a global country study report on taiwan in partial

TRANSCRIPT

1

A

GLOBAL COUNTRY STUDY REPORT

ON

TAIWAN

IN PARTIAL FULFILLMENT OF THE

REQUIREMENT OF THE AWARD FOR THE DEGREE OF

MASTER OF BUSINESS ADMINISTRATION

In

Gujarat Technological University

Batch : 2010-12

MBA SEMESTER III/IV

Shri Sunshine Group of Institutions

MBA PROGRAMME

Affiliated to Gujarat Technological University

Ahmedabad

April, 2012

2

INDEX

NO Particulars Page No.

1 Economy Overview of Taiwan 4

1.1 Demographic Profile of the Taiwan 5

1.2 Economic Overview of the Taiwan 8

1.3 Overview of Industries Trade and Commerce 12

1.4 Overview Different economic sectors of Taiwan 13

1.5 Overviews of Business and Trade at International Level 18

1.6 Present Trade Relations and Business Volume of

different products with India

20

1.7 PESTEL Analysis 22

2 Industry/ Sector/Company/Product/Service/New venture

specific study

25

2.1 Introduction of the selected Company / Industry / Sector

and its role in the economy of Taiwan

41

2.2 Structure, Functions and Business Activities of selected

Industry / Sector / Company

56

3.1 Comparative Position of selected Industry / Sector /

Specific Company / Product with India and Gujarat

74

3.2 Present Position and Trend of Business (import / export)

with India / Gujarat during last 3 to 5 years

89

4.1 Policies and Norms of selected country for selected 96

3

Industry/company for import / export including licensing /

permission, taxation & Policies and Norms of India for

Import or export to the selected country including

licensing / permission, taxation etc

4.2 Present Trade barriers for import / Export of selected

goods

106

5.1 Potential for import / export in India / Gujarat Market 115

5.2 Business Opportunities in future 122

5.3 Suggestion & Conclusion 132

6 Plagiarism Test Report 141

4

Background of the Country

In 1895, military defeat forced China to cede Taiwan to Japan. Taiwan reverted

to Chinese control after World War II. Following the Communist victory on the

mainland in 1949, 2 million Nationalists fled to Taiwan and established a

government using the 1947 constitution drawn up for all of China. Over the next

five decades, the ruling authorities gradually democratized and incorporated the

local population within the governing structure. In 2000, Taiwan underwent its

first peaceful transfer of power from the Nationalist to the Democratic

Progressive Party. Throughout this period, the island prospered and became one

of East Asia's economic "Tigers." The dominant political issues continue to be the

relationship between Taiwan and China - specifically the question of Taiwan's

eventual status - as well as domestic political and economic reform.

1) Demographic Profile of the Country

Population Size

This article is about the demographic features of the population in Taiwan,

including population density, ethnicity, education level, health of the populace,

economic status, religious affiliations and other aspects of the population.

The population in Taiwan was estimated in July 2011 at 23,188,087 spread

across a total land area of 35,980 km, making it the sixteenth most densely

populated country in the world with a population density of 641 people per km.

During the 20th century the population of Taiwan rose more than sevenfold, from

3.04 million in 1905 to 22.3 at December 31, 2000. This high growth was caused

by a combination of factors, very high fertility rates up to the 1960s, and low

mortality rates, and a surge in population as the Chinese Civil War ended, and

the Kuomintang forces retreated, bringing an influx of two million soldiers and

civilians to Taiwan in 1948 - 1949. Consequently, the natural growth of Taiwan

was very rapid, especially in the late 1940s and 1950s, with an effective growth

5

rate as high as 36.8 per 1,000 during 1951-1956. Including the Kuomintang

forces, which accounted in 1950 for about 25% of all persons on Taiwan,

immigration of mainland Chinese (now approximately 13% of the present

population) at the end of the 1940s was a major factor in the high population

growth of Taiwan. Some official government statistics for the period, including

those reported on this page, do not seem consistent with the known size of the

Kuomintang influx.

Net migration rate

During 2004-2010 Taiwan's migration rate was positive. On average the annual

net migration amounted to 22,000 people during that period, which is equivalent

to a rate of 1.0 per 1000 inhabitants per year.

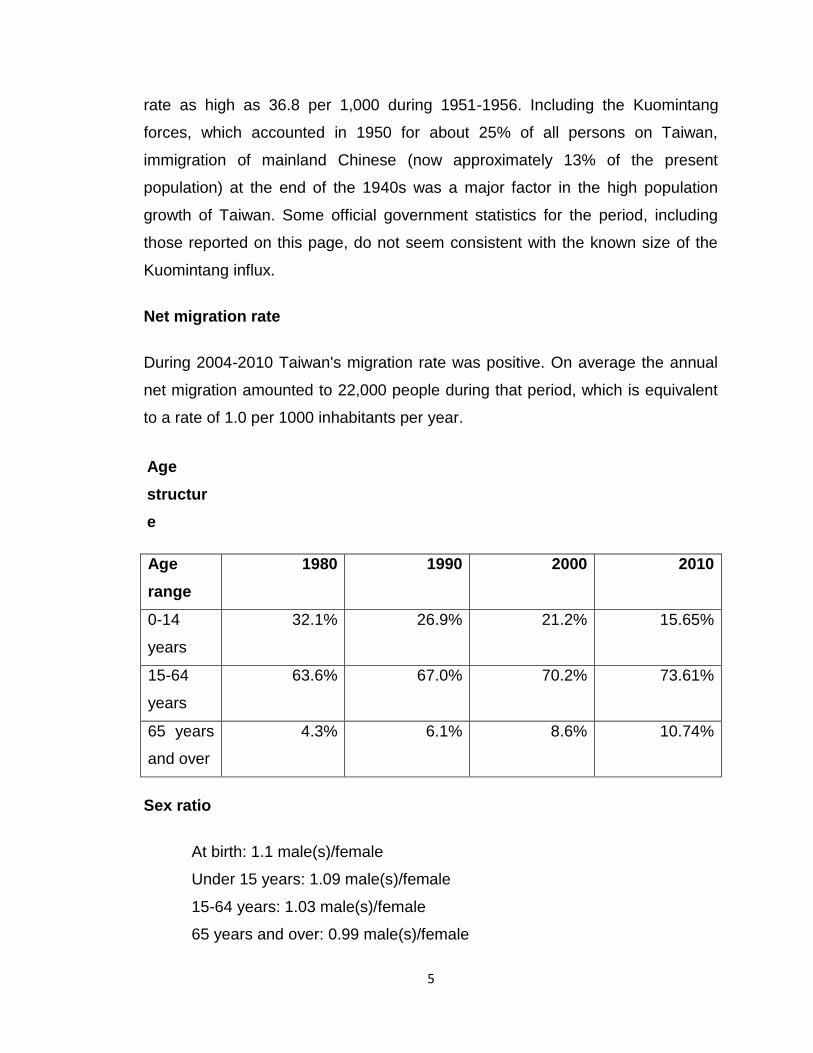

Age

structur

e

Age

range

1980 1990 2000 2010

0-14

years

32.1% 26.9% 21.2% 15.65%

15-64

years

63.6% 67.0% 70.2% 73.61%

65 years

and over

4.3% 6.1% 8.6% 10.74%

Sex ratio

At birth: 1.1 male(s)/female

Under 15 years: 1.09 male(s)/female

15-64 years: 1.03 male(s)/female

65 years and over: 0.99 male(s)/female

6

Total population: 1.04 male(s)/female (2010 est.)

Ethnicity (Overview)

Officially, the population of Taiwan consists, of which 84% identify as Taiwanese

included Hakka, while 14% are mainlanders Chinese, 2% are aborigines. A

confounding factor is intermarriage between these ethnic groups - to the extent

that it is doubtful whether the term "ethnicity" can be used at all.

Languages

Overview: Mandarin Chinese (official), Taiwanese (Min), Hakka dialects

Almost everyone in Taiwan born after the early 1950s can speak Mandarin,

which have been the official language and the medium of instruction in the

schools for more than four decades. The Mandarin spoken in Taiwan has minor

differences from that spoken in mainland China, South-east Asia and other

regions of the world.

The majority speak a dialect form of Min Nan (Southern Fujianese language),

commonly referred to as Taiwanese, which was the most common language. The

ethnic Hakka have a distinct Hakka dialect. Between 1900 and 1945 Japanese

was the medium of instruction and could be fluently spoken by many of those

educated during that period. Chinese romanisation in Taiwan uses both Hanyu

pinyin which has been officially adopted by the central government, and

Tongyong pinyin which some localities use. Wade-Giles, used traditionally, is

also found.

On Kinmen (Quemoy), the language spoken is also Min Nan. On the Matsu

Islands, the Foochow dialect, a Min Dong (Eastern Fujianese) dialect, is spoken.

The most widely spoken Taiwanese aboriginal languages today are Amis, Atayal,

Bunun, and Paiwan.

7

Religion

The Geert Hofstede analysis for Taiwan is almost identical to the model for

China. Long-term Orientation is the highest-ranking factor. As with other Asian

countries, relationships are a primary part of the culture. Individualism is the

lowest ranking. Like the Chinese, the Taiwanese are a collectivist society.

The Taiwanese migrated to Mainland China starting in AD 500. Taiwan has a

population of approximately 20.5 million. The official language is Mandarin

Chinese. Most businessmen speak and understand English. It is governed by a

multiparty republican system. Taiwan is often referred to as Nationalist China.

