a working report on the import department of prime bank...

TRANSCRIPT

A WORKING REPORT ON THE IMPORT DEPARTMENT OF PRIME BANK LTD.

by,

Faujia Ferdousy Rahman ID: 0410074

An Internship Report Presented in Partial Fulfillment Of the Requirements for the Degree Bachelor of Business Administration (BBA)

INDEPENDENT UNIVERSITY,BANGLADESH April 30, 2009

A WORKING REPORT ON THE IMPORT DEPARTMENT OF PRIME BANK LTD.

A WORKING REPORT ON THE IMPORT DEPARTMENT OF PRIME BANK LTD.

by,

Faujia Ferdousy Rahman ID: 0410074

has been approved April, 2009

______________________

Sylvana Maheen Ahmed Lecturer

School of Business Independent University, Bangladesh

30th April, 2009

Letter of Transmittal

April 30, 2009

Sylvana Maheen Ahmed

Lecturer, Finance

School of Business

Independent University, Bangladesh (IUB)

Dhaka, Bangladesh.

Subject: Submission of the internship working report.

Dear Madam,

With due respect, I would like to inform you that, it is a great pleasure for me to submit

the working report on “The Import Trade of Prime Bank Ltd.”, as a requirement for BBA

499 program. While conducting the working report, I have gathered extensive knowledge

on IT department of British American Tobacco, Bangladesh (BATB) and enjoyed

working there.

Sincerely Yours

………………………….

Faujia Ferdousy Rahman

ID# 0410074

Acknowledgement

First of all, I would like to thank to Almighty Allah for letting me finish my internship

report timely.

I would like to express my gratitude to my academic supervisor Ms. Sylvana Maheen

Ahmed from the core of my heart for her kind support, guidance, constructive

supervision, instructions, and advice and for motivating me to do this report.

I am also thankful to Head of HR Division of Prime Bank Limited for giving me the

opportunity to do the internship in Prime Bank Limited. I am also grateful to the

employees of Gulshan Branch specially import department for their cordial acceptance.

They have been very helpful in showing me the work process and provided relevant

information for my report whenever I approached. They never hesitated or did not feel

disturbed when I asked questions. It was a great opportunity to do internship in such an

organization. The experiences I have gathered will be very beneficial for building my

career.

Table of Contents

Pages Chapter one ......................................................................................................................... 1

1.0 Origin of the report.................................................................................................... 1 1.1 Objective of the report............................................................................................... 1 1.2 Source of Information................................................................................................ 1

Chapter two ......................................................................................................................... 3 2.0 Prime bank Ltd. ......................................................................................................... 3

Chapter three ....................................................................................................................... 4 3.0 Operational Processes in Prime Bank’s Import Trade department ........................... 4 3.1 FOREIGN EXCHANGE........................................................................................... 4

3.1.1 Legal basis of foreign exchange transactions..................................................... 4 3.1.2 Functions of Foreign Exchange Department...................................................... 5

3.2 Import ........................................................................................................................ 6 3.2.1 Legislative Bonding for Import.......................................................................... 7 3.2.2 Letter of Credit ................................................................................................... 7 3.2.3Types of Letter of Credit..................................................................................... 8 3.2.4 General Conditions of Import of Goods........................................................... 10 3.2.6 Parties of a Letter of Credit .............................................................................. 13 3.2.8 Depositing of Letter of Credit Margin and Other Charges .............................. 15 3.2.9 Accounting Treatment in Case of Letter of Credit Opening............................ 16 3.2.10 Issuing the Letter of Credit............................................................................. 16 3.2.11 Different Means of Payment .......................................................................... 17 3.2.12 Transmission of Letter of Credit .................................................................... 18 3.2.13 Receipt and Scrutiny of Documents............................................................... 18 3.2.14 Scrutiny of Documents ................................................................................... 19 3.2.15 Discrepant Documents and Notice................................................................. 20 3.2.16 Disclaim on Effectiveness of Documents ....................................................... 21 3.2.17 lodgment......................................................................................................... 22 3.2.18 Retirement of the Documents ......................................................................... 23 3.2.19 Financing Related with Import....................................................................... 24 3.2.20 Credits Occurred in Letter of Credit Operation ............................................. 25

Chapter four....................................................................................................................... 29 4.0 My responsibilities and my work............................................................................ 29

Chapter five ....................................................................................................................... 30 5.0 Results and conclusion ............................................................................................ 30

Chapter six......................................................................................................................... 31 6.0 Recommendations ................................................................................................... 31

References ......................................................................................................................... 33 Appendices ........................................................................................................................ 34

APPENDIX-A: List of Tables....................................................................................... 34 APPENDIX-B: List of Figures ..................................................................................... 36 Appendix-C: Few required Documents of L/C………………………………………..37

LIST OF FIGURES

Pages Figure 3.2.21.3: LC Opened during 2006 ......................................................................... 28 Figure 3.2.21.4: LC Opened during 2007 ......................................................................... 28 Appendix Figure 1.0: LC Opened during 2006 ................................................................ 36 Appendix Figure 2.0: LC Opened during 2007 ................................................................ 36

LIST OF TABLE

Pages Table 3.2.9: Depositing of Letter of Credit Margin and Other Charges ........................... 15 Table 3.2.21.1: Credits Occurred in Letter of Credit Operation ....................................... 26 Table 3.2.21.2: Endorsement by bank............................................................................... 27 Appendix Table 1.0: Details volume and type of commodities for L/C........................... 34 Appendix Table 2.0: Growth in L/C during 2006-2007 ................................................... 34 Appendix Table 3.0 : Monthly Influx of Foreign Currency in Terms of USD................. 35

Chapter one 1.0 Origin of the report

Present world is changing rapidly to face the challenge of competitive free market

economy. To keep pace with the trend every organization need executive with modern

knowledge. To provide fresh graduate with modern theoretical and professional knowledge in

banking and all other different institution management, Independent University, Bangladesh

has assigned the course BUS 499 for the students to help them out to have a practical

knowledge to work in a real official environment. Under this course the students are sent to

gather practical knowledge about working environment and activities. The report is a

requirement of the internship program for my BBA degree. The organization attachment

started on January 25, 2009 and ended on April 25, 2009. My organization supervisor Mr. Kazi

Muzibul Islam (Manager Operation, Gulshan Branch, Prime Bank Limited) suggested me the

topic of my report. The reason behind choosing this topic is that, recently the authority of

Prime Bank Limited (PBL) has given emphasis on the increase the Foreign Exchange (Export,

Import, Remittance) Business that helps the country to be economically strong as well as The

Bank itself.

1.1 Objective of the report 1.1.1 Primary Objective:

• To learn about Letter of Credit and its Procedure of Issuing, Lodgment & Retirement

1.1.2 Secondary Objective:

• To know about import financing activities

• To find out and provide recommendations for the internal and external lacking in the

daily operation that would help to Prime Bank Limited for more progress.

Similarly, from the import data’s I tried to figure out the recent trend in terms of import.

What sort of commodities are now being imported and whether there has been any change in

terms of quantity during the last few years.

1.2 Source of Information The information will be collected from the officers related with Foreign Exchange

department. Also the lack of services and satisfaction of customers, related information will be

collected from the clients.

A working report on Import department of Prime Bank Ltd.

2

2

1.2.1 Primary Source of Data Collections IS:

• Face to face conversation with the bank officers

• Appointment with the top officials of the Bank

• By interviewing L/C customers at PBL, Gulshan Branch and

• Daily activity conducted by me at bank.

1.2.2 Secondary Source of Data Collections:

• Official records of the clients

• Annual report of Prime Bank Limited

• Websites

• Different publications regarding banking functions

• Bangladesh Bank Report

• Newspapers

• Group Business Principal manual

• Group Instruction Manual & Business Instruction Manual

A working report on Import department of Prime Bank Ltd.

3

3

Chapter two 2.0 Prime bank Ltd.

