a study of consumers’ perception and key factors in

TRANSCRIPT

A STUDY OF CONSUMERS’ PERCEPTION AND KEY

FACTORS IN DECISION-MAKING TOWARD

ELECTRIC CARS IN

BANGKOK METROPOLITAN REGION

BY

MR. VOTSAWAT CHAICHITTI

AN INDEPENDENT STUDY SUBMITTED IN PARTIAL

FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE

OF MASTER OF SCIENCE PROGRAM IN MARKETING

(INTERNATIONAL PROGRAM)

FACULTY OF COMMERCE AND ACCOUNTANCY

THAMMASAT UNIVERSITY

ACADEMIC YEAR 2018

COPYRIGHT OF THAMMASAT UNIVERSITY

Ref. code: 25616002040845PKB

A STUDY OF CONSUMERS’ PERCEPTION AND KEY

FACTORS IN DECISION-MAKING TOWARD

ELECTRIC CARS IN

BANGKOK METROPOLITAN REGION

BY

MR. VOTSAWAT CHAICHITTI

AN INDEPENDENT STUDY SUBMITTED IN PARTIAL

FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE

OF MASTER OF SCIENCE PROGRAM IN MARKETING

(INTERNATIONAL PROGRAM)

FACULTY OF COMMERCE AND ACCOUNTANCY

THAMMASAT UNIVERSITY

ACADEMIC YEAR 2018

COPYRIGHT OF THAMMASAT UNIVERSITY

Ref. code: 25616002040845PKB

(1)

ABSTRACT

The automotive industry has had an important role in Thailand’s economy for

many years. In 2017, this industry contributed nearly 12% of the country’s GDP with

up to two million vehicles being produced (OICA, 2017), As a consequence, this has

made the country be ranked as the number one largest automotive producer in

Southeast Asia, fifth in Asia, and 12th in the world. In fact, the global automotive

industry has been moving toward zero carbon transport by reducing pollutant

emissions in the world. Therefore, the electric car revolution has become an attractive

investment market in recent years. However, building a domestic market for electric

cars is still a challenge and will likely take years to penetrate the Thai market due to a

variety of obstacles.

This study is a contemporary topic in applied marketing that focuses on the

subject area of the technological issue of electric cars in Thailand.

The purpose of this study aimed to understand the need for electric cars in the

Thai consumers’ mind focusing on the potential customers based on individual

characteristics, and the key driven factors that impact on purchasing electric cars. The

study was conducted using exploratory research and descriptive research. The

Independent Study Title A STUDY OF CONSUMERS’ PERCEPTION

AND KEY FACTORS IN DECISION-MAKING

TOWARD ELECTRIC CARS IN BANGKOK

METROPOLITAN REGION

Author Mr. Votsawat Chaichitti

Degree Master of Science Program in Marketing

(International Program)

Major Field/Faculty/University Faculty of Commerce and Accountancy

Thammasat University

Independent Study Advisor Professor K. Douglas Hoffman, Ph.D.

Academic Years 2018

Ref. code: 25616002040845PKB

(2)

exploratory research consisted of secondary research and in-depth interviews of four

respondents. The descriptive research was conducted using an online questionnaire

with 160 respondents. All the target respondents were Thai people aged 25-49 years

who lived in the Bangkok Metropolitan Region. The data acquired from the

questionnaire results were analyzed using the Statistical Package for the Social

Sciences (SPSS) in order to provide the result findings for each research objective.

As a result of the study, the respondents were grouped into three segments

based on attitude and lifestyle: 1) High-end Tech Savvy Consumers, 2) Eco-conscious

Consumers, and 3) Independent Quality-oriented Consumers. Furthermore, the key

important factors that significantly had an impact on the purchasing decision were the

Reliability of the technology, Design, Lower tax on EVs, and Charging stations

coverage in major cities.

Therefore, the findings would be beneficial for businesses or related

parties that are involved in the electric vehicle (EV) industry from the government,

public or private charging infrastructure, and auto manufacturers. This would be in

preparation for attracting early adopters of the brand new technology of EVs in

Thailand.

Keywords: Electric Cars, EVs, Automotive Industry

Ref. code: 25616002040845PKB

(3)

ACKNOWLEDGEMENTS

First of all, I would like to express my appreciation and gratitude to my

advisor, Professor K. Douglas Hoffman, for his support and guidance throughout the

entire independent study. His knowledge, dedication and positive attitude always

guided me along the way from emails to personal meetings.

I would also like to express my appreciation to all respondents who spent their

time and effort on the interviews and online survey. Lastly, I would like to thank all

my friends, colleagues, and, especially my family for their continuous support and

encouragement throughout my master’s degree journey.

Mr. Votsawat Chaichitti

Ref. code: 25616002040845PKB

(4)

TABLE OF CONTENTS

Page

ABSTRACT (1)

ACKNOWLEDGEMENTS (3)

LIST OF TABLES (7)

LIST OF FIGURES (8)

CHAPTER 1 INTRODUCTION 1

1.1 Background 1

1.1.1 Thailand Market Situation 2

1.2 Research Purpose 5

1.3 Research Objectives 5

CHAPTER 2 REVIEW OF LITERATURE 6

2.1 Electric Vehicles 6

2.2 Global Electric Vehicle Overview 7

2.3 Thailand’s Current Market Situation 7

2.4 Thailand’s Market Segment Situation 7

2.5 Thailand’s Market Research Situation 8

2.6 Summary of Literature Review 9

CHAPTER 3 RESEARCH METHODOLOGY 10

3.1 Exploratory Research Design 10

Ref. code: 25616002040845PKB

(5)

3.1.1 Secondary Research 10

3.1.2 In-depth Interview 11

3.2 Descriptive Research 11

3.2.1 Online Questionnaire 11

3.3 Sampling Plan 12

3.4 Recruitment Plan 12

3.4.1 Recruitment Criteria 12

3.4.2 Recruitment Method 13

3.5 Identification of Key Research Variables 13

3.6 Data Analysis Plan 14

CHAPTER 4 RESULTS AND DISCUSSION 15

4.1 Key Findings from the In-depth Interviews 15

4.1.1 In-depth Analysis 15

4.1.2 Preferences for Purchasing a Car 15

4.1.3 Consumers Knowledge about an Electric Car 16

4.1.4 Key Factors in Changing to an Electric Car 16

4.2 Key Findings from the Questionnaire Survey 17

4.2.1 Respondents’ Demographics 17

4.2.2 Consumer Segments by Attitude and Lifestyle 17

4.2.3 Consumers’ Perception toward Electric Cars 21

4.2.4 Electric Cars’ Attributes that Impact the Purchasing Decision 22

4.2.5 External Purchasing Factors on Electric Cars 24

4.2.6 Impact between Consumers’ Attitudes and the Purchasing

Factors 26

4.2.6.1 Impact of Electric Cars’ Attributes 26

4.2.6.2 Impact of External Purchasing Factors 27

Ref. code: 25616002040845PKB

(6)

4.2.7 Consumers’ Attitudes toward the Intention to Find More

Information on Electric Cars 28

4.2.8 Consumers’ Attitudes toward the Intention to Purchase Electric

Cars in the Future 29

4.2.9 Consumers’ Willingness to Pay 30

CHAPTER 5 CONCLUSIONS AND RECOMMENDATIONS 31

5.1 Key Findings from the Questionnaire Survey 31

5.1.1 Thai Consumers’ Perception toward Electric Cars 31

5.1.2 Key Electric Cars’ Attributes toward the Purchasing Decision 31

5.1.3 External Purchasing Factors on Electrics Cars 32

5.1.4 Thai Consumer Segments 32

5.1.5 Thai Consumers’ Intention to Purchase Electrics Cars 32

5.2 Recommendations 33

5.2.1 The Most Desired Segments 33

5.2.2 Focus on the Early Adopter Segments 33

5.2.3 Key Factors in Purchasing Electric Cars 34

5.3 Research Limitations 34

5.4 Suggestions for Future Research 35

REFERENCES 36

APPENDICES

APPENDIX A: In-depth Interviews Questions 39

APPENDIX B: Online Questionnaire Questions 40

APPENDIX C: Respondents’ Demographic Data 45

BIOGRAPHY 47

Ref. code: 25616002040845PKB

(7)

LIST OF TABLES

Tables Page

3.1: Participants collection 12

4.1: Finding key factors using the factor analysis 18

4.2: Segments from the cluster analysis 19

4.3: Consumers’ perception toward electric cars by segments 22

4.4: Importance of electric cars’ attributes toward the purchasing

decision by segments 23

4.5: Comparison of electric cars’ attributes between segments 24

4.6: Importance of external purchasing factors by segments 25

4.7: Comparison of the external purchasing factors between segments 26

4.8: Regression analysis between consumers’ attitudes and seven

electric cars’ attributes that had an impact on the purchasing decision 27

4.9: Regression analysis between consumers’ attitudes and seven external

factors that had an impact on purchasing electric cars 28

4.10: Consumers’ intention to seek more information by segments 29

4.11: Consumers’ intention to purchase electric cars by segments 29

4.12: Willingness to pay for an electric car by segments 30

Ref. code: 25616002040845PKB

(8)

LIST OF FIGURES

Figures Page

1.1: World vehicle production in 2017 2

1.2: World vehicle sales in 2017 3

1.3: Eighteen auto assemblers in Thailand 4

2.1: Age distribution of likely electric vehicle buyers 8

3.1: Research process 10

3.2: Conceptual model 13

3.3: Data analysis plan for the quantitative data 14

4.1: Association between the characteristics in each segment 20

Ref. code: 25616002040845PKB

1

CHAPTER 1

INTRODUCTION

1.1 Background

The global automotive industry is rapidly changing; consequently, the electric

car revolution has become an attractive investment market in recent years, as many

believe it will transform the future of transportation. However, the world is still in the

early stages of the adoption of electric vehicles (EVs) making up less than 1% of new

car sales globally. Currently, the factors on the supply side are accelerating electric

vehicle development, which includes government support on taxes, incentives as well

as regulations on pollutant emissions that are also pushing car manufacturers to invest

in research and development (R&D), particularly in the top three EVs’ markets of

China, Europe, and the US (Yun, 2018).

