30 june 2016 - the commercial real estate leader | united ... · pdf file... june 2016 |...

TRANSCRIPT

30 June 2016

2 CIVAS White Paper | June 2016 | Logistics | Colliers International

Hannah Jeong Director

Valuation and Advisory Services

Logistics real estate market investment

is highly sought by both regional and

local investors looking for high-yields.

Traditional retailers and manufacturers

have been the major demand drivers.

However, there is no doubt that the

fast-ever-growing E-commerce and

3PLs (Third Party Logistics) companies

are also emerging demand drivers.

Thanks to advanced mobile commerce

and arising internet penetration rate in

Asia, E-commerce together with 3PLs

businesses will continuously grow.

However, due to time constraints on

lengthy physical developments of

logistics centres, new supply is

projected to not be able to catch up with

the speed of this fast-growing demand,

at least for the next five years.

Therefore, the demand will continue to

outpace the supply in Asia.

In order to capture the rental premium

from these two sectors, the investors

need to build the logistics centres in a

close proximity to the city centres with

higher specifications and flexible

structures. The logistics centre will

evolve from a simple warehouse to a

more value-added centre and if the

buildings and facilities are ready to be

upgraded and transformable, they will

have a potential to generate higher

yields.

> Major Logistics Players

Major logistics players in Asia include GLP, Goodman,

Prologis, ERW (e-Shang and Redwood) and Mapletree,

which have heavy footprints in China, Japan, Hong

Kong and Singapore and are emerging in Korea and

other Southeast Asian counties. Of course there are

locally focused investors and fast-growing international

second movers in each country.

> E-Commerce market is far from saturation

Retail E-commerce sales share among total retail sales

is forecasted to increase significantly, especially in

China and India, in five years’ time, according to

eMarketer’s data (2014). Even mature markets like

Japan are still looking at almost doubling their E-

commerce sales share among total retail sales by 2019.

This indicates that logistics market demand from E-

commerce will continue to grow, which requires bigger

and larger scale warehouse spaces.

> 3PLs, raising star

Third Party Logistics (3PLs) is tightly connected and

benefited from the booming E-commerce industry

globally. In general, 3PLs require smaller scale logistics

warehouses but extensive network coverage for speedy

delivery. Proximity to city centres and residential

neighbourhoods are the key for logistics centres in

order to capture the growing demand from 3PLs. More

and more developers build multi-storey logistics centres

even for the markets where traditionally served by

single storey centres because of increasing industrial

land price in Asia, however, multi-storey logistics

centres are not the first choice for 3PLs.

> New Landscape

E-commerce’s new services such as E-fulfilment,

delivery consolidation and reverse logistics will change

the overall logistics real estate market landscape,

particularly for their location. Focus will be shifted from

the traditional logistics centre locations such as major

transportation nodes to the city centres. Further, higher

specifications including extra added-value spaces for

working and packing, extra cooling and heating facilities

for staff and higher ceiling height will be required to

accommodate rapidly transforming E-commerce

tenants.

3 CIVAS White Paper | June 2016 | Logistics | Colliers International

Contents Logistics, a Highly Sought Investment

Market ………………………………….. 4

Who are the Major E-commerce Players

by Market Share? ………………..……. 5

3PLs, Growing Demand …………..…. 6 How is E-commerce Changing the Logistics Real Estate Landscape? ……………………………. 7 Final Thoughts ………………………… 8 Asia Logistics Market Snapshot …….. 9

4 CIVAS White Paper | June 2016 | Logistics | Colliers International

Logistics, a Highly Sought Investment Market The logistics real estate market has been chased by

massive capital around the world, especially in Asia.

Given that it is a high yield-generating investment sector

with less intensive asset management involvement and

that it is also well supported by governments as a core

infrastructure of each country, it has continuously

received high attention from major investors. Large

pension funds such as CCPIB, APG and Ivanhoe

Cambridge are major Limited Partners (LPs) for various

real estate investment funds focusing on logistics

properties ranging from greenfield developments to

existing building acquisition and long-term asset

management.

