a guide to costing human rights - save the children's · 1.5 the role of costing within the...

TRANSCRIPT

A Guide to Costing Human Rights

Victor Steenbergen

2011

Author: Victor SteenbergenEdited by: S. J. ThomasTechnical editing: I. Bedi-ThomasGraphic design and layout: Martin Stuk [email protected]

Printed by: Printer.NL www.printer.nl/website/

First published in 2011 in The Netherlands byEqualinrightsLaan van Meerdervoort 702517 AN The HagueThe Netherlands

T: +31 (0)70 3644415F: +31 (0)70 3608982E: [email protected]: www.equalinrights.org

© Equalinrights 2011This work is published under the Creative Commons license and is available in digital format at www.equalinrights.org.

We gratefully acknowledge the financial support of ICCO, Bröt für die Welt, Norwegian Church Aid, Church of Sweden and DanChurchAid.

Table of Contents

AcknowledgementsIntroduction 9

Chapter1:FrontloadingHumanRightsintoGovernmentBudgets 11 1.1 Introduction 11 1.2 Frontloading human rights 11 1.3 Human Rights – A brief overview 12 1.4 The individual steps to frontloading human rights 15 1.5 The role of costing within the process of frontloading human rights 16 1.6 Conclusion 18

Chapter2:CostingHumanRights 19 2.1 Introduction 19 2.2 Concepts and definitions 19 2.2.1 What are costs? 20 2.2.2 Perspectives 21 2.2.3 Costing purpose 22 2.2.4 Unit costs 22 2.3 Conducting a cost analysis 22 2.3.1 Methods of costing 24 2.3.2 The ingredients approach 24 2.3.3 Gross costing 27 2.4 Costing human rights policies 29 2.5 The individual steps in costing human rights policy 30 2.6 Two hypothetical examples of costing human rights interventions 33 2.6.1 Hypothetical Example 1: Costing improved access to essential health services 33 2.6.2 Hypothetical Example 2: Costing improved basic access to water 36 2.7 Capacity-building for Costing Human Rights 38

Chapter3:CaseStudiesinCostingHumanRights 39 3.1 Basic costing analysis 39 3.1.1 Fundar in Mexico: The Maternal Mortality Project 39 3.1.2 Right to Food India: Costing a comprehensive package of right to food entitlements 40 3.1.3 Women’s Dignity in Tanzania: Where is the Money for Delivery Kits? 41 3.2 Costing from a rights-holder’s perspective 41 3.2.1 The People’s Budget, Kenya: Calculating the daily living expenses 41 3.2.2 The Right to Food India: Costing adequate calories. 42 3.2.3 The Housing Rights and Land Network Loss Matrix 43 3.3 Costing human rights legislature 43 3.3.1 The Domestic Violence Act in South Africa 43 3.3.2 The Child Justice Bill in South Africa 44 3.4 Alternative Costing Exercises 46 3.4.1 Costing the right to education in Guatemala 46 3.4.2 Costing food security interventions in Mozambique 48

Conclusion 50Bibliography 52

Acknowledgements

Many people have made considerable contributions to this document, and I am very grateful for all their suggestions, time, input and efforts. As such, this document really has been the product of a long, incremental process that I only joined very recently.

Firstly, I would like to thank the entire Equalinrights staff for their expertise, their patience and their time. Zairah Khan, project-officer for the Budgeting Human Rights project, requires considerable praise for her input into the Conceptual Framework. If I know anything about human rights and the human rights-based approach, it is entirely down to the persistent efforts of Lucy Royal-Dawson, who was able to answer every phone-call, and explain the same point once again. Finally, to Indira Bedi-Thomas and Cornelieke Keizer, thank you for putting your trust in me during my entire time at Equalinrights, and for the freedom I experienced.

For their comments and support in the production of this publication, I thank Waruguru Kaguongo (Researcher for the Centre for Human Rights), Ann Blyberg (Executive Director of the International Human Rights Internship Programme), Eitan Felner (Former Executive-Director of the Centre for Economic and Social Rights) and Akanksha Marphatia (Acting Head of International Education, ActionAid).

Many thanks also go out to the members of the ‘Global Initiative for Frontloading and Costing Human Rights’ (GIF). Special thanks to our partners ShelterForum, Centre for Human Rights and the Community Law Centre for hosting both Zairah and myself during our field visits, which really showed us the daily realities of human rights advocacy. Lastly, many thanks to Women’s Dignity for their open and helpful interviews.

9AGUIDETOCOSTINGHUMANRIGHTS

Realising any human right (civil, political, economic, social or cultural) requires resources to adequately fund the necessary personnel, infrastructure and other prerequisites. Government budgets therefore have crucial implications for the realisation of human rights because human rights laws and policies can only have an impact on people’s lives when these are also supported by government budgets to finance them (FAO, 2009). Yet, too often have governments adopted laws and policies that failed to be implemented due to insufficient funding (UNICEF, 2010).

Adopting a law to protect the fundamental human rights of women who have been the victim of domestic abuse, for instance requires financial resourcing. To grant police-officers, lawyers and judges enough time to investigate the case and issue a protection order, their salaries need to be paid. In the South African ‘Domestic Violence Act’, although the law was adopted, insufficient resources were made available to implement the law. This meant that the criminal justice system could not take on the cases of vast numbers of women, who were left helpless and traumatised by family violence (Vetten, 2005).

It is in this context that ‘Costing Human Rights’ offers its contribution to the existing tools of human rights advocacy. When a civil society organisation can define a policy’s implementation cost, it can claim human rights not only through policy, but also through a government’s budget allocations to advance the necessary policies, plans and programmes to realise human rights. When we know the level of resources required, we can also assess when a government’s actions are inadequate, and so set out a strong evidence-based case in human rights advocacy.

AimThe primary aim of this paper is to give an overview of all the central concepts and definitions relevant for costing human rights policy. In addition, this paper also attempts to improve the ability of civil society organisations to perform costing exercises by outlining the steps that every human rights costing analysis should take to identify the financial implementation costs of a human policy or intervention. We can then offer some recommendations for improving future practice by looking at some examples in the form of case studies.

While this paper aims to be a guide to human rights costing studies, it is in some parts biased towards the conceptual and closer to a methodological review. Interventions across human rights, across countries and across districts (local, regional or national) are likely to differ in the key questions to be addressed and will therefore imply different measurement approaches. For this reason, a detailed step-by-step user guide reflecting all the details within a human right, a country and scale is beyond the scope of a single paper. In our view, the production of such practical manuals will follow from applying these general guidelines to particular human rights interventions.

IntendedAudienceThis paper is written as an introduction for civil society organisations interested in human rights budget work, with a particular focus on calculating the cost of a human rights policy or intervention. The guide is intended for people who may not have had any previous experience with costing and as such does not require any specialist background in economics or accounting.

Introduction

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 10

Introduction

OverviewThis paper consists of three chapters. In the first, ‘costing human rights’ is placed within a wider process of frontloading human rights, and is defined as a methodological process that translates (inter)national human rights standards and obligations into the budget proposals required for effective implementation in public policy and budget cycles. The chapter offers a brief summary of Equalinrights’ conceptual framework for frontloading human rights (Steenbergen, 2011). It also contains an overview of the main characteristics and obligations of human rights. Lastly, we note that to take sufficient account of human rights requirement such as participatory processes or the need to identify the structural causes relating to limited realisation of the rights of marginalised groups, human rights-based costing should take place within the broader process of frontloading human rights.

