2,127 (june 30, 2014) php - 0 - - a brown company, inc. rosa anna duavit-santiago 02-6386832 contact...

TRANSCRIPT

- 1 -

3 1 1 6 8 SEC Registration Number

A B R O W N C O M P A N Y , I N C .

(Company’s Full Name)

(Business Address: No. Street City/Town/Province)

Atty. Rosa Anna Duavit-Santiago 02-6386832 Contact Person Company Telephone Number

1 2 3 1 1 7 - Q 0 6

Month Day FORM TYPE Month Day Fiscal Year Annual Meeting

Secondary License Type, if applicable

C F D Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings Total No. of Stockholders Domestic Foreign _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

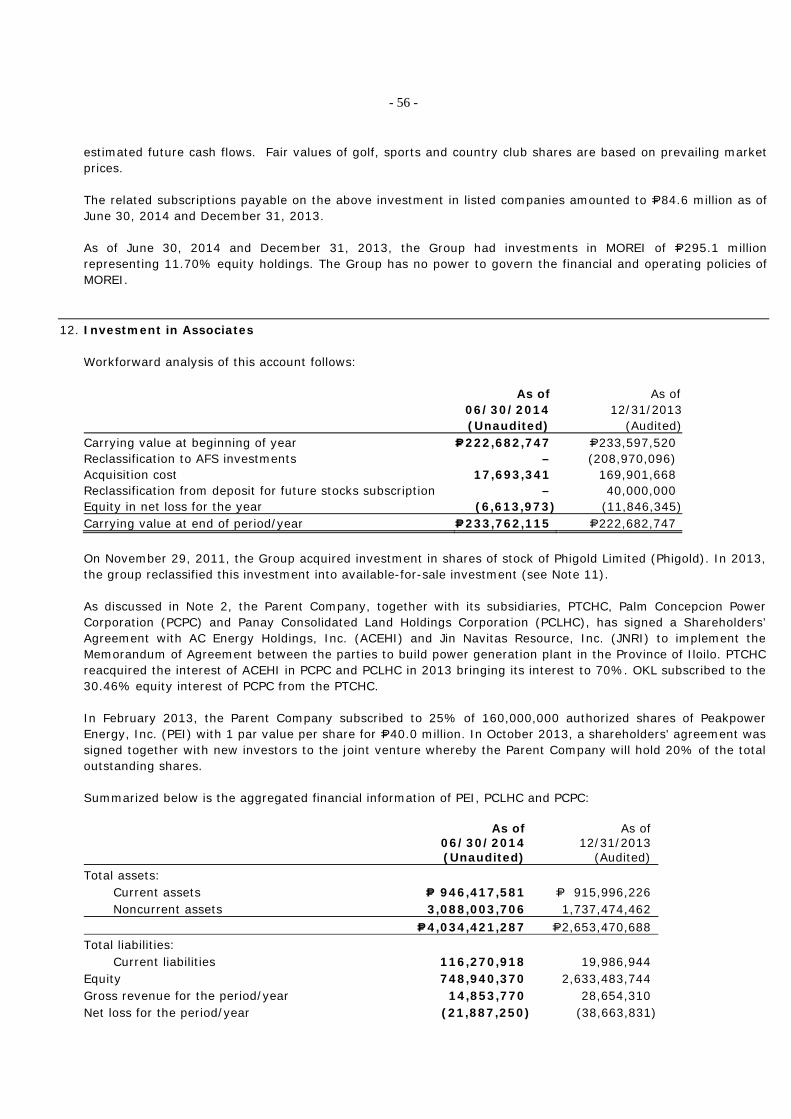

To be accomplished by SEC Personnel concerned

File number LCU Document I.D. Cashier Remarks = pls. use black ink for scanning purposes

A I R P O R T R O A D U P T O W N C A G A Y A N D E O R O C I T Y

STAMPS

2,127 (June 30, 2014) - 0 - Php 2,059,995,224 (June 30, 2014)

- 2 -

SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-Q

QUARTERLY REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SRC RULE 17(2)(b) THEREUNDER

1. For the 2nd quarter ended June 30, 2014 2. Commission Identification Number: 31168 3. BIR Tax identification No. 002-724-446-000 4. A BROWN COMPANY, INCORPORATED 5. Metro Manila, Philippines 6. Industry Classification Code: (SEC use only) 7. Xavier Estates Uptown, Airport Road, Balulang, Cagayan de Oro City 9000 8. Telephone Nos. (088) 858-8784 or (02) 638-6832 9. Former address in last report is: Rm. 3304-C, 33rd Floor West Tower, PSE Centre Ortigas Center, Pasig City (Liaison Office) 10. Securities registered pursuant to Sections 8 and 12 of the Code, or Sections 4 and 8 of

the RSA Title of each class Number of shares outstanding Common shares 1,732,865,522 Amount of debt outstanding: P2,059,995,224.00 11. Are any or all of the securities listed on a Stock Exchange? Yes, all of the common securities are listed in the Philippine Stock Exchange 12.a Yes, we have filed all reports required to be filed by Section 17 of the Code and SRC

Rule 17 thereunder or Sections 11 of the RSA and the RSA Rule 11(a)-1 thereunder, and Sections 26 and 141 of the Corporation Code of the Philippines, during the preceding 12 months (or for such shorter period the registrant was required to file such reports).

12.b Yes, we have been subject to such filing requirements for the past 90 days.

- 3 -

TABLE OF CONTENTS

Page Part I. Financial Information Item 1. Financial Statements

• Unaudited Consolidated Financial Statements Exhibit 1

- Consolidated Statement of Financial Position as of June 30, 2014 and December 31, 2013

- Consolidated Statement of Income for the Three Months Ended and Year-to-Date Ended June 30, 2014 and June 30, 2013

- Consolidated Statement of Comprehensive Income for the Three Months Ended and Year-to-Date Ended June 30, 2014 and June 30, 2013

- Consolidated Statement of Changes in Equity as of June 30, 2014, June 30, 2013 and December 31, 2013

- Consolidated Statement of Cash Flows for the Three Months Ended and Year-to-Date Ended June 30, 2014 and June 30, 2013

- Notes to Financial Statements - Aging of Receivables Exhibit 1-A - Segment Report Exhibit 1-B - Financial Soundness Indicators Exhibit 1-C - ABCI Group Chart Exhibit 1-D

Item 2. Management Discussion and Analysis of Financial Condition

And Results of Operations 4-10 Part II. Other Information Item 3. Performance Indicators 10

Signature 18

- 4 -

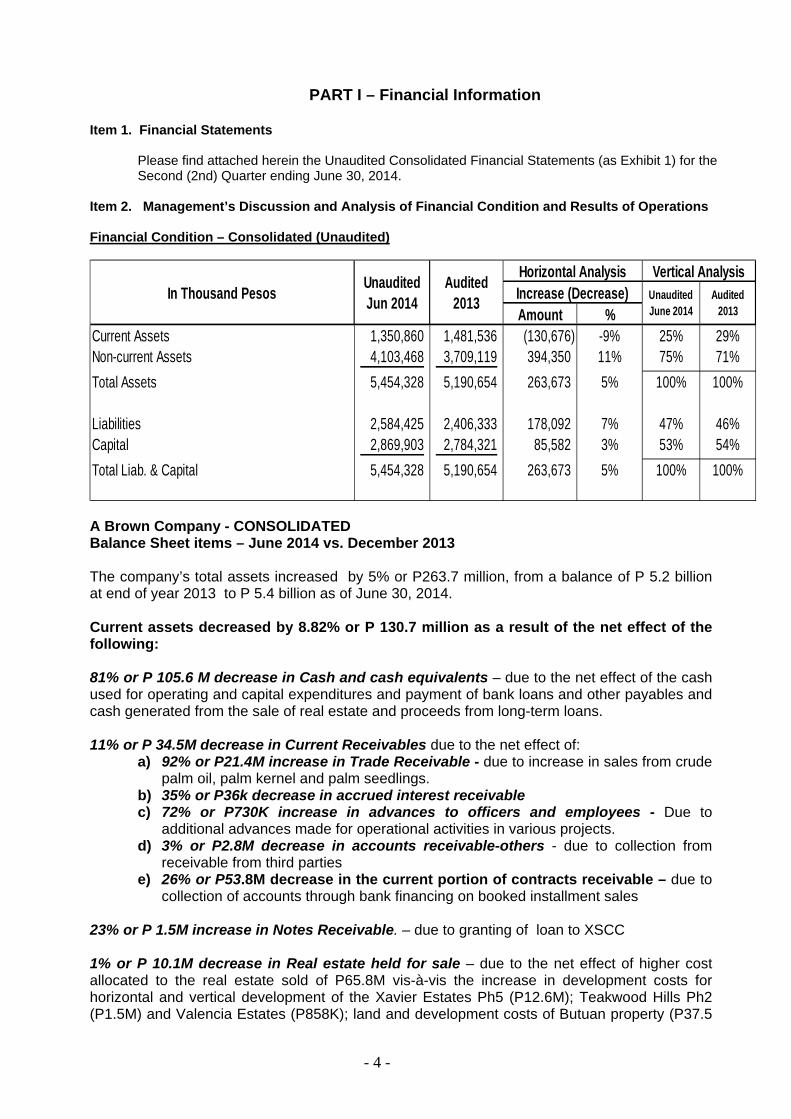

PART I – Financial Information Item 1. Financial Statements Please find attached herein the Unaudited Consolidated Financial Statements (as Exhibit 1) for the

Second (2nd) Quarter ending June 30, 2014. Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations Financial Condition – Consolidated (Unaudited)

A Brown Company - CONSOLIDATED Balance Sheet items – June 2014 vs. December 2013 The company’s total assets increased by 5% or P263.7 million, from a balance of P 5.2 billion at end of year 2013 to P 5.4 billion as of June 30, 2014. Current assets decreased by 8.82% or P 130.7 million as a result of the net effect of the following: 81% or P 105.6 M decrease in Cash and cash equivalents – due to the net effect of the cash used for operating and capital expenditures and payment of bank loans and other payables and cash generated from the sale of real estate and proceeds from long-term loans. 11% or P 34.5M decrease in Current Receivables due to the net effect of:

a) 92% or P21.4M increase in Trade Receivable - due to increase in sales from crude palm oil, palm kernel and palm seedlings.

b) 35% or P36k decrease in accrued interest receivable c) 72% or P730K increase in advances to officers and employees - Due to

additional advances made for operational activities in various projects. d) 3% or P2.8M decrease in accounts receivable-others - due to collection from

receivable from third parties e) 26% or P53.8M decrease in the current portion of contracts receivable – due to

collection of accounts through bank financing on booked installment sales

23% or P 1.5M increase in Notes Receivable. – due to granting of loan to XSCC 1% or P 10.1M decrease in Real estate held for sale – due to the net effect of higher cost allocated to the real estate sold of P65.8M vis-à-vis the increase in development costs for horizontal and vertical development of the Xavier Estates Ph5 (P12.6M); Teakwood Hills Ph2 (P1.5M) and Valencia Estates (P858K); land and development costs of Butuan property (P37.5

Amount %Current Assets 1,350,860 1,481,536 (130,676) -9% 25% 29%Non-current Assets 4,103,468 3,709,119 394,350 11% 75% 71%Total Assets 5,454,328 5,190,654 263,673 5% 100% 100%