EVs are slowly gaining a reputation in the automotive industry, offering low

or zero carbon transport that many people say will eventually dominate our roads in a

few years. Globally, EVs are on the rise with the market reaching 1.2 million sales in

2017, 57% higher than in 2016. China is leading the market with a 48% market share

that accounts for 580,000 unit sales followed by Europe with 26%, and North

America with 18% (Frost and Sullivan, 2018). The latest forecast expects sales of

EVs to increase to 11 million in 2025, and 30 million in 2030 (Bloomberg NEF,

2018). By 2040, 60 million EVs are projected to be sold, equivalent to 55% of the

global passenger car market.

Due to the rise of technology from EVs and environmental policies, many

developed countries are preparing themselves to adopt this future change that soon

will become a norm in the automotive market. On the other hand, in Thailand, electric

cars were launched for the first time in 2009, in the form of hybrid electric vehicles

(HEVs). Moreover, plug-in hybrid electric vehicles (PHEVs) have been assembled

locally in Thailand by luxury brands; such as, Mercedes-Benz and BMW since 2016

(Panyaarvudh, 2018). Nonetheless, the overall market penetration of EVs is still

limited. This is because the market has mainly focused on high-end customers as the

Ref. code: 25616002040845PKB

2

early adopter of this new technology due to the relatively higher price compared to

internal combustion engine (ICE) vehicles.

According to the Department of Land Transport report (2017), EVs comprise

less than 1% of the total number of passenger cars in Thailand. At present, the

majority of them are HEVs and PHEVs (more than 100,000 units), but the number of

total EVs is quite small, which is approximately more than 1,000 units on the road.

Overall, Thai consumers are now more comfortable with HEVs and PHEVs, which

still have an ICE using petrol along with large batteries while the adoption of total

EVs, which have no such engines, is still in the very early stage due to the lack of

public charging infrastructure. Additionally, the price of EVs is nearly US$61,000 due

to the high import duties while locally assembled models are not yet available

(Wijayasinha, 2018).

1.1.1 Thailand Market Situation

Thailand’s automotive industry has had an important role in the

country’s economy for many years. The industry contributed nearly 12% of

Thailand’s GDP with more than 1.98 million vehicles produced in 2017 (OICA,

2017). This success ranked the country as the number one largest automotive

producer in Southeast Asia, fifth in Asia, and 12th in the world (refer to Figure 1). By

2020, Thailand expects to increase its production to 3.5 million units of vehicles, or

an 80% rise from 2017.

(Source: International Organization of Motor Vehicle Manufacturers, 2017.)

Figure 1.1: World vehicle production in 2017

Ref. code: 25616002040845PKB

3

The country has a well-known reputation by all the world’s leading

automakers and assemblers that are located in Central Thailand. Global companies;

such as, Toyota, Isuzu, Honda, Mitsubishi, Nissan, BMW and others together account

for a share of nearly two million vehicles produced yearly (Helven, 2018; Rastogi,

2018). More than half of the total production is commercial vehicles (58%) with the

remainder comprising passenger cars (42%) (OICA, 2017). Thailand’s automotive

industry is almost 60% export-oriented. In recent years, the country exported over 1.1

million vehicles to ASEAN countries, Australia, the Middle East and Europe, which

generated more than US$18 billion for the country (Thailand Board of Investment,

2017).

In terms of unit sales for the domestic market, Thailand ranked second in

Southeast Asia, sixth in Asia and 20th in the world, which was over 0.8 million-unit

sales in 2017 (refer to Figure 2). This accounted for 46% of the total number of

vehicles distributed to the local market, which comprised 34% of passenger cars with

1,500 cc or smaller engines, including eco-cars, and 12% with 1,501 cc or larger

engines. With a total of 18 auto assemblers in Thailand (refer to Figure 3), this would

help ensure that Thailand’s economy would grow even stronger. The forecast for the

automotive sector will likely increase in both the domestic and export markets, by 5-

7%, and 3-5%, respectively (Yongpisanphob, 2018).

(Source: International Organization of Motor Vehicle Manufacturers, 2017.)

Figure 1.2: World vehicle sales in 2017

Ref. code: 25616002040845PKB

4

(Source: Thailand Board of Investment, 2017.)

Figure 1.3: Eighteen auto assemblers in Thailand

On the other hand, despite the high potential automotive market in Thailand,

the number of electric vehicle sales has remained rather small. According to the

consulting firm KPMG (2018), it has been forecast that electric vehicle sales in

Thailand would remain low in the near future, and comprise only 1% of all passenger

vehicles in the country. With the global trend, EVs are expected to gain up to 35% of

the total number of vehicles worldwide in 2040 (Bloomberg NEF, 2018). This is

because of the concern for improving air quality throughout many countries, as well

as reducing emission-driven cars to changing vehicles to having more

environmentally friendly technology, which is gaining popularity. By 2036, Thailand

is expected to have 1.2 million EVs with more than 690 charging stations nationwide

(Yongpisanphob, 2018).

The long-term plan from the government’s policy emphasizes on the

development of electric vehicle technology with the goal that Thailand will become a

regional electric vehicle production hub. Unfortunately, building a domestic market

for electric vehicles is still a challenge, and it is likely to take many years for EVs to

penetrate the Thai market. This is because EVs remain expensive, and there is a

limited number of charging stations, which do not cover the entire country (ibid)

The automotive industry is a crucial sector for both the domestic and export activity

of Thailand’s economy, which the industry is consistently growing. Therefore, the

study of this subject was considered to be significant because it would provide a better

understanding about Thai consumers and the key driven factors that would prepare the

automotive industry to further accelerate in the future.

Ref. code: 25616002040845PKB

5

1.2 Research Purpose

The purpose of this study aimed to understand the needs of EVs in the Thai

consumers’ mind focusing on the potential that customers perceive on electric cars

based on individual characteristics, and the key driven factors to buy electric cars. The

participants were a group of Thai people aged between 25-49 years who live in

Bangkok Metropolitan Region.

Therefore, this study would be beneficial for businesses or related parties that

are involved in the electric vehicle industry from the government, public or private

charging infrastructure, and auto manufacturers. This would be in preparation for

attracting the early adopter of the brand new technology of EVs in Thailand. The

concept of a contemporary topic in applied marketing was implemented in this study

under the subject area of the technological issue on the electric car in Thailand.

1.3 Research Objectives

The objective of the study was to identify in depth the potential that customers

perceive on electric cars based on individual characteristics and key factors driving

the intention to buy electric cars. This study included the following main objectives:

1.3.1 To determine the current perception and attitude of the Thai people

toward an electric car in Bangkok Metropolitan Region.

a. To determine the advantages of an electric car in the consumers’

perspective.

b. To determine the disadvantages of an electric car in the consumers’

perspective.

1.3.2 To identify important factors, which would influence the intention to

purchase an electric car in the future.

a. Electric car’s attributes that impact on purchasing decision

b. External factors that impact on purchasing decision

1.3.3 To define the electric car’s consumers’ segmentation based on

demographic and psychological factors.

Ref. code: 25616002040845PKB

6

CHAPTER 2

REVIEW OF LITERATURE

2.1 Electric Vehicles

There are three main types of electric vehicles (EVs) classified by the degree

that electricity is used as their energy source. Hybrid electric vehicles (HEVs) are

powered by both gasoline and electricity. The electric energy is generated by the car’s

own braking system to recharge the battery. HEVs start by using the electric motor

then the gasoline engine becomes activated as the speed rises to about 3.2 kilometers

(EVgo, 2018). HEVs are not plug-ins, as they cannot be recharged from the power

grid (BC Hydro, 2018).

Plug-in hybrid electric vehicles (PHEVs) can recharge the battery through

both regenerating braking and plugging in to an external power. Compared to the

regular HEVs, which can travel about 3.2 kilometers before the gasoline engine turns

on, PHEVs can go up to 16-64.5 kilometers before the gas engines start to operate

(EVgo, 2018).