In chapter two, we give an initial overview of the central concepts and definitions of costing, before introducing two central methods to conduct a cost analysis. Following this, we identify four steps that can guide the costing process of a particular human rights policy or intervention, and to conclude, we offer two hypothetical rights-based costing exercises to further elaborate on the methods of costing human rights policies.

In chapter three, we look at a number of case-studies for costing human rights. Due to the differences across human rights, and across context- and scale-specific elements of a human rights policy, it is not possible to provide a simple checklist of all that needs to be in place to ensure an effective costing-strategy. Therefore, the chapter illustrates different methodologies for different causes through a series of case-studies where human rights organisations have (tentatively) applied costing.

A GUIDE TO COSTING HUMAN RIGHTS 11

1.1IntroductionHuman rights are the moral rights that every human being possesses and is entitled to by virtue of being human. They are the claims that all people have to fundamental freedoms, entitlements and human dignity. These rights are enshrined in the Universal Declaration of Human Rights, the International Covenant on Civil and Political Rights (ICCPR) and the International Covenant on Social, Economic and Cultural Rights (ICESCR), collectively known as the International Bill of Human Rights.Indeed, by becoming a signatory to human rights covenants, a State places itself under a direct obligation to allocate sufficient public resources to the fulfilment of human rights (OHCHR, 2006). However, there is an inherent difficulty in holding governments accountable for their obligations to realise economic, social and cultural human rights, as noted by Roberston:

“[L]ittle progress has been made in creating a set of workable standards which are detailed, systematic, and authoritative and, as of yet, there is no answer to the question: What resources must be devoted to realizing ICESCR rights?” (Roberston, quoted in Felner, 2008).

In order to move towards a process where budget allocations reflect a State’s human rights obligations, it is necessary to identify the level of resources a government should allocate to advance the necessary policies, plans and programmes to realise human rights. In this document, we will refer to this methodological process to offer budget recommendations on the basis of (inter)national human rights standards as frontloading human rights. We will begin this chapter by introducing frontloading human rights. Next, we will provide a brief overview of the main characteristics and

obligations of human rights and human rights-based development. Subsequently, we will briefly describe the five steps that make up the methodological process of frontloading human rights. Lastly, we will highlight the role of costing human rights policy within the broader process of frontloading.

1.2FrontloadingHumanRights“From a human rights perspective, budgets are the concrete means by which governments either fulfil or violate human rights requirements. Just as, for many years, citizens of the world have come together to defend and expand our basic human rights, so now there is a global effort underway to bring citizens to the table, to monitor and influence government budget making.” (Promises to Keep, Schultz, 2002)

Civil society organisations have always been active proponents of human rights laws and policies, but only very recently has this advocacy begun to focus on government budgets. Government budgets have important implications for the realisation of human rights because human rights laws and policies can only have an impact on people’s lives when these are supported by government budgets to finance them (FAO, 2009). Too often have governments adopted laws and policies that were simply not implemented due to insufficient funding (UNICEF, 2010).

For this reason, many of the current tools and methods for human rights budgeting involves holding governments accountable for pre-made commitments, either through monitoring, tracking or analysing past government budgets allocations (Blyberg, 2009). Yet, while analysing past budget allocations helps scrutinise government budgets, it comes with a severe limitation. As argued by ‘Dignity Counts’ (2002):

Chapter 1: Frontloading Human Rights into Government Budgets

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 12

ChapterOne: Frontloading Human Rights into Government Budgets

“While an analysis of the budget can identify what has been spent or is being spent, it cannot ultimately determine what should be spent”

There is, therefore, a need for a methodology that can assist civil society organisations in claiming human rights not only through policy, but also to identify the resources a government should allocate to advance the necessary policies, plans and programmes to realise human rights. In contrast to other retrospective methods of human rights budgeting, the method of frontloadinghuman rights has therefore been developed by Equalinrights.1 This can be defined as a methodological process that translates (inter)national human rights standards and obligations into the budget proposals required for effective implementation in public policy and budget cycles (Steenbergen, 2011).

1.3HumanRights–ABriefOverviewBefore we discuss the individual steps for offering human rights-based budget recommendations, we will provide a brief overview of the main principles, characteristics and obligations of human rights. This section is a summary of the first chapter of Equalinrights’ conceptual framework for frontloading human rights (2011), which provides a more in-depth discussion of these concepts and obligations.

Human RightsHuman Rights, such as the right to health, education and adequate housing, are often misunderstood, or seen as mere indications of commitment to social policies covering health care, education policy or social housing. As a result, the implications a human right has on government action is also often misinterpreted (Diokno, 2008). The human right to the ‘highest attainable standard of health’, for instance, is not a right to be healthy, nor does it warrant

1 For more information, please see Victor Steenbergen (2011) ‘Frontloading Human Rights: A Conceptual Framework for Building Budgets and Realising Rights’, The Hague: Equalinrights.

maximising the total amount of healthy people in society. Instead, it encompasses a combination of ‘freedoms’ including the right to make decisions about one’s health and the right to non-discrimination, and ‘entitlements’, such as the right to culturally appropriate health services and a right to the underlying determinants of health, such as adequate sanitation, safe water, adequate food and shelter (Potts, 2009).

We can only understand what a human right means through its underlying principles. For instance, within the very concept of human rights lies the principle of universality; human rights can be claimed by every human being by virtue of being human. Related is their inalienability, which means that they cannot be taken away. Moreover, within the whole human rights framework, we see an interdependence and interrelatedness across human rights, so that the limited enjoyment of one human right affects the quality and enjoyment of another. Indeed, we cannot state that one right is more important than another because of their indivisibility; “they interact with each other, depend on each other and support each other to guarantee full human dignity” (Diokno, 2008).

Another underlying human rights principle is that all human beings are fundamentally equal, and entitled to their human rights without discrimination of any kind such as race, colour, sex, ethnicity, age, language, religion, political or other opinion, national or social origin, disability, property, birth or other status as explained by the human rights treaty bodies (UN Common Understanding, 2003).

The human right to “participate in the relevant decision-making processes” (CESCR, 2001) can also be seen as a fundamental human rights position, since such “active involvement in the determination of one’s own destiny is the essence of human dignity” (Robinson, in Potts 2009). A last key principle of human rights is that they are rights, so that States and other duty-bearers are accountable for

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 13

ChapterOne: Frontloading Human Rights into Government Budgets

their observance and have a legalobligationto comply with the standards enshrined in human rights instruments. When duty-bearers fail to comply with their duties, a rights-holder is entitled to “institute proceedings for appropriate redress before a competent court or other adjudicator in accordance with the ruleoflaw” (UN, 2003).

However, while these principles contribute to our conceptual understanding of human rights as a whole, they still do not provide sufficient clarity for, say, a government intending to adopt all the appropriate measures to realise the right to health. However, neither does the ICESCR – embodying the right to health - provide a great level of detail to define the meaning of the right to health. For this reason, the UN Committee on Economic, Social and Cultural Rights (CESCR) has issued “General Comments” which further identify a number of interrelated and essential elements that reflect both the freedoms and entitlements of each human right (Fundar, IBP, IHRIP, 2004). In this instance, CESCR argued that the freedoms and entitlements of the right to health are best divided into four normative elements: the availability of health facilities, goods and services; the accessibility of health services, physically (in distance), economically (in cost) and in a non-discriminating manner; the acceptability of health services in terms of ethics, culture, and gender; the qualityof health services (Diokno, 2008).

