a synthesis of theoretical and empirical research on sukuk · a synthesis of theoretical and...

TRANSCRIPT

A synthesis of theoretical and empirical research on sukukMuhamed Zulkhibri

Islamic Research and Training Institute, Islamic Development Bank, Jeddah, Saudi Arabia

Received 29 March 2015; revised 1 October 2015; accepted 22 October 2015

Available online 7 November 2015

Abstract

This paper provides a critical review of the theoretical and empirical literature on sukuk (Shari’ah-compliant bonds) from three perspectives:their underlying theory and nature, the operational issues and structures involved in sukuk, and the role of sukuk in economic development.The article suggests that the literature on sukuk is largely qualitative rather than quantitative research, with the bulk of academic research inthe form of conference and seminar papers. The research on sukuk in the form of journal articles, books, conference papers, reports, andmagazines has increased substantially, but it is still in relatively short supply in comparison to other research on Islamic finance. Thisunderdeveloped state of research on sukuk is mainly due to a lack of historical, reliable, and consistent data; a limited number of academicinstitutions dedicated to Islamic economics and finance; the small number of high-quality refereed journals as potential outlets for Islamicfinance research; the unresolved concept of sukuk among Shari’ah scholars; and the absence of a global standard and accreditation for Islamicfinance courses.Copyright © 2015, Borsa Istanbul Anonim Sirketi. Production and hosting by Elsevier B.V. This is an open access article under the CCBY-NC-ND license (http://creativecommons.org/licenses/by-nc-nd/4.0/).

JEL classification: G10; G01

Keywords: Islamic finance; Sukuk structure; Sukuk research

1. Introduction

In recent years, many developed and developing Muslimand non-Muslim countries have become interested in sukuk asone of the best alternative for raising finance beyondconventional finance. Nigeria, Morocco, and South Africa inAfrica, France and the United Kingdom in Europe,Kazakhstan in Central Asia, and Brunei in East Asia haveamended their laws and regulations to allow sukuk to beissued in their financial markets, and many other countries areplanning to do so. Thomson Reuters Zawya (2015) confirmsthat sukuk are becoming an increasingly important Islamicfinancial instrument in both Muslim and non-Muslimcountries. Sukuk have also become a significant tool forraising finance effectively and efficiently in term of the

allocation and mobilization of resources on internationalcapital markets.

Sukuk began to be broadly issued1 in February 1988 afterthe Council of the Islamic Fiqh Academy of the Organizationof Islamic Conference (OIC) held its fourth session in Jeddah,Saudi Arabia.2 Initially, the issuance of sukuk was in responseto the demands of issuers and investors in Muslim countries asan alternative mode for their financing and investment needsthat complies with the Shari’ah requirements. In May 2003,the Accounting and Auditing Organization for Islamic FinancialInstitutions published the “Standard for Investment sukuk, inwhich sukuk were defined as certificates of equal valuerepresenting undivided ownership shares in tangible assets,

E-mail address: [email protected] review under responsibility of Borsa Istanbul Anonim Sirketi.

1 The first modern sukuk issuance can be traced to 1983, when theMalaysian government launched a government bond known as governmentinvestment certificate (SPK) based on the concept of Qard al-Hasan(benevolent loans).

2 Resolutions and Recommendations of the Council of the Islamic FiqhAcademy, Resolution No. 30 (5/4), p. 61.

http://dx.doi.org/10.1016/j.bir.2015.10.0012214-8450/Copyright © 2015, Borsa Istanbul Anonim Sirketi. Production and hosting by Elsevier B.V. This is an open access article under the CC BY-NC-NDlicense (http://creativecommons.org/licenses/by-nc-nd/4.0/).

Available online at www.sciencedirect.com

Borsa Istanbul Review 15-4 (2015) 237–248http://www.elsevier.com/journals/borsa-istanbul-review/2214-8450

usufruct, and services.3 Recent innovations in Islamic financehave changed the dynamics of the Islamic capital market withrespect to sukuk and securities. On international capital markets,sukuk have developed into one of the most acceptable Islamicstructures for raising finance, which in turn has led to itsincreasing use in recent years by government and privateinstitutions (Kusuma & Silva, 2014).

The word sukuk comes from the plural of the Arabic wordsakk, or bonds or securities structured according to Shari’ahprinciples, which prohibit Islamic issuers and investors frominvesting in conventional securities. Sukuk are also calledIslamic bonds or Islamic investment certificates, which struc-ture securitized leases (ijarah) and other Islamic financing con-tracts, such as murabahah (sale with markup), musharakah (acombination of equity contribution and proportional profit andloss sharing on the basis of partnership), and mudarabah (part-nership between one person who contributes capital andanother who provides managerial skills) (McMillen, 2007a;Obaidullah, 2007).

In 1990, the first sukuk were issued in Malaysia by ShellMDS (a foreign-owned non-Islamic corporation). Since then,the market for sukuk has flourished, but Islamic financialmarkets are having difficulty in fully developing in manyemerging Muslim countries because Islamic finance is stilllimited with respect to interest rate swaps and other conven-tional derivative instruments. Managing risk requirements forsukuk and considerations of competitiveness should force thesukuk structures to further evolve and offer Shari’ah-compliantalternatives to traditional derivatives.

The sukuk market is also seen as a way to channel theworld’s growing pool of Shari’ah-compliant capital to be usedto promote sustainable and equitable economic development.As of 2014, the global sukuk market was worth more thanUS$600 billion, and it continues to drive the growth anddevelopment of Islamic finance (IIFM, 2014; ThomsonReuters Zawya, 2015). New sukuk markets are opening up ina number of countries, such as Morocco, Nigeria, Oman, andSouth Africa, and Tunisia is finalizing regulations to allowsukuk to be issued. The sukuk sector is the fastest-growingsegment of the global Islamic financial industry, with acompound annual growth rate (CAGR) close to 20 percent inbetween 2010 and 2014. The issuance of sukuk has increasedrapidly, there is still potential for further growth. Global sukukissuance totaled about US$114.5 billion in 2014 (see Fig. 1).Malaysia held about 65 percent of global sukuk issuance interms of market share, while the Middle East and NorthAfrica (MENA) accounted for 23.7 percent. Saudi Arabia, thesecond-most-active sukuk market, accounted for 10.3 percent,followed by Indonesia (5.4 percent), the United Arab Emirates(UAE) (5 percent), and Turkey (3.6 percent). Malaysianringgit–denominated issues topped the charts in value, with60 percent of total global issuance, at US$68.4 billion.

Sovereign issuances dominated the global sukuk market, withUS$439 billion, or more than 60 percent of total issuances in2004–2014 (see Table 1).

