7-1 intermediate accounting james d. stice earl k. stice © 2012 cengage learning powerpoint...

TRANSCRIPT

7-1

Intermediate Accounting

James D. Stice Earl K. Stice

© 2012 Cengage Learning

PowerPoint presented by Douglas Cloud Professor Emeritus of Accounting, Pepperdine University

The Revenue/Receivable/Cash Cycle

Chapter 7Chapter 7

18th Edition

7-2

The Operating Cycle of a Business

• The normal operating cycle of a business involves purchasing inventory (using either cash or credit), which is then sold, often on account.

• Once the receivable is collected, the cycle begins again.

• The normal operating cycle is the lifeblood of any business enterprise.

(continued)

7-3

• The recognition of revenue is generally related to the recognition of accounts receivable.

• Revenues are generally recorded when the earning process is complete and a valid promise of payment (or payment itself) is received.

• A receivable arising from the sale of goods is generally recognized when the title to the goods passes to a bona fide buyer.

(continued)

The Operating Cycle of a Business

7-4

The entry for recognizing revenue and a receivable from the sale of goods or services is as follows:Accounts Receivable xx

Sales xx

(continued)

The Operating Cycle of a Business

7-5

When the amount is collected, Accounts Receivable is credited and Cash is debited as follows:Cash xx

Accounts Receivable xx

The Operating Cycle of a Business

7-6

Types of Receivables

• Trade receivables, generally most significant category of receivables, result from the normal activities of a business.

• Trade receivables may be evidenced by a formal written promise to pay and classified as notes receivables.

In its broadest sense, the term In its broadest sense, the term receivablereceivable is applicable to all claims against others for is applicable to all claims against others for

money, goods, or services.money, goods, or services.

In its broadest sense, the term In its broadest sense, the term receivablereceivable is applicable to all claims against others for is applicable to all claims against others for

money, goods, or services.money, goods, or services.

7-7

Nontrade Receivables

Nontrade receivables include all other types of receivables. They arise from a variety of transactions, such as:1) The sale of securities or property other

than inventory2) Deposits to guarantee contract

performance or expense payment

3) Claims for rebates and tax refunds

4) Dividends and interest receivable

7-8

Sales Returns and Allowances

Red sweaters costing $600 are sold to a customer for $1,000. The customer calls and states that green sweaters were ordered and should have been shipped. Rather than return the sweaters, the customer agrees to keep the sweaters for a reduction in price—an allowance of $200. The return is recorded as follows:Sales Returns and Allowances 200

Accounts Receivable 200

(continued)

7-9

Suppose that instead of an allowance, the customer elects to return the sweaters. The return requires two entries.

Sales Returns and Allowances 1,000Accounts Receivable 1,000

Inventory 600Cost of Goods Sold 600

The first entry recognizes the return and the reduction of the customer’s account. The second entry reports that the sweaters are now in inventory.

Sales Returns and Allowances

7-10

Accounting for Bad Debts

• Bad debts occur when customers do not pay for items or services purchased on credit; thus, bad debts are uncollectible accounts receivable.

• Bad Debt Expense is reported as a selling or general and administrative expense.

• Accounts Receivable are reported on the balance sheet at net realizable value; that is, the expected cash value and not the present value.

(continued)

7-11

Uncollectible Accounts Receivable—Direct Write-Off Method

When a receivable proves to be uncollectible, the direct write-off method requires the following entry:

Bad Debt Expense xxxAccounts Receivable xxx

(continued)

7-12

• The use of the direct write-off method is not allowed under GAAP because it does not provide for the matching of expenses with current revenues and does not report receivables at their net realizable value.

• The direct write-off method is often used by small businesses because of its simplicity.

Uncollectible Accounts Receivable—Direct Write-Off Method

7-13

• Using the allowance method, which is required by GAAP, the amount of receivables that are not collectible has to be estimated.

Uncollectible Account Receivables—Allowance Method

7-14

• A typical entry to recognize bad debt expense, normally made as an end-of-the-period adjustment is as follows:

Bad Debt Expense xxAllowance for Bad Debts xx

To record estimated uncollectibleaccounts receivable for the period.

• Bad Debt Expense is reported as a selling or general and administrative expense.

(continued)

Establishing an Allowance for Bad Debts

7-15

• When positive evidence is available concerning the partial or complete worthlessness of an account, the account is written off using the following entry:

Note:Note: Bad Debt Expense Bad Debt Expenseisis notnot debited. debited.