Human Rights Obligations“The term ‘human right’ is more than just a moral declaration. It is a legal concept with very specific meanings and ramifications laid out by human rights [instruments]” (Schultz, 2002).

By becoming a signatory of the international human rights covenants, a State places itself under a number of direct, legal obligations. These obligations are generally of three kinds: to respect, to protect and to fulfil (Maastricht guidelines, paragraph 6).

• Theobligationtorespect:a state should refrain from any action that would interfere with the enjoyment of rights of the people in its territory.

• Theobligationtoprotect: a state should prevent actions by others that might lead to a violation or a diminishing of the enjoyment of human rights.

• The obligation to fulfil: a state should take action to ensure the full realisation of rights. The duty to fulfil in turn has been divided into the obligations to facilitate, promote and provide. The State must facilitate people’s ability to secure their rights, that is to say the State must engage in activities to ensure that people have access to resources to ensure the full enjoyment of their rights. The State must also actively promote access to rights by, amongst other things, adhering to various procedural and administrative requirements. Finally, the State must provide that right directly where persons or groups are unable to enjoy the right, for reasons beyond their control.

A related principle of economic, social and cultural rights is the duty of “achieving progressively the full realisation of the rights recognised in the present Covenant to the maximum of available resources” (CESCR, 1994). By ratifying an international treaty, Governments are not expected to guarantee the full enjoyment of all rights immediately. In recognition of the time it takes to raise revenue, implement laws and policies, train personnel, set up the appropriate bodies to monitor and hear complaints, roll out social programmes, and so on, States are expected to show that they are taking steps which are “deliberate, concrete, targeted and appropriate” (CESCR, 1994).

While ‘progressive realisation’ offers governments a measure to prevent them from being over-burdened financially, no criteria have yet been developed for defining ‘maximum availability of resources’. Therefore,

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 14

ChapterOne: Frontloading Human Rights into Government Budgets

the concept is often conceived as a ‘get out’ clause for States unwilling to fulfil their human rights obligations by invoking resource constraints (Felner, 2009). This has been addressed by the Committee on Economic, Social and Cultural Rights by emphasizing that each human right has a set of minimumcoreobligations (CESCR, Gen. Com. 3). Even in the presence of limited resources, a government is required to give first priority to these minimum, essential levels of primary health care, food, housing, water and sanitation.

Contextualising Human Rights LawWe cannot define the ‘meaning’ of a human right only in relation to international human rights obligations. As explained in greater detail in Steenbergen (2011), because human rights content and obligations are only partly defined by international law, they are also partly defined by the contextual conditions within a country. For example, realising the right to water means something different for the most marginalised rights-holders in an Indian slum than it does for a rural Kenyan community, yet for both groups the right to water is an obligation that must be fulfilled. The meaning of a right is thus partly determined by the fundamental claims of marginalised rights-holders, and implies a human rights obligation. In order to offer human rights recommendations, therefore, there is a need to understand the position of the most marginalised groups in a society and to identify the structural causes for the limited realisation of their rights. Rather than deriving the meaning of a right entirely from human rights law, this also has to be determined in relation to the local conditions and fundamental claims of marginalised rights-holders.

Human Rights-Based Policy MakingIn sum, Steenbergen (2011) draws out a number of international human rights standards that human rights-based policy making is obliged to meet:

• The policies should prioritise minimum essential levels of service

• The policies should be non-discriminatory and prioritise the most marginalised groups

• The process in making the policies should be transparent and participatory

• The content of the policies should meet both the freedoms and entitlements, as identified by CESCR through a number of interrelated and essential elements of each human right. In addition, these elements should be contextualised by an understanding of the position of the most marginalised groups in society and the structural causes relating to their limited realisation of rights.

Human rights-based development thus requires services to be provided on the basis of human rights standards rather than, for instance, the standard of cost-effectiveness,2 or, on the basis of charity. Policy based on the latter standard may indeed be counter to human rights standards. For example, it might be more cost-effective to provide health care to urban communities, rather than marginalised but more expensive rural communities. This would actively discriminate against individuals who are already facing a greater lack of access to health care. Conversely, when a service is expressed as a right, it brings with it standards to which all rights-holders are entitled, and which trigger obligations. In this instance, an individual in the rural community should be able to hold the duty-bearer (most commonly, the government) accountable to make these services available to his or her community,

2 When human rights standards offer different conclusions than cost-effectiveness, the former takes precedence over the latter. Yet, cost-effectiveness can also prove an important expression of human rights standards as States should look for the most effective, equitable and sustainable method to realise human rights (see Steenbergen, 2011). For instance, a key issue for human rights budget groups is the inefficient spending of corrupt officials, who grant excessively costly contracts to friends or relatives and pocket the difference. Thanks to Ann Blyberg for this useful addition.

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 15

ChapterOne: Frontloading Human Rights into Government Budgets

and make them accessible, acceptable and of sufficient quality.

This example demonstrates that if we would move from other standards of service provision to rights-based services, common ground may already exist. In the case of the right to health, an existing service may already offer a high quality service that is physically and economically accessible, but which inadvertently discriminates against one community on the basis of its geographical location. In this case, making the service more human rights-compliant would require only countering the discriminatory basis of the health care centre, such as providing cheap forms of transportation to the centre, rather than requiring the development of a new right to health-policy entirely.

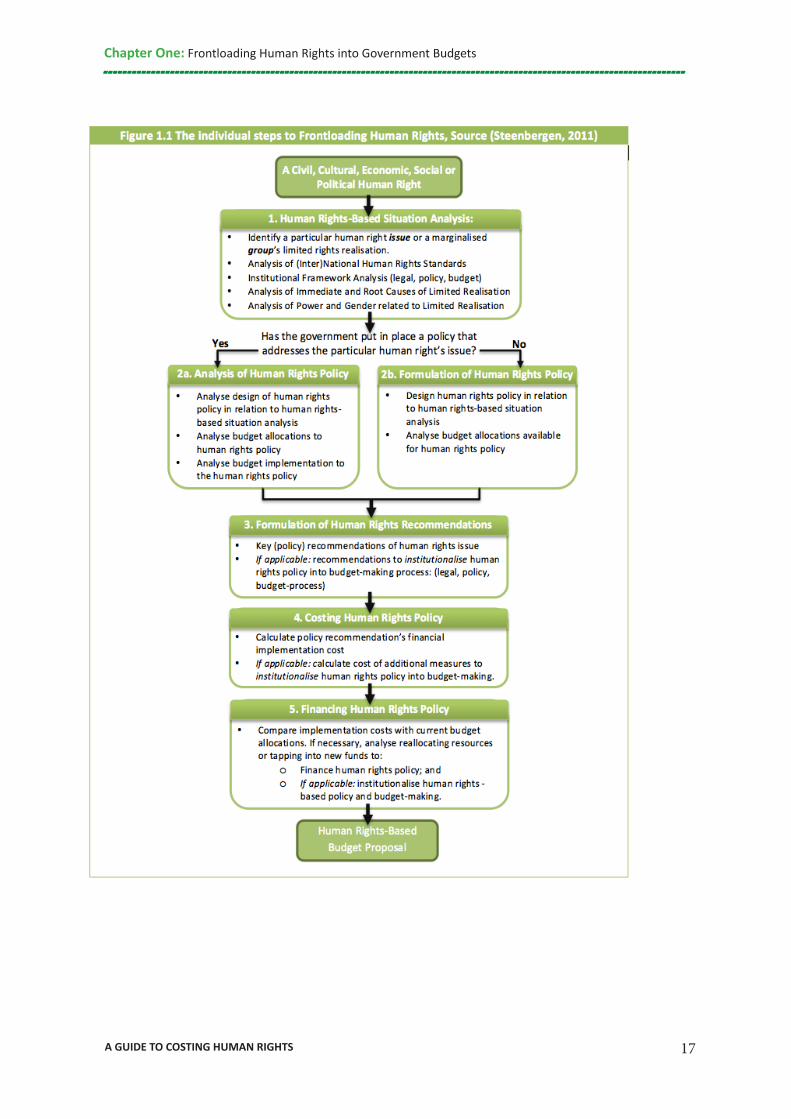

1.4 The Individual Steps to FrontloadingHumanRightsWe now move on to the individual steps required to offer human rights-based budget recommendations. The five steps that make up this methodological process have been described in Equalinrights’ Conceptual Framework for frontloading human rights (Steenbergen, 2011).

