2018 lender training - mhdc lender training.pdf · ... and fannie mae or usda rural development...

TRANSCRIPT

WELCOME TO MHDC LENDER TRAINING

AGENDA• MHDC Overview• Single Family Loan Programs

– First Place Program (MRB)– Next Step Program (TBA)– Mortgage Credit Certificate (MCC)

• Benefits/Restrictions of the program• Process & Forms • ServiSolutions, Master Servicer

MISSOURI HOUSING DEVELOPMENT COMMISSION (MHDC) OVERVIEW

MHDC is the state’s housing finance agency. Ouragency focuses on providing affordable housing to low-and moderate income Missourians through:

• Missouri Low Income Housing Tax Credit• Mortgage Credit Certificates• First Place Program• Next Step Program• Other housing programs

HOMEOWNERSHIP DEPARTMENT• Provides funding to purchase homes through

partnerships with lenders

• Injects gap financing into loans in the form of grantsand soft second mortgages

• Monitors compliance

• Assure funds are distributed statewide

• Provides support to lending partners

HOW TO BECOME A CERTIFIED LENDER

EFFECTIVE 8/1/13

Forming a

Partnershipwith

MHDC

LENDER REQUIREMENTS1. If the lender is a FNMA seller/servicer it must provide

lender number. It must also provide information per the TPO section of the FNMA selling guide:a) Resumes of principal officers and underwriting

personnelb) Lenders quality control proceduresc) Results of background check of principal officersd) Lender’s hiring procedures for checking employees,

including management, in the origination of mortgage loans against GSA excluded parties list, HUD LPD List and FHFA SCP list.

2. If the lender is a bank or savings and loan association, FDIC must insure the bank or savings and loan association depository accounts.

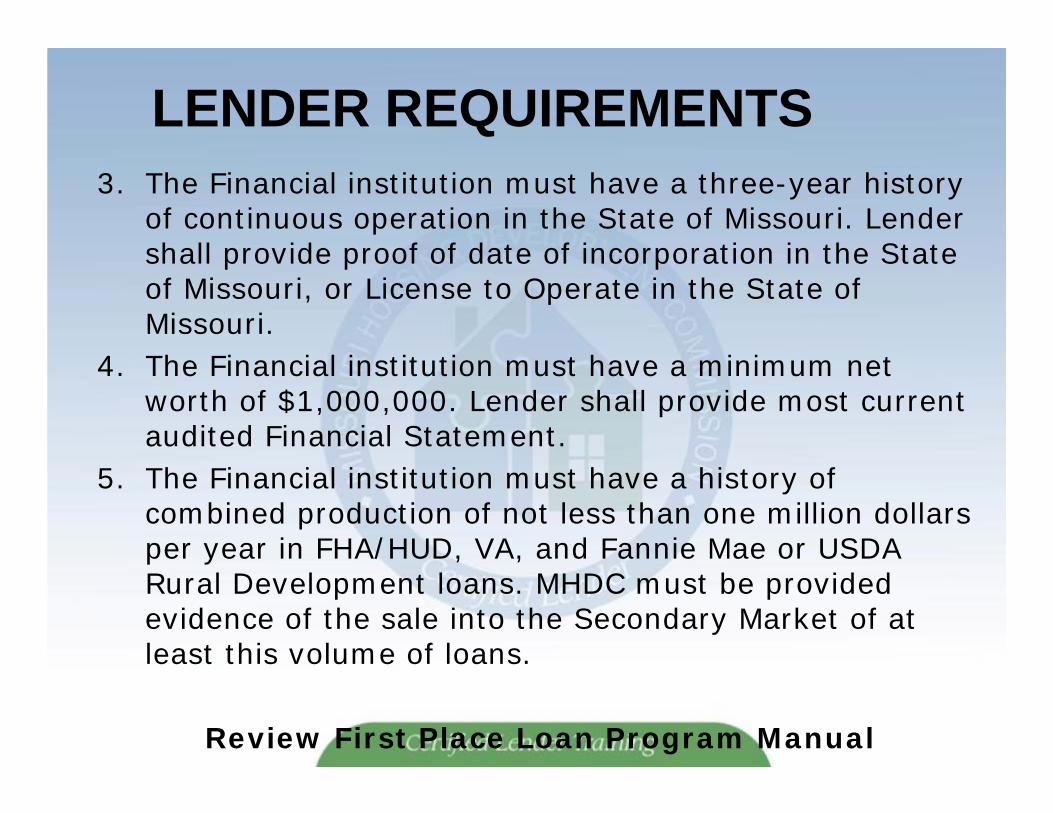

LENDER REQUIREMENTS3. The Financial institution must have a three-year history

of continuous operation in the State of Missouri. Lender shall provide proof of date of incorporation in the State of Missouri, or License to Operate in the State of Missouri.

4. The Financial institution must have a minimum net worth of $1,000,000. Lender shall provide most current audited Financial Statement.

5. The Financial institution must have a history of combined production of not less than one million dollars per year in FHA/HUD, VA, and Fannie Mae or USDA Rural Development loans. MHDC must be provided evidence of the sale into the Secondary Market of at least this volume of loans.

