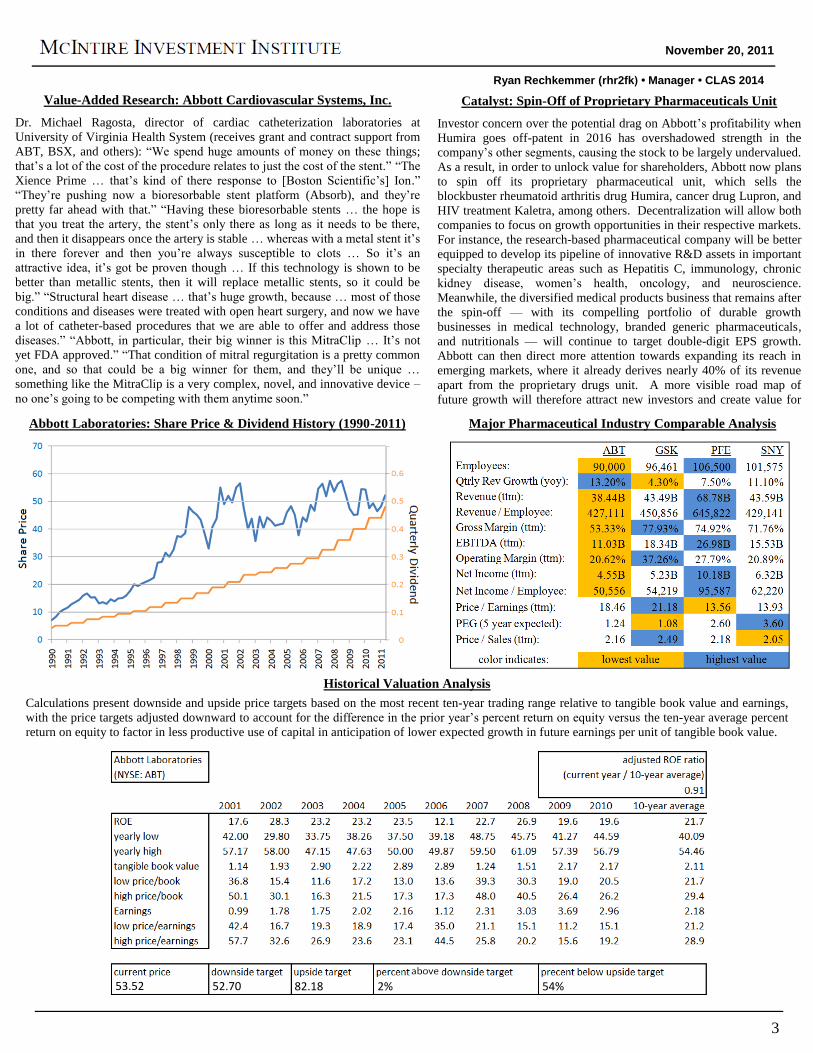

Abbott Laboratories: Share Price & Dividend History (1990-2011) Major Pharmaceutical Industry Comparable Analysis

Historical Valuation Analysis

Calculations present downside and upside price targets based on the most recent ten-year trading range relative to tangible book value and earnings,

with the price targets adjusted downward to account for the difference in the prior year’s percent return on equity versus the ten-year average percent

return on equity to factor in less productive use of capital in anticipation of lower expected growth in future earnings per unit of tangible book value.

