8th asean+3 bond market forum (abmf) meeting

TRANSCRIPT

8th ASEAN+3 Bond Market Forum (ABMF) Meeting Makati ShangriLa Hotel, Metro Manila, Philippines,

17 18 April 2012

1 of 2

DATE & TIME PROGRAM

17 Apr 2012 DAY 1: ABMF Sub Forum 1 (SF1)

08:30 – 09:00 Registration

ABMF SF 1

09:00 – 09:10 Welcome Remarks by Commissioner Ma. Juanita E. Cueto, Securities and Exchange Commission, Philippines

09:10 – 09:20 Opening Remarks by SF1 Chair (Mr. Tetsutaro Muraki, Tokyo-AIM)

09:20 – 10:20

Session 1: Developing common bond issuance program (Part 1) - Presentations by Prof. Shigehito Inukai, ADB consultant, and others on the

issues and approaches - Comments on Research and Discussion Issues by KOFIA

10:20 – 10:40 Coffee break

10:40 – 12:00 Session 2: Developing common bond issuance program (Part 2) - Q and A

12:00– 13:30 Lunch Break (hosted by BAP, Makati A-B)

13:30 – 15:00

Session 3: (Information session) : Mapping National Scale Ratings Across Sovereigns in Asia - Presentation by Mr. Faheem Ahmad, ACRAA - Q and A

15:00 – 16:00

Session 4: (Information session) : European Experience on developing cross-border bond transactions’ post-trade harmonisation - Presentation by Boon-Hiong Chan, Deutsche Bank - Q and A

16:00 – 16:20 Coffee break

16:20 – 17:20

Session 5: (Information session) : Information on Other Issues - Case Study on TPBM: ING N.V by Mr. Kazuhiro Iida, Tokyo AIM, Inc. - Current Issuance Window in the Japanese Bond Market by Ms. Reiko

Nobuhiro, Nomura Securities, Co., Ltd. - Q and A

17:20 – 17:50

Session 6: Other issues of SF1 - Updates and management of phase 1 reports (Mr. Seung Jae Lee) - Dissemination of the phase 1 reports (Mr. Matthias Schmidt) - Q and A

17:50 – 18:00 Wrap up by ADB Secretariat (Mr. Seung Jae Lee, ADB Secretariat)

18:00 – 18:10 Closing Remarks by SF1 Chair (Mr. Tetsutaro Muraki, Tokyo-AIM)

18:30 – 20:30 Cocktail dinner hosted by PDS Group (Banquet Hall & Mabini, Milkyway Restaurant)

8th ASEAN+3 Bond Market Forum (ABMF) Meeting Makati ShangriLa Hotel, Metro Manila, Philippines,

17 18 April 2012

2 of 2

DATE & TIME PROGRAM

18 Apr 2012 DAY 2: ABMF Sub Forum2 (SF2)

08:30 – 09:00 Registration

ABMF SF2

09:00 – 09:10 Welcoming Remarks by Mr. Noritaka Akamatsu, Deputy Head of OREI, ADB

09:10 – 09:20 Opening Remarks by SF2 Chair (Mr. Jong Hyung Lee, KSD)

09:20 – 10:40

Session 7: Focus of Phase 2 activities (Part 1) - Presentation by Dr. Taiji Inui, ADB consultant - Others on the issues and approaches (Mr. Shinji Kawai, ADB secretariat) - Philippine transaction flow by Mr. Antonino A. Nakpil, PDS Group

10:40 – 11:00 Coffee break

11:00 – 12:00 Session 8: Focus of phase 2 activities (Part 2) - Q and A

12:00 – 13:30 Lunch Break (hosted by ADB, Manila A-B)

13:30 – 14:30

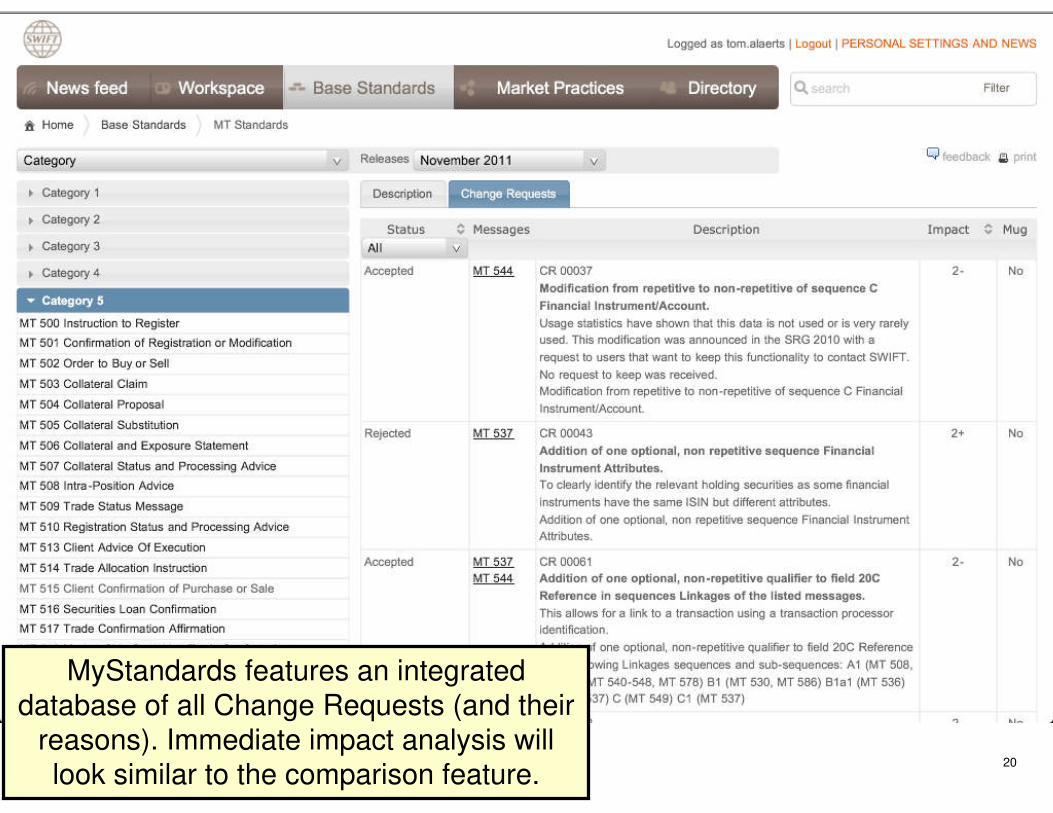

Session 9: (Information session) : Database for managing standards and market practice - Presentation by Alexandre Kech, SWIFT - Q and A

14:30 – 15:30

Session 10: (Information session) : Information on other issues - Recent progress in LEI discussion by Mr. Taketoshi Mori, The Bank of

Tokyo Mitsubishi UFJ Ltd. - Supplementary information on LEI by Ms. Rebecca Turner, Asia Securities

Industry & Financial Markets Association (ASIFMA) - Q and A

15:30 – 15:50 Coffee break

15:50 – 16:20

Session 11: Other issues of SF2 - Updates of phase 1 reports (Mr. Seung Jae Lee, ADB Secretariat) - Dissemination of the phase 1 reports (Mr. Matthias Schmidt) - Q and A

Wrap up session

16:20 – 16:50 Future work plan and Wrap up (Mr. Seung Jae Lee, ADB Secretariat) - Q&A

16:60 – 17:00 Closing remarks by SF2 Chair (Mr. Jong Hyung Lee, KSD)

17:30 – 20:30 Dinner hosted by Bureau of the Treasury (Plaza Moriones, Fort Santiago,Intramuros)

18th April 2012, Manila, Philippines

8th ABMF SF2 - Phase2 Questionnaire

Attachments

Taiji Inui

NTT DATA Corporation

ADB Consultant - Financial Information Technology Specialist

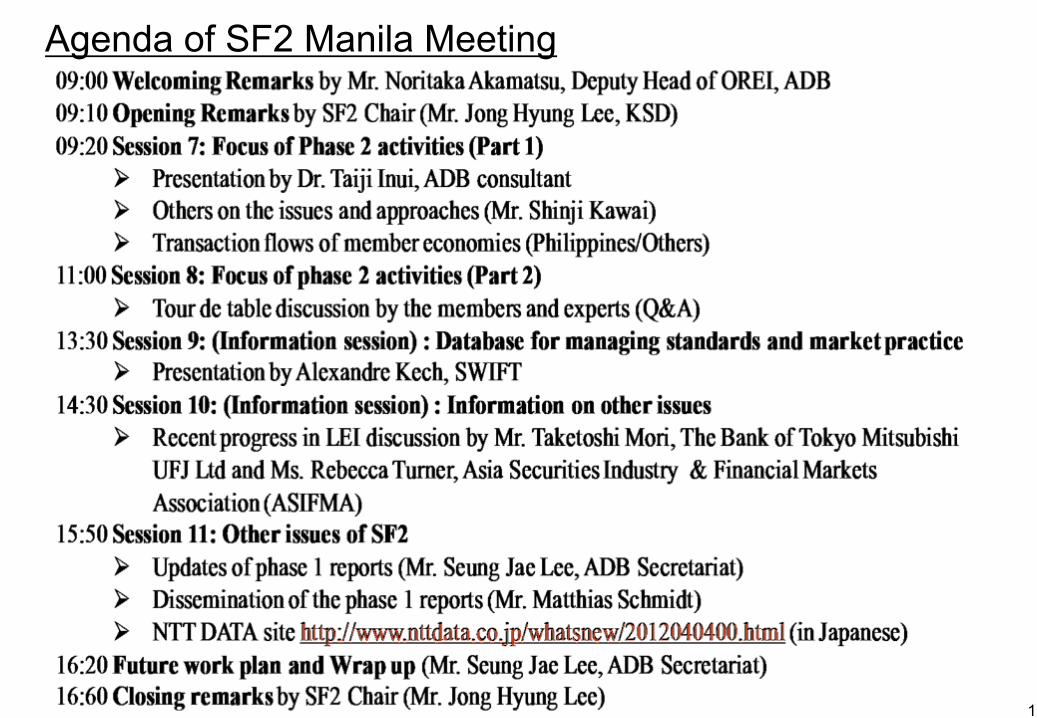

Agenda of SF2 Manila Meeting

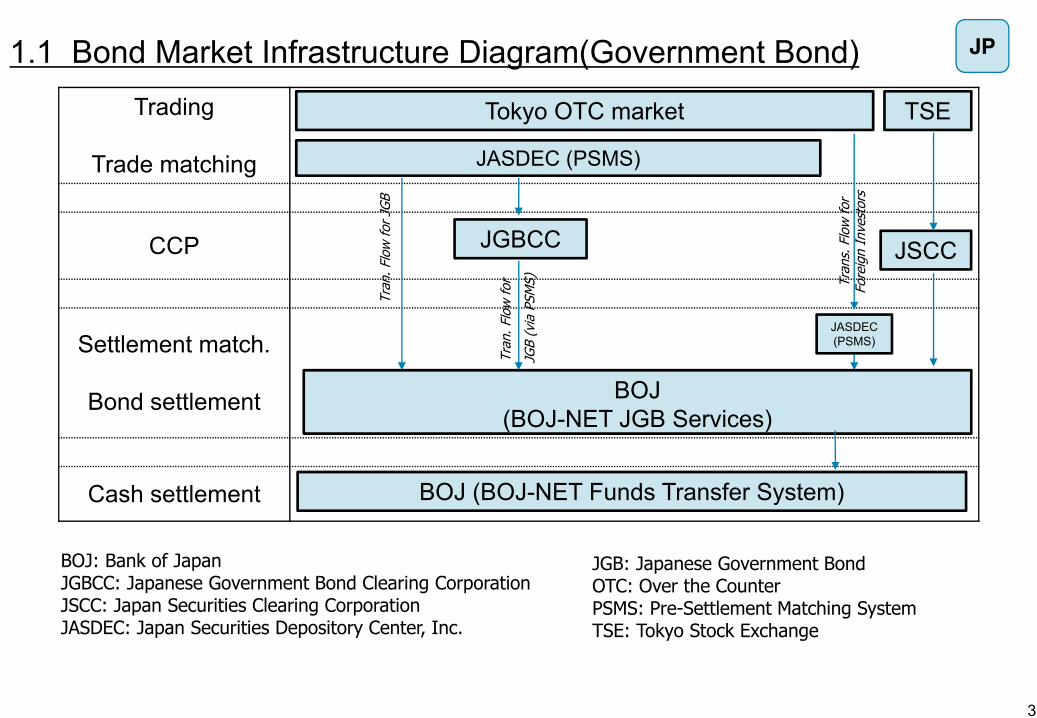

1

2

3

Trading

Trade matching

CCP

Settlement match.

Bond settlement

Cash settlement

JASDEC (PSMS)

JGBCC

BOJ

(BOJ-NET JGB Services)

BOJ (BOJ-NET Funds Transfer System)

BOJ: Bank of JapanJGBCC: Japanese Government Bond Clearing CorporationJSCC: Japan Securities Clearing CorporationJASDEC: Japan Securities Depository Center, Inc.

1.1 Bond Market Infrastructure Diagram(Government Bond)

TSE

JSCC

Tokyo OTC market

JASDEC

(PSMS)

Tra

n. Flo

w for

JGB

Tra

n. Flo

w for

JGB (

via P

SM

S)

Tra

ns.

Flo

w for

Fore

ign I

nve

stors

JGB: Japanese Government BondOTC: Over the CounterPSMS: Pre-Settlement Matching SystemTSE: Tokyo Stock Exchange

JP

4

Trading

Trade matching

CCP

Settlement match.

Bond settlement

Cash settlement

JASDEC (PSMS)

JASDEC

(Book-Entry Transfer System)

BOJ (BOJ-NET Funds Transfer System)

BOJ: Bank of JapanJASDEC: Japan Securities Depository Center, Inc.

1.2 Bond Market Infrastructure Diagram(Corporate Bond)

Note1: Non fixed income bonds such as convertible bonds are not included here.

Tokyo OTC market

JASDEC (PSMS)

Tra

ns.

Flo

w for

Fore

ign I

nve

stors

Tra

n. Flo

w for

Corp

ora

te B

ond

OTC: Over the CounterPSMS: Pre-Settlement Matching System

JP

JASDEC

(PSMS)

(Book Entry Transfer System)

Sell Side Buy Side1. Trade

2. Trade Report

4. Notice of Matching

Status

4. Notice of Matching

Status

2. Trade Report

14.Bond Settlement

13.Settlement Report

(Cash) 13. Settlement Report

(Cash)

15. Settlement Report

(Bond)

BOJ(BOJ NET)

12.Cash Settlement

8. Holding Bonds

9.Fund Settlement Data

for DVP

12. Notice of Receipt

Completion (Cash)

3. Trade Matching

6. Settlement Matching

10. Payment Request

(Cash)

11. Payment Instruction

(Cash)

7. Notice of Matching

Status

7. Notice of Matching

Status

15. Settlement Report

(Bond)

5

5. Standing Settlement

Instruction

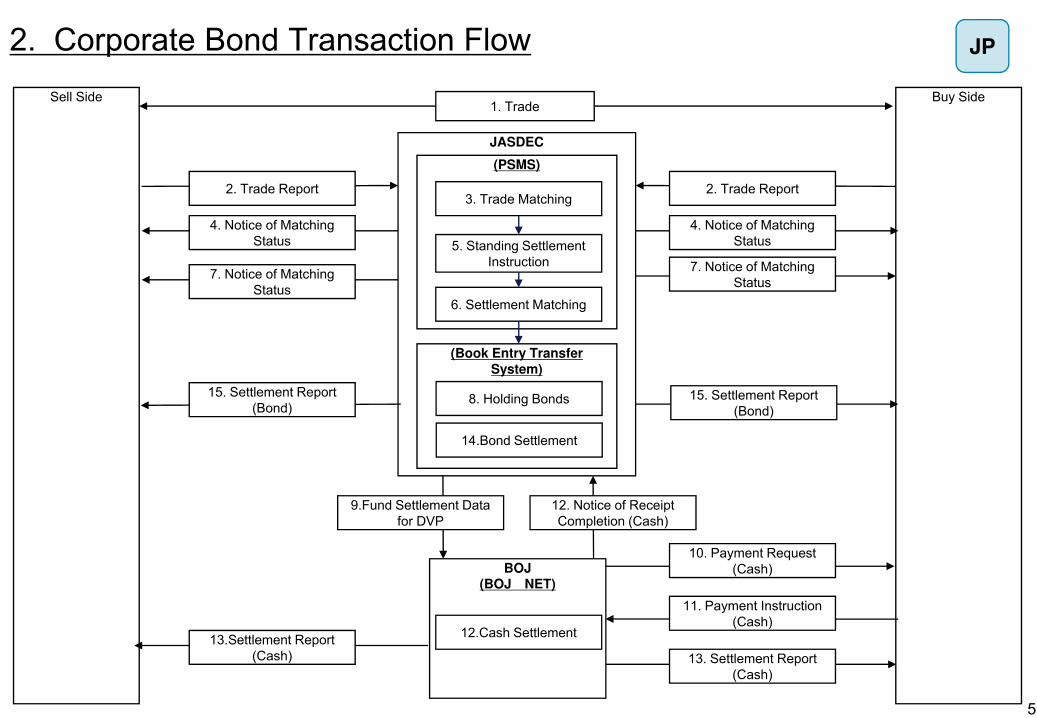

2. Corporate Bond Transaction Flow JP

1. The sell side and buy side trade corporate bond over-the-counter.

2. Both sell side and buy side send Trade Report data into PSMS (Pre-Settlement Matching System).

3. PSMS performs trade matching.

4. PSMS sends the Notice of Matching Status to both sides of trade.

5. PSMS produces Standing Settlement Instruction.

6. PSMS performs settlement matching and sends the data to Book Entry Transfer System.

7. PSMS sends Notice of Matching Status to sell side and buy side.

8. Book Entry Transfer System holds bonds..

9. Book Entry Transfer System sends Funds Settlement Data for DVP to BOJ-NET.

10. BOJ-NET sends Payment Request (Cash) to buy side.

11. Buy side sends Payment Instruction (Cash) to BOJ-NET.

12. BOJ-NET performs Cash Settlement and sends Notice of Receipt Completion (Cash) to Book Entry Transfer

System.