Liabilities 2,584,425 2,406,333 178,092 7% 47% 46%Capital 2,869,903 2,784,321 85,582 3% 53% 54%Total Liab. & Capital 5,454,328 5,190,654 263,673 5% 100% 100%

In Thousand Pesos Unaudited Jun 2014

Audited 2013

Horizontal Analysis Vertical AnalysisIncrease (Decrease) Unaudited

June 2014Audited

2013

- 5 -

M); Initao Coral Resort Estates (P19.6M); Mountain View Homes (P4.5M), and reclassification to land and improvements P20.2M 7% or P 18M increase in Prepayments and other current assets – due to the net effect of:

a) 14% or P8.2M increase in creditable withholding taxes; b) 2% or P 2.5M increase for deposit on land acquisition; c) 6% or P2.9M increase in prepaid expenses – due to increase in amortization of

prepaid taxes for the year, and payment of real estate sales commission for unbooked sales.

d) 15% or P4.1M increase in refundable deposit – due to deposit to service contractors. e) 2% or P 230K decrease in inventory - due to increase in sale of crude palm oil –

Inventory decrease (1.5M), and increase in aggregates inventory of P 1.3M. f) 9% or P886K increase in input VAT – related to the additions on construction in

progress in agri-business g) 40% or 366K decrease in other assets due to sale of inventory of crude palm oil

Non-current assets increased by 11% or P 394.5 million as a result of the net effect of the following: 26% or P 53.8M increase in non-current contract receivables due to additional booked installment sales. 9% or P84.2M increase in Available-for-sale investments – due to the increase in market value of investments. 5% or P11.1M increase in Investment in associates – due to the net effect of share in equity in net loss of Panay Consolidated Land Holdings Corp. (PCLHC) =( P 354k ), Palm Concepcion Power Corporation (PCPC) = (P 5.9M) and Peakpower Energy, Inc. = (P 313.7k) and additional investment of P17.4M made by Palm Thermal Consolidated Holdings Corporation (PTCHC) to PCPC. 3% or P8.9M decrease in Investment Properties - net – due to disposal of Nueva Ecija property (P 6.1M), reclassification of Antonia Center from PPE to Investment property and subsequently disposed (P3.4M) and the provision of Depreciation and impairment loss (P 2.8M). 5% or P20.5M increase in Property and Equipment - net – due to the net effect in:

a.) 21% or P3.4M decrease in land – due to reclassification of Antonia center to investment property.

b.) 2% or P1.8M increase in Building and improvements – due to additional materials for chalet construction.

c.) 2% or P 56k increase in leasehold improvements - due to renovation of credit and collection Cagayan office, Compliance office, Accounting Office and HRD Office.

d.) 2% or P 428k increase in furniture, fixtures and equipment – due to purchase of Computer server for C&C office =P160K, various office equipment and furniture for office use=P268K.

e.) 1% or P535k increase in transportation equipment – due net effect on disposal of Toyota Innova (P835K), acquisition of Toyota Fortuner P1.37M.

f.) 5% or P 146K increase in tools and other equipment – due to purchase of laboratory tools for the mill.

g.) 29% or P41.6M increase in construction in progress – as a result of the additional expenditures of the Refined, Bleached, Deodorized (RBD) refinery for the agri-business.

h.) 7% or P2.8M increase in other fixed assets – due to purchase of fuel tank, vacuum pump and 6 set plumber block, submersible pump(P483K), and generator set(P650K).

i.) and 9% or P23.8M Increase in Accumulated depreciation

- 6 -

4% or P 21.3M increase in Land and improvements - due to the net effect in: a) P 1.1M additions to land and improvements b) P 20.2 reclassification of accounts from Real estate held for sale

5% or P15.8M increase in Biological Assets – due to the additional capitalized costs for Opol plantation (P 11.8M), Kalabugao plantation (P3.6M), Tignapoloan (148K) and cassava plantation (P 358K) 2% or P666K decrease in Leasehold rights - due to amortization 28% or P192.5M increase in Investments and deposits – deposits made for future subscription to its affiliates. 8% or P 4.7M increase in deferred tax assets - due to additional tax effect or tax benefits on the available net operating loss carry-over and minimum corporate income 90% or P3.5K increase in other noncurrent asset Current liabilities increased by 14% of P108.4M as a result of the net effect of the following: 30% or P 65M increase in short term debt – due to availment of short term loan from PBCOM. 63% or P70.1M increase current of portion of long term debt due to the increase on the schedule of re-payment/amortization of principal for the next 12 months 10% or P29.5M decrease in accounts payable and accrued expenses – primarily due to the net effect of the following:

a) 10% or P18M decrease in accounts payable b) 18% or P 7M decrease in accrued expenses c) 4% or P 382K Increase in accrued interest payable d) 17% or P1.4M increase in retention payable e) 16% or P6.2M decrease in A/P-others

4% or P2.8M decrease in Deposit from Customers – due to the net effect of the higher amount of booked sales as compared to the increase in sales reservations Non-Current liabilities increased by 4% or P 69.7 million as a result of the net effect of the following: 7% or P103M increase in long-term debt – due to the additional loans availed of P263.7M less repayments of (P88.4M) less current portion of (P70.1M). 100% or P40M decrease deposit for future subscription – due to return of deposits 8% or P6.6M Increase in deferred tax liabilities – due to increase in the deferred income on sale of real estate Equity increased by 3% or P 85.6 million as a result of the net effect of the following: 58% or P84.2M increase in net unrealized gain on available for sale- due to the increase in market value of investments.

- 7 -

Results of Operations – Consolidated (Unaudited)

A Brown Company - CONSOLIDATED Results of Operations For the 2nd Quarter ending June 30, 2014 The consolidated financial statements for the quarter ending June 30, 2014 resulted to a net income after tax of P11.0 million compared to a P2.3 million net loss of last year for the same quarter due to the net effect of the following: 88% or P81.7M increase in Sales on a Quarter (QTR) and 62% or P124.4M on a Year-to-Date (YTD) due to:

a) Increase in real estate Sales by 36% or P27.9M on a QTR and 29% or P47.3M on a YTD – as 52 unitswere booked this quarter against 30 units last year of the same quarter; real estate sales in this quarter also include sale of investment properties amounting to P16.1M; On a YTD, 111 units were booked this year of 2014 against 65 units of last year

b) Increase in sales of crude palm oil by 491% or P49.7M on a QTR and 273% or P73.0M on a YTD - with the increase in quantity sold by 357% or 1,315.34 metric tons, from a volume of 368.27 metric tons for the 2nd quarter of 2013 to 1,683.61 metric tons in 2014 of the same quarter; the average selling price per metric ton increased by P7,349.39 per metric ton from P27,494.72 per metric ton last year to P34,844.11 per metric ton in this 2nd quarter of 2014. This quarter’s sales also include sale of recovered oil amounting to P1.16M for a volume of 126.7 metric tons with an average price of P9,168.68. Sales volume variance is P36,164,905, favorable and sales price variance is P19,107,946, favorable

c) Increase in Sales from palm seedlings and kernel nuts by 141% or P 2.1M on a QTR and 161% or P3.2M on a YTD – Due to the increase in quantity sold of palm kernel by 98% or 111.03MT with a corresponding increase in the average SP of 1,558.66/MT compared to last year’s volume and price for the same quarter. Sales in palm seedlings increased by 151% or 3,870 pcs with selling price of P 220 per piece.

d) Increase in sales from water services by 129% or P1.9M on a QTR and 11% or P0.7M on a YTD – The increase in the quarter’s revenue is due to the net effect of

Amount %Net Sales 174,727 93,031 81,696 88% 49% 37%Financial Income 4,978 9,317 (4,339) -47% 1% 4%Rental Income 2,343 1,885 458 24% 1% 1%Sale of aggregates 5,137 3,677 1,460 40% 1% 1%Other Income 2,340 1,248 1,092 87% 1% 0% Total Revenues 189,525 109,159 80,367 74% 53% 43%Cost of sales and services 103,365 57,315 46,051 80% 29% 23%General and Admin Expenses 47,963 50,031 (2,068) -4% 14% 20%Finance Cost 21,145 17,066 4,079 24% 6% 7%Marketing 9,112 8,025 1,087 14% 3% 3%Equity in net loss (gain) of an associate (6,052) (1,789) (4,263) 238% -2% -1%Provision for Impairment Loss 382 382 - 0% 0% 0% Total Cost and Expenses 175,915 131,030 44,885 34%Income(Loss) before Tax 13,610 (21,871) 35,482 -162%Tax expense(income) 2,606 (19,559) 22,165 -113% 1% -18%Income after Tax 11,004 (2,312) 13,316 -576% 6% -2%Unrealized loss on Available-For-Sale investments 28,168 (14,228) 42,396 -298%Comprehensive Net Income(Loss) 39,172 (16,541) 55,713 -337%

In Thousand PesosUnaudited June 30,

2014

Unaudited June 30,

2013

Horizontal Analysis Vertical AnalysisIncrease (Decrease) June

2014June 2013

- 8 -

the increase average selling price from P28.53 per cubic meter in the 2nd quarter of 2013 to P29.12 in this quarter and increase in the volume of billed water consumption from 106,631 cubic meters in 2013 to 118,631 cubic meters in 2014

e) Decrease in sales from fertilizers by 7% or P2k on a QTR and 15% or P5k on a YTD

47% or P4.3M decrease in financial income on a QTR and 49% or P10.2M on a YTD– due to the decrease in interest from money market placements of 94% or P2.8M and the decrease in interest income of 25% or P 1.5M from in house financing of real estate sale; On a YTD, interest from money market placements decreased by 94% or P7.5M and the interest from in house financing of real estate sale decreased by 22% or P2.8M 40% or P1.5M increase in Sales of aggregates on a QTR and 13% or P0.9M decrease on a YTD– due to the increase in sales volume from 5,776 cubic meter of the second quarter of 2013 to 6,355 cubic meter in the second quarter of 2014 and also due to the increase in selling price to cover the increase in extraction fee; average selling price increased from P635 per cubic meter during the second quarter of 2013 to P786 per cubic meter during the second quarter of 2014; On a YTD, the decrease is attributable to the lower quantity produced in the first quarter of 2014 24% or P0.5M increase in rental income on a QTR and 42% or P1.6M on a YTD - due to rental income from construction equipment 87% or P1.1M increase in other income on a QTR and 61% or P12.6M decrease on a YTD– due to the net effect of the following:

a) decrease in income from penalties and surcharges by 17% or P87k on a QTR and 39% or P552k on a YTD - updated payments from customers and due to the bank financing facility

b) decrease in income from forfeited deposits by 74% or P231k on a QTR and 2179% or P4.2M increase on a YTD – foreclosed accounts in the 2nd quarter of 2014 is lower compared to last year’s forfeited accounts of the same quarter; on a YTD, foreclosed accounts this year is higher as compared to last year

c) increase in other income by 87% or P1.1M on a QTR and 61% or P12.6M decrease on a YTD – due to the increase in income from sale of sludge oil, lot staking fee and driving range fee

80% or P46.1M increase in Cost of Sales on a QTR and 61% or P71.7M on a YTD due to:

a) 25% or P9.9M increase in cost of real estate on a QTR and 24% or P19.6M on a YTD – the increase is relatively due to increase in lots sold.

