(4q15) australia australian banks€¦ · please refer to page 12 for important disclosures and...

TRANSCRIPT

Please refer to page 12 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

AUSTRALIA

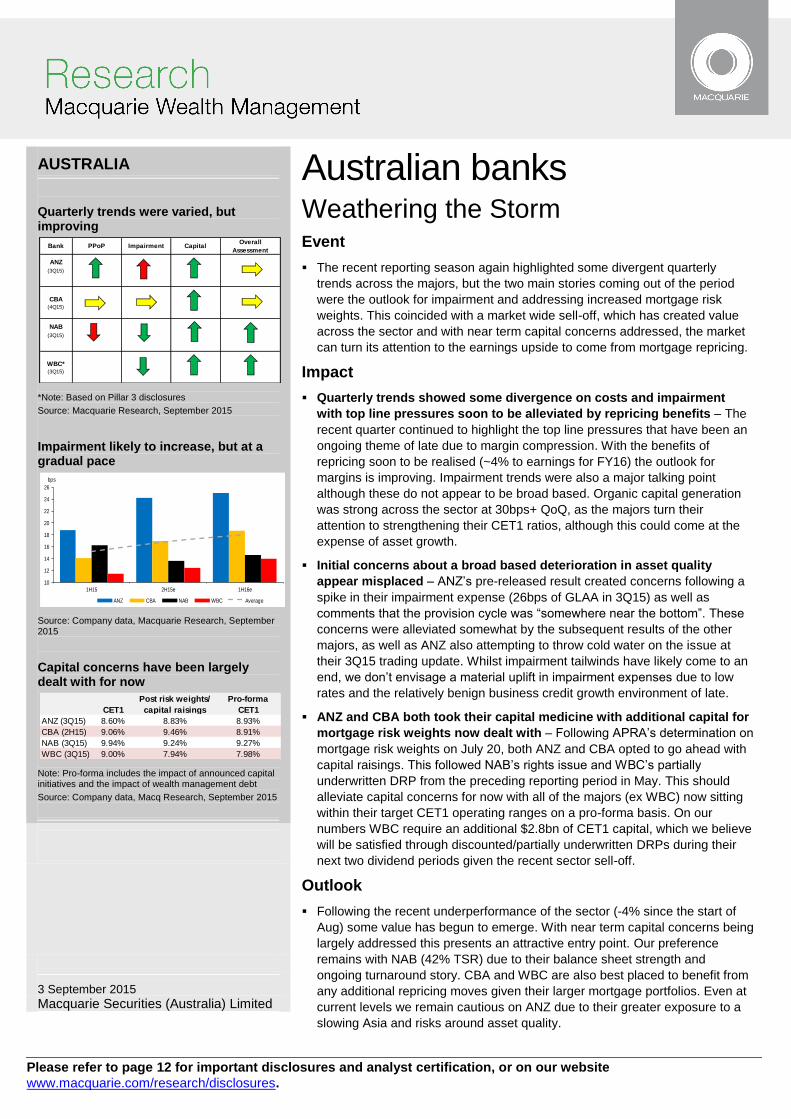

Quarterly trends were varied, but improving

*Note: Based on Pillar 3 disclosures

Source: Macquarie Research, September 2015

Impairment likely to increase, but at a gradual pace

Source: Company data, Macquarie Research, September 2015

Capital concerns have been largely dealt with for now

Note: Pro-forma includes the impact of announced capital initiatives and the impact of wealth management debt

Source: Company data, Macq Research, September 2015

3 September 2015 Macquarie Securities (Australia) Limited

Australian banks Weathering the Storm Event

The recent reporting season again highlighted some divergent quarterly

trends across the majors, but the two main stories coming out of the period

were the outlook for impairment and addressing increased mortgage risk

weights. This coincided with a market wide sell-off, which has created value

across the sector and with near term capital concerns addressed, the market

can turn its attention to the earnings upside to come from mortgage repricing.

Impact

Quarterly trends showed some divergence on costs and impairment

with top line pressures soon to be alleviated by repricing benefits – The

recent quarter continued to highlight the top line pressures that have been an

ongoing theme of late due to margin compression. With the benefits of

repricing soon to be realised (~4% to earnings for FY16) the outlook for

margins is improving. Impairment trends were also a major talking point

although these do not appear to be broad based. Organic capital generation

was strong across the sector at 30bps+ QoQ, as the majors turn their

attention to strengthening their CET1 ratios, although this could come at the

expense of asset growth.

Initial concerns about a broad based deterioration in asset quality

appear misplaced – ANZ’s pre-released result created concerns following a

spike in their impairment expense (26bps of GLAA in 3Q15) as well as

comments that the provision cycle was “somewhere near the bottom”. These

concerns were alleviated somewhat by the subsequent results of the other

majors, as well as ANZ also attempting to throw cold water on the issue at

their 3Q15 trading update. Whilst impairment tailwinds have likely come to an

end, we don’t envisage a material uplift in impairment expenses due to low

rates and the relatively benign business credit growth environment of late.

ANZ and CBA both took their capital medicine with additional capital for

mortgage risk weights now dealt with – Following APRA’s determination on

mortgage risk weights on July 20, both ANZ and CBA opted to go ahead with

capital raisings. This followed NAB’s rights issue and WBC’s partially

underwritten DRP from the preceding reporting period in May. This should

alleviate capital concerns for now with all of the majors (ex WBC) now sitting

within their target CET1 operating ranges on a pro-forma basis. On our

numbers WBC require an additional $2.8bn of CET1 capital, which we believe

will be satisfied through discounted/partially underwritten DRPs during their

next two dividend periods given the recent sector sell-off.

Outlook

Following the recent underperformance of the sector (-4% since the start of

Aug) some value has begun to emerge. With near term capital concerns being

largely addressed this presents an attractive entry point. Our preference

remains with NAB (42% TSR) due to their balance sheet strength and

ongoing turnaround story. CBA and WBC are also best placed to benefit from

any additional repricing moves given their larger mortgage portfolios. Even at

current levels we remain cautious on ANZ due to their greater exposure to a

slowing Asia and risks around asset quality.

Bank PPoP Impairment CapitalOverall

Assessment

ANZ

(3Q15)

CBA(4Q15)

NAB

(3Q15)

WBC*(3Q15)

10

12

14

16

18

20

22

24

26

1H15 2H15e 1H16e

bps

ANZ CBA NAB WBC Average

CET1

Post risk weights/

capital raisings

Pro-forma

CET1

ANZ (3Q15) 8.60% 8.83% 8.93%

CBA (2H15) 9.06% 9.46% 8.91%

NAB (3Q15) 9.94% 9.24% 9.27%

WBC (3Q15) 9.00% 7.94% 7.98%

Macquarie Wealth Management Australian banks

3 September 2015 2

Analysis

The recent reporting season again highlighted some divergent quarterly trends across the majors,

but the two main stories coming out of the period were the outlook for impairment and addressing

increased mortgage risk weights. This coincided with a market wide sell-off, which has created

value across the sector and with capital concerns addressed for now, the market can turn its

attention to the earnings upside to come from mortgage repricing.

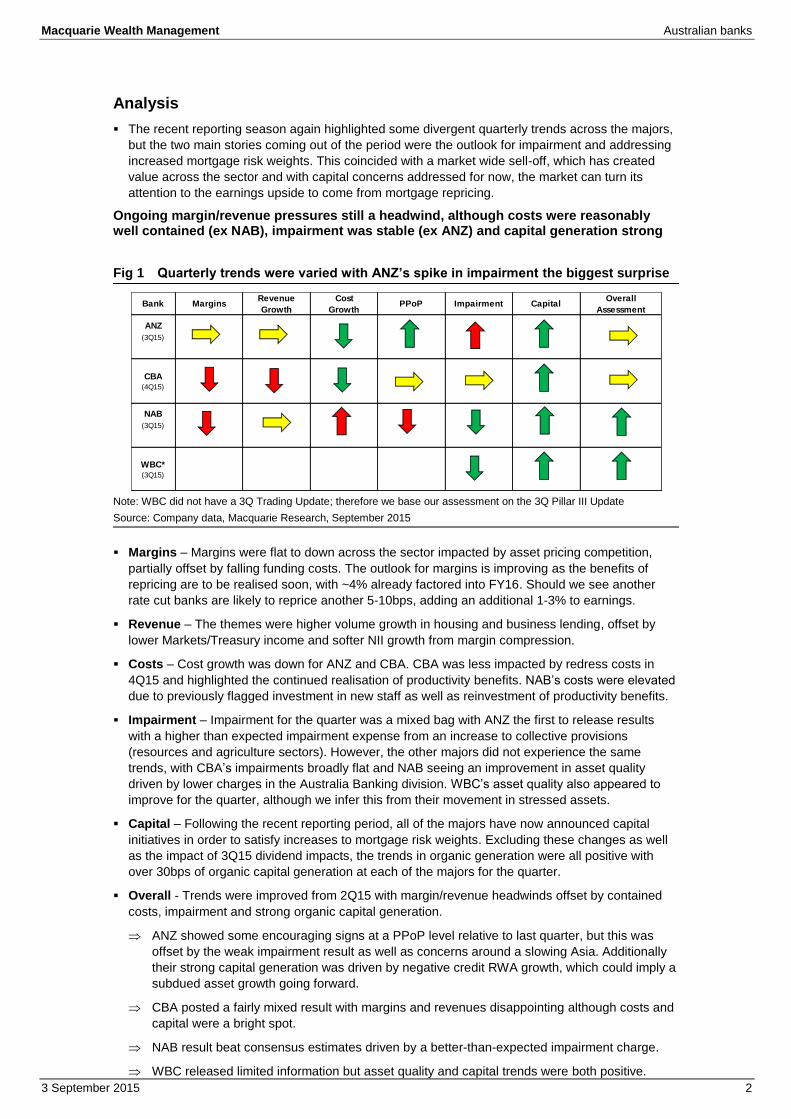

Ongoing margin/revenue pressures still a headwind, although costs were reasonably well contained (ex NAB), impairment was stable (ex ANZ) and capital generation strong

Fig 1 Quarterly trends were varied with ANZ’s spike in impairment the biggest surprise

Note: WBC did not have a 3Q Trading Update; therefore we base our assessment on the 3Q Pillar III Update

Source: Company data, Macquarie Research, September 2015

Margins – Margins were flat to down across the sector impacted by asset pricing competition,

partially offset by falling funding costs. The outlook for margins is improving as the benefits of

repricing are to be realised soon, with ~4% already factored into FY16. Should we see another

rate cut banks are likely to reprice another 5-10bps, adding an additional 1-3% to earnings.