Review First Place Loan Program Manual

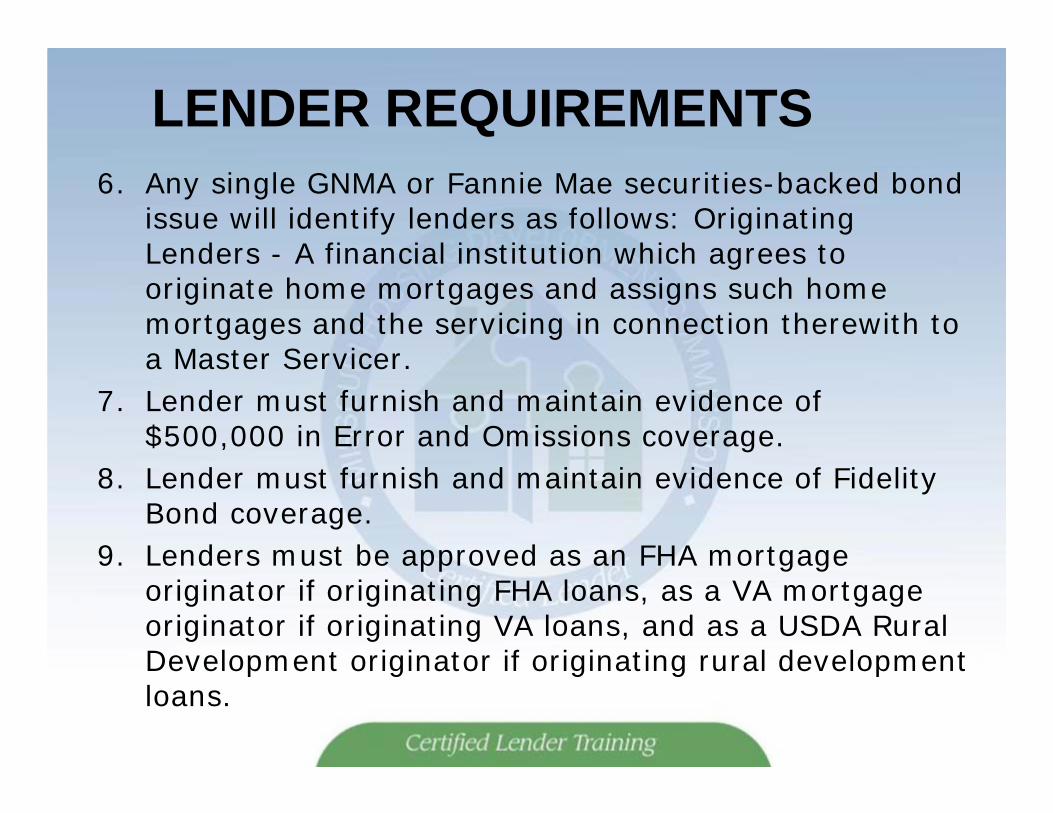

LENDER REQUIREMENTS6. Any single GNMA or Fannie Mae securities-backed bond

issue will identify lenders as follows: Originating Lenders - A financial institution which agrees to originate home mortgages and assigns such home mortgages and the servicing in connection therewith to a Master Servicer.

7. Lender must furnish and maintain evidence of $500,000 in Error and Omissions coverage.

8. Lender must furnish and maintain evidence of Fidelity Bond coverage.

9. Lenders must be approved as an FHA mortgage originator if originating FHA loans, as a VA mortgage originator if originating VA loans, and as a USDA Rural Development originator if originating rural development loans.

