a statistical modeling on women empowerment of … 15-16 40 projects/18 - j. jenitta edal... · a...

TRANSCRIPT

A Statistical Modeling on Women Empowerment of

Self Help Groups in Thanjavur District

The Report of Students Mini ProjectSubmitted

To

TAMILNADU STATE COUNCIL

FOR HIGHER EDUCATION

Chennai - 600 005

Submitted by

J.Jenitta Edal QueenII M.Sc (Statistics)

Department of StatisticsPeriyar E.V.R. College (Autonomous)

Trichy - 620 023.

OCTOBER 2016

CERTIFICATE

This is to certify that this project work entitled “STUDY ON

STATISTICAL MODELING ON WOMEN EMPOWERNMENT OF

SELF GROUPS IN THANJAVUR DISTRICT” is submitted to Tamilnadu

State Council For Higher Education, Chennai – 600 005 by J.Jenitta Edal

Queen, (Reg.No: 14ST06) under the scheme of Students Mini Project for the

year 2015-2016. This is a bonafide work carried out by her during the year

2015-2016.

Signature of the HOD Signature of the Guide

(Prof. SHANTHA RABINSON) (Dr.A.KACHI MOHIDEEN)

CONTENTS

Ch.No Title Page NO

I Introduction and Design of the

study01

II Review of Literature 04

III Methodology and Profile of

the study area12

IV Analysis and Interpretations 15

V Findings of the study and

conclusions24

Bibliography 28

Appendix - Questionnaire 31

1

CHAPTER – I

Introduction and Design of the study

1.1 Introduction

The concept of empowerment is defined as the process by which women take control

and ownership of their choices. The core elements of empowerment have been defined as

agency (the ability to define one’s goals and act upon them), awareness of gendered power

structures, self-esteem, and self-confidence (Kabeer, 2001). Empowerment can take place at a

hierarchy of different levels – individual, household, community and societal and is

facilitated by providing encouraging factors (e.g. exposure to new activities, which can build

capacities) and removing inhibiting factors (e.g. lack of resources and skills). In this

connection various factors like economic status, social awareness, leadership quality and

micro finance etc., play an effective role for promoting women empowerment through Self

Help Groups (SHGs).

1.2 Self Help Groups

SHG is a group of rural poor who have volunteered to organize themselves into a

group for eradication of poverty of the members. The basic principles of the SHGs are group

approach, mutual trust, organization of small and manageable groups, group cohesiveness,

spirit of thrift, demand based lending, collateral free, women friendly loan, peer group

pressure in repayment, skill training capacity building and empowerment. In order to enlarge

the flow of credit to the hard-core poor, NABARD launched a scheme of organizing them in

SHGs and linking the SHGs with Banks, in 1992. Though the SHG were started in 1997 in

Tamilnadu, the concept penetrated down only in recent years. Now there is a greater amount

of socio-economic emancipation among the members of the SHGs. Hence there is a need for

evaluating the social and economic impact of the SHG on their members. Among the various

districts of Tamilnadu, Thanjavur district occupies a predominant position in the starting of

2

SHGs. In this district the urban centers have more rural bias and the economic activities are

more agro based. Hence, the SHGs have been formed for meeting the needs of industrial and

agricultural activities.

1.3 Statement of the problem

Poverty and unemployment are the twin problems faced by the developing countries.

According to the Planning Commission, more than one third of India’s total population live

below the poverty line. In India, the financial institutions have not been able to reach the poor

households particularly women in the unorganized sector. Structural rigidities and overheads

led to high cost in advancing small loans. People’s participation in credit delivery and

recovery and linking of formal credit institutions to borrowers through the SHGs have been

recognized as a supplementary mechanism for providing credit support to the rural poor. The

SHGs are informal groups formed on a voluntary basis, for providing the necessary support

to their members for their social and economic emancipation. These groups are distinct from

co-operative societies, mainly in terms of their size, homogeneity and functions. Non-

Governmental Organizations (NGOs) play an important role in preparing the members by

changing their attitude to participate in-group activities.

The National Bank for Agriculture and Rural Development (NABARD) is a pioneer

in conceptualizing and implementing the concept of the SHGs through the pilot project of

linking SHGs with banks. In 1992 the project was commenced throughout the country

through a set of well-defined guidelines with special reference to the objectives, criteria for

selection of SHGs, size of group, assessment of credit needs, rate of interest, repayment

period and security. Efforts were also made by NABARD to popularize the project among

bankers and the NGOs by organizing a series of workshops and seminars at different levels.

3

The response from banks and the NGOs was encouraging and positive. The

distinguishing feature of the SHGs is creating social and economic awareness among the

members. The social awareness enables the members to lead their life in a sound hygienic

environment and pursue a better living. The women members involve themselves more in

taking decisions regarding the education of their children, the investment of the family,

managing the economic assets of the family and bringing up cohesion among the members of

the family and others for a better living. Every member of the SHGs has felt the need for

more involvement in economic activities. The spirit for social and economic up liftmen of

members is the significant contribution of each and every SHG.

1.4 Objectives of the study

The broad objective is to examine the role and performance of SHGs in promoting

women’s empowerment in the study area. However, the study has some specific objectives.

They are

1. To analyze the profile and background of SHGs members.

2. To analyze the economic gains derived by the members after joining the SHGs.

3. To examine the social benefits derived by the members.

4. To analyze the operating system of SHGs for the mobilization of saving, delivery of

credit to the needy, the role of SHG to improving the living status of people.

