2026-5727icagh.com/file/4th_qtr_journal_2014.pdf · the changing landscape of educational standards...

TRANSCRIPT

2026- 5727

OFFICIAL JOURNAL OF THE INSTITUTE OF CHARTERED ACCOUNTANTS [GHANA] DECEMBER,2014

MEMBERS OF COUNCIL (2014 – 2016)

Prof. K.B Omane-Antwi - President

Mr. Christian Sottie - Vice President

Mrs. Angela Peasah - Member

Dr. Williams A. Atuilik - Member

Ms. Rebecca Lomo - Member

Maj. (Rtd) D. Ablorh-Quarcoo - Member

Prof. Kwame Adom-Frimpong - Member

Ms. Grace Adzroe - Member

Mr. Richard Q. Quartey - Member

Mr. Kwasi Asante -Member

Mr. Kwasi Gyimah-Asante - Member

MEMBERS OF PUBLICATIONS COMMITTEE

Ms. Rebecca Atswei Lomo - Chairman

Mr. Joseph Hyde Jnr - Vice Chairman

Mr. Samuel Petterson Larbi - Member

Mrs. Esther Kenyenso - Member

Mr. Eric Oduro Osae - Member

Mr. Kwame Antwi-Boasiako - Member

Mr. Ibrahim Ommanu - Member

Mr. Fred N. K. Moore - Member/CEO

Ms. Abigail Armah - Member/Manager

SECRETARIAL ADDRESS

Institute of Chartered Accountants - Ghana

Okponglo, East Legon

P. O. Box GP 4268, Accra

Tel: +233(0)544336701-2/+233(0)277801422-4

CONTENT

EDITORIAL

IFAC NEWS

1.1 WCOA Rome: The Olympics of accountancy

1.2 Ian Ball receives IFAC Gold Service Award1.3 Public Sector fraud risk monitoring tool

launched 1.4 IFAC appoints rst female president1.5 Former Chairman of Kenyan Institute

received Sempier Award1.6 WCOA has come to an end

ICAG NEWS TIT BITS

Proposal for establishing faulty and

Special Interest groups within ICAG

ICAG signs MoU to collaborate with the

CAGD

Chartered Accountants challenged to be

professional

Public Sector adopts IPSAS

ICAG Inaugurates the Faculty System

FEATURES

The Changing Landscape of Educational Standards in the Accountancy Profession Strengthening Financial Markets and Institutions in AfricaFighting Corruption in Public Institutions: The role of the Internal AuditorAre you playing defence as a leader?

TECHNOLOGY CORNER

Six ways to use Social Media Adverts (Ads) to grow your Business

YOU AND YOUR HEALTH

5.1 Nutritional facts about Chicken

TECHNICAL MATTERS

6.1 Guidelines for Public Debt Management

6.2 Monetary and Macro-prudential Policies:

The case of Ghana

PAGE

2.1

2.2

2.3

2.4

2.5

3.1

3.2

3.3

3.4

4.1

1

2

2

3

3

4

5

5

6

6

7

8

9

13

16

19

22

24

28

THE PROFESSIONAL ACCOUNTANT

IN THIS ISSUE

i

31

“There is flattery in friendship”

William Shakespeare

“Until we extend the circle of our compassion to all living things we

will not ourselves fine peace”

Albert Schweitzer

“Don't be afraid of the space between your dreams and reality. If

you can dream it, you can make it so”

Belva Davis

“Always listen to experts. They will tell you what can't be done and

why”

Robert Heinlein

“Each new season grows from the leftovers from the past. That is

the essence of change, and change is the basic law”.

Hal Borland

QUOTES………..

ii

EDITORIALAfter Rome, what Next?

thThe 19 World Congress of Accountants (WCOA) held in Rome, Italy kicked off with nearly 4,000 participants from about 140 delegation from all over the world. The sheer number of delegates and the diverse background and culture of the attendees have prompted people to nickname the event “the Olympics of the profession”. This quadrennial event which was rst held in St. Louis in USA in 1904, has been held in different cities with different themes.

This year's event with the theme “2020 Vision – focus from the past, building the future” is very appropriate and could not have come at a better time, when the world's economy seems to be engulfed with mirage of problems. The theme for the congress tried to link the relationship between the past and the future; which past experiences need to be considered in bettering our future? What kind of a future do we want to build? What kind of future do we want to leave for the future generation? These are the major questions that need to be answered.

The key issue here is, why do some countries do better than the others? Why do some countries rise and fall? Jacob Soll wrote in his book,“The Reckoning: Financial Accountability and the Rise and Fall of Nations”, and I quote “From Renaissance Italy, the Spanish empire, and Louis XIV's France to the Dutch Republic, the British Empire, the early United States, effective accounting and political accountability have made the difference between a society's rise and fall”.

“Over and over again good accounting practices have produced the level of trust necessary to found stable governments and vital capitalist societies, and poor accounting and its attendant

lack of accountability have led to nancial chaos, economic crimes, civil unrest, and worse standard of living for most nations”.

The lack of accountability and poor accounting

will denitely lead to the fall of nations. These

are the natural consequences of our actions and

inactions, particularly from our leadership who

control public resources. Among the causes that

led to the collapse and decline of the great

ancient Roman Empire and other empires, were

economic troubles, public sector overspending

and government corruption. Sadly, more than

500 years on, these issues are still present

particularly in Africa. Nations are still in

recession after the debt crisis, and the threat of

corruption stemming from “shadowy and secret

dealings” remains in place.

There is the need for greater transparency in the

public sector to ght government's corruption,

which is a task not only for accountants but the

global business community. The public sector

fraud risk monitoring tool being developed by

CIPFA would go a long way in helping stem

corruption from our public sector organisations.

We should all embrace this tool to help us

identify fraud risk-prone areas so that we can

take measures to address them before they

become a canker which will be difcult to

eradicate.

The battle is on, the challenge has been thrown,

let us see how accountants in both public and

private sectors will rise to the occasion in

ensuring proper accountability, transparency,

good governance and proper utilization of

resources. By this, our nation Ghana will rise.

Enjoy your reading.

For editor Ofori Frimpong Henneh

1

1. IFAC NEWS1.1 WCOA Rome: The Olympics of accountancyBy Carlos Martin Tornero &Vincent Huck

thThe 19 World Congress of Accountants (WCOA) held in Rome kicked off with 4,000 participants from 140 delegations, which have prompted some to nickname the event “the Olympics of the profession”. The WCOA was rst held in St. Louis in USA, in 1904 and has since been held every four years, each time in a different city and with a different theme.

The WCOA 2014 theme is “2020 Vision – focus from the past, building the future”. In his welcome address at the opening ceremony, Consiglio Nazionale dei Dottori Commercialisti e degli Esperti contalili, (National Council of Professional and Expert Accountants president, )Gerardo Longobardi said, “This year the Congress is dedicated to the relationship between the past and the future – which past experiences need to be considered? What kind of a future do we want to build? And for whom? These are the major questions that need to be answered.

To that effect during the next four days, participants will debate three main issues: the access to credit, taxation and accountability in the public and private sector. In his welcome address IFAC outgoing president, Warren Allen said, “I have heard this event referred to as the Olympics of accounting. But unlike the Olympics, the WCOA is about collaboration and not competition.”

But in some ways, walking down the corridors of the Auditorium Parco Della Musica, where the event was held, does feel like a similar experience to visiting the Olympic Park with a host of languages spoken and a diversity of cultural attires from the traditional suit and tie to the Boubou (West African attire) and the Deel (Mongolian traditional dress).

Nigeria brought the largest delegation to the congress and before the ofcial opening of the WCOA 2014, delegates showed their support to their Nigerian colleagues by observing a minute of silence for the 46 victims from a bombing in a school in the North East of the country, believed to be the last attack by Boko Haram.

The second largest delegation came from the host country, Italy, with over 500 delegates. A number of countries were represented by more than 100 professionals such as Brazil, China, Japan, Ghana, Malaysia, Mongolia, UK and the USA.

Allen compared the inaugural congress, held in St. Loius 110 years ago and attended by 81 delegates, to the current attendance thus: “Our accounts are accurate: more than 3900 delegates from 140 countries”, he said. Nations are still in recession after the debt crisis, he said, and the threat of corruption stemming from “shadowy and secret dealings” remains in place. Allen called for greater transparency in the public sector to ght governments' corruption, which is a task not only for accountants but for the global business community.

