36-month ltros a pyrrhic victory

TRANSCRIPT

8/3/2019 36-Month LTROs a Pyrrhic Victory

http://slidepdf.com/reader/full/36-month-ltros-a-pyrrhic-victory 1/11

Nomura International plc

See Disclosure Appendix A1 for the Analyst Certification and Other Important Disclosures

Rates Insights

R A T E S S T R A T E G Y | E U R O P E

36-month LTROs: A pyrrhic victory? The large take- up at the ECB’s December 36- month operation (€489bn) has been

positive for bank liquidity, but we think at most it provides more breathing space for

European leaders to formulate an effective solution to the debt crisis. Through

these operations the ECB is providing an interim solution to the liability side of

bank balance sheets; it is not intended to resolve the significant impairment on the

asset side. Although there has been a large repricing of the front-end of sovereign

curves into and since the operation, we do not think this demand will persist as the

ECB ’s operation is not about adjusting the dynamics of the stock or flow demand

problems faced by European sovereigns. Although the operations have eased

funding pressure, which the continued holding of sovereign debt may have created,

it is increasingly the sole source of funding for some institutions. It also comes at a

cost as collateral haircuts require funding and result in increased subordination of

senior unsecured debt due to the pledging of assets as collateral, which may

impair term funding via private sector funding markets at a later date.

We do not think the 29 February 36- month LTRO will be as large as December’so peration, estimating €200 -300bn. If the ECB communicates further LTROs we

could see a reduced take up as banks would have further opportunities to access

ECB funding. If it is as large, or greater in size, we think the result would be

distinctly negative for European banks. The fundamental issues in Europe are

unchanged by these operations, but they have likely bought much needed time for

policymakers to conclude any proposed solutions. If unambiguous long-term

solutions are not provided while the positivity of the LTROs is in place peripheral

debt is unlikely to continue to perform. However until the February LTRO has been

conducted it may take a discrete risk event to reverse the current bullish trend

Trade recommendations:

We like scaling into June EUR FRA/OIS wideners (protection could be set using OTM Euribor calls).

- Enter at 47.5bp, target 67bp, stop 35bp.

Alternatively we like scaling into March ’12/ March ’13 FRA/OIS basis steepeners.

- Enter at -18bp, target 0bp, stop -25bp.

The ECB’s 3-year LTRO – the force behind the market rally

Fundamentals have not changed, but the LTRO spurred bigger moves forfront-end bonds than we expected.The LTRO has had a greater impact on bond yields than we expected, though this

may have been partly facilitated by continued illiquid conditions. Since the first 3yrLTRO auction on 21 December, which resulted in €489bn in demand, Italian andSpanish 2yr yields have declined 230bp and 185bp respectively, as the curvesbull-steepened. Many in the market expect the next LTRO auction on 29 Februaryto be even larger, expecting a number around €1trn, which many investors believewill spur a broad-based carry trade in Europe‟s debt market sufficient to markedlyease the financing burden of European sovereigns. As such, the provision of sucha sizable pool of liquidity has fuelled a growing optimism in the market.

In light of the LTRO-spurred rally, we analyse whether the LTRO has indeedformed a sea-change in the eurozone debt crisis. We conclude that:

The 3yr LTRO significantly reduced the tail-risk of a liquidity-driven

collapse by a European bank… …but that the ECB liquidity will have adverse unintended consequences

for private sector financing of banks…

…and that it is more expensive funding than commonly viewed…

Fixed Income Research

Contributing Strategist

Guy Mandy+44 (0) 20 7103 [email protected]

This report can be accessedelectronically via:www.nomura.com/research or onBloomberg (NOMR)

24 January 2012

8/3/2019 36-Month LTROs a Pyrrhic Victory

http://slidepdf.com/reader/full/36-month-ltros-a-pyrrhic-victory 2/11

Nomura | European Rates Insights

2

24 January 2012

…which pr ovides an effective floor to front-end rates as driven by ECBliquidity…

…both of which will limit the size of next month‟s LTRO…

…as such, without non-bank investor demand, we do not think the LTROwill lead to a durable flow of liquidity into Europe‟s non-core bondmarkets …

…meaning that we retain our bearish strategic view on non-core Europeanbond markets.

Reasons why the LTRO spurred bond buyingThe LTRO has clearly underpinned a rally in the front-end of European bondmarkets, a segment of the market that had already experienced improvedsentiment following the November slump, which saw some curves invert. We wouldhighlight several avenues – other than the obvious one of banks being providedwith a fresh liability which they needed to translate into an asset – through whichthe 3yr LTRO supported the front-end of bond markets.

Reducing the risk of a bank liquidity shock. The boost in liquidity provided bythe ECB essentially reduces the potential for a European bank to face a liquidity

crisis caused by solvency concerns. The effect of tempering the negative portion ofthe risk distribution has played a part in the general contraction seen in the market,and in this respect is justified in our view. It is important to note that the LTROfunding reduces but does not remove this risk. After all, the LTRO liquidity willprovide only part of a bank‟s liability base, and demand for funds reflects a bank‟sassessment of future funding needs and it may underestimate this requirement inour view.

