a handy guide to doing business in china - sbasf.cn · pdf file · 2018-01-30doing...

TRANSCRIPT

A publication of

DOING BUSINESS IN

CHINAA Handy Guide to

Doing Business in China 2017 1

General InformatIon 4• Economy��������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������5• Administration��������������������������������������������������������������������������������������������������������������������������������������������������������������������������������6

BusIness entItIes 7• TypesofBusinessEntities�����������������������������������������������������������������������������������������������������������������������������������������������������������8• ForeignInvestedEntities������������������������������������������������������������������������������������������������������������������������������������������������������������8• IncorporationofBusinessEntities��������������������������������������������������������������������������������������������������������������������������������������� 10• EstablishmentProcedures������������������������������������������������������������������������������������������������������������������������������������������������������ 12• AuditRequirements������������������������������������������������������������������������������������������������������������������������������������������������������������������ 13• AnnualCombinedFiling���������������������������������������������������������������������������������������������������������������������������������������������������������� 14• DissolutionandLiquidation���������������������������������������������������������������������������������������������������������������������������������������������������� 14

foreIGn exchanGe controls 17• OverviewofForeignExchangeControls��������������������������������������������������������������������������������������������������������������������������� 18• RemittanceofFundsOutofChina��������������������������������������������������������������������������������������������������������������������������������������� 18

taxatIon 20• OverviewofChinaTax�������������������������������������������������������������������������������������������������������������������������������������������������������������� 21

Ű TypesofTaxes 21Ű OverviewofKeyTaxRates 21Ű AdministrationandRegulations 22

• TypesofTaxes������������������������������������������������������������������������������������������������������������������������������������������������������������������������������ 23Ű ValueAddedTax(VAT) 23Ű ConsumptionTax(CT) 25Ű CustomsDuty 25Ű EnterpriseIncomeTax(EIT) 26Ű IndividualIncomeTax(IIT) 28Ű UrbanLandUseTax 31Ű RealEstateTax 31Ű VehicleandVesselUsageTax 31Ű StampDuty 31Ű LandAppreciationTax(LAT) 33Ű ContractualTax(DeedTax) 34Ű ResourceTax 34Ű CityMaintenanceandConstructionTaxandNationalEducationSurcharge 35Ű LocalEducationSurcharge 35Ű WithholdingTaxes 35

• Anti-avoidanceProvisions������������������������������������������������������������������������������������������������������������������������������������������������������� 36Ű TransferPricing 36Ű ControlledForeignCorporations(CFC)Rules 37Ű ThinCapitalisation 38Ű GeneralAnti-avoidanceProvisions 38

contents

2

manpower 39• ChinaLabourContractLaw���������������������������������������������������������������������������������������������������������������������������������������������������������������40• ConclusionofLabourContractsinChina�������������������������������������������������������������������������������������������������������������������������������������40• HiringExpatriateStaffinChina��������������������������������������������������������������������������������������������������������������������������������������������������������41• HiringLocalStaffinChina������������������������������������������������������������������������������������������������������������������������������������������������������������������42• SocialBenefitsinChina�����������������������������������������������������������������������������������������������������������������������������������������������������������������������43• WorkingHoursinChina����������������������������������������������������������������������������������������������������������������������������������������������������������������������44• PublicHolidaysandLeave�����������������������������������������������������������������������������������������������������������������������������������������������������������������45• Termination��������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������45• LabourDisputes������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������46• LegalResponsibility�����������������������������������������������������������������������������������������������������������������������������������������������������������������������������46

accountInG 48• AccountingRegulationsandStandards���������������������������������������������������������������������������������������������������������������������������������������49• PRCAdministrativeMeasuresforInvoices�����������������������������������������������������������������������������������������������������������������������������������52

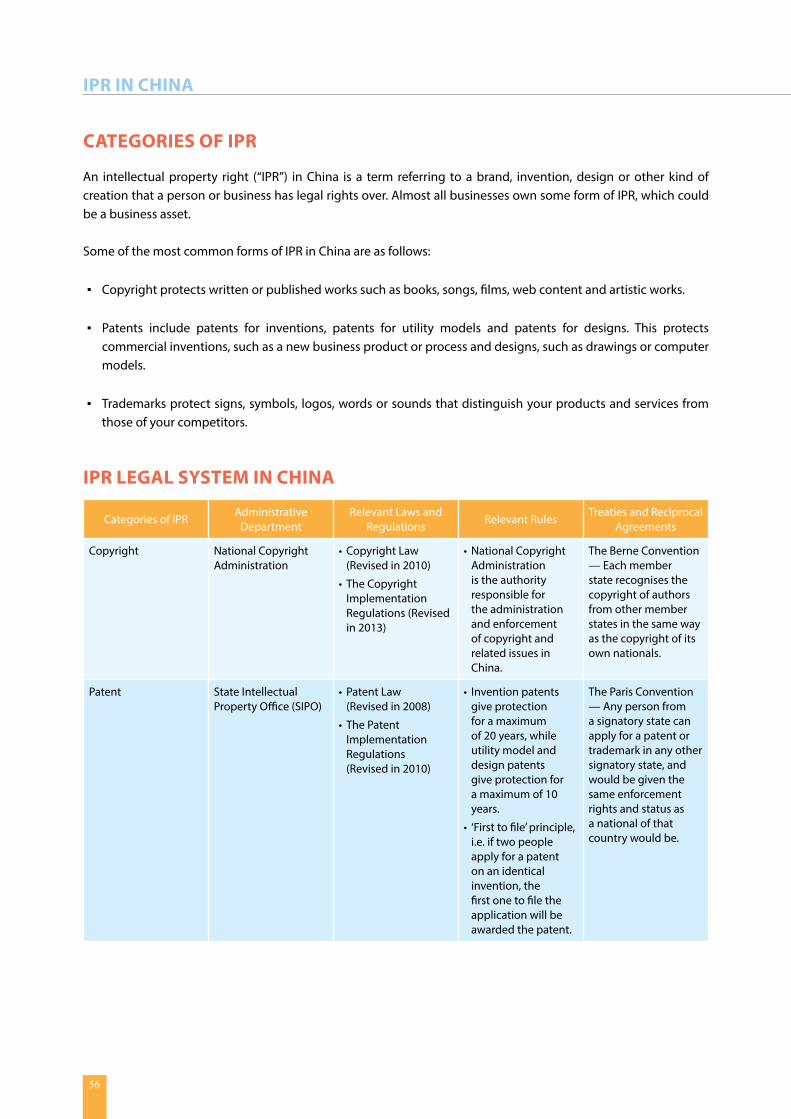

Intellectual property rIGhts (Ipr) In chIna 55• CategoriesofIPR����������������������������������������������������������������������������������������������������������������������������������������������������������������������������������56• IPRLegalSysteminChina������������������������������������������������������������������������������������������������������������������������������������������������������������������56• RegistrationofIPRsinChina������������������������������������������������������������������������������������������������������������������������������������������������������������57• HowtoProtectIPRsinChina������������������������������������������������������������������������������������������������������������������������������������������������������������57

lIstInG In chIna and sInGapore 58• ListinginChina�������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������59• ListinginSingapore�����������������������������������������������������������������������������������������������������������������������������������������������������������������������������60

aBout sBa stone forest 61

contents

Doing Business in China 2017 3

contents

dIsclaImerThisguideisdesignedtoprovideinformationondoingbusinessinChinaonly�Thisinformationisprovidedwiththeintentionthattheauthorsdonotofferanylegalorotherprofessionaladvice�Inthecaseofaneedforanysuchexpertise,pleaseconsulttheappropriateprofessional�Thisisnotanexhaustiveguideonthesubjectandwasnotcreatedtobespecifictoanyindividual’sororganisation’scircumstanceorneeds�

Everyefforthasbeenmadetomakethisguideasaccurateaspossibleanditshouldserveonlyasageneralguideorsupportingmaterial,notastheultimatesourceofsubjectinformation�

Thisguidecontainsinformationthatmightbedatedandisintendedonlyforaninformativepurposeatthetimeofpublication�Theauthorsshallbearnoliabilityorresponsibilitytoanyperson(s)orentityregardinganylossordamageincurred,orallegedtohavebeenincurred,directlyorindirectly,bytherelianceoninformationcontainedinthisguide,andshallnotberesponsibleforanyerrors,inaccuraciesoromissions�

copyrIGht notIceNopartofthispublicationmaybereproduced,storedinaretrievalsystem,ortransmittedinanyformorbyanymeans,electronic,mechanical,photocopying,recording,orotherwisewithoutthewrittenpermissionofSBAStoneForestCorporateAdvisory(Shanghai)Co�,Ltd�oralicencepermittingrestrictedcopying�Copyright©SBAStoneForestCorporateAdvisory(Shanghai)Co�,Ltd�2017Allrightsreserved�

4

General InformatIon

Doing Business in China 2017 5

theworld�Itisalsotheworld’slargestexporterandsecondlargestimporterofgoods�

Inaddition,Chinaisamemberofnumerousformaland informal multilateral organisations, includingtheWTO4,APEC5,BRICS6,theShanghaiCooperationOrganisation(SCO)7,theBCIM8andtheG-209�Chinaisseenasamajorregionalpower10withinAsia,andconsideredbysometobeapotentialsuperpower11�

China isnowthethirdmostvisitedcountry intheworld, welcoming both tourists and internationalentrepreneurs alike� Over 30 million foreignersentered China in 2014 for leisure, business orconferences� Among the world’s 500 largestmultinational enterprises, over 480 have businessoperations in China� With the development ofChina’sFreeTradeZones,moreforeignentitiesareenteringtheChinesemarket�By2015,over490,000foreign-investedenterprises (FIEs)hadestablishedoperations in China� Inbound Foreign DirectInvestment(FDI)exceededUS$126billionin2016�China’s outbound FDI increased rapidly in recentyears,withthenetinvestmentgrowingfromUS$6�8billionin2010toUS$14billionin2015�FDIintotheChinese mainland maintained steady growth in2015despitetheeconomicslowdownintheworld’ssecondlargesteconomy�

Like many other Asian countries, China’s foreignreserves have exceeded their optimum level inrecentyears�AccordingtotheStateAdministrationof ForeignExchangeofChina, its foreign reservesreached US$3�3 trillion by the end of 2015,surpassingJapantobecomethecountrywith thehighestforeignreservesintheworld�

With a long history of over 5,000 years and apopulationofmorethan1�38billion,China isoneoftheworld’sbiggestcountriescovering9�6millionsquare kilometres of land area and 4�7 millionsquarekilometresofterritorialwaters�

Itexercisesjurisdictionover23provincesincludingfive autonomous regions, four direct-controlledmunicipalities (Beijing, Tianjin, Shanghai andChongqing),andtwomostlyself-governingspecialadministrativeregions(HongKongandMacau)�

Chinaofficiallyrecognises56distinctethnicgroups,the largestofwhich istheHanpeople,whomakeup about 92% of the total population� Ethnicminorities, for example, Manchurians, Uighurs,TibetansandKoreans,accountforabout8%ofthepopulationinChina�Therearemorethan80livinglanguages in China, which include Mandarin —spokennativelyby70%of thepopulation—andvariousdialectssuchasShanghainese,Cantonese,andHokkien�

economy

Chinahadthelargestandmostcomplexeconomyin the world for much of the past two thousandyears,duringwhichithasseencyclesofprosperity1andslowdowns�Sincetheintroductionofeconomicreforms in 19782, China has become one of theworld’sfastestgrowing3majoreconomies�In2001,ChinaformallyjoinedtheWorldTradeOrganization�Inrecentyears,Chinahasmaintaineditshighrateofeconomicgrowth,withitsgrossdomesticproduct(GDP)growing7�3%yearonyearin2014toUS$10�3trillion, making it the second largest economy in

General InformatIon

1 https://en.wikipedia.org/wiki/Prosperity2 https://en.wikipedia.org/wiki/Chinese_economic_reform3 https://en.wikipedia.org/wiki/List_of_countries_by_real_GDP_growth_rate4 https://www.wto.org5 www.apec.org6 http://infobrics.org7 https://en.wikipedia.org/wiki/Shanghai_Cooperation_Organisation8 https://en.wikipedia.org/wiki/BCIM9 http://g20.org/English10 https://en.wikipedia.org/wiki/Regional_power11 https://en.wikipedia.org/wiki/Potential_superpowers

6

General InformatIon

information regarding registered capital,directors, shareholders and the constitutionaldocuments�

(4) State Administration of Foreign Exchange(“safe”) manages and monitors foreignexchange transactions, including inward andoutwardremittanceandpayments�

(5) Special approvals are needed for foreigninvestors toentera restricted industrydue tosome limitations� For example, pre-approvalfromtheStateFoodandDrugAdministration(“sfda”) isneeded if the investment involvespharmaceuticalproduction�

For information or enquiries on our CorporateAdvisoryservices,pleasevisit:www�SBASF�com

admInIstratIon

With its seat of government in the capital cityof Beijing, the National People’s Congress is thehighestorganofstatepowerinChina�Thecentraland highest organ of state administration is theState Council, which directly oversees varioussubordinatePeople’sGovernmentsattheprovince,direct-controlled municipality and autonomousregionlevels�

The Communist Party is the sole governing partyof China, while other political parties participateintheNationalPeople’sCongressandtheChinesePeople’sPoliticalConsultativeConference�Amulti-partycooperationandpoliticalconsultationsystemisadoptedundertheleadershipoftheCommunistParty�

In2013,theSecondSessionofthe18thConferenceof the Chinese Communist Party and the FirstSession of the 12th Conference of the NationalPeople’sCongressreviewedandapprovedthenewProposaloftheStateCouncilforInstitutionalReformand Functional Transformation� These reformsare expected to greatly improve administrativeefficiency, accelerate improvementof the socialistmarketeconomicsystemandprovideinstitutionalsecurity for building a moderately prosperoussocietyinChina�

Key admInIstratIve departments

(1) NationalDevelopmentandReformCommission(“ndrc”) coordinates development policyandalsoplaysamajorroleinapprovingsomerestrictedforeigninvestmentprojects�

(2) The establishment of Foreign InvestmentEnterprisesshallbeapprovedbytheMinistryofCommerce(“mofcom”),includingtheArticlesofAssociationandbusinessscope(areaswherebusinessactivitiesarepermitted)�

(3) All business entities need to maintainrecords of corporate documents with localbranches of State Administration for Industryand Commerce (“saIc”), including basic

Doing Business in China 2017 7

BusIness entItIes

8

BusIness entItIes

liability company or to operate as a partnershipwhereatleastonepartnerbearsunlimitedliability�IftheCJVisoperatedasalimitedliabilitycompany,a board of directors shall be set up, and if a CJVhas no legal person status, a joint managementcommittee shall be set up as the CJV’s authority�The profits of a CJV are allowed to be sharedby participants as specified in the joint venturecontract, and not necessarily in proportion totheir capital contribution� As a result, this type ofventure is idealwhen the foreign investor is onlylooking forashort-termproject�Afterobtainingafairorpremiumreturnon investment, the foreigninvestor returns themajority or full ownership oftheenterprisetotheChinesepartner�

A cooperative venture does not require a newbusinesslicenceifitisarrangedincontractualformunder the auspices of an existing joint ventureenterprise�Therearenoexpiryperiodsorlimitationsonthelengthoftheventure�Thecontractualtermscanberenewedatanytimeandforanyextendedperiod,subjecttotheapprovalofthegovernment�

Investment contributions fromeachparty arenotlimitedtofinancialcapitalbutmayalsoincludenon-financialassetssuchasintellectualpropertyrights,buildings, materials or machinery� The foreignparty’s investment in a cooperative joint venturethat has obtained the status of a Chinese legalperson in accordancewith the law shall generallynotbelessthan25%oftheregisteredcapitalofthecooperativejointventure�

equIty JoInt venture (eJv)AnEJVistypicallyalimitedliabilitycompanyusedforlong-termprojectsandrequiredtoberegisteredas a legal person� The main feature is that theprofits, risks and lossesof theEJV shall be sharedbythepartiestotheventureinproportiontotheirrespectivecontributionstoitsregisteredcapital�

Theminimum level of foreign participation in anEJVis25%oftheregisteredcapitalingeneral�Theregisteredcapitalisnotlimitedtofinancialcapital,butmayalsoencompassnon-financialassetssuchasintellectualpropertyrights,buildings,materials,ormachineryifapprovedbythegovernment�

types of BusIness entItIes

China’s Company Law recognises two types ofcompanies:

lImIted lIaBIlIty company There is no minimum capital contributionrequirement for this typeof entity�The registeredcapital of a limited liability company shall be thetotalcapitalcontributionssubscribedforbyalltheshareholders as registered with the registrationauthority�Thecapitalmaybecontributed incash,in kind or with intellectual property rights, landuse rights or other non-monetary assets whosevaluemay be assessed in financial terms and theownershipmaybe transferred in accordancewiththelaw�

company lImIted By shares A company limited by sharesmay be establishedeither by way of promotion or by way of stockflotation�Also,itshallhavenolessthantwoandnomorethan200promoters,ofwhomamajorityshallbedomiciledwithintheterritoryofChina�

Whereacompany limitedbyshares isestablishedby way of promotion, its registered capital shallbe the total share capital subscribed for by all itspromotersasrecordedbythecompanyregistrationauthority�

Whereajointstocklimitedcompanyisestablishedby way of stock flotation, its registered capitalshall be the total paid-in capital as recorded bythecompany registrationauthority�Establishmentbyshareoffer issubjecttotheapprovalofChina’sSecuritiesRegulatoryCommission�

foreIGn Invested entItIes

Foreign investors are allowed to register thefollowingtypesofentities:

cooperatIve JoInt venture (cJv)ACJVhas theoption to registerasa legalpersonwith limited liability, but it is notmandatory�Theparties in a CJV have the flexibility of choosingwhether to operate the enterprise as a limited

Doing Business in China 2017 9

BusIness entItIes

inthethreeconsecutiveyearspriortotheoffer�

The minimum level of foreign participation in aCLSFIis25%�ACLSFIcanbelistedeitherlocallyorabroad�

BuIld-operate-transfer proJect (Bot)BOTprojectsprovideenterpriseswithconcessionsfor key industrial or infrastructure projects inChina, such as bridges, railways, industrial parks,power plants, airports, subways and expressways�After financing and building the project, theenterpriseeitherimmediatelytransferstheprojectto another party or continues to operate it for anumberofyears�Whentheagreed-uponequitablereturnoninvestmentisachieved,theenterpriseisrequired to transfer full ownership and control tothe government�The terms, limitations, rules andregulations pertaining to BOT projects are oftenestablishedonanadhocbasis�

▪ The enterprise undertaking the project musttaketheformofalimitedliabilitycompany�

▪ Theregisteredcapitalshouldbeatleast25%oftheproject’stotalinvestment�

▪ The projects are usually established throughconditional franchise agreements that cannotexceed30years�

holdInG companyThe number of approved holding companiesin China is increasing� A holding company is anumbrella-structure arrangement that enablesa foreign company to hold together its jointventureandWFOEinvestmentsinChina�AholdingcompanycaneitherbeanEJVoraWFOE�Generally,thegovernmentallowsaforeigncompanytosetupawhollyforeign-ownedholdingcompanyinChinaif ithasagood reputation,financial strength,andadvanced technology, and undertakes projectsthatareinlinewiththestatepoliciesforindustrialsectors�

foreIGn-Invested partnershIpAforeigninvestedpartnershipmayhaveanumber

A party to a joint venturemay transfer its sharesin the registered capital onlywith the agreementoftheotherparty�Equitycannotbetransferredorwithdrawnunderanyscenariowithouttheapprovalofthegovernment�

There are registered capital/total investment ratiorequirementsthatneedtobeobserveddependingontheinvestmentsizeoftheventure�Pleasereferto the Establishment Procedures section of thisguidefordetails�

wholly foreIGn-owned enterprIse (wfoe)AWFOEreferstoacompanywhollyownedbyoneormoreforeigninvestors�TheWFOEisnowapopularoption for foreign businesses, as the investormay enjoy complete control over the businessentity and reap the full profit from its operation�Moreover,WFOEsalsoprovidebetterprotectionfortheinvestor’sintellectualpropertyrightscomparedwithothertypesofentities�

Theoperationtermvariesaccordingtothenatureof the enterprise; any extension of the operationterm is subject to the approval of the relevantgovernment authority� The establishment ofexport-orientedorhigh-techWFOEsisencouraged�

AWFOE can also set up a subsidiary inmainlandChina,which is recognisedas aChinesedomesticcompany�

company lImIted By shares wIth foreIGn Investment (clsfI)ACLSFIgenerallyadoptsthepromotionmethodforitsestablishment,whileshareisalsopermitted�

ACLSFIsetupbymeansofpromotionshallhavenofewerthantwobutnomorethan200initiators,ofwhomhalformoreshallhaveadomicileinChina�At leastoneof thepromotershas tobea foreignshareholder�

An EJV, CJV orWFOE may apply to convert to aCLSFI through a share flotation� Other than therequirements in theprecedingparagraph,aCLSFIestablishedbyashareflotationneedsatleastonepromoterthathasatrackrecordofbeingprofitable

10

IncorporatIon of BusIness entItIes

approval and reGIstratIon procedureTheapprovalofaforeigninvestmententerprise(FIE)in China depends on the nature of the proposedproject� In 2015, the National Development andReform Commission and Ministry of Commercein China released the updated“Catalogue for theGuidanceofForeignInvestmentIndustries”circular,which took effect on 10 April 2015� Under theCatalogue, foreign investment projects fall underthreecategories:

▪ EncouragedProjects

▪ RestrictedProjects

▪ ProhibitedProjects

Investmentprojectsthatdonotfallundertheabove-mentionedthreecategorieswouldberegardedaspermittedprojects�Differentpolicieswill apply todifferentcategoriesofprojects�Generally,itwouldbe easier to set up an FIEwithin the EncouragedProjectsorPermittedProjectscategoryandtheFIEcould enjoymorepreferential treatment from thebusiness and tax perspectives� Otherwise, therecouldberestrictionsontheformofinvestment(e�g�requirementsontheamountofinvestmentcomingfromtheChineseparty) forsomeoftherestrictedprojects�

The Ministry of Commerce (MOFCOM) and StateAdministration for Industry andCommerce (SAIC)have overall responsibility for approving theformation of FIEs, issuing approval certificates,and generally undertaking the examination andapprovalprocedures�Undernormalcircumstances,the following documents should be submitted tosupport the application: Project Proposal, Letterof Intent, Feasibility Study Report, Articles ofAssociation, Joint Venture Contract etc� However,thelistofdocumentsrequiredforsubmissionmayvary depending on the requirements of the localauthorities�

of foreign investors (either corporate or naturalpersons) and potentially Chinese investors� Thestateencouragesforeignenterprisesorindividualswith advanced technology and managementexperience to establish partnerships to promotedevelopment of the related industries in thedomesticmarket�

Ageneralpartnershipconsistsofgeneralpartnerswhobearunlimitedjointandseveralliabilityforthedebts of the partnership�Where there are specialprovisionsinthePartnershipEnterpriseLawontheformsof liabilitybornebygeneralpartners, thoseprovisions shall prevail� A professional entitywithspecialisedknowledgeandskillsthatprovidespaidservicestoitsclientsmayformaspecialisedgeneralpartnership�

A limited liability partnership consists of generalpartners and limited partners, with the formerbearingunlimitedjointandseveralliabilityforthedebts of the partnership and the latter bearingliabilityforsuchdebtsrespectivelywithinthelimitsof the capital contribution for which they havesubscribed�

Ageneralpartnermaymakecapitalcontributionsin cash or in kind, or in the form of intellectualproperty rights, land-use right or other propertyrights,orlabourservices�Alimitedpartnershallnotmake capital contributions in the form of labourservices�

representatIve offIce (ro)Before actually investing in China, many foreigninvestorschoosetoestablishrepresentativeoffices(ROs) to engage in market research and learnmoreabout thecountry�AnRO isoptionalbeforemaking an actual investment in China� It is notan independent legal entity andmust confine itsactivitiestopromotionoractingasa liaisonofficeonbehalf of itsheadoffice�AnRO isnot allowedto generate revenue, solicit business, engage inwarehousing or sign contracts with customers� Itcanhirelocalstaffthroughapprovedemploymentagencies�

It shouldalsoengage inactivities that service theheadofficedirectly�

BusIness entItIes

Doing Business in China 2017 11

In2015,theOrganisationCodeCertificateandTaxRegistrationCertificatewerecombinedwiththeBusinessLicence(“NewBusinessLicence”)�TheAdministrationofIndustryandCommercewillissuetheNewBusinessLicencewithin10workingdaysuponsuccessfulsubmissionoftheapplicationdocuments�Within30daysoftheissuanceoftheNewBusinessLicence,theFIEmustregisterwiththelocaltaxauthority�

comparIson of maIn Investment vehIcles

WFOE EJV CJV RO

advantages

• Foreigninvestorhasfullequitycontrolandmanagement

• Chinesepartnermayprovideland,building,equipmentaswellasexistingcustomers

• CollaborationwithChinesepartnerswhoholdaspeciallicenceinindustriesnotopentoWFOEs

• Profitsandrisksareclearlysharedinproportiontotheequityofeachpartner

• Chinesepartnermayprovideland,building,equipmentaswellasexistingcustomers

• CollaborationwithChinesepartnerswhoholdaspeciallicenceinindustriesnotopentoWFOEs

• Flexiblearrangementonformofcooperation,profit/responsibilitysharingetc�accordingtoitsJointVentureContract

• Foreigninvestorisallowedtorecoveritscapitalinvestmentuponcertainagreement

•Quickestwaytosetup

• Lowerriskforpurposeofinitialmarketassessment

disadvantages

• CannotsetupWFOEinspecificindustries

• Foreignpartnercanonlycontributeupto49%ofregisteredcapitalinspecificindustries

•Doesnothavefullequitycontrolandmanagement

• Cannotengageindirectbusinessactivitiesorenterintocontracts

•Mustengagelocalagenttohirelocalstaff

equity holding

• Foreigninvestor(s)contribute100%ofregisteredcapital

• AtleastoneforeigninvestorandoneChineseinvestor�Normally,foreigninvestorcontributesatleast25%ofregisteredcapital

•Notapplicable

Governance

•Onelegalrepresentative

•OneExecutiveDirectororBoardofDirectors(BOD)comprisingatleastthreedirectors

• ASupervisororBoardofSupervisorsshallalsobeappointed

•Onelegalrepresentative

• BODcomprisingatleastthreedirectors

• ASupervisororBoardofSupervisorsshallalsobeappointed

•Onelegalrepresentative

• BODcomprisingatleastthreedirectorsorJointManagementCommittee

• ASupervisororBoardofSupervisorsshallalsobeappointed

• ChiefRepresentative

tax

• Subjectto:enterpriseincometax,valueaddedtax,individualincometax

• Enjoytaxincentivessuchas“ReducedTaxRateforQualifiedAdvancedandNewTechnologyEnterprises”

• AvoidanceofDoubleTaxationAgreementsapply

•Generally,taxableonadeemedincomebasis,mainlyforenterpriseincometax,VATandindividualincometax(fordetails,pleaserefertoTaxationsection)

BusIness entItIes

12

WFOE EJV CJV RO

reporting and compliance

•Monthly/QuarterlytaxfilingandAnnualCombinedFiling •Monthly/QuarterlytaxfilingandAnnualAudit

lead time to establishment

• 2–4monthsforbusinessesthatdonotrequirespeciallicences(uponsubmissionofrequireddocuments)

• 3monthsforbusinessesthatdonotrequirespeciallicences(uponsubmissionofrequireddocuments)

• 1–2months(uponsubmissionofrequireddocuments)

estaBlIshment procedures

Thisisasimplifiedillustrationforreferencepurposesonly�

Requireddocumentsprovidedbyforeigninvestor

Applyforandobtain:

• RORegistrationCertificate

• ChiefRepresentativeCertificate

Applyforandobtain:

• Representative’sEmploymentPermit

• Representative’sForeignerResidencePermit

PrepareRO/companyseal,financialseal,chiefrepresentative/legalrepresentativeseal

OpenRMBbasicbankaccount,Openforeigncurrencycapitalbankaccount

(NotrequiredforRO)

Requireddocumentsprovidedbyforeigninvestor(s)

Applyforandobtainapprovalofname

Applyforandobtain:

• LetterofApprovalorCertificateofFiling

•NewBusinessLicence

Applyforandobtainitemssuchas:

• EmploymentPermit

• ResidencePermit

ApplyforandobtainForeignExchangeRegistrationCertificate

entI

tyK

ey

pers

on

nel

wfoe/Jvro wfoe/Jv

BusIness entItIes

Doing Business in China 2017 13

The contribution of the RC must be declaredthroughtheEnterpriseCreditInformationPublicitySystem within 20 working days from the date ofcontribution� IftheAdministrationof IndustryandCommenceverifiesthatanenterprisehasfailedtomakesuchadeclaration,itmayordertheenterprisetofulfilthisobligationwithinadefinitetimeperiod�

AnFIE is onlypermitted to repatriateprofits aftertax clearance has been obtained� Where FIEsare established with insufficient RC or TI, thecapital increase process can take a few monthsto obtain the necessary approvals� Foreigninvestors should therefore consider carefully theexpectedoperational funding requirementbeforedeterminingthelevelofTIandprofessionaladviceisencouragedinthisregard�

audIt requIrements

All foreign invested enterprises must appoint aChina-registeredCertifiedPublicAccountant(CPA)firmtoaudittheirfinancialstatementsattheendoftheaccountingyear(InChina,itison31December)andtoissueanauditor’sreport�Auditsarerequiredunder the company laws, accounting regulationsand income tax laws in China� Audited financialstatementsarealsousedfortaxreportingpurposes�Annualcorporateincometaxfilingsofnon-residententities(foreignenterprise’srepresentativeoffices)must be verified by a Certified Tax Agent (CTA)insteadofaCPAfirm�ButprovincialtaxbureausmaystillrequiresubmissionofaCPAreportfortaxfilingpurposes�The annual financial statements shouldbe submitted together with an auditor’s reportissuedbyaCPAfirmregisteredinChinawithinfourmonthsoftheendofthefiscalyear�(However,localauthoritiesmayimposeearlierdeadlinesincertaincases�)

The independentChinese auditor appointedby aforeigninvestedcompanyshouldbequalifiedandregistered with the Chinese Institute of CertifiedPublicAccountantstopractiseinChina�

capItal contrIButIonChina iscurrently implementinga“zeroregisteredcapital rule”, which means the authority will notverify a company’s capital injectionat the timeofregistration�Thisallowscompaniestocompletethebusiness registrationprocesswithout theneed toactuallyinjectanycapital�However,themethodofcapitalinjection,amountandschedulestillneedtobespecifiedinthecompanyarticlesofassociation�Thecapitalcontributionschemeisusedtoensureproper foreign investment goals and regulateinvestment behaviour� The registered capital ofan FIE refers to the capital registered at the StateAdministration for Industry andCommerce (SAIC)for establishment of the FIE, catering to the FIE’sinitialoperationalneeds�Theforeign investormayinjectcapitalaccordingtothecapitalcontributionscheme, but it is very difficult for FIEs to reducetheirregisteredcapitalduringtheoperatingperiodunderexistingregulations�

AfterthelatestAmendmenttoPRCCompanyLawbecameeffectiveon1March2014,theshareholderscan freely agree on the amount and contributionperiodbased on the actual needs� Capital canbecontributedbywayofcashandequipment,suchasproperties,plantandequipment(PPE),intellectualproperties (IP), and land-use rights� Registeredcapital (RC) is the total capital that should becontributedbytheshareholders�However,anotherrelated concept, “total investment”, should beconsideredbefore incorporation�Both theRCandtotal investment (TI) of an FIE need to be statedin its Articles of Association� The upper limit forloan financing (from bank / holding company) isrestrictedtothedifferencebetweentheTIandRC,whilealsobeingsubjecttothefollowingguidelinesforthedebt-equityratio�

TIMinimumRCRequirement

accordingtotheTI

LessthanUS$3million 70%ofTI

US$3–10million50%ofTIandnotlessthanUS$2�1million

OverUS$10–30million40%ofTIandnotlessthanUS$5million

OverUS$30millionorhigher

1/3ofTIandnotlessthanUS$12million

BusIness entItIes

14

Theliquidationcommitteeisrequiredto:

(1) Prepareastatementofassetsandliabilities;

(2) Notifycreditors;

(3) Managethecompany’sbusinessandoperationsduring the cessation period, but only to theextentthatthisrelatestotheliquidation;

(4) Obtaintaxclearance;

(5) Disposeofallassetsandsettleallliabilities;

(6) Distributesurplusassets to shareholdersaftersettlingallliabilities;and

(7) Representthecompanytosueortobesued�

When the liquidation committee prepares thestatementofassetsandliabilities,andifitisfoundthat the company has insufficient assets to settleallitsliabilities,thecommitteeshouldapplytotheCourtforadeclarationofbankruptcy�

When a bankruptcy declaration is made, theliquidation committee should hand over theliquidationaffairstotheCourt�

representatIve offIceWhen a foreign enterprise applies for closure ofits representative office due to the expiry of theresidence period or to terminate its businessoperations before the expiry, the following stepshave to be followed, according to theMinistry ofCommerce’sregulations:

(1) Submitanapplication;

(2) Settlealloutstandingliabilities;

(3) Obtaintaxclearancefromthetaxauthorities;

(4) Notify the State Administration for IndustryandCommerce;

(5) NotifyCustoms;and

(6) Notifyallotherrelevantauthorities(e�g�SAFE)

annual comBIned fIlInG

FIEs in China are required to undergo an onlineannual combined filing conducted by fourgovernment authorities, namely the Ministry ofFinance,MinistryofCommerce,StateAdministrationofTaxationandNationalBureauofStatistics�

Aspartofthefiling,FIEsarerequiredtomakeannualstatutory filings betweenmid-April and end-Junefollowingtheendofacalendaryear�Penaltieswillapplyfornon-compliance�

dIssolutIon and lIquIdatIon

lImIted lIaBIlIty company/company lImIted By sharesAcompanycanbedissolvedupon:

(1) Meeting the liquidation conditions in itsMemorandumandArticlesofAssociation;

(2) Approvalbyitsshareholders;

(3) Mergerordivision;

(4) TerminationbytheauthoritiesduetoviolationofChineselaw;or

(5) Shareholders’petitiontothepeople’scourttodissolvethecompanywhenthebusiness is inseriousdifficultiesthatwouldleadtosignificantlossesfortheshareholders

Any company that is dissolved due to (1), (2), (4),or (5) above shall be liquidated and a liquidationcommittee must be formed within 15 days� Ifthe company is a limited liability company, theliquidation committee must be formed by itsshareholders�Foracompanylimitedbyshares,themembersoftheliquidationcommitteehavetobeapprovedattheshareholders’meeting�

In the event that no liquidation committee isformed,creditorsofthecompanycanapplytotheCourttoenforcetheformationofthecommittee�

BusIness entItIes

Doing Business in China 2017 15

(3) Failureof the jointventureparties toperformtheircontractualobligationsundertheequityjoint venture agreement, such that the jointventureisunabletocontinue;

(4) Inabilitytocontinueoperationsduetofactorsoutsidethejointventureparties’control,suchasnaturaldisastersandwars;

(5) FailuretoachievetheobjectiveoftheEJV;or

(6) The joint venture meeting the terminationclausesasstatedintheagreement�

When the EJV is terminated on condition (2), (4),(5) or (6), the board of directors has to submitan application for termination to the originalexaminationandapprovalauthorities�

If the EJV is terminated as a result of one jointventure party failing to perform its contractualobligations (condition (3)), the non-performingparty is responsible for the losses and damagessufferedbythejointventure�

Upontermination,aliquidationcommitteewillbeformedtoadministerliquidationmatters�

wholly foreIGn-owned enterprIse (wfoe)AWFOEcanbeterminatedifoneofthefollowingconditionsismet:

(1) Uponexpiryoftheoperatingperiod

(2) Decisionbytheforeignshareholdertodissolveor liquidate when the WFOE is unable tocontinueitsbusiness

(3) Inabilitytocontinueoperationsduetofactorsoutsidetheforeignenterprise’scontrolsuchasnaturaldisastersandwars

(4) Bankruptcy

(5) Operatingagainstpublic interestandChineselaws

cooperatIve JoInt venture (cJv)Ajointventureagreementshouldstatetheexpiryofthejointventureortheprocedurestoterminatethe joint venture�ACJV canbe terminatedunderthefollowingcircumstances:

(1) Expiryoftheagreement;

(2) Inabilityoftheventuretocontinueitsbusiness;

(3) Failureof the jointventureparties toperformtheir contractual obligations under the CJVagreement, such that the joint venture isunabletocontinueoperating;

(4) The joint venture meeting the terminationclausesasstatedintheCJVagreement;or

(5) Terminationby theauthoritiesasa resultofabreachofChineselaws�

WhentheCJVisterminatedoncondition(2)or(4),theboardofdirectorshastosubmitanapplicationfor termination to the original examination andapprovalauthorities�

If the CJV is terminated as a result of one jointventure party failing to perform its contractualobligations (condition (3)), theother jointventurepartyhastherighttoclaimforlossesanddamagesagainstthenon-performingparty�Theperformingparty can also apply to the original examinationandapprovalauthoritiestoterminatetheCJV�

Upontermination,aliquidationcommitteeshouldbeformedtoadministerliquidationoftheCJV�

equIty JoInt venture (eJv)Thejointventureagreementshouldstatetheexpiryofthejointventureortheprocedurestoterminateit� An EJV can be terminated under the followingcircumstances:

(1) Expiryoftheagreement;

(2) Inabilitytocontinueitsbusiness;

BusIness entItIes

16

If thebankruptcompanyhasno remainingassetsfordistribution,theadministratorshallapplytotheCourttoconcludethebankruptcyadministration�

The introduction of the EBL demonstrates China’sintention to bring its insolvency framework inlinewith internationalpractices� Italsoprovidesadefined mechanism for foreign investors to dealwiththeirinvestmentsunderdistressedsituations�

For information or enquiries on our CorporateAdvisoryservices,pleasevisit:www�SBASF�com

(6) The WFOE meeting the conditions forterminationstatedintheArticlesofAssociationoftheWFOE

Based on Section 70 of the Detailed Rules of theWhollyForeign-OwnedEnterpriseAct, applicationfor termination can be submitted to the originalexamination and approval authorities whencondition(2),(3)or(4)aboveismet�Theexaminationand approval authorities’ approval date for thisapplicationshallbethedateoftermination�

Based on Section 71 of the same Act, if thetermination application is based on condition (1),(2), (3) or (6), a notice (the “Termination Notice”)has to be issuedwithin 15 days from the date oftermination to notify creditors� Within 15 daysfrom the date of issue of theTermination Notice,the WFOE has to table a liquidation proposaland nominate candidates to form a liquidationcommitteetoadministertheliquidation�

the enterprIse BanKruptcy lawThe Enterprise Bankruptcy Law (the “EBL”) wasupdated with effect from 1 June 2007� It waspreviously promulgated in 1986 in light of bothinternational and domestic experience with theobjectiveofensuringaclearerlegalbasisforformalbankruptcyproceedings�

TheEBLisapplicabletocompanies(whetherstate-orprivatelyowned) thatare insolventorat riskofbecoming insolvent�NaturalpersonsareexcludedfromthescopeoftheEBL�

TheEBLdefinesthepriorityofclaimsonabankrupt’sassetsasfollows:

(1) Securedclaims;

(2) Costs and expenses of the bankruptcyadministration;

(3) Employees’salaries,workman’scompensation,superannuation,etc�;

(4) Socialinsuranceandtaxes;

(5) Otherunsecuredclaims

BusIness entItIes

Doing Business in China 2017 17

foreIGn exchanGe controls

18

foreIGn exchanGe controls

overvIew of foreIGn exchanGe controls

rmB exchanGe rate reformTheRenminbi(“RMB”)orChinaYuan(“CNY”)istheofficialcurrencyinmainlandChina,andcomesintheYuan,Jiao,andFendenominations(1Yuan=10Jiao=100Fen)�

ThePeople’sBankofChinaisthenation’scentralbank(“CentralBank”),whichisresponsibleforformulatingtheexchangeratesbetweentheRMBandmajorforeigncurrencies(i�e�USD,EUR,HKD,JPYandGBP)�

AspartofeffortstoreformtheRMBexchangeratesystemsince2005,theCentralBanktookamajorstepon11August2015whenitadoptedthemiddleratethatismainlydeterminedbythemarket�However,theCentralBankcontinuestostrikeabalancebetweenensuringstabilityofitscurrencypolicyandexchangeratereforms�

The State Administration of Foreign Exchange (SAFE) is the authority in charge of foreign currency exchangecontrolinChina�

sImplIfIed domestIc and overseas dIrect Investment reGIstratIon procedureSince1June2015,SAFEhascancelledtheadministrativeexaminationandapprovalproceduresrelatingtoforeignexchangeregistrationapprovalsfordomesticandoverseasdirectinvestments�Instead,SAFEempowersbankstoreviewandhandlethedirectinvestment-relatedforeignexchangeregistrationandotherrelatedactivities�Theseincludefulfillingdutiessuchasexamination,reportingstatistics,aswellasmonitoringandrecord-filingofdomesticandoverseasdirectinvestmentswithinthescopeofSAFE’sauthorisationandundertheguidanceofSAFE�

Aftercompletingthedomesticdirectinvestmentregistration,theforeigninvestedenterprise(“FIE”)isallowedtoopenacapitalaccountinRMBoraforeigncurrencytocontributeitsregisteredcapitaltothiscapitalaccount�

enforcInG dIscretIonal foreIGn exchanGe settlement AnFIEcanremitforeignexchangecapitalinitscapitalaccountatitsdiscretionfrom1June2015�Theproportionofdiscretionarysettlementofforeignexchangecapitalofforeign-investedenterprisesistemporarilydeterminedas100%�TheSAFEmayadjusttheaforementionedproportioninduetimebasedontheinternationalbalanceofpaymentssituation�

remIttance of funds out of chIna

SAFEregulatesremittanceoffundsoutofChinaunderthetradingandcapitalcategories�

MajorcategoriesforremittingfundsfromChina:

No� TypeofRemittance Category KeyDocumentsRequired LegalCompliance

1 Purchaseofgoods Goods(tradeinnature)

• Purchasecontract

• Invoice

•Otherdocumentssupportingthispurchasetransaction

SAFEHuiFa[2012]No�38

2 Servicefeepayabletooverseasserviceprovider

Service(tradeinnature)

