90% lifeline ‘lifeline’ is an exciting new product from alico designed to be the market leader...

TRANSCRIPT

90%90%

LifelineLifeline

‘‘Lifeline’Lifeline’ is an exciting new product from ALICO designed to be the is an exciting new product from ALICO designed to be the

market leader in the field of market leader in the field of

protectionprotection

AgendaAgenda Why Lifeline? Basic Parameters Premiums Premium Payment Bonus Investment Options Charges Death Benefits Non payment of premiums Reinstatement Ages of Eligibility Terms & Maturity Dates Minimum and Maximum Death Benefits Riders available UND Guidelines Competitive Advantage ALICO/AIG-Company Strength UND flowchart Checklist Basic Medical UND Features, Explanations, Benefits

Designed to be win-win-winDesigned to be win-win-win

Protects family in times of needProtects family in times of need

Complements your client’s investment objectivesComplements your client’s investment objectives

Is part of a needs based financial solutionIs part of a needs based financial solution

Most successful ALICO product with other banksMost successful ALICO product with other banks

Why ‘Lifeline’ @ NBDWhy ‘Lifeline’ @ NBD

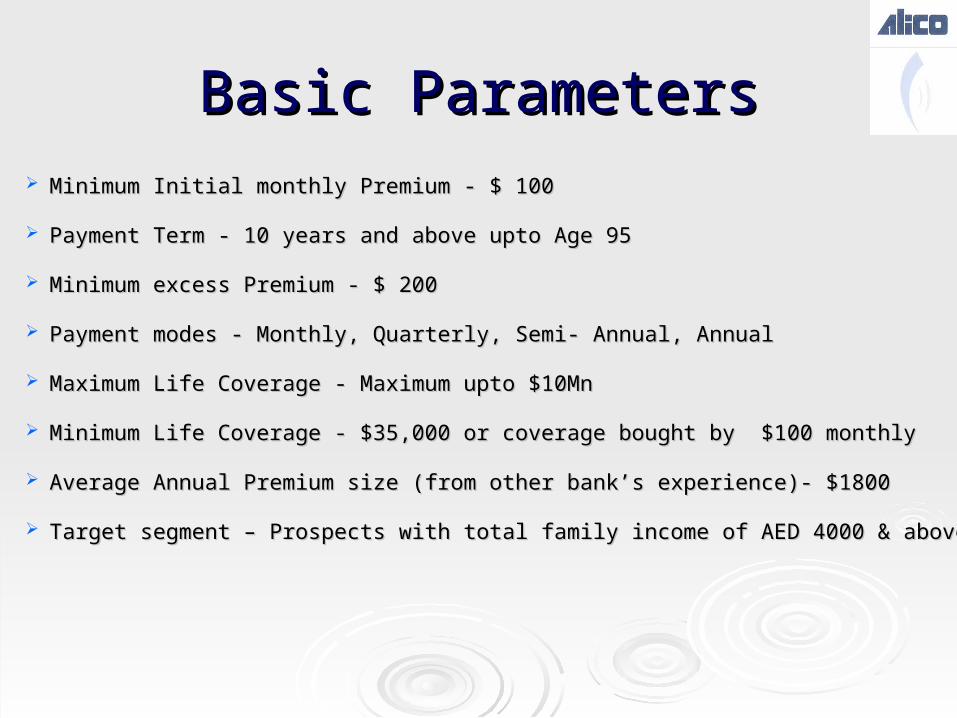

Basic ParametersBasic Parameters Minimum Initial monthly Premium - $ 100Minimum Initial monthly Premium - $ 100

Payment Term - 10 years and above upto Age 95Payment Term - 10 years and above upto Age 95

Minimum excess Premium - $ 200Minimum excess Premium - $ 200

Payment modes - Monthly, Quarterly, Semi- Annual, AnnualPayment modes - Monthly, Quarterly, Semi- Annual, Annual

Maximum Life Coverage - Maximum upto $10MnMaximum Life Coverage - Maximum upto $10Mn

Minimum Life Coverage - $35,000 or coverage bought by $100 monthlyMinimum Life Coverage - $35,000 or coverage bought by $100 monthly

Average Annual Premium size (from other bank’s experience)- $1800Average Annual Premium size (from other bank’s experience)- $1800

Target segment – Prospects with total family income of AED 4000 & aboveTarget segment – Prospects with total family income of AED 4000 & above

Premiums:Premiums:

For any given Face Amount there is For any given Face Amount there is aa range of range of premiumspremiums that the client can pay that the client can pay

Minimum PremiumMinimum Premium

The Minimum Premium is the smallest The Minimum Premium is the smallest premium that the company will accept for premium that the company will accept for any given Face Amountany given Face Amount

The lowest amount of premium that the The lowest amount of premium that the company will accept to start the policy company will accept to start the policy

Target PremiumTarget Premium

Target Premium is the ‘normal’ premium for any given Face Target Premium is the ‘normal’ premium for any given Face Amount to achieve Amount to achieve

Life cover upto a target age selected by the clientLife cover upto a target age selected by the client Desired Cash surrender value at a future dateDesired Cash surrender value at a future date

Target Premium is higher than the Minimum Premium fTarget Premium is higher than the Minimum Premium for any or any given Face Amountgiven Face Amount

Any premium over & above target premium is excess/dump-insAny premium over & above target premium is excess/dump-ins

Minimum Premium

Target Premium

Calculated forCalculated for

any given Face any given Face

Amount and AgeAmount and Age

Premium on which Premium on which full revenue is full revenue is

earnedearned

ExcessPremium

Premium on which 3% Premium on which 3% revenue is earnedrevenue is earned

Target PremiumTarget Premium

QuestionQuestion What is the advantage to the policy owner of paying What is the advantage to the policy owner of paying upto Target Premium?upto Target Premium?

a) The Face Amount will be highera) The Face Amount will be higher

b) The Life cover will beb) The Life cover will be longerlonger

c) The underwriting requirements will be relaxedc) The underwriting requirements will be relaxed

d) The monthly deduction for the Cost of Insurance will be lowerd) The monthly deduction for the Cost of Insurance will be lower

Write down your answer before turning to the next screenWrite down your answer before turning to the next screen

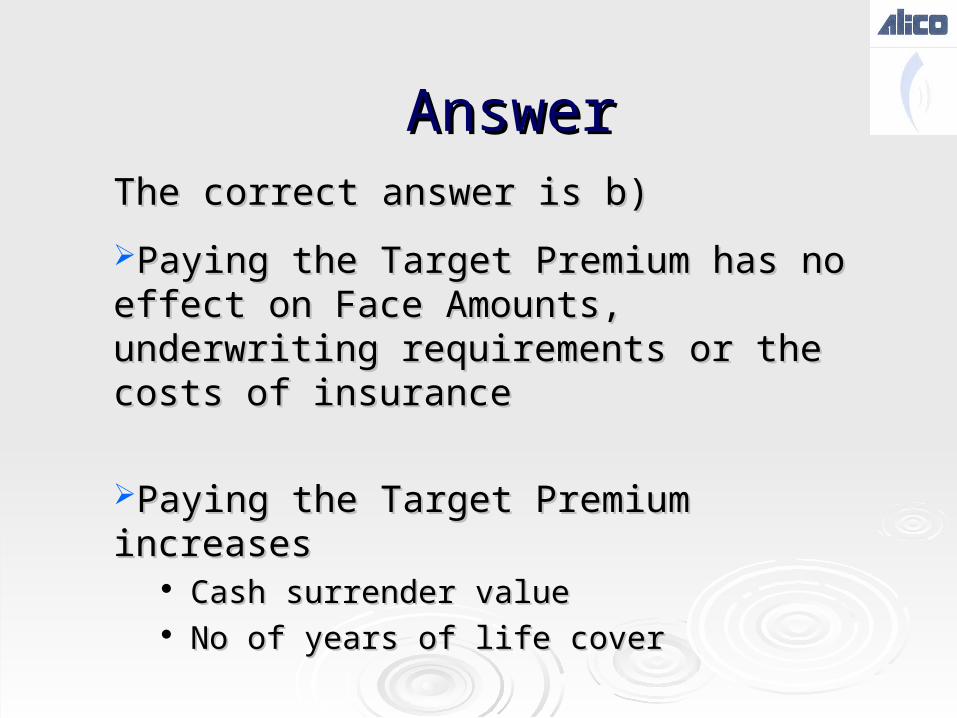

AnswerAnswer

Paying the Target Premium has no effect on Paying the Target Premium has no effect on Face Amounts, underwriting requirements or Face Amounts, underwriting requirements or the costs of insurancethe costs of insurance

Paying the Target Premium increasesPaying the Target Premium increases Cash surrender valueCash surrender value No of years of life coverNo of years of life cover

The correct answer is b)The correct answer is b)

The Premium Payment Bonus is a Loyalty Bonus, paid at the end of The Premium Payment Bonus is a Loyalty Bonus, paid at the end of the 5the 5thth and 10 and 10thth policy years policy years

The Bonus is 25% of the lowest premium paid during the preceding The Bonus is 25% of the lowest premium paid during the preceding 5 year period5 year period

The Bonus Is not applicable on excess premiumsThe Bonus Is not applicable on excess premiums

If the policy owner misses a premium in any year then the If the policy owner misses a premium in any year then the Premium Premium Persistency Bonus will be lost Persistency Bonus will be lost

If a policy owner misses the Premium Persistency Bonus at the end If a policy owner misses the Premium Persistency Bonus at the end of year 5, he /she can still qualify for the bonus paid at the end of of year 5, he /she can still qualify for the bonus paid at the end of year 10 year 10

Premium Payment BonusPremium Payment Bonus

Premium Payment BonusPremium Payment Bonus

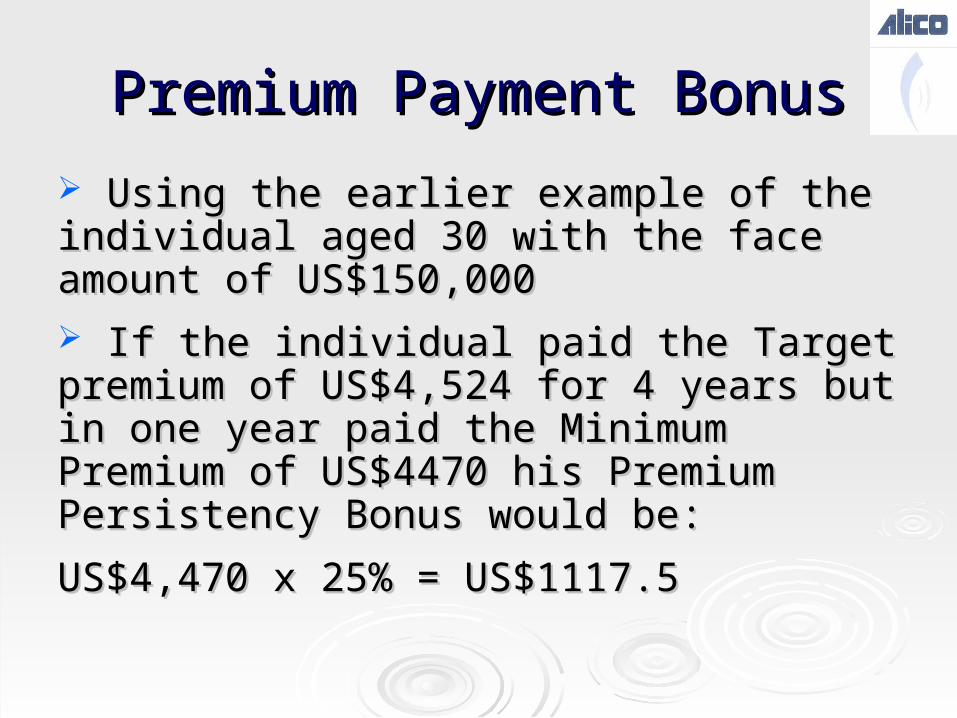

Using the earlier example of the individual Using the earlier example of the individual aged 30 with the face amount of US$150,000 aged 30 with the face amount of US$150,000 If the individual paid the Target premium of If the individual paid the Target premium of US$4,524 for 4 years but in one year paid the US$4,524 for 4 years but in one year paid the Minimum Premium of US$4470 his Premium Minimum Premium of US$4470 his Premium Persistency Bonus would be:Persistency Bonus would be:

US$4,470 x 25% = US$1117.5US$4,470 x 25% = US$1117.5

Premium Payment BonusPremium Payment Bonus

Year 5 Year 10

The Premium Payment Bonus will increase The Premium Payment Bonus will increase the cash values available to the policy ownerthe cash values available to the policy owner

Growing Cash Values

Increased Cash Values when the Bonus is paid

QuestionQuestion A client pays a Premium of US$3,000 for the first 5 A client pays a Premium of US$3,000 for the first 5 years of his policy. This includes an Excess Premium of years of his policy. This includes an Excess Premium of US$800US$800 What is the Premium Payment Bonus?What is the Premium Payment Bonus?

a) US$ 500b) US$ 550c) US$ 600d) US$ 750

Write down your answer before turning to the next pageWrite down your answer before turning to the next page