Replacement funding provides temporary support for bonds as proceeds are likely invested until needed . A number of banks would have taken ECB fundingin order to cover immediate requirements as well as for insurance to cover othercontingencies such as redemptions in the event that term funding markets remainshut when these liabilities fall due. (Around €450bn of unsecured bank debt is due

to redeem in 2012.) The drawing of liquidity for insurance purposes leads to ademand for returns to cover a portion of funding costs, which may lead someinstitutions to invest in short-maturity domestic paper. However, once the liabilitiesfall due the positions will likely be liquidated.

Anticipation of carry trades becomes self-reinforcing . There is also the effectthat investor expectations of a carry trade have on the market. In effect anticipationof carry trade flows into front-end sovereign bonds leads investors to invest in whatis deemed to be the trade de jour without knowing whether it has in fact occurred.As such the expectation of flow creates flow, driving bonds richer, and becomesself-reinforcing.

Increased ECB liquidity and GC repo richness help Spanish and Italian GC

repo . GC repo remains rich, partly due to the level of EONIA compressing levelsbut also due to the demand for high quality collateral. The levels of GC on coresovereign markets may have forced investors down the credit curve from a repoperspective, particularly in Spain and Italy where the additional liquidity from theECB has likely boosted the GC market in these countries. This may have been afactor in the tightening of the front-end of the curve, with the reopening of thismarket spurring some demand for front-end paper for use as collateral. Banks withliquidity may be utilising this to lend through repo channels on domestic bonds.

Reasons to doubt the durability of the LTRO rallyWhile the factors noted above have spurred demand for front-end bonds, a number

of factors question the durability of these flows, and similarly question the market‟sexpectation for next month‟s LTRO to be significantly larger that December‟s. Thissaid the ability for the market to maintain a positive bias could be tested by discreteevents in our view. These include the potential for a disorderly default in Greece aswell as continued downgrades of sovereigns, notably Italy, which could trigger achain of margin calls.

8/3/2019 36-Month LTROs a Pyrrhic Victory

http://slidepdf.com/reader/full/36-month-ltros-a-pyrrhic-victory 3/11

Nomura | European Rates Insights

3

24 January 2012

It seems that majority of recent peripheral sovereign supply take down has been bydomestic banks. Besides risk events, without greater demand from non-bankinvestors the currently level of supply absorption may not be sustainable. Thiscould pose problems once the February LTRO has been completed.

Mark-to-market risks remain key As the LTRO is a repo transaction the ECB takes in collateral in order to back any

loans. This highlights one of the key differences from QE, which entails the assetrisk being removed from the bank‟s balance sheet and replaced with cash. Under the LTRO framework the economic benefit remains with the bank. With the majorityof the funding being utilised by banks in peripheral countries, their asset base islikely to be for the most part correlated with the performance of domestic sovereignbonds. Figure 1 below shows the increase in realised volatility across peripheralbonds over the past few years. The significant increase in volatility, althoughcurrently working positively for collateral correlated with sovereign bonds, couldlead to greater variation margin call risk as collateral deviates from threshold levels.Asymmetry persists, with a major problem being a discrete risk event leading to amargin call, which could trigger a chain of margin calls.

Fig. 1: Peripheral debt volatility* –

mark-to-market risk

Source: Nomura Research, Bloomberg*60day rolling window

Fig. 2: Credit differentiation –

affect on curves

Source: Nomura Research, Bloomberg

Credit differentiation in place even on core curves The concerns about possible mark-to-market risk were perhaps evident to theextent that markets displayed a degree of credit differentiation. In the highest rated,highest quality markets (Germany and Netherlands), the provision of additionalliquidity further spurred demand, and investors were more willing to lengthenduration beyond the front-end. This resulted in a general flattening in 2s5s curvesin many higher-rated bond markets. In contrast, curves were far steeper in semi-core countries, and indeed in France, which lost its AAA rating from S&P. Giventhe lower degree of extension in stronger markets we do not expect a significantextension in periphery curves. (Figure 2)

ECB deposits. Unproductive liquidity provides negative carry.The eurozone financial system is flush with liquidity, such that excess liquidity inthe euro area is now at record highs at ~ €514bn. However, there are clear signsthat this is not being invested in eurozone bond markets to the extent that manyanticipate. Excess liquidity may still simply be surplus liquidity and may not find itsway into sovereign bond curves.

Bids in last week‟s ECB reverse liquidity operation to drain SMP purchasesamounted to €377bn to drain €217bn, showing €160bn in additional non-invested

liquidity. The immediate uplift in excess liquidity from the 21 December 36-monthLTRO was €200bn. However, including the shorter liquidity operations executed bythe ECB since the LTRO, at that date excess liquidity levels had in fact decreasedby approximately €60bn. There is clearly a significant chunk of incremental liquiditysince the LTRO that is not being invested in sovereign curves. This lends weight tothe argument that carry trade expectations may have become self-reinforcing.

