a corrected lagrange multiplier testapplication to stock market returns dissertation ... economics...

TRANSCRIPT

A CORRECTED LAGRANGE MULTIPLIER TEST WITH APPLICATION TO STOCK MARKET RETURNS

DISSERTATION

Presented in Partial Fulfillment of the Requirements for

The Degree Doctor of Philosophy in the Graduate

School of The Ohio State University

By

Edward Richard Percy, Jr., B.S., M.S., M.B.A.,C.P.A.,M.A.

* * * * *

The Ohio State University 2005

Dissertation Committee: Approved by Professor J. Huston McCulloch, Adviser Professor Paul Evans

___________________________ Professor Stephen R. Cosslett Adviser Economics Graduate Program

ii

ABSTRACT

This paper introduces a Lagrange Multiplier goodness-of-fit test that is not

biased by the presence of unknown model parameters even in finite samples. Many

well-known goodness-of-fit tests rely on the empirical distribution of residuals being

arbitrarily close to the “true” underlying error distribution; or, equivalently, that model

parameter estimates are actually equal to the parameter’s “true,” typically unknown

values. While this assumption may be approximately correct as for a very large sample

size, such tests are biased towards acceptance with finite sample sizes.

The test statistic of the proposed procedure is asymptotically chi-squared. Exact

finite sample sizes are calculated employing Monte Carlo simulations. Powers of the

test are shown under assumptions of various underlying data generating processes. For

samples of as few as 30 observations, size distortion is quite low.

Any unknown model parameters can be estimated by the maximum likelihood

principle without asymptotically biasing the test. Furthermore, the test is an

asymptotically, locally most powerful test in the class of unbiased tests against a general

set of alternatives.

The methods suggested are a necessary complement to classical procedures,

which often assume a normal error distribution, and nonparametric procedures that do

iii

not rely on a particular error distribution but do require that the unknown distribution

have a finite variance.

Linear, quadratic, and cubic splines are used to search for the best possible

alternative to an error distribution to be tested. These classes of alternative hypotheses

are shown to be members of a set which includes a variation of the classical Neyman

smooth tests and the Pearson chi-squared tests. Comparisons of size and power with

such tests are given.

An empirical example using stock return data is presented comparing symmetric

stable error distributions with generalized student-t distributions.

iv

Dedicated to my parents Marie K. and Edward R. Percy, Sr., my soul mate Georgia Ward, and my stepsons, Matt and Zach

v

ACKNOWLEDGMENTS

I want to express my deep appreciation and significantly acknowledge the vast

amount of input, inspiration and number of original ideas from my dissertation

supervisor, Professor J. Huston McCulloch. I wish to call especial attention to his vast

knowledge of leptokurtic distributions, my use of his excellent bibliography, and his

work, “A Spline Rao (LM) Test for Goodness of Fit: A Proposal,” (1999), which I have

used extensively as seed and, in some cases, the substance of ideas recorded herein.

I also want to thank the other members of my Dissertation Committee,

Professors Paul Evans and Stephen R. Cosslett for substantial counsel and comments,

both written and verbal during my work preceding this dissertation. Additionally, I

want to thank Professor Pok-Sang Lam for his ideas at the proposal stage and for giving

advice while on my Advisory Committee. Professor Nelson Mark may not remember,

but the germination of my interest in error distributions of financial series came from a

meeting with him. I asked him to suggest a research topic for me in his international

finance class and he suggested error distributions on forward premium foreign exchange

rates.

I want to thank the members of the Midwest Econometrics Group for their input

when preliminary ideas from this dissertation were presented, with special thanks to

vi

Professor Anil Bera, who reviewed some preliminary work, offered helpful comments,

and was kind enough to be an outside-the-university reference to recommend that my

work receive support through a university fellowship.

For the stock market return application, I want to thank Professor G. Andrew

Karolyi for providing information and location of the financial series on Kenneth

French’s website,

http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html.

I will close by repetitiously thanking Professor J. Huston McCulloch again; it

was through his contact that I met Dr. Bera and that I learned so much about leptokurtic

distributions. I cannot begin to list all the ideas that he has had in helping me;

additionally, I cannot imagine having a better adviser for this project.

vii

VITA

August 31, 1953……………………………. Born – Lockbourne AFB, Columbus, Ohio June, 1975…………………………………...B.S., Statistics (Major -35 hours) and

Mathematics (45 hours), The Ohio State University

March, 1977………………………………... M.S., Applied Statistics, The Ohio State

University November, 1977 – May 1978……………….Society of Actuary Examinations, 1, 2, & 3 July 1986…………………………………… M.B.A., Business Administration, Dayton

University November 1990…………………………….. Certified Public Accountant December 1998……………………………...M.A., Economics, The Ohio State

University 1975-1977…………………………………...Graduate Teaching Associate, Department

of Statistics, The Ohio State University 1978-1996…………………………………...Vice President, Actuarial and Group

Administration (most notable position among many), Central Benefits Mutual Insurance Company (formerly Blue Cross of Central Ohio)

1997-2002………………………………….. Graduate Teaching and Research

Associate, Department of Economics, The Ohio State University

2003-2004………………………………….. Assistant Professor, Finance and

Economics, Capital University

viii

2005…………………………………………Adjunct Professor, Economics, The Pontifical College Josephinum

2006………………………………………....Instructor, Economics, The Ohio State

University, Marion Campus, Delaware Branch

PUBLICATIONS

The Journal of Labor Economics, “The Long and Short of It: Maternity Leave Coverage and Women's Labor Market Outcomes” (Joint work with Masanori Hashimoto, Teresa Schoellner, and Bruce Weinberg) – (Submitted July 2004; status: revise and resubmit February 2005). “Cash Flow Analysis and Capital Asset Pricing Model”, developed for Keck Undergraduate Computational Science Education Consortium, supported by W.M. Keck Foundation, http://www.capital.edu/acad/as/csac/Keck/modules.html, August 2004. “Option Pricing”, developed for Keck Undergraduate Computational Science Education Consortium, supported by W.M. Keck Foundation, http://www.capital.edu/acad/as/csac/Keck/modules.html, February 2005.

FIELDS OF STUDY

Major Field: Economics Subfields: Econometrics Finance

ix

LIST OF FIGURES

Figure Page Figure 1.1. Two sample densities compared with the uniform distribution. 9 Figure 1.2. Corresponding CDFs to densities in Figure 1.1. 10

Figure 1.3. Comparison of standard normal density to a contrived density that the Pearson test with 10 bins will be unable to detect. 13

Figure 1.4. Additional densities that the Pearson test will be unable to detect. 14

Figure 2.1. Simple cubic spline basis vectors for m=7 28

Figure 2.2. Cubic B-Spline basis vectors for m=7 32

Figure 2.3. Determinants of Fisher information matrices from first 12 simple polynomial bases 37

Figure 2.4. Neyman-Legendre basis with m = 7 39

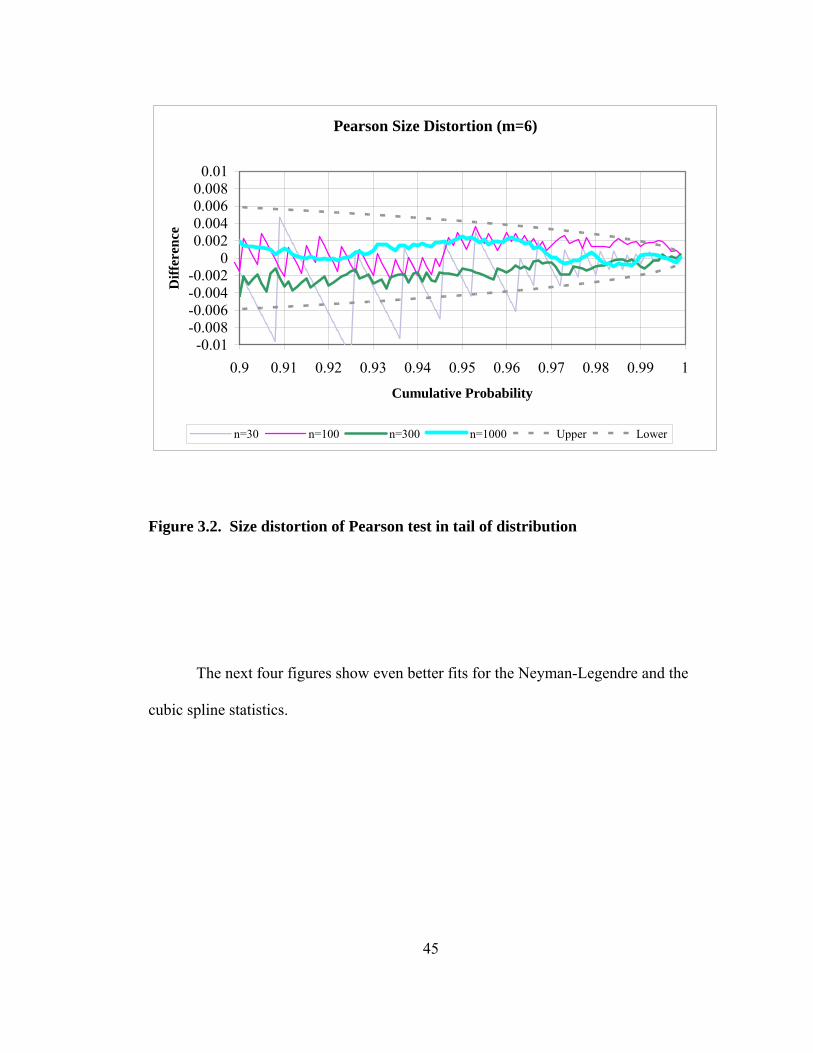

Figure 3.1. Size distortion of Pearson test; difference between chi-square distribution and empirical distribution 43 Figure 3.2. Size distortion of Pearson test in tail of distribution 45

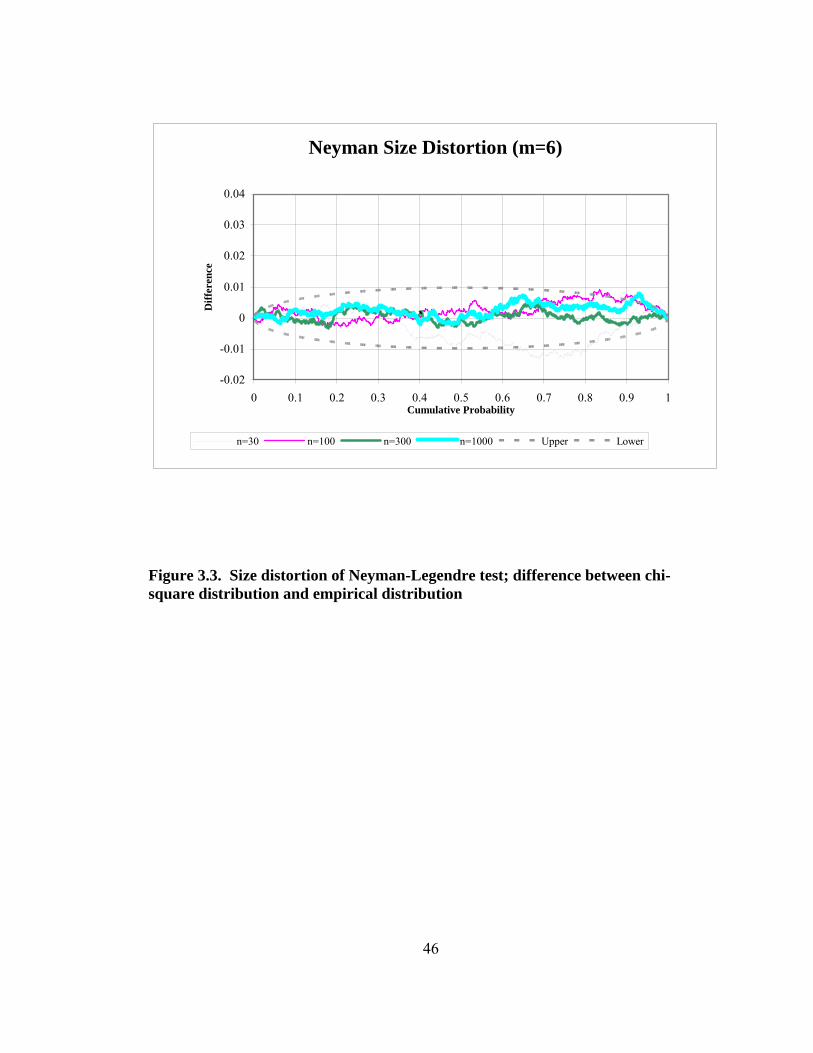

Figure 3.3. Size distortion of Neyman-Legendre test; difference between chi- square distribution and empirical distribution 46 Figure 3.4. Size distortion of Neyman-Legendre test in tail of distribution 47

x

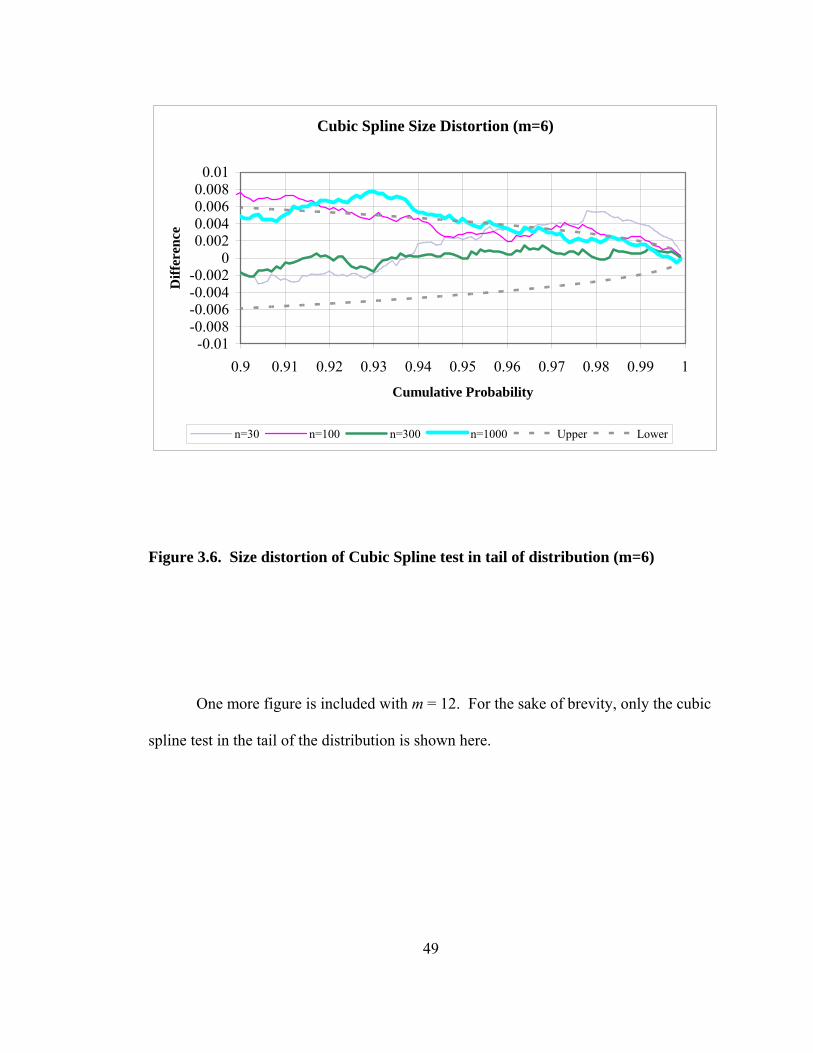

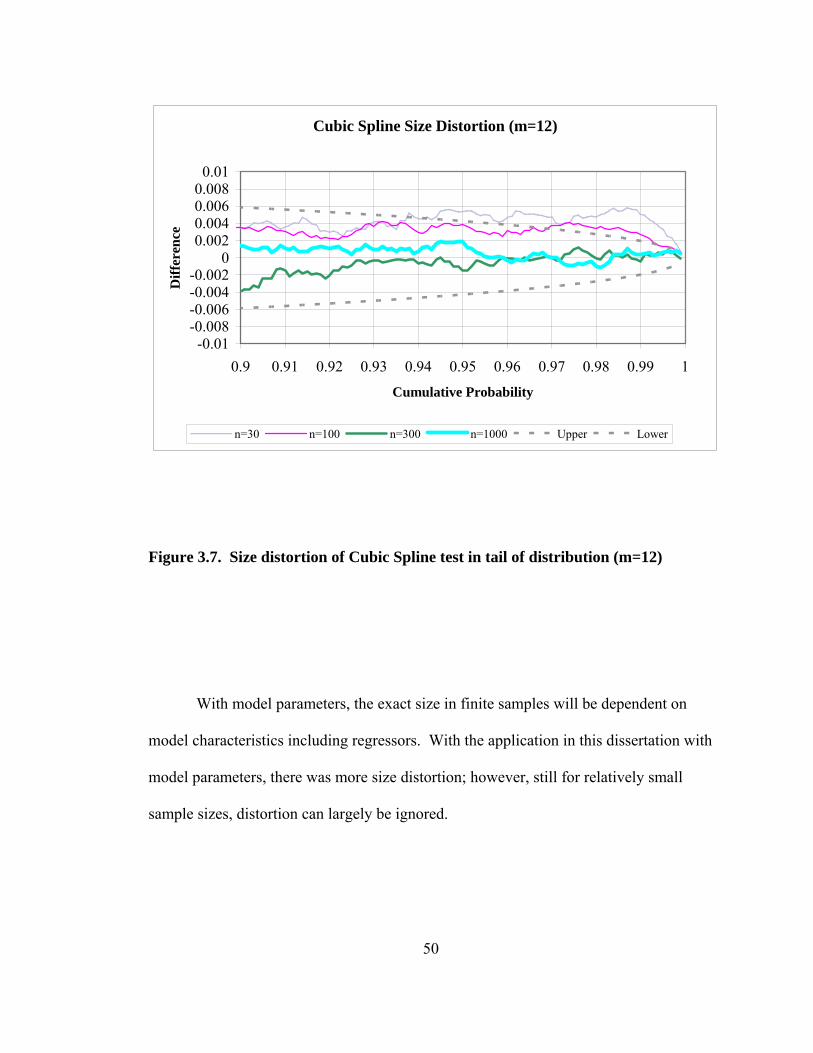

Figure Page Figure 3.5. Size distortion of Cubic Spline test; difference between chi-square distribution and empirical distribution 48 Figure 3.6. Size distortion of Cubic Spline test in tail of distribution (m=6) 49 Figure 3.7. Size distortion of Cubic Spline test in tail of distribution (m=12) 50

