9th halal certification bodies convention · (under tawarruq contract) channel funds via ria...

TRANSCRIPT

Strictly Private & Confidential

9TH HALAL CERTIFICATION

BODIES CONVENTION

ISLAMIC CROWDFUNDING VIA INVESTMENT

ACCOUNT PLATFORM AND SADAQA HOUSE

MOHD IZHAR PAWANCHEK

BANK ISLAM MALAYSIA BERHADEmail: [email protected]

2 APRIL 2018

TABLE OF CONTENTS

Page 2

. SECTION 1.0 – ISLAMIC CROWDFUNDING

. SECTION 2.0 – INVESTMENT ACCOUNT PLATFORM

. SECTION 3.0 – SADAQA HOUSE

Page 3

Page 6

Page 23

Page 3

SECTION 1.0 – ISLAMIC CROWDFUNDING

ISLAMIC CROWDFUNDING

Page 4

What is ‘Islamic Crowdfunding’?

Islamic Crowdfunding is sourcing money from a large number of individuals and non-

individuals to finance business venture or project in accordance with Shariah.

Investors/Donors Investors/Donors

ISLAMIC CROWDFUNDING

Page 5

How Crowdfunding Works?

▪ Crowdfunding provides the opportunity for entrepreneurs and social

entrepreneurs to raise funds from anyone with money to invest in a business or

donate in a project that can solve social problem.

▪ Crowdfunding provides a platform to anyone with an idea to pitch it in front of

ready investors.

▪ Crowdfunding operator generate revenue from a percentage of the funds raised.

Page 6

SECTION 2.0 – INVESTMENT ACCOUNT PLATFORM

INTRODUCTION OF INVESTMENT ACCOUNT PLATFORM

5

6

User friendly and

easily accessible

anywhere,

anytime

Open to different

types of business

and ventures of

varying size and

industries

An avenue for

Shariah-

Compliant

investment and

financing

Credit

assessment and

screening on the

listed ventures by

participating

Islamic banks

Rating on the listed

ventures by a

reputable rating

agency

Compliance to

disclosure

standard on

ventures facilitate

investors’ informed

decision making

2

1

34

WHAT IS IAP?

➢ The Investment Account

Platform (“IAP”) is a

multi-bank platform that

facilitates channeling of

funds from investors to

finance viable ventures.

Funds mobilised via IAP

are intermediated by

participating Islamic

banks through

investment account

(“IA”) products.

➢ IA is governed by

Islamic Financial

Services Act 2013 and

Development Financial

Institutions Act 2002.

Key Features

Page 7

www.iaplatform.com

Page 8

Provide Term Financing

(under Tawarruq contract)

Channel funds

via RIA product

(under Wakalah

contract)

2 3

Sponsoring Bank /

Investment Agent

www.iaplatform.com

Investment Booking

via IAP Portal

1

▪ Individual Investors

▪ Non-Individual Investors

Customer

Strong roles played by Sponsoring Bank, in line with its fiduciary duties:

▪ Due diligence

▪ Suitability assessment

▪ Performance monitoring

▪ Investment management

BROAD MECHANICS OF IAP

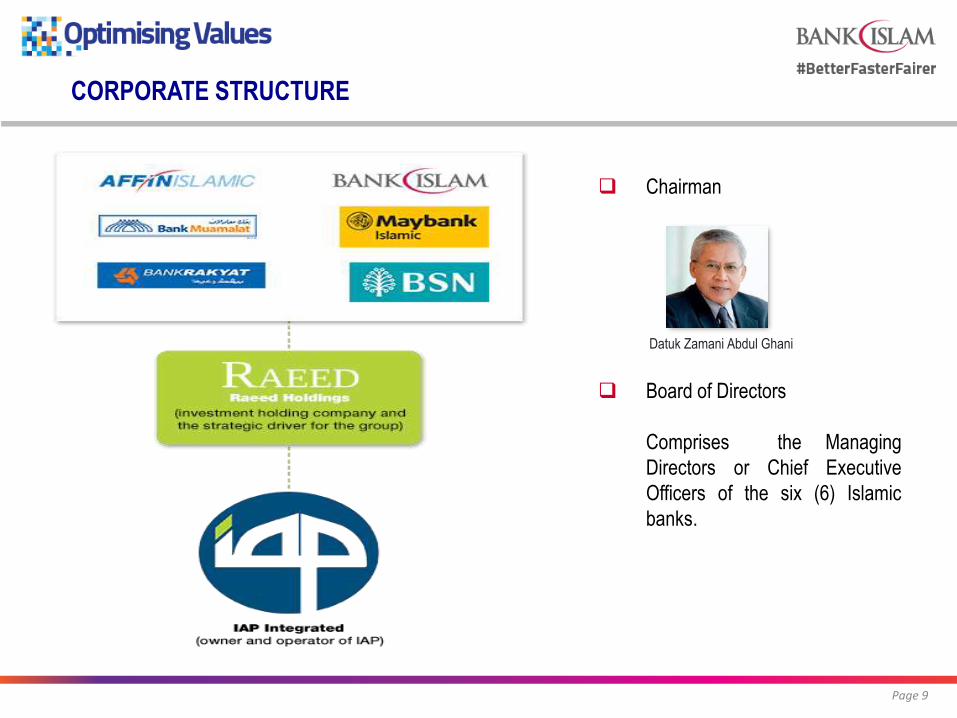

CORPORATE STRUCTURE

Page 9

Datuk Zamani Abdul Ghani

Chairman

Board of Directors

Comprises the Managing

Directors or Chief Executive

Officers of the six (6) Islamic

banks.

IAP WEBSITE

Page 10

www.iaplatform.com

TYPES OF VENTURES AND FACILITIES ON IAP

Type and Target Ventures Type of Financing Facility

Page 11

Any type of ventures, entities, purposes

involve in various type of industries:

➢ SMEs, Non-SMEs, PLCs, MNCs,

GLCs.

➢ Federal and State Institutions group of

companies.

Term Financing

➢ To part-finance CAPEX of the

Ventures.

➢ To part-finance the Working Capital

requirements of the Ventures.

➢ To part-finance any contracts

obtained by the Ventures.

PROCESS FLOW OF VENTURE ASSESSMENT

Page 12

The diagram below indicates the processes involved in raising funds via IAP:

EXECUTION PROCESS FOR IAP

Page 13

1. Project

Feasibility

Assessment

3. Bank Islam’s

Internal Credit

Process and

Approval

6. Appointment of

Solicitors for

Financing Docs

and Due

Diligence

9. Listing of

Financing into

IAP Portal

8. Execution

Financing Docs

and CP

Compliance

2. Finalisation of

Financing

Structure and

Indicative Terms

5. Appointment of

Rating Agency

and Issuance of

Credit Opinion

4. Issuance of

Letter of Offer to

Venture and

Acceptance

7. Preparation of

Listing

Information

10. Subscription

by Investors

11. Disbursement

EXECUTION PROCESS (3 to 4 Mths)

Page 14

INDEPENDENT RATING FOR VENTURES

Credit

Bureau

Reference

Base Rating

Parental

SupportCollateral

Issuer

rating

Standalone

rating

Rating Overlay

Issue

rating

Final Rating

Industry Business

FinancialManage-

ment

aaaaaa

bbbbbbcd

RATING METHODOLOGY

Page 15

INDEPENDENT RATING FOR VENTURES (Cont'd)

• One-off, point-in-time, issue-

specific ratings.

• Assigned by a RAM group

company (RAM Solutions Sdn

Bhd).

• Benchmarked against RAM

Ratings.

• Accompanied by a 2-page rating

rationale.

• Based on information provided by

the Venture via the Sponsoring

Bank.