13. BOJ-NET sends Settlement Report (Cash) to sell side and buy side.

14. Book Entry Transfer System performs bond settlement.

15. Book Entry Transfer System sends Settlement Report (Bond) to sell side and buy side.

2. Description of Corporate Bond Transaction Flow

6

JP

Sample Answer, Japan

3.1.1 Interest Payment of Government bond

3.2.1 Interest Payment of Corporate bond

3.3.1 Redemption Payment with final interest payment of

Government bond

3.4.1 Redemption Payment with final interest payment of

Corporate bond

7

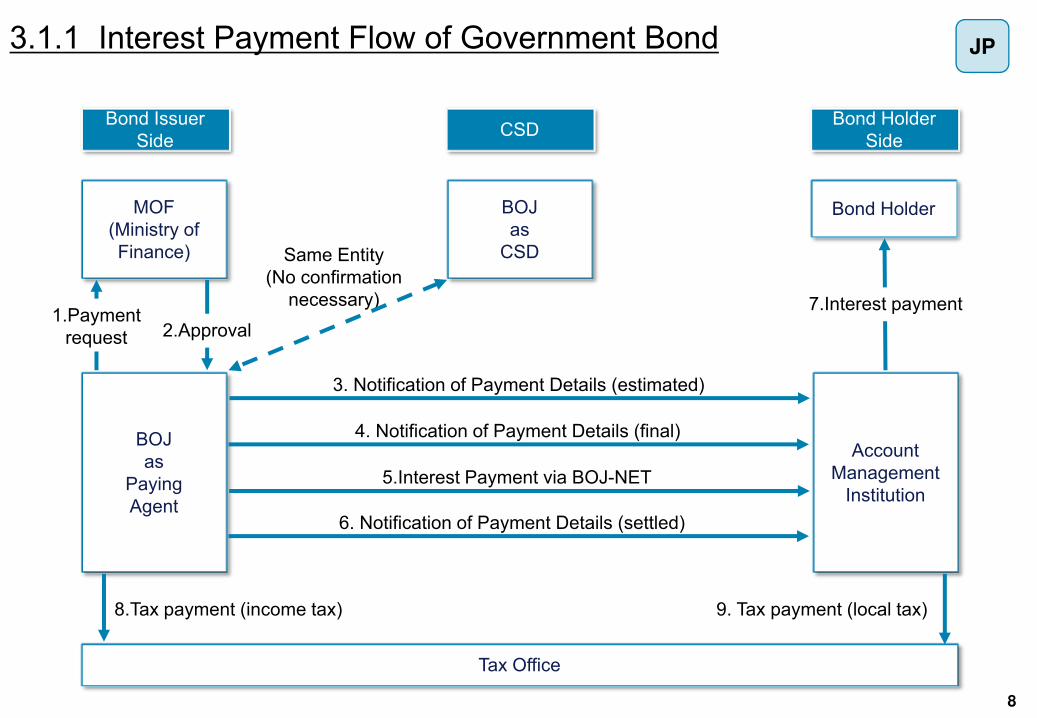

3.1.1 Interest Payment Flow of Government Bond

Bond Issuer

SideCSD

Bond Holder

Side

MOF

(Ministry of

Finance)

Account

Management

Institution

Tax Office

9. Tax payment (local tax)

BOJ

as

CSD

Bond Holder

7.Interest payment

8

BOJ

as

Paying

Agent

1.Payment

request 2.Approval

5.Interest Payment via BOJ-NET

8.Tax payment (income tax)

6. Notification of Payment Details (settled)

Same Entity

(No confirmation

necessary)

3. Notification of Payment Details (estimated)

4. Notification of Payment Details (final)

JP

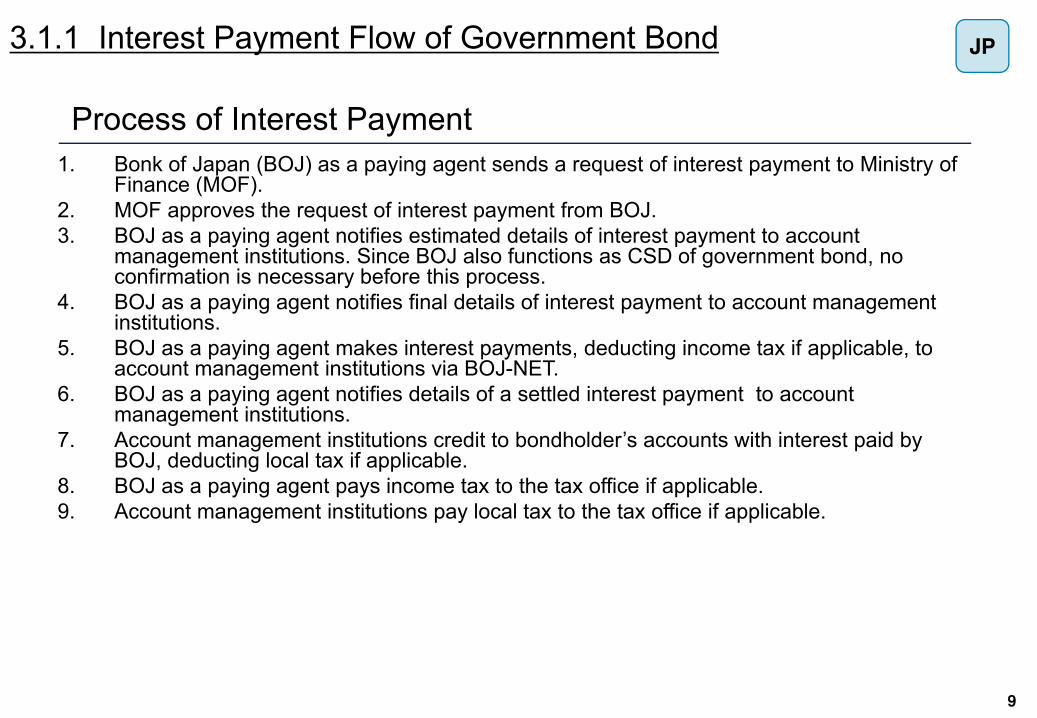

1. Bonk of Japan (BOJ) as a paying agent sends a request of interest payment to Ministry of Finance (MOF).

2. MOF approves the request of interest payment from BOJ.

3. BOJ as a paying agent notifies estimated details of interest payment to account management institutions. Since BOJ also functions as CSD of government bond, no confirmation is necessary before this process.

4. BOJ as a paying agent notifies final details of interest payment to account management institutions.

5. BOJ as a paying agent makes interest payments, deducting income tax if applicable, to account management institutions via BOJ-NET.

6. BOJ as a paying agent notifies details of a settled interest payment to account management institutions.

7. Account management institutions credit to bondholder’s accounts with interest paid by BOJ, deducting local tax if applicable.

8. BOJ as a paying agent pays income tax to the tax office if applicable.

9. Account management institutions pay local tax to the tax office if applicable.

Process of Interest Payment

9

3.1.1 Interest Payment Flow of Government Bond JP

3.2.1 Interest Payment Flow of Corporate Bond

Bond Issuer Side CSD Bond Holder Side

Bond Issuer Bond Holder

JASDEC

Tax Office

1.Payment

request

2.Fund

payment

3.Bondholder’s

tax status data

3.Bondholder’s tax

status data

4.Payment

request

5.Approval

6.Interest Payment (via BOJ Net)

7.Interest payment

8.Tax payment (income tax) 9.Tax payment (local tax)

Paying

Agent

Account

Management

Institution

10

JP

1. A paying agent sends a payment request of interest to a bond issuer.

2. A bond issuer makes fund payment to a paying agent.

3. Account management institutions of bond holders send the tax status data of bondholders to JASDEC.

4. JASDEC sends a payment request of interest to a paying agent.

5. A paying agent approves the request from JASDEC.

6. A paying agent makes interest payments, deducting income tax if applicable, to account management institutions via BOJ-NET.

7. Account management institutions credit to bondholder’s accounts with interest paid by a paying agent, deducting local tax if applicable.

8. A paying agent pays income tax to the tax office if applicable.

9. Account management institutions pay local tax to the tax office if applicable.

Process of Interest Payment

3.2.1 Interest Payment Flow of Corporate Bond

11

JP

3.3.1 Redemption Payment Flow with final Interest Payment of Government Bond

Bond Issuer

SideCSD

Bond Holder

Side

MOF

(Ministry of

Finance)

Account

Management

Institution

Tax Office

9. Tax payment (local tax)

BOJ

as

CSD

Bond Holder

3. Notification of Payment Details (estimated)

7.Redemption

payment

BOJ

as

Paying

Agent

1.Payment

request 2.Approval

5a.Redemption Payment via BOJ-NET(DVP)

8.Tax payment (income tax)

6. Notification of Payment Details (settled)

Same Entity

(No confirmation

necessary)

12

5b.Redemption

(DVP)

4. Notification of Payment Details (final)

JP

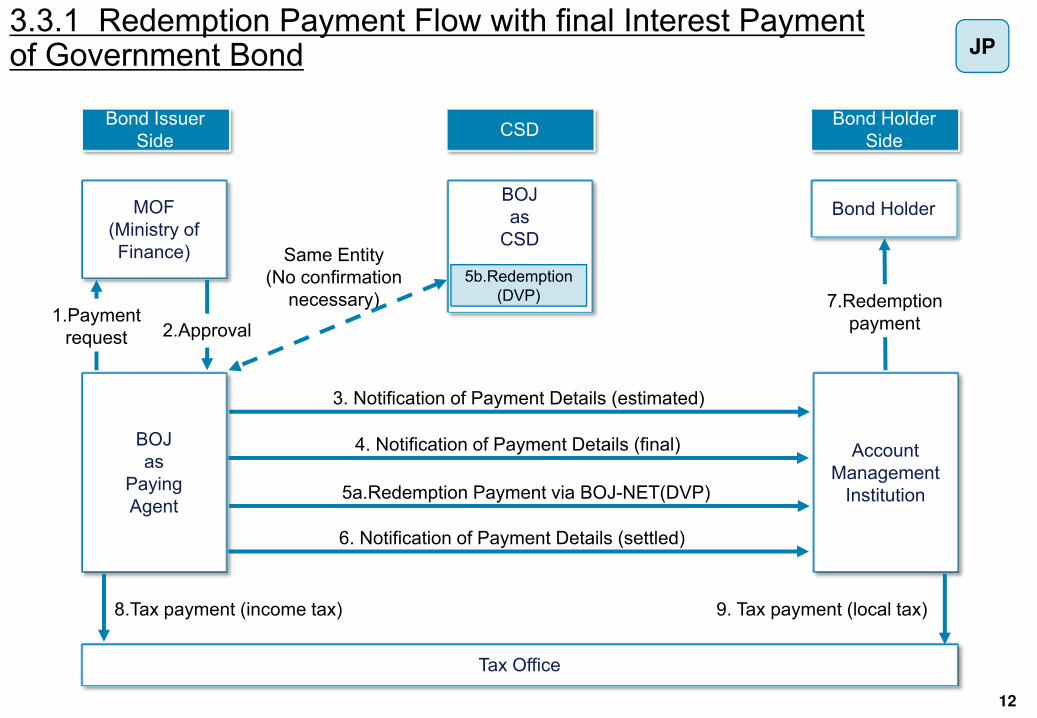

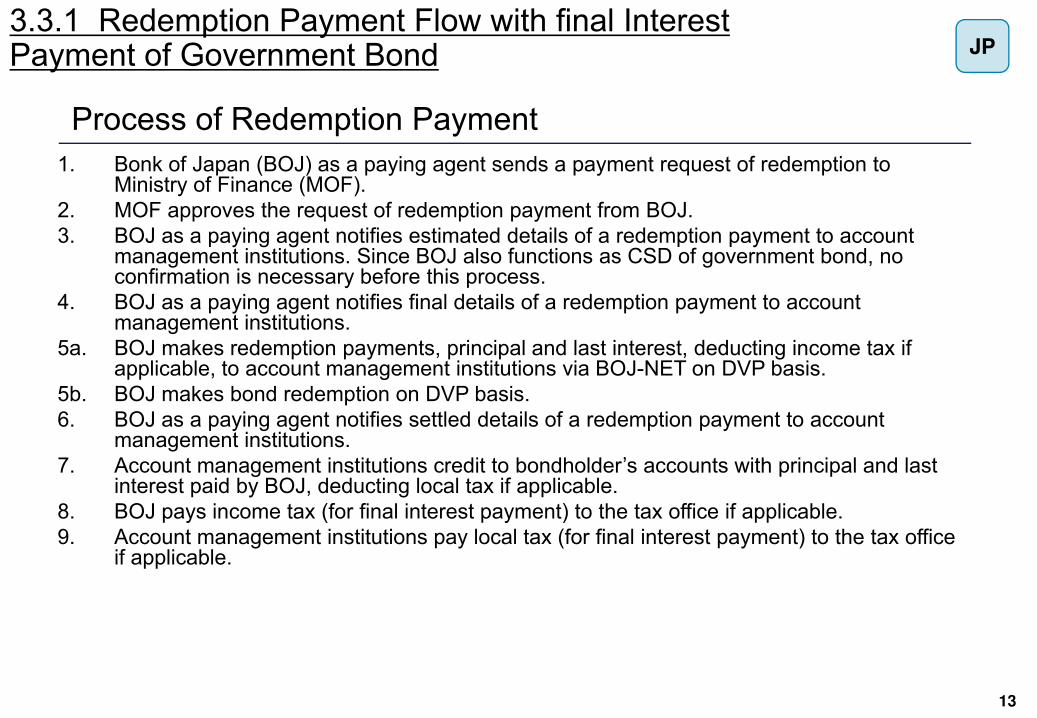

1. Bonk of Japan (BOJ) as a paying agent sends a payment request of redemption to Ministry of Finance (MOF).

2. MOF approves the request of redemption payment from BOJ.

3. BOJ as a paying agent notifies estimated details of a redemption payment to account management institutions. Since BOJ also functions as CSD of government bond, no confirmation is necessary before this process.

4. BOJ as a paying agent notifies final details of a redemption payment to account management institutions.

5a. BOJ makes redemption payments, principal and last interest, deducting income tax if applicable, to account management institutions via BOJ-NET on DVP basis.

5b. BOJ makes bond redemption on DVP basis.

6. BOJ as a paying agent notifies settled details of a redemption payment to account management institutions.

7. Account management institutions credit to bondholder’s accounts with principal and last interest paid by BOJ, deducting local tax if applicable.

8. BOJ pays income tax (for final interest payment) to the tax office if applicable.

9. Account management institutions pay local tax (for final interest payment) to the tax office if applicable.

Process of Redemption Payment

13

3.3.1 Redemption Payment Flow with final Interest Payment of Government Bond JP

3.4.1 Redemption Payment Flow with final Interest Payment of Corporate Bond

Bond Issuer Side CSD Bond Holder Side

Bond Issuer Bond Holder

Tax Office

1.Payment

request

2.Fund

payment

3.Bondholder’s

tax status data

3.Bondholder’s tax

status data

4.Payment

request

5.Approval

6a.Redemption Payment via BOJ-Net (DVP)

9.Redemption

payment

10.Tax payment (income tax) 11.Tax payment (local tax)

Account

Management

Institution

7.Redemption notice

6b.Redemption(DVP)

JASDEC

8.Delete bond registration

Paying Agent

14

JP

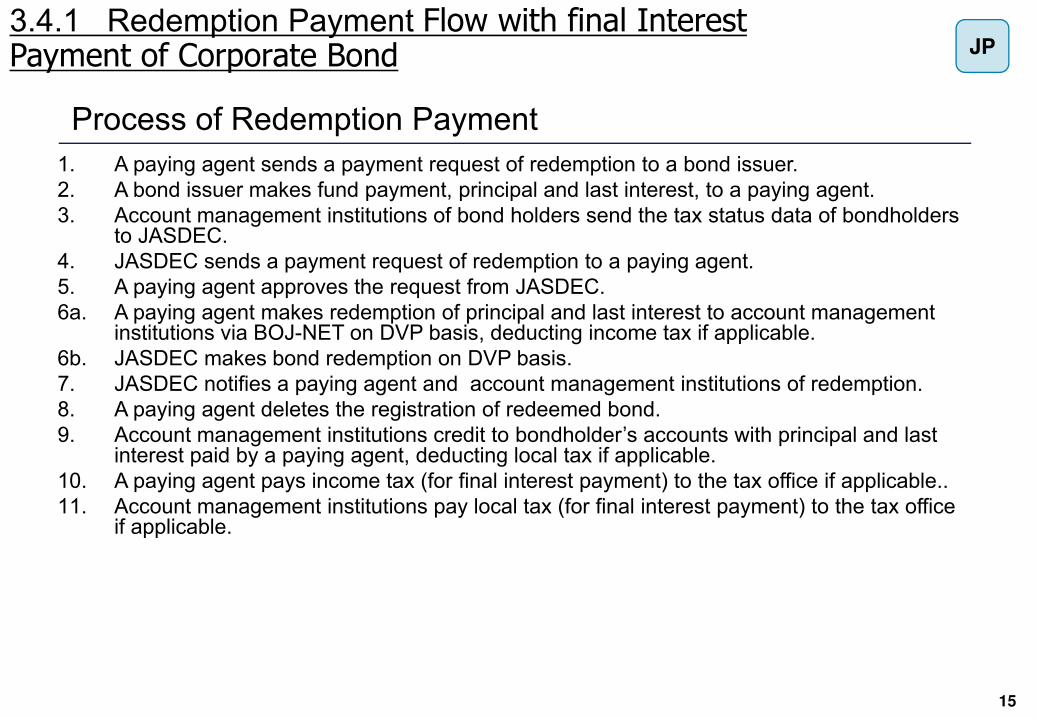

1. A paying agent sends a payment request of redemption to a bond issuer.

2. A bond issuer makes fund payment, principal and last interest, to a paying agent.

3. Account management institutions of bond holders send the tax status data of bondholders to JASDEC.

4. JASDEC sends a payment request of redemption to a paying agent.

5. A paying agent approves the request from JASDEC.

6a. A paying agent makes redemption of principal and last interest to account management institutions via BOJ-NET on DVP basis, deducting income tax if applicable.

6b. JASDEC makes bond redemption on DVP basis.

7. JASDEC notifies a paying agent and account management institutions of redemption.

8. A paying agent deletes the registration of redeemed bond.

9. Account management institutions credit to bondholder’s accounts with principal and last interest paid by a paying agent, deducting local tax if applicable.