Research on sukuk has gained momentum and popularityamong policymakers, academics, and practitioners since thelate 1990s. The amount of research in the form of articles,books, conference papers, and other materials—such asreports, magazines, blogs, and newspaper articles – hasincreased substantially. However, the literature concentrateslargely on descriptive analysis of sukuk structures, issuances,and Shari’ah issues, rather than empirical and scientificanalysis. Given the fact that research on sukuk has increaseddramatically, the objective of this article is to provide a criticalreview of the state of research on the sukuk and to evaluate thegaps in the literature so as to recommend directions for futureresearch. Issues in the existing literature and unansweredquestions are also identified.

3 Defined in Shari’ah Standards for Financial Institutions 2008, published bythe Accounting and Auditing Organisation for Islamic Financial Institutions, p.307, para. 2.

Fig. 1. Global sukuk issuance (in US$ billion). Source: Zawya, IFIS (2014).

Table 1Sovereign sukuk issuance (2004–2014).

Country No. of issuance Amount ($m)

Bahrain 226 12,545Gambia 401 194Malaysia 1388 351,494Pakistan 17 7669Brunei 113 6093Turkey 7 6900Hong Kong 1 1000Luxembourg 1 272Indonesia 65 21,890South Africa 1 500Senegal 1 200United Kingdom 1 340Qatar 17 19,655Nigeria 1 71Germany 1 123Singapore 5 193UAE 11 6855Yemen 2 250Sudan 26 2868Total 2285 439,111

Source: Zawya, IFIS (2014).

238 M. Zulkhibri /Borsa Istanbul Review 15-4 (2015) 237–248

This paper is organized as follows: Section 2 describes thechallenges involved in developing a sukuk market. Section 3offers a critical review of the existing literature on sukuk.Section 4 is the conclusion.

2. The challenges of developing a sukuk market

Sukuk are developing into a global asset class, supportingdevelopment with the participation of a wide range of issuersand investors irrespective of religious orientation. Internationaldevelopment agencies and multilateral institutions, such theWorld Bank and the Asian Development Bank, can explorevarious options for structuring and issuing more innovativesukuk as well as overcoming the limitations that currently existin the sukuk market to unleash their potential as a source ofdevelopment finance. This issue is interesting, as financial engi-neering of sukuk seems to be taking place by simply modifyingthe existing conventional products to be in accordance withIslamic legal requirements and maintaining the other objectivesof the capitalist financial system. Therefore, sukuk shouldessentially be structured in the spirit of creating an Islamicfinancial system, which is based on Islamic principles andserves the noble goals prescribed by Islam (Maqasidal-Shari’ah). However, efforts by Islamic scholars and practi-tioners are skewed toward structuring products and contracts toresemble those of existing conventional products to ensure thecontracts are legally valid.

Although sukuk markets are still in a formative stage, theyhave developed at a significant pace. If corporate sukuk areissued regularly, coupled with an initiative to develop a second-ary market and harmonize a regulatory framework, sukukmarkets will mature. At present, only a small proportion ofsukuk are traded, with most investors taking a buy-and-holdapproach. The major constraints on sukuk investments include:(1) there is neither a recognized secondary market nor activetrading; (2) most major investors use a buy-and-hold strategy;(3) there are few, if any, market makers; (4) some countries lackregulatory support; (5) a lack of harmonization exists amongsukuk structures; and (6) various Shari’ah boards use differentinterpretations.

Some scholars see sukuk not as Islamic financial instrumentsbut as “Islamic bonds” or fixed income instruments that are

Shari’ah-compliant (Al-Jarhi, 2013). Others argue that sukuk asShari’ah-compliant financial instruments have a broaderresponsibility to consider social goals such as sustainable devel-opment. Sukuk can be either asset based or asset backed.4 Table2 lists the fundamental differences between these two struc-tures. In asset-based sukuk, the sukuk holders have beneficialownership in the asset or equitable interest in the assets to aspecial purpose vehicle (SPV) issuer. The principal is coveredby the capital value of assets, but returns and repayment tosukuk holders are not directly financed by these assets. There-fore, it is not a true sale. The sukuk holders have recourse to theoriginator if there is a shortfall in payment. For this reason,these are merely credit-backed securities with no real recourseto physical assets. From the perspective of Shari’ah, it is essen-tial for sukuk to be backed by a specific, tangible asset through-out its entire tenure, and sukuk holders must have a proprietaryinterest in the assets that are being financed (Yean, 2009).

Malaysia has the largest sukuk market in the world and haspioneered many innovative sukuk structures (IIFM, 2014),despite facing many constraints in developing it. The stronggrowth of sukuk in Malaysia has been supported by thefollowing key factors: (1) the growing sophistication of sukukstructures; (2) the transparency of regulatory treatment; and(3) a strategic focus on developing a comprehensive Islamicfinancial system. Malaysia has adopted a holistic approach tostrengthening the sukuk market through rules that facilitatetheir issuance, a well-defined Shari’ah governance framework,competitive pricing, innovative sukuk structures and humancapital development, incentives for sukuk investmentactivities, and a comprehensive infrastructure for Islamiccapital markets.

To move the sukuk market forward as well as to capitalize onits enormous growth potential, the issue of Shari’ah harmoni-zation should be addressed with greater cooperation and coor-dination among the industry players. There is also an urgentneed for new capital market products to be restructured tocomply with Shari’ah as well as the creation of an internationalsukuk fund. There is also a need to diversify the type and

4 In practice, there are three kinds of sukuk: asset based, asset backed, andcash-flow finance.

Table 2Comparison of salient features of asset-backed and asset-based sukuk.

Feature Asset-based sukuk Asset-backed sukuk

Ownership Only provides artificial ownership rights to the “usufruct” ofcertain physical underlying assets, instead of relying on theobligor’s credit quality to ensure that the sukuk performs.

Asset-backed sukuk imply that ownership rights extend to theactual underlying assets such as physical real estate orrights/usufruct from particular intangible but valuable assets.

Asset recourse tothe investor

The recourse of the investor is to the creditworthiness of theultimate obligor

Recourse of the investors is to the asset-issuing vehicle, andsukuk investors bear any losses in case of impairment of thesukuk.

Rating Corporate rating methodology is used for asset-basedtransaction of sukuk whenever a corporate obligor is the keydriver affecting credit risk of sukuk.

Asset-backed rating methodology will be used for theasset-backed sukuk transaction, which involves securitization.Here, credit risk is determined solely by the performance ofunderlying assets.

Source: Adapted from Noor (2009).

239M. Zulkhibri /Borsa Istanbul Review 15-4 (2015) 237–248

maturity of the sukuk in the market and to help portfolio man-agers to manage their funds effectively. To address thesematters, investors and issuers should regularly circulate sukukwith different maturities to create a benchmark yield curve.Another aspect of growth is concerns over pricing issues (i.e.,securities need to be efficiently priced and credible), and furtherinitiatives to develop sukuk indicators are also needed for sukukmarkets.

