a corporate valuation of dong energy - au...

TRANSCRIPT

Authors: Marc Nyvang Hassing: mh86702 Martin Nørgaard: mn87728 Master program: Finance & International Business Academic supervisor: Otto Friedrichsen Number of characters: 184,894 + 21 tables + 21 figures

A corporate valuation of DONG Energy An analysis of the appropriate IPO price

School of Business and Social Sciences – Aarhus University – Economic and Business’ - August 2014

I

ABSTRACT The purpose of this thesis is to construct an in depth corporate valuation analysis of DONG

Energy in the light of what would be an appropriate IPO price in the current market. A

valuation applying the DCF and Multiples approaches together with a research on IPO

discounts will be the main drivers in the process of estimating a final IPO price for DONG

Energy.

DONG Energy’s strategic position is analyzed through a strategic analysis focusing on

DONG Energy’s resources and competences as well as the over all outlook for the industry.

The strongest asset of DONG Energy is their high competences and strong position in the

growing offshore wind market. However, DONG Energy’s Exploration & Production

activities have also positive forecasts.

The trends of DONG Energy’s financial performance are analyzed through a financial

analysis including the period from 2007 to 2013. Despite a stable revenue growth no real

trends has been observed. However, recent years poor financial performance as well as a

heavy investment program in transforming the energy system has increased DONG

Energy’s credit riskiness. Despite recent poor financial performance the future outlook for

DONG Energy is positive as the investments made in the past are expected starting to

generate cash flows. Additional the equity injection of DKK 13 billion made in 2014 have

stabilize DONG Energy’s capital structure and secured the execution of transforming the

energy system.

Applying the comparable firm method, this thesis finds indications about underwriting

premiums in the Danish IPO market, which is not in line with existing empirical evidence

about IPO discounts. However, the results were not significant and must therefore be

interpreted with great caution. Discounts or premiums on the Danish IPO market was also

tested applying first day return as a proxy. These results were significant on a 10%

confidence level and provide evidence about an 11.34% discount on the Danish IPO

market. The thesis also tested if there was difference between the discount given inside and

outside an IOP wave. However, neither the comparable firm method nor the first day return

method found any significant results.

Combining the theoretical fair value estimate form the valuation approaches with an IPO

discount, DONG Energy’s equity value is estimated to DKK 52,525 million or DKK

123.45 per share.

II

LIST OF CONTENT

1"INTRODUCTION"____________________________________________________________________________________"1!

1.1!INTRODUCTION!___________________________________________________________________________________!1!

1.2!PROBLEM!STATEMENT!____________________________________________________________________________!2!

1.3!METHODOLOGY!___________________________________________________________________________________!2!

1.4!DESCRIPTION!OF!DATA!AND!ITS!VALIDITY!__________________________________________________________!3!

1.5!DELIMITATIONS! __________________________________________________________________________________!3!

1.6!STRUCTURE!_______________________________________________________________________________________!4!

2"DONG"ENERGY" _____________________________________________________________________________________"6!

2.1!DONG!ENERGY!AT!A!GLANCE! _____________________________________________________________________!6!

3"STRATEGIC"ANALYSIS"OF"DONG"ENERGY"______________________________________________________"9!

3.1!INTERNAL!ANALYSIS!OF!DONG!ENERGY!___________________________________________________________!9!

3.2!PESTEL!ANALYSIS!OF!DONG!ENERGY!___________________________________________________________!11!

3.3!PORTERS!FIVE!FORCES!ANALYSIS!OF!DONG!ENERGY!______________________________________________!18!

3.4!SWOT!ANALYSIS!DONG!ENERGY!________________________________________________________________!20!

3.5!CONCLUSION!ON!DONG!ENERGY’S!STRATEGIC!POSITION!__________________________________________!23!

4"DEFINING"VALUATION"APPROACHED"AND"THEIR"ELEMENT"FOR"DONG"ENERGY"____"24!

4.1!DISCOUNTED!CASH!FLOW!(DCF)!VALUATION!____________________________________________________!25!

4.2!THE!FREEECASHEFLOW!(FCF)!___________________________________________________________________!26!

4.3!THE!WEIGHTED!AVERAGE!COST!OF!CAPITAL!(WACC)! ___________________________________________!27!

4.4!RELATIVE!VALUATION!BY!MULTIPLES!_____________________________________________________________!34!

5"FINANCIAL"ANALYSIS"OF"DONG"ENERGY" ____________________________________________________"36!

5.1!REFORMULATING!OF!THE!FINANCIAL!STATEMENTS!_______________________________________________!36!

5.2!FREE!CASH!FLOW!(FCF)!_________________________________________________________________________!43!

5.3!ANALYSIS!OF!HISTORICAL!PERFORMANCE!IN!MORE!DETAILS!_______________________________________!44!

6"BUGETING"________________________________________________________________________________________"50!

6.1!REVENUE!________________________________________________________________________________________!51!

6.2!NOPLAT!________________________________________________________________________________________!52!

6.3!INVESTED!CAPITAL!_______________________________________________________________________________!54!

6.4!RIOC!____________________________________________________________________________________________!54!

6.5!FREE!CASH!FLOW!________________________________________________________________________________!55!

7"VALUATION"OF"DONG"ENERGY"________________________________________________________________"56!

7.1!DFC!VALUATION!_________________________________________________________________________________!56!

7.2!SENSITIVITY!ANALYSIS!___________________________________________________________________________!57!

7.3!RELATIVE!VALUATION!BY!MULTIPLES!_____________________________________________________________!60!

III

7.4!FAIR!VALUE!ESTIMATION!OF!DONG!ENERGY!_____________________________________________________!61!

8"INITIAL"PUBLIC"OFFERING"(IPO)" _____________________________________________________________"62!

8.1!INTRODUCTION!AND!MOTIVATION!________________________________________________________________!62!

8.2!REVIEW!OF!RELEVANT!THEORY!___________________________________________________________________!64!

8.3!REVIEW!OF!RELEVANT!EMPIRICAL!EVIDENCE!_____________________________________________________!67!

8.4!HYPOTHESIS!_____________________________________________________________________________________!69!

8.5!METHODOLOGY!__________________________________________________________________________________!71!

8.6!TEST!STATISTICS!_________________________________________________________________________________!77!

8.7!DATA!COLLECTION!_______________________________________________________________________________!79!

8.8!DESCRIPTIVE!STATISTICS!_________________________________________________________________________!82!

8.9!EMPIRICAL!EVIDENCE!____________________________________________________________________________!83!

8.10!CONCLUSION!___________________________________________________________________________________!88!

9"DONG"ENERGY’S"IPO"PRICE"____________________________________________________________________"89!

10"CONCLUSION,"DISCUSSION"AND"FURTHER"REASEARCH"_________________________________"90!

10.1!CONCLUSION!___________________________________________________________________________________!90!

10.2!DISCUSSION!AND!FURTHER!RESEARCH!__________________________________________________________!92!

11"BIBLIOGRAPHY"_________________________________________________________________________________"93!

12"APPENDICIES"___________________________________________________________________________________"97!

IV

LIST OF TABLES !

Table!1!(!Estimation!of!the!capital!structure!............................................................................................................................!28!

Table!2!(!Comparison!of!Cost!of!Debt!measures!.......................................................................................................................!30!

Table!3!(!Bottom(up!beta!calculation!..........................................................................................................................................!33!

Table!4!(!The!Danish!Corporate!tax!rate!....................................................................................................................................!34!

Table!5!(!The!WACC!for!DONG!Energy!.........................................................................................................................................!34!

Table!6!(!Highlights!of!2013!peer!group!data!...........................................................................................................................!36!

Table!7!(!Capitalization!of!operating!leases!..............................................................................................................................!42!

Table!8!(!Free!Cash!Flow!calculation!............................................................................................................................................!44!

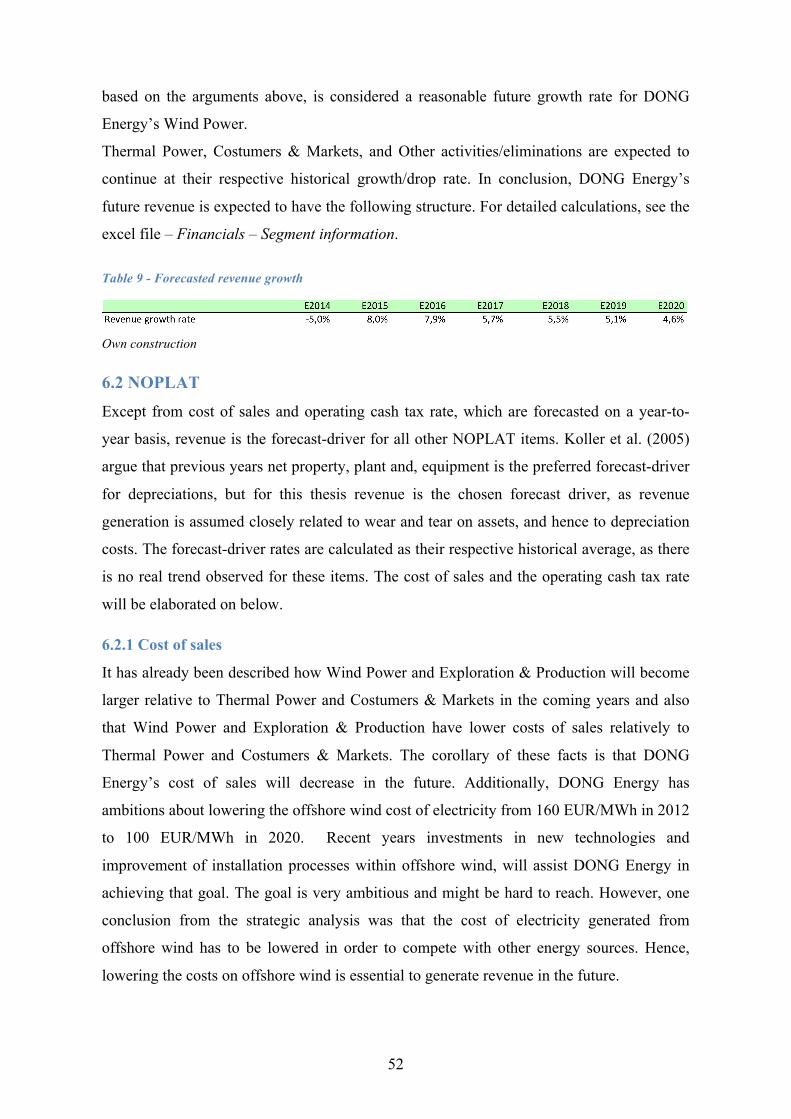

Table!9!(!Forecasted!revenue!growth!...........................................................................................................................................!52!