He concluded his keynote speech paraphrasing the adage “all roads lead to Rome”. On this occasion, all those roads lead “from” Rome, in reference to challenges ahead for the profession, this congress being the starting point.

1.2 Ian Ball receives IFAC Gold Service Award

IFAC outgoing president Warren Allen has

presented IFAC's former chief executive for ten

years and CIPFA current chairman, Ian Ball, with

the IFAC Gold Service Award at the WCOA

2014 in Rome, Italy. This award was established

in 2010 to recognize outstanding individual

contributions to improve the profession's

relevancy including protecting the public

interest, exemplifying professional conduct and

ethics; exceptional quality of work; and/or,

contributions to a particular project or initiative.

2

Presenting the award, Allen praised Ball for 10

years at IFAC's helm contributing to improve the

profession's relevancy and his leadership

through the nancial crisis, as well as his

advocacy for good nancial management by

governments. Receiving the award, Ball said, it

was special to be presented with this award

especially in Italy for two reasons, one personal

and one historical.

Ball said, although Pacioli is considered the

father of double entry accounting, this was

common practice in Italy for 2000 years before

he rst published his writings. Unfortunately

some governments have lost their ways since

those times. He concluded his acceptance

speech by quoting Jacob Soll who wrote in his

book “The Reckoning: Financial Accountability

and the Rise and Fall of Nations”. “From

Renaissance Italy, the Spanish empire, and

Louis XIV's France to the Dutch Republic, the

British Empire, the early United States, effective

accounting and political accountability have

made the difference between a society's rise and

fall”. “Over and over again good accounting

practices have produced the level of trust

necessary to found stable governments and vital

capitalist societies, and poor accounting and its

attendant lack of accountability have led to

nancial chaos, economic crimes, civil unrest,

and worse standard of living for most nations”.

1.3 Public sector fraud risk monitoring tool launched

CIPFA hoped this tool will give organizations a better understanding of the sources of fraud, so that they can efciently and timely react and tackle corruption. “When ghting fraud, knowledge and understanding of the risks you face, give you the power to act to prevent criminal activity and protect your organization”.

CIPFA chairman Ian Ball, who received IFAC's gold service award, said it is not a coincidence that the lack of accountability and poor accounting lead to the fall of nations. IFAC outgoing president Warren Allen, who presented the award to Ball, delved into history and made reference to the causes behind the decline of the ancient Roman Empire. Among those were economic troubles, public sector overspending and government corruption. Allen emphasized that more than 500 years on, those issues seem to be present nowadays. Nations are still in recession after the debt crisis, he said, and the threat of corruption stemming from “shadowy secret dealings” remains in place. Allen called for greater transparency in the public sector to ght government's corruption, which is a task not only for accountants but the global business community.

The Chartered Institute of Public Finance and

Accountancy (CIPFA) has launched a register,

specically designed to tackle global fraud risk

in the public sector. The register, a research

initiative, is aimed at collating the most common

fraud risks that government and public sector

organizations face country by country, according

to CIPFA. After the rst step, CIPFA will merge

those registers at country level into global one

next year.

1.4 IFAC appoints rst female presidentThe International Federation of Accountants (IFAC), has elected Olivia Kirtley as president, the rst woman appointed to the position. Hailing from the US, Kirtley is also the rst president elected from business and industry, rather than public accounting, and will hold the position of president for a two-year term ending in November 2016.

Kirtley was rst elected to the IFAC board in 2007, rising to the postion of deputy president in 2012. Her role will be taken over by Rachel Grimes from Australia. A certied public accountant and chartered global management accountant, Kirtley is also non-executive director of US Bancorp, ResCare Inc, and Papa John's International.

3

With a long-standing background in accounting

and management, she is a former chair of the

American Inst i tute of Cert ied Public

Accountants (AICPA) and the AICPA Board of

examiners. AICPA described Kirtley as a

“recognized advocate for strong corporate

governance” and outgoing president of IFAC

Warren Allen cited her as a “great source of

support” during his term.

Kirtley herself described her appointment as

coming at “an exciting time for IFAC” and said

“As president, I look forward to engaging with

member bodies and our many stakeholders as we

seek ways to advance the impact and value of our

profession and in serving the public interest”.

1.5 Former cha i rman of Kenyan institute receives IFAC Sempier awardIFAC has presented former chairman of the Institute of Certied Public Accountants of Kenya (ICPAK), Ndungu Gathinji with the IFAC Robert Sempier award. Created in 1991 the Robert Sempier award recognizes outstanding contributions to the accountancy profession by an individual over a period of many years.

Gathinji has represented Kenya on IFAC since 1987, where he pushed for the creation of the Development Nations Committee, now renamed Professional Accountancy Organization Development Committee. He was a member of the Standards Advisory Council of the International Accounting Standards Committee foundation. He helped found the African Stock Exchanges Association in 1993 and has served as its honorable secretary ever since. He practiced as a chartered accountant for 26 years before retiring as chairman of EY East Africa in 1997.

In his acceptance speech, Gathinji reected on

his life within the accounting profession from

the times of British colonial rule in Kenya and

the Mao Mao uprising till today and the

appointment of Olivia Kirtley as the rst female

president of IFAC. “We are still waiting for the

rst president of IFAC from Africa”, Gathinji

said before praising the continent's achievement

in the past 50 years. For those who have

preconceived ideas about African migrants who

put their life at risk to reach Europe or other

developed part of the world, Gathinji answered:

“This do or die attitude is a prerequisite to

bettering oneself”. “The best of Africa has yet to

come”, he concluded.

1.6 WCOA has come to an end

thThe 19 WCOA 2014 held in Rome has come to a close and the profession has reiterated its commitment to further collaborate in order to enhance its presence worldwide. The WCOA 2014 closed with a speech of the newly appointed IFAC president Olivia Kirtley, the

th16 of the organization and the rst female leader.

Kirtley highlighted the importance of further strengthening the profession globally and gave the example of Rwanda which in the past 20 years has gone from 54 qualied accountants in the aftermath of the genocide and concurrent civil war to over 200 in present days. She announced the rst three countries, out of ten, to benet f rom the UK Depar tment for International Development (DFID) £4.935m ($8.254m) funding to IFAC capacity building projects: Ghana, Rwanda and Uganda. She went on to emphasize the importance of accrual accounting in the public sector and invited the participants of the WCOA 2014 to “call [their] Minister of Finance now”, so that transparency and accountability in the public sector can be guaranteed.

thFinally she announced that the 20 World Conference of Accountants to take place in November 2018, will be held in Sydney, Australia.

4

1. ICAG NEWS TIT BITS

2.1 Proposal for establishing faculty and special interest groups within ICAG

The faculties and special interest groups will be specialist bodies within ICAG which will offer members' networking opportunities, inuence and recognition within clearly dened areas of technical expertise. As well as providing accurate and timely technical analysis, they will lead the way in many professional and wider business issues through stimulating debate, shaping policy and encouraging good practice.

The faculties will exist to enhance professional development of members. They will give you all the technical resources you need to carry out your role, as a member, to the highest standard, and stay ahead of the competition.

Benets of Faculty Membership· Access to a dedicated website with the

latest information plus a library of publications and guides.

· Magazines, e-bulletins and practical guides to keep you up-to-date with the latest developments and legislation.

· Nationwide events to help you stay in touch and share knowledge and experience with other members.

· H e l p w i t h y o u r p r o f e s s i o n a l development through CPDs.

· Create the chance to be heard. The faculties will dialogue, interact and respond to government and regulatory bodies on their policies and programs and inuence domestic and international policy and legislation.

· Te c h n i c a l u p d a t e s : p r o v i d e a comprehensive review of relevant pronouncements from accountancy bodies and other state institutions.

For example, the Financial Reporting faculty is the focus for chartered accountants working on nancial reporting. It will represent the Institute on nancial reporting matters, making representations to the government and other authorities, and public pronouncements on major nancial reporting issues. The faculties will be free stand alone bodies with their own constitution.

