24/05/2007 maria adler university of kaiserslautern department of mathematics 1 hyperbolic processes...

Post on 20-Dec-2015

212 views

TRANSCRIPT

24/05/2007

Maria AdlerUniversity of KaiserslauternDepartment of Mathematics 1

Hyperbolic Processes in Finance

Alternative Models for Asset Prices

224/05/2007

Hyperbolic Processes in Finance

Outline

The Black-Scholes Model Fit of the BS Model to Empirical Data Hyperbolic Distribution Hyperbolic Lévy Motion Hyperbolic Model of the Financial Market Equivalent Martingale Measure Option Pricing in the Hyperbolic Model Fit of the Hyperbolic Model to Empirical Data Conclusion

324/05/2007

Hyperbolic Processes in Finance

The Black-Scholes Model

0ttP price process of a security described by the SDE

tt

ttt

WtPP

dWPdtPdP

2exp

2

0 :

:

:0

0

ttW

volatility

drift

Brownian motion

rtBB

dtBrdB

B

t

ttt

tt

exp0

0

:0ttr interest rate

price process of a risk-free bond

424/05/2007

Hyperbolic Processes in Finance

Brownian motion has continuous paths stationary and independent increments market in this model is complete

allows duplication of the cash flow of

derivative securities and pricing by

arbitrage principle

The Black-Scholes Model

524/05/2007

Hyperbolic Processes in Finance

statistical analysis of daily stock-price data from 10 of the DAX30 companies

time period: 2 Oct 1989 – 30 Sep 1992 (3 years)

745 data points each for the returns

Result: assumption of Normal distribution underlying the

Black- Scholes model does not provide a good fit to

the market data

Fit of the BS Model to Empirical Data

624/05/2007

Hyperbolic Processes in Finance

Fit of the BS Model to Empirical Data

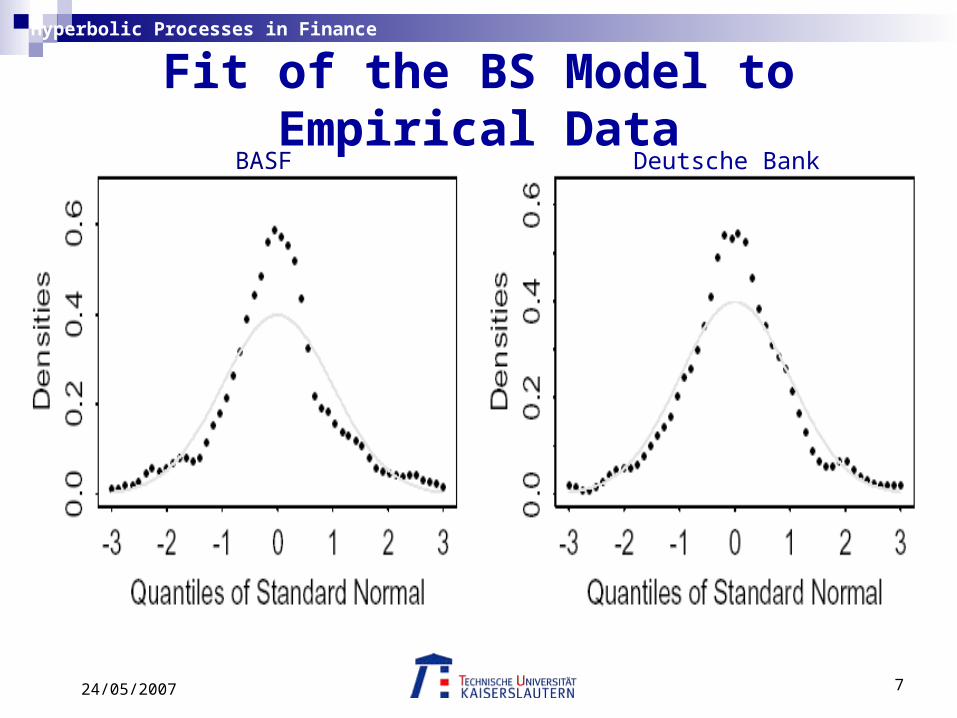

Quantile-Quantile plots & density-plots for the returns of BASF and Deutsche Bank to test goodness of fit:Fig. 4, E./K., p.7

724/05/2007

Hyperbolic Processes in Finance

Fit of the BS Model to Empirical Data

BASF Deutsche Bank

824/05/2007

Hyperbolic Processes in Finance

Brownian motion represents the net random effect of the various factors of influence in the economic environment

(shocks; price-sensitive information)

actually, one would expect this effect to be discontinuous, as the individual shocks arrive

indeed, price processes are discontinuous looked at closely enough (discrete ´shocks´)

Fit of the BS Model to Empirical Data

924/05/2007

Hyperbolic Processes in Finance

Fit of the BS Model to Empirical Data

Fig. 1, E./K., p.4

typical path of a Brownian motion continuousthe qualitative picture does not change if we change the time-scale,

due to self-similarity property

08.0,5.0,1000 P

0,2 ctcWtcW

1024/05/2007

Hyperbolic Processes in Finance

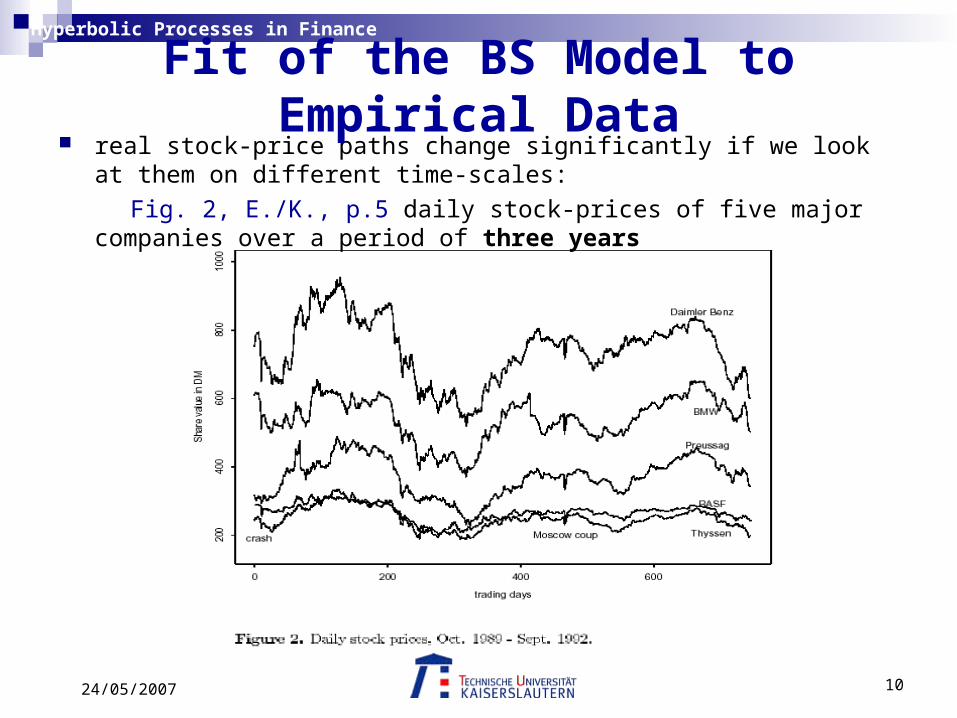

real stock-price paths change significantly if we look at them on different time-scales:

Fig. 2, E./K., p.5 daily stock-prices of five major companies over a period of three years

Fit of the BS Model to Empirical Data

1124/05/2007

Hyperbolic Processes in Finance

Fig. 3, E./K., p.6 path, showing price changes of the Siemens stock during a single day

