+91 9940680500 +91 9900093129+91 9940680500 +91 …casconline.org/images/casc bulletin december...

TRANSCRIPT

+91 9940680500 +91 9900093129+91 9940680500 +91 9900093129

in CCH iFirmin CCH iFirmin CCH iFirm

3CASC BULLETIN, DECEMBER 2017

EDITORIALDirect Taxes – Reforms Restart!The Government is continuing the path ofreforms, after getting the GST – the biggestIndirect Taxes Reforms – rolled out thoughyet to be successfully completed, has nowthought of Direct Taxes Reforms. In thisdirection it has constituted a task force fordrafting a new direct tax Legislationwherein there seven members have beennominated. It is interesting to see thecombination of members of the committee,the members drawn are not from theDepartment or Government. One of themember is from ICRIER, New Delhi, andaccording to their website the Research istheir prime academic activity. However,the three professional bodies whosemembers are actively involved in the at theimplementation level of any taxation lawin the country as well as are the guidinginstitution for its members as well asbusiness organisation are not part of thiscommittee, though there is one CharteredAccountant, in his individual capacity,nominated to the Committee and anotherChartered Accountant in his capacityChairman of India region,

Chairman of Emerging MarketsCommittee, EY and his profile does statethat he was part of the Justice EaswarCommittee.

The process of forming Committees andthereafter implementing in bits and pieces,the recommendations of the Committeeseven without reasoning why the same arenot implemented, has become part and

parcel of every Government. John MathaiCommittee was appointed by theGovernment of India on 1st April, 1953,with “Terms of reference to examine theincidence and suitability of central, Stateand Local taxation on various classes ofpeople and in particular with regard to (a)modification required in present system oftaxation and (b) fresh avenues of taxation.”

In 1956 Government of India hadrequested Mr. Nicholas Kaldor, a BritishEconomist, and formed a committeeheaded by him, to have a review of IndianTax System and based on itsrecommendation came the Wealth Tax,Capital gains Tax, Gift Tax and a personalexpenditure tax . Based on therecommendations of Prof. NicholasKaldor, the Wealth Tax Act, 1957, theExpenditure Tax Act, 1957 and the GiftTax Act, 1958 were introduced.

Committee for rationalization andsimplification of tax structure(Bhoothalingam Committee) submitted itsreport in 1967. Based on itsrecommendations, Summary AssessmentScheme was first introduced in 1968.

In 1970, a committee was constituted underthe name Direct Taxes Inquiry Committeeheaded by Justice K. N. Wanchoo as itschairman. The terms of reference was torecommend concrete and effective measureto unearth black money, to check taxavoidance through legal devices, includingformation of Trusts and to reduce taxarrears. The Committee recommended

4CASC BULLETIN, DECEMBER 2017

“reduction in tax rates, minimisation ofcontrols and licences, regulation ofdonation to political parties, creation ofconfidence among small tax payers,substitution of sales tax by excise duty,vigorous prosecution policy andcompulsory maintenance of accounts”.

In 1972, a committee on taxation ofagricultural income and wealth wasconstituted under the Chairmanship of Mr.K. N. Raj, to examine the present systemof taxation and the committeerecommended “partial integration ofagricultural incomes with non-agricultural incomes for the limitedpurposes of determining the rates oftaxation.”

Settlement Commission was establishedin 1976 on the basis of recommendationsof Wanchoo Committee.Based on therecommendations of Choksi Committee,Appellate functions were given to a newcadre of Commissioners known as CIT(Appeals) in the year 1978.

L. K. Jha Committee was set up forsimplification and rationalisation of taxlaws in 1987. The Direct Tax Law(Amendment) Act, 1987 introduceduniform previous year and brought aboutre-designation of ITO Group A asAssistant Commissioner of Income Tax,etc.

n 1991, the Dr. Raja J. Chellaiah committeewas constituted to examine the structureof direct and indirect taxes. The Committeerecommended restructuring and

rationalisation of personal Income Tax,Corporate Income Tax, wealth tax, Exciseduties, import tariffs, tax administrationand enforcement machinery. It alsorecommended a new tax regime calledservice tax.

In 2002, the Government of India had setup the Direct and Indirect Tax ReformsCommittee under the Chairmanship of Dr.Vijay L. Kelkar, with major terms ofreference being to recommend measuressimplification and rationalisation of directand indirect taxation.

The above is part of history (Source: Athesis submitted by CA. Prabhakar GovindKulkarni for the award of the degree ofDoctor of Philosophy in Commerce andManagement – Shivaji University, Kolhapuras well as Publication by Director ofIncome Tax (PR, PP & OL)) which majorityof us would not had occasion to have heardof or known about. Thereafter many morecommittees have been setup andrecommendation thereto has been receivedlike the Standing Committee of Direct taxesCode, 2010, Justice RV Easwar Committeeon Tax Simplification, 2015, Dr.Parthasarathi Shome Committee on the taxadministration reforms, 2014 and the listgoes on.

Based on the glimpse of history of taxreforms in India and in particular with thelatest impact of the biggest reform namelyimplementation of GST Law, weprofessionals can be rest assured that wewill not be without work for quite few moredecades either in the form of litigation or

5CASC BULLETIN, DECEMBER 2017

in helping the public in understanding andimplementing the law. The previousGovernment ventured in going for aradical change, in 2009, by bringing in theDirect Taxes Code which could see the lightat the end of the tunnel. But the FinanceMinister of new Government which cameto power in 2014, had gone on recordstating that most of the proposed code hasalready been integrated into the existinglaw and also stated that the jurisprudenceunder the Income Tax law is welldeveloped and thus concluded that thereis no merit in going ahead with DTC.

But now a new Committee has beenconstituted to draft an appropriate directtax legislation with “The Terms ofReference of the Task Force is to draft anappropriate direct tax legislation keepingin view:

(i) The direct tax system prevalent invarious countries,

(ii) The international best practices.

(iii) The economic needs of the countryand

(iv) Any other matter connected thereto.

The Task Force shall set its own proceduresfor regulating its work and shall submitits report to the Government within sixmonths.”

Now we can be sure that there is no radicalchange or new code in the ensuing budgetsession and one has to wait to knowwhether Budget 2019 will be presented ornot as the period will end in May 2019.

Proud Moments for Every Indians

It was a month of feeling proud for everyIndian. Firstly, Justice Dalveer Bhandaribecame an elected member of InternationalCourt of Justice after completing the periodof nominated member. He topped the votesin the 193 member General Assembly. Maybe it is also symbolic of the shifting globalorder where emerging economies aregrowing more powerful and big powersare declining.

On November 22nd, 2017, Google paidhomage to Mrs. Rukhmabai, the first IndianWoman physician, by displaying googleDoodle with her image. “Today’s Doodleby illustrator Shreya Gupta shows thecourageous doctor among her patients,doing the dedicated work of a skilledphysician,” said Google’s blog post on itsdoodles.”

Appeal

Members are requested to attend theprograms conducted by CASC and are alsorequested to send their suggestions and /or value additions to the services providedby CASC including this Bulletin. The samecan be sent by hard copy to the office ofthe CASC or emailed [email protected] or any of theMembers on the Management Committee.

For and on behalf of Editorial Board

Editor

6CASC BULLETIN, DECEMBER 2017

DISCLAIMER :The contents of this Monthly Bulletin are solely for informational purpose. Itneither constitutes professional advice nor a formal recommendation. Whiledue care has been taken in assimilating the write-ups of all the authors. Neitherthe respective authors nor the Chartered Accountants Study Circle acceptsany liabilities for any loss or damage of any kind. No part of this MonthlyBulletin should be distributed or copied (except for personal, non-commercialuse) without express written permission of Chartered Accountants Study Circle.

COPYRIGHT NOTICE :All information and material printed in this Bulletin (including but not flowchartsor graphs), are subject to copyrights of Chartered Accountants Study Circleand its contributors. Any reproduction, retransmission, republication, or otheruse of all or part of this document is expressly prohibited, unless prior permissionhas been granted by Chartered Accountants Study Circle. All other rightsreserved.

ANNOUNCEMENTS :

1. The copies of the material used by the speakers for the regular meetings heldtwice in a month is available on the website and is freely downloadable.

2. Earlier issues of the bulletin is also available on the website in the “News” column.

The soft copy of this bulletin will be hosted on the website shortly.