Table!10!(!Forecasted!costs!of!sales!..............................................................................................................................................!53!

Table!11!(!Forecasted!operating!cash!tax!rate!for!DONG!Energy!....................................................................................!53!

Table!12!(!Forecasted!invested!capital!growth!rate!for!DONG!Energy!.........................................................................!54!

Table!13!(!Expected!future!ROIC!for!DONG!Energy!................................................................................................................!55!

Table!14!(!Expected!future!free!cash!flow!for!DONG!Energy!..............................................................................................!55!

Table!15!(!The!effect!of!a!ROIC!at!10%!in!2016!and!12%!in!2020!...................................................................................!60!

Table!16!(!Fair!value!estimate(model!...........................................................................................................................................!62!

Table!17!(!Financial!report!associated!with!the!month!of!IPO!.........................................................................................!74!

Table!18!(!Search!strategy!(!Initial!sample!form!Zephyr!.....................................................................................................!80!

Table!19!(!Descriptive!statistics!from!the!comparable!firm!approach!..........................................................................!82!

Table!20!(!Descriptive!statistics!for!first!day!return!..............................................................................................................!83!

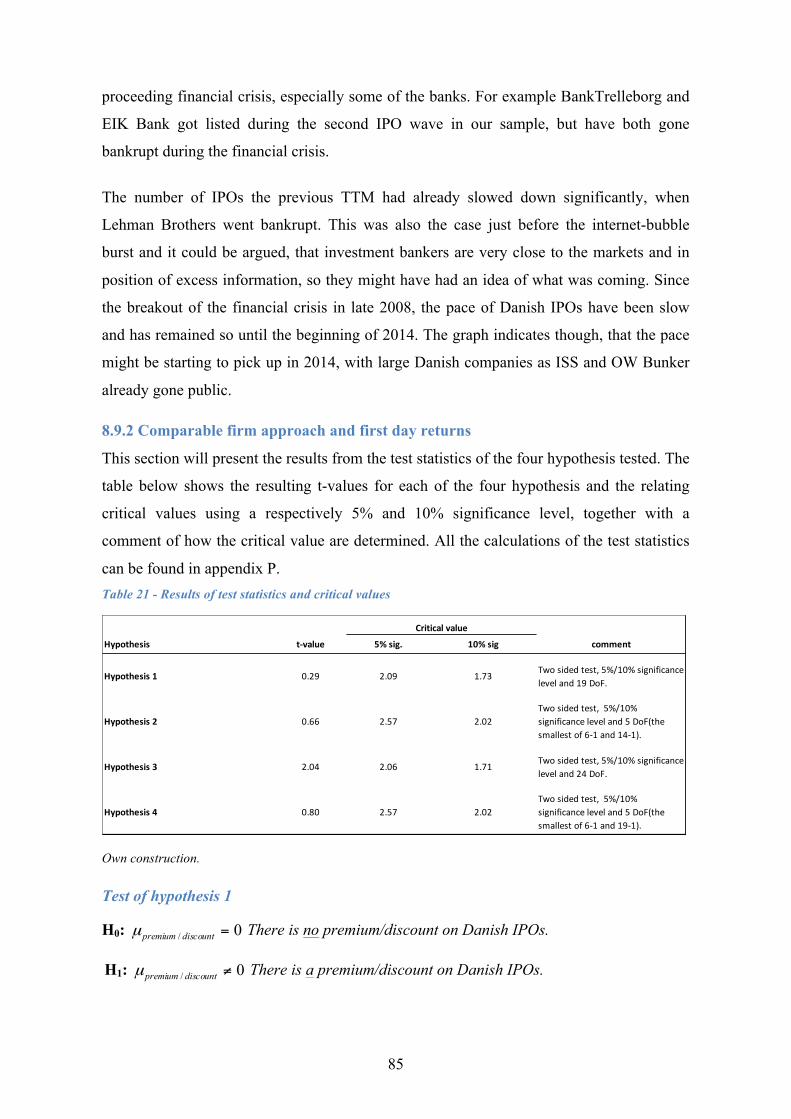

Table!21!(!Results!of!test!statistics!and!critical!values!.........................................................................................................!85!

V

LIST OF FIGURES !

Figure!1!(!The!thesis!structure!............................................................................................................................................................!5!

Figure!2!(!PESTEL!analysis!of!DONG!Energy!.............................................................................................................................!12!

Figure!3!(!GCP,!CO2,!and!gross!energy!consumption!in!the!Danish!market!................................................................!13!

Figure!4!(!Historical!development!in!selected!commodity!prices!.....................................................................................!14!

Figure!5!(!Conclusion!on!Porters!Five!Forces!............................................................................................................................!19!

Figure!6!(!SWOT!analysis!of!DONG!Energy!................................................................................................................................!21!

Figure!7!(!Comparison!of!Business!Performance!and!IFRS!.................................................................................................!38!

Figure!8!(!The!development!in!DONG!Energy's!equity!(2007(2013)!..............................................................................!40!

Figure!9!(!DONG!Energy's!historical!ROIC!..................................................................................................................................!45!

Figure!10!(!Breakdown!of!Invested!Capital!(average!numbers)!......................................................................................!46!

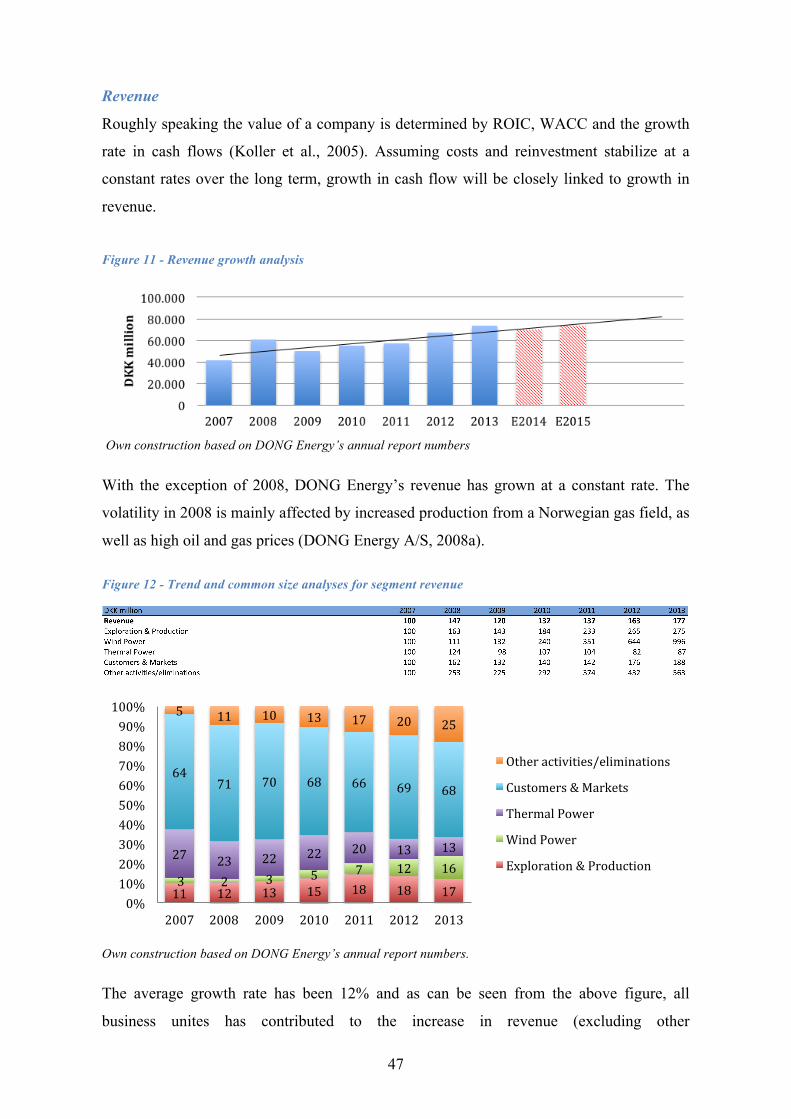

Figure!11!(!Revenue!growth!analysis!...........................................................................................................................................!47!

Figure!12!(!Trend!and!common!size!analyses!for!segment!revenue!...............................................................................!47!

Figure!13!(!Analysis!of!costs!as!a!percentage!of!revenue!.....................................................................................................!49!

Figure!14!(!Common!size!analysis!of!EBITDA!on!segment!level!.......................................................................................!49!

Figure!15!(!Calculating!the!value!of!DONG!Energy!................................................................................................................!56!

Figure!16!(!Sensitivity!analysis!on!NOPLAT(drivers!..............................................................................................................!57!

Figure!17!(!Sensitivity!to!change!in!the!WACC!.........................................................................................................................!58!

