a ccounting lecture-4 19-jan-2013 10/22/2015 1. d iscussion of a ssignment 10/22/2015 2

TRANSCRIPT

04

/20

/20

23

1

ACCOUNTINGLecture-4

19-Jan-2013

04

/20

/20

23

2

DISCUSSION OF ASSIGNMENT

04

/20

/20

23

3

WHAT WE DISCUSSED IN LAST CLASS?

Bookkeeping process Source documents/vouchers => Journal => Posting

=> Trial Balance => Financial Reports(BS, IS, CFS) Debit/Credit

AID Debit = Credit (Rational Balance Sheet Equation)

Journalizing Process Data from source documents/vouchers to Journals.

Chart of Accounts Coded (numbered) list of all account titles Varies across firms depending on sectors and

complexity and size of organization.

04

/20

/20

23

4

TERMS WE LEARNT IN LAST CLASS

Transaction documents Vouchers Journal / Book of original entry Day book General Journal Specialized Journal Debit Credit Journalizing Chart of Accounts

04

/20

/20

23

5

OBJECTIVES

Posting process Subsidiary Ledgers Bookkeeping process in computerized system Trial Balance Closing the books

04

/20

/20

23

6

BOOKKEEPING PROCESS IN DOUBLE-ENTRY ACCOUNTING SYSTEM

Journal/Day Books

Ledger

Trial Balance

Financial Statements(One Set)

Transaction Documents

04

/20

/20

23

7

STEP 3: POSTING INTO GENERAL LEDGER

What is general ledger? Traditionally, the general ledger was a bound or

loose-leaf book of ledger accounts. The general ledger is a collection of all ledger

accounts that support the organization’s financial statements.

What is a ledger account? A ledger account is a listing of all the increases

and decreases in a particular account.

04

/20

/20

23

8

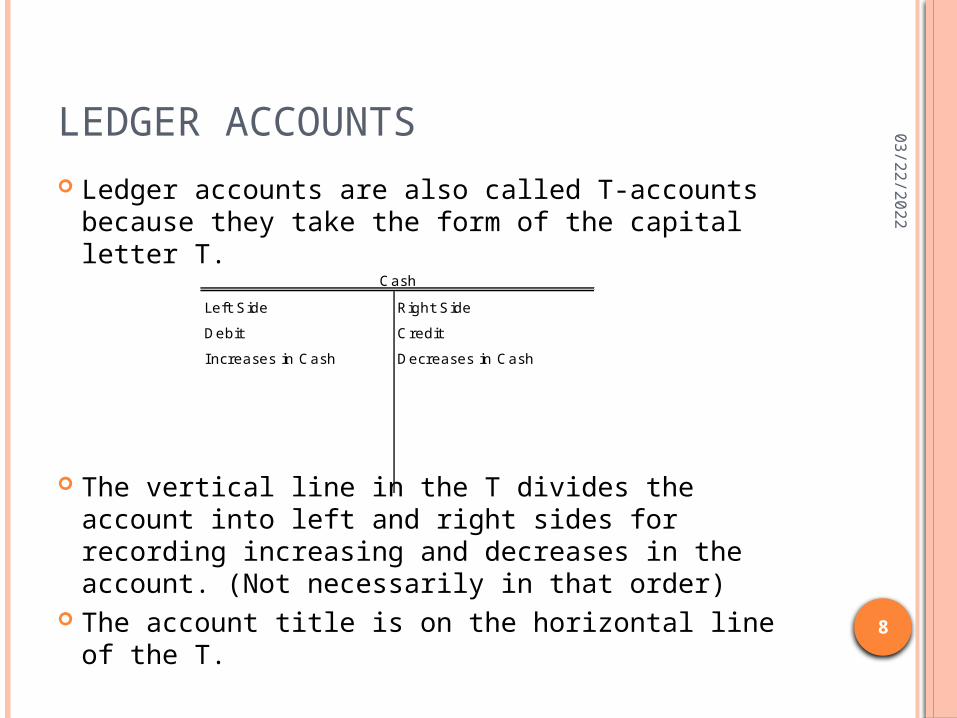

LEDGER ACCOUNTS

Ledger accounts are also called T-accounts because they take the form of the capital letter T.

The vertical line in the T divides the account into left and right sides for recording increasing and decreases in the account. (Not necessarily in that order)

The account title is on the horizontal line of the T.

Left Side Right Side

Debit Credit

I ncreases in Cash Decreases in Cash

Cash

04

/20

/20

23

9

LEDGER ACCOUNTS CONTINUED …

How do we place an entry on left(debit) or right(credit) side of the T accounts? Transferring entries into ledger T accounts from

general journal or special journals is a mechanical process.

Since every entry in the journal is already classified as either a debit or credit entry, the data is simply copied to T account.