Although the Taiwanese practice a variety of religions the culture is strongly

influenced by Confucianism.

About 93% of the population can be considered religious believers, most of

whom identify themselves as Buddhists or Taoists, Christian 4.5%, other 2.5%.

Fertility rate

The fertility rate of Taiwan is one of the lowest fertility rates ever recorded in the

world in historical times. It reached its lowest level in 2010: 0.90 children per

8

female. In 1980, the rate was still well above replacement level (2.515), but it

dropped to 1.88 in 1985, 1.81 in 1990, 1.78 in 1995, 1.68 in 2000, 1.12 in 2005.

2) Economic Overview of the Country

Taiwan now faces many of the same economic issues as other developed

economies. With the prospect of continued relocation of labor-intensive industries

to economies with cheaper work forces, such as in China and Vietnam, Taiwan's

future development will have to rely on further transformation to a high

technology and service-oriented economy. In recent years, Taiwan has

successfully diversified its trade markets, cutting its share of exports to the

United States from 49% in 1984 to 20% in 2002. Taiwan's dependence on the

United States should continue to decrease as its exports to Southeast Asia and

China grow and its efforts to develop European markets produce results.

Taiwan's accession to the WTO and its desire to become an Asia-Pacific

"regional operations center" are spurring further economic liberalization.

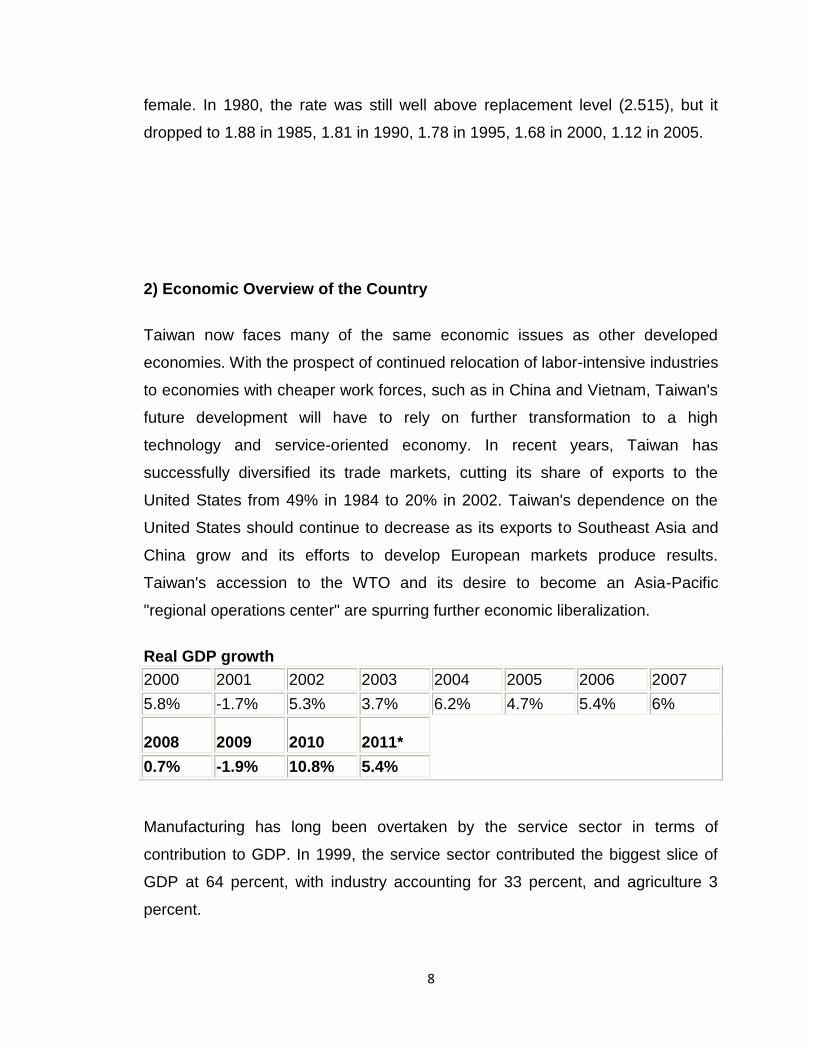

Real GDP growth

2000 2001 2002 2003 2004 2005 2006 2007

5.8% -1.7% 5.3% 3.7% 6.2% 4.7% 5.4% 6%

2008 2009 2010 2011*

0.7% -1.9% 10.8% 5.4%

Manufacturing has long been overtaken by the service sector in terms of

contribution to GDP. In 1999, the service sector contributed the biggest slice of

GDP at 64 percent, with industry accounting for 33 percent, and agriculture 3

percent.

9

The service sector is thriving and shows promise of further growth as the

spending power of the population increases. By the end of 1995, the growth of

the service sector exceeded that of the agricultural and manufacturing sectors by

more than 60 percent and has continued to do so. The different businesses that

fall under the service sector in Taiwan are: finance, insurance, and real estate;

commerce, including wholesale and retail business, food and beverages, and

international trade; social and individual services; transport, storage, and

telecommunications; commercial services, including legal, accounting, civil

engineering, information, advertising, designing, and leasing; governmental

services, and miscellaneous others.

The agricultural sector to GDP has been steadily declining since the 1980s when

Taiwan's government shifted the focus of its economic strategy to

industrialization. Few of the younger generation are willing to work in the

agricultural sector, preferring to pursue better opportunities in the other sectors.

Farmers make up only 8 percent of the labor force and produce less than 3

percent of the island's total GDP according to 1999 statistics. Consequently, the

sector diminished in importance while the manufacturing sector has risen to the

forefront. The agricultural sector will face even more problems when the country

is finally accepted as a member of the World Trade Organization (WTO). To

comply with the WTO's requirements, the government has been systematically

reducing the trade barriers on its traditionally well-protected agricultural goods,

leaving local produce to face increased competition from the foreign agricultural

products that will flood the domestic market when Taiwan becomes a full-fledged

member in the WTO.

Global financial crisis

10

Taiwan has recovered

quickly from the global

financial crisis of 2007-

2010, and its economy

has been growing

steadily. Its economy

faced a downturn in

2009 due to a heavy

reliance on exports

which in turn made it

vulnerable to world

markets. Unemployment reached levels not seen since 2003, and the economy

fell 8.36% in the fourth quarter of 2008. In response, the government launched a

US$5.6 billion economic stimulus package (3% of its GDP), provided financial

incentives for businesses, and introduced tax breaks. The stimulus package

focused on infrastructure development, small and medium-sized businesses, tax

breaks for new investments, and low-income households. Boosting shipments to

new overseas markets, such as Russia, Brazil, and the Middle East was also a

main goal of the stimulus. The economy has since slowly recovered; by

November 2010, Taiwan's unemployment rate had fallen to a two-year low of

4.73% and is expected to continue to drop through the first half of 2011. The

average salary has also been rising steadily for each month in 2010, up 1.92%

from the same period in 2009. Industrial output for November 2010 reached

another high, up 19.37% from a year earlier, indicating strong exports and a

growing local economy. Private consumption is also increasing, with retail sales

up 6.4% compared to 2009. After 10.5% economic growth in 2010, the World

Bank expects growth to continue and reach 5% for 2011.

Foreign trade

11

The second-largest technology trade show

in the world, is a global IT exhibition which

attracts many foreign investors.

Foreign trade has been the engine of

Taiwan's rapid growth during the past 40

years. Taiwan's economy remains export-

oriented, thus it depends on an open world

trade regime and remains vulnerable to downturns in the world economy. The

total value of trade increased over fivefold in the 1960s, nearly tenfold in the

1970s, and doubled again in the 1980s. The 1990s saw a more modest, slightly

less than twofold, growth. Export composition changed from predominantly

agricultural commodities to industrial goods (now 98%). The electronics sector is

Taiwan's most important industrial export sector and is the largest recipient of

U.S. investment. Taiwan, as an independent economy, became a member of the

World Trade Organization (WTO) as Separate Customs Territory of Taiwan,

Penghu, Kinmen and Matsu (often shortened to "Chinese Taipei"-both names

resulting from PRC interference on the WTO) in January 2002. In a 2011 report

by Business Environment Risk Intelligence (BERI), Taiwan ranked third-best

globally for its investment environment.

Taiwan is the world's largest supplier of contract computer chip manufacturing

(foundry services) and is a leading LCD panel manufacturer, DRAM computer

memory, networking equipment, and consumer electronics designer and

manufacturer. Textiles are another major industrial export sector, though of

declining importance as Taiwan due to labor shortages, increasing overhead

costs, land prices, and environmental protection. Imports are dominated by raw

materials and capital goods, which account for more than 90% of the total.

Taiwan imports most of its energy needs. The United States is Taiwan's third

largest trading partner, taking 11.4% of Taiwanese exports and supplying 10.0%

of its imports. China has recently become Taiwan's largest import and export

partner. In 2010, the PRC accounted for 28.0% and 13.2% of Taiwan's exports

12

and imports respectively (excluding Hong Kong). This figure is growing rapidly as

both economies become ever more interdependent. Imports from China consist

mostly of agricultural and industrial raw materials. Exports to the United States

are mainly electronics and consumer goods. As Taiwanese per capita income

level has risen, demand for imported, high-quality consumer goods has

increased. Taiwan's 2002 trade surplus with the United States was $8.70.