10. A paying agent pays income tax (for final interest payment) to the tax office if applicable..

11. Account management institutions pay local tax (for final interest payment) to the tax office if applicable.

Process of Redemption Payment

15

3.4.1 Redemption Payment Flow with final Interest Payment of Corporate Bond JP

Sample Answer, Indonesia

3.2.1 Interest Payment of Corporate bond

3.4.1 Redemption Payment of Corporate bond

16

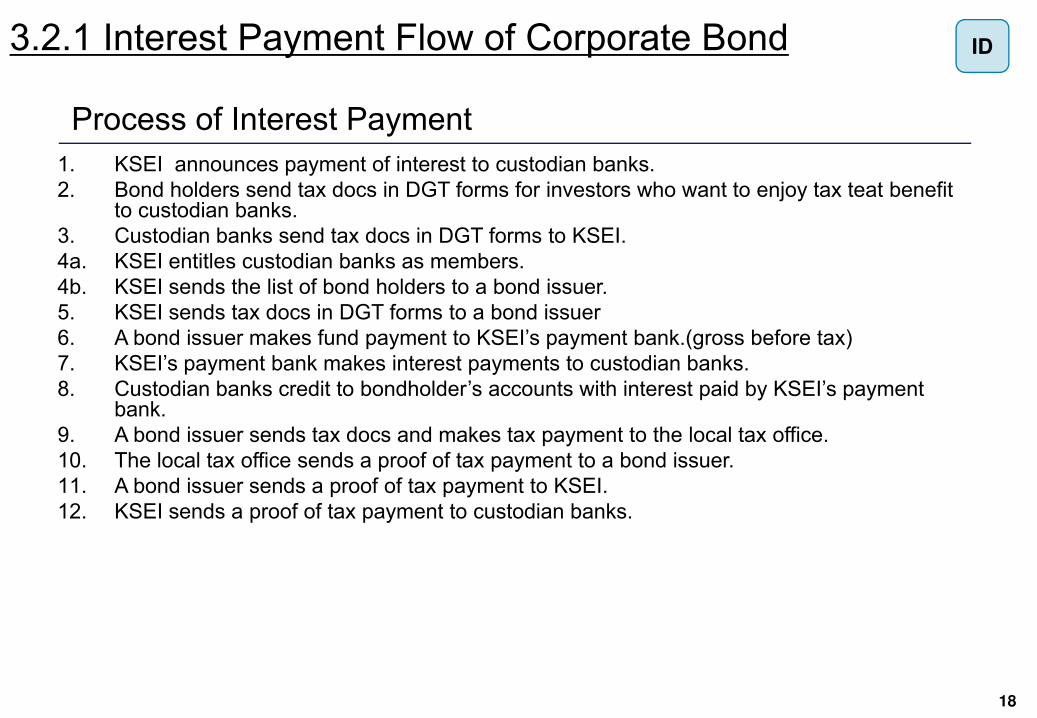

3.2.1 Interest Payment Flow of Corporate Bond

Bond Issuer Side CSD Bond Holder Side

Bond Holder

Tax Office

3.DGT Forms*2. Tax docs*

(DGT Forms)

8.Interest

payment

9.Tax docs

& tax payment

KSEI’s Payment

Bank

Custodian

Bank

1.Announcement

4b.List of bondholders

7.Interest

Payment

(net of tax)10.Proof of tax

payment

6.Fund payment

(gross before tax)

12.Proof of tax payment

*only if the foreign investors would like to enjoy the tax treaty benefits

4a. Member

Entitlement

5. DGT FormsBond Issuer

KSEI

11.Proof of

Tax Payment

17

ID

1. KSEI announces payment of interest to custodian banks.

2. Bond holders send tax docs in DGT forms for investors who want to enjoy tax teat benefit to custodian banks.

3. Custodian banks send tax docs in DGT forms to KSEI.

4a. KSEI entitles custodian banks as members.

4b. KSEI sends the list of bond holders to a bond issuer.

5. KSEI sends tax docs in DGT forms to a bond issuer

6. A bond issuer makes fund payment to KSEI’s payment bank.(gross before tax)

7. KSEI’s payment bank makes interest payments to custodian banks.

8. Custodian banks credit to bondholder’s accounts with interest paid by KSEI’s payment bank.

9. A bond issuer sends tax docs and makes tax payment to the local tax office.

10. The local tax office sends a proof of tax payment to a bond issuer.

11. A bond issuer sends a proof of tax payment to KSEI.

12. KSEI sends a proof of tax payment to custodian banks.

Process of Interest Payment

3.2.1 Interest Payment Flow of Corporate Bond

18

ID

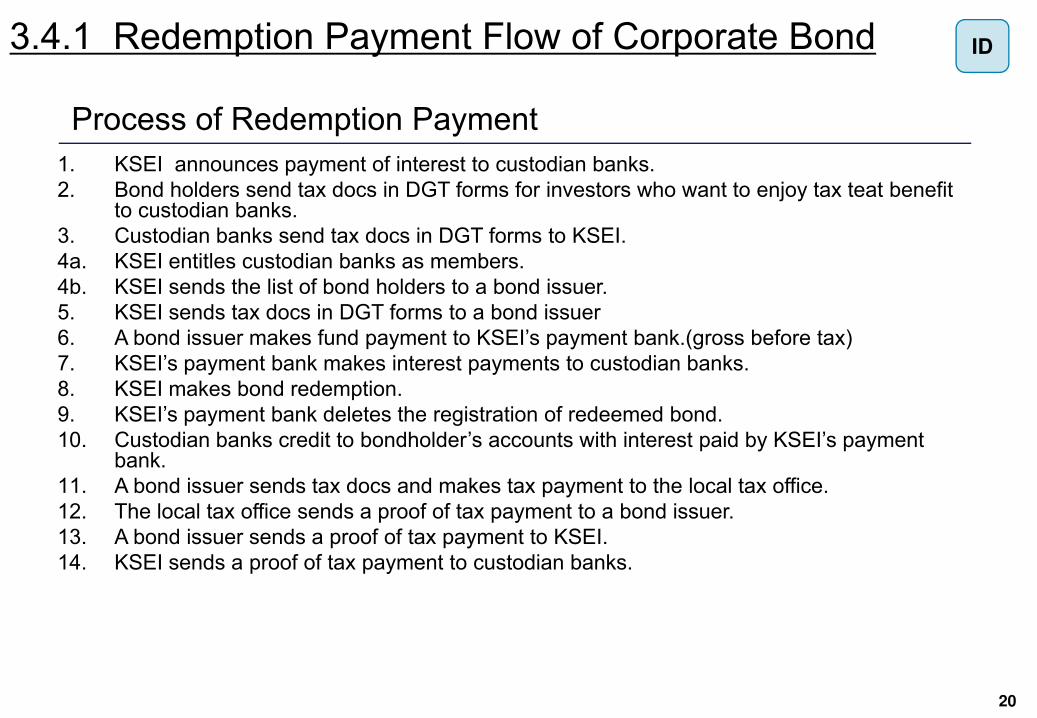

3.4.1 Redemption Payment Flow of Corporate Bond

Bond Issuer Side CSD Bond Holder Side

Bond Issuer Bond Holder

Tax Office

3.DGT Forms*2. Tax docs*

(DGT Forms)

10.Interest

payment

11.Tax docs

& tax payment

Custodian

Bank

1.Announcement

4b.List of bondholders

7.Interest

Payment

(net of tax)12.Proof of tax

payment

11.Proof of

Tax Payment

6.Fund payment

(gross before tax)

13.Proof of tax payment

*only if the foreign investors would like to enjoy the tax treaty benefits

4a. Member

Entitlement

5. DGT Forms

8. Redemption

9.Delete bond registration

KSEI

KSEI’s Payment Bank

19

ID

1. KSEI announces payment of interest to custodian banks.

2. Bond holders send tax docs in DGT forms for investors who want to enjoy tax teat benefit to custodian banks.

3. Custodian banks send tax docs in DGT forms to KSEI.

4a. KSEI entitles custodian banks as members.

4b. KSEI sends the list of bond holders to a bond issuer.

5. KSEI sends tax docs in DGT forms to a bond issuer

6. A bond issuer makes fund payment to KSEI’s payment bank.(gross before tax)

7. KSEI’s payment bank makes interest payments to custodian banks.

8. KSEI makes bond redemption.

9. KSEI’s payment bank deletes the registration of redeemed bond.

10. Custodian banks credit to bondholder’s accounts with interest paid by KSEI’s payment bank.

11. A bond issuer sends tax docs and makes tax payment to the local tax office.

12. The local tax office sends a proof of tax payment to a bond issuer.

13. A bond issuer sends a proof of tax payment to KSEI.

14. KSEI sends a proof of tax payment to custodian banks.

Process of Redemption Payment

3.4.1 Redemption Payment Flow of Corporate Bond

20

ID

Sample Answer, Korea

3.2.1 Interest Payment of Corporate bond

3.4.1 Redemption Payment of Corporate bond

21

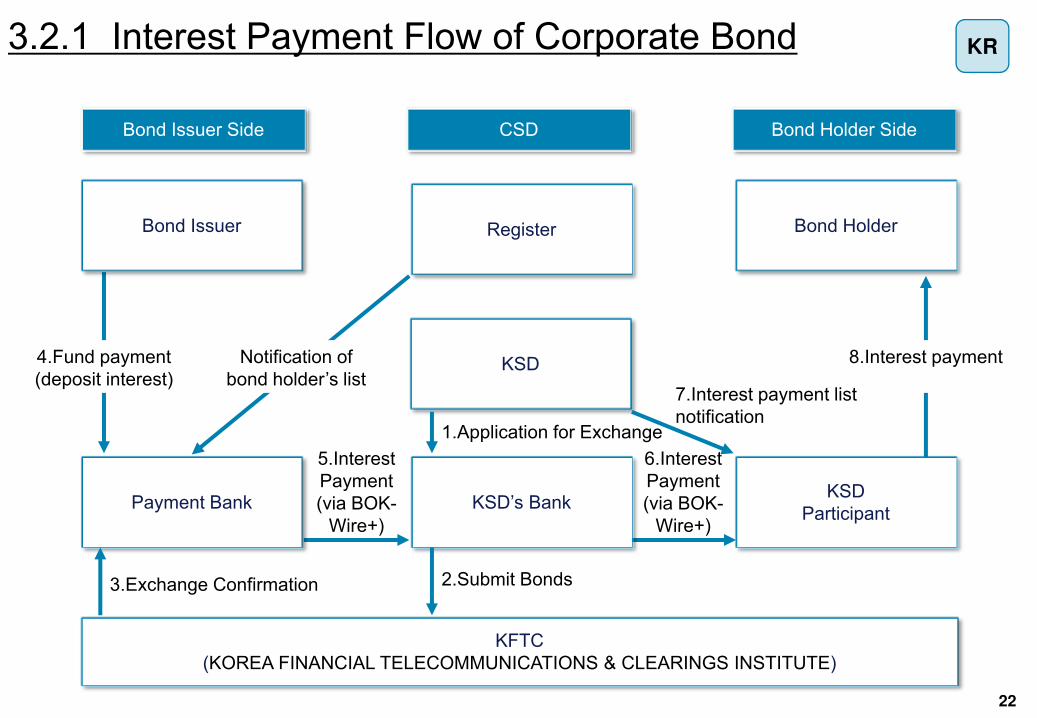

3.2.1 Interest Payment Flow of Corporate Bond

Bond Issuer Side CSD Bond Holder Side

Bond Holder

KSD

KFTC

(KOREA FINANCIAL TELECOMMUNICATIONS & CLEARINGS INSTITUTE)

4.Fund payment

(deposit interest)

8.Interest payment

Payment BankKSD

Participant

5.Interest

Payment

(via BOK-

Wire+)

RegisterBond Issuer

6.Interest

Payment

(via BOK-

Wire+)

KSD’s Bank

1.Application for Exchange

2.Submit Bonds3.Exchange Confirmation

Notification of

bond holder’s list7.Interest payment list

notification

22

KR

1. KSD sends an application for exchange to KSD’s bank.

2. KSD’s bank submit bonds to KFTC.

3. KFTC sends an exchange confirmation to a payment bank of a bond issuer.

4. A bond issuer makes fund payment for interest to a payment bank.

5. A payment bank makes netted fund payment to KSD’s bank.

6. KSD’s bank makes interest payment to KSD participants.

7. KSD notifies KSD participants of interest payment list.

8. KSD participants make interest payments to bondholders.

Process of Interest Payment

3.2.1Interest Payment Flow of Corporate Bond

23

KR

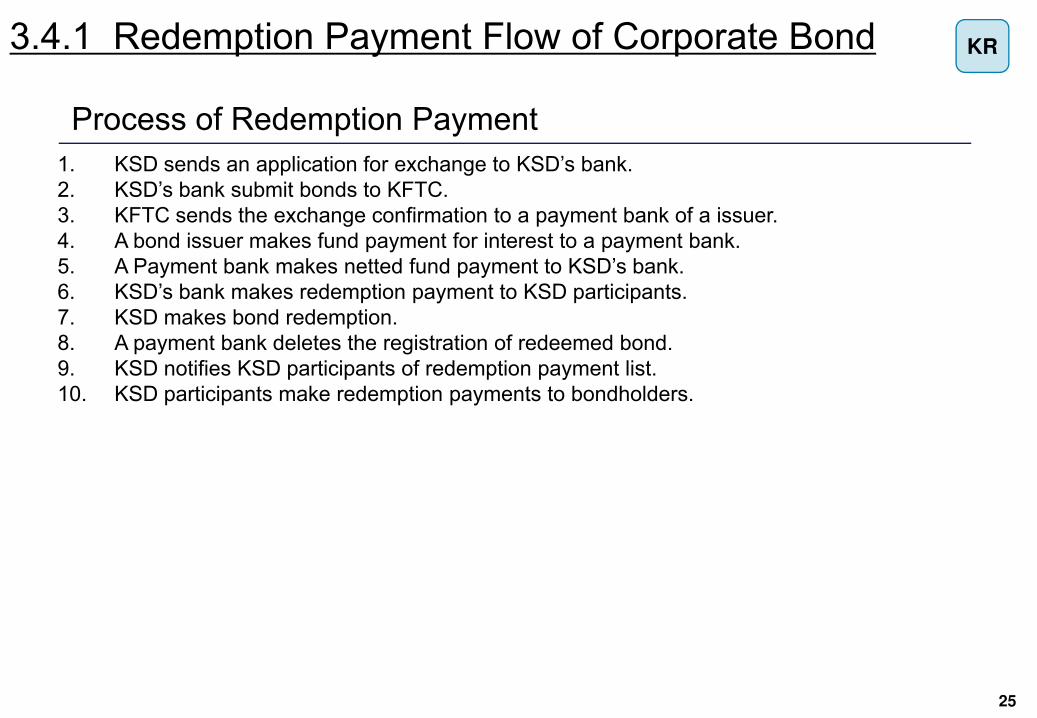

3.4.1 Redemption Payment Flow of Corporate Bond

Bond Issuer Side CSD Bond Holder Side

Bond Holder

KFTC

(KOREA FINANCIAL TELECOMMUNICATIONS & CLEARINGS INSTITUTE)

4.Fund payment

(deposit principal)

10.Redemption

payment

KSD

Participant

5.Redempti

on payment

(via BOK-

Wire+)

RegisterBond Issuer

KSD’s Bank

1.Application for Exchange

2.Submit Bonds3.Exchange Confirmation

Notification of

bondholder’s list

6.Redempti

on payment

(via BOK-

Wire+)

9.Redemption payment

list notification

7. Redemption

KSD

8.Delete bond registration

Payment Bank

24

KR

1. KSD sends an application for exchange to KSD’s bank.

2. KSD’s bank submit bonds to KFTC.

3. KFTC sends the exchange confirmation to a payment bank of a issuer.

4. A bond issuer makes fund payment for interest to a payment bank.

5. A Payment bank makes netted fund payment to KSD’s bank.

6. KSD’s bank makes redemption payment to KSD participants.

7. KSD makes bond redemption.

8. A payment bank deletes the registration of redeemed bond.

9. KSD notifies KSD participants of redemption payment list.

10. KSD participants make redemption payments to bondholders.

Process of Redemption Payment

3.4.1 Redemption Payment Flow of Corporate Bond

25

KR

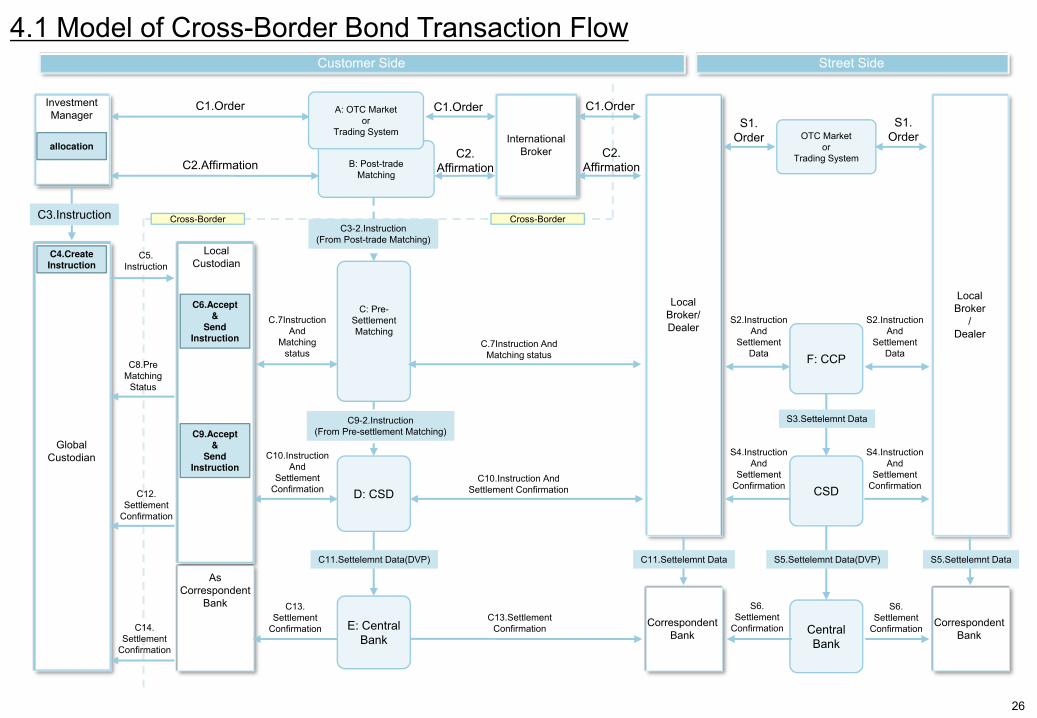

4.1 Model of Cross-Border Bond Transaction FlowCustomer Side Street Side

Investment

Manager

Local

Broker/

Dealer

Local

Broker

/

Dealer

D: CSD

E: Central

Bank

OTC Market

or

Trading System

CSD

Central

Bank

Global

Custodian

Local

Custodian

C3.Instruction

C11.Settelemnt Data(DVP)

International

BrokerB: Post-trade

Matching

Cross-Border

allocation

C4.CreateInstruction

C6.Accept&

SendInstruction

C9.Accept&

SendInstruction

C.7Instruction And

Matching status

C.7Instruction

And

Matching

status

C8.Pre

Matching

Status

C5.