Battery electric vehicles (BEVs) that are more often called electric vehicles

(EVs), are fully electric with rechargeable batteries and no gasoline engine. The

battery power is used to run the electric motor and all onboard electronics. The best

thing about battery electric vehicles is that they do not release any harmful emissions.

They are charged from only an external power source (ibid).

2.2 Global Electric Vehicle Overview

With the decreasing supplies of oil, the world is turning to electric mobility.

The majority of today's cars are still using an internal combustion engine (ICE) even

though hybrid cars are becoming a normal sight nowadays and total electric ones are

also gaining recognition. This could be seen with the global share of plug-in cars

reaching 2% in December 2017 (EVvolumes, 2017). They are actually simpler to

manufacture and to maintain, but the range is lower than that of cars with ICE since

Ref. code: 25616002040845PKB

7

battery technology has yet to offer the same energy density as gasoline. The charging

time and charger availability are also preventing the adoption of electric cars;

however, this is accelerating and expected to comprise 55% of all new car sales by

2040 (Bloomberg NEF, 2018).

Many countries have vowed to clean up their cities, air, and energy. The

Netherlands and Norway declared that they would end gas and diesel car sales by

2025. India pledged to do the same by 2030. Scotland will end the sales of such cars

by 2032, and England and France by 2040. Germany has also stated the same, but has

not yet set a date (Enyedi, 2018). China, selling 30% of passenger vehicles around the

world, also announced in September 2017, that the government is working on a

schedule to end the sale of ICE cars, but also to gradually reduce the subsidies for

electric cars (Roberts, 2017).

2.3 Thailand’s Current Market Situation

In Thailand, electric cars were launched for the first time in 2009, in the form

of hybrid electric vehicles (HEVs). In 2016, German brands implemented plug-in

hybrid electric vehicles (PHEVs) to serve the high-end automotive market (Bangkok

Post, 2018). Since then, electric cars have only comprised 1% of the total number of

passenger cars in Thailand with less than 85,000 hybrids and plug-in hybrids in the

country (Consultancy.asia, 2018; Nation, 2018). Although demand for electric cars is

expected to remain low in the near future, increased incentives, lower prices, and

better infrastructure will boost adoption in the long term (KPMG, 2018).

2.4 Thailand’s Market Segment Situation

Despite the low adoption rate of electric cars in Thailand, a study for Nissan

Motor (Thailand) Co., Ltd. conducted by Frost and Sullivan (2018) has shown that for

Thailand, there is a significant latent demand for electric vehicles in the Kingdom

with 44% of 300 respondents saying they would undoubtedly consider an EV when

they make their next purchase decision (Nissan Motor Thailand, 2018). The survey

also found that potential electric vehicle buyers are relatively young and have a strong

Ref. code: 25616002040845PKB

8

concern about the environment, with prospective customers ready to pay up to 50%

more to own an electric vehicle than they would for a comparable conventional ICE

car (Frost and Sullivan, 2018).

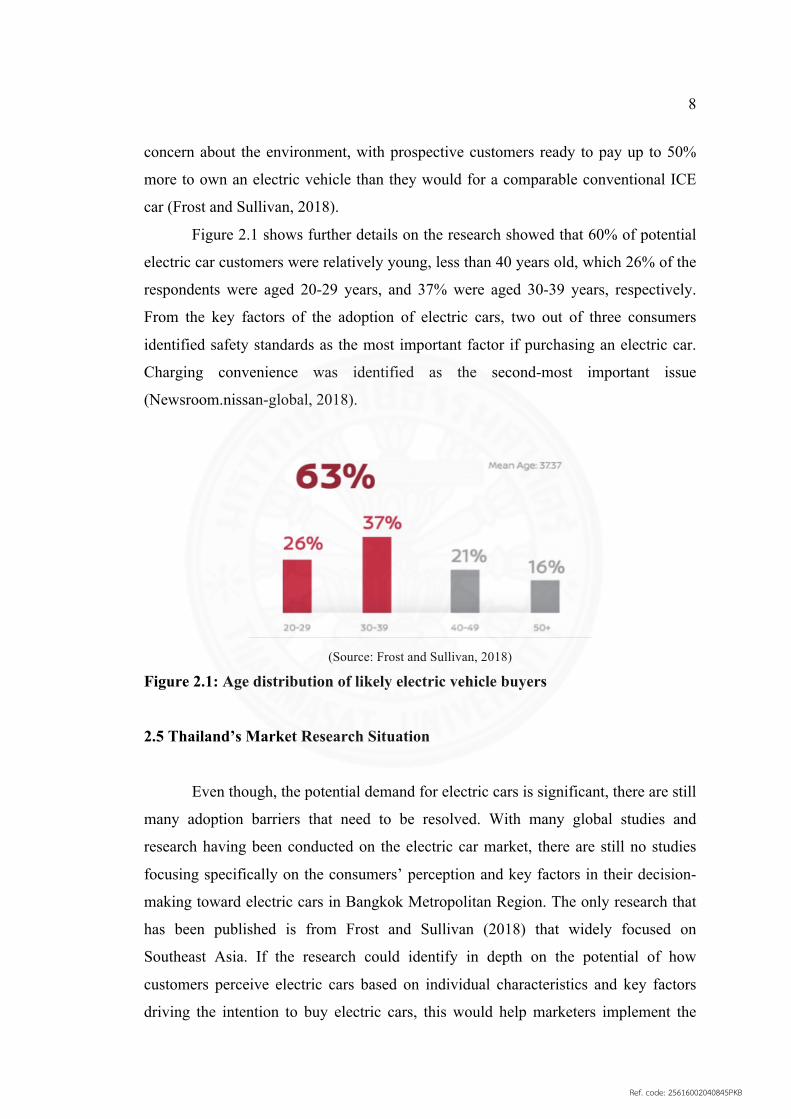

Figure 2.1 shows further details on the research showed that 60% of potential

electric car customers were relatively young, less than 40 years old, which 26% of the

respondents were aged 20-29 years, and 37% were aged 30-39 years, respectively.

From the key factors of the adoption of electric cars, two out of three consumers

identified safety standards as the most important factor if purchasing an electric car.

Charging convenience was identified as the second-most important issue

(Newsroom.nissan-global, 2018).

(Source: Frost and Sullivan, 2018)

Figure 2.1: Age distribution of likely electric vehicle buyers

2.5 Thailand’s Market Research Situation

Even though, the potential demand for electric cars is significant, there are still

many adoption barriers that need to be resolved. With many global studies and

research having been conducted on the electric car market, there are still no studies

focusing specifically on the consumers’ perception and key factors in their decision-

making toward electric cars in Bangkok Metropolitan Region. The only research that

has been published is from Frost and Sullivan (2018) that widely focused on

Southeast Asia. If the research could identify in depth on the potential of how

customers perceive electric cars based on individual characteristics and key factors

driving the intention to buy electric cars, this would help marketers implement the

Ref. code: 25616002040845PKB

9

right strategies and raise awareness to attract more customers in the market in the

future. As such, this current research included: 1) research on potential customers’

characteristics based on the age of 25-49 years, 2) key factors driving the adoption of

electric cars, and 3) the intention to purchase electric cars. This would be developed

further with an insight on the findings of these three areas of study.

2.6 Summary of Literature Review

From a summary of the literature review, it was found that (1) research on

electric vehicles and Thai consumers was limited, (2) research on electric vehicles and

consumers had not determined any consumers’ perception and attitude toward electric

vehicles in Bangkok Metropolitan Region, and (3) research on electric vehicles and

consumers had not determined any psychological factors that would drive the

individuals’ need toward purchasing electric vehicles. Thus, this proposed study

would provide contributions in these three areas.

Ref. code: 25616002040845PKB

10

CHAPTER 3

RESEARCH METHODOLOGY

This research study was conducted using two main research methods, which

were exploratory research and descriptive research. The exploratory research

consisted of secondary research and qualitative research (in-depth interviews). The

findings from the exploratory research were used as a basis to develop quantitative

research (online questionnaire). The sequence of this research is shown in Figure 3.1

below.

Figure 3.1: Research process

3.1 Exploratory Research Design

Secondary research and in-depth interviews were used to identify consumers’

perception and attitude on electric vehicles, and the key influential factors that drive

the individuals’ need toward purchasing electric vehicles. The findings from the

exploratory research were used as a basis to develop an online questionnaire under a

descriptive research design.

3.1.1 Secondary Research

Secondary research was used to gather background information

regarding the overview of EVs, as well as the automotive industry’s trends from both

the global and Thai markets. Public statistical data and information were researched

from credible sources; for example, the Electric Vehicle Association of Thailand

(EVAT), Department of Land Transport, Thailand Board of Investment, Krungsri

Industry Outlook, International Organization of Motor Vehicles Manufacturers

Ref. code: 25616002040845PKB

11

(OICA), KPMG Industry Focus, and Frost and Sullivan. In addition, journals and

online articles from reliable sources were used to identify the driven factors and

barriers of EVs among potential buyers.