Overview of Industries Trade & Commerce

The Taiwan Chamber of Commerce, also known as TCOC, is a

independent, non-profit organization of leading commercial firms, business

associations, and businessmen in the Republic of China (Taiwan).

It was founded on Sept.16, 1946 mainly to represent the interests of

Chinese business community, promote commercial development in line with

government policies, and establish international economic cooperation with

other countries.

13

The former body of TCOC was “Taiwan Commerce & Industry Economic

Association” in the Japanese occupation period. After the restoration of Taiwan in

1945, the "Taiwan Commerce & Industry Economic Association" was

immediately disbanded and the association was reorganized as the “Taiwan

Federation of Chamber of Commerce”. On Sept.16,1946, the first provincial

member representatives’ convention was convened in the Sun Yat-Sen

Community Center, Taipei, and Mr. Lin Hsiung-Cheng was the first chairman. At

that time, the “Taiwan Chamber of Commerce” established.

Under the excellent leadership and joint hard work of the chairmen, and

directors and supervisors of previous terms, the chamber always maintain the

objective of promoting domestic and foreign trade, stimulating economic

development, coordinating relationship between peer companies and increasing

mutual benefits. Therefore the chamber has become an important force in the

society that cannot be ignored.

4) Overview of Different Economic Sectors of Taiwan

Industrial output has gradually decreased from accounting for over half of

Taiwan's GDP in 1986 to just 31% in 2002. Industries have gradually moved to

capital and technology-intensive industries from more labor-intensive industries,

with electronics and information technology accounting for 35% of the industrial

structure. Industry in Taiwan primarily consists of many small and medium-sized

enterprises (SME) with fewer large enterprises.

Largest companies in Taiwan

Hon Hai Precision Ind (Technology Hardware & Equip), Taiwan Semiconductor

(Semiconductors), Formosa Petrochemical (Oil & Gas Operations), China Steel

(Materials), Chunghwa Telecom (Telecommunications Services)

(2010)

List of Industries

14

Information Technology

Agriculture

Energy

Computer and Peripheral Equipment

Security Systems & Equipments

Electronics

Iron and Steel

Banking, financial and related services

Automobile

Shipping and Transportation

Textiles

Information technology

Taiwan's information technology industry has played an important role in the

worldwide IT market over the last 20 years. In 1960, the electronics industry in

Taiwan was virtually nonexistent. However, with the government's focus on

development of expertise with high technology, along with marketing and

management knowledge to establish its own industries, companies such as

TSMC and UMC were established. The industry used its industrial resources and

product management experience to cooperate closely with major international

suppliers to become the research and development hub of the Asia-Pacific

region. The structure of the industry in Taiwan includes a handful of companies

at the top along with many small and medium-sized enterprises (SME) which

account for 85% of industrial output. These SMEs usually produce products on

an original equipment manufacturer (OEM) or original design manufacturer

(ODM) basis, resulting in less resources spent on research and development.

Due to the emphasis of the OEM/ODM model, companies are usually unable to

make in-depth assessments for investment, production, and marketing of new

products, instead relying upon importation of key components and advanced

technology from the United States and Japan. Twenty of the top information and

communication technology (ICT) companies have International Procurement

15

Offices set up in Taiwan. As a signer of the Information Technology Agreement,

Taiwan phased out tariffs on IT products since January 1, 2002.

Agriculture

Agriculture has served as a strong foundation for Taiwan's economic miracle.

After retrocession from Japan in 1945, the government announced a long-term

development strategy of "developing industry through agriculture, and developing

agriculture through industry". Thus, agriculture became the foundation for

Taiwan's economic development, while promoting growth in industry and

commerce. In 1951, agricultural production accounted for 35.8% of its GDP.

Today, agriculture only comprises about 2.6% of Taiwan's GDP or about US$1

billion. In 2002, farming accounted for 43.33% of the industry, with livestock

(30.02%) and fishing (26.41%) making up a significant portion of the rest. Since

its accession into the World Trade Organization and the subsequent trade

liberalization, the government has implemented new policies to develop the

sector into a more competitive and modernized green industry.

Energy

Wind turbines, such as these in Qingshui, Taichung, are part of the government's

efforts to increase sources of renewable energy.

Due to the lack of natural resources on the island, Taiwan is forced to import

many of its energy needs (currently at 98%).[54] Imported energy totaled

US$11.52 billion in 2002, accounting for 4.1% of its GDP.[55] Although the

industrial sector has traditionally been Taiwan's largest energy consumer, its

share has dropped in recent years from 62% in 1986 to 58% in 2002.[55] Taiwan's

energy consumption is dominated by oil (51.8%), followed by coal (30.4%),

nuclear power (8.7%), natural gas (8.6%), and hydroelectric power (0.3%).[56]

The island is also heavily-dependent on imported oil, with 72% of its crude oil

coming from the Middle East in 2002. Although the Taiwan Power Company

(Taipower), state-owned enterprise, is in charge of providing electricity for the

16

Taiwan area, a 1994 measure has allowed independent power producers (IPPs)

to provide up to 20% of the island's energy needs.[57] Indonesia and Malaysia

supply most of Taiwan's natural gas needs.[57] It currently has three operational

nuclear power plants with a fourth expected to come into operation by the end of

2012 at a cost of NT$280 billion (US$9.65 billion).[58]

Textiles Industry

Taiwan textiles industry's production value, manufacturers number and the

employees. The textiles industry of Taiwan is highly export-oriented. The export

value of textiles and apparel accounts for more than 80% of total textiles and

apparel production in the recent six years. Textiles industry's production value,

manufacturer number and the employees all reveal a decline phenomenon in the

past 10 years. The production value of textiles in Taiwan was NTD482.3 billion in

2010, down 22% from NTD615.4

Billion in 1997, the manufacturers in 2010 were reduced 1,876 units from 1997,

and there was decline in employment from the number of 285,730 in 1997 to

153,163 in 2010, down 46%.

Telecom Industry

In 2009, the total sales revenue from mobile services reached NTD154.3 billion

in Taiwan, down 5.4% yr-on-yr, and the sales revenue from fixed-line telephone

business was NTD96.8 billion, up 31$ yr-on-yr. In Taiwan, mobile business

income is far more than fixed-line telephone business revenue, because the

number of mobile phone subscribers is bigger than that of fixed-line telephone

subscribers and the charges of mobile services is higher than that of fixed-line

telephone business.

Chunghwa telecom is the largest telecom operator in Taiwan. In 2009, its

consolidated revenue reached NTD184 billion, representing a decline of 1.47%

over the same period in 2008. In 2009, the mobile services accounted for 40.27%

of the business of Chunghwa telecom, fixed-line network business 47.2%, and

17

internet and data services 12.42%. The revenue decline of Chunghwa telecom

was primarily incurred by decreasing fixed-line telephone business income.

Steel Industry

Taiwan’s steel industry turned out NT$403.58 billion worth of steel products in

the second quarter for a 4.6% growth from the first quarter or an 11% rise from

last year. In May 2011, China Steel Corporation (CSC)’s steel production volume

dropped 1.1% month-on-month (m-o-m) and 7.0% y-o-y to 770,653 tonnes. This

came on the back of a sales drop of 4.0% m-o-m and 9.8% y-o-y to 783,000

tonnes. However, a rise in steel prices ensured that the steelmaker’s sales

revenue fell just 0.2% m-o-m and 2.6% y-o-y to TWD20.72bn.

Semiconductor Industry

Semiconductor market of Asia, the fastest-growing area, reached US$123.5

billion in 2007, a 6% increase from 2006. Taiwan semiconductor industry grew

5.3% in 2007, outpaced the worldwide average of 3.2% due to the dramatic

growth of 23.6% in IC Design and 8.2% in Packaging. decreased by 3.9%, with a

3.2% increase in foundry and a 13.4% decrease in DRAM. Taiwan IC revenue

(including design, manufacturing, packaging, and testing) totaled NT$1,466.7

billion, a 5.3% growth from 2006, with NT$399.7 billion in design, a 23.6%

increase, NT$736.7 billion in manufacturing, a 3.9% down, NT$228.0 billion in

packaging, an 8.2% up, and NT$102.3 billion in testing, a 10.7% rise.

In 2007, Taiwan IC product revenue reached NT$684.2 billion (Table 1), a 5%

increase from 2006. Memory products comprised 44.2%, down from the 52.7% of

2006 due to the DRAM price erosion. Logic IC comprised 45.1% (38.7% in

2006), Micro component IC 5.8%, and Analog IC 4.8%. Information applications,

comprising 54.5% (59.7% in 2006), remained the largest application area.

Consumer applications reached 30.6% (27.8% in 2006), and communication ICs

accounted for 13.8% (11.4% in 2006).

18

The different businesses that fall under the service sector in Taiwan are:

finance, insurance, and real estate; commerce, including wholesale and retail

business, food and beverages, and international trade; social and individual

services; transport, storage, and telecommunications; commercial services,

including legal, accounting, civil engineering, information, advertising, designing,

and leasing; governmental services, and miscellaneous others.

5) Business and Trade at International level

The phenomenal growth of Taiwan's economy can be credited to its brisk foreign

trade. From 1970 until 1990, the country amassed huge surpluses from its

earnings in international trade, which peaked in 1987 when the trade surplus

reached US$18.7 billion. However, several other countries became alarmed at

Taiwan's huge surpluses and the corresponding economic power it might exert

on other economies. The United States demanded that Taiwan remove trade

restrictions and allow more foreign products into the country. Since then, Taiwan

has reduced or removed a significant number of trade barriers, thus allowing

foreign products to compete with local products in the domestic market. From

1992 to 1996, Taiwan's trade surplus declined by nearly 30 percent. However,

from 1998, trade figures have once more shown a steady rise and, according to

the Central Bank of China, Taiwan's foreign exchange reserves in 1999

amounted to US$106.2 billion, one of the highest in the world. In 2000,

Taiwanese exports reached US$148.38 billion against imports of US$140.01

billion, producing a trade surplus of US$8.37 billion.

