70-397 venture finance fall 2002 slide 1 class 7 notes due diligence part 1 © andrew w. hannah

Post on 20-Dec-2015

213 views

TRANSCRIPT

70-397 Venture Finance Fall 2002

Slide 1

Class 7 Notes

Due Diligence Part 1

© Andrew W. Hannah

70-397 Venture Finance Fall 2002

Slide 2

Agenda

• Homework due tonight• Teams email – did you send it?• Confidentiality Agreement – did you sign it?• Gurus in the Garage• Question Card C

• Midterm Evaluations• Diligence Overview

• Harvard Model• Market, Competition, and Comparables

• Gurus in the Garage

© Andrew W. Hannah

70-397 Venture Finance Fall 2002

Slide 3

Iraq Revisited

More information?What is Bush doing?

While England Slept revisited?

© Andrew W. Hannah

70-397 Venture Finance Fall 2002

Slide 4

Diligence

Defining Diligence,Frameworks and Performing Diligence,

Issues in Diligence

© Andrew W. Hannah and William Hulley

70-397 Venture Finance Fall 2002

Slide 5

Definition of Diligence

• Macro: Researching a company to determine:• Whether to commit to making an investment• The size of the commitment• The terms and conditions of the commitment

• Micro: Researching a company to determine:• Risks and opportunities• Unknowns• Future needs of time, people, money• Metrics for measuring success

© Andrew W. Hannah and William Hulley

70-397 Venture Finance Fall 2002

Slide 6

What Makes Doable Diligence?

• Do you have access to the right resources?• Primary research• Secondary research• Leveraging the company

• Do you have the right expertise?• Investment Model revisited• What deals have you done?

© Andrew W. Hannah and William Hulley

70-397 Venture Finance Fall 2002

Slide 7

What Makes Good Diligence?

• Addresses a single point of the decision

• In a timely and economic fashion

• And provides a clear answer

© William Hulley

70-397 Venture Finance Fall 2002

Slide 8

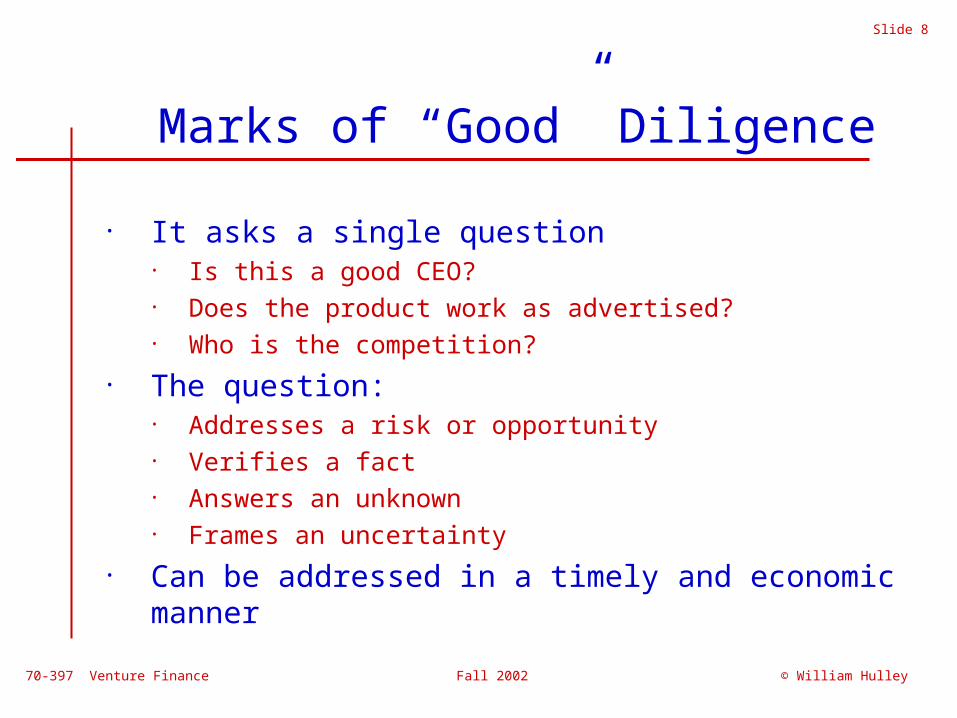

Marks of “Good” Diligence

• It asks a single question• Is this a good CEO?• Does the product work as advertised?• Who is the competition?

• The question: • Addresses a risk or opportunity • Verifies a fact • Answers an unknown • Frames an uncertainty

• Can be addressed in a timely and economic manner

© William Hulley

70-397 Venture Finance Fall 2002

Slide 9

Definitions of a Diligence Framework

• A target list of areas to evaluate in considering any investment opportunity

• A formal description of the rules used to judge any investment opportunity

• An attempt to rationalize ad hoc decisions about an investment opportunity

© William Hulley

70-397 Venture Finance Fall 2002

Slide 10

Why Create a Framework?

• Know what questions to ask on any deal

• Insure deal to deal evaluation consistency

• Set expectations, time frames and goals

• Limit emotion, politics, selling

• Understand the post-deal milestones, effort

© William Hulley

70-397 Venture Finance Fall 2002

Slide 11

The Harvard Framework

© Andrew W. Hannah

Business Opportunity

People

Deal

Context

70-397 Venture Finance Fall 2002

Slide 12

People

• The Entrepreneur• “An A-quality [person] with a B-quality project, but

not the other way around.” General Georges Doroit• With limited resources, a major mistake will kill the

company• Honesty, integrity and reliability are sacrosanct

• The Management Team• Relevant skill set• Commitment

• The Stakeholders: who is around the deal?

