3q/02 - lla default homepage · pdf filereceived auditor 2888 jan -7 ahkj--2u concordia parish...

TRANSCRIPT

RECEIVEDAUDITOR

2888 JAN -7 AHKJ--2U

CONCORDIA PARISH SHERIFFVidalia, Louisiana

Annual Financial Statementsand Independent Auditors' Report

as of June 30,2007with Supplemental Information Schedules

Under provisions of state law, this report is a publicdocument. A copy of the report has been submitted tothe entity and other appropriate public officials. Thereport is available for public inspection at the BatonRouge office of the Legislative Auditor and, whereappropriate, at the office of the parish clerk of court.

//3Q/02

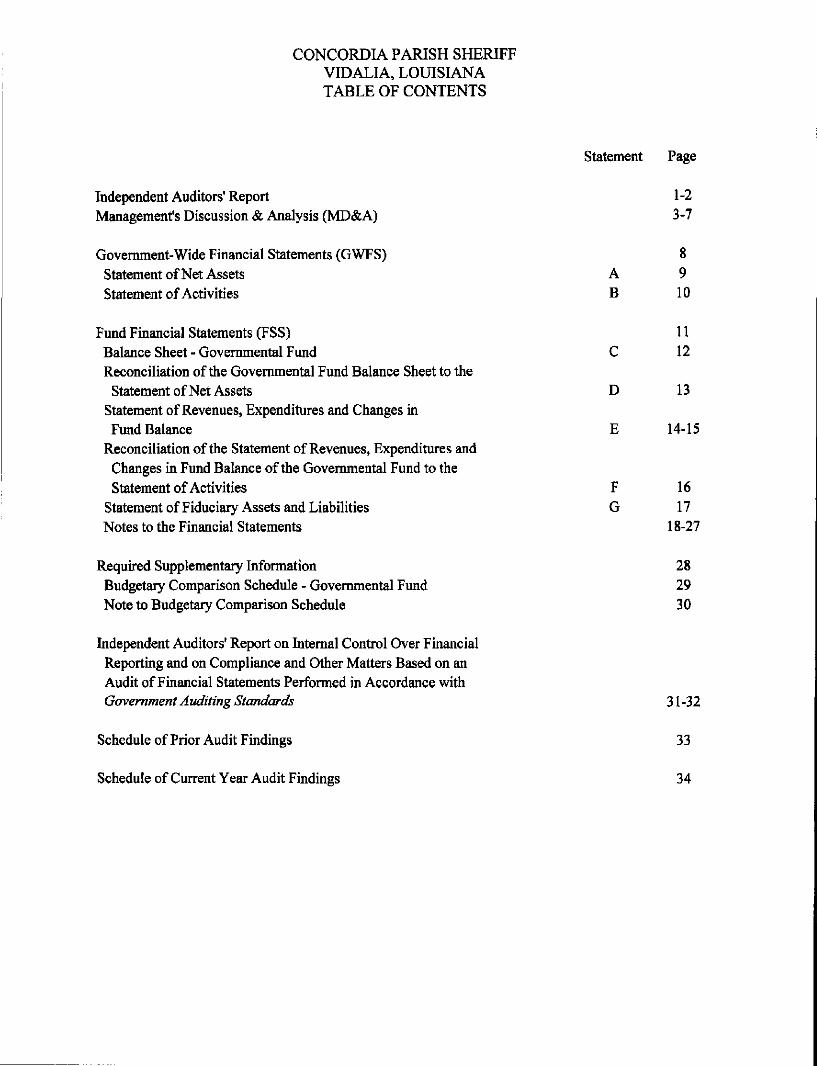

CONCORDIA PARISH SHERIFFVIDALIA, LOUISIANATABLE OF CONTENTS

Statement Page

Independent Auditors' Report 1-2Management's Discussion & Analysis (MD&A) 3-7

Government-Wide Financial Statements (GWFS) 8Statement of Net Assets A 9Statement of Activities B 10

Fund Financial Statements (FSS) 11Balance Sheet - Governmental Fund C 12Reconciliation of the Governmental Fund Balance Sheet to the

Statement of Net Assets D 13Statement of Revenues, Expenditures and Changes inFund Balance E 14-15

Reconciliation of the Statement of Revenues, Expenditures andChanges in Fund Balance of the Governmental Fund to theStatement of Activities F 16

Statement of Fiduciary Assets and Liabilities G 17Notes to the Financial Statements 18-27

Required Supplementary Information 28Budgetary Comparison Schedule - Governmental Fund 29Note to Budgetary Comparison Schedule 30

Independent Auditors' Report on Internal Control Over FinancialReporting and on Compliance and Other Matters Based on anAudit of Financial Statements Performed in Accordance withGovernment Auditing Standards 31 -32

Schedule of Prior Audit Findings 33

Schedule of Current Year Audit Findings 34

SWITZER, HOPKINS & MANGECertified Public Accountants

POST OFFICE BOX 478FERRIDAY, LOUISIANA 71334

DENNIS R. SWITZER, CPAH. MYLES HOPKINS, CPA

SUSAN L. MANGE, CPA

JOHN M. JONES, CPA 1921 -1983

1840 NORTH E.E. WALLACE BLVD.FERRIDAY, LOUISIANA 71334

TELEPHONE (318) 757-2600

FAX (3181 757-7206OFFICES IN NATCHEZ, MISSISSIPPI

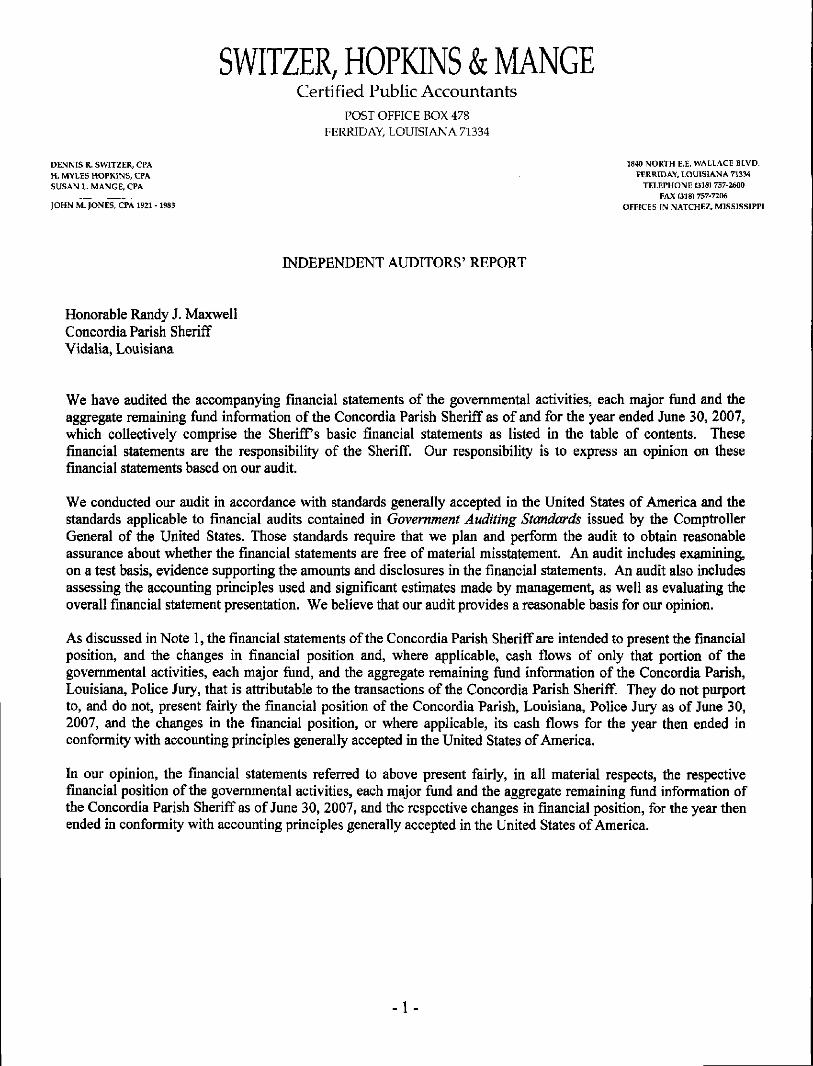

INDEPENDENT AUDITORS' REPORT

Honorable Randy J. MaxwellConcordia Parish SheriffVidalia, Louisiana

We have audited the accompanying financial statements of the governmental activities, each major fund and theaggregate remaining fund information of the Concordia Parish Sheriff as of and for the year ended June 30, 2007,which collectively comprise the Sheriffs basic financial statements as listed in the table of contents. Thesefinancial statements are the responsibility of the Sheriff. Our responsibility is to express an opinion on thesefinancial statements based on our audit.

We conducted our audit in accordance with standards generally accepted in the United States of America and thestandards applicable to financial audits contained in Government Auditing Standards issued by the ComptrollerGeneral of the United States. Those standards require that we plan and perform the audit to obtain reasonableassurance about whether the financial statements are free of material misstatement. An audit includes examining,on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includesassessing the accounting principles used and significant estimates made by management, as well as evaluating theoverall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

As discussed in Note 1, the financial statements of the Concordia Parish Sheriff are intended to present the financialposition, and the changes in financial position and, where applicable, cash flows of only that portion of thegovernmental activities, each major fund, and the aggregate remaining fund information of the Concordia Parish,Louisiana, Police Jury, that is attributable to the transactions of the Concordia Parish Sheriff. They do not purportto, and do not, present fairly the financial position of the Concordia Parish, Louisiana, Police Jury as of June 30,2007, and the changes in the financial position, or where applicable, its cash flows for the year then ended inconformity with accounting principles generally accepted in the United States of America.