Six faculties that have been established are;

v Audit and Assurance

v Taxation and Fiscal Policy

v Financial Reporting

v Corporate Financial Management

v Public Financial Management

v Corporate Governance

v Audit and Assurancev Corporate Financev Financial Managementv Financial Reportingv Financial Servicesv Information Technologyv Tax

Apart from the faculties, ICAEW also has other special interest groups (SIG) which provide p r a c t i c a l s u p p o r t , i n f o r m a t i o n a n d representation for chartered accountants working within a range of industry sectors including:

v Charity and Voluntary sectorv Entertainment and Mediav Farming and Rural Businessv Forensic auditv Healthcarev Interim Managementv Non-Executive Directorsv Public Sector

ICAEW has similar faculties which are organized under:

5

v Solicitorsv Tourism and Hospitalityv Valuation

Members and students can register for faculty membership of any of the areas they have interest and expertise free of charge.

2.2 ICAG signs MoU to collaborate with the Accountant –General's Department

The Controller and Accountant-General's D e p a r t m e n t ( C A G D ) , h a s s i g n e d a Memorandum of Understanding (MoU) on behalf of the public sector institutions with the Institute of Chartered Accountants (Ghana) (ICAG), to promote efciency in accounting practice in the country. The MoU which expires

thon 30 September, 2019, ensures that the two institutions will work together to improve on the public accountability in the country.

Under the MoU, the two institutions would work towards the adoption and implementation of the International Public Sector Accounting Standards (IPSAS), identifying Public Financial Management (PFM) skills gaps within the accountancy profession, particularly in the public sector and develop a PFM centre of excellence, as well as measures including training to improve PFM skills of ICAG Members and other professional accountants working in the public sector, among other activities.

Ms. Grace Adzroe, Controller and Accountant- General, signed on behalf of the CAGD, whilst Professor Omane-Antwi, President of ICAG signed on behalf of the Institute. In her speech, Ms. Adzroe stressed that the MoU will reshape the implementation of programmes to improve public nancial management. She further indicated that the MoU will introduce best practices into the accountancy profession in the country.

The Accountant-General mentioned the fact that, CAGD and ICAG, including other agencies, have developed a road map towards the adoption of IPSAS and that with high political support, the adoption of IPSAS will enhance quality and transparent nancial reporting in the public sector. Ms Adzroe expressed the hope that the agreement will help build the capacity of staff of the various government agencies to address the skills gap in accountancy practice in the public sector.

The President of the Institute, Prof. Omane-Antwi stressed that, the institute agreed to collaborate with the CAGD to strengthen the capacity of public nancial management of the country. He emphasised that the institute supports all PFM reforms that would improve scal discipline in government's accountability and urged all professional accountants, especially those in the public sector to lend their support to the effort. Other distinguished personalities at the function which took place at the ICAG House, included Dr. Williams Atuilik, Prof. Adom Frimpong (both Council members), and the Chief Executive Ofcer of ICAG, Mr. Fred Moore.

2.3 Chartered accountants challenged to be professional

The President of the Institute of Chartered Accountants Ghana (ICAG), Professor Omane-Antwi, has challenged accountants to exhibit professionalism and uphold high integrity in the discharge of their duties. He made this remark at

rdthe institute's 23 graduation and admission

thceremony in Accra on the 18 of October 2014, where 262 students were graduated with certicates in the chartered accountants (CA) programme and 17 graduated with certicates in Accounting Technician Scheme for West Africa (ATSWA).

Professor Omane-Antwi who chaired the ceremony, urged the graduands to fully support ICAG by participating in the programmes to inculcate high ethical standards in the activities of accountants. .

6

He advised them to live up to their professional calling as professional accountants without any form of ethical breaches such as 'cooking' of books. He stressed that the graduands should uphold the tenets of integrity in the discharge of their profession as chartered accountants and should bear in mind that the reputation of a thousand years may be destroyed by the conduct of one act of dishonour. Professor Omane-Antwi was worried that Ghana is engulfed in an act of unprecedented spate of corruption in all aspects of the ceremony, adding that it would only take the integrity to check the act of corruption.

The guest speaker for the occasion, Mr. Ebo Whyte advised the graduands to be content with their earnings and not engage in any form of fraudulent activities. He stressed that they should be responsible accountants and take the right path of doing their work because Ghana needs them to transform the nation.

The ceremony saw the admission of 230 graduates into membership.

2.4 Public Sector adopts IPSAS

The Institute of Chartered Accountants (Ghana) in collaboration with the Controller and Accountant-General 's Department have launched the adoption of the International Public

thSector Accounting Standards (IPSAS) on 27 October 2014 at the Golden Tulip Hotel, Accra. The event which was attended by a cross-section of staff from the Controller and Accountant-General, Auditor-General department, Practise Society, ICAG, Ministry of Finance, media houses and other dignitaries, was sponsored by STAR-Ghana.

IPSAS is meant to serve the public interest by requiring the presentation and disclosure of nancial transactions in a comprehensive and consistent manner.

As part of efforts to transit into the new accounting regime, the CAGD constituted a commit tee on which ICAG was ful ly represented to draft an implementation document and draw up a road map in ensuring a smooth adoption and implementation by 2016. The Minister for Finance, Mr Seth Terkper, who launched the document said he would soon take it to Cabinet for approval.

The Minister emphasised that, considering

many reported cases of fraud, such as those

emerging from the Judgment Debt Commission

and the recent scandal at the National Service

Secretariat, there was the need to strengthen the

system of accounting in order to curtail these

malfeasances. He urged all professional bodies

to beef up their standards on costing and pricing

so as to enhance the accounting system.

The Controller and Accountant-General, Ms. Grace Adzroe, remarked that over the past 15 years, government with the support of its development partners, has undertaken reforms of its public sector nancial management s y s t e m s . O n e o f s u c h m o v e s i s t h e implementation of the Ghana Integrated Financial Management Information Systems (GIFMIS) which has greatly helped in nancial reporting and monitoring of costs and government expenditures. The move to adopt the IPSAS, according to the document, is based on the importance of high quality nancial reporting standards “in shaping the relevance, reliability and quality of the general purpose nancial statements.”

The President of the Institute, Professor Omane-Antwi in his speech stressed the commitment of the Institute in ensuring the successful adoption and implementation of the IPSAS. He indicated the preparedness of the Institute to play a leading role in the implementation through training and capacity-building of public sector accountants so that the implementation of the new accounting standard becomes a success.

7

2.5 ICAG Inaugurates the faculty system

The Institute of Chartered Accountants, Ghana has inaugurated the faculty system which will be thoperational in 2015. The inauguration which took place in the 24 of November 2014 at the Fiesta Royale

Hotel in Accra saw the outdooring of the deans and vice deans of the various faculties

The above-listed distinguished personalities were inducted to head the faculties.

8

FACULTY DEAN VICE DEAN

Audit and Assurance Mr. Ferdinand Gunn [Managing Partner, Ernst &Young]

Mr. Oseini Amui [Partner, PwC Chartered Accountants]

Corpora te F inanc ia l Management

Prof. E. Marfo Yiadom [ Dean, UCC Business School]

D r. J o e F r a n c e [ B a n k i n g Supervision Department, BOG]

Financial Reporting Nana Sackey [Managing Partner, Deloitte]

Mrs. Nana Abena Adu-Gyam [Partner, Pannell Kerr Forster]

Corporate Governance Nii Adumansa Baddoo [Board Chairman, IAA]

Mr. K.B. Andah [Managing Partner, Baker Tilly Andah and Andah]

Taxat ion and Fisca l Policy

Mr. Emmanuel Asiedu [Partner, KPMG]

M r . I s a a c N y a m e [ T a x Consultant]

Mrs. Roberta Quarshie [Assistant Auditor-General]

1

2

3

Public Financial Management

Mr. Michael Gyam [Deputy Controller and Accountant-General]

4

5

6

3. FEATURES3.1 The Changing Landscape of Educational Standards in the Accountancy Profession

NDDr. Musa Inuwa Fodio,CAN presented at the 2

African Congress of Accountants (ACOA), May

14-16, 2013 held at Accra International

Conference Centre, Accra, Ghana.

