a comparison between brazilian cotton and alternative ... comparison between brazilian cotton and...

TRANSCRIPT

A Comparison Between Brazilian Cotton

and Alternative Origins

(from a spinning mill point of view)

Leon Piçon

Orta Anadolu

Cotton Purchasing Director

Overview

• A Brief Introduction of Orta

• Turkey - Cotton Market and Trade

• Brazilian Cotton (Quality Analysis and Performance)

• Quality of Cotton and it’s Impact on Orta Spinning&Weaving Process

• Comparison of Brazilian Cotton with Alternative Origins

Facts & Figures

• Established in 1953 as an affiliate of Karamanci Holding.

• Based in Turkey and Bahrain.

• An integrated facility consists of spinning, dyeing, weaving and finishing

processes.

• 65 million meters finished denim fabric.

• 700 different products.

• Ships to 40 different destinations.

• 9 showrooms worldwide:

•USA (2), Colombia, Italy, Belgium, Netherlands, Bangladesh, Hong

Kong, China.

• 6 offices worldwide:

• USA, UK, Spain, Germany, Tunsia, Australia.

TurkeyCotton Market & Trade

TURKISH COTTON MARKET & TRADE

Facts & Figures

Turkish Cotton

• 95% Irrigated.

• 100 % GMO Free Seed.

• 75% Machine Picked, 25 % Hand Picked.

• 90% Roller Ginned.

Planted area (Ha)

Production (MT)

Consumption (MT)

Imports (MT)

Yield (kgs/Ha)

2015/16 Season 380.000 610.000 1.393.000 806.000 1.604

Global Share 1,20% 2,51% 5,59% 10,87%

Global Ranking #12 #7 #4 #4 #3

COTTON PLANTINGS IN TURKEY

Cotton planted area lower and unstable

• High production costs.

• Better returns from alternative crops.

• No import tarrif. Domestic cotton prices

exposed to global cotton prices.

• Quality standards suitable for export markets

not available. Practically no export.

• Attaining the size of planted area last seen in

2007 unlikely.

0

200.000

400.000

600.000

800.000

Turkish Cotton Planted Acreage (Ha)

Acreage (Ha)

Source : USDA

COTTON IMPORTS INTO TURKEY

Uptrend in Cotton Imports

• Spinning capacity and domestic cotton

consumption continues to grow.

• Smaller crops, increased imports.

• Domestic cotton production unable to saturate

demand.

• High quality (contamination free) Turkish

cotton not available.

• Trading based on spot transactions, no futures

markets and risk management instruments to be

applied for domestic cotton market.

0

100.000

200.000

300.000

400.000

500.000

600.000

700.000

800.000

900.000

1.000.000

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Me

tric

to

ns

Turkey's Cotton Imports

Source : Turkish Ministry of Economy

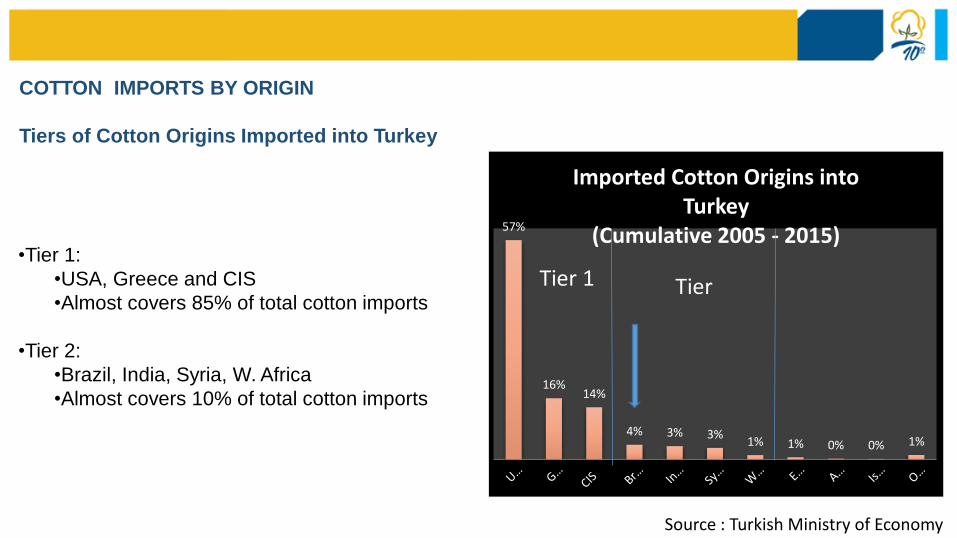

COTTON IMPORTS BY ORIGIN

Tiers of Cotton Origins Imported into Turkey

•Tier 1:

•USA, Greece and CIS

•Almost covers 85% of total cotton imports

•Tier 2:

•Brazil, India, Syria, W. Africa

•Almost covers 10% of total cotton imports

57%

16%14%

4% 3% 3%1% 1% 0% 0% 1%

Imported Cotton Origins into Turkey

(Cumulative 2005 - 2015)

Tier 1 Tier

Source : Turkish Ministry of Economy

COTTON IMPORTS BY ORIGIN

Tier 1 (USA, Greece and CIS)

•USA by far holds the bigest share of imported

cotton market into Turkey .

•Greece and Turkmenistan follow USA and

competing for the 2nd bigest market share.

0

100.000

200.000

300.000

400.000

500.000

600.000

700.000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Turkish Cotton Import OriginsTier 1

(Metric tons)

USA Greece CIS

Source : Turkish Ministry of Economy

COTTON IMPORTS BY ORIGIN

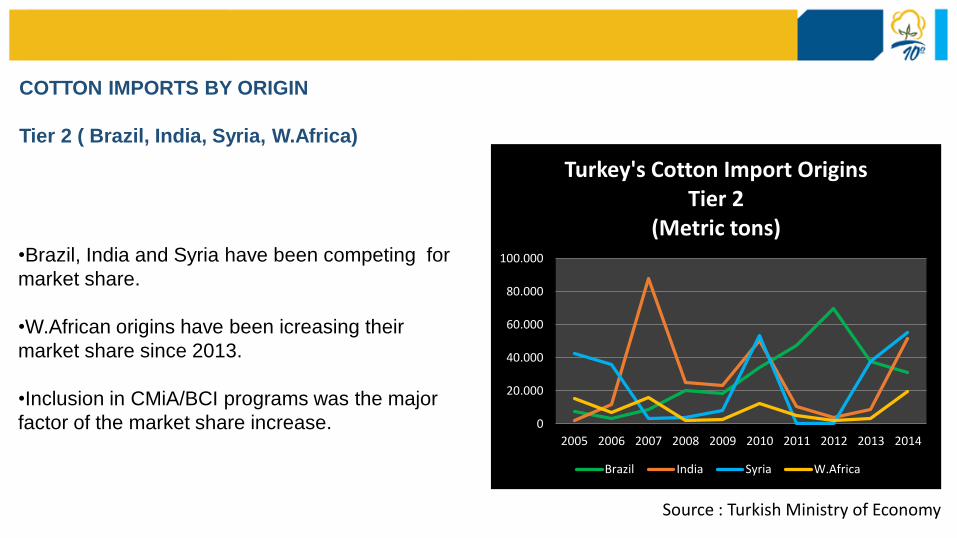

Tier 2 ( Brazil, India, Syria, W.Africa)

•Brazil, India and Syria have been competing for

market share.

•W.African origins have been icreasing their

market share since 2013.

•Inclusion in CMiA/BCI programs was the major

factor of the market share increase. 0

20.000

40.000

60.000

80.000

100.000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Turkey's Cotton Import OriginsTier 2

(Metric tons)