Taiwan is a major exporter of industrial products ranging from mechanical

appliances and accessories, electronics, electrical appliances, personal

computers and peripherals, metal products and transport equipment, to furniture

and clothing. The United States has been Taiwan's most important trading

19

partner over decades. However, as Taiwan pursued the expansion of its

economy, it began seeking out other trading partners, which resulted in a

decrease in trade with the United States. In the 1980s, 40 percent of Taiwan's

total exports were U.S.-bound; by 2000 only 23.5 percent of the island's total

exports were destined for the American market.

Export from Taiwan country list

Ranking for

2010

Countries

1 America 18 Brazil 35 South Africa

2 Germany 19 Mexico 36 UAE

3 Netherlands 20 Vietnam 37 Czech

4 Japan 21 Iran 38 Ukraine

5 UK 22 Denmark 39 New Zealand

6 Canada 23 Singapore 40 Israel

7 Italy 24 Finland 41 Columbia

8 Sweden 25 India 42 Portugal

9 Poland 26 Romania 43 Norway

10 Philippines 27 Indonesia 44 Chile

11 China 28 Malaysia 45 Argentina

12 Belgium 29 Saudi Arabia 46 Greece

13 Australia 30 Slovakia 47 Lithuania

14 Russia 31 Slovenia 48 Ireland

15 French 32 Korea 49 Switzerland

16 Spain 33 Turkey 50 British Virgin

Islands

17 Thailand 34 Hong kong

20

PRESENT TRADE RELATIONS & DIFFERENT PRODUCTS BUSINESS WITH INDIA

Trade Relations:

The bilateral relations between the Republic of India and Taiwan have

improved since the 1990s; India has expanded economic and strategic

cooperation with Taiwan.

India has sought to cultivate extensive ties with Taiwan in trade as well as

working together over weapons of mass destruction issues, environment and

fighting terrorism. Both sides have aimed to develop ties to counteract Chinese

rivalry with both nations.

The India-Taipei Association (ITA) Office has been established in Taipei

since 1995 to promote non-governmental interactions between India and Taiwan,

and to facilitate business, tourism, cultural and people-to-people exchanges.

The India-Taipei Association has also been authorized to provide all

consular and passport services. In 2002, India became the 28th nation to sign

the Investment Protection Agreement with Taiwan and in 2006, both nations

established the Taiwan-India Cooperation Council. Furthermore, Taiwan

promotes trade with India as a means to reduce the extent of their economic

dependence with China.

Business Products:

The Taiwan government has been trying to strengthen economic ties with

India and since 2003 has designated it as one of the target countries for

investment.

India is a perfect choice since it's a fast-growth country in the region with

surging demand for electronics, including such items as computers, routers,

21

monitors and industrial materials such as machinery tools, moulds, or

other heavy-duty machines, which all happen to be Taiwan's forte.

Taiwan's strength lies in hardware manufacturing and design — especially

in the field of ICT, green technology, machinery and auto parts. India, on the

other hand, is known for its world-famous software R&D expertise. There is

certainly a reason for both sides to combine force to boost their industries.

Taiwan Imports

Taiwan imports were worth 21473 Millions USD in November of 2011. A lack of

natural resources had made Taiwan dependent on imports. Taiwan imports

mostly mineral products and basic metals, electronic products, chemicals,

machinery. Main import partners are Japan (21% of total), Mainland China &

Hong Kong (14%), USA (10%), Europe (10%) and ASEAN countries (11%). This

page includes a chart with historical data for Taiwan's Imports.

Export in 2010 (est.) - $ 273.8 Billion

Import in 2010 (est.) - $ 247.3 Billion

22

7) PESTEL Analysis

PESTEL stands for Political, Economic, Social, Technical, Environment and

Legislative. It is a strategic planning technique that provides a useful framework

for analysing the environmental pressures on a team or an organisation.

A PESTEL Analysis can be particularly useful for groups who have become too

inward-looking. They may be in danger of forgetting the power and effect of

external pressures for change because they are focused on internal pressures.

Now let us see the PESTEL Analysis of Taiwan country.

Political view:

Taiwan is part of Republic of China (ROC) and hence it is having democratic

parties to rule the country. Taiwan is having Democratic Progressive Party or

DPP [TSAI Ing-wen]; Kuomintang or KMT (Nationalist Party) [MA Ying-

jeou]; Non-Partisan Solidarity Union or NPSU [LIN Pin-kuan]; People

First Party or PFP [James Soong].

Debate on Taiwan independence has become acceptable within the

mainstream of domestic politics on Taiwan; public opinion polls

consistently show a substantial majority of Taiwan people supports

maintaining Taiwan's status for the foreseeable future; advocates of

Taiwan independence oppose the stand that the island will eventually

unify with mainland China; advocates of eventual unification predicate

their goal on the democratic transformation of the mainland.

Economic view:

Taiwan’s economic performance is greatly dependent on its ability to export

goods and services, which in recent years have amounted to over 70% of GDP.

China, the U.S., and Europe, in that order, are Taiwan’s three most important

trading partners.

Taiwan’s economic outlook is rather bleak (not hopeful). China is now Taiwan’s

only hope to end 2011 with a decent growth rate which for the last 20 years

averaged 5.2% a year.

23

Social & cultural view:

In summary, for about 110 years starting with Koxinga's expedition to Taiwan in

1661, Taiwan remained an agrarian, immigrant society where the indigenous

culture slowly became marginalized.

Taiwan’s social environment laid the ground for the Nationalist government's

continuation of Chinese cultural development and modernization after

retrocession. It was on this foundation that Taiwan's cultural and educational

development took off.

Technology view:

The development of science and technology requires a steady influx (an arrival of

something in great numbers) of resources. The majority of Taiwan’s industries

are small- and medium-sized enterprises, with limited resources for R&D.

Industrial research and development has progressed from improving animal,

plant and fish species, to upgrading industrial production technology, and

advancing mechanization. However, faced with limited land and other resources,

these enterprises have, with government guidance, swiftly developed from

traditional industries into capital intensive, high-tech industries.

Ecological view:

Taiwan is developing green cities for regulating pollution rate as per government

prescribed terms and conditions. Recent development states that Taiwan has

successfully managed downsizing level of pollution by opening up green

gardens, cities and etc.

Legal view:

Corporate

Income Tax*:

24

Taxable Income Tax Rate

Up to NT$50,000 Exempt

NT$50,001 to NT$71,428 50% of taxable income less

NT$25,000

NT$71,429 to NT$100,000 15% of taxable income

NT$100,001 to over 25% of taxable income less

NT$10,000

Withholding

Tax*: 20% standard rate

Value Added

Tax*: 5%

Transaction

Tax*: 0.3%

(*Source: PriceWaterHouseCoopers, PWC)

25

INTRODUCTION OF THE COMPANY

GIANT MANUFACTURING

On a sunny day in 1972 in Tachia, a port city in western Taiwan, a new bicycle

company called Giant Manufacturing officially opened its doors. Back then, the

vast majority of the world bicycle market was dominated by established brands

such as Schwinn Corporation, Derby Cycle, and Huffy Corporation. A handful of

domestic us brands controlled 76% of the us market.

These firms had an enviably entrenched industry position in the us. From the

industry perspective, bicycles were a hard market to break into indeed: the level

of technological expertise was high, the name brand crucial, the distribution

painstakingly complex, and, perhaps most importantly, the distribution networks

of specialty shops were relationship-based and complex (Porter 1980; Porter

1996).

When these hurdles are combined with the high efficiencies of scale intrinsic to

bicycle production, the barriers to entry in that industry were indeed substantial

and Giant’s obstacles were great.

Given this, the rise of the bicycle maker Giant Manufacturing has been

surprising. By 1980, Taiwan was the largest exporter of bicycles in the world and

today with over $ 400 million in total sales; Giant Manufacturing is one of the

largest bicycle producers in the world.

Indeed, in 2001, Giant was named one of Fortune Magazine’s ‘20 best small

companies in the world’ (http://money.cnn.com/magazines/fortune). Perhaps

almost as surprising as Giant’s rise is the fall of the old guard of bicycle

producers.

Derby Cycle had gone into bankruptcy and was largely broken up, Schwann had

been sold out of bankruptcy to Pacific Cycle for a mere $86 million and then

acquired by Dorel Industries in 2004, and Huffy went into bankruptcy in 2004 for

restructuring, emerging in 2005. All this was during a period of 30 years of

healthy growth in the bicycle industry as a whole.

26

Giant Manufacturing began in 1972 as a low-end manufacturer and exporter of

bicycles. It received its first large break in 1981 when the largest us bike maker,

Schwinn, hired it to produce bicycles.

Giant provided engineering, technology, and volume sales, and Schwinn

received bicycles that were less expensive than those produced in the us, and

sold them under its own name in the us. By 1984, Giant was producing 700,000

bicycles a year for Schwann.