Bank is a financial institution that provides services related to money. Since bank operates

in the service industry having a strong customer relationship is of utmost importance. Prime

Bank Ltd has been operating in this industry since 1995 and belongs to the second generation

of private banks to be incorporated since the independence of Bangladesh. Today it holds’s the

No. 1 position in the CAMEL’s rating conducted by Bangladesh Bank. And in this report we

will try to figure out what sort of management approach actually helped Prime Bank to achieve

this position.

The Banking sector in Bangladesh has gone through tremendous changes over the last few

decades as the sector became more competitive with the inclusion of many new private banks,

each coming up with its own unique scheme of services. As competition rose, Prime Bank also

had to come up with its own unique managerial approach to keep up with the pace.

Prime Bank Ltd. has already made significant progress within a very short period of its

existence. The bank has already occupied an enviable position among its competitors after

achieving success in all areas of business operation. The bank offers all kinds of Commercial

Corporate and Personal Banking services covering all segments of society within the

framework of Banking Company Act and rules and regulations laid down by our central bank.

Diversification of products and services include Corporate Banking, Retail Banking and

Consumer Banking right from industry to agriculture, and real state to software.

A working report on Import department of Prime Bank Ltd.

4

4

Chapter three

3.0 Operational Processes in Prime Bank’s Import Trade department

3.1 Foreign Exchange Foreign Exchange Department is the international department of the bank. It deals globally.

It facilitates international trade through its various modes of services. It bridges between

importers and exporters. If the branch is authorized dealer in foreign exchange market, it can

remit foreign exchange from local country to foreign country. This department mainly deals in

foreign currency. This is why this department is called foreign exchange department.

The term foreign exchange has different connotations in different contexts. In terms of

section 2(d) of the Foreign Exchange Regulation (F. E. R.) Act 1947, as adapted in

Bangladesh, foreign exchange means foreign currency and includes instruments expressed in

foreign exchange, all deposits, credits and balance payable in foreign currency as well as

foreign currency instruments such as Draft, TC, Bill of Exchange, promissory note, and Letter

of Credit payable in any foreign currency.

The business of foreign exchange is getting increasingly complex and intensely competitive.

However, in the backdrop of phenomenal growth of Bangladesh’s external sector, foreign

exchange business provides a challenge as well as an excellent opportunity to accelerate

growth of bank’s own business. This is the Institution that facilitates international trade

payment as banking channel is the way of settlements. Besides, banks meet the other need of

foreign exchange transactions of the people of the country as they are authorized to deal in

foreign exchange upon receipt of permission from Central Bank under Foreign Exchange

Regulation Act. All exports and imports are executed through the intervention of banks. Side

by side, they provide funded and non funded credit facility in execution of International Trade.

3.1.1 Legal basis of foreign exchange transactions

Foreign exchange transactions are performed under some legal regulations, as follows:

• Foreign Exchange Regulation Act – 1947

• Import and Export Control Act- 1950

• Customs Act-1969

• The uniform customs and practices for documentary Credit (UCPDC) – 1993 revision &

International Chamber of Commerce Publication no – 500, is also an important law for

settlement of terms and conditions between exporter and importer in international trade.

A working report on Import department of Prime Bank Ltd.

5

5

• Import Policy Issued by Ministry of Commerce

• Export Policy Issued By Ministry of Commerce

• International Rules Issued by International Chamber of Commerce (ICC)/ Uniform Rules

and Practices

• Different Foreign Exchange Circulars issued by Bangladesh Bank

3.1.2 Functions of Foreign Exchange Department

Foreign Exchange Department performs many functions to facilitate the foreign exchange

transactions. These are:

• Facilitating Import Trade

• Facilitating Export Trade

• Providing Funded and Non-funded Credit Facility.

• Provide Non Commercial Remittance

• Maintaining Foreign Currency Accounts

• Selling of Foreign Currency Bond

• Preparation and Submission of Statements

The International Division placed at the Prime Bank’s head office at Motijheel is the

backbone of all international transaction that is conducted through the various branches of the

bank. A total of 42 branches of Prime Bank have the license to carry out international trade

functions. Each of these AD branches have foreign exchange department whose sole purpose is

to carry out cross border transaction demanded by the customers.

The functions of such Foreign Exchange Department can be divided into three sections:

• Export Section

• Import Section, and

• The Foreign Remittance Section

A working report on Import department of Prime Bank Ltd.

6

6

Figure 3.2: Foreign Exchange Business

We see that there is a sharp rise in Foreign Trade business between 2005 and 2006 which

had continued into 2008 as we will see in the upcoming portion of this report.

3.2 Import Import is the flow of goods and services purchased by economic agent staying in the country

from economic agent staying abroad.

We can simplify Import as a means purchase of goods and services from the foreign

countries into Bangladesh. Normally consumers, firms and Government of Bangladesh import

foreign goods to meet their various necessities.

Import section of the Foreign Exchange Department helps business and other people to

import goods. So seller always seeks guarantee for the payment for his goods exported. Here is

the role of bank. Bank gives export guarantee that it will pay for the goods on behalf of the

buyer. This guarantee is called Letter of Credit. Thus the contract between importer and

exporter is given a legal shape by the banker by its ‘Letter of Credit’.

When a buyer goes to import some goods from a foreign buyer, he request his bank makes

payments to the exporter of goods. And the bank recovers the amount from the importer.

A working report on Import department of Prime Bank Ltd.

7

7

3.2.1 Legislative Bonding for Import

Imports are foreign goods and services purchased by consumers, firms & Governments in

Bangladesh. To import, a person should be competent to be an ‘importer’. According to Import

and Export Control Act, 1950, the Office of Chief Controller of Import and Export (CCI & E)

provides the registration (IRC) to the importer. Import of good in Bangladesh is regulated by

the

• Ministry of Commerce in terms of the Import and Export Control Act, 1950;

• Import Policy Order and the Public Notice issued by the Office of the Chief Controller of

Imports and Exports (CCI&E)

• Import section of Foreign Exchange Department facilitates import related banking

services concerns to import of goods in cash foreign exchange. The main facilities

provided by the import section are:

• Opening of Letter of Credit

• Facilitating Payments to the Exporter on behalf of the Importer

• Providing Funded and Non-funded Credit Facility

• Issuing Bank Guarantee in foreign currency on behalf of Foreign Companies.

Now let’s see what are the details of these facilities of Letter of Credit

3.2.2 Letter of Credit

Letter of Credit is a guarantee or undertaking or commitment to the beneficiary/exporter for

making payment issued by the issuing bank on behalf of the importer upon fulfillment of some

conditions. Central Banks, therefore assure these things to happen simultaneously by opening

Letter of Credit guaranteeing payments to seller and goods to buyer. By opening a Letter of

Credit on behalf of buyer in favor of seller, commercial banks undertake to make payments to a

seller subject to submission of documents drawn on in strictly compliance with Letter of Credit

terms giving title of goods to the buyer. It is a conditional guarantee. The Letter of Credit thus

constitutes one of the most important methods of financing foreign trade.

In the Import Policy Order 2003-2006 Letter of Credit denoted as – ‘“Letter of Credit”

means a letter of credit opened for the purpose of import under this Order’

The expression “Documentary Credit(s)” and “Standby Letter(s)” means any arrangements,

however named or described, whereby a bank (“the issuing bank”) acting at the request and on

the instruction of a customer (the “Applicant”) or on its own behalf,

A working report on Import department of Prime Bank Ltd.

8

8

• Is to make a payment to or the order of a third party (“the Beneficiary”), or is to accept

and pay bills of exchange (Draft’s) drawn by the Beneficiary, Or

• authorizes another bank to effect such payment, or to accept and pay such bills of

exchange (Draft(s)),Or

• authorizes another bank to negotiate,

• Against stipulated document(s), provided that the terms and conditions of the Credit and

complied with.