Note:Note: Bad Debt Expense Bad Debt Expenseisis notnot debited. debited.

Writing off an Uncollectible Accounting Under the Allowance Method

Allowance for Bad Debts xxAccounts Receivable xx

To record the write-off of anuncollectible account.

7-16

Occasionally, an account that has been written off is unexpectedly collected. Assume a $1,500 account previously written off is collected. Two entries are required as shown next: the first to reverse the write-off entry; the second to record receipt of the cash.

Collecting a Written-off Account Under the Allowance Method

(continued)

7-17

Accounts Receivable 1,500 Allowance for Bad Debts 1,500

To reverse the entry made to write off the account.

Cash 1,500 Accounts Receivable 1,500

To record collection of the account.

The first entry is to reverse the write-off entry:

The second entry is to record receipt of the cash:

Collecting a Written-off Account Under the Allowance Method

7-18

Allowance for Bad Debts

• Allowance for Bad Debts is a contra-asset account that is subtracted from Accounts Receivable on the balance sheet.

• The actual write-off entry for $1,500 does not reduce net receivables, as shown below:

Accts. receivable $300,000 Accts. receivable $298,500

Less: Allowance for Less: Allowance forbad debts 15,000 bad debts 13,500

Net receivables $285,000 Net receivables$285,000

7-19

Estimating Uncollectibles Based on Percentage of Sales

When basing estimated uncollectibles on sales for the period, it is preferable to apply the percentage to credit sales. However, the percentage is frequently applied to total sales to avoid having to maintain separate records for cash and credit sales.

(continued)

7-20

• If 2% of sales is considered doubtful in terms of collection and sales for the period are $100,000, the charge for Bad Debt Expense would be 2% of the current period’s sales, or $2,000.

• The existing balance in Allowance for Bad Debts is ignored.

Bad Debt Expense 2,000Allowance for Bad Debts 2,000

To record estimated bad debt expensefor the period ($100,000 0.02 = $2,000).

Estimating Uncollectibles Based on Percentage of Sales

(continued)

7-21

If total accounts receivable for Lamberson Company are $50,000 and it is estimated that 3% of those accounts will be uncollectible, the allowance account needs to have a balance of $1,500 ($50,000 0.03). If the allowance account already has a $600 credit balance, the current-period adjusting entry is as follows:

Bad Debt Expense 900Allowance for Bad Debts 900

To record estimated bad debt expense for the period ($1,500 required balance $600 current balance = $900 adjustment).

Estimating Uncollectibles Based on A/R Balance

7-22

Aging Receivables

• The most commonly used method for establishing an allowance based on outstanding receivables involves aging receivables.

• Individual accounts are analyzed to determine those not yet due and those past due.

7-23

Aging Receivables

The amount derived from aging, $2,870, is the desired balance of the allowance account after the adjusting entry. If Allowance for Bad Debts already has a credit balance of $620 before adjustment, the following entry is needed:

Bad Debt Expense 2,250Allowance for Bad Debts 2,250

To record estimated bad debt expense for the period ($2,870 required balance $620 current balance = $2,250 adjustment)

7-24

Corrections to Allowance for Bad Debts

• If the allowance provisions are too large or small, a correction in the allowance as well as a change in the rate or in the method employed will be needed (if the amount is material).

• The effect of this change in accounting estimate would be reported in the current and future periods as an ordinary item on the income statement, usually as an addition or subtraction from Bad Debt Expense.

7-25

Helpful Reminder

• When bad debts are estimated based on a percentage of sales, bad debt expense is computed and the balance of the allowance account is then determined.

• When you are using the percentage-of-receivables method, the balance in the allowance account is computed, and then the amount of bad debt expense for the period is determined.

7-26

Warranties for Service or Replacement

• Many companies agree to provide free services on units failing to perform satisfactorily or to replace defective goods. These agreements are referred to as warranties.

• When warranties are priced separately from the product, the revenue for the sale should be divided between the product and the warranty service.

(continued)

7-27

MJW Video & Sound sells DVD players with a 2-year warranty. Past experience indicates that 10% of all systems sold will need repairs in the first year, and 20% will need repairs in the second year. The average repair cost is $50 per system.

Warranties for Service or Replacement

(continued)

7-28

The number of systems sold in 2012 and 2013 was 5,000 and 6,000, respectively. Actual repair costs were $12,500 in 2013 and $55,000 in 2014.

