9-1 copyright 2009 mcgraw-hill australia pty ltd ppts t/a business finance 10e by peirson slides...

TRANSCRIPT

9-1

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Chapter 9

Sources of Long-Term Finance: Equity

9-2

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Learning Objectives• Outline the characteristics of ordinary shares.

• Explain the advantages and disadvantages of equity as a source of finance.

• Outline the main sources of private equity in the Australian market.

• Disclose information when issuing securities.

• Outline the process of floating a public company.

• Discuss alternative explanations for the underpricing of initial public offerings (IPOs).

9-3

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Learning Objectives (cont.)• Discuss long-term performance of IPOs.

• Explain how companies raise capital through rights issues, placements, share purchase plans, and share options.

• Outline the different types of employee share plans.

• Outline the advantages of internal equity as a source of finance.

• Outline the effects of bonus issues, share splits and share consolidations.

9-4

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

The Characteristics of Ordinary Shares (OS)• Ordinary shares represent an ownership interest in

a business.

• Residual claim

– The holder has a claim to the profits of the business (through dividends). In the event of failure, the holder has a claim to the residual value of the assets after claims of all other entitled parties are met.

– Due to this residual claim, shareholders are more likely to lose their investment if the company fails (shareholders are said to provide the company’s risk capital).

– To compensate for this risk, shareholders expect a return that is greater than that received by lending.

9-5

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

The Characteristics of OS (cont.)• Fully and partly paid shares

– When new shares are created, they will have a stated issue price, which may be paid in full at issue.

– Alternatively, shares may be issued for part payment, with the balance paid in subsequent instalments, often referred to as calls.

– The size and timing of calls may be specified at the outset or determined at some date after issue.

– If the issue price has not been paid in full, shares are called partly paid or contributing shares.

– Instalment receipts are marketable securities for which only part of the issue price has been paid.

9-6

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

The Characteristics of OS (cont.)• Fully and partly paid shares (cont.)

– The balance of an instalment receipt is payable in a final instalment on or before a specified date.

– A well-known example is the Australian government’s sale of Telstra shares, which was executed through the issue of instalment receipts.

– Main differences from partly paid shares are:

timing and size of instalments are specified up front,

instalments are payable to vendor of shares rather than issuing company, and

holders of instalment receipts are entitled to the same dividends as ordinary shareholders.

9-7

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

The Characteristics of OS (cont.)• Limited liability:

– Protects shareholders' liability to meet a company’s debts. The liability is limited to any amount unpaid on the shares they hold.

• No liability (NL) companies:– Restricted to operating in the mining industry.

– Holders of partly paid shares are not obliged to pay calls made by the company — though shares are forfeited if calls are not paid.

• Rights of shareholders:– Entitled to proportional share of any dividend declared.

– Right to exert a degree of control over management through use of voting rights attached to ordinary shares — (typically need at least 50% of shares to execute rights).

– Shareholders have the right to sell their shares.