Rating Symbol * Credit Quality

aaa Superior

aa High

a Adequate

bbb Moderate

bb Low

b Very low

c High likelihood of default

d Default

* Suffix 1, 2 and 3 are applied to ratings in the six rating

categories (from “aa” to “c”) to denote the higher and

lower end of the respective rating band (e.g. bbb1,

bbb2, bbb3)

Features of ratings for IAP

Page 16

DEPOSIT ACCOUNT VS INVESTMENT ACCOUNT

Wadiah (safekeeping)

Murabahah (cost plus basis)

Qard (benevolent placement)

Musharakah (profit and loss sharing)

Deposit Account

Investment Account

Business/House/ Car/ Personal

Financing

Wakalah (agency agreement)

1. 2.

Pro

du

cts

Typ

es o

f IA

Op

tio

ns

for

Cu

sto

mer

s

Under IFSA, customers have the choice of placing funds in Islamic deposit acc. or investment acc.

Shariah Contracts

ISLAMIC

BANK

1. Deposit Account

• Principal guaranteed up to RM250,000 per depositor per bank

• Flexible fund withdrawal

• Many types of deposits e.g. current acc. and savings acc.

2. Investment Account

• Returns are based on performance of underlying assets

• Maturity and withdrawal conditions agreed at inception

Restricted Investment Account (RIA)

• Funds invested into specified assets with the investment

mandate by customers

• Requires matching between investment tenure and the maturity

of the underlying assets

• Customers are subject to specific withdrawal conditions agreed at

inception

Unrestricted Investment Account (URIA)

• Customers rely on Islamic banks’ expertise

• Islamic banks may combine investment account funds belonging to

many customers with similar risk profiles within a single or multiple

URIA pools to be invested in a group of assets

• Customers are subject to more flexible withdrawal terms compared to

RIA

Source: BNM

Mudarabah (profit sharing basis)

Page 17

FEATURES OF IA PRODUCTS – MUDARABAH CONTRACT

Investment

Account Holders

(IAH)

Sponsoring Bank

▪ Principal payment

▪ Profit as per agreed PSR

(IAH) e.g. 70:30

Invests IAH funds

Place investments with the Bank

Profit

Generates profit /

incurs loss

Loss

Loss to be borne by

the IAH

3c

3a

1

2

3

3b

▪ Profit as per agreed

PSR (Bank) e.g. 70:30

Specific Financing Asset i.e.

Venture

Investment Account based on Mudarabah contract

Page 18

FEATURES OF IA PRODUCTS – WAKALAH CONTRACT

Investment

Account Holders

(IAH)

Sponsoring Bank

▪ Principal payment

▪ Profit payment

(Note: profit earned may be equal to or

less than Expected Profit)

Sponsoring Bank as

Investment Agent

Profit

Generates profit /

incurs loss

Loss

Loss to be borne by

the IAH

3c

3b

▪ Wakalah Fee plus any

excess retained as

performance incentive

3a

1

2

3

Invests IAH funds

Specific Financing Asset i.e.

Venture

Investment Account based on Wakalah contract

Page 19

INFO ON VENTURES AVAILABLE TO INVESTORS

Product

Disclosure Sheet

(“PDS”)

This document refers to the terms on investment offered by the Sponsoring Bank namely the

Shariah contract such as ‘mudarabah’ or ‘wakalah’ and the respective profit sharing ratio

(PSR) or the expected profit, tenure of investment, minimum investment amount, principal

and profit distribution, fees and charges etc.

RAM Rating

Rationale

This documents refers to a write-up by RAM on the rating accorded and basis of the rating

including probability of default, the industry the Venture is involved in, commentary on some financial ratios and the management capability, as well as comments on other types of risks.

Terms of

FinancingThis document talks about the terms and conditions of the financing granted to the Venture including pricing, tenure, security structure, payment terms etc to the Sponsoring Bank.