5. To analyze the impact on income, expenditure and savings

6. To suggest appropriate policy intervention for the effective performance of SHGs.

4

CHAPTER – II

Review of Literature

Few studies are available related to women empowerment through SHG. It gives the

reviews of the past and present studies related to this topic as it is quite significant in nature

to understand the concepts.

Schuler Margres (1986) described three levels of empowerment to mobilize resources

to produce beneficial social change. First one is individual consciousness raising, the second

one is the development of collective consciousness and the third is to translate the collective

skills and resource in to political and legal action.

According to Bandura (1996), empowerment is the process of awareness and capacity

building, leading to a greater participation, greater decision making power and control of the

transformation action.

Zoe Oxaal (1997) stated that the concept of power is a root of the teem empowerment

that operates in different ways and at various levels. First is, power over that involves either a

relationship of domination or subordination and based in a socially sanctioned threats of

violence and intimation. It also invites active and passive resistance. The second is power to

that relates to the authority of decision-making, power to solve problems and can be creative

and inability. The third power with which involves bringing people together and organizing

them for a common purpose or common understanding to achieve collective goals. The fourth

is power with in that refers to self confidence, self awareness and assertiveness.

Karmakar (1999) has stated that a few NGOs had started the savings and the credit

programmes among the marine fishing folk through SHGs. He had found that the repayment

was 100 percent among women SHG and the choice of the SHG members was limited to

certain activities in the initial years because of the limited amount of credit available.

5

Empowerment, according to Beteille (1999) is both a means to an end and an end

itself. It is about radical social transformation of the ordinary and common people rather than

politician’s experts and other socially or culturally advantaged persons. He further stated that

empowerment and disempowerment go hand in hand: the empowerment of some sections of

society has to be accompanied by the disempowerment of other sections of it.

Vijayanthi (2000), in his study “Women’s empowerment through self help groups - A

participatory approach”, have made an attempt to study the decision making levels of

husband and wife in a family. She has measured the decision making power based on 31

items. These items have been grouped in to six factors.

• The factor one refers to decision making power related to education of children and

housing needs of the respondents.

• The second and third are closely related to decision making power on economic

aspects.

• The fourth factor has been decision making on persons affairs of the respondents.

• The fifth factor refers to items related to freedom to participate in community

activities.

• The sixth factor refers to the decision making of the women in the family affairs.

She concluded that the decision making has been high in factor -1 that is on freedom

to take decisions related to education of the children followed by taking decisions related to

family needs of the respondents. Decisions making related to personal affairs of the family

attending family functions and involvement in religious activities were taken by both husband

and wife.

Dahich (2001) in his paper “Banking with the poor -need for new savings linked loan

products” had examined the poverty incidence, financing for the poverty alleviation

6

programmes and micro credit. In his opinion segregating the small loans to form a separate

entity, banks would be able to reduce 89 percent of accounts by loosing only 12.9 percent of

their lending link as a result of reduction in their transactions costs.

Malaisamy and srinivasan R (2001) compared the micro finance performance of

SHGs and PACBs in Madurai district of Tamilnadu and found that majority of the PACBs

was willful defaulter which was not observed with SHGs. A comparison of over dues of

SHGs beneficiaries with those of cooperatives showed that the latter had a high level of over

dues compared to the former. The debt, asset ratio, educational level of the beneficiaries and

membership of SHGs have explained the variation in over dues. The transaction cost found to

be higher with SHGs due to higher interest rate as compared to cooperatives.

` Lakshmanan (2001) in his study in rural Tamilnadu observed that the saving of SHGs

increased from Rs 20 in the beginning to Rs 50. In the latest period the groups obtained

revolving fund; there is transparency in administration. Members are engaged in production

of mans with the sufficient encouragement and support of the husbands. The problem faced

by them includes high cost raw material. It was conclude that the SHG is really a boom,

which gives financial autonomy and make the participants economically independent.

Ponnarasi T and Saravanan M.P (2001) brought out case studies of five SHGs in

Guddalore district of Tamilnadu of the five groups, one has got the ‘Best SHG Award’ for it

has lent more than twice that of other groups, extended 90% of the loan for productive

purposes and also availed a large loan of Rs one lakh which was absent with other groups.

It was concluded that the SHGs have influenced greatly to the well being of the

villagers. Nedumaran S, Palanisami K, and Swami Nathan L.P(2001) in a study conducted in

Tamilnadu on the impact of SHGs found that more than 60% of the SHG members were

SC/STs. Nearly half of them registered high performance. The average loan availed is

7

positively associated with age. Net income received increased by 33% over pre SHG

situations. Social conditions also have improved and SHGs have contributed for the overall

improvement.

Srinivassan G, Varadharaj S, and Chandra Kumar M(2001) in their study on financial

performance of rural and urban SHGs in Coimbatore district of Tamilnadu with 50 SHGs in

terms of recovery index (ratio of total recovery to total lending ) thrift credit ratio (ratio of

total saving to total lending) and outstanding credit ratio (ratio of outstanding tototal lending )

revealed that the average membership was 17 , the average savings were Rs 16,333 and the

average total lending was Rs 17,537 and the average of defaults (Rs 956) were found to be

higher in rural SHGs than in urban SHGSs. Due to higher defaults , the rural SHGs showed

lower recovery index (80%) and higher average thrift credit ratio (0.14%) than the urban

SHGs (87% and 0.09 respectively) The average thrift credit ratioof urban SHGs (0.91) was

lower than the rural SHGs (0.93), implying that the overall financial performance of the

urban SHGs was better than that of the rural SHGs.