Chart 1: China Logistics Area Comparison by Key Players

Source: GLP (May 2016), Colliers International Remark:*e-Shang share did not include Redwood in this comparison.

Chart 2: Japan Logistics Area Comparison by Key Players

Source: GLP (May 2016)

Major logistics players in Asia include GLP, Goodman,

Prologis, ERW (e-Shang and Redwood) and Mapletree,

which have heavy footprints in China, Japan, Hong Kong

and Singapore and are emerging in Korea and other

Southeast Asian counties. Of course there are locally

focused investors and fast-growing international second

movers in each country. As shown in Chart 1 and 2, GLP

is the market leader in terms of physical asset size for

China and Japan, where the highest GDPs are recorded

in Asia.

Based on our research, Korean logistics warehouses are

largely owned and occupied by end users (e.g. Korean

major conglomerates and major E-commerce companies

such as Coupang) in Korea. International players

including GIC, Mapletree and Kendall Square logistics

properties also have a presence there.

Hong Kong and Singapore are relatively smaller markets

in Asia, although both have achieved the highest rents

and capital values (see Chapter 9 in page 8).

Singapore’s logistics warehouses are largely owned and

managed by various REITs, namely, Mapletree Industrial

Trust, Mapletree Logistics Trust, AIMS AMP REIT, VIVA

Industrial Trust REIT, Cambridge Industrial Trust REIT,

AREIT and Soilbuild REIT. In Hong Kong, active

investors are real estate investment funds focusing on

logistics properties (e.g. Goodman and Mapletree),

logistics companies (Kerry Logistics and SF Logistics)

and major domestic developers (Sun Hung Kai,

Hutchison Group and Kowloon Wharf).

Single storey logistics properties (average ceiling height

from 9 m to 15 m) are commonly found in China, Japan,

Korea and India. On the other hand, multi-storey

warehouses are predominated the market in Singapore

and Hong Kong due to limited land resources.

In terms of demand, major tenants that are committed in

high-quality logistics properties comprise traditional

retailers (automobile, furniture, apparel and other goods),

manufacturers, E-commerce and 3PLs (3rd Party

Logistics).

The market pays attention to E-commerce and 3PLs that

have the most active and fastest growing demand for

logistics warehouses, especially in China, Japan and

Korea. In India, the demand from E-commerce is

emerging as well. 3PL includes LTL logistics (Less Than

Truckload) and CEP (Courier, Express and Parcel) firms

that are tightly related to the growth of E-commerce. E-

commerce retailers carry significantly greater product

variety. They require larger spaces on average and

strategic locations with good connections to major

transportation nodes. 3PLs need more extensive

logistics warehouse networks as they need to ensure

fast and efficient door-to-door delivery.

9.9

1.5 1.5 1.3 0.9 0.8 0.9

0.5 0.2 0.2

0

2

4

6

8

10

12

GLP Blogis Goodman e-Shang Prologis Mapletree Yupei ACL BeijingProperties

Vailog

GF

A (

Mil

lio

ns s

q m

)

4.0

2.5

2.2

1.1 1.1

0.7 0.6 0.6 0.6

0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

GLP Prologis DaiwaHouse

Lasalle JLF Nomura RE Mitsubishi SG Realty GoodmanJapan

Mapletree

GF

A (

Mil

lio

ns s

qm

)

