a review of: global soft magnetic core shipments & nickel commodity prices spring-2009 tta...

TRANSCRIPT

A Review ofA Review of::

Global Soft Magnetic Core ShipmentsGlobal Soft Magnetic Core Shipments& Nickel Commodity Prices& Nickel Commodity Prices

A Review ofA Review of::

Global Soft Magnetic Core ShipmentsGlobal Soft Magnetic Core Shipments& Nickel Commodity Prices& Nickel Commodity Prices

Spring-2009 TTA MeetingsSpring-2009 TTA Meetings

May 14, 2009May 14, 2009

Spring-2009 TTA MeetingsSpring-2009 TTA Meetings

May 14, 2009May 14, 2009

Presented by theStaff of the

International Magnetics Association

TopicsTopics TopicsTopics

• Overview of Soft Magnetics IndustryOverview of Soft Magnetics Industry

• Ferrite PerformanceFerrite Performance

• Powder Core PerformancePowder Core Performance

• Nickel Commodity Price ImpactNickel Commodity Price Impact

• Challenges for 2009Challenges for 2009

• Overview of Soft Magnetics IndustryOverview of Soft Magnetics Industry

• Ferrite PerformanceFerrite Performance

• Powder Core PerformancePowder Core Performance

• Nickel Commodity Price ImpactNickel Commodity Price Impact

• Challenges for 2009Challenges for 2009

Soft Magnetic CoresSoft Magnetic CoresSoft Magnetic CoresSoft Magnetic Cores

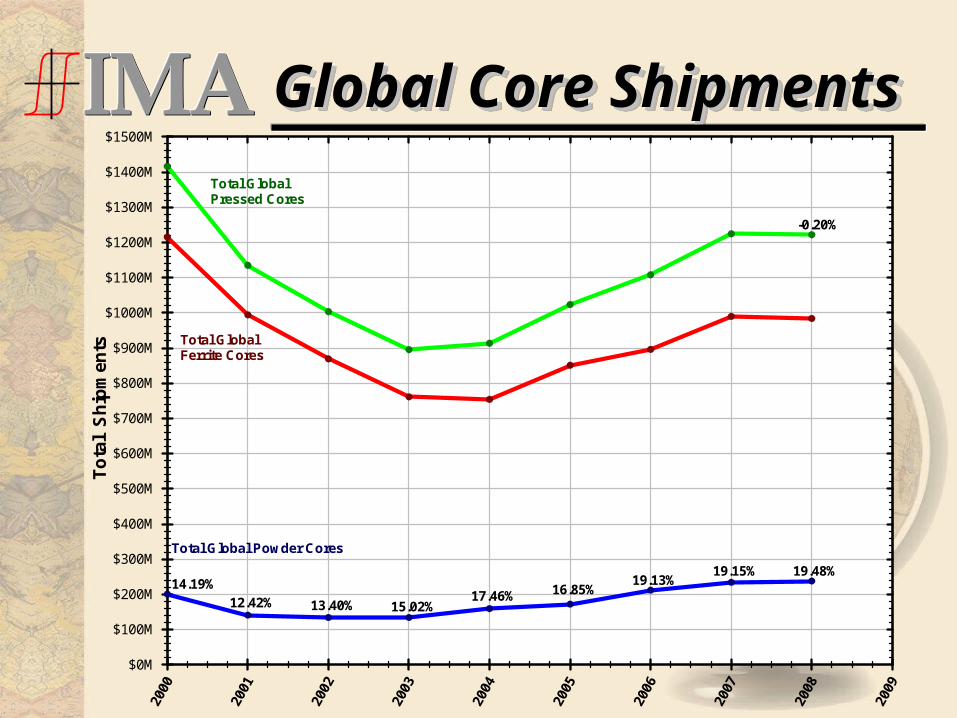

• Ferrites include MnZn and NiZn cores:Ferrites include MnZn and NiZn cores:– 2008 at -0.6% under 2007 (forecast was +5.5%).2008 at -0.6% under 2007 (forecast was +5.5%).

◦ 08Q1 & Q2 +15% to +30%; 08Q3 & Q4 -20% to -30%.08Q1 & Q2 +15% to +30%; 08Q3 & Q4 -20% to -30%.