Warranties for Service or Replacement

(continued)

7-29

To record estimated warranty expense:

2012201220122012

Warranty Expense 75,000Estimated Liability for Warranties 75,000

To record estimated warrantyexpense based on systems sold (5,000 0.30 $50 = $75,000).

Warranties for Service or Replacement

(continued)

7-30

To record the cost of actual repairs in 2012:

Estimated Liability for Warranties 12,500Cash 12,500

To record cost of actual repairs in 2012.

2012201220122012

Warranties for Service or Replacement

(continued)

7-31

To record estimated warranty expense:

Warranty Expense 90,000Estimated Liability for Warranties 90,000

To record estimated warrantyexpense based on systems sold (6,000 0.30 $50).

2013201320132013

Warranties for Service or Replacement

(continued)

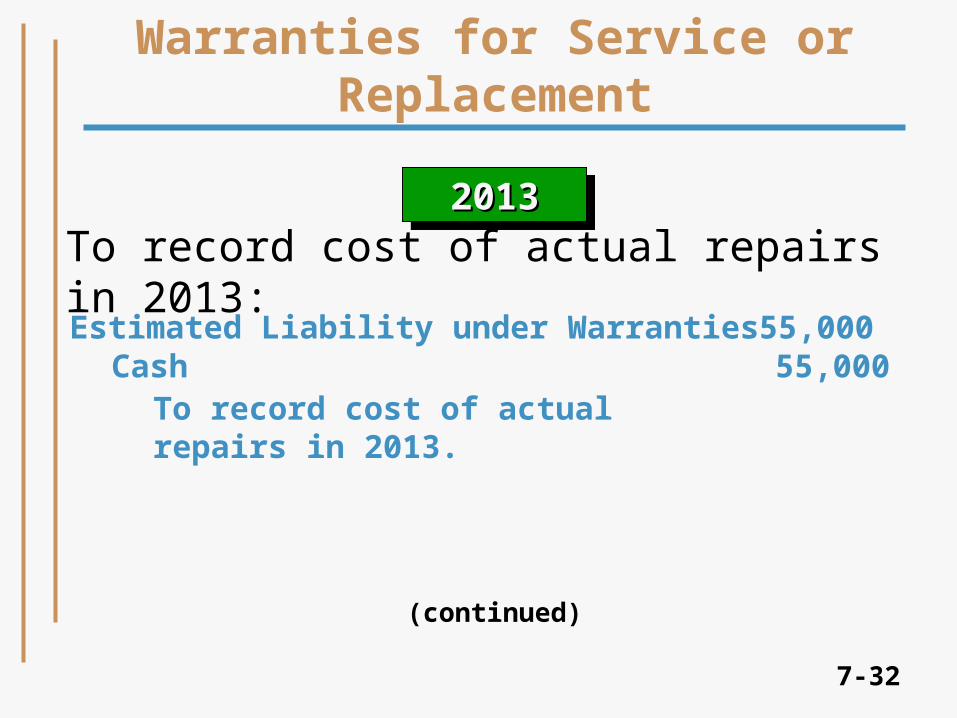

7-32

To record cost of actual repairs in 2013:Estimated Liability under Warranties 55,000

Cash 55,000To record cost of actual repairs in 2013.

2013201320132013

Warranties for Service or Replacement

(continued)

7-33

Periodically, the warranty liability account should be analyzed to see whether the actual repairs approximate the estimate.

Warranties for Service or Replacement

2012 sales still under warranty for 6 months:$50 x [5,000 units x (6/12 x 0.20)] $ 25,000

2013 sales still under warranty for 18 months:$50 x [6,000 units x (6/12 x.10) +6,000 units x (12/12 x .020)] 75,000

Total $100,000

The $100,000 approximation is The $100,000 approximation is reasonably close to the $97,500 reasonably close to the $97,500 balance in the allowance account.balance in the allowance account.