AnswerAnswer

The Premium Payment Bonus is only paid on The Premium Payment Bonus is only paid on amounts up to the Target Premiumamounts up to the Target Premium

US$3,000 - US$800 (Excess) = US$2,200US$3,000 - US$800 (Excess) = US$2,200The Premium Payment Bonus is paid at a rate The Premium Payment Bonus is paid at a rate of 25% of the lowest Premiumof 25% of the lowest Premium

US$2,200 x 25% = US$ 550US$2,200 x 25% = US$ 550

The correct answer is b)

Investment optionsInvestment options The policy owner can choose from The policy owner can choose from 2 2 investment funds depending on his attitude to riskinvestment funds depending on his attitude to risk

The Guaranteed Return AccountThe Guaranteed Return Account Vanguard Global Stock Index Vanguard Global Stock Index fundfund

The policy owner can spread his investment across two fundsThe policy owner can spread his investment across two funds

The proportion of his premium invested in any one fund must be 0% or a multiple of 10% of the premiumThe proportion of his premium invested in any one fund must be 0% or a multiple of 10% of the premium

4 transfers in a year free of $25 processing fee4 transfers in a year free of $25 processing fee

2% spread apply2% spread apply

Transfers out of GRA limited to a maximum of 25% in any policy yearTransfers out of GRA limited to a maximum of 25% in any policy year

Guaranteed Return AccountGuaranteed Return Account

Guarantees Guarantees that the crediting rate will not that the crediting rate will not fall below 3% over the lifetime of the planfall below 3% over the lifetime of the plan Current year 4%Current year 4%

Vanguard – Global Stock Index FundVanguard – Global Stock Index FundINVESTMENT OBJECTIVEINVESTMENT OBJECTIVE

This index fund seeks investment results and risk characteristics that This index fund seeks investment results and risk characteristics that track those of the Morgan Stanley Capital International (MSCI) World track those of the Morgan Stanley Capital International (MSCI) World Free Index—an unhedged, diversified, capitalisation-weighted Free Index—an unhedged, diversified, capitalisation-weighted benchmark consisting of common stocks of companies located in 23 benchmark consisting of common stocks of companies located in 23 developed countries across North America, Europe and the Asia/Pacific developed countries across North America, Europe and the Asia/Pacific region.region.

INVESTMENT STRATEGYINVESTMENT STRATEGYThe fund attempts to track its index by holding a portfolio of all, or a The fund attempts to track its index by holding a portfolio of all, or a representative sample, of the securities in the MSCI World Free Index in representative sample, of the securities in the MSCI World Free Index in roughly the same proportions as represented in the index itself.roughly the same proportions as represented in the index itself.

INVESTMENT RISK – Medium to High RiskINVESTMENT RISK – Medium to High Risk

Similar to investing in the broader world marketSimilar to investing in the broader world market Regarded lowest risk due to wide diversification in the aggressive Regarded lowest risk due to wide diversification in the aggressive

strategystrategy

ChargesCharges When an application is submitted and a policy is issued, ALICO incurs a When an application is submitted and a policy is issued, ALICO incurs a series of costsseries of costs

CommissionsCommissions

Underwriting costsUnderwriting costs

Policy and Fund Administration costsPolicy and Fund Administration costs

And the general cost of running the organisationAnd the general cost of running the organisation

ALICO applies charges to the policy to recoup those costsALICO applies charges to the policy to recoup those costs

Some charges can be taken from the premiumSome charges can be taken from the premium

Some charges can be taken from the fundsSome charges can be taken from the funds

ChargesCharges

Premium Load / Front end loadPremium Load / Front end load

Per Unit ChargesPer Unit Charges

Management ChargesManagement Charges

Administrative ChargesAdministrative Charges

Surrender/ Withdrawal ChargesSurrender/ Withdrawal Charges

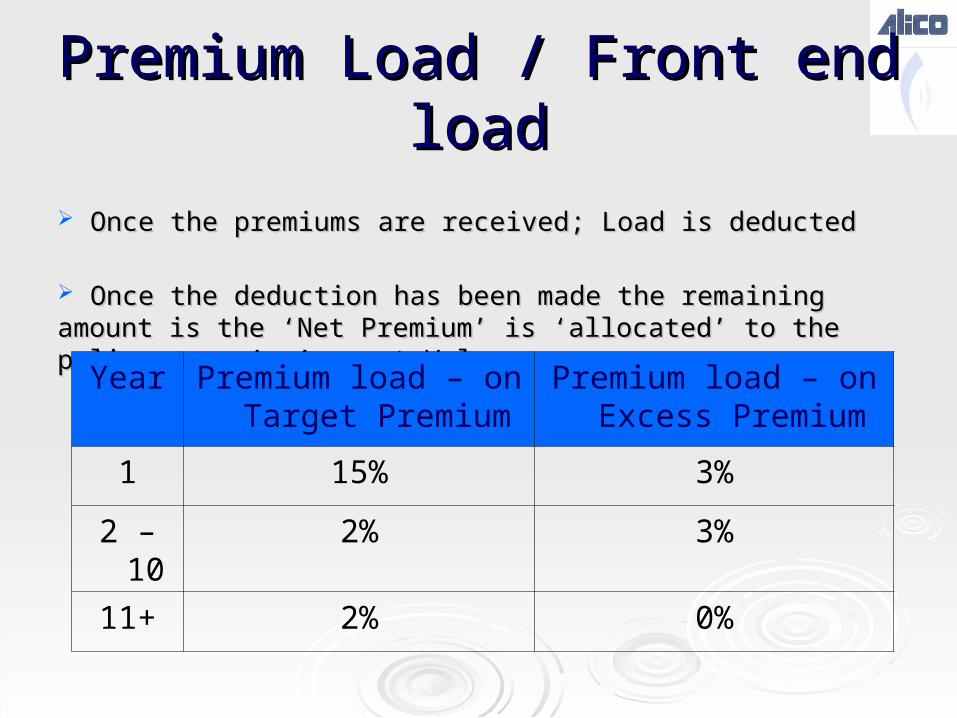

PremiumPremium Load / Front end load Load / Front end load

Once the premiums are received; Load is deOnce the premiums are received; Load is deductedducted

Once the deduction has been made the remaining amountOnce the deduction has been made the remaining amount is is the ‘Net the ‘Net Premium’ is ‘allocated’ to the policy owner’s Account ValuePremium’ is ‘allocated’ to the policy owner’s Account Value

Year Premium load – on Target Premium

Premium load – on Excess Premium

1 15% 3%

2 – 10

2% 3%

11+ 2% 0%

Per unit ChargesPer unit Charges

The Per Unit Charge is charged in years 2-15The Per Unit Charge is charged in years 2-15

This charge will be deducted monthly based on initial This charge will be deducted monthly based on initial annualized premium excluding rider and excess premiumannualized premium excluding rider and excess premium

Policy Year

Per unit charge - Annual

1 0%

2 – 10 13.725%

11 – 15 3.9216%

16 + 0%

Management ChargeManagement Chargess The Management Charge is used to pay the costs of The Management Charge is used to pay the costs of managing the Investment Strategies managing the Investment Strategies

The annual Management Charge is 1% The annual Management Charge is 1% oof the Client’s f the Client’s Account Value each yearAccount Value each year

The Management Charge is, however, reduced by a Fund The Management Charge is, however, reduced by a Fund Persistency Bonus. The annual management charge after the Persistency Bonus. The annual management charge after the deduction of the Fund Persistency Bonus isdeduction of the Fund Persistency Bonus is

Management Charge net of Persistency Bonus

Account Value<$50,00

0$50,000+

Year 1 1.00% 1.00%

Years 2 - 15 1.00% 0.50%

Years 16 + 0.75% 0.50%

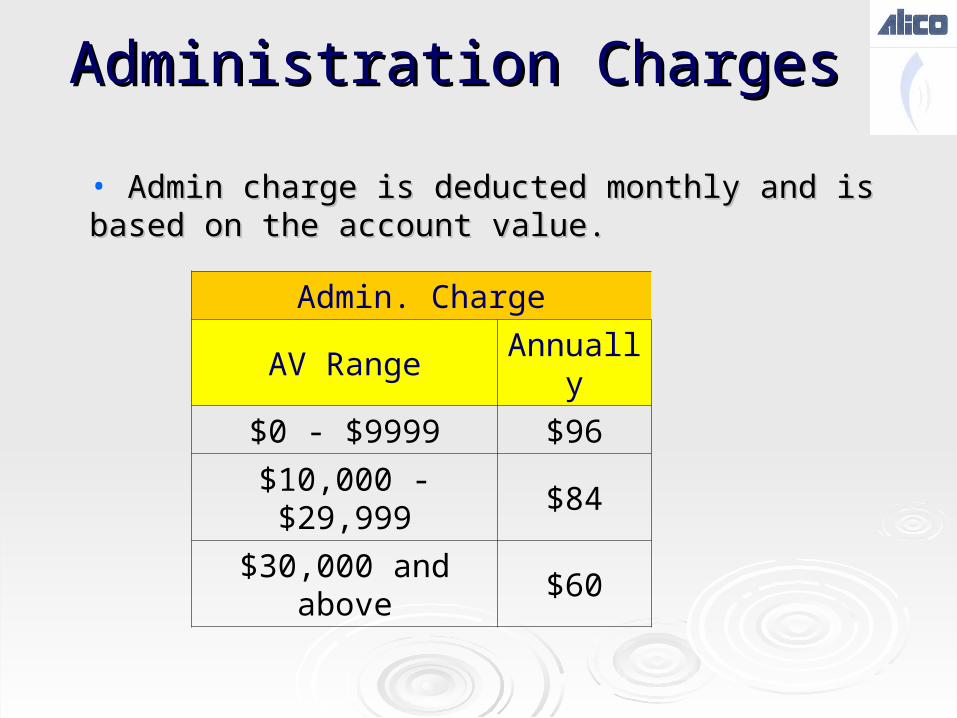

Administration ChargeAdministration Chargess

Admin. Charge

AV RangeAnnuall

y

$0 - $9999 $96

$10,000 - $29,999 $84

$30,000 and above $60

• Admin charge is deducted monthly and is based Admin charge is deducted monthly and is based on the account value.on the account value.

SurSurrender render ChargesCharges Surrender Charge applied on full surrenders is calculated Surrender Charge applied on full surrenders is calculated as a percentage of Annual Target Premiumas a percentage of Annual Target Premium

Surrender Charge is applied only if the policy owner Surrender Charge is applied only if the policy owner surrenders his policy in the first 10 yearssurrenders his policy in the first 10 years The charge is used to recoup the costs of setting up the The charge is used to recoup the costs of setting up the policy and paying commissionspolicy and paying commissions

Policy Year % of Premium

1 - 5 150%

6 90%

7 75%

8 60%

9 45%

10 20%

11+ 0%

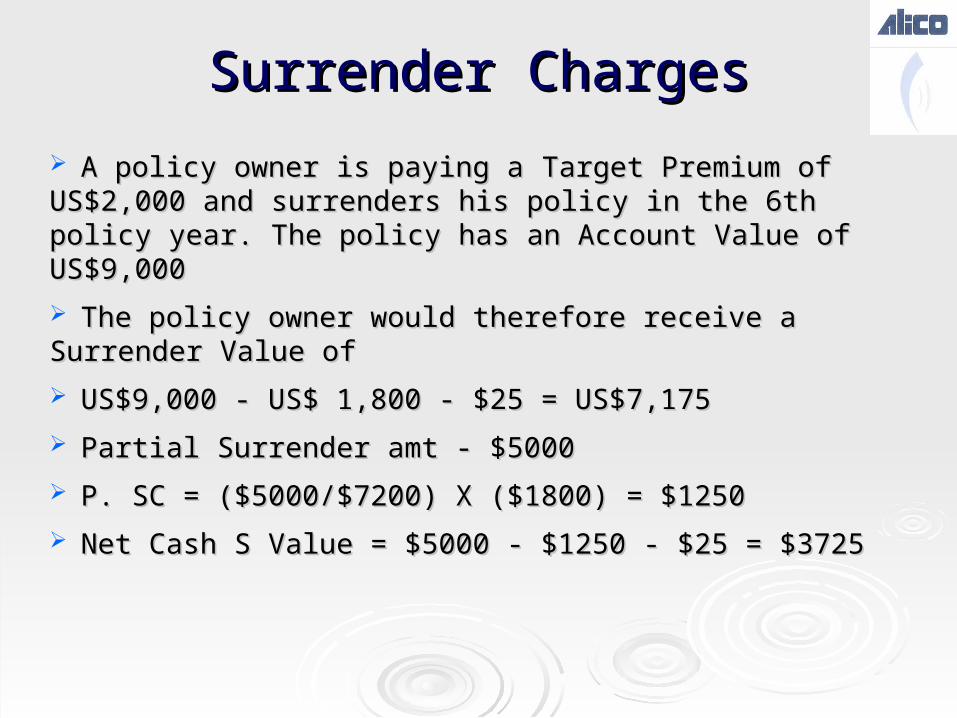

A policy owner is paying a Target Premium A policy owner is paying a Target Premium of US$2,000 and surrenders his policy in the of US$2,000 and surrenders his policy in the 6th policy year. The policy has an Account 6th policy year. The policy has an Account Value of US$9,000Value of US$9,000