Starting from the basis of a particular human right

Human rights are made up of both freedoms and entitlements and their meaning partly determined by international law and partly contextually, by the local conditions of the most marginalised groups. This means that it is important to incorporate the following principles into the analysis:

• Rights-holders have a right to be protected from all forms of discrimination and the most marginalised rights-holders should be prioritised in realisation of human rights.

• Rights-holders have a right to have their views heard and to contribute to decision-

making processes when this affects their lives.

These guidelines, along with the other human rights principles, provide a point of reference to the realisation of human rights. For example, when analysing the most urgent human rights concerns, rights-holders in all categories (gender, age, class, caste, religion, region, etc.) should be enabled to participate in the data collection and analysis, and their opinions represented in the process. These human rights principles should thus be considered throughout the analysis.

Stage 1: The Human Rights-Based Situation Analysis

Analysing the situation of rights-holders is a necessary first step to identifying what needs to be done in order to improve their human rights realisation. Multi-dimensional analysis will also help to ensure that programmes and policies are better informed and more likely to achieve their intended objective (Save the Children, 2008). A human rights-based situation analysis begins by contextualising all elements of (inter)national human rights law and mapping any violations while outlining gaps in the fulfilment of the particular human right issue or marginalised group’s limited rights realisation. An understanding of the human rights-based approach connects this analysis with the institutional framework analysis of the legal system, the relevant policy frameworks and the budget process. This is then combined with an analysis of immediate and root causes of the limited realisation of the particular human rights issue under analysis. Lastly, this stage calls for an analysis of the power and gender concerns relating to the limited rights realisation, reflecting the political nature of human rights realisation.

Stage 2: The Analysis or Formulation of Human Rights Policy in relation to the Budget

In stage 2, we use the findings of the human rights-based situation analysis either to design a human rights policy or to analyse

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 16

ChapterOne: Frontloading Human Rights into Government Budgets

a pre-existing human rights policy for its design, budget allocation and budget implementation.3

While a government needs to develop effective policies, plans and programmes to realise human rights, it is not enough simply to pass a law or policy to advance human rights since there is no guarantee that this will translate directly into adequate budget allocations and spending. Therefore, it is important to determine first whether the existing human rights policy is designed in an appropriate way (i.e. it is not discriminatory, but addresses the structural causes of the limited rights), and subsequently, whether the current budget allocations are sufficient to ensure the policy’s implementation. Lastly, it is useful to assess whether any structural causes prevent that a policy’s budget allocations from being translated into spending.

Stage 3: Formulating Human Rights Recommendations

The third stage summarises the human rights recommendations made in relation to the human rights-based situation and policy analysis. At this stage, additional institutional recommendations can be formed to address the greatest obstructions to budgets reflecting human rights policies. Here, procedural concerns such as access to information, participation and the budget process can also be addressed.

Stage 4: Costing Human Rights PolicyThe fourth stage makes a crucial bridge between human rights policy and human rights budgeting by costing the policy

3 States enjoy “a marginofdiscretion in selecting the means for implementing their respective obligations” (Maastricht guidelines, paragraph 8). For civil society, this means human rights-based policy recommendations only carry a legal weight when the State has already adopted specific policies but failed to implement these (e.g. because of insufficient funds). Yet, civil society organisations are always free to offer their recommendations. Many thanks to Eitan Felner for this crucial addition.

recommendations. Within these policies are activities and services requiring purchasing or paying staff salaries for the government to implement. These costs summed up constitute a policy recommendation’s total required allocation for effective implementation: the price of the human rights policy.

Stage 5: Financing Human Rights PolicyHaving determined policy and budget recommendations and defined their implementation cost, this stage compares the required implementation costs with current budget allocations. This step addresses the financing of the human rights policy wherever a gap is identified by analysing where best to reallocate resources or tap into new funds. The cost elements combined constitute the human rights-based budget proposal.

These steps are schematically illustrated on the next page in Figure 1.1.

1.5TheroleofcostingwithintheprocessoffrontloadinghumanrightsWhen we talk about ‘costing human rights’ in this paper, we refer to the fourth stage within the wider process of frontloading human rights. This is important to note, because there have been several attempts to answer the previous question “what resources must be devoted to realising ICESCR rights?” (Felner, 2008) whether directly on the basis of indicators, benchmarks or with statistical analysis. However, the conceptual framework to frontloading human rights (Steenbergen, 2011), argues that such approaches cannot take sufficient account of a number of human rights principles, such as the requirement of a participatory and transparent process, or the need to understand the position of marginalised groups in society and identify the structural causes relating to their limited realisation of rights. We argue that this can only be achieved by undertaking a human rights-based situation analysis and analysing current policies on the basis of design and budget allocation.

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 17

ChapterOne: Frontloading Human Rights into Government Budgets

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 18

ChapterOne: Frontloading Human Rights into Government Budgets

Therefore, it is true to say that the stage of costing human rights begins after recommendations are already formulated. The aim of the process of costing human rights policies is to identify the total implementation cost of human rights policy recommendations. These costs can then be compared with current budget allocations and the differences identified can be used as the basis for an alternative budget proposal.

1.6ConclusionThis chapter is a summary of Equalinrights’ conceptual framework for frontloading human rights (Steenbergen, 2011). We began by establishing the need for a methodology to assist civil society organisations in claiming human rights through budget allocations by identifying the resources a government should allocate to advance the necessary policies, plans and programmes to realise human rights. In contrast to other retrospective methods of human rights budget work, this method of frontloading human rights was defined as a methodological process to translate (inter)national human rights standards and obligations into the budget proposals required for effective implementation in public policy and budget cycles.

Next, we gave an overview of the main characteristics and obligations of human rights and human rights-based development, before describing the five steps that make up the process of frontloading human rights. In conclusion, we highlighted the role of costing human rights policy within the broader process of frontloading, beginning after human rights recommendations are formulated to devise a human rights-based budget proposal.

A GUIDE TO COSTING HUMAN RIGHTS 19

2.1IntroductionIn the previous chapter, we introduced the method of frontloading human rights as a methodological process to translate (inter)national human rights standards and obligations into budget proposals required for an effective implementation in public policy and budget cycles.

We argued that we can only ‘cost human rights’ after undertaking a human rights-based situation analysis and offering recommendations to current policies, plans and programmes on the basis of their design and budget allocations. In this chapter, we take such a human rights proposal as the starting point, and attempt to enrich the proposal through costing, that is, examining the financial requirements to ensure its implementation.

