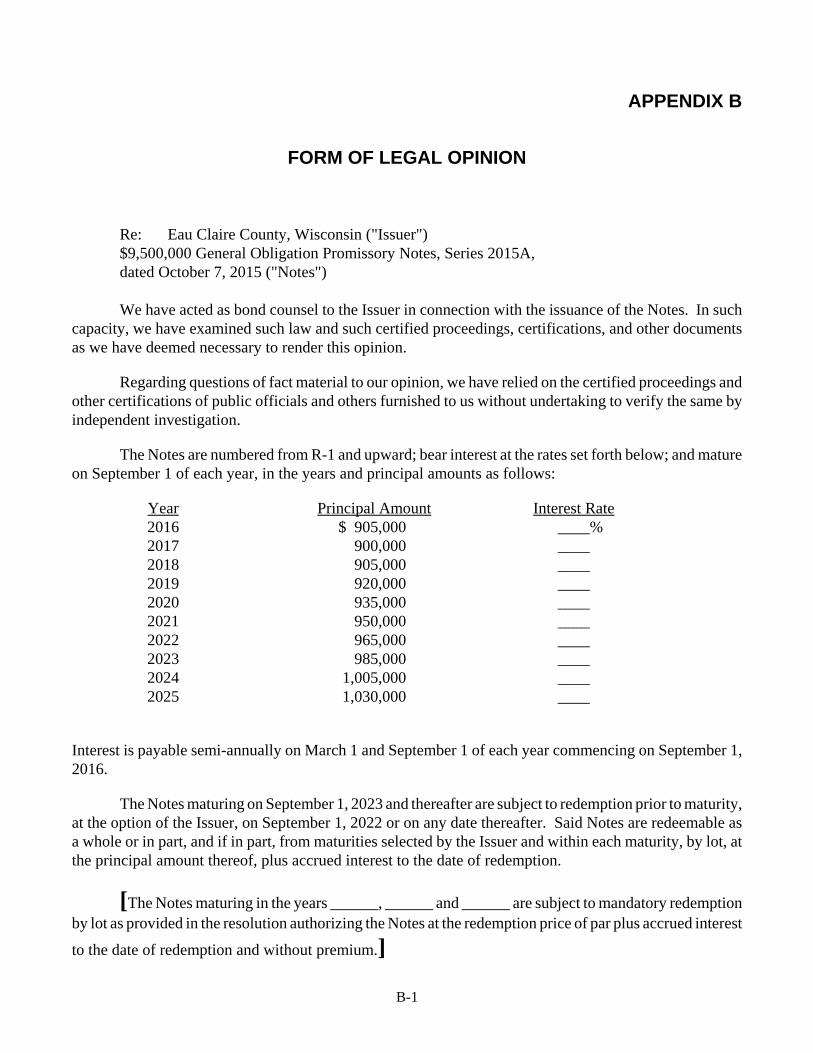

$9,500,000 general obligation promissory notes, … obligation promissory notes, series 2015a eau...

TRANSCRIPT

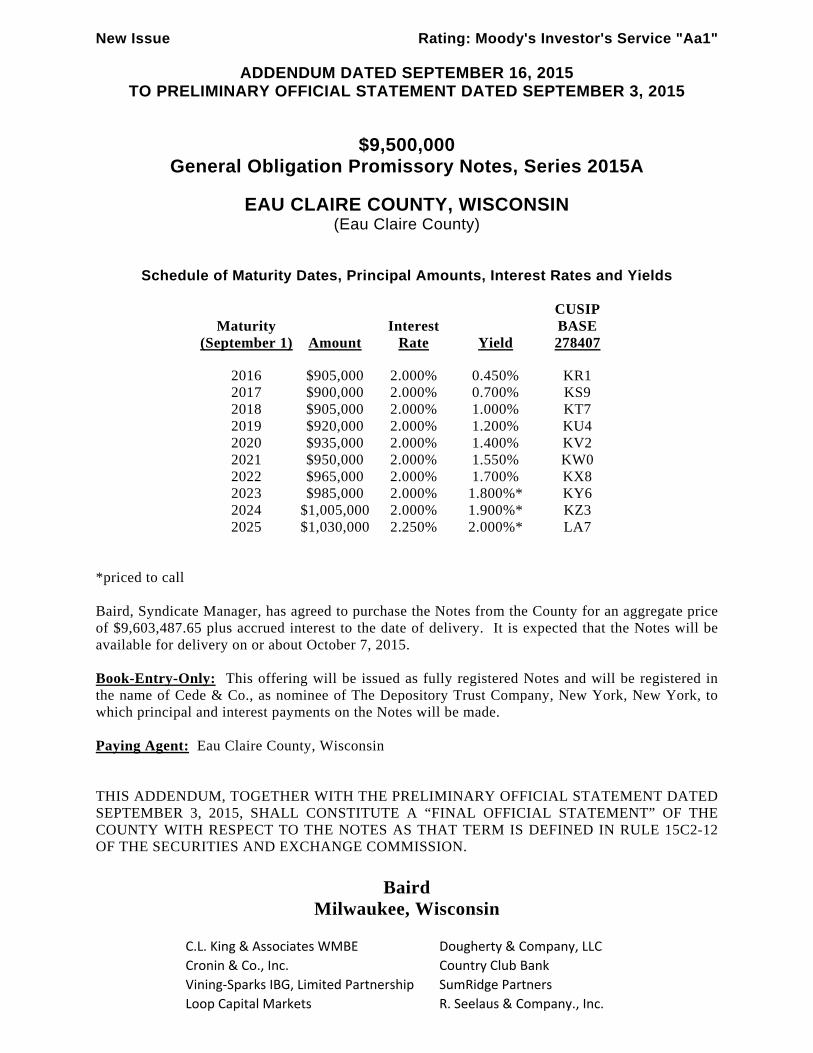

New Issue Rating: Moody's Investor's Service "Aa1"

ADDENDUM DATED SEPTEMBER 16, 2015 TO PRELIMINARY OFFICIAL STATEMENT DATED SEPTEMBER 3, 2015

$9,500,000 General Obligation Promissory Notes, Series 2015A

EAU CLAIRE COUNTY, WISCONSIN (Eau Claire County)

Schedule of Maturity Dates, Principal Amounts, Interest Rates and Yields

Maturity (September 1) Amount

Interest Rate Yield

CUSIP BASE 278407

2016 $905,000 2.000% 0.450% KR1 2017 $900,000 2.000% 0.700% KS9 2018 $905,000 2.000% 1.000% KT7 2019 $920,000 2.000% 1.200% KU4 2020 $935,000 2.000% 1.400% KV2 2021 $950,000 2.000% 1.550% KW0 2022 $965,000 2.000% 1.700% KX8 2023 $985,000 2.000% 1.800%* KY6 2024 $1,005,000 2.000% 1.900%* KZ3 2025 $1,030,000 2.250% 2.000%* LA7

*priced to call Baird, Syndicate Manager, has agreed to purchase the Notes from the County for an aggregate price of $9,603,487.65 plus accrued interest to the date of delivery. It is expected that the Notes will be available for delivery on or about October 7, 2015. Book-Entry-Only: This offering will be issued as fully registered Notes and will be registered in the name of Cede & Co., as nominee of The Depository Trust Company, New York, New York, to which principal and interest payments on the Notes will be made. Paying Agent: Eau Claire County, Wisconsin THIS ADDENDUM, TOGETHER WITH THE PRELIMINARY OFFICIAL STATEMENT DATED SEPTEMBER 3, 2015, SHALL CONSTITUTE A “FINAL OFFICIAL STATEMENT” OF THE COUNTY WITH RESPECT TO THE NOTES AS THAT TERM IS DEFINED IN RULE 15C2-12 OF THE SECURITIES AND EXCHANGE COMMISSION.

Baird

Milwaukee, Wisconsin

C.L. King & Associates WMBE Dougherty & Company, LLC

Cronin & Co., Inc. Country Club Bank

Vining‐Sparks IBG, Limited Partnership SumRidge Partners

Loop Capital Markets R. Seelaus & Company., Inc.

Coastal Securities, Inc. Sierra Pacific Securities

SAMCO Capital Markets Alamo Capital

WNJ Capital IFS Securities

Crews & Associates, Inc. Bernardi Securities, Inc.

Davenport & Co. L.L.C. UMB Bank,N.A.

Northland Securities, Inc. Central States Capital Markets

Ross, Sinclaire & Associates, LLC ORIGINAL ISSUE PREMIUM To the extent that the initial offering price of certain of the Notes is more than the principal amount payable at maturity, such Notes ("Premium Notes") will be considered to have bond premium. Any Premium Note purchased in the initial offering at the issue price will have "amortizable bond premium" within the meaning of Section 171 of the Code. The amortizable bond premium of each Premium Note is calculated on a daily basis from the issue date of such Premium Note until its stated maturity date (or call date, if any) on the basis of a constant instant rate compounded at each accrual period (with straight line interpolation between the compounding dates). An owner of a Premium Note that has amortizable bond premium is not allowed any deduction for the amortizable bond premium; rather the amortizable bond premium attributable to a taxable year is applied against (and operates to reduce) the amount of tax-exempt interest payments on the Premium Notes. During each taxable year, such an owner must reduce his or her tax basis in such Premium Note by the amount of the amortizable bond premium that is allocable to the portion of such taxable year during which the holder held such Premium Note. The adjusted tax basis in a Premium Note will be used to determine taxable gain or loss upon a disposition (including the sale, exchange, redemption, or payment at maturity) of such Premium Note. Owners of Premium Notes who did not purchase such Premium Notes in the initial offering at the issue price should consult their own tax advisors with respect to the tax consequences of owning such Premium Notes. Owners of Premium Notes should consult their own tax advisors with respect to the state and local tax consequences of owning the Premium Notes.

In the opinion of Quarles & Brady LLP, Bond Counsel, assuming continued compliance with the requirements of the Internal Revenue Code of 1986, as amended, under existinglaw interest on the Notes is excludable from gross income and is not an item of tax preference for federal income tax purposes. See "TAX EXEMPTION" herein for a moredetailed discussion of some of the federal income tax consequences of owning the Notes. The interest on the Notes is not exempt from present Wisconsin income or franchisetaxes.

The County will designate the Notes as "qualified tax-exempt obligations" for purposes of Section 265(b)(3) of the Internal Revenue Code of 1986, as amended, relating tothe ability of financial institutions to deduct from income for federal income tax purposes, interest expense that is allocable to carrying and acquiring tax-exempt obligations.