Brazil India Syria W.Africa

Source : Turkish Ministry of Economy

COTTON IMPORT ORIGINS

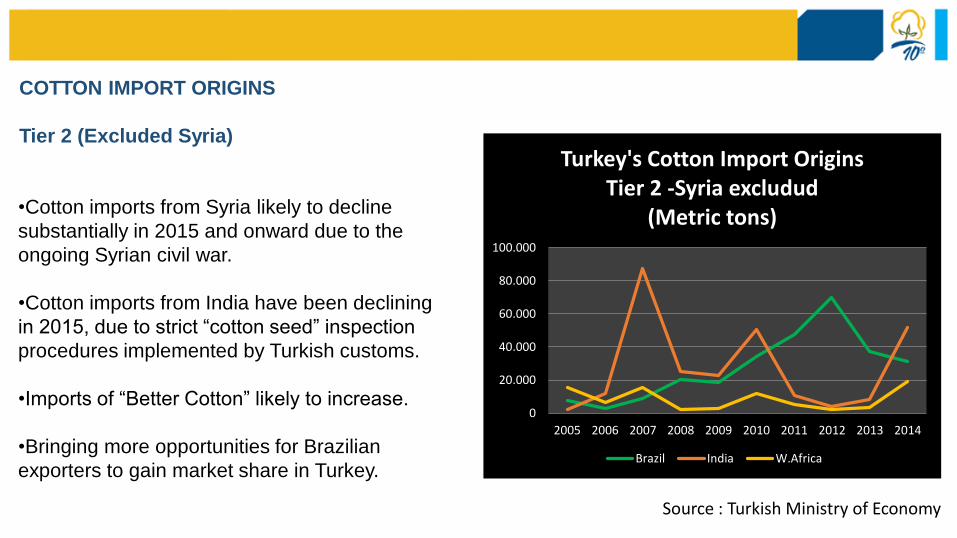

Tier 2 (Excluded Syria)

•Cotton imports from Syria likely to decline

substantially in 2015 and onward due to the

ongoing Syrian civil war.

•Cotton imports from India have been declining

in 2015, due to strict “cotton seed” inspection

procedures implemented by Turkish customs.

•Imports of “Better Cotton” likely to increase.

•Bringing more opportunities for Brazilian

exporters to gain market share in Turkey.

0

20.000

40.000

60.000

80.000

100.000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Turkey's Cotton Import OriginsTier 2 -Syria excludud

(Metric tons)

Brazil India W.Africa

Source : Turkish Ministry of Economy

BETTER COTTON SUPPLY CHAINS

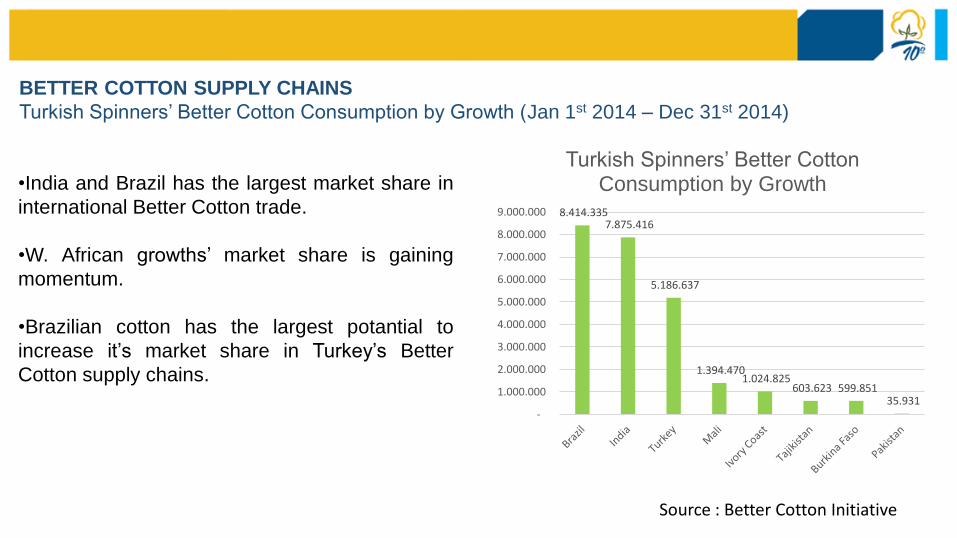

Turkish Spinners’ Better Cotton Consumption by Growth (Jan 1st 2014 – Dec 31st 2014)

•India and Brazil has the largest market share in

international Better Cotton trade.

•W. African growths’ market share is gaining

momentum.

•Brazilian cotton has the largest potantial to

increase it’s market share in Turkey’s Better

Cotton supply chains.

8.414.335 7.875.416

5.186.637

1.394.470 1.024.825

603.623 599.851 35.931

-

1.000.000

2.000.000

3.000.000

4.000.000

5.000.000

6.000.000

7.000.000

8.000.000

9.000.000

Turkish Spinners’ Better Cotton Consumption by Growth

Source : Better Cotton Initiative

BRAZILIAN COTTON IMPORTS INTO TURKEY

•Imports from Brazil have been steadily

increasing between 2005 - 2012.

•Brazilian cotton imports picked in 2012, and

steadily declined since than.