BACKGROUND

The accounting profession has never in its

history been confronted with the kinds of

challenges that it faces today. Some of the

challenges include:

The profession's reactions to the challenges led to radical innovations in the principles, standards and practice of accounting. These challenges and responses have widened the gap in accounting education – What accountants do and what accounting educators do. Public accounting rms recognised the problem over 20 years ago. Consistent with Bedford Report, a white paper issued by the big 8 audit rms in 1989 described the profession as }�Expanding }�Changing }�Becoming increasingly complex.

} Unending sensational accounting scandals

} Loss of public condence

} Loss of authority as self-regulating profession

The paper stressed that accountants are no longer mere information providers/nancial advisers but executive partners, and further suggested that the critical need for the profession is to re-examine its educational processes. The paper concluded that the “current environment” makes rea l curr iculum change essent ia l and necessitates a dynamic partnership between practitioners and academics. In late 1980s and early 1990s, IMA received complaints from nancial executives indicating that entry-level accountants were inadequately prepared and

lack skills necessary for success as entry corporate accountants. The IAESB has since its coming into being, been building on the work of IASCF. The foundation in 2002 identied some areas of change which included education standards and regulations. The overall mission of IAESB is to serve the public interest by the world w i d e a d v a n c e m e n t o f e d u c a t i o n a n d development for professional accountants leading to harmonised standards. Current trend is towards globalisation of educational standards for accounting profession.

DRIVERS OF CHANGE IN GLOBAL E D U C AT I O N A L S TA N D A R D S F O R ACCOUNTING PROFESSION

Unrelenting competitive pressure: - Rapid change has been the characteristic of the environment in which professional accountants work. Pressures for change are coming from expanded stakeholders including regulators and oversight bodies.

Impact of information and communication technologies: - ICT continues to advance at a rapid pace; Internet has revolutionised global communications; XBRL is an off-shoot of ICT development.

Demand for improvements in corporate governance and ethics; and growing concern for the environment and sustainable development

Globalisation of Business: - Business and organisations are engaging in ever more complex arrangements and transactions. Risk management has become more important

Focus on fair value accounting: - Fair value becomes the conceptual foundation of nancial reporting and valuation techniques are basic tools of accountants (which involves modelling)

Demand for new knowledge and skills: - Accountant to be a “Jack of all trade and a mini-master of all”; ICT, Managerial, Actuarial valuation etc as part of the challenges associated with IFRS. Judgement is now more important as well as reliance on conceptual framework.

9

Less reliance on memorization of rules and more focus on application of principles and use of best judgement

I M P L I C AT I O N S O F C H A N G E S I N EDUCATIONAL STANDARDS FOR THE ACCOUNTANCY PROFESSION

} Recognition of changes in educational standards for the Accounting profession

} Recognition by the profession that its only Real Capital is its Human Capital. Need for investment in human capital

} The need to change nationally-based accounting education systems to reect global dimension. Through collaborative efforts with academics, practitioners, government and regulatory agencies, industries, etc.

} Future accounting practitioners must have broad and specialized knowledge and skills

} A c c o u n t i n g p r a c t i t i o n e r s m u s t continually acquire new knowledge and skills (life-long learning) because of the rapidly changing environment in which the professional accountant works; i.e. IFRSs, IPSASs, ISAs, XBRL, IES, etc

} Future professional accountants need training in corporate governance, environment and sustainable reporting and ethics

} Need for continuous monitoring of the environment in which professional accountants operate to ensure that the educational process remains relevant

} N e e d f o r e d u c a t o r s d e l i v e r i n g professional accounting education program to respond to the changing needs of international accounting profession as we l l a s ind iv idua l p ro fess iona l accountants

T H E R O L E O F I N T E R N AT I O N A L ACCOUNTING EDUCATION STANDARDS BOARD (IAESB) IN SETTING STANDARDS FOR GLOBAL ACCOUNTING EDUCATION

The increased role of IAESB in developing and issuing high quality standards and other guidance to strengthen accounting education worldwide. IAESB focuses on: prequalication accounting education; practical experience and training as well as assessment of professional accountants; and continuing (post-qualication) professional education needed by accountants. All IFAC members were required to comply with IES 1-6 by January 2005, IES 7 by January 2006 and IES 8 by July 2008. Compliance (with black letter requirements) is self-enforced by professional bodies in collaboration with and involvement of national oversight as well as th i rd par t ies- univers i t ies , employers (government and private).

IES AND THE ACADEMICS

The International Association of Accounting Educators and Researchers (IAAER) is championing the course for design and implementation of accounting education program that achieves the IES objectives of prequalication education. IAAER is also creating awareness of the need for improvement in accounting education and research. IAAER proposes a Project Athena on IES targeted at faculty development program in developed and emerging economies. At various national levels academy and profession have perennially failed to settle on agreed core of accounting knowledge.

THE ROLE OF PROFESSIONAL BODIES IN PROMOTING IES

IFAC member bodies are expected to comply with IES. IES are targeted at the member bodies and not individual members. Member bodies are to determine detailed requirements of the pre-q u a l i c a t i o n , p o s t - q u a l i c a t i o n a n d development programs considering the diversity of culture, language and educational, legal and social systems in their countries, where member bodies are subject to legal or regulatory

10

authorities in their countries, they must consider IES and must advise legislative and regulatory authorities on same and seek for harmonization. Member bodies should assist the growing movement toward international reciprocity and comparability of qualications through IES. Member bodies are to work with other educators and academics to ensure that programs are relevant and logically sequential.

And skills (what exactly is a “work ready”

accounting graduate?) Accounting academics

generally feel that they are the arm of academia

that studies accounting rather than the academic

arm of the accounting profession.

Dilemma on what student of accounting in the

university or college should learn (emphasis),

K n o w l e d g e v o c a t i o n a l i s a t i o n

(commercialisation) which lend itself to

demands of the work place, Knowledge

commodication- which arises out of the

marketisation of courses (revenue drive),

Knowledge corporatisation- which focuses on

performance measurement and learning

outcomes. Knowledge professionalization-

which focuses on professional practice.