Instruction

C10.Instruction

And

Settlement

ConfirmationC10.Instruction And

Settlement Confirmation

C1.Order C1.Order

C2.AffirmationC2.

Affirmation

C1.Order

C2.

Affirmation

S1.

Order

S1.

Order

C12.

Settlement

Confirmation

C14.

Settlement

Confirmation

C13.

Settlement

Confirmation

C13.Settlement

Confirmation

Cross-Border

C: Pre-

Settlement

Matching

As

Correspondent

Bank

Correspondent

Bank

S5.Settelemnt Data(DVP)

S6.

Settlement

Confirmation

S6.

Settlement

ConfirmationCorrespondent

Bank

C11.Settelemnt Data S5.Settelemnt Data

S4.Instruction

And

Settlement

Confirmation

S4.Instruction

And

Settlement

Confirmation

F: CCP

S2.Instruction

And

Settlement

Data

S2.Instruction

And

Settlement

Data

S3.Settelemnt Data

C3-2.Instruction

(From Post-trade Matching)

C9-2.Instruction

(From Pre-settlement Matching)

A: OTC Market

or

Trading System

26

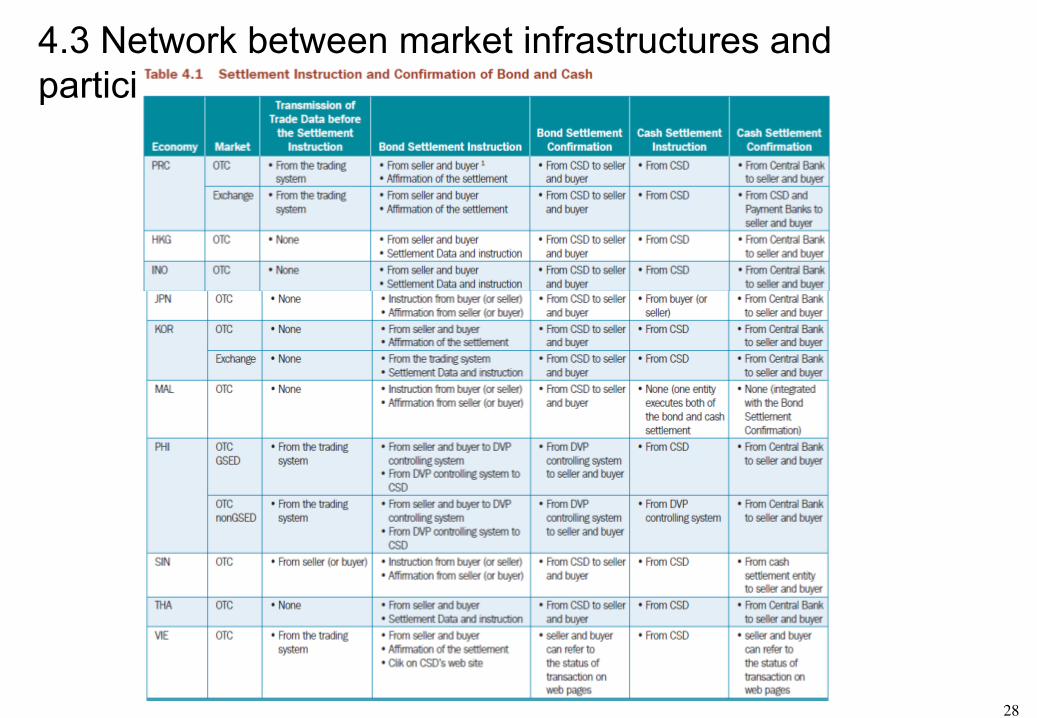

4.3 Network between market infrastructures and

participants

27

4.3 Network between market infrastructures and

participants

28

4.3 Network between market infrastructures and

participants

29

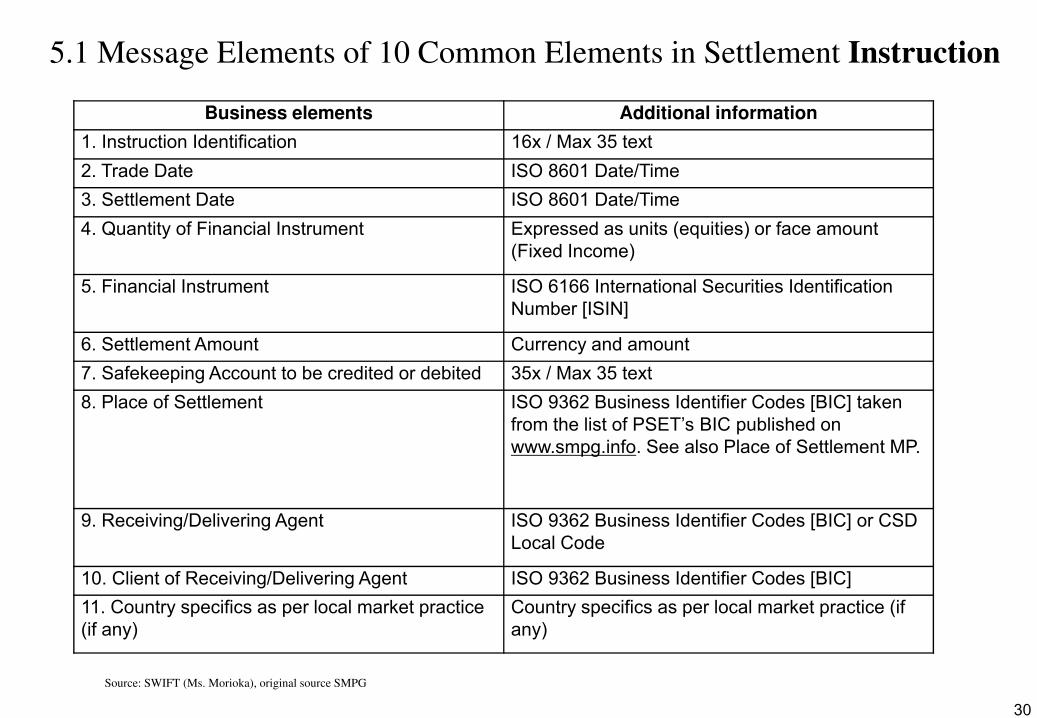

Business elements Additional information

1. Instruction Identification 16x / Max 35 text

2. Trade Date ISO 8601 Date/Time

3. Settlement Date ISO 8601 Date/Time

4. Quantity of Financial Instrument Expressed as units (equities) or face amount

(Fixed Income)

5. Financial Instrument ISO 6166 International Securities Identification

Number [ISIN]

6. Settlement Amount Currency and amount

7. Safekeeping Account to be credited or debited 35x / Max 35 text

8. Place of Settlement ISO 9362 Business Identifier Codes [BIC] taken

from the list of PSET’s BIC published on

www.smpg.info. See also Place of Settlement MP.

9. Receiving/Delivering Agent ISO 9362 Business Identifier Codes [BIC] or CSD

Local Code

10. Client of Receiving/Delivering Agent ISO 9362 Business Identifier Codes [BIC]

11. Country specifics as per local market practice

(if any)

Country specifics as per local market practice (if

any)

5.1 Message Elements of 10 Common Elements in Settlement Instruction

Source: SWIFT (Ms. Morioka), original source SMPG

30

5.2 Message Elements of 10 common elements in Settlement Confirmation

10 Common Elements in Settlement Instruction

Source: SMPG (Settlement Common Elements) 31

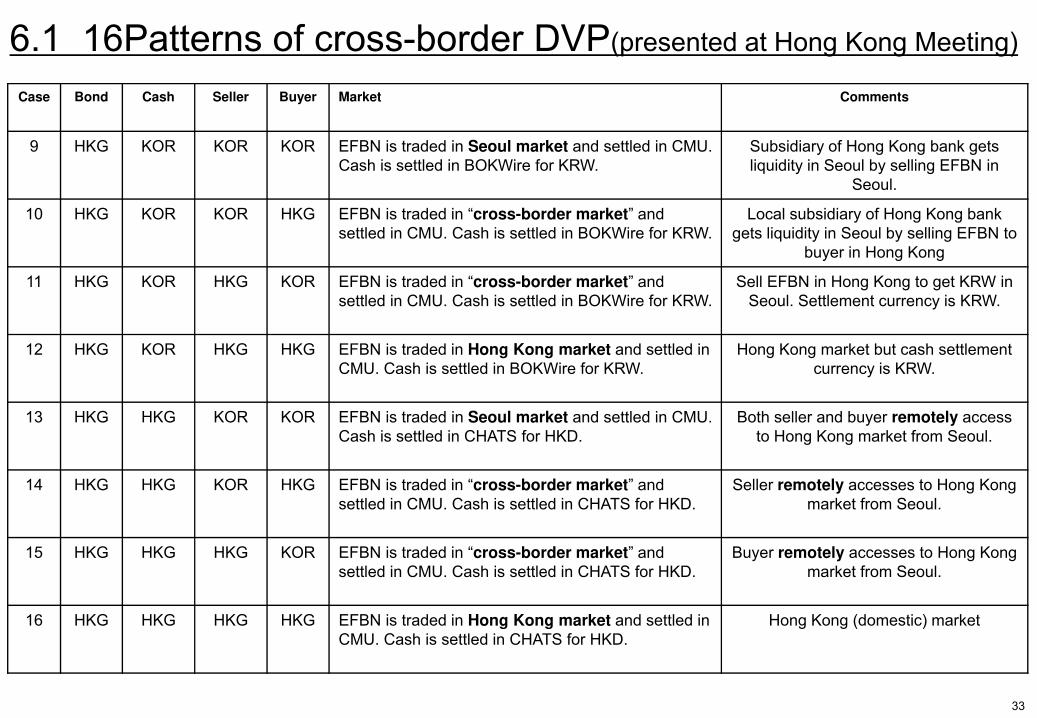

6. 16Patterns of cross-border DVP(presented at Hong Kong Meeting)

Case Bond Cash Seller Buyer Market Comments

1 KOR KOR KOR KOR KTB is traded in Seoul market and settled in KSD.

Cash is settled in BOKWire for KRW.

Seoul (Domestic) market

2 KOR KOR KOR HKG KTB is traded in “cross-border market” and settled

in KSD. Cash is settled in BOKWire for KRW.

Buyer remotely accesses to Seoul

market from Hong Kong

3 KOR KOR HKG KOR KTB is traded in “cross-border market” and settled

in KSD. Cash is settled in BOKWire for KRW.

Seller remotely accesses to Seoul

market from Hong Kong

4 KOR KOR HKG HKG KTB is traded in Hong Kong market and settled in

KSD. Cash is settled in BOKWire for KRW.

Both seller and buyer remotely access

to Seoul market from Hong Kong

5 KOR HKG KOR KOR KTB is traded in Seoul market and settled in KSD.

Cash is settled in CHATS for HKD.

Seoul market but cash settlement

currency is HKD.

6 KOR HKG KOR HKG KTB is traded in “cross-border market” and settled

in KSD. Cash is settled in CHATS for HKD.

Sell KTB in Seoul to buyer in Hong Kong.

Cash settlement currency is HKD.

7 KOR HKG HKG KOR KTB is traded in “cross-border market” and settled

in KSD. Cash is settled in CHATS for HKD.

Local subsidiary of Korean bank gets

liquidity in Hong Kong by selling KTB to

buyer in Seoul

8 KOR HKG HKG HKG KTB is traded in Hong Kong market and settled in

KSD. Cash is settled in CHATS for HKD.

Local subsidiary of Korean bank gets

liquidity in Hong Kong by selling KTB in

Hong Kong.

32

Case Bond Cash Seller Buyer Market Comments

9 HKG KOR KOR KOR EFBN is traded in Seoul market and settled in CMU.

Cash is settled in BOKWire for KRW.

Subsidiary of Hong Kong bank gets

liquidity in Seoul by selling EFBN in

Seoul.

10 HKG KOR KOR HKG EFBN is traded in “cross-border market” and

settled in CMU. Cash is settled in BOKWire for KRW.

Local subsidiary of Hong Kong bank

gets liquidity in Seoul by selling EFBN to

buyer in Hong Kong

11 HKG KOR HKG KOR EFBN is traded in “cross-border market” and

settled in CMU. Cash is settled in BOKWire for KRW.

Sell EFBN in Hong Kong to get KRW in

Seoul. Settlement currency is KRW.

12 HKG KOR HKG HKG EFBN is traded in Hong Kong market and settled in

CMU. Cash is settled in BOKWire for KRW.

Hong Kong market but cash settlement

currency is KRW.

13 HKG HKG KOR KOR EFBN is traded in Seoul market and settled in CMU.

Cash is settled in CHATS for HKD.

Both seller and buyer remotely access

to Hong Kong market from Seoul.

14 HKG HKG KOR HKG EFBN is traded in “cross-border market” and

settled in CMU. Cash is settled in CHATS for HKD.

Seller remotely accesses to Hong Kong

market from Seoul.

15 HKG HKG HKG KOR EFBN is traded in “cross-border market” and

settled in CMU. Cash is settled in CHATS for HKD.

Buyer remotely accesses to Hong Kong

market from Seoul.

16 HKG HKG HKG HKG EFBN is traded in Hong Kong market and settled in

CMU. Cash is settled in CHATS for HKD.

Hong Kong (domestic) market

33

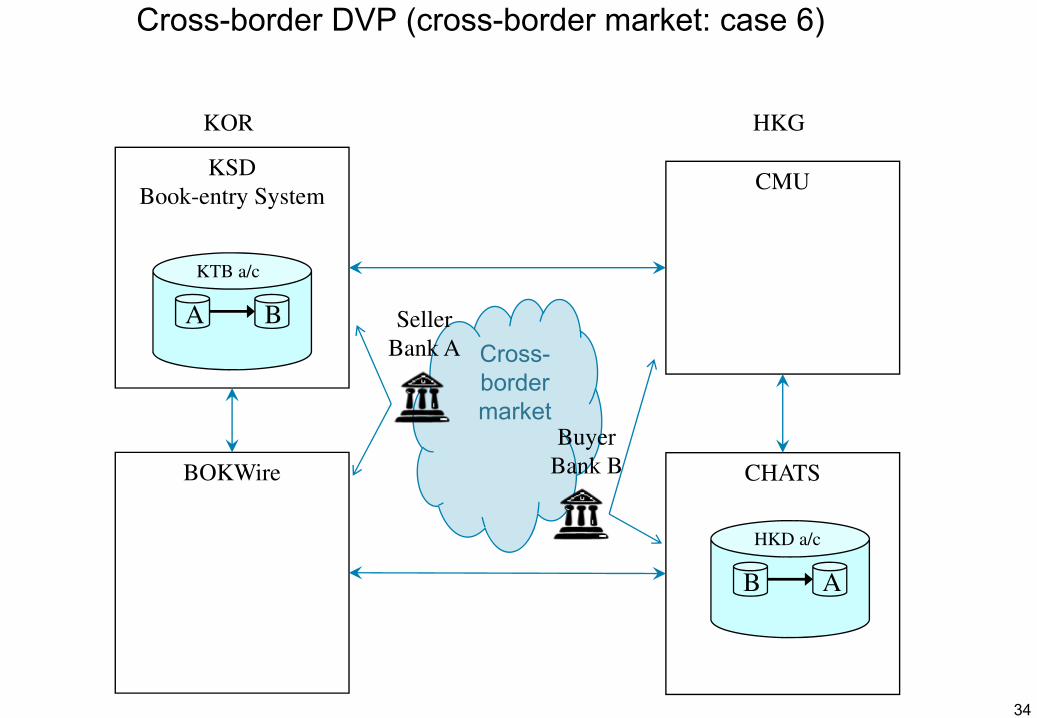

6.1 16Patterns of cross-border DVP(presented at Hong Kong Meeting)

Cross-border DVP (cross-border market: case 6)

34

KSD

Book-entry System

KTB a/c

BA

BOKWire

CMU

CHATS

HKD a/c

AB

Seller

Bank A

Buyer

Bank B

KOR HKG

Cross-

border

market

Cross-border DVP (Hong Kong market: case 8)

35

KSD

Book-entry System

KTB a/c

BA

BOKWire

CMU

CHATS

HKD a/c

AB

Seller

Bank A

Buyer

Bank B

KOR HKG

6.1 Cross-Border Bond Transaction Flow (Case6)

Economy-A Economy-B

Sell

side

Bond Market

(Exchange or OTC)

Buy

sideSeller → Buyer

Buyer → Seller

CSD-A

Central Bank-B

CSD-B

Book-Entry System

RTGS System

Cross-Border

Trade 1.Trade

instruction instruction

result

result

result

DVP

result

result

instruction

Access

Control

36

6. 2 Cross-Border Bond Transaction Flow (Case8)

Economy-A Economy-B

Sell

side

Bond Market

Buy

sideSeller → Buyer

Buyer → Seller

CSD-A

Central

Bank-B

CSD-B

Book-Entry System

RTGS System

Cross-Border

Trade Trade

instruction

instruction

result

result

DVP

result

result

instructionAccess

Control

37

Sell

side

result

instruction

7. Roadmap

Could you refer to the page 41 of handout

“Questionnaire for Phase2 of ABMF SF2 (draft)”,

please?

8. Follow-up of Phase 1 Survey

Could you refer to the page 60 of handout

“Questionnaire for Phase2 of ABMF SF2 (draft)”,

please?

8.2 Protocols and Message Formats in ASEAN+3 Bond Markets

Market①Between CSD and seller/buyer

②Between Cash Settlement System

and a seller/a buyer

Linkage Protocol Message Format Protocol Message Format

CN OTC direct link・TCP/IP

・HTTP, SOAP・XML and Text ・TCP/IP -

HK OTC direct link ・TCP/IP ・ISO15022 ・TCP/IP ・SWIFT

ID OTC terminal access・SNA. TCP/IP

will be adopted

・Proprietary.

SWIFT will be

adopted.

・SNA. TCP/IP will

be adopted.

Proprietary.

SWIFT will be

adopted.

JP OTC direct link ・TCP/IP

・Proprietary.

ISO20022 will be

applied (CSV and

XML)

・TCP/IP

Proprietary.

ISO20022 will be

adopted.