Costing offers an important contribution to the existing tools of human rights advocacy. As we have stated frequently above, too often have governments adopted laws and policies that were not implemented because insufficient funding was provided for their implementation (UNICEF, 2010). Yet, when an organisation has defined the implementation cost of a particular policy, it can hold the government to account to allocate the required resources to ensure its implementation. Thus, when we have defined the required resources for an implementation, this will highlight when a government’s actions are inadequate, and so offer a stronger basis for human rights-advocacy.

A second reason to reflect human rights obligations in a cost-figure is to emphasise the importance of particular elements. For instance, in the last chapter, we argued that the process of human rights-based policy making should be transparent and participatory. Yet, the institutionalisation of concepts such as

participatory policy-making or greater budget transparency can only be assured if the costs of rights-holders’ engagement, or the costs to create a platform through which budget information can be dispersed are earmarked separately.

In this chapter, we refer to costing a new ‘project’ or ‘intervention’, though, as mentioned earlier, it may not be necessary to develop an entirely new human rights-based policy. Instead, a service may already be provided that can be made more rights-compliant. In this respect, the ‘intervention costs’ can be seen as the adjustment costs to an existing service.

OverviewWe begin with an overview of the central concepts and definitions of costing, before introducing two central methods to conduct a cost analysis. Having examined the main theories and literature on ‘costing’, we outline four steps that can guide the costing of a particular human rights policy or intervention in a rights-compliant manner. We end with a call for more capacity-building in the area of costing for human rights.

2.2ConceptsanddefinitionsThere are a number of fundamental concepts that underlie costing. These offer several alternatives for the type and methods of costing that will be undertaken.

2.2.1 What are costs? A ‘cost’ is most often defined as the value of resources used to produce a good or service. However, there are different interpretations as to which costs to incorporate and which to exclude. Financial Accountants are primarily concerned with an intervention’s financial costs, that is, the actual expenditure on goods

Chapter 2: Costing Human Rights

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 20

ChapterTwo: Costing Human Rights

and services purchased, because these costs are used for financial planning and budgeting they only include the goods and services which are paid for in a project or intervention.

The emphasis of this paper will be on financial costs, since we intend to identify a government’s total financial requirements in ensuring a policy’s effective implementation. However, such a minimal perspective may not always be appropriate. As we will see in the case studies of Chapter 3, the Housing Rights and Land Network (HRLN) created a tool to identify the requisite level of compensation a government should pay to individuals who have been forcibly evicted. In such a situation, calculating only the direct costs of government expenditure on goods and services will be inadequate. For example, if someone stays home from work to prevent being evicted, it has a price not because of something the individual paid for, but what s/he could have made (foregone income) by going to work. This is to say that not everything with a cost-implication is necessarily a financial cost. In such a situation it is more appropriate to use economic costs, where costs are defined in terms of “the alternative uses that have been foregone by using a resource in a particular way” (UNAIDS, 2000). These are also known as opportunity costs.

The choice of whether to use financial or economic costs will depend on the objective of the analysis. If the purpose of the costing exercise is to compare expenditure against budget allocations, then only actual project expenditure should be recorded. Similarly, if we explore the affordability of the intervention, we should only be concerned with financialcosts. This means, for instance, that the foregone income of a volunteer (which has a price), can be left out of the analysis since it does not have to be paid.

However, if we aim to consider a project’s sustainability, then economic costs become more important. The intervention may have positive economic implications, as for instance, domestic access to water and sanitation can

lead to improved health status of workers and a gain in time spent working, leading to higher incomes and higher tax-returns. These economic benefits, in turn, may even be income-generating from a government’s perspective. However, these indirect effects will not show up in the limited scope of a government’s direct expenditure on goods and services, and so for budgeting purposes require the broader scope of economic costs. The ‘opportunity cost’ of ‘time’, (i.e. not having to walk to a well, but having domestic access to water), is a clear example of an economic cost that cannot be valued directly through a market price. 2.2.2 PerspectivesThe example of forced evictions already introduces the vital question of whose cost we are talking about. Is the costing analysis taking the perspective of government, and therefore only focused on the direct expenses of providing the intervention, excluding costs incurred by the private sector or households? Or, are we costing from a rights-holder’s perspective, examining the burden of limited realisation of rights and assessing how much a household should be compensated to improve its situation? Alternatively, the costing analysis could adopt a societal perspective, which would encompass the costs incurred by all members of society, including the private sector, the public sector and households. Such a perspective may help determine whether the intervention is beneficial for society overall (Mogyoroso and Smith, 2005). These perspectives are illustrated in Figure 2.1, where we see the differences and overlap across perspectives.

For the purpose of costing human rights, all three approaches can be appropriate at different times, and may indeed overlap. However, the greatest focus will generally be on government, since budgeting requires we measure the actual financial costs that are expected to be incurred in the near future. Yet, it may also be the case that households are burdened with costs that are inappropriate from a human rights perspective, such as out-

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 21

ChapterTwo: Costing Human Rights

of-pocket costs of health care, or indirect costs of education such as uniforms. Therefore, a rights-holder’s perspective could enrich the initial analysis and help assess the ‘hidden costs’ of an intervention (i.e. costs that government should bear, but currently does not).

The societal perspective is more useful for advocacy purposes, rather than creating budget provisions (White, 2005), though it may demonstrate that there is an economic incentive for society as a whole to invest in a particular human right. This societal perspective will largely fall beyond the scope of this paper, but calculating the economic benefit of health care, water facility or food provision on a country as a whole can be found, for example, in:

• WHO (2001), Macroeconomics and Health: Investing in Health for economic development. Geneva: WHO

• SIWI (2005), Making water a part of

economic development: the economic benefits of improved water management and services. Stokholm: SIWI.

• Dista, S. and Vicente, C. (2009), Estimating the Potential GDP Losses due to Hunger in Mozambique. Maputo:FAO

2.2.3 Costing PurposeIt is worthwhile to point out that there is no universally applicable costing methodology and that different methodologies can be applied depending on the purpose of the cost data. The appropriate ‘form’ of the cost analysis should be selected in relation to the question that it attempts to address. Table 2.1 below identifies four main purposes of costing for human rights and shows the appropriate method to address these purposes.

• Basic cost analysis seeks to describe the distributions of cost that are required to successfully implement a given program. The paper’s focus is primarily directed towards a basic-cost analysis.

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 22

ChapterTwo: Costing Human Rights

• Cost-feasibility analysis is used to determine the extent to which a program can be successfully implemented, given the existing budgetary limitations.

• Cost-of-non-realisedrightsanalysis seeks to identify the long-term economic benefit of a particular intervention, known as ‘cost-of-illness’ in health economics. For an example see WHO, “Guide to identifying the economic consequences of disease and injury”, 2009.

• Cost-sustainability analysis aims to assess the long-term economic sustainability of an intervention, bringing together the cost-of-non-realised rights with cost-feasibility analysis.

2.2.4 Unit costsFor every policy, we can distinguish between its inputs, outputs and outcomes. For instance, a programme might aim to improve the enjoyment of the right to education by offering primary school children a nutritious meal every day. Here, the inputs refer to the various goods (such as meal ingredients) and personnel (such as a chef to prepare the meals) needed to set up the programme. The outputs then refer to the services produced through the use of inputs, for instance, the meals provided to children, or the number of school children fed. Lastly, a programme’s outcomes refer to the ultimate impact on the broader society, resulting from the programme, which in this case could be in the form of improving children’s nutrition and their ability to learn in school. (Streak, 2002).