The development of sukuk market will be facilitated by thecreation of a guide for issuers and investors that can act as acomplete reference concerning Shari’ah decisions that aretransparent and fully disclosed. This guide would help ensureproper governance and wider acceptance of Shari’ah decisions,particularly on cross-border transactions as well as attainmentof the convergence of Shari’ah principles and interpretation toensure market confidence among investors. Continuousinvestments in intellectual capital and greater engagementamong Shari’ah scholars are needed to achieve convergence inthe sukuk market. The harmonization of standards and practicesare also important for the global acceptance of Islamic financialproducts including sukuk. In recent years, the Islamic FinancialServices Board (IFSB) has formulated comprehensive prudentialtreatment for sukuk investment by Islamic financial institutions,as stipulated in its capital adequacy standards based on Basel-IIIto ensure market confidence among investors. The new guidelinecan help increase the issuance of sukuk by highly ratedgovernments and companies as well as meet increased demandfor investing in sukuk by Islamic banks trying to meet Basel-IIIliquidity requirements.

3. What can we learn from sukuk literature?

Although the number of research publications on sukuk inthe form of articles, books, conference papers, market reports,and magazines has increased in recent years, the existingresearch on sukuk is relatively sparse. More empirical- orscientific-based literature on sukuk has been published in theform of conference papers and proceedings, but it concentrateslargely on descriptive- or qualitative-based analysis in theform of market reports, popular magazines, blogs, and newspaperarticles. Very little research on sukuk has been published orindexed by major academic publishers (see Table 3). The bulk

of the academic research on sukuk was done in the late 1990sin the form of conference and seminar papers.

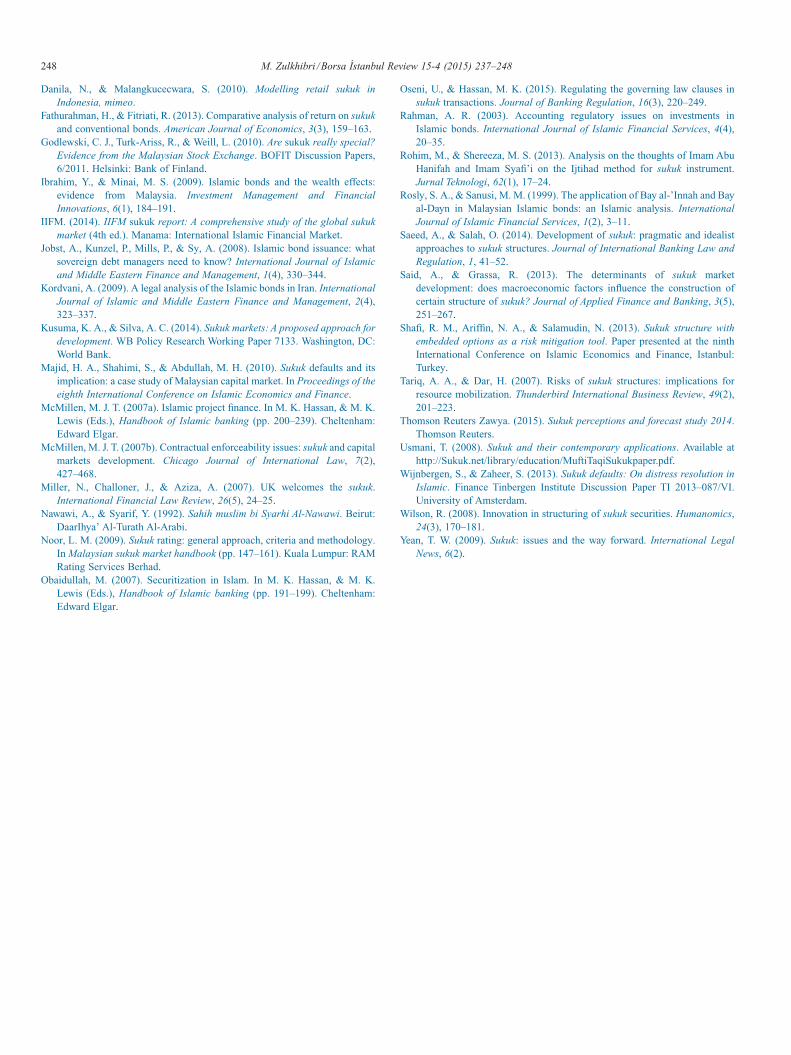

Research on Islamic finance, specifically on sukuk, is under-developed for several reasons, among them the limited numberof academic institutions and a shortage of quality-refereed jour-nals dedicated to the subject, the lack of a global standard andaccreditation for Islamic finance courses, the absence of avail-able and consistent data, and disagreement on the concept ofsukuk among Shari’ah scholars.5 Nevertheless, the existing lit-erature can be divided into at least three main areas of research(see Appendix): (1) research on the theoretical principles andnature of sukuk; (2) discussions on the operational mattersrelated to sukuk issuance and structure in practice; and (3) therole of sukuk in economic development.

3.1. Theoretical nature of sukuk

In the first group of research, the literature revolves aroundthe underlying theoretical and legal nature of sukuk from theperspective of Shari’ah. Debate is still ongoing amongIslamic scholars on the theoretical and legal aspects of sukuk.However, the epistemological formulation of sukuk comesfrom a combination of dalil al-al-naql (revealed knowledge)and dalil al-naqli (man-made knowledge) by using the ijtihad6method. The history of sukuk can be traced back to the era ofthe second caliph, Umar b. al-Khattab (A.D. 634–644). Sellingsukuk was also reported during the caliphate of Marwanb. al-Hakam (A.D. 684–685), which was prohibited afterobjections were raised by some of his companions. However,the term sukuk has actually existed since the time of CaliphMu’awiyah (A.D. 661–680). The literal meaning of sukuk, asan area of study, were formulated by Imam Al-Nawawi (A.D.1234–1277), a jurist from the Shafi’i school of fiqh (Islamicjurisprudence).7

In this regard, Rohim and Shereeza (2013) analyze thethoughts of Imam Shafi’i (A.D. 767–820) and Imam AbuHanifah (A.D. 699–767) on sukuk. The paper argues that theongoing debate among Shari’ah experts can be dividedbetween two main schools of thought: the first rejects sukukand is influenced by the qiyas (analogical) method of ImamShafi’i, which holds that sukuk have the conventionalcharacteristics of risk (gharar) and gambling (maisir); and thesecond accepts sukuk and is influenced by the thought ofImam Abu Hanifah, who contended that sukuk are subject tothe judgment of Islamic law and individual interpretation and

5 Definition of quality journal is based on the widely used journal rankingsand impact ratings, such as the Thompson Reuters Journal Citation Reports(JCR) Impact Factor and the Institute for Scientific Information (ISI) Web ofScience h-index, which reflect the position of a journal within its field, therelative difficulty of being published, and the prestige associated with it.