– 2009 forecast is for -15% to -30% (09Q1 -30 to -40%).2009 forecast is for -15% to -30% (09Q1 -30 to -40%).

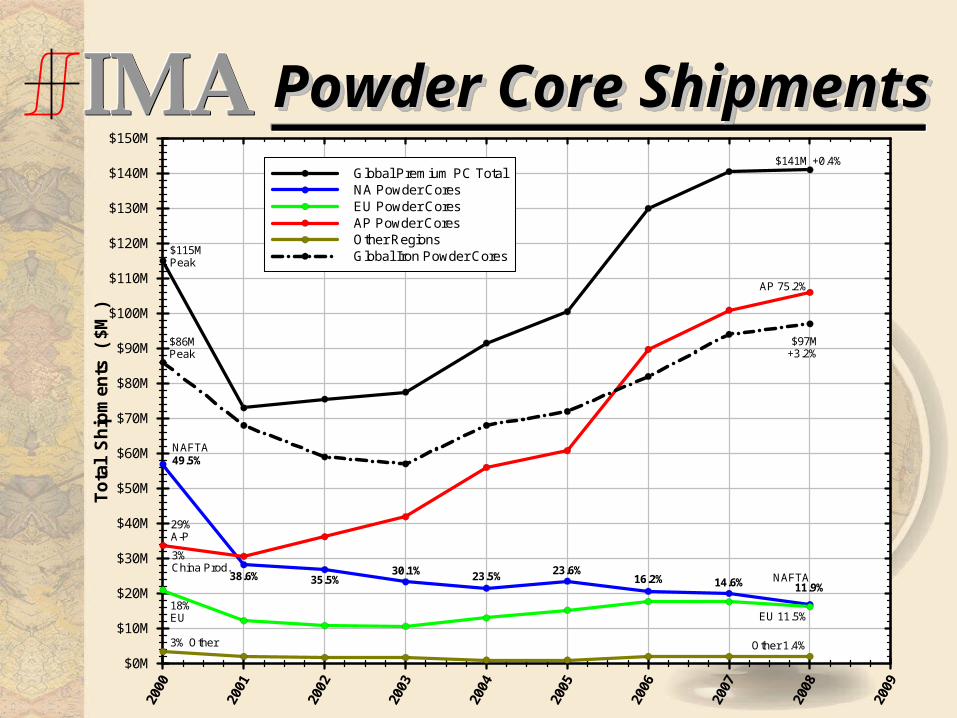

• Powder Cores have two segments:Powder Cores have two segments:– 2008 Premium Cores at +0.4% over 2007 (fcst. +8%).2008 Premium Cores at +0.4% over 2007 (fcst. +8%).

◦ 2009 forecasts are for a decline of -10%.2009 forecasts are for a decline of -10%.

– 2008 Iron Powder at +3.2% over 2007 (fcst. +7%).2008 Iron Powder at +3.2% over 2007 (fcst. +7%).◦ 2009 forecast not certain, typically not as volatile as Prem. 2009 forecast not certain, typically not as volatile as Prem.

PC.PC.

• Powder core industry still adding capacity.Powder core industry still adding capacity.– Will pose bottom line challenges in 2009.Will pose bottom line challenges in 2009.

• Ferrites include MnZn and NiZn cores:Ferrites include MnZn and NiZn cores:– 2008 at -0.6% under 2007 (forecast was +5.5%).2008 at -0.6% under 2007 (forecast was +5.5%).

◦ 08Q1 & Q2 +15% to +30%; 08Q3 & Q4 -20% to -30%.08Q1 & Q2 +15% to +30%; 08Q3 & Q4 -20% to -30%.

– 2009 forecast is for -15% to -30% (09Q1 -30 to -40%).2009 forecast is for -15% to -30% (09Q1 -30 to -40%).

• Powder Cores have two segments:Powder Cores have two segments:– 2008 Premium Cores at +0.4% over 2007 (fcst. +8%).2008 Premium Cores at +0.4% over 2007 (fcst. +8%).

◦ 2009 forecasts are for a decline of -10%.2009 forecasts are for a decline of -10%.

– 2008 Iron Powder at +3.2% over 2007 (fcst. +7%).2008 Iron Powder at +3.2% over 2007 (fcst. +7%).◦ 2009 forecast not certain, typically not as volatile as Prem. 2009 forecast not certain, typically not as volatile as Prem.