In our opinion, the financial statements referred to above present fairly, in all material respects, the respectivefinancial position of the governmental activities, each major fund and the aggregate remaining fund information ofthe Concordia Parish Sheriff as of June 30, 2007, and the respective changes in financial position, for the year thenended in conformity with accounting principles generally accepted in the United States of America.

- 1 -

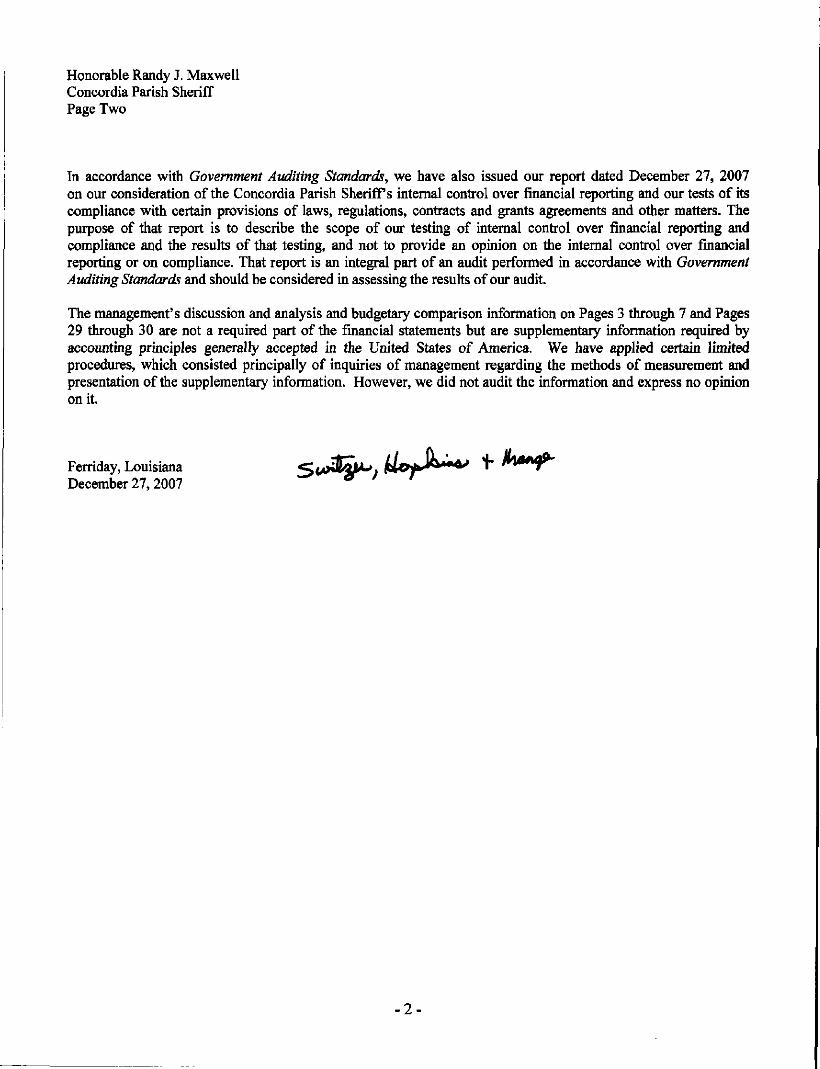

Honorable Randy J. MaxwellConcordia Parish SheriffPage Two

In accordance with Government Auditing Standards, we have also issued our report dated December 27, 2007on our consideration of the Concordia Parish Sheriffs internal control over financial reporting and our tests of itscompliance with certain provisions of laws, regulations, contracts and grants agreements and other matters. Thepurpose of that report is to describe the scope of our testing of internal control over financial reporting andcompliance and the results of that testing, and not to provide an opinion on the internal control over financialreporting or on compliance. That report is an integral part of an audit performed in accordance with GovernmentAuditing Standards and should be considered in assessing the results of our audit.

The management's discussion and analysis and budgetary comparison information on Pages 3 through 7 and Pages29 through 30 are not a required part of the financial statements but are supplementary information required byaccounting principles generally accepted in the United States of America. We have applied certain limitedprocedures, which consisted principally of inquiries of management regarding the methods of measurement andpresentation of the supplementary information. However, we did not audit the information and express no opinionon it.

Ferriday, LouisianaDecember 27,2007

- 2 -

CONCORDIA PARISH SHERIFFVIDALIA, LOUISIANA

MANAGEMENT'S DISCUSSION & ANALYSIS (MD&A)YEAR ENDED JUNE 30, 2006

INTRODUCTION

The discussion and analysis (MD&A) of the Concordia Parish Sheriffs financial performance provides an overallnarrative review of the Sheriffs financial activities for the year ended June 30, 2007. The intent of this discussionand analysis is to look at the Sheriffs performance as a whole; readers should also review the notes to the basicfinancial statements and the financial statements to enhance their understanding of the Sheriffs financialperformance.

The Concordia Parish Sheriffs office is located on Carter Street in Vidalia, Louisiana, with outlying facilitieslocated in all parts of Concordia Parish.

FINANCIAL HIGHLIGHTS

The financial statements included in this report provide insight into the financial status for the year. Based upon theoperations of the two years ended June 30, 2007, the Concordia Parish Sheriffs net assets decreased by $470,626 in2006 and decreased by $33,477 in 2007. This resulted in ending net assets of $10,037,336 in 2006 and $10,003,859in 2007.

1. The beginning cash balance for the Concordia Parish Sheriff was $5,463,827 as of June 30, 2005. Theending cash balance at June 30,2006 was $5,220,710 and it was $5,478,797 at June 30,2007.

2. The Sheriff had $10,594,408 in revenues for the year ended June 30, 2006 and $11,715,650 for the yearended June 30, 2007, which primarily consisted of property taxes, grants, prisoner upkeep and interestincome. There was $11,065,034 in expenditures including depreciation of $392,970 for the year endedJune 30, 2006 and $11,749,127 hi expenditures including depreciation of $408,998 for the year ended June30,2007.

OVERVIEW OF FINANCIAL STATEMENTS

This discussion and analysis is intended to serve as an introduction to the Concordia Parish Sheriffs basic financialstatements. The Sheriffs basic financial statements comprise three components: 1) government-wide financialstatements, 2) fund financial statements, and 3) notes to the financial statements.

Governmental-wide financial statements. The government-wide financial statements are designed to providereaders with a broad overview of the Sheriffs finances, in a manner similar to a private-sector business.

The statement of net assets presents information on all of the Sheriffs assets and liabilities, with the differencebetween the two reported as net assets. Over time, increases or decreases in net assets may serve as a usefulindicator of whether the financial position of the town is improving or deteriorating.

The statement of activities presents information showing how the Sheriffs net assets changed during the mostrecent fiscal year.

The government-wide financial statements outline functions of the Sheriff that are principally supported byproperty taxes and intergovernmental revenues (governmental activities). Fixed assets and related debt is alsosupported by taxes and intergovernmental revenues.

- 3 -

CONCORDIA PARISH SHERIFFVIDALIA, LOUISIANA

MANAGEMENT'S DISCUSSION & ANALYSIS (MD&A)YEAR ENDED JUNE 30,2006

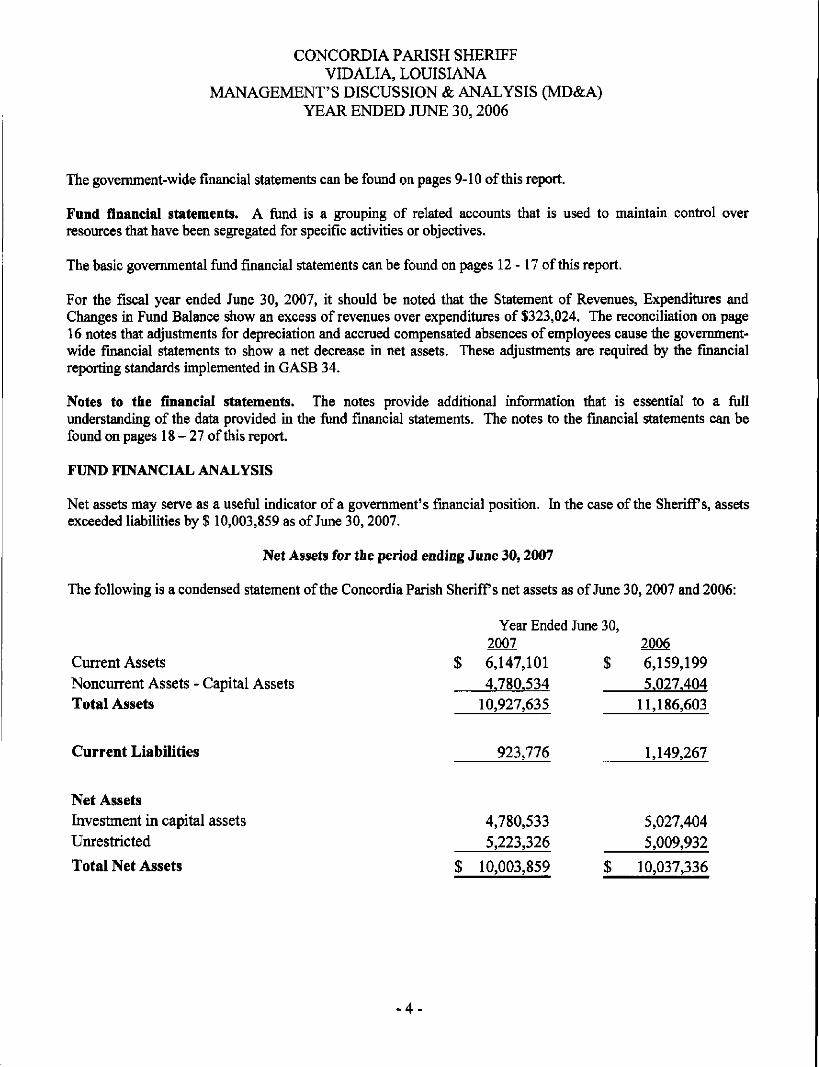

The government-wide financial statements can be found on pages 9-10 of this report.