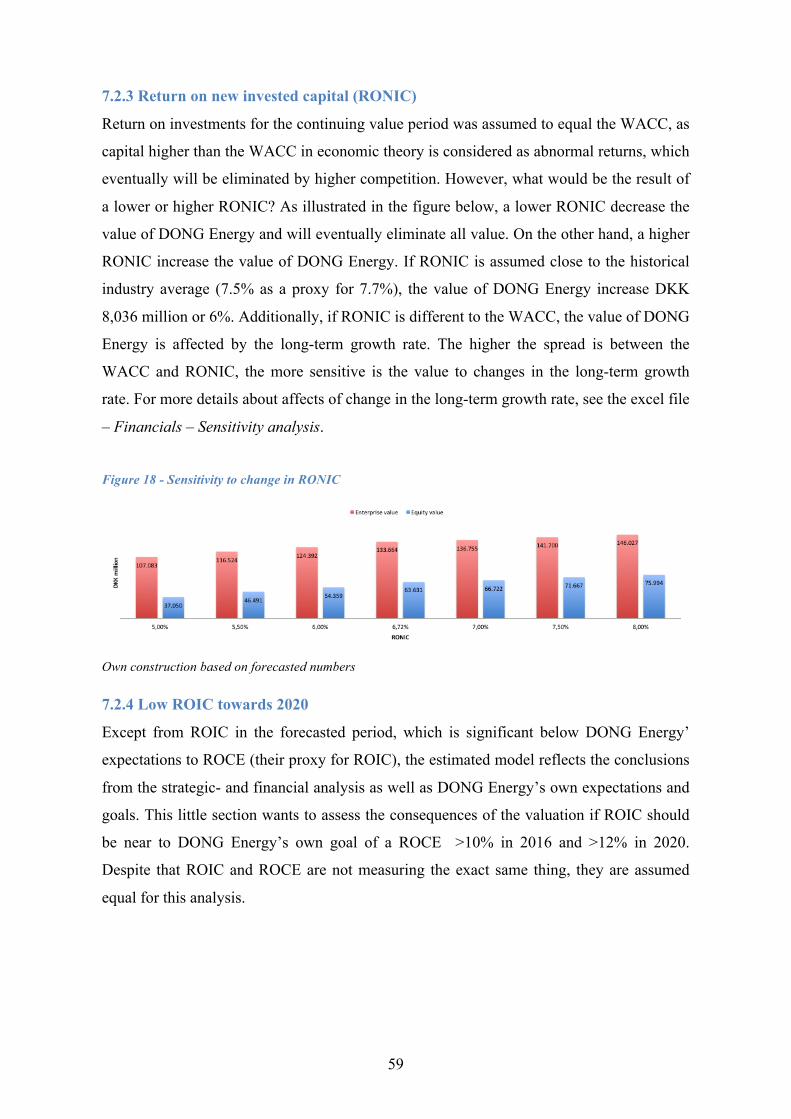

Figure!18!(!Sensitivity!to!change!in!RONIC!................................................................................................................................!59!

Figure!19!(!Summery!of!multiples!valuation!.............................................................................................................................!61!

Figure!20!(!Number!of!Danish!IPOs!previous!trailing!twelve!months!from!1997!to!2014!....................................!84!

Figure!21!(!IPO!pricing!model!..........................................................................................................................................................!89!

1

1 INTRODUCTION

1.1 introduction The purpose of this thesis is to construct an in depth corporate valuation analysis of DONG

Energy in the light of what would be an appropriate IPO price in the current market.

Different valuation approaches, and a research on IPO discounts will be the main drivers in

the process of estimating a final IPO price for DONG Energy. Both authors have a great

interest within the field of finance, and particular in corporate valuation and investment

banking. This thesis is seen as an excellent opportunity to use the knowledge acquired

throughout the years of studying, and to get the chance to dig deeper into the field of

corporate valuation and investment banking.

Recently global stocks have increased in value and indices such as S&P500 and the Danish

C20 are now traded around its nominal all time highs. This is a strong indication of a high

demand for equity investments, and as every economist should know, a high demand is best

satisfied with a lager supply. Thus, it might be a good time to put some new products on the

shelves. An increase in IPO activity has already been observed in 2013 and the IPO outlook

for 2014 is positive due to an overall positive global macroeconomic outlook (Pinelli,

Kelley, Choi, Steinbach, & Suszuki, 2013). Despite a high demand for equity, going public

is not an easy task and hiring an investment bank as the middlemen between companies and

the investing public is mandatory. The investments bank’s job is besides advisory, to set an

introduction price. In regard to IPO’s, this thesis will assess how much value is left on the

table in the IPO underwriting process. The Danish IPO market is the primarily interest for

this thesis, where we recently have seen introductions of Matas, ISS and OW Bunker.

DONG Energy is chosen as the case company for this thesis for more reasons. Firstly the

recent media debate about DONG Energy and its involvement with Goldman Sachs make it

an interesting and actual case. Further, DONG Energy is an interesting case from a

valuation point of view, as it works within multiple business units and is in a

transformation process. Finally, DONG Energy is interesting because it is expected to go

public listed within a few years.

2

1.2 Problem statement Estimating the value of a non-listed company is subject to uncertainty above the normal, as

it cannot be verified by the market’s opinion. The task of valuing an upcoming IPO is

complicated further by strategic price aspects, such as market sentiment. Thus, this

corporate valuation analysis of DONG Energy will apply different valuation methods to

determine a fair value price. An additional element to the valuation will be a research on

IPO discounts, in particular on the Danish market. Further, this thesis will review empirical

evidence on IPOs, including benefits and challenges linked to IPOs, and finally evaluate the

effect on the Initial Public Offering price for DONG Energy.

Thus, the overall goal is to give an answer to what would be the appropriate Initial Public

Offering price for DONG Energy primo 2014, and the key objectives are to answer the

following research questions:

E How is DONG Energy’s strategic situation?

E Which valuation approaches are most appropriate for valuing DONG Energy?

E What is the best estimate for DONG Energy’s cost of capital?

E What is the theoretical correct fair value estimate of DONG Energy?

E What are the general benefits and challenges of an IPO?

E How much if any value is left on the table in the IPO underwriting process?

E Does IPO discounts vary inside and outside of IPO waves?

1.3 Methodology This thesis works within the field of social sciences, meaning that there is no objective truth

about what is the right price for DONG Energy or other companies for that matter.

However, whether you believe in the efficient market hypothesis (EMH) or not, the market

price must be the closes to an objective price. Market prices fluctuate on a daily basis, and

reflect the data available to the market participants. DONG Energy is not yet a public

traded company, and has therefore no direct observable market value. Hence, the purpose

of this thesis is based on valuation approaches and IPO market sentiment aspects, to

estimate a final offering price for DONG Energy. This process will involve a large amount

of information and data. Thus, assumptions about how to handle this information and data,

in the best suitable way, have to be established. Information about DONG Energy and the

energy sector in general will be obtained through large, and competent sources such as

MarketLine, Energistyrelsen, and the European commission. For the financial analysis

3

DONG Energy’s published annual reports will be used as raw data. This data will be

reformulated in order to satisfy the requirements needed for the data input to the actual

valuation. The transformed data will primarily be applied in the discounted cash flow

(DCF) valuation approach in order to contribute to estimating a theoretical fair value for

DONG Energy. The corporate valuation will mainly be conducted after the method stated

in Koller et al. (2005). Secondary inputs are conducted from Damadoran (2012) and

Penman (2013). Thus, a solid theoretical basis forms the foundation for a reliable valuation.

The information and data about DONG Energy, the energy sector and corporate valuation

approaches were obtained without significant challenges. However, finding data on the

Danish IPO market was much more challenging and complex. This is elaborated on in more

details in section 8.

1.4 Description of data and its validity The data used for the corporate valuation of DONG Energy rely on public available

information; i.e. reports, webpages and articles. These sources all contribute to a detailed

knowledge about DONG Energy and their operating markets from a historical and future

point of view. In general these sources are considered objective, as independent parties

verify them. However, the authors are aware that information from DONG Energy’s

webpages and to some extent the information presented in their annual reports can be

biased. After all it must be kept in mind that DONG Energy are preparing for an IPO, and

thus want to look as good as possible.

The knowledgebase about corporate valuation, are obtained through Koller et al. (2005),

Damadoran (2012), and Penman (2013). All works are broadly accepted within the field of

valuation and are often used as textbooks at universities all over the world. As a supplement

various articles and empirical research data will contribute to complete the knowledgebase

about corporate valuation. The literature about IPO is obtained through academic article

databases, such as Business Source Complete and ScienceDirect. Thus, their results are

considered valid as they are based on broadly accepted research methods. The data input

for the analysis of the Danish IPO market is retrieved from Thomson One, which is one of

the world’s major data providers. Thus, these data are also considered valid.

1.5 Delimitations The value of DONG Energy will only be determined from the pre-selected valuation

approaches: Discounted Cash Flow valuation (DCF), and Relative valuation (multiples).

Hence, alternative valuation approaches such as Event Tree Analysis, Decision Tree

4

Analysis, Real Options Analysis, Adjusted Present Value, and Adjusted Value Added etc.

are omitted from this thesis. Hence, the conclusion is not as strong as it could have been if

it was verified by more valuation methods.

The strategic analysis is not the main driver for this thesis, and contains only the most

important strategic analyses. For a greater precision about DONG Energy, their products,

and the energy sector, the strategic analysis could have been expanded with a value chain,

product life cycle, Boston matrix, etc. However, the included models are considered to

provide the readers with the necessary information about DONG Energy’s strategic

position.

As a consequence of large investments in oil and gas fields as well as in offshore wind

projects, DONG Energy holds large tax loss carry forwards and unrecognized deferred tax

assets. These assets do affect the value of DONG Energy’s future cash flows, which to

some extent is accounted for in the tax estimating. However, the exact effect is considered

outside the scope of this thesis.