The surrender charge in year 6 is 90% of The surrender charge in year 6 is 90% of the Target Premiumthe Target Premium US$2,000 x 90% = US$1,800US$2,000 x 90% = US$1,800

For Example

SurSurrender render ChargesCharges

A policy owner is paying a A policy owner is paying a TargetTarget Premium of US$2,000 Premium of US$2,000 and surrenders his policy in the 6th policy year. The policy and surrenders his policy in the 6th policy year. The policy has an Account Value of US$9,000has an Account Value of US$9,000

The policy owner would therefore receive a Surrender The policy owner would therefore receive a Surrender Value of Value of

US$9,000 - US$ 1,800 - $25 = US$7,175US$9,000 - US$ 1,800 - $25 = US$7,175

Partial Surrender amt - $5000Partial Surrender amt - $5000

P. SC = ($5000/$7200) X ($1800) = $1250P. SC = ($5000/$7200) X ($1800) = $1250

Net Cash S Value = $5000 - $1250 - $25 = $3725Net Cash S Value = $5000 - $1250 - $25 = $3725

SurSurrender render ChargesCharges

Some policy owners may wish to keep their policy in force and surrender only Some policy owners may wish to keep their policy in force and surrender only a proportion of their Account Valuea proportion of their Account Value

The Partial Surrender Charge is applied to the amount withdrawn from the The Partial Surrender Charge is applied to the amount withdrawn from the Account ValueAccount Value

Calculations – Partial surrender/ Cash surrender value X Target Premium X Calculations – Partial surrender/ Cash surrender value X Target Premium X % surrender charge% surrender charge

$25 processing fee with every partial withdrawal$25 processing fee with every partial withdrawal

Partial surrender charges reduces face amount but not less than $35,000 or if Partial surrender charges reduces face amount but not less than $35,000 or if NCSV falls below $500NCSV falls below $500

Partial Surrenders are not permitted in the first policy yearPartial Surrenders are not permitted in the first policy year

From the second policy year the policy owner will be allowed 2 partial From the second policy year the policy owner will be allowed 2 partial surrenders per yearsurrenders per year

SurSurrender render Charges - Charges - PartialPartial

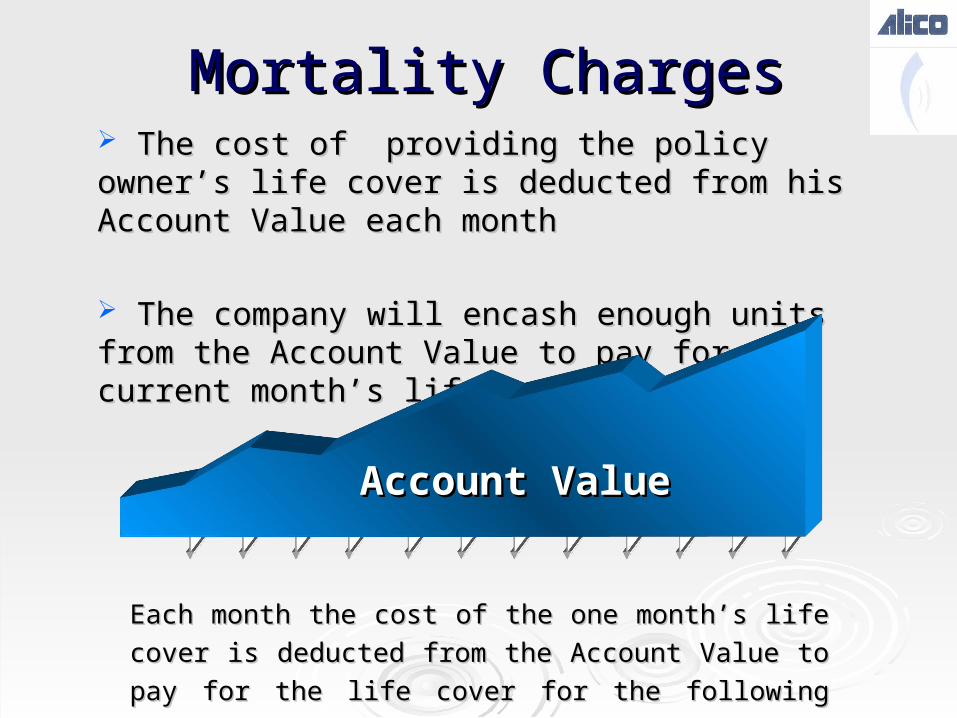

Mortality ChargesMortality Charges The cost of providing the policy owner’s life cover is The cost of providing the policy owner’s life cover is deducted from his Account Value each monthdeducted from his Account Value each month

The company will encash enough units from the The company will encash enough units from the Account Value to pay for the current month’s life coverAccount Value to pay for the current month’s life cover

Each month the cost of the one month’s life cover is Each month the cost of the one month’s life cover is

deducted from the Account Value to pay for the life deducted from the Account Value to pay for the life

cover for the following monthcover for the following month

Account ValueAccount Value

Death BenefitsDeath Benefits Lifeline gives the policy owner; life cover – Lifeline gives the policy owner; life cover –

The amount payable on death under the The amount payable on death under the plan is the greater of the Face Amount or plan is the greater of the Face Amount or the Account Valuethe Account Value

The monthly deductions to provide for the costs of insurance The monthly deductions to provide for the costs of insurance buys an amount of cover that is equal to the difference buys an amount of cover that is equal to the difference between the Face Amount and the Account Valuebetween the Face Amount and the Account Value

Face Amount - Option A

Account Value

The Face Amount is higher - the Face Amount would be payable on death

Death BenefitsDeath Benefits

Death BenefitsDeath Benefits

Face AmountOption A

Account Value

When the Account Value is higher - the Account Value would be payable on death

Death BenefitsDeath Benefits

Face Amount US$95,000

US$15,000

Life Insurance of

US$80,000 for which COI is

deducted monthly

• In this example the client had a Face Amount of In this example the client had a Face Amount of US$95,000 and an Account Value of US$15,000US$95,000 and an Account Value of US$15,000

• On his death ALICO would pay the US$15,000 On his death ALICO would pay the US$15,000 from his Account Value and Life insurance of from his Account Value and Life insurance of US$80,000 to make up the Face AmountUS$80,000 to make up the Face Amount

Face Amount

US$95,000

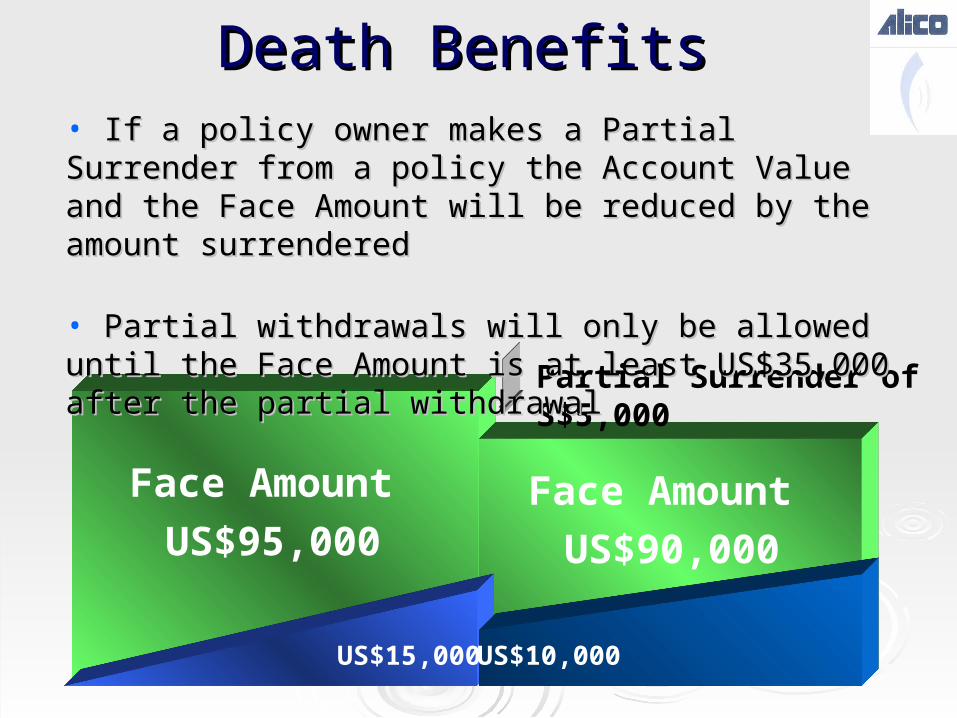

Death BenefitsDeath Benefits

Face Amount

US$90,000

US$15,000 US$10,000

Partial Surrender of S$5,000

• If a policy owner makes a Partial Surrender from If a policy owner makes a Partial Surrender from a policy the Account Value and the Face Amount a policy the Account Value and the Face Amount will be reduced by the amount surrenderedwill be reduced by the amount surrendered

• Partial withdrawals will only be allowed until the Partial withdrawals will only be allowed until the Face Amount is at least US$35,000 after the partial Face Amount is at least US$35,000 after the partial withdrawalwithdrawal

Death BenefitsDeath Benefits

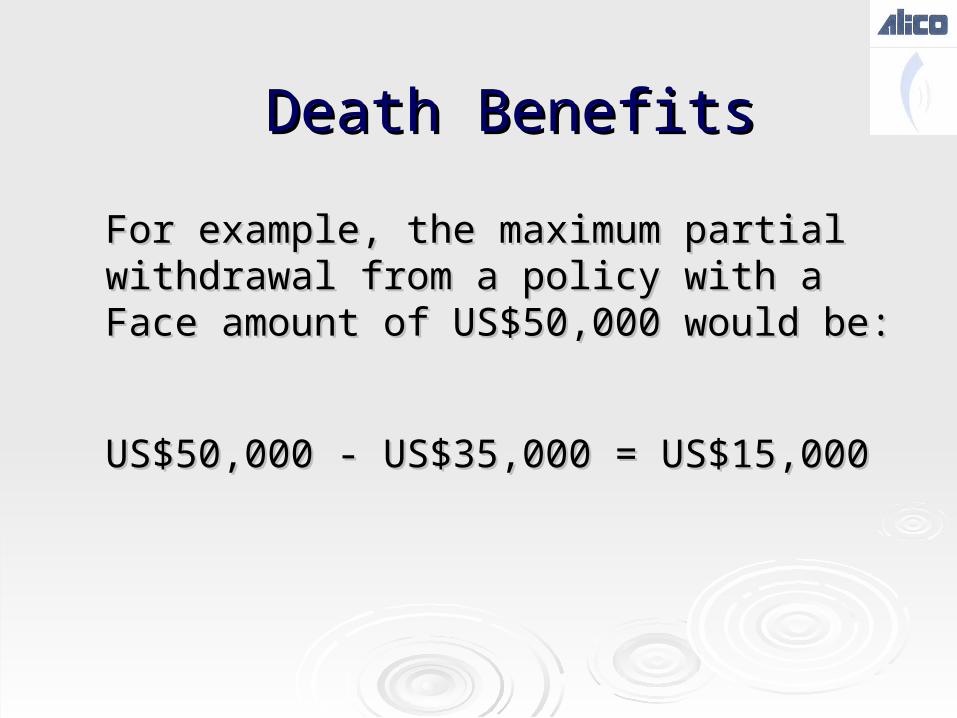

For example, the maximum partial For example, the maximum partial withdrawal from a policy with a Face amount withdrawal from a policy with a Face amount of US$50,000 would be:of US$50,000 would be:

US$50,000 - US$35,000 = US$15,000US$50,000 - US$35,000 = US$15,000

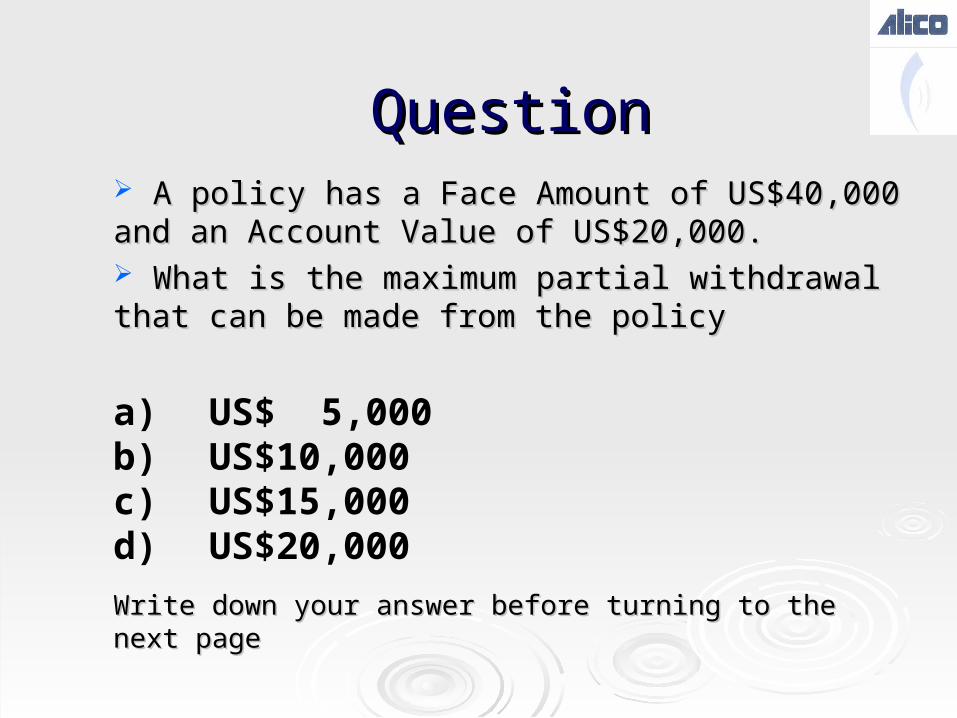

QuestionQuestion AA policy has a Face Amount of US$40,000 and an policy has a Face Amount of US$40,000 and an Account Value of US$20,000.Account Value of US$20,000. What is the maximum partial withdrawal that can be What is the maximum partial withdrawal that can be made from the policymade from the policy

a) US$ 5,000b) US$10,000c) US$15,000d) US$20,000

Write down your answer before turning to the next pageWrite down your answer before turning to the next page