0bp

5bp

10bp

15bp

20bp

25bp

30bp

35bp

40bp

45bp

2007 2009 2011

Market weighted 5-year 60d realised vol

Core 5-year 60d re alised vol

Semi-core 5-year 60d re alised vol

Periphery 5-year 60d re alised vol

-40bp

-30bp

-20bp

-10bp

0bp

10bp

20bp

30bp

40bp

50bp

60bp

70bp

80bp

90bp

100bp

110bp

120bp

130bp

Oct-11 Nov-11 Dec-11 Jan-12

Spread (RHS) Netherlands 2s5s France 2s5s

8/3/2019 36-Month LTROs a Pyrrhic Victory

http://slidepdf.com/reader/full/36-month-ltros-a-pyrrhic-victory 4/11

Nomura | European Rates Insights

4

24 January 2012

Downgrade risks in Italy could lead to a large ECB margin call A key risk in Europe is the continued downgrading of sovereigns. One in particularcould be Italy after S&P cut the sovereign to BBB+ last week. The ECB collateralframework allows for the highest rating on a sovereign to count as the overall rating,which indicates the collateral haircut bucket it falls into. If Moody‟s and Fitch bothcut their ratings on Italy to the BBB+ or below range, under current documentationthe ECB would call for an additional 5% margin across the BTPs curve. The impact

of the LCH move in Q4 2011 may provide some indication of the potential marketdisruption.

The effect could cause a repricing of other peripheral curves which, given theincreasing amount of peripheral collateral likely posted at the ECB, could cause achain of margin calls. Although we would expect the ECB to take action againstsuch an event, anticipation of it could undermine fleeting confidence.

Shortages of collateral for some institutions are highlighted by the move to broaden the range of bank loans accepted. One of the key restrictions on theamount of liquidity the ECB can inject into the system is the amount of collateralavailable, particularly the amount available to banks that have the greatest liquidityrisk. This was likely the reasoning behind the ECB‟s broadening of eligible

collateral rules at the December 2011 meeting, which includes accepting a broaderrange of bank loans. Details of this are expected towards the end of the month andwill come from the national central banks (NCBs). The NCBs already accept creditclaims, and although the new set of criteria will relax restrictions these are as yetunknown. The new loan arrangements are at the discretion of the NCBs.One proffered restriction is that a large amount of outstanding loans are registeredunder English law, with the ECB only accepting credit claims subject to the nationallaw of the euro-area countries. This should no doubt add to the pool of eligiblecollateral, with an advantage being that loans pledged to the ECB are not markedas frequently as traded instruments, though the haircut structure is far morepunitive – ranging from 8% for high quality, shorter than one year maturity loans to64.5% on BBB+/BBB- loans with maturities greater than 10 years. The greatestvolume of loans, particularly in high ECB usage countries such as Italy, are greater

than five years in maturity. Haircuts in this bucket start at 29%.

LTROs are increasingly punitive and lead to subordination of senior unsecured bank debt. The haircut structure and increased asset usage effectivelymeans that further ECB liquidity is increasingly punitive, utilising ever more balancesheet. The more the facility is used the greater the degree of subordination tosenior creditors, which previously would have partially relied on the assets, nowpledged to the ECB, as security against senior debt. This problem is particularlypertinent given that banks have already been using the covered bond markets toraise funds, which require over-collateralisation in order to achieve higher ratingsand to meet the criteria laid down by the ECB in order to be deemed eligiblecollateral for operations.

The LTRO funding is much higher than the headline 1% Bank balance sheets are levered, even if only to a small multiple, therefore assetsrequire funding. As such haircuts on the loans or other assets pledged to the ECBneed to be funded by the banks, despite unsecured funding no longer beingpossible for the majority of institutions (Figures 3 and 4). With the ECB effectivelythe only or primary source of bank funding in the euro area, this indicates thathaircuts will in essence be funded by the ECB. Following the circular nature of thisleads to ever greater tie-up of balance sheet via operations.

The cost of the haircuts and existing funding costs on leveraged banks balancesheets means that the cost of funding from the ECB is not 1%. For example, if afirm uses a 5-year maturity or greater loan book as collateral there is at minimum a29% haircut, but there would also be a capital charge levied under Basel rulings

given there is a requirement to hold varying amounts of capital against assetsrelated to their riskiness. As an example, we assume for simplicity a blended cost(cost of capital and funding) of 5% and a capital charge of 5% against the loanbook. In this case against a €100 asset there would be a €29 haircut and €5 capitalcharge giving €34 to fund through other sources. At a 5% blended rate the fundingcost would be €1.70. Adding to this the €1 cost via the ECB, the actual all-in cost is