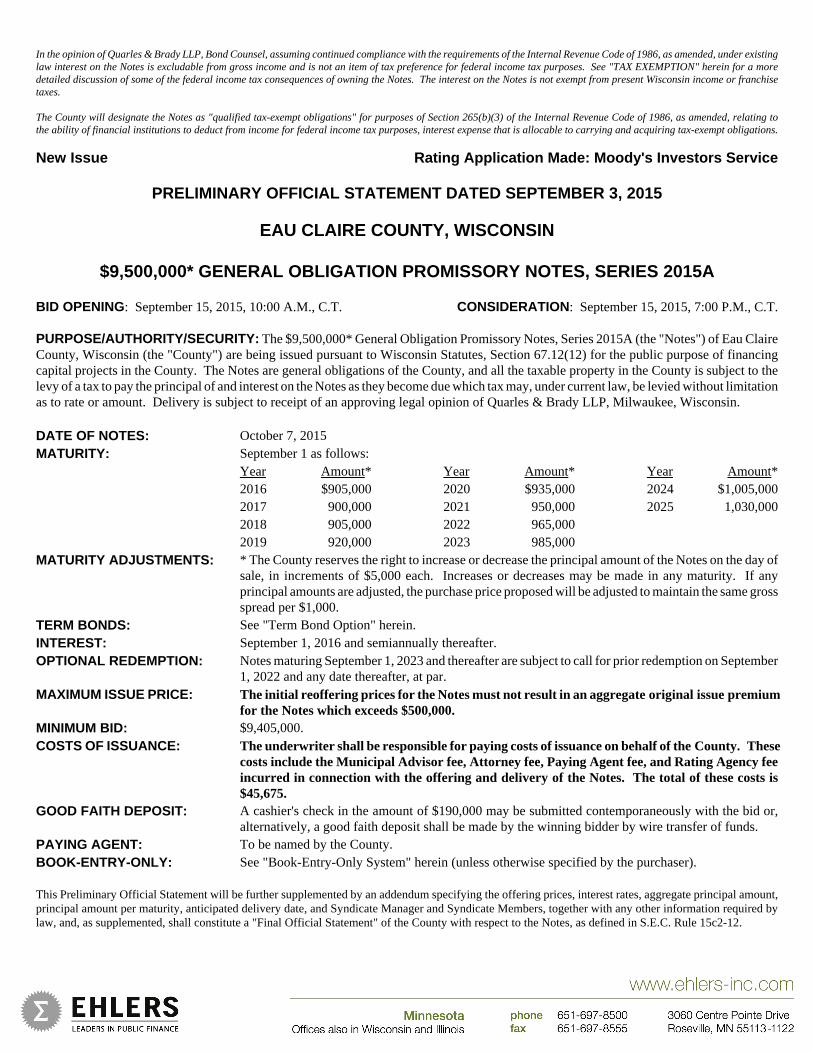

New Issue Rating Application Made: Moody's Investors Service

PRELIMINARY OFFICIAL STATEMENT DATED SEPTEMBER 3, 2015

EAU CLAIRE COUNTY, WISCONSIN

$9,500,000* GENERAL OBLIGATION PROMISSORY NOTES, SERIES 2015A

BID OPENING: September 15, 2015, 10:00 A.M., C.T. CONSIDERATION: September 15, 2015, 7:00 P.M., C.T.

PURPOSE/AUTHORITY/SECURITY: The $9,500,000* General Obligation Promissory Notes, Series 2015A (the "Notes") of Eau ClaireCounty, Wisconsin (the "County") are being issued pursuant to Wisconsin Statutes, Section 67.12(12) for the public purpose of financingcapital projects in the County. The Notes are general obligations of the County, and all the taxable property in the County is subject to thelevy of a tax to pay the principal of and interest on the Notes as they become due which tax may, under current law, be levied without limitationas to rate or amount. Delivery is subject to receipt of an approving legal opinion of Quarles & Brady LLP, Milwaukee, Wisconsin.

DATE OF NOTES: October 7, 2015MATURITY: September 1 as follows:

Year Amount* Year Amount* Year Amount*2016 $905,000 2020 $935,000 2024 $1,005,0002017 900,000 2021 950,000 2025 1,030,0002018 905,000 2022 965,0002019 920,000 2023 985,000

MATURITY ADJUSTMENTS: * The County reserves the right to increase or decrease the principal amount of the Notes on the day ofsale, in increments of $5,000 each. Increases or decreases may be made in any maturity. If anyprincipal amounts are adjusted, the purchase price proposed will be adjusted to maintain the same grossspread per $1,000.

TERM BONDS: See "Term Bond Option" herein.INTEREST: September 1, 2016 and semiannually thereafter.OPTIONAL REDEMPTION: Notes maturing September 1, 2023 and thereafter are subject to call for prior redemption on September

1, 2022 and any date thereafter, at par.MAXIMUM ISSUE PRICE: The initial reoffering prices for the Notes must not result in an aggregate original issue premium

for the Notes which exceeds $500,000.MINIMUM BID: $9,405,000.COSTS OF ISSUANCE: The underwriter shall be responsible for paying costs of issuance on behalf of the County. These

costs include the Municipal Advisor fee, Attorney fee, Paying Agent fee, and Rating Agency feeincurred in connection with the offering and delivery of the Notes. The total of these costs is$45,675.

GOOD FAITH DEPOSIT: A cashier's check in the amount of $190,000 may be submitted contemporaneously with the bid or,alternatively, a good faith deposit shall be made by the winning bidder by wire transfer of funds.

PAYING AGENT: To be named by the County.BOOK-ENTRY-ONLY: See "Book-Entry-Only System" herein (unless otherwise specified by the purchaser).

This Preliminary Official Statement will be further supplemented by an addendum specifying the offering prices, interest rates, aggregate principal amount,principal amount per maturity, anticipated delivery date, and Syndicate Manager and Syndicate Members, together with any other information required bylaw, and, as supplemented, shall constitute a "Final Official Statement" of the County with respect to the Notes, as defined in S.E.C. Rule 15c2-12.

ii

REPRESENTATIONS

No dealer, broker, salesperson or other person has been authorized by the County to give any information or to make any representation otherthan those contained in this Preliminary Official Statement and, if given or made, such other information or representations must not be reliedupon as having been authorized by the County. This Preliminary Official Statement does not constitute an offer to sell or a solicitation ofan offer to buy any of these Notes in any jurisdiction to any person to whom it is unlawful to make such an offer or solicitation in suchjurisdiction.

This Preliminary Official Statement is not to be construed as a contract with the Syndicate Manager or Syndicate Members. Statementscontained herein which involve estimates or matters of opinion are intended solely as such and are not to be construed as representations offact. Ehlers prepared this Preliminary Official Statement and any addenda thereto relying on information of the County and other sources forwhich there is reasonable basis for believing the information is accurate and complete. Bond Counsel has not participated in the preparationof this Preliminary Official Statement except as described herein and is not expressing any opinion as to the completeness or accuracy of theinformation contained therein. Compensation of Ehlers, payable entirely by the County, is contingent upon the sale of the issue.

COMPLIANCE WITH S.E.C. RULE 15c2-12

Certain municipal obligations (issued in an aggregate amount over $1,000,000) are subject to General Rules and Regulations, SecuritiesExchange Act of 1934, Rule 15c2-12 Municipal Securities Disclosure (the "Rule").

Preliminary Official Statement: This Preliminary Official Statement was prepared for the County for dissemination to potential customers.Its primary purpose is to disclose information regarding these Notes to prospective underwriters in the interest of receiving competitiveproposals in accordance with the sale notice contained herein. Unless an addendum is posted prior to the sale, this Preliminary OfficialStatement shall be deemed nearly final for purposes of the Rule subject to completion, revision and amendment in a Final Official Statementas defined below.

Review Period: This Preliminary Official Statement has been distributed to members of the legislative body and other public officials ofthe County as well as to prospective bidders for an objective review of its disclosure. Comments or requests for the correction of omissionsor inaccuracies must be submitted to Ehlers at least two business days prior to the sale. Requests for additional information or corrections inthe Preliminary Official Statement received on or before this date will not be considered a qualification of a proposal received from anunderwriter. If there are any changes, corrections or additions to the Preliminary Official Statement, interested bidders will be informed byan addendum at least one business day prior to the sale.

Final Official Statement: Upon award of sale of these Notes, the Preliminary Official Statement together with any previous addendum ofcorrections or additions will be further supplemented by an addendum specifying the offering prices, interest rates, aggregate principal amount,principal amount per maturity, anticipated delivery date, and Syndicate Manager and Syndicate Members, together with any other informationrequired by law, and, as supplemented, shall constitute a "Final Official Statement" of the County with respect to the Notes, as defined in theRule. Copies of the Final Official Statement will be delivered to the underwriter (Syndicate Manager) within seven business days followingthe proposal acceptance.

Continuing Disclosure: Subject to certain exemptions, issues in an aggregate amount over $1,000,000 may be required to comply withprovisions of the Rule which require that underwriters obtain from the issuers of municipal securities (or other obligated party) an agreementfor the benefit of the owners of the securities to provide continuing disclosure with respect to those securities. This Preliminary OfficialStatement describes the conditions under which these Notes are exempt or required to comply with the Rule.

CLOSING CERTIFICATES

Upon delivery of these Notes, the purchaser (underwriter) will be furnished with the following items: (1) a certificate of the appropriate officialsto the effect that at the time of the sale of these Notes and all times subsequent thereto up to and including the time of the delivery of theseNotes, this Preliminary Official Statement did not and does not contain any untrue statement of a material fact or omit to state a material factnecessary to make the statements therein, in the light of the circumstances under which they were made, not misleading; (2) a receipt signedby the appropriate officer evidencing payment for these Notes; (3) a certificate evidencing the due execution of these Notes, including statementsthat (a) no litigation of any nature is pending, or to the knowledge of signers, threatened, restraining or enjoining the issuance and delivery ofthese Notes, (b) neither the corporate existence or boundaries of the County nor the title of the signers to their respective offices is beingcontested, and (c) no authority or proceedings for the issuance of these Notes have been repealed, revoked or rescinded; and (4) a certificatesetting forth facts and expectations of the County which indicates that the County does not expect to use the proceeds of these Notes in a mannerthat would cause them to be arbitrage bonds within the meaning of Section 148 of the Internal Revenue Code of 1986, as amended, or withinthe meaning of applicable Treasury Regulations.

iii

TABLE OF CONTENTS

INTRODUCTORY STATEMENT . . . . . . . . . . . . . . . . . . . . . 1

THE NOTES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1GENERAL . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1OPTIONAL REDEMPTION . . . . . . . . . . . . . . . . . . . . . . 2AUTHORITY; PURPOSE . . . . . . . . . . . . . . . . . . . . . . . . 2ESTIMATED SOURCES AND USES . . . . . . . . . . . . . . 2SECURITY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2RATING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3CONTINUING DISCLOSURE . . . . . . . . . . . . . . . . . . . . 3LEGAL OPINION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4STATEMENT REGARDING BOND COUNSEL PARTICIPATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4TAX EXEMPTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4QUALIFIED TAX-EXEMPT OBLIGATIONS . . . . . . . . 5MUNICIPAL ADVISOR . . . . . . . . . . . . . . . . . . . . . . . . . 5MUNICIPAL ADVISOR AFFILIATED COMPANIES . 5RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

VALUATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7WISCONSIN PROPERTY VALUATIONS; PROPERTY TAXES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7CURRENT PROPERTY VALUATIONS . . . . . . . . . . . . 82015 EQUALIZED VALUE BY CLASSIFICATION . . . 8TREND OF VALUATIONS . . . . . . . . . . . . . . . . . . . . . . 8LARGER TAXPAYERS . . . . . . . . . . . . . . . . . . . . . . . . . 9

DEBT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10DIRECT DEBT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10DEBT LIMIT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10SCHEDULE OF BONDED INDEBTEDNESS . . . . . . . 11UNDERLYING DEBT . . . . . . . . . . . . . . . . . . . . . . . . . 13DEBT RATIOS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14DEBT PAYMENT HISTORY . . . . . . . . . . . . . . . . . . . . 14FUTURE FINANCING . . . . . . . . . . . . . . . . . . . . . . . . . 14

TAX LEVIES AND COLLECTIONS . . . . . . . . . . . . . . . . . . 15TAX LEVIES AND COLLECTIONS . . . . . . . . . . . . . . 15PROPERTY TAX RATES OF LARGER MUNICIPALITIES WITHIN THE COUNTY . . . . . . 16DEBT ISSUANCE CONDITIONS FOR COUNTIES . . 17LEVY LIMITS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

THE ISSUER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19COUNTY GOVERNMENT . . . . . . . . . . . . . . . . . . . . . . 19EMPLOYEES; PENSIONS . . . . . . . . . . . . . . . . . . . . . . 19FUNDS ON HAND . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20ENTERPRISE FUNDS . . . . . . . . . . . . . . . . . . . . . . . . . 20SUMMARY GENERAL FUND FINANCIAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21LIABILITIES FOR OTHER POST EMPLOYMENT BENEFITS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22LITIGATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

GENERAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . 23LOCATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23LARGER EMPLOYERS . . . . . . . . . . . . . . . . . . . . . . . . 23U.S. CENSUS DATA . . . . . . . . . . . . . . . . . . . . . . . . . . . 24EMPLOYMENT/UNEMPLOYMENT DATA . . . . . . . 24

EXCERPTS FROM FINANCIAL STATEMENTS . . . . . . . A-1

FORM OF LEGAL OPINION . . . . . . . . . . . . . . . . . . . . . . . B-1

BOOK-ENTRY-ONLY SYSTEM . . . . . . . . . . . . . . . . . . . . C-1

FORM OF CONTINUING DISCLOSURE CERTIFICATE..D-1

NOTICE OF SALE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . E-1

iv

BOARD OF SUPERVISORSTerm Expires

Gregg Moore Chairperson April 2016

Colleen Bates Vice Chairperson April 2016

Kathleen Clark Second Vice Chairperson April 2016

Corey Bauch Supervisor April 2016

Mark Beckfield Supervisor April 2016

Steve Chilson Supervisor April 2016

Mike Conlin Supervisor April 2016

Jim Dunning Supervisor April 2016

Katy Forsythe Supervisor April 2016

Gary Gibson Supervisor April 2016

Ray Henning Supervisor April 2016

Douglas Kranig Supervisor April 2016

Patrick LaVelle Supervisor April 2016

Robin Leary Supervisor April 2016

Paul Lokken Supervisor April 2016

John Manydeeds Supervisor April 2016

Joel Mikelson Supervisor April 2016

Sue Miller Supervisor April 2016

Mark Olson Supervisor April 2016

Stella Pagonis Supervisor April 2016

Paul Reck Supervisor April 2016

Stephannie Regenauer Supervisor April 2016

Jean D. Schlieve Supervisor April 2016

Tami Schraufnagel Supervisor April 2016

Nicholas Smiar Supervisor April 2016

Gordon Steinhauer Supervisor April 2016

Kevin Stelljes Supervisor April 2016

Gerald Wilkie Supervisor April 2016

Bruce Willett Supervisor April 2016

ADMINISTRATION

Kathryn Schauf, County Administrator

Janet Loomis, County Clerk

Glenda J. Lyons, County Treasurer

Scott Rasmussen, Director of Finance

PROFESSIONAL SERVICES

Quarles & Brady LLP, Bond Counsel, Milwaukee, Wisconsin

Ehlers & Associates, Inc., Municipal Advisors, Roseville, Minnesota(Other offices located in Pewaukee, Wisconsin, Chicago, Illinois and Denver, Colorado)

1

INTRODUCTORY STATEMENT

This Preliminary Official Statement contains certain information regarding Eau Claire County, Wisconsin (the"County") and the issuance of its $9,500,000* General Obligation Promissory Notes, Series 2015A (the "Notes").Any descriptions or summaries of the Notes, statutes, or documents included herein are not intended to be completeand are qualified in their entirety by reference to such statutes and documents and the form of the Notes to beincluded in the resolution authorizing the sale of the Notes ("Award Resolution") to be adopted by the Board ofSupervisors on September 15, 2015.

Inquiries may be directed to Ehlers & Associates, Inc. ("Ehlers" or the "Municipal Advisor"), Roseville, Minnesota,(651) 697-8500, the County's Municipal Advisor. A copy of this Preliminary Official Statement may be downloadedfrom Ehlers’ web site at www.ehlers-inc.com by connecting to the link to the Bond Sales and following the directionsat the top of the site.

THE NOTES

GENERAL

The Notes will be issued in fully registered form as to both principal and interest in denominations of $5,000 eachor any integral multiple thereof, and will be dated, as originally issued, as of October 7, 2015. The Notes will matureon September 1 in the years and amounts set forth on the cover of this Preliminary Official Statement. Interest willbe payable on March 1 and September 1 of each year, commencing September 1, 2016, to the registered owners ofthe Notes appearing of record in the bond register as of the close of business on the 15th day (whether or not abusiness day) of the immediately preceding month. Interest will be computed upon the basis of a 360-day year oftwelve 30-day months and will be rounded pursuant to rules of the MSRB. The rate for any maturity may not bemore than 1.00% less than the rate for any preceding maturity. (For example, if a rate of 4.50% is proposedfor the 2017 maturity, then the lowest rate that may be proposed for any later maturity is 3.50%.) All Notesof the same maturity must bear interest from date of issue until paid at a single, uniform rate. Each rate must beexpressed in an integral multiple of 5/100 or 1/8 of 1%.

Unless otherwise specified by the purchaser, the Notes will be registered in the name of Cede & Co., as nominee forThe Depository Trust Company, New York, New York ("DTC"). (See "Book-Entry-Only System" herein.) As longas the Notes are held under the book-entry system, beneficial ownership interests in the Notes may be acquired inbook-entry form only, and all payments of principal of, premium, if any, and interest on the Notes shall be madethrough the facilities of DTC and its Participants. If the book-entry system is terminated, principal of, premium, ifany, and interest on the Notes shall be payable as provided in the Award Resolution.

The County will select a bank or trust company to act as paying agent (the “Paying Agent”) or the County will actas Paying Agent. The County will pay the annual charges for Paying Agent services. If a Paying Agent is selected,the County reserves the right to remove the Paying Agent and to appoint a successor.

*Preliminary, subject to change.

2

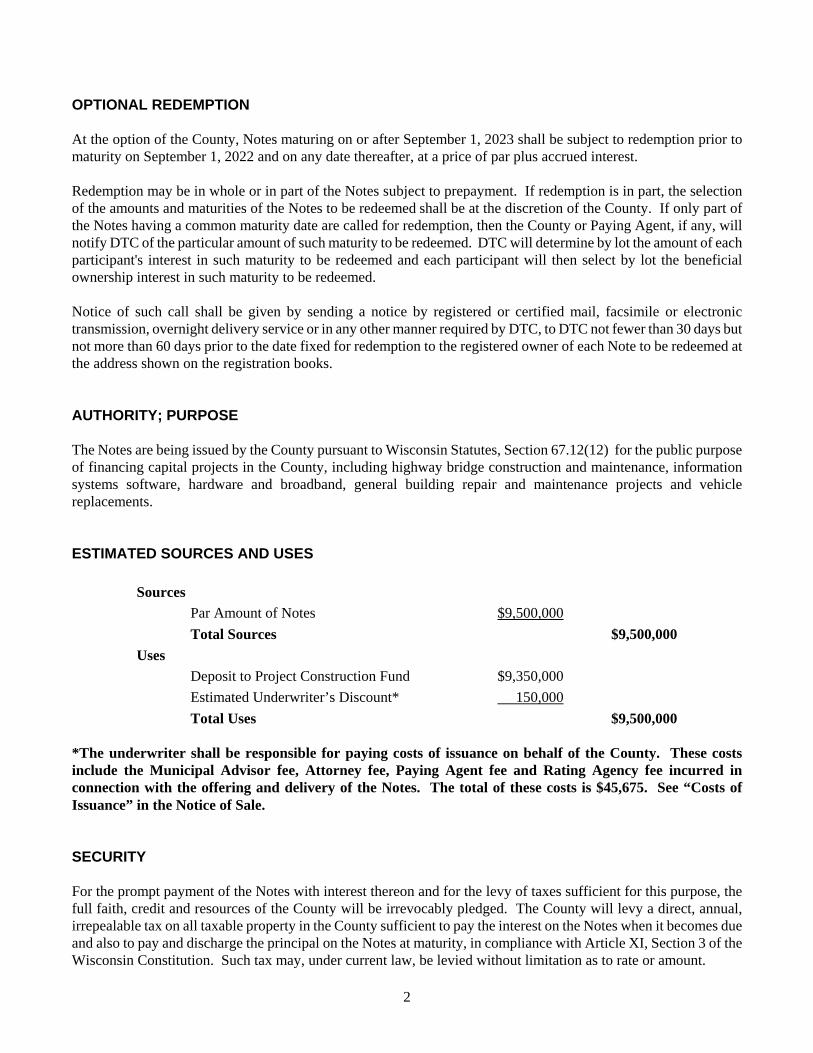

OPTIONAL REDEMPTION

At the option of the County, Notes maturing on or after September 1, 2023 shall be subject to redemption prior tomaturity on September 1, 2022 and on any date thereafter, at a price of par plus accrued interest.

Redemption may be in whole or in part of the Notes subject to prepayment. If redemption is in part, the selectionof the amounts and maturities of the Notes to be redeemed shall be at the discretion of the County. If only part ofthe Notes having a common maturity date are called for redemption, then the County or Paying Agent, if any, willnotify DTC of the particular amount of such maturity to be redeemed. DTC will determine by lot the amount of eachparticipant's interest in such maturity to be redeemed and each participant will then select by lot the beneficialownership interest in such maturity to be redeemed.

Notice of such call shall be given by sending a notice by registered or certified mail, facsimile or electronictransmission, overnight delivery service or in any other manner required by DTC, to DTC not fewer than 30 days butnot more than 60 days prior to the date fixed for redemption to the registered owner of each Note to be redeemed atthe address shown on the registration books.

AUTHORITY; PURPOSE

The Notes are being issued by the County pursuant to Wisconsin Statutes, Section 67.12(12) for the public purposeof financing capital projects in the County, including highway bridge construction and maintenance, informationsystems software, hardware and broadband, general building repair and maintenance projects and vehiclereplacements.

ESTIMATED SOURCES AND USES

Sources

Par Amount of Notes $9,500,000

Total Sources $9,500,000

Uses

Deposit to Project Construction Fund $9,350,000

Estimated Underwriter’s Discount* 150,000

Total Uses $9,500,000

*The underwriter shall be responsible for paying costs of issuance on behalf of the County. These costsinclude the Municipal Advisor fee, Attorney fee, Paying Agent fee and Rating Agency fee incurred inconnection with the offering and delivery of the Notes. The total of these costs is $45,675. See “Costs ofIssuance” in the Notice of Sale.

SECURITY

For the prompt payment of the Notes with interest thereon and for the levy of taxes sufficient for this purpose, thefull faith, credit and resources of the County will be irrevocably pledged. The County will levy a direct, annual,irrepealable tax on all taxable property in the County sufficient to pay the interest on the Notes when it becomes dueand also to pay and discharge the principal on the Notes at maturity, in compliance with Article XI, Section 3 of theWisconsin Constitution. Such tax may, under current law, be levied without limitation as to rate or amount.

3

RATING

General obligation debt of the County, with the exception of any outstanding credit enhanced issues, is currently rated"Aa1" by Moody’s Investors Service.

The County has requested a rating on this issue from Moody's Investors Service, and bidders will be notified as tothe assigned rating prior to the sale. Such a rating, if and when received, will reflect only the view of the ratingagency and any explanation of the significance of such rating may only be obtained from Moody's Investors Service.There is no assurance that such rating, if and when received, will continue for any period of time or that it will notbe revised or withdrawn. Any revision or withdrawal of the rating may have an effect on the market price of theNotes.

CONTINUING DISCLOSURE

In order to assist the Underwriters in complying with SEC Rule 15c2-12 promulgated by the Securities and ExchangeCommission, pursuant to the Securities Exchange Act of 1934 (hereinafter the "Rule"), the County shall covenantto take certain actions pursuant to a Resolution adopted by the Board of Supervisors by entering into a ContinuingDisclosure Undertaking (the "Disclosure Undertaking") for the benefit of holders, including beneficial holders. TheDisclosure Undertaking requires the County to provide electronically or in the manner otherwise prescribed certainfinancial information annually and to provide notices of the occurrence of certain events enumerated in the Rule.The details and terms of the Disclosure Undertaking for this issue are set forth in Appendix D to be executed anddelivered by the County at the time of delivery of the Notes. Such Disclosure Undertaking will be in substantiallythe form attached hereto.

