3,700,000 vélib’ users since july 15 2007 - iis windows...

TRANSCRIPT

1Paris, France – September 2007

H1 2007 RESULTSSeptember 12th 2007

3,700,000 Vélib’ users since July 15th 2007

2

BUSINESS OVERVIEW

Jean-François DecauxChairman of the Executive Board and Co-CEO

3

H1 2007 RESULTS

+ 7.7%

+ 5.7%

+ 3.5%

+ 7.3%

- 2.8%

- 88.3%

(In million €, under IFRS standards)

(1) Operating Margin = Revenues less Direct Operating Costs (excluding Maintenance spare parts and including SG&A costs)(2) EBIT = Earnings Before Interests and Taxes

= Operating Margin less Depreciation, amortization, provisions less Impairment of goodwill less Maintenance spare parts less Other operating income and expenses.

Revenues 1,019.0

Operating margin (1) 280.0

EBIT (2) 175.7

Net income Group share 114.1

Net cash flow from operations 144.3

Free cash flow 7.8

4

H1 2007 REVENUE BREAKDOWN

France

Rest of Europe

UK

North America

Asia-Pacific

Street Furniture

Billboard

By region (% of total)By business (% of total)

Transport28.3%

12.8%

6.5%

14.4%37.2%

24%

26%

50%

Rest of the World: 0.8%

5

Organic growth (%) (1) Reported growth (%)

H1 2007 REVENUE GROWTHBY BUSINESS

(1) Organic growth = excluding acquisitions /divestitures and the impact of foreign exchange.

12.1%

8.9%5.1%

7.7%

StreetFurniture BillboardTransport Group

12.3%

6.9%

StreetFurniture

BillboardTransport Group

8.1%

3.6%

6

H1 2007 REVENUE GROWTHBY REGION

8.1%

-2.0%

14.6%

16.4%

France (2)UK Rest of

EuropeNorth

AmericaAsia-

Pacific

7.8%

Organic growth (%) (1)

Rest of the World

14.7%

(1) Organic growth = excluding acquisitions /divestitures and the impact of foreign exchange.(2) Core advertising revenues in France decreased by 0.2% in the first half of 2007 compared to the same period last year

7

• Organic growth & renewals

• The bike revolution

• Sales & Marketing

H1 2007 BUSINESS HIGHLIGHTS

8

NEW AND RENEWED BUSINESS

NEW CONTRACTS RENEWALS

STREET FURNITURE • Spain Seville (Street furniture & bicycles)

• Japan

• Baltics Tallinn, Vilnius

• Norway Stavanger

TRANSPORT

• Belgium Brussels Airport

• China Shanghai subway (extension of previous contract)

STREET FURNITURE • France Paris (MUPIs®, Seniors®, bicycles)

Toulouse (Street furniture & bicycles)

Strasbourg

Nancy Mulhouse (Street furniture & bicycles)

Besançon (Street furniture & bicycles)

Rouen (Street furniture & bicycles)

