a pathway to clean audit opinions ias 21 ias 29 - c … pathway to clean audit...rupxodwlrq ri dxglw...

TRANSCRIPT

A Pathway to Clean Audit Opinions (IAS 21, IAS 29)

January 2020

Chengetai Mashavave

How did we get here

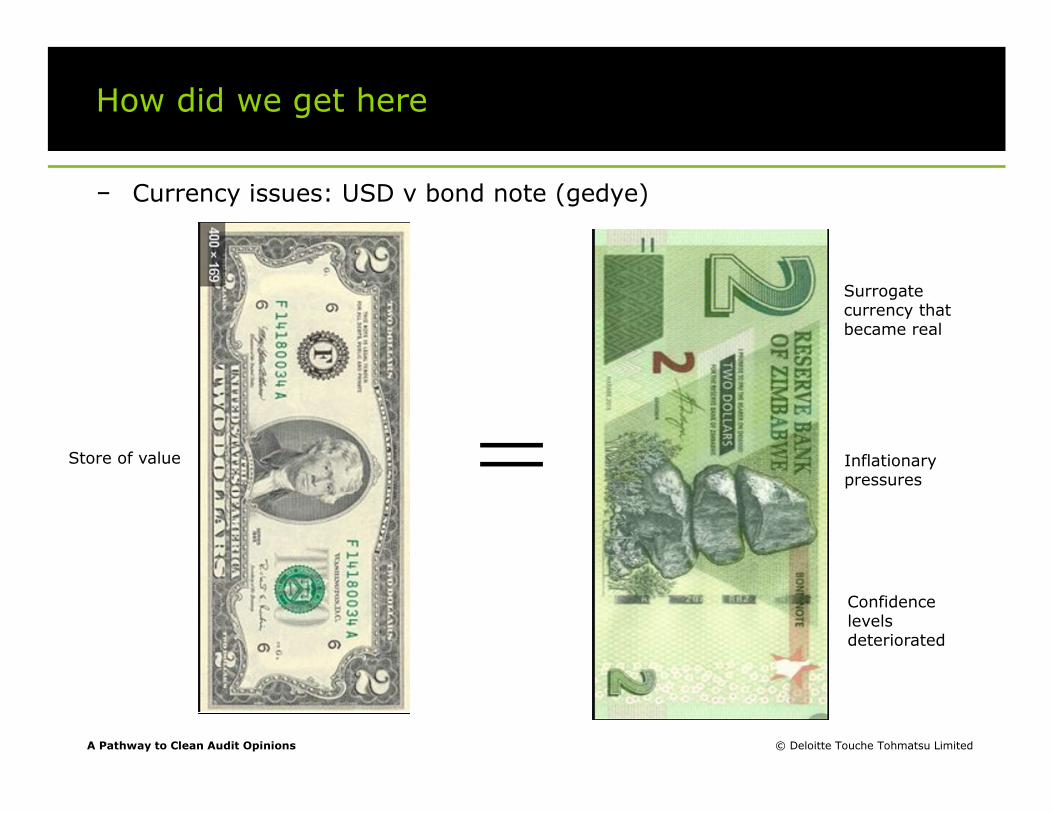

− Currency issues: USD v bond note (gedye)

© Deloitte Touche Tohmatsu LimitedA Pathway to Clean Audit Opinions

Inflationary pressures

Surrogate currency that became real

Confidence levels deteriorated

Store of value

Formulation of audit opinions

− Sufficiency and appropriateness of audit evidence

− materiality

− IFRS v laws & regulations

− Type of opinion (driven by primary users/purpose)?

© Deloitte Touche Tohmatsu LimitedA Pathway to Clean Audit Opinions

- Unqualified (emphasis of matter?)

- Qualified

- Adverse

- Disclaimer

IAS 21 considerations: 2020 and beyond

• Primary / functional currency; change from ZWL?