A unit cost is a cost for a ‘unit’ of a pre-defined part of an intervention. While it can be possible to calculate the unit cost of outcomes (e.g. the cost to improve child nutrition), in practice, this is very difficult due to uncertainty that an intervention will actually lead to an impact. Therefore, unit costs are often concerned with the cost per outputs, such as the cost of a hospital bed per person per day, the cost

of a house connection to water provision per person per year, or the cost of primary education per person per year (UNAIDS, 2000).

In order to accurately calculate such unit costs, it is necessary to identify all the different inputs (goods and services) needed to produce a given output. Hence, the unit cost per person per day to stay in a hospital bed and receive treatment is made up of a number of inputs of goods (such as equipment needed for treatment and the use of furniture and bed linen) and manpower (such as the nurses, doctors and administrators) to provide the ultimate output of a hospital bed in which the patient is cared for.

The methods employed in this guide to costing human rights are aimed at quantifying the unit costs of the human rights-based policy recommendations under analysis. These are then used to identify the total financial resources required to implement a human rights policy by multiplying the unit cost per person per day/year by the number of targeted rights-holders and the intervention’s time-span.

2.3ConductingacostanalysisIn the previous section, we introduced a number of key concepts and definitions to support the ensuing discussion. Moving to an overview of methods for costing, this paper will not consider the methods of calculating a programme’s economic benefits, financial affordability or sustainability. Instead, our focus will only be on the basic cost-analysis that aims to determine the implementation cost of a particular policy or programme.

2.3.1 Methods of CostingConducting a cost analysis means gathering and organising information about the resources required to create a programme or implement a policy (Barnett and Escobar, 1990). The ways in which to approach this will vary widely from case to case, and may be

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 23

ChapterTwo: Costing Human Rights

determined by the costing purpose and data availability. Our particular interest is in costing programmes or policies that result in both human rights outcomes and processes.

The two main costing methods described in this guide differ in their level of detail and complexity. On the one hand, there is the direct measurement of all the different elements within a programme, frequently called micro-costing or the ‘ingredients’approach, since it identifies all the goods and services required for the intervention as ‘ingredients’, costs these elements and aggregates them to reach a total intervention cost.

On the other, there is the estimation of costs using administrative databases, such as a Ministry’s budget, to identify the average cost of a service, known as the ‘gross-costing’method. In gross costing, an intervention is broken down into large components, and only large cost items are identified (Brouwer, 2001). Gross-costing can therefore be quite simple and opaque. Gross costing is also usually faster and requires less analysis than micro-costing, but may be less accurate because of the relatively large resource units (for example, the ‘unit’ will be the patient cost per hospital per day, rather than a single procedure or activity performed during a hospital stay).

Conversely, in micro-costing, a very detailed service delivery process (inventory) is established, where all relevant resource items are identified and measured separately. This approach is more reliable and precise, but

can be very time-consuming and technical and so may be impractical. However, it may be preferable to gross costing when there is uncertainty as to the accuracy or availability of data, or because the intervention has a small number of distinct elements that all have a considerable impact on the cost (Mogyorosy and Smith, 2005).

The decision to choose the ingredient or gross-costing approach depends on the objective of the exercise, and each method’s advantages and disadvantages are described below in Table 2.2. Often, there is a trade-off between (a) reliability and accuracy of cost information and (b) feasibility and costs of data collection (measurement). Due to its detail and accuracy, the ingredients approach is generally preferred, but this method can be impractical or too time-consuming to initiate (Mogyorosy and Smith, 2005). In practice, costing studies generally use a combination of the two approaches within one exercise, partly due to a lack of specific pre-existing data for certain key elements of the intervention. The level of detail and precision for an element within the cost analysis should depend largely on the influence it has on the overall cost-estimation.

Determining which method to choose for cost-assessment can be influenced by the following factors:(a) The type of intervention; small-scale

interventions are easier to analyse directly using the ingredients approach, but large-scale interventions may require gross costing.

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 24

ChapterTwo: Costing Human Rights

(b) The available and quality of existinginformation; when administrative data is unavailable, gross costing is impossible so that the ingredients-approach is needed.

(c) Thelevelofdetailandaccuracyrequired; the ingredients-approach is often more accurate and specific whilst gross costing offers a rougher estimation.

To show how these factors influence the choice of costing methods, we give the example of a programme aimed to widen a rural community’s access to medical services by introducing a small health care centre. The cost of providing such a health centre will be influenced by only a small number of elements such as salary costs, equipment and drugs which means that it would be fairly easy to directly identify the price and required quantity of all these different ‘ingredients’. However, it could be that the target community lives in an extremely mountainous region while the only available information on health centre-costs relate to urban areas. Lastly, this cost-analysis may be used directly by government officials to allocate resources, so that the level of detail and accuracy required is of great importance. In this instance, the ingredients approach would be most suitable: it is feasible because there are only a small number of elements to be costed; applicable pre-existing information is unavailable and the level of accuracy required is high.

Conversely, an intervention aimed to provide access to safe and clean water in a large city’s slum community would present the analyst with a large number of elements to address, such as the price of septic tanks, pipe network configuration and maintenance. This scenario would require a complex analysis, suggesting the ingredients approach would be unsuitable. Moreover, there might be information readily available by the ministry responsible for water which, in this case, would also be more accurate. Therefore, in this situation the gross-costing analysis may prove to be more appropriate.

In short, we can see that depending on the context, type and level of intervention and availability of information different methods can be appropriate. Applying one of these two costing methods to a human rights-based budgeting exercise depends on a thorough description of the intended intervention so that all of the associated elements can be incorporated into the analysis.

2.3.2 The Ingredients approachThe ingredients approach holds that the intervention cost is the sum of its parts, or ’ingredients’. Aggregating each element’s price and quantity will lead to the total intervention cost.

The first step of the ingredients approach is to translate a particular policy into a set of distinct activities (or outputs) and identify all the different inputs (goods and personnel) needed to produce these activities. In the second step, each input is divided into a sub-category and costed.

1. Translate the human rights intervention into a number of activities with inputs.To ensure that the final cost figure is comprehensive and precise, it is important to give a complete description of all the different activities within a human rights policy or intervention, and list all the required inputs for this programme to achieve its intended effects. Levin and McEwan (2001) argue that the level of accuracy and detail for listing each programme ingredient should be proportional to the ingredient’s overall contributions to the programme’s total costs. For instance, for the right to health or the right to education, personnel costs generally represent the most substantial programme cost and should therefore be analysed in more detail than other costs. If the distribution of programme costs is unclear at the outset, White, et al. (2005) argue that directly observing similar interventions might help, as well as conducting interviews with the individuals responsible for distributing programme resources of a similar intervention or consulting thematic experts.

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 25

ChapterTwo: Costing Human Rights

2. Cost all the inputs of the human rights intervention.After each element is identified, the ingredients are divided into sub-categories and can then be costed to establish the total intervention cost. While the division of programme-ingredients will vary largely across human rights, across different scales of intervention and across countries, Levin and McEwan (2001) offer a commonly made division into “(a) personnel costs, (b) facility costs, (c) equipment and materials costs, (d) required [rights-holder] inputs and (e) other program inputs”.