KR OTC direct link ・TCP/IP - ・TCP/IP -MY OTC terminal access ・TCP/IP - ・TCP/IP -

PHOTC

GSEDterminal access

・TCP/IP

・HTTPS・Proprietary ・TCP/IP ・SWIFT

SG OTC terminal access ・TCP/IP - ・TCP/IP -

TH OTC terminal access・TCP/IP

・HTTPS- ・TCP/IP -

VN OTC terminal access ・TCP/IP ・XML - -

40

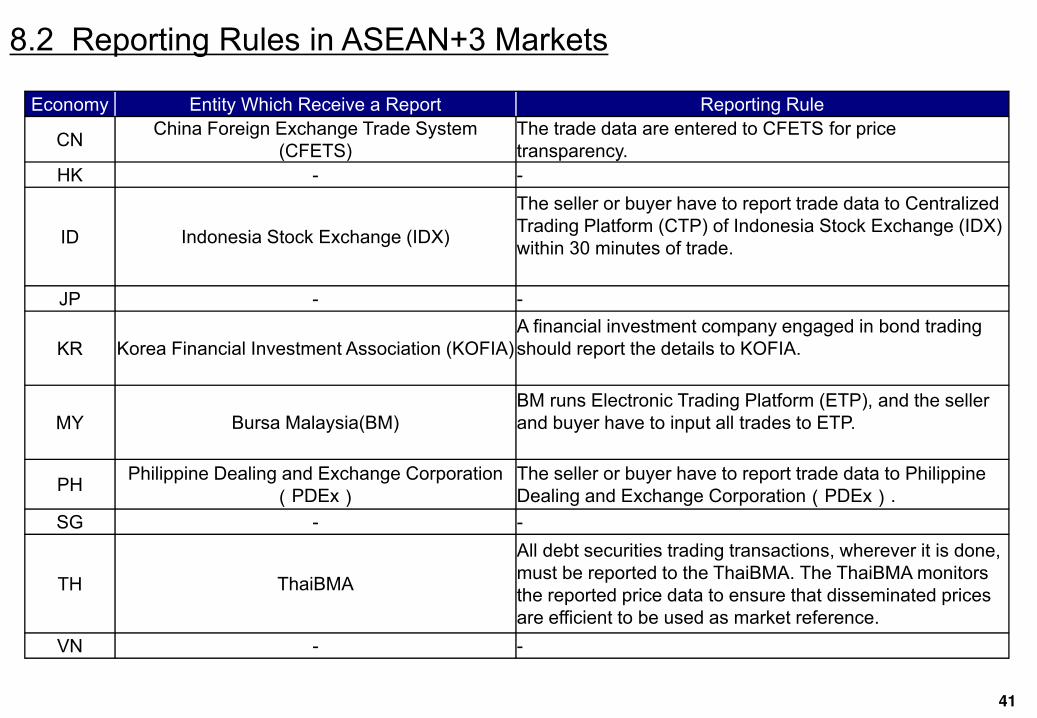

8.2 Reporting Rules in ASEAN+3 Markets

Economy Entity Which Receive a Report Reporting Rule

CNChina Foreign Exchange Trade System

(CFETS)

The trade data are entered to CFETS for price

transparency.

HK - -

ID Indonesia Stock Exchange (IDX)

The seller or buyer have to report trade data to Centralized

Trading Platform (CTP) of Indonesia Stock Exchange (IDX)

within 30 minutes of trade.

JP - -

KR Korea Financial Investment Association (KOFIA)

A financial investment company engaged in bond trading

should report the details to KOFIA.

MY Bursa Malaysia(BM)

BM runs Electronic Trading Platform (ETP), and the seller

and buyer have to input all trades to ETP.

PHPhilippine Dealing and Exchange Corporation

(PDEx)The seller or buyer have to report trade data to Philippine

Dealing and Exchange Corporation(PDEx).

SG - -

TH ThaiBMA

All debt securities trading transactions, wherever it is done,

must be reported to the ThaiBMA. The ThaiBMA monitors

the reported price data to ensure that disseminated prices

are efficient to be used as market reference.

VN - -

41

8.2 Matching Types in ASEAN+3 Markets

Trade matching Pre-settlement matching Settlement matching

CN CFETS - Central/Local

HK CMU Central/Local

ID - Telephone, facsimile, etc. Central

JP PSMS PSMS Local

KR B-TRis - Central/Local

MY (BMS ETP) RENTAS Local

PHFI trading system

/RoSSTelephone, facsimile, etc. Central /Local

SG - PTI, Telephone, etc. Local

TH - Telephone, facsimile, etc. Central

VN HNX - Central

42

8.2 Operating Hours

CSD Operating Hour (ASEAN time)

Open Cut off Time

CN CCDC - -

CSDCC - -

HK CMU 8:30 (7:30) 18:30 (17:30)

ID BI 6:30 (6:30) 19:00 (19:00)

JP BOJ 9:00 (7:00) 16:30 (14:30)

JASDEC 9:00 (7:00) 17:00 (15:00)

KR KSD 9:00 (7:00) 17:00 (15:00)

MY MyClear - -

PH BTr-RoSS 9:30 (8:30) 15:30 (14:30)

PDTC 8:00 (7:00) 18:00 (17:00)

SG MAS - -

TH TSD - -

VN VSD - -

43

8.2 Numbers and Codes in ASEAN+3 Markets

MarketSecurities

numbering

Financial Institution

IdentificationSecurities account Cash account

Character code and

language

CN OTC Proprietary code Proprietary code Proprietary code Proprietary code UNICODE (UTF8)

HK OTCISIN and proprietary

code(CMU issues) Proprietary code Proprietary code Proprietary codeCode supported by

SWIFT

ID OTCISIN and proprietary

code

BIC and proprietary

codeProprietary code Proprietary code -

JP OTCISIN and proprietary

code

BIC and proprietary

codeProprietary code Proprietary code UNICODE (UTF8)

KR OTCISIN and proprietary

code

Proprietary code

(account number)Proprietary code

・KSC5601 for

Korean

MY OTC - - - - -

PH OTC

ISIN and proprietary

code for

government

securities

Proprietary code

(PDS-assigned firm

codes)

Proprietary code Proprietary code UNICODE (UTF8)

SG OTC - - - - UNICODE (UTF8)

TH OTC ISIN BIC Proprietary code Proprietary code UNICODE (UTF8)

VN OTCISIN and proprietary

codeN/A Proprietary code N/A UNICODE (UTF8)

44

8.4.1 Account Structure of Government Bond JP

Account Structure

BOJ

JGB Account Book

Direct Participant X Direct Participant YAccount of

BOJ・・・

Own

Account

Customer’s

Account

Own

Account

Customer’s

Account

Own

Account

Customer’s

Account

Direct Participant X

Account Book

Indirect Participant A

Custo

mer’s

AccountOwn

Account

Customer’s

Account

Custo

mer’s

Account

Indirect Participant A

Account Book

Custo

mer’s

Account

Custo

mer’s

Account

Custo

mer’s

Account

Custo

mer’s

Account

Direct Participant X

Account Book

Foreign

Indirect Participant B

Custo

mer’s

AccountOwn

Account

Customer’s

Account

Foreign

Indirect Participant B

Account Book

Custo

mer’s

Account

Custo

mer’s

Account

Custo

mer’s

Account

Custo

mer’s

Account

Code Structure

Participant Code

4 Digits Numeric

Participant Type

4 Digits Numeric

Account Type

2 Digits Numeric

Account code of JGB Account Book (8Digits)

X X X X X X X X

Cu

sto

me

r Ⅰ

Participant type 01

・・

Cu

sto

me

r Ⅱ

Pro

prie

tary

Ⅰ

Pro

prie

tary

Ⅱ

Pro

prie

tary

Ⅲ

Cu

sto

me

r Ⅰ

Pro

prie

tary

Ⅳ

Participant type 02

Participant Account 1234Participant

Account 2345

11 12 01 02 03 11 04

Example of Participant’s Account

45

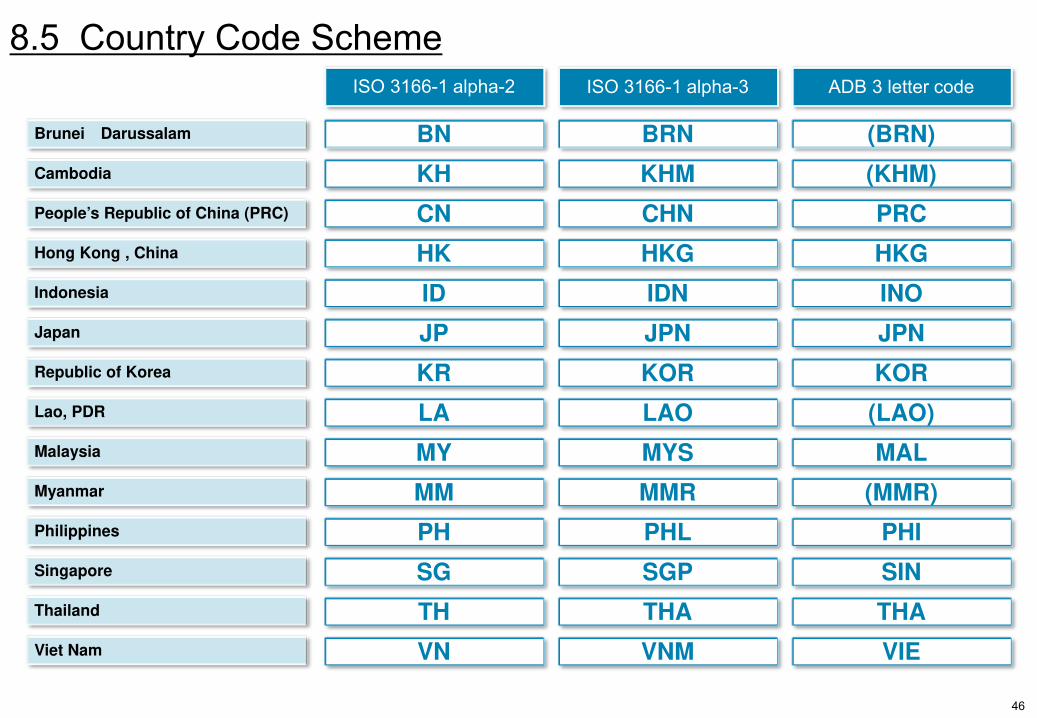

People’s Republic of China (PRC)

Hong Kong , China

Indonesia

Japan

Republic of Korea

Malaysia

Philippines

Singapore

Thailand

Viet Nam

Lao, PDR

ISO 3166-1 alpha-3ISO 3166-1 alpha-2 ADB 3 letter code

BRNBN (BRN)

Cambodia

Brunei Darussalam

Myanmar

KHMKH (KHM)

CHNCN PRC

HKGHK HKG

IDNID INO

JPNJP JPN

KORKR KOR

LAOLA (LAO)

MYSMY MAL

MMRMM (MMR)

PHLPH PHI

SGPSG SIN

THATH THA

VNMVN VIE

8.5 Country Code Scheme

46

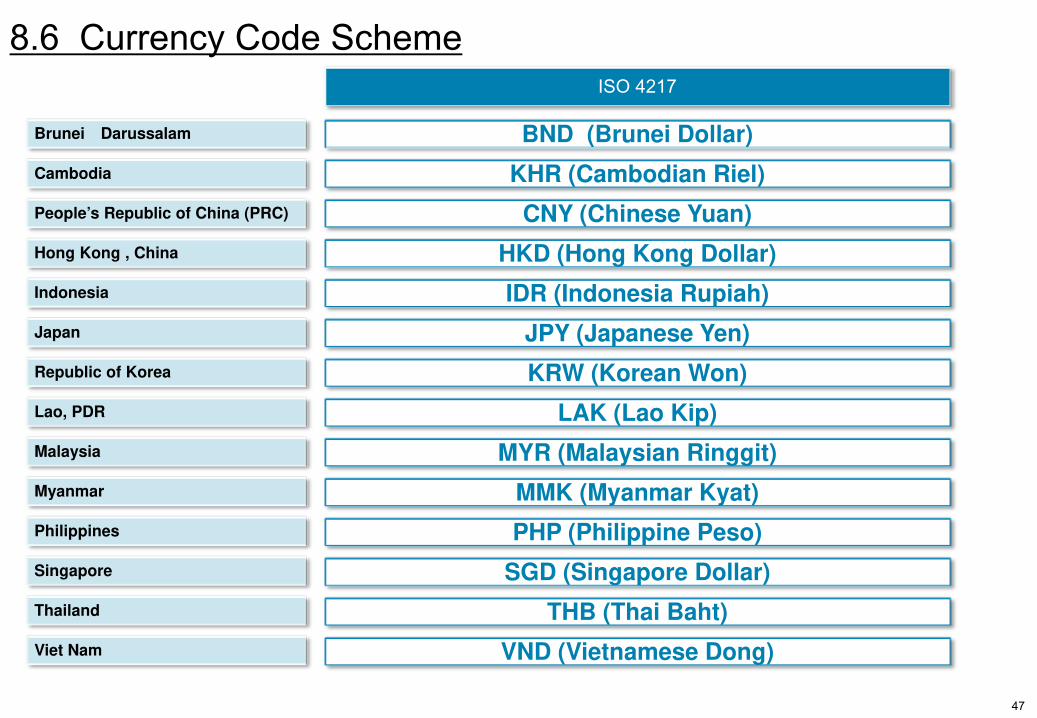

People’s Republic of China (PRC)

Hong Kong , China

Indonesia

Japan

Republic of Korea

Malaysia

Philippines

Singapore

Thailand

Viet Nam

Lao, PDR

ISO 4217

BND (Brunei Dollar)

Cambodia

Brunei Darussalam

Myanmar

KHR (Cambodian Riel)

CNY (Chinese Yuan)

HKD (Hong Kong Dollar)

IDR (Indonesia Rupiah)

JPY (Japanese Yen)

KRW (Korean Won)

LAK (Lao Kip)

MYR (Malaysian Ringgit)

MMK (Myanmar Kyat)

PHP (Philippine Peso)

SGD (Singapore Dollar)

THB (Thai Baht)

VND (Vietnamese Dong)

8.6 Currency Code Scheme

47

8.6 Detail business flowchart of government bond DVP transaction

Buyer

PSMS

(Pre-Settlement

Matching System)

Seller

Clearing System

(Japan Government

Bond Clearing

Corporation- JGBCC)

Trade execution Trade Matching

T

Notice of

Execution

1

Order Allocation

AllocationTrade

Report Data

Investment

Instruction

Data

Trade

Matching

Notice Data

of Trade

Matching

Status

Notice Data

of Trade

Matching

Status

Matched Trade

Report

48

JP

8.6 Detail business flowchart of government bond DVP transaction

Buyer

PSMS

(Pre-Settlement

Matching System)

Seller

Clearing System

(Japan Government

Bond Clearing

Corporation- JGBCC)

PSMS

(Pre-Settlement

Matching System)

CSD

(The BOJ-Net)

T ~(T + 2 )

Clearing

2

S - 1

Approval of

Obligation

Notice Data of

Approval of

Obligation

Notice Data of

Approval of

Obligation

Novation

Notice Data of

Novation

Notice Data of

Novation

Netting

Notice Data of

Netting

Notice Data of

Netting

DVP

Order

JGB Transfer Instruction

for DVP (For Deliverer

and Receiver of JGB)

1

49

JP

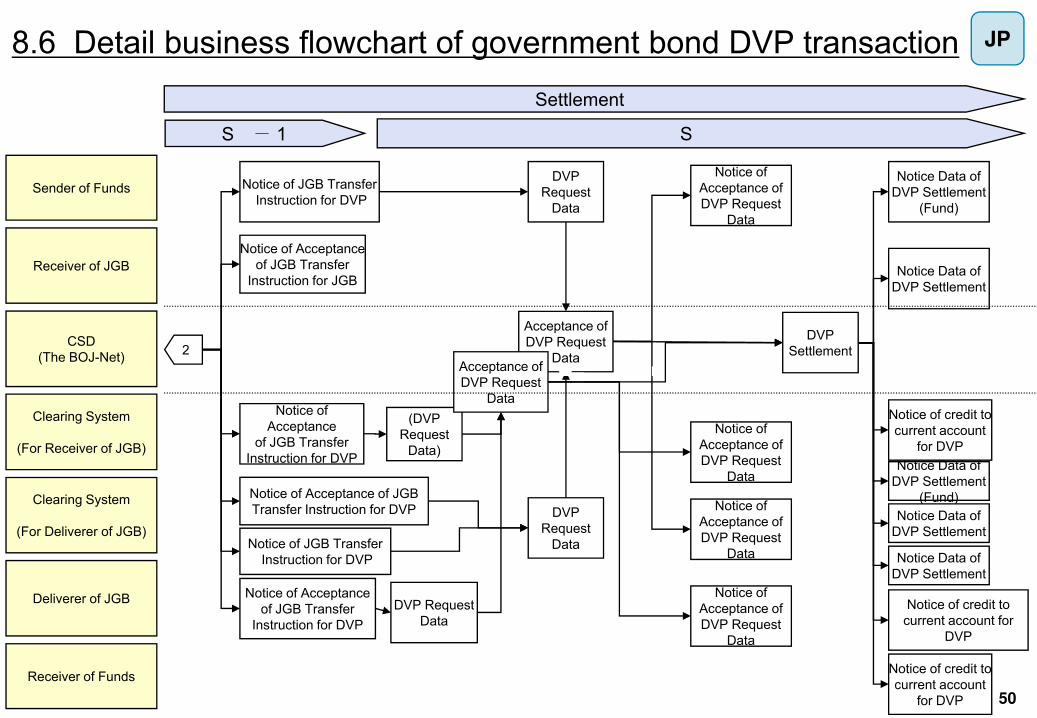

8.6 Detail business flowchart of government bond DVP transaction

Sender of Funds

Clearing System

(For Receiver of JGB)

Receiver of Funds

Clearing System

(For Deliverer of JGB)

CSD

(The BOJ-Net)

Deliverer of JGB

Receiver of JGB

Settlement

SS - 1

2

Notice of Acceptance

of JGB Transfer

Instruction for JGB

Notice of Acceptance

of JGB Transfer

Instruction for DVP

Notice of

Acceptance

of JGB Transfer

Instruction for DVP

Notice of Acceptance of JGB

Transfer Instruction for DVP DVP

Request

Data

DVP Request

Data

DVP

Request

Data

Acceptance of

DVP Request

Data

Notice of

Acceptance of

DVP Request

Data

Notice of

Acceptance of

DVP Request

Data

Notice of

Acceptance of

DVP Request

Data

(DVP

Request

Data)

DVP

Settlement

Notice Data of

DVP Settlement

(Fund)

Notice Data of

DVP Settlement

Notice of credit to

current account

for DVP

Notice Data of

DVP Settlement

Notice of

Acceptance of

DVP Request

Data

Notice Data of

DVP Settlement

(Fund)