b) 339% or P34.0M increase in cost of production of crude palm oil on a QTR and 204% or P49.8M on a YTD – the increase is relatively due to the increase in sales of crude palm oil

c) 27% of P0.8M increase in cost of hotel operations on a QTR and 23% or P1.2M on a YTD – due to the increase in fixed costs directly attributable to hotel operations

d) 17% or P0.3M decrease in cost of aggregates on a QTR and 46% or P1.6M on a YTD – the decrease is attributable to the increase in production during the second quarter of 2014 causing the fixed cost per unit to decrease

e) 17% or P0.2M increase in the production of water services on a QTR and 32% or P0.6M on a YTD – due to the increase in the direct operating costs of water services such as labor and electricity

f) 140% or P1.5M increase in the cost of palm seedlings and FFB on a QTR and 160% or P2.2M on a YTD – related to the increase in sales of palm seedlings and kernel nuts.

g) 7% or P1k decrease in cost of fertilizers on a QTR and 15% or P3k on a YTD 4 % or P2.1M decrease in General and Administrative Expenses on a QTR and 5% or P5.2M on a YTD - due to the following net effect of:

- 9 -

a) 0.2% or P51k increase in Personnel expenses on a QTR and 7% or P2.8M decrease on a YTD – the decrease on a YTD is due to the vacant position of an officer and a manager of the parent company

b) 1% or P94k increase in Depreciation and amortization on a QTR and 2% or P0.3M decrease on a YTD – due to the net effect of various additions and the fully depreciated property and equipment items

c) 1% or P33k decrease in Taxes and Licenses on a QTR and 3% or P0.3M on a YTD

d) 9% or P0.2M increase in utilities and supplies on a QTR and 7% or P0.2M on a YTD – due to additional office supplies for the new real estate projects and additional utility expenses incurred due to additional office space occupied by parent company

e) 21% or P0.4M decrease in repairs and maintenance on a QTR and 17% or P0.7M on a YTD - due to various repairs on vehicles and heavy equipment incurred in the 2nd quarter of last year as compared this year

f) 24% or P0.2M increase in rental expense on a QTR and 13% or P0.3M on a YTD– the increase pertains to the additional office space occupied by the parent company

g) 181% or P0.2M increase in Representation and Entertainment on a QTR and 5% or P21k on a YTD – higher cost of providing comfort/convenience (e.g. meals) to the prospective clients

h) 7% or P0.25M increase in security services on a QTR and 15% or P1.0M on a YTD - due to the increase in number of security personnel assigned to real estate (Butuan, Initao and Mountain Pines projects).

i) 27% or P0.63M increase in professional fees/retainers fee on a QTR and P4% or P0.2M on a YTD – due to the various consultancy services incurred by the group this year

j) 18% or P0.4M decrease in travel and transportation on a QTR and 15% or P0.6M on a YTD – due to the various site visitation for mill and plantation operations and power group operations during the 2ndt quarter of last year

k) 49% or P0.46M decrease in directors fees on a QTR and 42% or P0.5M on a YTD – directors fee of the 2nd quarter of 2013 includes bonus

l) 207% or P 0.1M increase in training and seminars on a QTR and 90% or P0.1M on a YTD – due to the minimal trainings and seminars conducted and attended last 2nd quarter of 2013 as compared to this year

m) 49% or P0.1M decrease in subscription and dues on a QTR and 21% or P0.1M on a YTD - there were lesser subscriptions of business magazines in the 2nd quarter of 2014 as compared to 2nd quarter of 2013

n) 51% or P27k decrease in notarization on a QTR and 53% or P60k on YTD - due to various contracts, deed of sale and waiver of rights notarized in the 2nd quarter of 2013

o) 74% or P71k decrease in litigation expenses on a QTR and 4% or P4k on a YTD – litigation expenses in the 2nd quarter of 2013 include legal fees for Yulo case

p) 125% or P56k increase in unrealized foreign exchange gain (loss) on a QTR and 11% on a YTD – due to changes in dollar exchange rates

q) 88% or P11k decrease in bank charges on a QTR and 90% or P27k on a YTD - due to payment of REM annotation for UBP loan during the 2nd quarter of 2013

r) 125% or P0.4M decrease in board meeting expenses on a QTR and 46% or P0.3M on a YTD – due to the various materials and other expenses incurred related to board meetings and annual reports in the 2nd quarter of 2013

s) 58% or P1.9M decrease in miscellaneous expenses on a QTR and 28% or P1.4M on a YTD – include community relations expenses such as scholar’s tuition and other humanitarian assistance; in the 2nd quarter of 2013, the Group incurred expenses during the conduct of medical mission

24% or P 4.1M increase in Finance costs on a QTR and 23% or P7.7M on a YTD - due to additional availment of loans

- 10 -

14% or P1.1M increase in Marketing expenses on a QTR and 12% or P1.9M on a YTD – due to the increase in commission expenses in relation to the increase in booked sales and increase in various sponsorships of events for ads and promotions 238% or P4.3M increase in Equity in net gain of associates on a QTR and 449% or P5.4M increase of Equity in net loss on a YTD – due to the deconsolidation of PCPC and PCLHC which the group has a share of P6.1M gain in the 2nd quarter of 2014 and P1.8M gain in the 2nd quarter of 2014 (see Note 12); On a YTD, the Group has a share of P6.6 loss in 2014 and P1.2 loss in 2013 Top Key Performance Indicators (Consolidated Figures)

The table below sets forth the comparative performance indicators of the Company and its majority-owned subsidiaries:

Financial Ratios Unaudited Unaudited Audited

Consolidated Figures 6/30/2014 6/30/2013 12/31/2013 Current ratio1 1.54:1 3.81:1 1.92:1 Current Debt to Equity ratio2 0.31:1 0.27:1 0.28:1 Total Debt to Equity ratio3 0.90:1 0.96:1 0.86:1 Return on Assets4 0.03% 0.04% 0.07% Return on Equity5 0.05% 0.07% 0.13%

1Current assets/Current liabilities 2Current liabilities/Stockholders’ equity 3Total liabilities/Stockholders’ equity 4Net income/Average total assets 5Net income/Average total equity Real Property Development:

Xavier Estates: The percentage of completion of Xavier Estates Phase 5- Ventura Residences is 84% as of June 30, 2014. This project has a saleable area of 5.8124 hectares. The units are classified according to house designs of which 84 units are 100% complete while the remaining 35 units are still under construction. For the 2nd quarter 2014, there were nine (9) lots sold in Xavier Estates compared to 10 lots for the same quarter last year. For Ventura Residences, there were three (3) house and lot packages recorded as sold in this quarter of the year while 10 house and lots for the 2nd quarter 2013.

Xavierville Homes: Phase 1 and 2 were 100% complete. Necessary retouching of existing and

completed units is being done for its housing component. Three (3) house and lot packages were sold in the 2nd quarter while only one (1) unit for the same quarter last year.

Teakwood Hills: As of the end of the period, horizontal development has three (3) phases

including the alteration. One phase of the project with 5.27 hectares of developmental area is 100% complete which was subdivided into 59 saleable lots. Another phase of the project with 40 hectares of developmental area is expected to generate 795 saleable lots. An alteration of the 40-hectare phase will add another 266 saleable lots from the additional 13.34 hectares of developmental area. The 40-hectare phase and its alteration are currently at 81% percentage-of-completion. For this year’s 2nd quarter, seven (7) units were sold compared to eight (8) lots for the same quarter last year.

St. Therese Subdivision: The subdivision is a 1.6720-hectare socialized housing project located

in mid- Balulang, Cagayan de Oro that will provide 155 lots of which 91 lots are row houses, 39 units are duplex, 16 single attached units. The remaining nine (9) units are corner lots which have been allotted for a new design. There were six (6) units sold for this year’s 2nd quarter.

Valencia Estates: The horizontal works is 100% done. The main gate, the multi-purpose hall and swimming pool were completed in 2012. Only one (1) lot was sold for the second quarter.

Coral Resort Estates: The project previously disclosed as Coral Pebbles Resort & Residences is located in Initao, Misamis Oriental with a total development area of 5.397 hectares. As of the end of the 2nd quarter, Phase 1-Cluster A of the project with a development area of 2.5361 hectares has been 97%

- 11 -

completed. Phase 1-Cluster B is currently at 55% percentage-of-completion. There were seven (7) lots that were sold for the second quarter.

West Highlands is a golf and residential estate located in Brgy. Bonbon, Butuan City. The estate

has a total developmental area of 25.9 hectares and is 289 feet above sea level which gives lot owners a panoramic view of historic Mt. Mayapay or the cityscape. The first cluster covers 4.4 hectares with 155 saleable lots. The second cluster covers 4.9 hectares with 91 saleable lots. The project’s Phase 1 percentage-of-completion is 79%. The spillway, concrete barrier, riprap and driving range are 100% done while the spine road is 95% complete as of the end of the period. There were 14 lots sold for this quarter as compared to the one (1) lot sold for the same quarter last year.

ABCI is engaged in quarrying and mining of basalt rocks for the production of construction aggregates of four different sizes as follow: 1 1/2" gravel, 3/4" gravel 3/8" gravel and crushed sand. The quarry site which is rocky in nature is located in Sitio Balaon, San Isidro, Talakag, Bukidnon. A total of 9,160 and 5,198 cubic meters of aggregates were produced for the three months ending June 30, 2014 and June 30, 2013, respectively. Oil Palm Plantation: As of June 30, 2014 (Both for ABERDI and Nakeen Corp.) For the Quarter Ending June 30, 2014

Location Plantation Area in Hectares Yields Gross Area Plantable Area Planted Area Bunches

Impasug-ong 4.140 4.140 4.140 1,105 Opol 1,089.855 630.77 623.26 53,947 (Access Road) (60.03) Kalabugao 1,276.53 1,087.75 920.55 (Uprooted) (55.00) Phase I 256.23 27,302 Phase II 262.92 24,763 Phase III 145.31 6,622 Phase IV 177.78 1,185 Phase V 78.32 - Tignapoloan 1,328.56 929.96 - - XE plantation 43.74 43.74 43.74 6,776 Total 3,742.825 2,696.362 1,591.69 121,700

As of June 30, 2013 (Both for ABERDI and Nakeen Corp.) For the Quarter Ending June 30, 2013 Location Plantation Area in Hectares Yields

Gross Area Plantable Area Planted Area Bunches Impasug-ong 4.140 4.140 4.140 1,525 Opol 1,089.855 630.770 623.160 4,801 Kalabugao 1,276.530 1,087.749 975.55 Phase I 256.23 30,562 Phase II 262.92 24,996 Phase III 200.30 17,323 Phase IV 177.78 424 Phase V 78.32 - Tignapoloan 1,328.56 929.960 - - XE plantation 43.74 43.74 43.74 6,881 Total 3,742.825 2,696.362 1,646.600 86,512

- 12 -

The following are the status of the four plantation areas as June 30, 2014:

Location Fruiting/Flowering Vegetative Impasug-ong 100% - Opol Phase Ia 54% 46% Phase Ib 30% 70% Phase IIa 40% 60% Phase IIb 100% Phase IIIa 100% Phase IVa 100% Phase Va 100% Kalabugao Phase Ia 100% - Phase Ib 70% 30% Phase IIa 100% - Phase IIb 70% 30% Phase IIIa 100% - Phase IIIb 40% 60% Phase IIIc - 100% Phase IVa 20% 80% Phase IVb - 100% XE plantation Phase I 100% Phase II 100%

Nursery Operation:

The oil palm seeds are sourced from Thailand. As of end of June 30, 2014, a total of 5,598 seedlings are available for planting covering an equivalent 41.16 hectares. Palm Oil Mill

A total of 8,921 metric tons of fresh fruit bunches derived from internal and external sources were processed and produced for the second quarter of 2014, compared to 1,927 metric tons in second quarter of 2013. This average of 2,973.62 metric tons of fresh fruit bunch per month for the three months of the second quarter of the year resulted to 1,768.38 metric tons of crude palm oil at an average oil extraction rate of 19.82% as compared to 641.97 metric tons of crude palm oil with a 20.00% oil extraction rate in same period last year. The kernels that were produced for this quarter totalled 203.37 metric tons as compared to 54.42 metric tons of last year’s second quarter. About 107.11 metric tons of effluent sludge oil was also produced for this quarter. In addition, sales generated from crude palm oil were from 1,683.61 metric tons for the quarter. There were also 224.48 metric tons of kernels and 126.70 metric tons of sludge oil sold for the quarter.