Ryan Rechkemmer (rhr2fk) • Manager • CLAS 2014

November 20, 2011

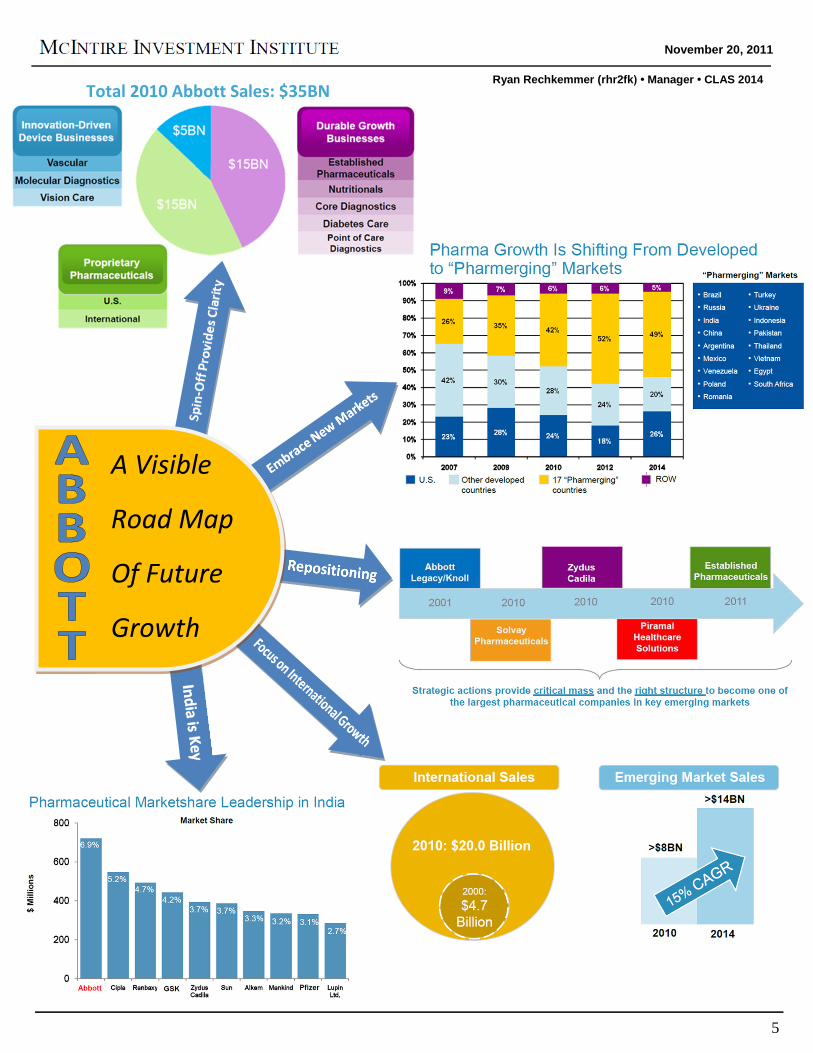

Catalyst: Spin-Off of Proprietary Pharmaceuticals Unit

Investor concern over the potential drag on Abbott’s profitability when

Humira goes off-patent in 2016 has overshadowed strength in the

company’s other segments, causing the stock to be largely undervalued.

As a result, in order to unlock value for shareholders, Abbott now plans

to spin off its proprietary pharmaceutical unit, which sells the

blockbuster rheumatoid arthritis drug Humira, cancer drug Lupron, and

HIV treatment Kaletra, among others. Decentralization will allow both

companies to focus on growth opportunities in their respective markets.

For instance, the research-based pharmaceutical company will be better

equipped to develop its pipeline of innovative R&D assets in important

specialty therapeutic areas such as Hepatitis C, immunology, chronic

kidney disease, women’s health, oncology, and neuroscience.

Meanwhile, the diversified medical products business that remains after

the spin-off — with its compelling portfolio of durable growth

businesses in medical technology, branded generic pharmaceuticals,

and nutritionals — will continue to target double-digit EPS growth.

Abbott can then direct more attention towards expanding its reach in

emerging markets, where it already derives nearly 40% of its revenue

apart from the proprietary drugs unit. A more visible road map of

future growth will therefore attract new investors and create value for

shareholders.

53.52 52.70 82.18 2% 54%

Value-Added Research: Abbott Cardiovascular Systems, Inc.

Dr. Michael Ragosta, director of cardiac catheterization laboratories at

University of Virginia Health System (receives grant and contract support from

ABT, BSX, and others): ―We spend huge amounts of money on these things;

that’s a lot of the cost of the procedure relates to just the cost of the stent.‖ ―The

Xience Prime … that’s kind of there response to [Boston Scientific’s] Ion.‖ ―They’re pushing now a bioresorbable stent platform (Absorb), and they’re

pretty far ahead with that.‖ ―Having these bioresorbable stents … the hope is

that you treat the artery, the stent’s only there as long as it needs to be there,

and then it disappears once the artery is stable … whereas with a metal stent it’s

in there forever and then you’re always susceptible to clots … So it’s an

attractive idea, it’s got be proven though … If this technology is shown to be

better than metallic stents, then it will replace metallic stents, so it could be

big.‖ ―Structural heart disease … that’s huge growth, because … most of those

conditions and diseases were treated with open heart surgery, and now we have

a lot of catheter-based procedures that we are able to offer and address those

diseases.‖ ―Abbott, in particular, their big winner is this MitraClip … It’s not

yet FDA approved.‖ ―That condition of mitral regurgitation is a pretty common

one, and so that could be a big winner for them, and they’ll be unique …

something like the MitraClip is a very complex, novel, and innovative device –

no one’s going to be competing with them anytime soon.‖

Ryan Rechkemmer (rhr2fk) • Manager • CLAS 2014

November 20, 2011

4

5

A Visible

Road Map

Of Future

Growth

Total 2010 Abbott Sales: $35BN

Ryan Rechkemmer (rhr2fk) • Manager • CLAS 2014

November 20, 2011