Manimekalai N and Rajeswari G (2001) studied the impact of SHG in creating

women entrepreneurship in rural areas of Tamilnaduby taking 150 SHG members. They

found that the SHGs have helped to initiate micro enterprises including farm and nonfarm

activities, trading and service units. It was reported that there was significant difference in the

mean performance of the entrepreneurs based on their age, education andprevious 50

experiences.

Kapur (2001) in her study tried to discuss, analyze and answer the

challengingquestions as to why despite all the efforts and progress made, still there continues

to be so much of gender discrimination and what strategies, actions and measures to be

undertaken to achieve the expected goal of empowerment. She opined that women’s

empowerment is much more likely to be achieved if women have total control over their own

8

organizations, which they can sustain both financially and managerially without direct

dependence on others.

A study conducted by NABARD (2002) covering 560 households from 223 SHGs

in11 states of India elucidated that there has been a positive result in enhancing the standard

of living of SHG members in case of asset ownership savings and borrowing capacityincome

generating activity and income levels. The average value of asset including livestock and

consumer durable has increased considerably the housing condition of the people is improved

from the mud walls to thatched roofs to brick walls and tiled roofs.

Almost all members developed saving habit in the past SHG. The trend of

consumption loans come down in contrast the loan for income generating purpose has

increased considerably during the pre-SHG period. Similarly the overall repayment of loans

improved and the average net income per household has increased about 33%. The

employment increased by 18% between the pre and the past SHG conditions. It should be

noted that after association with the SHGs they have improved their self confidence, self

worth and communication. In addition to this, they involved in addressing various social evils

and problems of the society.

Jothy K and Sunder J (2002) in their study of evaluating the programme of Tamilnadu

MahalirThittam Found that SHG women are currently involved in economic activities such as

production and marketing of agarbathis, candle and soap, readymade garments,pickles,

appalam, vathal, furtoys, bags, palm leaf products dhotis, herbal products, fancysea shell etc.

In addition the SHG women monitor the normal functioning of the ration shops, maintain

vigil to prevent brewing of illicit group, help the aged, deserted and windows to obtain loan.

For Narayanareddy (2002) empowerment is the process of enabling people,Especially

women to acquire and possess power resources to make decisions on their own or resist

9

decision that are made by others, which affect them. In this process, women should be

actively involved and act as agents of change Punithavathypandian and Eswaran (2002)

“Empowerment of women through Micro credit”have examined the saving patterns and

capacity building of the sample respondents through micro-credit.

They have also analyzed the impact of Micro credit on the economic and social

empowerment of women in sedapatti block in Madurai district. Women’s own income has

increased significantly through Micro credit provided has been micro in nature it has bought

in micro changes in the lives of women who received credit in terms of increase in income,

saving pattern and capacity building.

Ritu Jain et al (2003) has examined the functioning of self help groups in Kanpur

Dehat District. For the study, 25 women self help groups were selected ten women members

from the same village were selected as respondents, to study the impact of self help groups on

their socioeconomic status.

Pattanaik (2003) in her study reveals that SHGs are continuously striving for a better

future for tribal women as participants, decision makers and beneficiaries in the domestic,

economic, social and cultural spheres of life. But due to certain constraints like gender

inequality, exploitation, women torture for which various Self Help Groups is not organized

properly and effectively.

Malhotra (2004) in her book has examined how women entrepreneurs affect the

global economy, why women start business, how women’s business associations promote

entrepreneurs, and to what extent women contribute to international trade. It explores

potential of micro-finance programmes for empowering and employing women and also

discusses the opportunities and challenges of using micro-finance to tackle the feminization

of poverty. According to her, the micro-finance programmes are aimed to increase women’s

10

income levels and control over income leading to greater levels of economic independence,

they enable women’s access to networks and markets, access to information and possibilities

for development of other social and political role.

They also enhance perceptions of women’s contribution to household income and

family welfare, increasing women’s participation in household decisions about expenditure

and other issues leading to greater expenditure on women’s welfare.

Manimekalai (2004) in his article commented that to run the income generating

activities successfully the SHGs must get the help of NGOs. The bank officials should

counsel and guide the women in selecting and implementing profitable income generating

activities. He remarked that the formation of SHGs have boosted the self-image and

confidence of rural women.

Purushothaman (2004) reported that Micro credit intervention benefited many women

entrepreneurs. He observed these benefits in terms of women shifting from wage to self

employment, increased income, repayment of old debts, purchase of personal jewellery,

sending of girl children to school.

Mahendra Varman’s(2005) paper on “Impact of self help groups on formal banking

habits ” focused with the twin objectives of examing the association between the growth of

SHGs and the increase in female bank deposit accounts and the influence of SHGs in their

account holding on formal banks.

Sahu and Tripathy (2005) in their edited book views that 70 percent of world’s poor

are women. Access to poor to banking services is important not only for poverty alleviation

but also for optimizing their contribution to the growth of regional as well as the national

economy. Self Help Groups (SHGs) have emerged as the most vital instrument in the process

of participatory development and women empowerment. The rural women are the

11

marginalized groups in the society because of socio-economic constraints. They remain

backward and lower position of the social hierarchical ladder. They can lift themselves from

the morass of poverty and stagnation through microfinance and formation of Self-Help

Groups.

Venkatachalam G, Vijayarani K (2009) the concept of the SHGs can also be extended

to service sector which is increasing many folds in Tamilnadu. Never ideas to promote the

concept of the SHGs among rural poor, middle income group, development and expansion of

SHGs activities many fold will give very good results to the state economy.