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Brazilian Cotton Imports into Turkey

Brazilian Cotton Imports (Tons)

Source : Turkish Ministry of Economy

Brazilian Cotton

(Quality Analysis and Performance)

27

28

29

30

2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15

Brazilian CottonStaple

Roda Velha Sapezal

3,00

3,50

4,00

4,50

2008/092009/102010/112011/122012/132013/142014/15

Brazilian CottonMicronaire

Roda Velha Sapezal

BRAZILIAN COTTON

Staple & Micronaire (2008 – 2014)

Source: Kuhlmann Surveyors & Consultants

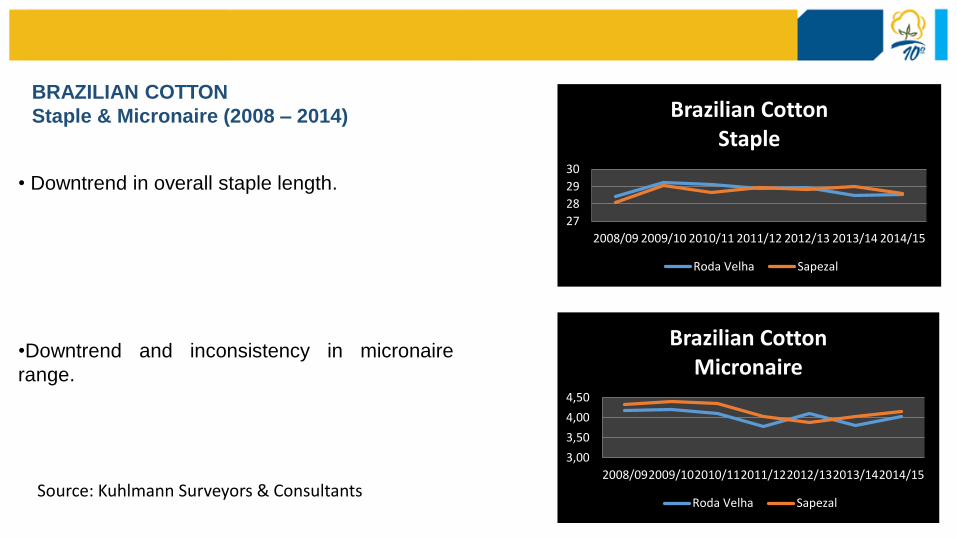

• Downtrend in overall staple length.

•Downtrend and inconsistency in micronaire

range.

80

82

84

2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15

Brazilian CottonUniformity

Roda Velha Sapezal

8

9

10

2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15

Brazilian CottonShort Fiber Content

Roda Velha Sapezal

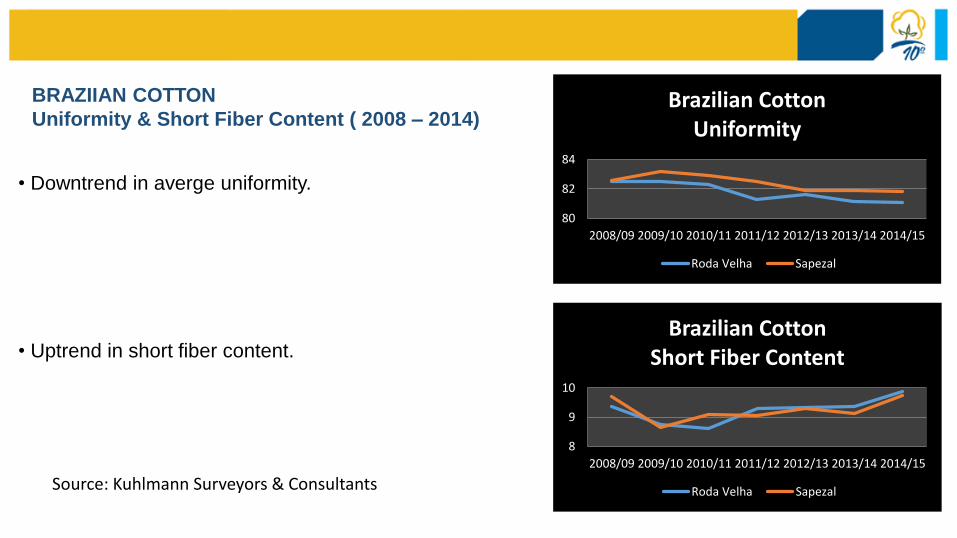

BRAZIIAN COTTON

Uniformity & Short Fiber Content ( 2008 – 2014)

Source: Kuhlmann Surveyors & Consultants

• Downtrend in averge uniformity.