© Andrew W. Hannah

70-397 Venture Finance Fall 2002

Slide 13

The Business Opportunity• The Model

• Short version of how the business will make money• Why will customers part with their cash?• Market size, value proposition, profit potential, sustainable

advantage• Customer: benefit vs. cost• Size:

• What is the upside?• Winning investors don’t do deals that lack the potential for

substantial returns because the risk is losing everything is high• Scale and/or scope

• Timing• Are the customers ready?• What are the customers doing now and what may come along

later?

© Andrew W. Hannah

70-397 Venture Finance Fall 2002

Slide 14

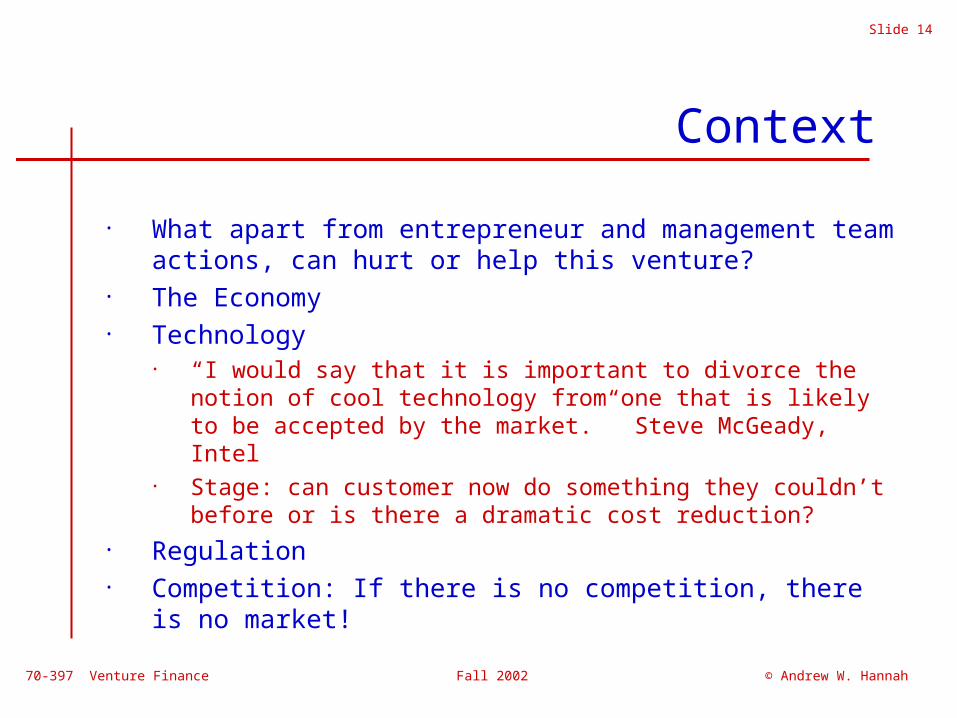

Context

• What apart from entrepreneur and management team actions, can hurt or help this venture?

• The Economy• Technology

• “I would say that it is important to divorce the notion of cool technology from one that is likely to be accepted by the market.” Steve McGeady, Intel

• Stage: can customer now do something they couldn’t before or is there a dramatic cost reduction?

• Regulation• Competition: If there is no competition, there is no

market!

© Andrew W. Hannah

70-397 Venture Finance Fall 2002

Slide 15

Evaluating the Deal

• People• Stakeholders• The team• Entrepreneur

• Business Opportunity• Size• The model• Customer• Timing

• Deal• Price • Structure

• Context• The economy• Technology• Regulation• Competition

The evaluation is the great time killer: 40 +hours

© Andrew W. Hannah

How would you rank order these?

70-397 Venture Finance Fall 2002

Slide 16

Understanding Risk

• Technological risk• Product/service risk• Market risk• Sales risk• Competitive risk• Financing risk• Operating risk• People risk

© Andrew W. Hannah

70-397 Venture Finance Fall 2002

Slide 17

Summary

• Investment decisions come in two flavors• The Macro - Should I, how much, what terms?• The Micro - What are the risks, opportunities, unknowns?

• Good diligence • Addresses a single point of the investment decision • In a timely and economic fashion• And provides a clear answer

• Good frameworks • Are useful across many deals• Clearly define what they do• Demonstrate their value at the micro and macro level

• Understand the risks

© Andrew W. Hannah and William Hulley

70-397 Venture Finance Fall 2002

Slide 18

Market Diligence

• Why does it matter?• Revenue potential

• Units and pricing matter• Market growth and shrinkage matter

• What are the supporting questions?• Who is the customer?• How many are there?• How much money do they spend on products like

this?• What else competes for that budget?

© Andrew W. Hannah and William Hulley

70-397 Venture Finance Fall 2002

Slide 19

Market Diligence (Cont.)

• Identify Sources of Information• Company information• Competitors product and company information• Analysts• Magazine• Regulatory filings• Trade associations• Customers

• Define format for reporting (see handout)• Question• Source – who, what, when• Answer

© Andrew W. Hannah and William Hulley

70-397 Venture Finance Fall 2002

Slide 20

Gurus in the Garage Discussion

• What are the themes?• Can the entrepreneur do it alone?• What does that say about how you perform due

diligence on the entrepreneur?• What does that say about geography?• What does that say about industry clustering?

• Can mentor capitalists be harmful?• What is the most important role of a mentor

capitalist?• Is the Valley the “one and only”

• What could kill the valley?

© Andrew W. Hannah

70-397 Venture Finance Fall 2002

Slide 21

Next Week

• Venture Capitalist on Due Diligence• Craig Gomulka, Draper Triangle • How VC’s do due diligence

• Diligence Card “A”• In Three Weeks (moved from 10/22 to 10/29)

• Diligence Card “B” – comparables• Read the PolyTronics business plan• WA: 114 – 141 (this is different than the

syllabus)

© Andrew W. Hannah