a quest for profits - modification and replacement parts...

TRANSCRIPT

Presented by:

Brad Morgenroth Executive Consultant, TeamSAI, Inc.

Economic Outlook For MRO

A Quest for Profits

MARPA 2013 Annual Conference

Airline Themes: Profit margin remains unacceptably low

While revenue has definitely improved, profits remain low relative to other

industries

― Worst return on capital among 30 industries

― History of extreme variation in financial performance

― Remain susceptible to external shocks that cannot be controlled

July 2013 TEAMSAI©2013

1

Typical Airline Cost Distribution

2% Profit

6% Tax/Fee

17% Maintenance

10% Ownership

38% Fuel

23% Labor

4% Other

Airline Themes: Capital, Finance, and Taxes

July 2013 TEAMSAI©2013

2

New aircraft …

― Increase revenue potential

― Lower fuel, maintenance, and potential

carbon emissions costs

― But increase aircraft ownership costs

Factor MD-80 737-800

P&L Considerations

Revenue 150 seats 160 seats

Fuel 950 gal/FH 680 gal/FH

Mx $2.4M/yr $2.1M/yr

Carbon 27k MT CO2 20 MT CO2

Taxes marginal

Balance Sheet Considerations

Own $1.9M/yr $3.6M/yr

Lease $0.2-0.7M/yr $2.3-4.2M/yr

737-800 net gain: $5M

Airline Themes: Maintenance & Engineering Costs

Maintenance is 15-20% of total operating

expenses

40-45% of M&E spend related to engines

― Most engine MRO in long term PBH deals

Contracting component MRO to a

comprehensive, single-source solution

growing in popularity ― Lower direct costs and improved ROIC

― Predictable cash flow

― Balance sheet improvement if asset sale included

New aircraft creating several opportunities ― Better designs with lower maintenance expense

― New leverage for striking comprehensive deals

July 2013 TEAMSAI©2013

3

MRO Current Fleet Planned Fleet

Airframe

Increased man hours due to aging fleet;

Shorter C check interval

Lower HMW man hours; Longer C check interval

Engine Locked into PBTH Locked in PBTH at higher

rate

Components Less expensive due to

availability of used parts

More expensive; Complex technology ; High cost of

spares; High material costs

Line Similar costs Similar costs

Segment %Share of 2013 Segment Spend

Engine >30%

Component 15-20%

Fleet & MRO

Global fleet outlook - commercial airline sector

22,529 in service aircraft in 2013 ― 19,890 jets

― 2,639 turboprops

In 2023, the fleet will grow to nearly

33,000 ― 3.7% CAGR growth rate expected

― 6,200 of the current fleet will retire

― Over 16,000 new deliveries in the period

• 38% of new aircraft will be replacements

July 2013 TEAMSAI©2013

5

Regionally, fleet growth rates vary significantly

July 2013 TEAMSAI©2013

6

2013-2023

Growth Rate

2023 Market

Share

0.6% 24%

2.4% 18%

5.3% 18%

7.7% 12%

5.0% 8%

6.6% 7%

6.2% 6%

4.8% 5%

10.8% 3%

Globally, the MRO growth outlook is healthy

Growth is expected to average

3.1% CAGR through 2023

$56.2B industry will grow to

$76.0B over the 10-year forecast

period

― 2023 forecast captures delivery of

significant new Airbus neo and Boeing

MAX fleets

Engine remains the largest

segment

― Engine and component MRO growth

rate expected to slow in second half of

forecast period due to honeymoon

period

July 2013 TEAMSAI©2013

7

MRO regional market shares change dramatically by 2023

Asia is driving the growth of the

global MRO market

Asia will be the largest MRO

market by 2023

― Few retirements

― Oldest aircraft contributing to MRO

MRO in North America expected

to suffer from large-scale fleet

replacement

July 2013 TEAMSAI©2013

8

Americas

Europe

Asia

ME/Africa

North American growth will be limited

Virtually no fleet growth over the

next 10 years

― 0.7% CAGR from 2013-2023

― 3,447 new deliveries and 2,646

retirements of current in-service aircraft

are forecasted

― 86% replacement rate

NA’s MRO expected to suffer from

large-scale fleet replacement

July 2013 TEAMSAI©2013

9

40% 43% 11% 12% 23% -5%

NA Share of the Global Change in MRO (2013-23)

Summing up the North American outlook

NA’s MRO growth will be impacted by:

― low net fleet growth

― aircraft with less-maintenance intensive HMV

― work and honeymoon periods

Asia Pacific, China, and the Middle East will experience the greatest

absolute growth

― Combined, these three regions will make up more than 60% of the increase ($12.1B)

July 2013 TEAMSAI©2013

10

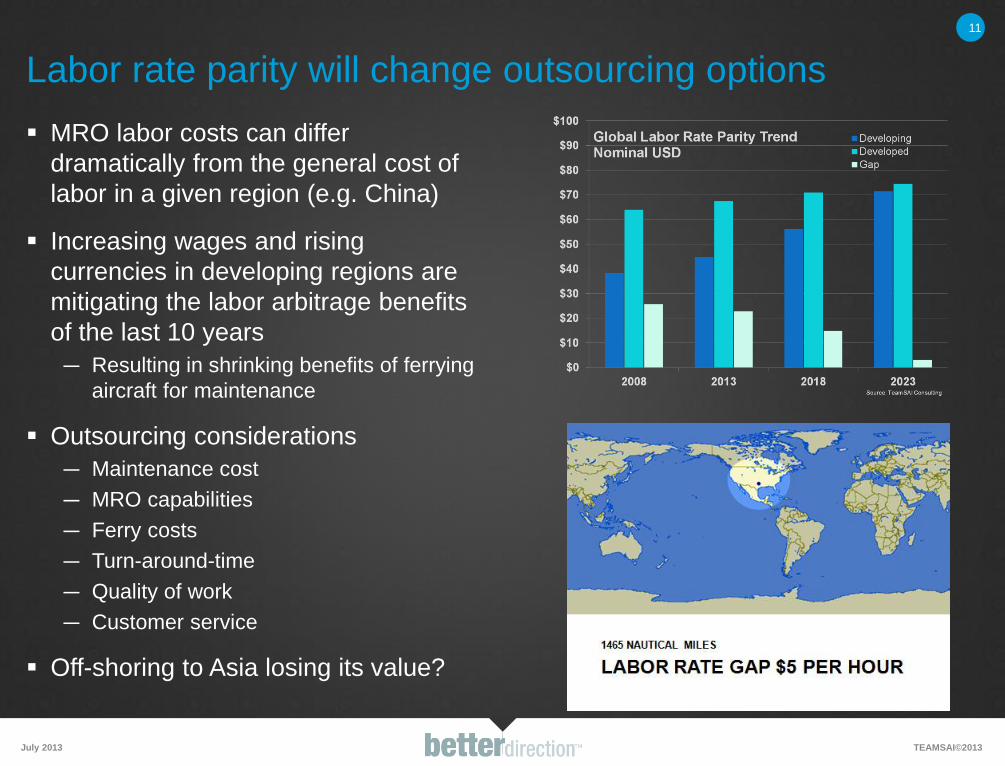

Labor rate parity will change outsourcing options

MRO labor costs can differ

dramatically from the general cost of

labor in a given region (e.g. China)

Increasing wages and rising

currencies in developing regions are

mitigating the labor arbitrage benefits

of the last 10 years

― Resulting in shrinking benefits of ferrying

aircraft for maintenance

Outsourcing considerations

― Maintenance cost

― MRO capabilities

― Ferry costs

― Turn-around-time

― Quality of work

― Customer service

Off-shoring to Asia losing its value?

July 2013 TEAMSAI©2013

11

MRO activity dominates the demand in any given year; more than 90% of total demand ― The remainder of the market is generated from rotables scrap replacements and new fleet support

requirements

The aftermarket parts market will grow at 3.0% CAGR over the 10-year period

July 2013 TEAMSAI©2013

Aftermarket parts market will reach nearly $30B in 2013

12

Almost 50% of the aftermarket parts demand ($13.7B) is generated from the NB fleet

WB aircraft, while only 20% of the total fleet, represent 41% of the spend ($11.6B)