When in 1985 Schwann and Giant ended their partnership, it was only a partial

break, since Schwann continued to outsource to Giant, though not to as great an

extent as before, but it was nevertheless a significant break.

This acted as a catalyst for Giant, who was at this point outsourcing for many us

bicycle producers, and was therefore spurred to create its own brand. Giant

began selling its own brand of bicycles first in Europe and then, in 1987, in the

us. It routinely offered bike distributors a 15% discount on bikes identical to those

sold by Schwinn without the name brand and could afford to gradually build

volume since it had its supporting production for the us companies.

Back in the 1970s Giant did something very surprising (the significance of which

will be addressed later). It reversed the trend of outsourcing to markets where

labor was cheap, and built a factory in the Netherlands. It chose this location, we

believe, because the Netherlands is considered a trendsetter in European design

and because of the excellent Rotterdam port and a large nearby airport.

Indeed, the Netherlands is also one of the largest recipients of us foreign direct

investment. This factory was meant to pick up on ideas and trends in the

European racing bike tradition. One of the interesting aspects of Giant product

line was that only 75%of it was standard, the remaining 25% was designed by

regional managers to have local appeal. Giant has designers in the us, Europe

and Asia and, twice a year, gathers them all together at its factories in Taiwan to

work out ways to lighten the frame, increase strength, etc.

27

Giant has recently begun establishing factories in China. In 1996, for example, it

produced 2.02 million bicycles, of which 1.5 million were produced in Taiwan,

550,000 in China, and 300,000 in the Netherlands. Currently they are the biggest

bike sellers in China, accounting for 3% of all bike sales in this growing market.

INTRODUCTION TO THE INDUSTRIAL BANK OF TAIWAN

Founded in 1999 by Chairman Kenneth Lo, the Industrial Bank of Taiwan (IBT)

has been committed to establishing teamwork and professionalism. In addition to

providing comprehensive financial services, the bank is seeking aggressively

cooperation or strategic alliance opportunities within and outside the financial

industry so as to expand operating scale and pursue sustained growth.

In 2000, IBT initiated its first round of acquisitions: IBT Securities (formerly Sheng

Ho Securities), IBTS Investment Consultation, and IBT Asset Management.

Meanwhile, IBT established a 100% owned subsidiary, IBT Management

Corp.(IBTM), a venture capital management firm. IBTM subsequently raised two

venture capital funds. The bank has tentatively completed its preliminary

conglomeration. In 2006, the bank started its second round of acquisition:

(1) Investing in China Bills Finance Corp.,

(2) Establishing IBTS Asia (Hong Kong) Limited,

(3) Purchasing EverTrust Bank in the U.S. and

(4) Acquiring Shen Hua Investment Trust. These moves have helped the bank to

expand its geographical presence, increase market share and enhance resource

integration.

Currently the IBT Group engages in industrial banking, securities, investment

consultation, asset management, bills finance, commercial banking, venture

28

capital and subsidiaries in the U.S. and Hong Kong. Looking forward, the Group

will continue its acquisition moves and aspire to become a global financial group.

ROLE OF INDUSTRIAL BANK OF TAIWAN

After integrating the firm’s brokerage, underwriting, bonds, futures, investment

trust, investment consultancy, and venture capital divisions, the IBT Group is now

capable of providing our corporate customers with a wide range of financial

services.

Our corporate customers require different financial services. They will need

services of capital injection, guidance on the initial registration at OTC,

application for banking facilities, issuance of corporate and convertible bonds,

hedging of interest and exchange risks, asset securitization, financial consultancy

services, project finance, and asset management, etc.. Thus, IBT is deciated to

meet all the customers' needs at their different business stages.

INTRODUCTION TO TRANSCEND

Transcend was founded in 1988 by Mr. Peter Shu and has its headquarters in

Taipei, Taiwan. Our extensive product portfolio has grown to include over 2,000

memory modules of every type, flash memory cards, USB flash drives, MP3

players, digital photo frames, portable hard drives, multimedia products and

accessories. Transcend products are available for proprietary equipment, as well

as for mass marketed PCs.

Transcend is a global company with offices around the world, thus we are able to

serve all the major markets and provide superior quality of service to our

customers. Our overseas offices were opened in California, USA (1990),

Germany (1992), The Netherlands (1996), Japan (1997), Hong Kong (2000),

China (2000), UK (2005), Maryland USA (2005), Osaka Japan (2007) and Seoul

Korea (2008). Transcend is a strategically integrated Hi-Tech company, not only

29

do we design, develop, and manufacture our branded products, but we also

market and sell our own devices. Transcend has a very successful retail store

chain in Taiwan and after we launched our initial foray into e-commerce in May

2000 our on-line sales have grown exponentially.

Transcend has always been a customer driven company, we focus our efforts on

providing the highest quality products with attentive after sales service and

support, that ensures total customer satisfaction. The corporate culture that

exists within Transcend is one of professionalism and teamwork. As a declaration

of our commitment to quality we implemented the Total Quality Control concept

throughout the company, and became the first memory module manufacturer in

Taiwan and the second in the world to receive ISO 9001 Certification.

Transcends Advanced R&D Teams have over 19 years of experience in

developing quality state-of-the-art Hi-Tech products that are at the very cutting

edge of technology. Our commitment to R&D ensures that we will continue to

produce superior quality innovative products keeping us at the forefront of our

industry and leaving the competition far behind.

As a company Transcend can best be described as, a World-Class leader in the

field of memory and consumer electronics, which brings you tomorrow’s World,

Today.

INTRODUCTION TO ACER

Acer Inc. is a multinational information technology and electronics corporation

headquartered in Xizhi, New Taipei City, Taiwan. Acer's products include desktop

and laptop PCs, tablet computers, servers, storage devices, displays, smart

phones and peripherals. It also provides e-business services to businesses,

governments and consumers. Acer is the fourth largest PC maker in the world.

In addition to its core business, Acer also owns the largest franchised computer

retail chain in Taipei, Taiwan.

30

The Acer Group is a family of four brands -- Acer, Gateway, Packard Bell and

eMachines. This unique multi-brand strategy allows each brand to offer a unique

set of brand characteristics that targets different customer needs in the global PC

market. Today, the Acer Group still strives to break the barriers between people

and technology. It ranks No. 4 for total PC and No. 2 for notebooks shipments*,

and has a global workforce of 8,000 employees. Revenues for 2011 reached

US$15.7 billion.

In 2006, Acer celebrated 30 years of long-term growth in the fast-paced IT

Industry. Today, the Acer Group stands firm to its commitment in developing

easy-to-use and dependable products that meet our customers' needs. Our long-

term mission is Breaking the barriers between people and technology through the

creation of empowering hardware, software and services.

Acer is devoted to designing IT products that improve usability and add value to

our customers needs -- be it at work or leisure. We believe innovation is not the

mere creation of new technologies and solutions, but the guarantee that users

receive the benefits of these developments, and feel truly empowered.

The Acer Group family of brands -- Acer, Gateway, Packard Bell and eMachines

-- and their respective sub-brands offer products with distinguished brand

characteristics that target different customer needs in the global PC market.

The successful mergers of Gateway Inc. (October 2007) and Packard Bell Inc.

(March 2008) by parent company, Acer Inc., completes the group's global

footprint by further strengthening its presence in the U.S. and Europe.

It began with eleven employees and US$25,000 in capital. Initially, it was

primarily a distributor of electronic parts and a consultant in the use of

microprocessor technologies. It produced the Micro-Professor MPF-I training kit,

then two Apple II clones; the Microprofessor II and III before joining the emerging

IBM PC compatible market, and becoming a significant PC manufacturer. The

company was renamed Acer in 1987.

31

In 1993, Acer posted record profits of $75 million; 43 percent of that year's net

was generated by the DRAM joint venture, considered "the most efficient in the

DRAM industry" by some observers. Total sales grew to $3.2 billion in 1994, and

net income increased to $205 million, as Acer America turned its first annual

profit in the 1990s. From 1994 to 1995, Acer advanced from 14th to ninth among

the world's largest computer manufacturers, surpassing Hewlett-Packard, Dell,

and Toshiba.

In 1995, the Aspire PC was unveiled. In 1996, Acer expanded into consumer

electronics, introducing many new, inexpensive videodisc players, video

telephones, and other devices to boost global market share, and in 1997

extended its laptop efforts by buying Texas Instruments' mobile PC division.

Considering two consecutive quarters of net losses in Q2+Q3 2011 and realized

to many products which Acer sells 101 individual notebook, netbook and

chromebook SKUs in the United States only, Acer will cut product lines by two

thirds begins in 2012.

Acer wins international-scale supercomputer contract

TAIPEI, TAIWAN (November 16, 2010) – Acer has been awarded the contract

for Taiwan’s National Center of High-performance Computing’s (NCHC) overhaul

of its major supercomputer in Taichung, central Taiwan. Scheduled for

completion at the end of March 2011, the supercomputer will offer High-

Performance Computing (HPC) services to a wide range of research and

industrial customers in Taiwan. The installation is expected to place in the top

50* of the TOP500 fastest supercomputers around the world.

ISO/TL Management System

Acer is an ISO 9001 and ISO 14001 certified company, meaning our quality

control and environmental management systems meet international standards.

The International Organization for Standardization (ISO) was established in

32

Geneva, Switzerland in February 1947 with the goal to promote standardization

of related activities in all countries around the world.