• Uptrend in short fiber content.

Quality of Cotton

and

The Impact on Orta

Spinning & Weaving Efficiency

FLOW CHART OF DENIM PRODUCTION

Critical Stages Affected by Quality Parameters of Cotton

SpinningBall

WarpingRope Dying

Long Chain Beaming

Sizing Weaving Finishing

Unf&

sfc All

Mic

Unf&

sfc All

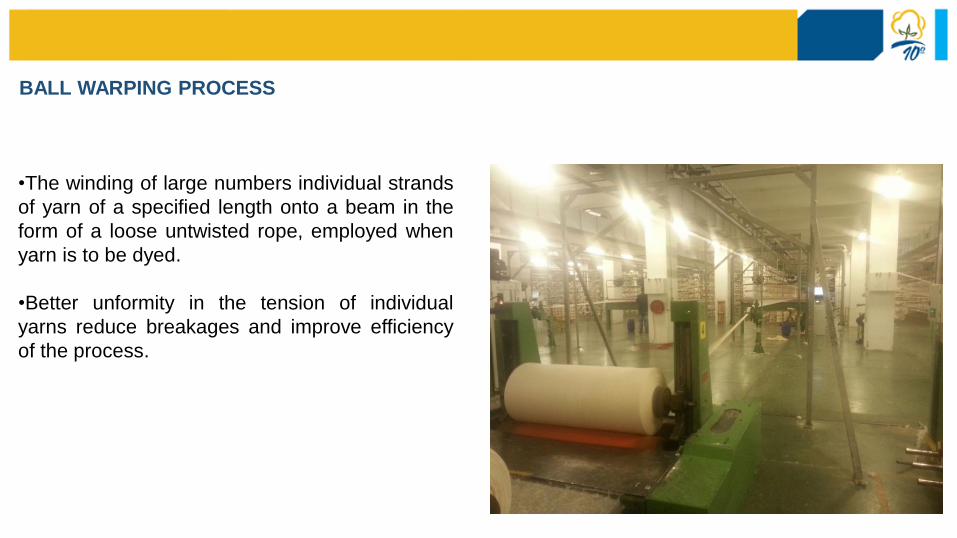

BALL WARPING PROCESS

•The winding of large numbers individual strands

of yarn of a specified length onto a beam in the

form of a loose untwisted rope, employed when

yarn is to be dyed.

•Better unformity in the tension of individual

yarns reduce breakages and improve efficiency

of the process.

BALL WARPING PROCESS

Brazilian Cotton Performance (dated Q1 – 2012)

• Best performance (least breakages) seen in lay

out consisting 50 % Brazilian + 50% US Cotton.

•Worst performance (more breakages) seen in

lay out consisting 100 % Brazilian.