Notice of JGB Transfer

Instruction for DVP

Acceptance of

DVP Request

Data

Notice of credit to

current account

for DVP

Notice of JGB Transfer

Instruction for DVP

Notice Data of

DVP Settlement

Notice of credit to

current account for

DVP

50

JP

9. Other issues

9.1 LEI

9.2 Data collection

9.3 Contribution to ISO

9.4 Challenges and future issues

9.5 Any other issues related to SF2

10. How do you think to foster cross-border STP?

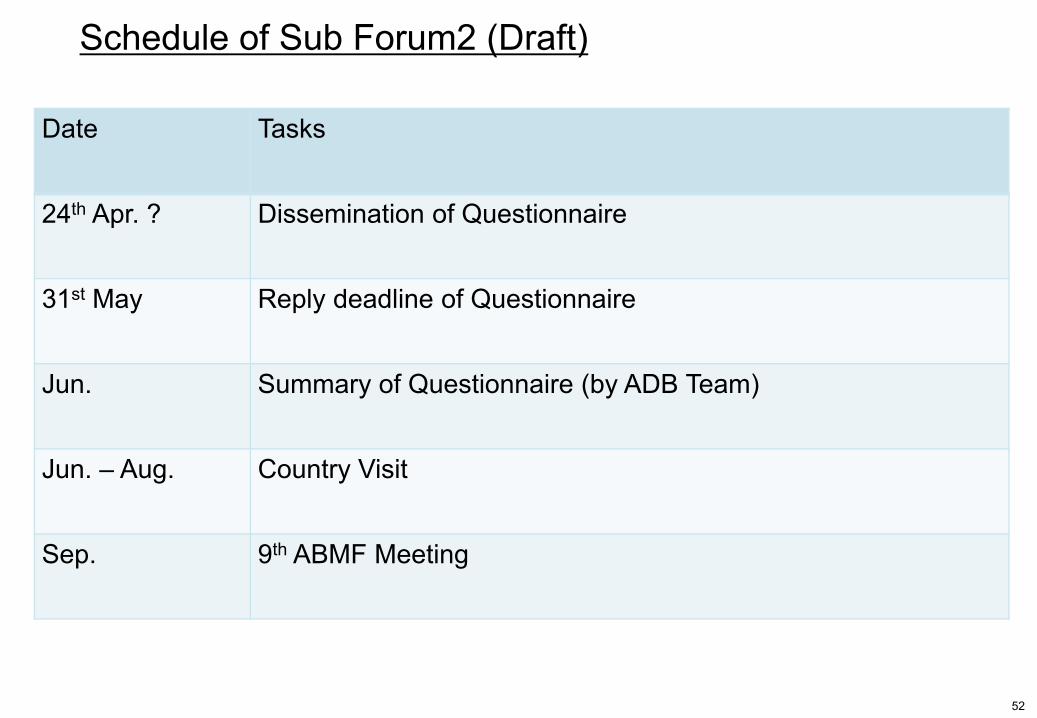

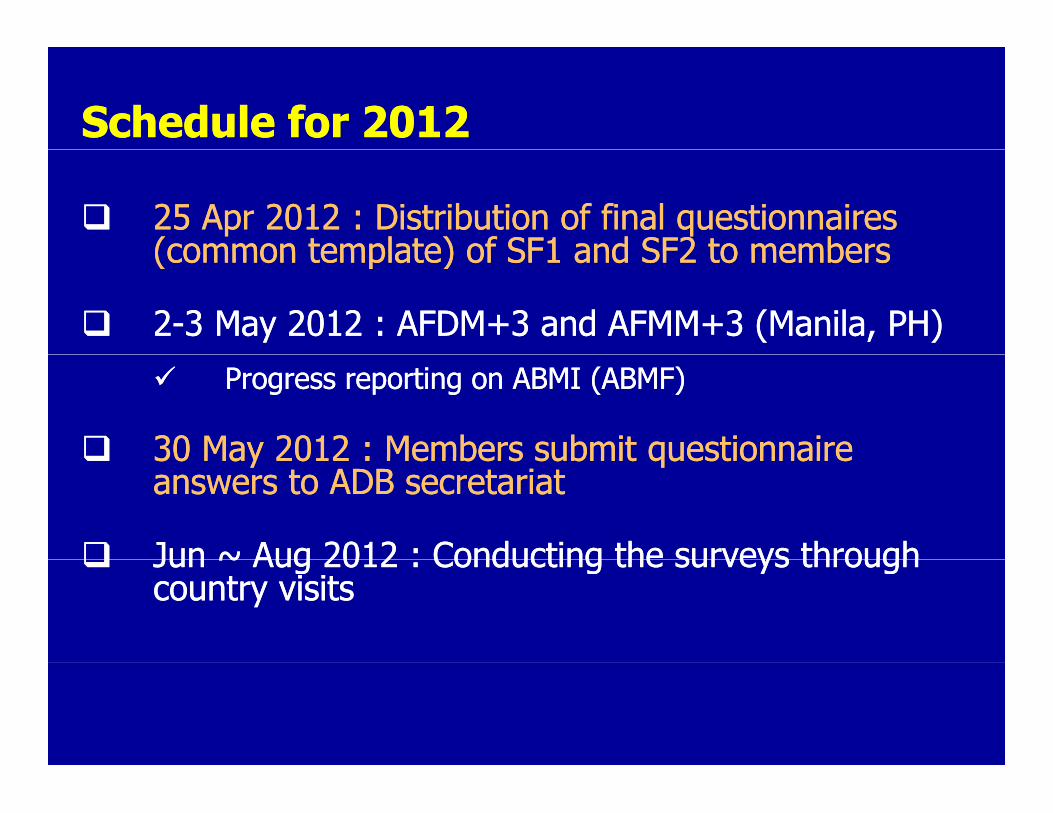

Date Tasks

24th Apr. ? Dissemination of Questionnaire

31st May Reply deadline of Questionnaire

Jun. Summary of Questionnaire (by ADB Team)

Jun. – Aug. Country Visit

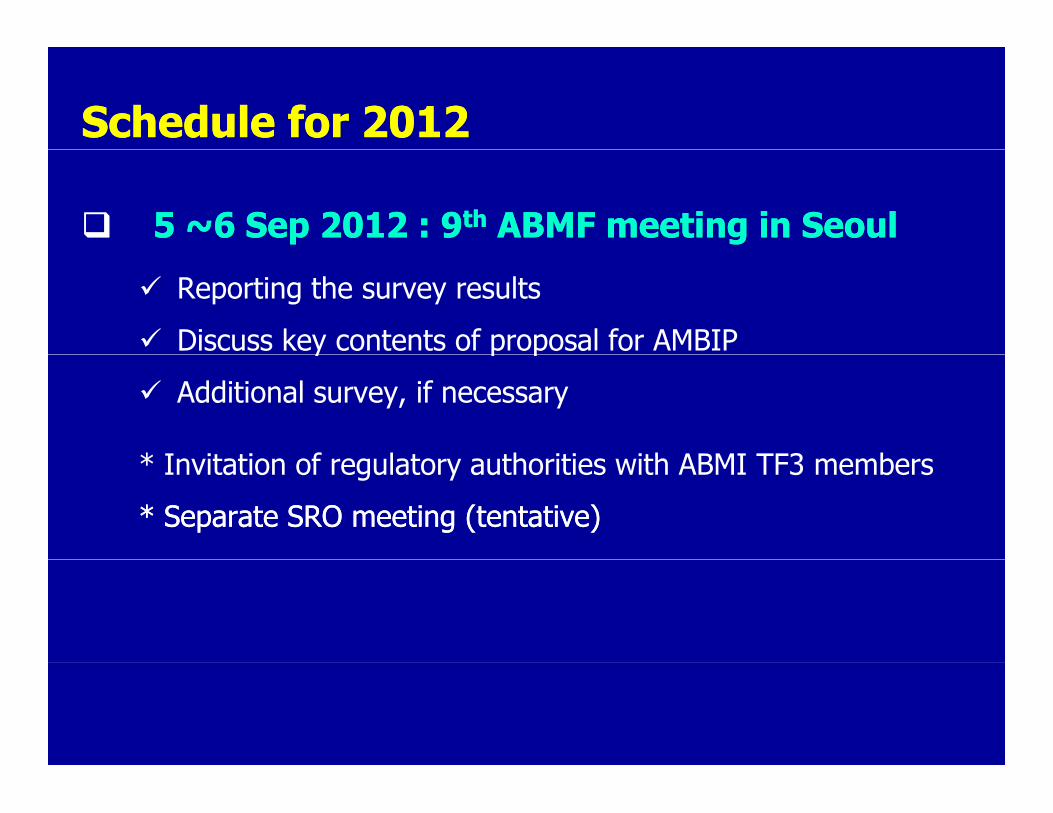

Sep. 9th ABMF Meeting

Schedule of Sub Forum2 (Draft)

52

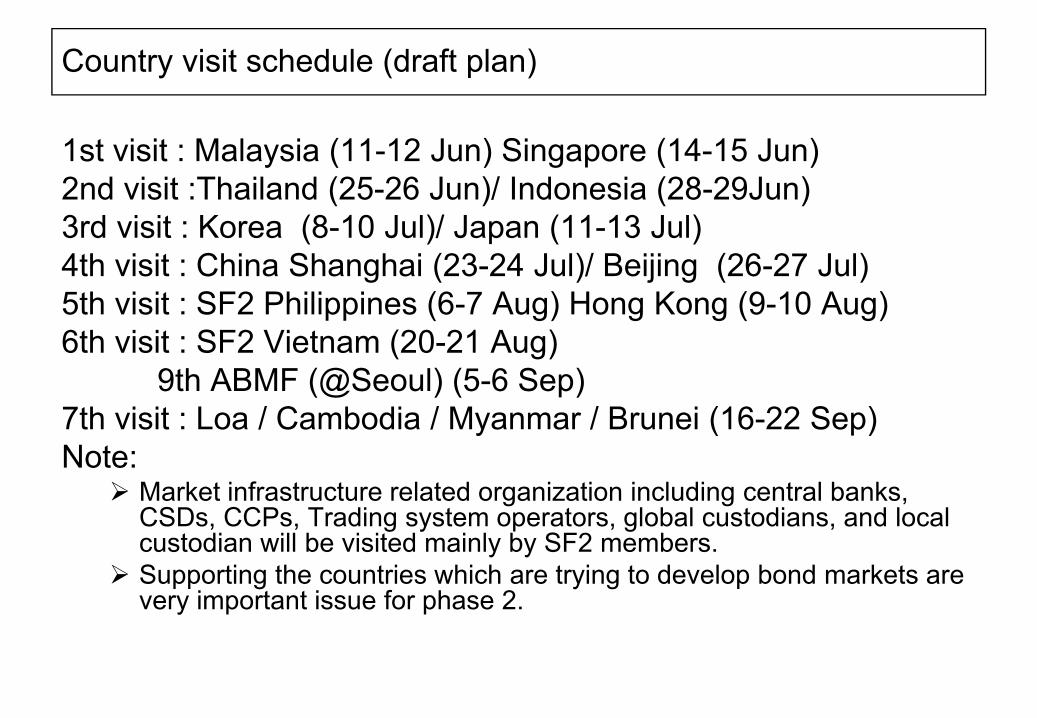

Country visit schedule (draft plan)

1st visit : Malaysia (11-12 Jun) Singapore (14-15 Jun)

2nd visit :Thailand (25-26 Jun)/ Indonesia (28-29Jun)

3rd visit : Korea (8-10 Jul)/ Japan (11-13 Jul)

4th visit : China Shanghai (23-24 Jul)/ Beijing (26-27 Jul)

5th visit : SF2 Philippines (6-7 Aug) Hong Kong (9-10 Aug)

6th visit : SF2 Vietnam (20-21 Aug)

9th ABMF (@Seoul) (5-6 Sep)

7th visit : Loa / Cambodia / Myanmar / Brunei (16-22 Sep)

Note: Market infrastructure related organization including central banks, CSDs, CCPs, Trading system operators, global custodians, and local custodian will be visited mainly by SF2 members.

Supporting the countries which are trying to develop bond markets are very important issue for phase 2.

54

Preaching

to Buddha

+3

Thank you so much

Taiji Inui ADB consultant

NTT DATA Corporation

Phone: +81-50-5547-1282

E-mail: [email protected]

This PowerPoint slides are made solely for the discussions at the 8th ABMF on 18 April 2012. Views

expressed are those of the presenter and do not necessarily reflect those of the Asian Development Bank,

NTT DATA CORPORATION or any other organizations.

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

Questionnaire for Phase2 of ABMF SF2 (draft)

8th ABMF-SF2, 18 April 2012, Manila

For all ABMF SF2 members and experts

Economy or country

Contact person

Institution

Mailing address

Phone number

e-mail address

Alternate person

Institution

Mailing address

Phone number

e-mail address

Notes:

National members (and experts) are expected to answer following questions as much as

possible.

If International Experts could voluntarily answer the following questions for all possible

economies, ADB Consultant for SF2 will be extremely appreciate it. Also, could you

comment on the draft contents of the Report of phase 2 (Appendix), please?

ADB consultant for SF2 does understand the above are extremely demanding request, but

very much appreciate kind support of SF2 members and experts where possible in order to

develop efficient and smooth cross-border bond trades and settlement for liquid and stable

bond markets in ASEAN+3.

Could you post the answer on the ADB site for phase 2 answer, or send the answer back to

Taiji Inui, ADB Consultant for SF2 by the end of May, please? Any questions and comments

are appreciated. Taiji Inui, e-mail: [email protected], phone:+81-80-5547-1282 (office),

+81-80-1103-6145 (mobile)

1

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

Introduction

Scope of the phase 2 activities of ABMF SF2, reported to and approved by ABMI TF3 Meeting

on 2 March in 2012 in Siem Reap, Cambodia. is as follows:

A) Continue identification of transaction flows, messaging and market practices.

DVP flows and procedures for corporate bonds

Interest payment and redemption of government bonds

Interest payment and redemption of corporate bonds

B) ISO 20022 Fit-and-gap analysis

C) Propose a roadmap and policy recommendations to standardize and harmonize

transaction flows

D) Information sharing: LEI, data collection,…

General explanations of the questionnaire

1) As a result of ABMF SF2 phase 1 survey, Government Bond Market Infrastructure

Diagram in ASEAN+3 was reported to ABMI TF3 and published. Corporate Bond

Market Infrastructure Diagram in ASEAN+3 will be presented as a result of phase 2

survey of ABMF SF2.

Phase 1 report of ABMF SF2 has discussed mainly about government bond

markets in ASEAN+3 and each market. But, as for the phase2 survey and

report of ABMF SF2, corporate bond markets will also be discussed.

SF2 members are expected to provide government bond market infrastructure

diagram and corporate bond market infrastructure diagram separately.

2) ABMF SF2 report to ABMI TF3 will be expanded including corporate bond market

description. DVP flows of corporate bonds will also be surveyed and analyzed as a

phase 2 activity.

SF2 members are expected to update and refine the phase 1 report based on

the new contents shown in Appendix describing government bond markets and

corporate bond markets separately.

ADB Consultant of SF2 will try to include bond markets and settlement

infrastructures including future plans and initiatives in Brunei Darussalam,

Cambodia, Lao PDR, and Myanmar as much as possible for the phase 2 report

with kind support of the 4 countries.

2

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

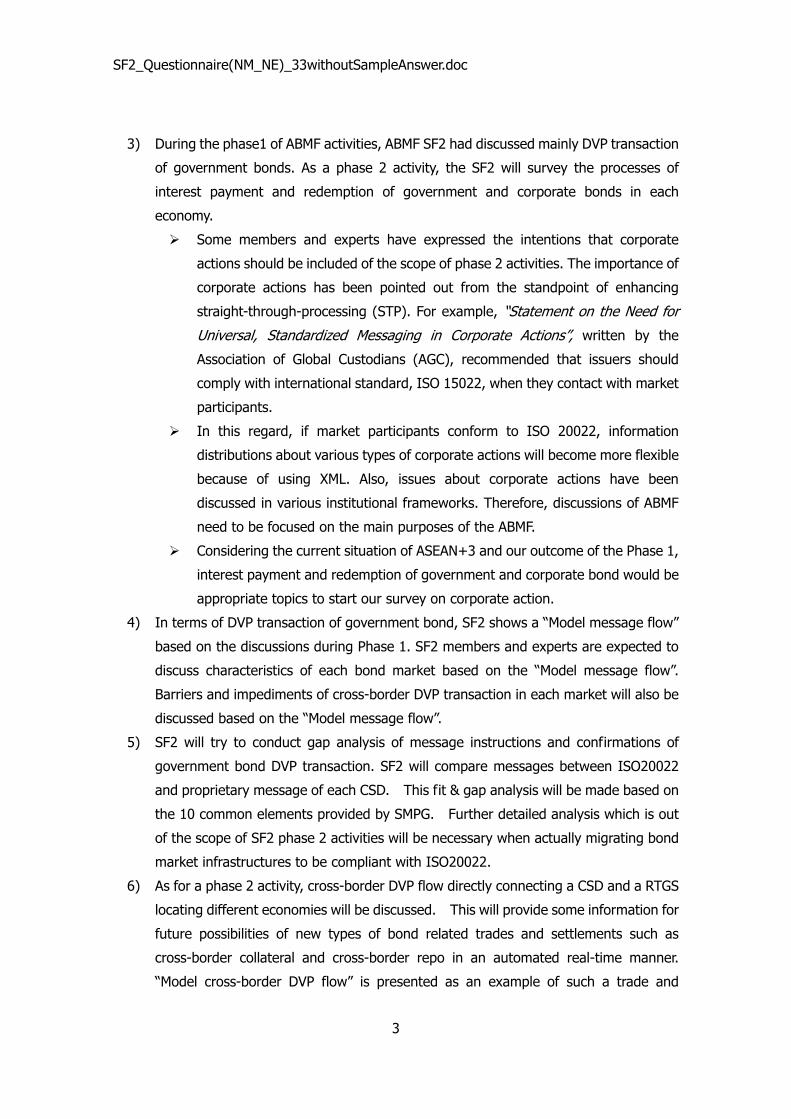

3) During the phase1 of ABMF activities, ABMF SF2 had discussed mainly DVP transaction

of government bonds. As a phase 2 activity, the SF2 will survey the processes of

interest payment and redemption of government and corporate bonds in each

economy.

Some members and experts have expressed the intentions that corporate

actions should be included of the scope of phase 2 activities. The importance of

corporate actions has been pointed out from the standpoint of enhancing

straight-through-processing (STP). For example, “Statement on the Need for

Universal, Standardized Messaging in Corporate Actions”, written by the

Association of Global Custodians (AGC), recommended that issuers should

comply with international standard, ISO 15022, when they contact with market

participants.

In this regard, if market participants conform to ISO 20022, information

distributions about various types of corporate actions will become more flexible

because of using XML. Also, issues about corporate actions have been

discussed in various institutional frameworks. Therefore, discussions of ABMF

need to be focused on the main purposes of the ABMF.

Considering the current situation of ASEAN+3 and our outcome of the Phase 1,

interest payment and redemption of government and corporate bond would be

appropriate topics to start our survey on corporate action.

