a01-depreciation overview eng final...depreciation method used, which in turn affects the amount of...

TRANSCRIPT

Topic A01: Depreciation Topic Overview P.1

BAFS Learning and Teaching Example As at April 2009

Learning Objectives: 1. To understand the concept of depreciation; 2. To comprehend methods of calculating depreciation charges; 3. To identify the factors to be considered when choosing a depreciation method; and 4. To determine the impact on profits by using different depreciation methods. Overview of Contents: Lesson 1 Concept of Depreciation Lesson 2 Common Methods of Calculating Depreciating Charges Lesson 3 Depreciation on Disposal of Fixed Assets Resources:

Topic Overview, Teaching Plan and Answers to Student Worksheet PowerPoint Presentation Student Worksheet

Suggested Activities:

Group Discussion Class Exercises Game

Topic Overview Topic BAFS Elective Part – Accounting Module – Financial Accounting

A01: Balancing Day Adjustments Relating to the Preparation of Financial Statements - Depreciation

Level S5 / S6 Duration 3 lessons (40 minutes per lesson)

Topic A01: Depreciation Topic Overview P.2

BAFS Learning and Teaching Example As at April 2009

Lesson 1

Theme Concept of Depreciation Duration 40 minutes Expected Learning Outcomes: Upon completion of this lesson, students will be able to: 1. Define depreciation; and 2. Identify the methods of calculating depreciation charges. Special requirement: As students are required to surf the Internet for information in Activity 3, teachers are suggested to conduct lessons in a room with appropriate equipment or in the computer room. Teaching Sequence and Time Allocation:

Activities Reference Time Allocation

Part I: Introduction Review the concept of depreciation An example of a Ferrari car is used to help students

grasp the concept of depreciation including the following terms:

Cost. Estimated useful life. Expected scrap value.

Activity 1 - Set up your own business and acquire

the fixed assets Students are asked to form groups of four or five

to set up their own business. The business can be a: Restaurant, Game Centre, Tutorial Centre, Karaoke or Supermarket.

Students discuss the name of the company, nature

of the business, the capital required, and most importantly, to list 5 essential fixed assets they must acquire. They record discussion outcomes on Worksheet p. 1.

PPT #1-9

PPT #10-12

Student Worksheet

p.1

5 minutes

10 minutes

Topic A01: Depreciation Topic Overview P.3

BAFS Learning and Teaching Example As at April 2009

Students are invited to provide verbal feedback.

Note that worksheet information will be used in future activities.

There is no right or wrong answer. Teacher may

verify and comment on practically and reasonableness of answers.

Part II: Content

Teacher tells students how to estimate useful life, calculate residual value, depreciable amount and discuss the depreciation methods.

Activity 2 - Group discussion

This is an extension of Activity1. Students remain in the same group to determine the estimated useful life, residual value and depreciable amounts of their fixed assets; and identify the possible depreciation methods to apply.

Groups will present their discussion outcomes.

Other classmates are encouraged to comment on the outcomes.

Teacher summarises suggested methods and

explains that there are various methods of allocating depreciable amounts.

PPT #13-16

Student Worksheet

pp.1 - 2

10 minutes

Activity 3 - A survey Students are divided into groups of four or five to

conduct a survey on deprecation methods used by listed companies.

Students choose listed companies from the assigned industry.

Students complete the survey and present their findings in the next lesson.

PPT #17

Student Worksheet

p.3

15 minutes

Part III: Conclusion Teacher concludes lesson and highlights the key

concepts. 5 minutes

Topic A01: Depreciation Topic Overview P.4

BAFS Learning and Teaching Example As at April 2009

Lesson 2

Theme Common Methods of Calculating Depreciation Charges Duration 40 minutes Expected Learning Outcomes: Upon completion of this lesson, students will be able to: 1. Calculate depreciation using the straight-line and reducing balance methods; 2. Compare the straight-line and reducing balance methods; and 3. Identify the factors to consider when choosing a depreciation method. Teaching Sequence and Time Allocation:

Activities Reference Time Allocation

Part I: Introduction Teacher recaps the calculation of depreciation using

straight-line method and reducing balance method.

PPT #18-19 3 minutes

Part II: Contents Survey presentation

Two representatives from each group present their findings on depreciation methods used by listed companies.

Based on their findings, students are asked to identify which depreciation methods are most widely used.

Teacher summarises and concludes the discussion.

PPT #20

Student Worksheet

p.3

7 minutes

Activity 4 – Case study and group discussion Students remain in the same group and continue to

complete the case study. Students complete Student Worksheet pp.4-7 to:

determine the annual depreciation and the impact of depreciation on profit

compare the straight-line and reducing balance methods

discuss the factors affecting the choice of depreciation methods

compute depreciation if their assets are bought for fractional periods

Compute depreciation after a revision of

PPT #21-26

Student Worksheet

pp. 4 -7

20 minutes

Topic A01: Depreciation Topic Overview P.5

BAFS Learning and Teaching Example As at April 2009

depreciation estimates Students present their answers, summarise the

differences and conclude the discussion.

Activity 5 - A mini-case Students remain in the same group to complete

Student Worksheet p.8, which reviews the depreciation charges and net book value from incomplete records.

Students present their answers, summarise the differences and conclude their discussion.

PPT #27-28

Student

Worksheet p. 8

7 minutes

Part III: Conclusion Teacher concludes lesson and highlights key concepts

learned. 3 minutes

Topic A01: Depreciation Topic Overview P.6

BAFS Learning and Teaching Example As at April 2009

Lesson 3

Theme Depreciation on Disposal of Fixed Assets Duration 40 minutes Expected Learning Outcomes: Upon completion of this session, students will be able to: 1. master the accounting treatment on disposal of fixed assets; and 2. handle the case of disposal in the form of trade-in. Teaching Sequence and Time Allocation:

Activities Reference Time Allocation

Part I: Introduction Teacher discusses the following issues relating to

disposal of fixed assets with receipt of cash: Accounting entries. Determination of profit/loss on disposal.