2a. Valuing personnel costAs personnel costs often represent one of the largest shares of the overall programme costs, it is important to represent these costs accurately. The ingredient approach often estimates the cost of personnel by determining the number of minutes each worker spends on activities to provide the service. In chapter three, we will see how a South African CSO used this method to price the time of police, judges and lawyers spent on cases of domestic violence, to determine the salary costs relating to the implementation of a particular law. Examining the time spent on a particular service and multiplying this by the salary costs per minute identifies the personnel cost of the intervention. This ‘time-per-activity’ study, as it is known in the literature, can be observed directly by staff members keeping track of the time spent on each activity throughout the day, it can done by asking employees to keep daily activity logs, or by surveying the programme manager (Smith, 2003, Box 2.1).

After a time-per-activity has been determined, the next step is to assign a cost to that time. While hourly or annual earnings might be obtainable through surveys, these are not necessarily accurate guides to total employment costs. When adopting a government perspective to costing, it is also important to include the cost incurred by employers such as benefits and taxes. Furthermore, time spent on non-work-related activities such as vacation, sick leave and administrative work offer additional costs that should be reflected in the hourly cost of personnel.

2b. Valuing facility costsHuman rights interventions often require infrastructure, even though the relative share of these ‘facility costs’ in relation to the programme’s total costs depends on the human right intervention in question. For instance, facility costs such as a school building makes up only a small part of the cost of primary education. In contrast, providing access to water and sanitation is largely infrastructural. Since these facility costs are often very complex ingredients to evaluate, the ingredients approach may be less useful when these costs make up a large proportion of the programme.

If an intervention uses rented or leased building facilities, the facility costs simply constitute the actual cost of the rent or lease, when the intervention requires a building to be purchased or constructed, one approach could be to estimate the cost of renting or leasing a similar space. An alternative approach could be to estimate the facility’s cost by assessing the price of a purchasing a local building of

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 26

ChapterTwo: Costing Human Rights

similar proportions (White, 2005). The HRLN’s costing tool for forced eviction (discussed in chapter three) mentions that the best reference for determining market price of properties would be reliable real estate agents, banks, or other parties involved in the sale and exchange of such properties. The standard methodology involves collecting three quotes/estimates and selecting the average, or taking the middle quote as the fair price.

In the case of a newly constructed building, land deeds would also be a factor. Determining the value of a plot of land may be difficult if market prices are unavailable. In such an eventuality, the HRLN costing tool (2005) suggests using the current market value of a comparable site in another location.

2c. Valuing equipment and materials costsIt is important to include in the cost exercise all equipment and materials necessary for the effective functioning of the intervention or programme, such as furnishing, office supplies and other miscellaneous materials. The cost of supplies and equipment can usually be found in manager surveys of similar government services or by contacting manufactures (HLRN, 2005).

2d. Valuing the cost of required rights-holders inputs

An intervention’s targeted rights-holders may be faced with direct or indirect user-fees (e.g. transportation, books, uniforms). These costs should be included to the extent that government is expected to provide them. The permissibility and scale of user-fees differs across human rights, and might be incorporated into the design of the programme or intervention. If no decision has been made whether or not to include these costs pre-analysis, having a separate overview of the direct and indirect costs to access these services should feed into a discussion post-analysis.

2e. Valuing the costs of other programme inputs

Other inputs could include items such as internet access fees, telephone bills, trainings or professional development activities (Odden, Archibald, Fermanich, & Gallagher, 2002). As this category of costs typically represents less than 5% of programme costs, some estimates use a rule of thumb of 5% to project these programme inputs (White, 2005).

Data qualityWhen some data is unavailable, the costs of inputs may have to be measured directly from real world information. In order to retain the integrity of the costing exercise, it is vital to ensure the quality of data. Smith (2003) presents three standards that affect quality of data collection; precision, accuracy and reliability.

The level of precision required in data collection depends on the intervention and the size of the costing element in relation to total cost. For smaller cost elements it can be justified to use a ‘lump-sum’ or percentage of total cost, as is often the case for stationery. If the element is relatively large, it is important to pay closer attention to data collection and assure greater precision.

Accuracy is important because even small reporting errors can accumulate through repetition. If time-per-activity is underestimated by even 10 or 15 minutes per event, this means the activity’s labour cost is underestimated and when scaled-up to larger groups, the inaccuracy will build up. If such estimates are inaccurate, it may be necessary to change the method of data collection, for instance from asking employees to keep daily activity logs to direct observation of a third party (Smith, 2003).

Lastly, in order to guarantee the reliability of the information, it is important to train data collectors to ensure that they understand the collection forms used to obtain the information (Smith, 2003).

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 27

ChapterTwo: Costing Human Rights

When to use: The ingredients-approach, which directly measures the cost of elements by observation or surveys, is most necessary when the available administrative data proves to be insufficient, as when estimating the cost of an innovative intervention that does not resemble previous programmes. Due to the labour intensity of data collection for the ingredients approach, however, its use may be limited to activities that are most likely to be affected by the intervention or for those elements where appropriate information is lacking (Barnett, 2009). However, sometimes an intervention has too many separate elements to use the ingredients approach, making the gross costing method more applicable.

2.3.3 Gross CostingWhenever reliable administrative data is available, a gross costing method can be used. Where the ingredients approach is a bottom up approach, this method is essentially a top down method. In gross costing, an intervention is broken down into large components and these large cost items are identified by scaling-down the pre-existing information from administrative databases, ministry budgets or development programmes, to ‘units’ such as the patient cost per hospital per day, or the cost of providing a household with a piped connection per year. The quantity of each service is then multiplied by the estimated unit cost to acquire the full intervention cost (Barnett, 2009).

Gross costing aims to generate estimates for the different elements of an intervention. Yet, the physical units on which these unit costs are based are relatively large. This makes the approach is easier and faster than the ingredients-approach, but also less detailed and accurate.

The first descriptive step of gross-costing is similar to that of the ingredients approach, to translate the human rights intervention into a number of activities with inputs. Yet, for

gross-costing, the ‘inputs’ can be less detailed, and bigger in size, so rather than costing the time required for a doctor to treat a particular illness, the cost-item would be the patient cost per hospital per day.

The second step to gross-costing is to collectcostingdata by using administrative databases, approaching the relevant government ministry or a thematic expert organisation to estimate the programme’s main cost components. In selecting the costing-data it is important to consider two main criteria. The first criterion is that of applicability; the information should be useable, functional and correspond to the programme’s main cost components. The second criterion is that of data reliability. In many countries, budgetary data from central government is the only available source for costing; however these come with well-known limitations. Tsang (1988) offers six cautionary notes in using national data for local costing: • Budgetary data describes planned

expenditure, rather than actual expenditure. There can be a large discrepancy in these two figures, and whenever information on the actual expenditure is available, it might be more difficult to obtain.

• Costing data from local or municipal government levels is often lacking, which means that decentralised costs such as, for example, education finance in India are quickly underestimated.

• Expenditure on a particular field may not always be classified entirely within one ministry. For example, education expenses are not entirely covered by the education ministry, as building costs come from the public works department, and pensions from the ministry of finance.

• Central-government data can be too aggregated to be useful. Furthermore, it might be unable to account for expenses on very particular inputs, such as textbooks or equipment at the school level. Government expenses can vary by school and across different regions.

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 28

ChapterTwo: Costing Human Rights

• Budgetary information is concerned only with government expenditure and does not include the costs associated with direct and indirect private costs of schooling, health or water, thereby being insufficient to incorporate the hidden cost of access to service provision.