Revenue – The themes were higher volume growth in housing and business lending, offset by

lower Markets/Treasury income and softer NII growth from margin compression.

Costs – Cost growth was down for ANZ and CBA. CBA was less impacted by redress costs in

4Q15 and highlighted the continued realisation of productivity benefits. NAB’s costs were elevated

due to previously flagged investment in new staff as well as reinvestment of productivity benefits.

Impairment – Impairment for the quarter was a mixed bag with ANZ the first to release results

with a higher than expected impairment expense from an increase to collective provisions

(resources and agriculture sectors). However, the other majors did not experience the same

trends, with CBA’s impairments broadly flat and NAB seeing an improvement in asset quality

driven by lower charges in the Australia Banking division. WBC’s asset quality also appeared to

improve for the quarter, although we infer this from their movement in stressed assets.

Capital – Following the recent reporting period, all of the majors have now announced capital

initiatives in order to satisfy increases to mortgage risk weights. Excluding these changes as well

as the impact of 3Q15 dividend impacts, the trends in organic generation were all positive with

over 30bps of organic capital generation at each of the majors for the quarter.

Overall - Trends were improved from 2Q15 with margin/revenue headwinds offset by contained

costs, impairment and strong organic capital generation.

ANZ showed some encouraging signs at a PPoP level relative to last quarter, but this was

offset by the weak impairment result as well as concerns around a slowing Asia. Additionally

their strong capital generation was driven by negative credit RWA growth, which could imply a

subdued asset growth going forward.

CBA posted a fairly mixed result with margins and revenues disappointing although costs and

capital were a bright spot.

NAB result beat consensus estimates driven by a better-than-expected impairment charge.

WBC released limited information but asset quality and capital trends were both positive.

Bank MarginsRevenue

Growth

Cost

GrowthPPoP Impairment Capital

Overall

Assessment

ANZ

(3Q15)

CBA(4Q15)

NAB

(3Q15)

WBC*(3Q15)

Macquarie Wealth Management Australian banks

3 September 2015 3

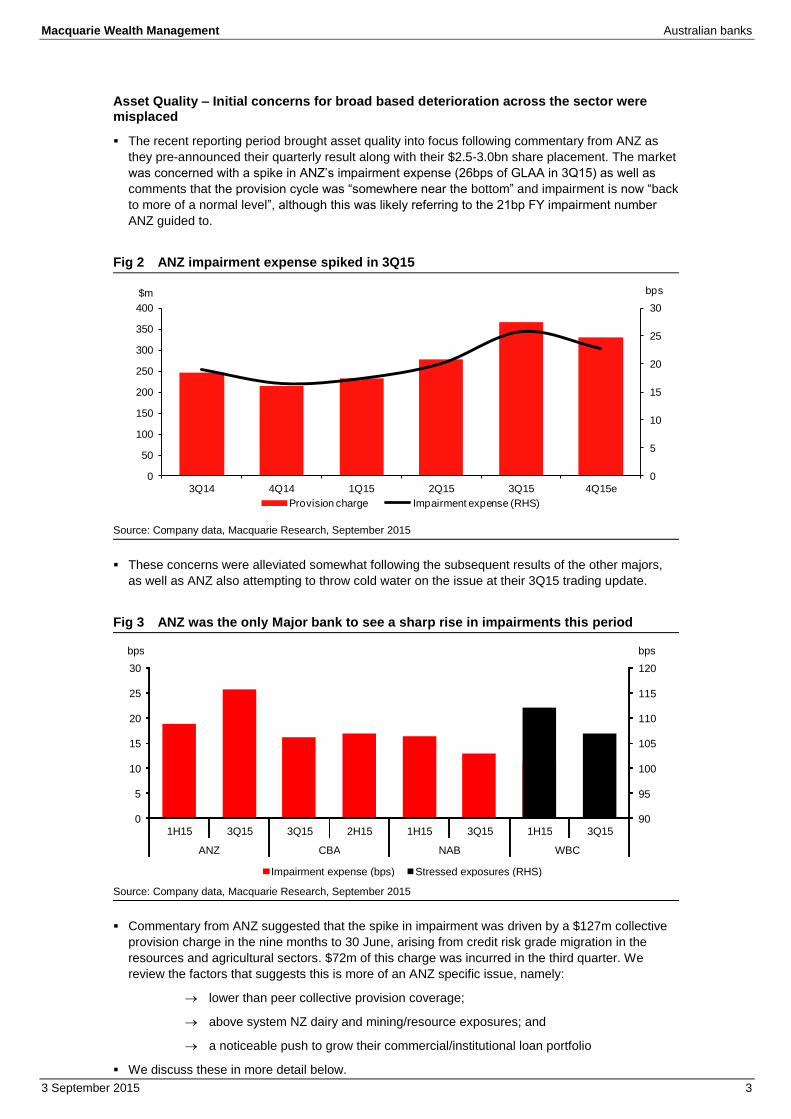

Asset Quality – Initial concerns for broad based deterioration across the sector were misplaced

The recent reporting period brought asset quality into focus following commentary from ANZ as

they pre-announced their quarterly result along with their $2.5-3.0bn share placement. The market

was concerned with a spike in ANZ’s impairment expense (26bps of GLAA in 3Q15) as well as

comments that the provision cycle was “somewhere near the bottom” and impairment is now “back

to more of a normal level”, although this was likely referring to the 21bp FY impairment number

ANZ guided to.

Fig 2 ANZ impairment expense spiked in 3Q15

Source: Company data, Macquarie Research, September 2015

These concerns were alleviated somewhat following the subsequent results of the other majors,

as well as ANZ also attempting to throw cold water on the issue at their 3Q15 trading update.

Fig 3 ANZ was the only Major bank to see a sharp rise in impairments this period

Source: Company data, Macquarie Research, September 2015

Commentary from ANZ suggested that the spike in impairment was driven by a $127m collective

provision charge in the nine months to 30 June, arising from credit risk grade migration in the

resources and agricultural sectors. $72m of this charge was incurred in the third quarter. We

review the factors that suggests this is more of an ANZ specific issue, namely:

lower than peer collective provision coverage;

above system NZ dairy and mining/resource exposures; and

a noticeable push to grow their commercial/institutional loan portfolio

We discuss these in more detail below.

0

5

10

15

20

25

30

0

50

100

150

200

250

300

350

400

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15e

bps$m

Provision charge Impairment expense (RHS)

90

95

100

105

110

115

120

0

5

10

15

20

25

30

1H15 3Q15 3Q15 2H15 1H15 3Q15 1H15 3Q15

ANZ CBA NAB WBC

bps bps

Impairment expense (bps) Stressed exposures (RHS)

Macquarie Wealth Management Australian banks

3 September 2015 4

Lower than peer collective provision coverage

Even after the increased charge during the period, ANZ’s collective provision as a % of their credit

risk-weighted assets (incl. GRCL) is still below peers. The less conservative approach taken by

ANZ with respect to their collective provision is one contributing factor to their spike in impairment

with the potential for more to come to be more aligned with peers.

Fig 4 ANZ has a lower than peer CP as a % of credit risk-weighted assets (incl. GRCL)

Source: APRA, Macquarie Research, September 2015

Above system NZ dairy and mining/resource exposures

As the largest lender in New Zealand, ANZ have the largest dairy exposure in terms of both dollar

value (NZ$11.3b) and as a % of GLAA (1.8%), which has been impacted by the significant fall in

the dairy price. On the domestic front ANZ’s resource/energy exposures are also near the top of

the peer group at 2.2% of total exposures as per APRA Pillar III disclosures.

Fig 5 ANZ is most exposed to NZ dairy...

Fig 6 ...and only behind CBA on exposures to resources/energy

Source: RBNZ, Macquarie Research, September 2015 Source: APRA, Company data, Macquarie Research, September 2015

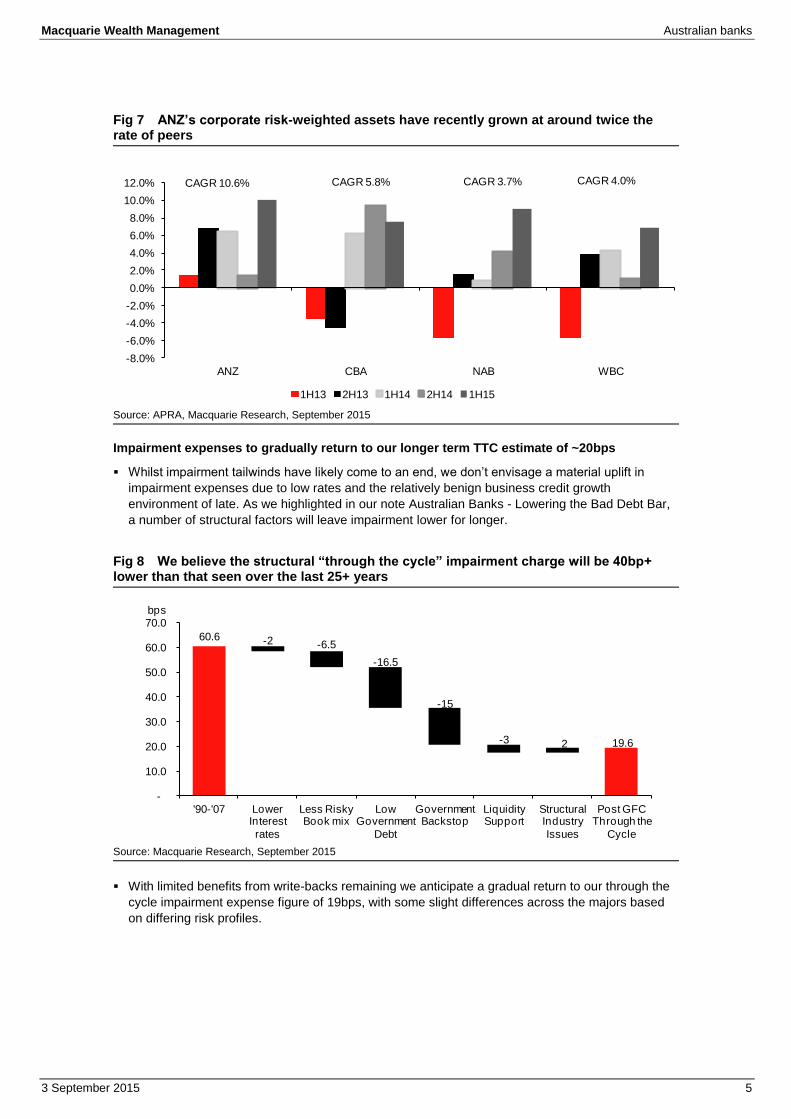

A noticeable push to grow their commercial/institutional loan portfolio ahead of peers

Since 1H13 ANZ have been growing their corporate risk-weighted assets at a much faster rate

than peers. This did appear to slow somewhat in the recent quarter, however with a CAGR around

double that of their peers in recent years could be starting to have an impact on the impairment

line.