8/3/2019 36-Month LTROs a Pyrrhic Victory

http://slidepdf.com/reader/full/36-month-ltros-a-pyrrhic-victory 5/11

Nomura | European Rates Insights

5

24 January 2012

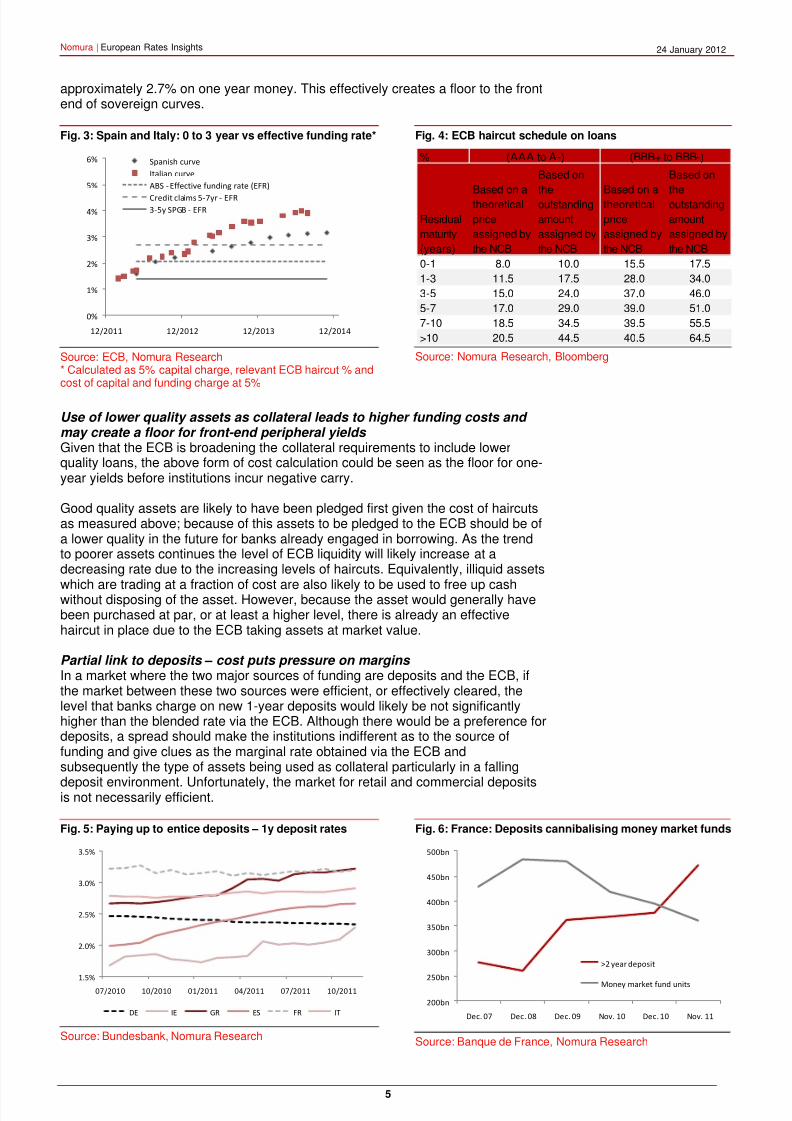

approximately 2.7% on one year money. This effectively creates a floor to the frontend of sovereign curves.

Fig. 3: Spain and Italy: 0 to 3 year vs effective funding rate*

Source: ECB, Nomura Research* Calculated as 5% capital charge, relevant ECB haircut % andcost of capital and funding charge at 5%

Fig. 4: ECB haircut schedule on loans

Source: Nomura Research, Bloomberg

Use of lower quality assets as collateral leads to higher funding costs and may create a floor for front-end peripheral yields Given that the ECB is broadening the collateral requirements to include lowerquality loans, the above form of cost calculation could be seen as the floor for one-year yields before institutions incur negative carry.

Good quality assets are likely to have been pledged first given the cost of haircutsas measured above; because of this assets to be pledged to the ECB should be ofa lower quality in the future for banks already engaged in borrowing. As the trendto poorer assets continues the level of ECB liquidity will likely increase at adecreasing rate due to the increasing levels of haircuts. Equivalently, illiquid assets

which are trading at a fraction of cost are also likely to be used to free up cashwithout disposing of the asset. However, because the asset would generally havebeen purchased at par, or at least a higher level, there is already an effectivehaircut in place due to the ECB taking assets at market value.

Partial link to deposits – cost puts pressure on margins In a market where the two major sources of funding are deposits and the ECB, ifthe market between these two sources were efficient, or effectively cleared, thelevel that banks charge on new 1-year deposits would likely be not significantlyhigher than the blended rate via the ECB. Although there would be a preference fordeposits, a spread should make the institutions indifferent as to the source offunding and give clues as the marginal rate obtained via the ECB andsubsequently the type of assets being used as collateral particularly in a falling

deposit environment. Unfortunately, the market for retail and commercial depositsis not necessarily efficient.

Fig. 5: Paying up to entice deposits – 1y deposit rates

Source: Bundesbank, Nomura Research

Fig. 6: France: Deposits cannibalising money market funds

Source: Banque de France, Nomura Research

0%

1%

2%

3%

4%

5%

6%

12/2011 12/2012 12/2013 12/2014

Spanish curve

Italian curve

ABS - Effective funding rate (EFR)

Credit claims 5-7yr - EFR3-5y SPGB - EFR

%

Residual

maturity

(years)

Based on a

theoretical

price

assigned by

the NCB

Based on

the

outstanding

amount

assigned by

the NCB

Based on a

theoretical

price

assigned by

the NCB

Based on

the

outstanding

amount

assigned by

the NCB

0-1 8.0 10.0 15.5 17.5

1-3 11.5 17.5 28.0 34.0

3-5 15.0 24.0 37.0 46.0

5-7 17.0 29.0 39.0 51.0

7-10 18.5 34.5 39.5 55.5

>10 20.5 44.5 40.5 64.5

(AAA to A-) (BBB+ to BBB-)

1.5%

2.0%

2.5%

3.0%

3.5%

07/2010 10/2010 01/2011 04/2011 07/2011 10/2011

DE IE GR ES FR IT

200bn

250bn

300bn

350bn

400bn

450bn

500bn

Dec. 07 Dec. 08 Dec. 09 Nov. 10 Dec. 10 Nov. 11

>2 year deposit

Money market fund units

8/3/2019 36-Month LTROs a Pyrrhic Victory

http://slidepdf.com/reader/full/36-month-ltros-a-pyrrhic-victory 6/11

Nomura | European Rates Insights

6

24 January 2012

French bank deposits have been increasing, in part due to the higher rates on offer,but this has effectively diverted funds that would previously have been placedwithin money market funds. The increase in rates offered on new deposits in orderto attract funds is more distinct in new business offered by Italian banks. The majordrawback with this is the impact on net interest margins and subsequently retainedincome in an environment with a capital shortage.