BILLBOARD

• France Paris – OPAC contract

SapporoKita-Kyushu SakaiHamamatsu

9

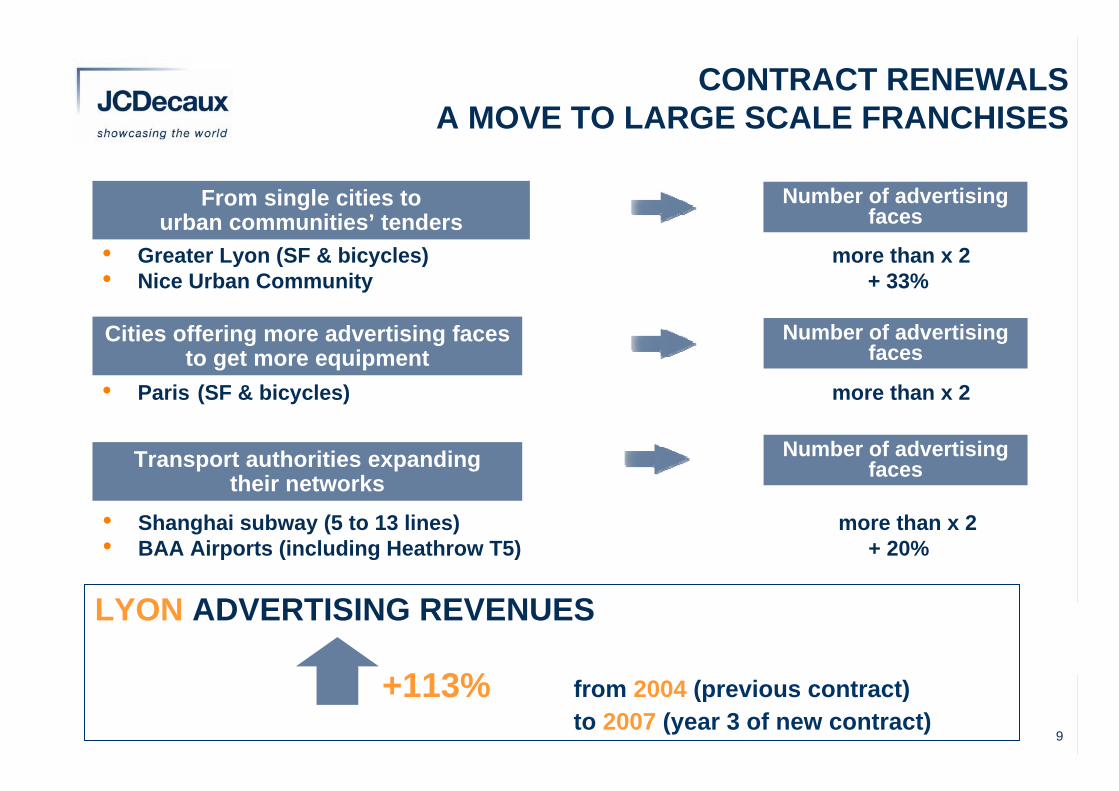

CONTRACT RENEWALSA MOVE TO LARGE SCALE FRANCHISES

• Greater Lyon (SF & bicycles) more than x 2• Nice Urban Community + 33%

From single cities to urban communities’ tenders

Number of advertising faces

Cities offering more advertising faces to get more equipment

• Paris (SF & bicycles) more than x 2

Number of advertising faces

Transport authorities expandingtheir networks

• Shanghai subway (5 to 13 lines) more than x 2• BAA Airports (including Heathrow T5) + 20%

Number of advertising faces

LYON ADVERTISING REVENUES

+113% from 2004 (previous contract)to 2007 (year 3 of new contract)