Venture’s

InfoThis set of documents refers to information relevant to the Venture including the management team and their profile, shareholders, financial performance, projects undertaken etc.

Page 20

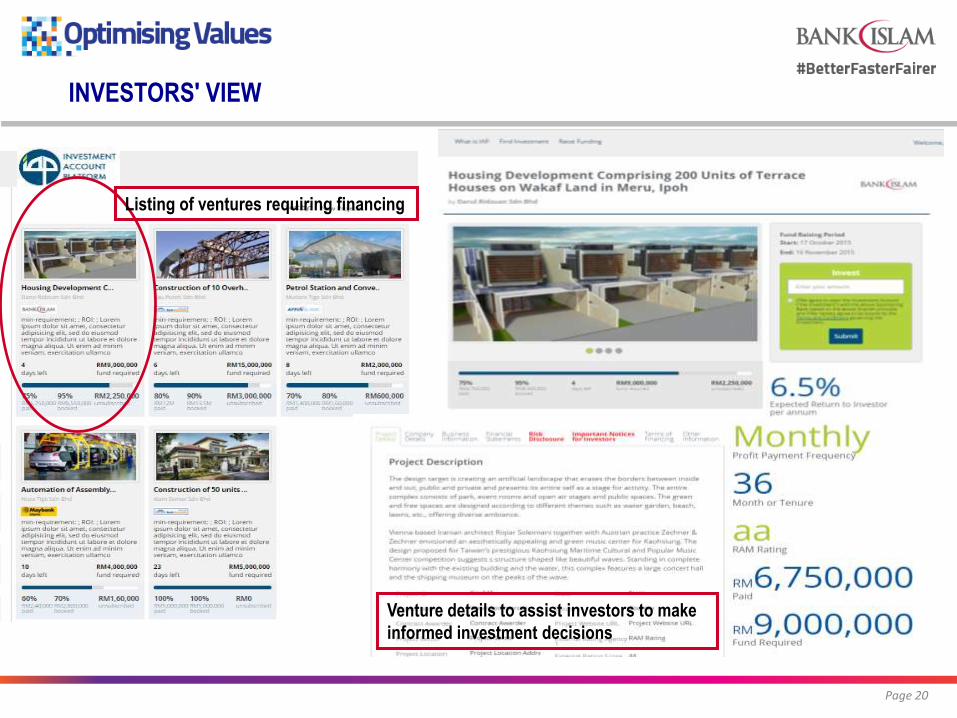

INVESTORS' VIEW

Venture details to assist investors to make

informed investment decisions

Listing of ventures requiring financing

Page 21

BENEFIT TO VENTURES AND INVESTORS

Ventures

One-stop centre for funding requirement via

online application

Possibility of securing the best financing

terms

Enhanced visibility to potential investors

No dilution in ownership and ability to

maintain control of the company

Wider choices of investment assets and risk-

return profile

Potential for higher returns than normal bank

deposit

Screening and monitoring by banks

Independent rating by reputable rating

agency to support investment decision

Investors

1

2

3

4

1

2

3

4

Venture /

Project

KOBIMBING

Ar Rahn

Muamalat

Ventures

Ar Rahn 2

Muamalat

Ventures

Listing

No.1 2 3 4 5 6 7 8

SBBank

Muamalat

Bank

Islam

Affin

Islamic

Maybank

Islamic

Bank

Islam

Bank

Muamalat

Affin

Islamic

Bank

Muamalat

PurposeWorking

Cap

Working

Cap

Project

Financing

Working

Cap

Project

FinancingWorking Cap

Project

Financing

Working

Cap

Economic

SectorTransport

Fin

ServicesRental

Fin

ServicesInfra Fin Services F&B Fin Services

Indicative

return

(p.a.)