(continued)

7-34

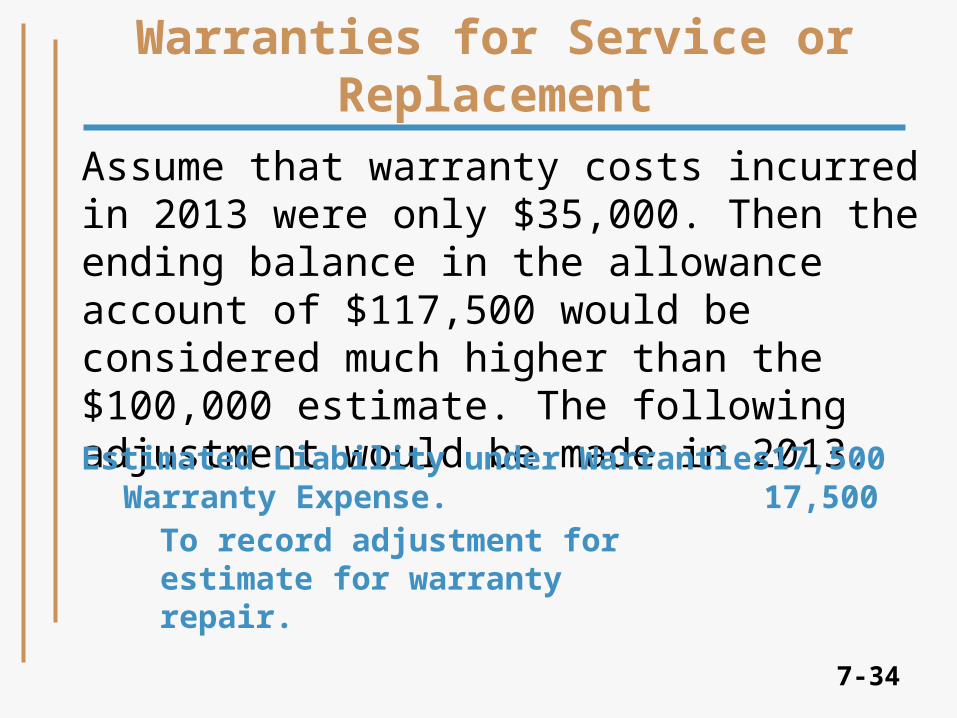

Assume that warranty costs incurred in 2013 were only $35,000. Then the ending balance in the allowance account of $117,500 would be considered much higher than the $100,000 estimate. The following adjustment would be made in 2013.

Warranties for Service or Replacement

Estimated Liability under Warranties 17,500Warranty Expense. 17,500

To record adjustment for estimate for warranty repair.

7-35

Monitoring Accounts Receivable

• The average collection period is the average number of days that lapse between the time that a sale is made and the time that cash is collected.

• It is calculated by dividing the average receivables outstanding by the average daily sales.

(continued)

7-36

In 2012, WS Corporation had average receivables of $354,250 and net sales of $1,650,000. The average collection period can be calculated as follows:

Average collection period = 78 days

Average receivable $354,250 Average daily sales ($1,650,000/365)

=

(continued)

Monitoring Accounts Receivable

7-37

Accounts receivable turnover = 4.7 times

Accounts receivable turnover is determined by dividing net sales by the average trade accounts receivable outstanding during the year. The calculation for 2012 is as follows:

Net sales $1,650,000 Average net receivables

$354,250

=

Monitoring Accounts Receivable

7-38

• Revenues and receivables have value because they will eventually be converted to cash.

• Cash is important because it provides the basis for measurement and accounting for all other items.

• The FASB identified the need to report information on cash and liquidity as one of the key objectives of financial reporting.

Cash Management and Control

(continued)

7-39

Composition of Cash

• Coins and currency not yet deposited

• Demand deposits

• Petty cash funds

• Cashier’s checks

• Personal checks

• Very short-term

interest-earning securities

Funds that can be withdrawn on demand

Sometimes referred to as cash equivalents

(continued)

7-40

Composition of Cash

• Deposits that are not immediately available for withdrawal or have other restrictions are sometimes referred to as time deposits.

• Time deposits are sometimes separately classified as temporary investments.

• Deposits in foreign banks that are subject to immediate and unrestricted withdrawal generally qualify as cash.

(continued)

7-41

Composition of Cash

• Cash balances specifically designated by management for special purposes should be reported separately, e.g. a bond sinking fund.

• A credit balance in the cash account resulting from the issuance of checks in excess of the amount on deposit is known as a cash overdraft.

7-42

Compensating Balances

• In connection with financing arrangements, it is common practice for a company to agree to maintain a minimum or average balance on deposit with a bank.

• These compensating balances are defined by the SEC as “that portion of any demand deposit maintained by a corporation . . . which constitutes support for borrowing arrangements . . .”