Power Generation – Coal-Fired Power Project

Palm Concepcion Power Corporation (PCPC) whose outstanding capital stock has been acquired by Palm Thermal Consolidated Holdings Corp. (PTCHC) in 2010 – is the project company that will construct and operate a 135-megawatt coal-fired power plant in Concepcion, Iloilo. This project will be a base-load plant and will make use of Circulating Fluidized Bed Combustion (CFBC) technology.

While only 135-megawatt is on a firm basis, the plant site and support units are programmed for two (2) units. The preparation for the second unit is projected to begin two to three (2 to 3) years after commissioning of the first unit if the power market in the region continues to expand as projected.

PCPC signed an agreement to tap the services of SNC - Lavalin, Inc., a global leader in the field of Engineering, Construction and Operations, as its Owner’s Engineer of the project in the early second quarter of 2012. SNC-Lavalin is providing technical advisory from the engineering stage up to the completion of the power project. Its services cover detailed engineering that will include review and evaluation of Engineering Procurement and Construction (EPC) specifications, system’s design parameters and operating features and development of conceptual layouts, among others. In early October 2012, PCPC signed a Connection Agreement with the National Grid Corporation of the Philippines (NGCP). This connection agreement paves the way and ensures dispatch of PCPC’s generation output to its customers via the facilities of system operator NGCP.

ABCI together with its subsidiaries, by then: PTCHC, PCPC and Panay Consolidated Land Holdings Corporation (PCLHC) signed a Memorandum of Agreement with AC Energy Holdings, Inc. (ACEHI) last September 2012. Towards the end of October 2012, PTCHC together with other principal stockholders of PCPC namely: ACEHI and Jin Navitas Resource, Inc. (JNRI) finalized and executed their

- 13 -

Shareholders’ Agreement to document and implement the PCPC shareholders’ respective agreements and undertakings, including the constitution of PCPC as the Project Company as well as to confirm the terms and conditions by which PCPC will be owned, managed and controlled, and by which PCPC shall implement the development and operation of its power generation project.

To implement the Shareholders Agreement, ABCI transferred all of its equity interest in PCLHC to its other wholly-owned subsidiary, PTCHC. With this, PCLHC ceased to be a direct subsidiary of ABCI. At the same time, ACEHI, JNRI and PTCHC subscribed to the remaining Nine Million shares (9 M shares) of PCLHC. As a result of these new subscriptions, PCLHC mirrored the same equity structure as that of PCPC, i.e. 30% PTCHC, 30% JNRI and 40% ACEHI as of end of 2012.

Last January 15, 2013, PCPC had its official ground breaking ceremony to launch the project. NLSC- the consortium of First Northeast Electric Power Engineering Corp. of China (NEPC), Liaoning Electric Power Survey & Design Institute and Shenyang Electric Power Design Institute Co., Ltd.- is the project’s general engineering, procurement and construction (EPC) contractor. Alstom Power of Europe, one of the world’s foremost suppliers of steam turbines and power generation equipment, will provide the steam turbine and generator for this project. SNC-Lavalin is also tapped as the Project Construction Manager.

However, as a result of ACEHI’s strategic decision to focus on its other existing power imminent in its development pipeline, PTCHC and ACEHI agreed the acquisition by PTCHC of ACEHI’s 40% interest in the 135-megawatt coal-fired power plant project in Iloilo on May 2013.

The financial closing was completed last July 2013 when lending banks: China Banking Corporation (Php 3.5B); Asian United Bank (Php 2.5B) and BDO Unibank, Inc. (Php 4B) signed the term loan financing totaling Php 10B to partially finance the Engineering, Procurement and Construction (EPC) and finance costs of the project. BDO Capital & Investment Corporation acted as the Lead Arranger and Sole Bookrunner for the term loan facilities.

Outlook for the Year and Onwards Real Estate Business: The Philippine real estate sector players believe that the industry is definitely bullish about prospects at least in a medium term, barring any major crisis. This outlook is based on the recent developments and urgent issues which the industry associations are advocating to be resolved and with the support of the policy-makers and lawmakers in charge on housing and urban development in helping the sector achieve its full potential as drivers of economic growth. A Department of Housing, better fiscal incentives and closer public-private partnership are all included in their work program.

Adding to these initiatives is the pronouncements by the business process outsourcing (BPO) sector about better business for this and incoming years which will mean more office spaces and employment are needed for its expansion. Though the country is considered as the most attractive BPO destination next to India, it has overtaken the leader in the number of new hires and in the revenue of call centers. In December 2010, the new hires in the Philippines since the start of the year totaled 15,000 as compared to the 13,800 hires of India. The Philippine revenues were placed at $ 5.5 billion against India’s $5.3 billion. Based on the IT-BPO Road Map 2011-2016 developed jointly by Everest Group and Outsource2Philippine in cooperation with the Business Processing Association of the Philippines, IT-BPO industry revenues are projected to reached $20 billion and jobs to 900,000 in five years, from the current $9 billion and the 500,000 jobs. (http://www.malaya.com.ph/12082010/busi2.html). Tourism, another booming sector also poses huge potentials considering the requirements for hotels, resorts, restaurants and related developments.

From the estimated 3.75 million units of housing need (defined as backlog plus new households) by 2010 according to the Medium-Term Philippine Development Plan (MTPDP 2004-2010), the housing gap has already reached 5.8 million units or about 800,000 units per year as embodied in the MTPDP 2011-2016 edition. This data has triggered for the mass and socialized housing to be listed by the Department of Trade and Industry as a priority industry. This housing backlog will offer an opportunity for real estate developers or dealers to be innovative and creative in filling this gap.

In support to narrow the ever increasing gap of housing need, the Housing and Urban Development Coordinating Council (HUDCC) - the highest policy making and coordination body on housing and urban development, announced that it has increased the target housing loans from 75,000 to 150,000 housing units setting aside P30 billion in new loanable funds for both buyers and developers. This is in line with the government’s thrust of facilitating access to a variety of housing options that are decent, affordable and responsive by providing incentives to low-cost mass housing developers. Investing on mass and socialized housing will enable the investors to enjoy certain incentives. Mass housing as defined by the Board of Investment (BOI) as those units sold at P400,000 up to P 3 million while the socialized housing covers units sold at less than P400,000 will provide ardor to developers to avail of income tax holidays while sourcing out financing needs from real estate finance providers at affordable interest rate. (Real Estate World, 1st Quarter 2011)

- 14 -

A considerable cause of this increasing backlog is population growth. It was reported that with the population growing at an annual rate of 2.32 percent, demand for shelter is also expected to increase. Given this, government policy makers are bent on providing more shelter assistance and pursuing strategies to encourage more private sector participation in housing production. In fact, “jumpstarting” the housing construction sector can spur economic growth and alleviate poverty by taking advantage of its multiplier effect. Housing has a high multiplier effect of 16.6 times, meaning that every 10 billion worth of housing units, it can contribute a total of Php 166 billion of economic activity for the country (MTDP 2004-2010).Thus, this positive ripple impact on the sub-sectors and allied industries that the housing provides is an evidence of the sector’s important role acting as driver of economic growth.

The issuance of the BIR Revenue Regulation No.16-2011 dated October 27, 2011 which was effective starting January 1, 2012 eliminated the burden of those prospective clients who will acquire residential property to pay the value added tax (VAT) of 12% for the gross selling price not exceeding Php 1,919,500.00 for the sale of residential lot and the gross selling price not exceeding Php 3,199,200.00 for the sale of residential house and lot. The Bureau responded the call to ease the imposition of VAT in consideration of the inflation for the last six years from the time of the passage of Republic Act 9337.

While pursuing new projects, the Company will continue to roll-out new phases in its existing project called Xavier Estates. It will expand its product offerings to build up its portfolio across a wider market. This will be complemented by intensified sales and marketing efforts to broaden market reach and tap the growing market of overseas-based Filipinos.

The management is also optimistic that sales will increase in 2014 due to steady global demand for Filipino labor. There is also an increasing demand from local professionals investing in affordable housing projects especially with the support from the local banks and PAG-IBIG for more affordable housing loan rates.

ABCI will complete the development of the property in Initao, Misamis Oriental (Coral Resort Estates) and in Butuan City (West Highlands). ABCI will venture on socialized and economic housing projects tapping the facility of PAG-IBIG as well as the banks through end-buyers’ financing.

The volume of aggregates derived from boulders is believed also to increase. Palm Oil Business:

The palm oil industry is a promising enterprise as the palm oil continuously being considered as the most important tropical vegetable oil in the global oils and fats industry, in terms of production and trade. It accounts for about 31%, ahead of soybean oil with 28% and rapeseed oil with 19%. Aside from its many food and non-food applications, it has been promoted as a feedstock for the production of biofuels in response to the depletion of world’s reserve on fossil fuels and skyrocketing price of oil in the world market. The significant growth of palm oil production, consumption and market share is also to a large extent due to its cost competitiveness and its inherent crop productivity yielding from 3.80 to 5 tons per hectare with minimum land utilization which is 9.3, 7.6 and 5.8 times higher than soybean oil, rapeseed oil and sunflower oil, respectively (Oil World 2008). Thus, it has been viewed as the cheapest, versatile and most productive oil among the three vegetable oils.

As the growing population would keep consuming more oil palm products processed to products of higher value-added, increase in oil palm production is to be expected. Domestic demand for palm oil is seen five percent annually from 1995 to 2015 according to the study by the University of Asia and the Pacific (http://ppdci.org/?p=20). Since oil palm thrives in tropical countries where agro-climactic conditions favor its growth, the Philippines has been suitable for its production with its neighboring countries, Indonesia and Malaysia as the leaders. The Philippines has 7.4 million hectares of idle land (Yosuf and Yew, 2009). In 1994, the Palm Oil Research Institute of Malaysia identified at least 300,000 hectares in eight provinces in Mindanao suitable for oil palm plantation. The Philippine Coconut Authority (PCA) and the Southern Philippines Development Authority (SPDA) have also identified some 447,000 hectares of potential areas in Mindanao and Visayas region suitable for oil palm planting. Based on the report presented during the mini-workshop on Oil Palm Planning conducted in June 2008, the Philippines has developed at least a total of more than 46,000 hectares of land for oil palm with only some 20,000 hectares of oil palm trees in year 2000. Caraga region registers as the largest area of more than 17,000 hectares or 37% of total oil palm area in the country. Major players include Filipinas Palm Oil Plantations, Inc., Agusan Plantations Inc. and Kenram Philippines Inc.