0.87% 0.87%

1.01%

0.90%

0.11% 0.04%

0.75%

0.80%

0.85%

0.90%

0.95%

1.00%

1.05%

ANZ CBA NAB WBC

CP as % of CRWA GRCL as % of CRWA

0.0%

0.5%

1.0%

1.5%

2.0%

ANZ CBA NAB WBC

Dairy % of GLAA

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

ANZ CBA NAB WBC

Resources % of total exposures

Macquarie Wealth Management Australian banks

3 September 2015 5

Fig 7 ANZ’s corporate risk-weighted assets have recently grown at around twice the rate of peers

Source: APRA, Macquarie Research, September 2015

Impairment expenses to gradually return to our longer term TTC estimate of ~20bps

Whilst impairment tailwinds have likely come to an end, we don’t envisage a material uplift in

impairment expenses due to low rates and the relatively benign business credit growth

environment of late. As we highlighted in our note Australian Banks - Lowering the Bad Debt Bar,

a number of structural factors will leave impairment lower for longer.

Fig 8 We believe the structural “through the cycle” impairment charge will be 40bp+ lower than that seen over the last 25+ years

Source: Macquarie Research, September 2015

With limited benefits from write-backs remaining we anticipate a gradual return to our through the

cycle impairment expense figure of 19bps, with some slight differences across the majors based

on differing risk profiles.

CAGR 10.6% CAGR 5.8% CAGR 3.7% CAGR 4.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

ANZ CBA NAB WBC

1H13 2H13 1H14 2H14 1H15

60.6

2 19.6

-2 -6.5

-16.5

-15

-3

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

'90-'07 Lower Interest

rates

Less Risky Book mix

Low Government

Debt

Government Backstop

Liquidity Support

Structural Industry

Issues

Post GFC Through the

Cycle

bps

Macquarie Wealth Management Australian banks

3 September 2015 6

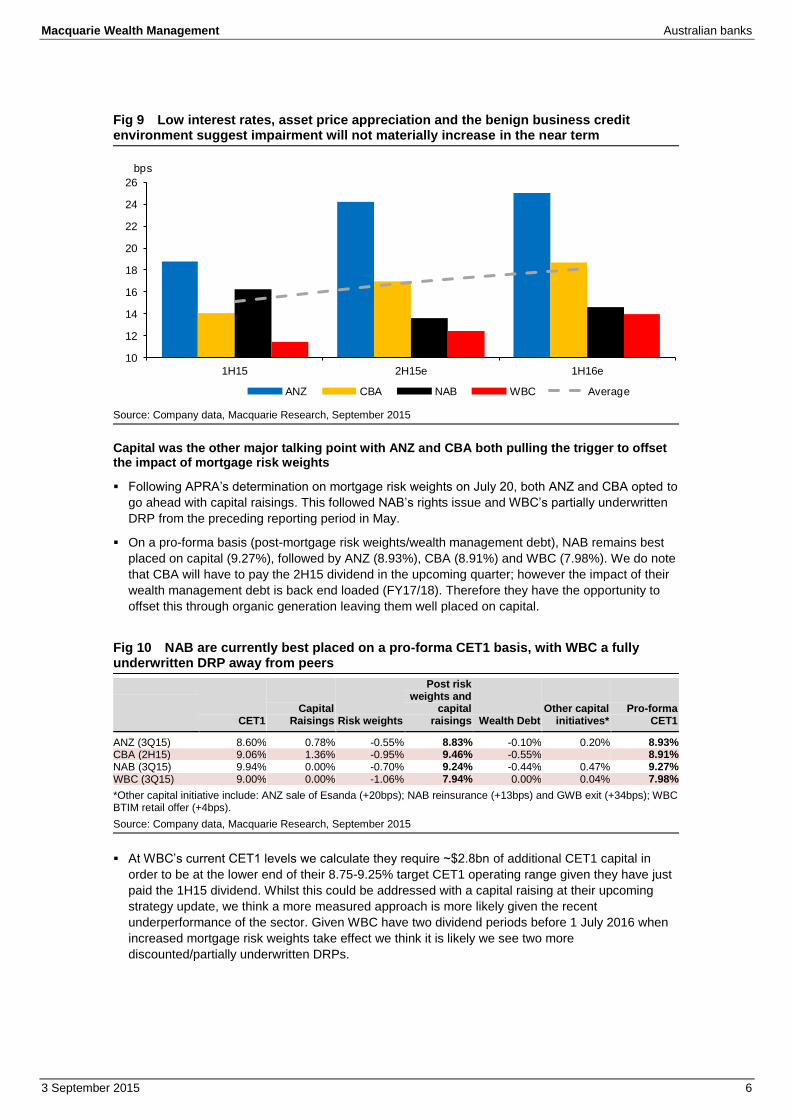

Fig 9 Low interest rates, asset price appreciation and the benign business credit environment suggest impairment will not materially increase in the near term

Source: Company data, Macquarie Research, September 2015

Capital was the other major talking point with ANZ and CBA both pulling the trigger to offset the impact of mortgage risk weights

Following APRA’s determination on mortgage risk weights on July 20, both ANZ and CBA opted to

go ahead with capital raisings. This followed NAB’s rights issue and WBC’s partially underwritten

DRP from the preceding reporting period in May.

On a pro-forma basis (post-mortgage risk weights/wealth management debt), NAB remains best

placed on capital (9.27%), followed by ANZ (8.93%), CBA (8.91%) and WBC (7.98%). We do note

that CBA will have to pay the 2H15 dividend in the upcoming quarter; however the impact of their

wealth management debt is back end loaded (FY17/18). Therefore they have the opportunity to

offset this through organic generation leaving them well placed on capital.

Fig 10 NAB are currently best placed on a pro-forma CET1 basis, with WBC a fully underwritten DRP away from peers

CET1 Capital

Raisings Risk weights

Post risk weights and

capital raisings Wealth Debt

Other capital initiatives*

Pro-forma CET1

ANZ (3Q15) 8.60% 0.78% -0.55% 8.83% -0.10% 0.20% 8.93% CBA (2H15) 9.06% 1.36% -0.95% 9.46% -0.55% 8.91% NAB (3Q15) 9.94% 0.00% -0.70% 9.24% -0.44% 0.47% 9.27% WBC (3Q15) 9.00% 0.00% -1.06% 7.94% 0.00% 0.04% 7.98%

*Other capital initiative include: ANZ sale of Esanda (+20bps); NAB reinsurance (+13bps) and GWB exit (+34bps); WBC BTIM retail offer (+4bps).

Source: Company data, Macquarie Research, September 2015

At WBC’s current CET1 levels we calculate they require ~$2.8bn of additional CET1 capital in

order to be at the lower end of their 8.75-9.25% target CET1 operating range given they have just

paid the 1H15 dividend. Whilst this could be addressed with a capital raising at their upcoming

strategy update, we think a more measured approach is more likely given the recent

underperformance of the sector. Given WBC have two dividend periods before 1 July 2016 when

increased mortgage risk weights take effect we think it is likely we see two more

discounted/partially underwritten DRPs.

10

12

14

16

18

20

22

24

26

1H15 2H15e 1H16e

bps

ANZ CBA NAB WBC Average

Macquarie Wealth Management Australian banks

3 September 2015 7

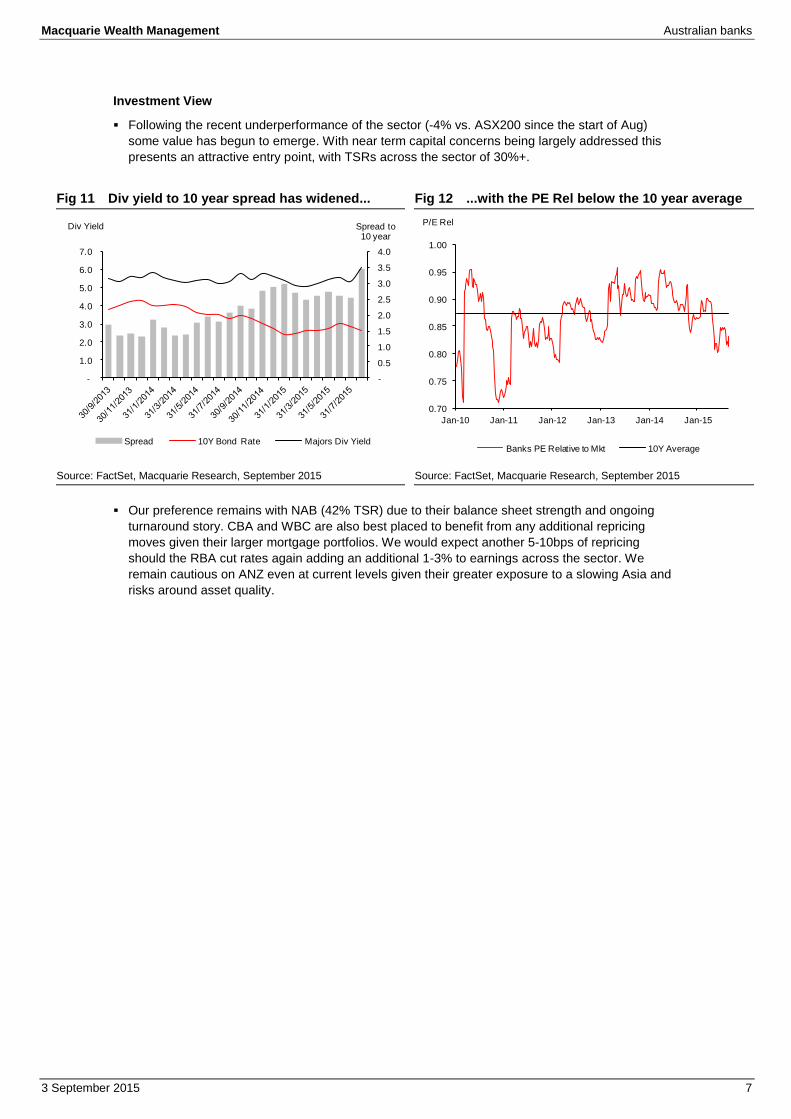

Investment View

Following the recent underperformance of the sector (-4% vs. ASX200 since the start of Aug)

some value has begun to emerge. With near term capital concerns being largely addressed this

presents an attractive entry point, with TSRs across the sector of 30%+.