On the other hand Letter of credit can be defined as a “Credit Contract” whereby the buyer’s

bank is committed (on behalf of the buyers) to place an agreed amount of money at the seller’s

disposal under some agreed conditions. Since the agreed conditions include amongst other

things, the presentation of some specified documents, the letter of credit is called Documentary

letter of credit. The uniform customs and practices for documentary Credit (UCPDC) published

by international Chamber of Commerce (1993) revision, publication no 500 define

Documentary Credit:

• Any arrangement however named or described whereby a bank (the issuing bank) acting

at the request and on the instructions of a customs (the Applicant) or on it’s own behalf,

• Authorize another bank to effect such payment or to accept and pay such bills of

exchange (Drafts)

• Authorize another bank to negotiate against stipulated documents provide that terms and

conditions are complied with.

3.2.3 Types of Letter of Credit

There are many types of Letter of Credits that are used in different countries of the world.

But International Chamber of Commerce (ICC) vides their UCPDC- 500, which denotes only

two types of LETTER OF Credits; mentioned:

• Revocable Letter of Credit

A revocable credit may be amended or cancelled by the issuing bank at any moment and

without prior notice to the beneficiary. That is to say, this type of letter of credit can be revoked

or cancelled at any time without consent of, or notice to the beneficiary.

In case of seller (beneficiary), revocable credit involves risk, as the credit may be amended

or cancelled while the goods are in transit and before the documents are presented, or although

presented before payments has been made. The seller would then face the problem of obtaining

payment on the other hand revocable credit gives the buyer maximum flexibility, as it can be

A working report on Import department of Prime Bank Ltd.

9

9

amended or cancelled without prior notice to the seller up to the moment of payment buy the

issuing bank at which the issuing bank has made the credit available. In the modern banking

the use of revocable credit is not widespread.

In this case the issuing banks must perform the following two roles:

• Reimburse another bank with which a revocable Credit has been made available for sight

payment, acceptance or negotiation – for any payment, acceptance or negotiation made by

such bank – prior to receipt by it of notice of amendment or cancellation, against

documents which appear on their face to be in compliance with the terms and conditions of

the Credit;

• Reimburse another bank with which a revocable Credit has been made available for deferred

payment, if such a bank has, prior to receipt by it of notice of amendment or cancellation,

take up documents which appear on their face to be in compliance with the terms and

conditions of the Credit.

• Irrevocable Letter of Credit

An irrevocable credit is a documentary credit, which cannot be revoked, varied or

changed/amended or cancelled without the consent of all parties- buyer (Applicant), seller

(Beneficiary), Issuing Bank, and Confirming Bank (in case of confirmed Letter of Credit).

Irrevocable Credit gives the seller greater assurance of payments, but he/she remains dependent

on an undertaking of a foreign bank. In the issuance of Irrevocable Letter of Credit both the

Issuing and Conforming Bank have some liability, mentioned bellow, as per UCPDC -500:

The following types of Letter of Credits are used in the Prime Bank, Gulshan Branch:

• Cash Letter of Credit

Payment made form cash foreign exchange not from export proceeds; There is not export L.

C. which backs the import Letter of Credit Payment term is at sight.

• Deferred Letter of Credit

The only difference between cash Letter of Credit and deferred Letter of Credit lied in the

terms of payment. Payment under deferred Letter of Credit is made after certain days of

presentation of the export bill. Letter of Credit the differed payment basis may be opened for

the following cases:

A working report on Import department of Prime Bank Ltd.

10

10

Items Period

Industrial Raw Materials (For own use) Maximum 180 days

Back to Back Imports Maximum 180 days

Agricultural Implements & Chemical Fertilizer Maximum 180 days

Capital Machinery Maximum 360 days

Coastal Vessel Maximum 360 days

Life Saving Drugs Maximum 90 Days

• Back to Back Letter of Credit

It is related with export documents and not discussed in this report

3.2.4 General Conditions of Import of Goods

• Import Trade Control Schedule Number

For import purpose, use of ITC Number (H.S. Code) with at least six digits corresponding to

the classification of goods as given in the Import Trade Control Schedule 1988, based on the

Harmonized Commodity Description and Coding System, shall be mandatory. The seven Digit

H.S. Code published by Bangladesh Bureau of Statistics may also be mentioned in the Letter of

Credit. Form, Letter of Credit and other relevant paper within a bracket in addition to normal

H. S. Code as mentioned above. No bank shall issue Letter of Credit Authorization form or

open Letter of Credit without properly mentioning I. T. C. number (H. S. Code) thereon.

• NOC (No Objection Certificate) On the basis of ROR (Right of Refusal)

a. No Objection Certificate on the basis of Right of Refusal (ROR) form any authority

shall not be required for import of any freely importable item by any Public Sector

agency.

b. In case of import of banned/restricted items for approval projects financed under foreign

aid the concerned Government Department/Agency will approach the Chief Controller

of the Import and Export directly for necessary permission together with a list of items

duly certified under proper seal and signature giving description, quantity/number, price

and H.S. Code Number against each item required to be imported. The details about the

aided project and specific provision of the relevant contract and other necessary

information shall also have to be furnished along with the list of the items. The Chief

Controller shall issue permission /permit on the basis of above documents.

A working report on Import department of Prime Bank Ltd.

11

11

• Restriction regarding source of procurement of goods

• Goods form Israel or goods originating from that country shall not be importable.

Goods also not are importable in the flag vessels of that country.

• All kinds of import form and export to Serbia and Montenegro, fragments of former

Socialist Republic of Yugoslavia, shall be banned.

• Pre-shipment inspection

Unless otherwise specified, pre-shipment inspection of imported goods shall not be

obligatory in case of import by private sector importers.

• Shipment of Bangladesh Flag Vessels

Subject to waiver specified below shipment of goods shall not be made on Bangladesh flag

vessels:

• Imports of goods up to maximum twenty metric tons in case of single individual

consignee or up to maximum 100 (one hundred) metric tons in case of group import

may be made in non Bangladeshi flag vessels. However the Director –General of

Shipping may notify general waivers in the following cases, such as (1) shipment of

goods from foreign ports which are not visited by Bangladeshi Vessels, and (2)

import of goods on the basis of specific agreement which provides C & F (Cost &

Freight) contract. In all other cases a certificate of waiver shall be obtained from the

Director General of Shipping of Importation of goods in non-Bangladeshi flag

vessels.Director-General of Shipping shall not apply in cases of import under such

foreign aids, loans or grants which contain specific provisions regarding shipment

of goods.

• In case of import and export of goods by export oriented industries shipment may be

made in non-Bangladeshi flag vessels.

• Import at competitive rate

• Import shall be made at the most competitive rate and importers may be requited, at

any time, to submit documents regarding the price paid or to be paid by them.

• Incase of import under United Commodity Aid in the Private sector goods shall be

imported at the most competitive rate by obtaining quotations from a minimum

three suppliers/indenters representing at least two countries abroad. This condition

shall however not apply for opening of Letter of Credit up TK. One lac. For import

A working report on Import department of Prime Bank Ltd.

12

12

at most competitive rate by the Public Sectors the condition mentioned at Para 27(8)

of this order shall apply.

• Import of C & F and FOB (free on Board) basis

All imports by sea, air and land route shall be made either on C & F or FOB basis. However

in case of import on FOB basis the concerned importer shall have to properly comply with the

circular issued by Bangladesh Bank in this regardProvisions in the relevant loan

agreement/projects agreement concluded with the foreign donors for import of CIF (Cost,

Insurance & Freight) basis, no import shall be allowed on CIF basis without prior approval

from the Ministry of Commerce. However, Bangladesh nations, living abroad, for sending

goods against their earned foreign exchange and foreign investors, for sending capital

machines and raw materials against their equity share portion shall be allowed on CIF basis.