• Transition from USD to ZWD: Oct 2018 to Mar 2019 and IAS 21 v IAS Zim (S.I. 33 and other related pronouncements)

• Exchange rates used (plus NOCLAR effects)

− Settled transactions (spot rate)

− Unsettled transactions

− Supreme Court ruling and effects on “forex debts”

© Deloitte Touche Tohmatsu LimitedA Pathway to Clean Audit Opinions

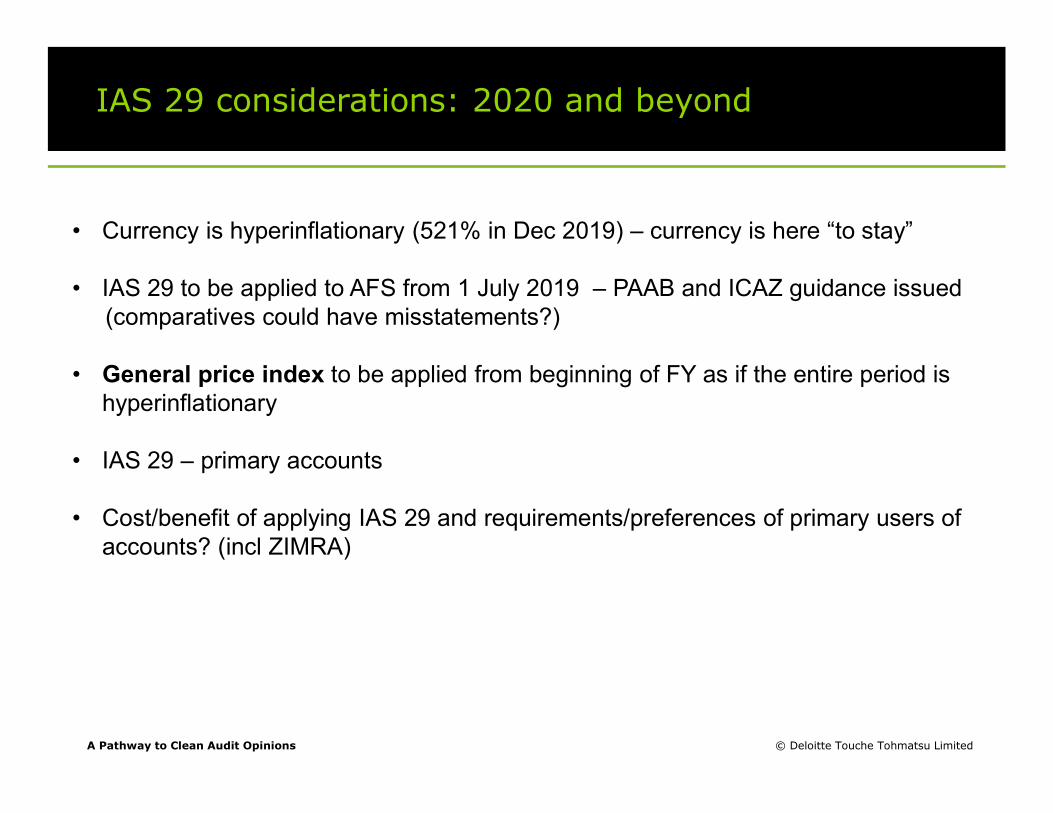

IAS 29 considerations: 2020 and beyond

© Deloitte Touche Tohmatsu LimitedA Pathway to Clean Audit Opinions

• Currency is hyperinflationary (521% in Dec 2019) – currency is here “to stay”

• IAS 29 to be applied to AFS from 1 July 2019 – PAAB and ICAZ guidance issued(comparatives could have misstatements?)