Fund financial statements. A fund is a grouping of related accounts that is used to maintain control overresources that have been segregated for specific activities or objectives.

The basic governmental fund financial statements can be found on pages 12-17 of this report.

For the fiscal year ended June 30, 2007, it should be noted that the Statement of Revenues, Expenditures andChanges in Fund Balance show an excess of revenues over expenditures of $323,024. The reconciliation on page16 notes that adjustments for depreciation and accrued compensated absences of employees cause the government-wide financial statements to show a net decrease in net assets. These adjustments are required by the financialreporting standards implemented in GASB 34.

Notes to the financial statements. The notes provide additional information that is essential to a fullunderstanding of the data provided in the fund financial statements. The notes to the financial statements can befound on pages 18-27 of this report.

FUND FINANCIAL ANALYSIS

Net assets may serve as a useful indicator of a government's financial position. In the case of the Sheriffs, assetsexceeded liabilities by $ 10,003,859 as of June 30,2007.

Net Assets for the period ending June 30,2007

The following is a condensed statement of the Concordia Parish Sheriffs net assets as of June 30,2007 and 2006:

Year Ended June 30,2007 2006

Current Assets $ 6,147,101 $ 6,159,199Noncurrent Assets - Capital Assets 4.780,534 5.027.404Total Assets 10,927,635 11,186,603

Current Liabilities 923,776 1,149,267

Net AssetsInvestment in capital assets 4,780,533 5,027,404Unrestricted 5,223,326 5,009,932

Total Net Assets $ 10,003,859 $ 10,037,336

- 4 -

CONCORDIA PARISH SHERIFFVIDALIA, LOUISIANA

MANAGEMENT'S DISCUSSION & ANALYSIS (MD&A)YEAR ENDED JUNE 30,2006

A large portion of the Sheriffs net assets ($4,780,533 or 48%) is its investment in capital assets such as equipmentand facilities less related debt expended in the acquisition of those assets.

The remaining balance of the net assets ($5,223,326 or 52%) may be used to pay current operating expenses.

The Sheriff had long-term debt due within one year, of $454,519 at June 30, 2007, which is completely made up ofaccruals to pay for compensated absences earned by employees. More information concerning this debt may befound on page 26 of the notes to the financial statements. Total liabilities of $923,776 are equal to 8% of the totalassets of the Sheriff.

The following is a summary of the statement of activities:

Revenues:Charges for services

Public SafetyCorrectionsMowing

General revenuesAd valorem taxesState supplemental payState revenue sharingInterestOther

GrantsTotal revenues and transfers

Expenses:Operating expenses

Public safetyCorrectionsMowing

Interest expensesTotal expenses

Increase in net assets

Net assets July 1Net assets June 30

Year Ended June 30,2007 2006

$ 359,2036,950,751336,106

2,159,215147,337128,760295,659217,364

1,121,255

11,715,650

$ 307,5276,528,913381,036

2,033,216141,321129,190178,490223,120671,595

10,594,408

4,193,6896,755,714

101,49314,138

$ 4,344,418 $7,312,061

92,648

11,749,127

$ (33,477) $

10,037,336$ 10,003,859 $ 10,037,336

11,065,034

(470,626)

10,507,962

- 5 -

CONCORDIA PARISH SHERIFFVIDALIA, LOUISIANA

MANAGEMENT'S DISCUSSION & ANALYSIS (MD&A)YEAR ENDED JUNE 30,2006

BUDGET AMENDMENTS

Amendments to the budget for revenues resulted from a change in revenues and expenditures from the amountsestimated at the beginning of the year.

MANAGEMENT'S COMMENTS

Many of the grants that were curtailed as a consequence of the expense of recovery from Katrina in the prior fiscalyear have been renewed during this fiscal period. However, all of them were not active for the full twelve monthsof the year, but were phased in as funds became available on the state level.

It was found that funds were available to be able to pay off the debt connected with the construction of theCorrectional Facility here in Concordia Parish during the fiscal year ended June 30, 2006, one year ahead ofschedule. The Sheriffs office can now operate the facility more effectively, continuing to provide jobs to parishresidents and maintain a facility owned completely by the residents of Concordia Parish.

Through effective management and technology improvements, property tax collections have improved and morefunds have been able to be collected and remitted to the various government offices around the parish.

REQUEST FOR INFORMATION

This financial report is designed to provide citizens, taxpayers, customers and creditors with a general overview ofthe Sheriffs finances and to show the Sheriffs accountability for the money it receives. Any questions about thisreport or request for additional information may be directed to Sandy Burget, Administrative Supervisor at (318)336-5231.

- 7 -

GOVERNMENT - WIDE FINANCIAL STATEMENTS (GWFS)

-8-

CONCORDIA PARISH SHERIFFGOVERNMENT-WIDE FINANCIAL STATEMENTS

STATEMENT OF NET ASSETSJUNE 30, 2007

Statement A

ASSETSCash and Cash Equivalents $ 5,478,797Accounts Receivable 101,114Due from Other Governmental Units 528,936Commodities Inventory 12,5 80Prepaid Expenses 25,674Capital assets - net 4,780,534

Total Assets $ 10,927,635

LIABILITIESAccounts payables 277,228Salaries and benefits payable 192,028Long-term liabilities:

Due within one year 454,520

Total Liabilities 923,776

NET ASSETSInvested in Capital Assets 4,780,533Unrestricted 5,223,326

Total Net Assets $ 10,003,859

The accompanying notes are an integral part of the basic financial statements.-9 -

CQ4-t

0)£€5to

«8

m ooo^ r̂ON m00 NO

00 t^ o o\rn ^ *nm t-- ^oON

(N

OO W"> C--CS ON —i—< Ol Ol ON

of

ON>n00

OO

•B W -32 S 5r ] - •• ^—oo §

u

cs m^ o

csON

•» rf. w

SP fl3 u£ &.S" W tT£ •*

u

o> U ^

•I * £[H <*-!

V

C

oUJ

m ^o >nCN r-oT o'm ON

00 00

o ^oof of-H ON

E -. S «

« fe Su6uc ">

U -"

J3T3 <»tZ o>

I 3£ H

bO

•*M M

to ofl

D.a3

to

CA3Oo

s 5c co> e3S^ Ww -»^ 1 ?Q C Q

toU CA45 •<-•

S S

o

coO

1

OoOJ

ao

j=O

oo

I—»30>w«<«K

esct

iv

w —^ I*£>- .S^ >

^ C K« r5 2 5c to \s 5

| S 6 o

FUND FINANCIAL STATEMENTS (FSS)

-11-

CONCORDIA PARISH SHERIFFBALANCE SHEET - GOVERNMENTAL FUND

JUNE 30, 2007

Statement C

ASSETSCash and Cash Equivalents $ 5,478,797Accounts Receivable 101,114Due from Other Governmental Units 528,936Commodities Inventory 12,580Prepaid Expenses 25,674

Total Assets $ 6,147,101

LIABILITIESAccounts Payable 277,228Salaries and benefits payable 192,028

Total Liabilities 469,256

FUND BALANCEUnrestricted 5,677,845

Total Assets and Fund Balance $ 6,147,101

The accompanying notes are an integral part of the basic financial statements.-12-

CONCORDIA PARISH SHERIFFRECONCILIATION OF THE GOVERNMENTAL FUND BALANCE SHEET

TO THE STATEMENT OF NET ASSETSJUNE 30, 2007

Statement D

Total Fund Balances for Governmental Funds (Statement C) $ 5,677,845

Total Net Assets reported for governmental activities inthe statement of net assets is different because:

Capital assets used in governmental activities are notfinancial resources and therefore are not reported inthe funds. Those assets consist of:

Land 87,500Building improvements, net of $1,145,053

accumulated depreciation 3,774,507Automobiles and equipment, net of $1,398,551

accumulated depreciation 918,527

Total Capital Assets 4,780,534

Long-term liabilities, including compensated absencesare not due and payable in the current periodand therefore, are not reported in the governmental funds.Accrued compensated absences (454,520)

Net Assets of Governmental Activities (Statement A) $ 10,003,859

The accompanying notes are an integral part of the basic financial statements.-13-