9-8

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

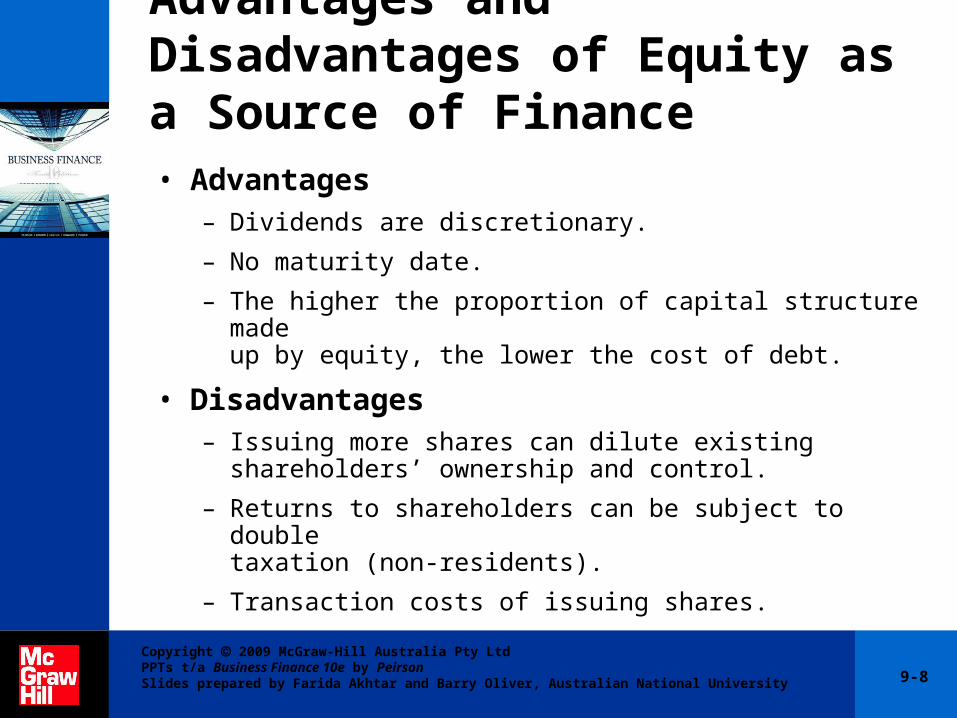

Advantages and Disadvantages of Equity as a Source of Finance• Advantages

– Dividends are discretionary.

– No maturity date.

– The higher the proportion of capital structure made up by equity, the lower the cost of debt.

• Disadvantages– Issuing more shares can dilute existing shareholders’

ownership and control.

– Returns to shareholders can be subject to double taxation (non-residents).

– Transaction costs of issuing shares.

9-9

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Private Equity• What is private equity?

– Securities issued to investors are not publicly traded. This includes family members and friends, but a more formal source is a private equity fund.

– Private equity or venture capital — not only for new ventures.

• Four categories of private equity financing:– Start-up: new companies, funds to develop products.– Expansion: additional funds required to manufacture and

sell products commercially.– Turnaround: assist a company in financial difficulty.– MBO: where a business is purchased by its management

team with the assistance of a private equity partner or fund.

• In illiquid markets, investors must hold funds for 5–10 years.

9-10

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Information problems and new ventures:

• Three information problems with new ventures:

– Information on venture value — incomplete and uncertain.

– Information asymmetry — either party, the entrepreneur or investor, may have more information than the other.

– Idea may be stolen by potential investors.

• New ventures are typically financed in stages to overcome uncertainty and information asymmetry problems.

• Entrepreneur may require confidentiality agreements with potential investors in order to prevent them from stealing the idea.

• Venture capitalists usually do not sign such agreements.

• Instead, they focus on establishing and protecting a reputation for honesty and integrity.

Private Equity (cont.)

9-11

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Sources of Finance for New Ventures• Sources include bank loans, private equities and IPO

funds.

• Stages of a venture include:– R&D phase.

– Start-up phase, equipment and personnel assembled.

– Rapid growth, if product is successful.

– Slower growth, followed by maturity and possible decline.

• Different sources of finance are appropriate at different stages.

• Personal savings, personal loans and home mortgages are the most likely sources at R&D stage.

• Business angel may enter the R&D stage if these other sources are exhausted.

