a pregnant pause economic prospects for the remainder of 2008 carl r. tannenbaum economic consultant...

TRANSCRIPT

A Pregnant Pause

Economic Prospects forthe Remainder of 2008

Carl R. TannenbaumEconomic [email protected]

Pregnant Pause, April 2008

Let’s Not Forget:Things Haven’t Been That Bad!Quarterly Change in US GDP, Annualized

“Potential”

-2%

0%

2%

4%

6%

8%

2001 2002 2003 2004 2005 2006 2007

Pregnant Pause, April 2008

Expansions: Not Always Smooth Sailing

-2%

0%

2%

4%

6%

1985 1989 1993 1997 2001 2005

Year over Year Growth in Real GDP

• Growth recessions punctuated the long expansions of the ’80s and ’90s

Pregnant Pause, April 2008

The Housing CorrectionTrends in Home Sales

4

5

6

7

8

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

(Mill

ions

, SAAR

)

Existing New

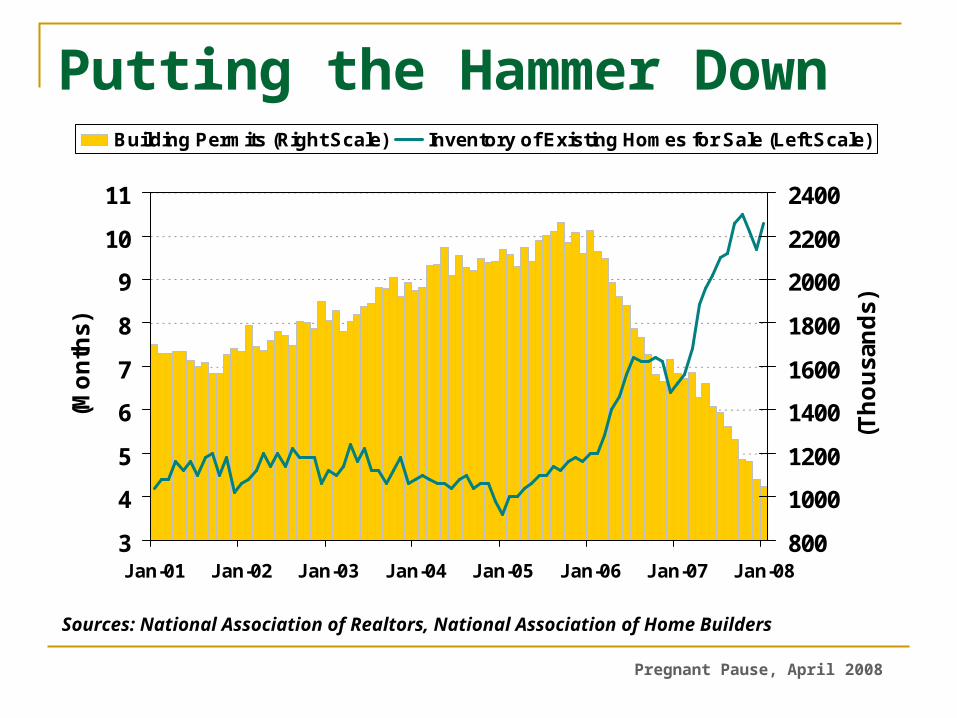

Sources: National Association of Realtors, National Association of Home Builders

Pregnant Pause, April 2008

3

4

5

6

7

8

9

10

11

Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

(Mo

nth

s)

800

1000

1200

1400

1600

1800

2000

2200

2400

(Th

ou

san

ds)

Building Permits (Right Scale) Inventory of Existing Homes for Sale (Left Scale)