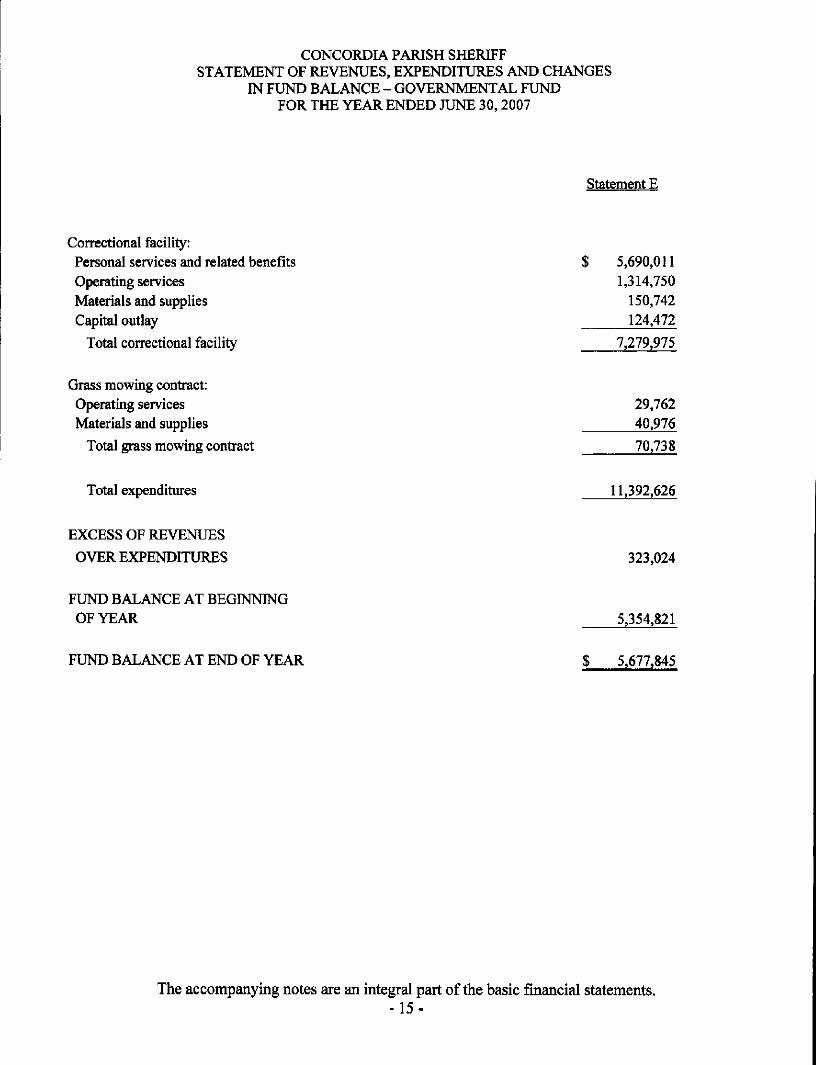

CONCORDIA PARISH SHERIFFSTATEMENT OF REVENUES, EXPENDITURES AND CHANGES

IN FUND BALANCE - GOVERNMENTAL FUNDFOR THE YEAR ENDED JUNE 30,2007

Statement E

REVENUESAd valorem taxes $ 2,159,215Intergovernmental revenuesFederal funds:

Grants: Correctional 313,893Public safety 88,532

State funds:State revenue sharing 128,760State supplemental pay 147,337State grants: Correctional 611,200

Public safety 107,630Mowing contract 336,106Miscellaneous 217,3 64

Fees, charges and commissions:Hydro patrol and disasters 125,389Sheriffs sales 41,910

Fines and forfeitures 19,493Civil and criminal fees 61,719Feeding and keeping prisoners-jail 110,692Feeding and keeping prisoners-CPCF 6,587,818Telephone commissions 235,053Commissary sales 127,880Interest income 295,659

Total revenues 11,715,650

EXPENDITURESPublic safetyPersonal services and related benefits 3,101,789Operating services 740,293Materials and supplies 17,921Travel and other charges 122,173Capital outlay 59,737

Total public safety 4,041,913

The accompanying notes are an integral part of the basic financial statements.-14-

CONCORDIA PARISH SHERIFFSTATEMENT OF REVENUES, EXPENDITURES AND CHANGES

IN FUND BALANCE - GOVERNMENTAL FUNDFOR THE YEAR ENDED JUNE 30, 2007

Statement E

Correctional facility:Personal services and related benefits $ 5,690,011Operating services 1,314,750Materials and supplies 150,742Capital outlay 124,472

Total correctional facility 7,279,975

Grass mowing contract:Operating services 29,762Materials and supplies 40,976

Total grass mowing contract 70,738

Total expenditures 11,392,626

EXCESS OF REVENUES

OVER EXPENDITURES 323,024

FUND BALANCE AT BEGINNINGOF YEAR 5,354,821

FUND BALANCE AT END OF YEAR $ 5,677,845

The accompanying notes are an integral part of the basic financial statements.-15-

CONCORDIA PARISH SHERIFFRECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES AND

CHANGES IN FUND BALANCE OF THE GOVERNMENTAL FUNDTO THE STATEMENT OF ACTIVITIES

YEAR ENDED JUNE 30, 2007

Statement F

Net change in Fund Balance at June 30,2007 -governmental activities (Statement E) $ 323,024

Governmental Funds report Capital Outlays asexpenditures. However, in the Statement ofactivities, the costs of those assets is allocatedover their estimated useful lives and reportedas depreciation expense.

Capital outlayDepreciation expense

Expenditures in Statement of Activities that do notinvolve current financial resources:

Book value of equipment soldAccrued compensation absences

$ 184,209(408,998)

(224,789)

(22,081)(109,631)

Changes in Net Assets at June 30,2007 -governmental activities (Statement B) $ (33,477)

The accompanying notes are an integral part of the basic financial statements.-16-

CONCORDIA PARISH SHERIFFSTATEMENT OF FIDUCIARY ASSETS AND LIABILITIES

JUNE 30,2007

Statement G

ASSETSCash and cash equivalentsAccounts receivable

TOTAL ASSETS

LIABILITIESDue to taxing bodies and others

SHERIFFSFUNDS

$ 75,85756,762

TAXCOLLECTOR

FUND

$ 52,006

26,790

INMATE

FUND

$ 324,3272,479

TOTAL

$ 452,19086,031

132,619 78,796 326,806 538,221

$ 132,619 $ 78,796 $ 326,806 $ 538,221

-17-

CONCORDIA PARISH SHERIFFVIDALIA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTSAS OF AND FOR THE YEAR JUNE 30, 2007

INTRODUCTION

As provided by Article V, Section 27 of the Louisiana Constitution of 1974, the Sheriff serves a four-year term asthe chief executive office of the law enforcement district and ex-officio tax collector of the parish. The sheriffadministers the parish jail system and exercises duties required by the parish court system, such as providingbailiffs, executing orders of the court, and serving subpoenas.

As the chief law enforcement officer of the parish, the Sheriff has the responsibility for enforcing state and locallaws and ordinances within the territorial boundaries of the parish. The Sheriff provides protection to the residentsof the parish through on-site patrols and investigations and serves the residents of the parish through theestablishment of neighborhood watch programs, anti-drug abuse programs, et cetera. In addition, when requested,the sheriff provides assistance to other law enforcement agencies within the parish.

As the ex-officio tax collector of the parish, the Sheriff is responsible for collecting and distributing ad valoremproperty taxes, state revenue sharing funds, fines, costs and bond forfeitures imposed by the district court.

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

A. BASIS OF PRESENTATION

The accompanying basic financial statements of the Concordia Parish Sheriff have been prepared in conformitywith governmental accounting principles generally accepted in the United States of America. The GovernmentalAccounting Standards Board (GASB) is the accepted standards setting body for establishing governmentalaccounting and financial reporting principles. The accompanying basic financial statements have been prepared inconformity with GASB Statement 34, "Basic Financial Statements - and Management's Discussion and Analysis -for State and Local Governments," issued in June 1999.

B. REPORTING ENTITY

The Sheriff is an independently elected official; however the Sheriff is fiscally dependent on the Concordia ParishPolice Jury. The Police Jury maintains and operates the parish courthouse in which the sheriff's office is locatedand provides funds for equipment and furniture of the Sheriffs office. Because the Sheriff is fiscally dependent onthe Police Jury, the Sheriff is a component unit of the Concordia Parish Police Jury, the financial reporting entity.

The accompanying financial statements present information only on the funds maintained by the sheriff and do notpresent information on the police jury, the general government services provided by that governmental unit, or theother governmental units that comprise the financial reporting entity.

C. FUND ACCOUNTING

The Sheriff uses funds to maintain its financial records during the year. Fund accounting is designed todemonstrate legal compliance and to aid management by segregating transactions related to certain sheriff functionsand activities. A fund is defined as a separate fiscal and accounting entity with a self-balancing set of accounts.