9-12

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

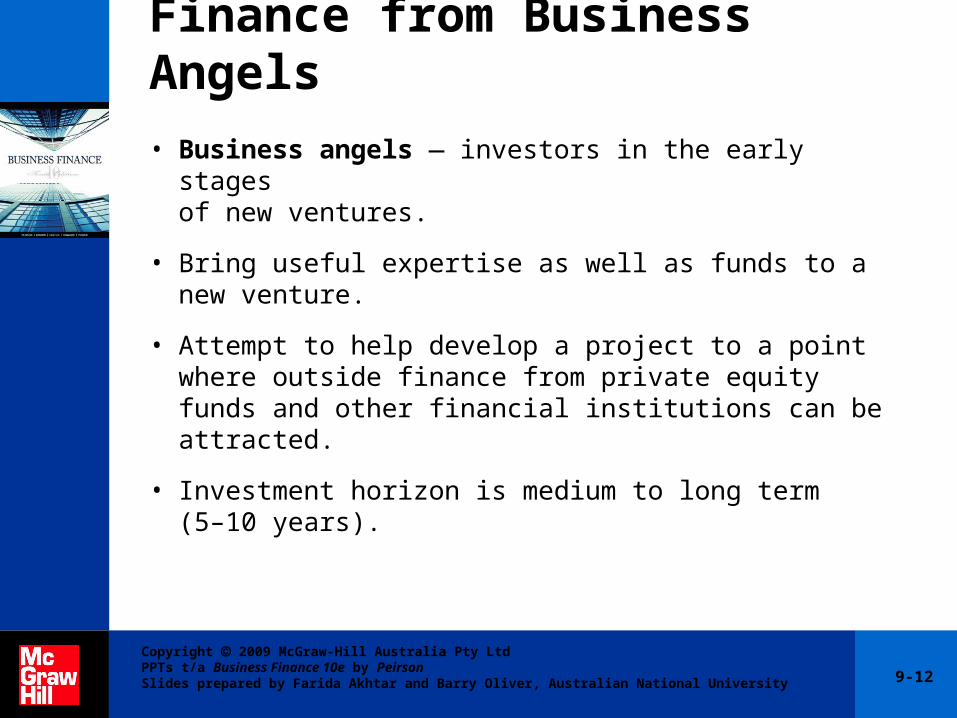

Finance from Business Angels

• Business angels — investors in the early stages of new ventures.

• Bring useful expertise as well as funds to a new venture.

• Attempt to help develop a project to a point where outside finance from private equity funds and other financial institutions can be attracted.

• Investment horizon is medium to long term (5–10 years).

9-13

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Finance from Private Equity Funds• ABS estimates $15.2b committed to private

equity market at 30 June 2007.

• As at June 2007, 280 private equity funds operated in Australia by 186 fund managers, investing in 1076 companies.

• According to ABS, these 186 managers reviewed 8769 potential investments in 2006–07, of which only 229 have been successful.

• Investments range from $500 000 to $20m over 3–7 years.

9-14

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Finance from Private Equity Funds(cont.)• Looking for projects with high growth prospects.

• Private equity investments are relatively risky — higher rates of return are typically required.

• To obtain private equity, require a well-structured and convincing business plan.

• Private equity fund managers usually require a seat on the board of the company.

• These managers specialise in new, fast-growing companies. They can offer specialised expertise to help the venture succeed.

9-15

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

• Private equity fund managers seek capital gains rather than dividends and will plan to divest within 3–7 years.

• While disposal of the investment can result in spectacular gain, the level of risk is high, it is to be expected that a significant proportion of the disposals that occur will involve loss. In some cases, project will fail and investment liquidated.

• Larger sources of private equity include superannuation funds, fund managers and banks.

• Government has encouraged private equity with incentives such as the Pooled Development Funds Program and the Innovations Investment Fund Program.

Finance from Private Equity Funds(cont.)

9-16

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Information Disclosure

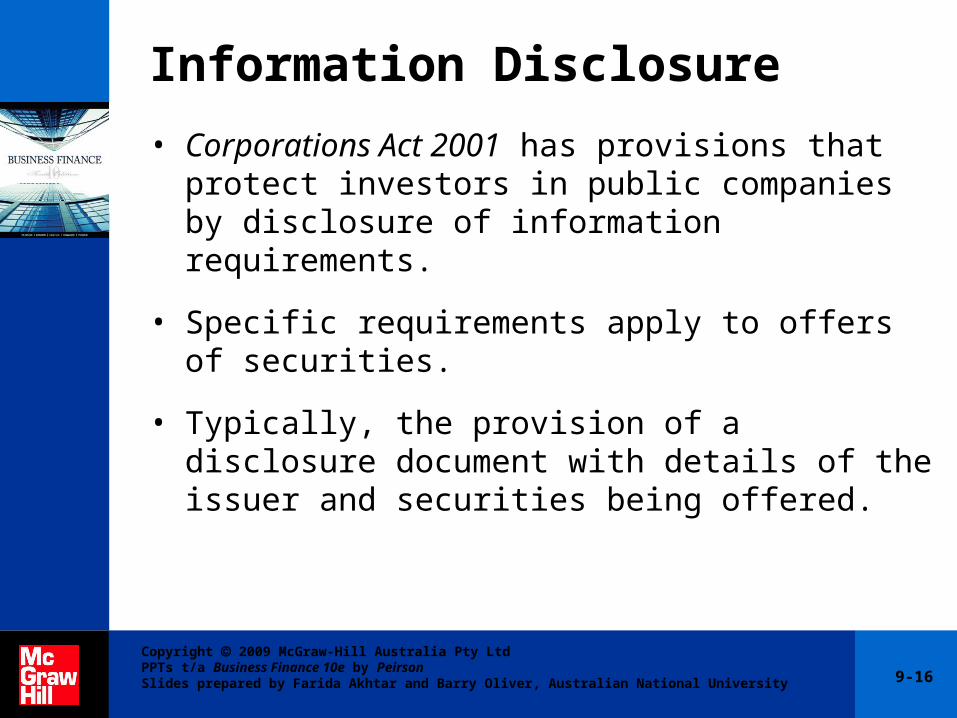

• Corporations Act 2001 has provisions that protect investors in public companies by disclosure of information requirements.