100,00%98,46%

113,08%

80% Turkish RG 20% SG 50% Brazil+50% US 100% Brazil

Ball Warping Breakages

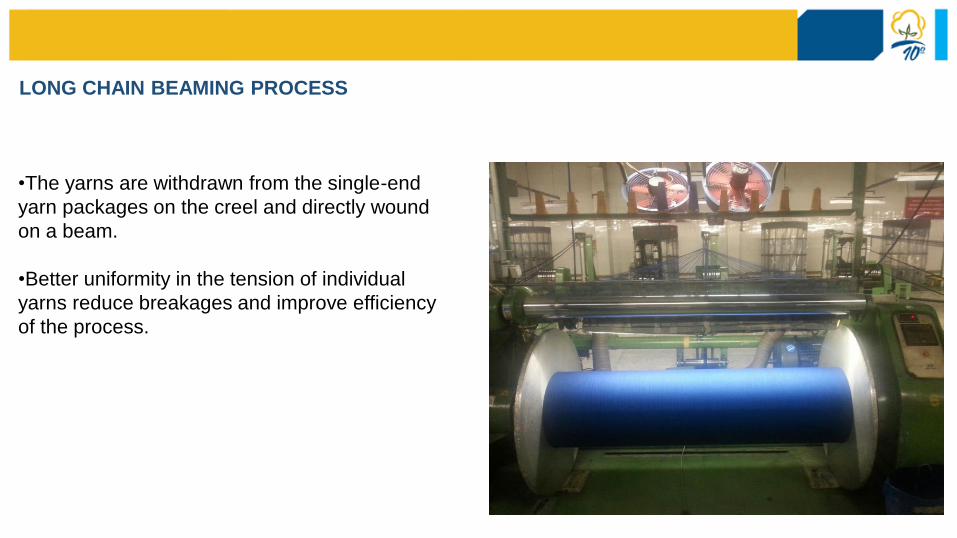

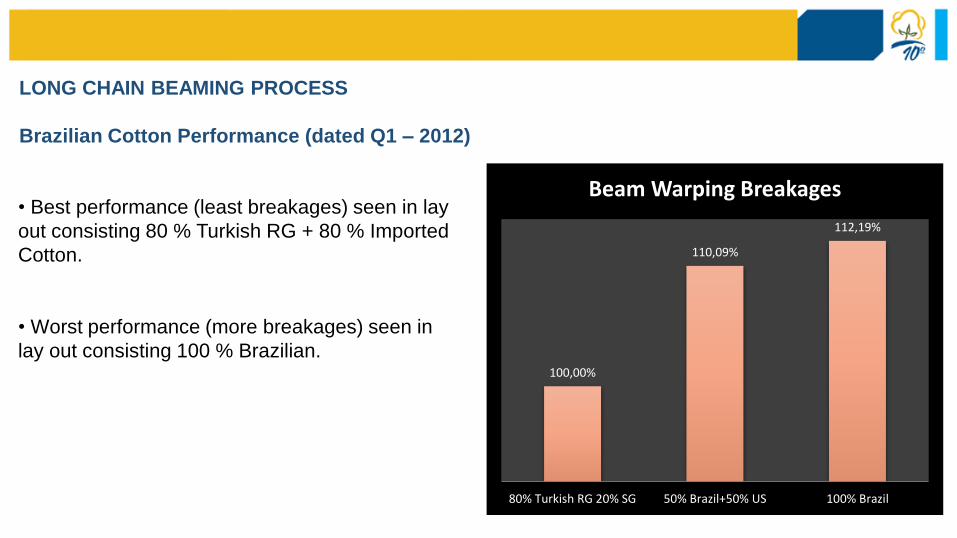

LONG CHAIN BEAMING PROCESS

•The yarns are withdrawn from the single-end

yarn packages on the creel and directly wound

on a beam.

•Better uniformity in the tension of individual

yarns reduce breakages and improve efficiency

of the process.

LONG CHAIN BEAMING PROCESS

Brazilian Cotton Performance (dated Q1 – 2012)

• Best performance (least breakages) seen in lay

out consisting 80 % Turkish RG + 80 % Imported

Cotton.

• Worst performance (more breakages) seen in

lay out consisting 100 % Brazilian.100,00%

110,09%

112,19%

80% Turkish RG 20% SG 50% Brazil+50% US 100% Brazil

Beam Warping Breakages

Comparison

Brazilian Cotton with Alternative Origins

A Comparison of Uniformity and Short Fiber Content

Saw Ginned Origins

Roller Ginned Origins

BrazilUSA

(Memphis/E)Greece Turkmenistan Mali Cameroon Turkey India

Uniformity 81,10 81,90 82,70 82,50 83,70 81,20 84,70 83,20

Short Fiber Content

9,70 8,50 7,90 8,30 7,30 9,80 6,00 6,40

Source : Orta Anadolu HVI Lab.

WEAKNESS OF BRAZILIAN COTTON

• High Variation and Inconsistancy in Physical Parameters within Lots

• Higher Short Fiber Content

• Lower Uniformity

STRENGTHS OF BRAZILIAN COTTON

• Large Size and Machanized Farming (Low Risk of Contamination)

• Saw Ginned (Less Trash – Higher Efficiency)

• Bale per Bale HVI (Quality Transparency)

• High Quality Packaging

• Strong corelation with NYF (Risk management applicable)

• Better Cotton Initiative and ABR Practices (Access to responsible textile supply chains)