-18-

CONCORDIA PARISH SHERIFFVIDALIA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTSAS OF AND FOR THE YEAR ENDED JUNE 30, 2007

Governmental Funds

Governmental funds account for all or most of the sheriffs general activities. These funds focus on thesources, uses and balances of current financial resources. Expendable assets are assigned to the variousgovernmental funds according to the purposes for which they may be used. Current liabilities are assignedto the fund from which they will be paid. The difference between a governmental fund's assets andliabilities is reported as fund balance. In general, fund balance represents the accumulated expendableresources which may be used to finance future period programs or operations of the sheriff. The followingis the sheriffs governmental fund:

General Fund - the primary operating fund of the sheriff and it accounts for all financialresources, except those required to be accounted for in other funds. The General Fund is availablefor any purpose provided it is expended or transferred in accordance with state and federal lawsand according to sheriff policy.

Fiduciary Funds

Fiduciary fund reporting focuses on net assets and changes in net assets. The only funds accountedfor in this category by the sheriff are agency funds. The agency funds account for assets held bythe sheriff as an agent for various taxing bodies (tax collections), for deposits held pending courtaction and deposits held for inmates. These funds are custodial in nature (assets equal liabilities)and do not involve measurement of results of operations. Consequently, the agency funds have nomeasurement focus, but use the modified accrual basis of accounting.

D. MEASUREMENT FOCUS/BASIS OF ACCOUNTING

Fund Financial Statements (FFS)

The amounts reflected in the General Fund, of Statements C and D, are accounted for using a current financialresources measurement focus. With this measurement focus, only current assets and current liabilities are generallyincluded on the balance sheet. The statement of revenues, expenditures, and changes in fund balances reports on thesources (i.e., revenues and other financing sources) and uses (i.e., expenditures and other financing uses) of currentfinancial resources. This approach is then reconciled, through adjustment, to a government-wide view of sheriffoperations.

The amounts reflected in the General Fund, of Statements C and D, use the modified accrual basis of accounting.Under the modified accrual basis of accounting, revenues are recognized when susceptible to accrual (i.e., whenthey become both measurable and available). Measurable means the amount of the transaction can be determinedand available means collectible within the current period or soon enough thereafter to pay liabilities of the currentperiod. The sheriff considers all revenues available if they are collected within 60 days after the fiscal year end.Expenditures are recorded when the related fund liability is incurred, except for interest and principal payments ongeneral long-term debt which is recognized when due, and certain compensated absences and claims and judgmentswhich are recognized when the obligations are expected to be liquidated with expendable available financialresources. The governmental funds use the following practices in recording revenues and expenditures:

-19-

CONCORDIA PARISH SHERIFFVIDALIA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTSAS OF AND FOR THE YEAR ENDED JUNE 30, 2007

Revenues

Ad valorem taxes and the related state revenue sharing are recorded in the year taxes are due and payable.Ad valorem taxes are assessed on a calendar year basis, become due on November 15 of each year, andbecome delinquent on December 31. The taxes are generally collected in December, January and Februaryof the fiscal year.

Intergovernmental revenues and fees, charges and commissions for services are recorded when the sheriffis entitled to the funds.

Interest on interest-bearing deposits is recorded or accrued as revenues when earned. Substantially all otherrevenues are recorded when received.

Expenditures

In the government-wide financial statements, expenses are classified by function. In the fund financialstatements, expenditures are classified by character and function.

Government-Wide Financial Statements (GWFS)

The Statement of Net Assets (Statement A) and the Statement of Activities (Statement B) displayinformation about the sheriff as a whole. These statements include all the financial activities of the sheriff.Information contained in these columns reflect the economic resources measurement focus and the accrualbasis of accounting. Revenues, expenses, gains, losses, assets and liabilities resulting from exchange orexchange-like transactions are recognized when the exchange occurs (regardless of when cash is receivedor disbursed). Revenues, expenses, gains, losses, assets and liabilities resulting from nonexchangetransactions are recognized in accordance with the requirements of GASB Statement No. 33, Accountingand Financial Reporting for Nonexchange Transactions.

Program Revenues - Program revenues included in the Statement of Activities (Statement B) are deriveddirectly from sheriff users as a fee for services; program revenues reduce the cost of the function to befinanced from the sheriffs general revenues.

E. BUDGETS

The Sheriff uses the following budget practices:

1. The Sheriff prepares a proposed budget for the general fund in June of each year for the year beginningJuly 1.

2. A summary of the proposed budget is published and the public notified that the proposed budget isavailable for public inspection. At the same time, a public hearing is called.

3. A public hearing is held on the proposed budget at least ten days after publication of the call for thehearing.

-20-

CONCORDIA PARISH SHERIFFVIDALIA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTSAS OF AND FOR THE YEAR ENDED JUNE 30, 2007

4. After the holding of the public hearing and completion of all action necessary to finalize and implement thebudget, the budget is adopted by the Sheriff.

5. All budgetary appropriations lapse at the end of each fiscal year.

6. Budgets are adopted on an accrual basis.

7. There was one amendment to the budget during the year ended June 30, 2006.

F. CASH AND CASH EQUIVALENTS

Cash includes amounts in demand deposits, interest-bearing demand deposits and time deposits. Under state law,the Sheriff may deposit funds in demand deposits, interest-bearing demand deposits, or time deposits with statebanks organized under Louisiana law or any other state of the United States, or under the laws of the United States.

G. INVENTORIES

Inventory of the Sheriffs General fund consists of food purchased by the Sheriff and commodities granted byvarious governmental agencies. The commodities are recorded as revenues when received; however, all inventoryitems are recorded as expenses when consumed. All purchased inventory items are stated at cost, which isdetermined by the flrst-in, first-out method.

H. PREPAID ITEMS

Certain payments for insurance reflect cost applicable to future accounting periods and are recorded as prepaiditems in both government wide and fund financial statements.

I. CAPITAL ASSETS

Capital assets, which include land, buildings, furniture, fixtures and equipment and vehicles, are reported in thestatement of net assets. Capital assets are capitalized at historical cost or estimated cost if historical is not available.

Donated assets are recorded as capital assets at their estimated fair market value at the date of donation. The Sheriffmaintains a threshold level of $500 or more for capitalizing capital assets. The costs of normal maintenance andrepairs that do not add to the value of the asset or materially extend assets lives are not capitalized.

Depreciation of all exhaustible capital assets is recorded as an allocated expense in the statement of activities, withaccumulated depreciation reflected in the statement of net assets. Depreciation is provided over the assets' estimateuseful lives using the straight-line method of depreciation. The range of estimated useful lives by type of asset is asfollows:

Vehicles 5-10 yearsBuildings 20 - 40 yearsFurniture, fixtures and equipment 5-20 years

In the fund financial statements, capital assets used in governmental fund operations are accounted for as capitaloutlay expenditures of the governmental fund upon acquisition.

-21-

CONCORDIA PARISH SHERIFFVIDALIA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTSAS OF AND FOR THE YEAR JUNE 30, 2007

J. COMPENATED ABSENCES

The Sheriff has the following policy relating to vacation and sick leave:

After one year of service, employees of the Sheriffs office receive five working days of noncumulative vacationleave. For each year thereafter, they receive a total of ten working days of noncumulative vacation leave.Employees receive the same number of cumulative sick leave days, which are not payable upon termination orretirement.

The sheriffs recognition and measurement criteria for compensated absences follows: GASB Statement No. 16provides that vacation leave and other compensated absences with similar characteristics should be accrued as aliability as the benefits are earned by the employees if both of the following conditions are met:

a. The employees' rights to receive compensation are attributable to services already rendered.

b. It is probable that the employer will compensate the employees for the benefits through paid timeoff or some other means, such as cash payments at termination or retirement.

GASB Statement No. 16 provides that a liability for sick leave should be accrued using one of the followingtermination approaches:

a. An accrual for earned sick leave should be made only to the extent it is probable that the benefitswill result in termination payments, rather than be taken as absences due to illness or othercontingencies, such as medical appointments and funerals.

b. Alternatively, a governmental entity should estimate its accrued sick leave liability based on thesick leave accumulated at the balance sheet date by those employees who currently are eligible toreceive termination payments as well as other employees who are expected to become eligible inthe future to receive such payments.

The current portion of the liability for compensated absences is not reported in the fund financial statements. Theliability is adjusted into the entity-wide on Statements A and B.

K. ESTIMATES

The preparation of financial statements in conformity with accounting principles generally accepted in the UnitedStates of America require management to make estimates and assumptions that affect the reported amounts ofassets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and thereported amounts of revenues, expenditures, and expenses during the reporting period. Actual results could differfrom those estimates.

-22-

CONCORDIA PARISH SHERIFFVIDALIA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTSAS OF AND FOR THE YEAR ENDED JUNE 30, 2007

NOTE 2 - LEVIED TAXES

The Sheriff is the ex-officio tax collector of the parish and is responsible for the collection and distribution of advalorem taxes. Ad valorem taxes attach as an enforceable lien on property as of January 1 of the following year.The taxes are based on assessed values determined by the Concordia Parish Tax Assessor and are collected by theSheriff. The taxes are remitted to the appropriate taxing bodies net of deduction for assessor's compensation andpension fund contributions.