Figure 3.8. Maximum likelihood estimates under assumption of Gaussian errors. 54 Figure 3.9. LM Test Statistics and p-values for Gaussian null hypothesis. 55 Figure 3.10. Maximum likelihood estimates under assumption of symmetric stable errors. 58 Figure 3.11. LM Test Statistics and p-values for stable null hypothesis. 59

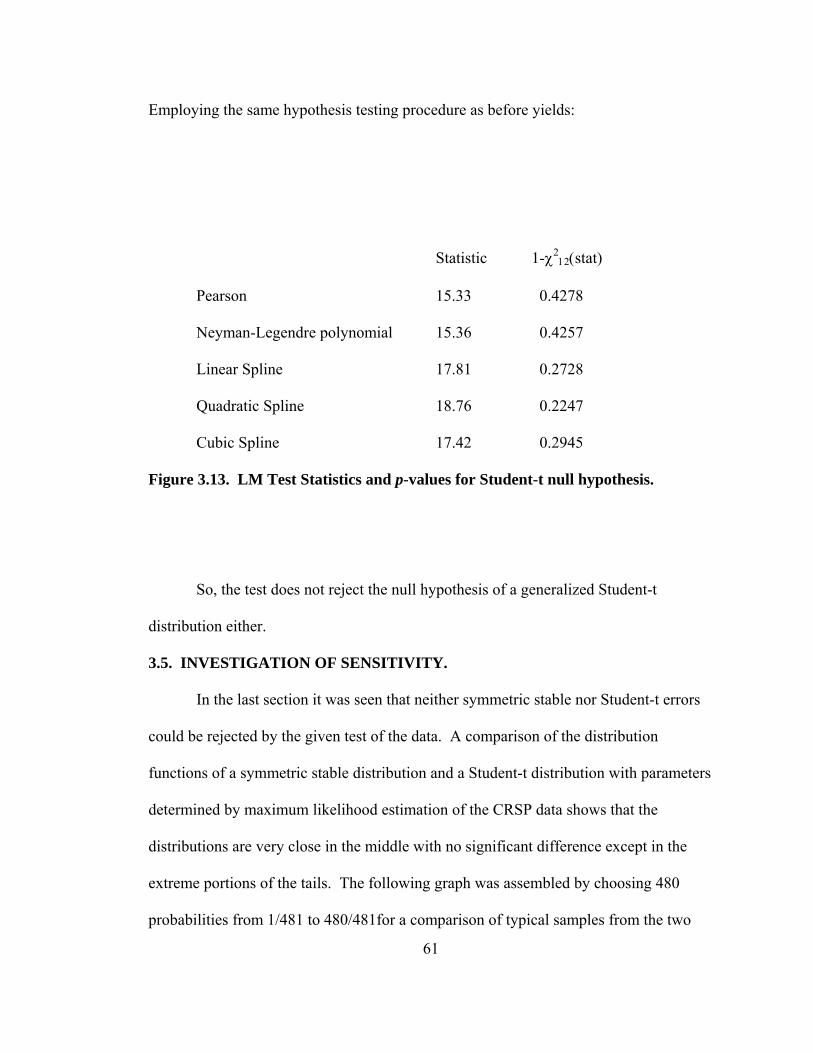

Figure 3.12. Maximum likelihood estimates under assumption of generalized Student-t errors. 60 Figure 3.13. LM Test Statistics and p-values for Student-t null hypothesis. 61

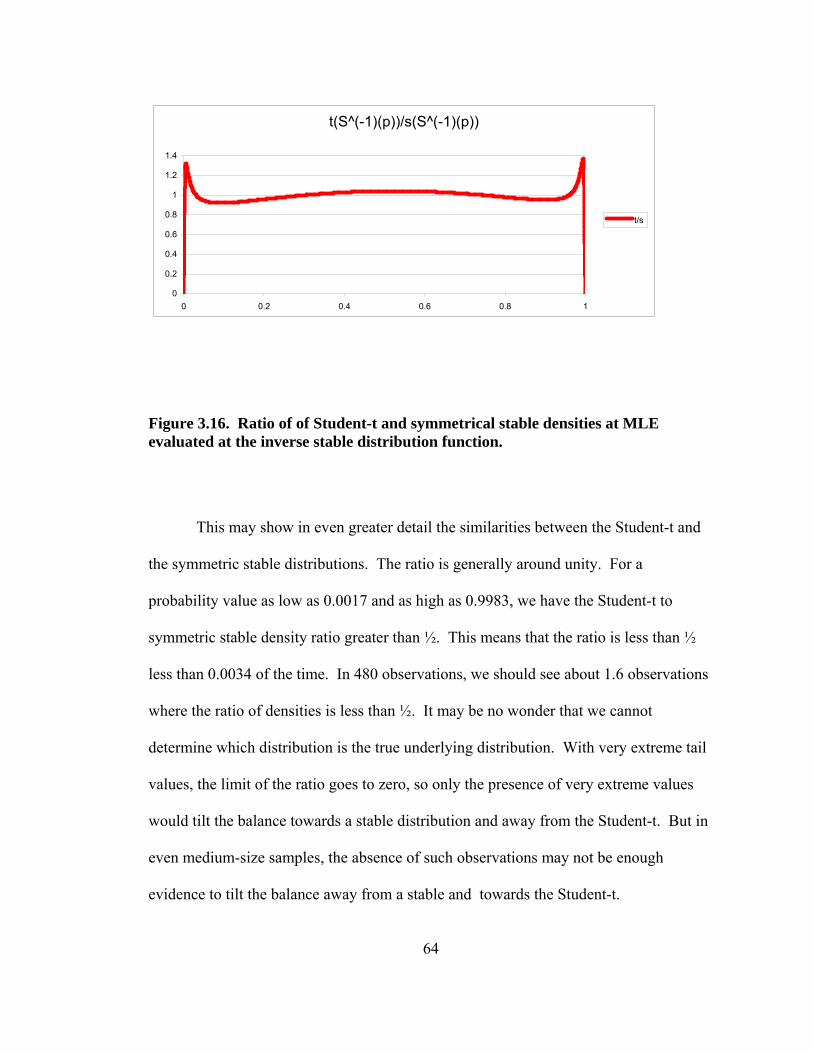

Figure 3.14. Comparison of inverse distribution functions of Student-t and symmetrical stable error distributions at MLE. 62 Figure 3.15. Comparison of upper tail of inverse distribution functions of Student-t and symmetrical stable error distributions at MLE. 63 Figure 3.16. Ratio of of Student-t and symmetrical stable densities at MLE evaluated at the inverse stable distribution function. 64 Figure 3.17. Tests of a null of symmetric stable distribution with an underlying Student-t distribution, sample size 480. 66 Figure 3.18. Tests of a second null of symmetric stable distribution with an underlying Student-t distribution, sample size 480. 67 Figure 3.19. Tests of a null of symmetric stable distribution with an underlying Student-t distribution, sample size 10,000. 68 Figure 4.1. Comparison of results of 90 tests where the null hypothesis and the underlying distributions were both symmetric stable distributions. 71

xi

Figure Page Figure 4.2. Comparison of summary results of 90 tests where the null

hypothesis and the underlying distributions were both symmetric stable distributions by type of test. 72

Figure 4.3 Empirical Distribution Functions of CRSP data. 74

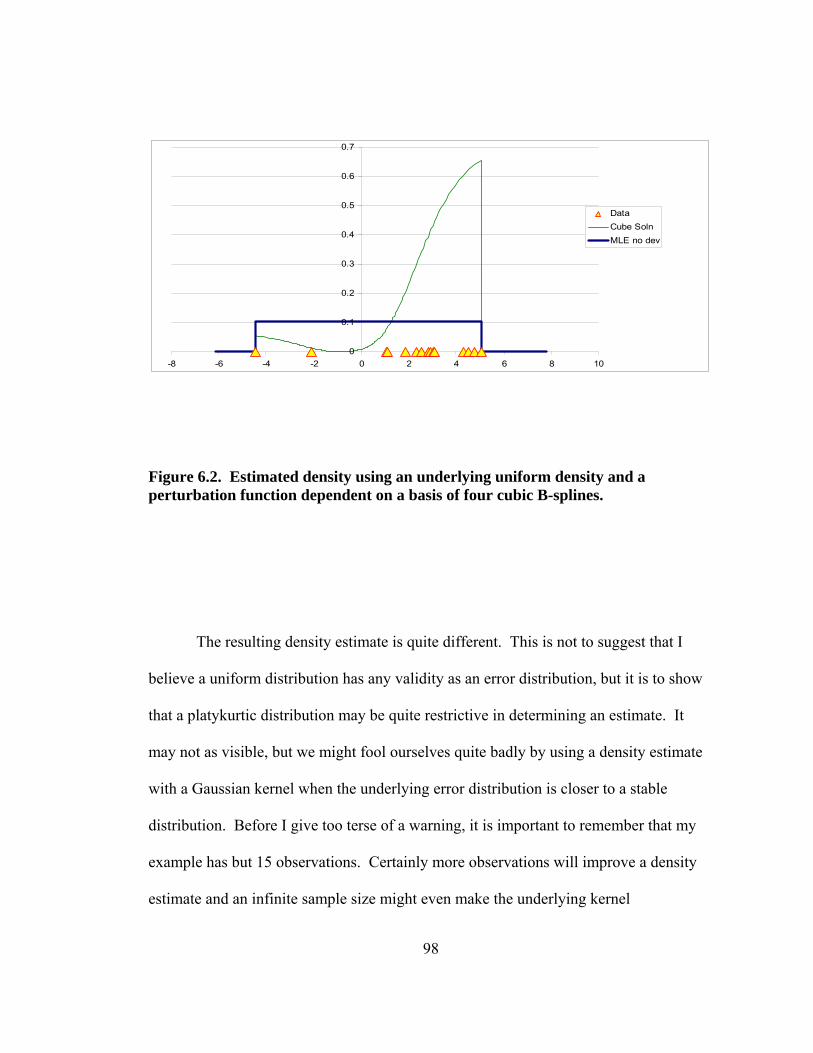

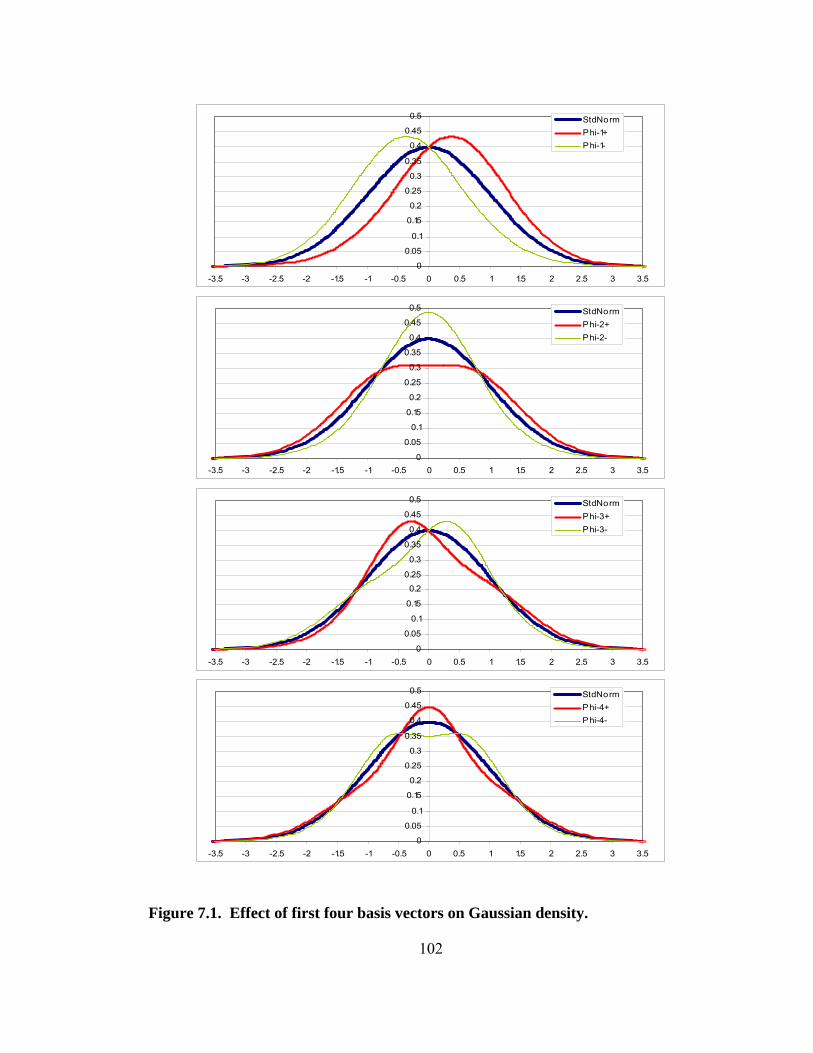

Figure 6.1. Estimated density using an underlying Gaussian and a perturbation function dependent on a basis of four cubic B-splines. 96 Figure 6.2. Estimated density using an underlying uniform density and a perturbation function dependent on a basis of four cubic B-splines. 98 Figure 7.1. Effect of first four basis vectors on Gaussian density. 102 Figure 7.2. Effect of basis vectors five through eight on Gaussian density. 103