10

H1 2007 BUSINESS HIGHLIGHTS

• Organic growth & renewals

• The bike revolution

• Sales & Marketing

11Paris, France2007

Lyon, France2005

Aix-en-Provence, France2006

Brussels, Belgium2006

Seville, Spain2007

Vienna, Austria2003

N°1 PROVIDER OF SELF-SERVICE BIKES FINANCED BY ADVERTISING

12

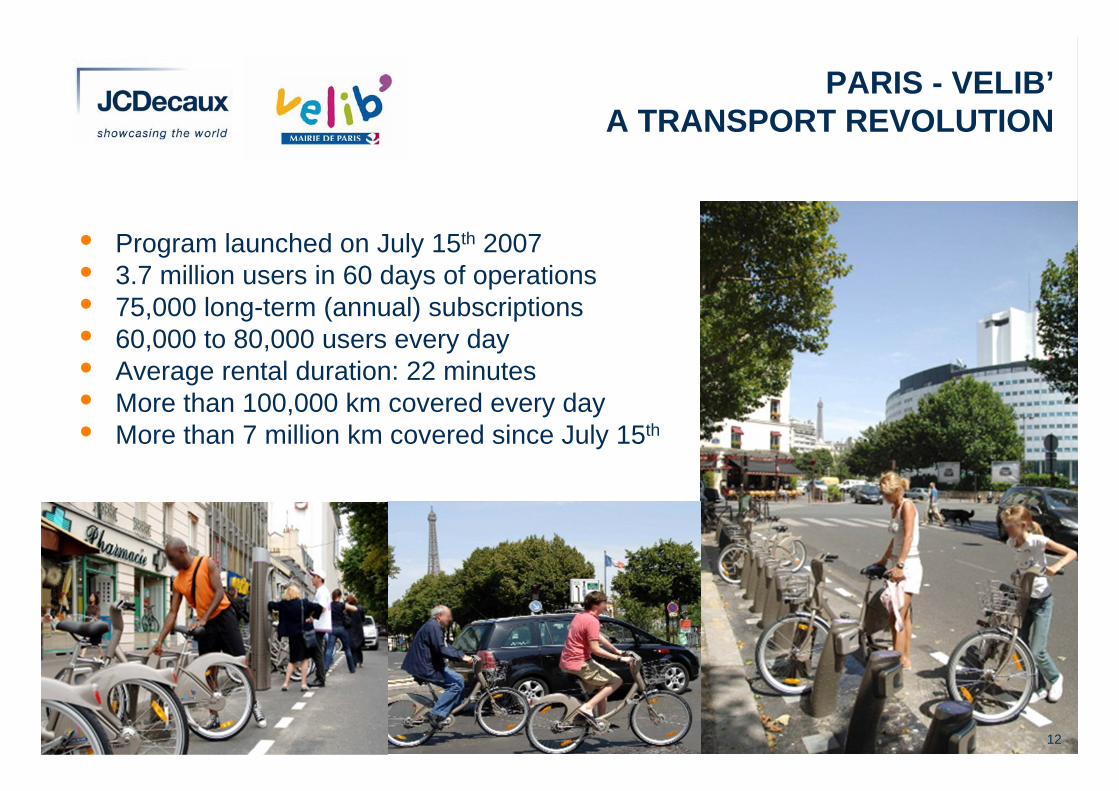

PARIS - VELIB’A TRANSPORT REVOLUTION

• Program launched on July 15th 2007• 3.7 million users in 60 days of operations• 75,000 long-term (annual) subscriptions • 60,000 to 80,000 users every day • Average rental duration: 22 minutes• More than 100,000 km covered every day• More than 7 million km covered since July 15th

12

13

SELF-SERVICE BIKESONE STRATEGY, SEVERAL BUSINESS MODELS

SIGNIFICANT

ADVERTISING

INVENTORY

MEDIUM-SIZEADVERTISING INVENTORY

LIMITEDADVERTISING INVENTORY

Paris5,900 advertising faces

Lyon 5,400 advertising faces

Marseille700 advertising faces

Toulouse 350 advertising faces

• 100% financed by Street Furniture advertising• Quality incentive paid to JCDecaux

(up to 12% of ad revenues + bicycle revenues)

• 100% financed by Street Furniture advertising• Yearly subscriptions (revenues go to JCDecaux)

• Rent paid by the city to JCDecaux• Partially financed by Street Furniture advertising• Advertising on bicycles (revenues go to JCDecaux)

• Largely financed by the city• Partially financed by Street Furniture advertising• Advertising on bicycles (revenues go to JCDecaux)• Yearly subscriptions (revenues go to JCDecaux)

14

• Organic growth & renewals

• The bike revolution

• Sales & Marketing

BUSINESS HIGHLIGHTS

15

3-YEAR PAN EUROPEANALLIANCE WITH SAMSUNG

Utilization of JCDecaux networks in 20 countries

All Samsung divisions included in the partnershipMobile phone, TV , MP3, white goods, digital cameras

All divisions of JCDecaux Street Furniture - Billboard - Transport

A GLOBAL COMPANY WORKING WITH GLOBAL BRANDS

&

16

A MULTI-FORMATPARTNERSHIP

London Paris

Lisbon AirportParis CDG Airport Barcelona Airport

Paris

London

17

Number of Innovate campaigns:

+61% from 440 in 2005 to 710 in 2006

• Creative outdoor advertising• Tailor-made execution• Using new technological solutions (Bluetooth®…)

Meeting advertisers’ demand for consumer engagement

NOW AVAILABLE IN 34 COUNTRIES

18Lisbon airport, Portugal – May 2007

SPECIAL BUILDVODAFONE

19

Paris, France – May 2007Allowing children to send pictures of their faces via the Internet to be posted on the banner.

INTERACTIVE LARGE FORMAT PANELDISNEYLAND PARIS 15th ANNIVERSARY

20Brussels, Belgium July 2007 Madrid, Spain

SPECIAL BUILDSTHE SIMPSONS MOVIE

21

SPECIAL EFFECTSDIE HARD 4

Brussels, Belgium July 2007

22

FINANCIAL HIGHLIGHTSGérard Degonse

Executive Vice-President, Finance & Administration

23

H1 2007 H1 2006 % change

P&L

(In million €, except %, under IFRS standards)

(1) Operating Margin = Revenues less Direct Operating Costs (excluding Maintenance spare parts and including SG&A costs)(2) EBIT = Earnings Before Interests and Taxes

= Operating Margin less Maintenance spare parts less Depreciation and provisions less Goodwill impairment less Other operating income and expenses(3) Due to the finalisation of the purchase accounting related to the acquisition of Media Partners International, H1 2006 EBIT and Net income Group share have been restated.