Fig 11 Div yield to 10 year spread has widened... Fig 12 ...with the PE Rel below the 10 year average

Source: FactSet, Macquarie Research, September 2015 Source: FactSet, Macquarie Research, September 2015

Our preference remains with NAB (42% TSR) due to their balance sheet strength and ongoing

turnaround story. CBA and WBC are also best placed to benefit from any additional repricing

moves given their larger mortgage portfolios. We would expect another 5-10bps of repricing

should the RBA cut rates again adding an additional 1-3% to earnings across the sector. We

remain cautious on ANZ even at current levels given their greater exposure to a slowing Asia and

risks around asset quality.

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Spread to10 year

Div Yield

Spread 10Y Bond Rate Majors Div Yield

0.70

0.75

0.80

0.85

0.90

0.95

1.00

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

P/E Rel

Banks PE Relative to Mkt 10Y Average

Macquarie Wealth Management Australian banks

3 September 2015 8

Financial Summaries

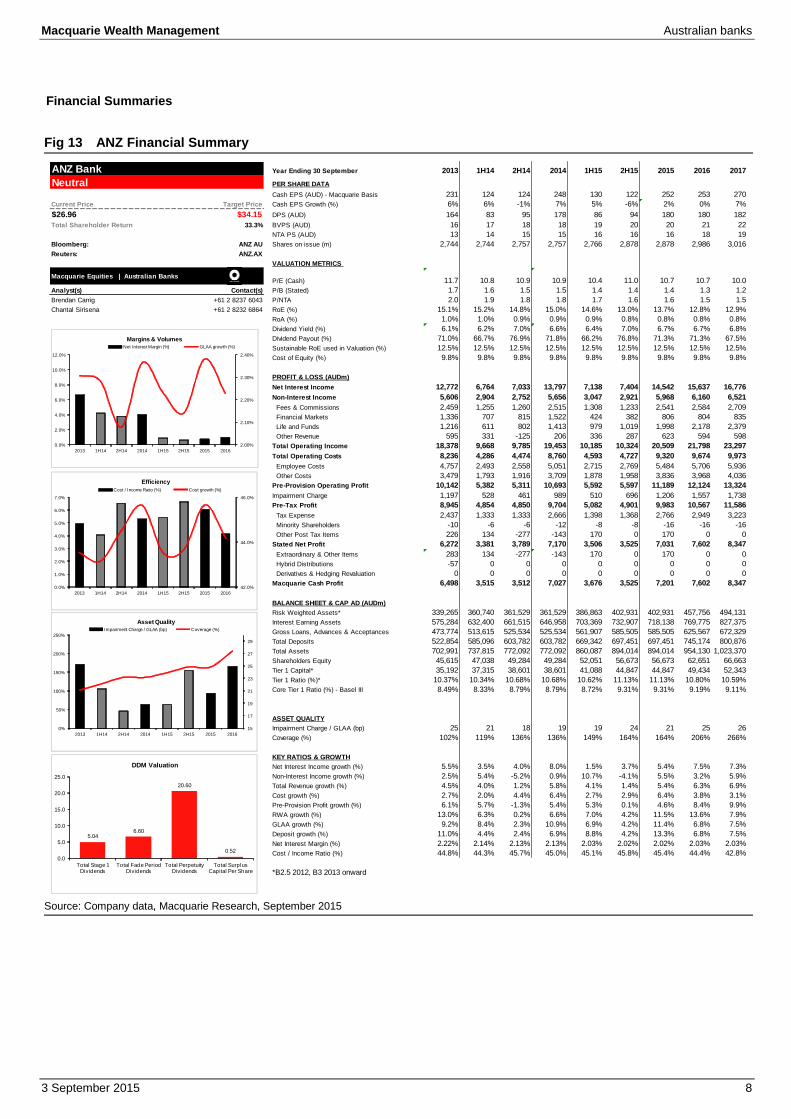

Fig 13 ANZ Financial Summary

Source: Company data, Macquarie Research, September 2015

ANZ Bank Year Ending 30 September 2013 1H14 2H14 2014 1H15 2H15 2015 2016 2017

Neutral PER SHARE DATA

Cash EPS (AUD) - Macquarie Basis 231 124 124 248 130 122 252 253 270

Current Price Target Price Cash EPS Growth (%) 6% 6% -1% 7% 5% -6% 2% 0% 7%

$26.96 $34.15 DPS (AUD) 164 83 95 178 86 94 180 180 182

Total Shareholder Return 33.3% BVPS (AUD) 16 17 18 18 19 20 20 21 22

NTA PS (AUD) 13 14 15 15 16 16 16 18 19

Bloomberg: ANZ AU Shares on issue (m) 2,744 2,744 2,757 2,757 2,766 2,878 2,878 2,986 3,016

Reuters: ANZ.AX

VALUATION METRICS

Macquarie Equities | Australian BanksP/E (Cash) 11.7 10.8 10.9 10.9 10.4 11.0 10.7 10.7 10.0

Analyst(s) Contact(s) P/B (Stated) 1.7 1.6 1.5 1.5 1.4 1.4 1.4 1.3 1.2

Brendan Carrig +61 2 8237 6043 P/NTA 2.0 1.9 1.8 1.8 1.7 1.6 1.6 1.5 1.5

Chantal Sirisena +61 2 8232 6864 RoE (%) 15.1% 15.2% 14.8% 15.0% 14.6% 13.0% 13.7% 12.8% 12.9%

RoA (%) 1.0% 1.0% 0.9% 0.9% 0.9% 0.8% 0.8% 0.8% 0.8%

Dividend Yield (%) 6.1% 6.2% 7.0% 6.6% 6.4% 7.0% 6.7% 6.7% 6.8%

Dividend Payout (%) 71.0% 66.7% 76.9% 71.8% 66.2% 76.8% 71.3% 71.3% 67.5%

Sustainable RoE used in Valuation (%) 12.5% 12.5% 12.5% 12.5% 12.5% 12.5% 12.5% 12.5% 12.5%

Cost of Equity (%) 9.8% 9.8% 9.8% 9.8% 9.8% 9.8% 9.8% 9.8% 9.8%

PROFIT & LOSS (AUDm)

Net Interest Income 12,772 6,764 7,033 13,797 7,138 7,404 14,542 15,637 16,776

Non-Interest Income 5,606 2,904 2,752 5,656 3,047 2,921 5,968 6,160 6,521

Fees & Commissions 2,459 1,255 1,260 2,515 1,308 1,233 2,541 2,584 2,709

Financial Markets 1,336 707 815 1,522 424 382 806 804 835

Life and Funds 1,216 611 802 1,413 979 1,019 1,998 2,178 2,379

Other Revenue 595 331 -125 206 336 287 623 594 598

Total Operating Income 18,378 9,668 9,785 19,453 10,185 10,324 20,509 21,798 23,297

Total Operating Costs 8,236 4,286 4,474 8,760 4,593 4,727 9,320 9,674 9,973

Employee Costs 4,757 2,493 2,558 5,051 2,715 2,769 5,484 5,706 5,936

Other Costs 3,479 1,793 1,916 3,709 1,878 1,958 3,836 3,968 4,036

Pre-Provision Operating Profit 10,142 5,382 5,311 10,693 5,592 5,597 11,189 12,124 13,324

Impairment Charge 1,197 528 461 989 510 696 1,206 1,557 1,738

Pre-Tax Profit 8,945 4,854 4,850 9,704 5,082 4,901 9,983 10,567 11,586

Tax Expense 2,437 1,333 1,333 2,666 1,398 1,368 2,766 2,949 3,223

Minority Shareholders -10 -6 -6 -12 -8 -8 -16 -16 -16

Other Post Tax Items 226 134 -277 -143 170 0 170 0 0

Stated Net Profit 6,272 3,381 3,789 7,170 3,506 3,525 7,031 7,602 8,347

Extraordinary & Other Items 283 134 -277 -143 170 0 170 0 0

Hybrid Distributions -57 0 0 0 0 0 0 0 0

Derivatives & Hedging Revaluation 0 0 0 0 0 0 0 0 0

Macquarie Cash Profit 6,498 3,515 3,512 7,027 3,676 3,525 7,201 7,602 8,347

BALANCE SHEET & CAP AD (AUDm)

Risk Weighted Assets* 339,265 360,740 361,529 361,529 386,863 402,931 402,931 457,756 494,131

Interest Earning Assets 575,284 632,400 661,515 646,958 703,369 732,907 718,138 769,775 827,375

Gross Loans, Advances & Acceptances 473,774 513,615 525,534 525,534 561,907 585,505 585,505 625,567 672,329

Total Deposits 522,854 585,096 603,782 603,782 669,342 697,451 697,451 745,174 800,876

Total Assets 702,991 737,815 772,092 772,092 860,087 894,014 894,014 954,130 1,023,370

Shareholders Equity 45,615 47,038 49,284 49,284 52,051 56,673 56,673 62,651 66,663

Tier 1 Capital* 35,192 37,315 38,601 38,601 41,088 44,847 44,847 49,434 52,343

Tier 1 Ratio (%)* 10.37% 10.34% 10.68% 10.68% 10.62% 11.13% 11.13% 10.80% 10.59%

Core Tier 1 Ratio (%) - Basel III 8.49% 8.33% 8.79% 8.79% 8.72% 9.31% 9.31% 9.19% 9.11%

ASSET QUALITY

Impairment Charge / GLAA (bp) 25 21 18 19 19 24 21 25 26

Coverage (%) 102% 119% 136% 136% 149% 164% 164% 206% 266%

KEY RATIOS & GROWTH

Net Interest Income growth (%) 5.5% 3.5% 4.0% 8.0% 1.5% 3.7% 5.4% 7.5% 7.3%

Non-Interest Income growth (%) 2.5% 5.4% -5.2% 0.9% 10.7% -4.1% 5.5% 3.2% 5.9%

Total Revenue growth (%) 4.5% 4.0% 1.2% 5.8% 4.1% 1.4% 5.4% 6.3% 6.9%

Cost growth (%) 2.7% 2.0% 4.4% 6.4% 2.7% 2.9% 6.4% 3.8% 3.1%

Pre-Provision Profit growth (%) 6.1% 5.7% -1.3% 5.4% 5.3% 0.1% 4.6% 8.4% 9.9%

RWA growth (%) 13.0% 6.3% 0.2% 6.6% 7.0% 4.2% 11.5% 13.6% 7.9%

GLAA growth (%) 9.2% 8.4% 2.3% 10.9% 6.9% 4.2% 11.4% 6.8% 7.5%

Deposit growth (%) 11.0% 4.4% 2.4% 6.9% 8.8% 4.2% 13.3% 6.8% 7.5%

Net Interest Margin (%) 2.22% 2.14% 2.13% 2.13% 2.03% 2.02% 2.02% 2.03% 2.03%

Cost / Income Ratio (%) 44.8% 44.3% 45.7% 45.0% 45.1% 45.8% 45.4% 44.4% 42.8%

*B2.5 2012, B3 2013 onward

2.00%

2.10%

2.20%

2.30%

2.40%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2013 1H14 2H14 2014 1H15 2H15 2015 2016