PPT

#29-32

5 minutes

Part II: Content Teacher discusses the following issues relating to

disposal of fixed assets in form of ‘Trade-in’: Accounting entries. Determination of profit/loss on disposal.

PPT

#33-35

5 minutes

Activity 6 - An auction game Students form groups of 4 or 5. Groups buy and sell assets in an open auction. They make accounting entries for buying and

selling. Concept of accumulated depreciation, net book

values and profit of disposal is applied.

PPT #36

Student

Worksheet p.9

25 minutes

Part III: Conclusion Teacher concludes lesson and highlights key points

learned. PPT #37 5 minutes

Topic A01: Depreciation Topic Overview P.7

BAFS Learning and Teaching Example As at April 2009

Suggested Answers of Worksheet Activity 1

SSeett uupp yyoouurr oowwnn bbuussiinneessss aanndd aaccqquuiirree tthhee ffiixxeedd aasssseettss Name of Company: ________________________________________________ Nature of Business (Choose one): Restaurant/ Game Centre/

Tutorial Centre / Karaoke/ Supermarket

The five most valuable fixed assets Fixed Asset Cost

(HK$) (A)

Estimated Useful Life

(Years)

Residual Value (HK$) (B)

Depreciable Amount (HK$)

(A) – (B) 1. Building 8,000,000 40 120,000 7,880,000

2. Furniture & fixtures

2,000,000 15 70,000 1,930,000

3. Office equipment 500,000 10 3,000 497,000

4. Air-conditioning system

1,000,000 10 6,000 994,000

5. Computer system 800,000 5 25,000 775,000

Topic A01: Depreciation Topic Overview P.8

BAFS Learning and Teaching Example As at April 2009

Activity 2 - Group Discussion It’s time to identify the fixed assets depreciation methods to be applied as stated in Worksheet p.1. Discuss how you will allocate the depreciable asset amount over the useful life.

Fixed Asset Depreciation Methods

1. Building Straight-line

2. Furniture & fixtures Straight-line

3. Office equipment Reducing balance

4. Air-conditioning system Reducing balance

5. Computer system Reducing balance

Activity 3 - A Survey Objective: To identify the depreciation methods used by listed companies Task: Each group of four or five students will:

(1) choose a listed company from an assigned industry; (2) visit the website of the company and access the most recent

annual report; (3) identify the various depreciation methods from the notes of

the financial statements; (4) summarise the findings in the following table.

Answer: (1) Name of company:

Hong Kong and China Gas Co. Ltd.

Topic A01: Depreciation Topic Overview P.9

BAFS Learning and Teaching Example As at April 2009

(2) Findings: Asset type Depreciation methods used

Property, plant and equipment

straight-line

Activity 4 - Case Study and Group Discussion Read the following case carefully and complete the tasks. Suppose your company has acquired all fixed assets identified in lesson 1 on 1 January Year 1. Annual depreciation expense changes by the depreciation method used, which in turn affects the amount of profit. To facilitate fund raising, your friend suggests you to choose the depreciation method that will maximise the reported profits for the first two years.

Assume either the straight-line or reducing balance method will be used. If necessary, state any other reasonable assumptions. Tasks:

(1) Determine the annual depreciation charges for the first five years.

(a) Using the method that maximises first 2 yrs reported profits.

Annual Depreciation ($) Fixed Asset

Depreciation method Year 1 Year 2 Year 3 Year 4 Year 5

1 Straight-line 197,000 197,000 197,000 197,000 197,000

2 Straight-line 128,667 128,667 128,667 128,667 128,667

3 Straight-line 49,700 49,700 49,700 49,700 49,700

4 Straight-line 99,400 99,400 99,400 99,400 99,400

5 Straight-line 155,000 155,000 155,000 155,000 155,000

Total 629,767 629,767 629,767 629,767 629,767

Topic A01: Depreciation Topic Overview P.10

BAFS Learning and Teaching Example As at April 2009

(b) Using the alternative method

*Teacher can assume different rates of depreciation for calculation. Annual Depreciation ($) Fixed

Asset Depreciation

Method* Year 1 Year 2 Year 3 Year 4 Year 5 1 Reducing

balance (10%) 800,000 720,000 648,000 583,200 524,880

2 Reducing balance (20%)

400,000 320,000 256,000 204,800 163,840

3 Reducing balance (40%)

200,000 120,000 72,000 43,200 25,920

4 Reducing balance (40%)

400,000 240,000 144,000 86,400 51,840

5 Reducing balance (50%)

400,000 200,000 100,000 50,000 25,000

Total 2,200,000 1,600,000 1,220,000 967,600 791,480

(2) Compare the annual depreciation patterns using straight-line and reducing balance methods. Straight-line: Depreciation charge spreads evenly over the useful life.

Reducing balance: A higher depreciation charge in the early years.

(3) Discuss the factors to consider when choosing the depreciation method. The depreciation method selected should reflect the pattern of

use according to which the asset’s economic benefits are

consumed by the company. For example, applying the straight

line method for assets with constant uniform service; applying

reducing balance method if there is a loss in asset value in a

certain period of time.

Topic A01: Depreciation Topic Overview P.11

BAFS Learning and Teaching Example As at April 2009

(4) Assuming that “Fixed asset No. 5” was purchased on 8 August Year 1.

(a) Suggest two methods for calculating depreciation expenses for fractional periods.

(i) Provide a full period asset depreciation in use at the

end of the period. This method implies that no

depreciation will be allocated for the year, if the asset

is sold during the year.

(ii) Based on one month's depreciation provision for one

month ownership, i.e. round depreciation to nearest

whole month.

(b) Calculate the straight-line asset depreciation charges for the year ended 31 December Year 1, using methods (i) and (ii) as suggested in (a) above. Assume no asset disposal during the year.