Putting the Hammer Down

Sources: National Association of Realtors, National Association of Home Builders

Pregnant Pause, April 2008

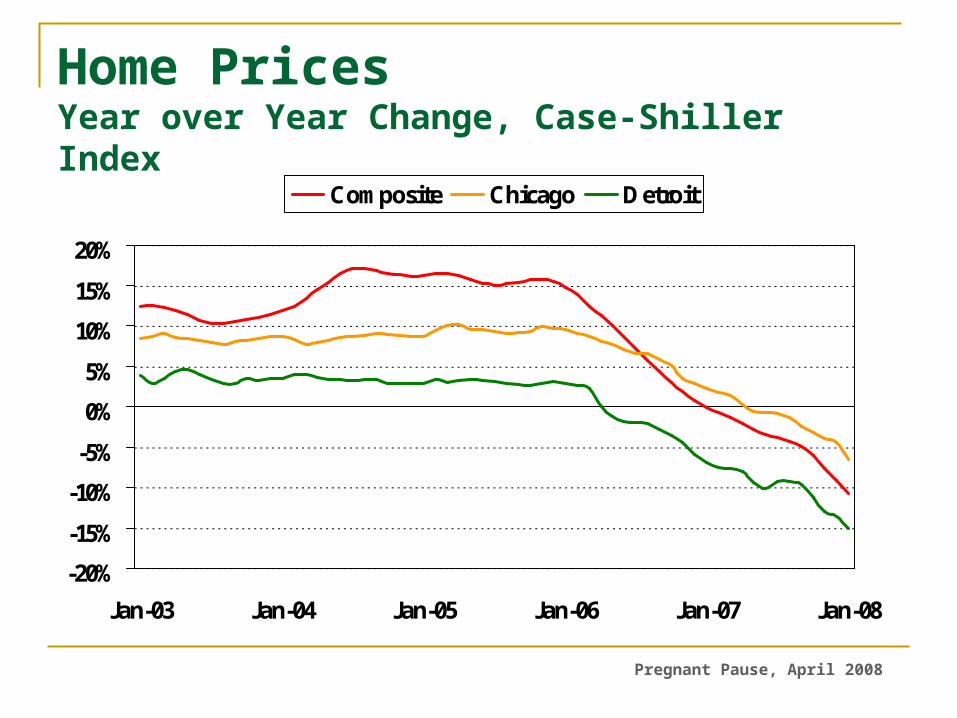

Home PricesYear over Year Change, Case-Shiller Index

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

Composite Chicago Detroit

Pregnant Pause, April 2008

FICO ScoresWeighted Average of FICO Scores for Total Originations

660

670

680

690

700

2002 2003 2004 2005 2006

Pregnant Pause, April 2008

ARM Share of new originations

0%

5%

10%

15%

20%

25%

30%

35%

40%

Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07

Pregnant Pause, April 2008

Past Their PrimeHome mortgages 30 or more days past due

Source: Mortgage Bankers Association

Pregnant Pause, April 2008

-40

-20

0

20

40

60

80

100

1990 1993 1996 1999 2002 2005 2008

All Mortgages Prime Nontraditional Subprime

Senior Loan Officer Survey: Home MortgagesNet Percentage of Respondents Tightening Credit

Source: Federal Reserve

Highest on record

Pregnant Pause, April 2008

Views on Sub-Prime

Not a complete disaster, but some very questionable practices

Break in housing prices causes contagion to other mortgage segments

A wake-up call for borrowers and lenders

Losses: $200 billion; widely dispersed

Pregnant Pause, April 2008

Borrowers

FinancialIntermediaries

Investors

The Modern Financial Reality

Pregnant Pause, April 2008

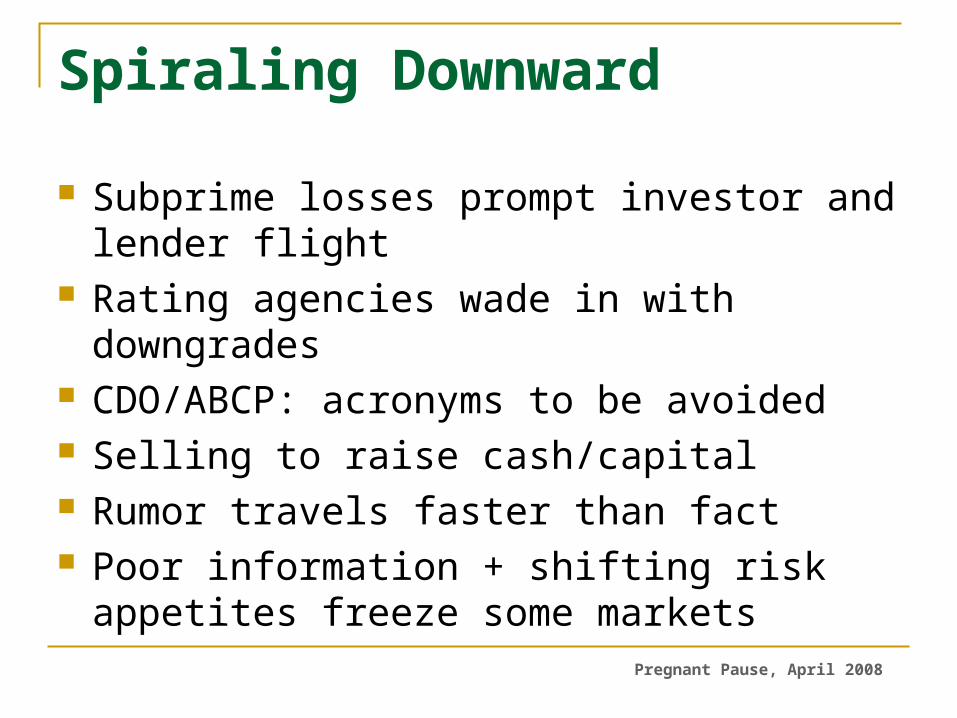

Spiraling Downward

Subprime losses prompt investor and lender flight

Rating agencies wade in with downgrades CDO/ABCP: acronyms to be avoided Selling to raise cash/capital Rumor travels faster than fact Poor information + shifting risk appetites

freeze some markets

Pregnant Pause, April 2008

Corporate CreditworthinessComposite of Credit Default Swaps

20

40

60

80

100

120

140

160

180

200

Apr-07 Jul-07 Oct-07 Jan-08

(Bas

is P

oint

s)