Margins & VolumesNet Interest Margin (%) GLAA growth (%)

42.0%

44.0%

46.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

2013 1H14 2H14 2014 1H15 2H15 2015 2016

Efficiency

Cost / Income Ratio (%) Cost growth (%)

15

17

19

21

23

25

27

29

0%

50%

100%

150%

200%

250%

2013 1H14 2H14 2014 1H15 2H15 2015 2016

Asset QualityImpairment Charge / GLAA (bp) Coverage (%)

5.046.60

20.60

0.52

0.0

5.0

10.0

15.0

20.0

25.0

Total Stage 1 Dividends

Total Fade Period Dividends

Total Perpetuity Dividends

Total Surplus Capital Per Share

DDM Valuation

Macquarie Wealth Management Australian banks

3 September 2015 9

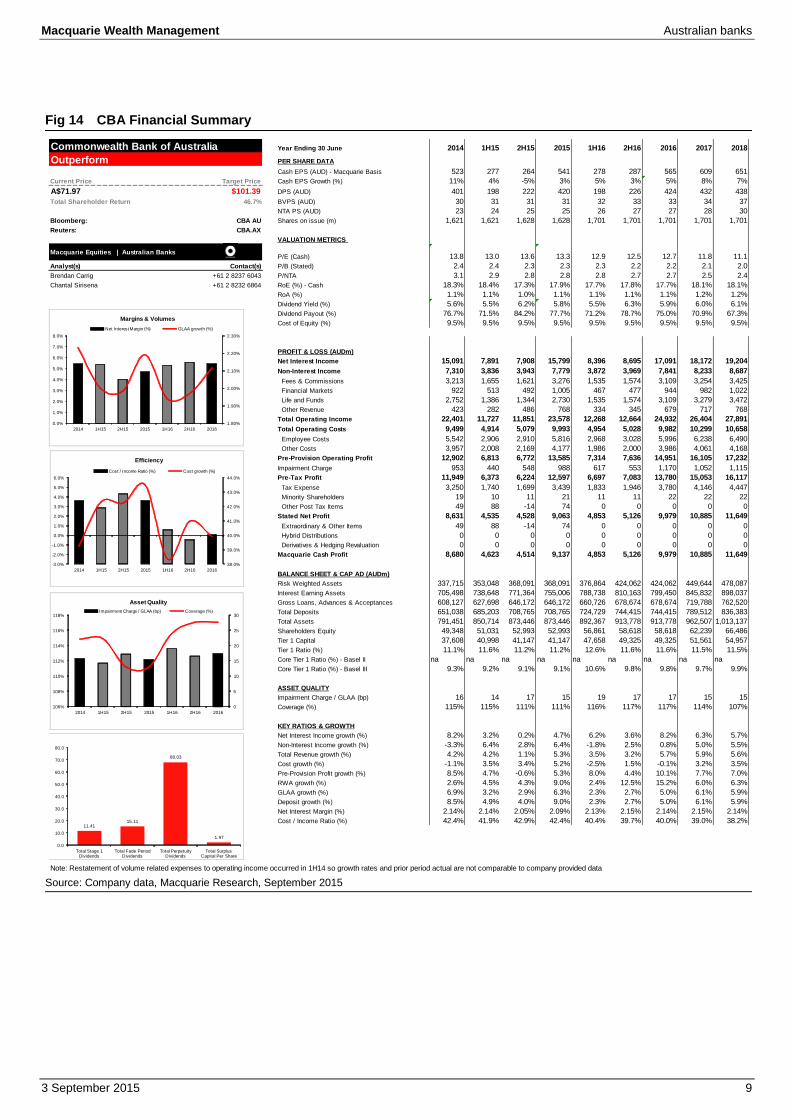

Fig 14 CBA Financial Summary

Source: Company data, Macquarie Research, September 2015

Commonwealth Bank of Australia Year Ending 30 June 2014 1H15 2H15 2015 1H16 2H16 2016 2017 2018

Outperform PER SHARE DATA

Cash EPS (AUD) - Macquarie Basis 523 277 264 541 278 287 565 609 651

Current Price Target Price Cash EPS Growth (%) 11% 4% -5% 3% 5% 3% 5% 8% 7%

A$71.97 $101.39 DPS (AUD) 401 198 222 420 198 226 424 432 438

Total Shareholder Return 46.7% BVPS (AUD) 30 31 31 31 32 33 33 34 37

NTA PS (AUD) 23 24 25 25 26 27 27 28 30

Bloomberg: CBA AU Shares on issue (m) 1,621 1,621 1,628 1,628 1,701 1,701 1,701 1,701 1,701

Reuters: CBA.AX

VALUATION METRICS

Macquarie Equities | Australian BanksP/E (Cash) 13.8 13.0 13.6 13.3 12.9 12.5 12.7 11.8 11.1

Analyst(s) Contact(s) P/B (Stated) 2.4 2.4 2.3 2.3 2.3 2.2 2.2 2.1 2.0

Brendan Carrig +61 2 8237 6043 P/NTA 3.1 2.9 2.8 2.8 2.8 2.7 2.7 2.5 2.4

Chantal Sirisena +61 2 8232 6864 RoE (%) - Cash 18.3% 18.4% 17.3% 17.9% 17.7% 17.8% 17.7% 18.1% 18.1%

RoA (%) 1.1% 1.1% 1.0% 1.1% 1.1% 1.1% 1.1% 1.2% 1.2%

Dividend Yield (%) 5.6% 5.5% 6.2% 5.8% 5.5% 6.3% 5.9% 6.0% 6.1%

Dividend Payout (%) 76.7% 71.5% 84.2% 77.7% 71.2% 78.7% 75.0% 70.9% 67.3%

Cost of Equity (%) 9.5% 9.5% 9.5% 9.5% 9.5% 9.5% 9.5% 9.5% 9.5%

PROFIT & LOSS (AUDm)

Net Interest Income 15,091 7,891 7,908 15,799 8,396 8,695 17,091 18,172 19,204

Non-Interest Income 7,310 3,836 3,943 7,779 3,872 3,969 7,841 8,233 8,687

Fees & Commissions 3,213 1,655 1,621 3,276 1,535 1,574 3,109 3,254 3,425

Financial Markets 922 513 492 1,005 467 477 944 982 1,022

Life and Funds 2,752 1,386 1,344 2,730 1,535 1,574 3,109 3,279 3,472

Other Revenue 423 282 486 768 334 345 679 717 768

Total Operating Income 22,401 11,727 11,851 23,578 12,268 12,664 24,932 26,404 27,891

Total Operating Costs 9,499 4,914 5,079 9,993 4,954 5,028 9,982 10,299 10,658

Employee Costs 5,542 2,906 2,910 5,816 2,968 3,028 5,996 6,238 6,490

Other Costs 3,957 2,008 2,169 4,177 1,986 2,000 3,986 4,061 4,168

Pre-Provision Operating Profit 12,902 6,813 6,772 13,585 7,314 7,636 14,951 16,105 17,232

Impairment Charge 953 440 548 988 617 553 1,170 1,052 1,115

Pre-Tax Profit 11,949 6,373 6,224 12,597 6,697 7,083 13,780 15,053 16,117

Tax Expense 3,250 1,740 1,699 3,439 1,833 1,946 3,780 4,146 4,447

Minority Shareholders 19 10 11 21 11 11 22 22 22

Other Post Tax Items 49 88 -14 74 0 0 0 0 0

Stated Net Profit 8,631 4,535 4,528 9,063 4,853 5,126 9,979 10,885 11,649

Extraordinary & Other Items 49 88 -14 74 0 0 0 0 0

Hybrid Distributions 0 0 0 0 0 0 0 0 0

Derivatives & Hedging Revaluation 0 0 0 0 0 0 0 0 0

Macquarie Cash Profit 8,680 4,623 4,514 9,137 4,853 5,126 9,979 10,885 11,649

BALANCE SHEET & CAP AD (AUDm)

Risk Weighted Assets 337,715 353,048 368,091 368,091 376,864 424,062 424,062 449,644 478,087

Interest Earning Assets 705,498 738,648 771,364 755,006 788,738 810,163 799,450 845,832 898,037

Gross Loans, Advances & Acceptances 608,127 627,698 646,172 646,172 660,726 678,674 678,674 719,788 762,520

Total Deposits 651,038 685,203 708,765 708,765 724,729 744,415 744,415 789,512 836,383

Total Assets 791,451 850,714 873,446 873,446 892,367 913,778 913,778 962,507 1,013,137

Shareholders Equity 49,348 51,031 52,993 52,993 56,861 58,618 58,618 62,239 66,486