(i) $155,000

(ii) $155,000 x 5/12

= $64,583

(5) Assume after one year of operation, you decide that the expected useful life of “Fixed asset No. 1” should last for 2 more years. Discuss and revise the annual depreciation charges previously determined in (1a).

Annual Depreciation ($) Fixed

Asset Year 1 Year 2 Year 3 Year 4 Year 5

1 197,000 187,390 187,390 187,390 187,390

Topic A01: Depreciation Topic Overview P.12

BAFS Learning and Teaching Example As at April 2009

Activity 5 - A Mini-Case

Read the following carefully and complete tasks. Mr. White, a manufacturer, bought two machines at the same price on 1 January Year 1. The machines have an estimated useful life of 5 years and a residual value of $800. As proper books of accounts are not kept, it is uncertain whether the straight-line or the reducing balance method was applied. The only information available is:

Machine A: Depreciation charges for year 1 and 2 are $1,055. Machine B: Depreciation charges for year 1 and 2 are $2,025

and $1,350 respectively. Task: Input missing data into the following table. Machine

A B

Depreciation method used Straight-line Reducing balance

Depreciation rate used 1/5 1/3

Costs $6,075 $6,075

Net book value at the end of Year 2 $3,965 $2,700

Depreciation charge for Year 3 $1,055 $900

Topic A01: Depreciation Topic Overview P.13

BAFS Learning and Teaching Example As at April 2009

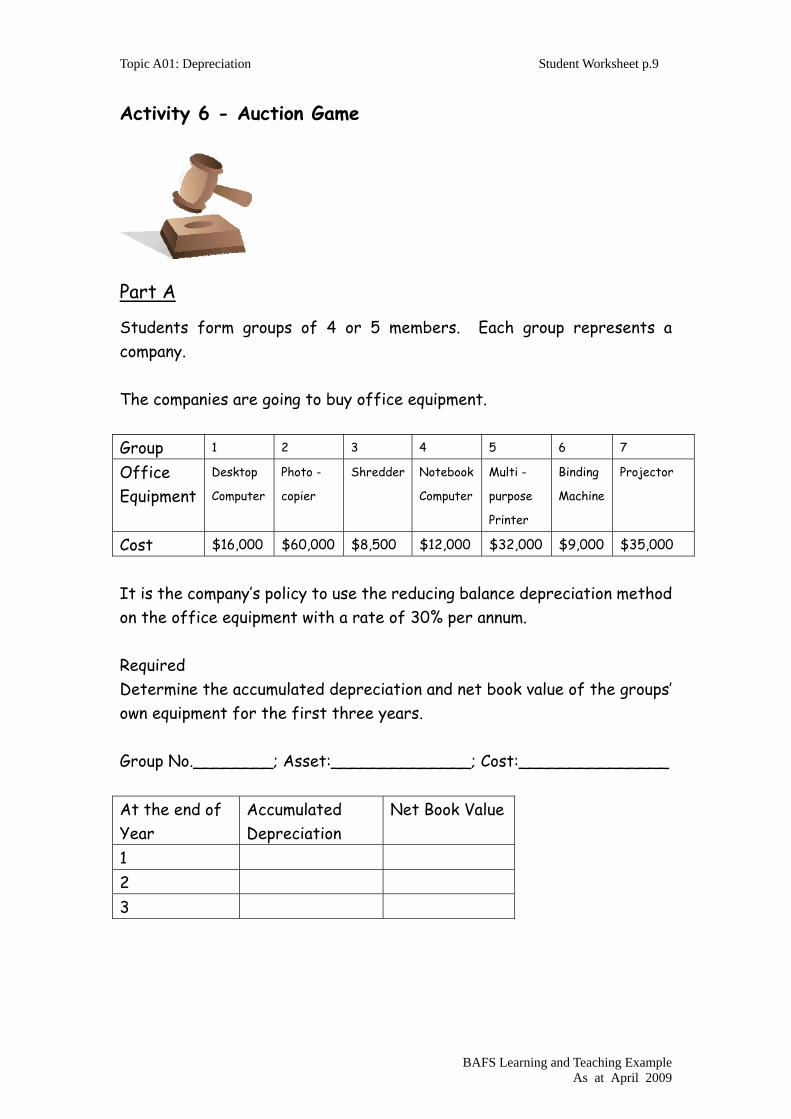

Activity 6 - Auction Game Part A Students form groups of 4 or 5 members. Each group represents a company. The companies are going to buy office equipment. Group 1 2 3 4 5 6 7

Office Equipment

Desktop Computer

Photo - copier

Shredder Notebook Computer

Multi - purpose Printer

Binding Machine

Projector

Cost $16,000 $60,000 $8,500 $12,000 $32,000 $9,000 $35,000

It is the company’s policy to use the reducing balance depreciation method on the office equipment with a rate of 30% per annum. Required Determine the accumulated depreciation and net book value of the groups’ own equipment for the first three years. Group No.___1_____; Asset: Desktop Computer__; Cost:_$16,000_ At the end of Year

Accumulated Depreciation ($)

Net Book Value ($)

1 4,800 11,200 2 8,160 7,840 3 10,512 5,488 Part B (Please refer to information in Part A) Time passes fast as 2 years has elapsed since purchasing the office equipment. Your company wants to sell the equipment to the second hand market prior to purchasing new. The second hand buyers are other student groups that will bid for your equipment in an open auction. The group offering the highest price will get your equipment.

Topic A01: Depreciation Topic Overview P.14

BAFS Learning and Teaching Example As at April 2009

Here are the auction steps: Step 1 How much does each group have? Teacher adds up the net book values of all groups’ equipment (Just call it ‘total net book values’). Cash owned by each group is determined by the following formula: Cash owned by each group =Total Net Book Values /No. of Groups x (1 + 10%) (The figure should be rounded up to the nearest thousand dollars) For example, if the ‘total net book values’ are $103,540 and there are 7 groups. Then, each group may have: $103,540/7 x (1+10%) = $16,271 So, in this example, each group should have $16,000 cash. Step 2 Why do other groups want to bid for your equipment? The group who buys the largest number of equipment wins a prize! Buyers can: 1. pay cash to the seller or 2. purchase the equipment as a ‘trade-in’. The ‘trade-out’ value of each

piece of equipment is pre-determined, for the purpose of this game, as $5,000.