Additional the stock option program is also considered outside the scope of this thesis, as

its value is associated with some uncertainty. However, assuming a doubling of the value

towards the IPO the value would have been approximately DKK 1.5 billion (Ritzau, 2014).

The effects of the current fluctuations in DONG Energy’s capital structure due to the DKK

13 billion equity injection and divestment in operating as well as non-operating activities

are not incorporated in the capital structure estimation, and hence DONG Energy’s cost of

capital. Thus, a constant cost of capital is applied throughout the thesis even that a year-to-

year estimation would have increased the accuracy of the DCF model. However, the value

of the FCF towards 2020, only accounts for 15% of the total value and the effect on the

total value of a year-to-year estimation of cost of capital is considered insignificant.

Additional delimitations and assumptions will be made throughout the thesis when deemed

necessary.

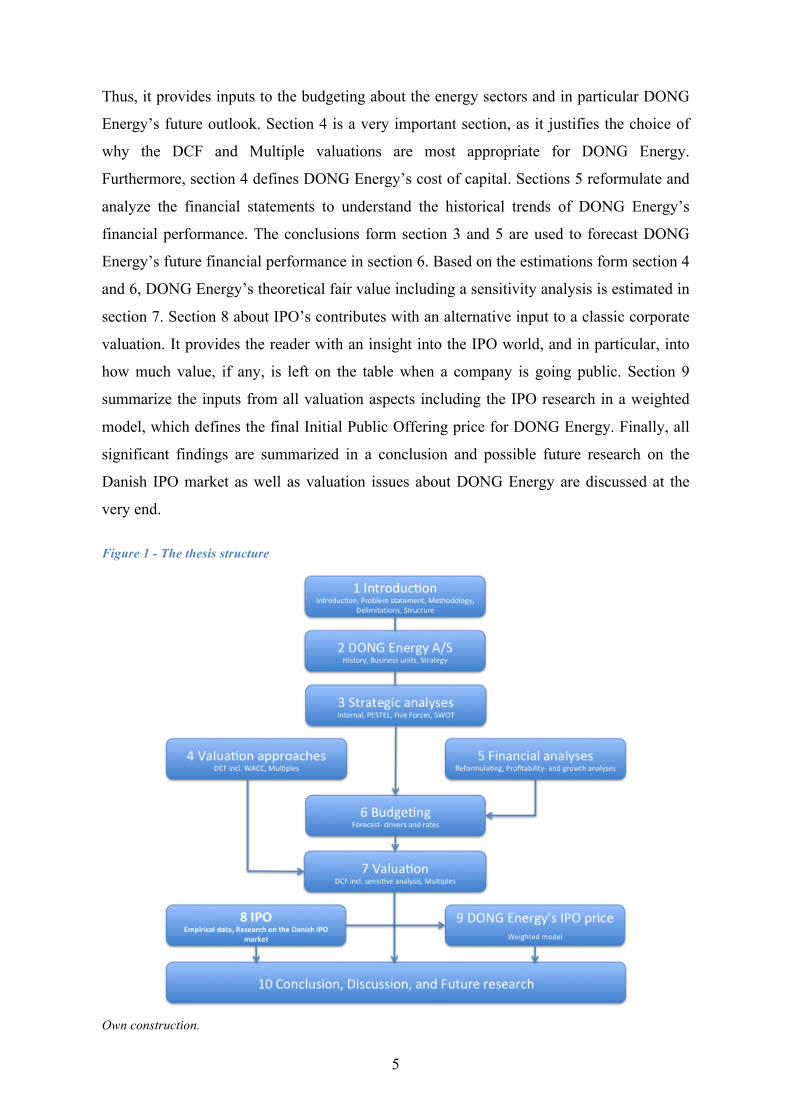

1.6 Structure An overview of the thesis structure is provided in figure 1 below. Section 1 serves the

frame for the thesis objectives. Section 2 provides the reader with the basic information

about DONG Energy including its history, business units and strategy. The strategic

analysis in section 3 elaborates on DONG Energy from an internal and external perspective.

5

Thus, it provides inputs to the budgeting about the energy sectors and in particular DONG

Energy’s future outlook. Section 4 is a very important section, as it justifies the choice of

why the DCF and Multiple valuations are most appropriate for DONG Energy.

Furthermore, section 4 defines DONG Energy’s cost of capital. Sections 5 reformulate and

analyze the financial statements to understand the historical trends of DONG Energy’s

financial performance. The conclusions form section 3 and 5 are used to forecast DONG

Energy’s future financial performance in section 6. Based on the estimations form section 4

and 6, DONG Energy’s theoretical fair value including a sensitivity analysis is estimated in

section 7. Section 8 about IPO’s contributes with an alternative input to a classic corporate

valuation. It provides the reader with an insight into the IPO world, and in particular, into

how much value, if any, is left on the table when a company is going public. Section 9

summarize the inputs from all valuation aspects including the IPO research in a weighted

model, which defines the final Initial Public Offering price for DONG Energy. Finally, all

significant findings are summarized in a conclusion and possible future research on the

Danish IPO market as well as valuation issues about DONG Energy are discussed at the

very end.

Figure 1 - The thesis structure

Own construction.

6

2 DONG ENERGY

2.1 DONG Energy at a glance The history goes back to the 27th of March 1972, where the Danish state founded Dansk

Naturgas A/S. The company was created as a vehicle to develop Danish energy activities.

In 1973 the name changed to Dansk Olie og Naturgas A/S and in 2002 it was changed to

DONG. DONG Energy A/S was established in 2006 through a merger of six Danish energy

companies; DONG, Energi E2, Elsam, Nesa, Frederiksberg Forsyning, and Københavns

Energi (DONG Energy A/S, 2014d).

The majority owner of DONG Energy is the Danish State which owns 57.3%. DONG

Energy got a DKK 13 billion equity injection in February 2014, where DKK 11 billion was

from new investors and DKK 2 billion was from existing minority-shareholders. This

equity injection reduced the majority ownership of the Danish State from 81.0% to 57.3%

and gave three new institutional investors; Goldman Sachs, ATP and PFA an ownership

share of respectively 18.0%, 4.9% and 1.8% (DONG Energy A/S, 2013b). The ownership

share of 18% in DONG Energy by Goldman Sachs was a widely discussed topic in the

Danish society during the beginning of 2014, because the Danish State is the Majority

owner. Meaning that DONG Energy is actually owned by the Danish people, who are very

skeptical about American investment banks such as Goldman Sachs. The ownership

composition before and after the equity injection is illustrated in appendix A.

Dong Energy has expanded significantly through both organic growth and several

acquisitions in Denmark and across Europe. Today, DONG Energy is one of the leading

energy groups in Northern Europe. DONG Energy is headquartered in Denmark and has

about 6.500 employees (DONG Energy A/S, 2013b). Dong Energy had revenue of DKK

73.105 billion and a net loss for the year of DKK 993 million in 2013, which was an 8.8%

increase in revenue and an improvement of 3.028 million in the net loss compared to 2012

(DONG Energy A/S, 2013b). As illustrated in appendix B, the revenue of DONG Energy

in 2013 was mainly generated in Denmark and the United Kingdom, with 47.06% and

26.65% respectively (DONG Energy A/S, 2013b). The Netherlands, Germany, Norway and

others accounts for respectively 13.53%, 8.33%, 2.55% and 1.88% of revenue in 2013

(DONG Energy A/S, 2013b).

7

DONG Energy supplies natural gas, oil, renewable energy, and electricity to customers in

Denmark, Norway, the Netherlands, the United Kingdom, Germany, France and Sweden.

DONG Energy is an integrated energy company and engaged in the exploration and

production of oil and gas, power generation, gas distribution, and wholesale energy

(MarketLine, 2013). DONG Energy’s operations can be divided into four different business

segments; Exploration & Production, Wind Power, Thermal Power, and Customers &

Markets.

Exploration & Production explores and produces oil and natural gas, which means they are

engaged in the upstream part of the oil sector. The activities of the Exploration &

Production business segment are focused on seas surrounding Denmark, Norway, the

United Kingdom, the Faroe Islands, and Greenland. Exploration & Production produced

approximately 87,000 BOE1 per day in 2013 and the target production by 2020 is 150,000

BOE per day (DONG Energy A/S, 2013b). In 2013, 15% of DONG Energy’s total revenue

came from this business segment.

The Wind Power business segment of DONG Energy has over 20 years experience within

offshore wind farm development and is a market leader in offshore wind power, having

built 35% of European offshore windmill capacity. Wind Power develops, constructs, and

operates wind farms in Denmark, France, Norway, and Sweden, as well as the UK and

Germany which are the largest growth markets (DONG Energy A/S, 2014b). Wind Power

work with all aspects of developing and constructing a wind farm, except actual production

of windmills, which includes the steps from early development to the construction phase

and operating and maintenance of the wind farms. Wind Power has developed and

constructed the largest portfolio of offshore wind farms in Northern Europe, which are

mainly located in the seas around Denmark, Germany and United Kingdom. Wind Power

has installed an offshore wind capacity of 2.1 GW in 2013 (DONG Energy A/S, 2013b) and

has a target of installed offshore wind capacity reaching 6.5 GW by 2020. In 2013, 14% of

DONG Energy’s total revenue came from this business segment (DONG Energy A/S,

2014a).

The Thermal Power business segment focuses on providing stable electricity and heat

production, while reducing the CO2 emissions in energy production. Most of Thermal

Power’s power stations combine production of electricity and heat. Thermal Power has

1!Barrels!of!Oil!Equivalent.!!