GL

P S

take

: 1

9.9

%

GL

P S

take

: 5

1.3

%

GL

P S

take

: 9

0-9

5%

5 CIVAS White Paper | June 2016 | Logistics | Colliers International

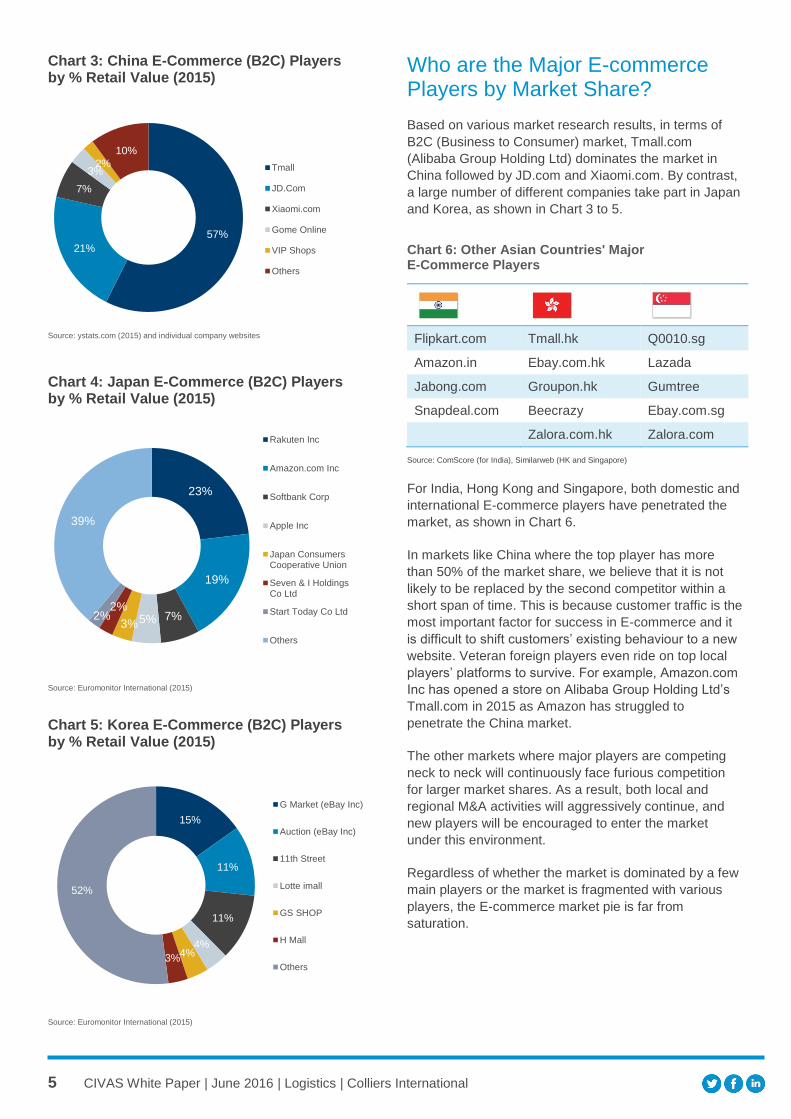

Chart 3: China E-Commerce (B2C) Players by % Retail Value (2015)

Source: ystats.com (2015) and individual company websites

Chart 4: Japan E-Commerce (B2C) Players by % Retail Value (2015)

Source: Euromonitor International (2015)

Chart 5: Korea E-Commerce (B2C) Players by % Retail Value (2015)

Source: Euromonitor International (2015)

Who are the Major E-commerce Players by Market Share?

Based on various market research results, in terms of

B2C (Business to Consumer) market, Tmall.com

(Alibaba Group Holding Ltd) dominates the market in

China followed by JD.com and Xiaomi.com. By contrast,

a large number of different companies take part in Japan

and Korea, as shown in Chart 3 to 5.

Chart 6: Other Asian Countries' Major E-Commerce Players

Flipkart.com Tmall.hk Q0010.sg

Amazon.in Ebay.com.hk Lazada

Jabong.com Groupon.hk Gumtree

Snapdeal.com Beecrazy Ebay.com.sg

Zalora.com.hk Zalora.com

Source: ComScore (for India), Similarweb (HK and Singapore)

For India, Hong Kong and Singapore, both domestic and

international E-commerce players have penetrated the

market, as shown in Chart 6.

In markets like China where the top player has more

than 50% of the market share, we believe that it is not

likely to be replaced by the second competitor within a

short span of time. This is because customer traffic is the

most important factor for success in E-commerce and it

is difficult to shift customers’ existing behaviour to a new

website. Veteran foreign players even ride on top local

players’ platforms to survive. For example, Amazon.com

Inc has opened a store on Alibaba Group Holding Ltd’s

Tmall.com in 2015 as Amazon has struggled to

penetrate the China market.