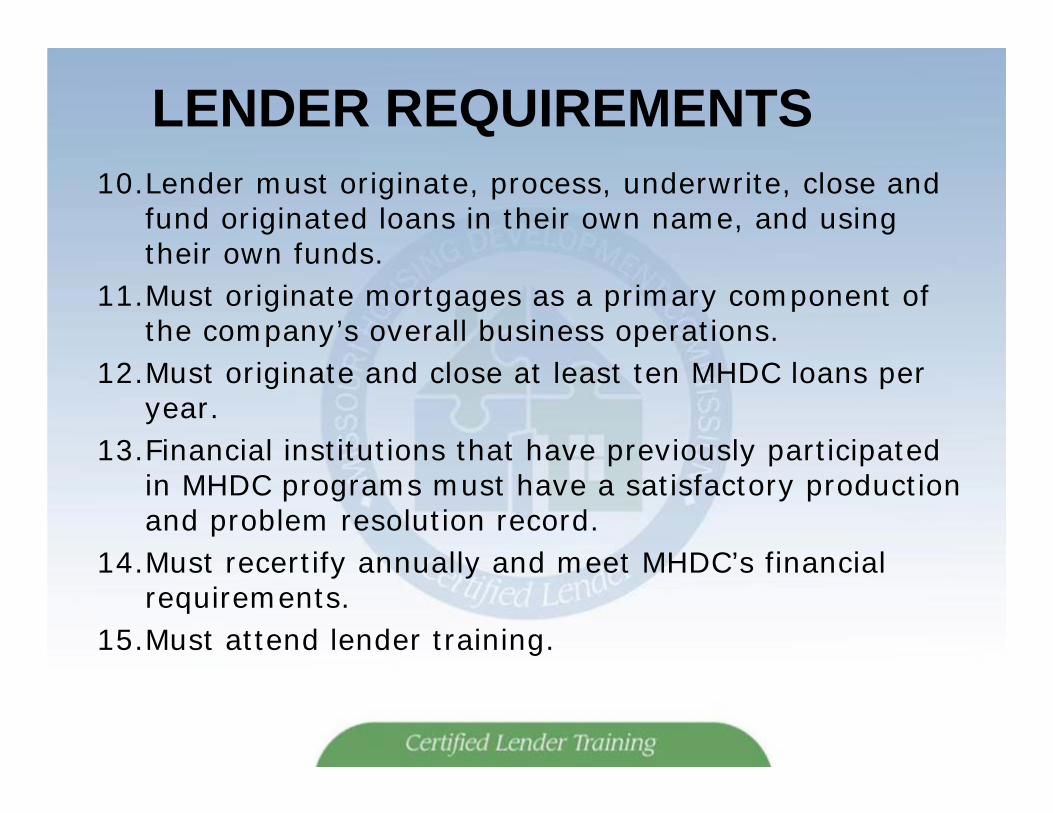

LENDER REQUIREMENTS10.Lender must originate, process, underwrite, close and

fund originated loans in their own name, and using their own funds.

11.Must originate mortgages as a primary component of the company’s overall business operations.

12.Must originate and close at least ten MHDC loans per year.

13.Financial institutions that have previously participated in MHDC programs must have a satisfactory production and problem resolution record.

14.Must recertify annually and meet MHDC’s financial requirements.

15.Must attend lender training.

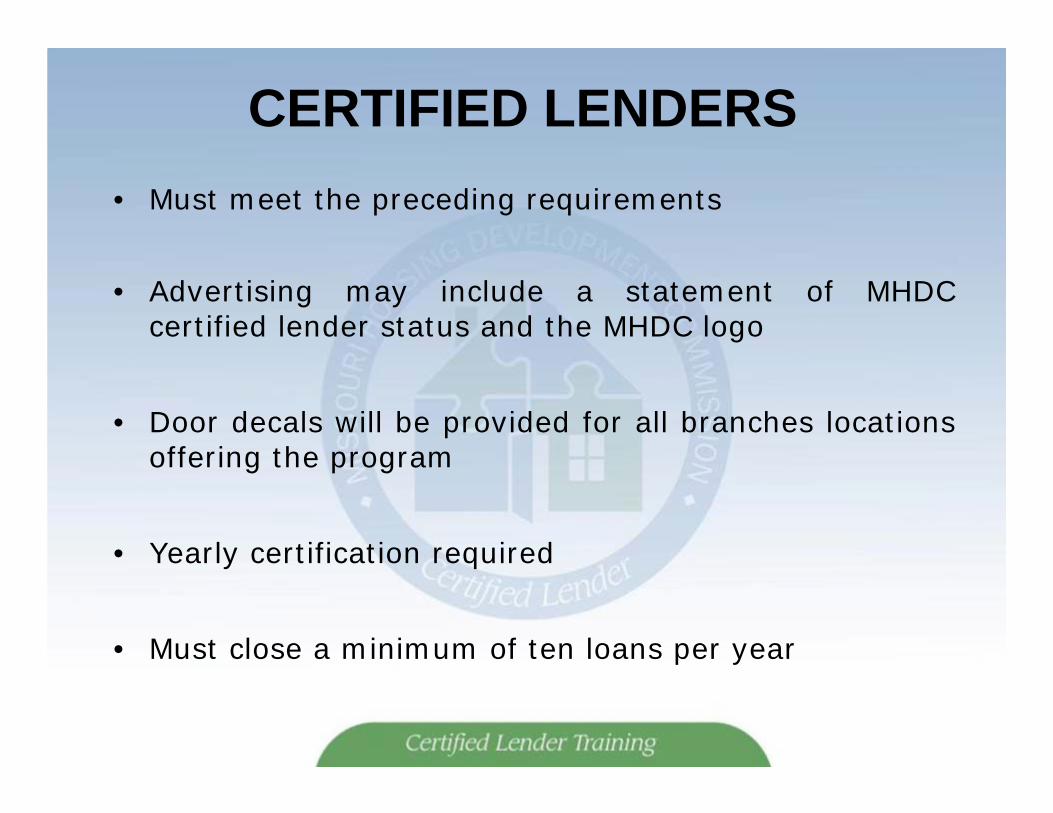

CERTIFIED LENDERS• Must meet the preceding requirements

• Advertising may include a statement of MHDCcertified lender status and the MHDC logo

• Door decals will be provided for all branches locationsoffering the program

• Yearly certification required

• Must close a minimum of ten loans per year

CERTIFIED LENDERS•Annually homeownership staff will evaluate to establish a “Top Performing” lender/loan officer list for our website based on production

•Annual “Lender of the Year” award will be given to a lender that demonstrates strong commitment to MHDC programs which will be based on lender grade and production

HOW TO BECOME A CERTIFIED LOAN OFFICER

LOAN OFFICER CERTIFICATION REQUIREMENTS

1.Your current employer must be anapproved certified lender and meet thelender eligibility requirements

2.Loan officers who have less than fiveyears experience in the First Place LoanProgram, must take the lender/loan officercertification training and pass the test witha percentage of 70 percent or higher

LOAN OFFICER CERTIFICATION REQUIREMENTS

3.Loan officers who have five or more yearsexperience in the First Place Loan Program,can opt out of taking the lender/loan officercertification training but must pass the testwith a percentage of 70 percent or higher

4.A loan officer’s certification will never expireas long as the loan officer shows activeparticipation and/or the lender in which youare employed is a certified lender