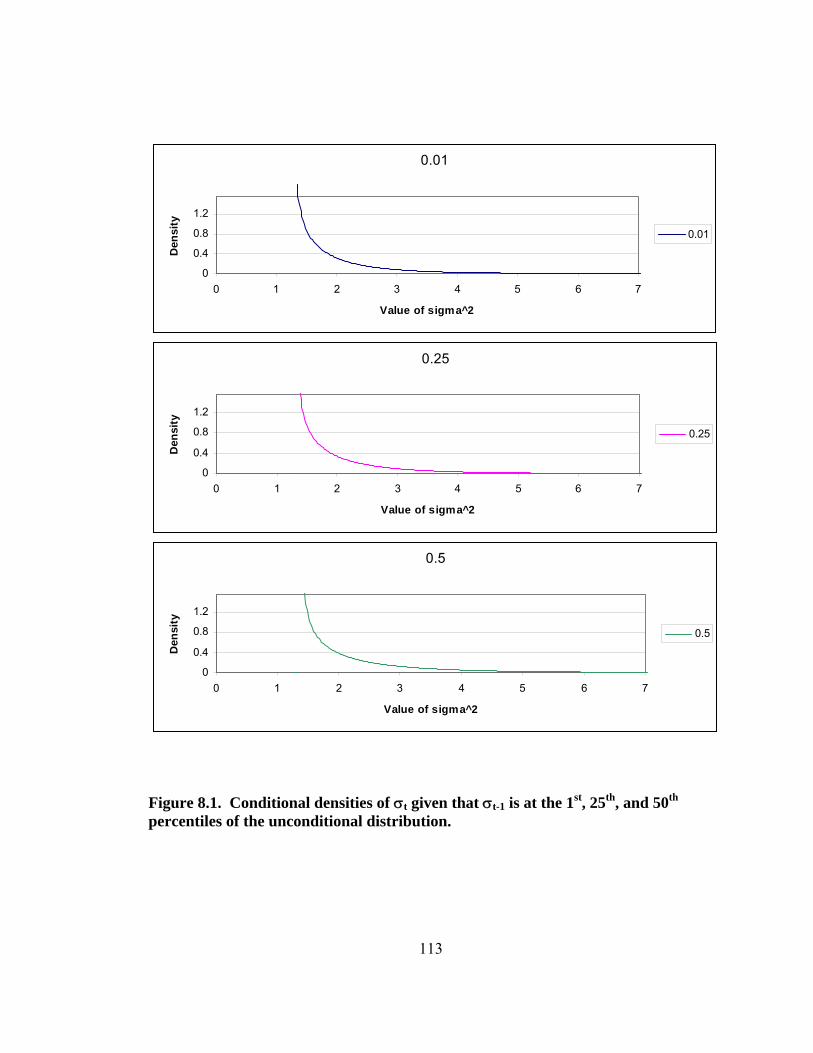

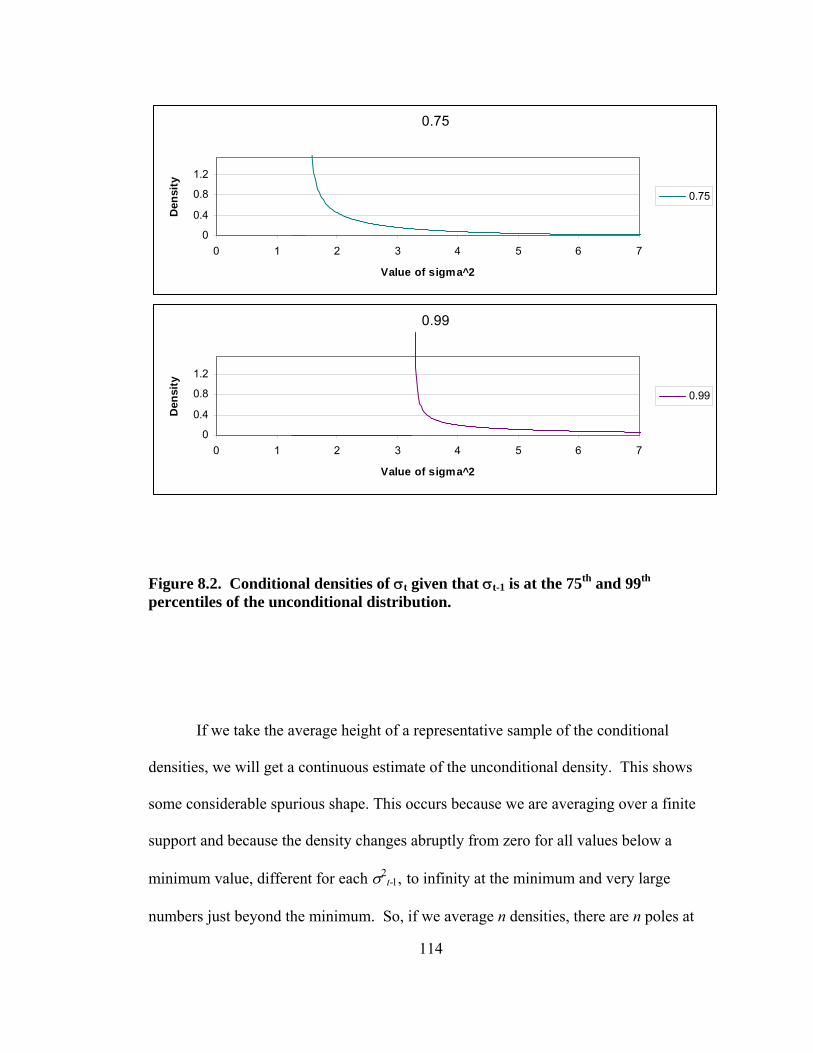

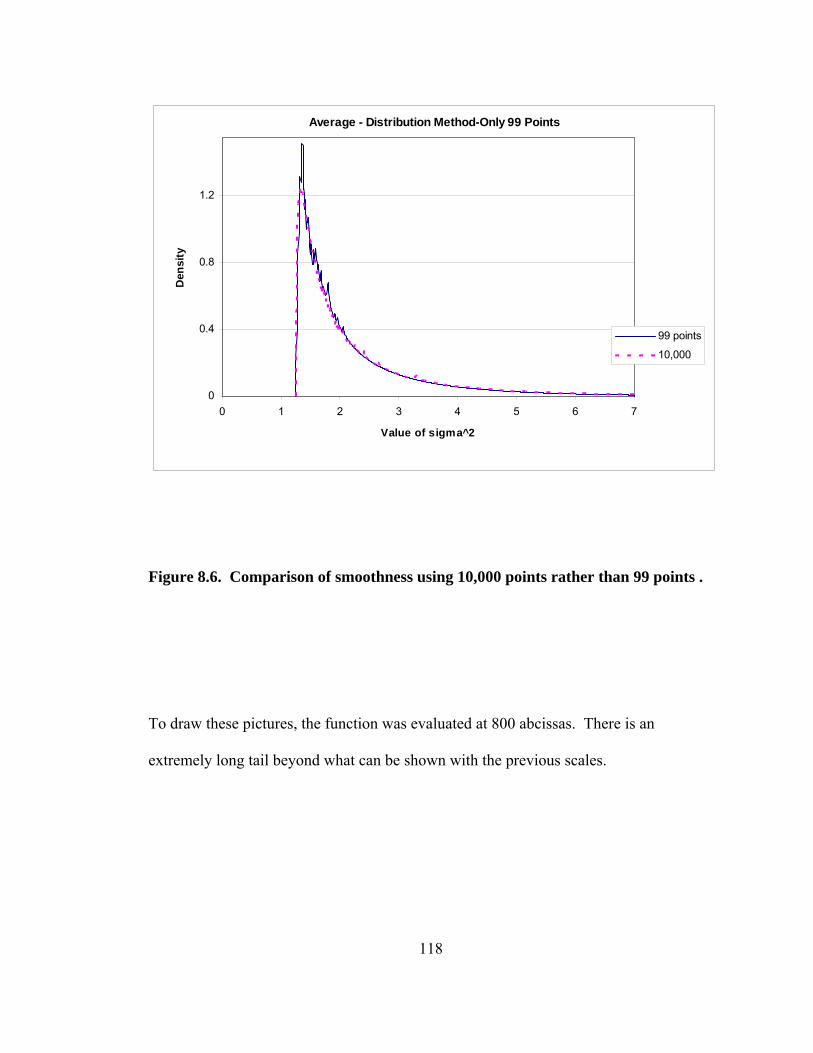

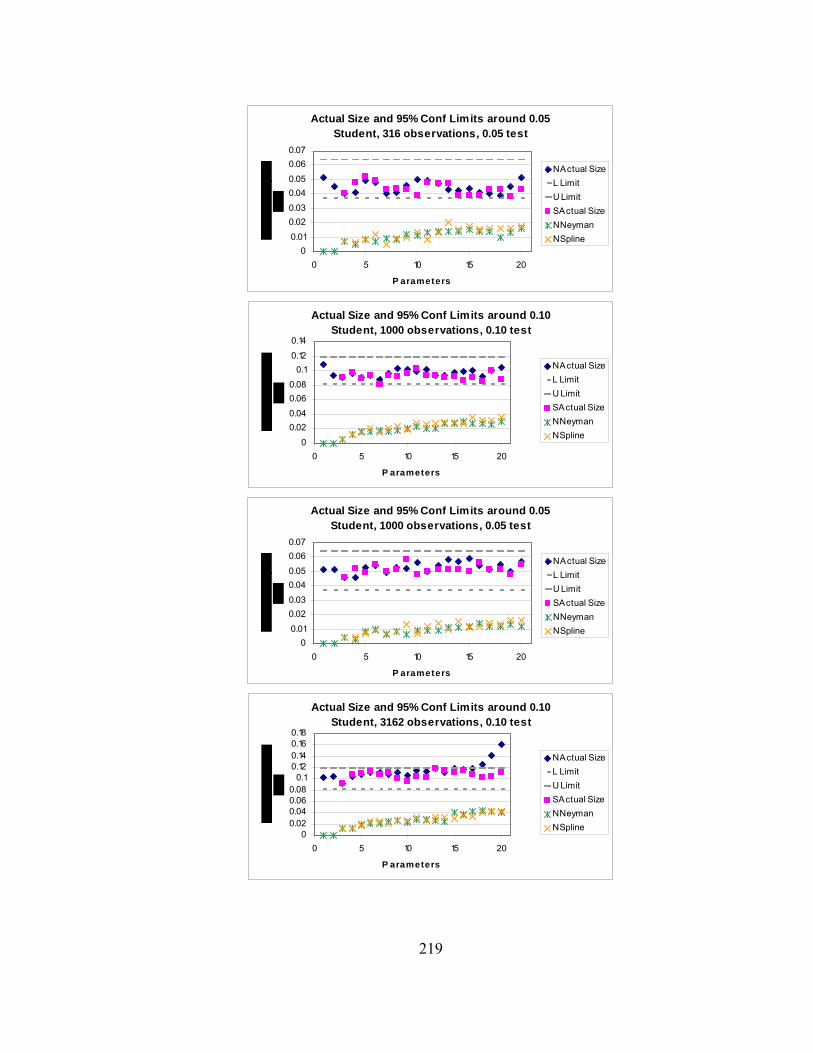

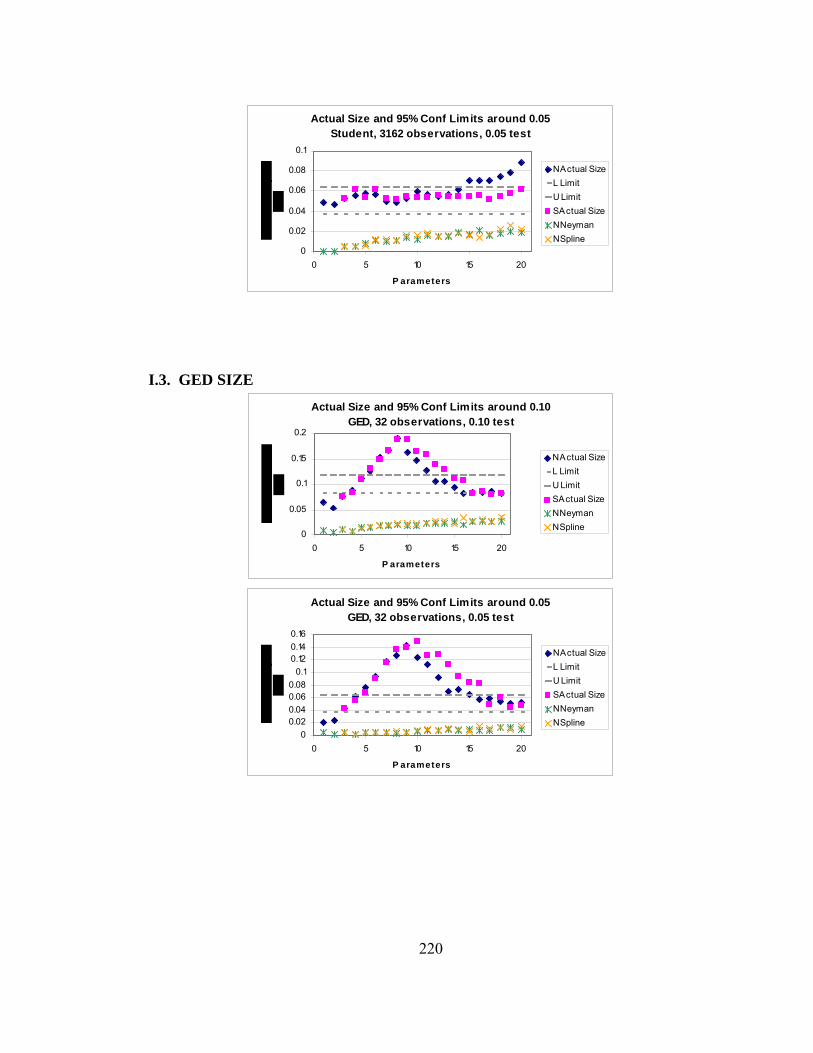

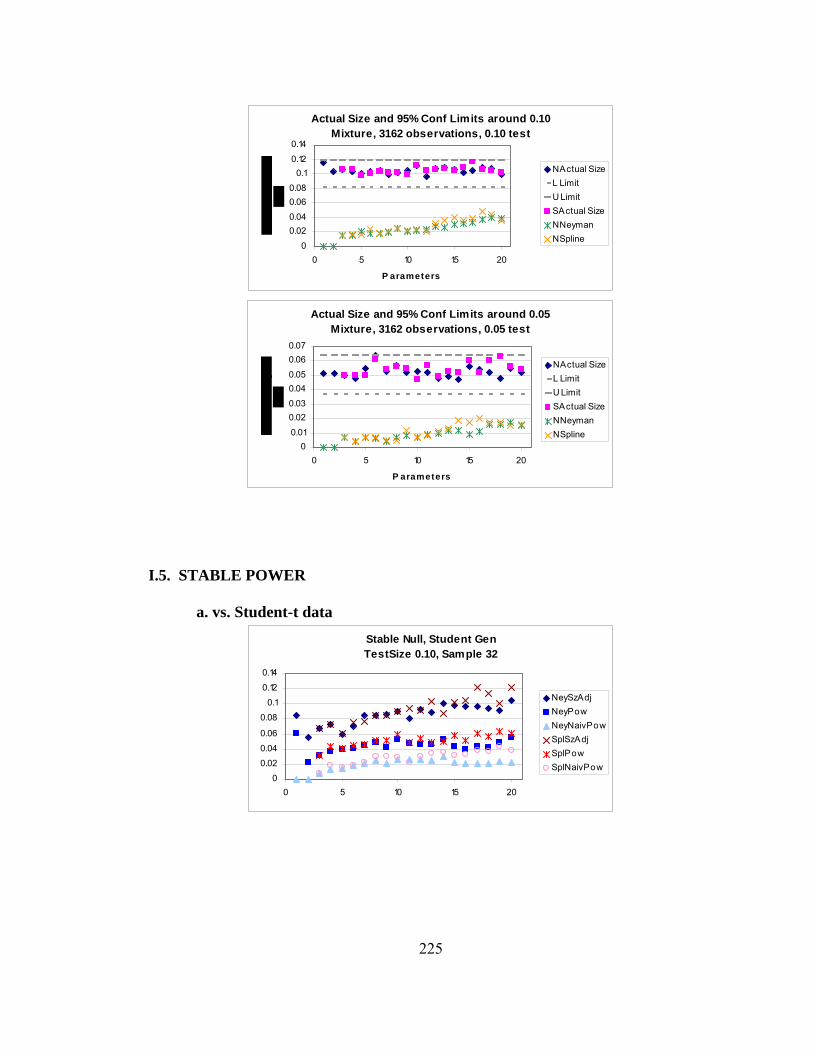

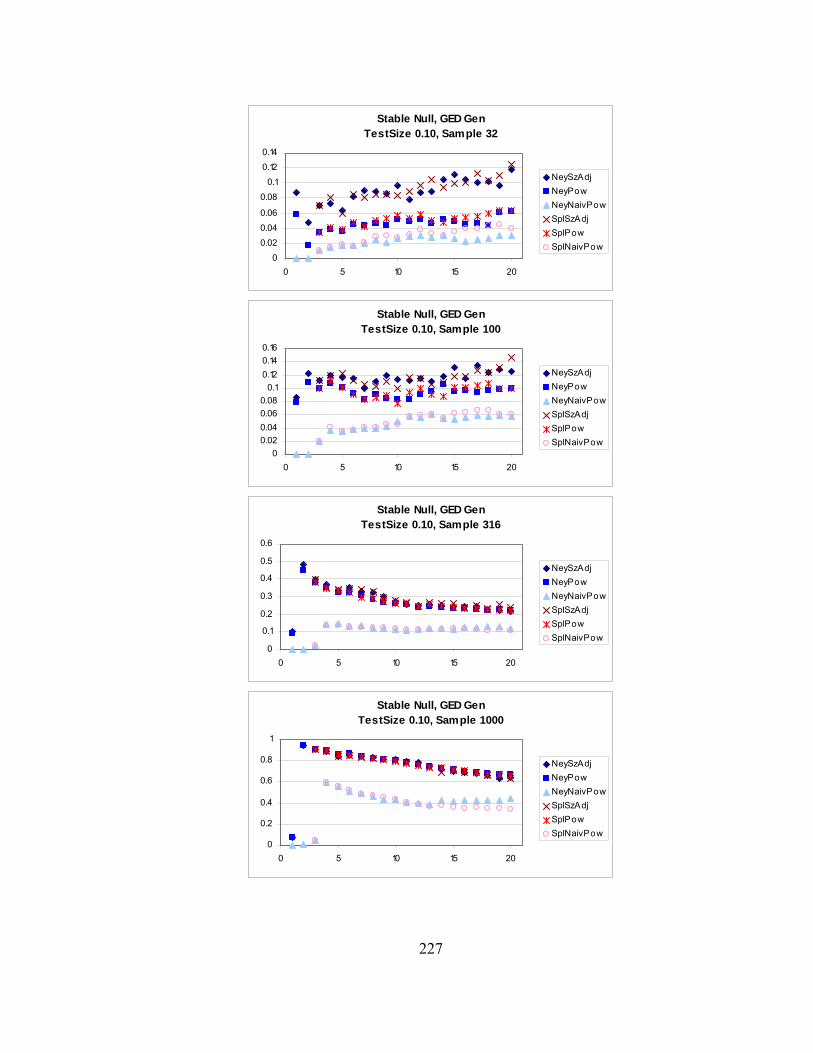

Figure 8.1. Conditional densities of σt given that σt-1 is at the 1st, 25th, and 50th percentiles of the unconditional distribution. 113 Figure 8.2. Conditional densities of σt given that σt-1 is at the 75th and 99th percentiles of the unconditional distribution. 114 Figure 8.3. Sum of 99 conditional densities to approximate the unconditional density. 115 Figure 8.4. Sum of 99 conditional cdfs to approximate the unconditional cdf. 116 Figure 8.5. Unconditional density derived from unconditional cdf. 117 Figure 8.6. Comparison of smoothness using 10,000 points rather than 99 points. 118 Figure 8.7. Upper tail of unconditional distribution of σ . 119 Figure 9.1. Empirical size of 0.10 tests using the naïve and corrected Cubic Spline and Neyman GFTs using numerical quadrature. 131 Figure 9.2. Power of tests to detect a GED with a stable null with 316 observations. 132

xii

Figure Page Figure 9.3. Power of tests to detect a GED with a stable null with 1000 observations. 133 Figure A.1. Various GED densities. The letter “a” represents the exponent “α.” 146 Figure D.1. Degrees of Freedom vs. Ratio of Moments in a Student-t Distribution 160 Figure D.2. Power vs. Ratio of Moments in a GED distribution 163