12

CHAPTER – III

Methodology and Profile of the study area

3.1 Methodology

The information for the study was collected from respondents using a questionnaire

insurvey method. They are selected by the method of SRS method in the manner that

theyspread over the study area Thanjavur district.

The sampled subject (Respondents) was interviewed with a questionnaire

whichconsisting of 45 items. Among these items the first 12 items are about the demographic

ofthe subjects like age, community, Religion, marital status, Type of family, Type of

house,Number of family members, Number of Children, Education and Occupation.

Theremaining 33 items are in the form of questions. The respondent’s are given with

variousoptions in are exhaustive manner. So as to enable them to respond to all the questions.

The questions are constructed to study the following variables: economic

status,awareness of team working , leadership quality, the literacy level, health status,

socialawareness, role of SHGs to improving the living status of people, role of SHGs

inproviding rural credit etc..

In general, all these variables are relevant to study the women empowerment

throughSHGs. The changes in the level of these variables will influence the changes in

thewomen empowerment. The value of each variable is observed from the responses given

toone of more questions. To each respondent, the value of each variable is computed as

theaverage of the scores assigned to the responses of the questions concerned.

At first, the variables are studied individually by the corresponding

descriptivestatistics including central and dispersion measures. This will enable to understand

thesignificance of the variables under study.

13

The study was carried out in selective clusters spread over six blocks of Thanjavur

district in Tamilnadu. In total, this study covers 14 SHGs. This study isbased on primary and

secondary data. The validity of any research is based on thesystematic method of data

collection and analysis. The primary data was collected from100 sample respondents from six

blocks in Thanjavur district. Forcollecting the first hand information from the SHG members,

100 of them were chosen bysimple random sampling method.

This project is mainly based on primary data. Questionnaire was the main tool usedto

collect the pertinent data from the selected sample respondents. For their purpose, a well

structured questionnaire was framed.

The application of statistical tools in the study is necessitated to check the

validity,independence, correlation, variation and consistency of the data. The sampling

techniqueis random sampling SHGs are randomly selected from Thanjavur district spread

over all the villages, panchayaths, and municipalities. The collected data are analyzedwith

the aid of Statistical Package for the Social Sciences (SPSS). Group members aretold that the

information collected would be used for research purposes only and than either the bank nor

the NGO would have access to individual data.

In order to gain through understanding of the structure, functions and performance

ofSHGs, the researcher visited various parts and blocks of Thanjavur district and conducted a

pre test before finalizing the interview schedule.

The information was collected during the weakly meetings of SHGs, training

sessionsand other gathering of SHG members. In some instants, data was collected from

thehomes of respondents.

14

3.2 Profile of the study area - Thanjavur district

Thanjavur district is in the east coast of Tamil Nadu. The district lies between 78O

45’ and 70O 25' of the Eastern longitudes and 9O 50' and 11O 25' of the Northern Latitudes.

The District is bound by Coloroon on the North which separates it from Ariyalur and

Tiruchirapalli district; Thiruvarur and Nagapattinam districts on the east; Palk Strait and

Pudukottai on the South and Pudukottai and Tiruchirapalli on the West.

The area of the district is 3396.57Sq.Km. It consists of nine Taluks-

Thiruvidaimarudur, Kumbakonam, Papanasam, Pattukottai, Peravurani, Orathanadu,

Thanjavur, Thiruvaiyaru and Budalur. The district headquarters is Thanjavur. Thanjavur

district is called ‘the Rice Bowl of Tamil Nadu’ because of its agricultural activities in the

delta region of river Cauvery. The temples, culture and architecture of Thanjavur are famous

throughout the world. It is an historical place ruled by Chola, Pandya, Nayak, Marathas and

was under British rule till Independence. The pursuits of these rulers are reflected in the great

monuments like Grand Anaicut, Big Temple and Serfoji Palace and Saraswathi Mahal

Library, etc. in the district.

Population of the district is 2405 thousand numbers as per Census 2011.The

population density is 708 persons per sq.km. The district is 35% urbanized and constitutes

literacy rate of 82.72%.

15

CHAPTER – IV

Analysis and Interpretations

The appropriate statistical tools have been used such as simple average, percentage,

standard deviation, correlation coefficient, paired t-test, ANOVA, χ2 - test, multiple

regression model, factor analysis and Garrett’s ranking principal and other relevant statistical

tests.

The descriptive analysis of the profile is done in the first and the inferential analysis

of multivariate impact of women empowerment through SHGs is done in the later part of this

analysis and interpretations. The broad categories of analysis of women empowerment

through SHGs discussed through chi-square test, paired t-test, regression model, factor

analysis and Garrett’s ranking principles. It is supported by interpretations and brief

explanation for better understanding of the results and observations .The brief explanations

are provide on the basis of feedback provided by the SHG members while responding to the

uestions in the interview schedule. The feedback provides the clarity and the reasons for

preferring particular option in the interview schedule. Thus, it helps to provide the essence of

impact of SHG membership.

The different kinds of statistical tools are of the great help in analyzing and

establishing the related variables. The variables are measured both on isolated and group

basis. The relevant variables are grouper together using factor analysis. Then, the dominating

variable in each factor is identified as key variable. The descriptive analysis of the sample is

done and inferential analysis using appropriate statistical tools is also done in this section.