8

focus on optimizing the current thermal-based production, but also increasing the use of

CO2-neutral biomass. Thermal Power has nine central power stations and one waste-to-

energy plant in Denmark and one gas-fired power station in the Netherlands. Thermal

Power has a target of over 50% of electricity and heat generation in Denmark coming from

biomass by 2020 (DONG Energy A/S, 2013b). The Thermal Power business segment is the

smallest of the four business segments measured by revenue, with only 12% of total

revenue coming from this business segment in 2013 (DONG Energy A/S, 2014a).

Customers & Markets handles DONG Energy’s customer and market-related activities

within trading, distribution and sale of electricity and natural gas to the Northern European

markets. Customers & Markets is responsible for buying and selling electricity and gas to

wholesale, business and residential customers in Denmark, Germany, the United Kingdom,

the Netherlands, and Sweden. Customers & Markets is a leading Danish distributor of

electricity and gas with market shares of 26% and 28% respectively. One of the targets of

Customers & Markets is to quadruple energy saving by their Danish customers by 2020.

The Customers & Markets business segment is by far the largest of the four business

segments measured by revenue, with 59% of total revenue coming from this business

segment in 2013 (DONG Energy A/S, 2014a).

The equity injection of DKK 13bn in Dong Energy from Goldman Sachs, ATP and PFA

has happened in an agreement between the shareholders of DONG Energy to seek an Initial

Public Offering (IPO) of DONG Energy, when the timing and market conditions are right.

The Danish State will remain majority shareholders in a potential future IPO which is

completely in line with a political agreement by a majority of the Danish Parliament

(DONG Energy A/S, 2013a). If an IPO of DONG Energy has not been completed

following the presentation of the 2017 annual financial statements, the new investors

(Goldman Sachs, ATP and PFA) has the option to sell their shares back to the Danish State

on pre-agreed terms (DONG Energy A/S, 2013d). This agreement means that DONG

Energy will seek to go public before the beginning of 2018, where the financial statements

for the year 2017 are presented. The IPO will happen when shareholders agree that the

timing and market conditions are right and with the current rally in the equity markets, the

IPO might not be in too a distant future. This thesis will analyze what the correct valuation

of DONG Energy is, if DONG Energy were to complete an IPO primo 2014.

9

3 STRATEGIC ANALYSIS OF DONG ENERGY The purpose of this strategic analysis is to keep DONG Energy’s strategic objectives up

against their resources and competences as well as the opportunities in the external

environment. The strategic analysis will together with the financial analysis in section 5

form the basis for the budgeting and thereby create value for the valuation of DONG

Energy. The analysis will not elaborate on the theories, but rather focus on the output form

the analyses tools applied. The strategic analysis will consist of an internal analysis, an

industry analysis, and a macro-environment analysis, which will be summarized in a

SWOT analysis in the end of this section.

3.1 internal analysis of DONG Energy The purpose of this internal analysis of DONG Energy is to provide a basic understanding

about the resources and competences held by DONG Energy, and whether these resources

and competences create sustainable competitive advantages. This internal analysis will

focus on how DONG Energy as a company creates value through its business activities.

However, instead of using the classic Value Chain framework developed by Michael Porter

back in 1985 step by step, this analysis only focuses on the value drivers in DONG Energy

that create value for the valuation part of this thesis. Thus, this analysis will be on a

corporate level and not on a business level, which could have been justified as each

business unit do have its own value chain.

3.1.1 A well diversified and integrated business model

In the description of DONG Energy it was mentioned that DONG Energy holds an

integrated business model. Thus, DONG Energy creates value in all stages of the energy

value chain, as they are active within exploration and production of oil and gas, power

generation, gas and el distribution, and wholesale of energy. This integrated and well

diversified business model has a stabilizing effect on DONG Energy’s cash flows and

overall risk profile, resulting in competitive advantage against less diversified peers in the

sector (MarketLine, 2013).

Exploration!&!Production!of!oil!and!gas!

Power!generation!

Energy!distribution!

Wholeslae!of!energy!

10

3.1.2 High expertise in offshore wind power projects

Currently, DONG energy is one of the world’s leading players in the offshore wind power

sector, where they develops, construct, and operates wind farms in Denmark, France,

Norway, Sweden, Germany, and UK (DONG Energy A/S, 2013b). DONG Energy has built

38% of the European offshore wind capacity and with more than 20 years of experience

within the offshore wind power sector, DONG Energy holds unique knowledge and skills

about all aspects of offshore wind projects (DONG Energy A/S, 2014b). Thus, DONG

Energy has a strong position in a growing market. In 2013 45% of DONG Energy’s gross

investment were invested in offshore wind and a strong pipeline of projects are lined up for

the future (DONG Energy A/S, 2013b). However, DONG Energy’s strong position and a

global focus towards more clean energy, it is still a challenge to make wind power

competitive to other energy sources. Therefor DONG Energy needs to focus on bringing

down the cost through technical developments and overall optimizations of processes.

DONG Energy’s goal is to bring the cost of electricity from offshore below 100 €/MWh. by

2020. If DONG Energy manages to bring down the costs on offshore wind energy, they are

expected to take an even stronger position in the market.

The business unit Wind Power uses a unique partnership model that attracts large

institutional and private investors. The model enables long-term investments in offshore

wind farms, where DONG Energy share cost and earning with the partners (DONG Energy

A/S, 2014b). Hence, it is possible to expand the capital base and at the same time spread the

risk of invested capital. The Wind Power business unit is currently performing a return on

capital employed (ROCE) of 4.6%, but based on DONG Energy’s competences and heavily

investments, as well as a political focus on clean energy, DONG Energy expects a return on

capital employed ROCE of 12-14% in 2020 (DONG Energy A/S, 2013b). The Wind Power

is considered to deliver relative stable income and will in the future contribute more and

positively to DONG Energy’s financial performance.

3.1.3 Leading and innovative company in the transformation of the energy system

DONG Energy wants to lead on in the transformation of the energy system towards

benefitting its stakeholders, including the environment by converting the strongest

technological breakthroughs to value-creating business models, products, services, and

systems (DONG Energy A/S, 2014e). Open innovation through strategic partnerships with

inter alia, Copenhagen University, Technical University of Denmark (DTU), related

companies, suppliers, and costumers, is one-way, DONG Energy tries to stand out and be

11

on top with the development in sustainable energy. With the establishment of Inbicon, the

world’s largest demonstration plant of second-generation bioethanol, DONG Energy is in a

strong position for the future bioethanol market. Furthermore, DONG Energy has filed a

number of patents in the bioethanol industry (DONG Energy A/S, 2014e), providing basis

for creating competitive advantages and hence the possibility for high margins.

3.1.4 Conclusion on the internal analysis

Technology is essential in all aspects of transforming the energy system. DONG Energy

invests heavily in new technologies and is well positioned in their markets, particular

within the offshore wind market, where DONG Energy is a world-leading player. Flexible

and effective production facilities are how DONG Energy will compete in the global

energy market.

In regard to the valuation of DONG Energy, this internal analysis will be used in the

budgeting process, as it provides an understating of DONG Energy’s value creating

activities. However, it does not give specific input data for the budgeting. These inputs will

instead be based on DONG Energy’s own and the market expectations.

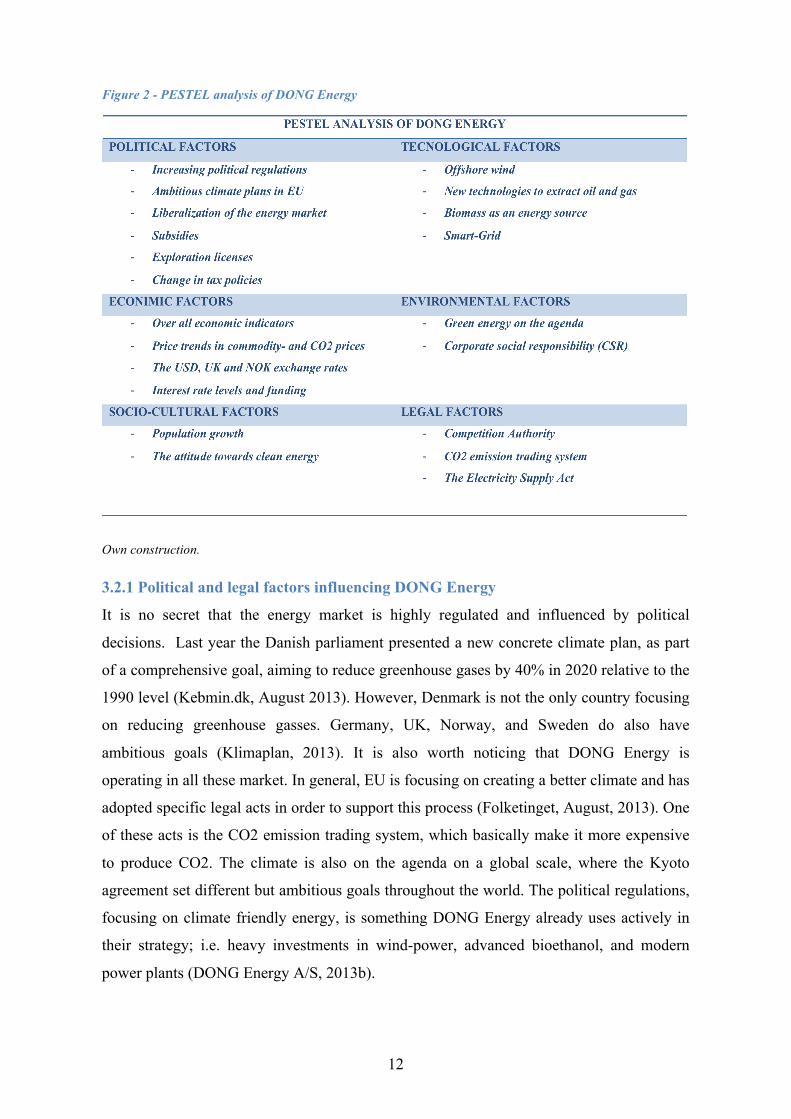

3.2 PESTEL analysis of DONG Energy

The purpose of the PESTEL analysis is to examine the most significant macro-environment

aspects, influencing DONG Energy. The PESTEL analysis distinguishes to some extent

between DONG Energy’s different business units and markets as each business unit and

market is exposed to specific external opportunities and risks. However, the Danish market

is considered as the main market and thus the main interest for this thesis. In general the

external environment is important to consider in order to make the right strategic decisions;

i.e. which markets and business units to focus on, and invest in.