July 2013 TEAMSAI©2013

RJ

NB

WB

MRO Activity Based Demand Only

TP

Aftermarket demand by aircraft class

13

Total Spares for MRO (Activity-Based Demand) 2013-2018 2018-2023 2013-2023

$Billions 2013 2018 2023 CAGR CAGR CAGR

HMV&Mod $0.10 $0.11 $0.13 2.3% 2.7% 2.5%

Engines $1.62 $1.79 $1.71 1.9% -0.9% 0.5%

Component $0.26 $0.29 $0.30 2.4% 1.1% 1.8%

Line $0.06 $0.07 $0.07 2.5% 1.3% 1.9%

Total Spares for MRO (Activity-Based Demand) $2.04 $2.25 $2.21 2.0% -0.4% 0.8%

2013 Forecast 2013 Forecast

Total Spares for MRO (Activity-Based Demand) 2013-2018 2018-2023 2013-2023

$Billions 2013 2018 2023 CAGR CAGR CAGR

HMV&Mod $1.30 $1.51 $1.90 3.1% 4.8% 3.9%

Engines $8.36 $10.50 $11.09 4.7% 1.1% 2.9%

Component $3.28 $3.96 $4.25 3.9% 1.4% 2.7%

Line $0.77 $0.95 $1.02 4.2% 1.5% 2.8%

Total Spares for MRO (Activity-Based Demand) $13.71 $16.92 $18.26 4.3% 1.5% 2.9%

2013 Forecast 2013 Forecast

Total Spares for MRO (Activity-Based Demand) 2013-2018 2018-2023 2013-2023

$Billions 2013 2018 2023 CAGR CAGR CAGR

HMV&Mod $0.12 $0.15 $0.19 4.9% 3.9% 4.4%

Engines $0.57 $0.70 $0.81 4.1% 3.0% 3.6%

Component $0.30 $0.37 $0.43 4.4% 3.4% 3.9%

Line $0.07 $0.08 $0.10 4.4% 3.4% 3.9%

Total Spares for MRO (Activity-Based Demand) $1.06 $1.31 $1.53 4.3% 3.3% 3.8%

2013 Forecast 2013 Forecast

Total Spares for MRO (Activity-Based Demand) 2013-2018 2018-2023 2013-2023

$Billions 2013 2018 2023 CAGR CAGR CAGR

HMV&Mod $0.92 $1.00 $1.24 1.7% 4.4% 3.1%

Engines $7.58 $9.85 $11.43 5.4% 3.0% 4.2%

Component $2.45 $2.76 $3.02 2.4% 1.8% 2.1%

Line $0.61 $0.71 $0.79 3.1% 2.2% 2.6%

Total Spares for MRO (Activity-Based Demand) $11.57 $14.32 $16.49 4.4% 2.9% 3.6%

2013 Forecast 2013 Forecast

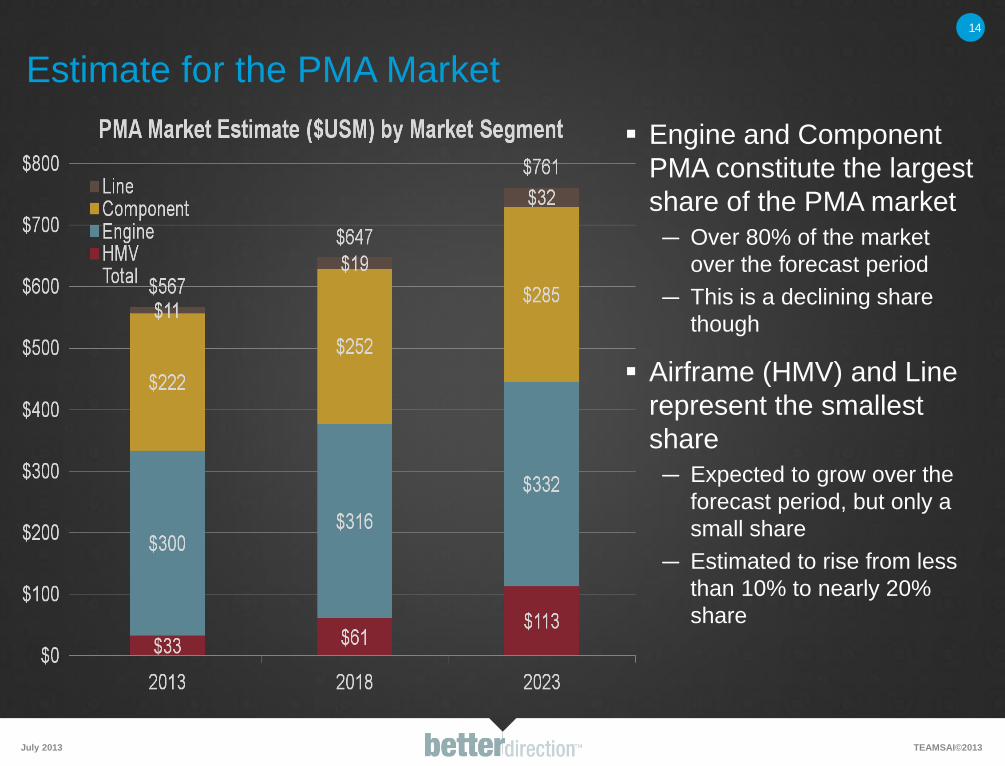

Estimate for the PMA Market

Engine and Component

PMA constitute the largest

share of the PMA market

― Over 80% of the market

over the forecast period

― This is a declining share

though

Airframe (HMV) and Line

represent the smallest

share

― Expected to grow over the

forecast period, but only a

small share

― Estimated to rise from less

than 10% to nearly 20%

share

July 2013 TEAMSAI©2013

14

PMA has made good penetration into aircraft market and some success in components

but has stalled in the high-value engine segment

Several factors mitigating against PMA in engines: ― Concerted effort by OEMs to block PMA and DER repairs

• Long Term Service Agreements (TotalCare, OnPoint, Engine Life) tie customers into OEM parts/repairs

• Long-Term Parts Supply contracts with MRO shops give price discounts in return for sole sourcing from

the OEM

• OEM-branded configurations and service centers – TRUEngines for CFM56 and CF6

– Some appraisers ascribe higher values to engines with pure OEM configuration

– e.g. IBA show value of CF6-80C2 with non-OEM parts and repairs as 25% lower than engine with

only OEM parts/repairs

– Engines make up most of the value of an older aircraft so engine valuation is key

― Lessors prohibit fitment of PMA and DER due to valuation and marketability concerns