In the previous five years, the County believes it has complied in all material respects with its prior undertakingsunder the Rule. A failure by the County to comply with any Disclosure Undertaking will not constitute an event ofdefault on this issue or any issue outstanding. However, such a failure may adversely affect the transferability andliquidity of the Notes and their market price. Due to widespread industry knowledge of bond insurance ratingchanges, bond insurance rating changes are not listed.

The County will file its continuing disclosure information using the Electronic Municipal Market Access ("EMMA")system or any system that may be prescribed in the future. Investors will be able to access continuing disclosureinformation filed with the MSRB at www.emma.msrb.org.

LEGAL OPINION

An opinion as to the validity of the Notes and the exemption from federal taxation of the interest thereon will befurnished by Quarles & Brady LLP, bond counsel to the County, and will accompany the Notes. The legal opinionwill be issued on the basis of existing law and will state that the Notes are valid and binding general obligations ofthe County; provided that the rights of the owners of the Notes and the enforceability of the Notes may be limitedby bankruptcy, insolvency, reorganization, moratorium, and other similar laws affecting creditors' rights and byequitable principles (which may be applied in either a legal or equitable proceeding).

4

STATEMENT REGARDING BOND COUNSEL PARTICIPATION

Bond Counsel has not assumed responsibility for this Official Statement or participated in its preparation (except withrespect to the section entitled ?Tax Exemption" in the Official Statement and the ?Form of Legal Opinion" found inthe Appendix B) and has not performed any investigation as to its accuracy, completeness or sufficiency.

TAX EXEMPTION

Quarles & Brady LLP, Milwaukee, Wisconsin, Bond Counsel, will deliver a legal opinion with respect to the federalincome tax exemption applicable to the interest on the Notes under existing law substantially in the following form:

"The interest on the Notes is excludable for federal income tax purposes from the gross income of the ownersof the Notes. The interest on the Notes is not an item of tax preference for purposes of the federal alternativeminimum tax imposed by Section 55 of the Internal Revenue Code of 1986, as amended (the "Code") oncorporations (as that term is defined for federal income tax purposes) and individuals. However, for purposesof computing the alternative minimum tax imposed on corporations, the interest on the Notes is included inadjusted current earnings. The Code contains requirements that must be satisfied subsequent to the issuanceof the Notes in order for interest on the Notes to be or continue to be excludable from gross income forfederal income tax purposes. Failure to comply with certain of those requirements could cause the intereston the Notes to be included in gross income retroactively to the date of issuance of the Notes. The Countyhas agreed to comply with all of those requirements. The opinion set forth in the first sentence of thisparagraph is subject to the condition that the County comply with those requirements. We express noopinion regarding other federal tax consequences arising with respect to the Notes."

The interest on the Notes is not exempt from present Wisconsin income or franchise taxes.

Prospective purchasers of the Notes should be aware that ownership of the Notes may result in collateral federalincome tax consequences to certain taxpayers. Bond Counsel will not express any opinion as to such collateral taxconsequences. Prospective purchasers of the Notes should consult their tax advisors as to collateral federal incometax consequences.

From time to time legislation is proposed, and there are or may be legislative proposals pending in the Congress ofthe United States that, if enacted, could alter or amend the federal tax matters referred to above or adversely affectthe market value of the Notes. It cannot be predicted whether, or in what form, any proposal that could alter one ormore of the federal tax matters referred to above or adversely affect the market value of the Notes may beenacted. Prospective purchasers of the Notes should consult their own tax advisors regarding any pending or proposedfederal tax legislation. Bond Counsel expresses no opinion regarding any pending or proposed federal tax legislation.

QUALIFIED TAX-EXEMPT OBLIGATIONS

The County will designate the Notes as "qualified tax-exempt obligations" for purposes of Section 265(b)(3) of theCode relating to the ability of financial institutions to deduct from income for federal income tax purposes, interestexpense that is allocable to carrying and acquiring tax-exempt obligations.

5

MUNICIPAL ADVISOR

Ehlers has served as Municipal Advisor to the County in connection with the issuance of the Notes. The MunicipalAdvisor will not participate in the underwriting of the Notes. The financial information included in this PreliminaryOfficial Statement has been compiled by the Municipal Advisor. Such information does not purport to be a review,audit or certified forecast of future events and may not conform with accounting principles applicable to compilationsof financial information. Ehlers is not a firm of certified public accountants. Ehlers is registered with the Securitiesand Exchange Commission and the Municipal Securities Rulemaking Board as a Municipal Advisor.

MUNICIPAL ADVISOR AFFILIATED COMPANIES

Bond Trust Services Corporation ("BTSC") and Ehlers Investment Partners, LLC ("EIP") are affiliate companies ofEhlers. BTSC is chartered by the State of Minnesota and authorized in Minnesota, Wisconsin and Illinois to transactthe business of a limited purpose Trust Company. BTSC provides Paying Agent services to debt issuers. EIP is aRegistered Investment Advisor with the Securities and Exchange Commission. EIP assists issuers with theinvestment of bond proceeds or investing other issuer funds. This includes escrow bidding agent services. Counties,such as this issuer, have or may retain BTSC and/or EIP to provide these services. If hired, BTSC and/or EIP wouldbe retained by the issuer under an agreement separate from Ehlers.

RISK FACTORS

Following is a description of possible risks to holders of these Notes without weighting as to probability. Thisdescription of risks is not intended to be all-inclusive, and there may be other risks not now perceived or listed here.

Taxes: The Notes of this offering are general obligations of the County, the ultimate payment of which rests in theCounty's ability to levy and collect sufficient taxes to pay debt service.

State Actions: Many elements of local government finance, including the issuance of debt and the levy of propertytaxes, are controlled by state government. Past and future actions of the State may affect the overall financialcondition of the County, the taxable value of property within the County, and the ability of the County to levyproperty taxes.

Property Tax Collection: Although the levying of the property tax for the payment of principal and interest on theNotes is irrepealable, and the County Clerk is mandated to carry the tax onto the rolls, the levy could be inadvertentlyomitted, causing a delay in payments when due. Property tax statements are distributed to taxpayers by the town,village and city clerks in December of the levy year. Current property tax settlement law directs counties to settlein full for all taxes levied by cities, villages, towns and school districts on or about August 20 of the collection year.

Ratings; Interest Rates: In the future, the County's credit rating may be reduced or withdrawn, or interest rates forthis type of obligation may rise generally, either possibility resulting in a reduction in the value of the Notes for resaleprior to maturity.

Tax Exemption: If the federal government taxes all or a portion of the interest on municipal bonds or notes or ifthe state government increases its tax on interest on bonds and notes, directly or indirectly, or if there is a change infederal or state tax policy, then the value of these Notes may fall for purposes of resale. Noncompliance by theCounty with the covenants in the Award Resolution relating to certain continuing requirements of the Code mayresult in inclusion of interest to be paid on the Notes in gross income of the recipient for United States income taxpurposes, retroactive to the date of issuance.

6

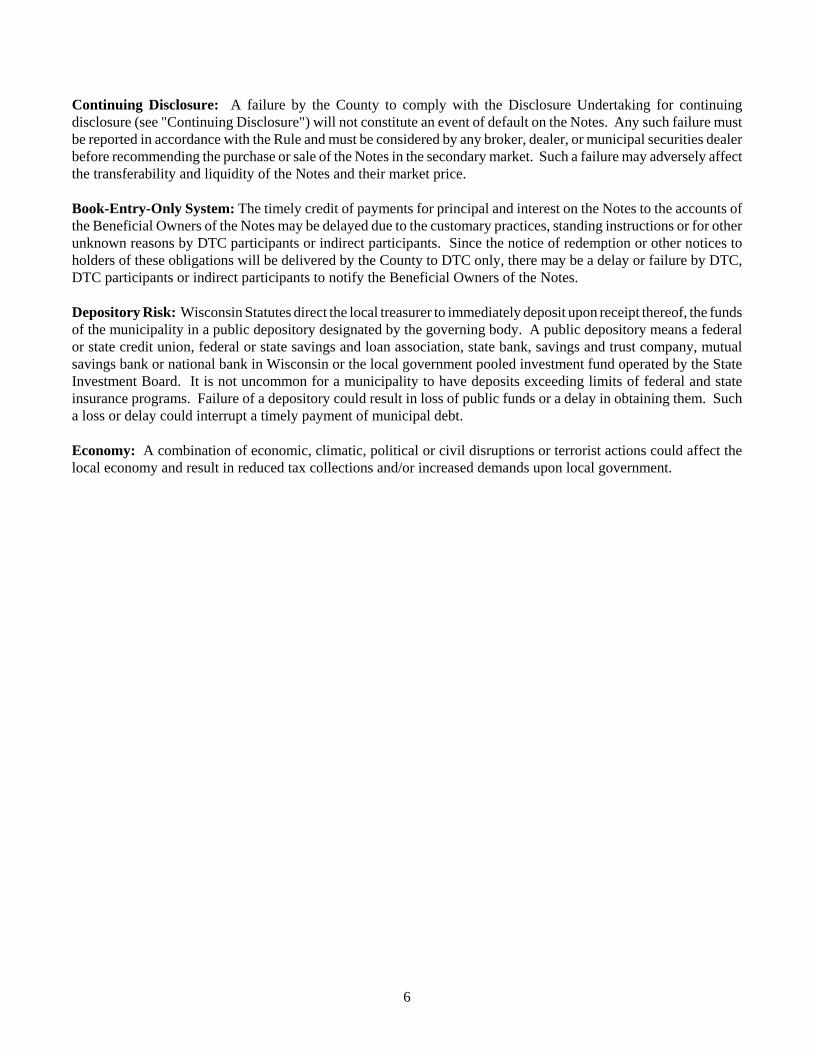

Continuing Disclosure: A failure by the County to comply with the Disclosure Undertaking for continuingdisclosure (see "Continuing Disclosure") will not constitute an event of default on the Notes. Any such failure mustbe reported in accordance with the Rule and must be considered by any broker, dealer, or municipal securities dealerbefore recommending the purchase or sale of the Notes in the secondary market. Such a failure may adversely affectthe transferability and liquidity of the Notes and their market price.

Book-Entry-Only System: The timely credit of payments for principal and interest on the Notes to the accounts ofthe Beneficial Owners of the Notes may be delayed due to the customary practices, standing instructions or for otherunknown reasons by DTC participants or indirect participants. Since the notice of redemption or other notices toholders of these obligations will be delivered by the County to DTC only, there may be a delay or failure by DTC,DTC participants or indirect participants to notify the Beneficial Owners of the Notes.

Depository Risk: Wisconsin Statutes direct the local treasurer to immediately deposit upon receipt thereof, the fundsof the municipality in a public depository designated by the governing body. A public depository means a federalor state credit union, federal or state savings and loan association, state bank, savings and trust company, mutualsavings bank or national bank in Wisconsin or the local government pooled investment fund operated by the StateInvestment Board. It is not uncommon for a municipality to have deposits exceeding limits of federal and stateinsurance programs. Failure of a depository could result in loss of public funds or a delay in obtaining them. Sucha loss or delay could interrupt a timely payment of municipal debt.

Economy: A combination of economic, climatic, political or civil disruptions or terrorist actions could affect thelocal economy and result in reduced tax collections and/or increased demands upon local government.