INTRODUCTION OF THE ASUS

ASUSTeK Computer Inc. (trading as ASUS)

Type Public

Traded as LSE: ASKD, TWSE: 2357

Industry Computer hardware Electronics

founded April 2, 1990

Founder(s) TH Tung ,Ted Hsu ,Wayne Hsieh, MT Liao

Headquarters Beitou District, Taipei, Taiwan

Area served Worldwide

Key people Jonney Shih (Chairman),Jerry Shen (CEO)

Products

Desktops, laptops, notebooks, mobile phones, network

equipments, monitors, motherboards, graphics cards, optical

storage, multimedia products, servers, workstations

Revenue US$19.07 billion (2010)

Profit US$390 million (2010)

Employees 113,324 (2010)

Website Asus.com

33

ASUSTeK Computer Inc. is a multinational computer hardware and electronics

company headquartered in Taipei, Taiwan. Its products include motherboards,

desktops, laptops, monitors, tablet PCs, servers, video cards, and mobile

phones. It also produces components for other manufacturers, including Apple

Inc., Dell, Falcon Northwest and Hewlett-Packard.

As of 26 November 2009, 29.2% of PCs sold in the previous 12 months

worldwide came with an ASUS motherboard.

ASUS appears in Business Week’s "InfoTech 100" and "Asia’s Top 10 IT

Companies" rankings. Wall Street Journal Asia ranks it number one in quality and

service, and it ranked first in the IT Hardware category of the 2008 Taiwan Top

10 Global Brands survey with a total brand value of US$1.324 billion

ASUS is listed on the London Stock Exchange (LSE: ASKD) and the Taiwan

Stock Exchange (TWSE: 2357).

Company Overview

ASUS Technology Private Limited manufactures and sells computer components

in India and internationally. The company’s products include desktop barebone

systems, servers, notebooks, handhelds, network devices, broadband

communications, LCD monitors, TVs, and wireless applications; and chassis,

power supply, and thermal products. Its products also include audio and graphic

cards, digital home, HSDPA cards, mobile phones, motherboards, multimedia,

optical storage devices, PDAs, peripherals, PNDs, workstations, and Webcams.

The company was founded in 2006 and is based in Mumbai, India with branch

offices in New Delhi, Bangalore, Chennai, and Kolkata. ASUS Technology

Private Limited operates as…

ASUS Technology Private Limited manufactures and sells computer components

in India and internationally. The company’s products include desktop barebone

systems, servers, notebooks, handhelds, network devices, broadband

communications, LCD monitors, TVs, and wireless applications; and chassis,

power supply, and thermal products. Its products also include audio and graphic

34

cards, digital home, HSDPA cards, mobile phones, motherboards, multimedia,

optical storage devices, PDAs, peripherals, PNDs, workstations, and Webcams.

The company was founded in 2006 and is based in Mumbai, India with branch

offices in New Delhi, Bangalore, Chennai, and Kolkata. ASUS Technology

Private Limited operates as a subsidiary of ASUSTeK Computer, Inc.

Companies in Taiwan Have Large Stakes in Markets for PCs, LCDs,

Semiconductors and Mobile Phones; Branded Businesses and Manufacturing

Operations Are Becoming More Distinct.

Taiwan`s information and communications technology (ICT) companies play a

key role in the global supply chain for electronics products. Taiwanese

companies account for about three-quarters of the world`s production of PCs and

half of the world`s liquid-crystal displays (LCDs). In addition, Taiwan makes

about a quarter of the world`s semiconductors and about a fifth of the world`s

mobile phones.

Taiwan has a population of 23 million and a land area of only 36,260 square

kilometers, less than half of a percent of the 9.6 million square kilometers of land

in China. Yet the well-educated, industrious people of Taiwan have helped to

carve out a huge niche in the global ICT industry.

The Economist Intelligence Unit (EIU), a renowned British think tank, last year

announced the results of a global study of IT industry competitiveness. Based on

the study, Taiwan's IT industry rose to second place from sixth place in the

previous year out of a total of 66 nations included in the study. The report noted

that Taiwan`s rise in the rankings owed mainly to its strong performance in R&D,

particularly regarding patented technology.

The Taiwan ICT industry has grown to a size that has resulted in substantial

diversification, and many large companies have separated manufacturing units

from branded operations in order to allow greater specialization in both of

these areas.

One example of this is Acer Inc., which in the last five years has grown to

become the world`s third-largest PC maker by market share. The company no

35

longer does manufacturing in house and spun off its production units into

separate companies including Wistron Corporation. Wistron now does

manufacturing for a wide range of companies including some of the best known

brands in the notebook computer business.

INTRODUCTION TO YOKO TECHNOLOGY CORP

Established in 1992, YOKO Technology Corp. is now a well-known professional

video surveillance system manufacturer in Taiwan. We have been dedicating to

R&D, manufacturing and marketing of video surveillance products. Accumulating

17 years of efforts, we have taken advantage of the vast experience in our core

technologies in CCTV field. YOKO has grown to be a world-renowned video

surveillance system manufacturer. According to the studies of a

famous market survey institute in Japan, YOKO had become the No. 1

manufacturer of the professional surveillance camera around the world in 2004.

YOKO has successfully developed a variety of CCTV Camera, Quad Processor,

Multiplexer, DVR, IP Camera, Video Server, Portable Product, CCTV Lens,

Monitor and other peripherals to meet all requirements from customers. It is the

best solution for “one-stop shopping ".

Our strong R&D team always devotes efforts to the full range of CCTV products.

All of YOKO merchandise are derived from a precise design, manufacturing and

testing process which assures good functions, stable quality, fast and punctual

delivery, as well as competitive pricing. We have hence gained a prestigious

success and recognition among our customers in the world. YOKO has grown to

be a high-tech manufacturer and integrator of video surveillance system.

In order to provide better service to our customers and accommodate to YOKO's

rapid growth, we relocated our business headquarters to a new site in September

2005. In the future, we will continue to build up the channels and locations

necessary for YOKO to become the world leader in CCTV equipment.

36

INTRODUCTION TO ORANGE ELECTRONIC CORPORATION LTD.

Company Name : Orange Electronic co., LTD

CEO : Aliber Hsu

Country : Taiwan Republic of China

Major Business Focus : Importer, Exporter, Manufacturer, OEM, ODM

Primary Export Products: TPMS, PWM motor controller, Ignition, regulator, auto

electronic parts.

Major Export Markets : United State, Mainland China, Japan, Republic of

Korea, Taiwan, Republic of China, United Arab Emirates, Germany, France,

United Kingdom, Canada, Saudi Arabia……(2011-01-07)

Orange Electronic Co., Ltd. Was found in 2005 in Tanzih, Taichung, committed to

high temperature, radio frequency and power management of three core

technology research, focus on wireless tire pressure monitoring system (TPMS),

currently world’s sixth largest supplier of tire pressure monitoring system,

production capacity has one million production level.

Orange Electronic North America is one of the nation’s most premier automotive

accessory providers supplying aftermarket and original equipment tire pressure

monitoring systems (TPMS). Operating out of Cincinnati, Ohio, Orange Electronic

is the North American affiliate of our parent company Orange Electronic.

Orange prides itself on high quality, easy to use TPMS and vehicle accessories

at competitive prices. The entirety of Orange’s product line is factory, wireless

and quality certified at multiple levels and in multiple countries, ensuring the

highest international quality and production standards. Avoiding the “middle-

man”, Orange is able to maintain low prices with straight-to-dealer shipping.

37

Orange’s TPMS sensors have a two-piece construction that saves users

expensive replacement costs. If the less costly valve is damaged, there is no

need to replace the sensor. A factor of the two-part construction, Orange sensors

can also be angled to conform to a wide range of tire rims, reducing the number

of SKU’s needed in-house.

Through our certified radio frequency (RF) patented technology, Orange TPMS

can be integrated into a variety of wireless devices including on-dash displays,

GPS, DVD and rear-view mirrors.

Since 2007 all vehicles are required to be equipped with a TPMS system.

Orange Electronics’ objective is to simplify and standardize the aftermarket

replacement of TPMS systems. With every vehicle utilizing TPMS, increases in

driver safety and tire tread life as well as savings in gasoline and carbon-

emissions will be realized in the US and abroad.

SEMA (Specialty Equipment Market Association) is an automobile aftermarket

association formed in 1963 bringing together aftermarket manufacturers, original

equipment manufacturers, car dealers, installers and retailers. Each year this

organization hosts the premier automotive specialty products show attracting

over 100 countries and 100,000 visitors worldwide.

At the 2007 show, Orange Electronic placed 1st in the new product category with

our retrofit TPMS kit. This award truly indicates that Orange TPMS is one of the

highest qualities and necessity as TPMS is newly mandated for all new vehicles

produced in the United States.

Orange Electronic passed many national certifications

Orange Electronic has placed a strong focus on creating innovative products of

the utmost quality. Indicative of this commitment, Orange has gained a number

international quality and safety certifications.

38

The company's growth process, gradually made such as the U.S. FCC,

European E-mark, the Japanese ARIB, South Korea MIC, Taiwan, Canada IC,

and Taiwan NCC and other major countries around the world of wireless

regulatory approvals, as well as through such FMVSS138, SAE J2657, CE ....

And so on TPMS certification testing standards, as well as ISO9001, TS16949

automotive quality standards such as global management system for product

quality endorsement is on the market consumers.