• Serviceagreement

• Invoice

•Otherdocumentssupportingthisservicetransaction

SAFEHuiFa[2013]No�30

Doing Business in China 2017 19

foreIGn exchanGe controls

No� TypeofRemittance Category KeyDocumentsRequired LegalCompliance

3 Dividendsandprofits Capital • ProofoftaxpaymentsubjecttoChina’staxregulations

SAFEHuiFa[2013]No�80

4 Foreignloans Capital • Foreignloanagreement

•OthersupportingdocumentsrequiredbySAFE

SAFEHuiFa[2013]No�19

ForinformationorenquiriesonourCorporateAdvisoryservices,pleasevisit:www�SBASF�com

20

taxatIon

Doing Business in China 2017 21

overvIew of chIna tax

types of taxesGenerally,taxesinChinaarecategorisedasfollows:

taxes on turnover:

▪ Valueaddedtax(VAT)

▪ Consumptiontax(CT)

▪ Customsdutyonexports/imports

taxes on property and transactions:

▪ Urbanlandusetax

▪ Realestatetax

▪ Vehicleandvesselusagetax

taxes / dues on natural resources:

▪ Resourcetax

▪ Taxontheoccupancyofcultivatedland

overvIew of Key tax rates

TaxCategory KeyTaxes TaxRate

TaxesonTurnover

VAT

• Salesofgoods,providingprocessing,repairormaintenanceservicesinChina,importinggoodsintoChina

• Leasingservicesoftangiblepersonalproperty

• Transportation,postalservices,basictelecommunications,construction,leasingofrealproperty,saleofrealproperty,ortransferofanylanduserights

• Apartfromitemsspecifiedabove(i�e�salesofservices)

• Foranycross-bordertaxableactivityconductedbyanentityorindividualwithintheterritory

ConsumptionTax

• “Luxurygoods”(tobacco,wines,cosmeticsetc�,dependsonthegood)

• Resource-intensivegoods

17%(basicrate),13%(reducedrate

forspecificproducts)

17%

11%

6%

0%

1%–45%

taxes on income:

▪ Individualincometax(IIT)

▪ Enterpriseincometax(EIT)

▪ Stamptax

▪ Landappreciationtax

▪ Contractualtax(Deedtax)

other taxes:

▪ Citymaintenanceandconstructiontax

▪ Educationsurcharge

taxatIon

22

TaxCategory KeyTaxes TaxRate

TaxesonIncome

IndividualIncomeTax

• Incomeonwagesandsalaries

• Productionandbusinessincome

•Others

EnterpriseIncomeTax

• Incomeofresidententerprises

• Lowertaxrate(e�g�HighTechnologyEnterprises)

• China-sourcedincomeofforeignenterpriseswithoutestablishmentinChina

• IncomeofforeignenterpriseswithestablishmentinChina,incomenotconnectedwiththeestablishment

3%–45%

5%–35%

20%–40%

25%

15%

10%to20%(withholdingtax)

10%to20%(withholdingtax)

admInIstratIon and reGulatIonsa) tax year

The taxyear is thecalendaryear�Taxquartersand taxmonthsarecalendarquartersandcalendarmonthsrespectively�

b) filing and payment

TypeofReturnPartyResponsible

forFilingFilingandPaymentDeadline

ValueAddedTax Taxpayer a) 1,5,10or15days’returnandpayment—within5daysofendofperiod�Finalreturnanddiscrepancyintaxamounttobesettledwithin15daysaftertheendofthefollowingmonth

b) 1month’sor1quarter’sreturnandpayment—within15daysfromtheendoftheperiod

c) Imports—within15daysafterCustomsissuesthetaxpaymentcertificate

d) Exports—applyforarefundoftaxpaidonamonthlybasis

ConsumptionTax Taxpayer a) 5,10or15days’returnandpayment—within5daysfromendofperiod�Finalreturnanddiscrepancyintaxamounttobesettledwithin15daysaftertheendofthefollowingmonth

b) 1month’sor1quarter’sreturnandpayment—within15daysfromtheendoftheperiod

c) Imports—within15daysafterCustomsissuesthetaxpaymentcertificate

CustomsDuty Taxpayeroragent Within15daysafterthedateoftheissuanceof

Customsdutypaymentcertificate

EnterpriseIncomeTax Taxpayer a) Quarterlyreturnandpayment—within15daysaftertheendofeachquarter

b) Annualreturnandpayment—within5monthsaftertheendofthetaxyear(togetherwithfinancialandaccountingrecords)

IndividualIncomeTax Withholdingagent(i�e�theemployer)

Within15daysaftertheendofeachmonth

taxatIon

Doing Business in China 2017 23

TypeofReturnPersonResponsible

forFilingFilingandPaymentDeadline

WithholdingTax Withholdingagent(i�e�purchaser)

Within15daysaftertheendofeachmonth

c) consolidated returnsChinagenerallydoesnotpermit thefilingofconsolidated returnsamonggroupcompaniesorcompaniesundercommoncontrol;eachcompanymustfileaseparatereturn�

d) statute of limitationsThestatuteoflimitationsforassessmentandcollectionisthreeyearsifanunderpaymentoftaxisduetothetaxpayer’sinadvertenterrorintaxcomputation(e�g�incorrectapplicationofaformula)�

TheperiodisextendedtofiveyearsiftheaccumulatedamountofunderpaidtaxisgreaterthanRMB100,000�Thestatuteoflimitationsperiodcouldbeupto10yearsforunderpaymentsofEITarisingfromtransferpricingissuesorarrangementswithoutabonafidebusinesspurpose�Thereisnostatuteoflimitationsfortaxevasion�

e) tax authoritiesTaxlegislationandpolicyaredevelopedjointlybyTheStateAdministrationofTaxation(SAT)andtheMinistryofFinance,withtheSATanditsprovincialandmunicipalofficesadministeringtaxationpolicies�EachlocalityinChinahasastatetaxbureauundertheSATandalocaltaxbureauunderboththeSATandthelocalgovernment�TheSATandstatetaxbureausaremainlyresponsibleforthecollectionandadministrationoftaxesthatcreaterevenueforthecentralgovernmentorrevenuethatissharedbetweenthecentralandlocalgovernments�

types of taxes

value added tax (vat)VATisanationaltax,withasinglerate imposedregardlessofthe locationoftheVATtaxpayer�VAT isgenerallyleviedonanypersonengagedinthesaleofgoodsortheprovisionofprocessing,repairorreplacementserviceswithinChina,aswellasontheimportationofgoodsintoChina�

TheVATreformpilotprogrammewaslaunchedinShanghaion1January2012followingtheChineseStateCouncil’sdecisionon26October2011�TheVAT reform (initiallyapplying to thenon-railway transportationandmodernservicesectors)hasbeenrolledoutnationwideandnewsectorshavebeenaddedtothescopeofthereform(i�e�railwaytransportationandpostalserviceshavebeenincludedwithinthescopeoftheVATreformsince1January2014;telecommunicationserviceshavebeenincludedsince1June2014)�

At the opening ceremony of theNational People’s Congress (NPC) held on 5March 2016, Premier Li Keqiangannouncedthateffectivefrom1May2016,VATwouldreplacethecurrentBusinessTax(“BT”)inallsectors,includingrealestate&construction,financial services& insurance,and lifestyle services (includinghospitality, foodandbeverage,healthcareandentertainment)�

TheVATreformaimstoresolvethedoubletaxationissuesarisingundertheindirecttaxsystem(becausenoVAT-likecreditmechanismisallowedundertheBTsystem,BTpaidcannotberecoveredbypurchasersagainsttheirownBTliability,norcanVATberecoveredbypurchaserswhoareonlyliabletoBT)andtofosterthedevelopmentofmodernserviceindustriesbygraduallytransitioningtheseindustriesfromliabilitytoBTtoliabilitytoVAT�

taxatIon

24

a) scope of vat:

• Salesandimportsofgoodsaswellastheprovisionofprocessing,replacementandrepairservices

• Since1August2013,thefollowingserviceshavealsobeensubjecttoVAT:modernservices,transportationservices,telecommunicationservicesandleasingoftangiblegoods

• Since1May2016,thefollowingserviceshavealsobeensubjecttoVAT:constructionservices,realestate,financialservices&insurance,lifestyleandotherservices

b) types of vat taxpayers:GeneralVATtaxpayersGeneralVATtaxpayersarethosewhosetaxablesalesvalueexceedsthethresholdofthesmall-scaletaxpayers�GeneralVATtaxpayerscandeductinputVATfromoutputVAT�Also,ageneralVATtaxpayermayincreasetheamountofpotentialoutputVATbecausegeneralVATtaxpayersareallowedtoissueVATreceipts�

If theturnoverofacompanyexceedsthethreshold, it ismandatory toapplyforthegeneralVATtaxpayerstatus�However,companiesbelowthatthresholdcanalsoapplytoberecognisedasageneralVATtaxpayer(subject to the approval of the supervising tax bureau)� once a small-scale taxpayer is recognised as a general taxpayer, the small-scale taxpayer status no longer applies even if its sales fall below the threshold in the future. [Note:Ageneraltaxpayerstatusneedstobegrantedbythetaxauthority�]

Small-scaleVATtaxpayersAsmall-scaleVATtaxpayerisonethathasanannualturnoverthatisbelowthethresholdasindicatedinthefollowingtable:

Activitythetaxpayerisengagedin Threshold(inclusive)

Productionofgoodsorprovisionoftaxableservices RMB500,000

Principallyintheproductionofgoodsortheprovisionof

taxableservices,andalsoengagedinthewholesalingorretailingofgoods

RMB500,000

Activitiesthatexcludewholesalingorretailingofgoods RMB800,000

c) calculation of vatTheVAT rate for a generalVAT payer is 17%,which is applicable to the provision of processing, repair orreplacementservicesandthevalueofproductsatimportation�Areducedrateof13%appliestocertainfood,goods,booksandutilities�Exportsaregenerallyzero-rated�TheratesundertheVATreformprogrammeareasfollows:17%fortheleasingofmoveableandtangiblegoods;11%forthetransportationsector,andpostalandbasic telecommunicationservices;and6%forvalue-addedtelecommunicationservicesandothermodernservices�Small-scaleVATpayerspayVATatarateof3%,butthereisnoinputVATcredit(i�e�thisisasimplifiedVATcalculationmethod)�

AftertheVATreform,thezeroratemaybeappliedtoR&D/designservicesprovidedtoforeignentitiesandinternational transportation services,whilequalifyingcross-border servicesmaybeVAT-exempt� InputVATincurredforzero-ratedservicesmayberefunded,butisunrecoverableforVAT-exemptservices�

taxatIon

Doing Business in China 2017 25

VATincurredonthepurchaseorconstructionoffixedassets(excludingimmoveableproperty)maybecreditedagainstoutputVAT�InputVATarisingfromthefollowingitems,however,isnotdeductibleagainstoutputVAT:

• Thepurchaseofgoodsandservicesforexclusiveuseinnon-VATtaxable,VAT-exemptprojectsorprojectssubjecttoasimplifiedVATcalculationmethod,welfareactivitiesorindividualconsumption