The other markets where major players are competing

neck to neck will continuously face furious competition

for larger market shares. As a result, both local and

regional M&A activities will aggressively continue, and

new players will be encouraged to enter the market

under this environment.

Regardless of whether the market is dominated by a few

main players or the market is fragmented with various

players, the E-commerce market pie is far from

saturation.

57%

21%

7%

3% 2%

10%

Tmall

JD.Com

Xiaomi.com

Gome Online

VIP Shops

Others

23%

19%

7% 5% 3%

2% 2%

39%

Rakuten Inc

Amazon.com Inc

Softbank Corp

Apple Inc

Japan ConsumersCooperative Union

Seven & I HoldingsCo Ltd

Start Today Co Ltd

Others

15%

11%

11%

4% 4%

3%

52%

G Market (eBay Inc)

Auction (eBay Inc)

11th Street

Lotte imall

GS SHOP

H Mall

Others

6 CIVAS White Paper | June 2016 | Logistics | Colliers International

“Japan’s logistics market demand from 3PL and

E-commerce increased over 125% and 270%

from 2006 to 2015 respectively." - GLP (2016 Company announcement)

As shown in Chart 7, retail E-commerce sales share

among total retail sales is forecasted to increase

significantly, especially in China and India, in five years’

time, according to eMarketer’s data (2014). In particular,

India has a great potential to catch up given its large

population and strong IT infrastructure. India’s current

offline retail structures are aged and out-dated in most of

the second tier cities due to lack of shopping centres in

the towns. Given that, people would try to buy new

trendy goods via E-commerce.

Even mature markets like Japan are still looking at

almost doubling their E-commerce sales share among

total retail sales by 2019. This indicates that logistics

market demand from E-commerce will continue to grow,

which requires bigger and larger scale warehouse

spaces. Prologis, one of the industry leaders, estimates

that every dollar of online sales needs three times more

distribution-and-warehouse space than one dollar of

bricks-and-mortar sales (quoted from the Wall Street

Journal, 14 June 2016).

Chart 7: Retail E-Commerce Sales % of Total Country

Retail Sales

Source: eMarketer (2014 Actual/ 2019 Estimation)

One of the main drivers for fast-growing E-commerce

sales is mobile commerce. Thanks to IT technology,

many people carry IT devices such as smartphones and

tablets. Moreover, as they are accustomed to using them

frequently, mobile commerce increased strongly. For

example, in Korea, the share of mobile commerce within

Internet retailing reached 45% in 2015, and is expected

to grow to 55% within five years (Euromonitor

International 2015).

However, physical developments of new logistics centres

require at least two to three years, and possible sites are

limited within the cities. As a result, logistics warehouses

supply will be behind demand from E-commerce and will

remain scarce.

Large E-commerce companies are also keen to build

their own logistics warehouses. However, renting high-

quality logistics warehouses or renting built-to-suit (BTS)

logistics warehouses would be a more flexible and

trouble-free solution for companies instead of going

through the various challenges - from obtaining

strategically located sites to actual construction. Alibaba

Group Holding Ltd obtained a number of vacant sites for

their logistics centre developments to accommodate their

fast ever growing business demand in China. However, it

will not be sufficient. Therefore, Tmall.com will continue

to be one of the major E-commerce tenants in China.

3PLs, Growing Demand

Chart 8: Asian Countries' Major 3PLs Players

Best Express

Alps Logistics

ACI Worldwide Express

Allcargo Logistics

Crown Logistics

DHL

Cainiao Network

DHL CJ Korea Express

Blue Dart Express

DHL Fedex

SF Express

Fedex DHL DHL Expeditors Kehne+Nagel

STO Express

Hitachi Transport System

Fedex DTDC Courier and Cargo

Fedex Network Courier

TTK Express

JFE Logistics

Hanjin Fedex Kerry Logistics

PCA Masters

UC Express

Kintetsu World Express

Hyundai Logistics

First Flight Panalpina Schenker

YTO Express

Nippon Express

OCS Gati Schenker TNT Express

Yunda Express

Sagawa Express

Sebang Express

Overnite Express

SF Express

Toll Logistics

ZJS Express

TNT Express

TNT Express

The Professional Courier Network

UPS UPS

ZTO Express

Yamato UPS TNT Express Yusen Yusen

Source: china.org.cn (China), Japan Institute of Logistics Systems (Japan), Journal of Korea