• Import by Mentioning “Country of Origin”

1. In all cases of import, “country if origin shall be mentioned clearly on goods,

package/container. A certificate regarding “country of origin” issued by the

concerned Government agency/approved authority/organization of the exporting

country must be submitted, along with import documents to the Customer Authority

at the time of release of goods.. Besides, 100% export oriented industries, which are

recognized by Custom Authority, shall be waived from the restriction of “country of

origin” subject to the conditions imposed by the Foreign Exchange Regulation Act,

Bangladesh Bank and Commercial bank,

2. In case of import of Limestone, in different consignments/lot by the rope-way or by

river, as raw-materials for Chattak Cement Factory, “country of origin” certificate

from the exporting country’s Government/approved authority/organization shall be

submitted once to the Customs authority at the time of release of goods, instead of

each consignment/lot for the quantity mentioned in Letter of Credit in case of river-

way and as per supplied carrying list as case of rode-way.

3.2.5 Some Instructions Issued by Bangladesh Bank for Opening and Operation of Letter of

Credit for Import of Goods

• All Letter of Credits and similar undertakings covering imports into Bangladesh must

be documentary Letter of Credits and should provide for payment to be made

A working report on Import department of Prime Bank Ltd.

13

13

against full sets of onboard (shipped) transport documents (BL, AIB, TR etc.)

showing dispatch of goods covered by Credit to a destination in Bangladesh;

• ADs are allowed to open divisible, transferable Letter of Credits for import into

Bangladesh under cash LCAF (Letter of Authorization Form);

• It is not permissible to open Letter of Credits in favor of beneficiaries in countries

from which import into are banned by the component authority;

• Letter of Credits to be opened only against firm contract between the Applicant and

beneficiary. The AD should see documentary evidence, before opening Letter of

Credit, that a firm order for the goods to be imported has been placed and accepted;

• The full description of goods to be imported along with unit price and quantity to be

given in the Letter of Credit;

• Confidential report of the exporter to be obtained by the AD himself where the

amount of Letter of Credit exceeds TK. 2,00,000 in case of import against proforma

invoices issued direct by foreign supplier and TK. 5,00,000 against indent issued by

local agents of the suppliers;

• Payments against discrepant documents may be made after the goods have been

cleared from the customs on the basis of the locative LCAF;

• Advanced remittance against import may be made after getting prior permission from

Bangladesh Bank where the goods are of specialized or capital nature.

3.2.6 Parties of a Letter of Credit

• APPLICANT FOR THE CREDIT: The importer or buyer on whose request and on whose

behalf the letter of credit is opened is called the applicant.

• ISSUING BANK/ OPENING BANK: The bank that opens a Letter of Credit, at the request

of the importer, is known as Issuing Bank. The Issuing Bank is the buyer’s bank and is

also called opening bank.

• BENEFICIARY: The party, normally the supplier of the goods, in whose favor the Letter

of Credit is opened is called beneficiary. The seller, after shipping the goods as per

terms of the credit, presents the documents to negotiating bank/conforming bank for

negotiation.

A working report on Import department of Prime Bank Ltd.

14

14

• ADVISING BANK: The bank is the exporter’s country, usually the foreign correspondent

of the importer’s bank; through which Letter of Credit is advised to the supplier is

called the ‘advising bank’.

• CONFORMING BANK: If the advising bank also adds its own undertaking to honor the

credit while advising the same to the beneficiary, it becomes the conforming bank. The

conforming bank, in addition, becomes liable to pay for documents in conformity with

the Letter of Credit terms and conditions.

• NEGOTIATING BANK: The Bank, which negotiates the bill (draft) of the exporter drawn

under the credit, is known as negotiating bank. If the advising bank is also authorized to

negotiate the bill (draft) drawn by the exporter it itself becomes the negotiating bank.

• ACCEPTING BANK: A bank that (as specified in the Letter of Credit) accepts time or

Usance drafts on behalf of the importer is called the accepting bank. The Letter of

Credit issuing bank can also take on the responsibility of an accepting bank.

• PAYING BANK: The bank that effects payment to the beneficiary (as named in the Letter

of Credit) is known as paying bank/drawee bank.

• REIMBURSING BANK: If the issuing bank does not maintain any account with THE

NEGOTIATING bank an alternate arrangement is made to reimburse it for the amount

payable under a credit form some other bank. The later bank is termed as reimbursing

bank. An authority to debit his account is sent to the bank with whom the account is

maintained to honor the claims placed by a negotiating bank.

3.2.7 Preparation of Proposal and submitting it to the Competent Authority for Obtaining

Permission of Opening Letter Of Credit

Before opening Letter of Credit the applicant must take permission from the competent

authority. Whether the authority has to be taken form the Branch or from the Head Office

depends on the amount of Letter of Credit and the percentage of margin. A proposal for

obtaining permission for opening Letter of Credit generally contains the following points:

• Name and address of the importer;

• Name and address of the Guarantor if any;

• Particular of Merchandise to be imported along with name of the item Harmonized

System (H.S.) Code, country of origin, quantity, unit price and purpose of import.

• Particulars/ Terms of LC along with name and address of the beneficiary, tenor of

payment, port of loading and discharge, shipment validity and expiry date etc.;

A working report on Import department of Prime Bank Ltd.

15

15

• Landed cost of the goods;

• Market price of the goods at Dhaka and Chittagong (if applicable);

• Name of the previous banker with outstanding liability (if any);

• Number of CD accounts and transaction performance through this account;

• Present liability position with the bank;

• Present liability position of allied/sister concerns with the bank

• Letter of Credit performance of the party during the year/previous year;

3.2.8 Depositing of Letter of Credit Margin and Other Charges

Before issuing Letter of Credit bank asks the applicant to deposit Letter of Credit margin

according to the terms of sanction and other necessary charges which includes commission,

handling charges, foreign correspondence charge, telex/SWIFT charge etc. as per terms and

conditions of sanction.

Before issuing Letter of Credit Bank asks the applicant to deposit the following, as per the

terms of the sanction:

Letter of Credit Margin As per Government. Circular

Commission As per internal policy (Letter of Credit

value .005 for first quarter, Subsequent

Quarter .003

Document Handling Charge 1500

SWIFT Charge 3500

Courier Charge (Except India)

Courier (India)

1500

300

VAT 15% Fixed on Commission Table 3.2.9: Depositing of Letter of Credit Margin and Other Charges

Margin charged against any particular Letter of Credit depends upon the Item or Goods of

the import. Margin varies between nil to 100%. Generally the higher value of margin the

higher it means that Bangladesh Bank discourages to import that goods or items.

A working report on Import department of Prime Bank Ltd.

16

16

3.2.9 Accounting Treatment in Case of Letter of Credit Opening

Now if the Officer thinks fit the application to open a Letter of Credit, the following entries

are given to realize the Letter of Credit commission, charges, postage, Letter of Credit margin

etc.

3.2.10 Issuing the Letter of Credit

In this stage, the issuing bank fills the bank-specified-form for issuing Letter of Credit.

Generally a Letter of Credit contains the following information and terms and conditions:

• Charges;

• Country of origin of goods;

• Currency and amount ;

• Date and place of the expiry of the Documentary Credits ;

• Description of goods and quantity ;

• Documents required for negotiation;

• Instruction for negotiating bank;

• Last date of shipment;

• Letter of Credit Authorization (LCA) number, IRC (Import Registration Certificate)

number and Harmonized System (HS) code;

• Mode of Carrying –Air/Ship/Truck;

• Name and address of beneficiary ;

• Name and address of the advising bank;

• Name and address of the applicant;

• Name of the issuing Bank and Branch;

• Negotiating bank preferably freely negotiable in any bank;

• Number of Letter of Credit and date of opening ;

• Payment Term-Sight/Usance ;

• Period of Negotiation ;

• Period of presentation ;

• Port of Loading and port of Discharge;

• Reimbursing Bank and payment mode;

• Terms and conditions regarding Transshipment and Partial Shipment;

A working report on Import department of Prime Bank Ltd.

17

17

Depending on the specific provision in the underlying sales-contract (mentioned below), it

may be necessary to incorporate one or more of the following additional terms in the Letter of

Credit-

• Whether the pay of the bank charges is on account of the opener or seller

• Whether, in case of bulk import, charter-party Bill of Lading (B/L) is acceptable or

not

• Whether shipment by chartered vessel is allowed, the following causes must be

stipulated in the Letter of Credit.