READER’S ATTENTION

You may please send your Feedback Contributions / Queries on Direct Taxes, IndirectTaxes, Company Law, FEMA, Accounting and Auditing Standards, Allied Laws orany other subject of professional interest at [email protected]

For Further Details contact :“The Chartered Accountants Study Circle”

“Prince Arcade”, 2-L, Rear Block, 2nd Floor, 22-A, Cathedral Road,Chennai - 600 086. Phone 91-44-28114283

Log on to our Website :www.casconline.org

For updates on monthly meetings and professional news.Please email your suggestions / feedback to [email protected]

7CASC BULLETIN, DECEMBER 2017

RECENT JUDGMENTS IN VAT CSTInput tax credit claim: The dealer wasfound to have effected purchases fromseveral dealers and availed of input-taxcredit on such purchases, but the sellershad not disclosed the relevant turnover intheir monthly returns or paid tax due andpayable to the Department. The noticeissued by the assessing officer proposedto reverse the input-tax credit of Rs.3, 73,69,631 availed of by the dealer. In a writpetition filed in this regard, a single judgeallowed the claim of input tax credit videthe decision in INFINITI WHOLESALELIMITED v. ASSISTANTCOMMISSIONER (CT) [2015] 82 VST 457(Mad).In an appeal, the division bench,affirming the decision of the single judge,stated that held that the show-causenotice issued by the assessing officerproposing to reverse the input-tax creditavailed of by the dealer lacking valid orsustainable basis. If the sales effected tothe dealer were not disclosed by such aseller either in the form of return filedmonthly or the tax collected from thedealer was not made over to theDepartment by such seller, action wouldlie against such defaulting seller and notagainst the purchaser. Instead of trying tocross verify the input-tax credit availed ofby the dealer with specific reference toeach component, action was directed bythe assessing officer against the dealer.[2017] 99 VST 341 (Mad) AC (CT),PRESENTLY THIRUVERKADUASSESSMENT CIRCLE,KOLATHUR,

CA. V.V. SAMPATHKUMARCHENNAI V.INFINITI WHOLESALELTD.(formerly known as WoolworthsWholesale (India) Pvt. Ltd.)

Input tax credit reversal: On writpetitions against the reversal of input-taxcredit based on verification done by theassessing officer or at the direction ofsuperior authorities, by comparing thereturns filed by the dealer with the datamaintained by the Commercial TaxDepartment the court held that (i) whenthe dealers had not challenged thecorrectness of the individual assessmentorders on the facts, but the manner inwhich proceedings had been issued andthe jurisdiction of the assessing officers todo so. Therefore, the writ petitions weremaintainable and the court could testwhether the procedure adopted by therespondents prior to and while passingthe orders was fair and reasonable andwhether it satisfied the statutoryrequirement and hence the writ petitionswere maintainable. (ii) That all that theassessing officers had done was to issueshow-cause notices to the dealers

8CASC BULLETIN, DECEMBER 2017

registered in their jurisdiction referring tothe information uploaded in the webportal of the Department and calling uponthe purchasing dealer to prove thenegative, the assessing officers had eithertotally ignored the directions issued inthe circular or there had been partialcompliance. When procedure which wasrequired to be followed, had been notadhered to that would suffice to set asidethe proceedings with direction forconsideration de novo. The show-causenotices were bereft of particulars at timesnot even disclosing the name or traderidentification number of the dealer at theother end, the invoice numbers were notfurnished and in certain cases, a screenshot of the web portal image was copiedin the show-cause notice. There werecases where allegations of mismatch weremade against dealer, who was registeredas large taxpayer units and in many cases,the dealer at the other end was a publicsector undertaking. Therefore, theDepartment should have embarked upona proper enquiry before confronting thedealer and calling upon him to explain.(iii) It is high time the Principal Secretaryand Commissioner of Commercial Taxesin consultation with his officers lay out adetailed procedure as to how to takeforward cases of mismatch, evolve acentral mechanism, which can go intothese aspect and furnish details in fullform to the respective assessing officers,who can decide for themselves as towhether there is a case made out to callupon their dealer to explain. [2017] 99

VST 343 (Mad) JKM GRAPHICSSOLUTIONS P LTD V.CTO, VEPERYASSESSMENT CIRCLE, CHENNAI

Alternative Remedy: Writ petitions filedby the appellant-dealer againstassessments under the TNVAT Act, 2006were dismissed by a judge on the groundof availability of alternative remedy. Onappeal the Court held that the alternativeremedy of appeal could be by-passed onlyunder three contingencies, namely, (i)violation of principles of natural justice; (ii)lack of jurisdiction on the part of theassessing officer; and (iii) lack ofcompetence or power to initiateproceedings. All these were absent in thiscase and hence the court directed thedealer to file statutory appeals within aperiod of four weeks from the date ofreceipt of a copy of this judgment, with25 per cent of the tax demanded underthe assessment orders; upon filing of suchappeals, together with 25 per cent of thetax demanded, the appellate authorityshall deal with the appeals independentlywith reference to the facts as well as lawand dispose of them within further periodof three months and till then, the dealershall have the benefit of an order ofinterim stay of the demand in respect ofthe remaining portions. [2017] 99 VST430 (Mad) V. V.V. AND SONS EDIBLEOIL LIMITED V.CTO -1 (FAC),VIRUDHUNAGAR

Recovery of tax: The Division Bench of theCourt had given three directions: thatappeal shall be filed by the dealer within

9CASC BULLETIN, DECEMBER 2017

four weeks along with 25% of the taxdemanded under the assessment order,that upon the dealer filing the appealtogether with 25% of the demand theappellate authority shall decide the appealindependently and dispose of it within afurther period of three months and thattill then the dealer shall be entitled tointerim stay in respect of the remainingdemand. The words “till then” meant “tillthe disposal of the appeals by theappellate authority”. The Division Benchgranted four weeks’ time to file appealsand three months’ time to dispose of theappeals. Therefore, altogether fourmonths were available for the purpose ofdeciding the appeals. Till such time staygranted would be in operation. Upon aspecial leave petition filed by the dealerit had been given six weeks’ time toapproach the authority with a rider thatif such appeals were not filed within suchtime, time shall not be extended beyondthat. Pursuant to this, appeals were filedwith 25 per cent of the demand and theappeals were also entertained by theappellate authority. Therefore, the time offour weeks given by the Division Benchhad been modified or extended by sixweeks’ time either from the date of theorder of the Supreme Court or from thedate of receipt of copy of the order fromthe Supreme Court. Meanwhile, theassessing authority passed an orderraising a demand to be paid within sevendays, on the ground that the dealer hasnot made a deposit of 25 per cent. Of thedemand and filed an appeal within four

weeks’ time in compliance with thedirection issued by the Division Bench ofthe court. Once the appeals had beenentertained the only limitation left wasthe three-month outer time-limit given bythe Division Bench within which theappeals shall be disposed of by theappellate authority. Therefore, the orderof the CTO was totally against the spiritof the two orders, one passed by theDivision Bench of the High Court and theother passed by the Supreme Court andquashed. [2017] 99 VST 433 (Mad) V. V.V. AND SONS EDIBLE OILS LIMITEDV. CTO-1 (FAC), VIRUDHUNAGAR

Revision: The dealer had been awardedcontracts for supply, erection andcommissioning of complete power plantson turnkey basis. The assessing authorityinitiated escapement proceedings. For theassessing authority to have entertained abelief of escapement of turnover of tax, itwas imperative on his part to haveconsidered the amount which accordingto him had been claimed in excess of thatwhich according to him was legallyallowable to the dealer. The assessingauthority had neither quantified thatamount nor compared it with the amountactually claimed and deducted by thedealer. The assessing authority could nothave entertained a bona fide belief ofescapement without first comparing thefigure of actual deduction availed of andthe figure which according to him waslegally allowable to the dealer asdeduction. In absence of any quantification

10CASC BULLETIN, DECEMBER 2017

whatsoever, escapement of turnover waspresumed without basis that such adeduction would otherwise in all caseshave been claimed in excess of eligible 10per cent of the contract value received orreceivable. For various contracts and forvaried reasons actual value/s of serviceand labour charges may be lower orhigher than 10 per cent. The mereexistence of such a belief would not besufficient to vest jurisdiction in theassessing authority to reassess the dealer.The belief must be shown to be foundedon reasonable grounds. No reason hadbeen assigned to reach such a belief (evenif it was assumed to exist). Thus to allowreassessment proceedings at presentwould only amount to allowing a fishingexpedition or roving inquiry, all fallingoutside the scope of reassessmentproceedings. The initiation ofreassessment proceedings against thedealer is based on presumptions devoidof factual basis or reasonable groundgermane to the information of beliefregarding escaped turnover. [2017]99VST 441 (All) BHEL V. STATE OF U. P.AND OTHERS

Amnesty Scheme: An application forclaiming the benefit of the tax Amnestyscheme was rejected. The main reason fornot granting the benefit of the AmnestyScheme to the dealer was that the Schemehaving been introduced on October 14,2014 was prospective in effect and,therefore, the dealer was not entitled tothe benefit thereof and the Scheme brings

within the ambit of the Scheme only thosedealers who make payment during theperiod of operation of the Scheme. At thetime of implementation of the Scheme, aconsiderable number of works contractorshad not obtained registration in the Stateand such registered as well as non-registered contractors had not dischargedtheir tax liabilities. It was considering theposition of the works contractors that theScheme had been introduced. Now, inview of the decision rendered by theSupreme Court on September 26, 2013 inthe case of Larsen and Toubro Limited v.State of Karnataka [2013] 65 VST 1 (SC),there was clarity in the legal position andwith a view to see that such contractorsand developers could pay taxes for theperiod from April 1, 2006 and such workscontractors arid developers could bebrought within the tax net, it had beendecided to grant remission of tax.Preamble and the memorandum of theAmnesty Scheme showed that the benefitof the Scheme was to be given in respectof transactions commencing from April 1,2006. The scheme by its very nature wasretrospective in effect, viz., applicable topast transactions. Admittedly, the dealersought the benefit of the Scheme inrelation to the years 2010-11, 2011-12 and2012-13 which were well within the ambitof the Scheme namely, between April 1,2006 and October 14, 2014. A dealer, tobe entitled to the benefit of the Scheme,shall have to have paid the taxesthereunder during the operation of theScheme. It did not in any manner

11CASC BULLETIN, DECEMBER 2017

preclude those dealers who had alreadypaid the tax prior to the coming into forceof the Scheme. The only condition is thatin case where the tax, interest and penaltyhas already been paid, the dealer shall notbe entitled to refund thereof. Stating so,the Court held that the respondents wereto forthwith grant the benefit of theAmnesty Scheme dated October 14, 2014to the dealer. [2017] 99 VST 461 (Guj)SAFAL DEVELOPERS V. STATE OFGUJARAT.