6 Ijtihad means making effort and endeavor in order to achieve presumption(zann) regarding a hukm (law) of the Shari’ah.

7 During this period, sukuk refers to securities or stock certificates issued bythe national leaders (rulers) to the person entitled to receive food items orobjects, who then they sell these securities or stock certificates before receivingthe goods (Nawawi & Syarif, 1992).

Table 3Publication of sukuk research from 1990 to 2014.

Database or publisher Total no. of journalsa No. of sukuk articlesb

Science Direct 5177 12Scopus Elsevier 5300 31Taylor & Francis 168 1Wiley-Blackwell 53 2Springer 92 0Inderscience 70 2Emerald Insight 84 11

a All journals classified under the subject of economics, finance, accounting,business and management.

b Using keyword “sukuk” or “Islamic Bonds” or “Islamic Securities.”.Source: author’s compilation.

240 M. Zulkhibri /Borsa Istanbul Review 15-4 (2015) 237–248

thus should be evaluating using the ijtihad method.Nevertheless, both schools of thought in essence acceptedsukuk as an Islamic financial instrument.8

Most Shari’ah scholars take the position that trade in debtinstruments (at prices different from their face value) as riba(usury). Distancing sukuk from debt is required in order tomake Islamic finance serve its purpose of enhancing prosperitywith justice and equity. Moreover, according to Usmani (2008),most current practices in sukuk issuance replicate the structureof conventional bonds (lack of ownership, right to a fixedreturn, and the guarantee of repayment of principal). Similarly,Rosly and Sanusi (1999) also criticize the application of BayAl-Innah (sale and buy-back contract) and Bay Al-Dayn (saleof debt contract) for sukuk issuance in Malaysia, which iscontrary to the opinion of the majority of Shafi’i scholars.

Other research argues that sukuk mirror conventional bondsto ensure an equivalent return, but are different in that the returnon sukuk is generated from an underlying asset and not from theobligation to pay interest (Miller, Challoner, & Aziza, 2007).The reason for this is to take into account the distinctive andspecific pricing risk characteristics in Islamic finance, with theaims of simplifying investors’ risk assessment of the newinvestments (Wilson, 2008). Therefore, many financiers takespecial care to make sukuk identical to other conventionalsecurities.

Although the process of issuing sukuk—rating, issuance andredemption procedures, coupon payments, and defaultclauses—are similar to that for conventional bonds, sukuk aredifferent types of instruments from conventional bonds. Thereturns on sukuk (ijarah, musharakah, and mudarabah) aremuch smaller than those for eurobonds. The evidence alsoshows that there is difference in price behavior (Ariff & Safari,2015; Cakir & Raei, 2007). The study suggests that, diversifi-cation by including sukuk in an investment portfolio signifi-cantly reduces the portfolio’s value-at-risk (VaR), compared toa portfolio of only conventional bonds.

There are few studies on the link between the sukuk issuanceannouncements and the stock markets. Most studies used theadverse selection mechanism, which favors the use of sukuk bylower-quality debtor companies to explain the differential reac-tion to stock market announcements. A more recent paper thatinvestigates investors’ reactions to the announcements of issuesof sukuk and conventional bonds shows a significant negativerelationship between an announcement of sukuk and the stockmarket reaction compared to the neutral stock market reactionto an announcement of conventional bonds (Godlewski et al.

2010). The view that differences exist between sukuk and con-ventional bonds is supported in the literature because themarket players are able to differentiate between these two typesof securities.

Other contentious issues related to sukuk are contracts forreselling salam sukuk (contract for deferred delivery) beforetaking possession, which might lead to gharar or riba, guaran-tees for sukuk, and using the London Interbank Offering Rate(LIBOR) as a benchmark in pricing sukuk (Al-Amine, 2008).These practices may not be acceptable for stringent Shari’ahinvestors. Nevertheless, Saeed and Salah (2014) argue that animbalance is created in the sukuk market between an idealisticapproach to sukuk structures and the pragmatic approach thathas been adopted by many sukuk practitioners. It is most likelythat, in practice, a combination of these two approaches will beused to develop the sukuk market.

3.2. Operational aspects of sukuk

The second group of literature focuses on the operationalaspects of sukuk with respect to issuance, risk, and structure.This includes legal and regulatory considerations, performance,and innovation in sukuk. As sukuk are securitized instruments,research in this regard also provides a framework for assessingand managing risk as well as addressing the legal and regula-tory issues involved in sukuk issuance and structure. Theseconsiderations and information form the basis of the research inevaluating the modus operandi of sukuk structures and theunderlying risks.

The literature has also identified legal and regulatorydivergence, which gives higher weight to the costs than thebenefits of sukuk issuance from the investors’ perspective(Jobst et al. 2008). The study points to two importantunresolved issues of legal and regulatory issues areharmonization with Shari’ah and important role inovercoming non-standard laws and regulations. In the samevein, it discusses the need to have a credible standard set forsound Islamic accounting standards, which can be adopted forsukuk issuance. A strong effort to improve and provide anideal accounting standard is necessary for enhancing reliablefinancial statements. This lack of standardization gives rise tolegal challenges to issuing sukuk in non-Islamic jurisdictions.Most of the literature claims that sukuk can benefit variousinternational stakeholders in a new form of investmentcooperation (Abdel-Khaleq & Richardson, 2007). However, inthe case of Iranian Ijara sukuk (leasing contract) issuance,harmonization, and standardization alone do not increase thelevel of efficiency of sukuk markets.

A few studies examine the nature and application of sukukstructuring techniques, with an emphasis on legal considerations(McMillen, 2007b), accounting regulatory issues (Rahman,2003) and governing law clause in a sukuk prospectus (Oseni& Hassan, 2015). The essences of the literature suggest that toensure the benefits of integration of the Islamic financialsphere with the Western financial sphere in a globalizedeconomy, there must be Shari’ah-compliant transactions inpurely secular Western jurisdictions in which the governinglaw recognizes Shari’ah as a matter of substantive and procedural

8 This is because Imam Abu Hanifah relied on the istihsan (juristicpreference) method, while Imam Shafi’i not only used the qiyas (deductiveanalogy) method but also employed the takhsis (exclusion) theory, the resourcelevels of legal sources theory and the language approach theory. However, thesetheories relied on by Imam Shafi’i are all in essence the istihsan theoryaccording to Imam Abu Hanifah. Takhsis (i.e., the specification or qualificationof a general text) could occur by means of rationality and circumstantialevidence (i.e., rationality (aql), custom (urf) and other rational proofs). It wouldfollow from this that takhsis is possible by means of speculative evidence suchas qiyas and solitary Hadith.