3.1.2 In-depth Interview

An in-depth interview was conducted during October 2018 by

interviewing four Thai people who lived in Bangkok Metropolitan Region. The in-

depth interview took approximately 30 minutes per respondent. The objectives of the

in-depth interviews were to discover the respondents’ knowledge, perception and

attitude of EVs in term of performance, safety, expense, social impact, key factors in

switching, and barriers from preventing them from using these vehicles. The example

of the questions for the in-depth interview is shown in Appendix A.

3.2 Descriptive Research

Descriptive research was conducted using an online questionnaire, which was

designed based on the key findings and insights from the exploratory research. The

descriptive research aimed to quantity the data to allow for the statistical analysis of

potential consumers’ characteristic, perception, and key factors in their decision-

making toward EVs.

3.2.1. Online Questionnaire

The survey research was conducted through an online channel with a

total of 160 respondents. The online questionnaire consisted of screening questions,

perception and attitude questions, key factors in decision-making, barriers of adoption

of EVs, and demographic questions. The example of the online questionnaire is

shown in Appendix B.

Ref. code: 25616002040845PKB

12

3.3 Sampling Plan

The sampling procedure employed for this project was based on the non-

probability technique. The convenience sampling allowed for convenient accessibility

in conducting the research that comprised an in-depth interview of four participants

and online questionnaire of 160 respondents. Prior to the launching of the

questionnaire, five pilot tests were conducted to validate the understanding of the

survey. Table 3.1 shows the sample size of each collection method.

Table 3.1: Participants collection

Data Collection Method

Sampling Method

Sampling Criteria

Pilot Study Sample Size

In-depth Interview

Convenience

Sampling

Male and Female,

25-49 years old,

Bangkok

Metropolitan

Region

-

4 people

Online

Questionnaire

Convenience

Sampling

Male and Female,

25-49 years old,

Bangkok

Metropolitan

Region

5 people

160 people

3.4 Recruitment Plan

3.4.1 Recruitment Criteria

This research study focused on Thai people aged between 25-49 years

who lived in the urban area of Bangkok Metropolitan Region. According to a survey

Ref. code: 25616002040845PKB

13

conducted by Frost and Sullivan (2018), the findings showed that people aged

between 20-49 years had a strong interest in buying EVs, or accounting for 84% of all

age ranges. As electric vehicle technology is still new in the Thai market, it could take

up to 10 years to influence the industry. Thus, this created an ideal study to

investigate this group of people, as they will become the potential customers of EVs.

3.4.2 Recruitment Method

Due to time constraints, a non-probability convenience sample was used

for all in-depth interviews and the online questionnaire. All respondents had to pass

the recruitment criteria to be able to participate in this research. Personal connections

were used to achieve the qualified participants for the in-depth interviews.

The online questionnaire used screening criteria questions to identify the

qualified participants. The online questionnaire was distributed through personal

contacts by means of social media applications; such as, LINE, Facebook and through

online public forums related to EVs; such as, Pantip and Facebook pages. The length

of the survey took approximately 10 minutes for the respondents to complete.

3.5 Identification of Key Research Variables

The independent variables and dependent variables in this study are

described in Figure 3.2 below.

Figure 3.2: Conceptual model

Ref. code: 25616002040845PKB

14

3.6 Data Analysis Plan

The key findings from the exploratory research were used as a guideline to

develop the descriptive research. The responses from the online questionnaire were

grouped and coded to ensure data accuracy for the data analysis. The Statistical

Package for the Social Sciences (SPSS) was used to analyze the frequency,

percentage and mean, conduct factor analysis and cluster analysis, and determine the

differences between the clusters. Figure 3.3 below shows an example of the data

analysis plan for the quantitative data.

Figure 3.3: Data analysis plan for the quantitative data

Ref. code: 25616002040845PKB

15

CHAPTER 4

RESULTS AND DISCUSSION

4.1 Key Findings from the In-depth Interviews

4.1.1 In-depth Analysis

A total of four in-depth interviews were conducted to understand the

consumers’ perception, basic knowledge and key factors in changing to use an electric

car in the Bangkok Metropolitan area. The questions covered the consumers’

preferences on purchasing a car, consumers’ knowledge about electric cars,

consumers’ perception of electric cars compared to internal combustion engine (ICE)

vehicles, and the key factors for changing to an electric car.

The interviewees were collected using convenience sampling with a

variety of career fields. One respondent was a female aged 26 years old who was

employed as a marketing promotion officer. Another two were males aged 28 years

old who worked as a dentist and interior designer, respectively. The last one was a

male aged 31 years old who worked as a sales manager and was about to have his first

child this year. All the respondents had their own cars and lived in the Bangkok

Metropolitan Region. The key findings of each interview are mentioned below.

4.1.2 Preferences for Purchasing a Car

In terms of choosing a car, three out of four respondents said they chose

a car based on the look and design of the vehicle as the most important factor.

However, the other one said he focused on the brand that had a high dealership

coverage in many cities to ensure the availability of maintenance services.

Nevertheless, all of them mentioned about the car’s performance, pricing and

maintenance costs.

On the types of cars, two out of four respondents said they owned a SUV

because they loved the versatility, greater space, and more passenger room. They also

mentioned that they felt safer driving a four-wheel drive vehicle, and it also served

their lifestyle of going on road trips quite often. The other two owned compact cars,

Ref. code: 25616002040845PKB

16

which they mostly used for the daily commute from their home to the office.

Moreover, these two respondents were more concerned on saving gas than the SUV

owners.

4.1.3 Consumers Knowledge about an Electric Car

All of the respondents did not fully understand what types of electric

cars were available in the market. They often got confused between hybrid, plug-in

hybrid, and full electric. In particular, they broadly associated hybrid and plug-in

hybrid as “hybrid cars” without knowing the differences. The full electric car was the

one they called an “electric car”, as they perceived it as the one that needed a charger.

However they could not differentiate electric cars while on the road.

Three out of four respondents associated hybrid cars with brands like

Toyota, Mercedes Benz, and BMW, as these were the vehicles they had seen the most

in the market. Moreover, the only full electric car on their mind was Tesla, which all

of them mentioned.

4.1.4 Key Factors in Changing to an Electric Car

All of the respondents had no concerns about the safety of electric cars,

as they said if the vehicles had already passed the manufacturer’s quality assurance,

then there should not be any safety problem. Moreover, they seemed to agree on the

saving of gas from electric cars, but two of them mentioned that they were skeptical

about the maintenance costs, as it could be more expensive in the long term.

Three of the respondents firmly pointed out about the charging

infrastructure, as they tended to go out of the city more, and this was a major factor of

using electric cars. However, one person said what would happen if she was caught in

traffic for two hours, and there were no charging stations nearby. This was a major

issue for them. Most of them strongly believed that electric cars would help reduce air

pollution. On the other hand, one person said it would only temporarily help the

environment because in the long run, if coals that are used to make electricity were

depleted, we would need to find a new solution for the environment again.

Ref. code: 25616002040845PKB

17

4.2 Key Findings from the Questionnaire Survey

4.2.1 Respondents’ Demographics

The online questionnaire was distributed to 243 respondents using

Surveymonkey.com However, 160 respondents met the criteria and completed the

questionnaire survey. The other 54 respondents did not qualify to pass the screening

questions, and the remaining 29 respondents did not fully complete the questionnaire

survey.

Number of Respondents: 160 people

Gender: 42% male and 58% female.

Age: The majority of respondents were aged between 25-29 years old (48%)

followed by the group aged 30-34 years old (22%).

Education: The majority of respondents had a bachelor’s degree or equivalent

(52%) as their highest level of education followed by the group with a

master’s degree (44%).

Occupation: The majority of respondents were officer workers (59%)

followed by a group of business owners (21%).

Monthly Income: 31% of respondents had a monthly income of

20,001 – 40,000 Baht/month followed by 30% of respondents that earned

40,001 – 60,000 Baht/month.

Fortunately, all target respondents were Thai nationals aged between 25-

49 years old, male and female, who lived in the Bangkok Metropolitan Region (refer

to Appendix C)

4.2.2 Consumer Segments by Attitude and Lifestyle

The factor and cluster analysis were conducted to classify all

respondents into segments based on their lifestyle and attitude. Initially, the factor

analysis was applied on 12 independent variables using the “Varimax Rotation”. The

results showed that those variables were grouped into four critical factors (refer to

Ref. code: 25616002040845PKB

18

Table 4.1), which were: 1) early adopter of technology with details oriented, 2) high-

end lifestyle, 3) adventure and independence, and 4) social responsibility.

Table 4.1: Finding key factors using the factor analysis

Rotated Component Matrix

Component

Early Adopter of Technology with Details

Oriented

High-end Lifestyle

Adventure and Independence

Social Responsibility

Q1 I am usually among the first to try new products.

.705 .221 .061 -.270

Q2 I like to update myself on new technology.

.799 -.057 .087 -.139

Q3 I want to look different than others. .570 .384 .020 .148

Q4 I like to pay attention to details when selecting products.

.653 -.085 .020 .310

Q5 I believe a higher price means higher quality.

.040 .857 .022 -.121

Q6 I prefer high-end products with a high reputation.