(continued)

7-43

Management and Control of Cash

1. Specifically assigned responsibilities for handling cash receipts

2. Separation of handling and recording cash receipts

3. Daily deposits of all cash received4. Voucher system to control cash payments

Basic characteristics of a cash control system are:

(continued)

7-44

5. Internal audits at irregular intervals6. Double record of cash—bank and books,

with reconciliations performed by someone outside the accounting function

These controls are more likely to be These controls are more likely to be found in large companies with many found in large companies with many employees.employees.

These controls are more likely to be These controls are more likely to be found in large companies with many found in large companies with many employees.employees.

Management and Control of Cash

7-45

Bank Reconciliation

A comparison of the bank balance with the book balance is usually made monthly by means of a summary known as a bank reconciliation.

Bank Bank balancebalance

Book Book balancebalance

(continued)

7-46

If, after considering these items, the bank statement and the book balances cannot be reconciled, a detailed analysis of both the bank’s records and the depositor’s books may be necessary to determine whether errors or irregularities exist on the records of either party.

(continued)

Bank Reconciliation

7-47

The following entries would be required on the books of Svendsen, Inc., as a result of the November 30 reconciliation:

Cash 98.50Interest Revenue 98.50

To record interest earned during November.

Cash 18.00Advertising Expense 18.00

To record correction for check payment of advertising recorded as $64 instead of the actual amount, $46.

(continued)

Preparing a Bank Reconciliation

7-48

Accounts Receivable 118.94Miscellaneous General Expense 3.16

Cash 122.10To record customer’s uncollectible check and bank charges for November.

Preparing a Bank Reconciliation

7-49

Presentation of Receivables in the Financial Statements

• Current receivables may be grouped in the balance sheet in the following classes: Notes receivable—trade debtors Accounts receivable—trade debtors Other receivables

• It is possible to combine trade notes and accounts receivable into a single amount.

• Restrictions on any receivables should be disclosed.

7-50

Receivables as a Source of Cash

Receivables may be converted to cash quickly in one of two ways:

• As a sale (either with or without recourse)

• As a secured borrowing

(continued)

7-51

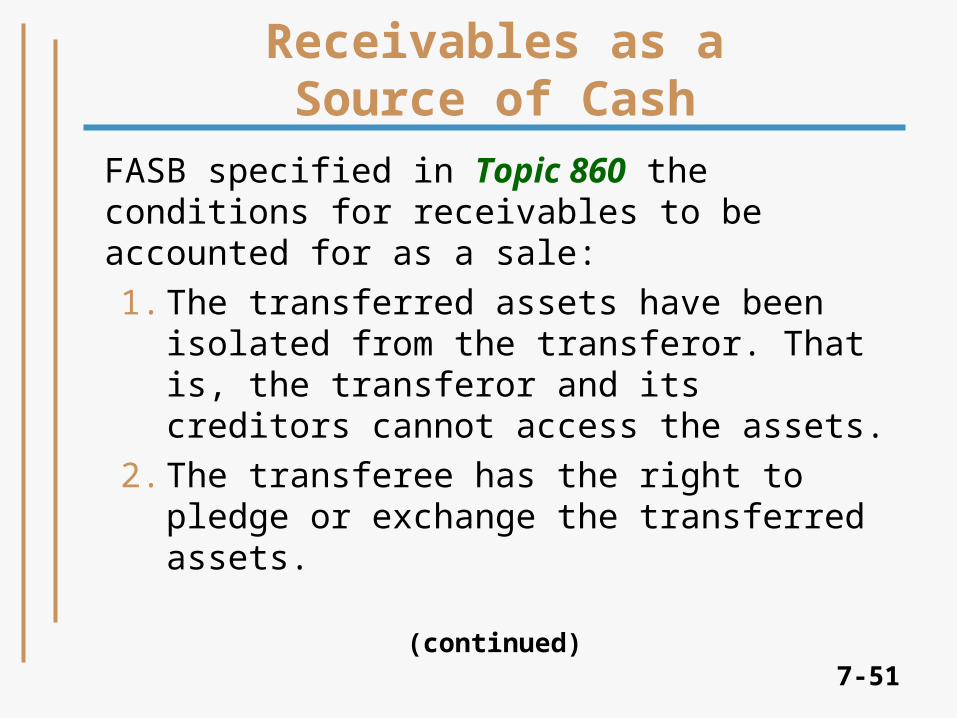

FASB specified in Topic 860 the conditions for receivables to be accounted for as a sale:

1. The transferred assets have been isolated from the transferor. That is, the transferor and its creditors cannot access the assets.