Figure F.1. Examples of quasi-random numbers and pseudo-random numbers over the unit square. 173 Figure G.1. Systematic portion of error function of 25th Neyman-Legendre basis vector 182

xiii

TABLE OF CONTENTS

Page Abstract………………………………………………………………………………….ii Dedication………………………………………………………………………………iv Acknowledgments……………………………………………………………………….v Vita……………………………………………………………………………………..vii List of figures…………………………………………………………………………...ix Chapters: 1. Introduction……………………………………………………………………… 1 1.1 What is the Error Distribution in Financial Series?........................................ 6 1.2 An “Ideal” Goodness-of-Fit Test…………………………………………….7 1.3 Some Well-Known Goodness-of-Fit Tests..................................................... 8 1.4 Presence of Estimated Model Parameters…................................................. 14 2. Preliminaries in the Development of an Appropriate Lagrange Multiplier Test. 18 2.1 Lagrange Multiplier (LM) Test for a Uniform Distribution………………. 18 2.2 Technical Considerations………………………………………………….. 22 2.3 Spline Lagrange Multiplier Test for a Uniform Distribution……………... 24 2.4 B-Spline Basis……………………………………………………………... 27 2.5 Neyman’s Smooth Test……………………………………………………. 33 2.6 Simple Polynomial Basis………………………………………………….. 36 2.7 Orthogonal Polynomial Basis……………………………………………... 38 3. The Lagrange Multiplier Test………………………………………………… 41 3.1 Lagrange Multiplier Test for a General Completely Specified Distribution 41 3.2 Finite Sample Properties with a Completely Specified Distribution…….... 42 3.3 LM Test for a General Distribution with Estimated Model Parameters....... 51

xiv

Page 3.4 First Test with Model Parameters…………………………………………. 53 3.5 Investigation of Sensitivity………………………………………………... 61 4. Results of Other GFTs…………………………………………………………. 70

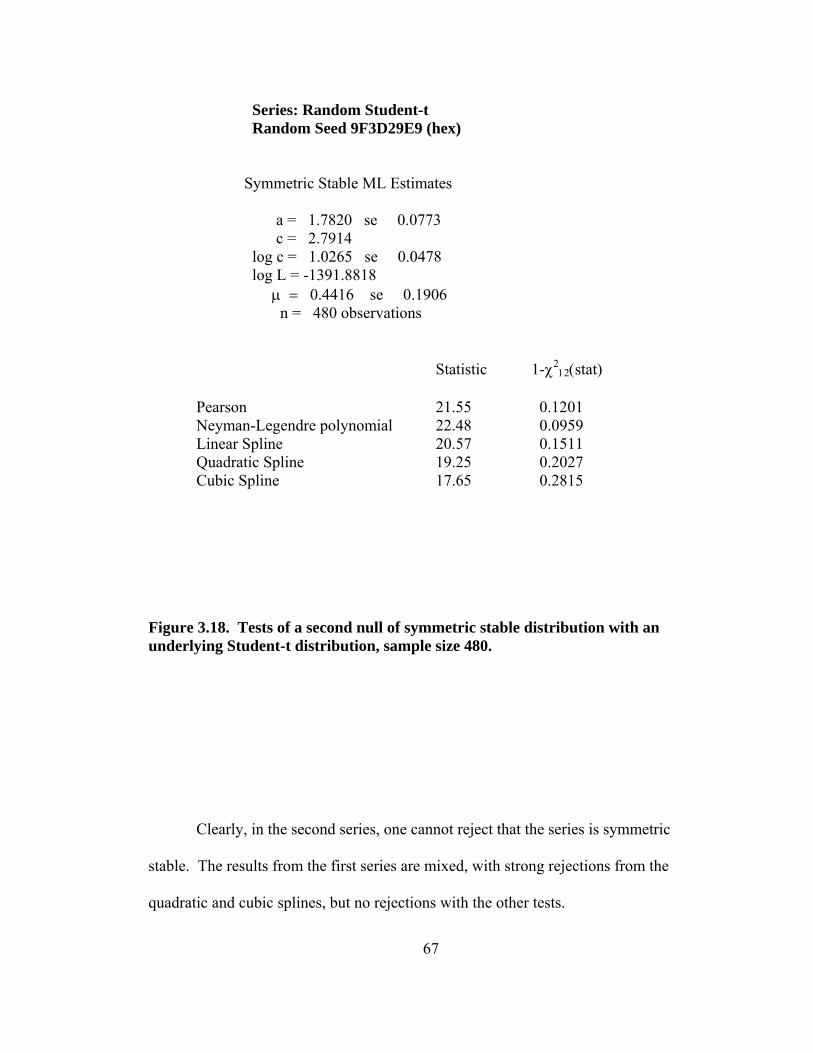

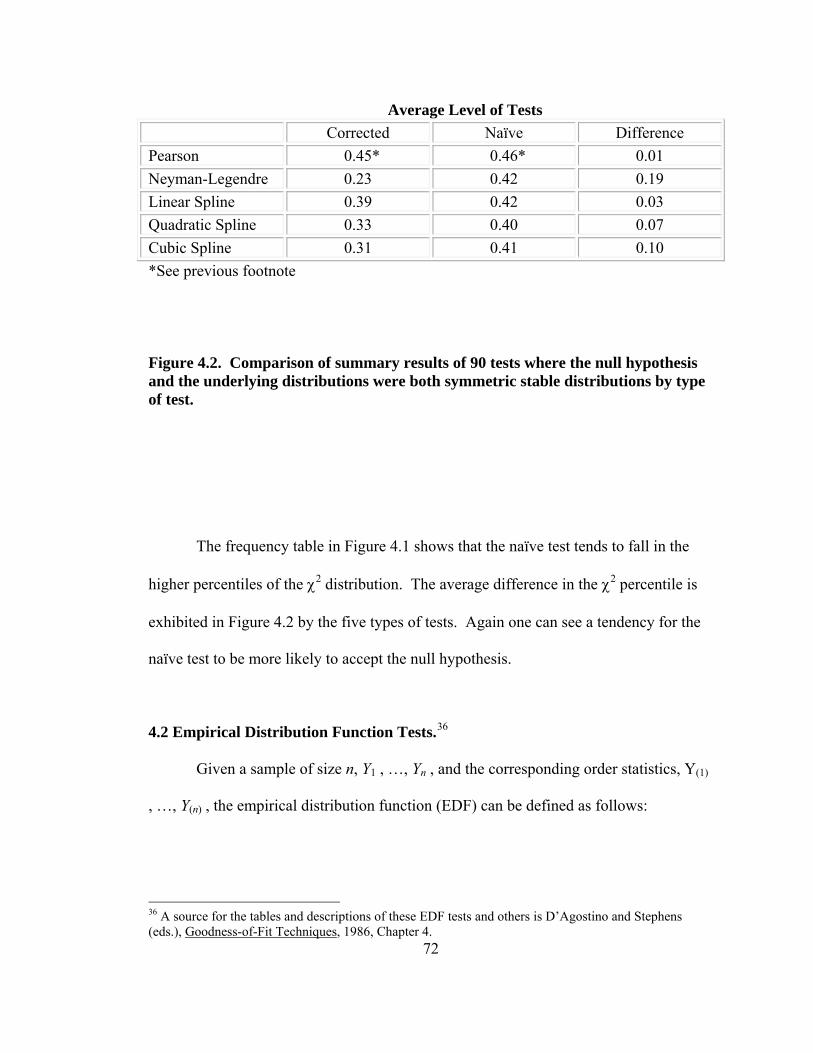

4.1 Residual Tests……………………………………………………………... 70 4.2 Empirical Distribution Function Tests…………………………………….. 72

5. Improvement in Results Due to Numerical Quadrature of Fisher Information Matrix………………………………………………………………………...… 76

5.1 Derivation of Fisher Information Matrix…………………………...………76 5.2 Numerical Two-Sided Differentiation………………………………...……82 5.3 Numerical One-Sided Differentiation……………………………………... 88 5.4 Romberg Integration………………………………………………………. 91

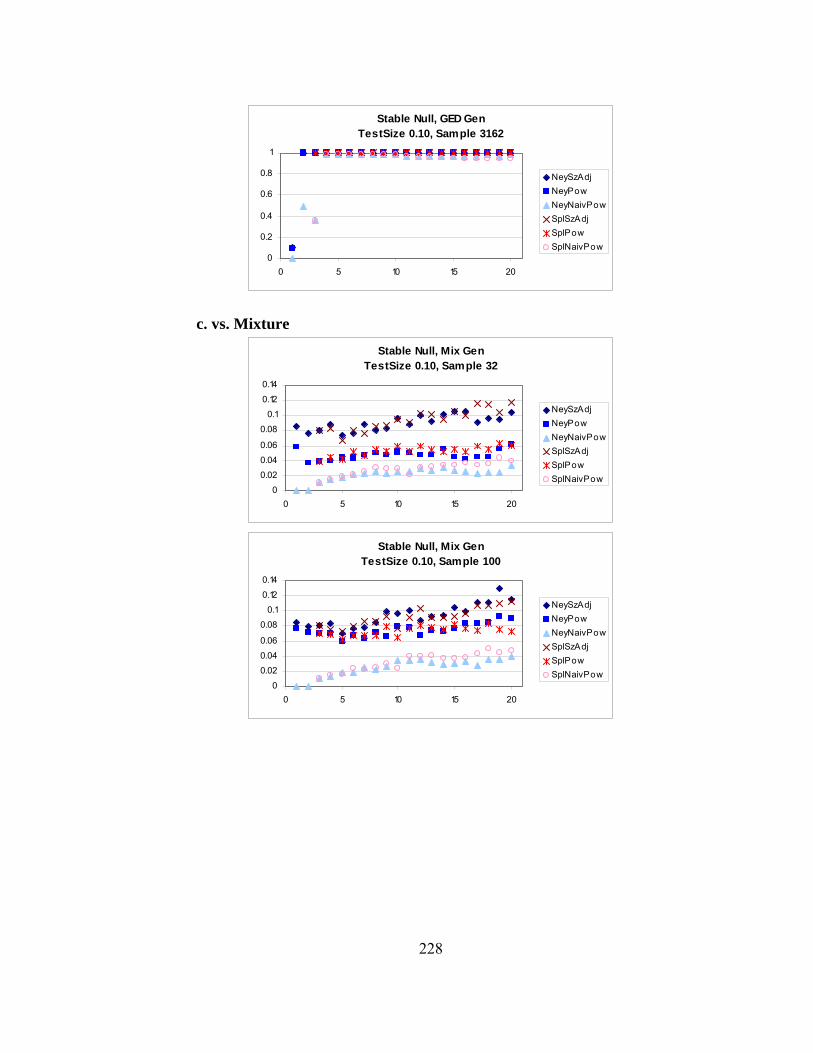

6. In the Event of Multiple Rejections or Non-Rejections………………………... 95 6.1 Multiple Rejections………………………………………………………... 95 6.2 Multiple Non-Rejections……………………………………………...…… 99 7. Meaning of Basis Vectors of Perturbation Functions……………………….... 101 8. Time Dependent Errors……………………………………………………….. 105 8.1 Examples Using Time Series Models………………………………….… 105 8.2 Estimation of σ1.......................................................................................... 109 9. Test Recommendations for Financial Data…………………………………… 126 9.1 Size Distortion…………………………………………………………….128 9.2 Power……………………………………………………………………...129 9.3 With a Stable Null………………………………………………………... 130 9.4 With a Student-t Null...…………………………………………………... 133 9.5 With a GED Null….....…………………………………………………... 134 9.6 With a Mixture Null.....…………………………………………………... 134 9.7 Basis Size vs. Sample Size………………………………………..……… 134 10. Conclusion……………………………………………………………………..140 Appendices: A. Densities and Distributions…………………………………………………….142

xv

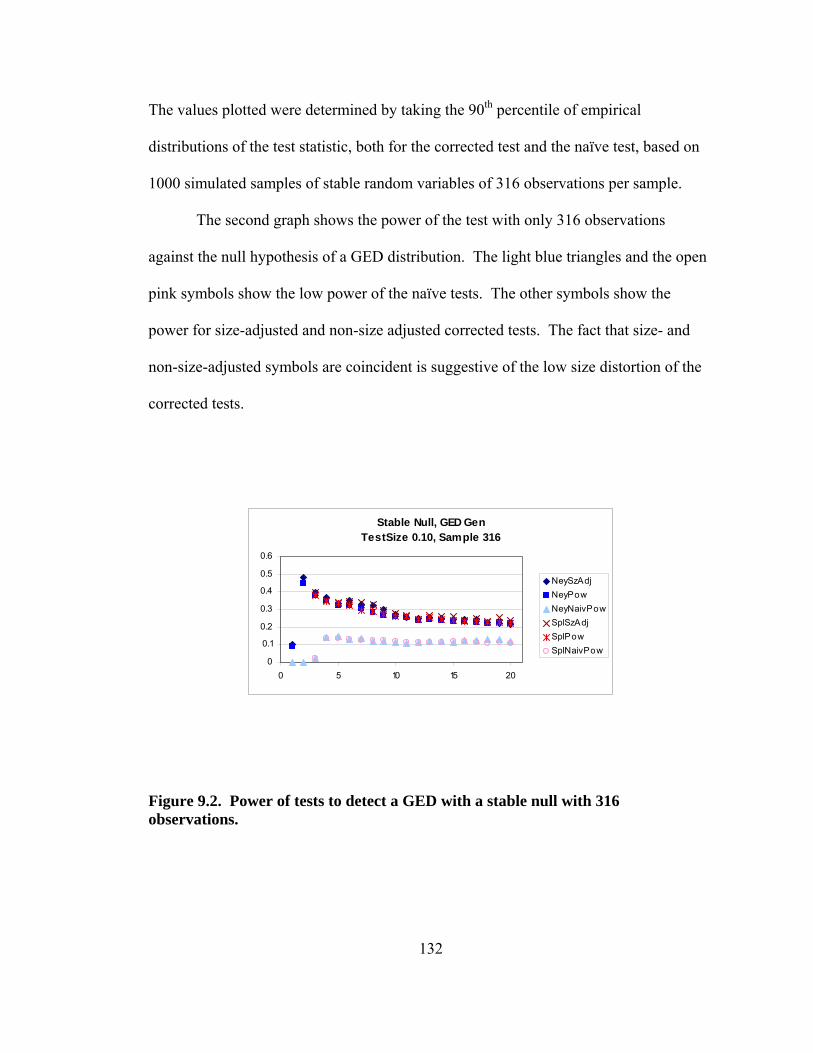

Page A.1 Stable Distributions……………………………………………………… 142 A.2 Pareto Distributions………………………………………………………143 A.3 Generalized Error Distributions (G.E.D.)……………………………….. 145 A.4 Student-t Distributions………………………………………………...… 147 A.5 Mixture of Two Gaussians………………………………………………. 148 A.6 Cauchy Distribution and Its Use in Integration Over the Infinite Real Line……………………………………………………………………….150 B. 1-1 Correspondence between a General Distribution and a Uniform over [0,1]151 C. Pseudo-Random Number Generator and Monte Carlo Methods……………... 152 C.1 Random Number Generator………………………………………….….. 152 C.2 Calculation of Empirical Quantiles…………………………………….... 154 C.3 Addition of 2-33 to Pseudo-Random Numbers…………………………… 155 D. Starting Values for Iterative Maximum Likelihood Estimation……………… 157 D.1 Initial Estimates for Parameters For Use In Maximum Likelihood Estimation………………………………………………….……………. 157 E. Invariance of LM Statistic with Respect to Linear Transformations or Exponentiation………………………………………………………………... 166 F. Unconditional Calculation of σ2…………………………………………….. 171 F.1 Quasi-Random Numbers……………………………………………….... 171 F.2 Rule of Thumb for Maximal “Reasonable” Values of σ2……………..… 177 G. Rounding Concerns…………………………………………………………... 179 G.1 Rounding Errors in Polynomials……………………………………….... 179 G.2 Rounding with GAUSS Software……………………………………….. 182 G.3 Evaluation of Polynomials by Horner’s Rule………………………...…. 185 H. Neyman and Spline Bases…………………………………………………..… 187 I. Size and Power with Various Null Hypotheses………………………………. 215 I.1 Stable Size………………………………………………………………... 215 I.2 Student-t Size…………………………………………………………….. 218 I.3 GED Size………………………………………………………………..... 220 I.4 Mixture Size…………………………………………………………….... 223 I.5 Stable Power……………………………………………………………... 225

xvi

Page I.6 Student-t Power………………………………………………………….. 230 I.7 GED Power……………………………………………………………..... 234 I.8 Mixture Power………………………………………………………….... 238 Bibliography……………………………………………………………………….... 243

xvii

THE LAGRANGE MULTIPLIER TEST

3.1 LAGRANGE MULTIPLIER TEST FOR A GENERAL COMPLETELY

SPECIFIED DISTRIBUTION

APPENDICES APPENDIX A…………………………………………………..…………………………….. who knows # APPENDIX B…………………………………………………..…………………………….. who knows # Bibliography……………………………………………………………………………………………. Big#

xviii

LIST OF FIGURES

Figure Page 2.1 blalahsldfkjl;skjdf………………………………………………………… 3 2.2 lkasjdfl;kjasdf…………………………………………………………… 4

1

CHAPTER 1

INTRODUCTION

Adler, Feldman and Taqqu (1998) preface their collection of papers with the

observation that ever since information has been gathered, it has either been categorized

as “good data” (translation: the investigator knew how to choose and perform the

appropriate statistical tests) or “bad data” (that is, the observations did not conform to

well-known and well-understood distributions, often having too many outliers or

outliers that were too far from what was expected). This may lead to some studies not

being completed at all, while others may interpret the data without taking advantage of

the totality of information present.