.104 .841 -.062 0.72

Q7 I like to do volunteer work. -.005 -.104 .444 .580

Q8 I prefer not to use plastic bags. -.036 .010 .053 .835

Q9 I like to try new activities. .157 .029 .752 .249

Q10 I like outdoor sports. -.092 -.094 .820 -.048

Q11 I love freedom. .275 .142 .354 .339

Q12 I dare to take a risk. .397 .076 .282 .122

Extraction Method: Principal Component Analysis. Rotation Method: Varimax with Kaiser Normalization.

Ref. code: 25616002040845PKB

19

In the second step, cluster analysis was applied to determine the attitude and

lifestyle patterns, which differentiated respondents into their own segments. As a

result, all respondents were divided into three segments: 1) High-end Tech Savvy

Consumers, 2) Eco-conscious Consumers, and 3) Independent Quality-oriented

Consumers (refer to Table 4.2).

Table 4.2: Segments from the cluster analysis

Final Cluster Centers

Cluster Factors

High-end Tech Savvy Consumers

(n=37)

Eco-conscious Consumers

(n=65)

Independent Quality-oriented

Consumers (n=58)

Early adopter of technology with details oriented.

.83901 .22134 -.78328

High-end lifestyle. .61910 -.78674 .48674

Adventure and independence. -.58879 .08413 .28132

Social responsibility. -.56899 .54568 -.24856

Ref. code: 25616002040845PKB

20

Figure 4.1: Association between the characteristics in each segment

The three segments can be described as below:

Segment 1: “High-end Tech Savvy Consumers” (n=37)

This segment represented the group of people who were early adopters of new

technology and always maintained their knowledge through the latest IT news. They

paid a lot of attention to details when selecting their products, which they did not

mind paying a premium price if the product quality and reputation were at the high-

end level. However, they did not pay much attention on saving the world by reducing

plastics or helping in voluntary work.

Segment 2: “Eco-conscious Consumers” (n=65)

This segment comprised the group of people who loved to make the world a

better place. They always showed concern for the environment by helping to reduce

all kinds of plastics and helping other people by doing voluntary work in their free

time. Moreover, they moderately maintained their know-how about the latest

technology with the willingness to adopt, as long as the technology could help shape

Ref. code: 25616002040845PKB

21

the world in a better way. However, they did not prefer luxury products or conduct

any extravagant buying.

Segment 3: “Independent Quality-oriented Consumers” (n=58)

This segment consisted of the group of people who loved freedom, activities

and high-quality products. They also liked to explore and try new activities, especially

outdoor activities and sports. Moreover, they preferred high-quality products with a

high reputation and did not mind spending for a premium price. Nevertheless, when it

came to technology, this group was low-tech, as they did not maintain an interest in

new technology and were the last group of people who would adopt it, as they found

it hard to learn new technology.

4.2.3 Consumers’ Perception toward Electric Cars

The respondents were asked to rate the following statements by using a

five-point Likert scale (1 Strongly Disagree - 5 Strongly Agree) on their opinions

about an electric car. According to the results from all respondents, the top four

positive statements were: 1) “EV is a gas saver.” (mean = 4.53), 2) “EV is the future

of transportation.” (mean = 4.48), 3) “EV is environmentally friendly.” (mean = 4.43),

and 4) “EV is advanced technology.” (mean = 4.26). Surprisingly, all three segments

positively agreed on the top four perception statements toward electric cars, as the

means were determined by each segment (refer to Table 4.3).

On the other hand, the two lowest statements that respondents seem to

somewhat disagree were: “EV charging stations are widely accessible.” (mean = 2.35)

and “EV can be driven in a long distance.” (mean = 2.71). This indicated the negative

perception toward electric cars in those two aspects.

Moreover, the analysis of variance (ANOVA) was applied to determine

whether there were significant differences among the three segments. The results from

Table 4.3 show that there was only one significant statement with p < 0.05: “EV is

smooth and silent.” Both the High-end Tech Savvy Consumers and Eco-conscious

Consumers had an equal means of 4.03, but Independent Quality-oriented Consumers

only had a mean of 3.71. Hence, the conclusion showed that there was no statistically

significant difference in the means from other statements between the three segments.

Ref. code: 25616002040845PKB

22

Table 4.3: Consumers’ perception toward electric cars by segments

All Respondents

(n=160)

High-end Tech Savvy Consumers

(n=37)

Eco-conscious Consumers

(n=65)

Independent Quality-oriented

Consumers (n=58)

ANOVA between

Segments

Perception Statements

toward Electric Cars

Mean S.D. Mean S.D. Mean S.D. Mean S.D. F Sig.

EV is advanced technology.

4.26 .63 4.22 .79 4.35 .51 4.19 .63 1.176 .311

EV is a gas saver. 4.53 .51 4.51 .51 4.62 .49 4.43 .53 2.014 .137

EV is environmentally friendly.

4.43 .63 4.41 .72 4.54 .56 4.33 .63 1.771 .174

EV is the future of transportation.

4.48 .59 4.46 .61 4.58 .50 4.38 .67 1.889 .155

EV has a higher safety standard.

3.51 .78 3.41 .86 3.62 .80 3.47 .68 1.028 .360

EV is worth the value.

3.53 .85 3.32 1.08 3.60 .81 3.59 .70 1.451 .237

EV has low maintenance cost.

2.84 1.10 2.51 1.22 3.05 1.18 2.83 .88 2.827 .062

EV charging stations are widely accessible.

2.35 1.22 2.24 1.34 2.42 1.36 2.34 .98 .232 .794

EV can be driven in a long distance.

2.71 1.07 2.70 1.08 2.86 1.18 2.55 .90 1.301 .275

EV is smooth and silent.

3.91 .77 4.03 .80 4.03 .79 3.71 .70 3.321 .039

4.2.4 Electric Cars’ Attributes that Impact the Purchasing Decision

As Table 4.4 shows, the respondents were asked to rate the importance

of electric cars’ attributes toward the purchasing decision by using a five-point Likert

scale (1 Not Important - 5 Very Important). The results showed that the top three

important attributes were: 1) “Safety standard” (mean = 4.68), 2) “Performance”

(mean = 4.43), and 3) “Maintenance costs” (mean = 4.39).

Ref. code: 25616002040845PKB

23

Table 4.4: Importance of electric cars’ attributes toward the purchasing decision

by segments

All Respondents (n=160)

High-end Tech Savvy Consumers

(n=37)

Eco-conscious Consumers

(n=65)

Independent Quality-oriented

Consumers (n=58)

Electric Cars’ Attributes

Mean S.D. Mean S.D. Mean S.D. Mean S.D.

Performance 4.43 .58 4.41 .60 4.54 .56 4.33 .57

Design 4.24 .58 4.27 .61 4.31 .61 4.14 .51

Safety standard 4.68 .53 4.59 .64 4.77 .46 4.62 .52

Competitive price 4.38 .61 4.32 .71 4.54 .59 4.24 .54

Maintenance costs 4.39 .65 4.32 .71 4.49 .66 4.33 .57

Reliability of the technology

4.38 .62 4.32 .71 4.55 .56 4.21 .59

Dealer coverage in my area

4.19 .75 4.05 .74 4.23 .84 4.22 .62

According to the ANOVA analysis among the segments, there were two

significant purchasing factors between segments with p < 0.05, which were

“Competitive price” and “Reliability of the technology”. Follow-up tests showed that

the mean score on both factors for Eco-conscious Consumers (mean = 4.54) and

(mean = 4.55) were significantly higher than the mean score for Independent Quality-

oriented Consumers (mean = 4.24), and (mean = 4.21) (refer to Table 4.5).

Ref. code: 25616002040845PKB

24

Table 4.5: Comparison of electric cars’ attributes between segments

Comparison of the Column Means a

High-end Tech Savvy Consumers

(n=37)

Eco-conscious Consumers

(n=65)

Independent Quality-oriented

Consumers (n=58)

ANOVA between

Segments

Electric Cars’

Attributes

(A) (B) (C) F Sig.

Performance 2.112 .124

Design 1.410 .247

Safety standard 1.757 .176

Competitive price C 3.948 .021

Maintenance costs 1.282 .280

Reliability of the technology

C 5.189 .007

Dealer coverage in my area

.770 .465

The results were based on two-sided tests assuming equal variances with a significance level of .05. For each significant pair, the key of the smaller category appeared under the category with a larger mean. a a. Tests were adjusted for all pairwise comparisons within a row of each innermost sub table using the Bonferroni correction.

4.2.5 External Purchasing Factors on Electric Cars

As seen in Table 4.6, the respondents were asked to rate the importance

of the external factors that had an impact on purchasing electric cars using a five-point

Likert scale (1 Not Important - 5 Very Important). From the results from all

respondents, the top three important factors were: 1) “Charging point at

home/apartment.” (mean = 4.65), 2) “Charging station coverage in major cities.”

(mean = 4.61), and 3) “Option for a faster charge.” (mean = 4.52). Additionally, all

three segments strongly agreed on the top three external factors that they saw as the

most important points.