Revenues 1,019.0 945.8 +7.7% Operating costs (739.0) (680.8)

Operating margin (1) 280.0 265.0 +5.7%Depreciation, spare parts & others (104.3) (95.2)(3)

Goodwill impairment - -EBIT (2) 175.7 169.8 (3) +3.5%Financial income (loss) (22.2) (22.2)

Tax (45.7) (44.7) (3)

Equity affiliates 9.2 5.6 (3)

Minority interests (2.9) (2.2)

Net Income Group share 114.1 106.3 (3) +7.3%

24

Operating margin (% of revenues) EBIT (% of revenues)

Street Furniture

Billboard TotalGroup

41.3%

27.5%

-50bp

17.9%

+240bp

Street Furniture

BillboardTransport TotalGroup

26.4%

17.2%

-240bp-80bp

10.7%

+320bp

5.6%0bp

-140bp

(under IFRS standards)

Transport

9.7%+10bp

MARGINS BY DIVISION

25

Operating margin (% of revenues)

38404143

4546454340

363537

39 3840

45

40

1985 ‘86 ‘87 ‘88 ‘89 ‘90 ‘91 ‘92 ‘93 ‘94 ‘95 ‘96 ‘97 ‘98 ‘99 ‘00 ‘01 ‘02

European Expansion US Expansion

‘03 ‘04 ‘05 ‘06

41 4243

41 42

Revenues x 6.6

STREET FURNITUREMARGINS AROUND 40%

H1 07

41

Note: French Gaap until 2004 – IFRS as of 2005

French renewalsEmerging markets’expansion

26

H1 2007 H1 2006 % change

P&L

(In million €, except %, under IFRS standards)

(1) Operating Margin = Revenues less Direct Operating Costs (excluding Maintenance spare parts and including SG&A costs)(2) EBIT = Earnings Before Interests and Taxes

= Operating Margin less Maintenance spare parts less Depreciation and provisions less Goodwill impairment less Other operating income and expenses(3) Due to the finalisation of the purchase accounting related to the acquisition of Media Partners International, H1 2006 EBIT and Net income Group share have been restated.

Revenues 1,019.0 945.8 +7.7% Operating costs (739.0) (680.8)

Operating margin (1) 280.0 265.0 +5.7%Depreciation, spare parts & others (104.3) (95.2)(3)

Goodwill impairment - -EBIT (2) 175.7 169.8 (3) +3.5%Financial income (loss) (22.2) (22.2)

Tax (45.7) (44.7) (3)

Equity affiliates 9.2 5.6 (3)

Minority interests (2.9) (2.2)

Net Income Group share 114.1 106.3 (3) +7.3%

27

(In million €, except %, under IFRS standards)

Net Cash flow from operating activities 144.3 148.5 -2.8%General Inv. & Renewal capex (59.0) (52.4)Adjusted free cash flow 85.3 96.1 -11.2%

Growth capex (incl. intangible asset) (77.5) (29.6)

Free cash flow 7.8 66.5 -88.3%Dividends (net) (88.5) (85.2)Equity increase 0.9 11.6 Financial investments (net) (9.1) (44.2)Others (1) (4.3) 9.8

Change in net debt (Balance Sheet) (2) 93.2 41.5

CASH FLOW STATEMENT

Note: Adjusted free cash flow = Free Cash Flow before Growth Capex.(1) Non cash variations (mainly due to consolidation scope variations, translation differences on net financial debt, the impact of IAS 39 and finance lease)(2) Excluding the IAS 32 impact, including the IAS 39 impact on both debt and financial derivatives and including the restatement of loans granted to

companies consolidated under the proportionate method

H1 2007 H1 2006 % change

28

CAPEX2004 - 2008

2004 20062005 2007(e) 2008(e)

168

92

141

59

93

141In m€

Growth capex

Renewal capex

General Inv.

25

1921 25 2523

80

617557

90

Paris

75

70

180(excl. Intangibles)

Growth capex / intangiblesIncl. € 78 m pre-payment to

Shanghai Metro(€ 39 m in 2007 - € 39 m in 2008)

260(excl. Intangibles)

29

A ROBUST FINANCIAL STRUCTURE

• SOUND FUNDAMENTALS

• STRONG GENERATION OF CASH FLOW

• A BALANCE SHEET READY FOR GROWTH & EXPANSION

30

GROWTH STRATEGY AND OUTLOOKJean-Charles Decaux

Co-CEO

31

A GROWTH MEDIA SECTOR

A GROWING SECTOROutdoor continues to benefit from the fragmentation of traditional media

NEW FORMATSDigital upside

EMERGING COUNTRIESIncreased exposure

32

Apart from the internet, onlycinema and outdoor are forecastto grow faster than the market to 2009. […] Outdoor continues to gain share as contractors invest

in better displays and betterresearch.