PC.PC.

• Powder core industry still adding capacity.Powder core industry still adding capacity.– Will pose bottom line challenges in 2009.Will pose bottom line challenges in 2009.

Global Core ShipmentsGlobal Core ShipmentsGlobal Core ShipmentsGlobal Core Shipments20

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

To

tal

Sh

ipm

ents

$0M

$100M

$200M

$300M

$400M

$500M

$600M

$700M

$800M

$900M

$1000M

$1100M

$1200M

$1300M

$1400M

$1500M

14.19%12.42% 13.40% 15.02%

17.46% 16.85%19.13%

Total Global Powder Cores

Total GlobalFerrite Cores

Total GlobalPressed Cores

19.15%

-0.20%

19.48%

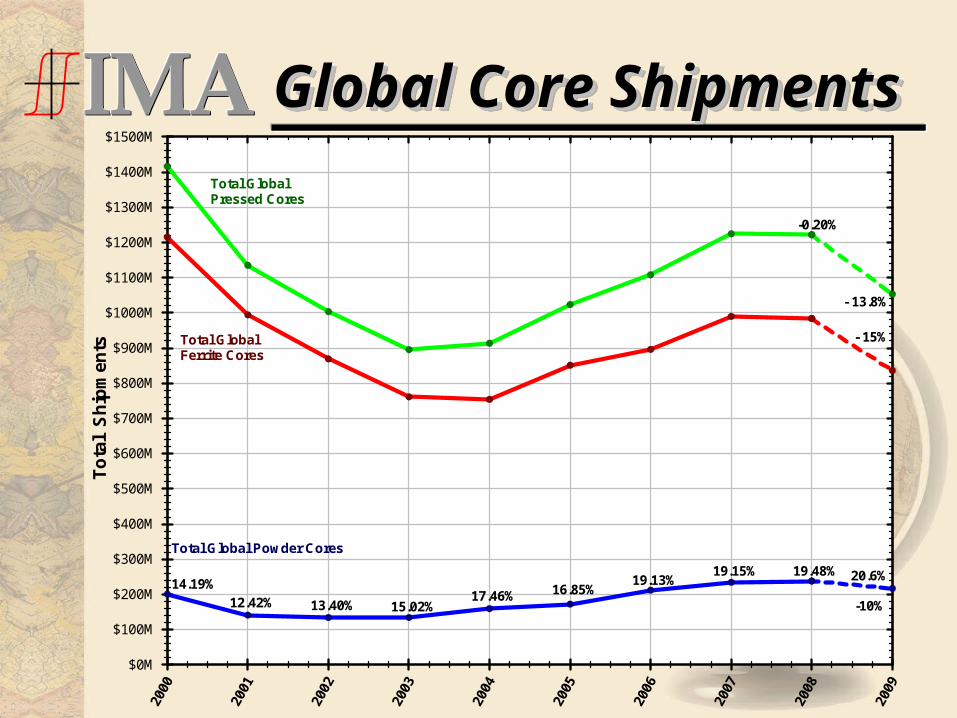

Global Core ShipmentsGlobal Core ShipmentsGlobal Core ShipmentsGlobal Core Shipments20