Proper distributional assumptions in econometric and financial models are of

critical importance. If the distribution of error terms is inconsistent with the assumed

model, then the assumed model is misspecified. If a set of assumptions concerning

error terms exists and is not used, then estimates of a model’s parameters are needlessly

inefficient.

Though there is a critical need in financial and economic models to match the

right tool to the right distribution, the tests suggested herein are not restricted to those

disciplines. This question is just as important in many other fields. Frequently, “bad

2

data” may simply be “misunderstood data.” With better tools, more studies can be

completed and better conclusions can be drawn.

Many often-used modeling techniques, such as Ordinary Least Squares (OLS)

and the Generalized Method of Moments (GMM), do not require the specification of the

distribution of the error terms. Appealing to different versions of the law of large

numbers, estimators of parameters using these techniques can be shown to be

consistent. In addition, estimators can be shown to be consistent under certain moment

conditions. Since some laws of large numbers depend only on the first moment,

specification of a finite variance is not even required. However, Maximum Likelihood

(ML) Estimators that exploit the properties of a particular distribution are not only

consistent but also asymptotically efficient.

In some cases the investigator may be satisfied with a lesser level of relative

efficiency in estimating the expected value of a random variable if the burden of

searching for a more efficient estimation method is too difficult. However, consider the

example of risk-averse agents making inferences concerning future values of a financial

time series. With risk-neutral agents, it may be enough to estimate expected values of

returns. However, with risk-averse agents it is well known that second and higher

moments of distributions matter in the selection of an optimal investment portfolio. In

addition, it is often desirable to place confidence limits on estimates of expected values,

to calculate variances and, perhaps, measures of skewness and kurtosis. To accomplish

these goals, one should not use the classical methodologies, such as least squares for

calculating means and variances conditional upon exogenous variables by using an

assumption that all error terms are from a random sample independently drawn from

3

normal distributions with an identical yet unknown mean and variance, unless the

assumptions of the model selected are at least approximately satisfied.

There are many tests that have been offered in the literature for determining

whether an observed sample is likely to have been drawn from a normal distribution.

There are also more robust, distribution-free or nonparametric tests that can be used.

However, in many cases taking advantage of additional distributional information may

lead to more efficient inferences and, for that reason, is to be preferred over the

automatic use of nonparametric methods.

With some models previous work by others suggest distributions to be

hypothesized. It is well known in financial literature that error terms of returns of many

assets are leptokurtic, having an unusually high number of observations several standard

deviations from the mean. This phenomenon suggests that it is inappropriate to make

an assumption of normality in dealing with estimates arising from the use of such

samples drawn from real world data. In addition it may be helpful to estimate

parameters by something other than minimizing a quadratic form. As is well known,

using least squares estimators is equivalent to using maximum likelihood estimators

when the underlying error distribution is Gaussian. With other distributional

assumptions, this relationship disappears.

Some applied practitioners show parameter estimates calculated both with and

without observations that have residuals more than a given number of standard errors

from zero. This disposing of data (or, in some cases, reducing some observations’

distances from the median or reducing their impact on the model) without just cause

should make theoreticians cringe. However, if the calculation methods are least-squares

4

based and the error terms are distributed with a distribution that has an infinite variance,

it may be that a truncated or “Winsorized”1 estimator actually has a greater probability

of lying within a given distance from the true parameter than the least squares estimator.

With financial time series, several non-Gaussian distributions have been

suggested with the hope that one of these may be more appropriate in making

inferences. Among these are stable distributions (also called stable Pareto-Lévy or

stable Paretian distributions), which include the normal distribution as a special case.

Other distributions that are considered as substitutes are mixtures of more than one

normal distribution, generalized Student-t distributions and distributions that are

mixtures of continuous distributions and discrete distributions which are used to

account for sudden increases or decreases in a sample. Since the early 1980s

Autoregressive Conditionally Heteroskedastic (ARCH) and Generalized Autoregressive

Conditionally Heteroskedastic (GARCH) models have also been used to try to explain

distributions of error terms that are not independent and identically distributed (IID).

Two additional reasons for attempting to determine the distribution of error

terms follow. First, if a particular distribution is determined not to be the underlying

distribution of the error terms, then, by implication, at least one of the necessary

assumptions for that distribution must be false. This may lead to a new understanding

of the observations and possibly a new theoretical model. Second, if a particular

distribution does have a reasonable possibility of being the underlying distribution of

the error terms, one can extrapolate to possible values that are not apparent in the 1 Perhaps coined by John Tukey in honor of the biostatistician, Charles P. Winsor, who supposedly adopted the practice of replacing outliers with values closer to the median of the residual distribution, so that such outliers would have less impact on a model’s parameters.

5

sample but could occur in the future. That is, with a theoretical distribution, tail

probabilities that are more remote than could be observed with the limited data can be

estimated.

This paper proceeds as follows. The remainder of the introduction outlines the

distributional conclusions and assumptions of previous studies on financial series,

offers a brief outline of a selected list of better-known influential goodness-of-fit tests

(GFTs), and discusses the special problems that exist with goodness-of-fit tests when

model parameters need to be estimated.

Chapter 2 introduces some preliminary work necessary to design the Lagrange

multiplier (LM) goodness-of-fit tests (GFTs). Chapter 3 introduces a completely

general LM GFT which has desirable size and power properties and presents and

analyzes an empirical example. Chapter 4 discusses the results of other conventional

GFTs. Chapter 5 introduces the need for more precise calculation of the Fisher

Information matrix and some numerical techniques to accomplish that, while Chapter 6

discusses what to do in the face of either multiple rejected or non-rejected hypotheses.

Chapter 7 gives the user insight into the meaning of various perturbing elements in the

alternative hypothesis. Chapters 8 expands the scope of the tests by showing how they

can work with time series, while 9 gives specific recommendations on how to use the

tests with financial data. Chapter 10 concludes.

There are several appendices some of which are highly recommended.

Appendix A gives various details of the densities and distributions that are used as null

hypotheses and also some that are used to aid in some of the numerical methods.

Appendix B justifies extending any GFT from a uniform distribution to a more general

6

distribution. Appendix C discusses how pseudo-random number generation is used and

a couple idiosyncratic procedures that I employ in its use. Appendix D shows some

method-of-moments and quantile estimators that are used for starting values for

maximum likelihood estimation of the more exotic distributions. Appendix E is

included to answer questions of using other sets of functions as bases for our alternative

hypotheses, particularly linear or exponential transforms. Appendix F goes hand-in-

hand with Chapter 8 and shows how one can use quasi-random numbers to obtain

unconditional maximum likelihood estimates of early variance terms in time series.

Appendix G identifies and addresses the many rounding concerns that are prevalent in

some of the methods herein. Appendix H provides a catalog of and some examples of

the many basis functions used in the GFTs. Appendix I shows much more in pictures

than Chapter 9 can in words to guide others in making choices as to proper GFTs to test

their assumptions.

1.1 WHAT IS THE ERROR DISTRIBUTION IN FINANCIAL SERIES?

There is a wide variety of opinion of the correct error distribution in many

financial series. Most researchers rule out Gaussian distributions after any testing of

skewness and kurtosis, although throughout the history of analysis, many have used

them; for example, Fama (1976) has suggested normal distributions for monthly returns

after previously (1965) being in the leptokurtic camp. Mandelbrot (1963),

Samorodnitsky and Taqqu (1995), and McCulloch (1996) have suggested the use of

stable distributions. A search for finite-variance leptokurtic distributions has included

Blattberg and Gonedes (1974), Hagerman (1978), Perry (1983), and Boothe and

Glassman (1987) investigating alternatives such as Student-t distributions. Praetz

7

(1972) and Clark (1973) explored the possibility of a mixture of normal distributions.

Among models with changing volatility, Campbell, Lo, and MacKinley (1997) report

the following studies which model for conditional leptokurtosis: Bollerslev (1987)

suggested the use of a Student-t distribution, Nelson (1991) tried a Generalized Error

Distribution, whereas Engle and Gonzalez-Rivera (1991), tried a non-parametric

approach.

With this literature and appropriate goodness-of-fit tests (GFTs), there would

seem to be a rich array of parametric distributions to choose from before one must

resort to nonparametric procedures. A challenge that this paper is aimed at is choosing

appropriate GFTs that can work well with all the above distributions.

1.2 AN “IDEAL” GOODNESS-OF-FIT TEST

In this section, I want to motivate a GFT by illustrating to the reader what we

would like to see if (1) we knew the specified model, (2) the true values of all its

parameters, (3) the true form of its error distribution function F(ε), and (4) an infinite

sample size. If we were able plot a histogram of the infinite number of values of the

form F(ε1), F(ε2), …, it would look like a uniform distribution over the unit interval.

One would expect any subinterval of the unit interval of length λ to contain a proportion

λ of the functional values.

Of course we will not have an infinite sample size, so we can expect some

variation in the heights of the bars in any histogram regardless of its partition of

intervals. Since we also do not know the error function but might like to test whether a

hypothesized error function is reasonable, we can imagine a test that specifies how far

from the uniform distribution one might expect the empirical function to deviate under

8

the assumption that we have chosen the correct error function. Additionally, instead of

constructing a histogram with a partition of intervals, we might try to fit the empirical

errors to some functional form defined over the unit interval and see how far such a

functional form is from a uniform distribution.

The presence of unknown model parameters will require that we make estimates

of the model parameters, so we will have to content ourselves with residuals which are

estimates of the error terms rather than the error terms themselves. Alas, the last

assumption, that we have correctly specified the model, is not investigated in this study,

but we will see that the complication of not knowing the values of model parameters,

which is one of the normal conditions of most studies, will be challenging enough to

stimulate a considerable body of work.

1.3 SOME WELL-KNOWN GOODNESS-OF-FIT TESTS

The Kolmogorov-Smirnoff (KS) statistic is the largest distance between the

empirical distribution function and a 45° line on the unit interval. KS is independent of

the hypothesized distribution and critical values are dependent on n, however it requires

knowledge of the true values of the parameters in a distribution. While this test statistic

is sensitive to the single data value that is “farthest” away from the population

cumulative distribution function (CDF), it does not directly take into account the

relative deviations of the other observations.

An Anderson-Darling type test statistic is a refinement of Kolmogorov-Smirnoff

that takes into account the smaller sampling variance of the values that are farther from

the median; however, it is still based on the single most extreme value, adjusted for

expected sampling variance. Andrews (1997) has offered a conditional K-S test that

9

accounts for the parameter estimation effects. Still, this test is based on a single point of

the empirical distribution.

The Cramér-von Mises test uses all the observations and is based on the

integrated squared distance between the empirical CDF and a 45° line. Since it is based

on a distribution function and not the density function directly, some densities may tend

to “fool” it. Consider the following example, adapted from McCulloch (1999), and

pictured below in Figure 1.1, along with a uniform density on the unit interval:

Let h1(z) =[ ]( ]

5 24 55 26 5

0,,1

0 otherwise

zz

⎧ ∈⎪ ∈⎨⎪⎩

and h2(z) = (5 24 57 46 7

0,

,1

0 otherwise

z

z

⎧ ⎡ ⎤∈ ⎣ ⎦⎪⎪ ⎤∈⎨ ⎦⎪⎪⎩

Sample Density 1

-0.5

0

0.5

1

1.5

0 0.2 0.4 0.6 0.8 1

z

Den

sity

h1(z) Uniform

Sample Density 2

-0.5

0

0.5

1

1.5

0 0.2 0.4 0.6 0.8 1

z

Den

sity

Uniform h2(z)

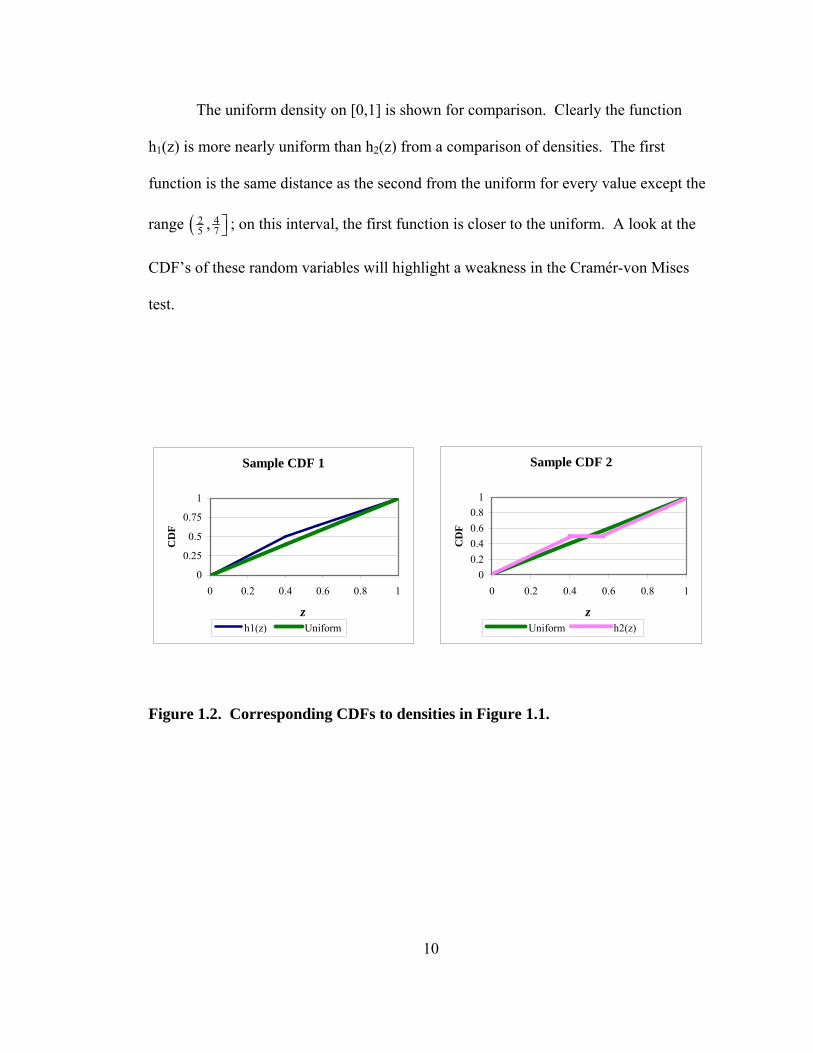

Figure 1.1. Two sample densities compared with the uniform distribution.

10

The uniform density on [0,1] is shown for comparison. Clearly the function

h1(z) is more nearly uniform than h2(z) from a comparison of densities. The first

function is the same distance as the second from the uniform for every value except the

range ( 2 45 7, ⎤⎦ ; on this interval, the first function is closer to the uniform. A look at the

CDF’s of these random variables will highlight a weakness in the Cramér-von Mises

test.

Sample CDF 1

0

0.25

0.5

0.75

1

0 0.2 0.4 0.6 0.8 1

z

CD

F

h1(z) Uniform

Sample CDF 2

00.20.40.60.8

1

0 0.2 0.4 0.6 0.8 1

z

CD

F

Uniform h2(z)

Figure 1.2. Corresponding CDFs to densities in Figure 1.1.

11

The CDF of h2(z) is the same distance from the 45° degree line as is h1(z)

everywhere except the interval ( 2 45 7, ⎤⎦ ; on this interval, its distance from the uniform is

smaller that the distance of h1(z). Thus, the integrated squared distance is smaller for

h2(z) than for h1(z). Therefore, the Cramér-von Mises test would be less likely to reject

h2(z) than h1(z) even though h2(z) departs more from the uniform. Since the

investigator is not likely to know the type of departure from the hypothesized

distribution a priori, it seems that a reasonable property for a GFT is to be more

sensitive to greater departures.

The best-known GFT is the Pearson χ2 test. It is safe to say that it appears in

more texts than any other GFT (See for example Hogg & Craig (1970)). For a

multinomial distribution with n observations the test is:

H0: pj = pj0 , j = 1, …, m+1 vs. H1: Not H0

The Pearson statistic is Qm = ( )2

1 0

01

m j j

jij

Obs np

np

+

=

⎡ ⎤−⎢ ⎥⎢ ⎥⎢ ⎥⎣ ⎦

∑ where Obsj is the number of

observations in the sample with the jth value.2 Any known distribution can be

transformed to a multinomial distribution with parameters {pj} by segmenting the

support of the distribution into m+1 sub-supports or “bins” and calculating the

population probability for each sub-support. It is not required that the pj be equal. This

statistic is easy to calculate, known to be asymptotically distributed as a χ2 statistic with

m degrees of freedom and can be used in a wide variety of situations. Its power is

dependent both on the choice of m and the choice of {pj}. It is intuitive that some 2 Here m+1 is used to facilitate future comparison with other tests. There are only m probability parameters being set since one of the parameters is constrained to be one minus the sum of the others.