Source: Bloomberg

Pregnant Pause, April 2008

New Debt Issues

0

100

200

300

400

500

600

700

$$ B

illions

2006 2007

Municipal

Treasury

Mortgage

Corporate

Agency

Asset-Backed

Source: SIFMA

Pregnant Pause, April 2008

Source: Federal Reserve

Commercial and Industrial LoansAll Commercial Banks

900

1000

1100

1200

1300

1400

1500

Jan '05 Jul '05 Jan'06 Jul '06 Jan '07 Jul '07 Jan '08

$$ B

illions

Annualized Growth: 13%

Annualized Growth: 27%

Pregnant Pause, April 2008

Tightening the Vise?

Rating Agencies

Congress

Bond Insurers

Regulators?

Pregnant Pause, April 2008

Senior Loan Officer Survey: Commercial Real EstateNet Percentage of Respondents Tightening Credit

-40

-20

0

20

40

60

80

100

1990 1993 1996 1999 2002 2005 2008

Source: Federal Reserve

-40

-20

0

20

40

60

80

100

1990 1993 1996 1999 2002 2005 2008

-40

-20

0

20

40

60

80

100

1990 1993 1996 1999 2002 2005 2008

-40

-20

0

20

40

60

80

100

1990 1993 1996 1999 2002 2005 2008

Highest on record

Pregnant Pause, April 2008

Impacts on Venture Capital/Private Equity Difficult to raise debt; difficult to sell companies

— Capital more costly or simply unavailable— Covenants tighter

More inward focus: managing existing deals as opposed to seeking new ones

Smaller deals, more minority interest Robin Hood economics: the discussion of

carried interest More restrictions just when we need fresh

capital the most?!

Pregnant Pause, April 2008

Signs of Investor ConservatismMoney Market Fund Assets

1000

1500

2000

2500

3000

3500

4000

2004 2005 2006 2007 2008

($$

Bill

ions

)

Source: ICI

US Treasury Yield Curve

0%

1%

2%

3%

4%

5%

6%

3 mo 6 mo 2 Yr 5 Yr 10 Yr 30 Yr

Maturity

Jun-07 Apr-08

Source: Bloomberg

• This money will eventually have to go back to work!

Pregnant Pause, April 2008

Conclusions: Credit

We’re working to avoid a credit crunch Wall Street firms remain under stress; high

vulnerability to event risk Effect on community banks has been limited,

but translation from Wall Street down to Main Street is possible

We’re seeing the downside of the modern financial markets

Pregnant Pause, April 2008

Real Personal ConsumptionYear over Year Change

0.0%

1.0%

2.0%

3.0%

4.0%

2004 2005 2006 2007 2008

Pregnant Pause, April 2008

Employment Trends

-100

0

100

200

300

400

Jan-05 Jan-06 Jan-07 Jan-08

(Th

ou

san

ds)

4.0%

4.5%

5.0%

5.5%

6.0%

Change in Payrolls (Left Scale) Unemployment Rate (Right Scale)

Source: Bureau of Labor Statistics

Pregnant Pause, April 2008

Mr. Bernanke’s Big Test

• Doesn’t want to reward Doesn’t want to reward reckless behaviorreckless behavior

• Expansion is less secureExpansion is less secure

• Inflation above comfort Inflation above comfort zonezone

• The financial system came The financial system came close to melting downclose to melting down