Tier 1 Capital 37,608 40,998 41,147 41,147 47,658 49,325 49,325 51,561 54,957

Tier 1 Ratio (%) 11.1% 11.6% 11.2% 11.2% 12.6% 11.6% 11.6% 11.5% 11.5%

Core Tier 1 Ratio (%) - Basel II na na na na na na na na na

Core Tier 1 Ratio (%) - Basel III 9.3% 9.2% 9.1% 9.1% 10.6% 9.8% 9.8% 9.7% 9.9%

ASSET QUALITY

Impairment Charge / GLAA (bp) 16 14 17 15 19 17 17 15 15

Coverage (%) 115% 115% 111% 111% 116% 117% 117% 114% 107%

KEY RATIOS & GROWTH

Net Interest Income growth (%) 8.2% 3.2% 0.2% 4.7% 6.2% 3.6% 8.2% 6.3% 5.7%

Non-Interest Income growth (%) -3.3% 6.4% 2.8% 6.4% -1.8% 2.5% 0.8% 5.0% 5.5%

Total Revenue growth (%) 4.2% 4.2% 1.1% 5.3% 3.5% 3.2% 5.7% 5.9% 5.6%

Cost growth (%) -1.1% 3.5% 3.4% 5.2% -2.5% 1.5% -0.1% 3.2% 3.5%

Pre-Provision Profit growth (%) 8.5% 4.7% -0.6% 5.3% 8.0% 4.4% 10.1% 7.7% 7.0%

RWA growth (%) 2.6% 4.5% 4.3% 9.0% 2.4% 12.5% 15.2% 6.0% 6.3%

GLAA growth (%) 6.9% 3.2% 2.9% 6.3% 2.3% 2.7% 5.0% 6.1% 5.9%

Deposit growth (%) 8.5% 4.9% 4.0% 9.0% 2.3% 2.7% 5.0% 6.1% 5.9%

Net Interest Margin (%) 2.14% 2.14% 2.05% 2.09% 2.13% 2.15% 2.14% 2.15% 2.14%

Cost / Income Ratio (%) 42.4% 41.9% 42.9% 42.4% 40.4% 39.7% 40.0% 39.0% 38.2%

Note: Restatement of volume related expenses to operating income occurred in 1H14 so growth rates and prior period actual are not comparable to company provided data

1.80%

1.90%

2.00%

2.10%

2.20%

2.30%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

2014 1H15 2H15 2015 1H16 2H16 2016

Margins & Volumes

Net Interest Margin (%) GLAA growth (%)

38.0%

39.0%

40.0%

41.0%

42.0%

43.0%

44.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2014 1H15 2H15 2015 1H16 2H16 2016

Efficiency

Cost / Income Ratio (%) Cost growth (%)

0

5

10

15

20

25

30

106%

108%

110%

112%

114%

116%

118%

2014 1H15 2H15 2015 1H16 2H16 2016

Asset Quality

Impairment Charge / GLAA (bp) Coverage (%)

11.4115.11

68.03

1.97

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

Total Stage 1 Dividends

Total Fade Period Dividends

Total Perpetuity Dividends

Total Surplus Capital Per Share

Macquarie Wealth Management Australian banks

3 September 2015 10

Fig 15 NAB Financial Summary

Source: Company data, Macquarie Research, September 2015

National Australia Bank Year Ending 30 September 2013 1H14 2H14 2014 1H15 2H15 2015 2016 2017

Outperform PER SHARE DATA

Cash EPS (AUD) - Macquarie Basis 251 131 85 216 136 135 271 283 307

Current Price Target Price Cash EPS Growth (%) 5% 3% -35% -14% 60% -1% 25% 5% 8%

A$29.93 $40.50 DPS (AUD) 190 99 99 198 99 99 198 201 207

Total Shareholder Return 41.9% BVPS (AUD) 17.89 18.21 18.41 18.41 18.97 19.01 19.01 20.06 21.26

NTA PS (AUD) 14.64 14.88 15.15 15.15 15.65 16.16 16.16 17.00 17.98

Bloomberg: NAB AU Shares on issue (m) 2,349 2,354 2,366 2,366 2,421 2,624 2,624 2,646 2,666

Reuters: NAB.AX

VALUATION METRICS

Macquarie Equities | Australian BanksP/E (Cash) 11.9 11.4 17.6 13.8 11.0 11.1 11.0 10.6 9.8

Analyst(s) Contact(s) P/B (Stated) 1.7 1.6 1.6 1.6 1.6 1.6 1.6 1.5 1.4

Brendan Carrig +61 2 8237 6043 P/NTA 2.0 2.0 2.0 2.0 1.9 1.9 1.9 1.8 1.7

Chantal Sirisena +61 2 8237 6864 RoE (%) 12.2% 13.6% 8.6% 11.1% 13.7% 13.1% 13.4% 13.2% 13.6%

RoA (%) 0.7% 0.7% 0.5% 0.6% 0.7% 0.7% 0.7% 0.8% 0.8%

Dividend Yield (%) 6.3% 3.3% 3.3% 6.6% 3.3% 3.3% 6.6% 6.7% 6.9%

Dividend Payout (%) 75.8% 75.4% 116.3% 91.5% 72.7% 73.4% 73.1% 70.9% 67.5%

Sustainable RoE used in Valuation (%) 12.8% 12.8% 12.8% 12.8% 12.8% 12.8% 12.8% 12.8% 12.8%

Cost of Equity (%) 9.6% 9.6% 9.6% 9.6% 9.6% 9.6% 9.6% 9.6% 9.6%

PROFIT & LOSS (AUDm)

Net Interest Income 13,407 6,843 6,932 13,775 7,121 7,251 14,372 15,786 16,729

Non-Interest Income 5,173 2,644 2,494 5,138 2,663 2,675 5,338 5,538 5,718

Fees & Commissions 3,561 1,804 1,848 3,652 1,221 1,261 2,482 2,616 2,673

Financial Markets 769 249 750 999 456 470 926 968 1,007

Life and Funds 1,335 723 717 1,440 781 801 1,582 1,651 1,717

Other Revenue -492 -132 -821 -953 205 143 348 303 321

Total Operating Income 18,580 9,487 9,426 18,913 9,784 9,926 19,710 21,324 22,447

Total Operating Costs 8,174 4,456 5,724 10,180 4,460 5,428 9,888 9,427 9,467

Employee Costs 4,362 2,292 2,240 4,532 2,329 2,376 4,705 4,319 4,493

Other Costs 3,812 2,164 3,484 5,648 2,131 3,052 5,183 5,109 4,974

Pre-Provision Operating Profit 10,406 5,031 3,702 8,733 5,324 4,499 9,823 11,897 12,980

Impairment Charge 1,934 528 349 877 455 394 849 929 1,028

Pre-Tax Profit 8,472 4,503 3,353 7,856 4,869 4,105 8,974 10,967 11,952

Tax Expense 2,337 1,263 1,229 2,492 1,424 1,173 2,597 3,159 3,444

Minority Shareholders -8 -3 0 -3 -20 0 -20 0 0

Other Post Tax Items 675 381 -315 66 -15 0 -15 0 0

Stated Net Profit 5,452 2,856 2,439 5,295 3,440 2,932 6,372 7,809 8,508

Extraordinary & Other Items 675 384 -315 69 -11 633 622 0 0

Hybrid Distributions -188 -90 -90 -180 -109 -109 -218 -218 -218

IoRE/Non Controlling Interest -3 0 0 0 0 0 0 0 0

Derivatives & Hedging Revaluation 0 0 0 0 0 0 0 0 0

Macquarie Cash Profit 5,936 3,150 2,034 5,184 3,320 3,456 6,776 7,591 8,290

BALANCE SHEET & CAP AD (AUDm)

Risk Weighted Assets * 362,078 367,224 367,652 367,652 393,238 389,109 389,109 445,901 471,239

Interest Earning Assets 662,028 707,170 715,993 711,582 745,411 757,524 751,468 792,694 840,042

Gross Loans, Advances & Acceptances 521,757 534,172 545,361 545,361 573,490 582,809 582,809 619,565 654,876

Total Deposits 559,238 582,739 599,059 599,059 634,650 644,341 644,341 684,977 724,016

Total Assets 808,427 846,014 883,301 883,301 958,587 969,376 969,376 1,019,303 1,067,866

Shareholders Equity 46,620 47,478 47,908 47,908 49,868 55,810 55,810 59,192 63,081

Tier 1 Capital 37,480 39,774 39,758 39,758 43,752 47,580 47,580 50,049 53,065

Tier 1 Ratio (%) * 10.4% 10.8% 10.8% 10.8% 11.1% 12.2% 12.2% 11.2% 11.3%

Core Tier 1 Ratio (%) - Basel III 8.4% 8.6% 8.63% 8.6% 8.9% 10.0% 10.0% 9.2% 9.4%

ASSET QUALITY

Impairment Charge / GLAA (bp) 37 20 13 16 16 14 15 15 16

Coverage (%) 63% 68% 76% 76% 146% 140% 140% 132% 125%

KEY RATIOS & GROWTH

Net Interest Income growth (%) 0.8% 0.6% 1.3% 2.7% 2.7% 1.8% 4.3% 9.8% 6.0%

Non-Interest Income growth (%) 5.0% 4.5% -5.7% -0.7% 6.8% 0.5% 3.9% 3.7% 3.2%

Total Revenue growth (%) 2.0% 1.7% -0.6% 1.8% 3.8% 1.5% 4.2% 8.2% 5.3%

Cost growth (%) 4.4% 6.1% 28.5% 24.5% -22.1% 21.7% -2.9% -4.7% 0.4%

Pre-Provision Profit growth (%) 0.1% -2.0% -26.4% -16.1% 43.8% -15.5% 12.5% 21.1% 9.1%

RWA growth (%) 9.3% 1.4% 0.1% 1.5% 7.0% -1.1% 5.8% 14.6% 5.7%

GLAA growth (%) 4.2% 2.4% 2.1% 4.5% 5.2% 1.6% 6.9% 6.3% 5.7%

Deposit growth (%) 4.9% 2.8% 4.1% 7.1% 3.8% 1.6% 5.4% 6.3% 5.7%

Net Interest Margin (%) 2.03% 1.94% 1.94% 1.94% 1.91% 1.91% 1.91% 1.99% 1.99%

Cost / Income Ratio (%) 44.0% 47.0% 60.7% 53.8% 45.6% 54.7% 50.2% 44.2% 42.2%

*B2.5 2012, B3 2013 onward

0.0%

0.5%

1.0%

1.5%

2.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

2013 1H14 2H14 2014 1H15 2H15 2015 2016

Margins & Volumes

Net Interest Margin (%) GLAA growth (%)

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

2013 1H14 2H14 2014 1H15 2H15 2015 2016

Efficiency

Cost / Income Ratio (%) Cost growth (%)

10

15

20

25

30

35

40

60%

70%

80%

90%

100%

110%

120%

130%

140%

150%

160%

2013 1H14 2H14 2014 1H15 2H15 2015 2016

Asset Quality

Impairment Charge / GLAA (bp) Coverage (%)