Right of Appeal: Section 84 of the WBTTAct, 2003 deals with appeal against aprovisional or other order of assessmentand recognises the right of the dealer toprefer an appeal against a Provisional orother order of assessment. Apart fromthe requirement of filing requisitedocuments to establish the claims, thereare three parts to the second proviso ofsection 84(1) of the Act. The first part isthat any appeal presented on or afterApril, 2015 must fulfil the rigoursspecified in that proviso. The second partis clause (a) of the second proviso whichrequires an appellant to deposit theentirety of the amount of tax, interest,penalty or late fee as the appellant admitsto be due and payable. The third part isthe requirement of payment of 15 per centof the amount of tax in dispute in suchappeal. There is no dispute with regardto the second part of the second provisoof section 84(1) of the Act. Therequirement of deposit of 15 per cent ofthe tax in dispute. Requirement of makingsuch a deposit cannot, ipso facto, be

construed as hardship let alone unduehardship. A dealer declares his own taxliability. Court held that no right ofdealers to carry on business standsinfringed by the second proviso to section84 of the Act. The right to prefer theappeal is sought to be made conditional.The conditions imposed are notunreasonable, arbitrary or violative of anyprovisions of the Constitution. Theprovisions for appeal, therefore, cannot besaid to have violated the right guaranteedunder article 19(1) (g) of the Constitutionof India. [2017] 100 VST 1 (Cal) VATECHWABAG UMITED V.DC SALES TAX,MIDNAPUR CHARGE AND OTHERS

Works contract or sale? : In the absenceof a statutory definition in precise terms,words, entries and items in taxing statutesmust be construed in terms of theircommercial or trade understanding, oraccording to their popular meaning. Inother Words they have to be constructedin the sense that the people conversantwith the Subject-matter of the statutewould attribute to them. The respondent-dealer entered into an agreement withthe South Eastern Railway for supply ofmachine-crushed track ballast for layingon both sides of railway track in differentlocations. The tender schedule specifiedloading of ballast into any type of railwaywagon/hopper with the contractor’s ownarrangements including all lead liftcrossing of railway line according to thedirection of the engineer-in-charge of thework. Whether a contract is one for thesale a goods or for executing works or

12CASC BULLETIN, DECEMBER 2017

rendering services is a question of factwhich depends on the terms of thecontract including the nature of workdischarging. The loading of ballastssupplied was a labour charge and couldnot be termed as a sale. On the otherhand, the supply and delivery of stacksincluding all other nature of works asagreed to between the parties was a sale.[2017] 100 VST 24 (Orissa) STATE OFORISSA AND OTHERS V.D. K.CONSTRUCTION AND OTHERS

First Charge, Recovery of tax: As persection 529A of the Companies Act, 1956,priority is given to the dues of the securedcreditor and the workers over thestatutory charge claimed by the State. Inview of section 529(1)(c) the priority ofthe secured creditor who stands outsidethe winding up is confined to theworkmen’s portion as defined in section529(3)(c). The secured creditor whichstands outside the winding upproceedings in view of provisions ofsection 529A can surely have priority overthe claim of the State in respect ofstatutory dues. The bank extended thefinancial assistance to the company and inorder to secure the finances the companymortgaged its immovable property andhypothecated its assets in favour of bank.The company defaulted in repayment ofthe loan and the bank in action forrecovery of dues under the SARFAESIAct, 2002 took possession of the propertyand put it to auction. The auction sale wasconducted and the property was sold to

the highest bidder. The bank received twonotices from the Commercial TaxDepartment calling upon the bank todeposit an amount of Rs. 46, 49,317 withit. The Court in a writ petition held thatit is open to the bank to stand outside thewinding up proceedings and claimenforcement of its security interest. If thebank instead of deciding to stand outsidepreferred to go before the company courtfor decision, it would become necessary torelinquish its Security in accordance withInsolvency Rules mentioned in section 529of the Companies Act, 1956. The bank wasa secured creditor in accordance with thesecond clause under section 529A(1)(b)read with proviso (c) to section 529(1) ofthe Companies Act, 1956 having overridingpreferential claim and opted to standoutside winding up to realise its security.The bank had a priority claim over thestatutory dues claimed by theDepartment. The notices were to bequashed. [2017] 100 VST 48 (Bom) AXISBANK LIMITED V.STATE OFMAHARASHTRA AND ANOTHER

Brand Franchisee fees: No sales tax isleviable on the dealer on the amountreceived by it as “brand franchisee fees”from contract bottling units formanufacturing beer under the brandname/trade name of the dealer. [2017]100VST 74 (Karn) STATE OF KARNATAKAV.UNITED BREWERIES LTD

(The author is a Chennai based CharteredAccountant. He can be reached [email protected])

13CASC BULLETIN, DECEMBER 2017

CASC CHENNAI, MEMBERSHIP FEE

Corporate MembershipCorporate Annual Membership 3,000.00Corporate Life Membership (20 Years) 20,000.00

Individual MembershipAnnual Membership 750.00Life Membership 7,500.00

CASC - HALL RENTHALL RENT FOR 2 HOURS 1,000.00HALL RENT FOR 2-4 HOURS 1,500.00HALL RENT FOR FULL DAY 2,500.00LCD RENT FOR 2 HOURS 600.00LCD RENT FOR 2-4 HOURS 800.00LCD RENT FOR FULL DAY 1,200.00

CASC BULLETIN - ADVERTISEMENT TARIFF - PER MONTH

Full Page Back Cover 2,500.00Full Page Inside Cover 2,000.00Half Page Back Cover 1,500.00Half Page Inside Cover 1,250.00Full Page Inside 1,200.00Half Page Inside 750.00Strip Advertisement Inside 500.00

Minimum 6 months advertisement is required.If advertisement is 12 months or above, special discount of 15% is available

The above amounts are Exclusive of Government Levies like GST. Applicabletaxes will be added

Your demand draft / cheque at par should be drawn in the name of“The Chartered Accountants Study Circle” payable at Chennai.

Kindly contact [email protected] for the updates.

Rs.

14CASC BULLETIN, DECEMBER 2017

CASE LAWS - SERVICE TAX

CA. VIJAY ANAND

1. RULE 6A OF SERVICE TAX RULES– ULTRA VIRES SECTION 94(2)(f)OF THE FINANCE ACT – SAIDSECTION DOES NOT EMPOWERTHE GOVT. TO DECIDE THETAXABILITY OF TOUROPERATORS SERVICESPROVIDED OUTSIDE TAXABLETERRITORY

In Indian Association of TourOperators V. UOI 2017(5)GSTL4(Del.), the petitioners aremembers of Indian tour operatorswho are engaged in the business ofarranging tours for foreign touristsvisiting India as well as herneighbouring countries. The petitionerseeks to declare that Rule 6A of theService Tax Rules, 1994 (‘ST Rules’),concerning ‘Export of services’ is ultravires the Finance Act 1994 (‘FA’) andhave also challenged the validity ofsection 94(2) (f) of the FA on theground that it gives unguided anduncontrolled power to the centralgovernment to frame rules regarding‘provisions for determining export oftaxable services’.

The High Court observed as under:-

1. Rule 6A of the ST Rules is a piece ofdelegated of legislation which is madeby the Central Government in exerciseof the powers under Section 94 (1)read with Section 94 (2) (f) of the FA.

The grounds on which delegatedlegislation can be challenged are well-settled and set out in G. P. Singh’sPrinciples of Statutory Interpretation,10th Edition wherein it wasmentioned that Delegated legislation isopen to the scrutiny of courts and maybe declared invalid particularly ontwo grounds: (a) violation of theConstitution; and (b) violation of theenabling Act and that the secondground includes within itself not onlycases of violation of the substantiveprovisions of the enabling Act, but alsocases of violation of the mandatoryprocedure prescribed. In addition, itmay also be challenged on the groundthat it is contrary to other statutoryprovisions or that it so arbitrary thatit cannot be said to be in conformitywith the statute or Article 14 of theConstitution or that it has beenexercised in bad faith.