• Shipping documents must include copies of Charter-party agreements and Mare’s

Receipt duly attested by negotiating Bank

3.2.11 Different Means of Payment

Importer settles the means of payment with the seller After making the purchase contract.

Import procedure differs with relation to different means of payment.

In our country in most cases, the Documentary/Letter of Credit makes import payment.

Purchase Contract contains which payment procedure has to be applied.

a) Cash in Advance:

Importer pays full, partial or progressive payment by a foreign DD, MT or TT. After

receiving payment, exporter will send the goods and the transport receipt to the importer.

Importer will take delivery of the goods from the transport company.

b) Open Account:

Exporter ships the goods and sends transport receipt to the importer. Importer will take

delivery of the goods and makes payment by foreign DD, MT, or TT at some specified date.

c) Collection Method:

Collection methods are either clean collection or documentary collection. Again,

Documentary Collection may be Document against Payment (D/P) or Document against

Acceptance (D/A). The collection procedure is that the exporter ships the goods and draws a

draft/ bill on the buyer. The exporter submits the draft/bill (only or with documents) to the

remitting bank for collection and the bank acknowledges this. Then the remitting bank sends

the draft/bill (with or without documents) and a collection instruction letter to the collecting

A working report on Import department of Prime Bank Ltd.

18

18

bank. Acting as an agent of the remitting bank, the collecting bank notifies the importer upon

receipt of the draft. The title of goods is released to the importer upon full payment or

acceptance of the draft/bill.

d) Letter of Credit:

Letter of credit is the well-accepted and most commonly used means of payment. It is an

undertaking for payment by the issuing bank to the beneficiary, upon submission of some

stipulated documents and fulfilling the terms and conditions mentioned in the letter of credit.

3.2.12 Transmission of Letter of Credit

The Letter of Credit duly signed by the authorized persons of the bank is then sent to

the advising bank. There are three modes of sending the Letter of Credits which are as follows:

• By mail/courier

• By telex: It was practiced earlier in the other branches, but from the very beginning of the

Banani Branch it did not transmit Letter of Credit though Telex.

• By SWIFT: SWIFT Stands for Society of World Wide Inter bank Financial

Telecommunication. This is special format maintained round the world. Through this

facility party can communicate within few minutes with other party staying any part of

the world. Prime Bank Limited, Gulshan Branch Provides this facility to the clients.

The advising bank verifies the authenticity of the Letter of Credit. Prime Bank has

corresponding relationship or arrangement throughout the world by which the Letter of Credit

is advised. Actually the advising bank does not take any liability if otherwise not requested.

3.2.13 Receipt and Scrutiny of Documents

After opening the Letter of Credit the next step would be to await shipment followed by

negotiation of documents by a bank abroad. The beneficiary of the Letter of Credit (supplier),

after effecting shipment of the goods as per Letter of Credit terms, prepare or collect necessary

documents as required under the terms of Letter of Credit and presents the drafts to the

negotiating bank along with the supporting documents for negotiation.

The negotiating bank negotiates the draft if the documents are found in order as per terms of

the Letter of Credit, pays the beneficiary. The negotiating bank will reimburse itself either by

debiting Prime Bank’s Account, if any, maintained with them (the NOSTRO Account) or will

seek reimbursing bank mentioned in Letter of Credit, if there is no account. Simultaneously,

the bank will send the documents to Prime Bank. The nature of documents has to be sent by the

A working report on Import department of Prime Bank Ltd.

19

19

negotiating bank will depend primarily on the terms of the Letter of Credit and secondly the

sales contact between the buyer and seller. However, generally the following documents are

asked to send:

• Bill of lading or Airway Bill or other evidence of shipment (e.g. Railway Receipt, Truck

Receipt, Barge Receipt)

• Certificate of Origin;

• Commercial Invoice;

• Draft or Bill of Exchange;

• Inspection of Survey Certificate;

• Marine Insurance Policy;

• Packing List;

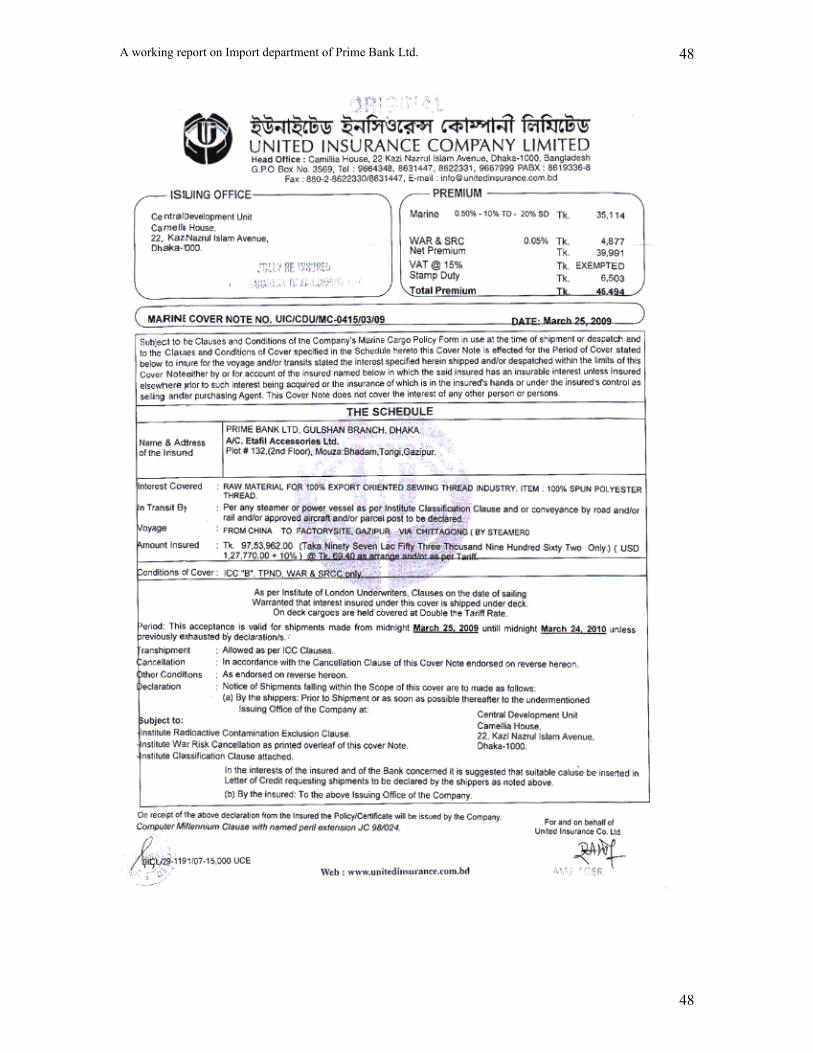

• Quality Control Certificate. (Appendix C)

3.2.14 Scrutiny of Documents

On receipt of the documents the branch shall immediately set itself to the task of scrutinizing

the documents. What they would ensure is that the documents received from the negotiating

bank are drawn strictly in conformity with the terms of the Letter of Credit and respond to the

requirement of the underlying Letter of Credit in every respect. Examination of the documents

generally includes the following points:

• Completeness of the documents;

• Consistency of the documents with each other;

• Compliance with the Uniform Customs and Practices for Documentary Credits (UCPDC)

issued by the International Chamber of Commerce, Paris.

One of the basic principles of documentary credit is that all parties deal with document and

not with goods (Articles 6 of UCPDC-500). That is why the documents should be scrutinized

properly. If any discrepancy in the documents is found, that is to be informed to the party. A

checklist may be followed for examining the documents.

In the UCPDC the Standard for Examining of Documents is mentioned as follows:

A working report on Import department of Prime Bank Ltd.