OUTDOOR ADVERTISING,A GROWING SECTOR

2007-2009 CAGR forecast growth

Total ad.market6.0%

Outdoor TV Print Radio Internet

7.7%

6.2%

3.5% 3.8%

19.2%

Source: Zenith Optimedia Forecast – June 2007

ZenithOptimedia’s Advertising Expenditure Forecasts, June 2007

33

NEW FORMATSDIGITAL OUTDOOR ADVERTISING

Digital Wall - New York JFK Airport The Torch - LondonTrackside Plasma TV – Hong Kong subway

AIRPORTS• Paris Airports• BAA Airports incl. Heathrow T5

• New York JFK Airport• Los Angeles (LAX) Airport

SUBWAYS• Hong Kong • Vienna• Prague

CITIES• London• Cannes• Ad-hoc campaigns in bus

shelters (plasma screens)

• Rational move to digital: step by step and selective• Particularly relevant to transit environment with captive audience• A way to extend and renew contracts

34

Heathrow T5 – London

Digital walkways

Photomontage

BAATHE FUTURE OF AIRPORT ADVERTISING

« Terminal 5 will act as a blueprint for the future of airport advertising and we are looking forward to rolling it out across all BAA airports in the future »Duncan Tolson, Director of Media at BAA

• One of the largest deployment of digital technology worldwide• State of the art digital technology• 700 digital locations across all BAA• Capex paid by BAA

• Heathrow T5 opening: March 2008• 280 digital locations

34

35

SHANGHAI SUBWAYA SUCCESSFUL RENEWAL & EXTENSION

Exclusive 15-year contractFrom 5 metro lines in 2007 to 13 metro lines by 2012China’s largest subway system

20075 lines

95 stations1.8 million pax/day

20109 lines

250 stations6 million pax/day

201213 lines

350 stations7.2 million pax/day

Shanghai World Expo

A landmark franchise strengtheningJCDecaux’ market leading position in China’s largest city

35

36

• China’s largest metro advertising contract

• Joint-venture with Shanghai metro- Financial rights: 65% JCD - 35% metro- Equity rights: 51% JCD - 49% metro

• Expected revenues€ 1.5 bn over 15 years @ 100%

• Different fee structure vs usualTransport contracts

- 15 years- no minimum guarantee- reduced annual revenue share- € 78 million pre-payment(€ 39 m in 2007 - € 39 m in 2008)

SHANGHAI SUBWAYA LANDMARK FRANCHISE

Contract descriptionSubway benchmark

2010 daily traffic(1)

2010 Yearly revenues(2)

Moscow 7.7 million -

Shanghai 6.0 million € 60 m

New York 5.7 million € 60 m

Paris 4.4 million € 100 m

€ 180 mLondon 3.2 million

(1) JCDecaux estimates assuming a yearly traffic growth of 2% as of 2006 for London, Moscow, New York and Paris subway systems(2) JCDecaux estimates of 2010 revenues

37

INCREASED EXPOSURE TO FAST-GROWING OUTDOOR MARKETS

Fastest-growing outdoor markets worldwideCountries showing double-digit growth in 2008 vs 2007 (Zenith Optimedia, June 2007)

Growth JCD presence

Eastern EuropeSlovakia +41% N°1Moldova +25%Russia +22% through BigBoardRomania +20% through AffichageLithuania +16% Bulgaria +16% Bosnia +13%Greece +12% through AffichageBelarus +11%Latvia +10% N°1Slovenia +10% N°1

Latin AmericaUruguay +10%

Growth JCD presence

Asia PacificChina +25%(1) N°1Indonesia +20%India +13%Hong Kong +13% N°1Singapore +12% Malaysia +10% Australia +10%

Middle East / AfricaUnited Arab E. +58%Qatar +47% Saudi Arabia +44%Kuwait +32%Egypt +20%Bahrain +17%South Africa +10%Algeria +10%

Ongoing business

development

(1) Data for the Chinese outdoor market are not available. 25% is the growth of total ad spend forecast by Zenith Optimedia in 2008.

38

THE RIGHT COMPANY IN THE RIGHT BUSINESS AT THE RIGHT TIME

• OUTDOOR:The only media (excl. Internet) gaining market share within the media mix

• JCDECAUX:- A well-balanced:

- Mix of activities- Geographic exposure

- Strong growth prospects from: - Well-established markets- Emerging countries

39

REVENUESWe continue to expect that our organic revenue growth in 2007 will be similar to that of 2006, within a likely range of 7-8%, reflecting an

acceleration of organic revenue growth in the second half due toongoing strength in the Transport division, a stronger growth rate in

Street Furniture and improved market conditions in France.

OUTLOOK FOR 2007

40Paris, France – September 2007

H1 2007 RESULTSSeptember 12th 2007

41Paris, France – September 2007

H1 2007 RESULTSSeptember 12th 2007

42Paris, France – September 2007

H1 2007 RESULTSSeptember 12th 2007