• Specific requirements apply to offers of securities.

• Typically, the provision of a disclosure document with details of the issuer and securities being offered.

9-17

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Offers of Unlisted Securities• Offers of unlisted securities include IPOs of

shares and offers of new classes of securities by listed companies.

• In these cases, securities do not have an obvious market price and information can help determine the appropriate price.

• Offer cannot proceed until disclosure document has been lodged with ASIC.

• Prospectus:

– Most comprehensive disclosure document.

– Contains details of the issue, capital sought, price, use of funds, etc.

9-18

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Offers of Unlisted Securities (cont.)– Non-financial information on issuer — description of

business and reports from directors and/or industry experts.

– Risks associated with business and expensive disclosure documents to prepare.

– Financial information on issuer — most recent and audited financial statements.

– Contributors to prospectus are liable for prosecution by investors over losses resulting from misstatements in, or omissions from, disclosure documents.

• Offer Information Statements (OIS):

– An OIS may be used instead of a prospectus in smaller capital raisings cases. Total raisings must be < $5m.

– OIS is less costly to prepare, less information to disclose.

9-19

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Offers of Listed Securities

• Disclosure requirements for offers of listed securities are less onerous.

• Listed entity is subject to continual disclosure requirements.

• Much of the relevant information is publicly available anyway.

• Market provides a guide on price.

9-20

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Offers that do not Need Disclosure• Various offerings may not require a disclosure

document:

– Small-scale offerings.

– Offers to sophisticated investors.

– Offers to executive officers and associates.

– Offers to existing security holders.

• These exemptions assume that participants have relevant skills or information to judge the merits of an offer.

9-21

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Floating a Public Company• A float is the term given to the company’s first

invitation for the public to subscribe for shares — an initial public offering (IPO).

• For a stock exchange listing, the company needs to satisfy the listing requirements of the exchange.

• A prospectus is required — a legal document that provides details of the company and the terms of the issue of shares.

• Companies unable to meet ASX listing requirements may list on Bendigo or Newcastle Stock Exchanges — aimed at smaller firms.

9-22

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Public vs Private Ownership• A company undertaking a float may be a new

company or an existing private company.

• Two reasons for a private company to float:

– Better access to capital markets.

– Allows private owners to cash in on the success of their business (creates a market for otherwise non-traded shares).

• Costs of going public include loss of control, listing fees, shareholder servicing costs, and information disclosure requirements.

9-23

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Pricing a New Issue• Difficult if there is no historic earnings record.

• Consider P/E ratios of existing companies in the same industry.

• Fixed price offer vs open pricing. Alternative approach is a book build.

• Reveal — investors willingness to pay for new shares.

• Open pricing mechanisms are less likely to generate abnormal returns to investors; constrained open pricing is preferred to attract investors — set a lower and upper bound on issue price.

• Available evidence suggests underpricing of IPOs on average.

9-24

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Underwriting and Managing a New Issue

• Service provided by a stockbroker or investment bank.

• For a fee, the underwriter contracts to purchase all shares for which applications have not been received by the closing date of the issue.

• If book building process is used to issue shares, there is no need for underwriting, but an institution needs to manage the issue.

• Underwriter can limit exposure by sub-underwriting.

9-25

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Selling a New Issue• If a stockbroker is an underwriter or lead

manager, he/she will usually act as selling agent for the issue.

• Promotion reduces the need to purchase underwritten shares and will generate brokerage fees.

• Even without underwriting, a broker is engaged to assist in the distribution of shares.

• Brokerage depends on size of issue, but usually ranges between 1% and 2% of funds raised.

9-26

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Costs of Floating a Company• Costs fall into three main categories:

– ASX listing fees, prospectus costs (legal, accounting, expert opinions and printing and distribution).

– Underwriters’ fees and brokers’ commissions (for 194 floats on ASX during 2007–09, listing costs averaged 5.8% of funds raised).

These costs depend on size of float and whether it is underwritten — depends on market conditions, size and quality of the broker engaged, and underlying business.

– Shares sold in an IPO are usually underpriced — on average, there is an immediate abnormal return to IPOs.

This represents a cost to owners of business — they are selling for less than it is really worth.

9-27

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Costs of Floating a Company (cont.)• Possible reasons for underpricing:

– Winner’s curse — attract investors who have difficulty estimating the future market price of the shares being offered.