From 2003 to 2009, the area planted to oil palm increased from about 25,227 hectares to 46,608 hectares, an increase of about 85% within a 7-year period or about 14% per year. Growing at an average of 82,500 metric tons in 2000, it is projected to reach 171,700 metric tons in 2015. Along with this data, the palm oil industry players need to expand the current plantations and out grower farms to grow more by 38,934 hectares by 2015.

In 2008, although the crude palm oil production exceeded 50,000 metric tons, it was not enough to meet the local demand. Hence, the country imported about 300,000 metric tons. This volume of crude

palm oil icope withThe demmillion toconsumpin 2011 to

A

neglect inmean thaCouncil (shall forf60,000 wmember the goveplantationPhilippinedomestic Inhectares comparedUS$ 400 P27.26 b

G

there willthe lack oplantation2nd quartalmost 1,The comexpansioNakeen Cand share

AWe startetons per additionametric toStearin w Power G Inserious iobjectiveselectric ponce agaexpansiothe explo

mport translah the domestand for palmns in 2012 i

ption of vegeto 9 billion by

According to n supporting at by 2022 thMPOC), estifeit in favor would-be oil countries of

ernment of Mns resulting e governmen demands, nn the PPDCof potential

d to 625,000million whileillion in 2022

Given the cur be disparityof adequate n in Kalabugter of 2014, ,592 hectarepany is anticn program aCorp. appliedeholders.

ABERDI will ed the groun

day. Assumal purchase ons of RBD

will be produc

Generation:

n support on addressins of the ene

power and eain, governmn in investm

oration, devel

ates to an imtic demand.

m oil is expecn considerattable oil. Bas

y 2043, an inc

Source: P

Philippine Pthe palm oil

he country smated to be of the Malapalm farmethe ASEAN

Malaysia, Into significa

nt neglectednow at P6.68CI report in th

area for pl0 hectares ine the Philippi2. (http://ppdc

rrent domesty between plocal producao, Impasugabout 3,743

es were plancipating the aggregating d for an Am

soon introdund works for ming the paof CPO from oil. After fra

ced monthly.

of attracting g the count

ergy sector aexpand rural ment should

ment. It is vitalopment, utili

mmediate req(http://ppdci

cted to increation with the sed on the screase of 29

PPDCI; Thoma

Palmoil Deveindustry to e

hall import, b576,596 MTysians (thrors and direclocated withdonesia andnt reduction

d the palm o billion annuhe recent paanting palm

n Thailand. Tnes importedci.org/wp-con

tic demand aroduction anction, the mag-ong, Bukidn3 (gross areated while absigning of ato 3,000 heended Articl

uce to the mthe RBD reflm oil mill ooutside sou

actionation, 7The Refiner

more investry’s energy are to raise e

electrificatiod ensure thal to harmonization and c

- 15 -

quirement of i.org/wp-contase by 25.7 mprojected w

statistics, wo%.(PPDCI; B

as M. (POTS K

elopment Couexpand to atbased on im

T of palm oil vugh import)

ct employmehin the equatd Thailand f

n in poverty,oil industry rally. ast, the cou

m oil has onlThe neighbord US$ 225 mntent/upload

and supply cnd consumptanagement hnon in 3-5 yea) hectares bout 1,105 hagreements wectares. Duees and Plan

market Refinefinery with a operates at rce of 500 m

798 metric try is schedul

stments andrequiremen

energy capaon in the cohat power snize policies conservation

80,000 hecttent/uploads/million tons i

world populatrld populatioBasiron, 201

KL, 2012)

uncil, Inc. (Pt least 144,00

mport trends valued at USthe opportu

ent of 288,00or which arefully support, and high eresulting to

ntry with an ly 54,748 hering country million at P6.ds/2011/08/po

conditions antion which nehas targeted ears time as were alreadectares are with local co

e to the synen of Merger a

ed Bleached fractionationfull capacity

metric tons ofons of Palmed to be ope

pursuing ints especially

acity, achieveuntry. Lest tupply is suand guidelinof natural re

ares of matu/2010/04/6thn 2020 baseion growth p

on is projecte2).

PPDCI), the g00 hectares reported by

S$ 634.26 miunity of givin00 rural wor

e highly suitated the expexport genehuge palm

estimated oectares planhas exported68 billion in 2osters-oil-pal

d projected eeds to be ato develop 2targeted in 2y acquired foprepared to

ommunities iergy and taxas approved

Deodorized n machine wiy of 700 mef CPO, the re

m Olein and erational by A

ndustrializatiy the Visayae a reliable athe current gfficient to snes among cesources for

ure oil palm phnpocreport.ped on the proparallel to theed to grow fr

government’by the year the Malaysiaillion or P27.

ng high farmrkers. With t

able for oil papansion of theration. In co

oil importati

of more thannted, laggingd palm oil am2010 and to lm.pdf)

growth in incaddressed. T2,000 hectar2010. As of tfor developm

be availablen Misamis Ox efficiency, by its Boar

(RBD) palmith a capacityetric tons perefinery will p

342 metric August 2014

on, the govas and Mindand adequatgrowth momsupport the concerned aenergy proje

plantation to pdf) ojected 52.3 e increasing rom 7 billion

s continued 2017 would an Palm Oil .26 billion. It

m income to the four (4) alm farming, he palm oil ontrast, the on to meet

n 1,000,000 g behind as mounting to increase to

coming yearsTo respond tres of oil palmthe end of th

ment, of whice for plantingOriental for it

ABERDI and of Director

m oil productsy of 50 metrer month anproduce 1,14tons of Palm.

vernment is danao. The te supply of

mentum stall anticipated

agencies on ects.

s, to m he ch g. ts

nd rs

s. ic

nd 40 m

- 16 -

Government figures reveal that the year 2015 will be critical period for the Visayas Grid, where an additional capacity of 100MW will be needed to avert shortages. This forecast was derived from a projection by the Department of Energy of an annual demand growth rate of 4.55%. However, recent figures from 2001-2008 revealed a much higher demand growth rate of 6.3%.

Coal-Fired Power Project To fill the anticipated tight power supply situation in Panay and the Visayas grids by 2016 as

economic activity continues to expand in the area, a 135-megawatt coal-fired power plant in Concepcion, Iloilo is currently under construction.

Project financial closure has been completed in July 2013 while construction activities in the project site have already started on the 3rd quarter of 2013 after the Notice to Proceed was duly issued to the Engineering, Procurement and Construction (EPC) contractor. The commissioning of the plant is expected to be made by mid-2016. The plant site and support units are programmed for 2 units, since the project is to construct a 2x135MW generation power plant starting with 1 unit of 135-megawatt.The preparations for the second unit is forecasted to begin two to three years after commissioning of the first unit if the power market in the region continues to expand as projected.

Bunker-Fired Power Project

In 2013, Peakpower Energy, Inc. (PEI) was set up to address the lack of base load power in the

Mindanao electric grid for the next 2 to 3 years and in the future to allow the partner electric cooperatives to meet their demand for peaking power. The salient points of the projects are: short gestation period (from construction to commissioning), and take or pay on the capital expenditure.

Last October 2013, ABCI along with Enterprise Holdings Corporation, World Power Alliance Limited and Power Mavens Holdings Limited executed a Shareholders’ Agreement for their joint investment in PEI. The agreement outlines the collective support and commitment of the shareholders to bring Mindanao’s economic development to the next level.

Wartsila Finland Oy will be the supplier of the bunker/diesel-fired engines to be used in these power plants. These are engines with excellent fuel flexibility and efficiency. Wartsila has around 48.8GW of installed power in 4,599 power plants all over the world. In the Philippines, it has over 2,000 MW of installed capacity.

Peakpower Soccsargen Inc. (PSI) is the project company under PEI that is developing the 20.9 MW bunker/diesel-fired power plant for the South Cotabato II Electric Cooperative, Inc. (SOCOTECO2). Last March 20th 2013, PSI and SOCOTECO 2 signed a Power Purchase and Transfer Agreement (PPTA) which was followed by a ground breaking and capsule laying on the 14th of August the same year. Last July 1st 2014, PSI received their Provisional Approval Rates from the Energy Regulatory Commission (ERC). PSI is about to commence with the testing and commissioning stage of construction.

Peakpower San Francisco, Inc. (PSFI) is the project company under PEI that is developing the 5.2 MW bunker/diesel-fired power plant for the Agusan del Sur Electric Cooperative, Inc. (ASELCO). Last May 29th 2013, PSI and ASELCO signed a PPTA which was followed by a ground breaking and capsule laying on the 21th of August the same year. Last July 1st 2014, PSI received their Provisional Approval Rates from ERC. PSFI has started with the electrical-mechanical stage of construction to be followed by testing and commissioning.

PSI and PSFI are set to commence commercial operations by the last quarter of 2014.

Hydro Power Project

Hydro Link Projects Corp. (HLPC), ABCI’s wholly-owned subsidiary has secured the Hydropower Service Contract from the Department of Energy (DOE) for the development of the Carac-an river in Cantilan, Surigao del Sur. The contract gives Hydro Link exclusive rights to explore, develop and utilize the hydropower potential of the Carac-an River. The project is part of ABCI’s plans to provide much-needed additional power capacities for the electric cooperatives and the Mindanao Grid and to continue to look for other projects similar to it. As part of compliance with the service contract, the project is currently undergoing a feasibility study as part of the pre-development stage. The project has a potential of about 26 MW of capacity and is expected to generate an average of188 GWh annual energy. The output of the power station will be connected to the nearest substation of the Surigao del Sur Electric Cooperative II. Being a registered DOE project, it will enjoy all the incentives accorded to this type of project which include a seven-year income tax holiday as provided by RA 9513 (Renewable Energy Act) and issued by Board of Investments (BOI).

- 17 -

Impact of Economic/Political Uncertainties: The country has finally obtained last June 2013 its much-coveted investment grade status from

Fitch Ratings, one of the three major international credit rating agencies that evaluate the government’s credit worthiness. This is the first time that the country was bestowed with an investment grade rating since the Philippines went back to the international bond market after it declared a moratorium in 1983 due to the tightness in sourcing dollars. The investment grade is a seal of good housekeeping that tells investors that it is safe to invest in the country. Fitch upgraded the Philippines’ long term Foreign-currency issuer default rating (IDR) to “BBB-“ from “BB+” and the long-term local currency IDR to “BBB” from “BBB” with stable outlook. This upgrade means a dramatic strengthening in the ability of the government to meet its foreign and local obligations. It also means a lowering of the borrowing cost of the country from both local and foreign creditors. This could, likewise, result in an improvement in the attractiveness of the country in the eyes of the foreign investors that could further pick-up economic domestic activities.

The Company’s performance will continue to hinge on the overall economic performance of the country. Interest rate movements may affect the performance of the real estate industry, including the Company. Good governance will definitely lead to better economy and better business environment and vice-versa. Political stability encourages people to work better and spend more and the investors to infuse funds for additional investment. Plus, given the other positive economic indicators like recovery in exports, sustained rise in remittances, and growing liquidity in the domestic financial market, the monetary officials agree that the government’s projected growth targets is attainable.