12

Figure 2 - PESTEL analysis of DONG Energy

Own construction.

3.2.1 Political and legal factors influencing DONG Energy

It is no secret that the energy market is highly regulated and influenced by political

decisions. Last year the Danish parliament presented a new concrete climate plan, as part

of a comprehensive goal, aiming to reduce greenhouse gases by 40% in 2020 relative to the

1990 level (Kebmin.dk, August 2013). However, Denmark is not the only country focusing

on reducing greenhouse gasses. Germany, UK, Norway, and Sweden do also have

ambitious goals (Klimaplan, 2013). It is also worth noticing that DONG Energy is

operating in all these market. In general, EU is focusing on creating a better climate and has

adopted specific legal acts in order to support this process (Folketinget, August, 2013). One

of these acts is the CO2 emission trading system, which basically make it more expensive

to produce CO2. The climate is also on the agenda on a global scale, where the Kyoto

agreement set different but ambitious goals throughout the world. The political regulations,

focusing on climate friendly energy, is something DONG Energy already uses actively in

their strategy; i.e. heavy investments in wind-power, advanced bioethanol, and modern

power plants (DONG Energy A/S, 2013b).

13

In regard to DONG Energy’s business activities, political decisions about subsidies, tax

policies and exploration licenses are of important character in order to sustain competitive.

Without subsidies and taxes, wind-power and other renewables cannot compete with other

energy sources in the current market and without exploration licenses, DONG Energy’s

resources are limited (DONG Energy A/S, 2013b). Subsidies are partly finance through

Public service obligations (PSO), a public tariff imposed on consumers.

A merger of six companies founded DONG Energy back in 2006. At that time the

European Competition Authority approved the merger conditional. A divestment in a gas

field was one of the conditions required in order to complete the merger. EU and Denmark

in particular have taken steps towards a more liberalized energy market. Since 2003, the

European energy market has been considered a free market, as consumers have free

supplier choice (Energistyrelsen, 2013a). Furthermore, Dong Energy’s activities in

Denmark are regulated by the Electricity Supply Act, which aims to ensure that the

country's electricity supply is planned and implemented in accordance with the interests of

security, economy, environment, and consumer protection (lov om elforsyning, 2013).

Thus, prices and customer services are considered as important competitive parameters in

the energy market.

3.2.2 Economic factors influencing DONG Energy

In general, every sector is affected by the development in the overall economy in one-way

or another, as it influence the demand after goods and services. The energy sector is no

exception, however, it is not that sensitive to volatility in the over all economic conditions,

as energy is indispensable in the modern society (DONG Energy A/S, 2013b).

Figure 3 - GCP, CO2, and gross energy consumption in the Danish market

Own construction based on numbers from Energistyrelsen.dk

14

Despite an increased GDP, Figure 3 documents that the actual energy consumption in the

Danish market has been very stabile throughout the period from 1990. This is possible due

to a better utilization of the energy produced, and thus a lower CO2 emission, which can be

linked to the political initiatives stated above. Due to all the political actions and

regulations in the energy market, the trend of better energy utilization is expected to

continue going forward. Thus, DONG Energy, and other companies in the energy sector

have to transform their production to rely more on climate friendly energy sources.

Furthermore, the climate protection trend opens up an opportunity within the energy

consulting business.

Oil, gas, coal and, el are important sources in the energy sector, and fluctuations in prices

affect the profitability across the different energy sources. The prices are determined by

supply and demand and figure 4 illustrates how volatile selected commodity prices have

been historical.

Figure 4 - Historical development in selected commodity prices

Own construction based on numbers from Eurostat and DataStream. DONG Energy’s business unit Exploration & Production is highly exposed to the

development in especially oil and gas prices. Because of the high uncertainty about future

energy prices the price imbalance between sales and procurement present a risk, as

purchase contacts are negotiated for longer time periods (DONG, 2013). To reduce market

price risk and fluctuations in cash flows, DONG Energy applies hedging instruments

(DONG, 2013). However, DONG Energy’s 2020 strategy transform their risk profile and

strives to reduce the exposure to variation in market prices. Already by 2016, DONG

Energy expects to reduce their electricity generation from power stations and wind farms

sold at market prices to below 10%. In comparison, 2/3 of the electricity generation was

sold at market prices in 2007 (Dong, 2013). On the other hand, DONG Energy expects to

15

increase the proportion of electricity generation settled at fixed prices from 10% in 2007 to

about 60 % in 2016 (DONG, 2013).

In general, variation in exchange rates effects an international company. The currencies of

principal to DONG Energy are GBP, USD and NOK. However, DONG Energy does apply

hedging instrument to reduce their exposure to variation in exchange rates to a minimum.

At the end of 2013 DONG Energy was exposed to GBP, USD and NOK by respectively 0.4

billion, 2.6 billion and 0 billion (DONG, 2013).

3.2.3 Socio-cultural factors influencing DONG Energy

Today, the world population have exceeded 7.2 billion people and are expected to reach 8

billion in the spring of 2024 (Worldometers, 2014). Thus, the demand for energy will

increase going forward. Furthermore, Energy is something affecting the day-to-day life for

almost everybody in the modern society. Without energy, people would not be able to turn

on their TV, heat up their houses, or fill up their car with fuel. Even though most of the

population growth is outside EU, the trend of people depending more and more of energy

will still affect DONG Energy positively. To meet the future demand, DONG Energy is

investing in new energy solutions which can compete with traditional energy sources such

as coal, oil, and gas (DONG Energy A/S, 2013b).

Coal, oil, and gas are to some extent limited, and currently 75% of the EU energy comes

from coal, oil, and gas. Additional, two thirds of the fossil fuels in EU are imported

(DONG Energy A/S, 2013c). Therefore alternative energy sources are needed in the future.

DONG Energy has started a journey involving a transition to more renewable energy with

less impact on the environment (DONG Energy A/S, 2013c). This is a clear indication that

the energy sources will change in the years to come.

Today, renewable energy accounts for 11% of EU's energy consumption and is expected to

have a value of $252.3 billion in 2017, compared to a value of $170.4 billion in 2012

(MarketLIne, July 2013,). Thus, the trend is going towards more clean energy in the

European market. As a significant player in the renewable energy market DONG Energy is

well positioned to take a share in the coming development, which may have a positive

effect on DONG Energy’s growth outlook.

16

3.2.4 Technological factors influencing DONG Energy

Technology is a key factor in the process of achieving the ambitious goals set by politicians

around the world. The current situation in the European energy market is that many power

stations are old and will be decommissioned in the next couple of decades (DONG Energy

A/S, 2013c). Thus, more modern and more efficient ones will replace these power stations.

Furthermore, the oil and gas production in EU is declining, and that makes EU a net

importer of oil and gas (DONG Energy A/S, 2013c). Therefore new technologies are

required to make EU less dependent on oil and gas, as well as make the energy production

more sustainable.

One way to become less dependent on oil and gas while, at the same time care more about

the environment is wind power and offshore wind power, in particular. In theory, the

potential of offshore wind will be able to supply 80% of the EU with electricity in 2030

(DONG Energy A/S, 2013c). Currently, DONG Energy has installed offshore wind farms

with the capacity to supply 5 million Europeans. However, a focus on innovation together

with continuing investments will increase DONG Energy’s offshore wind capacity to

supply 15 million by 2020 (DONG Energy A/S, 2013c).

Another alternative to fossil fuels, which have been available through technological

breakthroughs, is biomass (DONG Energy A/S, 2013c). Biomass energy is greener than

fossil fuels and more stabile than wind and solar power (DONG Energy A/S, 2013c).

Even though wind power and other renewable energy sources look more and more as the

answer to the future electricity production sources, oil and gas are still important energy

sources in the modern society. Actually, oil and gas are estimated to account for 53% of

EU’s energy consumption in 2035 (DONG Energy A/S, 2013c). Thus, it is important

continuously to develop new technologies to discover and extract oil and gas in the

underground. The development for extracting shale gas is an excellent example of how a

new technology can change the supply, and thus the prices in a market (Team Trefis,

February 2014).

One challenge with wind power is that it is not possible, or at least very expensive, to store

the produced energy. However, an intelligent energy system, named Smart grid, will make

the energy system more flexible; i.e. an integrating of the production, transmission,

distribution, and management of consumption. An important condition to make Smart grid

a reality is remote reading of electricity meters and hourly settlement. Hence, making

17

energy consumers able to react on price signals and take advantage of the opportunities to

move their energy consumption. The Danish parliament agreed in 2013 on establishment of

this technology remote reading of electricity meters and hourly settlement all over Denmark

by the end of 2020 (Energistyrelsen, 2013b).

3.2.5 Environmental factors influencing DONG Energy

DONG Energy has a central role in the transformation towards a greener society. As an

energy provider, DONG Energy carries a large responsibility in the process of reducing

CO2 emissions. DONG Energy has already undertaken its social responsibility by focusing

on renewing energy for society, supplying energy at competitive prices and producing

cleaner energy, such as offshore wind power and biomass energy (DONG Energy A/S,

2013c).