7

VALUATIONS

WISCONSIN PROPERTY VALUATIONS; PROPERTY TAXES

Equalized Value

Wisconsin Statutes, Section 70.57, requires the Department of Revenue to annually determine the equalized value(also referred to as full equalized value or aggregate full value) of all taxable property in each county and taxationdistrict. The equalized value is an independent estimate of value used to equate individual local assessment policiesso that property taxes are uniform throughout the various subdivisions in the State. Equalized value is calculatedbased on the history of comparable sales and information about value changes or taxing status provided by the localassessor. A comparison of the State-determined equalized value and the local assessed value, expressed as apercentage, is known as the assessment ratio or level of assessment. The Department of Revenue notifies each countyand taxing jurisdiction of its equalized value on August 15; school districts are notified on October 1. The equalizedvalue of each county is the sum of the valuations of all cities, villages, and towns within its boundaries. Taxingjurisdictions lying in more than one municipality, such as counties, school districts, or special taxing districts, usethe equalized value of the underlying units in calculating and levying their respective levies. Equalized values arealso used to apportion state aids and calculate municipal general obligation debt limits.

Assessed Value

The "assessed value" of taxable property in a municipality is determined by the local assessor, except formanufacturing properties which are valued by the State. Each city, village or town retains its own local assessor, whomust be certified by the State Department of Revenue. Assessed value is used by these municipalities to determinetax levy mill rates and to apportion levies among individual property owners. Beginning in 1986, the State requiredthat the assessed values must be within 10% of State equalized values at least once every five years. The localassessor values property as of January 1 each year and submits those values to each municipality the second Mondayin May. The assessor also reports any value changes taking place since the previous year, to the Department ofRevenue, by this same date.

8

CURRENT PROPERTY VALUATIONS

2015 Equalized Value $7,499,941,900

2015 Equalized Value Reduced by Tax Increment Valuation $7,217,049,100

2015 EQUALIZED VALUE BY CLASSIFICATION

Equalized Value Percent

Residential $4,784,838,900 63.80%

Commercial 1,889,211,000 25.19%

Manufacturing 230,763,400 3.08%

Agricultural 22,131,000 0.30%

Undeveloped 20,020,400 0.27%

AG Forest 54,580,000 0.73%

Forest 105,154,500 1.40%

Other 124,788,100 1.66%

Personal Property 268,454,600 3.58%

Total $7,499,941,900 100.00%

TREND OF VALUATIONS

Year

Equalized Value Reducedby Tax Increment

District ValueEqualized

ValuePercent Increase/Decrease

in Equalized Value

2011 $6,606,564,000 $6,727,328,500 + 0.61%

2012 6,577,462,500 6,722,050,200 - -0.08%

2013 6,744,500,200 6,907,862,700 + 2.76%

2014 6,971,604,400 7,173,688,100 + 3.85%

2015 7,217,049,100 7,499,941,900 + 4.55%

Source: Wisconsin Department of Revenue, Bureau of Equalization.

1 2015 Equalized Values are not yet available on a taxpayer basis.

9

LARGER TAXPAYERS

Taxpayer Type of Business/Property2014

Equalized Value1

Percent ofCounty's Total

EstimatedEqualized Value

Gerber Products Co./Nestle Foods Food Manufacturing $ 76,576,000 1.07%

Menard Inc. Retail 76,118,000 1.06%

Mayo Clinic Health System Medical Facility 73,080,000 1.02%

Oakwood Hills Mall Shopping Mall 72,859,000 1.02%

Keystone Corporation Investment Real Estate 41,996,000 0.59%

Marshfield Clinic Medical Facility 34,366,000 0.48%

Individual Investment Real Estate 32,752,900 0.46%

Hi-Crush Industries Sandmining and Manufacturing 28,911,200 0.40%

Arrowhead Properties LLC Investment Real Estate 26,593,100 0.37%

Royal Credit Union Financial Institution 21,834,000 0.30%

Total $485,086,200 6.76%

County's Total 2014 Equalized Value $7,173,688,100

10

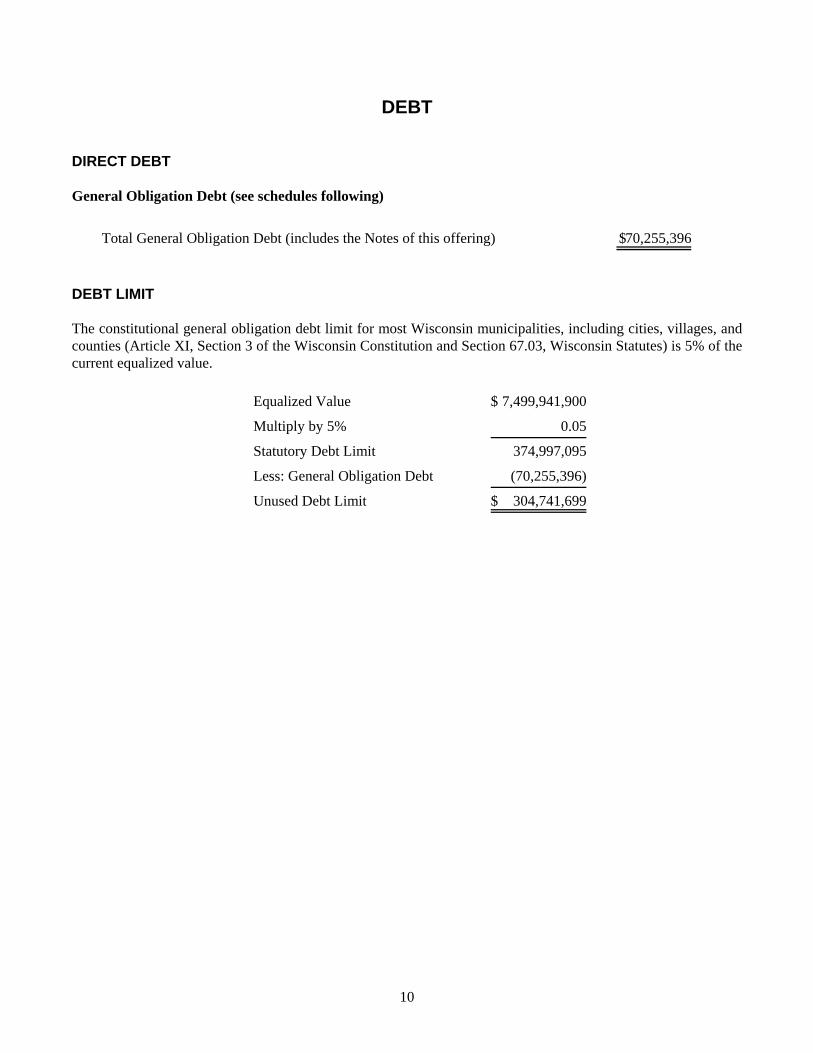

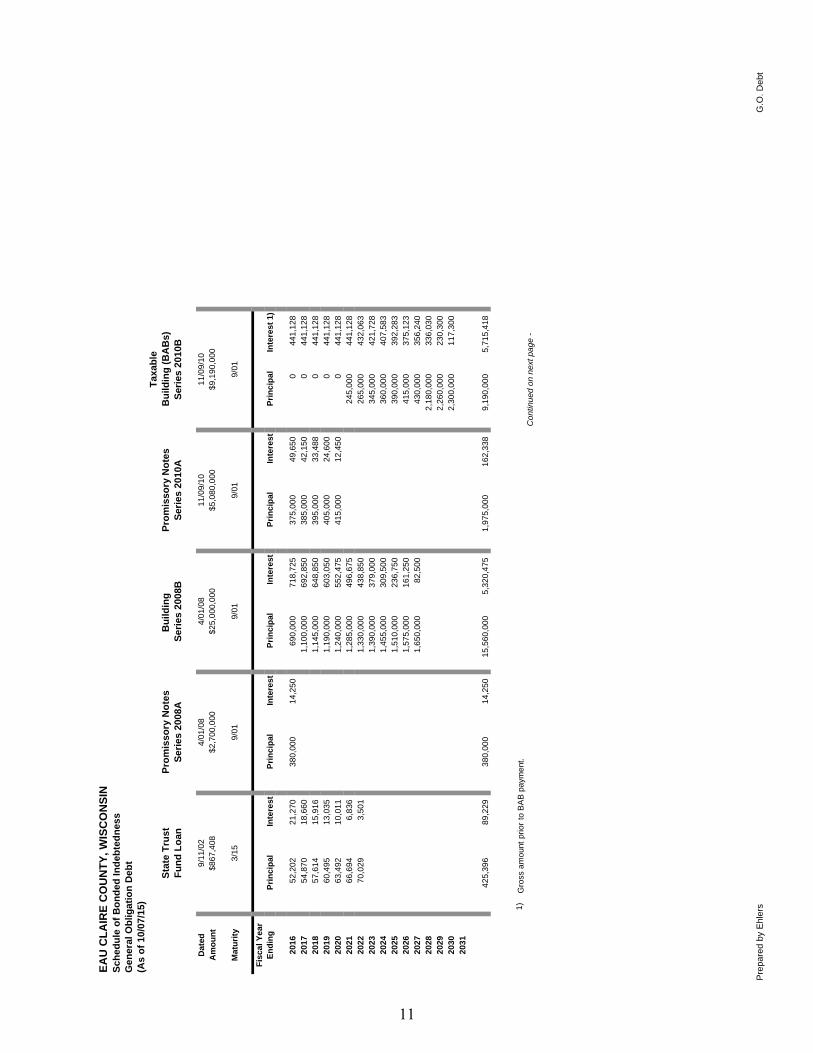

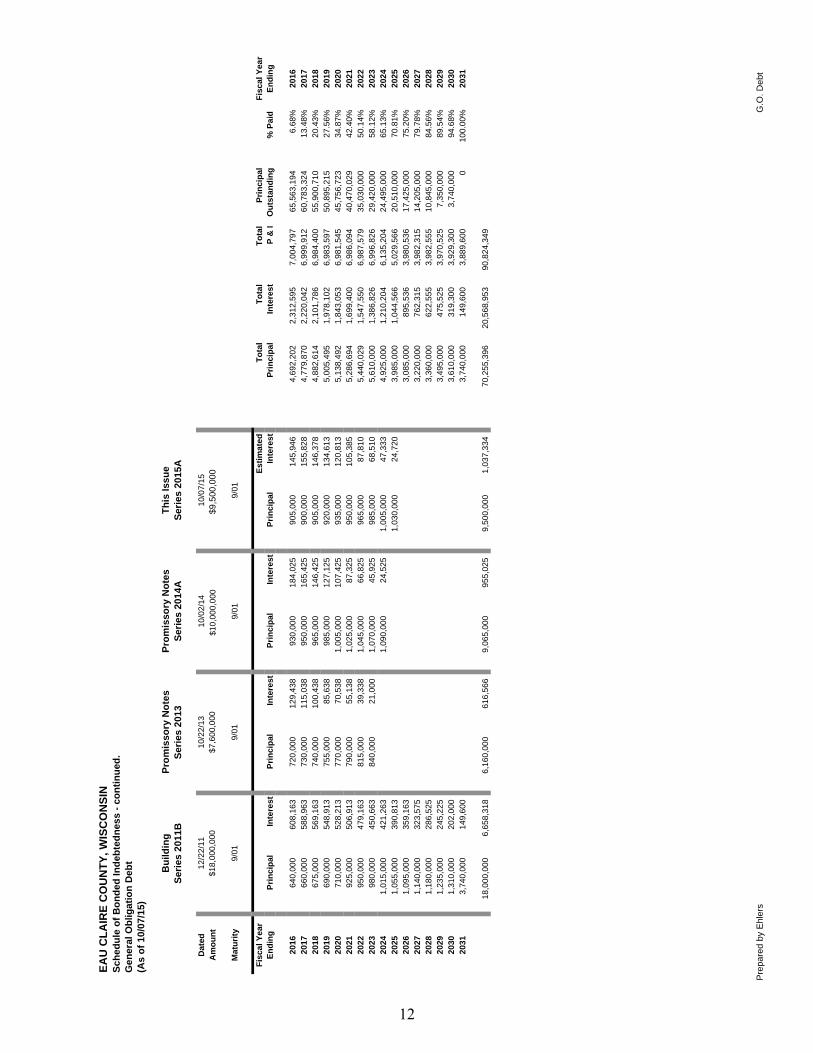

DEBT

DIRECT DEBT

General Obligation Debt (see schedules following)

Total General Obligation Debt (includes the Notes of this offering) $70,255,396

DEBT LIMIT

The constitutional general obligation debt limit for most Wisconsin municipalities, including cities, villages, andcounties (Article XI, Section 3 of the Wisconsin Constitution and Section 67.03, Wisconsin Statutes) is 5% of thecurrent equalized value.