We believe that the Company’s available cash, including cash flow from operations and drawings from existing and anticipated credit facilities, will provide sufficient liquidity to fund our projected operating, investment, capital expenditures and debt service requirements for the next twelve months. We have also implemented a number of initiatives under our liability management program to meet our debt service requirements in the short and medium term.

The Company does not expect to conduct any product research and development in the foreseeable future. No extraordinary purchase or sale of plant and equipment are expected beyond those in the regular course of the Company’s operations. The Brown Group of Companies foresees significant change in the number of employees at around 20 new employees (for 2014) if its proposed projects will push through. Hiring of employees will continue in the regular course of business. There are no events that will trigger direct or contingent financial obligation that is material to the company, including any default or acceleration of an obligation nor material off-balance sheet transactions, arrangements, obligations (including contingent obligations), and other relationships of the company with unconsolidated entities or other persons created during the reporting period. Material Event/s and Uncertainties:

The Company has no other events to report on the following: a) Any known trends, demands, commitments, events or uncertainties that will have a material

impact on its liquidity. b) Any material commitments for capital expenditures. c) Any known trends, events or uncertainties that have had or that are reasonably expected to

have a material favorable or unfavorable impact on net sales/ revenues/ income from continuing operations.

d) Any significant elements of income or loss that did not arise from the issuer’s continuing operations.

e) Any seasonal aspects that had a material effect on the financial condition or results of operations.

f) Any event/s that will trigger direct or contingent financial obligation that is material to the company, including any default or acceleration of an obligation.

g) Any material off-balance sheet transactions, arrangements, obligations (including contingent obligations), and other relationships of the company with unconsolidated entities or other persons created during the reporting period.

The Company has no other information that needs to be disclosed other than disclosures made under SEC Form 17-C (if any).

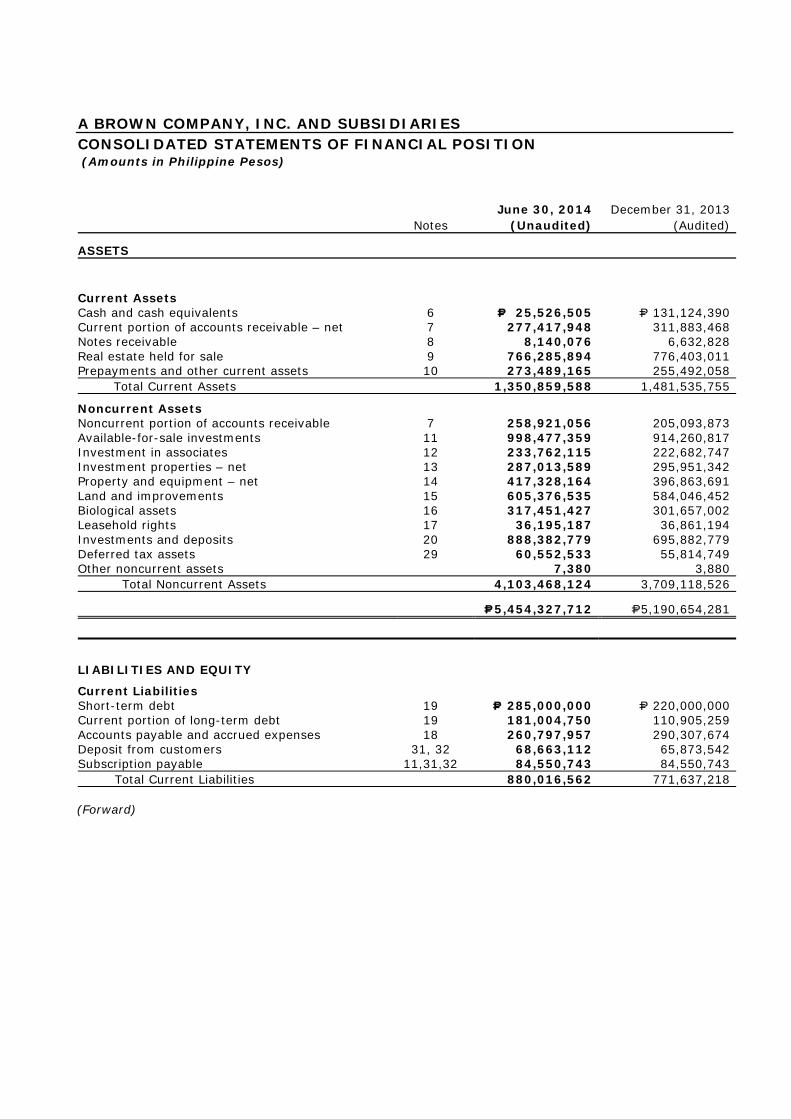

A BROWN COMPANY, INC. AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF FINANCIAL POSITION (Amounts in Philippine Pesos)

Notes June 30, 2014

(Unaudited) December 31, 2013

(Audited)

ASSETS

Current Assets Cash and cash equivalents 6 P= 25,526,505 P= 131,124,390 Current portion of accounts receivable – net 7 277,417,948 311,883,468 Notes receivable 8 8,140,076 6,632,828 Real estate held for sale 9 766,285,894 776,403,011 Prepayments and other current assets 10 273,489,165 255,492,058

Total Current Assets 1,350,859,588 1,481,535,755

Noncurrent Assets Noncurrent portion of accounts receivable 7 258,921,056 205,093,873 Available-for-sale investments 11 998,477,359 914,260,817 Investment in associates 12 233,762,115 222,682,747 Investment properties – net 13 287,013,589 295,951,342 Property and equipment – net 14 417,328,164 396,863,691 Land and improvements 15 605,376,535 584,046,452 Biological assets 16 317,451,427 301,657,002 Leasehold rights 17 36,195,187 36,861,194 Investments and deposits 20 888,382,779 695,882,779 Deferred tax assets 29 60,552,533 55,814,749 Other noncurrent assets 7,380 3,880

Total Noncurrent Assets 4,103,468,124 3,709,118,526

P=5,454,327,712 P=5,190,654,281

LIABILITIES AND EQUITY

Current Liabilities Short-term debt 19 P= 285,000,000 P= 220,000,000 Current portion of long-term debt 19 181,004,750 110,905,259 Accounts payable and accrued expenses 18 260,797,957 290,307,674 Deposit from customers 31, 32 68,663,112 65,873,542 Subscription payable 11,31,32 84,550,743 84,550,743

Total Current Liabilities 880,016,562 771,637,218

(Forward)

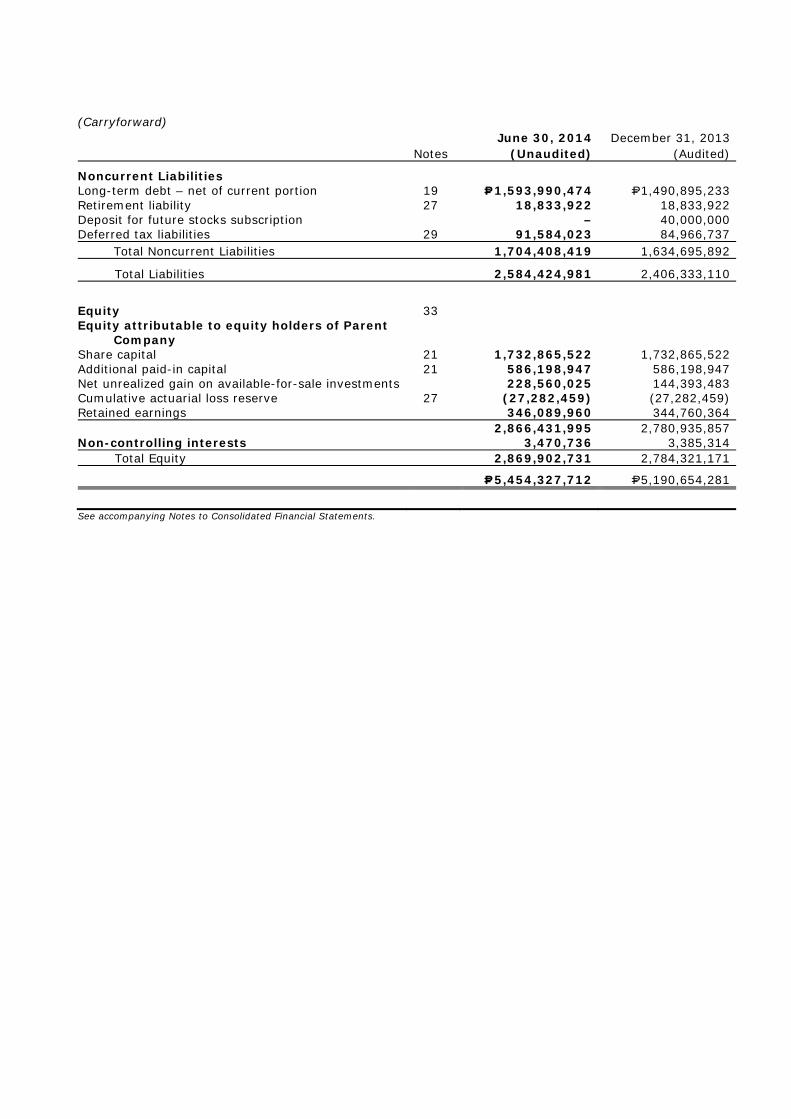

(Carryforward)

Notes June 30, 2014

(Unaudited) December 31, 2013

(Audited)

Noncurrent Liabilities Long-term debt – net of current portion 19 P=1,593,990,474 P=1,490,895,233 Retirement liability 27 18,833,922 18,833,922 Deposit for future stocks subscription – 40,000,000 Deferred tax liabilities 29 91,584,023 84,966,737

Total Noncurrent Liabilities 1,704,408,419 1,634,695,892

Total Liabilities 2,584,424,981 2,406,333,110

Equity 33 Equity attributable to equity holders of Parent

Company Share capital 21 1,732,865,522 1,732,865,522 Additional paid-in capital 21 586,198,947 586,198,947 Net unrealized gain on available-for-sale investments 228,560,025 144,393,483 Cumulative actuarial loss reserve 27 (27,282,459) (27,282,459) Retained earnings 346,089,960 344,760,364 2,866,431,995 2,780,935,857 Non-controlling interests 3,470,736 3,385,314

Total Equity 2,869,902,731 2,784,321,171

P=5,454,327,712 P=5,190,654,281

See accompanying Notes to Consolidated Financial Statements.