2. In General Officer Commanding-in-Chief v. Dr. Subhash ChandraYadav (supra), the Supreme Court

15CASC BULLETIN, DECEMBER 2017

held that it is well settled that rulesframed under the provisions of astatute form part of the statutewherein they have statutory force andthat before a rule can have the effectof a statutory provision, twoconditions must be fulfilled, namely,(1) it must conform to the provisionsof the statute under which it isframed; and (2) it must also comewithin the scope and purview of therule making power of the authorityframing the rule. If either of these twoconditions is not fulfilled, the rule soframed would be void. This principlewas also reiterated in UOI v. S.Srinivasan (2012) 7 SCC 683.

3. In Vasu Dev Singh v. Union ofIndia (2006) 12 SCC 753, it was heldthat an essential legislative functioncannot be delegated to the executiveand that it has to be exercised by thelegislature. The question that requiresto be answered is whether the levy oftax on services is an essential legislativefunction that cannot be delegated? Theanswer perhaps lies in the language ofSection 94 of the FA itself. Section94 (1) is the general power given to thecentral government to make rules tocarry out the provisions of Chapter Vof the FA. The words ‘carry out’necessarily imply providing amechanism for the levy enforcementand collection of service tax. The Rulesin this sense are instrumental andintended to achieve the objects of themain statute.

4. W.r.t. section 94(2), it basically lists outthe topics on which rules can be made.It talks of laying down the procedurefor carrying out various tasks set outin the FA or to provide the form inwhich returns are to be filed, appealspreferred. A perusal of Section 94 (2)(f) indicates that it empowers theCentral Government to make rules for‘determining’ when export of ‘taxableservices’ can be said to take place anddoes not empower to determinewhether there can be an export of non-taxable services viz., services providedoutside the taxable territory and thatit does not empower the making ofrules levying or making amenable theprovision of certain services to servicetax.

5. Section 94 (2) (hhh) permits makingrules regarding the ‘date fordetermination of rate of service tax’and ‘place of provision of taxableservice’ and does not provide formaking rules on determination oftaxability of a service. Subjectingcertain types of services to tax is anessential legislative function. In thiscase, since the FA envisages Chapter Vapplying only to taxable services,bringing non-taxable services withinthe ambit of service tax, isimpermissible.

6. Section 93B of the FA states that theRules made under section 94 wouldalso apply to any other service in so far

16CASC BULLETIN, DECEMBER 2017

as they are relevant to thedetermination of any tax liability orfor carrying out the provisions ofChapter V of the FA. However thewhole of Chapter V applies only totaxable service. If by means of rulesunder Section 94, what is nottaxable under the FA cannot be madetaxable, equally they cannot even byrules under Section 93 B. The words‘any other service’ occurring in Section93 B is subject to Section 64 (3) of theFA that precedes it. It cannot expandthe scope of Chapter V itself. Asalready noted, this is an essentiallegislative function and cannot bedelegated to the central government.

7. As already noticed Rule 6A (1) (d)treats even services provided outsidethe taxable territory i.e. where theplace of provision of service is outsideIndia, as an export of ‘taxable’ service.In view of the fact that since suchservice, by virtue of Section 66B readwith Section 65 (51) and (52) readwith Section 64 (1) and (3) of the FA,is not amenable to service tax in thefirst place, Rule 6A is ultra vires theFA. Even Section 94 (2) (hh) of the FApermits the Central Government todetermine when there would be anexport of ‘taxable service’ and not‘non-taxable service.’ Somethingwhich is impermissible under the FAcannot, by means of the rules madethereunder, be brought within the netof service tax.

8. Such tour operator services areintermediary services and under Rule 9of the PPSR 2012 the place of provisionof service is the location of the serviceprovider, the package tours serviceprovided by an Indian tour operator toa foreign tourist will, notwithstandingthat some part of it is provided outsideIndia, be treated as service provided inIndia. As a result no Indian touroperator can expect the service renderedby him to a foreign tourist to beconsidered as an ‘export of service’under Rule 6A as he will never be ableto meet the requirement of Rule 6A (1)(d) of the ST Rules. Thus under acombination of Rule 6A of the ST Rulesand Rule 9 of the Place of Provision ofServices, 2012 something which is non-taxable under the FA is sought to bebrought to tax.

9. By virtue of Section 64 (3) the whole ofChapter V applies only to taxableservices, and Section 66 C of the FA fallsin that very chapter, the rules made bythe central government under Section66 C has to necessarily be only in relationto taxable services viz., servicesprovided in the taxable territory ofIndia. The legal fiction of treatingservice rendered outside India to be aservice rendered in India cannot beintroduced by way of rules as it wouldpartake the character of an essentiallegislative function, which cannot bedelegated to the central government.Such service cannot be brought to taxwithout amending Section 64 (3) of theFA.

17CASC BULLETIN, DECEMBER 2017

10. Parliament has for the first time underthe Constitution (One Hundred andFirst Amendment) Act, 2016 effective8th September 2016 amended Article286 (1) to provide that there will be taxon the export of services out of theterritory of India. Article 286 (2) of theConstitution of India has beenamended simultaneously to providethat Parliament may by law formulatethe principles to determine when anexport of services takes place in any ofthe ways mentioned in Article 286(1). This is another indication thatthese tasks cannot be delegated to thecentral government to determine byrules.

11. In the case of an Indian tour operatororganizing a package tour for foreigntourists in India and its neighbouringcountries say Nepal and Bhutan, itwould comprise a composite bouquetof services and might involve severalsteps at each stage such as planning,scheduling and organizing the tour.Incidental steps would include fixingthe probable dates and venues,finalizing the itinerary, booking ofaccommodation in hotels in India andforeign countries, making travel andtransport arrangements, arranging visaand travel insurance, sight-seeing trips,catering arrangements, providingservices of tourist guides, providing atour leader to accompany the touringparty; arranging for complementarybags/snacks hampers, shopping bags,

passport pouches etc. The tasks mightinvolve co-ordinating with foreigncounterparts or directly the clientsthemselves through e-mails, phonecalls etc. Some of these services areprovided in the territory outside India,some possibly within India. When theservice is composite and a paymenttherefore is charged and made ina lump sum, it is difficult to make theapportionment of the charges as beingtowards services rendered in thetaxable territory i.e. India and thebalance towards those providedoutside India.

12. Apart from the fact that the provisionfor taxing export of services has to befound in the statute itself (and not inthe rules), the statute must also providethe machinery by which it can bedetermined with some certainty howmuch of the composite service can besaid to be rendered in the taxableterritory and of what value for thepurposes of levy and collection of tax.If there is no such machineryprovided, that would an additionalground of invalidation of the levyitself, relying on the decisionsin Govind Saran Ganga Saran v.Commissioner of Sales Tax AIR 1985SC 1041.

13. Rule 6A (1) of the ST Rules, insofar asit applies to export of tour operatorservices, suffers from the vice ofexcessive delegation inasmuch as thecentral government has been

18CASC BULLETIN, DECEMBER 2017

permitted to determine what shallconstitute export of services, bothtaxable and non-taxable. Such anessential legislative function could nothave been delegated to the centralgovernment.

14. Once the Parliament determines by lawwhat is amendable and not amenableto service tax, the modalities forworking out the procedure for levyand collection of such tax can be leftto the rules but the question ofwhether certain services should beamenable to tax cannot be left to bedetermined by rules made by thecentral government.

15. The Courts will not ordinarily questionlegislative wisdom. However, theCourts will strike down delegatedlegislation that is ultra vires the parentstatute.

Hence, the court concluded as under:-

a. Rule 6A (1) read with Section 6A (2) ofthe ST Rules, in1sofar as it seeks todescribe export of tour operatorservices to include non-taxable servicesprovided by tour operators, is ultravires the FA and in particular Section94 (2) (f) of the FA and is, therefore,invalid.

b. Section 94 (2) (f) or (hhh) of the FAdoes not empower the centralgovernment to decide taxability of thetour operator services providedoutside the taxable territory. They only

enable the central government todetermine what constitutes export ofservice, the date for determinationof the rate of service or the place ofprovision of taxable service.

c. Section 66 C of the FA enables thecentral government only to make rulesto determine the place of provision oftaxable service but not non- taxableservice.

Hence, the petition was disposed of inaforesaid terms.

2. MANPOWER RECRUITMENT ANDSUPPLY – DEPUTATION OFEMPLOYEES WITHIN THECOMPANY – NOT COVEREDUNDER MANPOWER SUPPLY7SERVICE

In Taisei Corporation V. CCE, NewDelhi 2017(5) GSTL61(Tri.-Del.), theappellant is an Indian project office ofa Japanese Company who has deployedemployees of the head office to Indianproject office. The adjudicatingauthority confirmed the demand underreverse charge under manpowersupply services, against which theappellant filed an appeal with theTribunal which observed as under:-

1. The appellant is a branch of Japanesecompany, undertaking the project workin India and is covered by theprovisions of Section 66A for any taxliability, on reverse charge basis, whensuch taxable services were receivedfrom outside India.

19CASC BULLETIN, DECEMBER 2017

2. Japanese company have sent some oftheir employees to their branch projectoffice in India, in connection withexecution of certain projects. Thesalaries and other perks are paid by theJapanese company and the same isshown as a debit in the accounts of theappellant (project office) in India. Noamount has been paid by the appellantto their head office in Japan.