Fit of the BS Model to Empirical Data

1224/05/2007

Hyperbolic Processes in Finance

Aim: to model financial data more precisely than with the BS model

find a more flexible distribution than the normal distr.

find a process with stationary and independent increments (similar

to the Brownian motion), but with a more general distr.

this leads to models based on Lévy processes

in particular: Hyperbolic processes

B./K. and E./K. showed that the Hyperbolic model is a more realistic market model than the Black-Scholes model, providing a better fit to stock prices than the normal distribution, especially when looking at time periods of a single day

Fit of the BS Model to Empirical Data

1324/05/2007

Hyperbolic Processes in Finance

Hyperbolic Distribution

introduced by Barndorff-Nielsen in 1977

used in various scientific fields: - modeling the distribution of the grain size of sand - modeling of turbulence - use in statistical physics

Eberlein and Keller introduced hyperbolic distribution functions into finance

1424/05/2007

Hyperbolic Processes in Finance

Density of the Hyperbolic distribution:

Hyperbolic Distribution

xxK

xhyp 22

221

22

,,, exp2

:1K modified Bessel function with index 1

characterized by four parameters:

:0 tail decay; behavior of density for x:0 skewness / asymmetry

shape

:R location

:0 scale

1524/05/2007

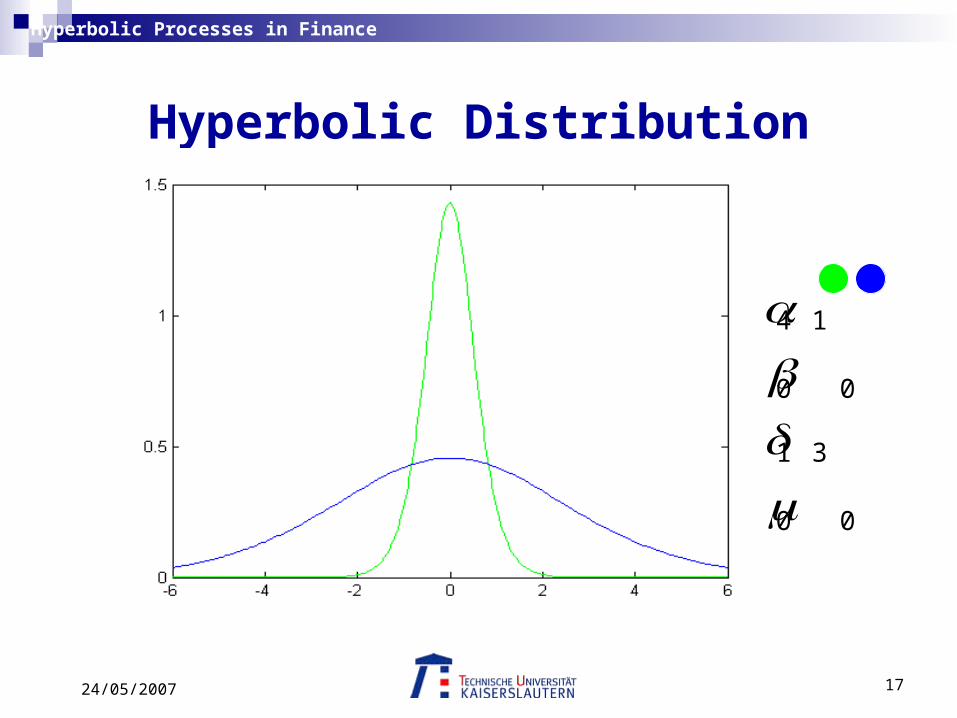

Hyperbolic Processes in Finance

Hyperbolic DistributionDensity-plots for different parameters:

1 9 0

0 0 0

1 1 1

0 0 0

1624/05/2007

Hyperbolic Processes in Finance

Hyperbolic Distribution

4 4

5 0

6 1

3 2

1724/05/2007

Hyperbolic Processes in Finance

Hyperbolic Distribution

4 1

0 0

1 3

0 0

1824/05/2007

Hyperbolic Processes in Finance

the log-density is a hyperbola ( reason for the name)

this leads to thicker tails than for the normal distribution, where the log-density is a parabola

Hyperbolic Distribution

xx 22 0

:, slopes of the asymptotics

: location

: curvature near the mode

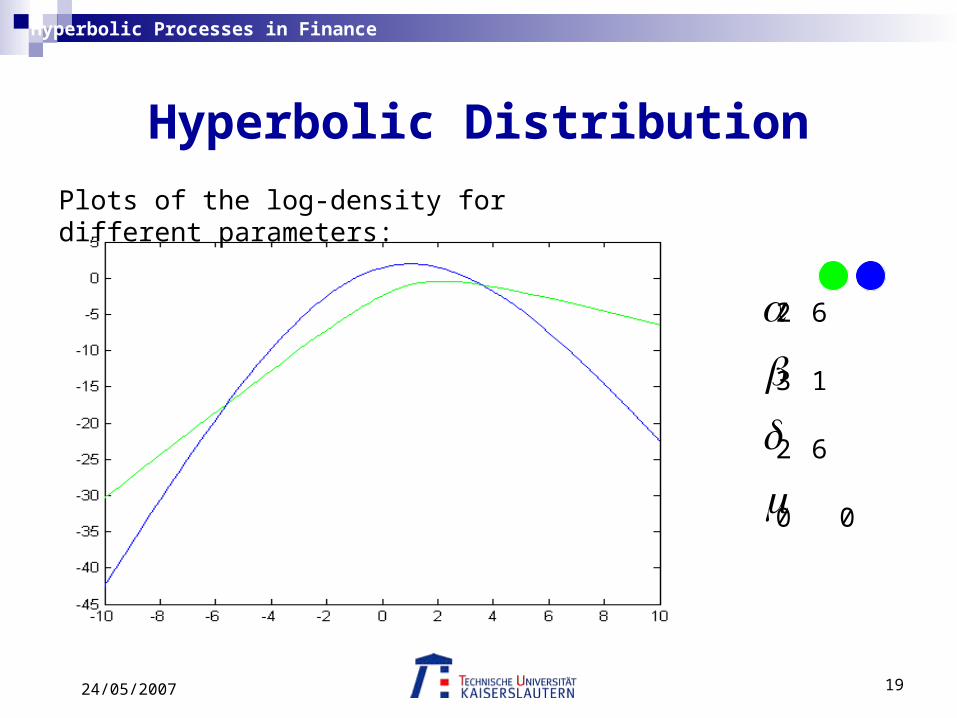

1924/05/2007

Hyperbolic Processes in Finance

Hyperbolic Distribution

Plots of the log-density for different parameters:

2 6

3 1

2 6

0 0

2024/05/2007

Hyperbolic Processes in Finance

Hyperbolic Distribution

2 2

3 1

2 10

0 0

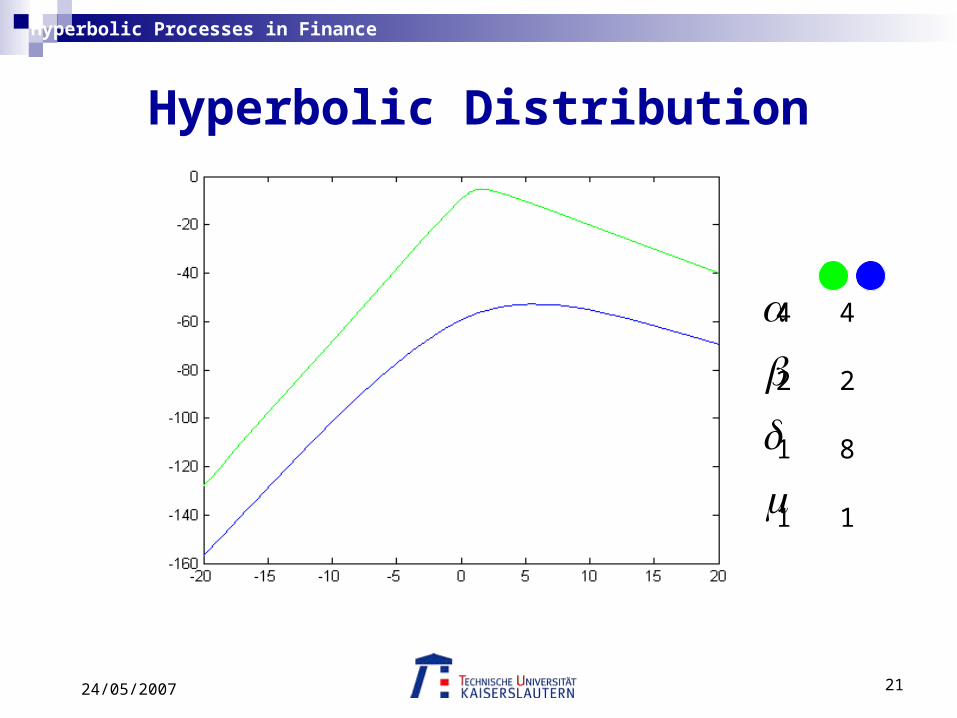

2124/05/2007

Hyperbolic Processes in Finance

Hyperbolic Distribution

4 4

2 2

1 8

1 1

2224/05/2007

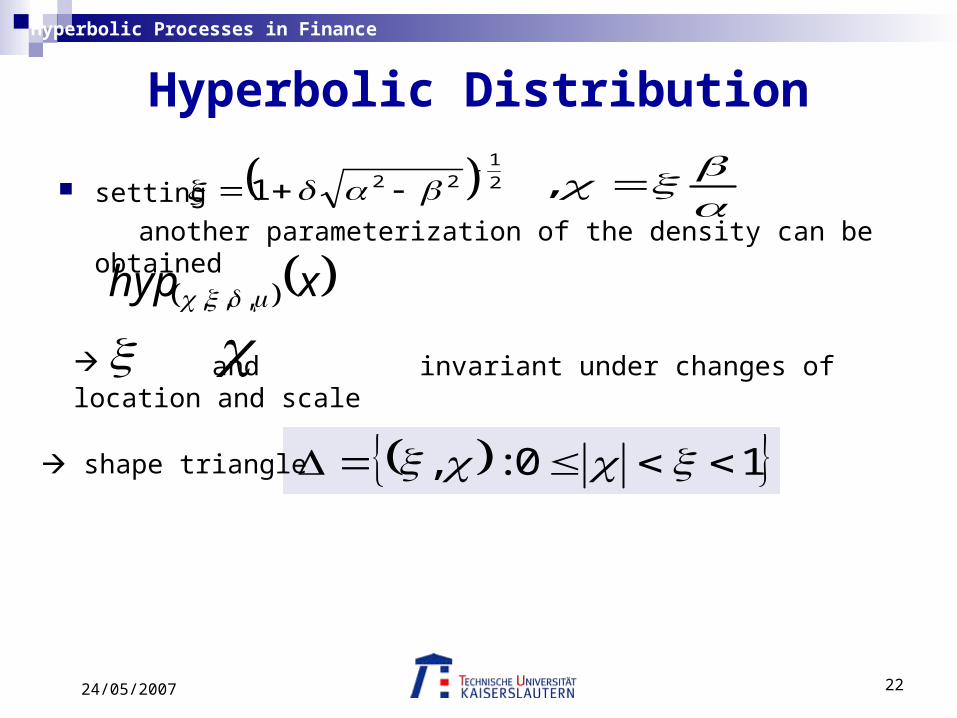

Hyperbolic Processes in Finance

setting

another parameterization of the density can be obtained

Hyperbolic Distribution

2

1221

,

xhyp ,,,

and invariant under changes of location and scale

10:, shape triangle

2324/05/2007

Hyperbolic Processes in Finance

Hyperbolic Distribution

Fig. 6, E./K., p.13

generalized inverse Gaussian

generalized inverse Gaussian

2424/05/2007

Hyperbolic Processes in Finance

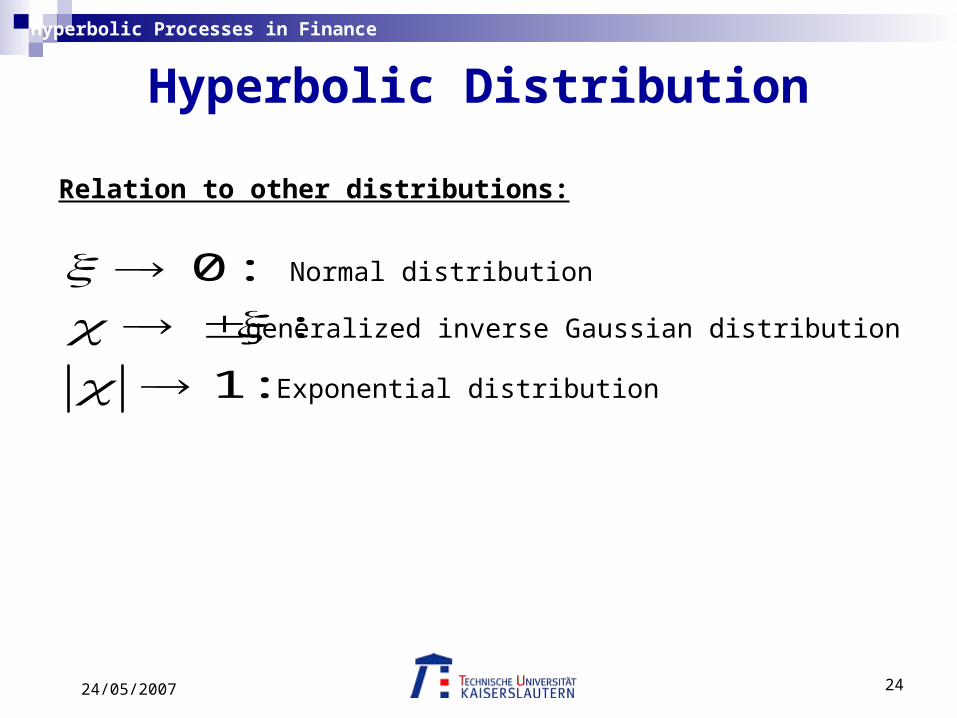

Relation to other distributions:

Hyperbolic Distribution

:1

:

:0

Normal distribution

generalized inverse Gaussian distribution

Exponential distribution

2524/05/2007

Hyperbolic Processes in Finance

Representation as a mean-variance mixture of normals:Barndorff-Nielsen and Halgreen (1977)

the mixing distribution is the generalized inverse Gaussian with density

Hyperbolic Distribution

xx

Kxd IG

1

1 2

1exp

2

• consider a normal distribution with mean and variance :2 2

22 , N

• such that is a random variable with distribution 2 xd IG

• the resulting mixture is a hyperbolic distribution xhyp ,,,

2624/05/2007

Hyperbolic Processes in Finance

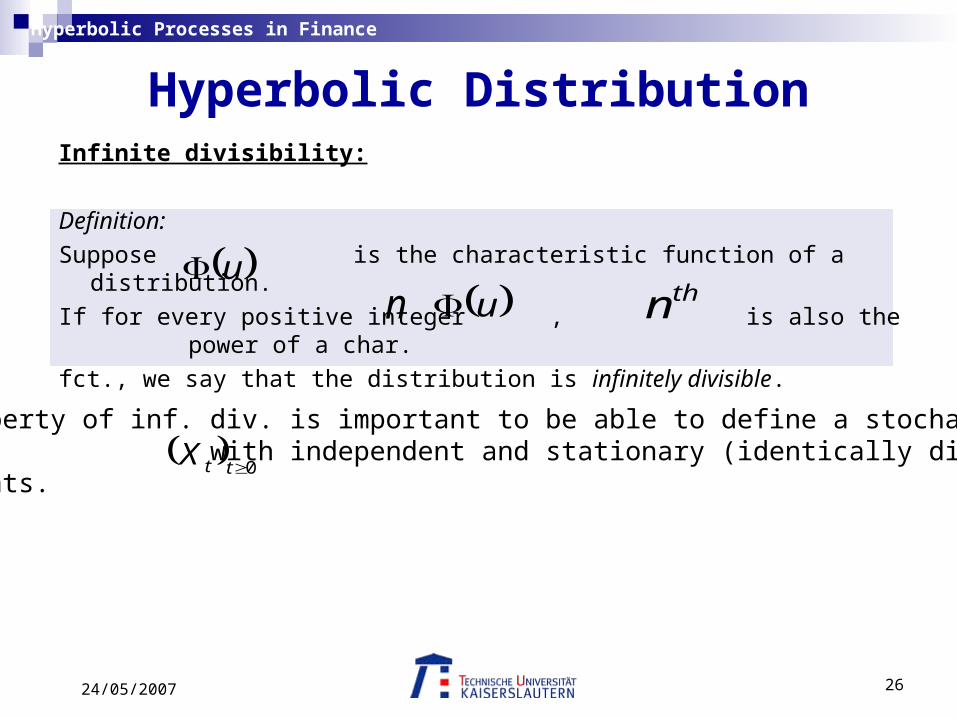

Infinite divisibility:

Definition:

Suppose is the characteristic function of a distribution.

If for every positive integer , is also the power of a char.

fct., we say that the distribution is infinitely divisible.

Hyperbolic Distribution

u u thnn

The property of inf. div. is important to be able to define a stochasticprocess with independent and stationary (identically distr.)increments.

0ttX

2724/05/2007

Hyperbolic Processes in Finance

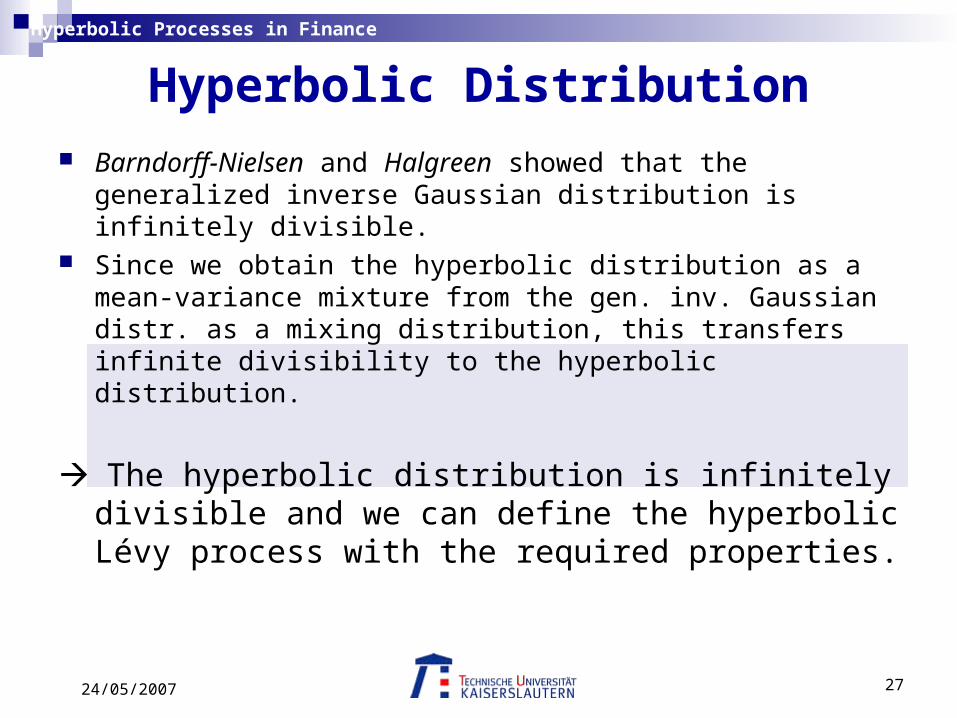

Barndorff-Nielsen and Halgreen showed that the generalized inverse Gaussian distribution is infinitely divisible.

Since we obtain the hyperbolic distribution as a mean-variance mixture from the gen. inv. Gaussian distr. as a mixing distribution, this transfers infinite divisibility to the hyperbolic distribution.

The hyperbolic distribution is infinitely divisible and we can define the hyperbolic Lévy process with the required properties.

Hyperbolic Distribution

2824/05/2007

Hyperbolic Processes in Finance

To fit empirical data it suffices to concentrate on the centered

symmetric case.

Hence, consider the hyperbolic density

Hyperbolic Distribution 0

0/0

1

1

0,

,1exp2

1

2

2

122

2

1,

x

Kxhyp

2924/05/2007

Hyperbolic Processes in Finance

Characteristic function:

The corresponding char. fct. to is given by

Hyperbolic Distribution

xhyp ,

222

2221

1

,;u

uK

Kuu

• All moments of the hyperbolic distribution exist.

3024/05/2007

Hyperbolic Processes in Finance

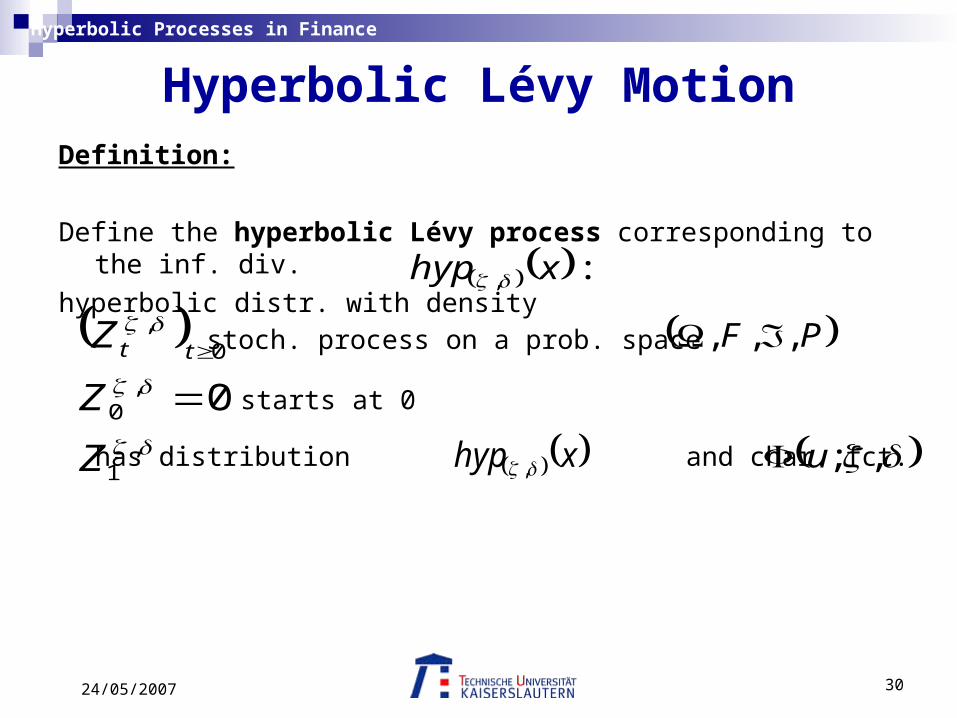

Hyperbolic Lévy MotionDefinition:

Define the hyperbolic Lévy process corresponding to the inf. div.

hyperbolic distr. with density :, xhyp

,1

,0

0,

0

Z

Z

Z tt

stoch. process on a prob. space

starts at 0

has distribution and char. fct.