4) In terms of DVP transaction of government bond, SF2 shows a “Model message flow”

based on the discussions during Phase 1. SF2 members and experts are expected to

discuss characteristics of each bond market based on the “Model message flow”.

Barriers and impediments of cross-border DVP transaction in each market will also be

discussed based on the “Model message flow”.

5) SF2 will try to conduct gap analysis of message instructions and confirmations of

government bond DVP transaction. SF2 will compare messages between ISO20022

and proprietary message of each CSD. This fit & gap analysis will be made based on

the 10 common elements provided by SMPG. Further detailed analysis which is out

of the scope of SF2 phase 2 activities will be necessary when actually migrating bond

market infrastructures to be compliant with ISO20022.

6) As for a phase 2 activity, cross-border DVP flow directly connecting a CSD and a RTGS

locating different economies will be discussed. This will provide some information for

future possibilities of new types of bond related trades and settlements such as

cross-border collateral and cross-border repo in an automated real-time manner.

“Model cross-border DVP flow” is presented as an example of such a trade and

3

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

settlement. SF2 members and experts are expected to point out some issues and

challenges related to market practices and standardization. Related cases are shown

in the Attachment.

As a result of phase1 survey, there are some extra transaction flows for foreign

exchange (FX) control in many countries as shown in the cross-border bond

transaction flows. This FX control barriers may be removed by direct connections

between CSD and RTGS systems utilizing cross-border DVP, cross-border

collateral, and cross-border repo. Also, by implementing such cross-border direct

connections, direct cross-border payments without relying on a vehicle currency

may be realized.

7) Regarding roadmap, SF2 will try to draw the roadmap. SF2 will rearrange the barriers,

which are pointed out from gap analysis of phase2 activity and “GoE Report of Task

Force 4” and will discuss how to overcome these barriers. Members and experts need

to argue the short, mid- and long term solutions for these barriers.

Practical issues such as settlement related barriers including market practices

regulated by SROs will be discussed mainly.

Laws and regulations, including tax, will be discussed as long as the issues are

related to message flows of government and corporate bonds.

8) SF2 will continue to follow up the phase 1 activities by refining and updating the

issues identified by GOE and ABMF SF2.

9) In terms of Legal Entity Identifier (LEI), SF2 will collect and update information for

SF2 members and experts to further discuss this issue and find out some direction in

each economy (possibly having some consensus in ASEAN+3).

10) In order to enhance cross-border bond transaction, transparency of market

information, such as listed bonds, limitation of non-residents, pricing and interest rate,

is important. SF2 will try to share information to discuss some infrastructures for data

collection and dissemination.

4

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

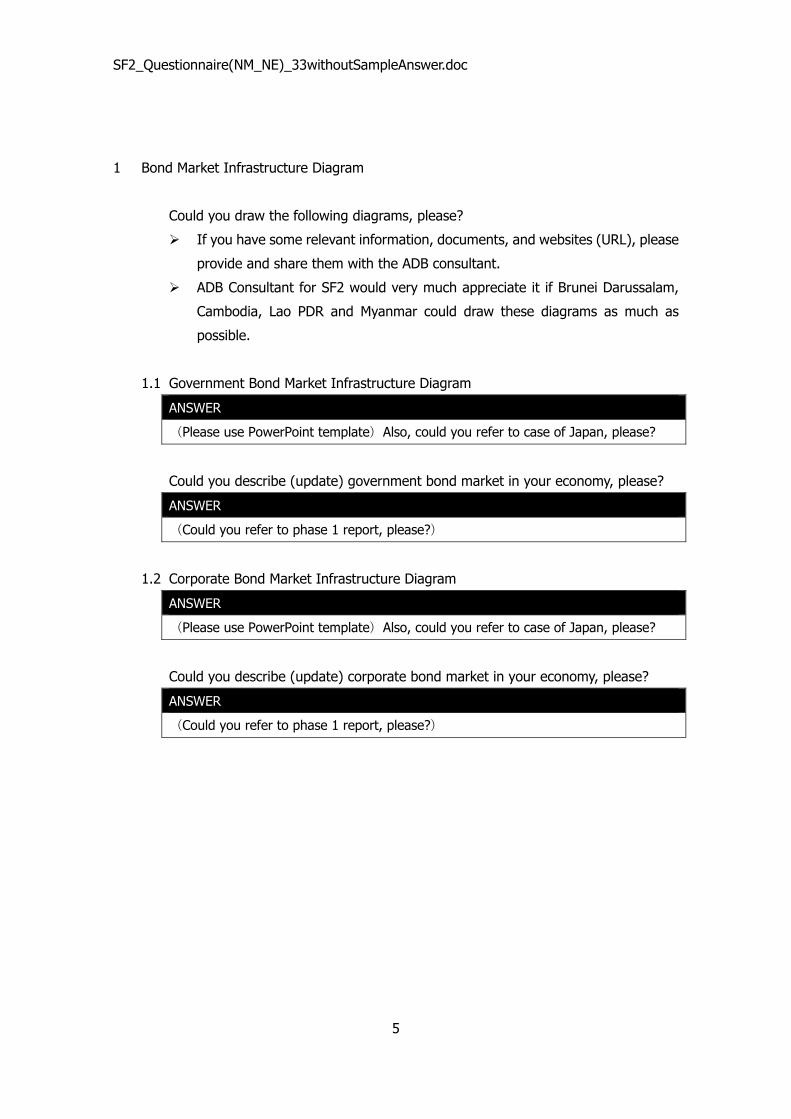

1 Bond Market Infrastructure Diagram

Could you draw the following diagrams, please?

If you have some relevant information, documents, and websites (URL), please

provide and share them with the ADB consultant.

ADB Consultant for SF2 would very much appreciate it if Brunei Darussalam,

Cambodia, Lao PDR and Myanmar could draw these diagrams as much as

possible.

1.1 Government Bond Market Infrastructure Diagram

ANSWER

(Please use PowerPoint template)Also, could you refer to case of Japan, please?

Could you describe (update) government bond market in your economy, please?

ANSWER

(Could you refer to phase 1 report, please?)

1.2 Corporate Bond Market Infrastructure Diagram

ANSWER

(Please use PowerPoint template)Also, could you refer to case of Japan, please?

Could you describe (update) corporate bond market in your economy, please?

ANSWER

(Could you refer to phase 1 report, please?)

5

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

2 Delivery-versus-Payment (DVP) flows of corporate bond in each market

Identifying DVP flow and procedure of corporate bond in each market to discuss

cross-border STP.

Draw the typical business flowchart of corporate bonds, domestic DVP transactions

and cross-border DVP transactions, based on the template of phase1 activities.

If you have some relevant information, documents and websites, please provide

and share with the ADB consultant.

ANSWER

(Please use PowerPoint template)When you draw them, please use sample

answers as a reference.

6

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

3 Interest payment & redemption

3.1 Interest payment of government bond

3.1.1 Draw the typical business flowchart for interest payment of typical

government bond to domestic investors.

ANSWER

(Please use PowerPoint template)

3.1.2 In case of investment by non-residents, are there any different procedures or

market practices in your economy comparing with domestic investor’s ones?

If yes, please write down details of differences.

ANSWER

3.1.3 Present issues and challenges including barriers, short-term solutions, and

medium- to long- term solutions.

ANSWER

3.2 Interest payment of corporate bond

3.2.1 Draw the typical business flowchart for interest payment of typical corporate

bond to domestic investors.

ANSWER

(Please use PowerPoint template)

3.2.2 In case of investment by non-residents, are there any different procedures or

market practices in your economy comparing with domestic investor’s ones?

If yes, please write down details of differences.

ANSWER

3.2.3 Present issues and challenges including barriers, short-term solutions, and

medium- to long- term solutions.

ANSWER

7

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

3.3 Redemption of government bond (with final interest payment)

3.3.1 Draw the typical business flowchart for redemption of typical government

bond to domestic investors. If redemption includes final interest payment,

please write the comments in the process definition.

ANSWER

(Please use PowerPoint template)

3.3.2 In case of investment by non-residents, are there any different procedures or

market practices in your economy comparing with domestic investor’s ones?

If yes, please write down details of differences.

ANSWER

3.3.3 Present issues and challenges including barriers, short-term solutions, and

medium- to long- term solutions.

ANSWER

3.4 Redemption of corporate bond (with final interest payment)

3.4.1 Draw the typical business flowchart for redemption of typical corporate bond

to domestic investors. If redemption includes final interest payment, please

write the comments in the process definition.

ANSWER

(Please use PowerPoint template)

3.4.2 In case of investment by non-residents, are there any different procedures or

market practices in your economy comparing with domestic investor’s ones?

If yes, please write down details of differences.

ANSWER

3.4.3 Present issues and challenges including barriers, short-term solutions, and

medium- to long- term solutions.

ANSWER

8

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

3.5 Other issues

If there is any issues and challenges including barriers, could you explain it

and provide us with short-term solutions, and medium- to long- term

solutions, please?

ANSWER

9

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

4 Fit and gap analysis for a channel using global custodians1 to settle cross-border trades

In ASEAN+3 most prevalent cross-border bond transactions are through global

custodians and settled as a DVP transaction in same market (country) domestically.

Therefore, cross-border line is located between global custodian and local custodian as

shown in Figure 4.1.

Purpose of fit & gap analysis of business flows and market practices is to identify gap of

DVP flow of government bond in each market with model cross-border DVP flow to

realize cross-border STP. In order to analyze, discuss the solutions against barriers and

to enhancement of cross-border DVP on each market, based on the phase1 survey of

DVP transaction flows. Output of analysis is to identify technical barriers including

market practices preventing the flow from cross-border STP.

4.1 Fit and gap analysis between typical cross-border DVP transaction and local

procedures

Based on the model cross-border DVP transaction flow (refer to Figure 4.1),

challenges and barriers in each market in terms of market practices and business

processes will be discussed from cross-border STP perspective.

Could you focus on new issues and issues related to each infrastructure,

please?

4.1.1 OTC Market (including exchange market) or trading system

A. Do you have a trading system for OTC Market handling cross-border

transactions in your economy? If yes, could you describe it, please?

What is the name of the system? Who developed the system? What are

specific characteristics (differences) of the system from conventional

and/or standard processes? When the system started production

operation? What are current challenges?

ANSWER

1 “Channel using global custodians” means that settlement processes go through not only

global custodians but also local custodians in each economy instead of directly connecting CSD with ICSD or other CSDs.

10

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

B. How you process allocation between investors and brokers for cross-border

bond transactions? What are challenges for cross-border transactions?

ANSWER

C. Do you have SSI (standing settlement instruction) database? If yes, who is

maintaining it? Also, how it is maintained? What are challenges from

cross-border transaction perspective?

ANSWER

4.1.2 Trade and post-trade Matching

Do you have trade and/or post-trade matching system other than trading

system? If yes, what is the name of the system? Also, could you

describe the system, please? Who developed the system? What are specific

characteristics (differences) of the system from conventional and/or

standard processes? When the system started production operation? What

are current challenges?

In general, when trading system is already implemented,

trade/post-trade matching is one of the functions of the trading

system.

ANSWER

4.1.3 Pre-Settlement Matching

Are there any system infrastructures for pre-settlement matching in your

economy? If yes, what is the name of the system? Also, could you describe

the system, please? When pre-settlement matching is carried out? For what

purposes the pre-settlement matching needs to be done? Do you have any

other alternative measure to conduct pre-settlement matching such as using

future date data entry of book-entry system? If there is no pre-settlement

matching system infrastructure, how pre-settlement matching is conducted

11

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

(telephone, facsimile, or e-mail)?

ANSWER

4.1.4 CSD (book-entry system)

What are the characteristics and differences of practices from other CSD

systems?

During the phase 1 survey, CSDs and its book-entry systems were mainly

discussed. 10 economies have book-entry systems.

ANSWER

4.1.5 Central Bank (RTGS system)

What are the characteristics and differences of practices from other RTGS

systems?

During the phase 1 survey, central banks and its RTGS systems were

mainly discussed. 9 economies have RTGS systems.

ANSWER

4.1.6 CCP

Are there any system infrastructures of CCP in your economy? If yes, please

describe the name of system(s) and explain the details of the system. In

addition, are there any intentions to apply the clearing procedures to the

non-residential transaction?

ANSWER

4.2 Details of message flows (refer to Figure 4.1)

Please make specifications of each message listed below.

C.1 / C.2 Order and Affirmation (between “OTC Market or Trading System”

12

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

and “Investment Manager and International Broker ”)

Answer

Manual operation or system interface

Type of line(s)

Protocol(s)

Interface(s)

Message Format(s)

C.3-2 Instruction (between Post-trade Matching system and pre-settlement

matching system)

Answer

Manual operation or system interface

Type of line(s)

Protocol(s)

Interface(s)

Message Format(s)

C.7 Instruction and Matching status

Answer

Manual operation or system interface

Type of line(s)

Protocol(s)

Interface(s)

Message Format(s)

C9-2.Instruction (From Pre-settlement Matching)

Answer

Manual operation or system interface

Type of line(s)

Protocol(s)

Interface(s)

Message Format(s)

C10.Instruction and Settlement Confirmation

Answer

13

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

Manual operation or system interface

Type of line(s)

Protocol(s)

Interface(s)

Message Format(s)

C11.Settelemnt Data (DVP)

Answer

Manual operation or system interface

Type of line(s)

Protocol(s)

Interface(s)

Message Format(s)

C13. Settlement Confirmation (Cash)

Answer

Manual operation or system interface

Type of line(s)

Protocol(s)

Interface(s)

Message Format(s)

S2.Instruction and Settlement Data

Answer

Manual operation or system interface

Type of line(s)

Protocol(s)

Interface(s)

Message Format(s)

4.3 Network between market infrastructures and the infrastructures and participants

Could you discuss how to connect each other by referring to the “Figure 4.4

Network Between Market Participants”, “Table 4.1 Settlement Instructions

and Confirmation of Bond and Cash”, and “Table 4.2 Protocols and Message

14

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

Formats in ASEAN+3 Bond Markets” of ABMF SF2 Report Part 1, please?

ANSWER

4.4 Market practices on government bond settlement

On the basis of assuming the observance of the government bond trade and

settlement related regulations, practices that the market participants must follow

to ensure a fair and efficient trades, to reduce settlement risks in changing

environment, and to facilitate smooth settlements in government securities

transactions are to be compared market by market.

Harmonization of market practices which are not stipulated by laws or acts

but agreed as rules by stakeholders such as SRO members will be an

important issue for cross-border STP.

4.4.1 Limitation on size of settlements

The upper limit on size of bond settlements

Each market participant should set an upper limit on size of settlements

processed in order to curb the daytime accumulation of settlements

outstanding and to resolve the delay of settlements by reducing the

amounts of government securities and funds necessary per settlement.

Do you have an upper limit on size of bond settlement? If yes, what is the size

and reason of the limit? How to handle transactions with face value exceeding

the upper limit? Do you have exceptions to the upper limit on size of

settlements? If yes, what kinds of transactions are exceptions?

ANSWER

4.4.2 Establishment of Cut-off time and Reversal time

A. Establishment of Cut-off time

For the purpose of recognizing Fails etc. aimed at completing all

settlements on the day, Cut-off time shall be the deadline decided by

market participants for government securities settlements prior to the

closing time of book-entry system of the CSD.

15

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

Do you have a cut-off time in your market? If yes, what time is cut-off time in

your market? What is the definition of cut-off time? Could you explain it,

please?

ANSWER

B. Establishment of Reversal time

Reversal time is the period during which parties executing the relevant

transaction can resolve fails if they have agreed to extend the delivery

deadline over Cut-off time, and correct errors in the case of any errors in

settlement procedures.

Do you have reversal time in your market? If yes, what time is reversal time?

What is the definition of reversal time? Could you explain it, please?

ANSWER

4.4.3 Guidelines for activities of market participants on the settlement day

Do you have any other guidelines and/or market practices for market

participants to observe? If yes, could you explain them, please?

ANSWER

4.4.4 Guidelines concerning Fails

A. Definition of a Fail

In general a fail means a situation whereby a party receiving government

securities has not received delivery of the relevant securities from the

delivering party after the end of the scheduled settlement date.

What is the definition of Fail in your market? What is the concept such as

good-faith efforts to resolve Fails? What are conditions to Guidelines

concerning Fails?

ANSWER

B. Guidelines related to Fails

16

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

Do you have guidelines related to Fails? If yes, what are guidelines related to

Fails?

ANSWER

C. Cost of Fails

Could you explain your policy regarding costs incurred under Fails?

ANSWER

D. Fails Charges

Could you explain how you handle Fails Charges, please?

ANSWER

E. Other issues related to Fails

ANSWER

4.4.5 Guidelines concerning bilateral netting

Do you have bilateral netting scheme? If yes, what is the netting scheme such

as netting structure, face value applicable to netting, settlement type (DVP or

not), contract time of original transactions (by what time), transaction types,

mode of possession (only book-entry transfer government securities),

transaction accounts applicable to netting, pairing method, effective timing of

netting in the case of the same settlement amount, and the account for fund

settlement?

ANSWER

What are operational procedures in netting such as pairing instructions,

exchange of comparison notices, deadline for comparisons, method to send

comparison notices, principle for sending of comparison notices, notice of

objection, and sections in charge of comparison?

ANSWER

17

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

Do you have prior confirmation, prior notice, and their relation with the

comparison notice?

ANSWER

4.5 Any other market practices

Any other market practices related to DVP transaction flows may be discussed. If

you have any ideas, please mention them.

ANSWER

18

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

5 Fit and gap analysis for government bond DVP transaction

Purpose of Fit & gap analysis of message items is to identify gap of government bond

settlement instruction (sese 023.001.01 of ISO 20022 and MT541,MT543 of ISO15022)

and confirmation (sese 025.001.01 of ISO 20022 and MT545, MT547 of ISO15022).

Comparing the messages between international standards and local proprietary, SF2 will

provide information about similarities and uniqueness of each market. In some cases,

market practices in ASEAN+3 may be better than that in other regions outside

ASEAN+3. In such a case, ASEAN+3 may contribute to forming international standard

positively though ABMF activities. Also, when each economy will develop new book

entry system complying with ISO20022, this analysis may help creation of requirement

definition document of new system.

Regarding ISO15022, following sites are referred:

http://www.iso15022.org/UHB/uhb2006/finmt543.htm

http://www.iso15022.org/UHB/UHB2005/finmt545.htm

Regarding ISO20022, following site is referred:

http://www.iso20022.org/documents/general/Securities_SnR_Maintenance_2011.zip

Goals of fit and gap analysis are to identify message items in each market different from

international standard. Dissolution of gaps will lead to enhance the interoperability and

promote straight-through-processing of cross-border bond transaction.