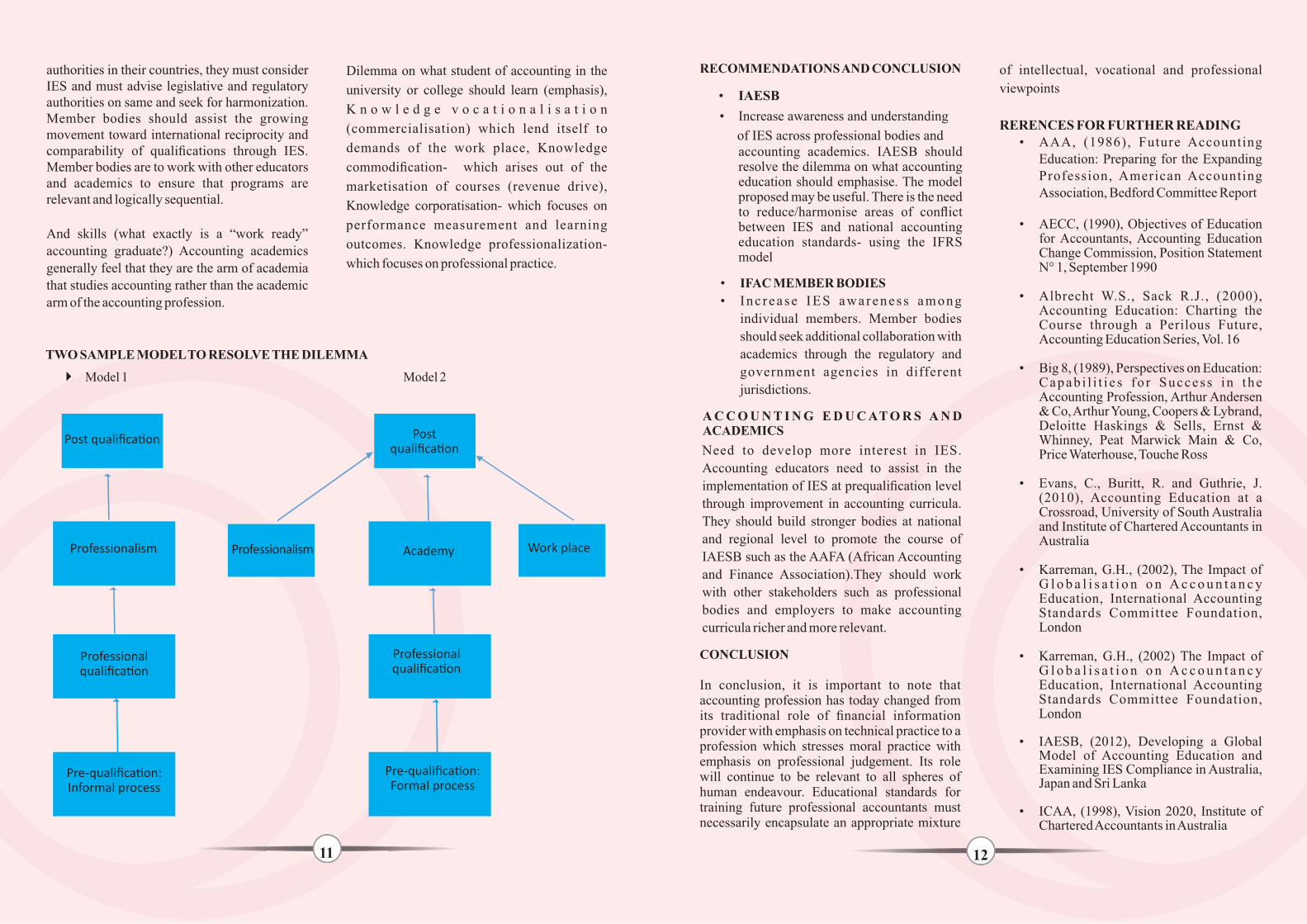

TWO SAMPLE MODEL TO RESOLVE THE DILEMMA

} Model 1� � � Model 2

Post qualifica�on

Professionalism

Professional qualifica�on

Pre-qualifica�on:Informal process

Professionalism

Post qualifica�on

Academy

Professional qualifica�on

Pre-qualifica�on:Formal process

Work place

11

RECOMMENDATIONS AND CONCLUSION

• IAESB

• Increase awareness and understanding

accounting academics. IAESB should

resolve the dilemma on what accounting education should emphasise. The model proposed may be useful. There is the need to reduce/harmonise areas of conict between IES and national accounting education standards- using the IFRS model

• IFAC MEMBER BODIES

• Inc rease IES awareness among

individual members. Member bodies

should seek additional collaboration with

academics through the regulatory and

government agencies in different

jurisdictions.

A C C O U N T I N G E D U C AT O R S A N D ACADEMICS

Need to develop more interest in IES.

Accounting educators need to assist in the

implementation of IES at prequalication level

through improvement in accounting curricula.

They should build stronger bodies at national

and regional level to promote the course of

IAESB such as the AAFA (African Accounting

and Finance Association).They should work

with other stakeholders such as professional

bodies and employers to make accounting

curricula richer and more relevant.

CONCLUSION

In conclusion, it is important to note that accounting profession has today changed from its traditional role of nancial information provider with emphasis on technical practice to a profession which stresses moral practice with emphasis on professional judgement. Its role will continue to be relevant to all spheres of human endeavour. Educational standards for training future professional accountants must necessarily encapsulate an appropriate mixture

of intellectual, vocational and professional

viewpoints

RERENCES FOR FURTHER READING• AAA, (1986), Future Accounting

Education: Preparing for the Expanding Profession, American Accounting Association, Bedford Committee Report

• AECC, (1990), Objectives of Education for Accountants, Accounting Education Change Commission, Position Statement N° 1, September 1990

• Albrecht W.S., Sack R.J., (2000), Accounting Education: Charting the Course through a Perilous Future, Accounting Education Series, Vol. 16

• Big 8, (1989), Perspectives on Education: Capab i l i t i e s fo r Success in the Accounting Profession, Arthur Andersen & Co, Arthur Young, Coopers & Lybrand, Deloitte Haskings & Sells, Ernst & Whinney, Peat Marwick Main & Co, Price Waterhouse, Touche Ross

• Evans, C., Buritt, R. and Guthrie, J. (2010), Accounting Education at a Crossroad, University of South Australia and Institute of Chartered Accountants in Australia

• Karreman, G.H., (2002), The Impact of G l o b a l i s a t i o n o n A c c o u n t a n c y Education, International Accounting Standards Committee Foundation, London

• Karreman, G.H., (2002) The Impact of G l o b a l i s a t i o n o n A c c o u n t a n c y Education, International Accounting Standards Committee Foundation, London

• IAESB, (2012), Developing a Global Model of Accounting Education and Examining IES Compliance in Australia, Japan and Sri Lanka

• ICAA, (1998), Vision 2020, Institute of Chartered Accountants in Australia

12

of IES across professional bodies and

• IFAC, (2006), SMO 2, International Education Standards for Professional Accountants and Other Guidance

• IFAC, (2007), International Accounting Education Standards Board, Strategic and Operational Plan 2007 – 2009

• IFAC, (2007), Developing Nations Committee, Strategic and Operational Plan 2007 – 2010

• I FA C , ( 2 0 0 7 ) , M e m b e r B o d y Compliance Program, Strategic and Operational Plan 2007 – 2010

• IFAC, (2003), IES 1, Entry Requirements to a Program of Professional Accounting Education

• IFAC, (2003), IES 2, Content of Professional Accounting Education Programs

• IFAC, (2003), IES 3, Professional Skills

• IFAC, (2003), IES 4, Professional Values, Ethics and Attitudes

• IFAC, (2003) , IES 5 , P rac t i ca l Experience Requirements

• IFAC, (2003), IES 6, Assessment of P r o f e s s i o n a l C a p a b i l i t i e s a n d Competence

• IFAC, (2004), IES 7, Continuing Professional Development: A Program of Lifelong Learning and Continuing D e v e l o p m e n t o f P r o f e s s i o n a l Competence

• IFAC, (2006), IES 8, Competence Requirements for Audit Professionals (Implementation 2008)

• Needles, B.E. Jr., (2005), Implementing International Education Standards: The G l o b a l C h a l l e n g e , A c c o u n t i n g Education: An International Journal, 14, March, 2005, 123-129

rd• The 103 American Assembly (2003), The Future of the Accounting Profession, the American Assembly, Columbia University

3.2 Strengthening Financial Markets and Institutions in AfricaBy Victor OgiemwonyiC.E.O/MDPartnership investment company plc“Africa doesn't need strongmen, it needs strong institutions.” – Barack Obama “The above quote by US president, Barack Obama during his address to the Ghanaian Parliament in 2009 underscores the need for strong institutions to regulate every sphere of our lives in Africa.”

To strengthen anything is to make it more stable, or sturdier than it presently is. It is the action taken to ensure that it will largely retain its form and integrity (i.e. its utility or tness for purpose) in the face of testing or challenging forces of any kind. In the context of nancial systems (the markets and the institutions together), strengthening will therefore imply a need to reduce nancial fragility and minimise systemic risks through the development of optimally functioning systems and market discipline – majorly by promoting sound principles and best practices.

At the multi-economy bloc level (like Africa), attaining stability will necessarily also have to include integration of the constituent economies' nancial systems. The ongoing trend in globalisation adds yet another layer of integration and, one must add, complexity, since Africa doesn't trade in isolation from the rest of the world.The absence of stability in a nancial system inevitably leads to nancial crises which themselves are usually heralded by an asset price bubble. While stable nancial systems do not banish bubbles per se, experiences from other nations and other economic blocs indicate that nancial institutions could and should be doing more to recognise and deter bubbles.How we proceed in our task of strengthening

13

Africa's nancial systems in the next few years has now become critically important if the economies of the African bloc, individually and collectively, are to be in a position to capture and enjoy the rosy range of GDP growth numbers being forecasted by the World Bank and other respected global economic institutions.

At the domestic/national level, in proffering practical solutions we are minded to partition the challenge into four distinct focus areas, namely:

§�Deepening our nancial markets ��§ Broadening our range of nancial instruments ��§ Improving our operational efciencies and ��§ Strengthening our nancial sector governance

The collective level also compels us to focus on a fth area: §�Deepening our nancial integration.