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

To

tal

Sh

ipm

ents

$0M

$100M

$200M

$300M

$400M

$500M

$600M

$700M

$800M

$900M

$1000M

$1100M

$1200M

$1300M

$1400M

$1500M

14.19%12.42% 13.40% 15.02%

17.46% 16.85%19.13%

Total Global Powder Cores

Total GlobalFerrite Cores

Total GlobalPressed Cores

19.15%

-0.20%

20.6%

- 13.8%

- 15%

-10%

19.48%

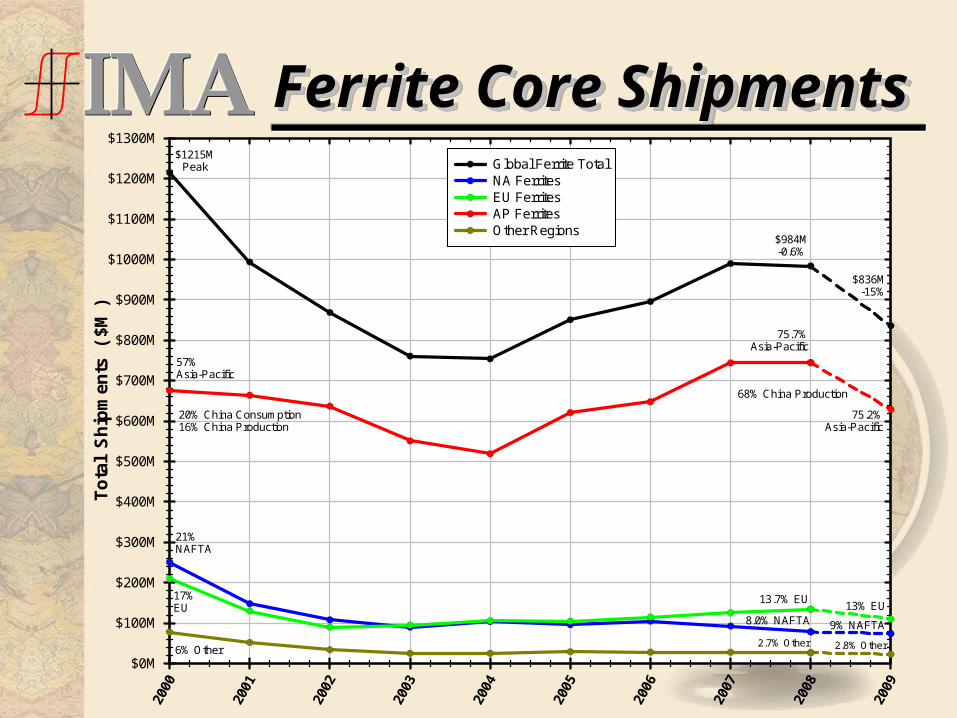

Ferrite Core ShipmentsFerrite Core ShipmentsFerrite Core ShipmentsFerrite Core Shipments20

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

To

tal

Sh

ipm

ents

(

$M )

$0M

$100M

$200M

$300M

$400M

$500M

$600M

$700M

$800M

$900M

$1000M

$1100M

$1200M

$1300M

Global Ferrite Total$1215M

Peak

$984M-0.6%

Ferrite Core ShipmentsFerrite Core ShipmentsFerrite Core ShipmentsFerrite Core Shipments20

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

To

tal

Sh

ipm

ents

(

$M )

$0M

$100M

$200M

$300M

$400M

$500M

$600M

$700M

$800M

$900M

$1000M

$1100M

$1200M

$1300M

Global Ferrite TotalNA FerritesEU FerritesAP FerritesOther Regions

$1215MPeak

$984M-0.6%

57%Asia-Pacific

20% China Consumption16% China Production

75.7%Asia-Pacific

68% China Production

21%NAFTA

17%EU

6% Other2.7% Other

13.7% EU

8.0% NAFTA

Ferrite Core ShipmentsFerrite Core ShipmentsFerrite Core ShipmentsFerrite Core Shipments20

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

To

tal

Sh

ipm

ents

(

$M )

$0M

$100M

$200M

$300M

$400M

$500M

$600M

$700M

$800M

$900M

$1000M

$1100M

$1200M

$1300M

Global Ferrite TotalNA FerritesEU FerritesAP FerritesOther Regions

$1215MPeak

$984M-0.6%

57%Asia-Pacific

20% China Consumption16% China Production

75.7%Asia-Pacific

68% China Production

21%NAFTA

17%EU

6% Other2.7% Other

13.7% EU

8.0% NAFTA

$836M-15%

75.2%Asia-Pacific

2.8% Other

13% EU

9% NAFTA

PowderPowder CoreCore ShipmentsShipmentsPowderPowder CoreCore ShipmentsShipments20

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

To

tal

Sh

ipm

ents

(

$M )

$0M

$10M

$20M

$30M

$40M

$50M

$60M

$70M

$80M

$90M

$100M

$110M

$120M

$130M

$140M

$150M

Global Premium PC TotalGlobal Iron Powder Cores

$115MPeak

$86MPeak

$141M +0.4%

$97M+3.2%

PowderPowder CoreCore ShipmentsShipmentsPowderPowder CoreCore ShipmentsShipments20

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

To

tal

Sh

ipm

ents

(

$M )

$0M

$10M

$20M

$30M

$40M

$50M

$60M

$70M

$80M

$90M

$100M

$110M

$120M

$130M

$140M

$150M

Global Premium PC TotalNA Powder CoresEU Powder CoresAP Powder CoresOther RegionsGlobal Iron Powder Cores

49.5%

38.6% 35.5%30.1% 23.5% 23.6%

16.2%11.9%

$115MPeak

$86MPeak

NAFTA

29%A-P

3%China Prod.