Orange electronic focus on U.S. market early, in view of the U.S. federal

government began to legislate for vehicles with TPMS, the market completely

dominated by the original supply, and worldwide supplier of TPMS technology

does not exceed 10. Orange's efforts to overcome technical barriers and

electronic access barriers abroad, completely specializes in market analysis and

develop a unique strategy for the use of information, early layout was not favored

by the major vendors selling after market), to provide OE replacement parts and

TPMS retrofit kits.

INTRODUCTION TO YULON

With the aim of "Using Generators to Save the Nation", the founder of the

company Mr. Ching-Ling Yen established the company on September 10, 1953.

Under the superior leadership of Mr. Yen, the company has not only built up a

solid and concrete foundation of automobile industry for our nation but also lead

the development of related industries and makes a remarkable contribution for

the progress and prosperity of our society. Mrs. Vivian Wu was elected by the

board of chairmen to be the 2nd chairperson of our company after the founder

Mr. Yen died on March 20, 1981.

In the beginning, YULON was named "YULON Machinery Co., Ltd", and the

business scope included machinery manufacturing and sales. YULON signed up

a technical collaboration agreement with Nissan in February 1957, and changed

the name to be "YULON Motor Co., Ltd" and officially manufactured sedan and

commercial truck.

39

From 1961 to 1980, the economy of Taiwan started to bloom, the average

income of the citizen was over 2,000 US dollars a year and the automobiles

market scale had reached 150,000 cars a year. With the assistant programs &

policy from the government, YULON started to expand production capacity and

open up the automobiles¡¦ market in Taiwan and took the lead of the entire

development of automobiles¡¦ industry in Taiwan.

From 1981 to 1990, the economy of Taiwan grew rapidly, the average income of

the citizen was over 10,000 US dollars a year and the automobiles market scale

had reached 350,000 cars a year. In order to build up car design capability in

Taiwan, YULON established the Sanyi manufacturer and engineering center in

1981, to bring in the most recent production technologies, to purchase production

equipments and to train production experts. "Feeling 101" was launched in 1986

and was the first motor vehicle designed and manufactured by our nation in

Taiwan. "Give the R. O. C. its own wheel".

From 1990 till now, the economy of Taiwan has become internationalized and

freedom, the average income of the citizen is even reached 13,000 US dollars a

year, the automobiles market scale has reached 400,000 to 500,000 cars a year

and YULON has set up a new standard of business management and

competition among traditional industries. In order to be adapted the entering to

WTO of our nation in the near future that will result in bringing all imported cars to

our local market, YULON moved Taipei headquarter, Taoyuan engineering

center, and Sin-Tien factory to Sanyi. By centralizing all workplaces, YULON was

able to reduce the cost of communication, reform company organization,

reconsolidate corporate resources as well as increase the competitiveness. The

benefit and efficiency of "workplace centralization" is quite remarkable and has

been well recognized and duplicated by the others.

In order to meet the challenge of current tough market situation and after the

upgrade of engineering center to YULON Asia Technology Center (YATC) in

November 1998, YULON used ¡§three circles strategy¡¨ to start the third wave of

40

corporate restructuring, and with our new corporate culture of "Innovation,

Speed, and Teamwork" to reach the optimal new vision of "The Leader of Moving

Value Chain in the Ethnic Chinese Auto Market". Responding to the globalization

of business strategy, YULON had moved the parts center from Chu-pa to Sanyi

plant and built up YULON Asia Parts Center (YAPC) in year 2000 to be the

logistics center of Taiwan, Mainland China and Hong Kong. In 1999, YULON

announced the investment to Nissan Motor Philippines Corporate (NMPC) and

moved forward to Southeast Asia market. In addition, in order to enforce the

product lines, YULON signed a formal alliance agreement with RENAULT and

became RENAULT sole distributor in Taiwan in year 2000.

On May 20th, 2003, YULON Motor and NISSAN Motor had a co-announcement,

YULON Motor split to two independent companies; one is YULON Motor Co.,

Ltd. and the other one is YULON-NISSAN Motor Co., Ltd. YULON will aim to

produce 120,000 cars in Taiwan and fulfill the goal of becoming the center of

manufacturing service. The goal of YULON¡¦s automobile business is to provide

the moving convenience to the consumers, and in the same time, to increase the

customer-made products as well as to develop the business of automobile

accessories and peripherals market. By assisting NISSAN in designing,

researching and manufacturing, and by more collaboration with NISSAN,

YULON-NISSAN will be able to anticipate NISSAN¡¦s operation in the Mainland

China¡¦s auto market and reach the goal of selling 550,000 cars in 2006 and

increase to 900,000 cars by 2009. In the future, YULON group will continue the

faith of "Keep the root in Taiwan, look forward the market in Mainland China and

international market", and make the best effort to pursuit the vision of "become

the biggest automobiles group among ethnic Chinese market".

41

Introduction of the selected Company / Industry / Sector and its

role in the economy of Taiwan

Giant Organization Chart:

Positioning of Giant Bicycle

Market share of giant

Giant has become a USD$1.2 Billion empire making it the largest bicycle

company in the world with a 10% global market share......and it all started here in

a factory on the nondescript outskirts or Taichung, Taiwan

42

The Giant Bicycle Company aims at taking us even beyond our automobiles –

into the world of cycling and wellness. Giant Manufacturing Co. Ltd. founded in

1972 is a Taiwanese bicycle company which bills itself as the world’s largest

bicycle manufacturer. Giant has manufacturing operations in Taiwan,

Netherlands, and China. Giant today is a top brand by itself and sells in over 50

countries through 10,000 retail stores.

So how does a small company from a small country become a big global

brand?

Great leadership King Liu was a charismatic leader with a powerful an inspiring

vision –To be the world’s best bicycle company. It was in Taichung in west-

central Taiwan a young 38 year old after trying his hand on several small

businesses chose to manufacture bicycles. He realized that riding bicycle was a

worldwide trend and his vision went way beyond the profitability of business – he

was into the growth of both cycling and cycling culture. Underlying his vision was

a strong belief that cycling is good for people’s health and well being and good

for the environment.

In the first decade of Giant’s growth overseas sales were very low and it was not

because of quality – it was more due a perception of lack of trust in a ‘Made in

Taiwan’ product. King Liu resolved to make Taiwan as synonymous with bikes as

Switzerland was with watches. It became his dream to turn Taiwan into a cycling

nation.

Building Brand started from Taiwan: That’s when Giant began to market

bicycles under their own brand name in Taiwan. King Liu’s cycling trip was

symbolic of cycling being a combination of lifestyle and leisure and also a natural

expression of success in life. As a result Taiwan enthusiastically celebrates the

first Sunday of May as national cycling day.

43

Giant went into an image change overdrive from the older heavy bicycle

stereotype to state of the art high-end bicycles. Commitment to sport of cycling

reflected through sponsorships of professional and amateur teams at

International and regional levels. Global Giant Mountain Bike Team and ONCE

level 1 road team became trend setters. Such sponsorship allows product

developers to see their designs in real world settings leading to further product

development.

Balancing innovation and efficiency simultaneously

(a) Innovative and entrepreneurial capabilities were triggered through the

bicycle ‘cluster effect’. Michael Porter in his cluster theory highlights how

several competitive benefits (innovation, knowledge exchange etc)

accrue when interconnected players within an industry are concentrated

in close proximity – in this case the Taiwanese bicycle cluster.

(b) Giant achieved cost efficiency by moving manufacturing facilities to China.

The cluster effect also helped reduce transaction costs, R&D costs and

attracts international customers due brand power generated by cluster.

Global Giant Local Touch – this ability was another source of competitive

advantage. Giant’s worldwide HQ oversees global considerations and

coordination such as brand mgt, product R&D & finance etc. Global

standardization through their superior wheel system and a light bicycle frame

system were patented and standardized (75%) for their products globally to

achieve economies of scale.

The local touch was captured through Giants regional sales companies who

were given freedom to collect analyze and react to local consumer needs and

market trends with 25% customization. As a result Giant US and Giant Europe

sell different selections of bicycles. To understand the Chinese environment and

draw maximum value from Chinese JV partners’ unique lower cost manufacturing

44

skills Giant practiced Guanxi in a spirit of trust and mutual respect and

cooperation.

Overseas Expansion

The Dutch just love their bicycles and ride them everywhere. It was natural for

Giant to pedal into this bicycle-friendly nation as an entry into the European

market. Here again King Liu rode more than 500 kilometers heralding a Green

World on Wheels Tour

Gain firsthand experience riding in one the most cycling friendly nations in the

world. It is King’s hope that his Green World on Wheels Tour will open up

communication with The Netherlands as Taiwan continues to improve its own

cycling infrastructure.

In 1980s Giant overtook American manufacturers with lightweight bicycles and

the European market with MTB (Mountain Bikes). In addition to light weight

frames were their high-quality shock absorber and aluminiumalloy bikes.

The Giant name now is synonymous with technological innovation and the state-

of-the-art throughout the global bicycle industry. Giant continues in 2011 to top all

other manufacturers in prestigious events and reviews of best bikes in the world

market.

Industrial Bank of Taiwan

Chairman Kenneth Lo

Positions Held

Chairman of Industrial Bank of Taiwan, Chairman of IBT Management

Corp., and Chairman of Boston Biotech Venture.

President Henry Peng

45

Position Held

President of Industrial Bank of Taiwan

As they approach the 21st century, our government has allowed the

establishment of industrial banks, turning a new chapter in our financial industry.

Industrial Bank of Taiwan became the first government-approved industrial bank

as a result of our solid business plan and quality of our staff members. We have

been striving to live up to the expectations of our clients by rendering

professional services through our service-oriented commitment.