3. The arrangement of deputingemployees from parent/head officeabroad to an Indian branch office willnot be covered for the tax liabilityunder supply of manpower. Thedeputation of employees within thecompany cannot be considered assupply of manpower. Further, noevidence has been presented as to thefact that the Japanese company isengaged in the activity of manpowerrecruitment or supply services.

4. Under such a situation, the liability ofthe appellant under ‘manpowerrecruitment and supply service’ cannotsustain, relying on the decision inAirbus Group India Pvt. Ltd. – 2016(45) S.T.R. 120 (Tri.-Del.).

5. While the original authority relied onthe provisions of Section 67 (2)Explanation-(c) to hold that the grossamount debited in the accounts of theappellant should be considered as aconsideration for receiving taxableservice, the said explanation states thatdebit entries, deduction from account

in any manner, is to be considered asa gross amount charged. Where thetransaction of taxable service is withany associated enterprise.

6. The transaction in the present case isnot between two associatedenterprises and that there is nothingon the record to indicate that thebranch project office in India can beconsidered as an associated enterpriseof Japanese company. The explanationwill cover only transactions betweenassociated enterprises as clarified bythe Board vide letter dated 29.02.2008.

Hence, the impunged orders are set asideand the appeals were allowed accordingly.

3. FRANCHISE AGREEMENT –CONSIDERATION RECEIVED FORRIGHT TO USE OF TRADE MARK– NOT ASSESABLE TO VAT

In McDonalds India Pvt. Ltd. V.Commr. Of Trade & Taxes, New Delhi2017(5) GSTL120(Del.), the petitioneris a wholly owned subsidiary ofMcDonald’s Corporation, Delawareand entered into joint ventureagreements, with Connaught PlazaRestaurants Private Limited,Hardcastle Restaurants PrivateLimited and Golden Kitchens PrivateLimited and held 50% of their capital,during the period under consideration.The petitioner also entered intofranchise agreements with variousfranchisees to allow them to adopt anduse the “McDonald’s system”, for the

20CASC BULLETIN, DECEMBER 2017

purpose of operating its restaurants inIndia for which they receive a fixedamount as location fee from thefranchisees, at the time of opening ofthe restaurants and further collectroyalty of approximately 5% of thegross sales, from the restaurantsoperated by the franchisees along withthe applicable service tax on ‘franchiseservice’.

The Commercial Taxes Department inDelhi confirmed the demand on theconsideration received under thefranchise agreement as a transfer ofright to use the goods, i.e., the trademark, being assessable to VAT thatwas also sustained by the Tribunal. Ona write petition before the HighCourt, it was observed as under:-

1. The arrangement is a compositecontract wherein, the trade mark andother services like knowhow, recipe,training, trade secrets, policies, etc. areprovided to the franchisee. The objectof the franchise agreement betweenMcDonald’s and its franchisee(s) is tooperate a comprehensive restaurantsystem (consisting of manuals,instructions etc., to run McDonald’s’restaurant(s) at the locations specifiedin the agreement, albeit, without anexclusive transfer of right to use thesame.

2. A perusal of article 366 (29A) of theConstitution of India indicates that fora tax to be levied on the sale or

purchase of goods, there has to be atransfer of the right to use the goodsand, hence, what needs to be assessedis whether the franchise agreementsgive rise to such a transfer of the rightto use the goods in addition toadjudging whether the nature of thecontent of the franchise agreements(for instance, that which comprises the“McDonald’s system”) is one of goodsor services.

3. The franchise agreement needs to beread in its entirety to understand theintention of the contract and it wouldbe incorrect to cull out only a sectionof the agreement to make it leviable toVAT. The franchise agreement intendsto make a non-exclusive transfer of thecomposite system of services that is notlimited to the trade mark, but isinclusive of a bunch of services, andhence, cannot be treated as goods andbe subject to VAT. By virtue of thisobservation alone, the levy under theDVAT is incorrect.

4. In Commissioner VAT, Trade andTaxes Department v. InternationalTravel House Ltd. [2009] (25) VST653,it was held that composite contractscannot be split up by taking from it thevalue of the goods for the purposes oftaxing the same under DVAT Act. Thepetitioners are solely engaged inproviding franchise services to theirfranchisees and the same would thusnot be liable to VAT under theprovisions of the DVAT Act, as the

21CASC BULLETIN, DECEMBER 2017

franchise service is expressly a taxableservice and cannot be treated as goods.

5. From a perusal of the facts of the cases,as well as the provisions of thefranchise agreements, it can beconcluded that what was intended tobe transferred was not the trade mark,but an entire gamut of services, whichincludesa guide that educates thefranchisees on various aspects ofbusiness and conduct to market thebusiness. To segregate the terms of theagreement to levy VAT on only specificaspects of it would be inexact.

6. Moreover, the petitioners are alreadypaying service tax levied on thefranchise agreements, and there can beno overlapping of taxes. The subjectmatters in List I and List II of theSeventh Schedule to the Constitutionare distinct and once a particular serviceis subject to service tax, it cannot betreated as a sale of goods and subjectto VAT.

7. The grant of a right, in the form oflicense to use the mark is primarily tobe utilized in the licensee’s product. Inusual cases of licensing, the trade markowner may not wish to use mark itsproducts or services in an area or regionand instead would license the mark, tobe used by the licensee’s products,subject to limitations. The licensee hasno right to initiate legal proceedings,in the event of infringementi.e. statutory right given to an owneror someone having proprietary rights

over the mark, to seek injunction anddamages). The property in the markalways vests with the owner.Therefore, when a trade vendor,distributor, establishment or anyoneelse permitted to sell articles or offerservices the trade marks (or brand)which belongs to another, it is incorrectto state that the brand or mark,associated with the product, constitutesthe sale rather than from sale of theunderlying goods or services that arethe subject of the trade mark (dishes ina restaurant) themselves.

8. It would be incorrect to conclude thatwhat is involved is not the sale of theproduct, but the intangible property ormark connected with the reputation ofthe mark, though that reputationguarantees a high demand for theproduct, from which the seller benefits.

9. For a transaction to constitute a transferof the right to use goods, there shouldmandatorily be a transfer of exclusiveright to use the goods beingtransferred. This was also highlightedin the dominant nature test as laiddown by the Supreme Court in BharatSanchar Nigam Ltd. V Union of India2006 (2) STR 161 (SC)...

10. In 20th Century Finance CorporationLtd. v. State of Maharashtra (2000) 119STC 182, it was held that a right to usegoods accrues only on transfer of rightand that the taxable event under article366(29A) (d) of the Constitution wasthe transfer of the right to use goods,

22CASC BULLETIN, DECEMBER 2017

and a distinction was set out betweena transfer of a right to use goods and amere permissive use of goods.

11. In State of Andhra Pradesh and Anr.v. Rashtriya Ispat Nigam Ltd.[2002] 126STC 114(SC), the Supreme Courtupheld the Andhra Pradesh HighCourt’s decision that the essence oftransfer is passage of control overthe economic benefits of propertywhich results in terminating rights andother relations in one entity andcreating them in another. This analogywas followed in Malabar Gold PrivateLtd. v CTO 2013(32) S.T.R.3(Ker.)where a Division Bench of the KeralaHigh Court concluded that the testslaid down in the BSNL’s case weresquarely applicable, that there were nogoods which were deliverable at anystage and there was no transfer of rightto use any trade mark.

12. For a transfer of the right to use goodsto be effective, such transfer of rightshould be one that the transferee canexercise in exclusion of others, whichis not the case in the present appealsand petitions, as the franchiseagreement only grants a non-exclusiveright, retaining the franchisor’s right totransfer the composite bunch ofservices to other parties, apart from itretaining ownership to the same.

Hence, the High Court held that theTribunal erred in holding thatconsideration received under the franchiseagreement (in McDonald’s case) was for

transfer of right to use the goods, i.e., thetrade mark, under the Delhi Sales Tax onRight to use Goods Act, 2002 and underthe Delhi Value Added Tax Act, 2004. Theassessment orders and notices impugnedin all the cases, and the orders of the DVATTribunal are hereby quashed. The appealsand writ petitions are, therefore, allowedin these terms. There shall be no order oncosts.

Hence, appeals were disposed of onaforesaid terms.

4. TAXABILITY OF COURSES OFONDON SCHOOL OF ECONOMICS– PROVIDED BY INDIANINSTITUTE – NOT LEVIABLE TOSERVICE TAX

In ITM International (P) Ltd. V. CST,Delhi 2017(5) GSTL 176 (Tri.-Del.),engaged in the field of education andcoaching. The adjudicating authorityconfirmed the demand under“Commercial Training or CoachingServices” on (a) fees received foroffering courses of London School ofEconomics (University of London)resulting in issue of degree by theUniversity of London and (b) feereceived for coaching provided forBusiness English and PersonalityDevelopment. On appeal, the judicialmember viewed that the entire demandmerits to be set aside whereas thetechnical member held that only thedemand beyond the normal periodneeds to be set aside. On reference toa third member, he observed as under:-

23CASC BULLETIN, DECEMBER 2017

1. On the issue regarding courses offeredby the appellant resulting in thedegrees/diplomas awarded byUniversity of London, these degrees/diplomas are to be considered asrecognized by law for the time beingin force. It is a well-known fact that thecolleges in India provide coursesresulting in degrees or diplomas butthe said degree and diplomas are issuedby the University or the main Instituteto which these colleges are affiliated.If it is to be held that as the degree isnot issued by the college which isproviding course, the college should beconsidered as a ‘commercial trainingor coaching centre’, subjected to servicetax, such interpretation will result inabsurd consequences. The degree ordiplomas are issued by the Universitiesor the main organization to which thecollege or an institute or a center isaffiliated.