241M. Zulkhibri /Borsa Istanbul Review 15-4 (2015) 237–248

law. Enforceability of Shari’ah can be achieved by incorporatingit into the law of the land and then choosing the law of theShari’ah incorporated jurisdiction as the governing law of therelevant transaction. Moreover, investments in sukuk give riseto a number of accounting and reporting issues related toaccounting recognition, measurement, and disclosure. A soundaccounting and reporting standard for Islamic financial instrumentsis the main requirement for a well-regulated Islamic financialmarket that meet the requirements of Shari’ah-compliant andmarket practicality.

Study with regard to sukuk default indicates that most of theproblems that trigger defaults or block smooth resolution ofdistress have arisen from conceptual mismatches between rel-evant jurisdictions, ill-defined property rights, and the choice oflegal structures (Majid et al., 2010; Wijnbergen & Zaheer,2013). In most cases, these problems can be traced to thestructures and clauses that made the sukuk similar to conven-tional bonds. Moreover, sukuk default occurs due to the breachof any binding obligations under the original terms of the agree-ment between the issuer and the sukuk holders. However, sukukdefault may not pose a significant threat to the overall sukukmarket. Therefore, Shari’ah-compatible risk mitigating tech-niques could be developed by embedding options and swapfeatures in sukuk as hedges, such as real estate (Shafi et al.2013; Tariq & Dar, 2007).

The importance of sukuk issuance announcements on share-holder wealth has been studied in the literature (Ahmad &Rahim, 2013; Alam et al. 2013), which points to a mixedpicture. Some studies show that, in the short run, the effect of asukuk announcement on firm value is negative, while otherstudies show a positive effect (Ashhari et al., 2009). The offer-ing size appears to have a negative impact on the cumulativeabnormal return for sukuk and is reported to be significantfactor in that return. A similar line of research demonstrates thatthe market reacts asymmetrically to the issuance of selectedsukuk. The evidence indicates positive, significant, and bothsymmetric and asymmetric market reactions to sukuk issuance.Hence, the capital market reacts positively and asymmetricallyto an announcement of sukuk issuance.

Studies that explore the use of alternative benchmarks forsukuk pricing are gaining momentum because the market failsto address the criticism that sukuk pricing is linked to theLIBOR (Wilson, 2008). Among the proposed alternatives toLIBOR are structuring sukuk securities with innovativestructures based on musharakah or a hybrid of different sukukstructures. Some of the studies suggest that alternativebenchmarks to LIBOR can be adopted and linked based onmacroeconomic indicators of real activity (i.e., GDP growth)for sovereign sukuk and firm performance for corporate sukuk.However, creating financial derivatives for sukuk structures iscontroversial and not always permissible by Shari’ah becausethey are regarded as mere “promises,” rather than real assets.

3.3. Sukuk and economic development

The third group research focuses on the development aspectsof economic sectors by using sukuk as instruments for capital

market development and as an alternative financing tool foreconomic development. This emphasis acknowledges that pro-viding interest-free financial contracts is not the primary aim ofhaving a financial system. In this light, the original expectationsof having a financial system and practices that are truly basedon Islamic principles is to serve the noble goals as prescribed byIslam (Maqasid al-Shari’ah). Sukuk are addressed in this lit-erature as vital vehicles for resource mobilization, whether inthe public or private sector, in particular by international devel-opment and multilateral development banks.

There is much research on the development of economicsectors using sukuk but not too many studies available on therelationship between sukuk and economic growth. However, theempirical studies that have been conducted so far have mainlyexamined the types of sukuk instruments and consumer andinvestor perceptions of sukuk with respect to economic devel-opment. In the short term, sukuk are driven by their owndynamics. The evidence argues that, because sukuk issuanceGranger-causes GDP, policy makers should introduce policiesto modernize the functional aspects of Islamic capital market(Ahmad et al. 2012) to include sukuk. Furthermore, becauseglobal markets in many Muslim countries are largely untapped,sukuk have a competitive advantage for international institu-tional investors.

The link between Islamic finance and corporate finance isalways an interesting topic in sukuk literature. Most studiespoint to the fact that investors react positively toannouncement of Islamic debt issuances (Ibrahim & Minai,2009). These findings are attributed to a larger investor basefor Islamic debt securities relative to that of conventionaldebt, which creates cost advantages, lowering the cost ofcapital. The literature also sees an important role for thegovernment to support the development of sukuk market andto find alternative financing for economic development.Specifically, the role for governments in Muslim countriesregarding financing the budget by mobilizing resource usingdomestic sukuk. However, exposure to exchange ratesincreases the risks for sovereign issuers of sukuk, particularlythose denominated in nondomestic currency.

Said and Grassa (2013) investigate similar issues on thedeterminants of sukuk market development in ten countries.The results show macroeconomic factors—GDP per capita,Muslim population, economic size, and trade openness as wellas regulatory quality—have a positive impact on the develop-ment of a sukuk market. However, the amount of sukuk issuedhas declined considerably in recent years, and the financialcrisis has negatively affected the development of the sukukmarket. At the same time, conventional bond markets contributepositively to the development of the sukuk market. It appearsthat the conventional bond market and the sukuk market arecomplements rather than substitutes.

4. Conclusion

The sukuk market has grown a great deal, but significantgaps remain. It faces constraints due to a lack of standardiza-tion, concerns over investor protection, and low liquidity

242 M. Zulkhibri /Borsa Istanbul Review 15-4 (2015) 237–248

mainly due to fragmentation. A holistic approach is needed tofacilitate the development of domestic markets and access tointernational markets. The development of money markets isimportant for a more active sukuk market. A standard solutionfor the design of suitable money market instruments in thesukuk market is still a work in progress, and the same applies toderivative products. Similarly, rating is a major challenge forpotential issuers in accessing the international markets, but abroad set of credit enhancement solutions is almost nonexistent.

Compared to the literature on conventional bonds, the existingresearch on sukuk is relatively thin, largely consisting of qualita-tive rather than quantitative work in the form of market reports,articles in popular magazine, blogs, and conference papers. Veryfew research papers on sukuk are published in top scientificacademic journals with impact factors. The underdeveloped lit-erature on sukuk, especially in the scholarly empirical research,can be attributed mainly to a lack of available historical, consis-tent, and reliable data as well as the limited number of Islamicjournals and funding for Islamic finance research.

The bulk of the literature focuses on operational matters ofsukuk issuance and structure in practice, which revolve around

their need to be Shari’ah-compliant. Limited literature hasundertaken study on capital markets and corporate financialaspects of sukuk, followed by their theoretical nature, and veryfew studies examine the implications of sukuk for the realeconomy. New research should provide a new theoreticalframework on sukuk and for sukuk practices that do not merelyreplicate and modify existing practices and label them asIslamic products.