AnswerAnswer

The Face Amount of the policy can not be The Face Amount of the policy can not be reduced by partial withdrawals to less than reduced by partial withdrawals to less than US$35,000US$35,000

The maximum partial withdrawal is thereforeThe maximum partial withdrawal is therefore

US$40,000 - US$35,000 = US$5,000US$40,000 - US$35,000 = US$5,000

The correct answer is a)

Increasing Death BenefitsIncreasing Death Benefits

The Face Amount can be varied to meet a The Face Amount can be varied to meet a client’s changing circumstancesclient’s changing circumstances

The Face Amount can be increased at any The Face Amount can be increased at any time after the 2nd policy anniversarytime after the 2nd policy anniversary

ALICO may require medical evidence ALICO may require medical evidence before the increase is allowedbefore the increase is allowed

An increase in Face Amount will increase An increase in Face Amount will increase the Minimum Premium and Target Premiumthe Minimum Premium and Target Premium

Target Premium

Increased Face Amount

Increased Premium

Increasing Death BenefitsIncreasing Death Benefits

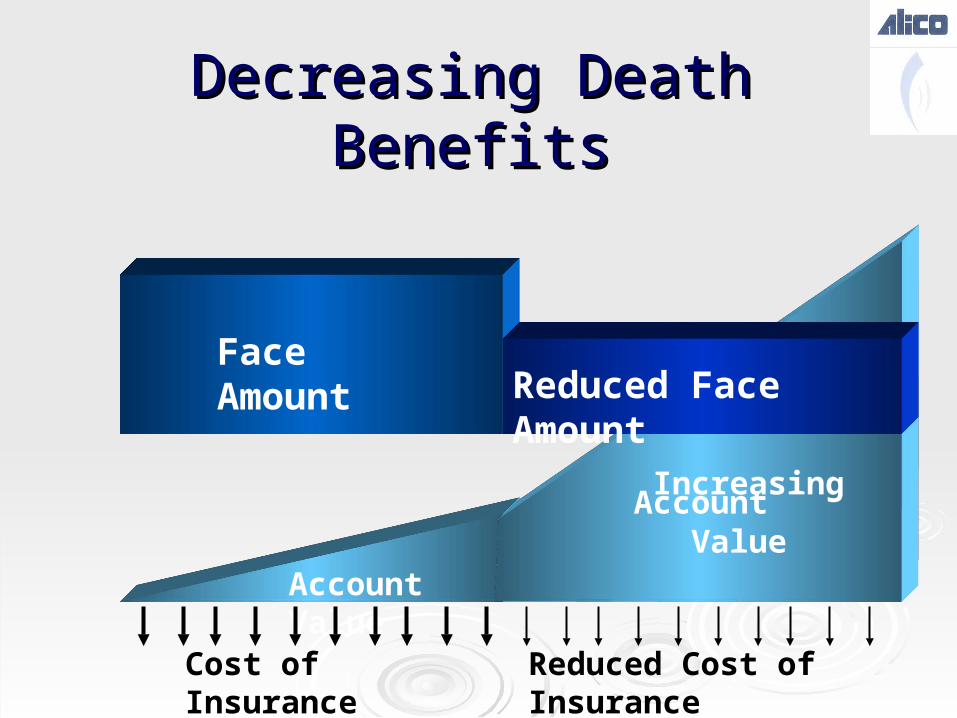

The Face Amount can be decreased at any time after the 5th policy The Face Amount can be decreased at any time after the 5th policy anniversaryanniversary

The reduction in the Face Amount will not decrease the premiumsThe reduction in the Face Amount will not decrease the premiums

But the monthly deductions from the Fund will reduce, and the But the monthly deductions from the Fund will reduce, and the Account Value will grow more quicklyAccount Value will grow more quickly

The minimum allowable decrease in the Face Amount is US$10,000The minimum allowable decrease in the Face Amount is US$10,000

The Face Amount cannot be decreased below US$35,000The Face Amount cannot be decreased below US$35,000

Decreasing Death BenefitsDecreasing Death Benefits

Face Amount

Account Value

Cost of Insurance Reduced Cost of Insurance

Increasing Account Value

Reduced Face Amount

Decreasing Death BenefitsDecreasing Death Benefits

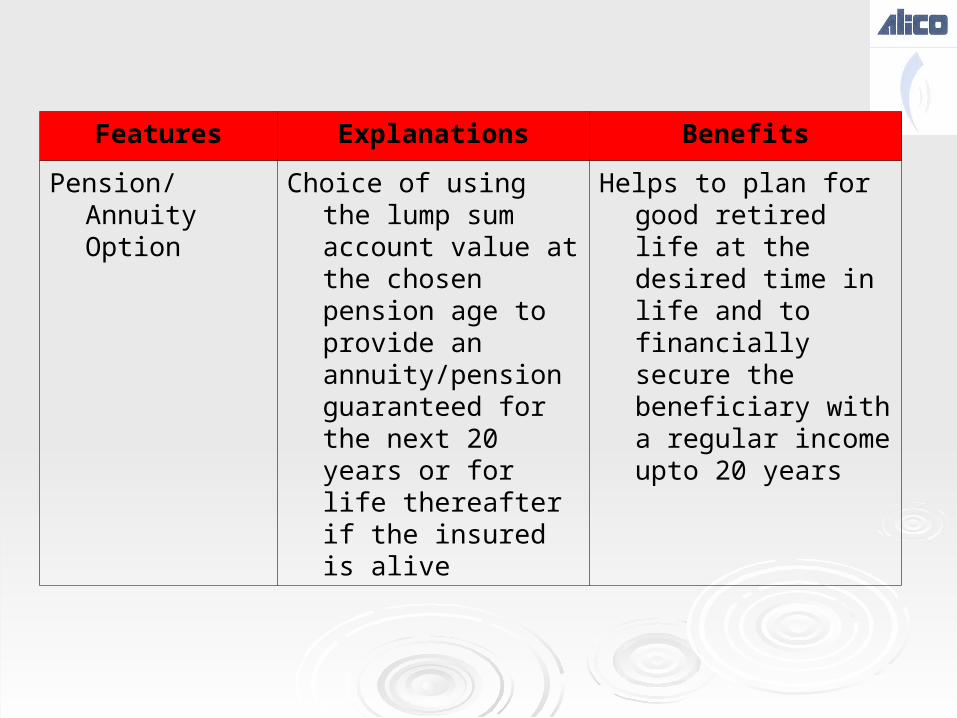

Choice of using the lump sum account value at the Choice of using the lump sum account value at the chosen pension age to provide an annuity/pension chosen pension age to provide an annuity/pension guaranteed for the next 20 years or for life guaranteed for the next 20 years or for life thereafter if the insured is alivethereafter if the insured is alive

BenefitsBenefits

Helps to plan for good retired life at the desired time Helps to plan for good retired life at the desired time in life and to financially secure the beneficiary with in life and to financially secure the beneficiary with a regular income upto 20 yearsa regular income upto 20 years

Pension/ Annuity OptionPension/ Annuity Option

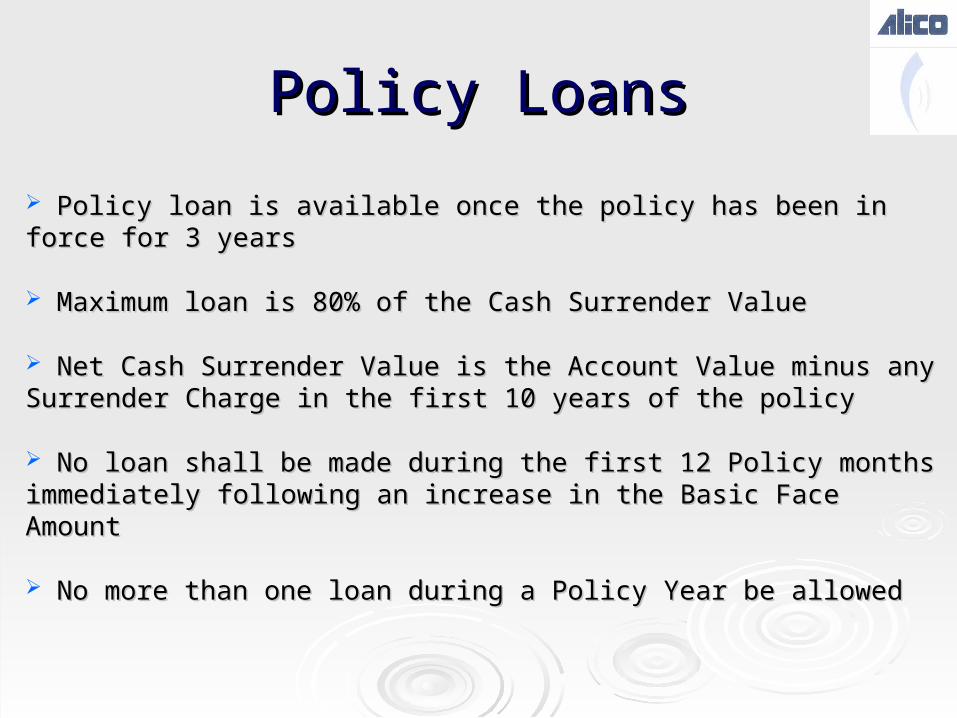

Policy LoansPolicy Loans

PPolicy loan is available once the policy has been in force for 3 yearsolicy loan is available once the policy has been in force for 3 years

Maximum loan is 80% of the Cash Surrender ValueMaximum loan is 80% of the Cash Surrender Value

Net Cash Surrender Value is the Account Value minus any Net Cash Surrender Value is the Account Value minus any Surrender Charge in the first 10 years of the policySurrender Charge in the first 10 years of the policy

No loan shall be made during the first 12 Policy months immediately No loan shall be made during the first 12 Policy months immediately following an increase in the Basic Face Amountfollowing an increase in the Basic Face Amount

No No more than one loan during a Policy Year be allowedmore than one loan during a Policy Year be allowed

QuestionQuestion

A client has been contributing to Lifeline for 12 years A client has been contributing to Lifeline for 12 years and has an Account Value of US$10,000and has an Account Value of US$10,000 What is the maximum loan that he could take from the What is the maximum loan that he could take from the policypolicy

a) US$7,500b) US$8,000c) US$9,000d) US$10,000

Write down your answer before turning to the next pageWrite down your answer before turning to the next page

AnswerAnswer

The maximum loan is 80% of the Net The maximum loan is 80% of the Net Surrender Value (the Account Value minus any Surrender Value (the Account Value minus any Surrender Charge and existing loans).Surrender Charge and existing loans).