LOAN OFFICER CERTIFICATION REQUIREMENTS

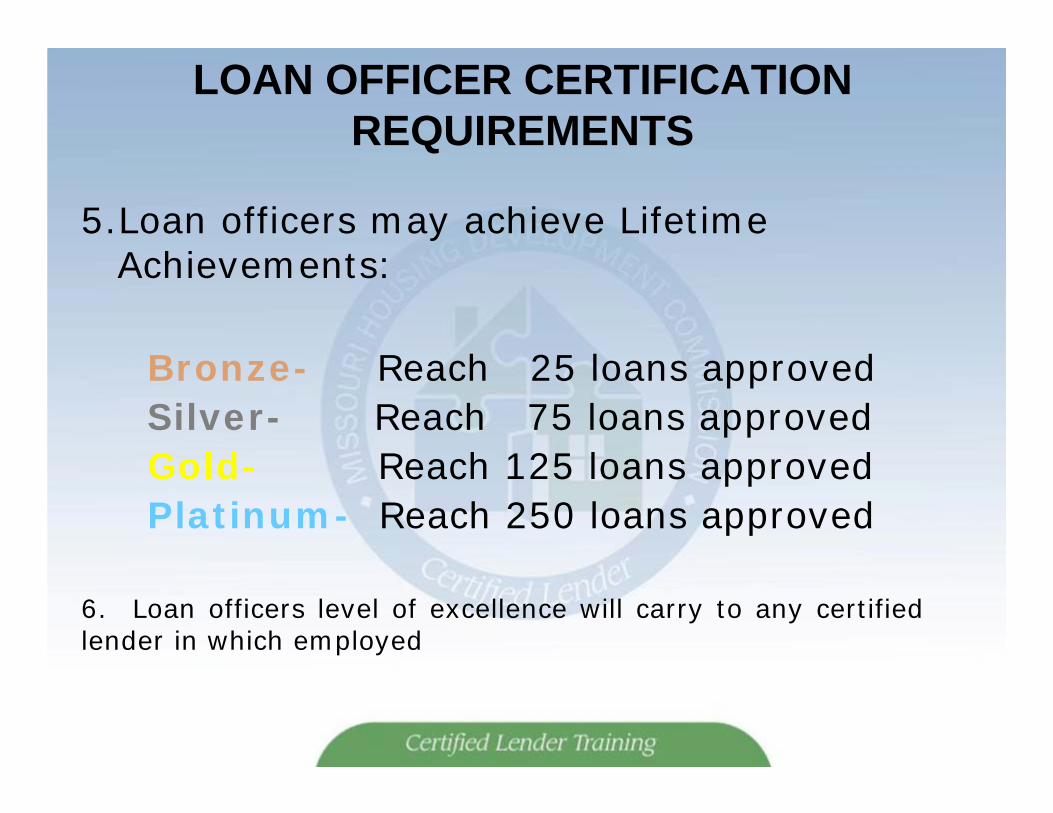

5.Loan officers may achieve Lifetime Achievements:

Bronze- Reach 25 loans approvedSilver- Reach 75 loans approvedGold- Reach 125 loans approvedPlatinum- Reach 250 loans approved