Holding peripheral debt has provided limitations and potentially caused funding problems In the current framework, with no euro-area solution, holding peripheral sovereigndebt has made it less likely that banks will be extended term funding. The generaldifficulties provided by the marking of sovereign assets through EBA stress testsand the accounting of this have left certain banks less inclined to increaseexposure to sovereign debt.

This lack of fresh term funding and reducing balance sheets could lead to banksallowing loans to roll off in order to raise cash. This would mean that loan bookswould need to be unpledged for them to gain the benefit of the loans rolling off intocash, lowering the degree to which the shorter-dated loan books are pledged to theECB.

How big will the next LTRO be?

The next 36-month operation is likely to be big; the question is how big? It shouldbe bigger than the shorter LTROs as the long-term operations have a majoradvantage with regards to the timing of the payment of interest on borrowings.Besides the haircut taken on the collateral, the interest cost, from a cashperspective, is only settled at the end of the term of the repo meaning a reductionin interim funding cash flows. This is a major advantage over the 1w/1m/3mfunding roll to cash-strapped banks.

Upside reasons to consider: The inclusion of a broader spectrum of loans should lead to a significant

amount of additional balance sheet available for repo through the ECBoperations. The downside to this is the significant haircuts on these assets.

With the reduction in credit criteria on loans eligible. There is perhapspotential for funds drawn through the ELAs in Greece and Ireland totransfer to the mainstream ECB LTROs.

Deposit levels in peripheral countries, and the degree to which they havebeen fluctuating, may be instructive as to the amount of funding that maybe taken down. The higher the volatility of these deposits the moreattractive the ECB insurance option should be.

Factors that could weigh on the overall size of the next operation:

Banks have taken a significant amount of ECB funding already, with amarked increase from Spanish and Italian banks. According to nationalcentral bank data, an incremental €26bn and €57bn was taken by banksdomiciled in those countries respectively. The Spanish take at the end ofDecember 2011 was €132bn against the €210bn borrowed by Italian banks. We think the funding taken will cover 2012 bank redemptions to asignificant degree.

Decreased volume of liquidity rolling from old LTROs and MROso For the December operation €50bn rolled for the October 12-

month operation as well as from the 3-month.

The ECB dropping its reserve ratio from 2% to 1% means liberation offunds, though this should largely affect MROs on the margin, but funds thatwere not provided through liquidity operations will now be available tobanks increasing available liquidity.

Bigger picture, the level of deleveraging in the banking sector as well asthe private sector could lead to reduced funding requirements.

8/3/2019 36-Month LTROs a Pyrrhic Victory

http://slidepdf.com/reader/full/36-month-ltros-a-pyrrhic-victory 7/11

Nomura | European Rates Insights

7

24 January 2012

In aggregate we think that the total level of funds taken down through the ECBoperation will be less than the previous round. In our estimation this is likely to bein the €200-300bn range.

If the size is bigger than this, perhaps in the range of €500bn or greater , the effecton bank balance sheets in Europe will be distinctly negative in our view, and wouldmake future wholesale and term funding from private sector sources significantly

more difficult.

What does this mean for short end rates and trades?

Euribor is falling, but it is unsecured funding...With the improved liquidity position of banks in the system and reduced risk of afunding shortage, as can be seen in bank CDS repricing tighter, Euribor fixingshave declined. This is understandable for a limited period of time, but the greaterextent that balance sheets are encumbered through the use of the ECB LTROfacilities the higher the loss to the holders of senior debt in the event of default onsenior debt and the greater the overall risk to the system. And of course, Euribor is

uncollateralised funding. We think the view that rates are set to be lower for longeris correct, but this is from a central bank perspective. With persistent bankingissues in Europe, in time Euribor could come under pressure, and if risk sentimentreverses, there could be a marked turnaround in the Euribor rally.

EONIA/ Euribor basis is expected to be increasingly a function of Euribor Although Euribor will likely be the main driver of the FRA-OIS spread, we thinkthere is potential for lower EONIA rates in some maturities. With the next 36-monthLTRO at the end of February and the potential length of these operations (1yr witha 2yr option) we expect excess liquidity to remain high for an extended periodanchoring EONIA. Without the cancellation of fine-tuning operations, spikes inEONIA through the maintenance period roll are unlikely. There could also bepotential for a cut in the deposit rate if the situation in Europe deteriorates further,

which may put further downward pressure on EONIA. The increased use of ECBfunding in lieu of wholesale funding negates the ECB‟s main argument in favour of a wide +/- 75bp policy-rate corridor, namely the need to avoid crowding out privatesector money market activity. However, while we see potential for lower EONIAfixes, we do not expect this to be a notable driver of the FRA-OIS basis. After all,while we expect the ECB to lower policy rates by a further 25bp in H1 2012, weexpect the policy corridor to be narrowed to +/- 50bp, keeping the floor of thedeposit rate at 25bp.