2. Consequently, the degree or diplomabeing issued by University of Londoncan be considered at par whileinterpreting the scope of commercialtraining or coaching centre.

3. The next question is whether such adegree or diploma is recognized by lawfor the time being in force. UGC,AICTE, etc. are recognizing bodies ofa University or an Institution.The degree or diploma awarded bythese institutions are being consideredas recognized by law for the timebeing in force. In Board’s Circular

dated 28.8.2012, it was clarified that the‘recognized by ay law’ will includesuch course as are approved orrecognized by any entity establishedunder a Central or a State law,including delegated legislation, for thepurpose of granting recognition to anyeducational course.

4. Govt. of India, Ministry of HumanResource Development videNotification dated 13.3.1995, haddecided that those foreignqualifications which are recognized/equated by Association of IndianUniversities are treated as recognizedfor the purpose of employment to postsand services under the CentralGovernment and that no separateorder for recognition of such foreignqualification was needed. The degree/diploma programmes offered by theappellant resulting in the issue ofcertificate by the University of London(LSE) which is treated as equivalent todegree or diploma of publicUniversities in India.

5. Consequent to the above, the appellantswill fall outside the scope of definitionfor ‘commercial training or coachingcentre’.

6. The department has been taking a viewthat when an educational institute isaffiliated to a university/institutionawarding a degree recognized by law,then the said institute is not acommercial training or coaching centre.

24CASC BULLETIN, DECEMBER 2017

7. Business English Course andPersonality Development courseoffered by the appellants will becovered by exemption NotificationNo.9/2003-S.T. In this connection,relying on the decision in Anurag Soniv. Commissioner – 2017 (52)STR18(Tri.-Del.)

Hence, the third member held that thedemand for service tax against theappellants is not sustainable and agreedwith the Member (Judicial).

5. ASSESSEE CARRYING ONMANUFACTURE ANDCONSTRUCTION SERVICE – INPUTCREDIT USED IN MANUFACTUREOF GOODS DENIED ASEXEMPTION UNDERNOTIFICATION NO.1/2006-ST. WASAVAILED –NOT SUSTAINABLE

In Alluglaze V. CCE, Mumbai-II 2017(5)GSTL262(Tri.-Mumbai.), the appellantis engaged in the manufacture ofAluminium goods and is also a serviceprovider for construction services forwhich they are separately registeredwith service tax department. Theadjudicating authority denied cenvatcredit on the input which was used inthe manufacture of aluminium doorsand windows which was cleared on thepayment of duty holding that theassessee has claimed abatementNotification No. 1/2006-ST dated 1-3-2006 and this was also sustained by

Commissioner (Appeals). On appeal,the Tribunal observed as under:-

1. Revenue has proposed to deny thecenvat credit in respect of input usedin the manufacture of doors andwindows, which were cleared onpayment of duty on the ground thatappellant in respect of construction ofservices claimed the exemptionNotification No.1/2006-ST whereas theappellants are carrying out twodifferent activities, one is manufactureand other is construction services, bothhave to be dealt with separately for allthe purposes.

2. W.r.t. the manufacture activity, theappellant has complied with all therules and regulations procedure suchas input was received on which creditwas taken the said input was used inthe manufacture of doors and windowsand it is cleared on the payment ofduty.

3. Hence, Cenvat credit availed onmanufacturing activity on such inputsis clearly admissible notwithstandingthe violation in respect of constructionservice.

Hence impugned order is not sustainableand the same is set aside. Appeal is allowedwith consequential relief if any, inaccordance with law.

(The author is a Chennai based CharteredAccountant. He can be reached at reached [email protected])

25CASC BULLETIN, DECEMBER 2017

EXCEL TIPS

CA DUNGAR CHAND U JAIN

PRINT TITLES

Excel's Print Titles enable us to print particular row andcolumn headings on each page of the report. Many a timewhile printing a Report or a Statement, it is seen that thename of the Company or Client is required to be printedin all pages. For the same, Print Titles comes handy toovercome this issue at one go.

Print titles thus help columns and rows of related data spillover to other pages that no longer show the row andcolumn headings on the first page.

It must also be noted that this option should not be confused with the Header optionavailable in Ms-Excel. In fact, Header and Printer Titles both get printed on the samepage one after the other i.e. Header information gets printed in the top margin of thereport whereas Print Titles appear in the body of the report at the top, in the case ofrows used as print titles, and on the left, in the case of columns.

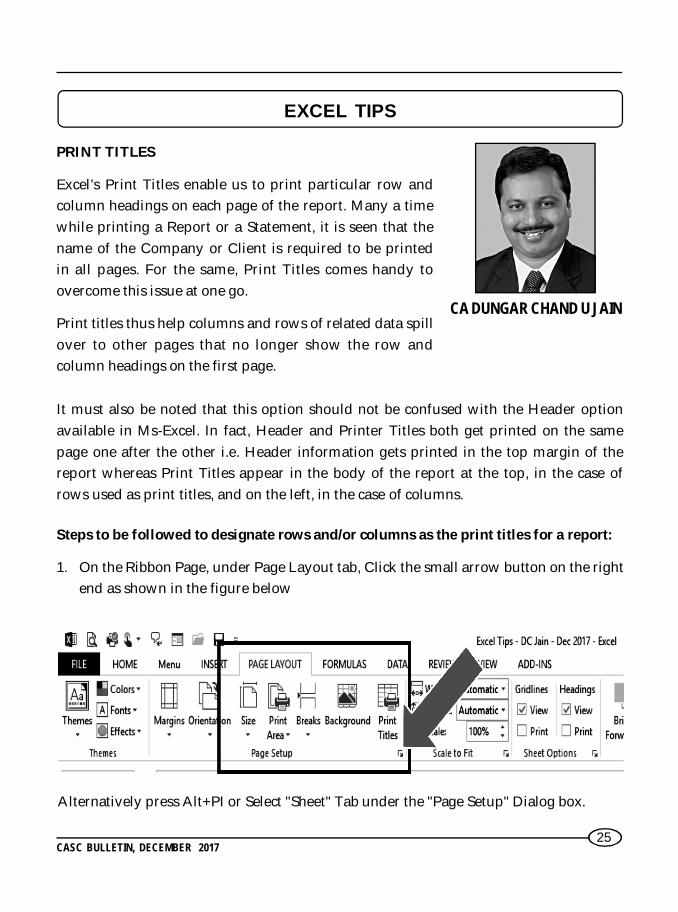

Steps to be followed to designate rows and/or columns as the print titles for a report:

1. On the Ribbon Page, under Page Layout tab, Click the small arrow button on the rightend as shown in the figure below

Alternatively press Alt+PI or Select "Sheet" Tab under the "Page Setup" Dialog box.

26CASC BULLETIN, DECEMBER 2017

2. Select the "Rows to Repeat at Top" text box and then drag through the rows withinformation you want to appear at the top of each page in the worksheet below.

If necessary, reduce the Page Setup dialog box to just the Rows to Repeat at Top textbox by clicking the text box's Collapse/Expand button. Note that Excel indicates theprint-title rows in the worksheet by placing a dotted line (that moves like a marquee)on the border between the titles and the information in the body of the report.

27CASC BULLETIN, DECEMBER 2017

Note that Excel indicates the print-title columns in the worksheet by placing a dottedline (that moves like a marquee) on the border between the titles and the information inthe body of the report.

4. Click OK or press Enter to close the Page Setup dialog box or click the Print Previewbutton to preview the page titles in the Print Preview pane on the Print screen.

3. Select the"Columns toRepeat at Left"text box andthen dragt h r o u g h t h erange ofcolumns withthe informationyou want toappear at the leftedge of eachpage of theprinted reportin thew o r k s h e e tbelow.

If necessary,reduce the PageSetup dialog boxto just theColumns toRepeat at Lefttext box byclicking itsC o l l a p s e /Expand button

28CASC BULLETIN, DECEMBER 2017

5. After you close the Page Setup dialog box, the dotted line showing the border of therow and/or column titles disappears from the worksheet.

Example:

This selects the First row and First Column which will get repeated in all pages of thereport.

And when the Print titles are no longer required in a report, open the Sheet tab of thePage Setup dialog box and then delete the row and column ranges from the "Rows toRepeat at Top" and the "Columns to Repeat at Left text boxes" before you click OK orpress Enter.

(The author is a Madurai based Chartered Accountant. He can be reached at [email protected])

29CASC BULLETIN, DECEMBER 2017

REFUND PROCESS IN GST REGIMEWorking capital is the lifeline of any business entity to functionsmoothly. To keep the cash flow position strong, GST includesprovisions relating to refunds of tax paid or of tax suffered byexporters or SEZ units. While the refund mechanism is continuedfrom the earlier service tax regime, the process of initiating therefund claim is marginally different under the GST regime.