6. Loan officers level of excellence will carry to any certifiedlender in which employed

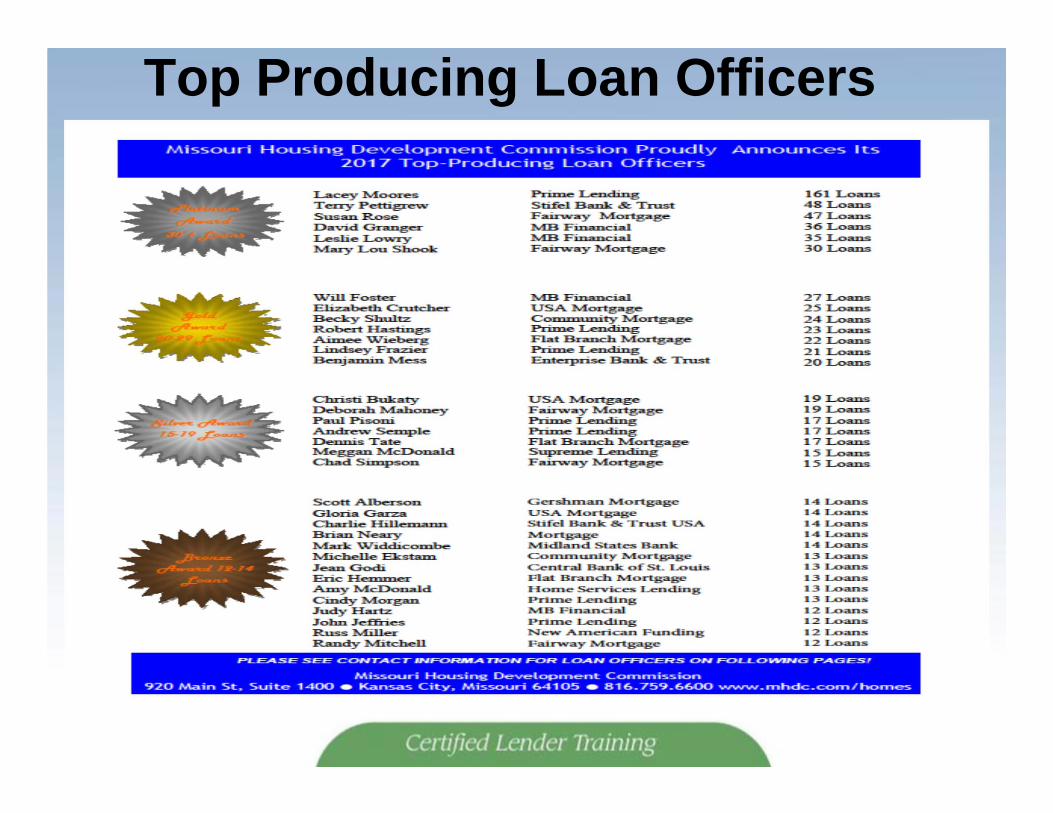

Top Producing Loan Officers

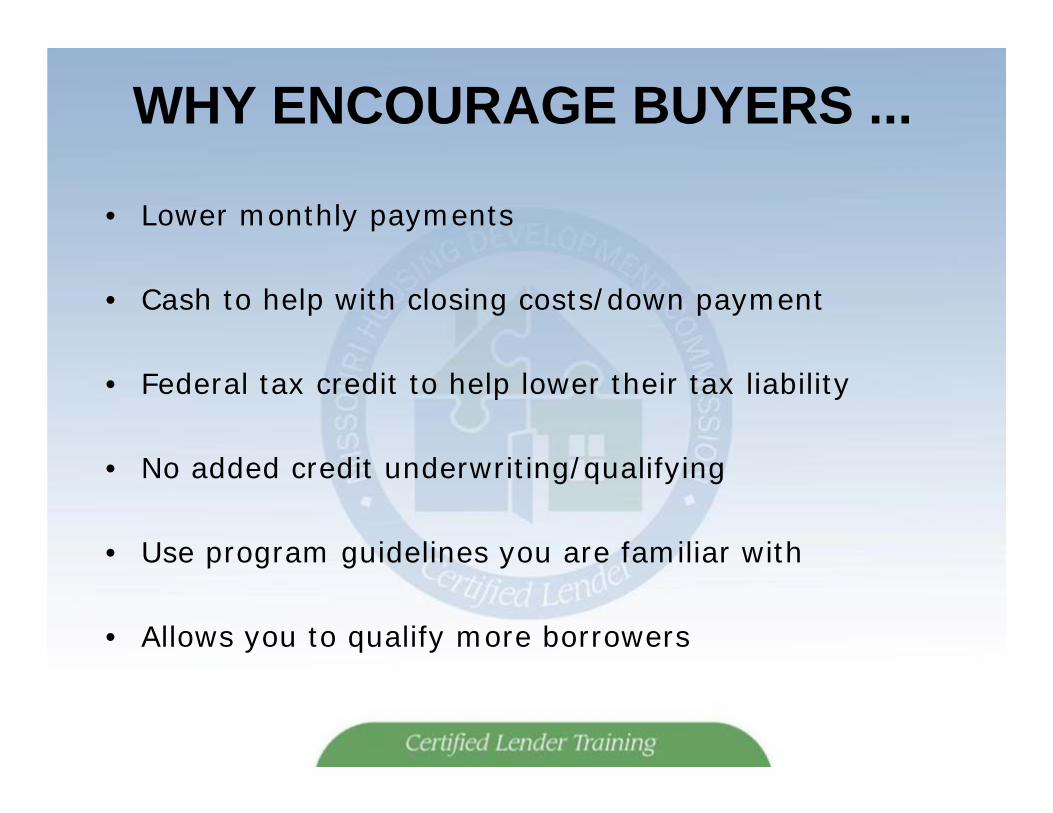

WHY ENCOURAGE BUYERS ...