The following is a summary of Concordia Parish levied ad valorem taxes for 2007:Levied Authorized Expiration

DESCRIPTION Millage Millage DateParish Tax:General Alimony Tax 2.78M 2.78M N/ALibrary 8.45M 8.45M 2008Highway, Drainage and Building Upkeep 9.94M 9.94M 2007Health Unit .80M .80M 2010Assessor 1.98M 1.98M N/ASheriffs Law Enforcement 8.62M 8.62M N/ASheriffs Special 12.00M 12.00M 2016School New Construction 12.55M 13.00M 2010School Maintenance 27.11M 27.11M 2012

Fifth Louisiana Levee District 3.86M 3.86M N/ARecreation District No. 1 2.74M 2.92M 2007Recreation District No. 2 6.29M 6.29M 2007Recreation District No. 3 3.89M 4.00M 2016Fire District No. 1 3.15M 3.15M 2016Fire District No. 2 Maintenance 6.75M 6.94M 2009Forestry Tax $.08/Acre $.08/Acre N/A

The following are the principal taxpayers and related ad valorem tax revenue for the sheriff:

TaxpayerCatalyst Old RiverUnion Underwear

Total

Type ofBusiness

Hydro ElectricClothing

AssessedValuation

$ 29,971,58011,850,210

$ 41,821,790

% of TotalAssessedValuation

29%12%

41%

Ad valorem TaxRevenue for

Sheriff$ 618,014

244,351

$ 862,365

-23-

CONCORDIA PARISH SHERIFFVIDALIA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTSAS OF AND FOR THE YEAR ENDED JUNE 30, 2007

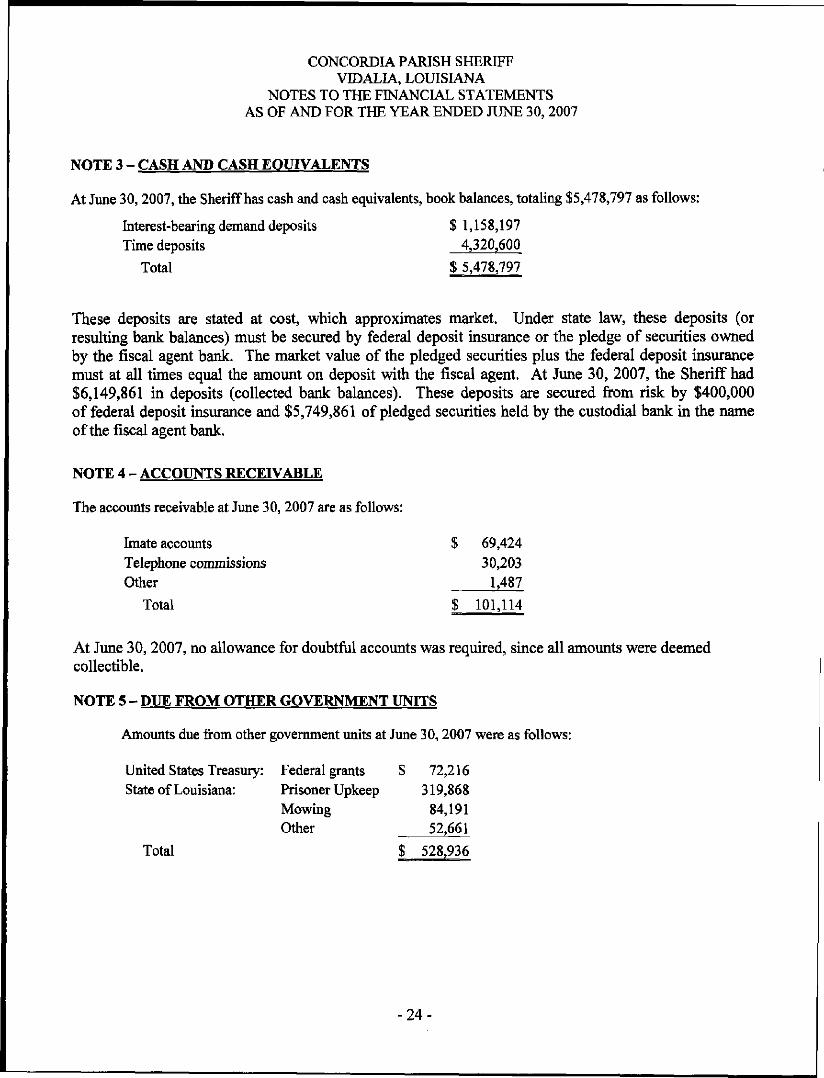

NOTE 3 - CASH AND CASH EQUIVALENTS

At June 30,2007, the Sheriff has cash and cash equivalents, book balances, totaling $5,478,797 as follows:

Interest-bearing demand deposits $ 1,158,197Time deposits 4,320,600

Total $ 5,478,797

These deposits are stated at cost, which approximates market. Under state law, these deposits (orresulting bank balances) must be secured by federal deposit insurance or the pledge of securities ownedby the fiscal agent bank. The market value of the pledged securities plus the federal deposit insurancemust at all times equal the amount on deposit with the fiscal agent. At June 30, 2007, the Sheriff had$6,149,861 in deposits (collected bank balances). These deposits are secured from risk by $400,000of federal deposit insurance and $5,749S861 of pledged securities held by the custodial bank in the nameof the fiscal agent bank.

NOTE 4 - ACCOUNTS RECEIVABLE

The accounts receivable at June 30, 2007 are as follows:

Imate accounts $ 69,424Telephone commissions 30,203Other 1,487

Total $ 101,114

At June 30,2007, no allowance for doubtful accounts was required, since all amounts were deemedcollectible.

NOTE 5 - DUE FROM OTHER GOVERNMENT UNITS

Amounts due from other government units at June 30,2007 were as follows:

United States Treasury: Federal grants $ 72,216State of Louisiana: Prisoner Upkeep 319,868

Mowing 84,191Other 52,661

Total $ 528,936

-24-

CONCORDIA PARISH SHERIFFVIDALIA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTSAS OF AND FOR THE YEAR ENDED JUNE 30,2007

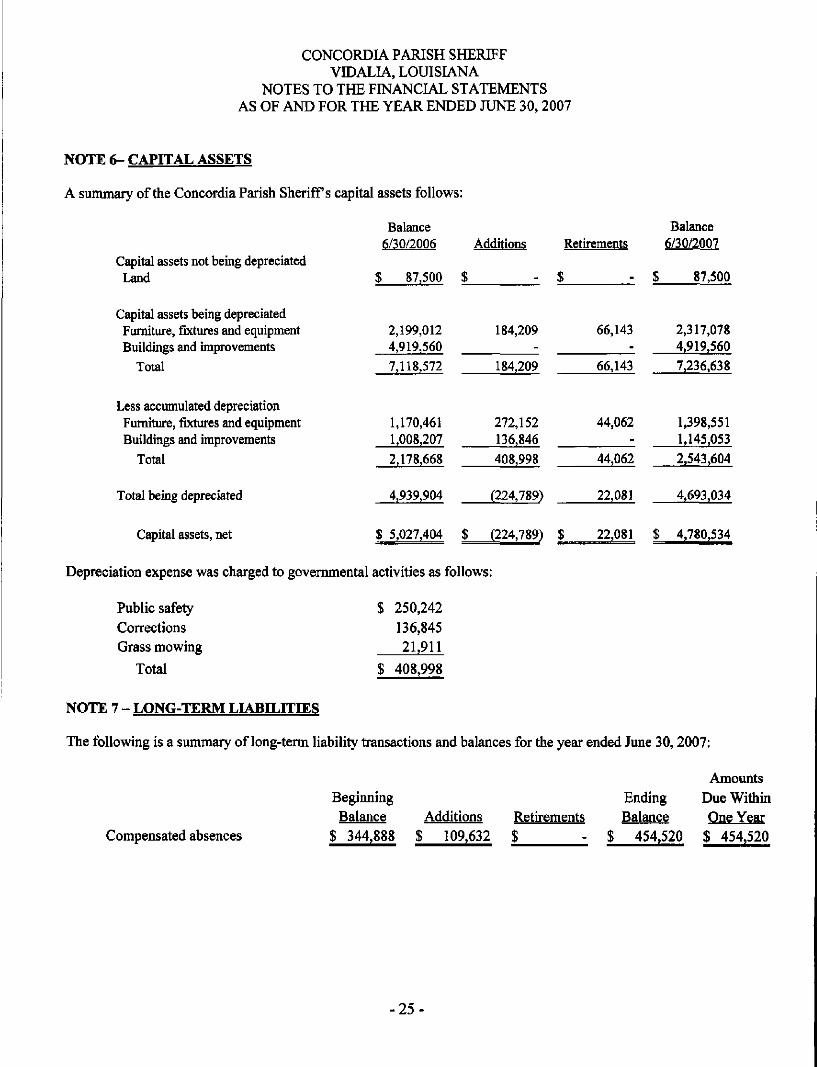

NOTE 6- CAPITAL ASSETS

A summary of the Concordia Parish Sheriffs capital assets follows:

Capital assets not being depreciatedLand

Capital assets being depreciatedFurniture, fixtures and equipmentBuildings and improvements

Total

Less accumulated depreciationFurniture, fixtures and equipmentBuildings and improvements

Total

Total being depreciated

Capital assets, net

Balance6/30/2006 Additions Retirements

$ 87,500 $ - $

2,199,012 184,209 66,1434,919,560

7,118,572 184,209 66,143

1,170,461 272,152 44,0621,008,207 136,846

2,178,668 408,998 44,062

4,939,904 (224,789) 22,081

$ 5,027,404 $ (224,789) $ 22,081

Balance6/30/2007

$ 87,500

2,317,0784,919,560

7,236,638

1,398,5511,145,053

2,543,604

4,693,034

$ 4,780,534

Depreciation expense was charged to governmental activities as follows:

Public safety $ 250,242

Corrections 136,845

Grass mowing 21,91 1

Total

NOTE 7 - LONG-TERM LIABILITIES

$ 408,998

The following is a summary of long-term liability transactions and balances for the year ended June 30,2007:

AmountsBeginning Ending Due WithinBalance Additions Retirements Balance One Year

Compensated absences $ 344,888 $ 109,632 $ $ 454,520 $ 454,520

-25-

CONCORDIA PARISH SHERIFFVIDALIA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTSAS OF AND FOR THE YEAR ENDED JUNE 30, 2007

NOTE 8 - PENSION PLAN

Plan Description - Substantially all employees of the Concordia Parish Sheriffs Office are members of theLouisiana Sheriffs Pension and Relief Fund (System), a multiple-employer (cost-sharing), public employeeretirement system (PERS), controlled and administered by a separate board of trustees.