The scope of fit and gap analysis is government bond messages only. If there are some

CSDs of government bond, please mention in respective CSD.

5.1 Fit and gap analysis of 10 Common Elements for securities settlement instruction

between ISO 20022 and local practices in terms of business element name,

definition, format, multiplicity, optional or mandatory and others. 10 Common

Elements are listed below.

Elements of answer:

Business Element Name

Please specify the element name of each CSD in accordance with each

19

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

ISO20022 message item

Definition & Explanation

Please describe the definition and explanation of business elements in

each CSD

Message Format

Please answer the massage format in your market, ISO20022 compliant

or proprietary. If it’s ISO20022 compliant, please describe further details

about tag structure.

Element Format

Please describe the format of each message item, text or number types

and length (minimum and maximum) of each message item.

Multiplicity

Please check each message item, single or multiple.

Optional or mandatory

Please check each message item, optional or mandatory.

Others

Other relevant information, if any.

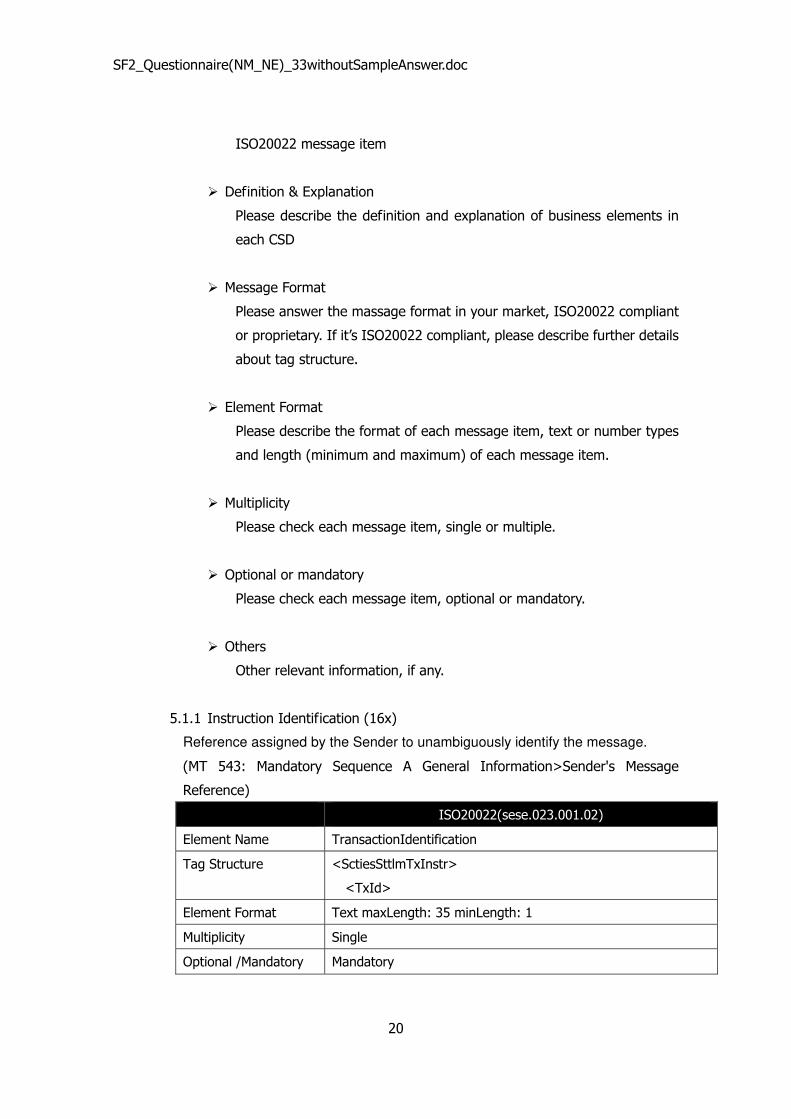

5.1.1 Instruction Identification (16x)

Reference assigned by the Sender to unambiguously identify the message.

(MT 543: Mandatory Sequence A General Information>Sender's Message

Reference)

ISO20022(sese.023.001.02)

Element Name TransactionIdentification

Tag Structure <SctiesSttlmTxInstr>

<TxId>

Element Format Text maxLength: 35 minLength: 1

Multiplicity Single

Optional /Mandatory Mandatory

20

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

Answer

Element Name

Definition&Explanation

Message Format

Element Format

Multiplicity

Optional /Mandatory

5.1.2 Trade Date (Date/Time)

Date/time at which the trade was executed.

(MT 543: Mandatory Sequence B Trade Details> Trade Date/Time)

ISO20022(sese.023.001.02)

Element Name TradeDetails

>TradeDate

Tag Structure <SctiesSttlmTxInstr>

<TradDtls>

<TradDt>

<Dt>/<DtTm>

Element Format ISODate:YYYY-MM-DD

ISODateTime: UTC time format (YYYY-MMDDThh:mm:ss.sssZ),

local time with UTC offset format (YYYY-MM-DDThh:mm:ss.sss

+/-hh:mm), or local time format (YYYY-MM-DDThh:mm:ss.sss)

Multiplicity Single

Optional /Mandatory Optional

Answer

Element Name

Definition&Explanation

Message Format

Element Format

Multiplicity

Optional /Mandatory

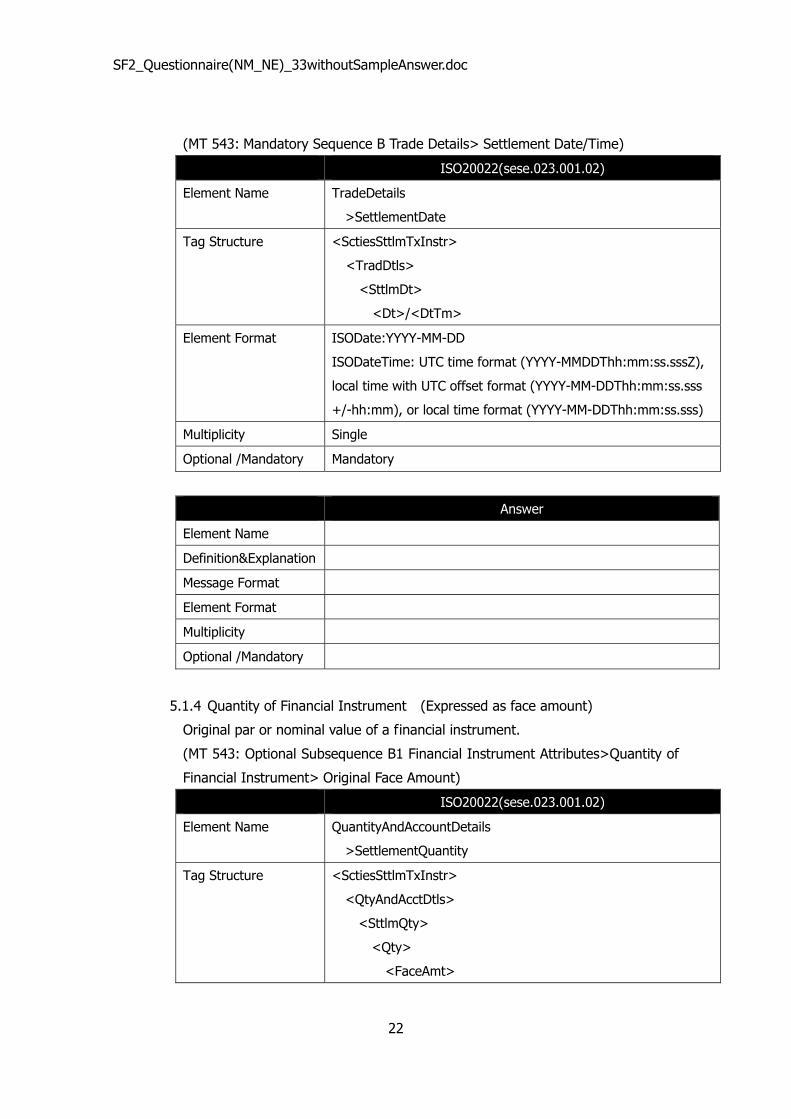

5.1.3 Settlement Date (Date/Time)

Date/time at which the financial instruments are to be delivered or received.

21

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

(MT 543: Mandatory Sequence B Trade Details> Settlement Date/Time)

ISO20022(sese.023.001.02)

Element Name TradeDetails

>SettlementDate

Tag Structure <SctiesSttlmTxInstr>

<TradDtls>

<SttlmDt>

<Dt>/<DtTm>

Element Format ISODate:YYYY-MM-DD

ISODateTime: UTC time format (YYYY-MMDDThh:mm:ss.sssZ),

local time with UTC offset format (YYYY-MM-DDThh:mm:ss.sss

+/-hh:mm), or local time format (YYYY-MM-DDThh:mm:ss.sss)

Multiplicity Single

Optional /Mandatory Mandatory

Answer

Element Name

Definition&Explanation

Message Format

Element Format

Multiplicity

Optional /Mandatory

5.1.4 Quantity of Financial Instrument (Expressed as face amount)

Original par or nominal value of a financial instrument.

(MT 543: Optional Subsequence B1 Financial Instrument Attributes>Quantity of

Financial Instrument> Original Face Amount)

ISO20022(sese.023.001.02)

Element Name QuantityAndAccountDetails

>SettlementQuantity

Tag Structure <SctiesSttlmTxInstr>

<QtyAndAcctDtls>

<SttlmQty>

<Qty>

<FaceAmt>

22

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

Element Format fractionDigits: 5 minInclusive: 0 totalDigits: 18

Multiplicity Single

Optional /Mandatory Mandatory

Answer

Element Name

Definition&Explanation

Message Format

Element Format

Multiplicity

Optional /Mandatory

5.1.5 Financial Instrument (International Securities Identification Number: ISIN)

This field identifies the financial instrument. (MT 543: Optional Subsequence B1

Financial Instrument Attributes>Identification of the Financial Instrument)

ISO20022(sese.023.001.02)

Element Name FinancialInstrumentIdentification>ISIN

Tag Structure <SctiesSttlmTxInstr>

<FinInstrmId>

<ISIN>

Element Format [A-Z0-9]{12,12}

Multiplicity Single

Optional /Mandatory Mandatory

Answer

Element Name

Definition&Explanation

Message Format

Element Format

Multiplicity

Optional /Mandatory

5.1.6 Settlement Amount (Currency and amount)

Total amount of money to be paid or received in exchange for the financial

instrument (MT 543: Repetitive Mandatory Sequence C Financial

23

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

Instrument/Account>Settlement Amount)

ISO20022(sese.023.001.02)

Element Name Settlement Amount

>Amount

Tag Structure <SctiesSttlmTxInstr>

<SttlmAmt>

<Amt>

Element Format ActiveCurrencyAndAmount

fractionDigits: 5 minInclusive: 0 totalDigits: 18

ActiveCurrencyCode

[A-Z]{3,3}

Multiplicity Single

Optional /Mandatory Mandatory

Answer

Element Name

Definition&Explanation

Message Format

Element Format

Multiplicity

Optional /Mandatory

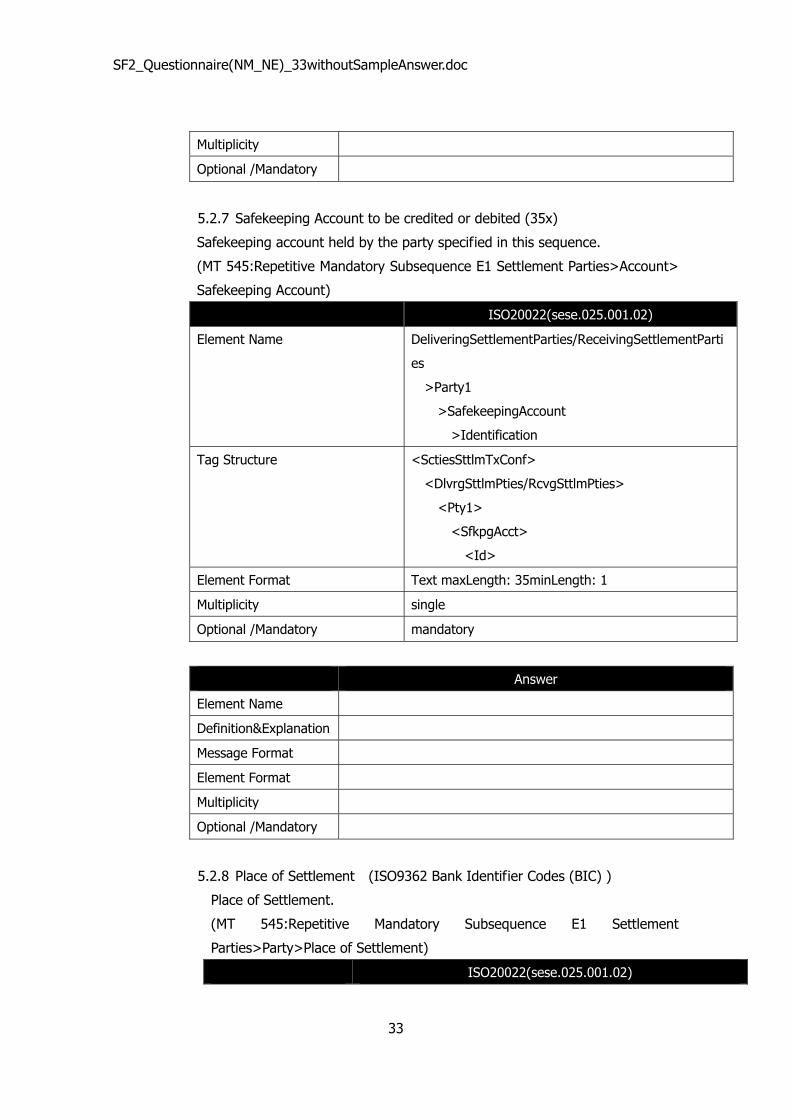

5.1.7 Safekeeping Account to be credited or debited (35x)

Account where financial instruments are maintained.

(MT 543:Repetitive Mandatory Sequence C Financial

Instrument/Account>Account >Safekeeping Account)

ISO20022(sese.023.001.02)

Element Name DeliveringSettlementParties/ReceivingSettlementParties

>Party1

>SafekeepingAccount

>Identification

Tag Structure <SctiesSttlmTxInstr>

<DlvrgSttlmPties/RcvgSttlmPties>

<Pty1>

<SfkpgAcct>

24

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

<Id>

Element Format Text maxLength: 35 minLength: 1

Multiplicity Single

Optional /Mandatory Mandatory

Answer

Element Name

Definition&Explanation

Message Format

Element Format

Multiplicity

Optional /Mandatory

5.1.8 Place of Settlement (ISO9362 Bank Identifier Codes (BIC) )

Place of settlement. (MT 543:Repetitive Mandatory Subsequence E1 Settlement

Parties> Party> Place of Settlement)

ISO20022(sese.023.001.02)

Element Name StandingSettlementInstructionDetails

> Delivering/ Receiving SettlementParties

>Depository

> Identification

> AnyBIC

Tag Structure <SctiesSttlmTxInstr>

<StgSttlmInstrDtls>

<DlvrgSttlmPties/ RcvgSttlmPties >

<Dpstry>

<Id>

<AnyBIC>

Element Format [A-Z]{6,6}[A-Z2-9][A-NP-Z0-9]([A-Z0-9]{3,3}){0,1}

Multiplicity Single

Optional /Mandatory Mandatory

Answer

Element Name

Definition&Explanation

25

SF2_Questionnaire(NM_NE)_33withoutSampleAnswer.doc

Message Format

Element Format

Multiplicity

Optional /Mandatory

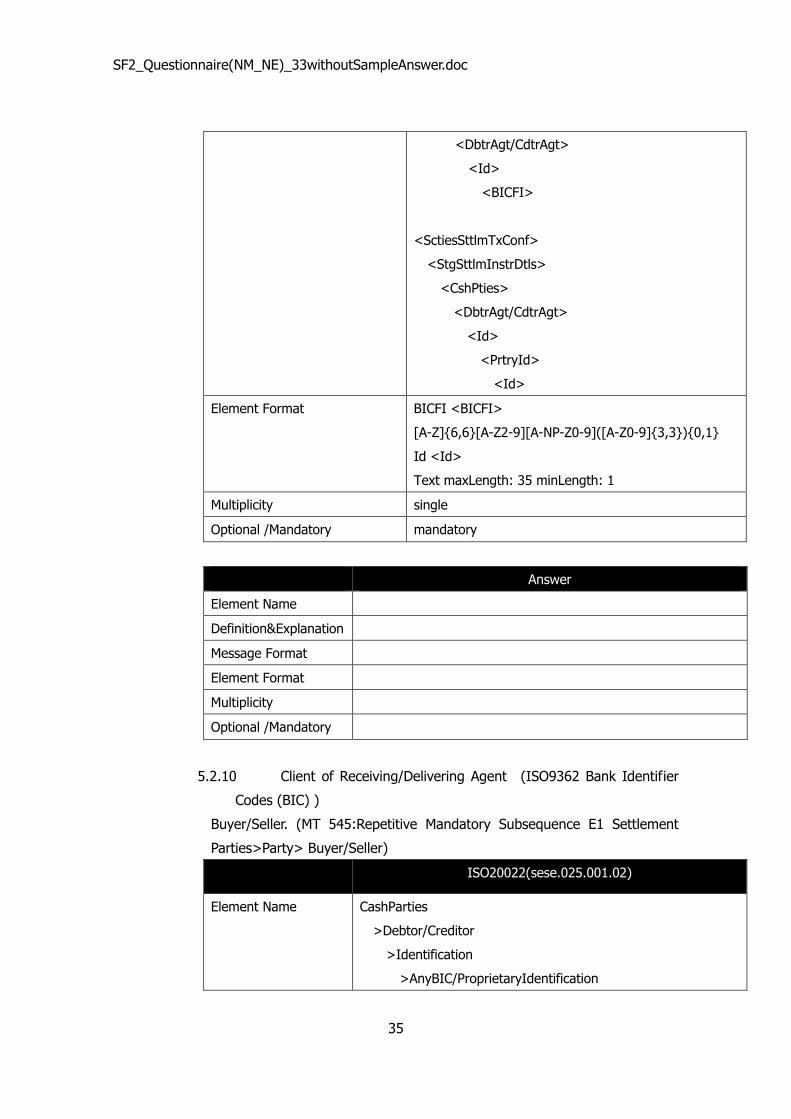

5.1.9 Receiving/Delivering Agent (ISO9362 Bank Identifier Codes (BIC) or CSD

Local Code)

Receiving/Delivering party that interacts with the Place of Settlement.

(MT 543: Repetitive Mandatory Subsequence E1 Settlement

Parties>Receiving/Delivering Agent)

ISO20022(sese.023.001.02)