• Lower monthly payments

• Cash to help with closing costs/down payment

• Federal tax credit to help lower their tax liability

• No added credit underwriting/qualifying

• Use program guidelines you are familiar with

• Allows you to qualify more borrowers

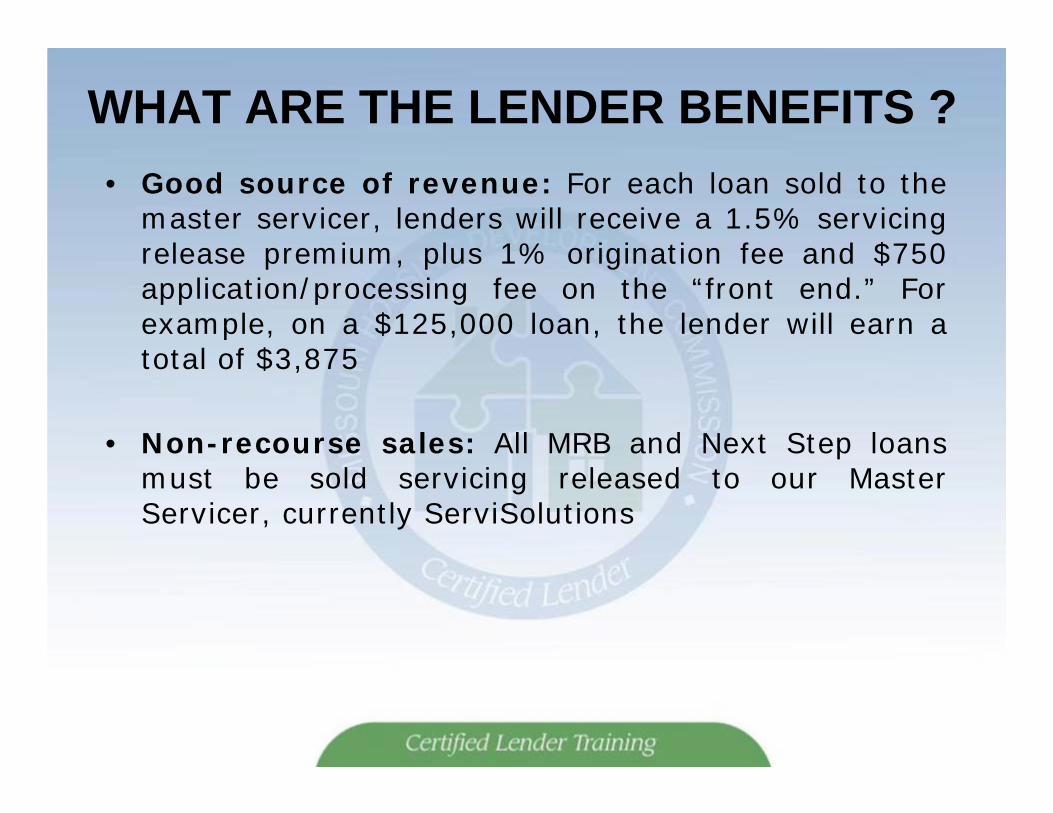

WHAT ARE THE LENDER BENEFITS ?• Good source of revenue: For each loan sold to the

master servicer, lenders will receive a 1.5% servicingrelease premium, plus 1% origination fee and $750application/processing fee on the “front end.” Forexample, on a $125,000 loan, the lender will earn atotal of $3,875

• Non-recourse sales: All MRB and Next Step loansmust be sold servicing released to our MasterServicer, currently ServiSolutions

WHAT ARE THE LENDER BENEFITS ?

• No forward placement risk: Whenthese loans are originated, the rate andfees paid are guaranteed, provideddelivery takes place within the reservationperiod

• CRA (Community Reinvestment Act):Participation in the first-time homebuyerprogram constitutes a CRA-eligibleactivity, in most cases

WHAT ARE THE RESTRICTIONS ?• IRS regulations limit the maximum sales price for

properties using the program

• Properties in 100 year flood plains not eligible for financing

• Applicants must be first-time homebuyers, except in targetareas and/or a qualified veteran or using the Next StepProgram

• Some restrictions may apply to the sale of the home under some programs

• IRS regulations limit maximum income of applicants usingprogram

WHAT ARE THE RESTRICTIONS ?• MHDC restricts the amount of fees that may be

charged, eliminating “junk fees”; underwriting fee,

e-mail fee, etc.

• No Manual Underwriting

• Minimum Credit Score 620, maximum DTI is 45%

• Secondary financing is only acceptable from other

government agencies

WHAT PRODUCTS ARE ACCEPTABLE?

• Lenders can use familiar products such as:– FHA,– RD (USDA),– VA, and– Conventional (HFA preferred)

• Borrower selects the following:– Type of loan (FHA, RD, VA, etc.)– Type of fund (CAL, Non CAL, or MCC)