As the policy is more than 10 years old there As the policy is more than 10 years old there is no Surrender Penaltyis no Surrender Penalty

The maximum loan isThe maximum loan is

US$10,000 x 80% = US$8,000US$10,000 x 80% = US$8,000

The correct answer is b)

Policy LoansPolicy Loans

Interest on the loan will be charged at a rate which will be Interest on the loan will be charged at a rate which will be determined by ALICOdetermined by ALICOThe interest is currently 8%The interest is currently 8%Policy loans can only be taken against funds held in the Policy loans can only be taken against funds held in the Guaranteed Return AccountGuaranteed Return Account

If the amount of the loan is higher than the value of the If the amount of the loan is higher than the value of the Guaranteed Return Account a transfer must be made into Guaranteed Return Account a transfer must be made into the Account from another Strategythe Account from another Strategy

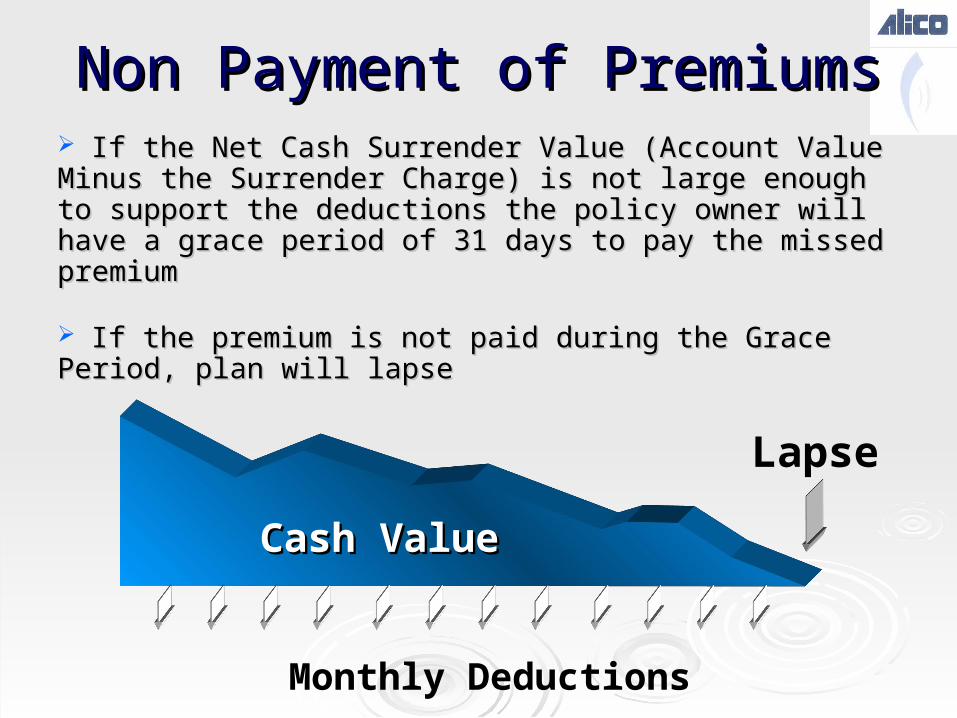

Non Payment of PremiumsNon Payment of Premiums

If a policy owner fails to pay his premiums, the monthly If a policy owner fails to pay his premiums, the monthly deductions to maintain the policy will be deducted from the deductions to maintain the policy will be deducted from the Account ValueAccount Value

Monthly Deductions

Account ValueAccount Value

Non Payment of PremiumsNon Payment of Premiums If the Net Cash Surrender Value (Account Value Minus If the Net Cash Surrender Value (Account Value Minus the Surrender Charge) is not large enough to support the the Surrender Charge) is not large enough to support the deductions the policy owner will have a grace period of 31 deductions the policy owner will have a grace period of 31 days to pay the missed premiumdays to pay the missed premium

If the premium is not paid during the Grace Period, plan If the premium is not paid during the Grace Period, plan will lapsewill lapse

Cash ValueCash Value

Monthly Deductions

Lapse

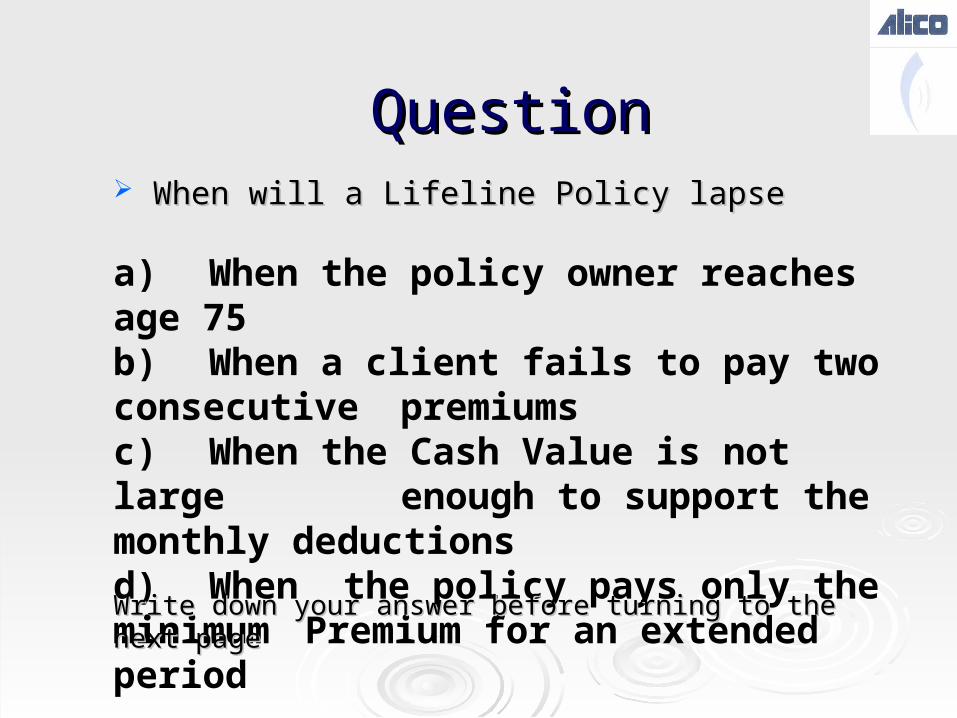

QuestionQuestion When will a Lifeline Policy lapse When will a Lifeline Policy lapse

a) When the policy owner reaches age 75 b) When a client fails to pay two consecutive premiumsc) When the Cash Value is not large enough to support the monthly deductionsd) When the policy pays only the minimum Premium for an extended period

Write down your answer before turning to the next pageWrite down your answer before turning to the next page

AnswerAnswer

The payment of the Minimum Premium will The payment of the Minimum Premium will support the policysupport the policy

The plan will lapse if the Cash Value is not The plan will lapse if the Cash Value is not large enough to support the monthly deductionslarge enough to support the monthly deductions

The correct answer is c)

ReinstatementReinstatement

A policy which has lapsed may be reinstated A policy which has lapsed may be reinstated within 3 years of the grace period and the lapse within 3 years of the grace period and the lapse of the plan of the plan

Lapse

Reinstatement within 3 years

ReinstatementReinstatement

The policy owner’s written request to The policy owner’s written request to reinstate the planreinstate the plan Evidence of health and satisfactory Evidence of health and satisfactory

insurabilityinsurability The payment of enough premium to The payment of enough premium to

keep the plan in force for 12 monthskeep the plan in force for 12 months

Reinstatement can take place when each of the following have been received

Ages of EligibilityAges of Eligibility

The minimum acceptable age for Lifeline is 3 monthsThe minimum acceptable age for Lifeline is 3 months

The maximum acceptable age is 65 (last birthday)The maximum acceptable age is 65 (last birthday)

Eligible for the plan

3 Months Age 65

Terms and Maturity DatesTerms and Maturity Dates Lifeline is written to mature on the policy anniversary immediately after the policy owner Lifeline is written to mature on the policy anniversary immediately after the policy owner reaches age 95reaches age 95

Premium payment term can be 10 years and abovePremium payment term can be 10 years and above

As no Surrender Charge is applied on surrenders after the 10th policy anniversaryAs no Surrender Charge is applied on surrenders after the 10th policy anniversary; ; policy policy owner can use the policy to provide the cash for his medium to long term financial goalsowner can use the policy to provide the cash for his medium to long term financial goals

Age 96

Policy must mature

Age 95

Minimum and Maximum Death Minimum and Maximum Death BenefitsBenefits

The minimum Face Amount available with The minimum Face Amount available with Lifeline is US$35,000Lifeline is US$35,000 The maximum Face Amount available with The maximum Face Amount available with Lifeline is US$10,000,000Lifeline is US$10,000,000

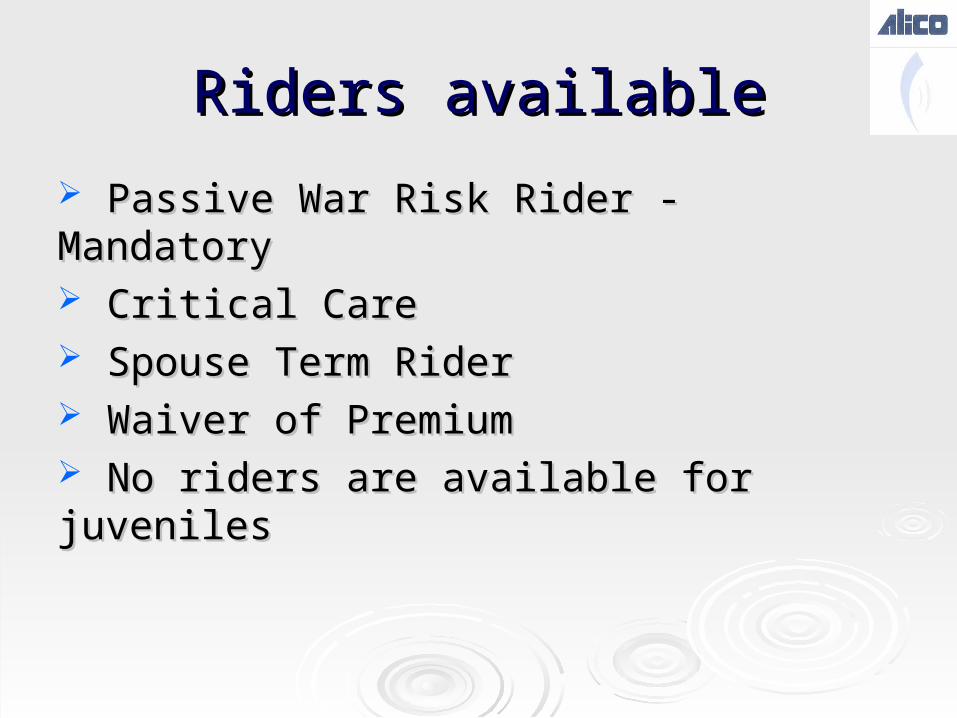

Riders availableRiders available

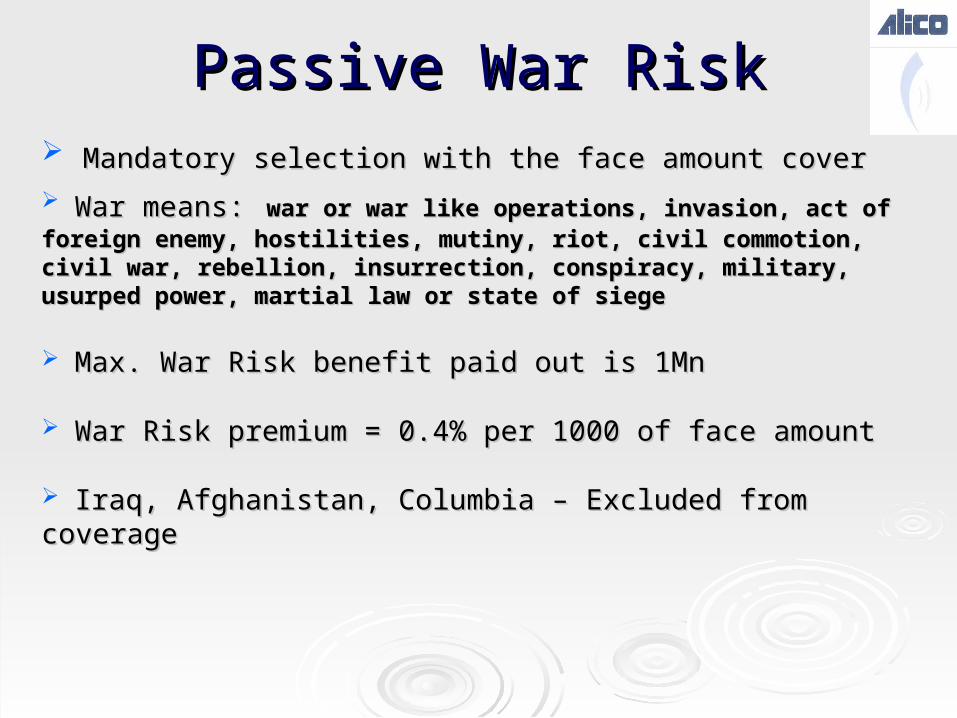

Passive War Risk Rider - MandatoryPassive War Risk Rider - Mandatory Critical CareCritical Care Spouse Term RiderSpouse Term Rider Waiver of PremiumWaiver of Premium No riders are available for juvenilesNo riders are available for juveniles

PasPassive War Risksive War Risk Mandatory selection with the face amount coverMandatory selection with the face amount cover

War meWar means:ans: war or war like operations, invasion, act of foreign war or war like operations, invasion, act of foreign enemy, hostilities, mutiny, riot, civil commotion, civil war, rebellion, enemy, hostilities, mutiny, riot, civil commotion, civil war, rebellion, insurrection, conspiracy, military, usurped power, martial law or state insurrection, conspiracy, military, usurped power, martial law or state of siegeof siege

Max. War Risk benefit paid out is 1MnMax. War Risk benefit paid out is 1Mn

War Risk premium = 0.4% per 1000 of face amountWar Risk premium = 0.4% per 1000 of face amount

Iraq, Afghanistan, Columbia – Excluded from coverageIraq, Afghanistan, Columbia – Excluded from coverage

Waiver of PremiumWaiver of Premium

In the event of insured’s disability – In the event of insured’s disability –

premiums are waived off until the end of termpremiums are waived off until the end of term

Insured needs to be disabled for a period of Insured needs to be disabled for a period of

6 months for WP6 months for WP

Spouse Term RiderSpouse Term Rider

For STR, passport copy with visa page of spouse is requiredFor STR, passport copy with visa page of spouse is required

Maximum STR cover is 100k or upto 50% of husband’s Maximum STR cover is 100k or upto 50% of husband’s

insurance cover whichever is lowerinsurance cover whichever is lower In the event of insured’s death – claim amt + spouse can buy In the event of insured’s death – claim amt + spouse can buy another policy upto the level of STR amt (Med is reqd.)another policy upto the level of STR amt (Med is reqd.)