2. The transferee has the right to pledge or exchange the transferred assets.

Receivables as a Source of Cash

(continued)

7-52

3. The transferor does not maintain effective control over the assets through either (a) an agreement to repurchase them before their maturity or (b) the ability to cause the transferee to return specific assets.

Receivables as a Source of Cash

7-53

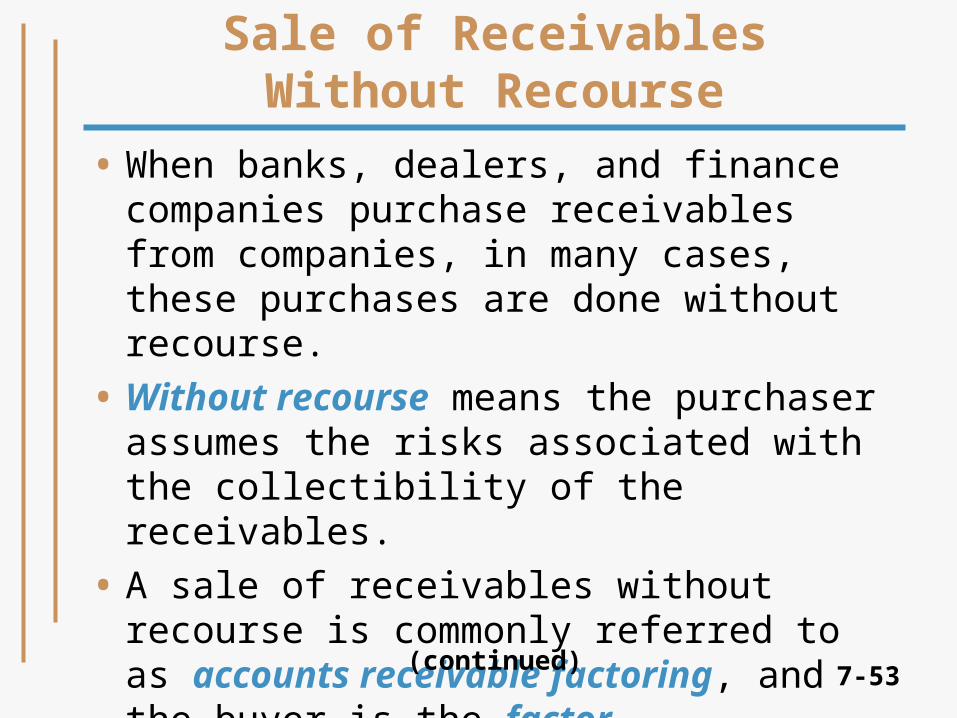

Sale of Receivables Without Recourse

• When banks, dealers, and finance companies purchase receivables from companies, in many cases, these purchases are done without recourse.

• Without recourse means the purchaser assumes the risks associated with the collectibility of the receivables.

• A sale of receivables without recourse is commonly referred to as accounts receivable factoring, and the buyer is the factor.

(continued)

7-54

a) failure of the debtors to pay when due,b) the effects of prepayments, orc) adjustments resulting from defects in the

eligibility of the transferred receivables.”

Recourse is defined by the FASB as “the right of a transferee of receivables to receive payment from the transferor of those receivable for any of the following reasons:

(continued)

Sale of Receivables Without Recourse

7-55

• Assume that $10,000 of receivables are factored, that is, sold without recourse, to a finance company for $8,500.

• An allowance for bad debts equal to $300 was previously established for these accounts.

• The finance company withheld 5% of the purchase price as protection against sales returns and allowances.

(continued)

Sale of Receivables Without Recourse

7-56

Cash 8,075Receivable from Factor 425Allowance for Bad Debts 300Loss from Factoring Receivables 1,200

Accounts Receivable 10,000To record the factoring of receivables.

Computations:Cash: $8,500 – $425 = $8,075Factor receivable: $8,500 5% = $425Factoring loss: ($10,000 – $300) – $8,500 = $1,200

(continued)

Sale of Receivables Without Recourse

7-57

Cash 425Receivable from Factor 425

To record the final settlement associated with previously factored receivables.

Assuming there were no returns or allowances, the final settlement would be recorded as follows:

Sale of Receivables Without Recourse

7-58

Selling receivables with recourse means that a purchaser (bank or finance company) advances cash in return for receivables but retains the right to collect from the seller if debtors (seller’s customers) fail to make payments when due.