The essence of zero rating is to make Indian goods and servicescompetitive in the international market by ensuring that taxes donot get added to the cost of exports. In this background, it isessential that Government liberalizes the process of refunds andgives exporters better incentive to improve the current exportlevel.

C.A. DEBASIS NAYAK& C.A. DIVYA RAMESH

In this article, we have analyzed below few key features relating the refund mechanismunder the GST regime.

Why Refund?

As per section 16 of IGST Act 2017, Exports and supplies to SEZ are zero rated. In a zerorating transaction, the entire supply chain of a particular zero rated supply is tax free i.e.there is no burden of tax either on the input side or output side. This is in contrast withexempted supplies, where only output is exempted from tax but tax is suffered on theinput side.

The objective of zero rating of exports and supplies to SEZ is sought to be achievedthrough

the provision contained in Section 16(3) of the IGST Act, 2017, which mandates that aregistered person making a zero rated supply is eligible to claim refund in accordancewith the provisions of Section 54 of the CGST Act, 2017, under either of the followingoptions, namely: –

• The exporter may supply goods or services or both under bond or Letter ofUndertaking, subject to such conditions, safeguards and procedure as may beprescribed, without payment of integrated tax and claim refund of unutilized inputtax credit of CGST, SGST / UTGST and IGST; or

• The exporter may supply goods or services or both, subject to such conditions,safeguards and procedure as may be prescribed, on payment of integrated tax andclaim refund of such tax paid on goods or services or both supplied.

30CASC BULLETIN, DECEMBER 2017

The second category pertains to refund of integrated tax paid for the zero-rated suppliesmade by suppliers who opt for the route of export on payment of integrated tax andclaim refund of such tax paid.

There can be two sub-categories of such suppliers namely:1. Exporter of goods2. Service exporters and persons making supplies to SEZ

Export of GoodsThe normal refund application in GST RFD-01 is not applicable in this case. There is noneed for filing a separate refund claim as the shipping billfiled by the exporter is itselftreated as a refund claim.

As per rule 96 of the CGST Rules, 2017, the shipping bill filed by an exporter shall bedeemed to be an application for refund of integrated tax paid on the goods exportedout of India and such application shall be deemed to have been filed only when:-

a. The person in charge of the conveyance carrying the export goods duly files an exportmanifest or an export report covering the number and the date of shipping bills orbillsof export; and

b. The applicant has furnished avalid return in FORM GSTR-3 or FORM GSTR3B, as thecase may be.

Thus, once the shipping bill and export general manifest (EGM) is filed and a valid returnis filed, the application for refund shall be considered to have been filed and refund shallbe processed by the department.

The details of the relevant export invoices contained in FORM GSTR-1 shall be transmittedelectronically by the common portal to the system designated by the Customs and thesaid system shall electronically transmit to the common portal, a confirmation that thegoods covered by the said invoices have been exported out of India.

Service Exporters and Persons making supplies to SEZA service exporter or persons making supplies to SEZ Unit may choose to first pay IGSTand then claim refund of the IGST so paid.

In these cases, the suppliers will have to file refund claim in FORM GST RFD – 01 on thecommon portal, as per Rule 89 and Rule 96A of the CGST Rules,2017.

Service Exporters need to file a statement containing the number and date of invoicesand the relevant Bank Realization Certificates or Foreign Inward Remittance Certificates,as the case may be, along with the refund claim.

31CASC BULLETIN, DECEMBER 2017

In so far as refund is on account of supplies made to SEZ, the DTA supplier will have tofile the refund claim in such cases. The second proviso to Rule 89 stipulates that in respectof supplies to a Special

Economic Zone unit or a Special Economic Zone developer or in case of deemed exports,the application for refund shall be filed by the –

• Supplier of goods after such goods have been admitted in full in the Special EconomicZone for authorized operations, as endorsed by the specified officer of the Zone;

• Supplier of services along with such evidence regarding receipt of services forauthorized operations as endorsed by the specified officer of the Zone;

• Recipient of the deemed export supplies or the supplier of deemed export suppliesin case where the recipient does not avail ITC and furnishes such undertaking thatthe supplier may claim the refund.

Proof of receipt of goods or services as evidenced by the specified officer of the zone isa pre-requisite for filing of refund claim by the DTA supplier.

General guidelines for Refund – Rule 89

A. Annexure and documents

The claim for refund has to be filed along with the following documents in Annexure 1to Form GST RFD - 01:

• A statement containing the number and date of invoices and the relevant BankRealization Certificates or Foreign Inward Remittance Certificates, as the case maybe,in a case where the refund is on account of the export of services;

• A statement containing the number and date of invoices along with the evidenceregarding the endorsement specified in the second proviso to sub-rule (1) in the caseof the supply of goods made to a Special Economic Zone unit or a Special EconomicZone developer;

• A statement containing the number and date of invoices, the evidence regarding theendorsement specified in the second proviso to sub-rule (1) and the details of payment,along with the proof thereof, made by the recipient to the supplier for authorizedoperations as defined under the Special Economic Zone Act,2005, in a case where therefund is on account of supply of services made to a Special Economic Zone unit or aSpecial Economic Zone developer;

32CASC BULLETIN, DECEMBER 2017

• A declaration to the effect that the Special Economic Zone unit or the Special EconomicZone developer has not availed the input tax credit of the tax paid by the supplier ofgoods or services or both, in a case where the refund is on account of supply of goodsor services made to a Special Economic Zone unit or a Special Economic Zone developer;

• A Certificate in Annexure 2 of FORM GST RFD-01 issued by a chartered accountantor a cost accountant to the effect that the incidence of tax, interest or any other amountclaimed as refund has not been passed on to any other person, in a case where theamount of refund claimed exceeds two lakh rupees.

B. Treatment to electronic credit ledger

Where the application relates to refund of input tax credit, the electronic credit ledgershall be debited by the applicant by an amount equal to the refund so claimed.

C. Refund formula for zero-rated supply

In the case of zero-rated supply of goods or services or both without payment of taxunder bond or letter of undertaking in accordance with the provisions of sub-section (3)of section 16 of the Integrated Goods and Services Tax Act, 2017, refund of input taxcredit shall be granted as per the following formula –

Refund Amount = (Turnover of zero-rated supply of goods + Turnover of zero-ratedsupply of services) x Net ITC ÷Adjusted Total Turnover

D. Refund formula for inverted duty structure

In the case of refund on account of inverted duty structure, refund of input tax creditshall be granted as per the following formula –

Maximum Refund Amount = {(Turnover of inverted rated supply of goods) x Net ITC÷Adjusted Total Turnover} - tax payable on such inverted rated supply of Goods

Grant of Provisional Refund

Zero rated suppliers will be entitled to provisional refund of 90% of the claim in termsof Section 54(6) of CGST Act, 2017.

Rule 91 of CGST Rules, 2017 provide that the provisional refund is to be granted within7 days from the date of acknowledgement of the refund claim. An order for provisionalrefund is to be issued in Form GST RFD 04 along with payment advice in the name ofthe claimant in Form GST RFD 05. The amount will be electronically credited to theclaimant’s bank account.

33CASC BULLETIN, DECEMBER 2017

Rule 91 also prescribe that the provisional refund will not be granted if the person claimingrefund has, during any period of five years immediately preceding the tax period to whichthe claim for refund relates, been prosecuted for any offence under the Act or under anearlier law where the amount of tax evaded exceeds two hundred and fifty lakh rupees.

Manual claim of Refund

• Due to the non-availability of the refund module on the common portal, theapplications/documents/forms pertaining to refund claims on account of zero-ratedsupplies shall be filed and processed manually.

• The application for refund of integrated tax paid on zero-rated supply of goods to aSpecial Economic Zone developer or a Special Economic Zone unit or in case of zero-rated supply of services is required to be filed in FORM GST RFD-01A (as notified inthe CGST Rules vide notification No. 55/2017 – Central Tax dated 15.11.2017) by thesupplier on the common portal and a print out of the said form shall be submittedbefore the jurisdictional proper officer along with all necessary documentary evidencesas applicable (as per the details in statement 2 or 4 of Annexure to FORM GST RFD –01), within the time stipulated for filing of such refund under the CGST Act.

• The application for refund of unutilized input tax credit on inputs or input servicesused in making such zero-rated supplies shall be filed in FORM GST RFD- 01A onthe common portal and the amount claimed as refund shall get debited from theamount in the electronic credit ledger to the extent of the claim. The common portalshall generate a proof of debit (ARN- Acknowledgement Receipt Number) whichwould be mentioned in the FORM GST RFD-01A submitted manually, along with theprint out of FORM GST RFD-01A to the jurisdictional proper officer, and with allnecessary documentary evidences as applicable, within the time stipulated for filingof such refund under the CGST Act.

• The registered person needs to file the refund claim with the jurisdictional taxauthority to which the taxpayer has been assigned as per the administrative. It isreiterated that the Central Tax officers shall facilitate the processing of the refundclaims of all registered persons whether or not such person was registered with theCentral Government in the earlier regime.