Fig. 7: Front end bases compressing

Source: ECB, Nomura Research

Fig. 8: March ’12/March ’13 basis curve

Source: Nomura Research, Bloomberg

The counter-trend trade –

FRA-OIS spread wideners The FRA-OIS bases have been compressing as general rates levels have movedlower and a consensus trade in the market is to position for a further compressionof the basis. The moves yesterday with a higher EONIA fix and lower Euribor fixhave caused the basis to contract significantly, largely on the March IMM, but havealso provided better levels for entry into wideners.

-9bp

-6bp

-3bp

0bp

3bp

6bp

30bp

35bp

40bp

45bp

50bp

55bp

60bp

65bp

1st IMM 2nd IMM 3rd IMM 4th IMM 5th IMM 6th IMM

1 day change

23/01/2012

20/01/2012

-60bp

-40bp

-20bp

0bp

20bp

40bp

30bp

40bp

50bp

60bp

70bp

80bp

90bp

100bp

Oct-11 Nov-11 Dec-11 Jan-12

Spr ead (RHS) FRA /O IS sp re ad IMM1 FRA /O IS spr ead IMM5

8/3/2019 36-Month LTROs a Pyrrhic Victory

http://slidepdf.com/reader/full/36-month-ltros-a-pyrrhic-victory 8/11

8/3/2019 36-Month LTROs a Pyrrhic Victory

http://slidepdf.com/reader/full/36-month-ltros-a-pyrrhic-victory 9/11

Nomura | European Rates Insights

9

24 January 2012

DISCLOSURE APPENDIX A1ANALYST CERTIFICATIONSI, Guy Mandy hereby certify (1) that the views expressed in this report accurately reflect my personal views about any or all of the subjectsecurities or issuers referred to in this report, (2) no part of my compensation was, is or will be directly or indirectly related to the specificrecommendations or views expressed in this report and (3) no part of my compensation is t ied to any specific investment bankingtransactions performed by Nomura Securities International, Inc., Nomura International plc or any other Nomura Group company.

Issuer Specific Regulatory Disclosures

Mentioned companies

Issuer name Disclosures

FEDERAL REPUBLIC OF GERMANY 11

GOVERNMENT OF PORTUGAL/PORTUGAL 11

Hellenic Republic 11

REPUBLIC OF IRELAND 11,49

Republic of Italy 11

Disclosures required in the U.S.

49 Possible IB related compensation in the next 3 months Nomura Securities International, Inc. and/or its affiliates expects to receive or intends to seek compensation for investment banking

services from the company in the next three months.

Disclosures required in the European Union

11 Liquidity provider Nomura International plc and/or its affiliates (collectively "Nomura") is a primary dealer and/or liquidity provider in European, UnitedStates and Japanese government bonds. As such, Nomura will generally always hold positions in these bonds, which from time to time,may be considered a significant financial interest.

IMPORTANT DISCLOSURES

Online availability of research and additional conflict-of-interest disclosures

Nomura Japanese Equity Research is available electronically for clients in the US on NOMURA.COM, REUTERS, BLOOMBERG and

THOMSON ONE ANALYTICS. For clients in Europe, Japan and elsewhere in Asia it is available on NOMURA.COM, REUTERS andBLOOMBERG.Important disclosures may be accessed through the left hand side of the Nomura Disclosure web page http://www.nomura.com/research orrequested from Nomura Securities International, Inc., on 1-877-865-5752. If you have any difficulties with the website, please email [email protected] for technical assistance.The analysts responsible for preparing this report have received compensation based upon various factors including the firm's totalrevenues, a portion of which is generated by Investment Banking activities.Unless otherwise noted, the non-US analysts listed at the front of this report are not registered/qualified as research analysts underFINRA/NYSE rules, may not be associated persons of NSI, and may not be subject to FINRA Rule 2711 and NYSE Rule 472 restrictions oncommunications with covered companies, public appearances, and trading securities held by a research analyst account.

ADDITIONAL DISCLOSURES REQUIRED IN THE U.S.

Principal Trading: Nomura Securities International, Inc and its affiliates will usually trade as principal in the fixed income securities (or inrelated derivatives) that are the subject of this research report. Analyst Interactions with other Nomura Securities International, IncPersonnel: The fixed income research analysts of Nomura Securities International, Inc and its affiliates regularly interact with sales andtrading desk personnel in connection with obtaining liquidity and pricing information for their respective coverage universe.

Valuation Methodology - Global Strategy

A “Relative Value” based recommendation is the principal approach used by Nomura‟s Fixed Income Strategists / Analysts when t hey make“Buy” (Long) “Hold” and “Sell” (Short) recommendations to clients. These recommendations use a valuation methodology that identifiesrelative value based on:a) Opportunistic spread differences between the appropriate benchmark and the security or the financial instrument,b) Divergence between a country‟s underlying macro or micro-economic fundamentals and its currency‟s value andc) Technical factors such as supply and demand flows in the market that may temporarily distort valuations when compared to anequilibrium priced solely on fundamental factors.

In addition, a “Buy” (Long) or “Sell” (Short) recommendation on an individual security or financial instrument is intended to convey Nomura‟sbelief that the price/spread on the security in question is expected to outperform (underperform) similarly structured securities over a threeto twelve-month time period. This outperformance (underperformance) can be the result of several factors, including but not limited to: creditfundamentals, macro/micro economic factors, unexpected trading activity or an unexpected upgrade (downgrade) by a major rating agency.