Additional points to note 1. Game is limited to 25 minutes. No limits on each bid. 2. Once a company wins the bid, it must buy the asset as decisions are final. 3. Students must act professional and respectful to all bidders during the

bidding process.

Topic A01: Depreciation Topic Overview P.15

BAFS Learning and Teaching Example As at April 2009

After a series of fierce competition, the results of the auction are: Note to teacher: The below just shows one of the possible outcomes of the auction. Net Book

Value ($) (figures provided by each group)

Bought by (Group)

Auction Price ($)

Group 1 Desktop Computer

5,488 6 4,000

Group 2 Photocopier

20,580 5 16,000

Group 3 Shredder

2,916 1 3,000

Group 4 Notebook Computer

4,116 3 14,000

Group 5 Multi-purpose Printer

10,976 1 Trade-in the Printer with Shredder + Cash $2,000

Group 6 Binding Machine

3,087 4 15,000

Group 7 Projector 12,005 1 14,000 The total number of equipment owned by each group is: Group No. of Equipment 1 2 2 0 3 1

Topic A01: Depreciation Topic Overview P.16

BAFS Learning and Teaching Example As at April 2009

4 1 5 1 6 1 7 0 The winner of the Auction Game is Group __1__ Note to Teacher: Do not use cash total amount to determine the winner because the cost of asset of each group is different. Part C: To record the transactions in accounting records of own group Your group no.:______1________ 1. Cash Movement $ Opening balance (This figure is calculated with the aforementioned formula. Let’s use $16,000)

16,000

Add: Sale to Group _6__ 4,000 Less: Purchase from Group _3_ (3,000) Purchase from Group _5_ (2,000) Purchase from Group _7_ (14,000) Closing balance 1,000 2. Accounting Entries As seller (Asset sold:_Desktop Computer__) $ $ Dr. Cash 4,000 Dr. Provision of Depreciation -

Office Equipment (Desktop Computer) 10,512

Dr. Profit & Loss – Loss on Disposal 1,488 Cr. Office Equipment (Desktop Computer –

Cost) 16,000

--------------------------------------------------------------------------------------

Topic A01: Depreciation Topic Overview P.17

BAFS Learning and Teaching Example As at April 2009

As buyer pays with 100% cash (Asset bought: Shredder ) $ $ Dr. Office Equipment (Shredder – Cost) 3,000 Cr. Cash 3,000 As buyer pays with 100% cash (Asset bought: Projector ) $ $ Dr. Office Equipment (Projector – Cost) 14,000 Cr. Cash 14,000 -------------------------------------------------------------------------------------- As buyer, by way of trade-in (Asset traded-in:_Multi-purpose printer_; Asset traded out: Shredder ) $ $ Dr. Office Equipment (Multi-purpose Printer-

Cost) 7,000

Dr. (Shredder just purchased from auction, no provision of depreciation required)

Cr. Office Equipment (Shredder – Cost) 3,000 Cr. Cash 2,000 Cr. Profit & Loss – Profit on Exchange of

Equipment 2,000

1

BAFS Elective Part Accounting Module –Financial Accounting

Topic A01: Balancing Day Adjustments Relating to the Preparation of Financial Statements - Depreciation

Technology Education Section Curriculum Development Institute

Education Bureau, HKSARGApril 2009

IntroductionThis session aims to help students understand the concept and the calculation of depreciation. Impacts on profits by using different depreciation methods are also determined.

DurationThree 40-minute lessons

ContentsLesson 1 - Concept of DepreciationLesson 2 - Common Methods of Calculating Depreciating ChargesLesson 3 - Depreciation on Disposal of Fixed Assets

2

Topic A01Depreciation 2 BAFS Compulsory Part

Learning and Teaching Example

Lesson One

Concept of Depreciation

Lesson 1

Students are able to define what depreciation is and identify the methods of calculating depreciation charges.

3

Topic A01Depreciation 3 BAFS Compulsory Part

Learning and Teaching Example

Concept of Depreciation

Almost every fixed asset has finite useful life.Hence the value of a fixed asset decreases year by year.We call the decrease in value, the ‘Depreciation’.

Teacher may ask students to raise some examples of fixed assets as a warm up of the lesson. (Answers may be buildings, motor vehicles and machines, etc.)

4

Topic A01Depreciation 4 BAFS Compulsory Part

Learning and Teaching Example

Do you want to own a Ferrari?

Teachers may use the example to help students build a clear concept of depreciation.

5

Topic A01Depreciation 5 BAFS Compulsory Part

Learning and Teaching Example

If yes, how much does it cost?

Around HK$ 2 million

There is no exact answer. Teacher should encourage students to speculate.

Teacher can research the market price for accuracy. HK$2 million is just the market price of a common Ferrari at the time of this writing.

The cost of a fixed asset is its original purchase cost. In this case, HK$2 million is the cost of the car.

6

Topic A01Depreciation 6 BAFS Compulsory Part

Learning and Teaching Example

How long will it last for?

Nobody knows. But it may be 20 years!

There is no exact answer. Teachers should encourage students toguess.

Teacher can also Inform students that the accountant will make judgments based on professional knowledge.

’20 years’ in this case is the estimated useful life of the car. Estimated useful life is the period over which an asset is expected to be available for use by an entity. (HKAS16)

7

Topic A01Depreciation 7 BAFS Compulsory Part

Learning and Teaching Example

How much will it cost at the end of its life?

No one really knows …. but the scrap value of it may be HK$10,000.

Here is another instance when an accountant must make a professional judgment.

The HK$10,000 is called the expected scrap value.

8

Topic A01Depreciation 8 BAFS Compulsory Part

Learning and Teaching Example

How much does the value of this Ferrari drop during these 20 years?