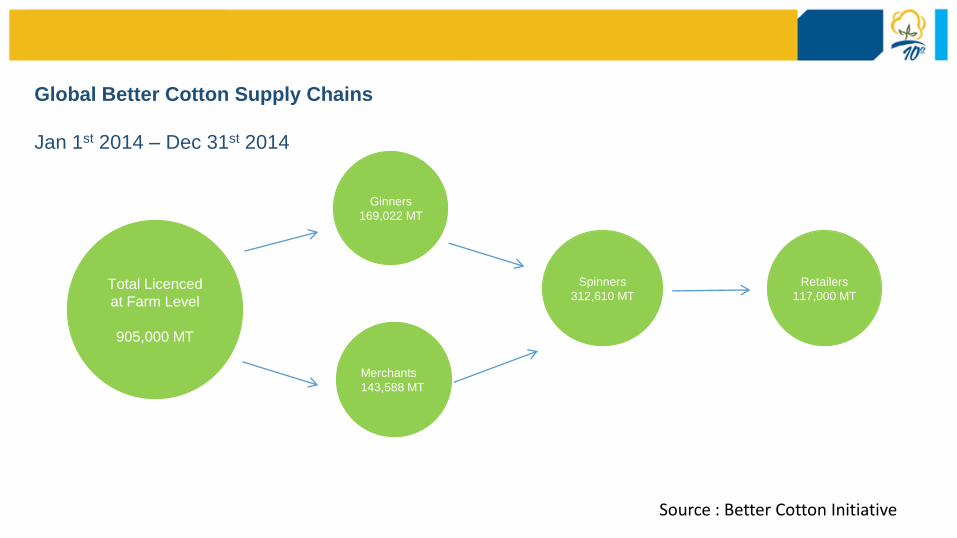

Global Better Cotton Supply Chains

Jan 1st 2014 – Dec 31st 2014

Total Licenced

at Farm Level

905,000 MT

Merchants

143,588 MT

Ginners

169,022 MT

Spinners

312,610 MT

Retailers

117,000 MT

Source : Better Cotton Initiative

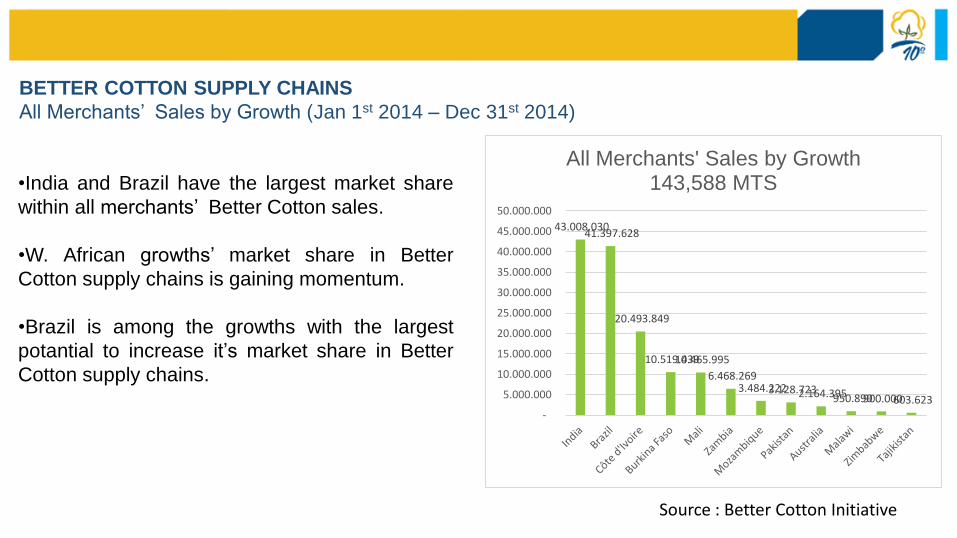

BETTER COTTON SUPPLY CHAINS

All Merchants’ Sales by Growth (Jan 1st 2014 – Dec 31st 2014)

•India and Brazil have the largest market share

within all merchants’ Better Cotton sales.

•W. African growths’ market share in Better

Cotton supply chains is gaining momentum.

•Brazil is among the growths with the largest

potantial to increase it’s market share in Better

Cotton supply chains.

43.008.030 41.397.628

20.493.849

10.519.439 10.465.995

6.468.269 3.484.222 3.128.723 2.164.395 950.890 900.000 603.623

-

5.000.000

10.000.000

15.000.000

20.000.000

25.000.000

30.000.000

35.000.000

40.000.000

45.000.000

50.000.000

All Merchants' Sales by Growth 143,588 MTS

Source : Better Cotton Initiative

Thank You

Leon Piçon

Orta Anadolu

Cotton Purchasing Director