16

4.1 Descriptive Analysis of profile of SHG members

Age

frequency %<25 4 426 - 30 8 831 - 40 46 4641 - 50 30 3051 - 60 10 1061 - 70 2 2Total 100 100

It is seen from Age frequency table, that 46% of the respondents belong to the age

group 31-40 years. It reveals that the age group 31-40 years population is more inclined

and willing to embrace SHG for their benefits.

Community

frequency %OC 8 8BC / MBC 58 58SC 26 26ST 8 8

100 100

05

101520253035404550

<25 26 - 30 31 - 40 41 - 50 51 - 60 61 - 70

17

It is reported from community frequency table that 58% of the respondents belong to

BC/ MBC category, 26% of the respondents belong to SCcategory, 8% of the respondents

belong to ST category. Majority of the SHG members belong to backward section of the

society. They are over who look up to the government desperately for some help.

Religion

frequency %Hindu 76 76muslim 4 4Christian 20 20others 0 0

100 100

0

10

20

30

40

50

60

OC BC / MBC SC ST

0

50

100

Hindumuslim

Christianothers

18

Religion wise distribution of respondents output shows the majority 76% of the

members belong to the Hindu followed by 20% of them are Christian whereas 4% of the

members were Muslim. Thus, it is inferred that most of the members in the SHGs are the

Hindus.

Education

Frequency %literate 6 6primary 32 32secondary 24 24Intermediate 32 32Degree & Above 6 6

100 100

It is observed that, 32% people have primary level education, 24% people have higher

secondary level education, 6% people have degree and above.

So, it is conclude that the people who have primary level education they are having

more interest to join the SHG and expecting some facilities or help from the SHGs.

0

5

10

15

20

25

30

35

40

45

Less than5000

5001 -10000

10001 -15000

15001 -20000

20001 -25000

19

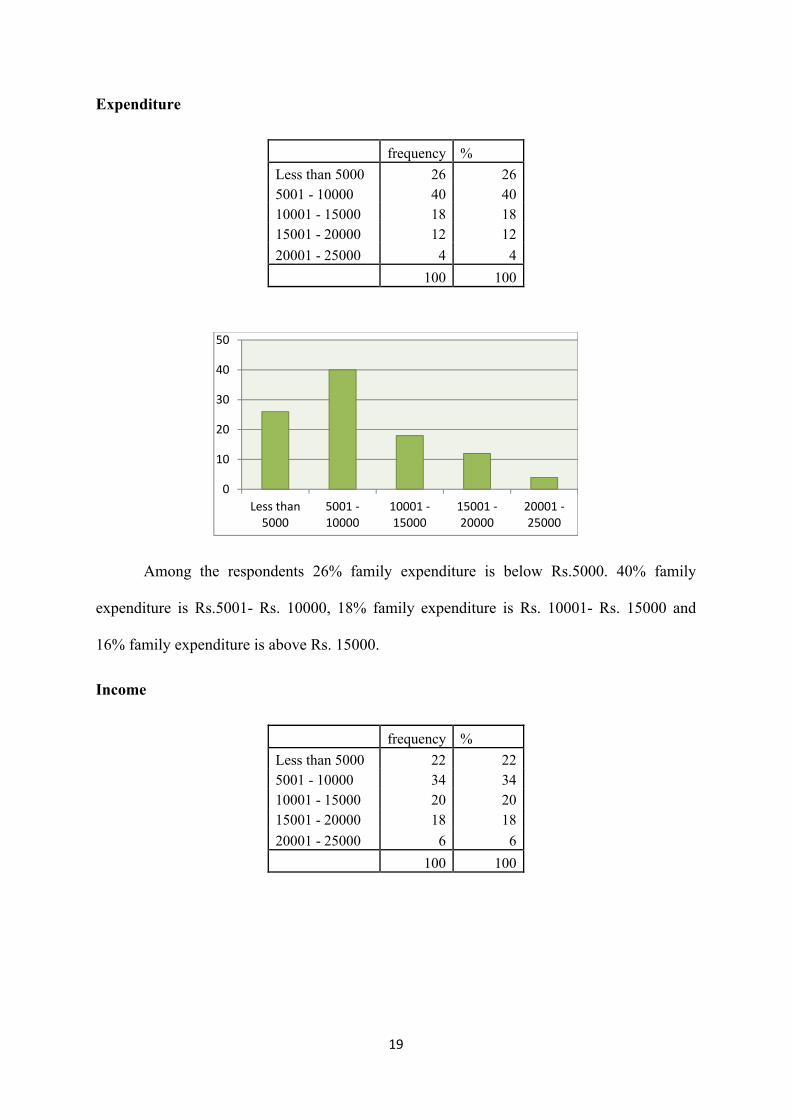

Expenditure

frequency %

Less than 5000 26 265001 - 10000 40 4010001 - 15000 18 1815001 - 20000 12 12

20001 - 25000 4 4

100 100

Among the respondents 26% family expenditure is below Rs.5000. 40% family

expenditure is Rs.5001- Rs. 10000, 18% family expenditure is Rs. 10001- Rs. 15000 and

16% family expenditure is above Rs. 15000.

Income

frequency %

Less than 5000 22 225001 - 10000 34 3410001 - 15000 20 2015001 - 20000 18 18

20001 - 25000 6 6

100 100

0

10

20

30

40

50

Less than5000

5001 -10000

10001 -15000

15001 -20000

20001 -25000

20

Among the respondents 22% family income is below Rs.5000. 34% family income is

Rs.5001- Rs. 10000, 20% family income is Rs. 10001- Rs. 15000 and 18% family income is

Rs. 15001 – 20000, 6% family income is Rs.20001 – 25000.