04

/20

/20

23

10

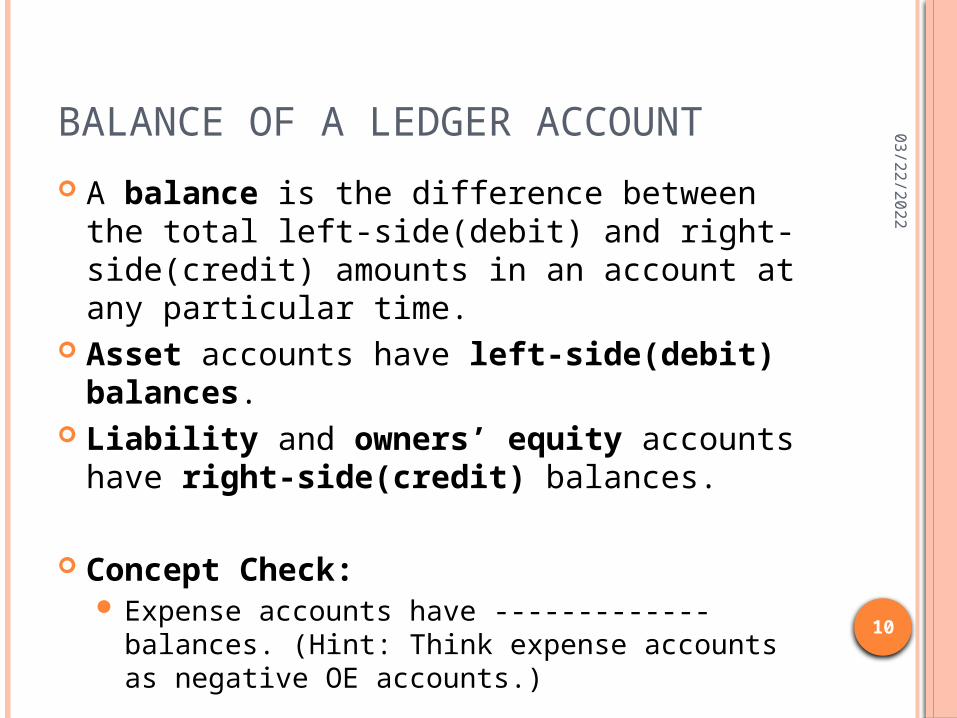

BALANCE OF A LEDGER ACCOUNT

A balance is the difference between the total left-side(debit) and right-side(credit) amounts in an account at any particular time.

Asset accounts have left-side(debit) balances.

Liability and owners’ equity accounts have right-side(credit) balances.

Concept Check: Expense accounts have ------------- balances.

(Hint: Think expense accounts as negative OE accounts.)

04

/20

/20

23

11

POSTING PROCESS

The transferring of amounts from the general journal (daily listing) to the appropriate T-accounts in general ledger is called posting.

04

/20

/20

23

12

POSTING PROCESS CONTINUED … Cross-referencing is the process of using

numbering, dating, and/or some other form of identification to relate each general ledger posting to the appropriate journal entry.

Note that a single transaction from the journal might be posted to several ledger accounts.

A popular format is shown below with an extra column containing running balance. General Ledger

Date Explanation J ournal Ref. Debit Credit Balance2-J an-13 Capital stock issued to Sandeep 1 400,000.00 400,000.00