STR will continue if main insured is disabled and WP starts STR will continue if main insured is disabled and WP starts paying for the policypaying for the policy

CI for Spouse if selected will be issued as Stand aloneCI for Spouse if selected will be issued as Stand alone

Critical CareCritical Care 32 Dread Diseases32 Dread Diseases

• Stand Alone (cannot be cancelled for 1Stand Alone (cannot be cancelled for 1stst five years) five years)

• Level Premium (At Entry Age) Level Premium (At Entry Age)

• Renewable up to age 75 (guaranteed renewability)Renewable up to age 75 (guaranteed renewability)

• Telemedicine / E-Consultation (Second Medical Opinion)Telemedicine / E-Consultation (Second Medical Opinion)

• Payment upon Diagnosis Payment upon Diagnosis

• Waiting Period 120 daysWaiting Period 120 days

• Max CI cover = 5 times annual incomeMax CI cover = 5 times annual income

• Max of CI, RBP from ALICO = 5 times annual incomeMax of CI, RBP from ALICO = 5 times annual income

• Real CI cover which separates the Life Insurance needs Real CI cover which separates the Life Insurance needs – non accelerated– non accelerated

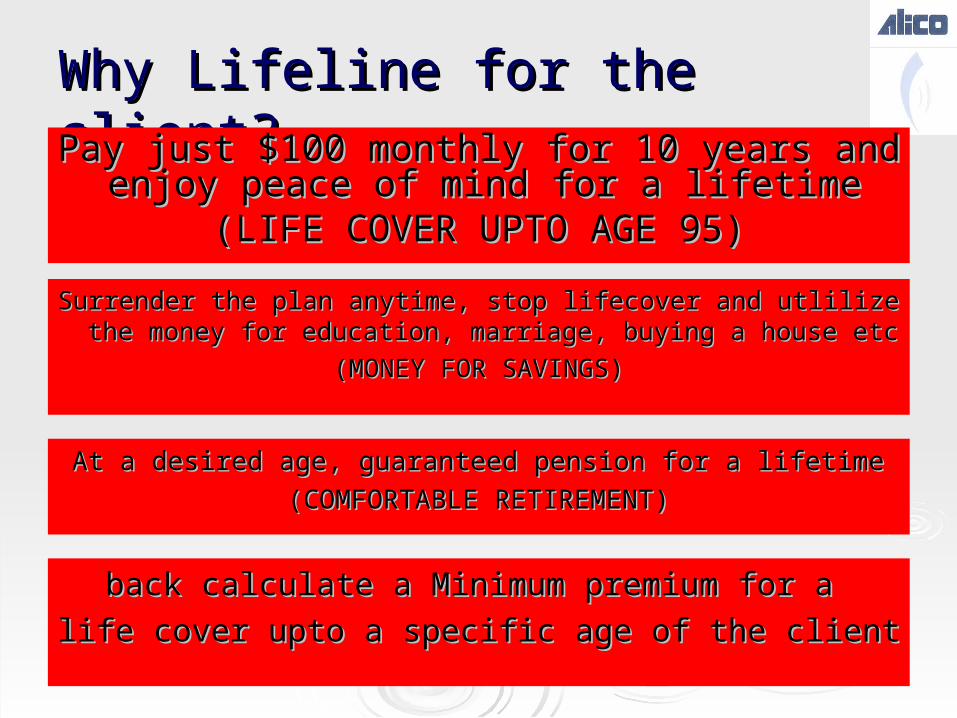

Why Lifeline for the client?Why Lifeline for the client?

Surrender the plan anytime, stop lifecover and utlilize the Surrender the plan anytime, stop lifecover and utlilize the money for education, marriage, buying a house etc money for education, marriage, buying a house etc

(MONEY FOR SAVINGS)(MONEY FOR SAVINGS)

At a desired age, guaranteed pension for a lifetimeAt a desired age, guaranteed pension for a lifetime

(COMFORTABLE RETIREMENT)(COMFORTABLE RETIREMENT)

back calculate a Minimum premium for a back calculate a Minimum premium for a

life cover upto a specific age of the clientlife cover upto a specific age of the client

Pay just $100 monthly for 10 years and enjoy Pay just $100 monthly for 10 years and enjoy peace of mind for a lifetime peace of mind for a lifetime

(LIFE COVER UPTO AGE 95)(LIFE COVER UPTO AGE 95)

Sales ProcessSales ProcessAED 10,000 - Monthly family income

AED 3,000 – Rent

AED 1,500 – Car Loan

AED 3,000 – Living

AED 2,500 – Net Disposable Income

Short Term needsAED 500

Long Term needsAED 2,000

Capital Plus Plan for $680 per month

DEATH

Annual expenseof the family

= AED 90,000 = $ 24,523

In your country – 50% = $12,261.5 per annum

Fixed Deposit amount to give $12,261.5

as annual interest at 5% = $245,230

Lifeline Plan with Face amount of

$245,230

Monthly expense of the family remains same = AED 7,500

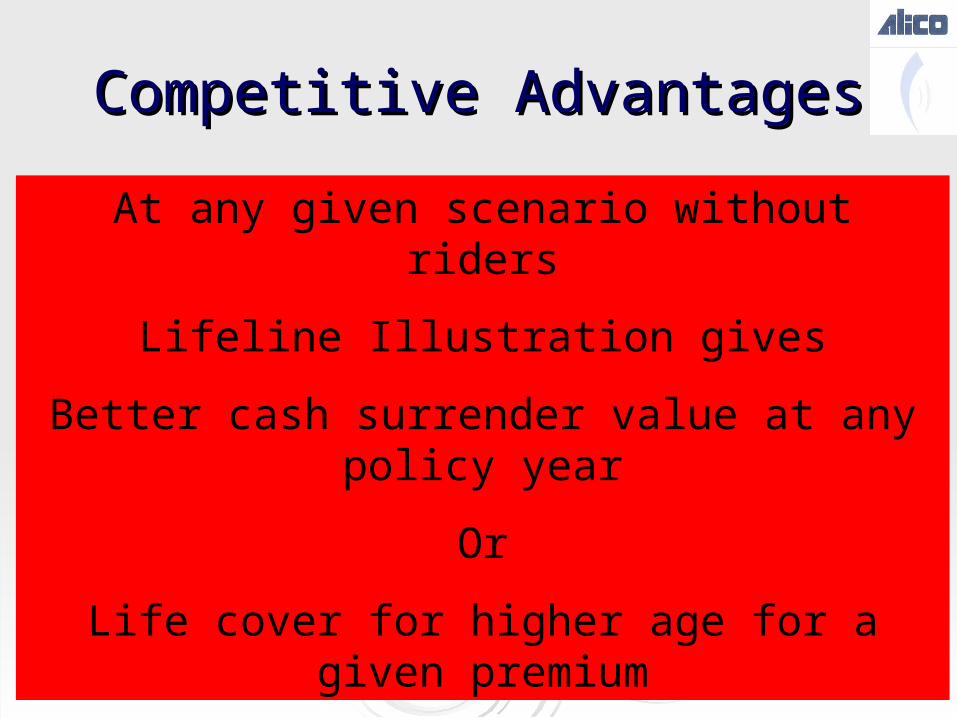

Competitive AdvantagesCompetitive Advantages

At any given scenario without riders

Lifeline Illustration gives

Better cash surrender value at any policy year

Or

Life cover for higher age for a given premium

Competitive AdvantagesCompetitive Advantages

ParametersParameters ALICOALICO CompetitionCompetition

Guaranteed return fundGuaranteed return fund 3% per annum3% per annum Cumulative of an average of Cumulative of an average of 2.75% per annum over 10 yrs2.75% per annum over 10 yrs

Pension OptionPension Option √√

Competitive AdvantagesCompetitive Advantages

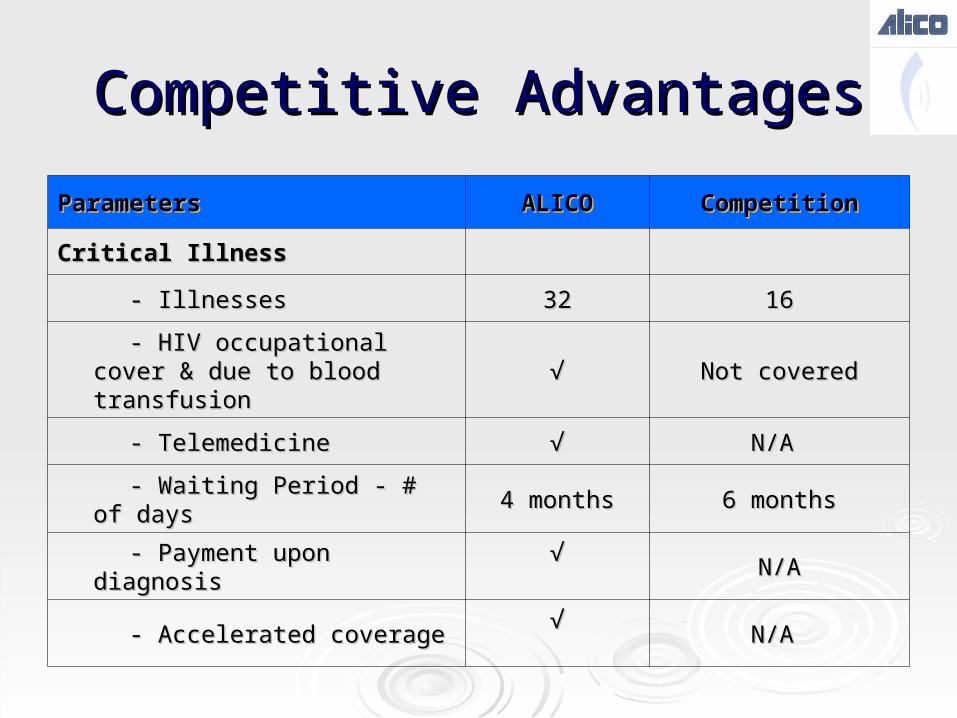

ParametersParameters ALICOALICO CompetitionCompetition

Critical IllnessCritical Illness

- Illnesses- Illnesses 3232 1616

- HIV occupational cover & due to - HIV occupational cover & due to blood transfusionblood transfusion √√ Not coveredNot covered

- Telemedicine- Telemedicine √√ N/A N/A

- Waiting Period - # of days- Waiting Period - # of days 4 months4 months 6 months6 months

- Payment upon diagnosis- Payment upon diagnosis √√N/AN/A

- Accelerated coverage- Accelerated coverage √√

N/A N/A

Competitive AdvantagesCompetitive Advantages

ParametersParameters ALICOALICO CompetitionCompetition

ServicesServices

- Commitment of 2 day service response- Commitment of 2 day service response √√ N/AN/A

- Quick turnaround medical results - 2 Days - Quick turnaround medical results - 2 Days from the date of medicals donefrom the date of medicals done √√ N/AN/A

- Well knit Medical facilities inside Gulf- Well knit Medical facilities inside Gulf √√ N/AN/A

Competitive AdvantagesCompetitive Advantages

ParametersParameters ALICOALICO CompetitionCompetition

Application FormApplication Form - # of pages - # of pages 22 99

Medical QuestionnaireMedical Questionnaire - # of pages - # of pages 11 66

DocumentationDocumentation

- Application- Application √√ √√

- Financial Planner- Financial Planner √√

- Proof of residence (i.e. Utility bill)- Proof of residence (i.e. Utility bill) √√

- Illustration- Illustration √√ √√

- Passport Copy- Passport Copy √√ √√

Competitive AdvantagesCompetitive Advantages

ParametersParameters ALICOALICO CompetitionCompetition

Guaranteed return fundGuaranteed return fund 3% per annum3% per annum Cumulative of an average of Cumulative of an average of 2.75% per annum over 10 yrs2.75% per annum over 10 yrs

Pension OptionPension Option √√

Competitive AdvantagesCompetitive Advantages

ParametersParameters ALICOALICO CompetitionCompetition

Critical IllnessCritical Illness

- Illnesses- Illnesses 3232 1616

- HIV occupational cover & due to - HIV occupational cover & due to blood transfusionblood transfusion √√ Not coveredNot covered

- Telemedicine- Telemedicine √√ N/A N/A

- Waiting Period - # of days- Waiting Period - # of days 4 months4 months 6 months6 months

- Payment upon diagnosis- Payment upon diagnosis √√N/AN/A

- Accelerated coverage- Accelerated coverage √√

N/A N/A

Competitive AdvantagesCompetitive Advantages

ParametersParameters ALICOALICO CompetitionCompetition

ServicesServices

- Commitment of 2 day service response- Commitment of 2 day service response √√ N/AN/A

- Quick turnaround medical results - 2 Days - Quick turnaround medical results - 2 Days from the date of medicals donefrom the date of medicals done √√ N/AN/A

- Well knit Medical facilities inside Gulf- Well knit Medical facilities inside Gulf √√ N/AN/A

ALICO – AIG strengthALICO – AIG strength

ALICO, member of American International Group, AIG, is ALICO, member of American International Group, AIG, is incorporated in 1921 in Delaware, U.S.A.incorporated in 1921 in Delaware, U.S.A.