• Governmental budget data can be unreliable or inconsistent in defining cost categories over time, and different governmental sources may offer contradictory information.

After collecting the data from the budget line, the Ministry’s accounts or the thematic expert organisation, the aim is to ‘scale-down’ the total allocation to the appropriate unit cost (see Box 2.2).

Estimates / extrapolation based on (published) studies.A special case for gross-costing occurs when similar services or activities have already been valued. In such cases, information can be used from the intervention’s public study, report or analysis. It may also be helpful to contact the programme managers directly to discover more detail about the costing exercise in order to assess the quality and reliability of these estimates. However, it is important to assess the similarities of the two interventions as well, before using the information. Furthermore, the gross-costing approach aims to cost the intervention by identifying its unit costs. Yet, several cost studies do not report unit costs separately and/or their sources (Mogyorosy and Smith, 2005).

Data QualityFor the ingredients approach, we presented standards that affect quality of data collection. However, as gross costing is concerned with existing sources of information, we cannot rely on these same standards. Instead, Bailey (2009) presents the standards of completeness, no overlap and reliability.

When using pre-existing information to identify the costs of all the large components of an intervention, it is important to have completeness so that all the different elements are adequately represented in the data (Bailey, 2009).

When using data from different sources, it is especially important that no cost is double counted. This no overlapprinciple will prevent over-estimating the intervention cost. (Bailey, 2009)

Lastly, all sources of information used to value different elements of the intervention should be trust-worthy and up-to-date, only then is it suitable for budgeting purposes (Bailey, 2009).

When to use: The gross costing method is the most appropriate approach when an intervention has a large number of elements to address and where information is readily available from administrative databases, ministry budgets or development programmes. As gross-costing generally relies on large, aggregated datasets such as national statistics and national ministry budgets, it is based on

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 29

ChapterTwo: Costing Human Rights

the assumption that there is only a minor variation between contexts. However, it should be noted that this assumption is not always justified. Indeed, providing services to remote communities in rural areas will most likely have a higher than average cost. For this reason, it is essential to identify which elements are representative of the actual costs and which are under- or over-estimated. In the absence of disaggregated figures for the cost of service provision in rural communities, it might still be appropriate to rely on the national average but include a margin of difference to account for location (e.g. an additional 10%), rather than reject the national figures altogether and having to provide new figures entirely using the ingredients approach. Margin variables could then be estimated by asking experts or the initial source of data, such as the ministry.

Using Mixed Methods Lastly, in the face of missing data or difficulties in collecting data, a mixedmethod may prove easier to use than only adopting an ingredients-approach, while being more accurate than using only a gross-costing assessment. A mixed model also allows analysts to tailor the cost measurement to the study objective and decide for which elements to identify the unit cost using an ingredients-approach, and for which they can use a gross-costing method. When cost items are representative, a gross-costing method can be used, whereas the ingredients approach could be adopted where accuracy is paramount and data collection is feasible but not too time-consuming (Mogyorosy and Smith, 2005).

2.4CostingHumanRightsPoliciesNow that we have given an overview of the central concepts and definitions of costing, and introduced two different methods, we will return to our initial aim to identify the total financial requirements to implement a human rights policy. Here we can identify two ways in which a human rights-based costing study differs from a conventional costing study.

1. Costing human rights-based policiesHuman rights-based policy-making goes

beyond service provision and gives primacy to the rights-holder. For the right to health, for instance, the focus is on improving the availability, accessibility and quality of health, as expressed in the international legal framework. Rights-based policy-making also gives particular attention to the most vulnerable and marginalised groups. Yet, while costing human rights policy should be seen within the broader process of frontloading and begins only after human rights recommendations are already formulated, this principle is still important. The reason for defining a policy’s resource requirements is so that we can hold government accountable and allocate sufficient resources to it. However, providing essential services to marginalised groups will have a higher than average cost, either because of location or some other special requirements. We should adequately reflect the higher costs of their service-provision in the cost calculations, therefore, to ensure that policies affecting the most marginalised groups are properly implemented.

This is less of an issue for the ingredients-approach, as measuring itemised costs directly means that comparing groups or using average cost values does not occur. Costing at the level of detailed elements will more likely reflect the higher cost of requirements of the most vulnerable community, since it is based on actual financial data. However, the gross costing-approach relies on the underlying assumption that there is only a small variation between settings and their associated costs and this cannot always be justified. The distinction between actual and (national) average unit-costs is partly dealt with in the section ‘when to use gross-costing’. It is very important to identify which elements are representative of the actual costs and which are under- or over-estimated. In the absence of disaggregated figures, however, one approach would be to use national averages and include an additional location margin to the figures to account for regional variations of cost (e.g., an additional 10%), rather than not use the national figures at all or use the ingredients approach.

--------------------------------------------------------------------------------------------------------------------------

A GUIDE TO COSTING HUMAN RIGHTS 30

ChapterTwo: Costing Human Rights

2. Emphasising the importance of procedural human rights elements

In the introduction we argued that one reason to reflect human rights obligations in a cost-figure is to emphasise the importance of particular elements. For instance, in the last chapter, we argued that the process of human rights-based policy making should be transparent and participatory. Yet, institutionalising concepts such as participatory policy-making, or greater budget transparency can only be achieved if sufficient funds are allocated to finance the costs of rights-holders’ engagement, or the costs to create a platform through which budget information can be dispersed. Subsequently, while procedural costs may not always be substantial in relation to intervention cost, it can still be important to earmark these separately to ensure sufficient funds are allocated to institutionalise these procedures. Procedural recommendations will differ from case to case, and for different human rights, as illustrated by the hypothetical examples in section 2.6.

2.5 The Individual Steps in Costing HumanRightsPolicyWe will now present the four stages needed to calculate the financial requirements of a human rights policy. While each step will have different components depending on the particular human right intervention and its context, every human rights costing analysis will undertake these four stages (White, 2005):

• Stage 1: Translate the human rights intervention into a number of activities with inputs.

• Stage 2: Define the parameters of the costing-study.

• Stage 3: Collect the data on the various inputs needed to produce these activities.

• Stage 4: Analyse data, acquire unit costs and identify the total implementation cost of an intervention.

Stage 1: Translate the human rights intervention into a number of activities with inputs.Before we begin costing an intervention, it is important to have clarified some fundamental questions: what is the main aim of the programme and how does it intend to achieve it? Phillips and Huff-Rouselle (2001) offer a number of points that can be included at this stage: (1) A brief history of the situation that makes

the intervention necessary. This can be accompanied by a brief background of the country, the sector and human right of the programme.

(2) The main activities and methods of the programme: how will it achieve its objectives?

(3) Organisational issues of the programme: once implemented, how will the programme be structured and managed (geographically, hierarchically, functionality, etc.)?

(4) How should the programme be financed: entirely government funded, or through a cost-sharing exercise with the community, or through public-private partnerships?

(5) List all the elements required for the programme to achieve its intended objectives.

To identify all the intervention elements, it can be helpful to develop a flowchart or taxonomy, such as in Figure 2.1, an example of an intervention aimed to improve access to the right to education. However, this is a simplification of the recommendations that a frontloading-exercise would offer. As noted in the previous chapter, a costing-study can only be done by going through a human rights-based situation analysis. This analysis will identify the most urgent concerns related to a particular human rights issue or a marginalised group’s limited rights realisation, and explain the structural causes, and enable a comparison with existing policies on the basis of design and budget allocation. We offer this simplified taxonomy to illustrate the key costing methods.