��§ Deepening Our Financial Markets

In its broadest sense, the depth of a nancial market refers to the quantities of the securities available for trading in

§ The market. In any market, it is i m p o r t a n t t h a t d e m a n d - s u p p l y equilibrium is attained at reasonably optimal volume levels, lest scarcity-driven articial upward price pressures begin to take hold. In the Nigerian context, whilst depth might not be an issue in the government bond markets, it is an entirely different story in the relatively larger but largely untradeable stock market.

§ The growth that has taken place on the funding side, particularly with the consolidation and restructuring of the pension funds industry, has not been matched by a concomitant expansion of market liquidity. Indeed, with the possible exception of South Africa, market depth is a signicant challenge in most African nancial markets.

§ Prescribing relatively high oat rates - the proportion of a listed business's issued nancial instrument mandatorily made available for trading - will be a good way to begin the deepening process.

§ The recent introduction, in Nigeria, of well-funded market makers willing and able to act as counterparties to trades is another step in the right direction. Increasing activity levels should be expected to translate into decreasing transaction costs which in turn will attract more activity in an expanding prosperity loop.

Any growth on the funding side of the equation, whether as a result of increased internal allocations or because of external inows, which is not matched by a comparable increment in absorption capacity on the asset side will, ultimately, result in price ination, aka price bubble! A classic case of “too much money chasing too few goods”.

§

§ The Nigerian stock market boom-bust experience over the period 2007 to 2010 is a ready attestation to this surprisingly common phenomenon.

�§ Broadening our range of nancial

instruments

§ Simply put, nancial markets exist to allocate and manage risks, and there's no better weapon in the risk management arsenal than diversication. To broaden our markets is to expand the range of diversication opportunities available to investors; success at doing this will obviously manifest in an increased market size.

§ We propose a two-phase approach to broadening the market and this must necessarily be hitched to the individual national economic growth engines. There's no point trying to sprint before learning to walk; such an approach will avoid a one-size-ts-all solution.

1414

§ In the rst phase we should focus on creating or expanding the number of tradable instruments available under the basic asset types – equities, bonds (sovereign and corporate) as well as commodities (minerals and agro-related). Thousand-stock markets should be our rallying cry!

§ An immediate proactive approach to implementing this phase in tandem with the predicted GDP growth of the next few years should make it easier to attain in a shorter time frame than would otherwise be expected in a at-l i n i n g o r s l u g g i s h g r o w t h environment. Our SMEs are ready and waiting to be taken to the next level.

§ With a broadened and already deepened market, it becomes easier to implement the second phase – creating a vibrant and economically useful derivatives market to further enrich and strengthen the risk management milieu. This is the point at which we will recommend the introduction of derivative products like futures (and CFDs), options, and swaps as well as securitisation products.

§ Prudence dictates that a robust derivatives market cannot and should not be built on an anaemic underlying assets market.

§ Firstly building a broad and deep market of valuable underlying securities and asset classes is an unavo idab l e p r e r equ i s i t e f o r establishing a successful derivatives market. Absent broadened and deepened nancial markets, and the national and continental African growth stories may likely come to a premature termination, if not reversal.

Boosting efciencies will need to be tackled from three perspectives or initiatives: § Improvement in the quality and

institutional competence levels of

operating rms as well as a properly

registered and continually trained and

motivated professional cadre.

frictionless and inexpensive.

All three aspects must be deemed equally important if we are to develop the capacity and sophistication that will be needed to support the realisation of Africa's immense potential in both the short and long runs.

Strengthening our nancial sector governanceGovernance encapsulates “the range of institutions and practices by which authority is exercised” and in the present context refers to the mechanisms we already have in place as well as those that will be needed for tomorrow. There can be no strong nancial system without strong enforcement.

In Africa, more often than not, problems arise not because of the lack of rules, but as a result of poor, indifferent or selective enforcement. The failure of regulation (local and international) to predict the global nancial crisis and the gross underestimation of its severity compel us to rethink our regulatory thrust: proactive regulation with the primary aim of preventing systemic crises. Such a refocused regulatory framework will need to be based on a set of simple goal-driven criteria that are enforced on a timely basis.

At the same time, it will need to be dynamic in its ability to adapt to a uid environment where change is the norm rather than the exception. Sincerity of purpose, transparency of action and consistency of application are the obvious prerequisites for this kind of regulation.

15

§ Sensible acquisition and/or development

of locally-sensitive cost-effective enabling technologies and platforms .

§�Institution of transparent t-for-purpose

processes that make transaction execution

§ Improving our operational efciencies It is also critical that the quality and quantity of available information be greatly improved.

Ultimately, governance is much more than enacting rules, approving legislation, publishing standards and establishing new institutions. Meaningful and lasting nancial reform can only come from behavioural change and this is only achievable by the introduction of incentives capable of inducing appropriate behaviour. This approach will necessitate creating a system of rewards and penalties that are perceived by market participants as being in their own best (self) interests.

Deepening our nancial integration and cooperation

The recurrence of global nancial crises with alarming regularity tells us that new and better coordinated frameworks are needed for the regulation of nancial systems.

It has now become obvious that while the benets of globalisation are undeniably immense, they denitely do come with attachments that are also not ignorable. Countries that have climbed aboard the globalisation train (i.e. “liberalised their economies”) without rst resolving economic infrastructural weaknesses on the home front were often visited by severe economic disruptions, widespread social upheavals and often t imes poli t ical leadership collapse.

In addition to weak domestic nancial systems, the non-availability of complete, adequate and timely information to assist investors undertake viable assessments of an economy's capacity to absorb external shocks as well as its general nancial soundness often leads to contagion – the negative perception/assessment based on a similarity i n d e x l i k e g e o g r a p h i c a l l o c a t i o n (“neighbourhood effect”) or some other political economic indicator.

Summarily, and in conclusion, to promote nancial stability within the African bloc, we must focus simultaneously on strengthening our individual domestic markets as well as improving our intra-African and extra-African frameworks.

Proposition��§ Clear rules should be put in place and everyone involved should be asked for an

opinion and a consensus agreed and

published as rules for everyone. One will

know how it will be operated if there were

any crisis. This is important to slow

down the pace of contagion when

markets start to correct irrationally.

��§ The Central Banks (CBs) should ensure

that all relevant nancial institutions; not

just commercial banks, should have

access to liquidity against a broad range

of eligible assets.

ü�Bagehot's Rule: In times of crisis,

Central Banks (CBs) should lend

freely but against collateral & at a

penalty rate, to avoid moral

hazards.

§ Financial Intermediaries should focus more on risk management; placing more emphasis on the liquidity risk.

3.3 Fighting Corruption in Public Institutions: The Role of the Internal Auditor.

By Paul Kwame Awuah

Corruption is a complex social phenomenon,

which has become rooted in all facet of society in

the world especially in the developing world. For

so many years, the issue of corruption has caused

severe damage in public institutions in Ghana

resulting in serious nancial loss to the state,

damage to organisational performance and loss

of credibility. It has seriously eroded public

16

condence and undermines the legitimacy of the spending of taxpayers' money by public institutions.

Fighting corruption in Ghana has not been easy for some time now mostly due to lack of political will to ght this social canker. However, it has been suggested that the surest way of ghting corruption in our public institutions is the practice of sound corporate governance system and one of the key corporate mechanism necessary to ght corruption is the internal audit units. This has become necessary due to the relevance of the agency theory in the public sector. In both private and the public sector, the providers of the economic resources are separate from the management of the organisations. The owners require the management to use the resources provided judiciously for the benet of the owners.This is normally referred to as the Agency theory or the agent/principal relationship. In the private sector the managers of the companies are the agents and the shareholders (owners) the principal. In the public sector, the citizens are the principal and government ofcials are the agents. In practice the principal delegates the day- to – day decision

•

making of the organisation to the managers who are agents to the owners.

The problem that normally arises from this relationship is that in most cases the decisions taken by the agents are not in the interest of the principal but rather to the advantage of their own selsh interest. In most public institutions in Ghana, Directors, chief executives, politicians and other key public ofcials in responsible positions mostly pursue their own personal objectives like payment of fat sitting allowances, collection of kickbacks, , frequent travels etc.,. These corrupt practices in our public institutions are some of the reasons why most Ghana ians a r e f ac ing economic h a r d s h i p s . T h i s a s s e r t i o n w a s collaborated in a recent report by the transparency international when they reported that in some countries especially in the developing world poor families have to pay bribes before they can seek medical attention from government hospitals. The report went on to say that corruption by politicians and some public sector workers has led to the failure in the delivery of basic services like good education, adequate and affordable electricity supply and proper healthcare.