PF ,,,

xhyp , ,;u

3124/05/2007

Hyperbolic Processes in Finance

Hyperbolic Lévy Motion

For the char. fct. of we get

,tZ

,tZ

ttiuZ uueE t

,;,;,

The density of is given by the Fourier Inversion formula:

duuuxxf tt

,;cos1

0

,

only has hyperbolic distribution ,1Z

0t

3224/05/2007

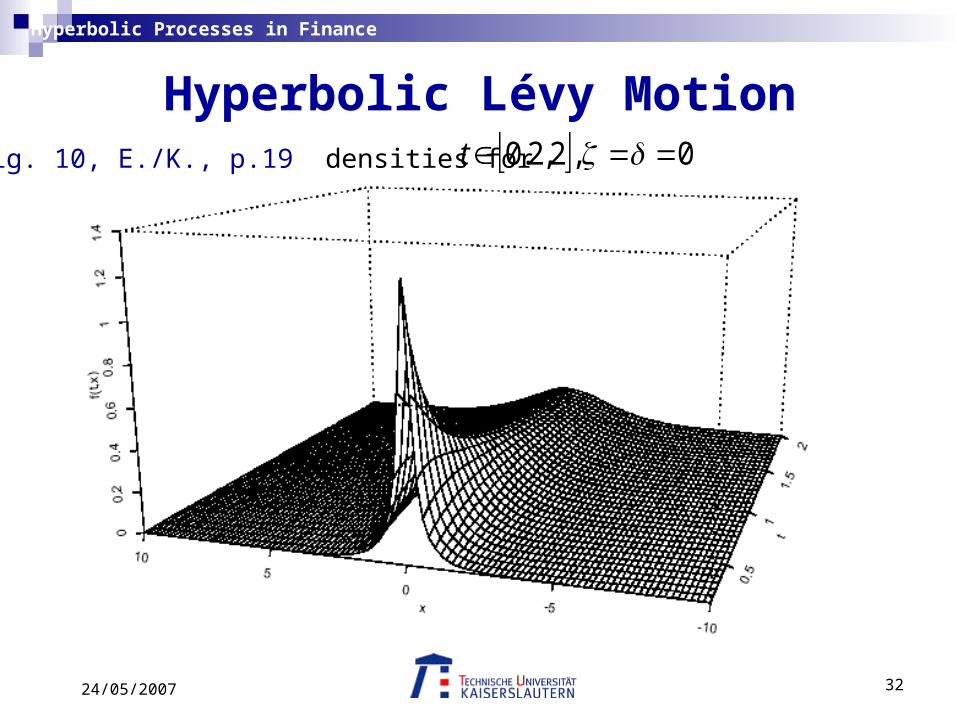

Hyperbolic Processes in Finance

Fig. 10, E./K., p.19 densities for 0,2,2.0 t

Hyperbolic Lévy Motion

3324/05/2007

Hyperbolic Processes in Finance

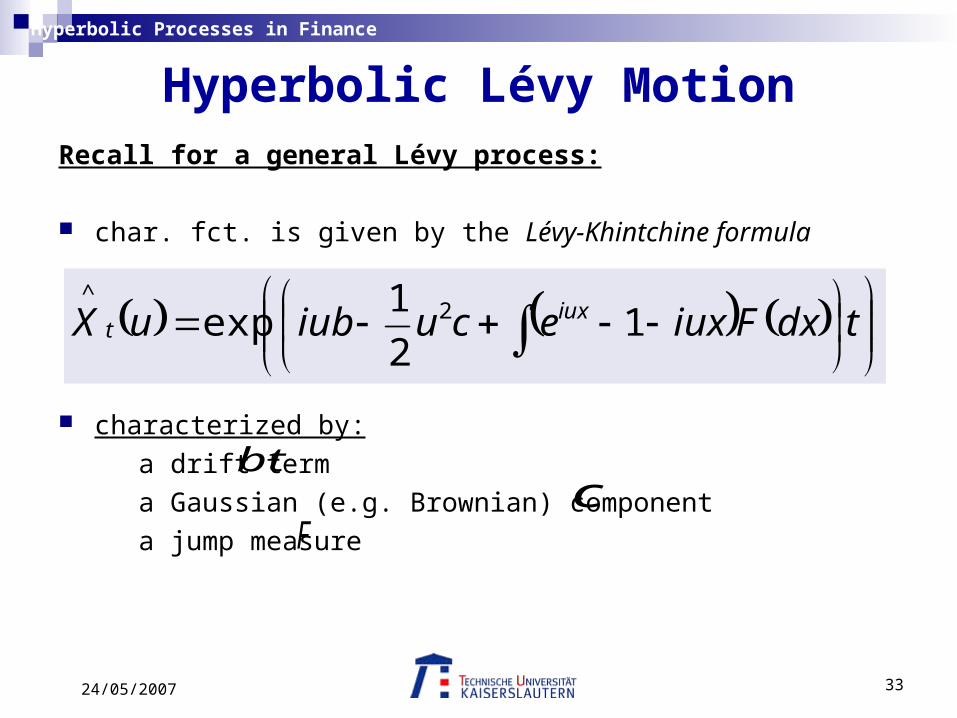

Recall for a general Lévy process:

char. fct. is given by the Lévy-Khintchine formula

characterized by:

a drift term

a Gaussian (e.g. Brownian) component

a jump measure

Hyperbolic Lévy Motion

tdxFiuxecuiubuX iux

t 12

1exp 2

^

btc

F

3424/05/2007

Hyperbolic Processes in Finance

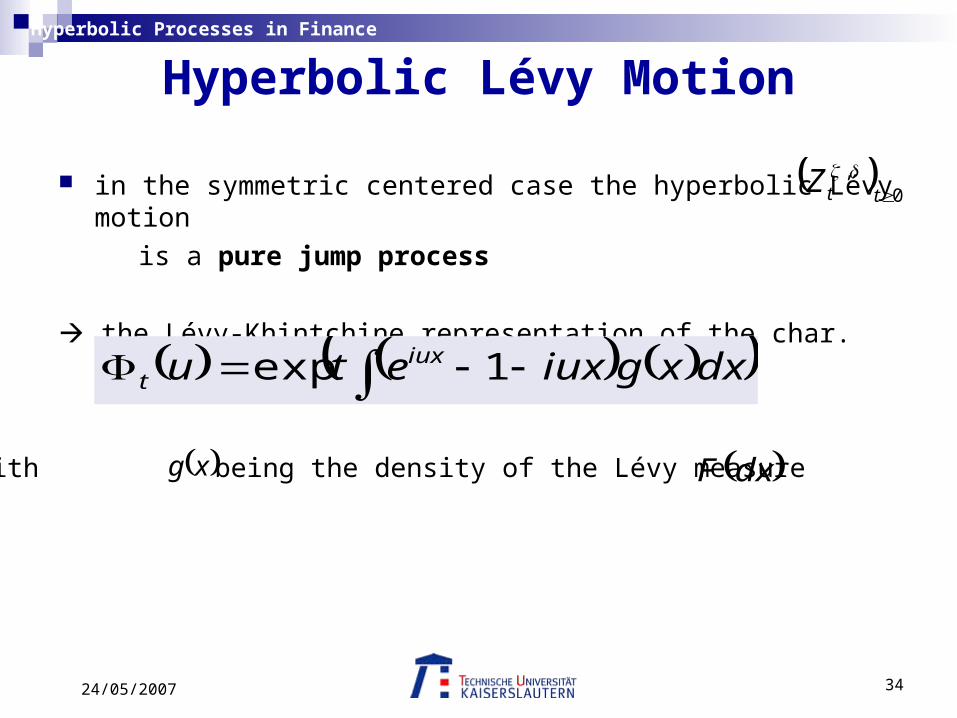

in the symmetric centered case the hyperbolic Lévy motion

is a pure jump process

the Lévy-Khintchine representation of the char. function is

Hyperbolic Lévy Motion

0,

ttZ

dxxgiuxetu iuxt 1exp

xg dxFwith being the density of the Lévy measure

3524/05/2007

Hyperbolic Processes in Finance

Hyperbolic Lévy MotionDensity of the Lévy measure:

1J

x

xdy

yYyJy

yx

xxgxg

exp

22

2exp1

,;0

21

21

2

2

• and are Bessel functions• using the asymptotic relations about Bessel functions, one can deduce that behaves like 1 / at the origin (x 0)

1Y

xg 2x

- Lévy measure is infinite, - hyp. Lévy motion has infinite variation,- every path has infinitely many small jumps in every finite time-interval

3624/05/2007

Hyperbolic Processes in Finance

The infinite Lévy measure is appropriate to model the everyday movement of ordinary quoted stocks under the market pressure of many agents.

The hyperbolic process is a purely discontinuous process but there exists a càdlag modification (again a Lévy process) which is always used.

The sample paths of the process are almost surely

continuous from the right and have limits from the left.

Hyperbolic Lévy Motion

3724/05/2007

Hyperbolic Processes in Finance

Hyperbolic Model of the Financial Market

rtBB

dtBrdB

B

t

ttt

tt

exp0

0

0ttr

0ttY

price process of a risk-free bond

interest rate process

tttt dZYdtbYdY 0ttZ

sZ

tsstt eZtZYY

0

0 1exp

price process of a stock

hyperbolic Lévy motion

3824/05/2007

Hyperbolic Processes in Finance

to pass from prices to returns: take logarithm of the price process

Hyperbolic Model of the Financial Market

sts

s

t

t

ZZ

tZ

Y

0

1log

log

results in two terms:

hyperbolic term

sum-of-jumps term

after approximation to first order the remaining term is

since Lévy measure is infinite and there are infinitely many small jumps, the small jumps predominate in this term; squared, they become even smaller and are negligible

2

tso

sZ

the sum-of-jumps term can be neglected and to a firstapproximation we get hyperbolic returns

3924/05/2007

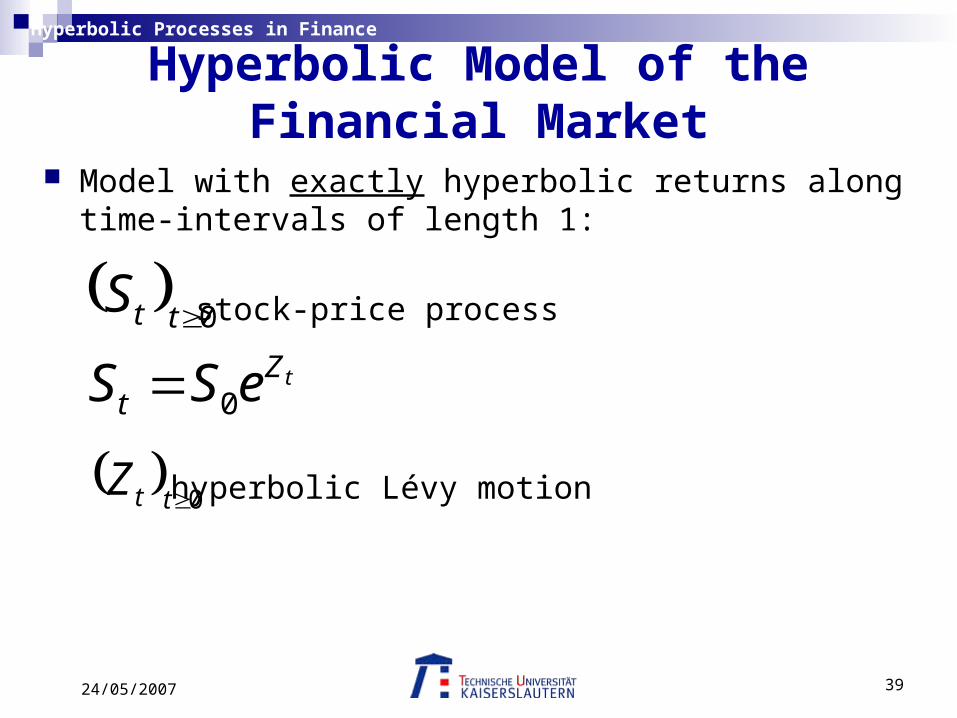

Hyperbolic Processes in Finance

Model with exactly hyperbolic returns along time-intervals of length 1:

Hyperbolic Model of the Financial Market

tZ

t

tt

eSS

S

0

0

stock-price process

0ttZ hyperbolic Lévy motion

4024/05/2007

Hyperbolic Processes in Finance

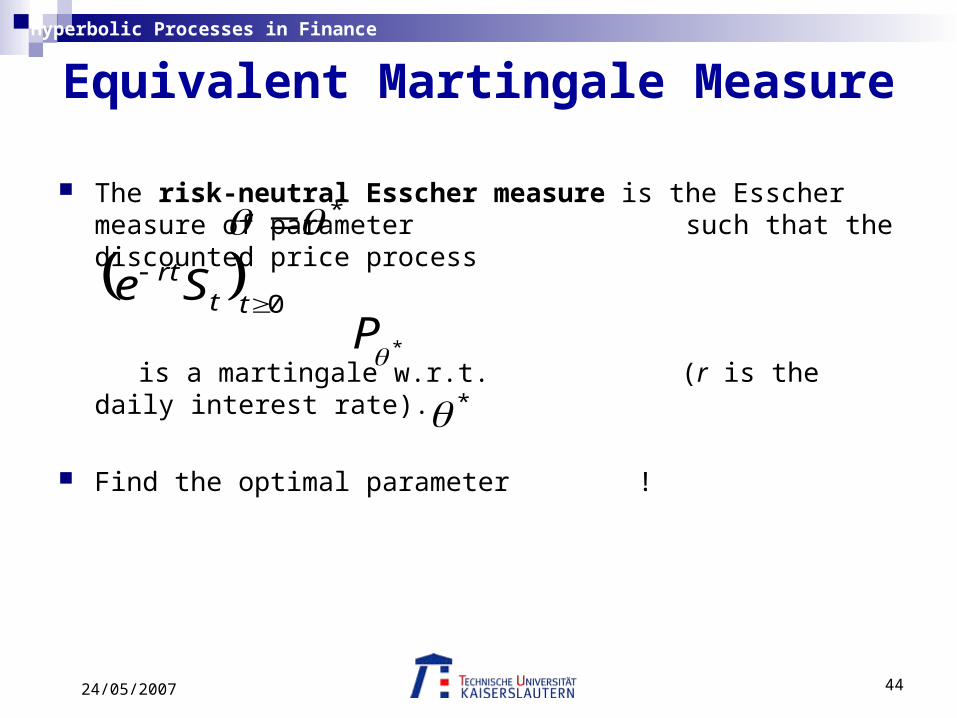

Equivalent Martingale Measure

Definition:

An equivalent martingale measure is a probability measure Q, equivalent to P such that the discounted price process

is a martingale w.r.t. to Q.