– Potential investors will be influenced by the action of other investors and will subscribe to popular IPOs.

– Underpricing provides benefits gain from greater liquidity.– Underpricing leaves a good taste with investors, raising

the price at which subsequent share issues by the company can be sold.

– Empirical finding suggests — greater returns on IPOs reflect investors rational behaviour then these returns should be related to information availability to investors and benefits drive from underpricing.

• Underpricing of IPOs is a phenomenon that is yet to be fully explained.

9-28

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Costs of Floating a Company (cont.)• Long-term performance of IPOs (LTPIPOs):

– Several studies have found that shares of newly listed companies tend to under perform during the first few years after listing.

– Market model — CAPM not ideal to estimate the betas of the securities because pre-listing return data does not exist for IPOs — this makes it difficult to accurately assess LTPIPOs.

– Researchers have used two approaches to tackle LTPIPOs: Compare post-listing returns on IPO companies to one or more

market indices, without risk adjustment. Compare IPOs companies’ return with a control sample of other

listed companies matched on the basis of one or more characteristics such as size and industry.

– In summary, there is mixed empirical evidence of LTPIPOs, and the significance of the ‘new issues puzzle’ still remains controversial.

9-29

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Subsequent Ordinary Share Issues: Rights Issues

• An issue of new shares to existing shareholders in proportion to their current shareholding.

• It requires a prospectus.• Existing shareholders’ right to take up new shares sold

to another party via stock exchange trading renounceable issues.

• Where the right is exercisable only by the existing shareholders, the issue is non-renounceable.

• Subscription price — must pay price to obtain new shares.

• Ex-rights date — the date on which a share begins trading ex-rights.

• Cum-rights — when shares are traded cum-rights, the buyer is entitled to participate in the forthcoming rights issue.

9-30

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Valuation of Rights• The ex-rights price should fall by the value of the right

attached to each share. The theoretical value of a right (R) is given by:

• The theoretical value of a share ex-rights (X) is given by:

• Theoretically, a rights issue has no value to shareholders.

• However, the announcement can have an impact on shareholders’ wealth — information content, rights issues are usually bad news, with information about expected future cash flows.

( )1

N M SR

N

−=

+

1

NM SX

N

+=

+

9-31

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Private Issues (Placements)• Directly place equity — without the need of disclosure

document.

• Placements can be underwritten and they can be a very inexpensive way of accessing equity.

• Book build is a popular mechanism for private placement.

• Advantages:

– Can be quickly arranged and finalised, lower issue costs than a rights issue, and board can direct the placement.

• Disadvantages:

– Dilution of proportion of the ownership of the company for non-participating investors.

– Placements at a discount to market will reduce the value of existing shareholders’ investments, contrary to premium at market.

9-32

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Contributing Shares and Instalment Receipts• Shares on which only part of the issue price has been paid.

• The issuing company can call up the unpaid part (reserve capital) of the issue price in one or more instalments.

• Instalment receipts are issued when existing fully paid shares are offered to the public, with the sale price to be paid in two instalments.

• The instalment receipts differ from partly issued shares due to the following factors:

– Timing of instalment is specified at the time of original sale.

– Instalments are payable to the vendor of the shares.

– Holders of instalment receipts are entitled to the same dividends as holders of fully paid shares.

9-33

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Share Purchase Plans

• ASX-listed companies can raise limited funds from existing shareholders through share purchase plans.

• Prospectus not required as long as they comply with ASIC Policy Statement 125.

• Limit of $5000 from each shareholder p.a.

• Attractive because shares are issued at a discount to market price, and there are no brokerage fees.

9-34

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Share Options• Share options give the holder the right, but not the

obligation, to purchase an ordinary share at a stated price at a future date.

• Exercise of the option will depend on the exercise price relative to the market price of the share around the exercise date.

• Company options may be issued free with the underlying share or sold at a price set by the issuing company:

– To employees.

– As a sweetener to an equity issue.

– As a sweetener to a private debt issue.

• Company options often restrict the holder from exercising the option for a certain period after it has been granted.

9-35

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Choosing between Equity-Raising Methods• Several external sources of equity have been considered.

• Most involve long-term arrangements; for a significant one-off equity raising, only rights issues and placements are practical.

• Companies generally prefer placements to rights issues — bias for placements up to regulatory limits.

• Advantages of placements include speed (days rather than weeks) and lower transaction costs; also shares can be placed with ‘friendly’ shareholders.