Tough choices, but pulling Tough choices, but pulling out all stopsout all stops

Pregnant Pause, April 2008

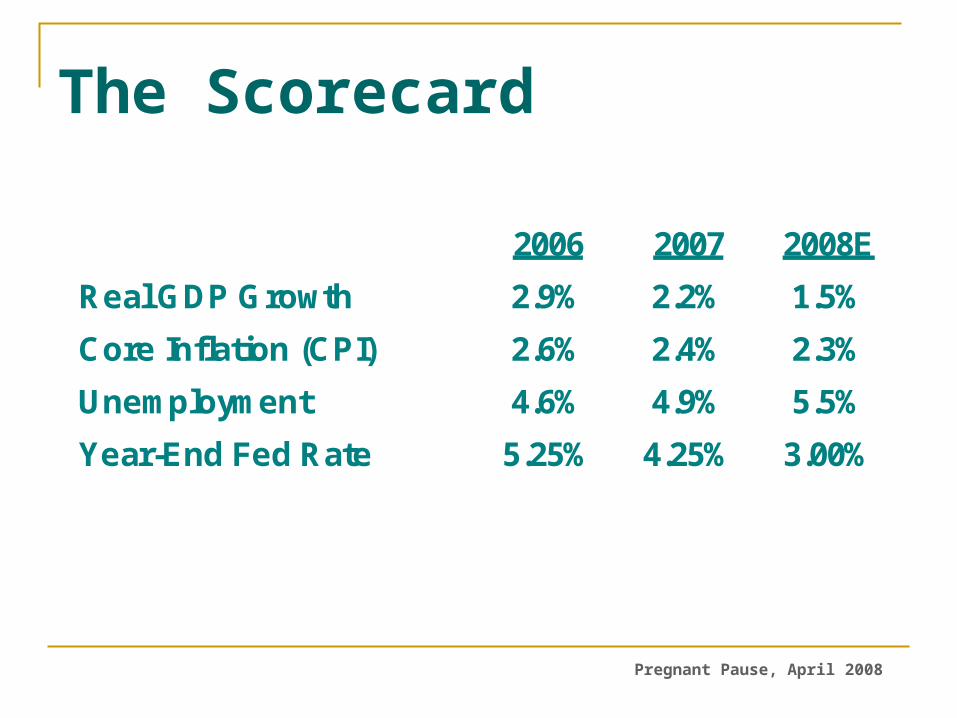

The Scorecard

2006 2007 2008E

Real GDP Growth 2.9% 2.2% 1.5%

Core Inflation (CPI) 2.6% 2.4% 2.3%

Unemployment 4.6% 4.9% 5.5%

Year-End Fed Rate 5.25% 4.25% 3.00%

Pregnant Pause, April 2008

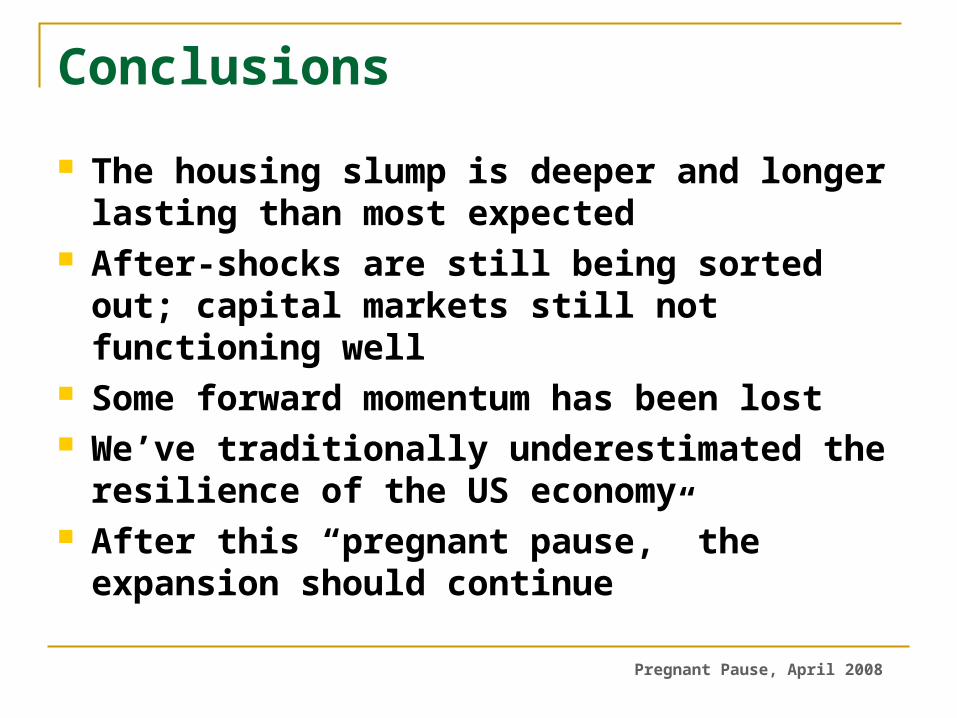

Conclusions

The housing slump is deeper and longer lasting than most expected

After-shocks are still being sorted out; capital markets still not functioning well

Some forward momentum has been lost We’ve traditionally underestimated the

resilience of the US economy After this “pregnant pause,” the expansion

should continue

A Pregnant Pause

Economic Prospects forthe Remainder of 2008

Carl R. TannenbaumEconomic [email protected]