This is the depreciation of the Ferrari during the 20 years.

Bingo! It is HK$1,990,000!

Cost minus Expected Scrap Value = HK$2,000,000 - HK$10,000 = HK$1,990,000

Actually, this figure is the asset depreciation during its estimated useful life. Depreciation can be viewed as the reduction of asset value during the estimated useful life.

9

Topic A01Depreciation 9 BAFS Compulsory Part

Learning and Teaching Example

Depreciation

The reduction of the asset value during the estimated

useful life.

Teacher provides the definition of depreciation.

10

Topic A01Depreciation 10 BAFS Compulsory Part

Learning and Teaching Example

Causes of Depreciation

Physical deteriorationObsolescenceLimited period of use

Teacher shows the causes of depreciation.

Remarks:1. Physical deterioration is due to asset use. For example, machines,

motor vehicles and buildings, etc., will wear out after years of use.2. Obsolescence means out-of-date. Computers is an example to

illustrate obsolescence.3. Limited period of use arises when assets have a finite legal life, for

examples, lease of building and patent rights, etc.

11

Topic A01Depreciation 11 BAFS Compulsory Part

Learning and Teaching Example

Activity 1

Acquire fixed assets for your new business

Teacher refers to student worksheet p.1 for Activity1.

Students will learn the concept of depreciation through the starting of a virtual business.

Students’ tasks include purchasing the new business fixed assets.

12

Topic A01Depreciation 12 BAFS Compulsory Part

Learning and Teaching Example

Activity 1

Form group of four to five students. Your group is going to set up your own business. The nature of business can be restaurant, game centre, tutorial centre, karaoke or supermarket.Discuss among yourselves the name of the company and the nature of business.

Students can choose the business that they are interested most and assign the name of the company for the sense of ownership.

13

Topic A01Depreciation 13 BAFS Compulsory Part

Learning and Teaching Example

Activity 1

Most important, you need to list 5 most valuable fixed assets.State their purchase cost, estimated useful life and estimated residual value.

Students are required to give presentation of their answers.

There is no right or wrong answer. Students will learn the concept of depreciation when setting up a virtual business.

Teacher may use personal judgment on the reasonableness of the students’ answers. Creative ideas are welcome.

Teacher asks students to fill in the column “ estimated useful life” and “residual value” into the table on student worksheet p.1.

14

Topic A01Depreciation 14 BAFS Compulsory Part

Learning and Teaching Example

Activity 1

Depreciable amount of fixed assets

= Cost of an asset (A) Less Residual value (B)

Teacher asks students to calculate the depreciable amounts into the table on student worksheet p.1.

Remarks:The residual value of an asset is the estimated amount after deducting the estimated costs of disposal, if the asset were already of the age and in the condition expected at the end of its useful life.(HKAS16)

15

Topic A01Depreciation 15 BAFS Compulsory Part

Learning and Teaching Example

Common Depreciation Methods

Straight-line method a constant charge over the useful life

Diminishing balance method (also known as reducing balance method)

a decreasing charge over the useful lifeUnits of production method

based on the expected use or output

Before starting Activity 2, teacher introduces the common depreciation methods.

Students in Activity 2 will identify the possible depreciation methods to apply to fixed assets set up in Activity 1 and insert into the table on their Student Worksheet p.1

Groups will present their discussion outcomes.

16

Topic A01Depreciation 16 BAFS Compulsory Part

Learning and Teaching Example

Activity 2

Identify appropriate depreciation methods

Students are required to complete Activity 2 on student worksheet p.2.

17

Topic A01Depreciation 17 BAFS Compulsory Part

Learning and Teaching Example

Activity 2

Identify depreciation methods that may be applied to fixed assets in Activity 1.Students remain in the same group and discuss how to allocate the assets depreciable amount over their useful lives.

This is the extension of Activity 1. Students remain in same group. Teacher asks students to identify the possible depreciation methodsthat may be applied for the assets and insert into Student Worksheet p.2.

Students present their discussion outcomes.

Teacher explains that there are various methods to allocate the depreciable amount, including:

Straight-line method – a constant charge over the useful lifeDiminishing balance method / reducing balance method – a decreasing charge over the useful lifeUnits of production method – based on the expected use or output

18

Topic A01Depreciation 18 BAFS Compulsory Part

Learning and Teaching Example

Activity 3: A Survey

To identify depreciation methods used by listed companiesEach group is required to:

choose a listed company from assigned industry;visit the company website & review most recent annual report;identify various depreciation methods used by asset types from notes of financial statement; andsummarise findings on student worksheet p.3.

Students choose a listed company from industries like banking, transportation, properties & construction, utilities and telecommunications. Students write down the survey results on Student Worksheet p.3. and present their findings in lesson 2.

End of Lesson 1

19

Topic A01Depreciation 19 BAFS Compulsory Part

Learning and Teaching Example

Lesson Two

Common methods of calculating depreciation

charges

Lesson 2

Students are able to calculate and compare depreciation charges under different methods and identify the factors that need to be considered when choosing a depreciation method.

20

Topic A01Depreciation 20 BAFS Compulsory Part

Learning and Teaching Example

Depreciation Methods

Straight-line method Cost – Estimated residual value

Expected useful life

Reducing balance method (Cost – Accumulated depreciation)

x Depreciation rate

Teacher recaps the calculation of depreciation under straight-line method and reducing balance method.

21

Topic A01Depreciation 21 BAFS Compulsory Part

Learning and Teaching Example

Presentation of the survey findings

Teacher asks students to present their work recorded in Lesson 1Activity 3.

After the presentations, teacher asks students to identify the most widely used depreciation method (expected to be the straight-line method).

Teacher concludes the presentation by highlighting that different industries use different depreciation methods.

Suggested answer:• Hong Kong and China Gas Co. Ltd. - Depreciation of property, plant

and equipment is calculated on a straight-line basis.