2-J an-13 Borrowed at 10% int. 2 100,000.00 500,000.00

3-J an-13 Bought Store Equipment 3 15,000.00 485,000.00

CASH Account No. 100

04

/20

/20

23

13

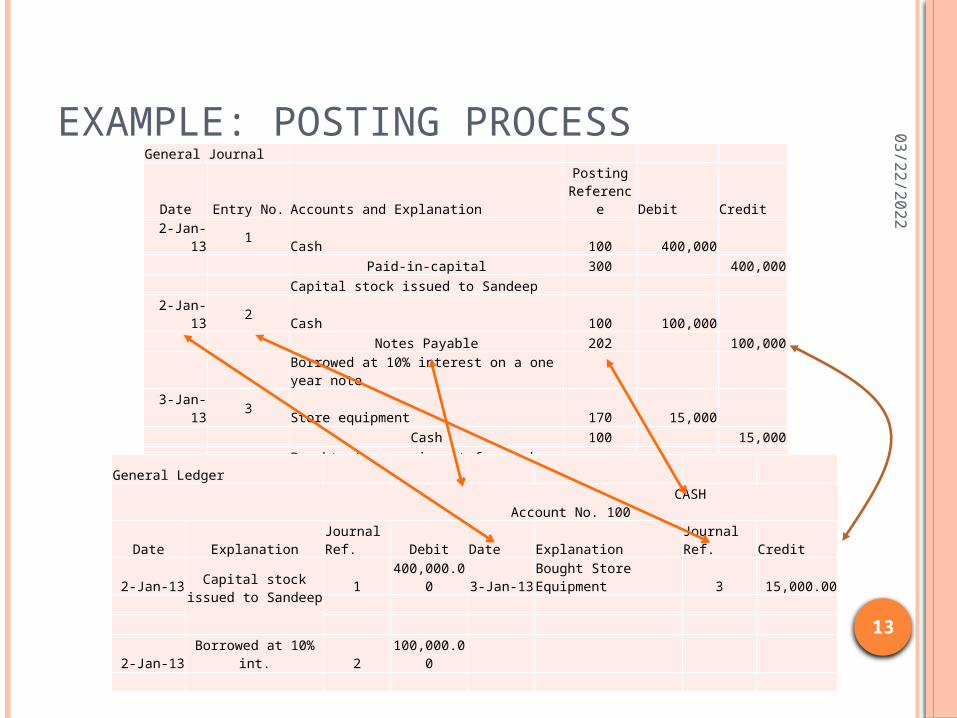

EXAMPLE: POSTING PROCESSGeneral Journal

Date Entry No. Accounts and ExplanationPosting

Reference Debit Credit

2-Jan-13 1 Cash 100 400,000

Paid-in-capital 300 400,000

Capital stock issued to Sandeep

2-Jan-13 2 Cash 100 100,000

Notes Payable 202 100,000

Borrowed at 10% interest on a one year

note

3-Jan-13 3 Store equipment 170 15,000

Cash 100 15,000

Bought store equipment for cash

General Ledger

CASH Account No. 100

Date ExplanationJournal Ref. Debit Date Explanation

Journal Ref. Credit

2-Jan-13 Capital stock issued to Sandeep

1400,000.0

0 3-Jan-13Bought Store Equipment 3 15,000.00

2-Jan-13Borrowed at 10%

int. 2100,000.0

0

BOOKKEEPING PROCESS IN Computerized System 0

4/2

0/2

02

3

14

Journal/Day Books

Trial Balance

Financial Statements(One Set)

Transaction Documents

LedgersTransaction

EntryScreens

04

/20

/20

23

15

NEED FOR SPECIAL JOURNALS

For small business, one can enter entries into only one book that is general journal.

But as the business expands and the number of transactions becomes large, it may become cumbersome to enter all transactions into a single journal.

For quick, efficient and accurate recording of business transactions, Journal is sub-divided into special journals.

04

/20

/20

23

16

SPECIAL JOURNALS

Basis for special Journals: Similar nature of transactions. Repetitiveness of a type of transaction.

For example, All cash transactions can be recorded in one book. All credit sales transactions in another book. Similarly, all credit purchases in yet another book.

These special journals are also called daybooks or subsidiary books.

Advantage of Special Journals: Division of labor Economical Ease of managerial reporting

04

/20

/20

23

17

COMMON JOURNALS

Special Journal Purpose (Record Transactions related to )

Cash Book Cash receipts and cash payments

Purchases Book Credit purchases of goods

Purchases Return (Return Outwards) Book

Purchase return of goods

Sales Book Credit sales of merchandise

Sales Return (Return Inwards) Book

Return of goods by customer. Sales to these customer were on credit.

Journal Proper or Journal Residual or General Journal

Record all transactions that do not find place in special journals

04

/20

/20

23

18

CENTRAL THEME OF SPECIAL JOURNALS

Since the nature of transaction in a special journal is known, either debit or credit side journalizing is done in the special journal. The other side of entry is implicit.

When data is posted from journal to the ledger, both debit and credit sides of transaction are posted.

Examples to illustrate it.

04

/20

/20

23

19

SPECIAL JOURNAL: EXAMPLE

Books of Konia SupplierSales(Journal Book)

Date Invoice No.Name of the Customer(Account to be Debited) L.F Amount

6-Apr-10 178 Raman Traders 4,850.00

9-Apr-10 180 Nutan Enterprises 21,000.00

28-Apr-10 209 Raman Traders 85,000.00

30-Apr-10 110,850.00

Posting into Ledger Accounts

General Ledger

Date Explanation J ournal Ref. Debit Credit Balance6-Apr-10 Sales 178 4,850.00 4,850.00

28-Apr-10 Sales 209 85,000.00 89,850.00

Date Explanation J ournal Ref. Debit Credit Balance

9-Apr-10 Sales 180 21,000.00 21,000.00

Date Explanation J ournal Ref. Debit Credit Balance

30-Apr-10

Sundaries as per sales book 110,850.00 110,850.00

Sales Revenue Account No. XXX

Raman Traders Account No. XXX

Nutan Enterpriese Account No. XXX

04

/20

/20

23

20

SUBSIDIARY LEDGERS

A subsidiary ledger is a group of similar accounts whose combined balances equal the balance in a specific general ledger account.

The general ledger account that summarizes a subsidiary ledger's account balances is called a control account or master account.

Example: an accounts receivable subsidiary ledger (customers' subsidiary ledger) includes a separate account for each customer who makes credit purchases.

The combined balance of every account in this subsidiary ledger equals the balance of accounts receivable in the general ledger.

04

/20

/20

23

21

SUBSIDIARY LEDGER CONTINUED …. Posting a debit or credit to a subsidiary ledger

account and also to a general ledger control account does not violate the rule that total debit and credit entries must balance because subsidiary ledger accounts are not part of

the general ledger; they are supplemental accounts that provide the

detail to support the balance in a control account. Example: In our sales book example, we could

have a control account-Accounts Receivable account. On periodic basis, balance from all customer subsidiary accounts will be added and recorded into control account.

Note: Subsidiary ledger itself can contain control ledger account.

04

/20

/20

23

22

ANY DOUBTS?

04

/20

/20

23

23

THANK YOU.