Equalized Value $ 7,499,941,900

Multiply by 5% 0.05

Statutory Debt Limit 374,997,095

Less: General Obligation Debt (70,255,396)

Unused Debt Limit $ 304,741,699

EA

U C

LA

IRE

CO

UN

TY

, WIS

CO

NS

INS

ched

ule

of

Bo

nd

ed In

deb

ted

nes

sG

ener

al O

blig

atio

n D

ebt

Dat

edA

mo

un

t

Mat

uri

ty

Fis

cal Y

ear

En

din

gP

rin

cip

alIn

tere

stP

rin

cip

alIn

tere

stP

rin

cip

alIn

tere

stP

rin

cip

alIn

tere

stP

rin

cip

alIn

tere

st 1

)

2016

52,2

0221

,270

380,

000

14,2

5069

0,00

071

8,72

537

5,00

049

,650

044

1,12

820

1754

,870

18,6

601,

100,

000

692,

850

385,

000

42,1

500

441,

128

2018

57,6

1415

,916

1,14

5,00

064

8,85

039

5,00

033

,488

044

1,12

820

1960

,495

13,0

351,

190,

000

603,

050

405,

000

24,6

000

441,

128

2020

63,4

9210

,011

1,24

0,00

055

2,47

541

5,00

012

,450

044

1,12

820

2166

,694

6,83

61,

285,

000

496,

675

245,

000

441,

128

2022

70,0

293,

501

1,33

0,00

043

8,85

026

5,00

043

2,06

320

231,

390,

000

379,

000

345,

000

421,

728

2024

1,45

5,00

030

9,50

036

0,00

040

7,58

320

251,

510,

000

236,

750

390,

000

392,

283

2026

1,57

5,00

016

1,25

041

5,00

037

5,12

320

271,

650,

000

82,5

0043

0,00

035

6,24

020

282,

180,

000

336,

030

2029

2,26

0,00

023

0,30

020

302,

300,

000

117,

300

2031

425,

396

89,2

2938

0,00

014

,250

15,5

60,0

005,

320,

475

1,97

5,00

016

2,33

89,

190,

000

5,71

5,41

8

1)C

ontin

ued

on n

ext p

age

-

Tax

able

(As

of

10/0

7/15

)

Fu

nd

Lo

anS

erie

s 20

08A

Ser

ies

2008

BS

erie

s 20

10A

Ser

ies

2010

B

9/11

/02

4/01

/08

4/01

/08

11/0

9/10

11/0

9/10

$867

,408

$2,7

00,0

00$2

5,00

0,00

0$5

,080

,000

$9,1

90,0

00

3/15

9/01

9/01

9/01

9/01

Pro

mis

sory

No

tes

Bu

ildin

g (

BA

Bs)

Sta

te T

rust

Pro

mis

sory

No

tes

Bu

ildin

g

Gro

ss a

mo

unt

prio

r to

BA

B p

aym

ent

.

Pre

pare

d by

Ehl

ers

G.O

. Deb

t

11

EA

U C

LA

IRE

CO

UN

TY

, WIS

CO

NS

INS

ched

ule

of

Bo

nd

ed In

deb

ted

nes

s -

con

tin

ued

.

Dat

edA

mo

un

t

Mat

uri

ty

Fis

cal Y

ear

Est

imat

edT

ota

lT

ota

lT

ota

lP

rin

cip

alF

isca

l Yea

rE

nd

ing

Pri

nci

pal

Inte

rest

Pri

nci

pal

Inte

rest

Pri

nci

pal

Inte

rest

Pri

nci

pal

Inte

rest

Pri

nci

pal

Inte

rest

P &

IO

uts

tan

din

g%

Pai

d

En

din

g

2016

640,

000

608,

163

720,

000

129,

438

930,

000

184,

025

905,

000

145,

946

4,69

2,20

22,

312,

595

7,00

4,79

765

,563

,194

6.68

%20

1620

1766

0,00

058

8,96

373

0,00

011

5,03

895

0,00

016

5,42

590

0,00

015

5,82

84,

779,

870

2,22

0,04

26,

999,

912

60,7

83,3

2413

.48%

2017

2018

675,

000

569,

163

740,

000

100,

438

965,

000

146,

425

905,

000

146,

378

4,88

2,61

42,

101,

786

6,98

4,40

055

,900

,710

20.4

3%20

1820

1969

0,00

054

8,91

375

5,00

085

,638

985,

000

127,

125

920,

000

134,

613

5,00

5,49

51,

978,

102

6,98

3,59

750

,895

,215

27.5

6%20

1920

2071

0,00

052

8,21

377

0,00

070

,538

1,00

5,00

010

7,42

593

5,00

012

0,81

35,

138,

492

1,84

3,05

36,

981,

545

45,7

56,7

2334

.87%

2020

2021

925,

000

506,

913

790,

000

55,1

381,

025,

000

87,3

2595

0,00

010

5,38

55,

286,

694

1,69

9,40

06,

986,

094

40,4

70,0

2942

.40%

2021

2022

950,

000

479,

163

815,

000

39,3

381,

045,

000

66,8

2596

5,00

087

,810

5,44

0,02

91,

547,

550

6,98

7,57

935

,030

,000

50.1

4%20

2220

2398

0,00

045

0,66

384

0,00

021

,000

1,07

0,00

045

,925

985,

000

68,5

105,

610,

000

1,38

6,82

66,

996,

826

29,4

20,0

0058

.12%

2023

2024

1,01

5,00

042

1,26

31,

090,

000

24,5

251,

005,

000

47,3

334,

925,

000

1,21

0,20

46,

135,

204

24,4

95,0

0065

.13%

2024

2025

1,05

5,00

039

0,81

31,

030,

000

24,7

203,

985,

000

1,04

4,56

65,

029,

566

20,5

10,0

0070

.81%

2025

2026

1,09

5,00

035

9,16

33,

085,

000

895,

536

3,98

0,53

617

,425

,000

75.2

0%20

2620

271,

140,

000

323,

575

3,22

0,00

076

2,31

53,

982,

315

14,2

05,0

0079

.78%

2027

2028

1,18

0,00

028

6,52

53,

360,

000

622,

555

3,98

2,55

510

,845

,000

84.5

6%20

2820

291,

235,

000

245,

225

3,49

5,00

047

5,52

53,

970,

525

7,35

0,00

089

.54%

2029

2030

1,31

0,00

020

2,00

03,

610,

000

319,

300

3,92

9,30

03,

740,

000

94.6

8%20

3020

313,

740,

000

149,

600

3,74

0,00

014

9,60

03,

889,

600

010

0.00

%20

31

18,0

00,0

006,

658,

318

6,16

0,00

061

6,56

69,

065,

000

955,

025

9,50

0,00

01,

037,

334

70,2

55,3

9620

,568

,953

90,8

24,3

49

(As

of

10/0

7/15

)

Ser

ies

2011

BS

erie

s 20

13

12/2

2/11

10/2

2/13

$18,

000,

000

$7,6

00,0

00

9/01

9/01

Bu

ildin

gP

rom

isso

ry N

ote

s

9/01

Gen

eral

Ob

ligat

ion

Deb

t

Pro

mis

sory

No

tes

Ser

ies

2014

A

10/0

2/14

$10,

000,

000

Th

is Is

sue

Ser

ies

2015

A

10/0

7/15

$9,5

00,0

00

9/01

Pre

pare

d by

Ehl

ers

G.O

. Deb

t

12

1 Only those taxing jurisdictions with general obligation debt outstanding are included in this section.

2 2014 equalized values are shown for school districts and technical college districts, due to 2015equalized values not being available yet.

13

UNDERLYING DEBT1

Taxing District

2015EqualizedValuation

%In County

TotalG.O. Debt

County'sProportionate

Share

Cities of:

Altoona $ 535,775,700 100.00% $ 13,445,000 $13,445,000

Augusta 86,557,400 100.00% 1,874,450 1,874,450

Eau Claire 4,664,452,100 96.35% 101,115,000 97,426,204

Villages of:

Fall Creek 64,228,600 100.00% 422,708 422,708

Fairchild 12,471,900 100.00% 131,787 131,787

Towns of:

Bridge Creek 154,869,800 100.00% 59,155 59,155

Clear Creek 56,564,000 100.00% 79,413 79,413

Drammen 66,272,900 100.00% 51,277 51,277

Fairchild 28,685,300 100.00% 80,000 80,000

Seymour 273,570,100 100.00% 581,246 581,246

Union 344,364,600 100.00% 129,534 129,534

School Districts of:2

Altoona 632,066,819 100.00% 24,085,000 24,085,000

Augusta 311,892,608 100.00% 8,422,000 8,422,000

Cadott 316,987,376 0.61% 12,040,555 73,992

Eau Claire Area 5,969,732,422 95.45% 51,530,000 49,183,898

Eleva-Strum 233,110,850 24.00% 1,993,359 478,393

Elk Mound Area 299,772,706 3.54% 7,670,000 271,379

Fall Creek 280,897,565 100.00% 4,860,000 4,860,000

Mondovi 377,460,204 21.12% 3,719,669 785,737

Osseo-Fairchild 382,607,560 21.63% 12,085,000 2,614,357

Stanley-Boyd Area 335,815,875 4.38% 1,000,000 43,812

Technical College Districts of:

Chippewa Valley 21,548,825,671 33.29% 29,800,000 9,920,536

14

County's Share of Total Underlying Debt $215,019,877

DEBT RATIOS

G.O. Debt

Debt/EqualizedValue

$7,499,941,900

Debt/Per Capita

100,477

Total General Obligation Debt $ 70,255,396 0.94% $ 699.22

County's Share of Total Underlying Debt 214,888,090 2.87% 2,138.68

Total $285,143,486 3.81% $2,837.90

DEBT PAYMENT HISTORY

The County has never defaulted in the payment of principal and interest on its debt.

FUTURE FINANCING

The County reports no plans for additional financing in the next three months.