In general, the environment and society are top priorities in the way DONG Energy do

business. However, if DONG Energy is not able to secure a sound return for its owners,

they cannot maintain business in the long term. In the report DONG Energy in society,

DONG Energy does officially work with the concept corporate social responsibility, which

is a balanced approach for organizations to address economic, social, and environmental

issues in a way that aims to benefit people, communities, and society (Leonard & McAdam,

2003).

DONG Energy is not the only company focusing on corporate social responsibility (CSR).

Organizations continuously demonstrate increased commitment to CSR, as they consider it

necessary to define their role in society in order to create value to its stakeholders

(Lindgreen & Swaen, 2010). One part of CSR is the environment, which, among others,

does involve energy. DONG Energy provides advisory service on how in particular large

corporation can reduce energy consumption for the benefit of both the environment and

their competitive advantages. Currently, DONG Energy has entered into over 135 climate

partnership agreements (DONG Energy A/S, 2014c)

3.2.6 Conclusion on the PESTEL analysis

One of the most important macro-environmental factors to DONG Energy is the global

focus on clean energy. In the coming period, political subsidies and regulation are of

important character to make clean energy competitive, in particular offshore wind. At some

point in the future, new technologies and a socio-cultural attitude towards clean energy,

will contribute to make clean energy both competitive and attractive. Thus, contribute to

18

make the world less dependent on fossil energy sources. However, DONG Energy is not

just offshore wind power, and is thus also affected by other factors than a global focus on

clean energy. A large proportion of the revenue in DONG Energy is directly, or indirectly

linked to the development in the commodity prices: oil, gas, el, and coal. The profitability

in the business unit Exploration & Production is in particular affected by the oil and gas

prices. Thus, DONG Energy needs a risk management strategy in order to mange these cash

flows.

3.3 Porters five forces analysis of DONG Energy Porters Five Forces was developed by Professor Michael Porter in 1979 and has shaped a

generation of research within competitive strategy (Porter, 2008). The target of Porters Five

Forces is to determine the long-run profitability of the industry that DONG Energy operates

in, since a company’s profitability is mainly determined by the attractiveness of the

industry in which it operates (Porter, 2008). Porter’s Five Forces is used to analyze the

competitive intensity and attractiveness of the industry, where the attractiveness of an

industry is given by the overall profitability in the industry. Porter’s five forces is a

framework to analyze the underlying structure of the industry and the analysis is conducted

by examining the following five forces; Rivalry among existing competitors, bargaining

power of buyers, bargaining power of suppliers, threat of substitute products, and services,

threat of new entrants (Porter, 2008). For each of the five forces there will be made an

analysis on several parameters, which will characterize the degree of the force being high

or low. The scale will be from 1 to 5, where one is low and five is high. The average score

is assessed as low from 1-2.5; medium-low from 2.5-2.8, medium between 2.8-3.2,

medium-high from 3.2-3.5 and high above 3.5.

Understanding the competitive forces and their underlying causes provides a framework for

anticipating and influencing the competition and profitability of the industry over time

(Porter, 2008). Understanding the underlying structure of the industry is therefore essential

for creating an effective corporate strategy. The analysis will focus on the five forces in

relation to the operations of DONG Energy and will create a foundation for assessing the

future profitability of DONG Energy, by identifying the competitive situation and

attractiveness in the industry, in which DONG Energy operates. This is essential

information, when performing a valuation of DONG Energy, since it allow us to make

better estimates for the future growth and profitability potential of DONG Energy’s

different business segments. The five forces will be analyzed in relation to DONG Energy’s

19

four business segments: Exploration & Production, Wind Power, Thermal Power and

Customers & Markets. Only the conclusions of the analysis will be presenter here. For a

detailed analysis about the five see appendix C.

3.3.1 Conclusion on porters five forces Figure 5 - Conclusion on Porters Five Forces

Own construction.

The competitive situation in the industries, in which DONG Energy operates, are assessed

to be medium-high with an average score of 3.32. The rivalry among existing competitors

is especially high, because of high entry and exit barriers, together with high fixed costs

and the lack of differentiation in the industry. The threat from substitute products or

services are also high, mainly due to the increased focus on sustainable renewable energy

and the risk of substituting energy from oil, gas, or thermal power with renewable sources

as wind, solar, biomass, rain, water, or geothermal energy. DONG Energy is only involved

in renewable energy from wind power and a bit from biomass, which can be substituted

from other renewable sources. Furthermore, shale gas is also a threat. If shale gas is starting

to be extracted in Europe, then it can substitute other fossil fuels and potential make energy

prices decline significantly, as it happened in the US.

Bargaining power of buyers is quite strong, which is mainly driven by the liberalization of

the European energy market. Buyers are strongly independent of suppliers, since there are

many suppliers delivering the same standardized product. Furthermore, the liberalization

has made it easy and cheap to switch between suppliers and increased the bargaining power

of buyers.

3.25

3.30

2.60

3.55

3.90

0

1

2

3

4

5Bargaining0power0of0buyers

Bargaining0power0of0suppliers

Threat0of0new0entrantsThreat0of0substitute0products0or0services

Rivalry0among0existing0competitors

20

Bargaining power of suppliers is assessed to be medium-high. The suppliers have

significant size and financial muscle, which increased bargaining power of suppliers. On

the other hand there are several large suppliers, which increase the buyers’ independence of

each supplier. The agreements negotiated in this industry are of very large amounts and

therefore the contract has to be very comprehensive, which makes it expensive and difficult

to switch suppliers and further increases the bargaining power of suppliers. The threats

from new entrants are low, mainly because of high barriers to entry, regulations,

importance of economics of scale and non-abnormal profitability.

From this analysis it can be concluded that the competition in the industries in which

DONG energy operates, will be rather strong in the future, especially due to increased focus

on renewable energy. The growth of the oil and gas industry and the electricity industry is

forecasted to be modest in the future, while the offshore wind power industry is forecasted

to have significant growth, as discussed in threat of new entrants. The overall profitability

in the industries was currently assessed to be normal and with the increased competition

going forward, it is not expected to reach abnormal levels. The overall attractiveness of the

industries, which DONG Energy operates in, are assessed to be reasonable, and not high.

This is due to strong competition, non-abnormal profitability, and only significant growth

in the wind power market. All this is considered vital information for the valuation of

DONG Energy.

3.4 SWOT analysis DONG Energy To sum up on the strategic analysis a critical SWOT analysis is applied. The purpose of this

analysis is to connect DONG Energy’s strategic goals to its internal competences and

weaknesses and to the opportunities and threats observed in the external environment.

21

Figure 6 - SWOT analysis of DONG Energy

Own construction.

Firstly, it is worth to recall DONG Energy’s strategic goals towards 2020:

• Quadruple our installed capacity within offshore wind power to 6.5 GW and bring

down cost to 100 €/MWh.

• Double the production of oil and natural gas to 150.000 BOE/D.

• Double the share of biomass in the electricity and heat production at our Danish

power stations.

The strategic goals towards 2020 give an indication of how DONG Energy looks upon the

future in the energy market, or at least where DONG Energy wants to use its capabilities to

take advantage of the opportunities in the market. Together with the inputs form the

Internal, the PESTEL, and the Five Forces analyses; this SWOT analysis will elaborate on

how DONG Energy will achieve these goals.

3.4.1 Quadruple the installed capacity within offshore wind power

The political global focus on reducing CO2 emission along with socio-cultural preferences

towards clean energy creates great opportunities for DONG Energy, which during the last

couples of years, have invested heavily in offshore wind projects (DONG Energy A/S,

2013b). To meet the ambitious goals set by politicians a transformation of the current

energy system is needed; i.e. a transformation from high dependency on traditional energy

sources such as oil, gas, and coal into more renewable energy. Currently, about 75% of the

EU energy comes from oil, gas, while renewable energy only accounts for about 11%

(DONG Energy A/S, 2013c; MarketLIne, July 2013). The European renewable energy

22

market is a growing market and is expected to have a value of $252.3 billion in 2017

(MarketLIne, July 2013). The offshore wind power market is expected to have a value of

€10 billion in 2020 corresponding to a CAGR of 14.42%. DONG Energy wants to lead on

this transformation and the previous analyses confirm that DONG Energy has the

competences to exploit the opportunities in the market. Despite that the offshore wind

market is expected to be highly competitive, DONG Energy is expected to be a significant

player in the future offshore wind power market. A strong market position combined with

lowering the costs will have a positive effect on DONG Energy’s future financial

performance. Thus, DONG Energy’s goal about increase ROCE to between 12-14% in

2020 seems achievable.

3.4.2 Double the production of oil and natural gas to 150.000 BOE/D

It is not only within the offshore wind power that DONG Energy holds a strong market

position. DONG Energy is also one of the largest Danish players within Exploration &

Production and occupies significant positions in Norway and UK (DONG Energy A/S,

2013b). Along with Wind Power, Exploration & Production are in focus in DONG

Energy’s 2020 strategy. In 2013 DONG Energy invested 45% of its gross investments in

Exploration & Production (DONG Energy A/S, 2013b). No matter how much DONG

Energy wants to focus on clean energy, they cannot just ignore energy sources such as oil

and gas. According to CEO Henrik Poulsen, oil and gas will be needed many years to come

in order to keep society going. Therefore, DONG Energy invests in Exploration &

Development to meet these needs (DONG Energy A/S, 2013c). The large investments in

Exploration & Production are a necessity to double the production of oil and gas, but make

it not necessarily a good investment. The risk of substituting products, such as shale gas, is

something DONG Energy must take into consideration, as it will have a significant

influence on the profitability in Exploration & Production. In recent years, unfavorable gas

contracts have affected DONG Energy’s profitability in a negative way, as DONG Energy

in the financial years 2012 and 2013 DONG Energy have reported losses of DDK 4,021

million and DKK 993 million respectively (DONG Energy A/S, 2012, 2013b). To make the

business unit Exploration & Production achieve the strategic goal about a ROCE on 20%,

Dong Energy need to focus on a high success rate of oil and gas exploration, change the

cost levels and pay close attention to the development in the oil and gas prices. The strong

market position in Denmark and the northern part of Europe with a well-developed

infrastructure is a good foundation for achieving the goal. However, the limited

geographical area can be a disadvantage to DONG Energy in the long run.