All sheriffs, deputies and other employees who are found to be physically fit, who earn at least $400 per monthdepending on year employed, and who were at least age 18 years or older at the time of original employment arerequired to participate in the System. Employees are eligible to retire at or after age 55 with at least 12 years ofcredited service and receive a benefit, payable monthly for life, equal to a percentage of their final-average salaryfor each year of credited service. The percentage factor to be used for each year of service is 3.33 percent for eachyear of total service. In any case, the retirement benefit cannot exceed 100 percent of then* final-average salary.Final-average salary is the employee's average salary over the 36 consecutive or joined months thatproduce the highest average.

Employees who terminate with at least 12 years of service and do not withdraw their employee contributions mayretire at or after age 55 and receive the benefit accrued to their date of termination as indicated previously.Employees who terminate with at least 20 years of credited service are also eligible to elect early benefits betweenages 50 and 55 with reduced benefits equal to the actuarial equivalent of the benefit to which they would otherwisebe entitled at age 55. The System also provides death and disability benefits. Benefits are established or amendedby state statute.

Members are not required to make any contributions to the plan. The Concordia Parish Sheriffs Office is requiredto contribute at an actuarially determined rate. The combined rate is 21% of annual covered payroll. TheConcordia Parish Sheriffs Office contributions for the year ending June 30,2007 were $1,394,663.

The Louisiana Sheriff Pension and Relief fund issues a publicly available Actuarial Valuation and requiredsupplementary information. That information may be obtained by writing to Sheriffs Pension and Relief Fund,6554 Florida Blvd., Suite 215, Baton Rouge, LA 70806 or by calling (800) 586-9049.

NOTE 9 - POST RETIREMENT BENEFITS

The Concordia Parish Sheriff provides group health, dental and life insurance benefits to retirees who are at least 55years of age and who are entitled to receive benefits from the Louisiana Sheriffs Pension and Relief Fund. Thefiscal year cost of these benefits, which were established by legislative act in the year 2001, was $16,696. Theretired employees are not required to contribute any of the cost of this benefit. At June 30, 2007, six retiredemployees were participants.

NOTE 10 - EXPENDITURES OF THE SHERIFF'S OFFICE PAD) BY THE PARISH POLICE JURY

The Sheriffs office is located in the parish courthouse. Expenditures for operation and maintenance of the parishcourthouse, as required by state statute, are paid by the Concordia Parish Police Jury and are not included in theaccompanying financial statements

-26-

CONCORDIA PARISH SHERIFFVIDALIA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTSAS OF AND FOR THE YEAR ENDED JUNE 30,2007

NOTE 11 - LITIGATION

The Sheriffs Office was involved in various lawsuits at June 30, 2007. It is not possible at present for theConcordia Parish Sheriffs legal counsel to predict the outcome or the range of potential loss, if any, that may resultfrom those actions. No provision for any liability that may result has been made in the financial statements, but thelawsuits are considered to be within the Sheriffs insurance limits and therefore should not have any effect on itsfinancial statements. The Concordia Parish Sheriff is not aware of any claims or assessments that should bereflected in the accompanying financial statements.

NOTE 12 - RISK MANAGEMENT

The Concordia Parish Sheriff is exposed to various risks of loss related to torts; theft of, damage to, and destructionof assets; errors and omissions; injuries to employees, and natural disasters. The Sheriff maintains commercialinsurance coverage covering each of those risks of loss. Management believes such coverage is sufficient topreclude any significant uninsured losses to the Sheriff.

-27-

REQUIRED SUPPLEMENTARY INFORMATION

-28-

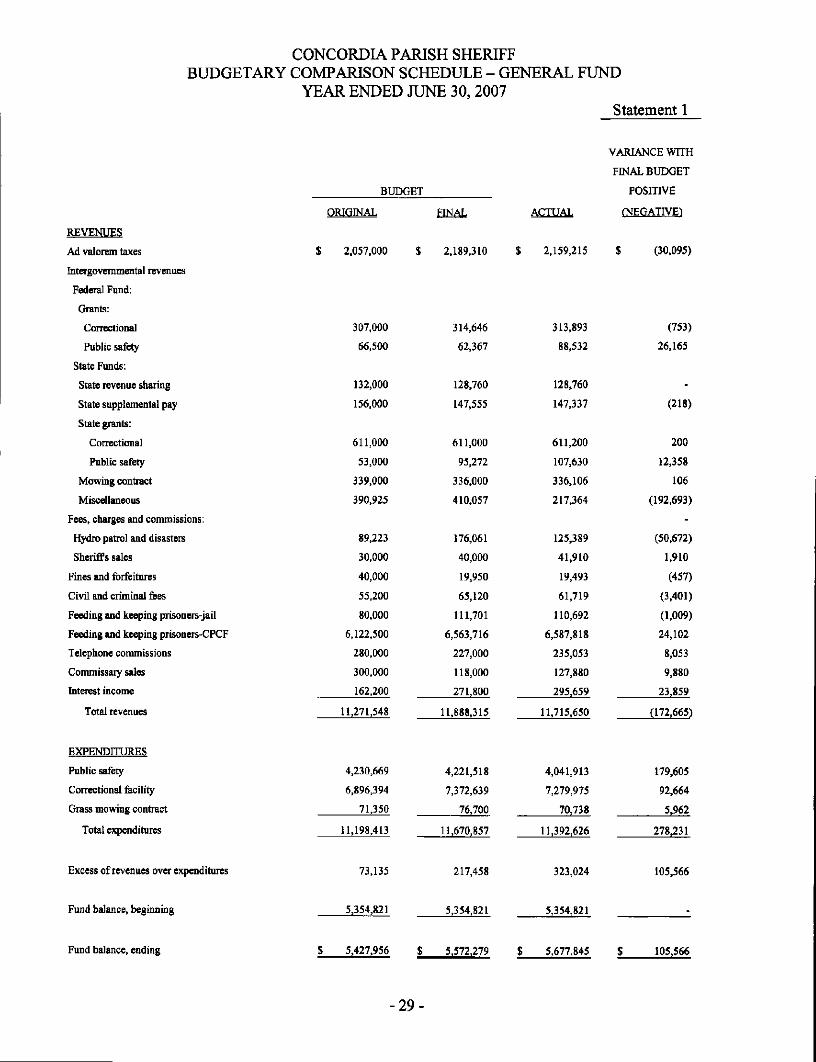

CONCORDIA PARISH SHERIFFBUDGETARY COMPARISON SCHEDULE - GENERAL FUND

YEAR ENDED JUNE 30,2007Statement 1

BUDGET

REVENUES

Ad valorem taxes

Intergovernmental revenues

Federal Fund:

Grants:

Correctional

Public safety

State Funds:

State revenue sharing

State supplemental pay

State grants:

Correctional

Public safety

Mowing contract

Miscellaneous

Fees, charges and commissions:

Hydro patrol and disasters

Sheriffs sales

Fines and forfeitures

Civil and criminal fees

Feeding and keeping prisoners-jail

Feeding and keeping prisoners-CPCF

Telephone commissions

Commissary sales

Interest income

Total revenues

EXPENDITURES

Public safety

Correctional facility

Grass mowing contract

Total expenditures

Excess of revenues over expenditures

Fund balance, beginning

ORIGINAL

$ 2,057,000

307,000

66,500

132,000

156,000

611,000

53,000

339,000

390,925

89,223

30,000

40,000

55,200

80,000

6,122,500

280,000

300,000

162,200

11,271,548

4,230,669

6,896,394

71,350

11,198,413

73,135

5,354,821

FINAL

$ 2,189,310

314,646

62,367

128,760

147,555

611,000

95,272

336,000

410,057

176,061

40,000

19,950

65,120

111,701

6,563,716

227,000

118,000

271,800

11,888,315

4,221,518

7,372,639

76,700

11,670,857

217,458

5,354,821

$ 2,159,215

313,893

88,532

128,760

147,337

611,200

107,630

336,106

217,364

125,389

41,910

19,493

61,719

110,692

6,587,818

235,053

127,880

295,659

11,715,650

4,041,913

7,279,975

70,738

11,392,626

323,024

5,354,821

VARIANCE WTTH

FINAL BUDGET

POSITIVE

(NEGATIVES

$ (30,095)

(753)

26,165

(218)

200

12,358

106

(192,693)

(50,672)

1,910

(457)

(3,401)

(1,009)

24,102

8,053

9,880

23,859

(172.665)

179,605

92,664

5,962

278,231

105,566

Fund balance, ending S 5.427.956 S 5,572,279 $ 5.677.845 105,566

-29-

CONCORDIA PARISH SHERIFF

NOTE TO BUDGETARY COMPARISON SCHEDULEFOR THE YEAR ENDED JUNE 30, 2007

General Budget Policies

A proposed budget, prepared on the modified accrual basis of accounting, is published in the official journal at leastten days prior to the public hearing. A public hearing is held at the Concordia Parish Sheriffs office during themonth of June for comments from taxpayers. The budget is established and controlled by the sheriff at the objectlevel of expenditure. Appropriations lapse at year-end and must be reappropriated for the following year to beexpended.