A BROWN COMPANY, INC. AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF INCOME (Amounts in Philippine Pesos)

For the quarter ending

June 30 Year-to-Date

Note 2014

(Unaudited)2013

(Unaudited)6/30/2014

(Unaudited) 6/30/2013

(Unaudited)

REVENUES Sales 22 P=174,727,373 P= 93,031,102 P=324,116,641 P=199,708,644Financial income 23 4,978,312 9,317,190 10,499,447 20,734,139Sales of aggregates 5,136,857 3,677,062 6,107,795 7,010,979Rental income 20, 28 2,342,956 1,885,446 5,358,237 3,762,975Others 24 2,339,956 1,247,985 8,177,985 20,824,890 189,525,454 109,158,785 354,260,105 252,041,627

COST AND EXPENSES Cost of sales and services 25 103,365,419 57,314,889 189,810,897 118,072,710General and administrative 26 47,962,945 50,031,178 92,648,765 97,875,452Finance costs 19 21,144,579 17,065,885 40,644,676 32,993,580Marketing 9,111,611 8,024,969 18,095,386 16,224,062Equity in net loss (gain) of an associate 12 (6,051,741) (1,788,906) 6,613,972 1,205,456Provision for impairment loss 13 382,150 382,150 764,300 764,300 175,914,963 131,030,165 348,577,996 267,135,560

INCOME (LOSS) BEFORE INCOME TAX 13,610,491 (21,871,380) 5,682,109 (15,093,933)

INCOME TAX EXPENSE (BENEFIT) 29 Current 2,466,619 2,830,542 3,581,083 14,006,852Deferred 139,777 (22,389,526) 686,008 (31,510,621) 2,606,396 (19,558,984) 4,267,091 (17,503,769)

NET INCOME (LOSS) P=11,004,095 (P=2,312,396) P=1,415,018 P=2,409,836

NET INCOME (LOSS) ATTRIBUTABLE TO: Equity holders of the Parent Company P=10,961,714 (P=1,649,730) P=1,329,596 P=3,039,887Non-controlling interests 42,381 (662,666) 85,422 (630,051)

P=11,004,095 (P=2,312,396) P=1,415,018 P=2,409,836 BASIC AND DILUTED EARNINGS

(LOSS) PER SHARE 30

Attributable to:

Equity holders of the Parent Company P= 0.00633 (P=0.00119) P= 0.00077 P=0.00219

See accompanying Notes to Consolidated Financial Statements.

A BROWN COMPANY, INC. AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (Amounts in Philippine Pesos)

For the quarter ending June 30 Year-to-Date

Note

2014 (Unaudited)

2013 (Unaudited)

6/30/2014 (Unaudited)

6/30/2013 (Unaudited)

NET INCOME (LOSS) P=11,004,095 (P= 2,312,396) P= 1,415,018 P= 2,409,836

OTHER COMPREHENSIVE INCOME Unrealized gain (loss) on available-for-

sale investments 11 28,168,105 (14,228,319) 84,166,542 10,854,921

COMPREHENSIVE NET INCOME (LOSS) P=39,172,200 (P=16,540,715) P=85,581,560 P=13,264,757

Attributable to: Equity holders of the Parent Company P=39,129,819 (P=15,878,049) P=85,496,138 P=13,894,808 Non-controlling interests 42,381 (662,666) 85,422 (630,051)

P=39,172,200 (P=16,540,715) P=85,581,560 P=13,264,757

See accompanying Notes to Consolidated Financial Statements.

- 23 -

A BROWN COMPANY, INC. AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY (Amounts in Philippine Pesos)

Notes

As of 06/30/2014 (Unaudited)

As of 06/30/2013 (Unaudited)

As of12/31/2013

(Audited)

EQUITY ATTRIBUTABLE TO EQUITY HOLDERS OF PARENT COMPANY

SHARE CAPITAL - P=1 par value Authorized – 2,000,000,000 shares in

2014 and 2013, 1,620,000,000 shares in 2012

Subscribed – 1,732,865,522 shares in 2014 and 2013, 1,386,293,229 shares in 2012 21

Balance at beginning of year P=1,732,865,522 P=1,386,293,229 P=1,386,293,229Issuance during the period/year – – 346,572,293Balance at end of year 1,732,865,522 1,386,293,229 1,732,865,522 STOCK DIVIDENDS DISTRIBUTABLE 34 – 346,573,307 – ADDITIONAL PAID-IN CAPITAL 21 586,198,947 586,198,947 586,198,947 NET UNREALIZED GAIN ON

AVAILABLE-FOR-SALE INVESTMENTS

Balance at beginning of year 144,393,483 146,894,874 146,894,874Net unrealized gain (loss) during the

period/year 11 84,166,542 10,854,921 (2,501,391)Balance at end of period/year 228,560,025 157,749,795 144,393,483

CUMULATIVE ACTUARIAL LOSS

RESERVE 27 Balance at beginning of year as previously

reported (27,282,459) – – Adjustments – – (24,206,991)Balance at beginning of year as restated (27,282,459) – (24,206,991) Actuarial loss as previously reported – – (3,075,468)Adjustments – – –Actuarial loss as restated – – (3,075,468) Balance at end of period/year (27,282,459) – (27,282,459) (Forward)

- 24 -

(Carryforward)

As of 06/30/2014 (Unaudited)

As of 06/30/2013 (Unaudited)

As of 12/31/2013

(Audited) RETAINED EARNINGS Balance at beginning of year as previously

reported P= 344,760,364 P= 685,835,631 P= 685,835,631 Adjustments – – 1,941,382 Balance at beginning of year as restated 344,760,364 685,835,631 687,777,013 Stock dividends declared and distributed – – (346,572,293) Dividend declaration – (346,573,307) – Increase in retained earnings due to

deconsolidated subsidiaries – 4,526,951 – Net income during the period/year 1,329,596 3,039,887 3,555,644 Balance at end of period/year 346,089,960 346,829,162 344,760,364 Total Equity Attributable to Equity Holders of

Parent Company P=2,866,431,995 P=2,823,644,440 P=2,780,935,857 NON-CONTROLLING INTERESTS Balance at beginning of year 3,385,314 2,952,530 2,952,530 Net income (loss) during the period/year 85,422 (630,051) 432,784 Increase/(Decrease) in noncontrolling interests due to re/(de)consolidated subsidiaries 642,764,608 Balance at end of period/year 3,470,736 645,087,087 3,385,314 P=2,869,902,731 P=3,468,731,527 P=2,784,321,171 See accompanying Notes to Consolidated Financial Statements

- 25 -

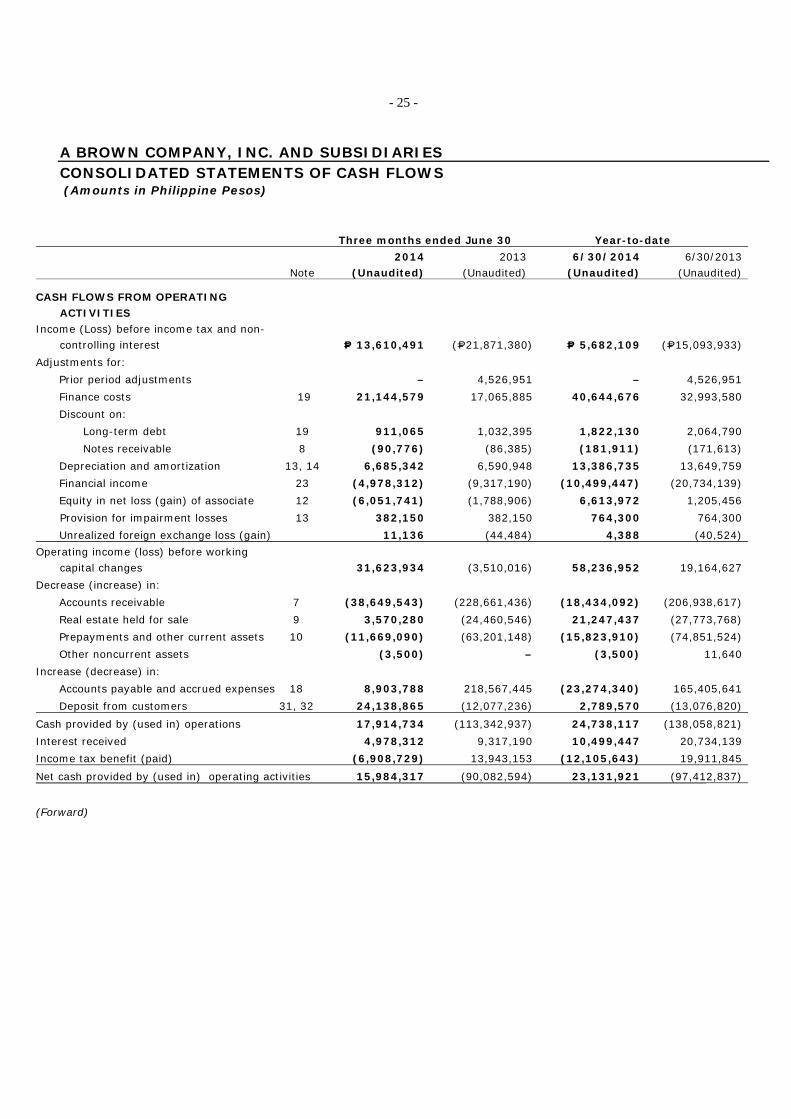

A BROWN COMPANY, INC. AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF CASH FLOWS (Amounts in Philippine Pesos)

Three months ended June 30 Year-to-date

Note 2014

(Unaudited)2013

(Unaudited) 6/30/2014

(Unaudited) 6/30/2013

(Unaudited)

CASH FLOWS FROM OPERATING ACTIVITIES

Income (Loss) before income tax and non-controlling interest P= 13,610,491 (P=21,871,380) P= 5,682,109 (P=15,093,933)

Adjustments for: Prior period adjustments – 4,526,951 – 4,526,951 Finance costs 19 21,144,579 17,065,885 40,644,676 32,993,580 Discount on:

Long-term debt 19 911,065 1,032,395 1,822,130 2,064,790 Notes receivable 8 (90,776) (86,385) (181,911) (171,613)

Depreciation and amortization 13, 14 6,685,342 6,590,948 13,386,735 13,649,759 Financial income 23 (4,978,312) (9,317,190) (10,499,447) (20,734,139) Equity in net loss (gain) of associate 12 (6,051,741) (1,788,906) 6,613,972 1,205,456 Provision for impairment losses 13 382,150 382,150 764,300 764,300 Unrealized foreign exchange loss (gain) 11,136 (44,484) 4,388 (40,524)

Operating income (loss) before working capital changes 31,623,934 (3,510,016) 58,236,952 19,164,627

Decrease (increase) in: Accounts receivable 7 (38,649,543) (228,661,436) (18,434,092) (206,938,617) Real estate held for sale 9 3,570,280 (24,460,546) 21,247,437 (27,773,768) Prepayments and other current assets 10 (11,669,090) (63,201,148) (15,823,910) (74,851,524) Other noncurrent assets (3,500) – (3,500) 11,640

Increase (decrease) in: Accounts payable and accrued expenses 18 8,903,788 218,567,445 (23,274,340) 165,405,641 Deposit from customers 31, 32 24,138,865 (12,077,236) 2,789,570 (13,076,820)

Cash provided by (used in) operations 17,914,734 (113,342,937) 24,738,117 (138,058,821) Interest received 4,978,312 9,317,190 10,499,447 20,734,139 Income tax benefit (paid) (6,908,729) 13,943,153 (12,105,643) 19,911,845 Net cash provided by (used in) operating activities 15,984,317 (90,082,594) 23,131,921 (97,412,837)

(Forward)

- 26 -

(Carryforward)

Three months ended

June 30 Year-to-date

Note 2014

(Unaudited)2013

(Unaudited) 6/30/2014

(Unaudited)6/30/2013

(Unaudited)

CASH FLOWS FROM INVESTING ACTIVITIES

Additions to: Property and equipment 14 (P= 34,640,352) (P=229,724,318) (P= 49,721,979) (P=253,519,240) Investment properties – (64,601,005) – (64,601,005) Land and improvements 15 (500,083) (7,938,691) (1,146,662) (12,655,159) Land rights 17 – – – (75,030)