12

power will be lost due to the reduction of information by grouping the data to test

continuous distributions. This grouping has the effect of assigning an equal density to

all possible values within each bin and also, perhaps, assigning nearby values that

happen to be in different bins very different density values. The following example will

highlight possible problems with this type of test.

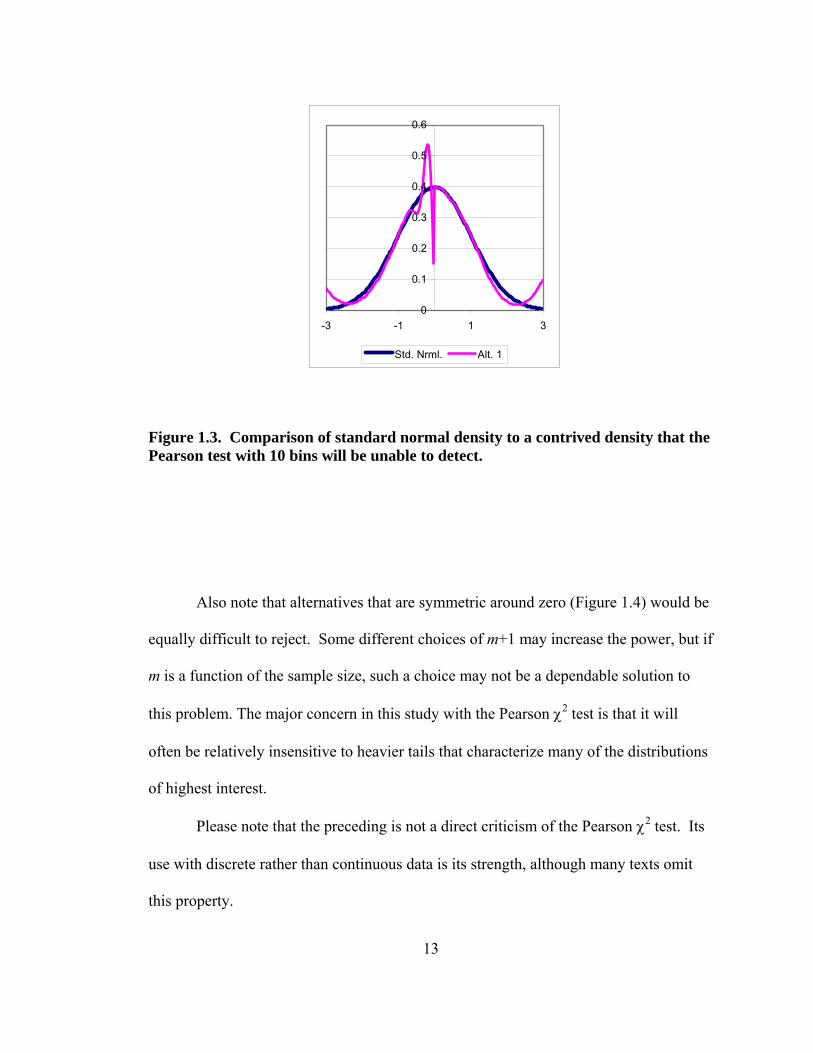

Consider a test to determine whether n observations are from a standard normal

distribution with m + 1 = 10. For equiprobable bins, one would need 9 breakpoints

1

10j− ⎛ ⎞Φ ⎜ ⎟

⎝ ⎠, j = 1, …, 9, where Φ is the standard normal distribution. Below is a graph

of a standard normal density and also a contrived density (Figure 1.3) that integrates to

½ on either side of zero; it also integrates to very close to 0.1 between consecutive

standard normal deciles. Consequently, a Pearson χ2 test could not tell the difference

between a normal distribution and the pictured alternative.

13

0

0.1

0.2

0.3

0.4

0.5

0.6

-3 -1 1 3

Std. Nrml. Alt. 1

Figure 1.3. Comparison of standard normal density to a contrived density that the Pearson test with 10 bins will be unable to detect.

Also note that alternatives that are symmetric around zero (Figure 1.4) would be

equally difficult to reject. Some different choices of m+1 may increase the power, but if

m is a function of the sample size, such a choice may not be a dependable solution to

this problem. The major concern in this study with the Pearson χ2 test is that it will

often be relatively insensitive to heavier tails that characterize many of the distributions

of highest interest.

Please note that the preceding is not a direct criticism of the Pearson χ2 test. Its

use with discrete rather than continuous data is its strength, although many texts omit

this property.

14

0

0.1

0.2

0.3

0.4

0.5

0.6

-3 -1 1 3

Std. Nrml. Alt. 2

0

0.1

0.2

0.3

0.4

0.5

0.6

-3 -1 1 3

Std. Nrml. Alt. 3

Figure 1.4. Additional densities that the Pearson test will be unable to detect.

1.4 PRESENCE OF ESTIMATED MODEL PARAMETERS

In most models the residuals are estimates of the unknown underlying errors.

Roughly speaking, one can visually assess and infer a distribution of error terms from a

histogram of residuals. However, a visual assessment should be reduced to a

mathematical assessment since histograms will necessarily differ from underlying

distributions and what is desired is a determination of whether or not the histogram in

question is statistically significantly different from the hypothesized theoretical

distribution. For this task, GFTs must be designed to meet the varying needs of each

situation.

15

In general, the error random variables to be tested are unobservable. With a

standard regression model:

yi = h(Xi;β )+ ε i (Eq. 1.3.1)

is assumed to be true with i = 1 , …, n, where yi is the ith observed dependent variable,

Xi is a row vector (with dimension k) of known constants (or is uncorrelated with the

vector of ε’s),3 β is a k-vector of unknown coefficients, and εi is an unobservable

random variable with some distribution, with E(εi) = 0 (or possibly the median of εi’s

distribution is zero), Pr(εi < z) = F(z;γ), γ ∈ Γ, and εi is independent of εj if i ≠ j. The

function h(Xi;β ) could be linear or non-linear.

Under these assumptions we would like to test whether the vector

ε = 1 nε ε′

⎡ ⎤⎣ ⎦L is distributed according to the given function or if it has some other

distribution. Typically, one must estimate β and γ, after which one can find a vector of

residuals (e) that is an estimate of ε, rather than ε itself. McCulloch (1999) reports the

fact that if parameters are to be estimated from the data, standard tests are biased

towards acceptance of the null hypothesis, citing Mood, Graybill & Boes (1974), Bera

and McKenzie (1986), and Bai (1997). He continues to convey that such tests “may

even be asymptotically invalid.” DeGroot (1986) reports that Chernoff and Lehmann

(1954) established that the use of maximum likelihood estimates, when testing whether

a given distribution is normal, changes the asymptotic distribution of the test statistic

under the null hypothesis in such a way as to result in smaller values. Given that larger

values are necessary to reject the null hypothesis, this results in a greater than desired

3 As usual, it is further assumed that the matrix composed of rows of the Xi’s is of rank k.

16

level of acceptance. Work completed in this dissertation provides empirical evidence to

support this for the application of stock market returns.

Intuitively, any “good” estimators of the parameters seek to fit the model as

closely as possible. For example, with a classical linear regression and leptokurtic

errors, the sum of the squared true errors will almost surely be greater than4 the sum of

the squared residuals. This will tend to conceal the large errors that a test for

leptokurtosis would be seeking.

Rayner and Best suggest a solution to the problem of testing for normality using

residuals of Eq. 1.3.1 for a classical linear model, with the error terms assumed to be

IID with the CDF given as N(0,σ2). First, start with your favorite goodness-of-fit

statistic (GFS), using the residuals. By taking advantage of the familiar result from

linear regression:

e = Mε , where M = I – X(X′X)-1X′ (Eq. 1.3.2)

it is possible to simulate several new sets of pseudo-residuals by generating random

variables from a standard normal distribution and multiplying these normal random

variates by M. Conveniently, the matrix M must be calculated only once for a given

model. It is unnecessary to estimate σ2 for most purposes unless the statistic chosen is

not invariant with respect to σ2. For each set of pseudo-residuals, calculate a GFS.

Thus, under an assumption of normality, you can form a Monte Carlo distribution for

the goodness-of-fit statistic. Use the distribution to determine a p-value for the original

GFS.

4 With a continuous error distribution, the probability is zero that the maximum likelihood estimates will, in fact, equal the true parameter values, so equality of the sums of squares has probability zero.

17

This method should be reasonable in many cases for its purpose, but some

difficulties exist. If the random errors are not independent and a variance matrix Ω is

known, M can be modified in the familiar way for generalized least squares. However,

generally Ω must be estimated complicating any interpretation between the ε vector and

the residuals. M has dimensions n × n and may be troublesome for especially large

databases. This procedure may not be able to be extended in a straightforward manner

to accommodate other situations that may arise such as non-linear regression or non-

Gaussian error terms. So, the search remains for suitable alternate tests.

18

CHAPTER 2

PRELIMINARIES IN THE DEVELOPMENT OF AN APPROPRIATE LAGRANGE MULTIPLIER TEST

2.1 LAGRANGE MULTIPLIER (LM) TEST5 FOR A UNIFORM DISTRIBUTION

Consider a random sample x = (x1, …, xn)′ from an unknown distribution F(X).

One would like to test:

H0: X ~ U(0,1) vs. H1: Not H0

One could parameterize the alternative hypothesis in the following way:

H1: X ~ G(z) where G(z) = ( )0

1

0 0

1 0 1

1 1

mzj j

j

z

v dv z

z

α φ=

<⎧⎪

⎡ ⎤⎪ + ≤ ≤⎢ ⎥⎨⎢ ⎥⎪ ⎣ ⎦

⎪ >⎩

∑∫ .

To assure that G(1) = 1, {φ j; j = 1, …,m} is chosen so each element, φ j, integrates to

zero on the unit interval. For the set of alternative hypotheses not to contain redundant

representations, {φ j; j = 1, …, m} must contain linearly independent elements.6 It will

also be convenient to require that φ j is bounded on the unit interval. With no additional

definition, the density associated with G can be written as: 5 Such tests are also called “efficient score” tests, just “score” tests, or sometimes “Rao score” tests in honor of the first to suggest this type of test. 6 As will be discussed later, any set of linearly independent functions that integrate to zero may be chosen which will be sensitive to possibly different departures with different power.

19

g(z) = G′(z) = ( )

11 0 1

0 otherwise

m

j jj

z zα φ=

⎧+ ≤ ≤⎪

⎨⎪⎩

∑ (Eq. 2.1.1)

Also, Pr(xi < z) = G(z) for each i ∈ {1, …, n}. It can also be seen that H0 is nested in H1

if one allows for α j = 0, j = 1, …, m. This nesting is what allows the use of a Lagrange

multiplier statistic, since the parameter space of the null hypothesis is a subset of that of

the alternate hypothesis.

Consider α = (α1, …, α m)′ ≠ (0, …, 0). Then for any choice of nonzero basis

functions {φ j}, g(z) is a function different than the uniform density on the unit interval.7

For α near the origin in ℜm, g(z) can be seen as a perturbation of the uniform density,8

using perturbation functions, {φ j; j = 1, …, m}. So, that ( )1

01g z dz =∫ , it is helpful to

choose {φ j; j = 1, …, m} such that ( )1

0 j v dvφ∫ = 0.

The likelihood function of interest is:

L(α;x) = 1

( ; )n

ii

g x α=

∏ ⇒ Λ(α;x) = ( )1

log ;n

ii

g x α=∑ = ( )

1 1log 1

n m

j j ii j

xα φ= =

⎛ ⎞+⎜ ⎟⎜ ⎟

⎝ ⎠∑ ∑ ,

where Λ is the logarithm of the likelihood function. The jth first derivative, evaluated at

α = 0, is:

7 This is guaranteed by the linear independence of the elements of {φ j; j = 1,…,m}. 8Many features, methods of calculation, and inferences of the Pearson χ2 test, the Neyman Ψ2 test (to be discussed at the end of this section), and the proposed spline test are parallel. The differences in the tests are centered on the choice of a basis of perturbation functions.

20

( )

( )( )

1 10

1 0

log

1

n nj i

j imj i i

k k ik

xL xxα

α

φφ

αα φ= ==

= =

∂= =

∂+

∑ ∑∑

,

so the transpose of the “score” vector of first derivatives, evaluated at α = 0, for the LM

Statistic is:

( ) ( ) ( )11 1

0 , ,n n

i m ii i

s x xφ φ= =

⎛ ⎞′ = ⎜ ⎟

⎝ ⎠∑ ∑K

A typical element of the Hessian matrix is:

( ) ( )

( )

2

21

11

n j i j i

mij jk k i

k

x x

x

φ φα α

α φ

′

=′

=

−∂ Λ∂ ∂ ⎡ ⎤

⎢ ⎥⎣ ⎦

= ∑+∑

,

so a typical element of the Fisher information matrix, evaluated at the null hypothesis,

for the LM statistic is:

( ) ( ) ( )

( )( ) ( )

2

0 0 021 1

1

log0

1

n nj i j i

j j j i j imj j i i

k k ik

x xLI E E E x x

xα α α

φ φφ φ

α αα φ

′′ ′= = =

′ = =

=

⎧ ⎫⎪ ⎪

⎛ ⎞ − ⎡ ⎤⎪ ⎪∂= − = − =⎜ ⎟ ⎨ ⎬ ⎢ ⎥⎜ ⎟∂ ∂ ⎡ ⎤ ⎣ ⎦⎪ ⎪⎝ ⎠ +⎢ ⎥⎪ ⎪

⎣ ⎦⎩ ⎭

∑ ∑∑

= ( ) ( ) ( ) ( ) ( ) ( ) ( )1 1

0 00 01 1

;n n

j i j i j i j i i i j ji i

E x x x x g x dx n z z dzα αφ φ φ φ α φ φ′ ′ ′= =

= =

⎡ ⎤ = =⎣ ⎦∑ ∑∫ ∫

The LM statistic is s′(0)I(0)-1s(0). Since the null hypothesis is a point of

dimension zero in ℜm, this statistic is asymptotically distributed as a χ2(m) as n

increases to infinity. The test rejects the null hypothesis in favor of the unspecified

alternative if the LM statistic is greater than a pre-specified percentile of χ2(m).

21

The finite sample distribution for various values of n and m can be tabulated by

Monte Carlo simulation. For a given n, as m is increased, the power of the test relative

to specific alternative distributions was thought to increase, at least to a point. It was

anticipated that m should be an increasing function of n. McCulloch (1971, 1975)

suggests m ≈ n , whereas Li (1997) suggests m = an2/5. Simulations suggested that

different m were more appropriate for particular alternate hypotheses rather than

increasing with some power of n.

Two common estimators of the Fisher information matrix9 are the local

information matrix (the negative of the empirical Hessian of the log likelihood function)

and the Outer Product of the Gradient Estimator (OPG). Both estimators are consistent

estimators for the Fisher information matrix. A typical element of the local information

matrix is, evaluated at the null hypothesis is:

( ) ( )2

10

log n

j i j iij j

L x xα

φ φα α ′

=′ =

∂−

∂ ∂= ∑

The OPG estimator is also an empirical estimator. It is based on the

contributions to the gradient matrix, a typical element of which is:

( ) ( )0

log , ij i

j

L xx

α

αφ

α=

∂=

∂.

The typical element of the OPG matrix is:

( ) ( ) ( ) ( )1 10

log , log ,n ni i

j i j ij ji i

L x L xx x

α

α αφ φ

α α ′′= ==

∂ ∂=

∂ ∂∑ ∑ .

9 See for example Davidson and MacKinnon (1993) or McCulloch (1999)

22

Although in this case the estimators turn out to have the same form, that is not

always the case. In general, since the Hessian and the OPG depend on the sample rather

than the expectation, there is additional error included that inherently makes inferences

poorer than if the Fisher information matrix can be computed.

2.2 TECHNICAL CONSIDERATIONS

There are two technical points to discuss. The first of these is a requirement that

the parameter space for the null hypothesis is not on the boundary of the parameter

space for the alternative hypothesis (with the parameter space being defined as those

α that allow g to be a legitimate density).10 Intuitively, α = 0 is an interior point of the

parameter space, since at α = 0, g(z;α) = 1, for all values of z on the unit interval; and,

evidently, under the null hypothesis, there is a limiting local maximum at α = 0 as the

sample size increases to infinity. A more formal proof of the origin being an interior

point follows:

Proof. Since φ j integrate to zero, g(z;α) will integrate to one regardless of the choice of α. So it is sufficient to show that a neighborhood exists around α = 0 such that g(z;α) ≥ 0, for all z. Since each φ j is bounded on the unit interval, let

max ,j j jM U L⎡ ⎤= −⎣ ⎦ where Uj is the upper bound of φ j and Lj is the lower

bound. Further define { }max jjM M= . Now define a neighborhood around zero

by {α = (α1, …, αm) : { }1 , 1, ...,j j mmM

α ≤ ∀ ∈ }. Then, g(z;α) = 1 + α′ϕ(z)

where ϕ(z) = (φ1(z), …, φm(z))′, which is always nonnegative based on the inequality below:

( ) ( )1 1

1; 1 1 1 1 0m m

j jj j

g z z M M MmmM

α α ϕ α α= =

′= + ≥ − ≥ − ≥ − =∑ ∑

10 See Rayner and Best (1989), p. 34.

23

So, all elements of 1: jAmM

α α⎧ ⎫= ≤⎨ ⎬⎩ ⎭

% produce valid densities and the origin is an

interior point of that set.