ALICO operates directly and through subsidiaries in 55 ALICO operates directly and through subsidiaries in 55 countries in the Middle East, Europe, Latin America, countries in the Middle East, Europe, Latin America, Africa, the Far East, South Asia, The Caribbean and Africa, the Far East, South Asia, The Caribbean and CanadaCanada

With 50 years plus presence in the Gulf region, ALICO With 50 years plus presence in the Gulf region, ALICO has great experience in selling insurance products.has great experience in selling insurance products.

ALICO is a AA+ rated company – No other company is ALICO is a AA+ rated company – No other company is more able to paymore able to pay

Lifeline – Example Lifeline – Example Male, Age 30Male, Age 30 Coverage:Coverage:

US$ 100,000 Life InsuranceUS$ 100,000 Life Insurance War Risk War Risk

Term of payment 10 yearsTerm of payment 10 years 6% assumed yield6% assumed yield Monthly Contribution $104 for coverage for 20 yearsMonthly Contribution $104 for coverage for 20 years Monthly Contribution $104 for coverage till age 80Monthly Contribution $104 for coverage till age 80 Monthly Contribution $104 for coverage till age 95Monthly Contribution $104 for coverage till age 95 With cash surrender value of $20,621 at age 55With cash surrender value of $20,621 at age 55

Lifeline – Example Lifeline – Example Male, Age 50Male, Age 50 Coverage:Coverage:

US$ 100,000 Life InsuranceUS$ 100,000 Life Insurance War Risk War Risk

Term of payment 10 yearsTerm of payment 10 years 6% assumed yield6% assumed yield Monthly Contribution $126 for coverage for 20 yearsMonthly Contribution $126 for coverage for 20 years Monthly Contribution $170 for coverage till age 80Monthly Contribution $170 for coverage till age 80 Monthly Contribution $235 for coverage till age 95 with Monthly Contribution $235 for coverage till age 95 with

cash surrender value of $10,572 at age 60cash surrender value of $10,572 at age 60

Lifeline – Example Lifeline – Example Male, Age 30Male, Age 30 Coverage:Coverage:

$100,000 of Life Insurance$100,000 of Life Insurance War Risk War Risk $50,000 of CC cover$50,000 of CC cover WPWP

Term of payment 10 yearsTerm of payment 10 years 6% assumed yield6% assumed yield Monthly Contribution $166 for coverage for 20 yearsMonthly Contribution $166 for coverage for 20 years Monthly Contribution $233 for coverage till age 80Monthly Contribution $233 for coverage till age 80 Monthly Contribution $242 for coverage till age 95 with cash Monthly Contribution $242 for coverage till age 95 with cash

surrender value of $20,621 at age 55surrender value of $20,621 at age 55

Lifeline – Example Lifeline – Example Male, Age 30Male, Age 30 Coverage:Coverage:

$500,000 of Life Insurance$500,000 of Life Insurance $100,000 of CC$100,000 of CC War RiskWar Risk WPWP

Term of payment 10 yearsTerm of payment 10 years 6% assumed yield6% assumed yield Monthly Contribution $445 for coverage for 20 yearsMonthly Contribution $445 for coverage for 20 years Monthly Contribution $652 for coverage till age 80Monthly Contribution $652 for coverage till age 80 Monthly Contribution $732 for coverage till age 95 with cash surrender Monthly Contribution $732 for coverage till age 95 with cash surrender

value of $133,960 at age 60value of $133,960 at age 60

Lifeline – Underwriting FlowchartLifeline – Underwriting Flowchart

NBD Alico UND Data entryExisting ins with Alico?

Assessment of riskFurther requirements

ALICO is committed to ensure a turn around time of two days for policy issuance from the date of submission with all requirements

Decision made

Check list of documents required Check list of documents required to join the ‘Lifeline’ planto join the ‘Lifeline’ plan• Application with full details furnished by the client. Signature Application with full details furnished by the client. Signature and name of the sales agent (Witness) and the client to be and name of the sales agent (Witness) and the client to be furnished.furnished.

• Illustrations print out signed by the client.Illustrations print out signed by the client.

• Provide valid passport copy with valid visa page of the clientProvide valid passport copy with valid visa page of the client

• In case of face amount request of above $250,000 or age of In case of face amount request of above $250,000 or age of client above 55, client needs to go through medical check up.client above 55, client needs to go through medical check up.

• In case of face amount request of above $500,000, client In case of face amount request of above $500,000, client needs to furnish and sign the confidential financial report needs to furnish and sign the confidential financial report (UND52).(UND52).

• In case of face amount request of above $750,000 both the In case of face amount request of above $750,000 both the client and the sales agent needs to furnish and sign the client and the sales agent needs to furnish and sign the financial report (UND52 and UND54)financial report (UND52 and UND54)

Underwriting GuidelinesUnderwriting Guidelines No Medical underwriting for coverage up to: $250K/ Age 55No Medical underwriting for coverage up to: $250K/ Age 55

3-day maximum turnaround time for medical cases (after the 3-day maximum turnaround time for medical cases (after the medical is donemedical is done

All coverage starts from the date of application or date of All coverage starts from the date of application or date of medical donemedical done

All riders are contestable at any point of timeAll riders are contestable at any point of time

Misrepresentation is not contestable after 2 yearsMisrepresentation is not contestable after 2 years

UND6 form for any amendment required in the applicationUND6 form for any amendment required in the application

Compulsory Medicals for Nationalities – Somalia, Tanzania, Compulsory Medicals for Nationalities – Somalia, Tanzania,

Nigeria, CISNigeria, CIS

Underwriting GuidelinesUnderwriting Guidelines

• Housewife can buy ‘WL’ with max cover upto 200K or Housewife can buy ‘WL’ with max cover upto 200K or upto 50% of husband’s insurance cover whichever is lowerupto 50% of husband’s insurance cover whichever is lower

• All children should have equal insured coverage; no All children should have equal insured coverage; no partialitypartiality

• Maximum life cover = 10 times annual incomeMaximum life cover = 10 times annual income

• 88thth and 9 and 9thth month of pregnancy – cannot buy insurance month of pregnancy – cannot buy insurance

• 11stst to 7 months of pregnancy – cannot buy any living to 7 months of pregnancy – cannot buy any living

benefit (CI)benefit (CI)

• one month after delivery – can buy insuranceone month after delivery – can buy insurance

• 20 cigarettes per day and above is medical and mostly 20 cigarettes per day and above is medical and mostly

sub std.sub std.

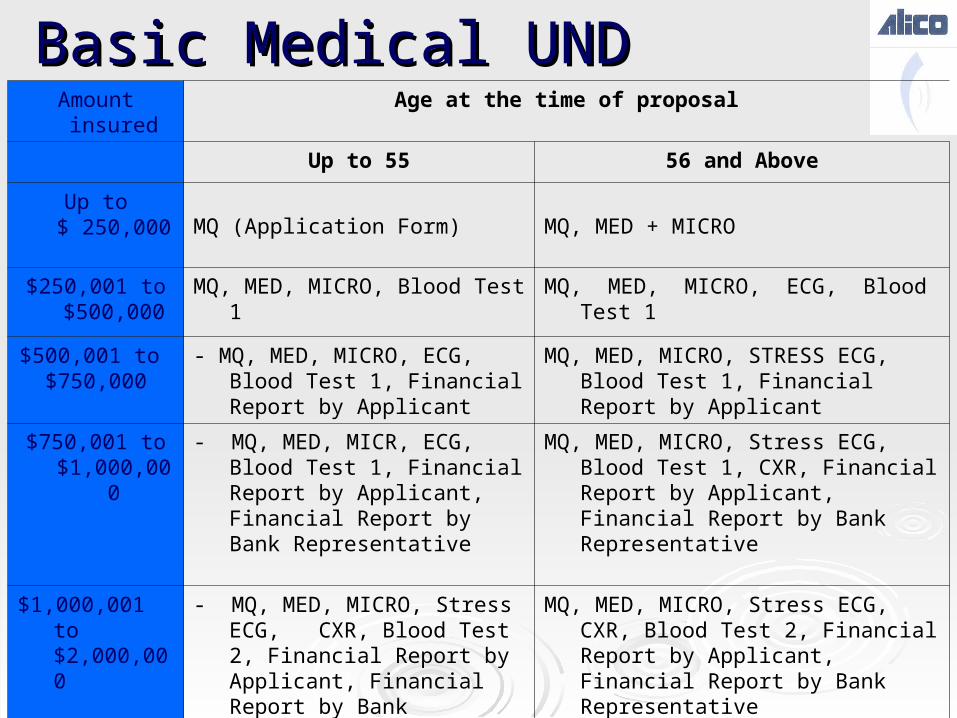

Amount insured Age at the time of proposal

Up to 55 56 and Above

Up to$ 250,000 MQ (Application Form) MQ, MED + MICRO

$250,001 to $500,000

MQ, MED, MICRO, Blood Test 1 MQ, MED, MICRO, ECG, Blood Test 1

$500,001 to $750,000

- MQ, MED, MICRO, ECG, Blood Test 1, Financial Report by Applicant

MQ, MED, MICRO, STRESS ECG, Blood Test 1, Financial Report by Applicant

$750,001 to $1,000,000

- MQ, MED, MICR, ECG, Blood Test 1, Financial Report by Applicant, Financial Report by Bank Representative

MQ, MED, MICRO, Stress ECG, Blood Test 1, CXR, Financial Report by Applicant, Financial Report by Bank Representative

$1,000,001 to $2,000,000

- MQ, MED, MICRO, Stress ECG, CXR, Blood Test 2, Financial Report by Applicant, Financial Report by Bank Representative

MQ, MED, MICRO, Stress ECG, CXR, Blood Test 2, Financial Report by Applicant, Financial Report by Bank Representative

Above2,000,000 USD

Refer to ALICO Refer to ALICO

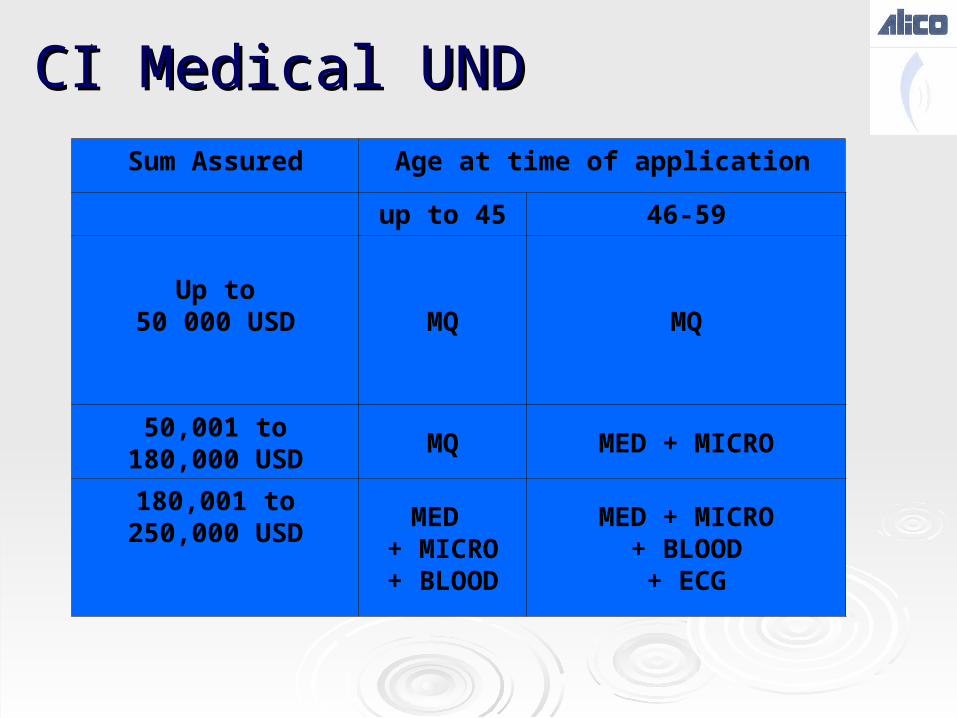

Basic Medical UNDBasic Medical UND

:

Sum Assured Age at time of application

up to 45 46-59

Up to50 000 USD MQ MQ

50,001 to 180,000 USD MQ MED + MICRO

180,001 to 250,000 USD

MED + MICRO+ BLOOD

MED + MICRO+ BLOOD

+ ECG

CI Medical UNDCI Medical UND

Definition: Owner/Holder and InsuredDefinition: Owner/Holder and Insured The person who is buying Insurance is made is ‘Proposed The person who is buying Insurance is made is ‘Proposed

Insured’Insured’

The person who pays premium is ‘Owner/Applicant’The person who pays premium is ‘Owner/Applicant’

If Insured dies – LL is closed and A/C value paid to If Insured dies – LL is closed and A/C value paid to beneficiarybeneficiary

If Owner dies – LL can be continued by another person If Owner dies – LL can be continued by another person (Insurable interest) paying the premiums; or NCSV is paid to (Insurable interest) paying the premiums; or NCSV is paid to beneficiarybeneficiary