6.50% 6.60% 6.08% 4.90% 6.30% 7.50% 7.00% 7.00%

Fund

required

RM10.0

mil

RM6.0

mil

RM3.9

mil

RM60.0

mil

RM12.0

mil

RM20.0

mil

RM3.3

mil

RM20.0

mil

Financing

Tenure3 years 5 years 2 years 3 years 1.5 years 0.5 years 3.5 years 1 year

RAM

ratingbbb2 bbb3 a3 Unrated a3 a3 a3 a3

Financing

ContractTawarruq Tawarruq Tawarruq Various Tawarruq Musyarakah Tawarruq Musyarakah

IA

ContractWakalah Wakalah Mudarabah Mudarabah Wakalah Wakalah Mudarabah Wakalah

Listing

DateMay 2016 Nov 2016 Nov 2016 April 2017 April 2017 Sep 2017 Dec 2017 Feb 2018

IAP Listing as at 5 March 2018

Page 23

SECTION 3.0 – SADAQA HOUSE

THE IDEA AND PHILOSOPHY OF SADAQA HOUSE

Page 24

Concept

Sadaqa House is a donation platform operated by Bank Islam which enables

funds to be channelled to the needy communities through Bank Islam partners. It

was launched on 19 January 2018. This is one of the efforts to create more

sustainable economic development, community and environment.

Driving Factors of Sadaqa House Establishment

1. Perfecting the Islamic Economics system - for Islamic banking and finance to

serve the Muslim community, it should cover the different aspects of the

economy, namely siasi (government), tijari (private) and ijtima’i (social

welfare).

2. Inequality and poverty in Malaysia.

3. Zakah distribution in Malaysia.

4. Rapid development of crowdfunding.

5. Public trust and confidence in banking institutions.

SADAQA HOUSE MODEL

Page 25

SADAQAH PORTAL

SOURCE OF FUNDS

Internet

Banking

Individual

DonorsCorporate

Donors

USE OF FUNDS

Invest in low

risk, short term

investment

STRATEGIC PARTNERS

NGO1/

Project 1

NGO2/

Project 2NGO3/

Project 3

Profit

Bank Islam

Credit Card

Tap Mobile

Banking

Scheduled

Payments

www.globalsadaqah.com

SADAQA HOUSE MODEL

Page 26

SOURCE OF FUND FUND MANAGEMENT USAGE OF FUND

▪Phase 1 (launching) –

public donation with a

match offer from BIMB

through digital platform.

▪Donation will be directly

paid to BIMB collection

account (via Ethis’

platform)

▪Phase 2 – other

collection channels.

▪Sadaqa House collection

account.

▪ Investment – placement

in low risk investment

(TDT-i) for a short term

period.

▪Manage by Shariah

Division.

▪Community of front

liners/strategic partners -

NGOs are identified via

Request For Proposal

process.

▪Approval by the Zakat

and Charity Committee.

▪Monitoring by Corporate

Responsibilities

Department and Shariah

Division.

SADAQA HOUSE MICROSITE

Page 27

www.globalsadaqah.com

SADAQA HOUSE PROJECTS

Page 28

IJN PATIENT: SUPPORT YU

JUN’S PDA OCCLUSION

SURGERY COST

GOAL: RM15,000

RAISED: RM1,820

FUNDING HEALTH FINANCIAL

AID – IJN FOUNDATION

GOAL: RM300,000

RAISED: RM65,018

IJN PATIENT: SUPPORT AIMAN’S

TOF SURGERY COST

GOAL: RM10,000

RAISED: RM5,520

SADAQA HOUSE PROJECTS

Page 29

IJN PATIENTS: SUPPORT

HAIKAL’S HEART

SURGERY COST

GOAL RM5,000

RAISED RM5,000

COMMUNAL

INFRASTRUCTURE – FISH

DRYING CABIN

GOAL: RM300,000

RAISED: RM5,037

SOLAR SYSTEM –

RENEWABLE ENERGY

GOAL: RM200,000

RAISED: RM22,250

Page 30