Certainly there are values of Aα ∉ % that also produce densities. Next, it will be

shown that all values of α that allow g to remain nonnegative everywhere on the unit

interval are in a convex set in ℜm. So, the null hypothesis will be shown to be an

interior point of a convex parameter space.

As has been stated, g(z;α), is not a probability density function for some choices

of α. Although care was taken in the construction of g so that it would integrate to one

over the unit interval, some choices of α could cause g to be negative over some portion

of that interval. Were we constructing a likelihood ratio statistic, this would be more

troublesome, since the maximum likelihood estimate of α would have to be constrained

to choices that allowed g to be a legitimate density function. It is expected that for most

problems, an unconstrained11 maximum likelihood estimator may not even exist.12

However, the Lagrange multiplier statistic does not require calculation of the

unconstrained maximum likelihood statistic. It merely requires a comparison of the

gradient (roughly, slope) relative to the Hessian (roughly, curvature), evaluated at the

null hypothesis. If the judgment is that the gradient is near enough to zero, then the null

is not rejected. Nearby α’s to the α = 0 point of the null hypothesis will be densities as

11 Since g is constructed to integrate to 1 over the unit interval, choices of α that allow g to be negative over regions of the unit interval that do not contain data allow the “likelihood” function to increase, possibly without limit, over regions that do contain data, which would cause the function to be unbounded. It should also be noted that some non-density g’s will cause the “likelihood” function to take negative values, if an odd number of observations occur in the region on which g is negative. 12 A constrained likelihood may exist depending on the choice of basis functions.

24

will be shown more formally relative to the previous technical point addressed. In fact,

all the g(z;α) that are legal densities are near one another in the sense that the values of

α that allow g to remain nonnegative are in a convex set in ℜm.

Proof. Let α = (α1, …, αm)′ ∈ ℜm, ϕ(z) = (φ1(z), …, φm(z))′. Assume the contrary: at least one of the densities is not in a common convex region of ℜm. Then there must be at least one function g(z;ω) that becomes negative at some point z0 ∈ [0,1], such that ω is a convex combination13 of ξ and ζ, where g(z;ξ) and g(z;ζ) are nonnegative everywhere on the unit interval.14

So, g(z0; tξ + (1-t)ζ) = 1 + ( tξ + (1-t)ζ)′ϕ(z0) < 0 ⇒ tξ′ϕ(z0) + (1-t)ζ′ϕ(z0) < -1 Since g(z0;ξ) = 1 + ξ′ϕ(z0) ≥ 0 and g(z0;ζ) = 1 + ζ′ϕ(z0) ≥ 0, tξ′ϕ(z0) + (1-t)ζ′ϕ(z0) ≥ -t – (1-t) = -1, which is a contradiction.

So, the assumption that g(z;ω) becomes negative at some point z0 ∈ [0,1] is impossible

and, thus, the densities are in a convex region of ℜm.

2.3 SPLINE LAGRANGE MULTIPLIER TEST FOR A UNIFORM

DISTRIBUTION

It is required that ( )1

0 j v dvφ∫ = 0; one way of assuring this is to choose any set

of functions {ψj} that are integrable over [0,1] and with ψ j(z) = Ψj′(z), and define

φ j(z)= ψ j(z) - ( )1

0 j v dvψ∫ , since ( )1 1

0 0( )j jv u du dvψ ψ⎡ ⎤−⎢ ⎥⎣ ⎦∫ ∫ =

( ) ( ){ } 11

0 0

vuj j u v

v v u==

= =⎡ ⎤Ψ − Ψ⎣ ⎦ = Ψj(1) − [Ψj(1) − Ψj(0)] − Ψj(0) = 0 .

If we wanted to define a cubic spline, we could, for example, define

13 ω = tξ + (1-t)ζ for some t ∈ [0,1] 14 ω,ξ, and ζ are all choices of α ∈ ℜm

25

( ) 3

1, 2

3max , 0 3, 4, ,2

j

j

z j

z jz j mm

ψ

⎧ =⎪⎪ ⎧ ⎫= ⎨ −⎪ ⎪⎛ ⎞− =⎨ ⎬⎜ ⎟⎪ −⎝ ⎠⎪ ⎪⎪ ⎩ ⎭⎩

K.

The bottom functional form can be visualized as translating the function z3+, such that

its origin is at each of the set of points {0, (m-2)-1, 2(m-2)-1, …, (m-3) (m-2)-1}, where

33 0

0 0z zz

z+ ⎧ ≥⎪= ⎨

<⎪⎩, the positive portion of z3.

The value, first derivative and second derivative of the ψ j’s are zero at 23

−−

mj , where

the positive portion of the function begins; so, the addition of a multiple of ψ j to a

cubic function (or to a different cubic spline) results in a cubic spline. Thus, this set of

ψ j’s form a basis for cubic splines with equidistant knots on [0,1].15

It appears that, using the cubic spline basis, the Fisher information matrix can be

calculated directly, so reliance on estimates in this case is unnecessary. The φ’s that are

in the integrand of the typical element of this Fisher information matrix are cubic

polynomials over part of their range and constant functions over the other part. So, it is

only necessary to integrate zero-degree, cubic and sextic polynomials. Thus, we must

evaluate linear, quartic and septemic polynomials at zero, one, and all knotpoints.

Some benefits and concerns of this type of basis will be presented in the next chapter.

There is nothing a priori to compel the selection of cubic splines instead of

quadratic or linear splines. In fact even an exponentiated spline, using expressions of 15 A spline is a function of a given number m of piecewise polynomials (or some other general function) of a given degree n, each defined on a subset of a range, connected at m-1 points in the range, called nodes or knots, such that the values and derivatives up to degree m-1 of consecutive polynomials are identical at the nodes. Thus, cubic splines require values and first and second derivatives of consecutive cubic polynomials to be equal at the knots.

26

the form “ ( )exp j jα φ ” in the alternative hypothesis, may be a reasonable basis for a

test.16 Quadratic and cubic splines are more aesthetic than linear splines in constructing

likely alternative densities in that their knots are not discernible since the first

derivatives of contiguous polynomials are equal. Cubic splines perhaps are to be

preferred to quadratic splines since they are allowed to bend twice in a subinterval so

they may be better at imitating the tails of some alternative distributions, but that

characteristic may be at the expense of some other desired feature.

At this point, it can be noted that the Pearson χ2 test is equivalent to a zero-

degree spline GFT for a continuous distribution. Recall the structure of the hypotheses:

H0: pj = pj0 , j = 1, …, m+1 vs. H1: Not H0

If each of the pj0 is set to a constant p, then H0 becomes the uniform discrete

distribution. So a random sample, x = (x1, …, xn)′ from an unknown distribution F(X)

can be tested using:

H0: X ~ U(0,1) vs. H1: X ~ G(z)

where g(z) can be of the form of equation Eq. 2.1.1, H1:17

16 Please see Appendix E for a proof that the proposed LM statistic is invariant to linear combinations and exponentiation of basis functions, regardless of whether the basis functions are polynomials, splines, or some other bounded function. 17 There are alternative representations as well, with one being:

g(z) = ( )1

1m

k kk

zα φ=

+ ∑ , where, ( ) [ ]1

11

,, 1, ,

10 0,1

otherwise

k km m

k

m

k mz

z zφ

−

−

⎧ ⎡ ⎤⎣ ⎦⎪=⎨

⎪⎩

∈= ∉

−K

27

g(z) = ( )1

1m

k kk

zα φ=

+ ∑ , where, ( ))1

1 1

1

1 ,

1 ,1 , 1, ,

0 otherwise

k km m

mk m

z

z z k mφ

−+ +

+

⎧ ⎡∈ ⎣⎪⎪ ⎡ ⎤= − ∈ =⎨ ⎣ ⎦⎪⎪⎩

K .

This zero-degree spline Lagrange multiplier test statistic (ZSLM) would be formed in

the same way as that of the cubic spline Lagrange multiplier test statistic (CSLM), by

using the score vector and Fisher information matrix indicated by the log likelihood

function.

The score evaluated at the null hypothesis is:

( ) ( ) ( )11 1

0 , ,n n

i m ii i

s x xφ φ= =

⎛ ⎞′ = ⎜ ⎟

⎝ ⎠∑ ∑K ,

a typical element of which would be (nj - nm+1), where nj is the number of observations

in the jth bin, or in the interval [ 11 1,j j

m m−+ + ) and nm+1 is the number of observations in the

last bin, or in the interval [ 1 ,1mm+ ].

A typical element of the Fisher information matrix is

( ) ( ) ( )1

00j j j jI n z z dzφ φ′ ′= ∫ ,

so diagonal elements are 21

nm+ and off-diagonal elements are 1

nm+ . Such a matrix is easy

to invert, with the inverse’s diagonal elements being mn and the off-diagonal elements

equal to 1n− .

2.4 B-SPLINE BASIS

Although the theoretical choice of a basis allows for any set of linearly

independent bounded functions, there are numerical considerations in choosing a basis

28

so that reasonable results can be obtained. The simple cubic spline basis pictured below

with seven members has a Fisher information matrix that is poorly conditioned for

inversion for large m. The seventh member is barely visible ranging from a minimum

value of -0.0004 to a maximum of 0.0076 which would necessitate that its coefficient

might be 2 to 3 orders of magnitude greater than a coefficient from one of the first few

basis members. The difference in magnitude increases greatly as m increases.

-0.5

-0.25

0

0.25

0.5

0.75

0 0.2 0.4 0.6 0.8 1

Figure 2.1. Simple cubic spline basis vectors for m=7

29

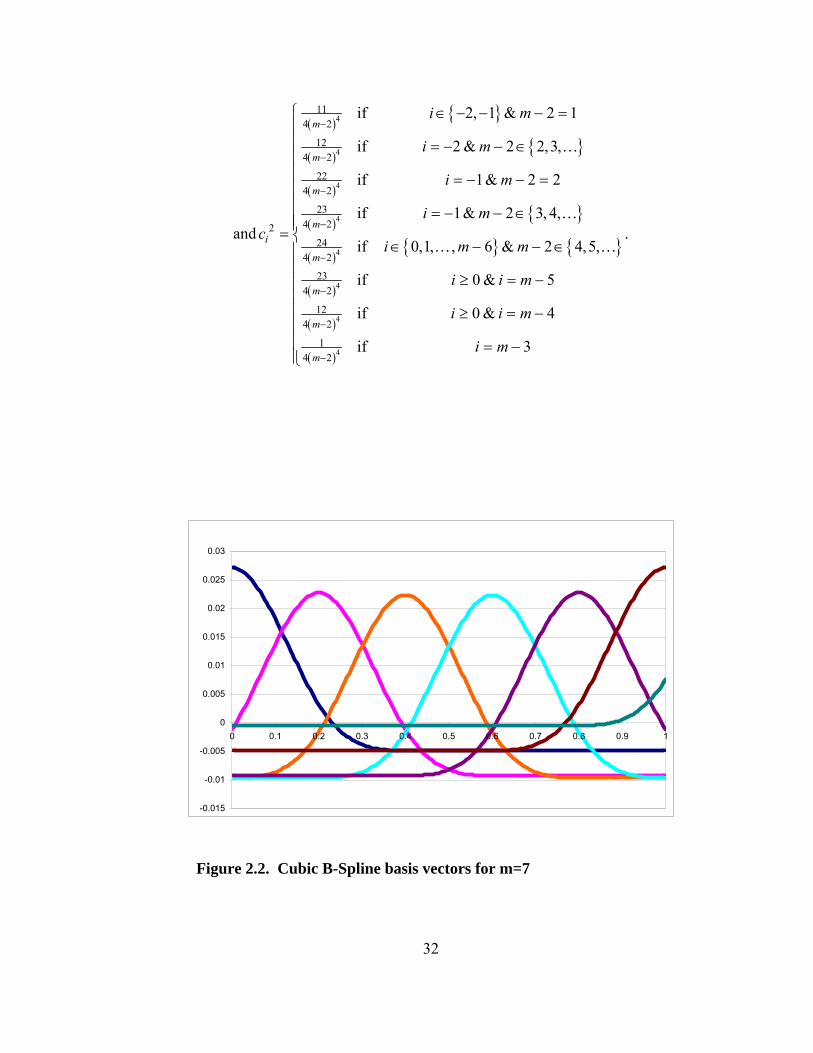

Another basis for splines, typically called B-splines,18 and the one that is used in

the new Lagrange multiplier test, is presented below; it is visually shown in Figure 2.2.

It has the advantage that all the basis members are of the same order of magnitude and

the Fisher information matrix will be dominated by a strong diagonal and be nearly

sparse. Using B-splines, the linear spline matrix will be nearly tridiagonal, the

quadratic spline matrix will have larger values on the main diagonal plus the four

diagonals nearest the main diagonal, while the cubic spline matrix will have its largest

values on the seven main diagonals. As such, this choice of bases is much better

conditioned for inversion of Fisher information matrices and for accumulating the

corresponding scores.

In general, B-splines of order k (k=1 corresponding to linear splines, k=2

corresponding to quadratic splines, k=3 corresponding to cubic splines, and so on)

require k+1 basis functions for the first segment, with the requirement of adding one

basis function for each additional segment. However, the splines that we are interested

in have a requirement of integrating to zero over the unit interval. Consequently, we

can construct the splines with one fewer basis function.

Linear B-spline functions look like “tent” functions increasing linearly from

zero to a maximum from one knot point to the next, then decreasing from that

maximum back to zero. Since this application requires the functions to integrate to zero

on [0,1], these “tents” will be translated downward so that some of their range will be

negative.

18 See Judd, p. 227

30

The functional form for the linear spline basis with m equal segments (and m+1

knots) is shown below. Superscripts of “1” will distinguish these basis functions from

the quadratic spline basis functions, which have a superscript of “2” and the cubic

spline basis functions which have a superscript of “3”:

( ) ( )1 1 1, 0,1, , 1i i ix x c i mφ ψ= − = −K , where

( )1

1 2 1 2

ifif

0 otherwise

i i im m m

i i ii m m m

x xx x xψ

+

+ + +

⎧ − ≤ ≤⎪= − ≤ ≤⎨⎪⎩

and{ }2

2

11

12

if 0,1, , 2

if 1m

im

i mc

i m

⎧ ∈ −⎪= ⎨= −⎪⎩

K.

It must be understood that the functions need not be defined outside the unit interval.

For ease of exposition, that contingency is ignored. For example, the second segment

of ψm-11 by the above definition is defined on the interval [1, (m+1)/m] but is

unnecessary for this application.

If the segments are unequal in length, one can substitute {x0 , x1 , …, xm} for

{ }0,1, ,im i m= K as boundaries for the various domain segments in the above formula,

where x0 and xm substitute for zero and one, respectively, while x1, x2, …, xm-1 are the

desired knot points.

The formula for quadratic splines is a bit more complicated with three non-

trivial expressions defining each basis function. In addition, there must be one more

function than in the basis for the linear spline to produce the same number of

polynomial segments in the quadratic spline; so with m basis functions, one can

describe only m-1 quadratic segments and m-2 knots.

( ) ( )2 2 2 , 1, 0,1, , 2i i ix x c i mφ ψ= − = − −K , where

31

( )

( )( ) ( ) ( ) ( )

( )

2 11 1 1

2 3 1 1 21 1 1 1 1 12

23 2 31 1 1

if

if

if

0 otherwise

i i im m m

i i i i i im m m m m m

ii i im m m

x x

x x x x xx

x xψ

+− − −

+ + + + +− − − − − −

+ + +− − −

⎧ − ≤ ≤⎪⎪ − − + − − ≤ ≤⎪= ⎨⎪ − ≤ ≤⎪⎪⎩

and

( )

( ){ }

( ){ } { }

( )

( )

3

3

3

3

3

43 1

53 1

623 1

53 1

13 1

if 1& 1 1

if 1& 1 2,3,

if 0,1, , 4 & 1 3, 4,

if 0 & 3

if 2

m

m

i m

m

m

i m

i m

i m mc

i i m

i m

−

−

−

−

−

⎧ = − − =⎪⎪ = − − ∈⎪⎪ ∈ − − ∈= ⎨⎪

≥ = −⎪⎪

= −⎪⎩

K

K K .

The formula for cubic splines has four non-trivial expressions defining each

basis function. The m basis functions describe m-2 cubic segments and the

corresponding m-3 knots.