34CASC BULLETIN, DECEMBER 2017

• All communication in regard to the FORMS mentioned shall be done manually, withinthe timelines as specified in the relevant rules, till the module is operational on thecommon portal, and all such communications shall also be recorded appropriately inthe refund register

• After the refund claim is processed in accordance with the provisions of the CGSTAct and the rules and where any amount claimed as refund is rejected under rule 92of the CGST Rules, either fully or partly, the amount debited, to the extent of rejection,shall be re-credited to the electronic credit ledger

Listing below the detailed procedure for manual filing of Refund claims according toCircular 17/17/2017 dated 15th November, 2017.

# Category of Refund Process of refund

1 Refund of IGST paid on export of goods

No separate application is required as shipping bill itself will be treated as application for refund.

2 Refund of IGST paid on export of services / zero rated supplies to SEZ units or SEZ developers

Printout of FORM GST RFD- 01A needs to be filed manually with the jurisdictional GST officer (only at one place - Centre or State) along with relevant documentary evidences, wherever applicable.

3 Refund of unutilized input tax credit due to the accumulation of credit of tax paid on inputs or input services used in making zero-rated supplies of goods or services or both

FORM GST RFD-01A needs to be filed on the common portal. The amount of credit claimed as refund would be debited in the electronic credit ledger and proof of debit needs to be generated on the common portal. Printout of the FORM GST RFD- 01A needs to be submitted before the jurisdictional GST officer along with necessary documentary evidences, wherever applicable.

35CASC BULLETIN, DECEMBER 2017

Other situations arising for which Refund has to be filed

• Excess amount payment of tax accumulated due to mistake or misinterpretation

• Finalization of provisional assessment

• Refund of Pre-deposit for filing appeal assimilating refund coming in pursuance of an

appellate authority's order

• Payment of duty/tax during the investigation but no/ less liability arises in the event

of finalization of investigation/adjudication

• Refund of tax payment on purchases done by Embassies or UN bodies

• Credit collection due to output being tax exempt or nil-rated

• Credit collection due to inverted duty structure i.e. when the rate of tax on inputs is

higher than the arte of tax on output (other than nil-rated or fully exempt supplies)

• Year-end or volume based incentives provided by the supplier through credit notes

• Tax Refund for Foreign Tourists

With the constant changes in the application for Refund and the industry-grievances

regarding delayed filing of claim due to lack of clarity, it is expected that the GST council

work out an easy solution. Inward foreign currency is essential for the economy to grow,

which would be facilitated through exports.

Ease of filing refund claims would be a step towards ease of doing business.

(The authors are Chennai based Chartered Accountants. They can be reached at [email protected] &

36CASC BULLETIN, DECEMBER 2017

POWER OF NATIONAL COMPANY LAW TRIBUNAL TOCANCEL VARIATION OF RIGHTS OF CLASS SHAREHODERS

CS. S. DHANAPAL

Section 43 of the Companies Act, 2013 providesthat the share capital of a Company can only beof two kinds, either Equity Share Capital orPreference Share Capital and that the EquityShare Capital may be with or withoutdifferential rights. This provision empowers acompany to issue equity shares with differentialrights thereby constituting different class ofshares. Similarly preference shares may also beissued with variations in them with respect tothe rate of dividend, tenure, convertibility etc.each kind constituting a class.

Section 48 provides for the manner in which the rights of a class of shareholders may bevaried. It also provides for the members to apply to the Tribunal for cancelling suchvariation of rights by the Company if such variation affects their interest.

VARIATION OF RIGHTS OF A CLASS OF SHARES

Section 48 provides for variation of rights of a class of shareholders. The said Sectioncontains that where the share capital of a company is divided into different classes ofshares, the rights attached to the shares of any class may be varied with the consent inwriting of the holders of not less than three-fourths of the issued shares of that class orby means of a special resolution passed at a separate meeting of the holders of the issuedshares of that class.

Such variations can be carried out only if either the Memorandum or Articles permit thevariation or if the terms of issue of the shares provide for the variation, i.e. the terms ofissue do not expressly prohibit the variation.

Further it also contains that if the variation of rights of one class affects the rights ofsome other class, then consent of such other class should also be maintained in the samemanner as that of the original class.

37CASC BULLETIN, DECEMBER 2017

APPROVAL PROCESS FOR VARIATION OF CLASS RIGHTS

PROCEDURE FOR MAKING APPLICATION TO THE TRIBUNAL FORCANCELLATION OF VARIATION OF RIGHTS

Step 1 – Drafting and filing of petition to NCLT

Section 48 provides for cancellation of variation of the rights of a class of shareholders,on an application made by the shareholders belonging to the said class and with theapproval of the Tribunal.

Who can object to the cancellation?

Holders of at least 10% of the issued share capital of the class can object to the variationby not consenting to such variation or by voting against the special resolution in thegeneral meeting

38CASC BULLETIN, DECEMBER 2017

To whom application should be made?

Application for cancellation of variation should be made to the NCLT Bench, within whosejurisdiction the registered office of the company is situated.

Who can make application?

The shareholders, who are entitled to object to the variation/make the application forcancellation, can authorize one or more persons among themselves to make the applicationon their behalf to the Tribunal. Such authorization should be in writing by way of a letterof authority.

Time limit for making application

An application for cancellation of variation of rights under section 48 shall be made within21 days after the date on which the consent was given or the resolution was passed, asthe case maybe.

Form for making application

Application under section 48 to cancel a variation of the rights attached to the shares ofany class shall be made in Form NCLT 1.

Step 2 – Advertisement of Petition

The applicant has to, least 14 days before the date of the filing of the petition, advertisethe application in accordance with rule 35 of the NCLT Rules.

An affidavit shall be filed to the Tribunal, not less than 3 days before the date fixed forhearing, stating whether the petition has been advertised in accordance with Rule 35.The affidavit shall be accompanied with proof of advertisement.

Step 3 – Receiving objections and serving copy on Registrar / Regional Director

A copy of the objections received, if any, from any person(s) whose interest is likely tobe affected by the application, shall be served on the ROC and Regional Director, on orbefore the date of hearing.

39CASC BULLETIN, DECEMBER 2017

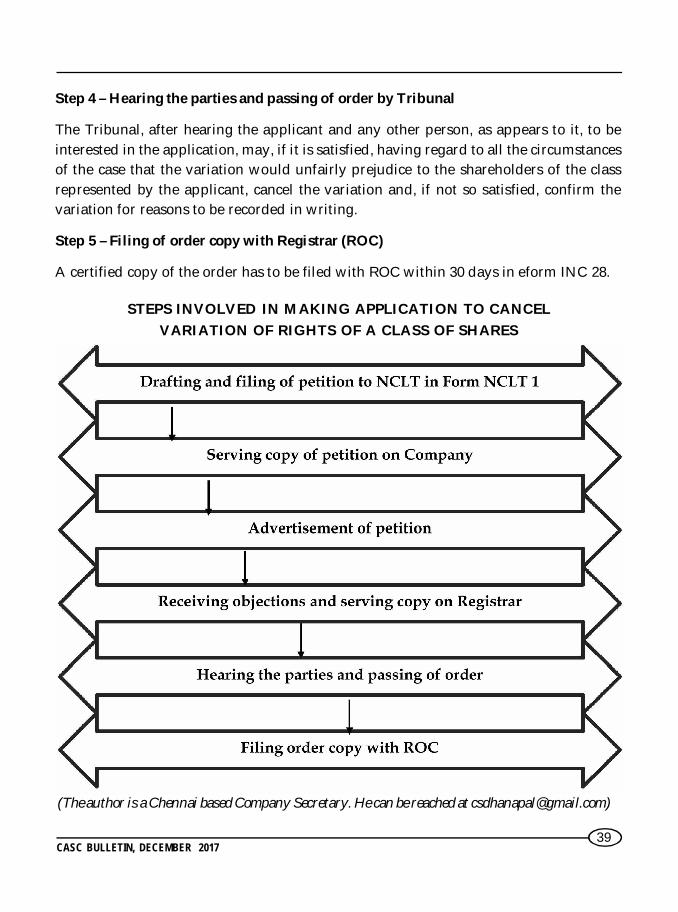

STEPS INVOLVED IN MAKING APPLICATION TO CANCELVARIATION OF RIGHTS OF A CLASS OF SHARES

(The author is a Chennai based Company Secretary. He can be reached at [email protected])

Step 4 – Hearing the parties and passing of order by Tribunal

The Tribunal, after hearing the applicant and any other person, as appears to it, to beinterested in the application, may, if it is satisfied, having regard to all the circumstancesof the case that the variation would unfairly prejudice to the shareholders of the classrepresented by the applicant, cancel the variation and, if not so satisfied, confirm thevariation for reasons to be recorded in writing.

Step 5 – Filing of order copy with Registrar (ROC)

A certified copy of the order has to be filed with ROC within 30 days in eform INC 28.

40CASC BULLETIN, DECEMBER 2017

CASE STUDIES AND THEIR REPLIES

CA. E. CHAITANYA