20

20

a) Banks must examine all documents stipulated in the Credit with reasonable care, to

ascertain whether of not they appear, on their face, to be in compliance with the terms

and conditions of the Credit

b) The Issuing Bank, the Conforming Bank, if any or a Nominated bank acting on their

behalf, shall each have a responsible time, not to exceed seven banking days following

the day of receipt of the documents, to examine the documents and determine whether to

take up documents and to inform the party from which it received the documents

accordingly.

c) If a credit contains conditions without stating the document(s) to be presented in

compliance there with, bank will deem such conditions as not stated and will disregard

them.

3.2.15 Discrepant Documents and Notice

a) When the Issuing Bank authorizes another bank to pay, incur a deferred payment

undertaking, accept Draft(s), or negotiate against documents which appear on their face to be

incompliance with the terms and conditions of the Credit, the Issuing Bank and the

Conforming Bank, if any are bound:

I. To reimburse the Nominated Bank which has paid, incurred a differed payment

undertaking accepted Draft(s) or negotiated,

II. To take up the documents.

b) Upon receipt of the documents the Issuing Bank, and/or Conforming Bank, if any, or

Nominated Bank, acting on their behalf, must determine on the basis of the documents alone

whether or not they appear on their face to be in compliance with the terms and conditions of

the Credit. If the documents appear on their face not be in compliance with the terms and

conditions of the Credit, such banks may refuse to take up the documents.

c) The Issuing Bank determines that the documents appear on their face not to be in

compliance with the terms and conditions of the Credit, it may in its sole judgment approach

the Applicant for a waiver for the discrepancy.

d) i. If the issuing Bank and/or Conforming Bank, if any, or a Nominated bank acting on their

behalf, decides to refuse the documents, it must give notice to that effect by telecommunication

A working report on Import department of Prime Bank Ltd.

21

21

or, if that is not possible, by other expeditious means, without delay but not later that the close

of the seventh banking day following the day of receipt of the documents. Such notice shall be

given the bank form which it received the documents, or to the Beneficiary, if it received the

documents directly from him.

ii. The issuing Bank and/or Conforming Bank, if any shall then be entitled to claim from the

emitting bank, with interest, of any reimbursement which has been made to that bank.

e) If the issuing Bank and/or Conforming Bank, if any, fails to act in accordance with the

provisions of this Article and/or hold the documents at the disposal of, or return them to the

presenter, the issuing Bank and/or Conforming Bank, if any, shall be precluded form claiming

that the documents are not in compliance with the terms and conditions of the Credit.

f) If the reimbursing bank draws the attention of the issuing Bank and/or Conforming Bank, if

any, to any discrepancy (ies) in the document(s) or advises such banks that it has paid, incurred

a deferred payment undertaking, accepted Draft(s) or negotiated under reserve or against an

indemnity in respect of such discrepancy (ies), the Issuing Bank, if any, shall not be thereby

relieved from any of their obligations under any provisions of this Article.

3.2.16 Disclaim on Effectiveness of Documents

Banks assume no liability or responsibility for the form sufficiency, accuracy, genuineness,

falsification or legal effect of any document(s), or for the general and/or particular conditions

stipulated in the document(s) or superimposed thereon; nor do they assume any liability or

responsibility, quantity, weight, quality, condition, packing, delivery, value of existence of the

goods represented by any document(s), or for the goods faith or acts and/or omissions,

solvency, performance or standing of the consignors, the carrier, the forwards , the consignees

or the insurance of the goods or any other person whomsoever.

Then the following things can happen. These are indicated in the following:

1. Discrepancy found but the importer accepts - then the bank will lodge the documents

2. Discrepancy found and importer not agreed to accept - Issuing bank would intimate

negotiating bank for revised document or return the documents to the negotiating

bank for necessary action. Here issuing bank is not bound to pay because the

documents send by exporter is not in accordance with the terms of Letter of Credit.

A working report on Import department of Prime Bank Ltd.

22

22

3. Documents are OK but importer is not willing to retire the documents - In this case

bank is obligated to pay the price of exported goods. Since importer did not pay for

bill of exchange, this payment by bank is one kind of credit to the importer and this

credit in banking is known as Forced Payment against Documents (PAD).

4. Everything is O.K. but importer fails to clear goods from the port and request bank to

clear - In this case banks clear the goods and takes delivery of the same by paying

customs duty and sales tax etc. So, this expenditure is debited to the importer’s

account and in banking it is called LIM.

The above mentioned description could be pointed out as under:

a. The seller being satisfied with the terms and the conditions of the credit makes shipment of

the goods as per Letter of Credit terms.

b. After making the shipment of the goods in favor of the importer the exporter submits the

documents to the negotiating bank.

c. After receiving all the documents, the negotiating bank then checks the documents against

the credit. If the documents are found in order, the bank will pay, accept or negotiate to Prime

Bank

d. Branch & Bank received seal to be affixed on the forwarding schedule

e. The Bill of Exchange & transport documents must immediately be crossed to protect loss or

fraudulent.

3.2.17 lodgment

After the scrutiny the following steps are taken step-by-step to process for lodgment of

import documents received form the negotiation bank. Usually payment is made within seven

days after the documents have been received. If the payment is become deferred, the

negotiating bank may claim interest for making delay. However, after receiving the documents

Banani Branch authority contacts with an importer, in which procedure they want to collect the

documents.

Lodgment Constitutes the Followings:

• Conversion of foreign currency amount of the bill and the foreign bank charges

separately into Taka by applying Bills Collection (B.C.) selling rate ruling on the date

of lodgment is done. If forward exchange was, the booked rate is applied.24 Payment

against Documents (PAD) is created by Debiting PAD Account and Crediting Head

Office Account. Full particulars of the documents are entered in the prescribed PAD

A working report on Import department of Prime Bank Ltd.

23

23

Register allotting a consecutive serial number in the register. If the forward exchange

rate is booked then the booked rate is applied. Payment against Documents (PAD) is

created by Debiting PAD Account and Crediting Head Office Account. Full particulars

of the documents are entered in the prescribed PAD Register allotting a consecutive

serial number in the register.

• Documents are endorsed by putting seal and signature.

• “Inter-Brach credit advice” (IBCA) is sent to the Head Office along with a prescribed

statement to provide them credit for the payment from their overseas account through

Prime Bank Limited General Account.

• Head Office (International Division) in receipt of the IBCA and the statement will

respond the entry by debit to branch account (through Prime Bank Limited General

Account) and contra credit to NOSTRO Account of the negotiating bank abroad.

• As soon as above formalities are completed the importers are served with PAD bill

intimations for retirement of concerned import document.

3.2.18 Retirement of the Documents

On receipt of cost memo/lodgment voucher the importer pays the necessary amount. This

stage of the documentary credit operation is known as ‘Retirement of Import Bills’. The branch

will prepare the retirement voucher to reflect the amount of cost and other charges to be

collected from the importer, adjustments of margin and PAD Account. Thereafter the

documents may be handed over to the importer against proper acknowledgement after

certification and endorsement. The certifications by authorized personnel of the bank are as

follows:

• The invoice is certified by the authorized officer of the bank with the exchange rate as

applied in lodgment;

• The bill of Exchange received from negotiating bank on issuing bank by the beneficiary;

• The Transport Documents evidencing the carrying of goods as per Letter of Credit term

has to the endorsed by the AD branch.

On receipt of intimation, the importer is given necessary instructions with regard to

retirement of the bill, disposal of the shipping documents and clearance of the goods from the

customs authorities. The importer may ask the bank to retire the bill by Debiting his account or

may request for the providing LIM or LTR facility, if arranged earlier.

A working report on Import department of Prime Bank Ltd.

24

24

On intimation the importer approaches with a letter for retirement of the document against

full payment with up to date interest and charges payable. Bank prepares cost memo in printed

form on account of the concerned party giving details head of charges payable.

3.2.19 Financing Related with Import

Advances against Import Bill are originated for the lodgment of shipping documents

received from foreign correspondents against Letter of Credit estimated by the Bank on behalf

of its customers. Threes bills of lodged by debiting PAD account and crediting HO account.