5.647.42

24.58

1.14

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Total Stage 1 Dividends

Total Fade Period Dividends

Total Perpetuity Dividends

Total Surplus Capital Per Share

DDM Valuation

Macquarie Wealth Management Australian banks

3 September 2015 11

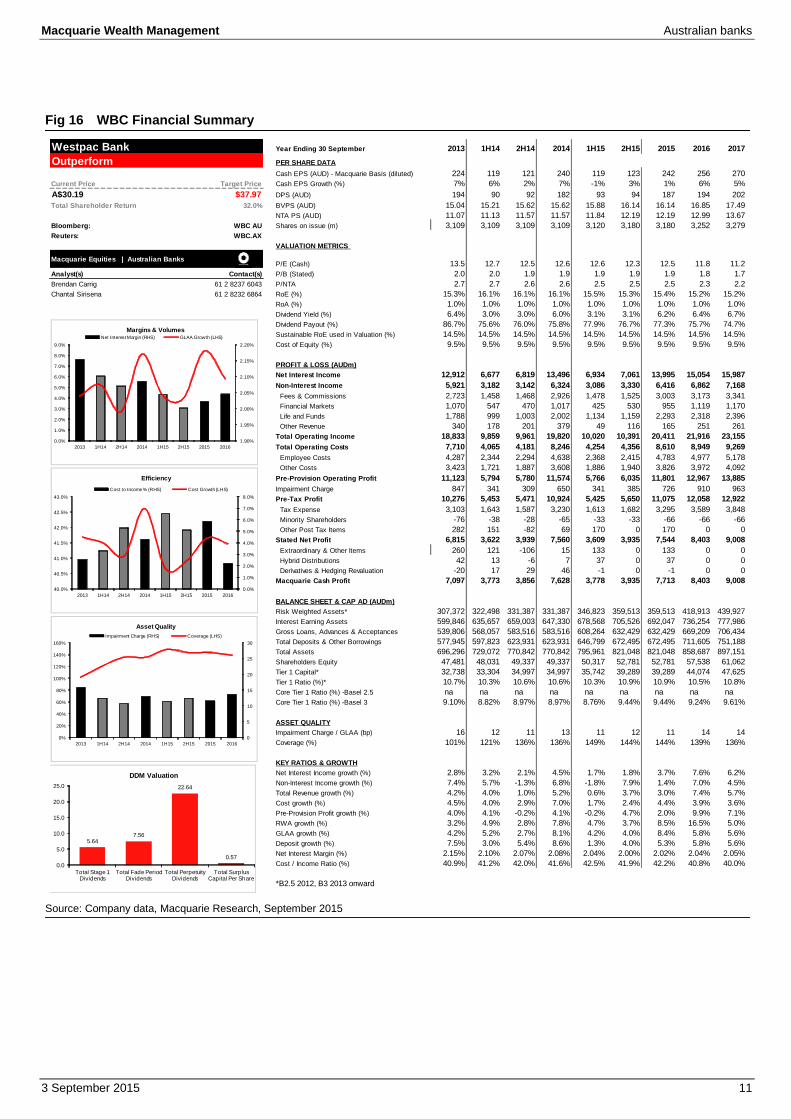

Fig 16 WBC Financial Summary

Source: Company data, Macquarie Research, September 2015

Westpac Bank Year Ending 30 September 2013 1H14 2H14 2014 1H15 2H15 2015 2016 2017

Outperform PER SHARE DATA

Cash EPS (AUD) - Macquarie Basis (diluted) 224 119 121 240 119 123 242 256 270

Current Price Target Price Cash EPS Growth (%) 7% 6% 2% 7% -1% 3% 1% 6% 5%

A$30.19 $37.97 DPS (AUD) 194 90 92 182 93 94 187 194 202

Total Shareholder Return 32.0% BVPS (AUD) 15.04 15.21 15.62 15.62 15.88 16.14 16.14 16.85 17.49

NTA PS (AUD) 11.07 11.13 11.57 11.57 11.84 12.19 12.19 12.99 13.67

Bloomberg: WBC AU Shares on issue (m) 3,109 3,109 3,109 3,109 3,120 3,180 3,180 3,252 3,279

Reuters: WBC.AX

VALUATION METRICS

Macquarie Equities | Australian BanksP/E (Cash) 13.5 12.7 12.5 12.6 12.6 12.3 12.5 11.8 11.2

Analyst(s) Contact(s) P/B (Stated) 2.0 2.0 1.9 1.9 1.9 1.9 1.9 1.8 1.7

Brendan Carrig +61 2 8237 6043 P/NTA 2.7 2.7 2.6 2.6 2.5 2.5 2.5 2.3 2.2

Chantal Sirisena +61 2 8232 6864 RoE (%) 15.3% 16.1% 16.1% 16.1% 15.5% 15.3% 15.4% 15.2% 15.2%

RoA (%) 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0%

Dividend Yield (%) 6.4% 3.0% 3.0% 6.0% 3.1% 3.1% 6.2% 6.4% 6.7%

Dividend Payout (%) 86.7% 75.6% 76.0% 75.8% 77.9% 76.7% 77.3% 75.7% 74.7%

Sustainable RoE used in Valuation (%) 14.5% 14.5% 14.5% 14.5% 14.5% 14.5% 14.5% 14.5% 14.5%

Cost of Equity (%) 9.5% 9.5% 9.5% 9.5% 9.5% 9.5% 9.5% 9.5% 9.5%

PROFIT & LOSS (AUDm)

Net Interest Income 12,912 6,677 6,819 13,496 6,934 7,061 13,995 15,054 15,987

Non-Interest Income 5,921 3,182 3,142 6,324 3,086 3,330 6,416 6,862 7,168

Fees & Commissions 2,723 1,458 1,468 2,926 1,478 1,525 3,003 3,173 3,341

Financial Markets 1,070 547 470 1,017 425 530 955 1,119 1,170

Life and Funds 1,788 999 1,003 2,002 1,134 1,159 2,293 2,318 2,396

Other Revenue 340 178 201 379 49 116 165 251 261

Total Operating Income 18,833 9,859 9,961 19,820 10,020 10,391 20,411 21,916 23,155

Total Operating Costs 7,710 4,065 4,181 8,246 4,254 4,356 8,610 8,949 9,269

Employee Costs 4,287 2,344 2,294 4,638 2,368 2,415 4,783 4,977 5,178

Other Costs 3,423 1,721 1,887 3,608 1,886 1,940 3,826 3,972 4,092

Pre-Provision Operating Profit 11,123 5,794 5,780 11,574 5,766 6,035 11,801 12,967 13,885

Impairment Charge 847 341 309 650 341 385 726 910 963

Pre-Tax Profit 10,276 5,453 5,471 10,924 5,425 5,650 11,075 12,058 12,922

Tax Expense 3,103 1,643 1,587 3,230 1,613 1,682 3,295 3,589 3,848

Minority Shareholders -76 -38 -28 -65 -33 -33 -66 -66 -66

Other Post Tax Items 282 151 -82 69 170 0 170 0 0

Stated Net Profit 6,815 3,622 3,939 7,560 3,609 3,935 7,544 8,403 9,008

Extraordinary & Other Items 260 121 -106 15 133 0 133 0 0

Hybrid Distributions 42 13 -6 7 37 0 37 0 0

Derivatives & Hedging Revaluation -20 17 29 46 -1 0 -1 0 0

Macquarie Cash Profit 7,097 3,773 3,856 7,628 3,778 3,935 7,713 8,403 9,008

BALANCE SHEET & CAP AD (AUDm)

Risk Weighted Assets* 307,372 322,498 331,387 331,387 346,823 359,513 359,513 418,913 439,927

Interest Earning Assets 599,846 635,657 659,003 647,330 678,568 705,526 692,047 736,254 777,986

Gross Loans, Advances & Acceptances 539,806 568,057 583,516 583,516 608,264 632,429 632,429 669,209 706,434

Total Deposits & Other Borrowings 577,945 597,823 623,931 623,931 646,799 672,495 672,495 711,605 751,188

Total Assets 696,296 729,072 770,842 770,842 795,961 821,048 821,048 858,687 897,151

Shareholders Equity 47,481 48,031 49,337 49,337 50,317 52,781 52,781 57,538 61,062

Tier 1 Capital* 32,738 33,304 34,997 34,997 35,742 39,289 39,289 44,074 47,625

Tier 1 Ratio (%)* 10.7% 10.3% 10.6% 10.6% 10.3% 10.9% 10.9% 10.5% 10.8%

Core Tier 1 Ratio (%) -Basel 2.5 na na na na na na na na na

Core Tier 1 Ratio (%) -Basel 3 9.10% 8.82% 8.97% 8.97% 8.76% 9.44% 9.44% 9.24% 9.61%

ASSET QUALITY

Impairment Charge / GLAA (bp) 16 12 11 13 11 12 11 14 14

Coverage (%) 101% 121% 136% 136% 149% 144% 144% 139% 136%

KEY RATIOS & GROWTH

Net Interest Income growth (%) 2.8% 3.2% 2.1% 4.5% 1.7% 1.8% 3.7% 7.6% 6.2%

Non-Interest Income growth (%) 7.4% 5.7% -1.3% 6.8% -1.8% 7.9% 1.4% 7.0% 4.5%

Total Revenue growth (%) 4.2% 4.0% 1.0% 5.2% 0.6% 3.7% 3.0% 7.4% 5.7%

Cost growth (%) 4.5% 4.0% 2.9% 7.0% 1.7% 2.4% 4.4% 3.9% 3.6%

Pre-Provision Profit growth (%) 4.0% 4.1% -0.2% 4.1% -0.2% 4.7% 2.0% 9.9% 7.1%

RWA growth (%) 3.2% 4.9% 2.8% 7.8% 4.7% 3.7% 8.5% 16.5% 5.0%

GLAA growth (%) 4.2% 5.2% 2.7% 8.1% 4.2% 4.0% 8.4% 5.8% 5.6%

Deposit growth (%) 7.5% 3.0% 5.4% 8.6% 1.3% 4.0% 5.3% 5.8% 5.6%

Net Interest Margin (%) 2.15% 2.10% 2.07% 2.08% 2.04% 2.00% 2.02% 2.04% 2.05%

Cost / Income Ratio (%) 40.9% 41.2% 42.0% 41.6% 42.5% 41.9% 42.2% 40.8% 40.0%

*B2.5 2012, B3 2013 onward

1.90%

1.95%

2.00%

2.05%

2.10%

2.15%

2.20%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

2013 1H14 2H14 2014 1H15 2H15 2015 2016

Margins & VolumesNet Interest Margin (RHS) GLAA Growth (LHS)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

40.0%

40.5%

41.0%

41.5%

42.0%

42.5%

43.0%

2013 1H14 2H14 2014 1H15 2H15 2015 2016

Efficiency

Cost to Income % (RHS) Cost Growth (LHS)

0

5

10

15

20

25

30

0%

20%

40%

60%

80%

100%

120%

140%

160%

2013 1H14 2H14 2014 1H15 2H15 2015 2016

Asset Quality

Impairment Charge (RHS) Coverage (LHS)