DISCLAIMERS

This document contains material that has been prepared by the Nomura entity identified at the top or bottom of page 1 herein, if any, and/or,

with the sole or joint contributions of one or more Nomura entities whose employees and their respective affiliations are specified on page 1herein or identified elsewhere in the document. Affiliates and subsidiaries of Nomura Holdings, Inc. (collectively, the 'Nomura Group'),include: Nomura Securities Co., Ltd. ('NSC') Tokyo, Japan; Nomura International plc ('NIplc'), UK; Nomura Securities International, Inc.('NSI'), New York, US; Nomura International (Hong Kong) Ltd. („NIHK‟), Hong Kong; Nomura Financial Investment (Korea) Co., Lt d. („NFIK‟),Korea (Information on Nomura analysts registered with the Korea Financial Investment Association ('KOFIA') can be found on the KOFIAIntranet at http://dis.kofia.or.kr ); Nomura Singapore Ltd. („NSL‟), Singapore (Registration number 197201440E, regulated by the MonetaryAuthority of Singapore); Capital Nomura Securities Public Company Limited („CNS‟), Thailand; Nomura Australia Ltd. („NAL‟), Australia(ABN 48 003 032 513), regulated by the Australian Securities and Investment Commission ('ASIC') and holder of an Australian financialservices licence number 246412; P.T. Nomura Indonesia („PTNI‟), Indonesia; Nomura Securities Malaysia Sdn. Bhd. („NSM‟), Malaysia;

8/3/2019 36-Month LTROs a Pyrrhic Victory

http://slidepdf.com/reader/full/36-month-ltros-a-pyrrhic-victory 10/11

Nomura | European Rates Insights

10

24 January 2012

Nomura International (Hong Kong) Ltd., Taipei Branch („NITB‟), Taiwan; Nomura Financial Advisory and Securities (India) Private Limited(„NFASL‟), Mumbai, India (Registered Address: Ceejay House, Level 11, Plot F, Shivsagar Estate, Dr. Annie Besant Road, Worli, Mumbai-400 018, India; Tel: +91 22 4037 4037, Fax: +91 22 4037 4111; SEBI Registration No: BSE INB011299030, NSE INB231299034,INF231299034, INE 231299034, MCX: INE261299034); Banque Nomura France („BNF‟), regulated by the Autorité des marches financiersand the Autorité de Contrôle Prudentiel; NIplc, Dubai Branch („NIplc, Dubai‟); NIplc, Madrid Branch („NIplc, Madrid‟) and NIplc, Italian Branch(„NIplc, Italy‟).

This material is: (i) for your private information, and we are not soliciting any action based upon it; (ii) not to be construed as an offer to sellor a solicitation of an offer to buy any security in any jurisdiction where such offer or solicitation would be illegal; and (iii) based uponinformation from sources that we consider reliable, but has not been independently verified by Nomura Group.

Nomura Group does not warrant or represent that the document is accurate, complete, reliable, fit for any particular purpose ormerchantable and does not accept liability for any act (or decision not to act) resulting from use of this document and related data. To themaximum extent permissible all warranties and other assurances by Nomura group are hereby excluded and Nomura Group shall have noliability for the use, misuse, or distribution of this information.Opinions or estimates expressed are current opinions as of the original publication date appearing on this material and the information,including the opinions and estimates contained herein, are subject to change without notice. Nomura Group is under no duty to update thisdocument. Any comments or statements made herein are those of the author(s) and may differ from views held by other parties withinNomura Group. Clients should consider whether any advice or recommendation in this report is suitable for their particular circumstancesand, if appropriate, seek professional advice, including tax advice. Nomura Group does not provide tax advice.

Nomura Group, and/or its officers, directors and employees, may, to the extent permitted by applicable law and/or regulation, deal asprincipal, agent, or otherwise, or have long or short positions in, or buy or sell, the securities, commodities or instruments, or options or otherderivative instruments based thereon, of issuers or securities mentioned herein. Nomura Group companies may also act as market makeror liquidity provider (as defined within Financial Services Authority („FSA‟) rules in the UK) in the financial instruments of the issuer. Wherethe activity of market maker is carried out in accordance with the definition given to it by specific laws and regulations of the US or other jurisdictions, this will be separately disclosed within the specific issuer disclosures.

This document may contain information obtained from third parties, including ratings from credit ratings agencies such as Standard & Poor‟s.Reproduction and distribution of third party content in any form is prohibited except with the prior written permission of the related third party.Third party content providers do not guarantee the accuracy, completeness, timeliness or availability of any information, including ratings,and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the useof such content. Third party content providers give no express or implied warranties, including, but not limited to, any warranties ofmerchantability or fitness for a particular purpose or use. Third party content providers shall not be liable for any direct, indirect, incidental,exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including lost income orprofits and opportunity costs) in connection with any use of their content, including ratings. Credit ratings are statements of opinions and arenot statements of fact or recommendations to purchase hold or sell securities. They do not address the suitability of securities or thesuitability of securities for investment purposes, and should not be relied on as investment advice.