Ref. code: 25616002040845PKB

25

Table 4.6: Importance of external purchasing factors by segments

All Respondents (n=160)

High-end Tech Savvy Consumers

(n=37)

Eco-conscious Consumers

(n=65)

Independent Quality-oriented

Consumers (n=58)

External Purchasing

Factors

Mean S.D. Mean S.D. Mean S.D. Mean S.D.

Charging station coverage in major cities.

4.61 .52 4.54 .51 4.69 .47 4.55 .57

Charging point at home/apartment.

4.65 .55 4.54 .56 4.74 .54 4.62 .56

Option for a faster charge.

4.52 .65 4.35 .75 4.69 .56 4.45 .65

Ability to charge at work.

4.36 .76 4.35 .68 4.45 .79 4.26 .76

Lower tax on EVs. 4.17 .95 4.05 1.10 4.42 .86 3.97 .88

Priority parking for EV drivers.

3.86 .97 3.95 1.05 3.94 1.01 3.71 .86

Toll discounts. 3.82 1.09 3.68 1.31 4.02 1.08 3.71 .92

Based on the ANOVA analysis among the segments, there were two

significant external purchasing factors with p < 0.05, which were “Option for a faster

charge.” and “Lower tax on EVs.” In addition, the follow-up tests showed that the

mean score on the “Option for a faster charge.” factor for Eco-conscious Consumers

(mean = 4.69) was significantly higher than the mean score for High-end Tech Savvy

Consumers (mean = 4.35). Furthermore, the mean score on the “Lower tax on EVs.”

factor for Eco-conscious Consumers (mean = 4.42) was significantly higher than the

mean score for Independent Quality-oriented Consumers (mean = 3.97) (refer to

Table 4.7).

Ref. code: 25616002040845PKB

26

Table 4.7: Comparison of the external purchasing factors between segments

Comparison of the Column Means a

High-end Tech Savvy Consumers

(n=37)

Eco-conscious Consumers

(n=65)

Independent Quality-oriented

Consumers (n=58)

ANOVA between

Segments

External Purchasing

Factors

(A) (B) (C) F Sig.

Charging stations coverage in major cities.

1.543 .217

Charging points at home/apartment.

1.659 .194

Option for a faster charge.

A 3.980 .021

Ability to charge at work.

.945 .391

Lower tax on EVs. C 3.957 .021

Priority parking for EV drivers.

1.080 .342

Toll discounts. 1.692 .187

The results were based on two-sided tests assuming equal variances with a significance level of .05. For each significant pair, the key of the smaller category appeared under the category with a larger mean. a a. Tests were adjusted for all pairwise comparisons within a row of each innermost sub table by using the Bonferroni correction.

4.2.6 Impact between Consumers’ Attitudes and the Purchasing Factors

4.2.6.1 Impact of Electric Cars’ Attributes

Table 4.8 shows the simple linear regression analysis between

consumers’ attitudes (dependent variable) and seven electric cars’ attributes

that had an impact on the purchasing decision (independent variable). A

significant regression equation was found (F (7,153) = 623.297, p < .000),

with an R square of .966.

As a result, the coefficients for the “Reliability of the

technology” and “Design” were significant at p < .05. Therefore, these two

Ref. code: 25616002040845PKB

27

attributes were the key predictors for having an impact on purchasing electric

cars.

Table 4.8: Regression analysis between consumers’ attitudes and seven electric

cars’ attributes that had an impact on the purchasing decision

Predictors (Independent Variables)

Standardized Coefficients

Coefficients a

Electric Cars’ Attributes That Had an Impact on the Purchasing Decision

Beta t Sig.

Performance .225 1.835 .068

Design .344 2.890 .004

Safety standard .004 .028 .978

Competitive price .175 1.218 .225

Maintenance costs -.291 -1.926 .056

Reliability of the technology .507 4.242 .000

Dealer coverage in my area .022 .231 .818

a. Dependent Variable: I am interested in purchasing an electric car in the future.

4.2.6.2 Impact of External Purchasing Factors

Table 4.9 shows the simple linear regression analysis between

consumers’ attitudes (dependent variable) and seven external factors that had

an impact on the purchasing of electric cars (independent variable). A

significant regression equation was found (F (7,153) = 533.115, p < .000),

with an R square of .961.

As a result, the coefficients for “Lower tax on EVs.” and

“Charging stations coverage in major cities.” were significant at p < .05.

Therefore, these two external factors were the key predictors for having an

impact on purchasing electric cars.

Ref. code: 25616002040845PKB

28

Table 4.9: Regression analysis between consumers’ attitudes and seven external

factors that had an impact on purchasing electric cars

Predictors (Independent Variables)

Standardized Coefficients

Coefficients a

External Factors That Had an Impact on Purchasing Electric Cars

Beta t Sig.

Charging stations coverage in major cities.

.352 2.094 .038

Charging points at home/apartment. .274 1.555 .122

Option for a faster charge. .249 1.708 .090

Ability to charge at work. -.128 -.976 .331

Lower tax on EVs. .266 2.846 .005

Priority parking for EV drivers. -.036 -.425 .671

Toll discounts. .008 .091 .928

a. Dependent Variable: I am interested in purchasing an electric car in the future.

4.2.7 Consumers’ Attitudes toward the Intention to Find More

Information on Electric Cars

The answers from the statement “I am interested to find out more

information about electric cars.” (five-point Likert scale) indicated the consumers’

attitudes toward their intention to obtain more information about electric cars. The

overall attitude from all respondents was positive (mean = 3.66). As shown in Table

4.10, an ANOVA showed that there were no significant differences of attitudes

between the segments (F (2,157) = 2.217, p>.05). However, Eco-conscious

Consumers showed the most interest in seeking more information about electric cars

(mean = 3.81).

Ref. code: 25616002040845PKB

29

Table 4.10: Consumers’ intention to seek more information by segments

I am Interested to Find More Information about Electric Cars.

Mean

S.D.

F

Sig

High-end Tech Savvy Consumers (n=37)

3.67 .973

Eco-conscious Consumers (n=65)

3.81 .768

Independent Quality-oriented Consumers (n=58)

3.48 .922

2.217

.112

All respondents (n=160) 3.66 .882

4.2.8 Consumers’ Attitudes toward the Intention to Purchase Electric

Cars in the Future

The answers from the statement “I am interested in purchasing an

electric car in the future.” (five-point Likert scale) indicated the consumers’ attitudes

toward purchasing an electric car. The overall attitude from all respondents was

positive (mean = 4.01). As shown in Table 4.11, Eco-conscious Consumers showed

the most interest in purchasing an electric car (mean = 4.16), which was significantly

higher than Independent Quality-oriented Consumers (mean = 3.81) (F (2,157) =

3.044, p < .05).

Table 4.11: Consumers’ intention to purchase electric cars by segments

I am Interested in Purchasing an Electric Car in the Future.

Mean

S.D.

F

Sig

High-end Tech Savvy Consumers (n=37)

4.05 .941

Eco-conscious Consumers (n=65)

4.16 .719

Independent Quality-oriented Consumers (n=58)

3.81 .826

3.044

.050

All respondents (n=160) 4.01 .824

Ref. code: 25616002040845PKB

30

4.2.9 Consumers’ Willingness to Pay

Table 4.12 shows the Chi-square test between the segments; there were

significant differences on the willingness to pay between the segments (Chi-square =

22.03, p < .05). Half of the Eco-conscious Consumers were willing to pay for an

electric car that was priced less than one million Baht (51%), while the majority of

High-end Tech Savvy Consumers (38%) and Independent Quality-oriented

Consumers (38%) were willing to pay between 1,000,001 - 1,500,000 Baht for each

electric car.

Table 4.12: Willingness to pay for an electric car by segments

High-end Tech Savvy

Consumers (n=37)

Eco-conscious Consumers

(n=65)

Independent Quality-oriented

Consumers (n=58)

Chi-square Test between Segments

How Much Would You Like to Pay for an Electric Car?

n % n % n % Chi-square

Sig.

Below 1,000,000 Baht 7 19% 33 51% 17 29%

1,000,001 - 1,500,000 Baht

14 38% 17 26% 22 38%

1,500,001 - 2,000,000 Baht

7 19% 8 12% 13 22%

2,000,001 - 2,500,000 Baht

5 13% 5 8% 5 9%

2,500,001 - 3,000,000 Baht

4 11% 1 1.5% 0 0%

Above 3,000,000 Baht 0 0% 1 1.5% 1 2%

22.030

.015*, b, c

*. The Chi-square statistics were significant at the .05 level. b. More than 20% of the cells in this sub table had the expected cell counts less than 5. The Chi-square results may be invalid. c. The minimum expected cell count in this sub table was less than one. The Chi-square results may be invalid.

Ref. code: 25616002040845PKB

31

CHAPTER 5

CONCLUSIONS AND RECOMMENDATIONS

5.1 Key Findings from the Questionnaire Survey

5.1.1 Thai Consumers’ Perception toward Electric Cars

The top four statements, which had a positive perception toward electric

cars were: 1) EV is a gas saver (mean = 4.53), 2) EV is the future of transportation

(mean = 4.48), 3) EV is environmentally friendly (mean = 4.43), and 4) EV is

advanced technology (mean = 4.26). On the other hand, the two statements with a

negative perception indicated by the lowest means were: 1) EV charging stations are

widely accessible (mean = 2.35), and 2) EVs can be driven in a long distance (mean =

2.71). As a result, the majority of respondents still believed in the lack of charging

stations and the lack of sufficient battery performance for a long driving distance.