Formal budgetary integration is employed as a management control device during the year. Budgeted amountsincluded in the accompanying budgetary comparison schedule include the original adopted budget amounts and allsubsequent amendments.

Budget Basis of Accounting

All governmental funds' budgets are prepared on the modified accrual basis of accounting. Budgeted amounts areas originally adopted or as amended by the Sheriff. Legally, the Sheriff must adopt a balanced budget; that is, totalbudgeted revenues and other financing sources including fund balance must equal or exceed total budgetedexpenditures and other financing uses. State statutes require the Sheriff to amend its budgets when revenues plusprojected revenues within a fund are expected to be less than budgeted revenues by five percent or more and/orexpenditures within a fund are expected to exceed budgeted expenditures by five percent or more.

- 3 0 -

SWITZER HOPKINS & MANGECertified Public Accountants

POST OFFICE BOX 478FERRIDAY, LOUISIANA 71334

DENNIS R. SWITZER, CPAH. MYLES HOPKINS, CPASUSAN L. MANGE, CPA

JOHN M. JONES, CPA 1921 -1983

1840 NORTH E.E. WALLACE BLVD.FERRIDAY, LOUISIANA 71334

TELEPHONE (318) 757-2600FAX (318) 757-7206

OFFICES IN NATCHEZ, MISSISSIPPI

REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTINGAND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT

OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCEWITH GOVERNMENT AUDITING STANDARDS

Honorable Randy J. MaxwellConcordia Parish SheriffVidalia, Louisiana

We have audited the financial statements of the governmental activities, each major fund and the aggregateremaining fund information of the Concordia Parish Sheriff as of and for the year ended June 30, 2007, whichcollectively comprise the Concordia Parish Sheriffs basic financial statements and have issued our report thereondated December 27, 2007. The auditor's report on the financial statements is modified to reflect that the financialstatements do not include the financial data of the Concordia Parish, Louisiana, Police Jury, the primarygovernment. We conducted our audit in accordance with auditing standards generally accepted in the United Statesand the standards applicable to financial audits contained in Government Auditing Standards, issued by theComptroller General of the United States.

Internal Control Over Financial Reporting

In planning and performing our audit, we considered the Concordia Parish Sheriffs internal control over financialreporting as a basis for designing our auditing procedures for the purpose of expressing our opinion on the financialstatements, but not for the purpose of expressing an opinion on the effectiveness of the Concordia Parish Sheriff'sinternal control over financial reporting. Accordingly, we do not express an opinion on the effectiveness of theConcordia Parish Sheriffs internal control over financial reporting,

A control deficiency exists when the design or operation of a control does not allow management or employees, inthe normal course of performing their assigned functions, to prevent or detect misstatements on a timely basis. Asignificant deficiency is a control deficiency, or combination of control deficiencies, that adversely affect theConcordia Parish Sheriffs ability to initiate, authorize, record, process, or report financial data reliably inaccordance with generally accepted accounting principles such that there is more than a remote likelihood that amisstatement of the Concordia Parish Sheriffs financial statements that is more than inconsequential will not beprevented or detected by the Concordia Parish Sheriffs internal control.

-31-

Honorable Randy J. MaxwellConcordia Parish SheriffPage Two

A material weakness is a significant deficiency, or combination of significant deficiencies, that results in more thana remote likelihood that a material misstatement of the financial statements will not be prevented or detected by theConcordia Parish Sheriffs internal control.

Our consideration of the internal control over financial reporting was for the limited purpose described in the firstparagraph of this section and would not necessarily identify all deficiencies in the internal control that might besignificant deficiencies or material weaknesses. We did not identify any deficiencies in internal control overfinancial reporting that we consider to be material weaknesses, as defined above.

Compliance and Other Matters

As part of obtaining reasonable assurance about whether Concordia Parish Sheriffs financial statements are free ofmaterial misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contractsand grants, noncompliance with which could have a direct and material effect on the determination of financialstatement amounts. However, providing an opinion on compliance with those provisions was not an object of ouraudit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances ofnoncompliance or other matters that is required to be reported under Government Auditing Standards.

This report is intended for the information and use of management of the Concordia Parish Sheriff and theLegislative Auditor of the State of Louisiana. However, this report is a matter of public record and its distributionis not limited.

Ferriday, LouisianaDecember 27,2007 N

-32-

CONCORDIA PARISH SHERIFF

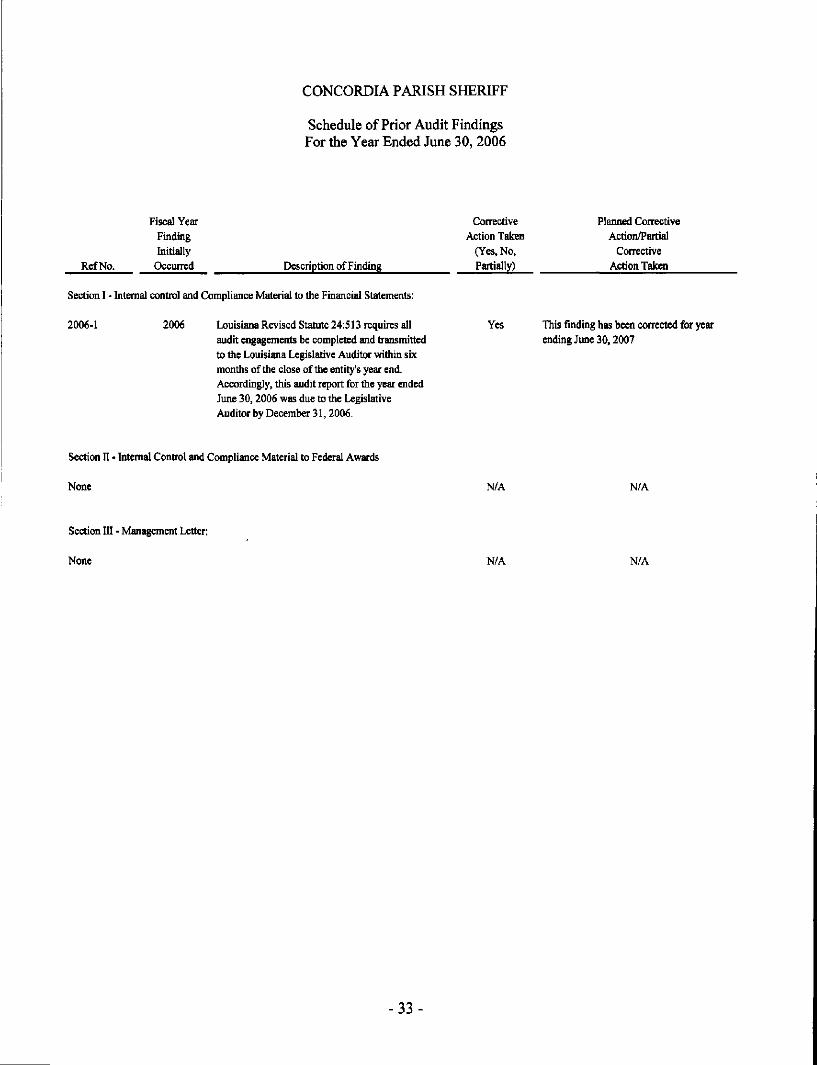

Schedule of Prior Audit FindingsFor the Year Ended June 30, 2006

RefNo.

Fiscal YearFindingInitially

Occurred Description of Finding

CorrectiveAction Taken

(Yes, No,Partially)

Planned CorrectiveAction/Partial

CorrectiveAction Taken

Section I - Internal control and Compliance Material to the Financial Statements:

2006-1 2006 Louisiana Revised Statute 24:513 requires allaudit engagements be completed and transmittedto the Louisiana Legislative Auditor within sixmonths of the close of the entity's year end.Accordingly, this audit report for the year endedJune 30,2006 was due to the LegislativeAuditor by December 31,2006.

Yes This finding has been corrected for yearending June 30,2007

Section IT - Internal Control and Compliance Material to Federal Awards

None N/A N/A

Section in - Management Letter:

None N/A N/A

- 3 3 -

CONCORDIA PARISH SHERIFF

Schedule of Current Year Audit FindingsFor the Year Ended June 30, 2007

Name(s) of AnticipatedContact Completion

RefNo. Description of Finding Corrective Action Planned Person(s) Date

Section I - Internal Control and Compliance Material to the Financial Statements:

None N/A N/A N/A

Section n - Internal Control and Compliance Material to Federal Awards

None N/A N/A N/A

Section ffl - Management Letter:

None N/A N/A N/A

- 3 4 -