• An important question that comes into

mind is that how can the citizens who pays tax for the development of the nation exercise control over politician and other government ofcials who are supposed to ensure that monies collected from and on behalf of the citizenry are put into good use? What effective mechanisms can be put in place to ensure that government ofcials periodically properly account for their stewardship to the citizens?

• Theoretically, Ghana can boast of a lot of legislations which have been put in place to ensure that funds assigned to various government institutions are judiciously used for the benet of the people. The nancial Administration Act, 2003 (ACT

•

17

• In Ghana, corruption has become prominent in public institutions due to factors like wide discretionary powers of s t a t e f u n c t i o n a r i e s , m i n i m a l accountability, weak punitive mechanism f o r c o r r u p t b e h a v i o u r , l a c k o f t r ansparency, low sa l a r i e s to government employees and absence of incentives for honesty and integrity. According to anti-corruption watchdog's 2 0 1 3 G l o b a l C o r r u p t i o n barometer(GCB) report in July, 2013, 54% of the 2000 respondents in Ghana reported that corruption has increased in the past two years (2011 to 2013) .According to the report Ghana police service top the list of the most corrupt institution in the Ghana followed by political parties.

654), The Financial Administration Regulations, 2004(L.I. 1802), The public Procurement Act, 2003(ACT 663), The Internal Audit Agency ACT, 2003(ACT, 658) are examples of such regulations which have been enacted to ensure nancial discipline in our public institutions but the biggest problem is how to ensure compliance of the provisions in these regulations. Brieng the press on the outcome of a self-assessment process under the United Nations Convention Against Corruption (UNCAC) l a s t yea r, a depu ty commissioner of human rights and administrative justice (CHRAJ) in charge of Anti-corruption and Public Education Mr. Richard Quayson conceded that in terms of legislation Ghana is doing well in ghting corruption but we are weak when it comes to the practical implementation of these regulations.

• In addition to the legislations there are other mechanisms that are being used in ghting corruption in public institutions. One of such mechanisms is the establishment of internal audit units in various government institutions. Internal audit represent a key indispensable corporate governance checks and balances that if well functioned can help to monitor nancial activities in government insti tutions. A well-functioned internal audit unit can play a vital role in the governance and accountability process in the public sector through their assessment of the effectiveness of key organisational controls as risk management processes. They are also responsible for the strengthening of public sector internal controls systems to ensure that public sector ofcials conduct activities fairly, transparency and honesty. In every organisation especially in the public sector, the internal auditor plays a crucial role in ghting corruption because they have the best access to detail information on nancial transactions, procurement procedures and the use of funding.

For the past ten years internal auditing have received massive recognition in the nanc ia l management p rocess in government institutions especially with the enactment of the internal audit agency act in 2003(Act 658). The Act was enacted as part of efforts to strengthen the internal controls in public institutions to ensure effectiveness and efciency in the use of government resources and to minimise corruption.

The Internal Audit Agency Act gave birth to the Internal Audit Agency, a central body mandated to coordinate, facilitate and provide quality assurance within the public sector and to operate as an oversight body. The agency since its establishment has ensured that all public sector institutions have a well-established internal audit units. The agency within its powers has put all the necessary measures in place including the provision of auditing standards and the periodic workshops for all internal auditors to ensure that internal auditors in public institutions function effectively as a key public sector corporate governance mechanism.

The question that will once again come into mind is why is it that corruption is still rife in our public institutions despite the rejuvenation of internal audit units in our public institutions? The issue with independence has been one of the reasons why internal auditors have not been effective in protecting government resources. There is a perception that internal auditors in our public institutions are not independent because of the powerful nature of senior public servants to w h o m t h e y r e p o r t . T h i s l a c k o f independence has affected the objectivity of most internal auditors in public institutions. The integrity of some internal auditors is also questionable. It is believed that some internal auditors are also engaged in corrupt practices in public institutions. Some internal auditors are found chasing suppliers to pay kickbacks to them before

•

•

18

approving their invoices for payment. Political interference is another reason why in te rna l audi tors in publ ic institutions cannot function effectively.It is believed that some internal auditors have been strategically be put in some institutions where they can easily be manipulated and there are also situations whereby some internal auditors succumb to political pressure for fear of losing their jobs.

• Notwithstanding the above problems with internal audit units in the public sector, the unit remains one of the key corporate governance mechanisms if well properly structured can help ght corruption in our public institutions, which is increasing at an alarming frequency. The issue with independence should be a source of concern to the internal Audit Agency. I am therefore calling for the immediate amendment to the Internal Audit Agency Act to ensure that auditors in the public institutions report directly to the Agency and not to the politicians and heads of institutions. This will help improve the independence and objectivity of internal auditors. The attraction and retention of competent internal audit also remains one of the serious challenges in the public sector. The inability to attract and retain c o m p e t e n t p r o f e s s i o n a l s i s a contributing factor to the failure of internal audit units to ght corruption in the public sector.

The internal auditor is a respectful and honourable position reserve for men and women with integrity and not for people with questionable characters. Anybody who is appointed as an internal auditor in a n y p u b l i c i n s t i t u t i o n h a s t h e responsibility to maintain a good ethical standard of himself and his authority as a good example to ensure adherence to rules and regula t ions , procedures and recommended acceptable practices. The modern internal auditor should therefore be fully prepared to adhere to the principles of integrity, condentiality, objectivity, and competency and above

3.4 Are you playing defence as a leader?In sporting teams we hear about the importance of the “defence” to win games, however this is one factor that has no place in the business and leadership environment. The idea of defence is to prevent a threat from breaking the line and making ground against an opposition. Therefore if you are a defensive leader then you must be presenting yourself as an opposition to the workplace rather than a team member. A leader that becomes defensive and tries to block his or her employees from making ground is in fact the same as your teammate tackling you just before you score a try. How would you react to seeing a fellow teammate act in this way on a sporting eld?

· Everyone else in the team would alienate

you

· People will avoid you

· No one would trust you

· No respect

· You have broken ethical and moral

obligations

· You are full of self interest and

importance

· You care only for yourself and your own

game, not the results of the team

What happens then when this is present in the business environment?

If you are a leader and are creating a defensive team you are effectively stopping the team from performing at all. The result of treating others within the workplace as a threat creates a culture of negativity and loss of forward momentum. As a leader your job is to lead them, play to their strengths and ensure that each person has a clear understanding of their role and position. As a leader you encourage brilliance and the ability of individuals to produce inspiring results and reward them for doing so.

19

all be able to detect and report issues on corruption without fear or favour.

The best example of the defensive environment is use of the term “Think outside the box”. In reference to the term “threat”, if you are threatened by the performance of a team member you are not t to lead. Experience has shown that those that act to block threats ultimately are left without a team to lead and in turn make their job more difcult by a multiple of ten. Leading the individuals to shine is the ultimate form of leadership and as such you have to lead a team to victory. The accolades are not taken from the leader for the outstanding performance of those around them. As a leader you should be embracing the idea of creativity and thinking at all times. The human brain is forever thinking and wanting to create, it is its nature to do so, as such you should be continually embracing it and enabling your team to perform to their strength and produce the results they are capable of.

Telling traits of a defensive business environment:

Ÿ Lack of input by employees

Ÿ Lack of communication

Ÿ Negative behaviors and emotional state

Ÿ Poor staff retention

Ÿ Lack of enthusiasm

Ÿ Lack of respect for the business

Ÿ Lack of respect for others

Ÿ Poor workplace culture

These are just some of the key traits that are present in the business environment that have a dramatic effect on the overall position of the business and ultimately its success. As leaders you have an obligation to those around you as well as the obligation to the business, the moment that your own self-interest takes precedent over the environment in which you lead is the moment the walls will fall down around you.

It is not an impossible task to run around; you can change the direction of the workplace and create a team with a powerful culture. It will take some work and some restructuring, but it is possible. More importantly, the result of turning around

How can you improve your leadership?