As the acceptance and growth of sukuk continue, research onsukuk should be pushed further into mainstream economics andfinance. Collective efforts by Islamic finance experts, educa-tors, and trainers are greatly needed to expand the currentunderstanding of sukuk. Research should also explore variouspossibilities of using scientific approaches for understandingsukuk behavior as well as ways of structuring more innovativesukuk. In addition, more research on sukuk is needed to identifyfactors affecting sukuk pricing and performance of varioussukuk structures, differentiate between risk-sharing and risk-shifting approaches for sukuk, and understanding the impact ofsukuk on market functioning with respect to economic devel-opment and social welfare.

Appendix.

Table 4Summary of related literature on sukuk.

Author(s) Type of research Objectives Methodology Findings

Rohim and Shereeza (2013) Nature of sukuk; Qualitative Analyze the thought of ImamAbu Hanifah and ImamShafi’i on sukuk instruments.

Descriptive analysis. The study finds that bothschools of thought in essenceaccepted sukuk as an Islamicfinancial instrument

Usmani (2008) Nature of sukuk; Qualitative Analyze the mechanisms ofsukuk and on the extent towhich these comply with theprecepts and principles ofIslamic jurisprudence.

Descriptive analysis. The study proposes that sukukbe issued for new commercialand industrial ventures. Thereturns of enterprises shouldbe returned to sukuk holdersregardless of the amount aftercosts.

Rosly and Sanusi (1999) Nature of sukuk; Qualitative Analyze pertinent issues onthe creation of Islamic bondsin Malaysia and analyze theunderlying reasons behindthe rejection of bay’ al-in hand bay’ al dayn.

Descriptive analysis. The study finds no significantShari’ah justification of bay’al-inah. While the trading ofIslamic bonds at a discountusing bay’ al-dayn has beenfound unacceptable by themajority of ulema’ (JumhurUlama’) including al-Shafi’i.

Cakir and Raei (2007) Nature of sukuk; Quantitative Analyze the differencebetween sukuk andeurobonds for the sameissuer. This paper assessesthe impact of bonds issuedaccording to Islamicprinciples (sukuk), on thecost and risk structure ofinvestment portfolios.

Value-at-risk (VaR) methodbased on delta-normalmethod and Monte Carlosimulation method.

This paper shows that sukuk– contrary to earlier literature– are different types ofinstruments from conventionalbonds, as evidenced by theirdifferent price behavior. Theanalysis employing thedelta-normal as well asMonte-Carlo simulationmethods implies such gainsare present and in certaincases very significant.

(continued on next page)

243M. Zulkhibri /Borsa Istanbul Review 15-4 (2015) 237–248

Table 4 (continued)

Author(s) Type of research Objectives Methodology Findings

Godlewski, Turk-Ariss, andWeill (2010)

Nature of sukuk; Quantitative Examine whetherannouncements of sukuk andconventional bond issueslead to significant abnormalreturns for the issuers forMalaysian listed companies,which issued conventionalbonds and sukuk.

A standard market model toestimate abnormal returnsaround the event date for asecurity issue

The study finds the absenceof significant stock marketreaction to conventionalbond announcements,negative reaction to sukukissues and, as a corollary, asignificant differencebetween stock marketreactions to sukuk andconventional bond issues.

Ariff and Safari (2015) Nature of sukuk; Quantitative Examine whether sukukinstruments are equivalent toconventional bonds aspracticed by the market.

Statistical and causality testsusing a large traded data seton sukuk and conventionalbonds.

The results suggest thatsukuk instruments are pricedsignificantly differently andthat their yields are notGranger-caused byconventional security yieldsor vice versa. This empiricalfinding does not support themarket’s current practicesbased on the assumption thatsukuk are like normal bonds.

Jobst, Kunzel, Mills, and Sy(2008)

Operational aspects of sukuk;Qualitative

Review the current state ofthe sukuk market, examinespertinent legal and economicimplications of Shari’ahcompliance on theconfiguration of sukukissuance, and informs thedebate about the prospects ofsukuk issuance by sovereignissuers

Descriptive analysis. The study suggests thatadministrative considerationscan lead to additional costswhile limiting fiscalflexibility. The initialstructuring and issuancecosts of sukuk are likely tobe higher than they are for astandard security. Sovereignissuers’ revenues may needto be ring-fenced, effectivelylimiting fiscal flexibility.Non-Islamic sovereigns, inparticular, would need toconsider the necessaryorganizational changesneeded to administer theShari’ah-compliant structure.

Kordvani (2009) Operational aspects of sukuk;Qualitative

Examines the key elementsof sukuk within the contextof the Shi’a fiqh(jurisprudence) and theprinciples of contract law inIran, which is basedprimarily on the Shi’a fiqh.

Descriptive analysis. An examination of Shi’ajurisprudence on the contractof ijarah (leasing contract)shows that such anadjustment can beaccomplished in Iran. It hasbeen shown how obstacles tothe legitimacy oflease-to-purchase agreementshave been overturned byrelying on a more flexibleinterpretation of contractualconditions.

(continued on next page)

244 M. Zulkhibri /Borsa Istanbul Review 15-4 (2015) 237–248

Table 4 (continued)

Author(s) Type of research Objectives Methodology Findings

Rahman (2003) Operational aspects of sukuk;Qualitative

Examines contemporaryaccounting regulatory issueson Islamic bonds or Islamicprivate debt securities (IPDS)or sukuk. Investments inIslamic bonds (sukuk) giverise to a number ofaccounting and reportingissues.

Descriptive analysis. The study suggests that aproper development of theIslamic financial marketrequires a well-regulatedIslamic financial instrumentthat is in accordance withIslamic accountingregulations. It requires asound accounting andreporting standard forIslamic financial instrumentsthat meet the requirements ofShari’ah and can bepracticed.

Fathurahman and Fitriati(2013)

Operational aspects of sukuk;Quantitative

Analyze the ratio betweenyields on sukuk andconventional bonds usingmodel calculations yield tomaturity and portfoliooptimization model

Basic statistical tests forsukuk and conventionalbonds in Indonesia.

The paper concludes that themean yield to maturity ofsukuk is greater than themean yield of conventionalbonds. In term risks, sukukstandard deviation isrelatively larger than thestandard deviation ofconventional bonds.

Wijnbergen and Zaheer(2013)

Operational aspects of sukuk;Quantitative

Examine the resolutionprocess following default,not the reasons the defaultwas triggered and the recentsukuk (near) defaults from anIslamic finance perspective.

Case studies of four sukukdefaults.