P&W foray into CFM56 PMA has failed ― Biggest target customer (UAL) parked fleet shortly after launch and limited interest since then

Asset managers (e.g. GA Telesis, AJ Walter) are harvesting used parts from retiring

aircraft and buying surplus stock thus pressuring PMA for end-of-life products

PMA market dynamics

July 2013 TEAMSAI©2013

15

OEMs dominate new products while sunset products are dominated by asset managers with

surplus parts and tear-downs. Thus, PMA prospects brightest with mature products.

Market challenges

and responses

17

Time since EIS

New / In Production Sunset Mature

Response: prepare for necessary capabilities

July 2013 TEAMSAI©2013

Challenge: OEM dominance is changing the business model

Airframe and component OEMs

will increase their presence in the

market mirroring engine OEMs’

successful strategy

― Technology in new aircraft give OEMs

an opportunity to penetrate market

• Restricting IP and charging high

licensing fees

― OEMs pursuing support contracts at

point of sale to enter market

• Crucial for airframe OEMs entry

into aftermarket

How will the smaller independent

MRO survive?

July 2013 TEAMSAI©2013

18

Response strategies for Independent MRO survival

Become a niche player

― Target lessors with fleet support packages

― Look to LCCs

• MRO contracting is essential to their

business model

― Develop a reputation as a best in class

― Create a value proposition around

flexibility and speed

― Consider partnering with an OEM

Consider speed and quality as a financial performance multiplier

― Higher productivity through LEAN improves margins and revenue

― Customer proximity and service can drive sales

― High quality results in less rework and lower costs

July 2013 TEAMSAI©2013

19

Focus: leverage flexibility and speed for a better customer experience

Aircraft and component OEMs are following the example set by engine makers ― Boeing GoldCare, Airbus FHS, Moog Total Support, Honeywell MSP

― Given that parts make up a small part of airframe MRO, the case for airframe LTSA and disintermediation of

traditional MRO is unproven

― Component PMA packages needed to match whole component deals from OEMs – consolidation and/or

JVs?

Operating leases forecast to grow to at least 50% of aircraft and current contracting

trends suggest PMA take-up will be limited

― Softening of stance from some lessors (non-aerofoil PMA permitted by some)

Engine OEMs continuing pressure on PMA and DER ― Restricting availability of technical data

― Increasing pace of modifications to key parts

― “Influencing Parts” said to limit lives of LLPs

― TrueLLP program from GE

Appraisers marking down resale value of engines containing PMA ― Residual value guarantees possible?

Challenge: PMA Relevance

July 2013 TEAMSAI©2013

20

Technical and regulatory case for PMA had been made and won but commercial battle with

OEMs is intensifying and PMA industry needs to respond with commercial initiatives

Airline cost pressures having outsized impact on MRO

July 2013 TEAMSAI©2013

21

Brad Morgenroth Executive Consultant

TeamSAI, Inc.

404-762-7257 Ext. 108

Thank you! WWW.TEAMSAI.COM