4.2 Inferential Analysis on women empowerment

4.2.1 Chi-square (χ2) test

The chi-square test can be used to test for the discrepancy between the observed and

expected number of cases in the data. Also it is used to test for independence of attributes.

Consider the cross tabulation of some characteristic across two categorical variables.

The resulting table is called a two-way frequency table as a contingency table. One

characteristic of an attribute is shown along the rows and other is shown along the columns.

Each cell of the table gives the count of the number of cases corresponding to that cell.

Testing the Independence of attributes

Age

The relationship between Age and other variables like number of members in the

group, group size, who suggested joining the SHG, income or savings of group, any

achievement of group, how did you know about SHG, poverty is the reason, unemployment

is the reason, for emergency needs, for loan, main function of SHG, any participation in the

local government, feel happy after joining SHG are analyzed using χ2 test.

Less than 5000

5001 - 10000

10001 - 15000

15001 - 20000

20001 - 25000

21

H0: There is no dependency between age and any other variable (listed above).

H1: There is dependency between age and any other variable (listed above).

Age – Chi-square Test

Variable Chi-square value Degrees of freedom p- value

Religion 69.912 44 .008

Community 115.472 66 .0001

Educational Status

193.507 88 .0001

Income 664.476 308 .0001

Expenditure 797.472 462 .0001

If the p-value is less than 0.05, then the chance for the wrong rejection of null

hypothesis is zero. Therefore, we may reject H0. Hence we conclude that there is dependency

between age and Religion, Community, Educational Status, Income, Expenditure.

Community

The relationship between Community and other variables like number of members in

the group, group size, who suggested joining the SHG, income or savings of group, any

achievement of group, how did you know about SHG, poverty is the reason, unemployment

is the reason, for emergency needs, for loan, main function of SHG, any participation in the

local government, feel happy after joining SHG are analyzed using χ2 test.

H0: There is no dependency between age and any other variable (listed above).

H1: There is dependency between age and any other variable (listed above).

22

Community – Chi-square Test

VariableChi-square

valueDegrees of freedom p- value

Age 115.472 66 .0002

Religion 5.442 6 .489

Educational Status 44.644 12 .0003

Income 89.841 42 .0002

Expenditure 123.537 63 .0003

If the p-value is less than 0.05, then the chance for the wrong rejection of null

hypothesis is zero. Therefore, we may reject H0. Hence we conclude that there is dependency

between Community and Age, Educational Status, Income, Expenditure.

Also, there is a chance for no dependency between Community and Religion.

Religion

The relationship between Religion and other variables like number of members in the

group, group size, who suggested joining the SHG, income or savings of group, any

achievement of group, how did you know about SHG, poverty is the reason, unemployment

is the reason, for emergency needs, for loan, main function of SHG, any participation in the

local government, feel happy after joining SHG are analyzed using χ2 test.

H0: There is no dependency between age and any other variable (listed above).

H1: There is dependency between age and any other variable (listed above).

23

Religion – Chi-square Test

Variable Chi-square value Degrees of freedomp- value

Age 69.912 44 .0080

Community 5.442 6 .4890

Educational Status

24.737 8 .0020

Income 51.536 28 .0040

Expenditure 155.188 42 .0003

If the p-value is less than 0.05, then the chance for the wrong rejection of null

hypothesis is zero. Therefore, we may reject H0. Hence we conclude that there is dependency

between Religion and Age, Educational Status, Income, Expenditure.

Also, there is a chance for no dependency between Religion and Community.

24

CHAPTER - V

Findings of the study and Conclusions

5.1 Findings of the study

The following are the major findings of the study:

∑ Most of the women of the SHGs in the study area were belonged to the age group 31-

40 years

∑ The majority of the respondents are Hindus in Thanjavur district. It is a Hindu

dominated area. The other religions which have their presence are Christian and

Muslims.

∑ The economic activities and life style vary to an extent based on the religion and the

community they belong to.

∑ Majority of the SHG members in Thanjavur district belong to backward section of the

society.

∑ Most of the SHG members of the family earning isRs. 5000 to Rs. 10,000.

∑ Most of the family of SHG members, regarding income, expenditure and savings

levels is not poor.

∑ There is a chance for no dependency between religion and other factors like number

of members in the group, group size, who suggested joining the SHG, income, any

achievement of group, poverty, unemployment, emergency needs,for loan, etc.

∑ The majority of the SHG members have little or no education. It reflects the hard

reality of literacy level in the area under study. The literacy rate certainly needs

improvement. The lack of education could be one of the important reasons for being

hit by the poverty.

25

5.2 Suggestions

Considering the findings of the study, the following suggestions were prescribed.

• Literacy and numeric training is needed for the poor women to benefit from SHG.

• The members of the SHG should be more active, enthusiastic and dynamic to

mobilize their savings by group actions. In their process, NGOs should act as a

facilitator and motivator.

• Meetings and seminars may be organized where the members will get a chance to

exchange their views and be able to develop their group strength by interactions.

• Income generating activities should be increased.

• Communication and leadership skills should be given much importance to improve

the personality development and group discussion skills.

• SHG members are properly trained and informed before their venture.

• Monitoring should be to make sure that people are on the path charted out and the

members have the capacity to take the next step.

• Potential members of old groups can be taken to visit the new groups to clarify

various aspects of SHG functioning.

• Able leaders from a few groups can be motivated resolution responsibilities.