These case studies makeclear that most of theproblems that triggereddefaults or blocked smoothresolution of distressafterward arose fromill-defined property rightsand conceptual mismatchesbetween relevantjurisdictions and the legalstructures chosen. In mostcases, the problems can betraced back to clauses andstructures that made thesukuk more like conventionalbonds.

Tariq and Dar (2007) Operational aspects of sukuk;Qualitative

Assess the sukuk structuresand analyze the various risksunderlying the Islamicsovereign and corporatesukuk structures.

Descriptive analysis. The study highlights thatdifferent Shari’ahperceptions could be a risk,which may affect sukukpricing. Furthermore,through Shari’ah-compatiblefinancial engineering, sukukcan also become highlycompetitive in the marketand accessible to the publicas an investment opportunity.

Shafi, Ariffin, andSalamudin (2013)

Operational aspects of sukuk;Qualitative

Identify strategies to reducesukuk risk, propose sukukmodel with embedded optionand a mathematical model tocompute returns beforeconversion

Descriptive analysis. The study suggests theapplication of sukuk withembedded options as tomitigate the risk faced bysukuk holders. Embeddedoptions are a way to mitigatethe risk, so the studyproposes using a real asset,such as real estate.

(continued on next page)

245M. Zulkhibri /Borsa Istanbul Review 15-4 (2015) 237–248

Table 4 (continued)

Author(s) Type of research Objectives Methodology Findings

Wilson (2008) Operational aspects of sukuk;Qualitative

Examines the market for, andusage of, sukuk, notably astools for liquiditymanagement. There is alsoan analysis of different sukukstructures from a financialperspective.

Descriptive analysis. The study proposes sukukbased on participatorystructures, with risk sharingby investors, as a wayforward. The risk with theseproposed structures is ofvariable returns rather thanof default, which may wellbe more acceptable toinformed investors in anycase.

Alam, Hassan, and Haque(2013)

Operational aspects of sukuk;Quantitative

Examines the impact ofsukuk and conventionalbonds announcement onshareholder wealth and theirdeterminants using 79 sukukand 87 conventional bondsover the period of2004–2012 in six developedIslamic financial market.

Event study methodology tocalculate the abnormalreturns of sukuk orconventional bond issuanceand a multivariateregression.

The study shows that from ashort-run perspective, theeffect of announcement ofsukuk on firm value isnegative, while the effect ofannouncement ofconventional bond is positivefor all periods except for thepost-crisis period. Therefore,in spite of having a religiousmotivation to issue sukuk,the negative effect mighthinder firms in raising fundsfor sukuk.

Ashhari, Chun, and Nassir(2009)

Operational aspects of sukuk;Quantitative

Study the impact of Islamicbond and conventional bondsannouncement onshareholder wealth for firmslisted on the Bursa Malaysia(stock market) for the period2001 to 2006.

A standard event studymethodology with betarefinement using Blume’smethod.

The study finds that thereis a wealth effect on sukukissues announcement butnot for conventional bondannouncement. The studyfurther establishes thatthe size of the bondoffering is a significantfactor in stock returns forboth sukuk and conventionalbonds, but the sign forsukuk was negative andcontrary to that forconventional bonds.

Ahmad and Rahim (2013) Operational aspects of sukuk;Quantitative

Investigate whether themarket reacts asymmetricallyto the issuance of selectedsukuk structures (ijarah andmusharakah) in Malaysia.

Event study methodologyusing cumulative averageabnormal return onsymmetric and asymmetricevents.

The results support thehypothesis of positive marketreaction on FTSE KLCIindex after ijarah andmusharakah issuance inMalaysia. The positivemarket reactions can beinterpreted in two ways.First, the market can readilydistinguish the news.Second, there are confidenceeffects that shareholderswealth will be increasedthrough the issuance of ijaraand musharakah sukuk.

Majid, Shahimi, andAbdullah (2010)

Operational aspects of sukuk;Qualitative

Discuss the sukuk defaults inMalaysia and its implicationson the Malaysian capitalmarket with special referenceto the selected Malaysiandefaulted sukuk.

Descriptive analysis The study indicates thatsukuk default in Malaysiamay not pose a significantthreat to the local capitalmarket. However, it doeshave an impact on theoverall reputation ofMalaysia as the hub forglobal Islamic finance.

(continued on next page)

246 M. Zulkhibri /Borsa Istanbul Review 15-4 (2015) 237–248

References

Abdel-Khaleq, A., & Richardson, C. (2007). New horizons for Islamicsecurities: emerging trends in sukuk offerings. Chicago Journal ofInternational Law, 7(2), 409–425.

Ahmad, N., Daud, S. N., & Kefelia, Z. (2012). Economic forces and the sukukmarket. Procedia: Social and Behavioral Sciences, 65, 127–133.

Ahmad, N., & Rahim, A. S. (2013). Sukuk ijarah vs. sukuk musyarakah:investigating post-crisis stock market reactions. International Journal ofHumanities and Management Sciences, 1(1), 87–91.

Al-Amine, M. A. (2008). Sukuk market: innovations and challenges. IslamicEconomic Studies, 15(2), 1–22.

Al-Jarhi, M. A. (2013). Gaps in the theory and practice of Islamic economics.JKAU: Islamic Economics, 26(1), 243–254.

Alam, N., Hassan, M. K., & Haque, M. A. (2013). Are Islamic bonds differentfrom conventional bonds? International evidence from capital market tests.Borsa Istanbul Review, 13(3), 22–29.

Ariff, M., & Safari, M. (2015). Valuation of Islamic debt instruments, thesukuk: Lessons for market development. In H. A. El-Karanshawy, A. Omar,T. Khan, S. S. Ali, H. Izhar, & W. Tariq, et al. (Eds.), Islamic banking andfinance – Essays on corporate finance, efficiency and product development.Doha, Qatar: Bloomsbury Qatar Foundation.

Ashhari, Z. M., Chun, L. S., & Nassir, A. M. (2009). Conventional vs. Islamicbond announcements: the effects on shareholders’ wealth. InternationalJournal of Business and Management, 4(6), 105–111.

Cakir, S., & Raei, F. (2007). Sukuk vs. Eurobonds: Is there a difference invalue-at-risk?. IMF Working Paper, No. WP/07/237. Washington, DC:International Monetary Fund.

Table 4 (continued)

Author(s) Type of research Objectives Methodology Findings

Ibrahim and Minai (2009) Sukuk and economicdevelopment

Examine the wealth effect ofIslamic debt issuance and itsdeterminants.

Event study analysis andcross-sectional regression

The study finds thatinvestors reacted positivelyto the announcement ofIslamic debt issues, whilethey are indifferent to theannouncement ofconventional issues.

Danila andMalangkucecwara (2010)

Sukuk and economicdevelopment

Examine factors that affectretail sukuk investment byindividual investors.