15

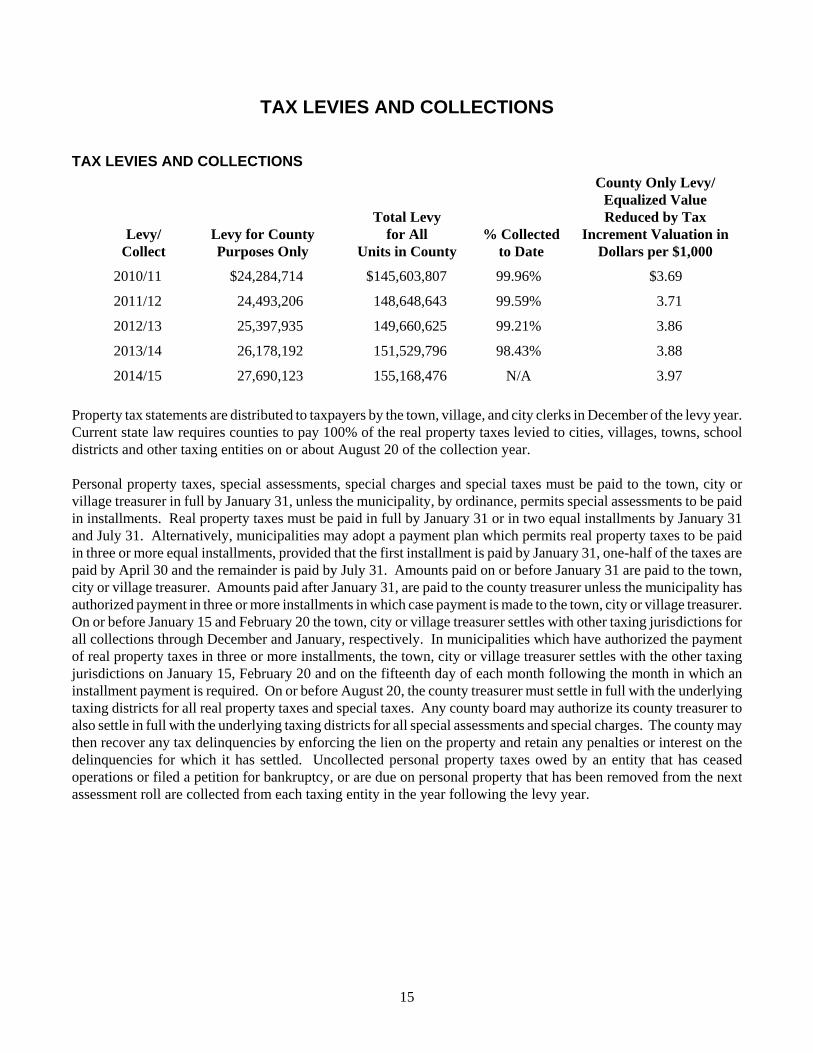

TAX LEVIES AND COLLECTIONS

TAX LEVIES AND COLLECTIONS

Levy/Collect

Levy for CountyPurposes Only

Total Levyfor All

Units in County% Collected

to Date

County Only Levy/Equalized ValueReduced by Tax

Increment Valuation inDollars per $1,000

2010/11 $24,284,714 $145,603,807 99.96% $3.69

2011/12 24,493,206 148,648,643 99.59% 3.71

2012/13 25,397,935 149,660,625 99.21% 3.86

2013/14 26,178,192 151,529,796 98.43% 3.88

2014/15 27,690,123 155,168,476 N/A 3.97

Property tax statements are distributed to taxpayers by the town, village, and city clerks in December of the levy year.Current state law requires counties to pay 100% of the real property taxes levied to cities, villages, towns, schooldistricts and other taxing entities on or about August 20 of the collection year.

Personal property taxes, special assessments, special charges and special taxes must be paid to the town, city orvillage treasurer in full by January 31, unless the municipality, by ordinance, permits special assessments to be paidin installments. Real property taxes must be paid in full by January 31 or in two equal installments by January 31and July 31. Alternatively, municipalities may adopt a payment plan which permits real property taxes to be paidin three or more equal installments, provided that the first installment is paid by January 31, one-half of the taxes arepaid by April 30 and the remainder is paid by July 31. Amounts paid on or before January 31 are paid to the town,city or village treasurer. Amounts paid after January 31, are paid to the county treasurer unless the municipality hasauthorized payment in three or more installments in which case payment is made to the town, city or village treasurer.On or before January 15 and February 20 the town, city or village treasurer settles with other taxing jurisdictions forall collections through December and January, respectively. In municipalities which have authorized the paymentof real property taxes in three or more installments, the town, city or village treasurer settles with the other taxingjurisdictions on January 15, February 20 and on the fifteenth day of each month following the month in which aninstallment payment is required. On or before August 20, the county treasurer must settle in full with the underlyingtaxing districts for all real property taxes and special taxes. Any county board may authorize its county treasurer toalso settle in full with the underlying taxing districts for all special assessments and special charges. The county maythen recover any tax delinquencies by enforcing the lien on the property and retain any penalties or interest on thedelinquencies for which it has settled. Uncollected personal property taxes owed by an entity that has ceasedoperations or filed a petition for bankruptcy, or are due on personal property that has been removed from the nextassessment roll are collected from each taxing entity in the year following the levy year.

16

PROPERTY TAX RATES OF LARGER MUNICIPALITIES WITHIN THE COUNTY

Full value rates for property taxes expressed in dollars per $1,000 of equalized value (excluding TIF) that have beencollected in recent years have been as follows:

Year Levied/Year Collected Schools1 County Local Other2

Total Full ValueEffective Rate3

City of Altoona

2010/11 $10.79 $3.93 $6.12 $0.47 $21.63

2011/12 11.17 3.95 6.11 0.51 23.16

2012/13 11.43 4.00 6.11 0.50 23.92

2013/14 11.51 4.02 6.11 0.51 24.15

2014/15 12.64 4.07 6.11 0.55 27.51

City of Eau Claire

2010/11 $11.79 $3.53 $8.14 $0.20 $22.44

2011/12 11.92 3.55 8.35 0.20 22.82

2012/13 11.87 3.60 8.52 0.20 23.03

2013/14 11.31 3.65 8.75 0.17 22.84

2014/15 10.76 3.75 8.72 0.20 22.40

Source: Property Tax Rates were extracted from bulletins prepared by the Wisconsin Department of Revenue,Division of State and Local Finance.

17

DEBT ISSUANCE CONDITIONS FOR COUNTIES

Wisconsin counties may not issue general obligation bonds or promissory notes unless the county qualifies for oneof the exceptions allowed under the statute, as described below.

General obligation bonds or notes can be issued by a county only if one of the following conditions is met: (a) thebonds or notes are approved at a referendum; (b) the county board adopts a resolution that sets forth its reasonableexpectation that the issuance will not cause the county to exceed its debt levy rate limit; (c) the debt is issued forregional projects; (d) the debt is issued to refund existing debt or (e) the resolution authorizing the debt is approvedby a vote of at least 3/4 of the members elect of the county board. In addition, counties generally are prohibited fromusing the proceeds of general obligation bonds or notes to fund the operating expenses of the general fund of thecounty or to fund the operating expenses of any special revenue fund of the county that is supported by propertytaxes, although this prohibition does not apply to notes issued to pay unfunded prior service liability contributions.

The resolution authorizing the issuance of the Notes as adopted by at least 3/4 of the members elect of the CountyBoard.

LEVY LIMITS

Section 66.0602 of the Wisconsin Statutes, imposes a limit on property tax levies by cities, villages, towns andcounties. No city, village, town or county is permitted to increase its tax levy by a percentage that exceeds itsvaluation factor (which is defined as a percentage equal to the greater of the percentage change in the politicalsubdivision's January 1 equalized value due to new construction less improvements removed or zero percent). Thebase amount in any year to which the levy limit applies is the actual levy for the immediately preceding year. Thislevy limitation is an overall limit, applying to levies for operations as well as for other purposes.

A political subdivision that did not levy its full allowable levy in the prior year can carry forward the differencebetween the allowable levy and the actual levy, up to a maximum of 1.5% of the prior year's actual levy. The useof the carry forward levy adjustment needs to be approved by a majority vote of the political subdivision's governingbody (except in the case of towns) if the amount of carry forward levy adjustment is less than or equal to 0.5% andby a super majority vote of the political subdivision's governing body (three-quarters vote if the governing body iscomprised of five or more members, two-thirds vote if the governing body is comprised of fewer than five members)(except in the case of towns) if the amount of the carry forward levy adjustment is greater than 0.5% up to themaximum increase of 1.5%. For towns, the use of the carry forward levy adjustment needs to be approved by amajority vote of the annual town meeting or special town meeting after the town board has adopted a resolution infavor of the adjustment by a majority vote if the amount of carry forward levy adjustment is less than or equal to 0.5%or by two-thirds vote or more if the amount of carry forward levy adjustment is greater than 0.5% up to the maximumof 1.5%.

Special provisions are made with respect to property taxes levied to pay general obligation debt service. Those aredescribed below. In addition, the statute provides for certain other exclusions from and adjustments to the tax levylimit. Among the items excluded from the limit are amounts levied for any revenue shortfall for debt service on arevenue bond issued under Section 66.0621. Among the adjustments permitted is an adjustment applicable when atax increment district terminates, which allows an amount equal to the prior year's allowable levy multiplied by 50%of the political subdivision's percentage growth due to the district's termination.

18

With respect to general obligation debt service, the following provisions are made:

(a) If a political subdivision's levy for the payment of general obligation debt service, including debt service on debtissued or reissued to fund or refund outstanding obligations of the political subdivision and interest on outstandingobligations of the political subdivision, on debt originally issued before July 1, 2005, is less in the current year thanin the previous year, the political subdivision is required to reduce its levy limit in the current year by the amount ofthe difference between the previous year's levy and the current year's levy.

(b) For obligations authorized before July 1, 2005, if the amount of debt service in the preceding year is less thanthe amount of debt service needed in the current year, the levy limit is increased by the difference between the twoamounts. This adjustment is based on scheduled debt service rather than the amount actually levied for debt service(after taking into account offsetting revenues such as sales tax revenues, special assessments, utility revenues, taxincrement revenues or surplus funds). Therefore, the levy limit could negatively impact political subdivisions thatexperience a reduction in offsetting revenues.

(c) The levy limits do not apply to property taxes levied to pay debt service on general obligation debt authorizedon or after July 1, 2005.

The Notes were authorized after July 1, 2005 and therefore the levy limits do not apply to taxes levied to pay debtservice on the Notes.

19

THE ISSUER

COUNTY GOVERNMENT

The County was organized in 1856 and is governed by a 29-member Board of Supervisors. All are elected to two-year terms. Current terms all expire in 2016. The appointed County Administrator and elected County Clerk andCounty Treasurer are responsible for administrative details and financial records.

EMPLOYEES; PENSIONS

The County has 502 full-time, 49 part-time and 47 seasonal employees. The County is a participant in the WisconsinRetirement System (WRS) covering all protective employees on a non-contributory basis. The annual employer'scontribution rate, which is actuarially determined by the State, provides for funding of prior service costs, includinginterest, over 40 years beginning January 1, 1990. See the Notes to Financial Statements in Appendix A for a detaileddescription of the plan.

Recognized and Certified Bargaining Units

All eligible County personnel are covered by the Municipal Employment Relations Act (MERA) of the WisconsinStatutes. Pursuant to that law, employees have limited rights to organize and collectively bargain with the municipalemployers. MERA was amended by 2011 Wisconsin Act 10 (the "Act") and by 2011 Wisconsin Act 32, which alteredthe collective bargaining rights of public employees in Wisconsin.

Certain legal challenges have been brought with respect to the Act. On May 26, 2011, the Dane County Circuit Court(the "Circuit Court") issued a decision which voided the legislative action taken with respect to the Act due toviolations of the State's Open Meetings Law. However, on June 14, 2011, the Supreme Court of Wisconsinoverturned the Circuit Court's decision by vacating and declaring all orders and judgments of the Circuit Court withrespect to the Act to be void. As a result, the Act took effect on June 29, 2011, the day after it was published inaccordance with State statutes.

As a result of the amendments to MERA, the County is prohibited from bargaining collectively with municipalemployees, other than public safety or transit employees, with respect to any factor or condition of employmentexcept total base wages. The County or employee union has the option to pursue mediation and grievance arbitration.Voluntary impasse resolution procedures are prohibited for municipal employees, other than public safety or transitemployees, including binding interest arbitration. Strikes by any municipal employee or labor organization areexpressly prohibited. As a practical matter, it is anticipated that strikes will be rare. Furthermore, if strikes do occur,they may be enjoined by the courts. Impasse resolution for public safety or transit employees is subject to final andbinding arbitration procedures, which do not include a right to strike. Interest arbitration is available for transitemployees if certain conditions are met.