Port Economic Association, Vol.30, No.03, 2014, 209-230 (Korea), researchandmarkets.com

(India), HKTDC (HK), Singapore Economic Development Board (Singapore)

Remark: Listed in alphabetical order excluding each country’s Post Office Services.

12.4%

5.9%

10.3%

0.8%

3.0%

8.2% 6.3%

33.6%

9.7%

14.7%

4.8% 3.8%

20.4%

12.8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Others Asia-Pacific

WorldWide

2014 2019

7 CIVAS White Paper | June 2016 | Logistics | Colliers International

Third Party Logistics (3PLs) is tightly connected and

benefited from the booming E-commerce industry

globally. For example, Singapore Post announced that

its estimated E-commerce-related revenue increased

18.9% YoY (FY 2013/2014 vs. FY 2014/2015), which

was the biggest performance driver given that its overall

revenue increased 12% at the same time in 2015.

Singapore Post also made a large number of

acquisitions to enhance its E-commerce-related logistics

service and platform. Although Singapore’s E-commerce

market is relatively smaller, it is a great example of how

seriously E-commerce can impact the 3PLs industry.

3PLs need to handle significantly increased delivery and

warehousing volume, thanks to booming E-commerce.

Hence, 3PLs became an important demand driver for the

logistics real estate market. For instance, as per GLP’s

2016 announcement, Japan’s logistics market demand

from 3PLs and E-commerce increased over 125% and

270% from 2006 to 2015, respectively.

In general, 3PLs require smaller scale logistics

warehouses but extensive network coverage for speedy

delivery. According to comScore, Inc, Asian shoppers

are avid technology users and the least patient, with

48% expecting next-day shipping to be offered by

retailers, the highest in any market globally. Same-day

shipping or next-day shipping is a common practice in

Asia. Therefore, 3PL companies spin a web extensively

in order to get closer to their customers. Proximity to city

centres and residential neighbourhoods are the key for

logistics warehouses in order to capture the growing

demand from 3PLs.

3PLs requires frequent truck traffic in and out as well as

efficient loading/uploading system. Therefore 3PLs

prefer a single storey logistics centre type for their sole

use in order to prevent traffic congestion. More and more

developers build multi-storey logistics warehouses even

for the markets where traditionally served by single

storey centres because of increasing industrial land price

in Asia, however, multi-storey logistics centres are not

the first choice for 3PLs.

How will E-commerce change the Logistics Real Estate Landscape?

Traditionally, logistics warehouses are located near

major transportation nodes including airports and

seaports. Highway accessibility is one of the top

priorities for traditional logistics warehouses. However,

the following services from E-commerce will gradually

change the warehouse building standard and add

different location criteria.

> E-Fulfilment Service

Due to emerging demand from E-

commerce, developers' and investors’

checklist for new logistics centres has

been changed to generate higher rental

income.

One of the new forms is E-fulfilment centre driven by E-

commerce. In the US, where large E-commerce giants

started their business, E-fulfilment service provided by

logistics companies is quite mature. Once Asia's E-

commerce market becomes more mature, E-fulfilment

service providers will be developed as well.

As E-commerce merchants need convenience, visibility

and speed to accommodate fast-changing customer

appetite, E-fulfilment logistics centres need (1) to be

located close to the city centres, (2) to provide extra

added-value spaces for working and packing and (3) to

have higher specifications such as extra cooling and

heating facilities for staff and higher ceiling height.

These requirements are particularly driven from E-

fulfilment centres (a new service type from E-

commerce), where a vendor sends all its products to an

E-fulfilment centre. The centre then takes care of

everything from getting online orders, packing, labelling

and on-time delivery service. This is a labour-intensive

service that requires even larger logistics space than that

of general logistics business. Logistics investors should

take into account this new format in the near future when

the overall Asia E-commerce market becomes more

mature.