However, these statements may not be believed in the mind of auto manufacturers or

charging station companies, as both aspects of perception are a main area for

improvement toward a better understanding in the consumers’ mind.

5.1.2 Key Electric Cars’ Attributes toward the Purchasing Decision

The top three electric cars’ attributes toward the purchasing decision

were: 1) Safety standard (mean = 4.68), 2) Performance (mean = 4.43), and 3)

Maintenance costs (mean = 4.39). The remaining attributes were also important as

they had a mean of > 4.00; these were the Reliability of the technology, Competitive

price, Design, and Dealer coverage in my area.

However, from the results of the simple linear regression analysis

between the consumers’ attitude (dependent variable) and seven electric cars’

attributes on the purchasing decision (independent variable), the two attributes

“Reliability of the technology” and “Design” were the significant predictors that had

an impact on purchasing electric cars, even though their means were not the highest.

Ref. code: 25616002040845PKB

32

5.1.3 External Purchasing Factors on Electrics Cars

The top three external purchasing factors were: 1) Charging point at

home/apartment (mean = 4.65), 2) “Charging station coverage in major cities” (mean

= 4.61) and 3) “Option for a faster charge” (mean = 4.52).

However, from the results of the simple linear regression analysis

between the consumers’ attitude (dependent variable) and seven external factors that

had an impact on purchasing electric cars (independent variable), the two external

factors “Lower tax on EV” and “Charging stations coverage in major cities” were the

significant predictors that had an impact on purchasing electric cars.

5.1.4 Thai Consumer Segments

The respondents were classified into three segments according to their

attitude and lifestyle. The three segments were: 1) High-end Tech Savvy Consumers,

2) Eco-conscious Consumers, and 3) Independent Quality-oriented Consumers.

Segment 1: “High-end Tech Savvy Consumers” were people who loved new

technology and high-end products, but they did not pay attention to being

environmentally friendly. Segment 2: “Eco-conscious Consumers” were people who

loved to make the world a better place. They cared about environmental issues and

also maintained an interest in technology, but they were price sensitive. Segment 3:

“Independent Quality-oriented Consumers” were people who loved new activities and

outdoor sports. When it came to products, they were willing to pay more for better

product quality. However, they were low-tech and barely had any interest in

technology.

5.1.5 Thai Consumers’ Intention to Purchase Electrics Cars

Eco-conscious Consumers were the segment that had the highest

intention to purchase electric cars, which was significantly higher than the

Independent Quality-oriented Consumers segment. The consumers’ attitude was the

key predictor for the intention to purchase electric cars.

Ref. code: 25616002040845PKB

33

5.2 Recommendations

The results from this study provided important findings, which would truly be

beneficial for all types of organizations and companies involved in this early stage of

electric car technology in Thailand.

5.2.1 The Most Desired Segments

Base on the results, “Eco-conscious Consumers” were the most desired

group of people with the highest mean of intention to purchase an electric car and also

the biggest segment (41%) among the three. This group of people searched for the

best for society and was environmentally friendly, which was aligned with the electric

cars’ purpose to reduce air pollution. Moreover, these people were willing to adopt

new technology and ready to change to use EVs, so to make the world a better place.

Nevertheless, one of the major concerns of this group was they were price sensitive

and lacked purchasing power.

Even though they would love to adopt this technology, due to the early

stage of electric cars in Thailand, the majority of global auto manufacturers have set

the premium price at a minimum of 1,500,000 Baht or above. According to the

results, the majority of this group (77%) was willing to pay the maximum of

1,500,000 or below, which did not meet with the current market pricing. In fact, this

could indicate that this group would not be among the early adopters at this point in

time in Thailand. This would be because there is still some gap between the supply

and demand in pricing. In the future, this group might have a major role in being

potential customers, as the price could remain the same until electric cars became

more popular and all the well-known automakers decided to introduce lower tier

models with more affordable prices.

5.2.2 Focus on the Early Adopter Segments

“High-end Tech Savvy Consumers” were a group of people who were

obsessed with new technology, and usually among the first to adopt new products. As

well, they always searched for the best or high-quality product with a high reputation.

Ref. code: 25616002040845PKB

34

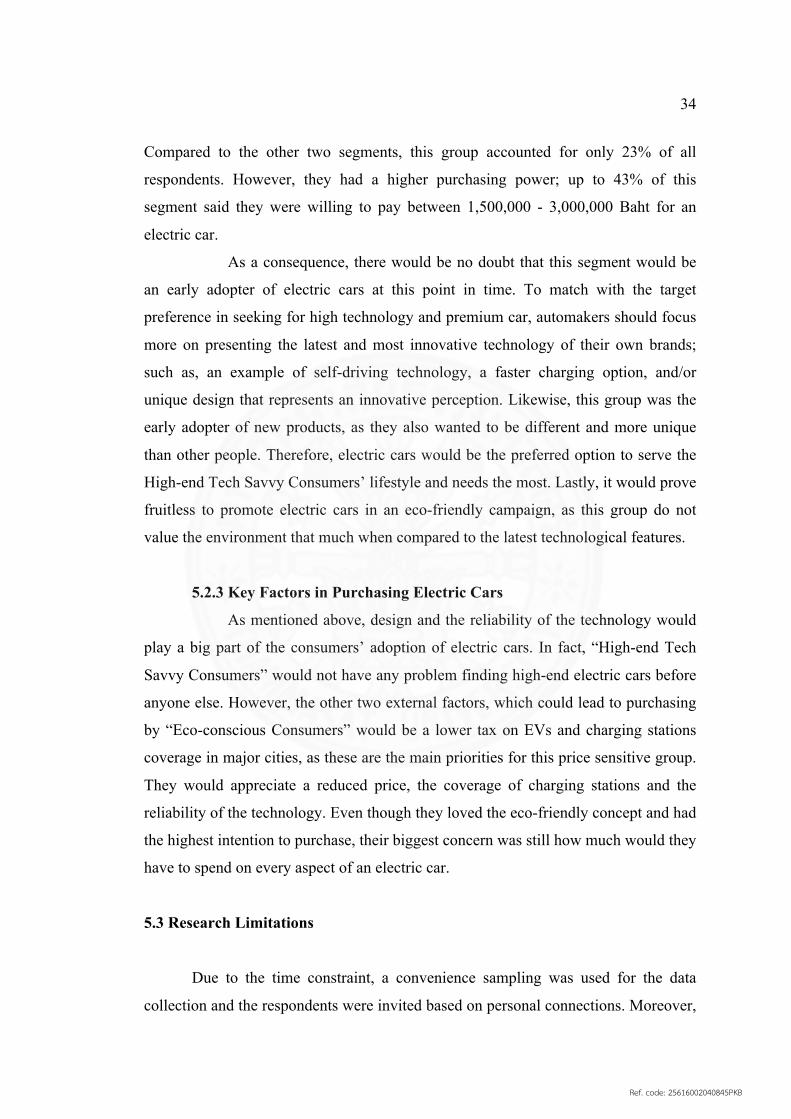

Compared to the other two segments, this group accounted for only 23% of all

respondents. However, they had a higher purchasing power; up to 43% of this

segment said they were willing to pay between 1,500,000 - 3,000,000 Baht for an

electric car.

As a consequence, there would be no doubt that this segment would be

an early adopter of electric cars at this point in time. To match with the target

preference in seeking for high technology and premium car, automakers should focus

more on presenting the latest and most innovative technology of their own brands;

such as, an example of self-driving technology, a faster charging option, and/or

unique design that represents an innovative perception. Likewise, this group was the

early adopter of new products, as they also wanted to be different and more unique

than other people. Therefore, electric cars would be the preferred option to serve the

High-end Tech Savvy Consumers’ lifestyle and needs the most. Lastly, it would prove

fruitless to promote electric cars in an eco-friendly campaign, as this group do not

value the environment that much when compared to the latest technological features.

5.2.3 Key Factors in Purchasing Electric Cars

As mentioned above, design and the reliability of the technology would

play a big part of the consumers’ adoption of electric cars. In fact, “High-end Tech

Savvy Consumers” would not have any problem finding high-end electric cars before

anyone else. However, the other two external factors, which could lead to purchasing

by “Eco-conscious Consumers” would be a lower tax on EVs and charging stations

coverage in major cities, as these are the main priorities for this price sensitive group.

They would appreciate a reduced price, the coverage of charging stations and the

reliability of the technology. Even though they loved the eco-friendly concept and had

the highest intention to purchase, their biggest concern was still how much would they

have to spend on every aspect of an electric car.

5.3 Research Limitations

Due to the time constraint, a convenience sampling was used for the data

collection and the respondents were invited based on personal connections. Moreover,

Ref. code: 25616002040845PKB

35

the study would not represent the entire population of the age range of 25-49 years old

in the Bangkok Metropolitan Region.