Sale of ReceivablesWith Recourse

(continued)

7-59

Secured Borrowing

• With an assignment of receivables: There are no special accounting problems

involved. Simply record the loan.

• With specific assignment: Specified accounts receivable pledged Accounts Receivable reclassified on balance

sheet Footnote disclosure of loan provisions required

(continued)

7-60

• On July 1, 2013, Provo Mercantile Co. assigns receivables total $300,000 to Salem Bank as collateral on a $200,000, 12% note. Provo Mercantile does not notify its account debtors and will continue to collect the assigned receivables.

• Salem assesses a 1% finance charge on assigned receivables in addition to the interest on the note.

(continued)

Secured Borrowing

7-61

Derecognition of Receivables: IAS 39

The purpose of the three conditions in FASB ASC Section 860-10-40 is to identify receivable transfers in which economic ownership of the receivables has been transferred. IAS 39 contains the same concept but applied slightly differently.

(continued)

7-62

IAS 39 contains a 2-step test for derecognition.

1. Determine whether the receivable transfer involves a transfer of “substantially all of the risks and rewards of ownership of the [receivable].” If so, the transfer is accounted for as a sale of the receivable.

Derecognition of Receivables: IAS 39

(continued)

7-63

2. If the receivable transfer does not involve the transfer of substantially all the risks and rewards of ownership, determine whether control of the receivable has been transferred. If so, account for the receivable transfer as a sale. If not, the transfer is treated as a secured loan.

Derecognition of Receivables: IAS 39

7-64

Notes Receivable

A promissory note is an unconditional written promise to pay a certain sum of money at a specified time.

• The note is signed by the maker and is payable to the order of a specified payee or bearer.

• Notes usually involve interest stated at an annual rate.

• Most notes are negotiable notes.

7-65

Valuation of Notes Receivable

• Notes receivable are initially recorded at their present value.

• When a note is exchanged for property, goods, or services, the present value equals the current cash selling price of the items exchanged.

• An interest-bearing note is written as a promise to pay principal (or face amount) plus interest at a specified rate.

(continued)

7-66

• A non-interest-bearing note does not specify an interest rate, but the face amount includes the interest charge.

• The present value is the difference between the face amount and the interest included in that amount, sometimes called the implicit (or effective) interest.

Valuation of Notes Receivable

7-67

Special Valuation Problems

When a note is exchanged for cash:

• It should be recorded at its face amount

and

• any difference between face and cash proceeds should be recorded as premium or discount on the note.

(continued)

7-68

When a note is exchanged for property, goods, or services in an arm’s-length transaction:

• the present value of the note is usually evidenced by the terms of the note or supporting documents

• there is a general presumption that the interest specified by the parties to a transaction represents fair and adequate compensation for the use of funds

Special Valuation Problems

(continued)

7-69

Valuation problems arise when one of the following conditions exists:

• No interest rate is stated

• The stated rate does not seem reasonable, given the nature of the transaction and surrounding circumstances

• The stated face amount of the note is significantly different from the current cash equivalent sales price of similar property, goods, or service

Special Valuation Problems

7-70

1. Determine the maturity value of the note.Maturity value = Face amount ÷ InterestInterest = Face amount x Interest rate x Interest periodInterest period = Date of note to date of maturityThe maturity value is the amount you will receive when the note matures.

(continued)

Determine the Amount to be Received from the Bank

7-71

Determine the Amount to be Received from the Bank

2. Determine the amount of discount.Discount = Maturity value x Discount rate x Discount periodDiscount period = Date of discount to date of maturity

The amount of time you have to wait to get the The amount of time you have to wait to get the money is termed the money is termed the discount perioddiscount period..The amount of time you have to wait to get the The amount of time you have to wait to get the money is termed the money is termed the discount perioddiscount period..

3. Determine the proceeds:Proceeds = Maturity Value ‒ Discount

7-72

Imputing an Interest Rate

• If there is no current market price for either the property, goods, or services or the note, then the present value of the note must be determined by selecting an appropriate interest rate and using that rate to discount future receipts to the present.

• The imputed interest rate is determined at the date of exchange and is not altered thereafter.

7-73

Impact of Uncollectible Accounts on Cash Flows

A decrease in receivables can occur when the:

• customers pay on account

and

• customers never pay and the account is written off

7-74

Chapter 7Chapter 7

The EndThe EndThe EndThe End

$

₵

7-75