Nothing is ever beyond repair; a great leader never gives up on his team. Do whatever it takes and never be afraid to ask for help, nobody has all the answers, even as a leader.

An effective leader is someone who can build trust, makes decisions, and takes decisive actions towards achieving goals and objectives. Effective leadership is all about balance – it is about understanding the different styles of leadership, how to use the various leadership styles and most importantly, when to use them. Leadership failures are commonly due to the inability and the failure to understand one's default leadership style and how it affects others around you, and not knowing how and when to apply the various leadership styles to obtain the results that you want. Effective leadership is about knowing when to be nice and when to be demanding. It is about understanding when to give and when to take. It is about knowing when to coach and when to be directive. It is about knowing when to be democratic and when to be authoritative.

20

and creating this positive leadership will be more rewarding and prosperous than you ever managed, not just for you but also for your entire team.

Ÿ Open communication and feedback at any time

Ÿ Regular input sessions as a teamŸ Find individual's strengths and develop

themŸ Find individual's weaknesses and develop

themŸ Have everyone understand each other's'

roles and positionsŸ Encourage individuals to pursue an ideaŸ Give constructive feedback on thoughts

presented (never ignore them)

Ÿ Never take credit for someone else's ideaŸ Never put down an idea, especially in

front of othersŸ Be true to your word.

It is about understanding when to set the pace

and when to allow your people to run their own

race.

Leadership is also about awareness. A leader

cannot be effective being nice all of the time.

Neither can a leader be effective by being

coercive and demanding all of the time. An

effective leader is one who is not only socially

aware, but also emotionally aware.Being

socially and emotionally aware will enable the

leader to effectively read the social situation and

understand the political, emotional and social

undercurrents. This will enable the leader to

know what leadership styles to apply, when to

apply those styles and how best to apply the

various leadership styles within different social,

emotional and political contexts.

Leadership is about individual personality. An

effective leader must also be able to understand

the personality make-up of their individual team

members because each individual is different

and each will respond and react differently to

different stimuli and motivation.

Understanding the basic personality make-up of each team member will enable the leader to understand how best to engage each individual and know exactly what motivates each person and what drives each individual.

Effective leadership is about the right people. Effective leadership is about having the right people on-board the team. With the right people on-board the team, a leader can only become even more effective. Having the right people in terms of cultural t, aptitude, personality, skills, qualications and experience will help put the team on the right track and enable the team to stay the course and reach for the stars.

If you are wondering why your team is not performing to expectations and you wish to know how to lead your team to higher performance, perhaps you should begin by identifying your own leadership styles. Your leadership styles drives the way you communicate with your team, and that in turn determines how your team members perceive your message and how they respond back to you. Ultimately, it is your leadership style that determines the end results that you get.

21

4 . T E C H N O L O G Y CORNER4.1 Six Ways to Use Social Media Adverts (Ads) to Grow Your Business

Back in 2011, social media users began to see a mysterious new breed of messages show up in their Twitter feeds: paid ads dressed up to look just like regular Tweets. Fast forward three years, and these Promoted Tweets – along with Facebook ads and similar offerings on other social networks – are ofcially one of the fastest growing sectors of online advertising. And while user opinions of native social ads may vary from indifference to annoyance, the results seem to speak for themselves.

Facebook native ads that appear in users' news feeds are clicked on 49 times more often than traditional banner ads in the right sidebar, according to AdRoll. Promoted Tweets have shown engagement rates of 1-3 percent – exceptional considering that normal banner ads are clicked on just.2 percent of the time.

For businesses, native ads offer additional advantages, like ne-tuned targeting, analytics and cost effectiveness when compared to traditional marketing campaigns. The following six tips should be helpful for marketers considering a foray into the world of native social advertising.

1. Use free social media to beta-test your paid social adsIf your company is on social media, you are likely already sending out multiple Tweets, Facebook Posts and LinkedIn Updates every day. Some of these messages will resonate with followers; others will not. Using free analytical tools it is easy to track which ones are being clicked, shared and commented on.

It is precisely these high-performing messages

that make great candidates for native social ads.

You already know they “work”, taking the

guesswork out of the creative process. All you

are doing is taking a tried and true message and

paying to put it in front of a newer, larger

audience.

2. Take advantage of targeting featuresOne of the major rubs with traditional ads is inefciency. For example every time a die-hard Prius owner which runs on electricity sees adverts for a fuel-guzzling SUV, for example, it represents a major waste of resources. Social ads minimize this type of spillage. On LinkedIn, Sponsored Updates can be targeted to particular regions (countries, cities, etc) and industries, as well as to specic job titles and even particular companies. Twitter allows advertisers to drill down based on region, gender, device and literally hundreds of different interest categories. Messages can even be aimed at specic brands and their respective followers, enabling businesses to go directly after the competition and its client base.

Meanwhile, Facebook's Sponsored Posts can be blasted out to a nearly endless list of interest groups. Facebook can even go after “lookalike audiences”, i.e users who have already expressed interest in products similar to yours.

3. Rotate ads frequentlyWith TV commercials and other traditional “interruption ads” repetition is the name of the game. But Promoted Tweets and Sponsored Posts appear right in users' news feeds. Not only are engagement rates bound to plummet if you hammer users on their home turf with repetitive messaging, but you may end up losing more business than you gain. The remedy here is fresh, ever-changing ad content. Because tweets and posts are generally short and sweet, this is hardly a heavy burden. At the same time, social ads can be used by targeting them to multiple demographics. Rotating the same message through a series of different, highly targeted groups, in fact, is of the easiest ways to extend the life and utility of native social ads.

22

One of the great virtues of native social ads is instant feedback. Minutes after sending out a Promoted Tweet or Sponsored Post, for example, it is possible to gauge its effectiveness. Detailed analytics reports and charts show who is clicking and how often. Before doubling down on a single social ad, we have found it effective to send out several “test” ads to small audiences and wait to see the results. For minimal spend, we get a clear, data-driven picture of which ad performs best. Then we will back the winning message with additional spending to ensure it reaches the largest audience. This will depend on the product or service that is being advertised. Different ads will get better impressions at different times.

4. Use small samples to test your social ads

5. Understand how ads are sold

Different networks sell ads in different ways. On Twitter, companies pay on an engagement basis. Every time users take an “action” – click, retweet, favorite, etc – a fee is assessed. Meanwhile, Facebook and LinkedIn offer the option of paying per impression, while companies are charged whenever their ad shows up in user's streams (regardless of whether or not it is clicked on). With Twitter, make sure the engagement you want is the engagement you are getting. Twitter counts all RTs, URL clicks as well as clicks on ANY @, # or image in the tweet as an engagement. You pay each time any of those occur. If your goal is to drive visits to a specic web URL avoid including too many @ handles or #s since you pay each time someone clicks on those and you will burn through your budget in no time.

Though the difference may seem academic, it is critical to bear these two pricing models in mind and to design Tweets and Posts accordingly. For example, since we pay Twitter each time users click on our ads, it is important that people be genuinely interested in the content waiting on the other side. This requires drafting Tweets that are clear and straightforward – in essence, the opposite of “link bait”. The goal here is to drive genuine prospects to our site, not merely to attract as many eyeballs as possible.

6. Design your ads with smartphones in mind

Social media is consumed overwhelmingly on mobile devices. Twitter users spend 86 percent of their time on the service on mobile. Facebook users are not far behind at 68 percent. This means most native social ads are being viewed on mobile devices, as well. And this comes with certain benets and caveats. First, messages have to be optimized for viewing on small mobile screens. For Promoted Tweets, this is hardly a challenge, given the 140-character limit. For Facebook's Sponsored Posts, this requires keeping messages short and sweet and ideally, imaged-based.

But the fact that native social ads viewed on a device people carry around with them at all times also opens up unique marketing possibilities. Twitter recently unveiled a feature enabling paid Tweets to be targeted by zip code. Users walk into a neighborhood, for instance, and suddenly Promoted Tweets for the local pub, dry cleaner or McDonald's pop up in their Twitter stream. This kind of “geofencing” technology, which Facebook has had since 2011, enables businesses to court the kind of walk-in customers mostly to act on limited-time deals and in-store specials.