Via strategic alliances with internationally renowned investment banks, we could

continuously roll out financial products that meet customer requirements. After

our bank’s listing on the local exchanges, we hope to enter the international

financial arena to provide strong support to our corporate clients in their overseas

business efforts. We also hope to become, ultimately, one of the best investment

banks in the Asia-Pacific region.

Banking industry faces a huge challenge after Taiwan’s accession into WTO and

the emergence of financial holding companies. The declining profit margin from

traditional banking business poses significant threat to our existing business. In

addition to our traditional banking businesses, we are devoted to developing new

value-added businesses and increasing shareholders returns. Meanwhile, we

have been working closely with many financial institutions to broaden our product

offerings.

Going forward, we will continue to enhance our earning capabilities and create

a win-win situation for both clients and shareholders.

CORE VALUES OF THE COMPANY

46

The IBT focuses on core values of “honor,” “integrity,” “team work,” “innovation,”

“professionalism,” and “meritocracy.” With visions and professionalism, the bank

continues to enhance its earning capabilities and pursue a sustainable growth.

IBT is dedicated to our clients, shareholders, employees and society. For clients,

we will deliver high-quality professional services and develop innovative financial

products to meet their needs. For shareholders, we strive to achieve sustained

growth to ensure maximum return. For employees, we promote teamwork and

have sound incentive plan. For society, we intend to actively participate in public

service to make a better tomorrow for our society.

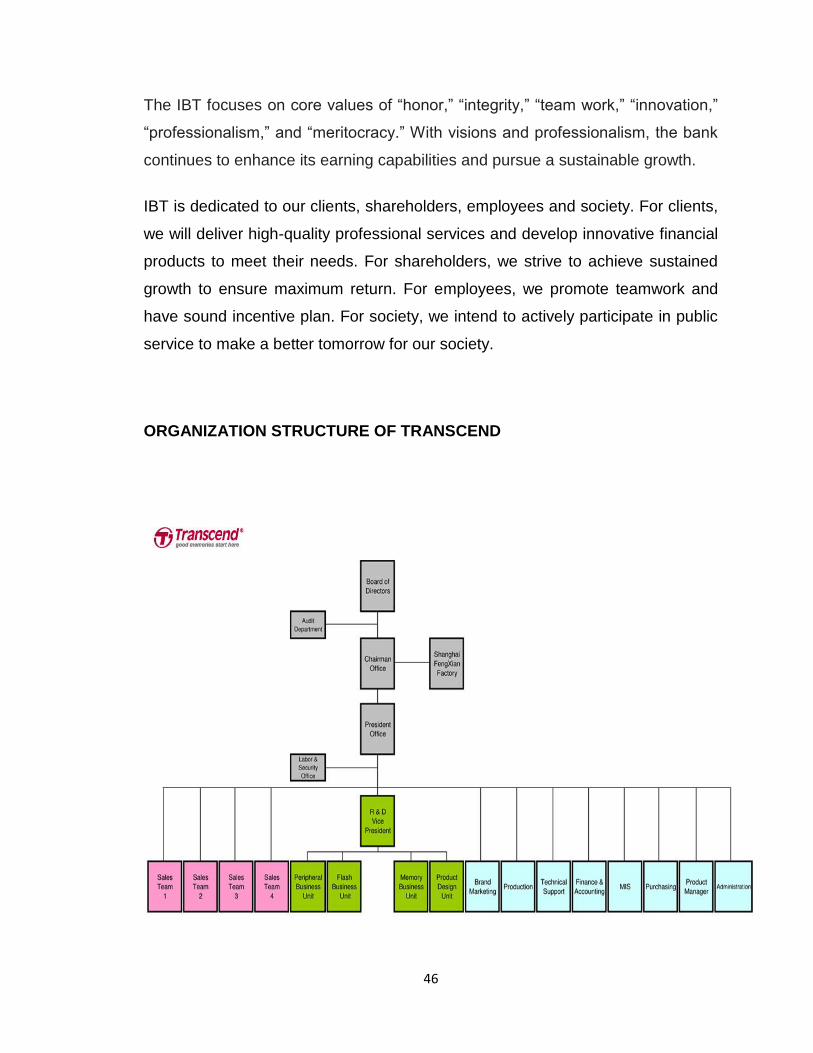

ORGANIZATION STRUCTURE OF TRANSCEND

47

BUSINESS ACTIVITIES OF TRANSCEND

For over 20 years, Transcend has produced high reliability DRAM memory

modules and flash-based devices for use in both commercial and industrial

environments. Continuing research and development investment allows

Transcend to create advanced products for industrial computing applications

worldwide. Leveraging years of industrial-grade manufacturing expertise,

Transcend has built a great reputation as one of the world’s most innovative

developers of high quality and reliable industrial-grade memory devices.

Transcend offers comprehensive IPC solutions. Our clients include leading

vendors in the industrial computing field and our products are widely used in a

variety of industries, such as industrial automation, medical equipment,

military/defense, data acquisition, banking/ATM, gaming, transportation,

POS/POI, kiosks, and digital signage.

Transcend’s industrial-grade products target at extremely demanding

applications in rugged environments in terms of shock, vibration, humidity and

temperature. In addition to standard products, we offer customized industrial-

grade products to fit your specific application demands.

Structure of Acer Computers

Client-server organizational structure

In order to carry out its vision of a decentralized confederation of business

units, Acer reorganized itself into a “client-server” organizational structure In the

clientserver structure, all of Acer’s business units and affiliated companies were

48

expected to act as clients or play dual client/server roles in support of other

member companies. The clients and servers were separated according to either

product lines or regions. Strategic Business Units (SBUs) were responsible for

the design, development and production of components and systems and were

also responsible for OEM sales and marketing. Regional Business Units (RBUs)

were primarily Acer-brand marketing companies, responsible for specific regional

territories. They developed new distribution channels, assembled finished

products, provided support for dealer and distributor networks, and created new

joint ventures in key local markets.

Acer established four special functional teams (IT, logistics, customer service,

and brand management) directly from headquarters to oversee these four key

functions throughout the various business groups. The IT Steering Committee,

responsible for coordinating IT across the entire Acer Group, consists of chief

information officers (CIOs) from each of Acer’s business units. In addition

headquarters may also assign cross-group task teams to implement short-term

projects that cut across business units.

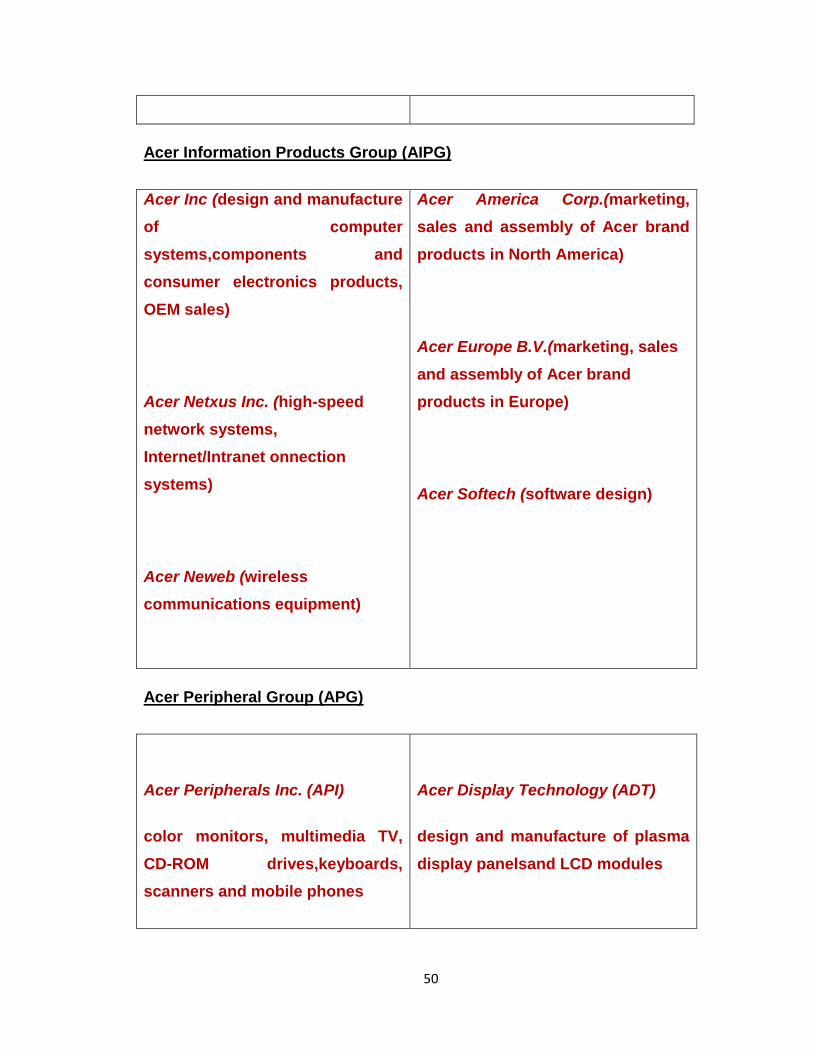

Functions & business units of Acer computers

Acer International Services Group (AISG)

Acer Computer International

(Marketing, sales and assembly of

Acer brand products in Asia, Africa,

the Middle East, Australia, New

Zealand and CIS countries)

AASOFT (software content