• All the members in SHGs may not have the same caliber and expertise. The

inefficiency members of the groups should be identified and can impart training to

them in order to make them competent.

• Frequent awareness camps can be organized to create the awareness about the

different schemes of assistance available to the participants in the SHGs.

26

5.3 Conclusions

Women’s Empowerment has become a significant component of human development

in India. The last decades have witnessed significant changes in the status and role of women

in our society. There has been shift in policy approaches from the concept of welfare in the

seventies to development in the eighties and now to empowerment in the current scenario. In

a nutshell, SHGs help the members are able to improve the socio-economic conditions,

standard of living, women literacy level, decision making, participation of social awareness

programs, participation of training programs, participation of political activities, offer

employment opportunities to neighbors etc.

The study has revealed that SHG is an important tool which helps the rural women to

acquire power for their self supportive life and nation building efforts. The empowerment of

women through SHGs would lead benefits not only to the individual women but also for the

family and community as whole through collection action for development these SHGs.

Empowering women is not just for meeting their economic needs but also more holistic social

development. The SHGs empower women and train them to take active part in socio-

economic progress of the nation. Pandit Jawaharlal Nehru said, “To awaken the people, it is

women who must be awakened; once she is on the move, the family moves, the village

moves and nation moves.”

Now the women are awakened by the SHGs. SHGs have undoubtedly begun to make

a significant contribution in poverty alleviation and empowerment of poor, especially women

in the areas of Thanjavur.

The present study is an attempt to analyses the socio-economic development of

members and the performance of SHGs in Thanjavur district. The performance of SHGs was

good. The greater percentage of women were impacted positively by being members of

27

SHGs. Women’s participation in SHGs enabled them to discover inner strength, gain self

confidence, social, economical, political and psychological empowerment and capacity

building. So, women empowerment has increased slightly through SHGs. Based on the

analysis of statistical modeling, we conclude that women empowerment has achieved a new

dimension through SHGs.

28

BIBLIOGRAPHY

1. 1.Schuler M.A. (1986), Women, Law and Development: An Exploration of Legal

Educational and Organizational Strategies to raise the status of Law-Income Third

World Women, Dissertation: George Washington university, Washington, D. C.

pp.253.

2. 2.Bandura, A. (1996), Social Foundation of Thought, Prentice Hall, England Cliffs,

New Jersey, pp.81-85.

3. 3.Zoeoxaal (1997), Gender and Empowerment, Institute of Development Studies,

Sally Baden Publisher.

4. 4.Karmakar, K.G. (1999), Rural Credit and Self Help Groups-Micro Finance needs

and concepts in India, Sage Publications India Pvt. Ltd., New Delhi, pp. 1-39.

5. 5.Beteille (1999), Empowerment, Economic and Political Weekly, Vol.34, No. 10/11

Mar. 6-19, pp.589-597.

6. Mayoux, Linda (2000), Sustainable learning for women's empowerment: Way

forward in microfinance, New Delhi.

7. Vijayanthi, K.N. (2000), Women Empowerment through Self Help Groups-A

participatory Approach, Social Change, Vol.30, No.3-4, September-December, pp.64-

87.

8. Dahich, C.L. (2001), Banking with the poor need for new savings linked loan

products, Urban Credit journal of NAFCUB, Vol. XXIII, No.1, March, pp.5-15.

9. Kabeer, N. (2001), “Resources Agency Achievements: Reflections on the

Measurement of Women’s Empowerment – Theory and Practice”, SIDA Studies, No.

3.

10. Kapoor, Pramilla (2001), Empowering the Indian Women, Publications Division,

Ministry of Information and Broadcasting, Government of India.

29

11. Malaisamy, A. and Srinivasan, R. (2001), An position of Self-Help Group and PACP

Beneficiaries in Madurai District of TamilNadu, Indian Journal of Agriculture

Economic”, Vol.56, No.3, July-September, pp.489.

12. Lakshmanan, S. (2001), Working of Self-Help Groups with particular reference to

mallipalayam Self-Help Group, Gobichettipalayam Block, Erode District, TamilNadu,

Indian Journal of Agriculture Economics, Vol.56, No.3, July-September,pp.457

13. Ponnarasi, T. and Saravanan, M.P. (2001), Comparative study on performance of

Self- Help Groups-a case with agaranallur village in cuddalore District, TamilNadu,

Indian Journal of Agriculture Economic, Vol.56, No.3, July-september, pp.469.

14. Nedumaran, S. Palanisami, K. and Swaminathan, L.P. (2001), Performance and

impact of Self-Help Groups in TamilNadu, Indian Journal of Agriculture Economic,

Vol.56, No.3, July-September, pp.471.

15. Manimekalai, N. and Rajeswari (2001), Nature and performance of Informed Self-

Help Groups-a case from TamilNadu, Indian Journal of Agriculture Economic,

Vol.56, No.3, July-September, pp.453.

16. Srinivasan, G., Varadharaj, S. and Chandrakumar, M. (2001), Financial Performance

of rural and Urban Self-Help Groups-A Comparative Analysis, Indian Journal of

Agriculture Economic, Vol.56, No.3, July-September, pp.478.

17. NABARD (2003), Progress of SHG-Bank Linkage in India: 2002-2003,

www.nabard.org.

18. Jothy, K. and Sunder, I. (2002), Self-Help Groups under the Women’s development

programme in TamilNadu: Achicevements, bottlenecks and recommendations, Social

Change, Vol.32, No.3 & 4, September-December, pp.195-204.