Descriptive analysis The study supports theimportant role of Muslimgovernments in financing thebudget through domesticsukuk issuance, but not to beexposed to exchange raterisks related to sukukdenominated in nondomesticcurrency. The result alsosuggests that the rate ofreturn (mudarabah deposit)and foreign exchange ratehave an impact on sukukprice.

Ahmad, Daud, and Kefelia(2012)

Sukuk and EconomicDevelopment; Quantitative

Examine macroeconomicinfluences on sukuk issuancein Malaysia based onaggregate level data

Vector autoregressive model(VAR)

The findings indicate that thecausality runs from sukuk toGDP. In the short-horizon,sukuk is driven by its owndynamics. The study arguesthat since sukuk issuanceGranger-causes GDP, policymakers should introducepolicies to modernize thefunctional aspects of Islamiccapital market.

Said and Grassa (2013) Sukuk and economicdevelopment; Quantitative

Investigate the influence ofthe macroeconomic factorsthe construction of a certainstructure of sukuk in themost sukuk issuers’ countriesnamely: Saudi Arabia,Kuwait, UAE, Bahrain,Qatar, Indonesia, Malaysia,Brunei, Pakistan, andGambia.

Multivariate regression The results show thatmacroeconomicfactors—GDP per capita,Muslim population,economic size and tradeopenness as well asregulatory quality—have apositive impact on thedevelopmentof sukuk market. However,since the amount of sukukissued has declinedconsiderably in recentyears, the financial crisishas affected negatively thedevelopment of sukukmarket.

247M. Zulkhibri /Borsa Istanbul Review 15-4 (2015) 237–248

Danila, N., & Malangkucecwara, S. (2010). Modelling retail sukuk inIndonesia, mimeo.

Fathurahman, H., & Fitriati, R. (2013). Comparative analysis of return on sukukand conventional bonds. American Journal of Economics, 3(3), 159–163.

Godlewski, C. J., Turk-Ariss, R., & Weill, L. (2010). Are sukuk really special?Evidence from the Malaysian Stock Exchange. BOFIT Discussion Papers,6/2011. Helsinki: Bank of Finland.

Ibrahim, Y., & Minai, M. S. (2009). Islamic bonds and the wealth effects:evidence from Malaysia. Investment Management and FinancialInnovations, 6(1), 184–191.

IIFM. (2014). IIFM sukuk report: A comprehensive study of the global sukukmarket (4th ed.). Manama: International Islamic Financial Market.

Jobst, A., Kunzel, P., Mills, P., & Sy, A. (2008). Islamic bond issuance: whatsovereign debt managers need to know? International Journal of Islamicand Middle Eastern Finance and Management, 1(4), 330–344.

Kordvani, A. (2009). A legal analysis of the Islamic bonds in Iran. InternationalJournal of Islamic and Middle Eastern Finance and Management, 2(4),323–337.

Kusuma, K. A., & Silva, A. C. (2014). Sukuk markets: A proposed approach fordevelopment. WB Policy Research Working Paper 7133. Washington, DC:World Bank.

Majid, H. A., Shahimi, S., & Abdullah, M. H. (2010). Sukuk defaults and itsimplication: a case study of Malaysian capital market. In Proceedings of theeighth International Conference on Islamic Economics and Finance.

McMillen, M. J. T. (2007a). Islamic project finance. In M. K. Hassan, & M. K.Lewis (Eds.), Handbook of Islamic banking (pp. 200–239). Cheltenham:Edward Elgar.

McMillen, M. J. T. (2007b). Contractual enforceability issues: sukuk and capitalmarkets development. Chicago Journal of International Law, 7(2),427–468.

Miller, N., Challoner, J., & Aziza, A. (2007). UK welcomes the sukuk.International Financial Law Review, 26(5), 24–25.

Nawawi, A., & Syarif, Y. (1992). Sahih muslim bi Syarhi Al-Nawawi. Beirut:DaarIhya’ Al-Turath Al-Arabi.

Noor, L. M. (2009). Sukuk rating: general approach, criteria and methodology.In Malaysian sukuk market handbook (pp. 147–161). Kuala Lumpur: RAMRating Services Berhad.

Obaidullah, M. (2007). Securitization in Islam. In M. K. Hassan, & M. K.Lewis (Eds.), Handbook of Islamic banking (pp. 191–199). Cheltenham:Edward Elgar.

Oseni, U., & Hassan, M. K. (2015). Regulating the governing law clauses insukuk transactions. Journal of Banking Regulation, 16(3), 220–249.

Rahman, A. R. (2003). Accounting regulatory issues on investments inIslamic bonds. International Journal of Islamic Financial Services, 4(4),20–35.

Rohim, M., & Shereeza, M. S. (2013). Analysis on the thoughts of Imam AbuHanifah and Imam Syafi’i on the Ijtihad method for sukuk instrument.Jurnal Teknologi, 62(1), 17–24.

Rosly, S. A., & Sanusi, M. M. (1999). The application of Bay al-’Innah and Bayal-Dayn in Malaysian Islamic bonds: an Islamic analysis. InternationalJournal of Islamic Financial Services, 1(2), 3–11.

Saeed, A., & Salah, O. (2014). Development of sukuk: pragmatic and idealistapproaches to sukuk structures. Journal of International Banking Law andRegulation, 1, 41–52.

Said, A., & Grassa, R. (2013). The determinants of sukuk marketdevelopment: does macroeconomic factors influence the construction ofcertain structure of sukuk? Journal of Applied Finance and Banking, 3(5),251–267.

Shafi, R. M., Ariffin, N. A., & Salamudin, N. (2013). Sukuk structure withembedded options as a risk mitigation tool. Paper presented at the ninthInternational Conference on Islamic Economics and Finance, Istanbul:Turkey.

Tariq, A. A., & Dar, H. (2007). Risks of sukuk structures: implications forresource mobilization. Thunderbird International Business Review, 49(2),201–223.

Thomson Reuters Zawya. (2015). Sukuk perceptions and forecast study 2014.Thomson Reuters.

Usmani, T. (2008). Sukuk and their contemporary applications. Available athttp://Sukuk.net/library/education/MuftiTaqiSukukpaper.pdf.

Wijnbergen, S., & Zaheer, S. (2013). Sukuk defaults: On distress resolution inIslamic. Finance Tinbergen Institute Discussion Paper TI 2013–087/VI.University of Amsterdam.

Wilson, R. (2008). Innovation in structuring of sukuk securities. Humanomics,24(3), 170–181.

Yean, T. W. (2009). Sukuk: issues and the way forward. International LegalNews, 6(2).

248 M. Zulkhibri /Borsa Istanbul Review 15-4 (2015) 237–248