5.647.56

22.64

0.57

0.0

5.0

10.0

15.0

20.0

25.0

Total Stage 1 Dividends

Total Fade Period Dividends

Total Perpetuity Dividends

Total Surplus Capital Per Share

DDM Valuation

Macquarie Wealth Management Australian banks

3 September 2015 12

Important disclosures:

Recommendation definitions

Macquarie - Australia/New Zealand Outperform – return >3% in excess of benchmark return Neutral – return within 3% of benchmark return Underperform – return >3% below benchmark return Benchmark return is determined by long term nominal GDP growth plus 12 month forward market dividend yield

Macquarie – Asia/Europe Outperform – expected return >+10% Neutral – expected return from -10% to +10% Underperform – expected return <-10%

Macquarie First South - South Africa Outperform – expected return >+10% Neutral – expected return from -10% to +10% Underperform – expected return <-10%

Macquarie - Canada

Outperform – return >5% in excess of benchmark return Neutral – return within 5% of benchmark return Underperform – return >5% below benchmark return

Macquarie - USA Outperform (Buy) – return >5% in excess of Russell 3000 index return Neutral (Hold) – return within 5% of Russell 3000 index return Underperform (Sell)– return >5% below Russell 3000 index return

Volatility index definition*

This is calculated from the volatility of historical price movements. Very high–highest risk – Stock should be

expected to move up or down 60–100% in a year – investors should be aware this stock is highly speculative. High – stock should be expected to move up or down at least 40–60% in a year – investors should be aware this stock could be speculative. Medium – stock should be expected to move up or down at least 30–40% in a year. Low–medium – stock should be expected to move up or down at least 25–30% in a year. Low – stock should be expected to move up or down at least 15–25% in a year. * Applicable to Asia/Australian/NZ/Canada stocks only

Recommendations – 12 months Note: Quant recommendations may differ from Fundamental Analyst recommendations

Financial definitions

All "Adjusted" data items have had the following adjustments made: Added back: goodwill amortisation, provision for catastrophe reserves, IFRS derivatives & hedging, IFRS impairments & IFRS interest expense Excluded: non recurring items, asset revals, property revals, appraisal value uplift, preference dividends & minority interests EPS = adjusted net profit / efpowa* ROA = adjusted ebit / average total assets ROA Banks/Insurance = adjusted net profit /average total assets ROE = adjusted net profit / average shareholders funds Gross cashflow = adjusted net profit + depreciation *equivalent fully paid ordinary weighted average number of shares All Reported numbers for Australian/NZ listed stocks are modelled under IFRS (International Financial Reporting Standards).

Recommendation proportions – For quarter ending 30 June 2015

AU/NZ Asia RSA USA CA EUR Outperform 46.23% 58.36% 47.27% 44.20% 60.65% 43.01% (for US coverage by MCUSA, 9.68% of stocks followed are investment banking clients)

Neutral 37.67% 25.65% 29.09% 49.29% 34.19% 40.93% (for US coverage by MCUSA, 5.53% of stocks followed are investment banking clients)

Underperform 16.10% 15.99% 23.64% 6.52% 5.16% 16.06% (for US coverage by MCUSA, 1.38% of stocks followed are investment banking clients)

ANZ AU vs ASX 100, & rec history

(all figures in AUD currency unless noted)

CBA AU vs ASX 100, & rec history

(all figures in AUD currency unless noted)

WBC AU vs ASX 100, & rec history

(all figures in AUD currency unless noted)

NAB AU vs ASX 100, & rec history

(all figures in AUD currency unless noted)

Note: Recommendation timeline – if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, September 2015

12-month target price methodology

ANZ AU: A$34.15 based on a DDM/PE methodology

CBA AU: A$101.39 based on a DDM/PE methodology

WBC AU: A$37.97 based on a DDM methodology

NAB AU: A$40.50 based on a DDM/PE methodology

Company-specific disclosures: ANZ AU: MACQUARIE CAPITAL (NEW ZEALAND) LIMITED or one of its affiliates managed or co-managed a public offering of securities of Australia and New Zealand Banking Group Ltd in the past 12 months, for which it received compensation. WBC AU: MACQUARIE CAPITAL (AUSTRALIA) LIMITED or one of its affiliates managed or co-managed a public offering of securities of Westpac Banking Corp in the past 12 months, for which it received compensation. MACQUARIE CAPITAL (AUSTRALIA) LIMITED or one of its affiliates managed or co-managed a public offering of securities of Westpac Banking Corp in the past 24 months, for which it received compensation. MACQUARIE EQUITIES LIMITED or one of its affiliates is currently managing or co-managing a public offering of securities of Westpac Banking Corp. NAB AU: Macquarie and its affiliates collectively and beneficially own or control 1% or more of any class of National Australia Bank's equity securities. MACQUARIE EQUITIES LIMITED or one of its affiliates managed or co-managed a public offering of securities of National Australia Bank Ltd in the past 12 months, for which it received compensation. MACQUARIE CAPITAL (AUSTRALIA) LIMITED or one of its affiliates managed or co-managed a public offering of securities of National Australia Bank Ltd in the past 12 months, for which it received compensation. Macquarie Capital (Australia) Limited or one of its affiliates may provide National Australia Bank Limited investment advisory services for which it may or may not receive compensation.

Macquarie Wealth Management Australian banks

3 September 2015 13

Important disclosure information regarding the subject companies covered in this report is available at www.macquarie.com/disclosures.

Target price risk disclosures: ANZ AU: Any inability to compete successfully in their markets may harm the business. This could be a result of many factors which may include geographic mix and introduction of improved products or service offerings by competitors. The results of operations may be materially affected by global economic conditions generally, including conditions in financial markets. The company is exposed to market risks, such as changes in interest rates, foreign exchange rates and input prices. From time to time, the company will enter into transactions, including transactions in derivative instruments, to manage certain of these exposures. CBA AU: Any inability to compete successfully in their markets may harm the business. This could be a result of many factors which may include geographic mix and introduction of improved products or service offerings by competitors. The results of operations may be materially affected by global economic conditions generally, including conditions in financial markets. The company is exposed to market risks, such as changes in interest rates, foreign exchange rates and input prices. From time to time, the company will enter into transactions, including transactions in derivative instruments, to manage certain of these exposures. WBC AU: Any inability to compete successfully in their markets may harm the business. This could be a result of many factors which may include geographic mix and introduction of improved products or service offerings by competitors. The results of operations may be materially affected by global economic conditions generally, including conditions in financial markets. The company is exposed to market risks, such as changes in interest rates, foreign exchange rates and input prices. From time to time, the company will enter into transactions, including transactions in derivative instruments, to manage certain of these exposures. NAB AU: Any inability to compete successfully in their markets may harm the business. This could be a result of many factors which may include geographic mix and introduction of improved products or service offerings by competitors. The results of operations may be materially affected by global economic conditions generally, including conditions in financial markets. The company is exposed to market risks, such as changes in interest rates, foreign exchange rates and input prices. From time to time, the company will enter into transactions, including transactions in derivative instruments, to manage certain of these exposures.

Analyst certification: The views expressed in this research reflect the personal views of the analyst(s) about the subject securities or issuers and no part of the compensation of the analyst(s) was, is, or will be directly or indirectly related to the inclusion of specific recommendations or views in this research. The analyst principally responsible for the preparation of this research receives compensation based on overall revenues of Macquarie Group Ltd (ABN 94 122 169 279, AFSL No. 318062) (“MGL”) and its related entities (the “Macquarie Group”) and has taken reasonable care to achieve and maintain independence and objectivity in making any recommendations. General disclosure: This research has been issued by Macquarie Securities (Australia) Limited (ABN 58 002 832 126, AFSL No. 238947) a Participant of the Australian Securities Exchange (ASX) and Chi-X Australia Pty Limited. This research is distributed in Australia by Macquarie Equities Limited (ABN 41 002 574 923, AFSL No. 237504) ("MEL"), a Participant of the ASX, and in New Zealand by Macquarie Equities New Zealand Limited (“MENZ”) an NZX Firm. Macquarie Private Wealth’s services in New Zealand are provided by MENZ. Macquarie Bank Limited (ABN 46 008 583 542, AFSL No. 237502) (“MBL”) is a company incorporated in Australia and authorised under the Banking Act 1959 (Australia) to conduct banking business in Australia. None of MBL, MGL or MENZ is registered as a bank in New Zealand by the Reserve Bank of New Zealand under the Reserve Bank of New Zealand Act 1989. Any MGL subsidiary noted in this research, apart from MBL, is not an authorised deposit-taking institution for the purposes of the Banking Act 1959 (Australia) and that subsidiary’s obligations do not represent deposits or other liabilities of MBL. MBL does not guarantee or otherwise provide assurance in respect of the obligations of that subsidiary, unless noted otherwise. This research is general advice and does not take account of your objectives, financial situation or needs. Before acting on this general advice, you should consider the appropriateness of the advice having regard to your situation. We recommend you obtain financial, legal and taxation advice before making any financial investment decision. This research has been prepared for the use of the clients of the Macquarie Group and must not be copied, either in whole or in part, or distributed to any other person. If you are not the intended recipient, you must not use or disclose this research in any way. If you received it in error, please tell us immediately by return e-mail and delete the document. We do not guarantee the integrity of any e-mails or attached files and are not responsible for any changes made to them by any other person. Nothing in this research shall be construed as a solicitation to buy or sell any security or product, or to engage in or refrain from engaging in any transaction. This research is based on information obtained from sources believed to be reliable, but the Macquarie Group does not make any representation or warranty that it is accurate, complete or up to date. We accept no obligation to correct or update the information or opinions in it. Opinions expressed are subject to change without notice. The Macquarie Group accepts no liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this research and/or further communication in relation to this research. The Macquarie Group produces a variety of research products, recommendations contained in one type of research product may differ from recommendations contained in other types of research. The Macquarie Group has established and implemented a conflicts policy at group level, which may be revised and updated from time to time, pursuant to regulatory requirements; which sets out how we must seek to identify and manage all material conflicts of interest. The Macquarie Group, its officers and employees may have conflicting roles in the financial products referred to in this research and, as such, may effect transactions which are not consistent with the recommendations (if any) in this research. The Macquarie Group may receive fees, brokerage or commissions for acting in those capacities and the reader should assume that this is the case. The Macquarie Group‘s employees or officers may provide oral or written opinions to its clients which are contrary to the opinions expressed in this research. Important disclosure information regarding the subject companies covered in this report is available at www.macquarie.com/disclosures.