• Thepurchaseofyachts,motorcyclesandmotorvehiclesthataresubjecttoconsumptiontaxandforthetaxpayer’sownuse

• Goodsandrelevantservicespurchasedthatarelostinanunusualmanner

• Goodsandrelevantservicespurchasedandconsumedorusedforproductsorfinishedgoodsthatarelostinanunusualmanner

• Thepurchaseofpassengertransportationservices

AVATrefundmaybeavailableinanexportsituation�ExportsgenerallyattractazerorateofVAT,i�e�zerooutputVATonexport,alongwitharefundofinputVATincurredonmaterialspurchaseddomesticallyfortheexportofgoods�However,astheVATrefundraterangesfrom0%to17%,manyproductsdonotenjoyafullrefundofinputVAT�

d) administration and regulationsAcompanyisrequiredtoregisterwiththelocaltaxauthoritiesatthetimeofincorporationtohaveitsstatusrecognisedaseitherageneralVATpayerorsmall-scaleVATpayer�

VAT returnsaregenerallyfiled foreachcalendarmonthandmustbesubmittedbefore the15thdayof thefollowingmonth�A taxpayer that importsgoodsmustpay taxwithin15daysafter the issuanceof the taxpaymentcertificatebythecustomsauthorities�

consumptIon tax (ct)Consumptiontaxappliestotheproduction,processingandimportofprescribednon-essentialandluxuryaswellas resource-intensive goods, such as tobacco, alcoholic drinks, cosmetics, fuel, expensivewatches, disposablewoodenchopsticks,yacht,golf,jewellery,cartyres,motorcyclesandmotorcars�Thetaxiscalculatedbasedonthequantityorpriceofgoodssoldorincertaincases,acombinationofboth�Forexample,thetaxrateforgasolineisRMB0�2alitreandthereforebasedonthequantity�Ontheotherhand,thetaxrateforcigarsis40%ofthesalesprice�

The proportional consumption tax rate ranges from 3% to 56% on the revenue of different types of goods�Consumptiontaxpaidonexportsisfullyrefundable�

customs dutyImportdutiesareleviedatbothgeneralandpreferentialrates�ThepreferentialratesapplytoimportsoriginatingfromcountriesorregionsthathavesignedagreementswithChinacontainingreciprocalpreferentialtariffclauses,andthegeneraltariffratesapplytoimportsoriginatingfromallotherjurisdictions�However,iftheStateCouncilCustomsTariffCommissiongrantsspecialapproval,preferentialtariffratesmaybeappliedtoimportsthatwouldotherwisebesubjecttothegeneralrates�

taxatIon

26

Toencourage foreign investment, foreign investmententerprises (FIEs) thatmeetcertainrequirementsmaybeexemptfromcustomsdutiesontheimportationofmachineryandequipmentforself-use�

a) customs valuationImportcustomsdutyisleviedbasedontheCostInsuranceFreight(CIF)value�ExportcustomsdutyiscalculatedbasedontheFreeonBoard(FOB)priceofgoodslessexportduty�

b) reduction and exemptionCustomsdutieswillbereducedorpayersareexemptfromthemunderthefollowingcircumstances:

ReductionorExemption Exemption

•Goodsdamaged,destroyedorlostenroutetothecustomsterritoryoratthetimeofunloading

•Goodsdamaged,destroyedorlostduetoforcemajeureafterunloadingbutpriortorelease

•Goodsdiscoveredtobealreadyleaking,damagedorrottenatthetimeofthecustomsinspection,providedthatthedamageisproventobeduetoreasonsotherthanimproperstorage

• Commoditiescoveredbyconcludedinternationaltreaties

• Applicabletocertainareas(bondedareas,economicdevelopmentzones,etc�)

• Importedgoodswithspecialusage(scientificresearchandeducationalpurposes,fordisabledpersons,fordesignatedenterprisescoveredbythe“DomesticComponentContent”policy,etc�)

• Commoditiesundercertainspecialtrademodes(processingtrade,consignmentsales,etc�)

• ConsignmentofgoodswheretheestimatedcustomsdutyislessthanRMB50

•Advertisingmaterialandsamplesofnocommercialvalue

•Goodsandmaterialsthatarerenderedgratisbyinternationalorganisationsorforeigngovernments

• Fuel,stores,beveragesandprovisionsforuseenrouteloadedonanymeansoftransport,whichareintransitacrossthefrontier

• Exported/importedgoodsthatareshippedbackinto/outofthecustomsterritoryforjustifiedreasons

• Certainmachineryandequipmentimportedforself-usepurposesbyFIEsunderprojectscategorisedasencouragedorrestricted

c) temporary exemptionCustoms may grant temporary exemption treatment to Temporary Import / Export Commodities� Thesecommoditieshavetobereshippedoutoforintothecustomsterritorywithinsixmonths�AguaranteeletterorsecuritydepositofanamountequivalenttothecustomsdutymustbesubmittedtoCustoms�

Itemsthatqualifyfortemporaryexemptionincludetradesamples,exhibits,engineeringequipment,vehiclesandvesselsforconstruction,instrumentsandtoolsforinstallation,cinematographicandtelevisionapparatus,containers,theatricalcostumesandparaphernalia�

d) payment of customs dutyThepayeroritsagentshallmakeatimelycustomsdeclarationandsettlethecustomsdutywithin15daysaftertheissuancedateofthecustomsdutypaymentcertificate�Latepaymentpenaltieswillbeimposedat0�05%dailyontheoverduecustomsduty�

enterprIse Income tax (eIt) Resident enterprises have to pay enterprise income tax on their worldwide income� Foreign companies withan establishment need to pay income tax connected to this establishment� Foreign companies without anestablishmentaresubjecttoenterpriseincometaxonincomederivedfromwithinChina�

taxatIon

Doing Business in China 2017 27

a) tax formulaTaxliability=[Totalrevenue–Non-taxablerevenue–Tax-exemptrevenue–DeductibleCosts–DeductibleExpenses–Losses]xApplicabletaxrate–Taxcredit

• Thestandardtaxrateis25%�Forhighandnewtechnologyenterprises,therateis15%�

• Taxreductionsareavailableforenvironmentallyfriendlyprojects�

b) tax registrationEnterprisesarerequiredtoregisterwiththelocaltaxauthoritieswithin30daysfromthedateofobtainingthebusinesslicenceorbusinessregistrationcertificate�

Anon-residententerprisethathascontractualprojectsorprovidesserviceswithintheterritoryofChinashallregisterwiththetaxauthoritieswheretheprojectislocatedwithin30daysfromthedateofconcludingtheproject/servicecontract�

c) tax creditTaxcreditwillbeallowedontheamountofincometaxactuallypaid(inaccordancewiththeforeigntaxlaws)bytheenterpriseoutsideChina,fortheincomederivedbytheenterpriseoutsideChina�However,thecreditamount shouldnot exceed the amountofChina income taxpayableon the foreign-sourced income�Anyexcesstaxcreditcanbecarriedforwardforamaximumperiodoffiveyears�

d) assessment and administrationThetaxyearstartsonJanuary1andendsonDecember31�

All enterprises are required to submit provisional tax returns and advance tax payments on a monthly/quarterlybasis(tobedeterminedbythetaxauthorities)inRMB,within15daysaftertheendofthemonth/quarter�AnannualCIT return shouldbefiled togetherwith itsfinancialandaccounting reportsandotherrelevantinformation(e�g�relatedpartytransactionsannualreturn)withinfivemonthsfromtheendofeachtaxyearregardlessofwhethertheenterpriseisinaprofitorlossposition�Anydeficiencyshallbepaidwithinfivemonthsfromtheendofeachtaxyearandanyexcesspaymentshallberefunded�

EnterprisesinagrouparenotallowedtopayCITonaconsolidatedbasis,unlessapprovedbytheStateCouncil�

e) permanent establishment for non-resident enterpriseAnestablishmentorplaceisdefinedintheCITregulationsasanestablishmentorplaceinChinaengaginginproductionandbusinessoperations,includingthefollowing:

• Managementorganisations,businessorganisations,andrepresentativeoffices

• Factories,farmsandplaceswherenaturalresourcesareexploited

• Placeswherecontractorprojects,suchasconstruction,installation,assembly,repairandexplorationareundertaken

• Otherestablishmentsorplaceswhereproductionandbusinessactivitiesareundertaken

• Business agentswho regularly sign contracts, store and deliver goods, etc�, on behalf of the non-TaxResidentEnterprise

taxatIon

28

IndIvIdual Income tax (IIt)

a) payment and calculationWhetherornotforeignersworkinginChinaareliabletopayIITinChinadependsonseveralkeyfactors:

• Expatriate’slevelofincome

• Durationofstay

• Paymentsource

• Positionsheldbytheexpatriateinhishostcountryandhomecountrycompany

LevelofincomeTaxable incomeincludesthebasesalary, incentivecompensationssuchascommissionsandbonuses,cashallowancesandcontributionstoanoverseasinsurancescheme�

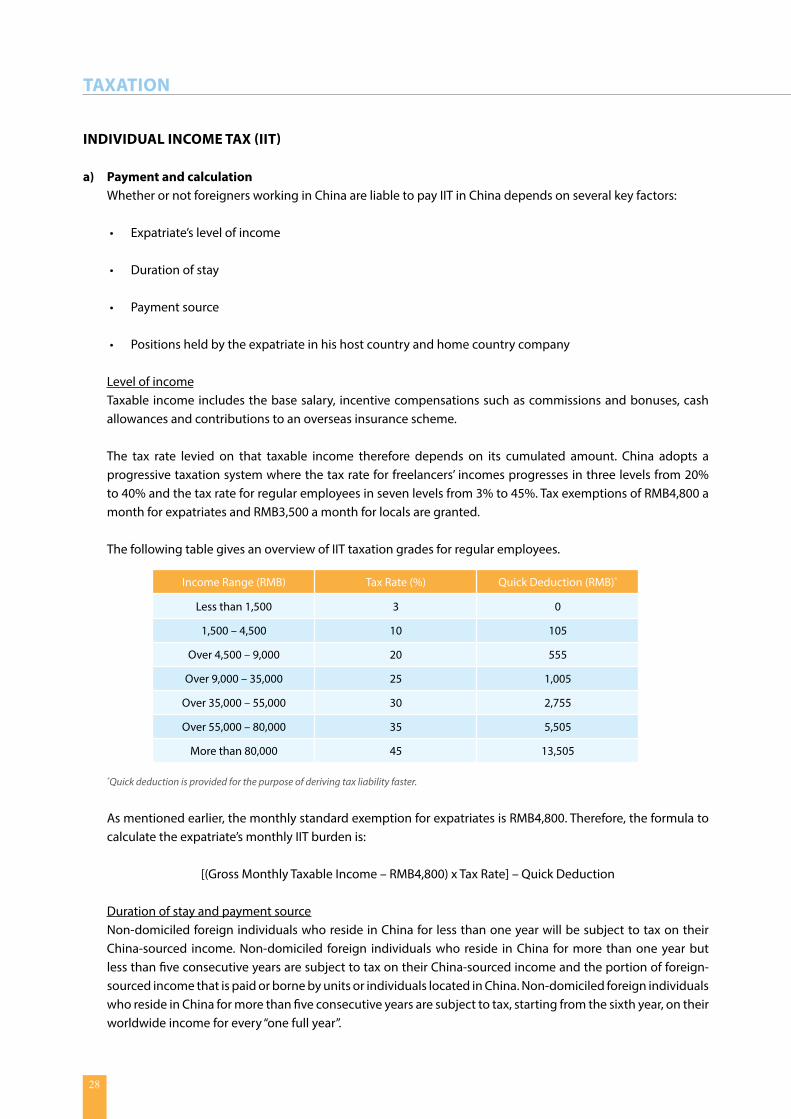

The tax rate levied on that taxable income therefore depends on its cumulated amount� China adopts aprogressivetaxationsystemwherethetaxrateforfreelancers’incomesprogressesinthreelevelsfrom20%to40%andthetaxrateforregularemployeesinsevenlevelsfrom3%to45%�TaxexemptionsofRMB4,800amonthforexpatriatesandRMB3,500amonthforlocalsaregranted�

ThefollowingtablegivesanoverviewofIITtaxationgradesforregularemployees�

IncomeRange(RMB) TaxRate(%) QuickDeduction(RMB)*

Lessthan1,500 3 0

1,500–4,500 10 105

Over4,500–9,000 20 555

Over9,000–35,000 25 1,005

Over35,000–55,000 30 2,755

Over55,000–80,000 35 5,505

Morethan80,000 45 13,505

*Quick deduction is provided for the purpose of deriving tax liability faster.

Asmentionedearlier,themonthlystandardexemptionforexpatriatesisRMB4,800�Therefore,theformulatocalculatetheexpatriate’smonthlyIITburdenis:

[(GrossMonthlyTaxableIncome–RMB4,800)xTaxRate]–QuickDeduction

DurationofstayandpaymentsourceNon-domiciledforeignindividualswhoresideinChinaforlessthanoneyearwillbesubjecttotaxontheirChina-sourced income�Non-domiciled foreign individualswho reside inChina formore thanoneyearbutlessthanfiveconsecutiveyearsaresubjecttotaxontheirChina-sourcedincomeandtheportionofforeign-sourcedincomethatispaidorbornebyunitsorindividualslocatedinChina�Non-domiciledforeignindividualswhoresideinChinaformorethanfiveconsecutiveyearsaresubjecttotax,startingfromthesixthyear,ontheirworldwideincomeforevery“onefullyear”�

taxatIon

Doing Business in China 2017 29

5-yearthresholdforindividualincometaxFiveyearsisanimportantthresholdfordeterminingexpatriateIITliability:anexpatriatewhoisataxresidentinChinaforfiveconsecutiveyearswillhavetopayPRCIITonhisglobalincome,nomatterwhereitwasderivedandbywhomitwasborne�Thismeansthatafterfiveyearsoftaxresidency,anexpatriatewillbetaxedinChinaonhis/herworldwideincome�Thisruleshouldalwaysbekeptinmind,sincegoingoverthe5-yearthresholdcansignificantlyincreaseanexpatriate’staxburden�

However,the5-yearthresholddoesnotnecessarilyapplytoeveryexpatriatewhowouldliketoliveinChinaforaprolongedperiodofmore than5years�Thereare twopossible scenarios inwhich IIT liabilityon theexpatriate’sworldincomecouldbeavoided�

Scenario1:BeforethefifthyearThefirstscenarioisthattheexpatriateleavesChina,beitforbusinesspurposesorforvisitinghishomecountry,formorethan90daysconsecutivelyormorethan30daysforasingletripwithinanygivenyearbeforehe/shehasbeenataxresidentfor5years�Bydoingthis,theexpatriatehasbrokentaxresidencyandthe“clock”forthe5-yearthresholdwillbereset�Forexample,theexpatriatecanarrangetoleaveChinaforthenecessarytimeperiodinthefifthyearofhistaxresidency�Uponhisreturn,taxresidencywillthereforebecountedfromyearoneagain�

Scenario2:AfterthefifthyearInthesecondscenario,theexpatriatemighthavemissedthedeadlineforleavingChinaforanappropriatenumberofdaysandhasalreadybeenataxresidentformorethan5years�Therearenowtwopossibilitiesfortheexpatriate:

(1) Forthesixthyear,theexpatriatecouldarrangetospendmorethan90consecutivedaysormorethan30daysinasingletripoutsideofChina�Thiswouldmeanthattheexpatriatehasbrokentaxresidencyinthisyear�AllofhisChina-sourcedincomewillbesubjecttoIIT,butnothisworldwideincome�However,thismeasurewillnot“resettheclock”ofthe5-yearthresholdandhastoberepeatedintheseventhandallsubsequentyears�

(2) If inthesixthyear,theexpatriatestaysinChinaforlessthan183/90days(dependingonthetaxtreatybetweenhis home country andChina), then tax residency is alsobroken�Only his/herChina-sourcedincomebornebyaChinaentitywillbesubjecttoIIT�Furthermore,the“clock”ofthe5-yearthresholdwillalsoberesetandthismeasurethereforedoesnotneedtoberepeatedeveryyear�Inotherwords,iftheexpatriatemanagestotraveloutofChinaformorethanhalf/threequartersofthesixthyear,the5-yearthresholdwillnotbeapplicableanduponhisreturn,taxresidencywillbecalculatedfromyearoneagain�

Othertaxableincome(e�g�freelancer)

• IncomederivedintheterritoryofChinasuchasfromdesign,decoration,installation,legal,accounting,consultancy,andlecturing

• IncomebelowRMB4,000:taxableincomeafterdeductingRMB800

• IncomeoverRMB4,000:taxableincomeafterdeducting20%

ChiefRepresentativeandRepresentativeofRepresentativeOfficeIftheexpatriateisactingastheChiefRepresentativeorRepresentative,his/herindividualincometaxliabilitiesmaybecomputedona“timeapportionment”basisaccordingtothenumberofdaysspentinChina�

taxatIon

30

b) tax registrationExpatriateswhoareliabletopayindividualincometaxarerequiredtoregisterwiththetaxauthoritieswithin30daysoftheindividualtriggeringthetaxableevent�

Whatistobeincludedinemploymentincome?

• Wages • Long-serviceawards

• Severancepayments

• Personaltaxespaidbyemployersonbehalfofemployees

• Dividends

• Allowances

• Subsidies

• Stockoptions

• Salaries

• Bonuses

• Year-endbonuses

Thefollowingfringebenefitsreceivedbyexpatriatesareexemptfromindividualincometax:

• Housing,mealandlaundryallowancesreceivedinanon-cashformoronareimbursementbasis

• ReimbursementofrelocationexpensesuponcommencementorcessationofChinaassignment

• Perdiem

• Homeleaveallowance—twotripspercalendaryear

• Allowancesforlanguagetrainingandchildren’seducation

• Mandatorysocialsecuritybenefits

c) tax creditTaxcreditwillbeallowedontheamountofincometaxpaidbytheindividualoutsideChina,fortheincomederived by the individual outside China� However, the credit amount shall not exceed the amount of theindividual’sChinaincometaxpayableontheforeign-sourcedincome�Theexcesstaxcredit(aftersettingofftheindividual’sChinaincometaxpayableforthatyear)canbecarriedforwardforamaximumperiodoffiveyears�

d) assessment and administrationThetaxyearstartsonJanuary1andendsonDecember31�

Individualincometaxisassessedonamonthlybasis�AllChinesecitizensareallowedamonthlydeductionofRMB3,500�ExpatriateshavebeengivenamonthlydeductionofRMB4,800witheffectfrom1September2011�Thetaxableincome,afterthemonthlydeduction,willbetaxedonaprogressivebasisataraterangingfrom3%to45%�

Theemployerisprimarilyresponsibleforwithholdingindividualincometaxfromemployees�ThetaxwithheldshallberemittedtotheStateTreasurywithin15daysaftertheendofeachmonth�Otherwise,penaltieswillbeimposed�Inaddition,individualswithanannualincomeexceedingRMB120,000arerequiredtokeeprecordsofincomefromallsourcesandreporttothelocaltaxauthoritybyMarch31everyyear�

taxatIon

Doing Business in China 2017 31

urBan land use taxWhereenterprisesor individualsareusingstate-owned land in thecities,countysites,administrative townsorindustrialandminingareas,theurbanlandusetaxislevied�

Urbanlandusetaxiscalculatedonanannualbasisbymultiplyingtheareameasurementofthelandactuallyusedandthefixedquantitytaxrate�Thetaxratevariesdependingonthelocationoftheland�

real estate taxRealestate(property)taxisleviedonanannualbasisandpayableonaninstalmentbasis�Thelocaltaxauthoritieswilldeterminewhentherealestatetaxesarepayable�

Anindividual’sresidentialrealestateiscurrentlyexemptfromrealestatetaxunlessitisrentedout�

a) who pays the real estate tax?

Circumstance PersonResponsibleforPayment

Wheretherealestateisbeingusedbytheowner Owner

Wheretherealestateismortgaged Mortgagee

Wheretheownerormortgageedoesnotusetherealestate,orownershipoftherealestateisnotyetestablished

Custodianoruserofrealestate

b) calculation of real estate taxAnnualrealestatetaxpayable=TaxbasisxTaxrate

Circumstance TaxRate TaxBasis

Enterprisesusingtheirownrealestate

1�2% 70%to90%oftheoriginalvalueofrealestate

Enterprises/individualsrentingouttheirrealestate

12%or4%* Rentalincome

Individualsresidingintheirownrealestate

0% Notapplicable

* A reduced tax rate of 4% is applied to individuals renting out residential real estate.

vehIcle and vessel usaGe taxOwnersormanagersofvehiclesandvesselsusedwithin the territoryofChinaare requiredtopayvehicleandvesselusagetax�Taxisassessedonnettonnageofthevesselorvehicle,oronaperunitbasis�

assessment and administrationVehicleandvesselusagetaxisassessedonanannualbasiswithpaymenttobemadetogetherwiththecompulsorytrafficaccidentliabilityinsuranceformotorvehicles�

stamp dutyStamp duty, ranging from 0�005% (for loan agreements) to 0�1% (for leasing agreements, property insurancecontracts,warehousingandstoragecontracts)appliestoprescribedcontracts,writtencertificatesoftransferofpropertyrights,businessaccountbooksandpermits�Therateonsharetransactionsis0�1%forshareslistedonadomesticstockexchange�

taxatIon

32

Item Scope TaxRate

Purchaseandsalescontracts Contractsofsupply,pre-purchase,procurement,purchaseforanorganisationorenterprise,purchaseandsalecombinationsandcooperation,adjustment,compensation,barteretc�

0�03%ofthepurchaseorsalesprice

Processingcontracts Processing,specificorders,renovations,repairs,printing,advertising,mappingandtesting

0�05%oftheincomefromprocessingorotherrelatedactivities

Engineeringprojectreconnaissanceanddesigncontracts

Prospectingcontractsanddesigncontracts

0�05%ofthefeesreceived

Constructionandinstallationprojectcontracts

Constructioncontractsandinstallationcontracts

0�03%ofthecontractamount

Propertyleasingcontracts Contractsfortheleasingofhousing,vessels,aircraft,motorisedvehicles,machinery,toolsandequipment

0�1%oftheleasingfee

Commoditytransportationcontracts Contractsforthetransportofgoodsbycivilaircraft,rail,ship,riverandroadandcoordinatedtransportcontracts

0�05%ofthetransportcost

Storageandcustodycontracts Storagecontractsandcustodycontracts

0�1%ofthestorageorcustodyfee

Loancontractssignedbetweenbanksorotherfinancialinstitutionsandborrowers

Notincludinginterbankshort-termloansonwhichinterestiscalculateddaily�Receiptsshallbeusedasacontractandstampdutyshallbepaidasforacontract�

0�005%oftheamountborrowed

Propertyinsurancecontracts Property,liability,guarantee,andcreditinsurancecontracts�Receiptsshallbeusedasacontractandstampdutyshallbepaidasforacontract�

0�1%oftheinsurancepremium

Technologycontracts Technologydevelopment,transfer,consultancyandservicecontracts

0�03%ofthestatedvalue

Documentsoftransferofpropertyrights

Documentsoftransferofpropertytitles,copyright,exclusiverightofuseoftrademarks,patentsandproprietarytechnologyusagerights

0�05%ofthestatedvalue

Businessbooksofaccount Booksofaccountsforrecordingcapitalandcapitalsurplus

Booksofaccountsforothers

0�05%

RMB5perbook

Documentationofrightsandlicences Propertyownershipcertificates,industrialandcommercialbusinesslicences,trademarkregistrationcertificates,patentcertificatesandlandusecertificates

RMB5perdocument

taxatIon

Doing Business in China 2017 33

land apprecIatIon tax (lat)Gainsonthesaleof realproperty,netofdevelopmentcosts,aresubject to theLAT�LATapplies toall typesofland,constructionand immoveableproperty, includingcommercial, industrialandresidentialsites�Thecurrentregulationsprovideforadeductionofqualifyingfinancingexpenses,relatedtaxes,andadministrationandsellingexpenses,withprescribedcapsindifferentsituations�Asuperdeductionequalto20%ofthecombinedpropertydevelopmentandlandpurchasecost isavailabletorealestatedevelopmentcompanies�LATischargedinfourbandsrangingfrom30%to60%,dependingonthepercentageofgainrealised�

a) calculation of latLand appreciation tax is calculated on the value added gained by the entities or individuals through theassignmentoftheState-ownedlanduserights,buildingsandotherfacilitiesattachedtotheland�

Valueaddedgained=Incomederived(cashand/orotherassets)–Deductibleitems

Landappreciationtaxpayable=ValueaddedgainedxApplicabletaxrate–Quickcalculationdeduction

Deductibleitemswillinclude:

• Costofobtaininglanduserights

• Costofdevelopingtheland,includingconstructioncosts

• Marketingexpenses,managementexpensesandfinancialexpenses

• Taxes and dues relating to the transfer of State-owned land use rights, buildings and other facilitiesattachedtotheland

• Theassessedpriceforthetransferofoldbuildings

• OtherdeductionsspecifiedbytheMinistryofFinance

b) exemptionsTaxpayersareexemptfromlandappreciationtaxunderthefollowingcircumstances:

• Thevalueaddedamountoftheordinaryresidentialbuildingsconstructedandsoldbythetaxpayerforciviluseislessthan20%ofthedeductibleitems�

• The land is compulsorily acquired by the State due to State- or municipal-planned constructionrequirements�

• Subject to the approvalof the tax authorities, an individual is transferringhis/herordinary residentialpropertyduetoachangeofemployment�

• Thetaxpayerhadusedthepropertyashis/herprimaryresidenceforatleastfiveyears�

taxatIon

34

c) tax rates

ValueAddedAmount TaxRate QuickCalculationDeduction

Valueaddedamount<50%ofdeductibleitems 30% Notapplicable

Valueaddedamount>50%ofdeductibleitemsbut<100%ofdeductibleitems

40% Deductibleamountx5%

Valueaddedamount>100%ofdeductibleitemsbut<200%ofdeductibleitems

50% Deductibleamountx15%

Valueaddedamount>200%ofdeductibleitems 60% Deductibleamountx35%

contractual tax (deed tax)Where landuse rights or building ownership rights are transferredwithin China, the transferee enterprises orindividualshavetheobligationtopaydeedtax�Thetransferoflandorbuildingownershiprightsrefersto:

▪ ThegrantofState-ownedlanduserights

▪ Thetransferoflanduserights,includingsale,giftorexchange

▪ Buyingandsellingofbuildings

▪ Agiftofbuildings

▪ Theexchangeofbuildings

a) tax ratesThe deed tax ranges from 3% to 5%, and the actual rates will be determined by the provincial or localgovernments�

b) paymentTheobligationofthetransfereetopaydeedtaxarisesonthedatewhenthecontractforthelandorbuildingownershiptransferissignedorwhenthedocumentsfortheownershiptransferareobtained�

Thetransfereeisrequiredtofilethedeedtaxreturnwiththelocaltaxauthoritieswithin10daysfromthedateoftheobligationtopaydeedtax�Thelocaltaxauthoritieswillsetthetimelimitonwhenthetaxmustbepaid�Anylatepaymentwillincurapenaltyof0�05%perdayontheoverdueamount�

resource taxTheresource(naturalresources)taxisleviedonenterprisesandindividualsengagedintheexploitationofmineralproducts or theproductionof saltwithin the territory of China andwaters under the country’s jurisdiction�Anationwidereformoftheresourcetaxwaslaunchedin2011,changingthetaxbasisfromvolumetosellingpriceforcertaincategoriesoftaxableresources,e�g�,crudeoil,naturalgasandcoal�Formostothertaxableresources,thetaxisstillcalculatedbasedonthevolumeofproductssoldorself-used,atrevisedtaxrates�Theresourcetaxispayabletothelocalauthoritiesattheplaceofproductionorexploitation�

taxatIon

Doing Business in China 2017 35

a) taxable products and tax rates

Product TaxRate

Crudeoil 5%–10%ofsalesvolume

Naturalgas 5%–10%ofsalesvolume

Coal RMB0�30–5pertonne

Othernon-metallicmineralores RMB0�50–20pertonneorcubicmetre

Ferrousmetallicmineralores RMB2–30pertonne

Non-ferrousmetallicmineralores RMB0�40–30pertonne

Liquidsalt RMB2–10pertonne

Solidsalt RMB10–60pertonne

b) assessment and administrationPaymentshallbemadetothelocaltaxauthoritieswherethetaxableproductisminedorproduced�Thelocaltaxauthoritiesshalldeterminethetimelimitforpaymentasfollows:

BasisPeriod FilingandPaymentDeadline

1day

• Provisionalpaymentwithin5daysoftheendoftheperiod;and

• Finalreturnandanydiscrepancyinthetaxamountshouldbesettledwithin10daysfromthestartofthefollowingmonth�

3days

5days

10days

15days

1month Within10daysaftertheendoftheperiod

cIty maIntenance and constructIon tax and natIonal educatIon surcharGeThecitymaintenanceandconstructiontaxandnationaleducationsurchargeapplytoentitiesandindividualsthataresubjecttoVATorconsumptiontax�Thenationaleducationsurchargeisleviedataflatrateof3%,whiletheratesforcitymaintenanceandconstructiontaxdependonthelocationofthetaxpayerorwithholdingagent:7%foralocationinacity,5%foracountyandtownarea,and1%inotherlocations�

local educatIon surcharGeThelocaleducationsurcharge,whosecollectionmechanismisalmostthesameasthatofthenationaleducationsurcharge,mayapplyatthediscretionofthelocalgovernment�However,aftertheMinistryofFinanceissuedanoticein2010tourgealllocalgovernmentstoimposethelocaleducationsurchargeataflatrateof2%,withaviewtounifyingtheapplicationofthesurchargeacrossthecountry,the2%ratehasbeenappliedinallprovincesthroughoutChina�

wIthholdInG taxesa) dividends

A10%withholdingtaxondividendspaidtoanon-residentcompanyhasbeenineffectsince2008�

Previously, dividendspaidby aChinese companywith at least 25%of foreignparticipationwere exempt�It should be noted, however, that dividends paid out of pre-2008 earnings continue to be exempt fromwithholdingtax�The10%withholdingtaxmaybereducedunderanapplicabletaxtreaty�

taxatIon

36

b) InterestInterestisgenerallysubjecttoa10%withholdingtaxunlesstherateisreducedunderataxtreaty�InterestfromcertainloansmadetotheChinesegovernmentorresidententerprisesisexempt�

c) royaltiesThewithholdingtaxrateonroyaltiesandfeesarisingfromthelicensingoftrademarks,copyrightsandknow-howandrelatedtechnicalservicefeesisgenerally10%�Royaltiesaregenerallysubjecttoa6%VAT,exceptforpaymentsmadeinconnectionwiththeuseoftechnology,whereanexemptionmaybegranted�

d) wage tax/social security contributionsTheemployermustwithholdindividualincometaxonbehalfoftheemployeeandremitthedeductedamounttothetaxauthorities�

The employer must contribute approximately 20% of basic payroll to the state-administered retirementscheme�Theemployermustalsocontributetoamedicalinsurancefund,maternityinsurance,unemploymentinsuranceandwork-relatedinjuryinsurance�Thetotalemployercontributionmaybeuptoabout40%oftheemployee’sbasemonthly salary,although the ratescanvaryacross thecountry�Theemployee is requiredto contribute a certain percentage of his/hermonthly salary to the above-mentioned funds, subject to athresholdsetbythelocalauthorities�

ForeignindividualslegallyworkinginChina(includingbothlocallyhiredindividualsandthosesecondedfromabroadtoworkinChina)arerequiredtoparticipateinthesamesocialsecurityschemeasdescribedabove,unlessanexemptionisprovidedunderanapplicablebilateralsocialsecuritytotalisationagreement�However,enforcementmayvaryindifferentcities�

antI-avoIdance provIsIons

Theanti-avoidanceprovisionshavebeenincludedinthecorporateincometax(CIT)lawandapplytotaxpayerswhoenteredintotaxavoidancearrangements�Theseprovisionsarelistedbelow:

▪ Transferpricingrules;

▪ Controlledforeigncorporations(CFC)rules;

▪ Thincapitalisation;and

▪ Generalanti-avoidanceprovision