Any MSCI sourced information in this document is the exclusive property of MSCI Inc. („MSCI‟). Without prior written permission of MSCI,this information and any other MSCI intellectual property may not be reproduced, re-disseminated or used to create any financial products,including any indices. This information is provided on an "as is" basis. The user assumes the entire risk of any use made of this information.MSCI, its affiliates and any third party involved in, or related to, computing or compiling the information hereby expressly disclaim allwarranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of this information.Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in, or related to, computing or

compiling the information have any liability for any damages of any kind. MSCI and the MSCI indexes are services marks of MSCI and itsaffiliates.

Investors should consider this document as only a single factor in making their investment decision and, as such, the report should not beviewed as identifying or suggesting all risks, direct or indirect, that may be associated with any investment decision. Nomura Groupproduces a number of different types of research product including, among others, fundamental analysis, quantitative analysis and shortterm trading ideas; recommendations contained in one type of research product may differ from recommendations contained in other typesof research product, whether as a result of differing time horizons, methodologies or otherwise. Nomura Group publishes research productin a number of different ways including the posting of product on Nomura Group portals and/or distribution directly to clients. Differentgroups of clients may receive different products and services from the research department depending on their individual requirements.

Figures presented herein may refer to past performance or simulations based on past performance which are not reliable indicators of futureperformance. Where the information contains an indication of future performance, such forecasts may not be a reliable indicator of futureperformance. Moreover, simulations are based on models and simplifying assumptions which may oversimplify and not reflect the futuredistribution of returns.

Certain securities are subject to fluctuations in exchange rates that could have an adverse effect on the value or price of, or income derivedfrom, the investment.

The securities described herein may not have been registered under the US Securities Act of 1933 (the „1933 Act‟), and, in such case, maynot be offered or sold in the US or to US persons unless they have been registered under the 1933 Act, or except in compliance with anexemption from the registration requirements of the 1933 Act. Unless governing law permits otherwise, any transaction should be executedvia a Nomura entity in your home jurisdiction.

This document has been approved for distribution in the UK and European Economic Area as investment research by NIplc, which isauthorized and regulated by the FSA and is a member of the London Stock Exchange. It does not constitute a personal recommendation, asdefined by the FSA, or take into account the particular investment objectives, financial situations, or needs of individual investors. It isintended only for investors who are 'eligible counterparties' or 'professional clients' as defined by the FSA, and may not, therefore, beredistributed to retail clients as defined by the FSA. This document has been approved by NIHK, which is regulated by the Hong KongSecurities and Futures Commission, for distribution in Hong Kong by NIHK. This document has been approved for distribution in Australiaby NAL, which is authorized and regulated in Australia by the ASIC. This document has also been approved for distribution in Malaysia byNSM. In Singapore, this document has been distributed by NSL. NSL accepts legal responsibility for the content of this document, where itconcerns securities, futures and foreign exchange, issued by their foreign affiliates in respect of recipients who are not accredited, expert orinstitutional investors as defined by the Securities and Futures Act (Chapter 289). Recipients of this document in Singapore should contactNSL in respect of matters arising from, or in connection with, this document. Unless prohibited by the provisions of Regulation S of the 1933Act, this material is distributed in the US, by NSI, a US-registered broker-dealer, which accepts responsibility for its contents in accordance

with the provisions of Rule 15a-6, under the US Securities Exchange Act of 1934.This document has not been approved for distribution in the Kingdom of Saudi Arabia („Saudi Arabia‟) or to clients other than 'professionalclients' in the United Arab Emirates („UAE‟) by Nomura Saudi Arabia, NIplc or any other member of Nomura Group, as the case may be.Neither this document nor any copy thereof may be taken or transmitted or distributed, directly or indirectly, by any person other than thoseauthorised to do so into Saudi Arabia or in the UAE or to any person located in Saudi Arabia or to clients other than 'professional clients' inthe UAE. By accepting to receive this document, you represent that you are not located in Saudi Arabia or that you are a 'professional client'in the UAE and agree to comply with these restrictions. Any failure to comply with these restrictions may constitute a violation of the laws ofSaudi Arabia or the UAE.

8/3/2019 36-Month LTROs a Pyrrhic Victory

http://slidepdf.com/reader/full/36-month-ltros-a-pyrrhic-victory 11/11

Nomura | European Rates Insights 24 January 2012

NO PART OF THIS MATERIAL MAY BE (I) COPIED, PHOTOCOPIED, OR DUPLICATED IN ANY FORM, BY ANY MEANS; OR (II)REDISTRIBUTED WITHOUT THE PRIOR WRITTEN CONSENT OF A MEMBER OF NOMURA GROUP. Further information on any of thesecurities mentioned herein may be obtained upon request. If this document has been distributed by electronic transmission, such as e-mail,then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed,arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of thisdocument, which may arise as a result of electronic transmission. If verification is required, please request a hard-copy version.

Nomura Group manages conflicts with respect to the production of research through its compliance policies and procedures (including, butnot limited to, Conflicts of Interest, Chinese Wall and Confidentiality policies) as well as through the maintenance of Chinese walls andemployee training.

Additional information is available upon request. Disclosure information is available at the Nomura Disclosure web page:http://go.nomuranow.com/research/globalresearchportal/pages/disclosures/disclosures.aspx

Copyright © 2011 Nomura International plc. All rights reserved.

Nomura International plc Tel: +44 20 7102 1000

1 Angel Lane, London EC4R 3AB

Caring for the environment: to receive only the electronic versions of our research, please contact your sales representative.