> Consolidation Service

Further, large Internet platform B2C

companies need to provide extra

consolidation delivery service if

customers order from different vendors

that are registered on the

same website. Customers want to receive one

consolidated package in order to save on delivery cost,

and this requires another central hub logistics distribution

centre for consolidation.

8 CIVAS White Paper | June 2016 | Logistics | Colliers International

> Reverse Logistics

Many E-commerce logistics facilities

accept returns, and floor space must

be allocated for returns processing

and restocking activities.

China newly implemented a return policy via Internet

purchase without giving any reason effective March

2014. When the E-commerce market becomes more

mature in Asia, this reverse logistics will be a compulsory

requirement. This will require additional strategic logistics

centres.

Final Thoughts Due to uncertainties in the global economy and the

slowdown in China and India, overall trading and retail

businesses in Asia are currently experiencing a

downturn, making investors concerned about the

demand side of the logistics real estate sector. Although

there is certain downsizing of traditional retailers’

businesses, thriving E-commerce and proliferous 3PLs

are making up the shortfall and supporting the logistics

real estate market in Asia.

Apart from China where Tmall.com (under Alibaba Group

Holdings Ltd) largely dominates the market, various local

and international E-commerce companies face fierce

competition in other Asian countries such as Japan,

Korea, India, Hong Kong and Singapore. Healthy

competition has continued to encourage more E-

commerce entrants in the market. Regardless of whether

the market is dominated by a few main players or

fragmented with various players, the E-commerce

market is far from saturation.

Retail sales via E-commerce in China and India are

forecasted to triple or quadruple in the next five years.

Established markets like Japan and Korea will still see

significant share increases over the next years. As a

consequence of growing E-commerce, a large number of

new local 3PLs have setup and global 3PLs are

aggressively increasing their footprints.

However, due to time constraints on lengthy physical

developments of logistics warehouses, new supply is

projected to not be able to catch up with the speed of this

fast-growing demand, at least for the next five years.

Although major E-commerce companies target to build

their own logistics warehouses, we expect that they will

not be able to solely absorb their massive trading volume

in-house and E-commerce will remain as the major

demand for the logistics real estate sector.

As the Asian E-commerce market becomes more

mature, E-commerce together with 3PLs are changing

the overall logistics real estate landscape and investors

need to pay attention to their requirements in order to

capture this rapid growing demand with rental premium.

E-commerce companies generally carry a wide variety of

products which require larger scale logistics warehouses.

Prologis, one of the industry leaders, estimates that

every dollar of online sales needs three times more

distribution-and-warehouse space than one dollar of

bricks-and-mortar sales (quoted from the Wall Street

Journal, 14 June 2016). Therefore, larger floor plates are

important for E-commerce tenants.

In terms of location, traditionally logistics warehouses

were located near major transportation nodes. However,

new centres need to be either inside or near to city

centres. Even though logistics rents in the city centres

are at least 20% more expensive compared to the sub-

urban areas, proximity to city centres are the key for

3PLs as Asian customers expect same day or next day

delivery. New services such as E-fulfilment, delivery

consolidation and reverse logistics will also need to be

as close to the city as possible.

Investors also need to consider more flexible building

structures with higher specifications to accommodate

fast transformation of the E-commerce industry in the

long term. For example, a higher ceiling height will be

able to add a mezzanine floor for packing and labelling if

the traditional warehouse needs to cater for E-fulfilment

service.

The logistics centre will evolve from a simple warehouse

to a more value-added centre and if the buildings and

facilities are ready to be upgraded and transformable,

they will have a potential to generate higher yields with

rental premium.