To Create PAD, the documents received form the negotiating bank is to be scrutinized

thoroughly whether they are in order as per L. C terms. If on scrutiny, the documents are found

in order, lodgment of the same is done as PAD, after converting the Foreign currency into Taka

at the conversion rate.

• Loan Against Imported Merchandise (LIM)

Parties who are not in position to retire the documents, they maybe allowed to retire the

PADs through LIM Account on retaining sufficient margin n the landed cost of the goods or as

prescribed by Bangladesh Bank.

Even if they are reluctant to provide aforesaid margin, goods may be allowed to be cleared

through LIM account under forced circumstances to same the consignment form incurring

demurrage, pilferage, and auction and to protect the interest of the Bank.

• Under such circumstances, goods are cleared only through approved Clearing Agent of the

Bank.

• The consignment after clearance is stored in Bank’s own go-down duly insured against all

risks.

• The delivery of the consignment is made on the parties against payment only, without

resorting to any borrowing from the Bank on that behalf.

• Loan Against Trust Receipts (LTR)

Advances against a Trust Receipt obtained from the Customer are allowed to only first

class tested parties when documents covering an import shipment of other goods pledged to the

Bank as scrutiny are given without payment. However, for such advances prior

permission/sanction form Head Office must be obtained.

A working report on Import department of Prime Bank Ltd.

25

25

The customer holds the goods or their sale –proceeds in trust for the Bank, till such time, the

loan allowed against the Trust Receipts is fully paid off.

• Period Of Trust Receipt

The Advance allowed against Trust Receipt must be adjusted within the stipulated period. It

should be noted that the sale proceeds of goods held in trust must be deposited in the Bank by

the borrower initially irrespective of the period of Trust Receipt.

Fortnightly statement of sale of LTR goods to be obtained forms the customer and be

reviewed to ensure that the sale proceeds have been properly deposited towards adjustment of

the loan.

• Collateral Security

Collateral security valuing double of the amount o LTR to be obtained. Any exception to

this rule requires approval by Head Office.

3.2.20 Credits Occurred in Letter of Credit Operation

During Letter of Credit operation some Credit facilities evolved to the importer and exporter.

This credit facilitates are mentioned below

Payment Against

Document (PAD)

a. This loan is related to cash Letter of Credit.

b. After opening Letter of Credit, foreign exporter sends goods to

the importer and a bill of exchange along with shipping

documents to the Letter of Credit opening bank. Upon receiving

bill of exchange and other documents, bank immediately make

payment to the exporter if no discrepancies are found on the

shipping documents. Bank hands over the shipping documents to

the importer only after his recovery of the payment from the

importer. Since bank pay to exporter on the basis of shipping

documents, this is called Payment against Documents.

Loan Against

Imported

Merchandise

a. LIM is occurred from PAD.

b. After payment to the exporter on the basis of shipping

documents, bank recovers the amount from the importer.

A working report on Import department of Prime Bank Ltd.

26

26

(LIM) Sometimes for financial crisis, importer fails to pay the amount

stipulated in bill of exchange to the Opening Bank. In this case,

he request to the bank to treat PAD as credit and handover the

shipping documents to him so that he can clear the imported

goods from the port. Then banks convert the PAD to regular

credit and hand over the documents to the importer, and take the

imported goods as security for the loan. Since this loan is given

on the imported goods, this is called Loan against Imported

Merchandise. Duration of this loan is one month only. If the loan

is no repaid after one month, it is treated as forced LIM.

IP Loan a. When Letter of Credit opener has no sufficient fund to

purchase

Foreign Exchange to open Letter of Credit, then bank provides

him credit to purchase necessary foreign exchange under the

WES/SEM. This loan is called Import Loan under WES/SEM or

IP loan.

Table 3.2.21.1: Credits Occurred in Letter of Credit Operation

• Shipping Guarantee

Shipping Guarantee is given to the Party or Client when goods arrive prior to arrival of

documents. This happens mostly in cases of air shipment, shipment by truck from Land or

shipment by post parcel. In such cases bank endorses non-negotiable shipping documents for

clearance of the goods subject to scrutiny and the documents being in order and settlement of

the bank dues against the relative bills.

For giving guarantee bank charges Tk. 250 from the parties account.

A working report on Import department of Prime Bank Ltd.

27

27

• Endorsement by the Bank

The bank endorses the documents in following manner:

Document Endorsement

Bill of Exchange Receive/Payment for The Prime Bank

Limited

Commercial Invoices Invoice value certifies & remitted for The

Prime Bank Limited

Bill of Lading, Airway Bill, Truck Challan Deliver / Pay to the order of M/S ---, for

The Prime Bank Limited

LCA For The Prime Bank Limited

Table 3.2.21.2: Endorsement by bank

Then importer releases the importers goods from the port authority with the help of the

Clearing and Forwarding (C&F) agent, who, clears the goods from the port and hands over the

goods to the importers.

After completion of all official requirements C&F agent submits the bill of entry of the

banks. The Bill of Entry is wanted from the party for maintaining the evidence as the goods has

been arrived.

• Cost

At the time of retirement of the shipping documents against payment by debit to the account

of the importer the branch prepares cost memo in printed from covering the bill amount and

foreign currency charges etc. giving detailed heads of charges payable by the applicant which

includes

• Delivery of Shipping Documents

If the bill is to be realized by debit to the importer’s account, the documents are handed over

to the importer to his duly authorized clearing and forwarding agent for clearance of the goods

form customs at his own account.

A working report on Import department of Prime Bank Ltd.

28

28

• Payment to the Foreign Bank Import of Goods

Negotiating Bank is authorized to Debit Head Office Account (PBL) directly, if the

account is maintained with them. Negotiating Bank is authorized to obtain reimbursement

claim form foreign correspondent with which account is maintained by Head Office (PBL)

Where reimbursement is provided subsequent to the receipt of documents, an authority

Letter is to send to correspondent abroad with whom account is maintained by Head Office to

make payment to the Negotiating Bank to debit of PBL account maintained with them for the

amount of the documents.

Import is another primary form of foreign trade, where foreign commodities are brought

into the country for consumption. Prime Banks has been providing this services to its client

since it began operation in the mid 90’s. Various sorts of commodities are imported in to

Bangladesh from Fast Moving Consumer Goods to Capital Machinery. (See Appendix B,

Appendix Figure 1.0, Appendix Figure 2.0)

Now if we want to compare the volume of different genre of goods being imported we

would see that most of the imports in Bangladesh are industrial raw materials and it represents

almost 50% of the total imports. Then we have Consumer Goods contributing to 15% of the

total import.

A working report on Import department of Prime Bank Ltd.

29

29

Chapter four 4.0 My responsibilities and my work

The import trade process in Prime Bank Ltd is a prolonged process. It involves intense file

work. The import trade department of Prime Bank Gulshan Branch consists of four bank

officials, including department Head. As an intern I assisted each of them in their work. Being

an intern I had limited authority regarding financing and other delicate activities, for example

lodgment of L/Cs. Issuing L/Cs, Repoting to Bangladesh Bank, Issuing and sending PSI(Pre-

Shipment Investigation) letter, filing huge number of L/C related documents etc were my

routine work. Most of my knowledge were gathered through observing activities of officers,

face to face conversation with the bank officers, appointment with the top officials of the Bank,

by interviewing L/C customers at PBL, Gulshan Branch and other secondary sources.

A working report on Import department of Prime Bank Ltd.

30

30

Chapter five 5.0 Results and Conclusion

Every year the foreign transaction of Prime Bank ltd has been on the rise contributing more

and more to the country’s economic growth. And the last few years were no different with

significant rise in remittance during the last quarter of 2008. However the didn’t show any

signs of restrains and neither did it show any changes in terms of commodities being traded, as

the volume of trade kept on increasing. No matter whatever the challenges are in the area of Foreign Trade, Prime Bank is fully

equipped to face any obstacle. For the last 5 Years they have hold the Number 1 position in the

Bangladesh Banks CAMELS rating and hopes to be on top this year as well.