Complication in the Hyperbolic model:

financial market is incomplete

no unique equivalent martingale measure (infinite number of e.m.m.) we have to choose an appropriate e.m.m. for pricing purposes

0

0

tt

rt

tt

t SeB

S

4124/05/2007

Hyperbolic Processes in Finance

Two approaches to find a suitable e.m.m.:

1) minimal-martingale measure

2) risk-neutral Esscher measure

In the Hyperbolic model the focus is on the risk-neutral Esscher measure. It is found with the help of Esscher transforms.

Equivalent Martingale Measure

4224/05/2007

Hyperbolic Processes in Finance

Esscher transforms:

The general idea is to define equivalent measures via

Equivalent Martingale Measure

1log

,exp0 0

Z

t t

sssF

eE

dsdZdP

dP

t

choose to satisfy the required martingale conditions

The measure P encapsulates information about market behavior;pricing by Esscher transforms amounts to choosing the e.m.m. which is closest to P in terms of information content.

* s

4324/05/2007

Hyperbolic Processes in Finance

In the hyperbolic model:

Equivalent Martingale Measure

tZt eSS 0

tZeEtM ,moment generating function of the hyperbolic Lévy motion 0ttZ

• The Esscher transforms are defined by

01, ttZ

t MeL t

• The equiv. mart. measures are defined via tF

LdP

dP

t

is called the Esscher measure of parameterP

4424/05/2007

Hyperbolic Processes in Finance

The risk-neutral Esscher measure is the Esscher measure of parameter such that the discounted price process

is a martingale w.r.t. (r is the daily interest rate).

Find the optimal parameter !

Equivalent Martingale Measure

*

0

ttrtSe

*P

*

4524/05/2007

Hyperbolic Processes in Finance

If is the density corresponding to the hyp. process,

define a new density via

Equivalent Martingale Measure

xht 0ttZ

dyyhe

xhexh

ty

tx

t

;

Density corresponding to the distribution of under the Esscher measure

0ttZP

4624/05/2007

Hyperbolic Processes in Finance

To find consider the martingale condition:

(expectation w.r.t. the Esscher measure )

This leads to:

The moment generating function can be computed as

Equivalent Martingale Measure

* 0

!*; SSeE t

rt *

P

reM

M

1,

1,1*

*

u

u

uK

KuM ,1,

222

2221

1

4724/05/2007

Hyperbolic Processes in Finance

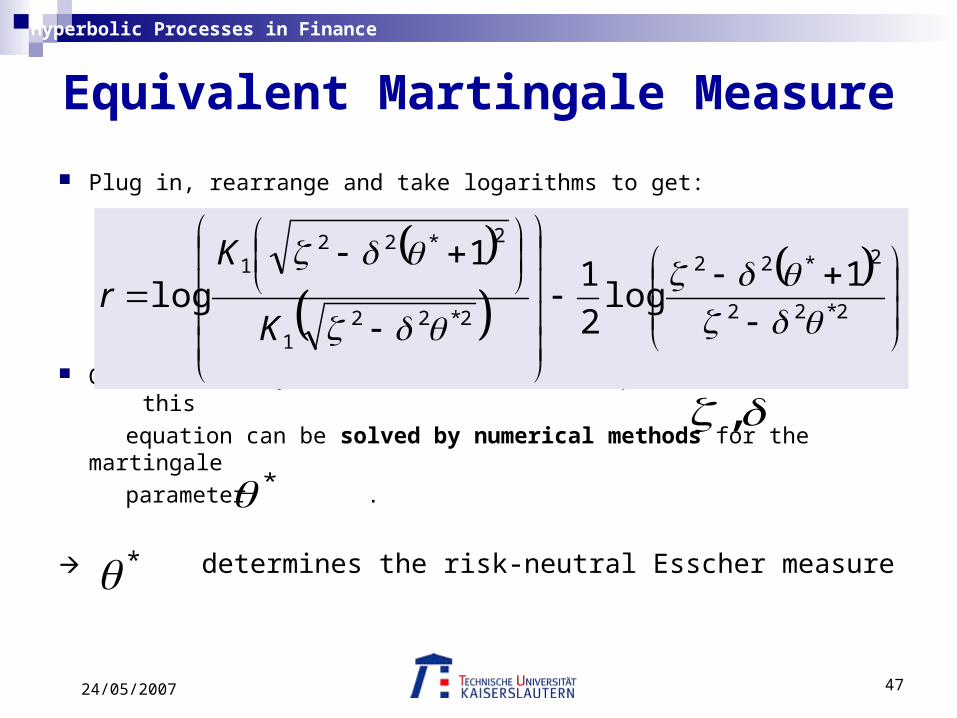

Plug in, rearrange and take logarithms to get:

Given the daily interest rate r and the parameters this

equation can be solved by numerical methods for the martingale

parameter .

determines the risk-neutral Esscher measure

Equivalent Martingale Measure

2*22

2*22

2*221

2*221 1

log2

11

log

K

Kr

,

**

4824/05/2007

Hyperbolic Processes in Finance

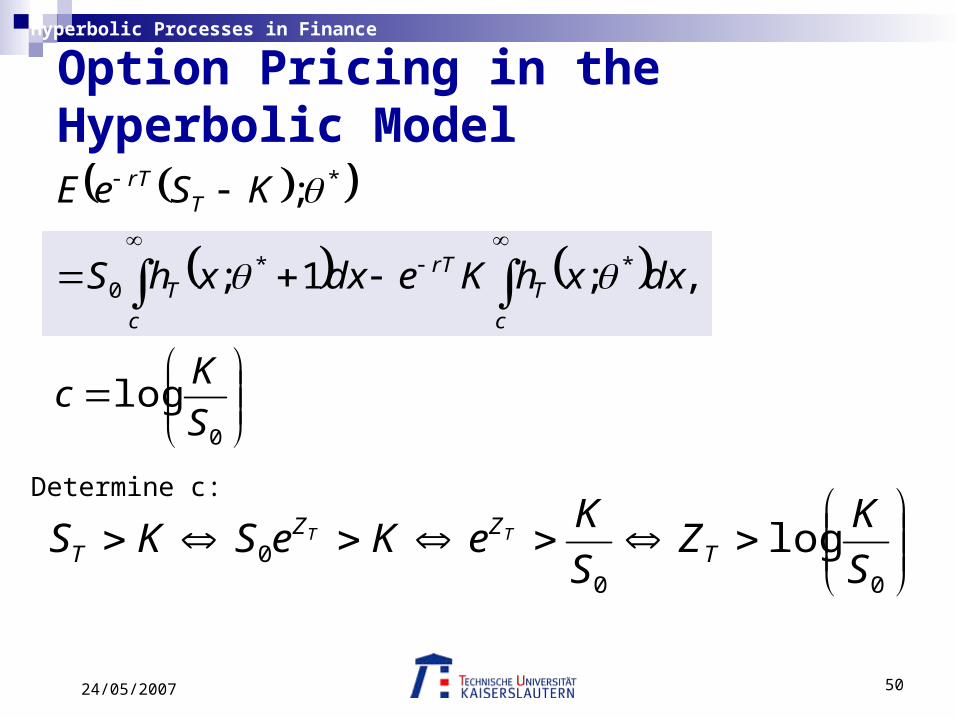

Option Pricing in the Hyperbolic ModelPricing a European call with maturity T and strike K ,

using the risk-neutral Esscher measure:

A usefull tool will be the Factorization formula:

Let g be a measurable function and h, k and t be real numbers, then

hkSgEhSEhSgSE tktt

kt ;;;

4924/05/2007

Hyperbolic Processes in Finance

Option Pricing in the Hyperbolic Model By the risk-neutral valuation principle (using the risk-neutral Esscher

measure) we have to calculate the following expectation:

*; KSeE TrT

**0 ;1; KSKPeKSPS T

rTT

Pricing-Formula for a European callwith strike K and maturity T

010 dS tdKe rT2

5024/05/2007

Hyperbolic Processes in Finance

0

**0

*

log

,;1;

;

S

Kc

dxxhKedxxhS

KSeE

c

TrT

c

T

TrT

Option Pricing in the Hyperbolic Model

000 log

S

KZ

S

KeKeSKS TZZ

TTT

Determine c:

5124/05/2007

Hyperbolic Processes in Finance

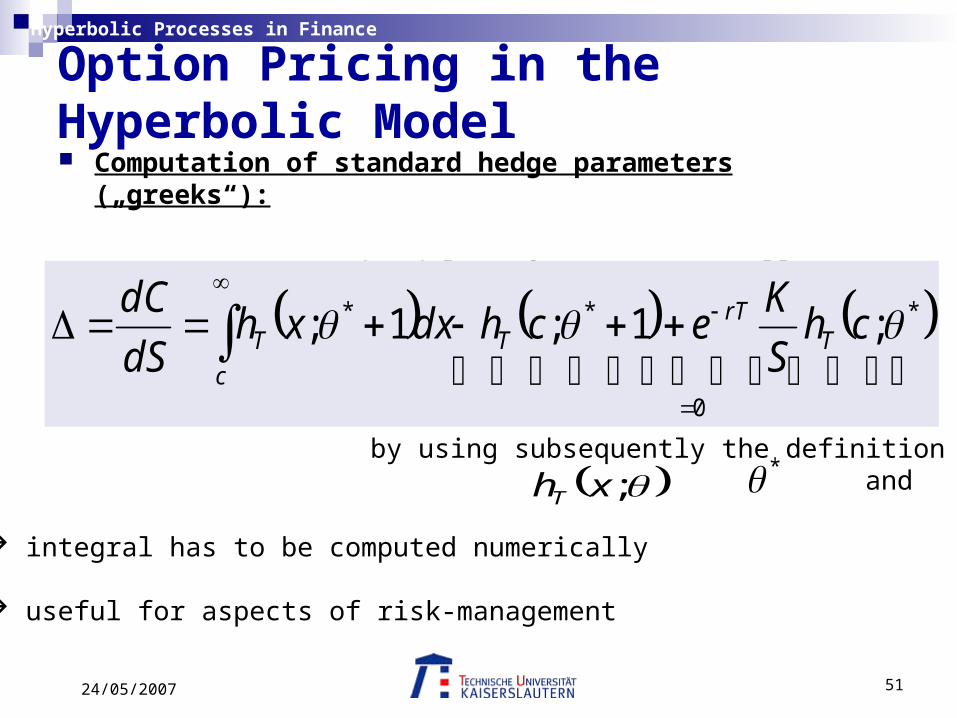

Computation of standard hedge parameters („greeks“):

E.g. compute the delta of a European call C:

Option Pricing in the Hyperbolic Model

0

*** ;1;1;

chS

Kechdxxh

dS

dCT

rTT

c

T

by using subsequently the definition of and ;xhT

* integral has to be computed numerically

useful for aspects of risk-management

5224/05/2007

Hyperbolic Processes in Finance

E./K. performed the same statistical analysis for the hyperbolic model as for the Black-Scholes model (to fit empirical data)

E.g. consider again the QQ-plots and density plots: Fig. 8, E./K., p.16 BASF Fig. 9, E./K., p.17 Deutsche Bank

Fit of the Hyperbolic Model to Empirical Data

5324/05/2007

Hyperbolic Processes in Finance

Fit of the Hyperbolic Model to Empirical Data

5424/05/2007

Hyperbolic Processes in Finance

Fit of the Hyperbolic Model to Empirical Data

5524/05/2007

Hyperbolic Processes in Finance

Fit of the Hyperbolic Model to Empirical Data

5624/05/2007

Hyperbolic Processes in Finance

Fit of the Hyperbolic Model to Empirical Data

5724/05/2007

Hyperbolic Processes in Finance

QQ-plots: almost no deviation from straight line;

assumption of hyperbolic distribution is supported

density plots: hyperbolic distribution provides an almost excellent fit

to the empirical data, esp. at the center and tails

Fit of the Hyperbolic Model to Empirical Data

The hyperbolic distribution fits empirical data better than the normal distribution.

5824/05/2007

Hyperbolic Processes in Finance

B./K. performed a similar study:

- daily BMW returns during Sep 1992 – Jul 1996 (100 data points)

- standard estimates for mean and variance of normal distribution

- computer program to estimate parameters of the hyp. distr.

maximum likelihood estimates:

Fig. 2, B./K., p.14 Density plots

Fit of the Hyperbolic Model to Empirical Data

^^^^

,,,

Comparison of option prices obtained from the Black-Scholes model and the hyperbolic model with real market prices shows, that the hyperbolic model provides a better fit.

5924/05/2007

Hyperbolic Processes in Finance

Fit of the Hyperbolic Model to Empirical Data

6024/05/2007

Hyperbolic Processes in Finance

Conclusion

The hyperbolic distribution provides a good fit for a range of financial data, not only in the tails but throughout the distribution

more accurate model for stock prices / returns

The hyperbolic model should esp. be preferred over the classical Black-Scholes model, when modeling daily stock returns, i.e. when looking at time periods of a single day.

6124/05/2007

Hyperbolic Processes in Finance

For longer time periods the Black-Scholes model is still appropriate:

E./K. estimated the parameters of the hyperbolic distr.

(2nd param.) for the stock returns of Commerzbank, considering

different time periods, i.e. 1, 4, 7, ……., 22 trading days

Conclusion

,

6224/05/2007

Hyperbolic Processes in Finance

Conclusion

^

^

^

the pairs ( , ) are given in the shape triangle and one can see, that the parameters tend to the normal distribution limit as the number of trading days increases

Fig. 7, E./K., p.15

Normal DistributionLimit

6324/05/2007

Hyperbolic Processes in Finance

References Bingham, Kiesel (2001): Modelling asset returns with hyperbolic distributions. In "Return Distributions in Finance", Butterworth- Heinemann, p. 1-20

Eberlein, Keller (1995): Hyperbolic distributions in finance. Bernoulli 1, p. 281-299

Barndorff-Nielsen, Halgreen (1977): Infinite divisibility of the hyperbolic and generalized inverse Gaussian distributions. Wahrscheinlichkeitstheorie und verwandte Gebiete 38, p. 309-311

Hélyette Geman: Pure jump Lévy processes for asset price modelling. Journal of Banking & Finance 26, p. 1297-1316

6424/05/2007

Hyperbolic Processes in Finance

Thank you for participating!