30

19. Narayana Reddy, G. (2002), Empowering Women through Self-Help Groups and

Micro Credit: The case of NIRD Action Research Projects, Journal of Rural

Development, Vol.21 (4), pp.511-535.

20. Pattanaik, Sunanda, “Smaranika, 2003”, Empowerment through SHG: A Case Study

of Gajapati District.

21. Ritu Jain, R.K., Kusha and Srivastava, A.K. (2003) Socio, Economic Impact through

SHGs, Yojana, Vol.47, No.7, July, pp.11-12.

22. Malhotra, Meenakshi (2004), Empowerment of Women, Isha Books, Delhi.

23. Manimekalai, K. (2004), “Economic Empowerment of Women Through Self-Help

Groups”, Third Concept, February.

24. Purushothaman, P. (2004), Marketing Support to the SHGs, Kurushetra, February

2004.

25. Mahendra Varman, P. (2005), Impact of Self Help Groups on formal banking habits,

Economic and Political Weekly, April 23, pp.1705.

26. Sahu and Tripathy (2005), Self-Help Groups and Women Empowerment, Anmol

Publications Pvt. Ltd., New Delhi.

27. Venkatachalam, G. and Vijayarani, K. (2009), Poverty Alleviation through Self Help

Groups, TamilNadu Journal of Co-operation, Vol:9, No.3, pp.16.

31

APPENDIX – QUESTIONNAIRE

A STATISTICAL MODELING ON WOMEN EMPOWERMENT OF

SELF HELP GROUPS

Questionnaire

District Name: Village Name:

Name of the Respondent:

Name of the SHG: Date of SHG Formation:

Part-I

Socio –Economic Status of women

1. Age

2. Religion: 1) Hindu (2) Muslim (3) Christian (4) Others

3. Caste category: (1). OC (2). BC/MBC (3) SC (4) ST

4. What is your level of literacy?

(1) Illiterate (2) Primary (3) Secondary (4) Intermediate (5) Degree and above

5. What is your marital status?

(1)Married, (2). Unmarried(3). Divorced (4). Widowed(5) Separated.

6. What is your Household size : ___________(no’s)

7. Family Particulars

Sl.No

NameRelationship

with headSex

Age (years)

Education Occupation

A

B

C

D

32

8. Are you living in own house? (1). Yes (2). No

9. What is the type of your house?

1). RCC, (2). Tiled, (3). Thatched.

10. What is your occupation?_________________

11. Do you have own land? (if Yes) How many acres of land you have?______

12. What is your monthly income? Rs.__________

13. What is your monthly expenditure? Rs.__________

PART-II

Intervention of SHG in the lives of an Individual woman

14. What is your group size?

15. Since how long you are the member of the group?

16. Who motivated you to join Self Help Groups? 1)Government 2) NGO, 3) Others

17. What are the reasons for joining SHGs?

1) ____________ 2) ____________3)______________ 4)______________

18. Did you get trainings after joining SHGs? (1). Yes (2). No.

19. Have you know the rules and bye-laws of your SHG? (1). Yes (2). No

20. Who take decisions on day to day functioning of your group?

1) Animator & Representatives only 2) All the members with A&R

21. Are you satisfied with the functioning of your Group? (1). Yes (2). No

22. If you are satisfied, what is the satisfaction level over the functioning of your SHG?

(1). Good, (2). Very Good, (3). Satisfactory (4). Bad.

23. How much is your monthly savings amount Rs_____/month, Total Rs.__________

24. Have you taken any internal loan from your Group?

If Yes, Amount, Rs.____________

33

25. What is the system of loan repayment period followed in your SHG?

(1). Monthly (2). Weekly (3). Fortnightly (4) Flexible

26. What is the status of repayment? 1) Fully Repaid (2). Being Repaid.

27. Is your SHG loan amount is adequate for your needs? (1). Yes (2). No.

28. What are the other sources of credit you are accessed now?

(1) SHG internal lending scheme (2) Bank Loan (3) Micro Finance Loans

(4)Government Scheme Loan

29. Which of these loan is easily accessible for your credit need?

(1) SHG internal lending scheme (2) Bank Loan (3) Micro Finance Loans

4)Government Schemes Loan.

Part-III

Woman Empowerment

30. What is your opinion on woman empowerment through SHG intervention?

Sl.No

Empowerment Measures

Before joining SHG

(Yes/No)

After joining SHG

(Yes/No)

Ranking of Empowerment

level (1,2,3,4,5)*

A Monthly income increasedB Monthly savings increasedC Self-confidence level increasedD Concentration on Child Education,

Health and Hygiene increasedE Control over the Expenditure of the

Family increasedF Credit/ Loan facilities accessibility

increasedG High interest rate loans decreased H Loan Repayment capacity through

income generating activities

I Self-Awareness level increasedJ Social status gainedK Decision making power gained L Participation in social activities

34

M Knowledge on banking procedure * (1- Good 2, Very Good 3, Better 4, Best, 5, Excellent)

31. Did you learn any new skills after joining SHGs?(1). Yes (2). No.

32. What is your opinion on the attitude of the banks towards SHGs?

(1). Negative (2).Positive

33. Did you face any difficulties at the time of getting Bank loans? (1). Yes (2). No

34. Is there any delay in sanctioning of loan by banks?(1). Yes (2). No

35. Is there any issues you faced with your family while functioning with the SHG?

(1). Yes (2). No

36. Have you received any Government scheme or assistance through SHG?

(1). Yes (2). No

37. What are your suggestions to improve the functioning of the SHGs?