22

Topic A01Depreciation 22 BAFS Compulsory Part

Learning and Teaching Example

Activity 4

Case Study and Group Discussion

Teacher asks students to form the same groups as in Lesson 1. Then let them read the case carefully and complete tasks as stated in Student Worksheet p.4, which aims to:

• determine the annual depreciation;• compare the straight-line and reducing balance methods,

including the impact on profits;• identify the factors affecting the choice of depreciation

methods;• determine the amount of depreciation for fractional periods;

and• determine how to calculate the depreciation expense if the

estimated useful life has been revised.

Teacher invites students to present their answers.

23

Topic A01Depreciation 23 BAFS Compulsory Part

Learning and Teaching Example

Activity 4

Determine the first 5 years annual depreciation chargesa) Use method that can maximise

the first 2 years reported profits b) Then, use alternative method to

do the re-calculation

• To maximise first 2 years reported profits, reducing balance method is not preferred as a higher depreciation is available in earlier years.

• Teacher helps students to check the answers.

• Suggested answers:1a: Straight-line method1b: Reducing balance method

24

Topic A01Depreciation 24 BAFS Compulsory Part

Learning and Teaching Example

Activity 4

Compare the annual depreciation patterns using straight-line and reducing balance methods.

Teacher helps students to check the answers

Suggested answers:Straight-line method: Depreciation charge spreads evenly over the useful life.Reducing balance method: A higher depreciation allowance available in the early years.

25

Topic A01Depreciation 25 BAFS Compulsory Part

Learning and Teaching Example

Activity 4

Discuss the factors that you will consider when choosing the depreciation method to be applied.

Teacher points out that:• The depreciation method selected should reflect the pattern of usage in

which the asset’s economic benefits are consumed by the company. • For example, assets with constant uniform service will be depreciated

by using straight-line method; whereas, the loss in value of asset is a function of time, reducing balance depreciation method will be used.

26

Topic A01Depreciation 26 BAFS Compulsory Part

Learning and Teaching Example

Activity 4

Suggest two methods for calculating depreciation expense for fractional periods.

Students may suggest various methods for calculating depreciation for less than a year and for less than a month. Teacher reviews thereasonableness of answers.

Suggested answers:1.Provide a full period depreciation on assets in use at period end.

• This method implies that no depreciation will be provided for the year if the asset is sold during the year.

2.Based on one month's ownership provision for depreciation• That rounds depreciation to the nearest whole month.

27

Topic A01Depreciation 27 BAFS Compulsory Part

Learning and Teaching Example

Activity 4

Discuss how you will revise the annual depreciation charges if the useful life of an asset has been revised.

Teachers helps students to check the answers.

Suggested answer:• No need to revise prior periods’ depreciation expenses. • Annual depreciation expense = remaining undepreciated cost /

remaining useful life

28

Topic A01Depreciation 28 BAFS Compulsory Part

Learning and Teaching Example

Activity 5

A mini-case

• Students remain in the same group.• Teacher asks students to read the case and complete the tasks.• The case helps students to identify the depreciate method,

depreciation rate and deprecation charges from incomplete records.• Students provide answers and feedback.

29

Topic A01Depreciation 29 BAFS Compulsory Part

Learning and Teaching Example

Activity 5﹕Suggested answer

A B

Depreciation method used Straight-line Reducing balance

Depreciation rate used 1/5 1/3

Costs $6,075 $6,075

Net book value at the end of Year 2 $3,965 $2,700

Depreciation charge for Year 3 $1,055 $900

Machine

Show calculation and explain that sometimes figures are from incomplete records.

Suggested answer:Machine A: Costs = [1055*5+800] Machine A : NBV at the end of Yr. 2=[6,075-1,055*2]Machine B : Depreciation rate = 2025/6075Machine B : NBV at the end of Yr. 2=[6075*(1-1/3)-1350]

End of Lesson 2

30

Topic A01Depreciation 30 BAFS Compulsory Part

Learning and Teaching Example

Lesson Three

Depreciation on disposal of fixed assets

Lesson 3

Presents calculation and accounting treatment of 2 types of disposals:1. Disposal with receipt of cash2. Disposal in the form of ‘trade-in’

31

Topic A01Depreciation 31 BAFS Compulsory Part

Learning and Teaching Example

Disposal of Fixed Assets with Receipt of Cash

This lesson will discuss the accounting treatment of fixed assets disposal.Two major areas will be discussed: a. Disposal of fixed assets with receipt of cash; andb. Disposal of fixed assets involving ‘trade-in’.

32

Topic A01Depreciation 32 BAFS Compulsory Part

Learning and Teaching Example

Accounting entries

Dr CashDr Accumulated Depreciation of Fixed Assets

Cr. Fixed Assets (Cost)Cr. Profit & Loss: Profit on Disposal

Teacher shows accounting entries under disposal of fixed assets with receipt of cash and highlights:

1. If the asset is bought on credit, the ‘Dr Cash’ should be replaced by ‘Dr Debtor’.

2. If there is a loss on disposal, the credit of ‘Profit & Loss: Profit on Disposal’ should be changed to the debit of ‘Profit & Loss: Loss on Disposal’.

33

Topic A01Depreciation 33 BAFS Compulsory Part

Learning and Teaching Example

Profit on Disposal

Mathematically, calculate as:

Profit on Disposal = Cash – Net Book Value of the Fixed Asset= Cash – (Cost - Accumulated Depreciation)

Teacher introduces the rationale behind accounting entries through the mathematical calculation of the profit on disposal.

Calculation can be used as a quick check on the profit on disposal determined from accounting entries.

34

Topic A01Depreciation 34 BAFS Compulsory Part

Learning and Teaching Example

Disposal of Fixed Assets in the form of ‘Trade-in’

Old assets with certain cost remained can sometimes be exchanged for new assets with the additional payment, either in cash or on credit.