18%EU

3% Other

$141M +0.4%

$97M+3.2%

AP 75.2%

NAFTA

EU 11.5%

Other 1.4%

14.6%

PowderPowder CoreCore ShipmentsShipmentsPowderPowder CoreCore ShipmentsShipments20

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

To

tal

Sh

ipm

ents

(

$M )

$0M

$10M

$20M

$30M

$40M

$50M

$60M

$70M

$80M

$90M

$100M

$110M

$120M

$130M

$140M

$150M

Global Premium PC TotalNA Powder CoresEU Powder CoresAP Powder CoresOther RegionsGlobal Iron Powder Cores

49.5%

38.6% 35.5%30.1% 23.5% 23.6%

16.2%11.9%

$115MPeak

$86MPeak

NAFTA

29%A-P

3%China Prod.

18%EU

3% Other

$141M +0.4%

$97M+3.2%

AP 75.2%

76% ChinaProduction

NAFTA

EU 11.5%

Other 1.4% Other 1.6%

EU 12.6%

NAFTA12.6%

73.2%AP

$90M-7%

$127M-10%

14.6%

Nickel Price ImpactNickel Price ImpactNickel Price ImpactNickel Price Impact20

03

2004

2005

2006

2007

2008

2009

Nic

kel

Co

mm

od

ity

($/

lb)

$0

$5

$10

$15

$20

$25

Nickel Daily AverageNickel Monthly HighNickel Monthly Low

Nickel Price Doubled02Q4 to 03Q4

Nickel Price Average of $6.75 per Pound,04Q1 through 06Q1

Nickel Triples in Value,05Q4 through 06Q4

Nickel Quadruples in Value,05Q4 through 07Q1

Nickel Price ImpactNickel Price ImpactNickel Price ImpactNickel Price Impact20

03

2004

2005

2006

2007

2008

2009

Nic

kel

Co

mm

od

ity

($/

lb)

$0

$5

$10

$15

$20

$25

Nickel Daily AverageNickel Monthly HighNickel Monthly Low

Nickel Price Doubled02Q4 to 03Q4

Nickel Price Average of $6.75 per Pound,04Q1 through 06Q1

Nickel Triples in Value,05Q4 through 06Q4

Nickel Quadruples in Value,05Q4 through 07Q1

Continued Volatility,07Q1 through 08Q4

Stabilityin 2009 ?

Challenges for 2009Challenges for 2009Challenges for 2009Challenges for 2009

• The past 6-8 months have been difficult for The past 6-8 months have been difficult for most core manufacturers.most core manufacturers.– Bookings declines in 08Q4 and shipment declines for Bookings declines in 08Q4 and shipment declines for

current months of 2009 are off 30% to 40% YTY.current months of 2009 are off 30% to 40% YTY.

• Excess production capacity in ferrites and Excess production capacity in ferrites and powder cores (most located in China).powder cores (most located in China).– Chinese do not have a correct global view of the Chinese do not have a correct global view of the

markets and Western competitors sizes.markets and Western competitors sizes.

• What will happen in the raw material What will happen in the raw material markets: iron, nickel, manganese, etc.?markets: iron, nickel, manganese, etc.?

• The past 6-8 months have been difficult for The past 6-8 months have been difficult for most core manufacturers.most core manufacturers.– Bookings declines in 08Q4 and shipment declines for Bookings declines in 08Q4 and shipment declines for

current months of 2009 are off 30% to 40% YTY.current months of 2009 are off 30% to 40% YTY.

• Excess production capacity in ferrites and Excess production capacity in ferrites and powder cores (most located in China).powder cores (most located in China).– Chinese do not have a correct global view of the Chinese do not have a correct global view of the

markets and Western competitors sizes.markets and Western competitors sizes.

• What will happen in the raw material What will happen in the raw material markets: iron, nickel, manganese, etc.?markets: iron, nickel, manganese, etc.?

QuestionsQuestions QuestionsQuestions

????