Investments and deposits 20 – 94,640,000 (192,500,000) 76,785,626 Increase in:

Biological assets 16 (5,820,177) (22,110,104) (15,128,418) (35,668,826) Available-for-sale investments – (789,600) (50,000) (789,600) Goodwill 2 – (44,367,290) (44,367,290)

Loan to a related party 8 644,663 404,600 (1,325,337) (595,400) Proceeds from disposal of investment property 13 – – 6,105,485 – Proceeds from disposal of property and

equipment 14 – 1,300 – 114,820 Increase (Decrease) in Investment in an

associate 12 (17,393,341) 24,648,179 (17,693,341) 24,627,424

Net cash used in investing activities (57,709,290) (249,836,929) (271,460,252) (310,743,680)

CASH FLOWS FROM FINANCING ACTIVITIES Payments of:

Finance costs 19 (P=29,708,314) (P=23,912,960) (P=53,637,768) (P=47,879,479)Long-term debt 19 (69,005,279) (4,320,000) (97,375,398) (10,884,816)Cash dividend (3,447) – (447)

Proceeds from long term debt Short-term debt 70,000,000 – 70,000,000 20,000,000Long-term debt – – 263,748,000 –

Deposits received for future stock subscription – 869,484,000 – 869,484,000Return of deposits for future stock subscription – – (40,000,000) –Increase in noncontrolling interests of subsidiaries – 642,764,608 – 642,764,608Net cash provided by (used in) financing

activities (28,713,593) 1,484,012,201 142,734,834 1,473,483,866EFFECT OF EXCHANGE RATE CHANGES ON CASH AND CASH EQUIVALENTS 6 (11,136) 44,484 (4,388) 40,524NET INCREASE/ (DECREASE) IN CASH AND CASH EQUIVALENTS (70,449,702) 1,144,137,162 (105,597,885) 1,065,364,873

CASH AND CASH EQUIVALENTS AT BEGINNING OF PERIOD/YEAR 95,976,207 916,487,239 131,124,390 995,259,528

CASH AND CASH EQUIVALENTS AT END OF PERIOD/YEAR

6 P= 25,526,505 P=2,060,624,401 P= 25,526,505 P=2,060,624,401

See accompanying Notes to Consolidated Financial Statements.

- 27 -

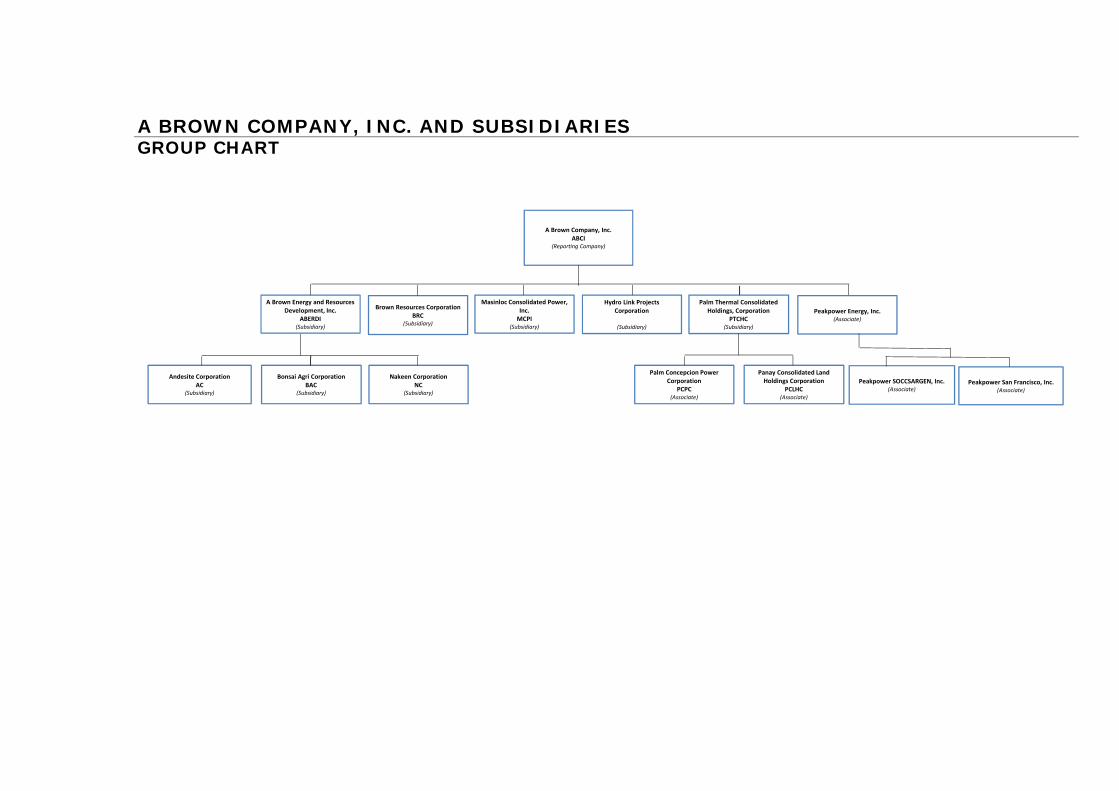

A BROWN COMPANY, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Amounts in Philippine Pesos) 1. Corporate Information

A Brown Company, Inc. (Parent Company) was incorporated and registered with the Philippine Securities and Exchange Commission (SEC) on December 21, 1966 as Bendaña Brown Pizarro and Associates, Inc. to primarily engage in the business of property development and to invest in shares of stocks of listed companies. On October 1, 1992, the Parent Company amended its articles of incorporation to change its registered name to EPIC Holdings Corporation, which was further amended on July 1, 1993 to its current registered name. On February 8, 1994, the Parent Company was listed in the Philippine Stock Exchange. The Parent Company’s principal purpose is to invest in, purchase, or otherwise acquire and own, hold, use, sell, assign, transfer, mortgage, pledge, exchange, or otherwise dispose of real and personal property of every kind and description, including of shares of stock, bonds, debentures, notes, evidences of indebtedness, and other securities or obligations of any other corporation, associations, domestic or foreign, for whatever lawful purpose or purposes the same may have been organized without being a stock broker or dealer, and to pay therefor in money or by exchanging therefor stocks, bonds, or other evidences of indebtedness or securities of this or any other corporation and while the owner or holder of any such real or personal property, stocks, bonds, debentures, contracts or obligations, to receive, collect and dispose of the interest, dividends, and income arising from such property and to possess and exercise in respect thereof all the rights, powers and privileges of ownership, provided the corporation shall not exercise the functions of a trust corporation. The principal activities of the operating subsidiaries are as follows: Name of Subsidiary Principal Activity A Brown Energy and Resources

Development, Inc. (ABERDI) Manufacturing, trading of goods on wholesale and retail basis and other services.

Brown Resources Corporation (BRC) Real estate holding and management of chalet operations. Andesite Corporation (AC), Bonsai Agri

Corporation (BAC) and Nakeen Corporation (NC)

Development of land for palm oil production and sale of palm seedlings and crude palm oil.

Masinloc Consolidated Power, Inc. (MCPI) Operating of power plants and/or purchase, generation,

production supply and sale of power. However, as of June 30, 2014, the Company has not yet started commercial operations.

Palm Thermal Consolidated Holdings, Corp.

(PTCHC) Holding of properties of every kind and description.

Hydro Link Projects Corp. (HLPC) Developing, constructing and operating power generating plants

On June 13, 2012, the SEC approved the amendment of the Company’s By-Laws to amend and define the functions of its Executive Chairman and President, remove the requirement that the Company’s vice presidents must be a member of the Board, and to impose certain requirements on granting of bonuses to its BOD, officers and employees. On October 5, 2012, the Parent Company’s Board of Directors (BOD) approved during their meeting the private placement of 250.0 million of its listed common shares consisting of 173.6 million treasury common shares and 76.4 million common shares owned by a shareholder. The Placement Shares, with a par value of P=1 per share

- 28 -

was sold at a price of P=2.89 per share and crossed in the Exchange on October 8, 2012. The BOD likewise approved the issuance of an equal number of shares of the Parent Company at an issue price equal to the net proceeds per share in favor of the lending shareholder. The shares will be issued out of the increase in the Parent Company’s authorized capital stock from P=1.32 billion divided into 1.32 billion shares with a par value of P=1 to P=1.62 billion divided into 1.62 billion shares with par value of P=1. On December 28, 2012, the SEC approved the Company’s application for increase in authorized capital stock. Subsequently, the 76.4 million common shares were issued. On June 7, 2013 the Parent Company’s Board of Directors (BOD) unanimously approved the proposed 25% stock dividend declaration or equivalent to 346.6 million of the Parent Company’s outstanding shares. The shares will be distributed to the stockholders record as of September 12, 2013 and shall be issued out of the increase in the Parent Company’s authorized capital stock from P=1.62 billion divided into 1.62 billion shares with par value of P=1 to P=2.0 billion divided into 2 billion shares with par value of P=1. On August 16, 2013, the SEC approved the Parent Company’s application for increase in authorized capital stock. Subsequently, 346.6 million shares were issued. The Parent Company’s registered office and principal place of business is at Xavier Estates, Upper Balulang, Cagayan de Oro City, Philippines (see Note 36).

2. Basis of Preparation

The consolidated financial statements of the Group have been prepared using the historical cost basis, except for available-for-sale investments which are measured at fair values. These consolidated financial statements are presented in Philippine Peso, which is the Group’s functional and reporting currency. All values are rounded to the nearest peso, except when otherwise indicated. Statement of Compliance The accompanying consolidated financial statements of the Group have been prepared in compliance with Philippine Financial Reporting Standards (PFRS). PFRS includes statements named PFRS, Philippine Accounting Standards (PAS) and International Financial Reporting Interpretations Committee (IFRIC) interpretations issued by the Financial Reporting Standards Council. Principles of Consolidation The consolidated unaudited financial statements consist of the financial statements of the Parent Company and its subsidiaries as of end of the first three quarters of each year. This report covers the period ending June 30, 2014. The consolidated financial statements of the subsidiaries are prepared for the same reporting year as the Parent Company, using consistent accounting policies. Subsidiaries are consolidated from the date on which control is transferred to the Group and cease to be consolidated from the date on which control is transferred out of the Group. Consolidated financial statements are prepared using uniform accounting policies for like transactions and other events in similar circumstances. Intercompany balances and transactions, including intercompany profits and unrealized profits and losses are eliminated. Noncontrolling interests represent interests in certain subsidiaries not held by the Parent Company and are presented separately in the consolidated statements of income, consolidated statements of comprehensive income and consolidated statements of changes in equity and within equity in the consolidated statements of financial position, separately from equity attributable to the Parent Company.

- 29 -

The subsidiaries and the percentage of ownership of the Parent Company are as follows:

Percentage of ownership

Name of subsidiary Nature of business 2014 2013

ABERDI Manufacturing and trading/Service/Agriculture

100

100

AC Agriculture 100 100 BAC Agriculture 100 100 NC Agriculture 100 100

BRC Real estate holding/Hotel operations 100 100 MCPI Power plant operation 49 49 PTCHC Holdings 100 100 HLPC Power plant operation 100 100

All of the above subsidiaries were incorporated in the Philippines.