23

3.4.3 Double the share of biomass in the electricity and heat production at the Danish

power stations

Dong Energy do also invest in new technologies within biomass and have already obtained

some patents within biomass technology. Patents as well as making the electricity and

heating supply efficient and flexible are key success factors for DONG Energy in order to

achieve their goal about biomass. The liberalization of the European energy market

emphasizes the importance of being efficient and thus able to produce electricity and heat at

competitive prices. In particular because electricity and heat are very standardized products.

As part of doubling the share of biomass in electricity and heat production at the Danish

power stations, DONG Energy wants to increase the biomass share of electricity and

heating generation in Denmark to minimum 50% in 2020 (DONG Energy A/S, 2013b).

DONG Energy has high competences within biomass energy, and as biomass energy

contributes positively to a cleaner environment, it seems reasonable for DONG Energy to

include biomass energy in the future product portfolio. The biomass energy is expected to

have a positive effect on DONG Energy’s business unit Thermal Power and thus contribute

to delivering annual operating cash flows of DKK 600-800 million from Danish power

stations.

3.4.3 Additional aspects

DONG Energy is market leader in wholesale of electricity and gas in the Danish market

and occupies leading electricity and gas positions in UK, Germany and Netherland (DONG

Energy A/S, 2013b). DONG Energy does also have a central position in the Danish

Thermal Power market, where they generate around one-third of the Danish heat

consumption (DONG Energy A/S, 2013b). The strong positioning puts DONG Energy in a

favorable situation in terms of competitive advantages. However, the competition

authorities can prevent DONG Energy from increasing its market share in the Danish

market. Thus, DONG Energy can be forced to seek new markets to create growth.

3.5 Conclusion on DONG Energy’s strategic position DONG Energy has a well-balanced and integrated business model and holds many

competences in particular within the growing offshore wind market. Their strong position

gives a competitive advantage in the short to medium term. However, an attractive market

attract new enters and hence increase competition, which eventually will eliminate DONG

Energy’s competitive advantages. However, DONG Energy’s future success depends not

only on wind power. A strong position on the Danish energy market, high competences

24

within biomass energy, and promising prospects for oil and gas exploration and production,

will also contribute to DONG Energy’s future performance. A new equity injection in the

beginning of 2014 has stabilized the financial situation of DONG Energy, which had been

under pressure due to recent poor financial performance. Thus, there are good prospects for

DONG Energy to continue investing in the transformation of the energy system. However,

energy is a very standardized product and can easily be substitutes. Therefore, DONG

Energy needs to pay attention to the development of for example shale gas and be prepared

to adapt their strategy to fundamental changes in the energy sector.

4 DEFINING VALUATION APPROACHED AND THEIR

ELEMENT FOR DONG ENERGY When it comes to make a valuation many different approaches can be applied. These

approaches range from the simple to the very sophisticated and make very different

assumptions about what fundamentals that define value (Damodaran, 2012; Koller,

Goedhart, Wessels, McKinsey, & Company, 2005). Hence, the value of the same object can

vary depending on the approach applied. However, they have some common characteristics

and can be categorized which make it easier to distinguish between different approaches, in

different situations. Broadly speaking, there are three categories of approaches to valuation:

discounted cash flow valuation (DCF), relative valuation (multiples), and contingent claim

valuation (options) (Damodaran, 2012).

As no approach is superior to all others, testing more approaches up against each other can

enhance the validity of the valuation. However, not every single valuation can be applied,

and finding the right approaches must be a trade off between:

E Minimizing the costs i.e. the time use regarding creation, implementation and use of

the approach.

E Optimizing the accuracy i.e. avoid systematic mistakes in the estimation process.

Hence, the choice of valuation approaches is a weighting of each approach’s advantages

and disadvantages in the given situation. The situation considered in this thesis is the initial

public offering of DONG Energy. Thus, there are two major things to consider when it

comes to choosing the most appropriate valuation approaches for DONG Energy. Firstly,

what valuation approaches are most suitable for an IPO company? Secondly, what

valuation approaches are most suitable for a diversified energy company? Most firms

conducting an IPO in the US are young growth companies for which it can be difficult to

25

forecast future cash flows (Kim & Ritter, 1999). Hence, the DFC approach will be

associated with high uncertainty and is likely to be very imprecise. Instead it is widely

recommended in both academic and practitioner publication to use accounting numbers in

conjunction with comparable firm multiples when valuing an IPO company (Kim & Ritter,

1999). However, with the recent IPOs of OW Bunker, ISS, Matas, and Pandora, the Danish

IPO market seems different from the US; i.e., Danish IPOs are exit strategies for private

equity funds. Further, DONG Energy may be considered a large, and to some extent,

mature company for which it is possible to estimate fairly precise future cash flows. Hence,

the DCF approach will work just fine for a valuation of DONG Energy. Notice that in

regard to the comparable firm approach it is crucial that there exists a highly comparable

peer group, otherwise we are comparing apples with bananas (How, Lam, & Yeo, 2007;

Kim & Ritter, 1999).

Based on the above arguments and what models are common applied (Damodaran, 2012;

How et al., 2007; Kim & Ritter, 1999; Koller et al., 2005; Roosenboom, 2012) the DCF and

the multiple approaches are the ones found most relevant for the purpose of valuing DONG

Energy. The DCF approach will be the main body in the valuation, while the multiples

approach is used to verify the value found. Next part will provide a theoretical introduction

to the two approaches and an analysis of estimating the approaches’ elements in relation to

DONG Energy.

4.1 Discounted Cash Flow (DCF) Valuation Originally the DCF approach was designed to value straight-line investment grade bonds,

generating well-defined equal cash flows. However, the DCF approach has developed over

the years and become suitable for valuing other assets than investment grade bonds.

Actually, the DCF approach is the foundation on which all other valuation approaches are

built (Damodaran, 2012). Notice that this valuation is valuing the free cash flow to all

investors and not only equity investors. First of all, because the focus is on a corporate

valuation of DONG Energy, but also because the capital structure is embedded in the cash

flows, which make the forecasting difficult by only focusing on the equity (Koller et al.,

2005). For instance, if DONG Energy change its debt-to-equity ratio, it will change the risk

for equity holders, thus the cost of equity must be adjusted. However, the capital structure

is not a direct part of the cost of equity and can be missed in the valuation. Hence, the cash-

flow-to-equity valuation approach is not minimizing the cost or optimizing the accuracy.

Even though the DCF model is the most common used valuation model, it has its

limitations. As can be seen from the formula below, the value is highly sensitive to both the

26

estimation of the future free cash flows and the WACC. Thus, it is important to be very

careful when estimating these elements.

The basis of the DCF approach is to estimate the firm value by estimating all future free

cash flows (FCF) and discount them back to today applying a appropriate cost of capital

(WACC), reflecting the risk embedded in the cash flow estimation.

E(FCF) = expected free cash flows; WACC = weighted average cost of capital; T =

number of time periods.

4.2 The Free-Cash-Flow (FCF) Even though it might seem simple and straightforward to calculate the firm value, it is not.

Much more complex procedures take place behind the scenes. Estimating the free-cash-

flows is a multi-step procedure involving reformulating the reported financial statement

(which will be elaborated later on), analyzing the historical performance, and then finally

forecast future cash flows based on historical performance and the strategic analysis

(Damodaran, 2012; Koller et al., 2005; Penman, 2013). Forecasting one year ahead can be

complicated enough, and thus it become meaningless to forecast far into the future

(Damodaran, 2012; Koller et al., 2005; Penman, 2013). However, a company like DONG

Energy is expected to last long into the future, if not forever. Hence, the free-cash-flows far

into the future also need to be discounted back to today as they contribute to the overall

value of the company. Instead of predicting these individual year-by-year cash flows, a

perpetuity-based continuing value will be applied (Koller et al., 2005). Hence, the firm

value becomes the sum of the forecasted period, which can vary from year to year and the

continuing value.

The continuing value is calculated by the following key value driver formula

NOPLAT = net operating profit less adjusted tax; g = the long run growth rate in

NOPLAT; RONIC = the long run return on new invested capital; WACC = weighted

average cost of capital.

Firm_Valuet =E(FCFt )

(1+WACCt )t

t=1

T

∑

Firm_Valuet =FCF1

(1+WACC)+

FCF2(1+WACC)2

+...+ FCFt(1+WACC)t

+Continuing_ value(1+WACC)t

Continuing_Valuet =NOPLATt+1 1−

gRONIC

"

#$

%

&'

WACC − g

27

4.3 The Weighted Average Cost of Capital (WACC) The other important element in estimating the firm value of DONG Energy is the Weighted

Average Cost of Capital (WACC).

D = market value of debt; E = market value of equity; D+E = market value of the firm; rd

= required return on debt; re = required return on equity; Tm = marginal tax rate.

As can be seen from the formula, the WACC consist of four elements, which here will be

dealt with in relation to DONG Energy.

4.3.1 The capital structure

First the long-term capital structure has to be estimated. The market value weights for each

financing element are better estimates, because market values reflect the true economic

claim of each type of financing outstanding (Damodaran, 2012; Koller et al., 2005).