As the economy of Bangladesh is increasing so is the country foreign trade and Prime

Banks like always have played its role in making sure that things go smoothly. However, since

sky is the limit, the bank is still evolving every day striving to provide its Foreign Exchange

customer and others with the best possible service.

Export, Import and Remittance are all showing positive trends even after the global

challenges that we are facing today. Hyped fuel and rice price all over the world along with the

country’s own political instability couldn’t bring down the nations economy and 2009 still

seems to be another promising year for us.

A working report on Import department of Prime Bank Ltd.

31

31

Chapter six 6.0 Recommendations

We all know that there is always room for improvement and sky is the limit. Even thought

the Foreign Exchange services that Prime Bank is providing is top notch, there is more they

can do in order to make their services even better and of international standards. Given below

are some recommendations that the Bank may benefit from,

• Increase the number of Nostro Accounts:

Nostro Accounts are Foreign Currency accounts that the banks hold with foreign Banks

operating in different courtiers. If they increase the number of such account then, payments for

L/C could be easily made through those accounts rather than forwarding the foreign currency

through other foreign banks, which results in higher expenses.

• Automation

Prime Bank has already brought software called Temenos Globus, famous banking software

which is now being implemented to all of its branches. Some further simplification and

modification to the software might actually help the bank gain momentum in providing

international trade services like Export, Import and Remittance.

• Increase Limit on L/C Value

Every LC has limits on its total value, imposed on them according to the Bangladesh Banks

regulations, and based on the risk factors. However the Banks stills has the authority to make

some changes to the limit within a certain specified range. Hence, if Prime Bank is more

flexible than it can open more L/C’s with higher values thus increasing their profitability,

however in this case they would be taking more risk.

• Rate of interest on LTR

Payments for L/C’s could also made through pre arranged credit facilities that the customer

may have with the Bank. Usually, the rates of interest on these credits are excessively high

which actually discourages the customers. Reducing interest on such credit facilities would

actually induce the clients to do more global trade thus increasing the banks profit as well as

the well being of the country’s Economy.

A working report on Import department of Prime Bank Ltd.

32

32

• LC margin BB

Before opening an L/C a customer is required to pay the bank a certain percentage of the

total L/C value in advance, called the margin. If Prime Banks reduces the rate of margin then

perhaps they can attract more customers. At the moment, Companies with good relationship

with the banks only benefits with lower margin level over others.

• Reduce Charges

In order to do any kind of foreign trade whether be it Remittance, Export or even Import

charges are applicable everywhere. Charges includes, SWIFT charges (Charge for sending the

L/C electronically), Document Handling Charges, Stamps Charges as well as VAT. If such

charges could be reduced people Prime Bank will definitely attract more customers.

• Relax restriction on certain products

Prime Bank has put some restriction on the import of certain products due to bad experience

form the past. If they could ward of their fear and start importing such products again they

would definitely be adding few more figures to the banks profit.

• Doesn’t open smaller LC value

Being a well reputed Bank, Prime no longer wants to conduct smaller L/C request coming

form SME’s and as a result they are neglecting a huge number of potential customers. The

bank now pays more attention to big customers and if their attitude toward smaller business

doesn’t change soon, they might fall far behind its competitor.

A working report on Import department of Prime Bank Ltd.

33

33

References "Bangladesh Bank." Bangladesh Bank. 5 Mar. 2009 <http://www.bangladesh-bank.org/>.

Chaudhury , A.J.. Commercial bank restructuring in Bangladesh. Dhaka: BG Press, 2000.

"Prime-bank Limited." Prime-bank Limited. 30 Mar. 2009 <http://www.prime-bank.com/>.

"Prime-bank Limited." Prime-bank Limited: Annual Reports 2006,2007,2008 . 30 Mar. 2009

<http://www.prime-bank.com/annual_report.htm>.

Publications, Usa International Business. Bangladesh Central Bank & Financial Policy

Handbook (World Business, Investment and Government Library). New York: Intl

Business Pubns Usa, 2005.

Module-2: International Trade Management and Finance . Dhaka: Prime Bank Training

Institute, 2005.

A working report on Import department of Prime Bank Ltd.

34

34

Appendices APPENDIX-A: List of Tables

SECTORS L/C

Opened in

2006

Percentage

of Total

L/C

Opened in

2006

L/C

Opened in

2007

Percentage

of Total

L/C

Opened in

2007

CONSUMER GOODS 74615.74 11% 125967.26 15%

INTERMEDIATE GOODS 55984.35 8% 61874.08 7%

INDUSTRIAL RAW MATERIALS 335250.74 51% 431961.88 50%

PETROLEUM & PETROLEUM

PRODUCTS

0 0% 0 0%

CAPITAL MACHINERY 68547.46 10% 78295.38 9%

MACHINERY FOR MISC.

INDUSTRIES

47447.09 7% 65019.6 7%

OTHERS 78570.64 12% 105252.33 12%

Total 660416.02 100% 868370.53 100%

Appendix Table 1.0: Details volume and type of commodities for L/C

Appendix Table 2.0: Growth in L/C during 2006-2007

Total L/C Opened at Prime Bank Ltd

Year 2006 Year 2007 Percentage Growth

660416.02 868370.53 31.49%

A working report on Import department of Prime Bank Ltd.

35

35

2006 2007

January 8,110,892 8,204,230

February 9,418,614 10,613,865

March 7,448,790 11,130,763

April 9,964,298 12,797,982

May 12,009,278 14,230,098

June 10,858,600 13,614,019

July 17,906,701 14,373,589

August 23,624,640 11,597,671

September 11,994,048 15,295,374

October 9,503,281 15,605,268

November 28,883,806 18,262,798

December 12,093,509 17,916,560

Total 161,816,457 163,642,218

Average 13,484,705 13,636,851

St. Deviation 6,625,184 2,970,004

Appendix Table 3.0 : Monthly Influx of Foreign Currency in Terms of USD

A working report on Import department of Prime Bank Ltd.

36

36

APPENDIX-B: List of Figures

LC Opened in 2006

CONSUMER GOODS11%

INTERMEDIATE GOODS8%

INDUSTRIAL RAW MATERIALS

52%

PETROLEUM & PETROLEUM PRODUCTS

0%

CAPITAL MACHINERY10%

OTHERS12%MACHINERY FOR MISC.

INDUSTRIES7%

Appendix Figure 1.0: LC Opened during 2006

LC Opened in 2007

CONSUM ER GOODS15% INTERM EDIATE

GOODS7%

INDUSTRIAL RAW M ATERIALS

50%

PETROLEUM & PETROLEUM PRODUCTS

0%

CAPITAL M ACHINERY9%

M ACHINERY FOR M ISC. INDUSTRIES

7%

OTHERS12%

Appendix Figure 2.0: LC Opened during 2007

A working report on Import department of Prime Bank Ltd.

37

37

Appendix-C: Few required Documents of L/C

A working report on Import department of Prime Bank Ltd.

38

38

A working report on Import department of Prime Bank Ltd.

39

39

A working report on Import department of Prime Bank Ltd.

40

40

A working report on Import department of Prime Bank Ltd.

41

41

A working report on Import department of Prime Bank Ltd.

42

42

A working report on Import department of Prime Bank Ltd.

43

43

A working report on Import department of Prime Bank Ltd.

44

44

A working report on Import department of Prime Bank Ltd.

45

45

A working report on Import department of Prime Bank Ltd.

46

46

A working report on Import department of Prime Bank Ltd.

47

47

A working report on Import department of Prime Bank Ltd.

48

48

A working report on Import department of Prime Bank Ltd.

49

49

A working report on Import department of Prime Bank Ltd.

50

50

A working report on Import department of Prime Bank Ltd.

51

51

A working report on Import department of Prime Bank Ltd.

52

52