In addition, this study on electric cars in Thailand is still limited and lacks

previous academic studies. Therefore, the secondary resources and global academic

studies on electric cars were utilized as the guideline for this study, which sometimes

the references could lead to global implications and trends.

5.4 Suggestions for Future Research

This study did not cover any particular brand of electric car, brand association

with the intention to purchase, comparison between the competitors in the market, or

focus on customers’ satisfaction if electric cars were more accepted in the Thai

market.

Thus, future research should consider the above objectives to examine the key

factors in purchasing electric cars more in-depth. In particular, brand association to

gain more insights and see the impact of each brand on consumers’ attitudes and

perception toward electric cars should also be investigated.

In conclusion, if in the future electric cars do become more well-known and

gain more reputation on the road, by studying the consumers’ satisfaction and

dissatisfaction would be ideal to continuously improve the automotive industry to

serve both the global and domestic markets even better.

Ref. code: 25616002040845PKB

36

REFERENCES

Bangkok Post. (2018, February). Powering the EV surge. Retrieved from

https://www.bangkokpost.com/business/news/1414335/powering-the-ev-surge

BC Hydro. (2018). Electric vehicle technologies & types. Retrieved from

https://www.bchydro.com/powersmart/electric-vehicles/owning-an-electric-

vehicle/technology.html

Bloomberg NEF. (2018). Electric Vehicle Outlook 2018 | Bloomberg New Energy

Finance. Retrieved from https://about.bnef.com/electric-vehicle-outlook/

Consultancy.asia. (2018, April). Study shows popularity of electric vehicles in

Thailand remains low. Retrieved from

https://www.consultancy.asia/news/754/study-shows-popularity-of-electric-

vehicles-in-thailand-remains-low

Enyedi, S. (2018). Electric cars — Challenges and trends. 2018 IEEE International

Conference on Automation, Quality and Testing, Robotics (AQTR).

doi:10.1109/aqtr.2018.8402776

EVgo. (2018). Battery & Plug-in Hybrid Electric Vehicles. Retrieved from

https://www.evgo.com/why-evs/types-of-electric-vehicles/

EVvolumes. (2017). Global Plug-in Sales for 2017-Q4 and the Full Year (prelim.).

Retrieved from http://www.ev-volumes.com/news/global-plug-in-sales-for-2017-

q4-and-the-full-year-prelim/

Frost & Sullivan. (2018). Global Electric Vehicle Market Outlook. Retrieved from

http://www.frost.com/sublib/display-report.do?id=MDAB-01-00-00-

00&bdata=bnVsbEB QEJhY2tAfkAxNTQ0MTY0ODIwOTE1

Ref. code: 25616002040845PKB

37

Frost & Sullivan. (2018, January). The Future of Electric Vehicles in South East Asia.

Retrieved from https://go.frost.com/AT_FutureofElectricVehicles_SA

Helven, Y. (2018, February 15). Automotive Outlook Thailand. Retrieved from

https://www.globalfleet.com/en/manufacturers/asia-pacific/features/automotive-

outlook-thailand

KPMG. (2018, January). Electric vehicle trends. Retrieved from

https://home.kpmg.com/th/en/home/insights/2018/02/th-electric-vehicles-industry-

focus.html

Newsroom.nissan-global. (2018). One in three Southeast Asian consumers open to

buying electric car. Retrieved from https://newsroom.nissan-

global.com/releases/one-in-three-southeast-asian-consumers-open-to-buying-

electric-car

Nissan Motor Thailand. (2018). Some 44% of Thai consumers will consider an EV

when making their next vehicle purchase decision, research shows. Retrieved

from https://en.nissan.co.th/news/purchase-decision-research.html

OICA. (2017). Production Statistics. Retrieved from

http://www.oica.net/category/production-statistics.

Panyaarvudh, J. (2018, September 26). Electric vehicles on the fast track in Thailand.

Retrieved from

http://www.nationmultimedia.com/detail/Startup_and_IT/30354739

Rastogi, V. (2018, August 13). Thailand's Automotive Industry: Opportunities and

Incentives. Retrieved from

https://www.aseanbriefing.com/news/2018/05/10/thailands-automotive-industry-

opportunities-incentives.html

Ref. code: 25616002040845PKB

38

APPENDICES

Ref. code: 25616002040845PKB

39

APPENDIX A

IN-DEPTH INTERVIEWS QUESTIONS

1. What is your favorite type of car?

2. What are the main factors in buying a car?

3. What are the top three factors in choosing a car? Please rank them from the

most important to the third most important.

4. What kind of car do you have?

5. Why did you decide to buy this car?

6. Do you have any ideas about electric cars?

7. What comes to your mind first when you think about electric cars?

8. What type of electric cars have you seen in Thailand?

9. Do you know the difference between hybrid, plug-in hybrid and battery

electric cars?

10. What do you think about electric cars in Thailand?

11. How often have you seen electric cars in Bangkok?

12. Do you know any electric car brands?

13. How did you hear about them?

14. Compared with normal gasoline cars, what way do you think electric cars are

different in terms of performance? Positive or Negative? Please explain?

15. What about in terms of safety?

16. In terms of costs and expenses?

17. What impacts do you think electric cars can have on the environment and

society?

18. If you ever decide to buy an electric car, what would be the most important

factors for you to switch from a gasoline car? Please rank the top three

factors?

19. Do you think our country is ready for electric cars now?

20. What about in the future? What would need to be done for people to start

using electric cars?

Ref. code: 25616002040845PKB

40

APPENDIX B

ONLINE QUESTIONNAIRE QUESTIONS

Part 1: Screening Questions

1. Do you live in Bangkok Metropolitan area?

• Yes

• No (End of survey)

2. How old are you?

• Below 25 (End of survey)

• 25-29

• 30-34

• 35-39

• 40-44

• 45-49

• Above 49 (End of survey)

Part 2: Personality

3. Please rate how much do you agree or disagree on the following statements.

(1 Strongly Disagree - 5 Strongly Agree)

• I am usually among the first to try new products

• I like to update myself on new technology

• I want to look different than others

• I like to pay attention in details when selecting products.

• I believe higher price means higher quality

• I prefer high-end products with a high reputation

• I like to do volunteer work

• I prefer not to use plastic bags

• I like to try new activities

• I like outdoor sports

• I love freedom

Ref. code: 25616002040845PKB

41

• I dare to take a risk

Part 3: Electric car introduction

4. Do you know electric car?

• Yes

• No

In this survey, we will only focus on electric cars that need a plugin charging

with external power, which are 2 main types.

Plug-in hybrid electric vehicles (PHEVs) can recharge battery through both

regenerating braking and plugging in to an external power. Plug-in hybrid electric

vehicles can go up to 10-40 miles before the gas engines start to operate.

Battery electric vehicles (BEVs) are more often called as electric vehicles (EVs), are

fully electric with rechargeable batteries and no gasoline engine. The battery power is

used to run the electric motor and all onboard electronics. The best thing of battery

electric vehicles is that they do not release any harmful emissions. Battery electric

vehicles are charged from external power source only.

5. Have you ever seen electric car?

• Yes

• No

Part 4: Perception and attitude toward electric car

6. Please rate the following statements on how you think about electric car. (1

Strongly Disagree - 5 Strongly Agree)

• EV is advanced technology

• EV is a gas saver

• EV is environmental friendly

• EV is the future of transportation

• EV has a higher safety standard

Ref. code: 25616002040845PKB

42

• EV is worth the value

• EV has low maintenance cost

• EV charging stations are widely accessible

• EV can be driven in a long distance

• EV is smooth and silent

7. Please rate the following statements on how you think about people driving an

electric car. (1 Strongly Disagree - 5 Strongly Agree)

• A person is a tech savvy

• A person is concerned on the environment

• A person is wealthy

• It might be for old people

• This is a family person

• A person is smart

• A person is stylish

• A person is ready to take risk

8. I am interested to find our more information about electric car.

Please rate. (1 Strongly Disagree - 5 Strongly Agree)

Part 5: Factors on purchasing electric car

9. Please rate the following attributes that impact you on purchasing electric car

in the future. (1 Not Important - 5 Very Important)

• Performance

• Design

• Safety Standard

• Competitive Price

• Maintenance Cost

• Reliability of Technology

• Dealer coverage in my area

Ref. code: 25616002040845PKB

43

10. Please rate the following external factors that impact you on purchasing

electric car in the future. (1 Not Important - 5 Very Important)

• Charging station coverage in major cities

• Charging point at home/apartment

• Option for a faster charge

• Ability to charge at work

• Lower Tax on EVs

• Priority Parking for EV drivers

• Toll Discounts

11. I am interested in purchasing electric car in the future.

Please rate. (1 Strongly Disagree - 5 Strongly Agree)

12. How much would you like to pay for an electric car?

• Below 1,000,000 Baht

• 1,000,001 – 1,500,000 Baht

• 1,500,001 – 2,000,000 Baht

• 2,000,001 – 2,500,000 Baht

• 2,500,001 – 3,000,000 Baht

• Above 3,000,000 Baht

Part 6: Personal Information

14. Gender