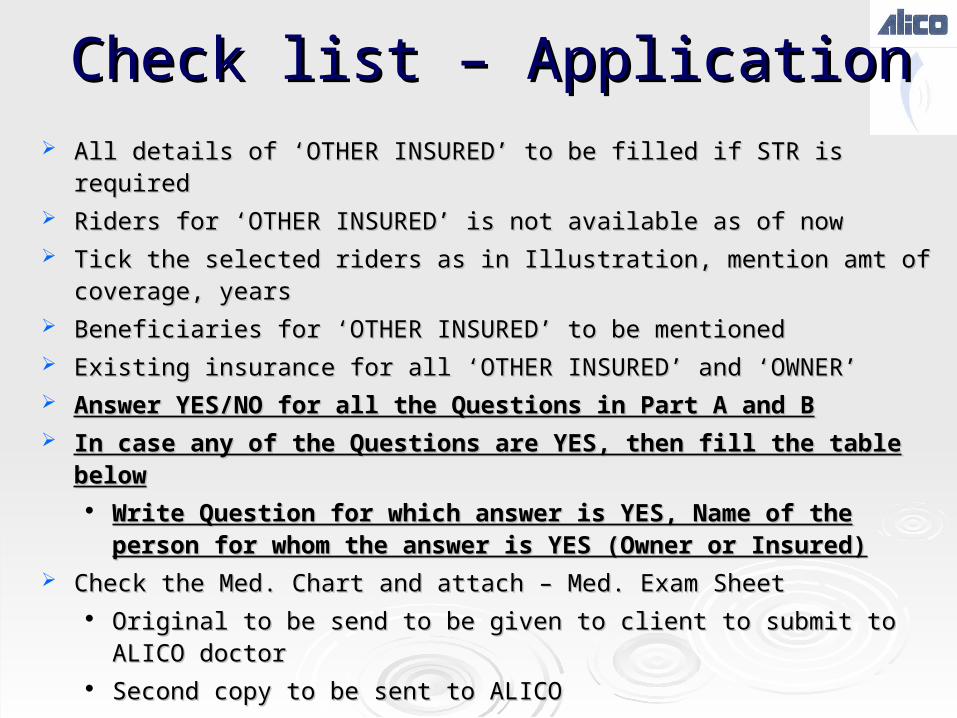

Check list – ApplicationCheck list – Application Full name as in passport (should match with Illustration)Full name as in passport (should match with Illustration) Passport No, Sex, DOB as in passport, Age last Birthday (as in Illustration)Passport No, Sex, DOB as in passport, Age last Birthday (as in Illustration) Nationality (as in passport), any other nationality, place of birth, Marital StatusNationality (as in passport), any other nationality, place of birth, Marital Status Average Annual Income – last 12 months, Other sources of incomeAverage Annual Income – last 12 months, Other sources of income Residence Address with Flat No, Street No, Area, Emirate, Country, TelResidence Address with Flat No, Street No, Area, Emirate, Country, Tel Occupational Status – all the fields, with Office address; PO BoxOccupational Status – all the fields, with Office address; PO Box Applicant/owner name – owner/holder and Insured is different, Rel. to insuredApplicant/owner name – owner/holder and Insured is different, Rel. to insured Send correspondence to – Send correspondence to – Amt of insurance in words, in USD, Plan Duration, Mode of payment, Modal Amt of insurance in words, in USD, Plan Duration, Mode of payment, Modal

planned premium (TP + excess)planned premium (TP + excess) Riders – WP, CC – mention amtRiders – WP, CC – mention amt Multiple Beneficiaries allowedMultiple Beneficiaries allowed Fund allocation to be in multiples of 10% ( in line with strategy in Fund allocation to be in multiples of 10% ( in line with strategy in

illustration)illustration)

All details of ‘OTHER INSURED’ to be filled if STR is requiredAll details of ‘OTHER INSURED’ to be filled if STR is required Riders for ‘OTHER INSURED’ is not available as of nowRiders for ‘OTHER INSURED’ is not available as of now Tick the selected riders as in Illustration, mention amt of coverage, yearsTick the selected riders as in Illustration, mention amt of coverage, years Beneficiaries for ‘OTHER INSURED’ to be mentionedBeneficiaries for ‘OTHER INSURED’ to be mentioned Existing insurance for all ‘OTHER INSURED’ and ‘OWNER’Existing insurance for all ‘OTHER INSURED’ and ‘OWNER’ Answer YES/NO for all the Questions in Part A and BAnswer YES/NO for all the Questions in Part A and B In case any of the Questions are YES, then fill the table belowIn case any of the Questions are YES, then fill the table below

Write Question for which answer is YES, Name of the person for Write Question for which answer is YES, Name of the person for whom the answer is YES (Owner or Insured)whom the answer is YES (Owner or Insured)

Check the Med. Chart and attach – Med. Exam SheetCheck the Med. Chart and attach – Med. Exam Sheet Original to be send to be given to client to submit to ALICO doctorOriginal to be send to be given to client to submit to ALICO doctor Second copy to be sent to ALICOSecond copy to be sent to ALICO Third copy to be retained in the bankThird copy to be retained in the bank

Check list – ApplicationCheck list – Application

Features Explanations Benefits

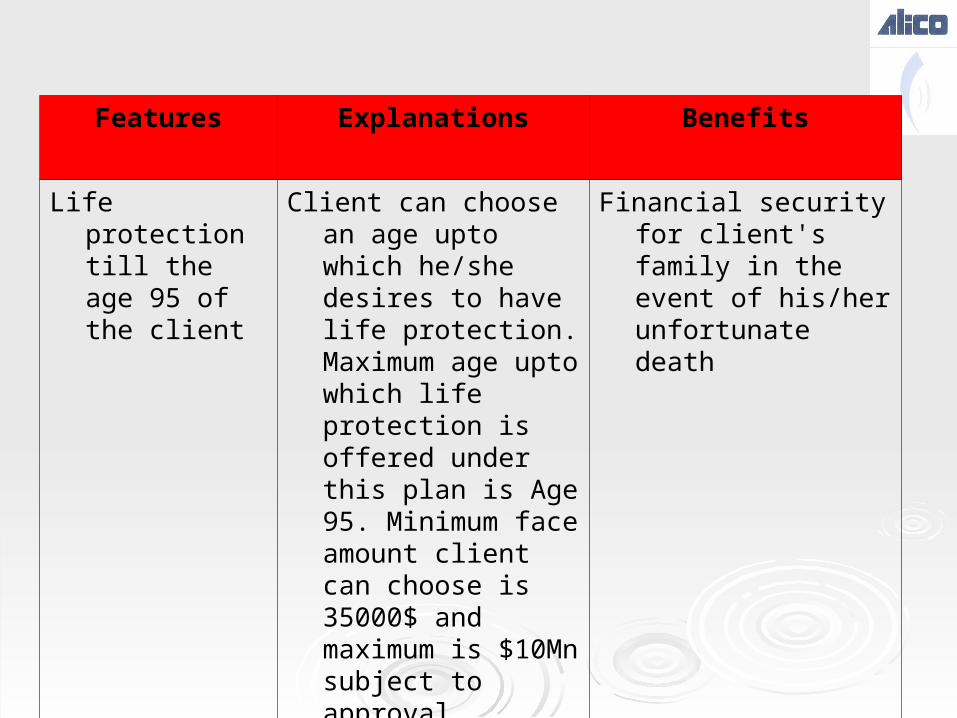

Life protection till the age 95 of the client

Client can choose an age upto which he/she desires to have life protection. Maximum age upto which life protection is offered under this plan is Age 95. Minimum face amount client can choose is 35000$ and maximum is $10Mn subject to approval

Financial security for client's family in the event of his/her unfortunate death

Features Explanations Benefits

Shorter premium payment term of 10 years

client needs to contribute premiums to the plan only for 10 years and get extended life protection till an age (less than 95) he/she desires

An expat client living in UAE needs to pay only for a period of 10 years when he has the disposable income, but get life protected till an age (less than 95) he/she desires

Features Explanations Benefits

Pension/ Annuity Option

Choice of using the lump sum account value at the chosen pension age to provide an annuity/pension guaranteed for the next 20 years or for life thereafter if the insured is alive

Helps to plan for good retired life at the desired time in life and to financially secure the beneficiary with a regular income upto 20 years

Features Explanations Benefits

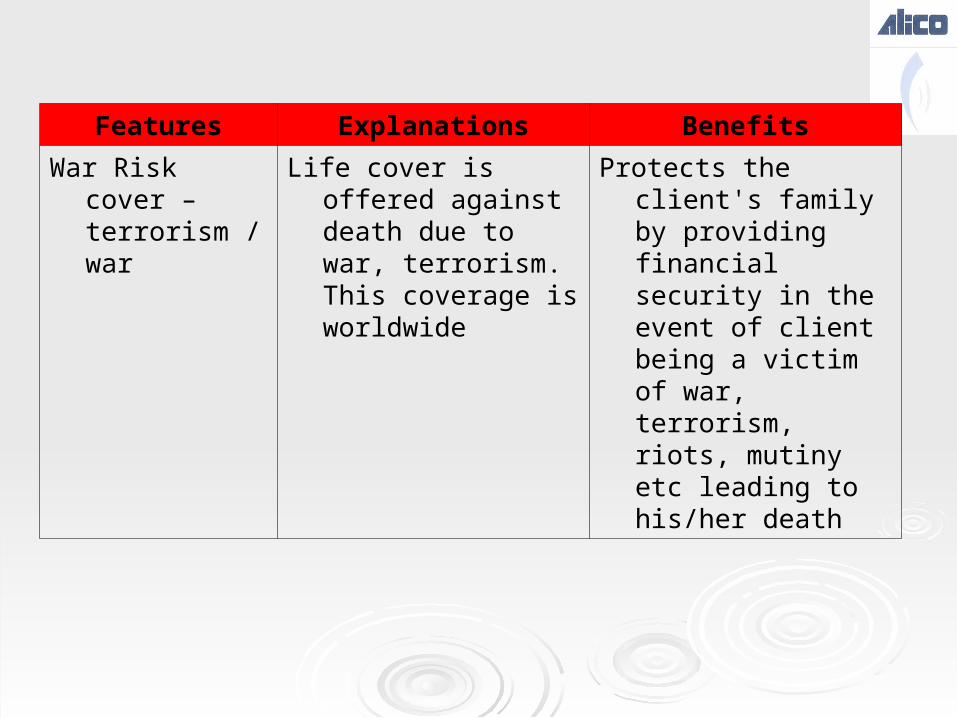

War Risk cover – terrorism / war

Life cover is offered against death due to war, terrorism. This coverage is worldwide

Protects the client's family by providing financial security in the event of client being a victim of war, terrorism, riots, mutiny etc leading to his/her death

Features Explanations Benefits

Flexibility in Increase/decrease of the Sum Assured amount

Face Amount increases can be made after the 2nd policy year subject to evidence of insurability. There is a limit of one increase per year. The minimum amount of increase is USD 10,000. The maximum amount of increase will be 50% of initial face amount. Face amount decreases can be made after 5 years as long as the resulting Face Amount is not less than $35,000

According to the change of needs in client's life, his/her requirement of life coverage may also change. Lifeline provides to increase or decrease the face amount accordingly.

Features Explanations Benefits

Optional/ Additional Insurance Benefits

Waiver of premium - in case of client becoming totally and permanantly disabled, ALICO will pay the premiums on behalf of the client so that his/her financial objectives are achieved. Critical Illness - In the event of client being diagnosed of any of the 32 critical illness + tele medicine, a lumpsum amount is paid out to the client which he/she can use for the treatment of the illness. CI coverage amount is not deducted from the life coverage in the event of client's death after ALICO pays out CI coverage amount Spouse Term Insurance - To protect spouse's life.

Offers comprehensive protection and thus financial security to the client and to his/her family in the event of the client becoming disabled or contracting a critical illness

Features Explanations Benefits

Low minimum premium

With as little as US$100 per month, you can start a savings plan

You can have access to 3 different investment funds, covering all major markets and sectors, which generally require a much higher premium per fund to invest into.

Why Lifeline - for bank; for youGuaranteed "2 day" Turn

around timeResponse from ALICO to the bank

for a Non medical case will be within 2 working days. For a medical cases, response within 3 days of client completing the required medical examinations

RM/ Bank spends less time per client and sell more policies and make more revenue

ALICO's Local administration

The team is based in Sharjah. Everything is handled locally, from processing to issuing policy. Closer to the market : Allows us to understand your requirements better and fine tune servicing where needed

Quick and prompt pre and post sales service. It will be percieved by the client as " I care" - This will strengthen the relationship of the bank with your client

Easy Documentation requirements at the time of applying

3 page simple application form signed , Passport copy with valid visa page, Illustration signed

Non probing to the client and reduces customer remorse, user friendly to the sales agent in the bank. This means bank spends less time per client and sell more policies and make more revenue

Relaxed Medical underwriting

No medical underwriting requirements if the client is choosing a face amount of less than 250,000$ and client is of age less than 55

RM/ Bank spends less time per client and sell more policies and make more revenue

Thank youThank you

&&

All the best All the best