• Rights issues are seen as equitable to existing shareholders.

9-36

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Choosing between Equity-Raising Methods (cont.)• Combination issues:

– When amount of funds is sought to be above the ceiling, company could make a placement in combination with other equity raising; for example, share purchase plan or non-renounceable rights issue.

• Different features of combination issues:

– Issue price is determined by book build, which is then used to determine share prices for the second component of the issue. (See p. 262, Macquarie Bank example)

– Three offers of shares: a placement, an institutional entitlement offer, and a retail entitlement offer. (See p. 263, Alesco Corporation example)

9-37

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Employee Share Plans• Companies raise significant funds through

employee share plans.

• Primary purpose of such plans is to motivate senior managers and other employees by giving them an ownership interest in the company.

• Types of employee share plans:– Fully paid share plans.

– Partly paid share plans.

– Option plans.

– Employee share trusts.

– Replicator plans.

9-38

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Internal Equity Financing

• Internal equity financing refers to the positive net cash flows generated by a company — funds from operations.

• Management can influence the level of retained profits by the dividend policy.

Total Internal Equity Finance = operating profit before tax

+ depreciation charge

- income tax - dividend payments

9-39

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Depreciation Charges• The above equation might give the impression

that depreciation is a source of finance.

• Depreciation reduces profits and, therefore, the funds available for distribution as dividends.

• A profitable company will end up retaining funds at least equivalent to depreciation charges.

9-40

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Dividend Reinvestment Plans• Allows shareholders the choice of reinvesting their

dividends in the company (by purchasing additional shares).

• Advantages– Avoids relatively high transaction costs if shareholders used

dividends to acquire additional shares.

– Shares often issued at a discount to current market price.

– If companies achieve a sufficient reinvestment rate, it enables them to pay franked dividends, which transfer tax credits to shareholders and retain cash to fund investments.

• Disadvantages– Reinvestment of dividends could be dysfunctional if

company has few prospects for future profitable investments, and/or if cash position is quite healthy.

– By increasing the company’s equity base, a DRP dilutes key indicators such as EPS.

9-41

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Managing a Company’s Equity Structure: Bonus Issues• ‘Free’ issue of shares made to existing shareholders in

proportion to their current investment.• Equivalent to a rights issue with a subscription price of

zero.• Should have no effect on shareholders’ wealth, but there

may be an announcement effect due to the information conveyed.

• A bonus issue may be made:– To provide the market with information.– To maintain total dividend payout with management reducing the

dividend per share.– If a company’s shares are thinly traded.

• Bonus issues are treated as dividends for taxation purposes unless made from the share premium reserve (identified for tax purposes).

9-42

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Share Splits• Made by companies with a ‘thin’ market for their shares.

• Existing shares are replaced by new shares issued at a ratio of greater than 1 for 1. Large Australian companies that have made recent share splits include Computershare, Patrick Corporation and Toll Holdings.

• Justified as a means to increase liquidity and affordability of shares to retail investors. Theoretically, a share split should have no effect on share price or volume.

• Empirical evidence on benefits is mixed:– Number of shareholders and transactions both rise

after share splits but little evidence of volume increases.– Splits increase bid-ask spreads and return volatility, signs

of lower liquidity.

9-43

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Share Consolidations• A share consolidation or reverse split

decreases the number of shares on issue and increases the price per share.

• Reasons for share consolidations:

– Raise share price to a popular trading range and overcome perceptions that the company is not respectable because of its low share price.

– Reduce transaction costs and lower the cost of maintaining the company’s share registry.

9-44

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

Summary• New ventures can seek finance from wealthy

individuals and private equity funds.

• New share issues must satisfy disclosure requirements — usually with a prospectus.

• Ordinary shares have a residual claim on a company — lowers financial risk.

• Benefits of equity finance — company is not required to pay dividends or redeem shares, also lowers cost of debt finance.

9-45

Copyright 2009 McGraw-Hill Australia Pty Ltd PPTs t/a Business Finance 10e by PeirsonSlides prepared by Farida Akhtar and Barry Oliver, Australian National University

• Initial public offering of shares is referred to as floating a company. The long-term performance of IPOs still remains controversial.

• Book build is an increasingly popular means of issuing new securities.

• Existing public companies can raise funds through the use of rights issues, private placements, contributing and preference shares, and share options.

• Internal equity — retained earnings is a low-cost and popular source of finance.

Summary (cont.)