35

Topic A01Depreciation 35 BAFS Compulsory Part

Learning and Teaching Example

Accounting entries

Dr Assets: Cost of New Assets (in Fair Value)Dr Accumulated Depreciation of Old Assets

Cr Assets (Cost of Old Assets)Cr CashCr Profit & Loss: Profit on Disposal

Teacher shows accounting entries under the form of ‘Trade-in’ and highlights:

1. If there is loss on disposal, the credit of ‘Profit & Loss: Profit on Disposal’ should be changed to the debit of ‘Profit & Loss: Loss on Disposal’.

2. If the asset is bought on credit, ‘Cr Cash’ should be replaced by ‘Cr Creditor’.

36

Topic A01Depreciation 36 BAFS Compulsory Part

Learning and Teaching Example

Profit on Disposal in the form of ‘Trade-in’

Mathematically, can be calculated:

Disposal profits as Trade-in = (Fair value of new asset –cash paid for new asset) –Net book value of the old asset

Teacher introduces the rationale behind accounting entries and mathematical calculations of the profit disposal. The calculation can be used as a quick check on the profits disposal determined fromaccounting entries.

37

Topic A01Depreciation 37 BAFS Compulsory Part

Learning and Teaching Example

Activity 6

An Auction Game

Students practice the following:a. Applying depreciation on fixed assets to determine net book value.b. Making accounting entries on fixed asset disposals for buyer and seller.c. Acquiring fixed asset in form of ‘trade-in’.d. Simulating an auction process.e. Recording cash flows related to the auction.

Students should refer to the worksheet for instruction. It is assumed that the maximum no. of groups is 7. Each group consists of 4 to 5 students. The group may be assigned by the teacher or chosen bystudents themselves. Maximum game time is 25 minutes.

38

Topic A01Depreciation 38 BAFS Compulsory Part

Learning and Teaching Example

Auction Game (Part A)

Calculate the depreciation of the asset

Students form groups of 4-5 members. Each group represents a company. Each company will purchase one assigned asset. Students are required to calculate the asset depreciation on worksheet p.9.

39

Topic A01Depreciation 39 BAFS Compulsory Part

Learning and Teaching Example

Auction Game (Part B)

Your company offers its assets to the second hand market and then buys new assets.

Teacher helps students conduct an auction. In this auction, each group can sell its assets and bid other groups’ assets.

Teacher also helps students calculate how much money they have and explains the reasons for auction step by step.

40

Topic A01Depreciation 40 BAFS Compulsory Part

Learning and Teaching Example

Action Game (Part C)

Now, record all auction related transactions.(Worksheet p.12-14)

Students must refer to student worksheet p.12-14 to record all auction related transactions.

41

Topic A01Depreciation 41 BAFS Compulsory Part

Learning and Teaching Example

Experiences gained from the Game and this Lesson

a. Applying depreciation to fixed assets to determine net book values.

b. Making accounting entries on fixed assets disposals for buyer & seller.

c. Acquiring fixed asset as ‘trade-in’.

Students may have fun and enjoy this game. However, it is important to learn the principles and understand how to use.

Teacher concludes the lesson and highlights the key points learned.

42

Topic A01Depreciation 42 BAFS Compulsory Part

Learning and Teaching Example

The End

End of Lesson 3.

Topic A01: Depreciation Student Worksheet p.1

BAFS Learning and Teaching Example As at April 2009

BAFS Elective Part – Accounting Module – Financial Accounting Topic A01: Balancing Day Adjustments Relating to the Preparation of Financial Statements - Depreciation

Activity 1

SSeett uupp yyoouurr oowwnn bbuussiinneessss aanndd aaccqquuiirree tthhee ffiixxeedd aasssseettss Name of Company: ________________________________________________ Nature of Business (Choose one of them): Restaurant/ Game Centre/

Tutorial Centre / Karaoke/ Supermarket

The five most valuable fixed assets

Fixed Asset Cost

(HK$) (A)

Estimated Useful Life (Years)

Residual Value (HK$) (B)

Depreciable Amount (HK$) (A) – (B)

1.

2.

3.

4.

5.

Topic A01: Depreciation Student Worksheet p.2

BAFS Learning and Teaching Example As at April 2009

Activity 2 - Group Discussion

It’s time to identify the fixed assets depreciation methods to be applied as stated in Worksheet p.1. Discuss how you will allocate the depreciable asset amount over the useful life.

Fixed Asset Depreciation Methods

1.

2.

3.

4.

5.

Topic A01: Depreciation Student Worksheet p.3

BAFS Learning and Teaching Example As at April 2009

Activity 3 - A Survey

Objective: To identify the depreciation methods used by listed companies Task: Each group of four or five students will:

(1) choose a listed company from an assigned industry; (2) visit the website of the company and access the most recent

annual report; (3) identify the various depreciation methods from the notes of

the financial statements; (4) summarise the findings in the following table.

Answer: (1) Name of company:

(2) Findings:

Asset type Depreciation methods used

Topic A01: Depreciation Student Worksheet p.4

BAFS Learning and Teaching Example As at April 2009

Activity 4 - Case Study and Group Discussion

Read the following case carefully and complete the tasks. Suppose your company has acquired all fixed assets identified in lesson 1 on 1 January Year 1. Annual depreciation expense changes by the depreciation method used, which in turn affects the amount of profit. To facilitate fund raising, your friend suggests you to choose the depreciation method that will maximise the reported profits for the first two years.

Assume either the straight-line or reducing balance method will be used. If necessary, state any other reasonable assumptions. Tasks:

(1) Determine the annual depreciation charges for the first five years.

(a) Using the method that maximises first 2 yrs reported profits.

Annual Depreciation ($) Fixed Asset

Depreciation method Year

1 Year

2 Year

3 Year

4 Year

5

1

2

3

4

5

Total

Topic A01: Depreciation Student Worksheet p.5

BAFS Learning and Teaching Example As at April 2009

(b) Using the alternative method

Annual Depreciation ($) Fixed Asset

Depreciation method Year

1 Year

2 Year

3 Year

4 Year

5

1

2

3

4

5

Total

(2) Compare the annual depreciation patterns using straight-line and reducing balance methods.