• General price index to be applied from beginning of FY as if the entire period is hyperinflationary

• IAS 29 – primary accounts

• Cost/benefit of applying IAS 29 and requirements/preferences of primary users of accounts? (incl ZIMRA)

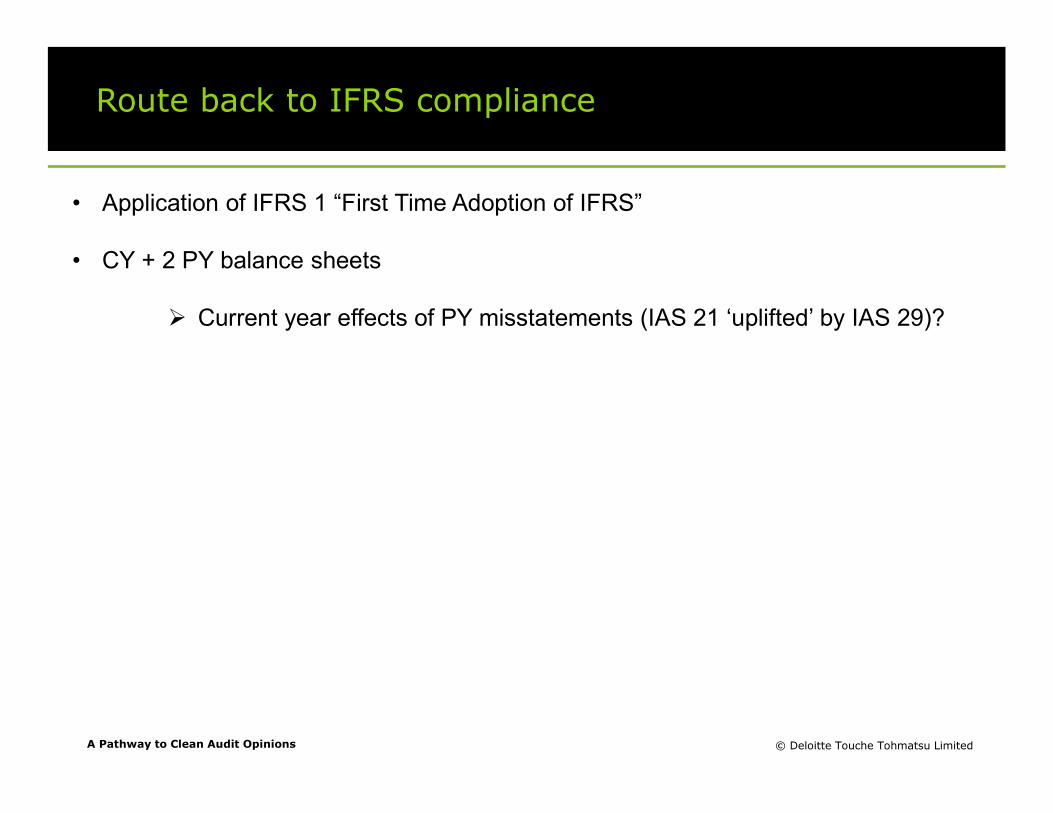

Route back to IFRS compliance

© Deloitte Touche Tohmatsu LimitedA Pathway to Clean Audit Opinions

• Application of IFRS 1 “First Time Adoption of IFRS”

• CY + 2 PY balance sheets

Current year effects of PY misstatements (IAS 21 ‘uplifted’ by IAS 29)?

A Pathway to Clean Audit Opinions © Deloitte Touche Tohmatsu Limited

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited ("DTTL"), our global network of member firms and our related entities. DTTL (also referred to as "Deloitte Global") and each of our member firms are legally separate and independent entities. DTTL does not provide services to clients. Please see www.deloitte.com/about to learn more.

Deloitte is a leading global provider of audit and assurance, consulting, financial advisory, risk advisory, tax and related services. Our network of member firms in more than 150 countries and territories serves four out of five Fortune Global 500® companies. Learn how Deloitte's approximately 286,000 people make an impact that matters at www.deloitte.com.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms or their related entities (collectively, the "Deloitte network") is, by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2019. For information, contact Deloitte Touche Tohmatsu Limited.