( ) ( )3 3 3, 2, 1, 0,1, , 3i i ix x c i mφ ψ= − = − − −K , where

( )

( )( ) ( ) ( )( )( ) ( )( )( )( ) ( )( )( ) ( ) ( )

( )

3

3 12 2 2

2 22 3 1 4 1 1 22 2 2 2 2 2 2 2 2

2 23 4 1 3 4 2 2 32 2 2 2 2 2 2 2 2

34 3 42 2

if

if

if

if

i

i i im m m

i i i i i i i i im m m m m m m m m

i i i i i i i i im m m m m m m m m

i i im m m

x

x x

x x x x x x x x

x x x x x x x x

x x

ψ

+− − −

+ + + + + + +− − − − − − − − −

+ + + + + + + +− − − − − − − − −

+ + +− − −

=

− ≤ ≤

− − + − − − + − − ≤ ≤

− − + − − − + − − ≤ ≤

− ≤ ≤ 2

0 otherwise

⎧⎪⎪⎪⎪⎨⎪⎪⎪⎪⎩

32

and

( ){ }

( ){ }

( )

( ){ }

( ){ } { }

( )

( )

( )

4

4

4

4

4

4

4

4

114 2

124 2

224 2

234 22

244 2

234 2

124 2

14 2

if 2, 1 & 2 1

if 2 & 2 2,3,

if 1& 2 2

if 1& 2 3, 4,

if 0,1, , 6 & 2 4,5,

if 0 & 5

if 0 & 4

if 3

m

m

m

mi

m

m

m

m

i m

i m

i m

i mc

i m m

i i m

i i m

i m

−

−

−

−

−

−

−

−

⎧ ∈ − − − =⎪⎪ = − − ∈⎪⎪ = − − =⎪⎪ = − − ∈⎪⎪= ⎨

∈ − − ∈⎪⎪

≥ = −⎪⎪⎪ ≥ = −⎪⎪ = −⎪⎩

K

K

K K.

-0.015

-0.01

-0.005

0

0.005

0.01

0.015

0.02

0.025

0.03

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

Figure 2.2. Cubic B-Spline basis vectors for m=7

33

Figure 2.2 is an illustration of a seven-function basis for cubic B-splines. Note

that there are 3 pairs of mirror-image functions and a function that is a bit below zero on

[0,0.8] and rising cubically on [0.8,1].

Starting from the left, the first and sixth basis functions contain only two cubic

segments (not including the constant segment). The second and fifth functions contain

three cubic segments, the third and fourth functions are the only ones that contain all

four cubic segments, while the seventh function contains only one cubic segment.

2.5 NEYMAN’S SMOOTH TEST

A GFT to which the CSLM is also closely related would be Neyman’s smooth

test.19 Smooth tests were so named because the alternative distributions varied

“smoothly” away from the null hypothesized distribution. Neyman called this test a Ψ2

test (which can be contrasted with Pearson’s χ2 test). Neyman constructed an

alternative hypothesis of order m (to a null of a uniform random variable on [0,1] ) to be

( ) ( ) ( )1

; expm

m j jj

g z K zα α α π=

⎧ ⎫⎪ ⎪= ⎨ ⎬⎪ ⎪⎩ ⎭∑ , 0 ≤ z ≤ 1, m = 1,2,…

where K(α) is the constant necessary for gm to be a density, and the πj are orthonormal

polynomials of degree j that integrate to zero on the unit interval. As in the general

case, the null hypothesis is that α = 0. With the exponentiation, there is no problem

with gm(z;α) taking negative values. We can reparameterize Neyman’s alternative as

19 See Rayner and Best (1989), p.7 and p.46-48. The choices of indices, variable and parameter names have been changed to show the parallel with the CSLM and ZSLM.

34

gm(z;α) = ( )

( )

1

1

01

exp 1

exp 1

m

j jj

m

j jj

z

z dz

α π

α π

=

=

⎧ ⎫⎪ ⎪+⎨ ⎬⎪ ⎪⎩ ⎭⎧ ⎫⎪ ⎪+⎨ ⎬⎪ ⎪⎩ ⎭

∑

∑∫, 0 ≤ z ≤ 1, m = 1,2,…

With this parameterization, the integral in the denominator is a constant depending on

the α vector of which can be represented by C(α) = ( )e

K α . Neyman’s test statistic is

Ψ2m=

( )2

1 1where

m nj i

j jj i

yU U

n

π

= =

=∑ ∑ . This test statistic is asymptotically χ2(m) .

Neyman expected that values of m of 4 or 5 would be sufficient to test a large enough

class of alternatives. Ψ2m was a likelihood ratio test statistic rather than a Lagrange

multiplier statistic. Since Neyman thought an m of 4 or 5 would be sufficient, it was not

necessary in practice to compute K(α) for larger values of m. To change this to a

Lagrange multiplier test with possibly larger values of m, which is concerned with

perturbations only in the neighborhood of the null hypothesis, it will be convenient to

simplify calculations by substituting a regular polynomial form in place of Neyman’s

exponentiated polynomial.

Using this structure, one definition could be:

g(z) = ( )1

1m

j jj

zα φ=

+ ∑ , where, ( ) [ ]11 0,1

0 otherwise

jj

jz z

zφ +⎧ − ∈⎪= ⎨⎪⎩

.

The corresponding LM test statistic, which is identical to an LM test statistic based on

an exponentiation, is formed in the same way as shown in Chapter 2.1, by using the

score vector and Fisher information matrix indicated by the log likelihood function:

35

Score: ( ) ( ) ( )11 1

0 , ,n n

i m ii i

s x xφ φ= =

⎛ ⎞′ = ⎜ ⎟

⎝ ⎠∑ ∑K , a typical element of which would be

1 1

nj

ii

nxj=

−+∑ . A typical element of the Fisher information matrix is

( ) ( ) ( )1

00j j j jI n z z dzφ φ′ ′= ∫ , or

1 1 11 10

( )( )( 1)( 1)( 1)

j jj j

njjn z z dzj j j j

′′+ +

′− − =

′ ′+ + + +∫ .

One difference between the CSLM test and Neyman’s test is that the CSLM is

more sensitive to differences that are local to a specific part of the unit interval.

Because Neyman’s exponentiated polynomials were defined over the entire interval,

each polynomial affected the likelihood of every data point. For this reason,

polynomials have to make compromises since, in order to fit one point better, it may be

necessary to fit other points that are not nearby more poorly. Splines are more pliable

and better able to fit points in a particular interval without affecting more distant

intervals as much. Additionally, higher-powered polynomials are computationally more

troublesome because of significant rounding errors when adding together terms with

greatly varying orders of magnitude between their coefficients.

“Experience with polynomials derived by truncating [Taylor]20 series[, especially in their use with estimating transcendental functions,] may mislead one into thinking that the use of high order polynomials does not lead to computational difficulties. However it must be appreciated that truncated [Taylor] series are not typical of polynomials in general. [Truncated Taylor series] have the special feature that the terms decrease rapidly in size for values of x in the range for which they are appropriate. A tendency to underestimate the difficulties involved in working with general polynomials is perhaps a consequence of one’s experience in classical analysis. There it is natural to regard a polynomial as a very desirable function since it is bounded in any finite region and has derivatives of all orders. In numerical work, however, polynomials having

20 Text uses the term “power” instead of Taylor

36

coefficients which are more or less arbitrary are tiresome to deal with by entirely automatic procedures.”21

Although there is more initial work to calculating and understanding splines,

they have some numerical properties that are more desirable than polynomials while the

tradeoff in the other properties is not severe. Splines retain the polynomial properties of

being bounded in any finite region and have derivatives of all orders at all points

excluding the relatively small finite number of knotpoints. Other concerns about

rounding are contained in Appendix G.

The Pearson, Neyman, and spline tests are all meet the criteria of the Neyman-

Pearson lemma against simple alternatives. So, it is expected that each test will work

better for alternatives that are of the form determined by their respective perturbing

functions. Tests with other bases of perturbing functions should be better for still other

distributions.

2.6 SIMPLE POLYNOMIAL BASIS

For practical computations with most software using double precision with 32-

bit processors, a basis of simple restricted polynomials, {xm – (m + 1)-1}, m = 1,2, …,

will likely be difficult to work with as m increases since the rows of the Fisher

information matrix are nearly linearly dependent.

It is very easy to compute the cells of such matrices. Each cell is

( ) ( ) ( )1 1 1ij

i j i j+ + + + where i is the row index and j is the column index. However,

21 Wilkinson, J. H., Rounding Errors in Algebraic Processes, p.38

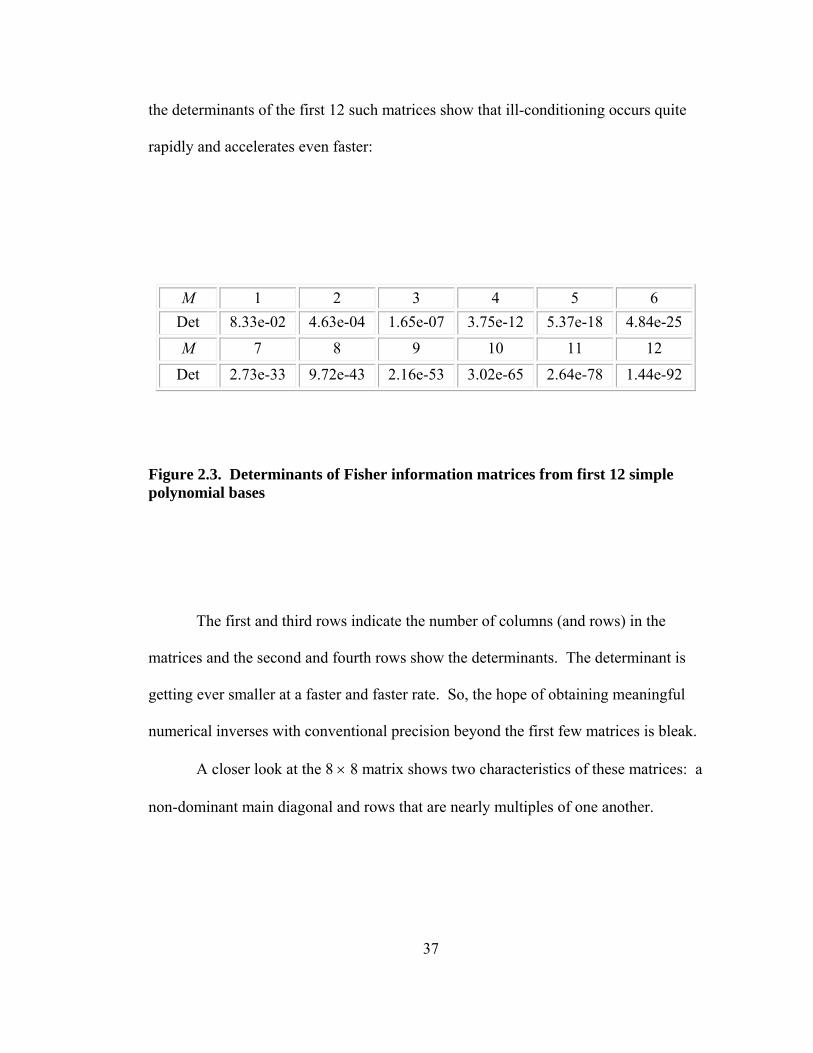

37

the determinants of the first 12 such matrices show that ill-conditioning occurs quite

rapidly and accelerates even faster:

M 1 2 3 4 5 6 Det 8.33e-02 4.63e-04 1.65e-07 3.75e-12 5.37e-18 4.84e-25

M 7 8 9 10 11 12

Det 2.73e-33 9.72e-43 2.16e-53 3.02e-65 2.64e-78 1.44e-92

Figure 2.3. Determinants of Fisher information matrices from first 12 simple polynomial bases

The first and third rows indicate the number of columns (and rows) in the

matrices and the second and fourth rows show the determinants. The determinant is

getting ever smaller at a faster and faster rate. So, the hope of obtaining meaningful

numerical inverses with conventional precision beyond the first few matrices is bleak.

A closer look at the 8 × 8 matrix shows two characteristics of these matrices: a

non-dominant main diagonal and rows that are nearly multiples of one another.

38

0.0833 0.0833 0.0750 0.0667 0.0595 0.0536 0.0486 0.04440.0833 0.0889 0.0833 0.0762 0.0694 0.0635 0.0583 0.05390.0750 0.0833 0.0804 0.0750 0.0694 0.0643 0.0597 0.05560.0667 0.0762 0.0750 0.0711 0.0667 0.0623 0.0583 0.05470.0595 0.0694 0.0694 0.0667 0.0631 0.0595 0.0561 0.05290.0536 0.0635 0.0643 0.0623 0.0595 0.0565 0.0536 0.05080.0486 0.0583 0.0597 0.0583 0.0561 0.0536 0.0510 0.04860.0444 0.0539 0.0556 0.0547 0.0529 0.0508 0.0486 0.0465

⎡ ⎤⎢ ⎥⎢⎢⎢⎢⎢⎢⎢⎢⎢⎢⎣ ⎦

⎥⎥⎥⎥⎥⎥⎥⎥⎥⎥

This suggests the topic of the next section: If a simple basis does not work, why not try

an orthogonal one?

2.7 ORTHOGONAL POLYNOMIAL BASIS

Alternatively, one can search for orthogonal polynomials so that the Fisher

information matrix is diagonal with an uncomplicated inverse. A recursive formula for

Legendre-type polynomials is shown below. The Legendre polynomials are typically

defined on the range [-1,1], so a change of variable is necessary so that the resultant

polynomials are orthogonal on our range of interest, [0,1].

Let p0(x) = 1 and p1(x) = 2x – 1. Then a recursive formula which will generate

as many orthogonal polynomials as necessary on [0,1] is:

pm+1 = [(2m + 1)(2x – 1) pm(x) – m pm-1(x)] / (m + 1), m = 1,2, …,

with ( )21

0

12 1mp x dx

m⎡ ⎤ =⎣ ⎦ +∫ , while, as designed, ( ) ( )1

00, if .m kp x p x dx m k⎡ ⎤ ⎡ ⎤ = ≠⎣ ⎦ ⎣ ⎦∫

The first few such polynomials are:

p0(x) = 1

p1(x) = 2x – 1

p2(x) = 6x2 - 6x + 1

39

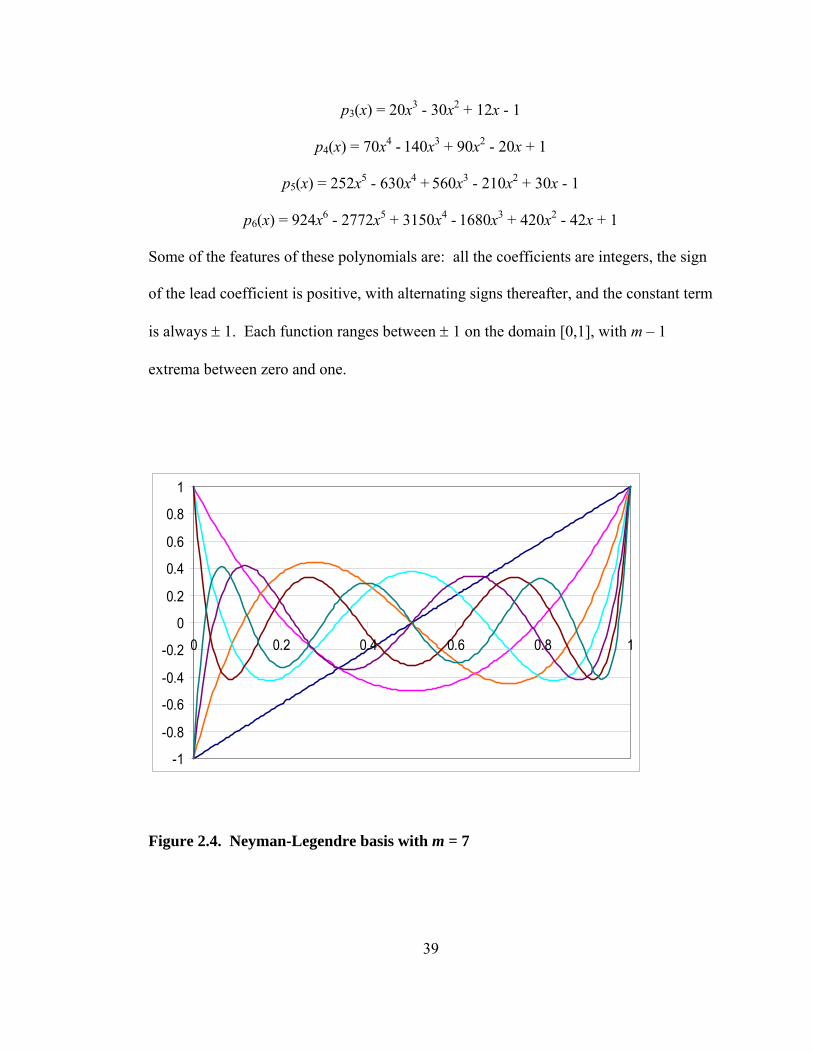

p3(x) = 20x3 - 30x2 + 12x - 1

p4(x) = 70x4 - 140x3 + 90x2 - 20x + 1

p5(x) = 252x5 - 630x4 + 560x3 - 210x2 + 30x - 1

p6(x) = 924x6 - 2772x5 + 3150x4 - 1680x3 + 420x2 - 42x + 1

Some of the features of these polynomials are: all the coefficients are integers, the sign

of the lead coefficient is positive, with alternating signs thereafter, and the constant term

is always ± 1. Each function ranges between ± 1 on the domain [0,1], with m – 1

extrema between zero and one.

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

0 0.2 0.4 0.6 0.8 1

Figure 2.4. Neyman-Legendre basis with m = 7

40