(3) Discuss the factors to consider when choosing the depreciation method.

Topic A01: Depreciation Student Worksheet p.6

BAFS Learning and Teaching Example As at April 2009

(4) Assuming that “Fixed asset No. 5” was purchased on 8 August Year 1.

(a) Suggest two methods for calculating depreciation expenses for fractional periods.

(i)

(ii)

(b) Calculate the straight-line asset depreciation charges for the year ended 31 December Year 1, using methods (i) and (ii) as suggested in (a) above. Assume no asset disposal during the year.

(i)

(ii)

Topic A01: Depreciation Student Worksheet p.7

BAFS Learning and Teaching Example As at April 2009

(5) Assume after one year of operation, you decide that the useful life of “Fixed asset No. 1” should last for 2 more years. Discuss and revise the annual depreciation charges previously determined in (1a).

Annual Depreciation ($) Fixed

Asset Year 1 Year 2 Year 3 Year 4 Year 5

1

Topic A01: Depreciation Student Worksheet p.8

BAFS Learning and Teaching Example As at April 2009

Activity 5 - A Mini-Case

Read the following case carefully and complete the tasks. Mr. White, a manufacturer, bought two machines at the same price on 1 January Year 1. The machines have an estimated useful life of 5 years and a residual value of $800. As proper books of accounts are not kept, it is uncertain whether the straight-line or the reducing balance method was applied. The only information available is::

Machine A: Depreciation charges for year 1 and 2 are $1,055. Machine B: Depreciation charges for year 1 and 2 are $2,025

and $1,350 respectively. Task: Input missing data into the following table.

Machine

A B

Depreciation method used

Depreciation rate used

Costs

Net book value at the end of Year 2

Depreciation charge for Year 3

Topic A01: Depreciation Student Worksheet p.9

BAFS Learning and Teaching Example As at April 2009

Activity 6 - Auction Game

Part A

Students form groups of 4 or 5 members. Each group represents a company. The companies are going to buy office equipment. Group 1 2 3 4 5 6 7

Office Equipment

Desktop

Computer

Photo -

copier

Shredder Notebook

Computer

Multi -

purpose

Printer

Binding

Machine

Projector

Cost $16,000 $60,000 $8,500 $12,000 $32,000 $9,000 $35,000

It is the company’s policy to use the reducing balance depreciation method on the office equipment with a rate of 30% per annum. Required Determine the accumulated depreciation and net book value of the groups’ own equipment for the first three years. Group No.________; Asset:______________; Cost:_______________ At the end of Year

Accumulated Depreciation

Net Book Value

1

2

3

Topic A01: Depreciation Student Worksheet p.10

BAFS Learning and Teaching Example As at April 2009

Part B

(Please refer to information in Part A) Time passes fast as 2 years has elapsed since purchasing the office equipment. Your company wants to sell the equipment to the second hand market prior to purchasing new. The second hand buyers are other student groups that will bid for your equipment in an open auction. The group offering the highest price will get your equipment. Here are the auction steps: Step 1 How much does each group have? Teacher adds up the net book values of all groups’ equipment (Just call it ‘total net book values’). Cash owned by each group is determined by the following formula:

Cash owned by each group =Total Net Book Values /No. of Groups x (1 + 10%) (The figure should be rounded up to the nearest thousand dollars) For example, if the ‘total net book values’ are $103,540 and there are 7 groups. Then, each group may have: $103,540/7 x (1+10%) = $16,271 So, in this example, each group should have $16,000 cash. Step 2 Why do other groups want to bid for your equipment? The group who buys the largest number of equipment wins a prize! Buyers can: 1. pay cash to the seller or 2. purchase the equipment as a ‘trade-in’. The ‘trade-out’ value of each

piece of equipment is pre-determined, for the purpose of this game, as $5,000.

Topic A01: Depreciation Student Worksheet p.11

BAFS Learning and Teaching Example As at April 2009

Additional points to note 1. Game is limited to 25 minutes. No limits on each bid. 2. Once a company wins the bid, it must buy the asset as decisions are

final. 3. Students must act professional and respectful to all bidders during the

bidding process. After a series of fierce competition, the results of the auction are: Net Book

Value ($) Bought by (Group)

Auction Price ($)

Group 1 Desktop Computer

Group 2 Photocopier

Group 3 Shredder

Group 4 Notebook Computer

Group 5 Multi-purpose Printer

Group 6 Binding Machine

Group 7 Projector

Topic A01: Depreciation Student Worksheet p.12

BAFS Learning and Teaching Example As at April 2009

The total number of equipment owned by each group is: Group No. of Equipment 1 2 3 4 5 6 7

The winner of the Auction Game is Group ____

Part C: To record the transactions in accounting records of own

group

Your group no.:______________ 1. Cash Movement $ Opening balance Add: Sale to Group ___ Sale to Group ___ Less: Purchase from Group ___ Purchase from Group ___ Purchase from Group ___ Closing balance

Topic A01: Depreciation Student Worksheet p.13

BAFS Learning and Teaching Example As at April 2009

2. Accounting Entries As seller (Asset sold:___________) $ $ Dr. Dr. Cr. Cr. ----------------------------------------------------------------------------------- As buyer pays with 100% cash (Asset bought: ) $ $ Dr. Cr. As buyer pays with 100% cash (Asset bought: ) $ $ Dr. Cr. As buyer pays with 100% cash (Asset bought: ) $ $ Dr. Cr. -----------------------------------------------------------------------------------

Topic A01: Depreciation Student Worksheet p.14

BAFS Learning and Teaching Example As at April 2009

As buyer, by way of trade-in (Asset traded-in:___________; Asset traded out: __ ) $ $ Dr. Dr. Cr. Cr. As buyer, by way of trade-in (Asset traded-in:___________; Asset traded out: __ ) $ $ Dr. Dr. Cr. Cr.