On September 14, 2012, the Circuit Court issued a decision which declared that certain portions of the Act violatedState Constitutional rights to freedom of speech and association and equal protection, including portions of the Actthat prohibit collectively bargaining with municipal employees with respect to any factor or condition of employmentexcept total base wages. On September 18, 2012, the State Attorney General filed an appeal to the Circuit Court’sdecision and requested a stay on the enforcement of the decision until such an appeal is decided. On October 22,2012, the Circuit Court denied the motion for the stay until the appeal is decided. As a consequence, until the appealis decided, local governments and school districts may be prohibited from following the portions of the Act that havebeen found unconstitutional. The outcome of these legal proceedings cannot be predicted at this time.

The following bargaining units represent employees of the County:

Union Contract Expires

Sheriff Non-Supervisory December 31, 2015

FUNDS ON HAND (including investments, as of June 30, 2015)

Fund Amount

Demand and Time Deposits $10,372,599

U.S. Agencies 1,913,530

Commercial Paper 6,068,084

WMMIC Escrow Pool 240,324

LGIP 4,191,175

Petty Cash 3,770

Total Funds on Hand $22,789,482

ENTERPRISE FUNDS

Cash flows for the County's enterprise funds have been as follows as of December 31 each year:

2012 2013 2014

Highway Department

Total Operating Revenues $ 7,916,628 $ 8,923,162 $ 9,033,867

Less: Operating Expenses (14,798,223) (16,270,547) (13,058,899)

Operating Income $ (6,881,595) $ (7,347,385) $ (4,025,032)

Plus: Depreciation 475,879 469,399 469,339

Revenues Available for Debt Service $ (6,405,716) $ (6,877,986) $ (3,555,693)

Airport

Total Operating Revenues $ 998,198 $ 978,224 $ 964,053

Less: Operating Expenses (1,980,737) (2,157,742) (2,394,298)

Operating Income $ (982,539) $ (1,179,518) $ (1,430,245)

Plus: Depreciation 1,184,016 1,309,603 1,379,559

Revenues Available for Debt Service $ 201,477 $ 130,085 $ (50,686)

20

21

SUMMARY GENERAL FUND FINANCIAL INFORMATION

Following are summaries of the revenues and expenditures and fund balances for the County's General Fund for the fiscal yearsshown below. These summaries are not purported to be the complete audited financial statements of the County. Copies of thecomplete audited financial statements are available upon request. See Appendix A for excerpts from the County's 2014 auditedfinancial statements.

FISCAL YEAR ENDING DECEMBER 31GENERAL FUND 2010 2011 2012 2013 2014REVENUES

Taxes $16,206,270 $17,208,468 $19,057,958 $19,444,906 $20,666,222Intergovernmental 6,687,423 5,629,066 4,757,223 4,740,452 5,010,810Licenses and permits 205,099 222,197 263,875 301,688 320,502Fines, forfeitures and penalties 949,686 850,094 785,328 833,113 735,178Public charges for services 2,687,209 2,498,028 2,948,007 2,907,755 3,798,280Intergovernmental charges for services 1,073,468 1,438,103 1,268,841 1,530,386 1,808,627Investment income 296,853 232,891 256,436 111,549 92,746Miscellaneous 922,482 794,114 837,633 1,199,043 1,464,687

Total Revenues $29,028,490 $28,872,961 $30,175,301 $31,068,892 $33,897,052

ExpendituresCurrent General government $10,035,022 $10,520,810 $10,841,775 $11,358,549 $11,977,645 Public safety 11,820,508 12,511,891 12,812,378 13,535,660 13,755,155 Public works 26,594 0 0 647 0 Health and human services 2,259,436 2,210,114 2,124,822 2,296,171 2,269,770 Culture, recreation, and education 1,603,222 1,600,376 1,529,750 1,534,341 1,637,030 Conservation and development 3,074,382 2,004,795 2,002,975 2,239,631 2,568,583

Debt Service 56,651 36,374 0 0 0

Total Expenditures $28,875,815 $28,884,360 $29,311,700 $30,964,999 $32,208,183

Excess of revenues over (under)expenditures

$152,675 ($11,399) $863,601 $103,893 $1,688,869

Other Financing Sources (Uses)Operating transfers in 2,027,800 1,636,930 131,352 0 0Operating transfers out (154,887) (164,990) (149,051) (153,773) (165,942)Total Other Financing Sources (Uses) $1,872,913 $1,471,940 ($17,699) ($153,773) ($165,942)

Excess of revenues and other financingsources over (under) expenditures andother uses

$2,025,588 $1,460,541 $845,902 ($49,880) $1,522,927

General Fund Balance January 1 9,098,148 11,123,736 11,843,576 12,689,478 12,276,784Residual Equity Transfer in (out) 0 (740,701) 0 (362,814) 2,000

General Fund Balance December 31 $11,123,736 $11,843,576 $12,689,478 $12,276,784 $13,801,711

DETAILS OF 12/31 FUND BALANCEReserved $3,822,620 $0 $0 $0 $0Unreserved:

Designated 4,356,656 0 0 0 0Undesignated 2,944,460 0 0 0 0

Nonspendable 0 2,970,669 2,939,897 2,993,966 1,362,627Assigned 0 1,035,756 912,700 736,200 815,318Unassigned 0 7,837,151 8,836,881 8,546,618 11,623,766

Total $11,123,736 $11,843,576 $12,689,478 $12,276,784 $13,801,711

22

LIABILITIES FOR OTHER POST EMPLOYMENT BENEFITS

The County does not pay directly for retirees’ post-employment benefits. The County has some obligations for post-employment benefits as mandated by State Statutes. Specifically, the County is required to allow retirees to becovered by the County’s health care plan as long as the retiree pays his/her premiums. Retiree membership in ahealth care plan typically increases costs of the premiums. This increased cost is commonly known as implicit pricesubsidy.

LITIGATION

There is no litigation threatened or pending questioning the organization or boundaries of the County or the right ofany of its officers to their respective offices or in any manner questioning their rights and power to execute anddeliver these Notes or otherwise questioning the validity of these Notes.

The County Attorney reports that any litigation and claims currently pending against the County are being handledby the County's insurance carrier or outside counsel and will not affect the issuance of these Notes.

1 Includes corporate headquarters.

2 Includes classified and unclassified staff. In addition, 2,732 students are employed by the University.

3 Includes full-time, part-time, temporary and seasonal employees.

23

GENERAL INFORMATION

LOCATION

The Eau Claire County, with a 2010 U.S. Census population of 98,736, and a current estimated population of100,477, comprises an area of 645 square miles and is located approximately 107 miles east of the Minneapolis-St.Paul, Minnesota metropolitan area. For additional information regarding the County, please visit its website atwww.co.eau-claire.wi.us.

LARGER EMPLOYERS

Larger employers in the County include the following:

Firm Type of Business/Product

EstimatedNo. of

Employees

Luther Midelfort Mayo Health System Health care 3,604

Menard’s1 Retail 2,500

United Health Group Health insurance 1,600

Sacred Heart Hospital Hospitals 1,400

University of Wisconsin-Eau Claire Post-secondary education 1,3912

Eau Claire Area School District Elementary and secondary education 1,388

City of Eau Claire Municipal government and services 1,2603

Chippewa Valley Technical College Post-secondary education 1,154

Hutchinson Technology Inc. Computer storage device manufacturer 750

Eau Claire County County government and services 598

Source: ReferenceUSA, written and telephone survey (August 2015), Wisconsin Manufacturers Register, and theWisconsin Department of Workforce Development.

24

U.S. CENSUS DATA

Population Trend: Eau Claire County

2000 U.S. Census 93,142

2010 U.S. Census 98,736

2014 Estimated Population 100,477

Percent of Change 2000-2010 + 6.01%

Income and Age Statistics

Eau ClaireCounty

State ofWisconsin

UnitedStates

2013 per capita income $25,287 $27,523 $28,155

2013 median household income $48,090 $52,413 $53,046

2013 median family income $67,630 $66,534 $64,719

2013 median gross rent $699 $759 $9042013 median value owner occupied units $150,000 $167,100 $176,700

2013 median age 33.5 yrs. 38.7 yrs. 37.3 yrs.

State of Wisconsin United States

County % of 2013 per capita income 89.81% 89.81%County % of 2013 median family income 104.50% 104.50%

Housing Statistics

Eau Claire County

2000 2013 Percent of Change

All Housing Units 37,474 42,278 12.82%

Source: 2000 and 2010 Census of Population and Housing, and 2013 American Community Survey (Based on afive-year estimate), U.S. Census Bureau (www.factfinder2.census.gov).

EMPLOYMENT/UNEMPLOYMENT DATA

Average Employment Average Unemployment Rate

Year Eau Claire County Eau Claire County State of Wisconsin

2011 54,040 6.4% 7.8%

2012 54,881 5.8% 7.0%

2013 54,738 5.7% 6.8%

2014 55,653 4.6% 5.5%

2015, June 55,428 4.3% 4.9%

Source: Wisconsin Department of Workforce Development.

A-1

APPENDIX A

EXCERPTS FROM FINANCIAL STATEMENTS

Reproduced on the following pages are excerpts from the County's audited Financial Statements for the fiscal yearending December 31, 2014. The Financial Statements have been prepared by the County and audited by a certifiedpublic accountant. The Management’s Discussion and Analysis and the Notes to Financial Statements are an integralpart of the audit and any judgment of the Financial Statements should be based on the Financial Statements as awhole.

Copies of the complete audited financial statements for the past three years and the current budget are available uponrequest from Ehlers.

A-2

A-3

A-4

A-5

A-6

A-7

A-8

A-9

A-10

A-11

A-12

A-13

A-14

A-15

A-16

A-17

A-18

A-19

A-20

A-21

A-22

A-23

A-24

A-25

A-26

A-27

A-28

A-29

A-30

A-31

A-32

A-33

A-34

B-1

APPENDIX B

FORM OF LEGAL OPINION

Re: Eau Claire County, Wisconsin ("Issuer")$9,500,000 General Obligation Promissory Notes, Series 2015A,dated October 7, 2015 ("Notes")

We have acted as bond counsel to the Issuer in connection with the issuance of the Notes. In suchcapacity, we have examined such law and such certified proceedings, certifications, and other documentsas we have deemed necessary to render this opinion.

Regarding questions of fact material to our opinion, we have relied on the certified proceedings andother certifications of public officials and others furnished to us without undertaking to verify the same byindependent investigation.

The Notes are numbered from R-1 and upward; bear interest at the rates set forth below; and matureon September 1 of each year, in the years and principal amounts as follows:

Year Principal Amount Interest Rate2016 $ 905,000 ____%2017 900,000 ____ 2018 905,000 ____ 2019 920,000 ____ 2020 935,000 ____ 2021 950,000 ____ 2022 965,000 ____ 2023 985,000 ____ 2024 1,005,000 ____ 2025 1,030,000 ____

Interest is payable semi-annually on March 1 and September 1 of each year commencing on September 1,2016.

The Notes maturing on September 1, 2023 and thereafter are subject to redemption prior to maturity,at the option of the Issuer, on September 1, 2022 or on any date thereafter. Said Notes are redeemable asa whole or in part, and if in part, from maturities selected by the Issuer and within each maturity, by lot, atthe principal amount thereof, plus accrued interest to the date of redemption.

[The Notes maturing in the years ______, ______ and ______ are subject to mandatory redemptionby lot as provided in the resolution authorizing the Notes at the redemption price of par plus accrued interest