9 CIVAS White Paper | June 2016 | Logistics | Colliers International

Asia Logistics Market Snapshot

Chart 9: Market Snapshot

City, Country

Type

Face Unit Rent (US$

/ sqm) From To

Net Yield

From To

Rent Trends

Unit Capital Value

(US$ / sqm) From To

Beijing, China Single Storey

5.6 6.5 5.00% 6.50% Up 770 1,135

Shanghai,

China

Single Storey

4.3 6.6 5.50% 7.00% Up 650 955

Hong Kong,

China

High rise

13.9 19.4 4.50% 5.25% Down 3,470 4,850

Singapore High rise

15.0 19.8 5.75% 7.00% Down 5,848 6,877

Gyunggi

Province,

Korea

Single Storey

6.1 11.7 7.00% 8.50% Stable 919 1,126

Greater

Tokyo, Japan

Single Storey

6.8 12.2 4.50% 5.50% Stable 1,340 2,240

Mumbai

Metropolitan

Region, India

Single Storey

1.5 2.4 8.00% 12.00% Stable 56 149

Delhi NCR,

India

Single Storey

1.6 8.1 6.00% 10.00% Stable 91 181

Bangalore,

India

Single Storey

1.6 3.6 6.00% 10.00% Up 37 186

Source: Colliers International Valuation and Advisory Remark: Currency conversion as at date of 1 April 2016 (Bloomberg)

Chart 10: Logistics Performance Index Score (2014)

Source: Worldbank

Remark: Index score from 5 (highest) to 0 (lowest) based on six areas including customs, infrastructure, intentional shipments, logistics competence, tracking & tracing and timeliness.

The LPI is based on a worldwide survey of operators on the ground (global freight forwarders and express carriers), providing feedback on the logistics “friendliness” of the countries in which they operate and those they trade with.

Chart 11: Population (2015)

Source: IMF

Chart 12: GDP per Capita (2015)

Source: Worldbank

4.12 4.01 4.00 3.92 3.91 3.83 3.67 3.53

3.08

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

Germany UnitedKingdom

Singapore UnitedStates

Japan HongKong

Korea,Republic

of

China India

1,371.9

126.9 50.7

1,314.1

7.3 5.5

-100

100

300

500

700

900

1,100

1,300

1,500

13,801

38,216 36,601

6,266

56,428

85,198

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Tota

l P

opula

tio

n (

mill

ions)

GD

P p

er C

apita

(U

SD

)

Worldwide Ranking 1 4 5 9 10 15 21 28 54

Copyright © 2016 Colliers International.

The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has been made to ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any inaccuracies. Readers are encouraged to consult their professional advisors prior to acting on any of the material contained in this report.

About Colliers International Group Inc.

Colliers International Group Inc. (NASDAQ: CIGI; TSX: CIG) is an industry leading global real estate services company with more than 16,000 skilled professionals operating in 66 countries. With an enterprising culture and significant employee ownership, Colliers professionals provide a full range of services to real estate occupiers, owners and investors worldwide. Services include strategic advice and execution for property sales, leasing and finance; global corporate solutions; property, facility and project management; workplace solutions; appraisal, valuation and tax consulting; customized research; and thought leadership consulting.

Colliers professionals think differently, share great ideas and offer thoughtful and innovative advice that help clients accelerate their success. Colliers has been ranked among the top 100 outsourcing firms by the International Association of Outsourcing Professionals’ Global Outsourcing for 11 consecutive years, more than any other real estate services firm.

colliers.com

554 offices in

66 countries on

6 continents United States: 153

Canada: 34

Latin America: 24

Asia Pacific: 231

EMEA: 112

$2.5 billion in annual revenue

2 billion square feet under management

16,000 professionals and staff

Primary Author:

Hannah Jeong

Director | Hong Kong

+852 2822 0589

Contributors:

David Faulkner

Executive Director | Asia

+852 2822 0525

Vincent Cheung

Executive Director | Asia

+852 2822 0527

Flora He

Senior Director | China

+86 10 8518 9605

Seow-Leng Goh

Executive Director | Singapore

+65 6531 8561

Amit Oberoi

National Director | India

+91 124 456 7571

Yoshinori Nagai

Senior Manger | Japan

+81 3 5563 2180

Jasmine Kim

Managing Director | Korea

+82 2 3775 7350