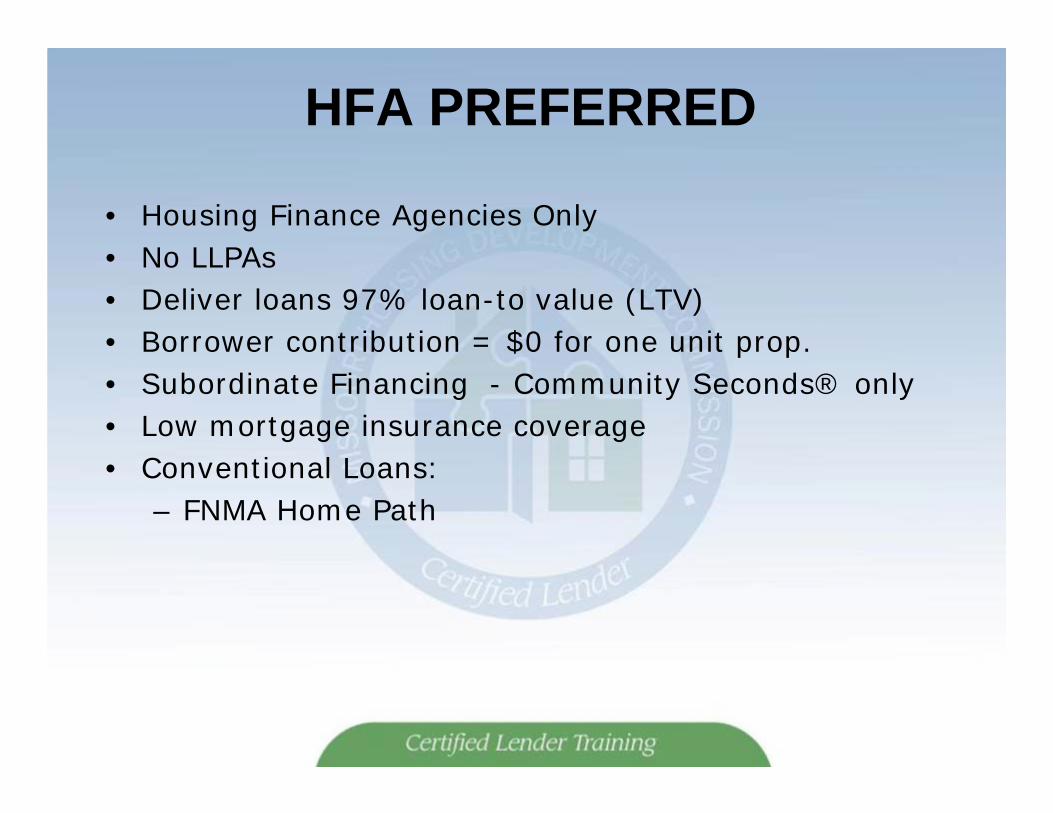

HFA PREFERRED

• Housing Finance Agencies Only• No LLPAs• Deliver loans 97% loan-to value (LTV)• Borrower contribution = $0 for one unit prop.• Subordinate Financing - Community Seconds® only• Low mortgage insurance coverage• Conventional Loans:

– FNMA Home Path

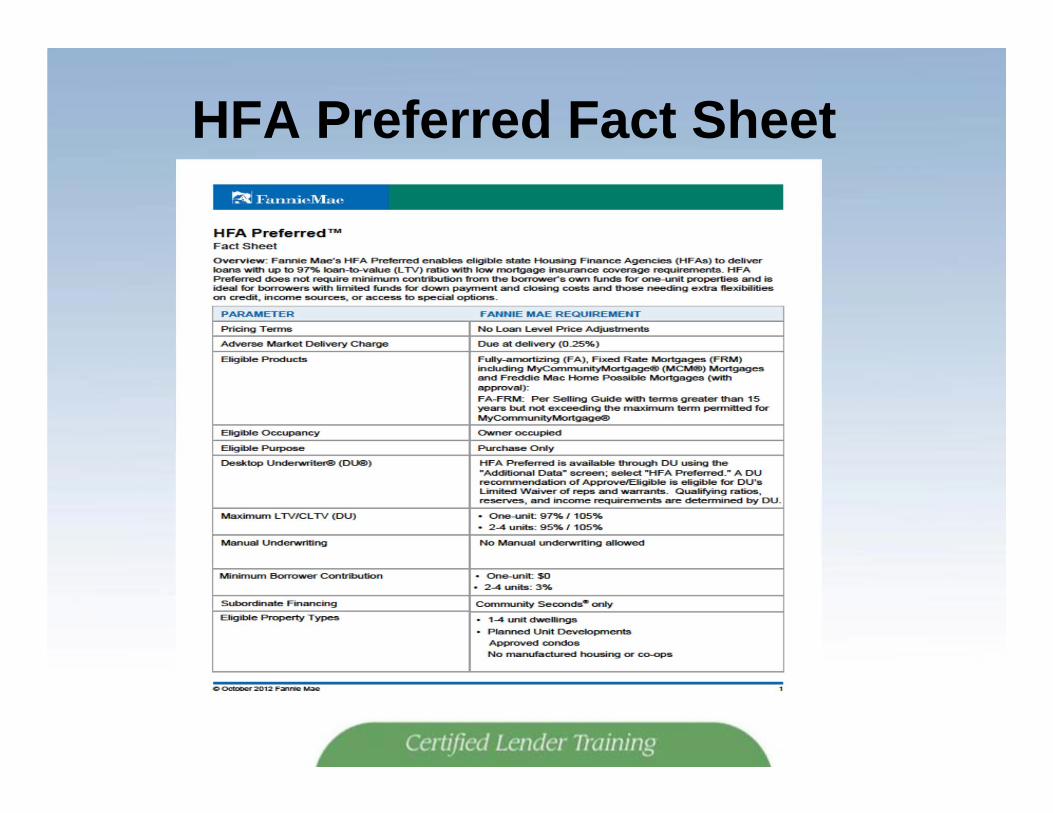

HFA Preferred Fact Sheet

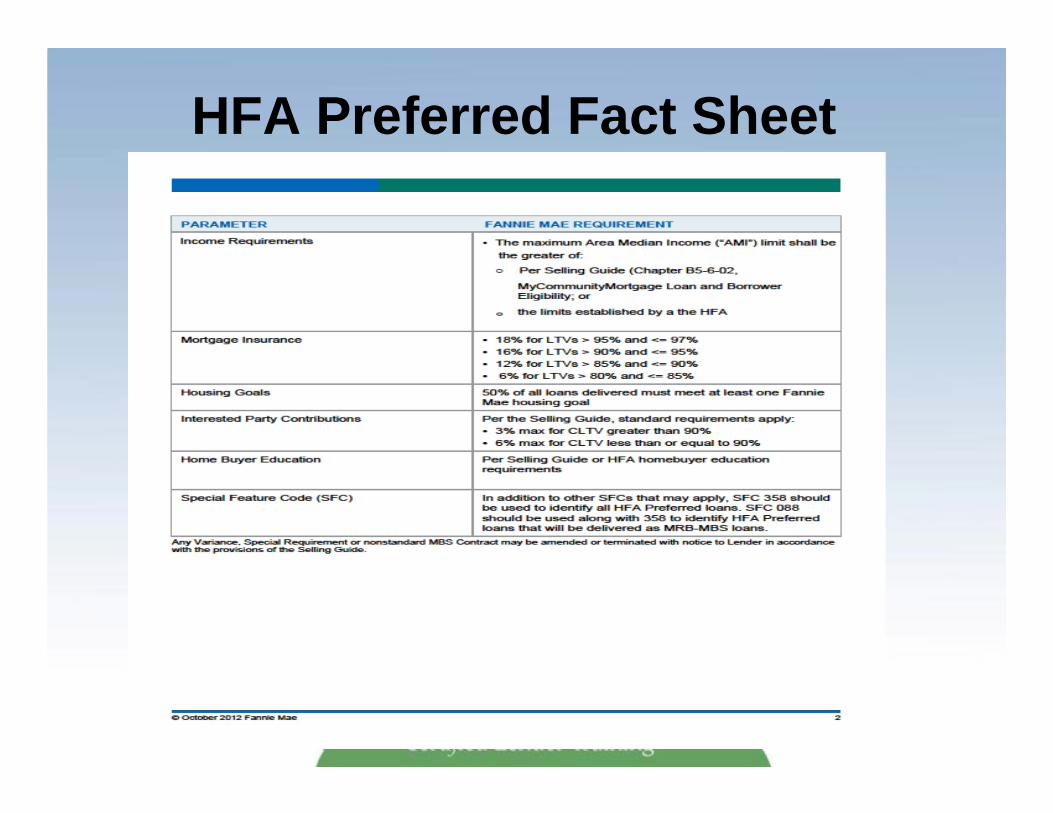

HFA Preferred Fact Sheet

Borrower (s) must meet Mortgage Revenue Bond (MRB) requirements1. Borrower(s) must be first-time homebuyer(s)

2. Property cannot be located in Flood Zone A

3. Household income cannot exceed limits set byMHDC

4. Sales price cannot exceed limits set by MHDC

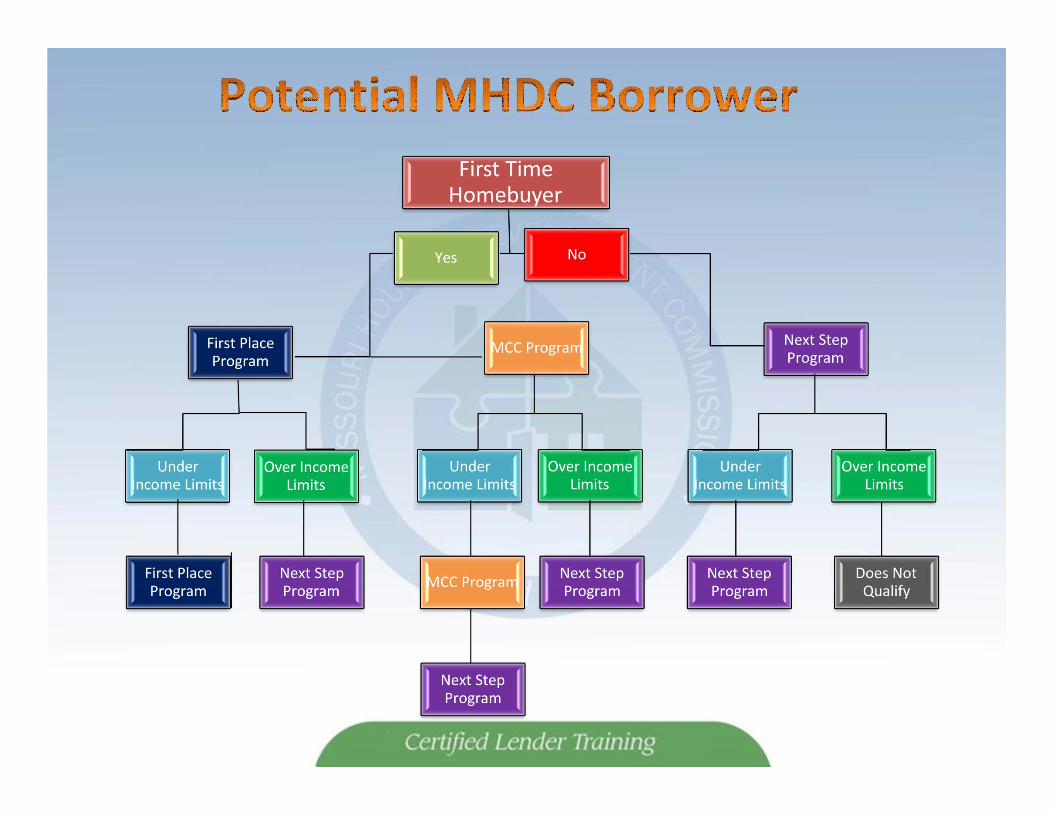

FIRST-TIME HOMEBUYER

A First-Time Home Buyer is defined as a person who:

• Has not had a present ownership interest in theirprincipal residence within the last three years;

• Has not taken a real estate tax deduction (on schedule A) for any residence within the last three years and;

• Has not taken a mortgage interest deduction (onschedule A) for any residence in the last threeyears.

FIRST-TIME HOMEBUYER

• All adult persons who will reside in the home must meet the First-Time Home Buyer qualification

• The only exception to this requirement is if theapplicant is purchasing a home in a federally targetedarea or is a qualified veteran

FLOOD ZONES

• No part of the property can lie within a 100-year flood plain

• Any property lying within flood zone A will not be eligible for any MHDC program

• Any property lying within flood zone D must have prior approval from MHDC

• Lender must indicate the flood zone letter on the Lender’s Certificate (form #520)

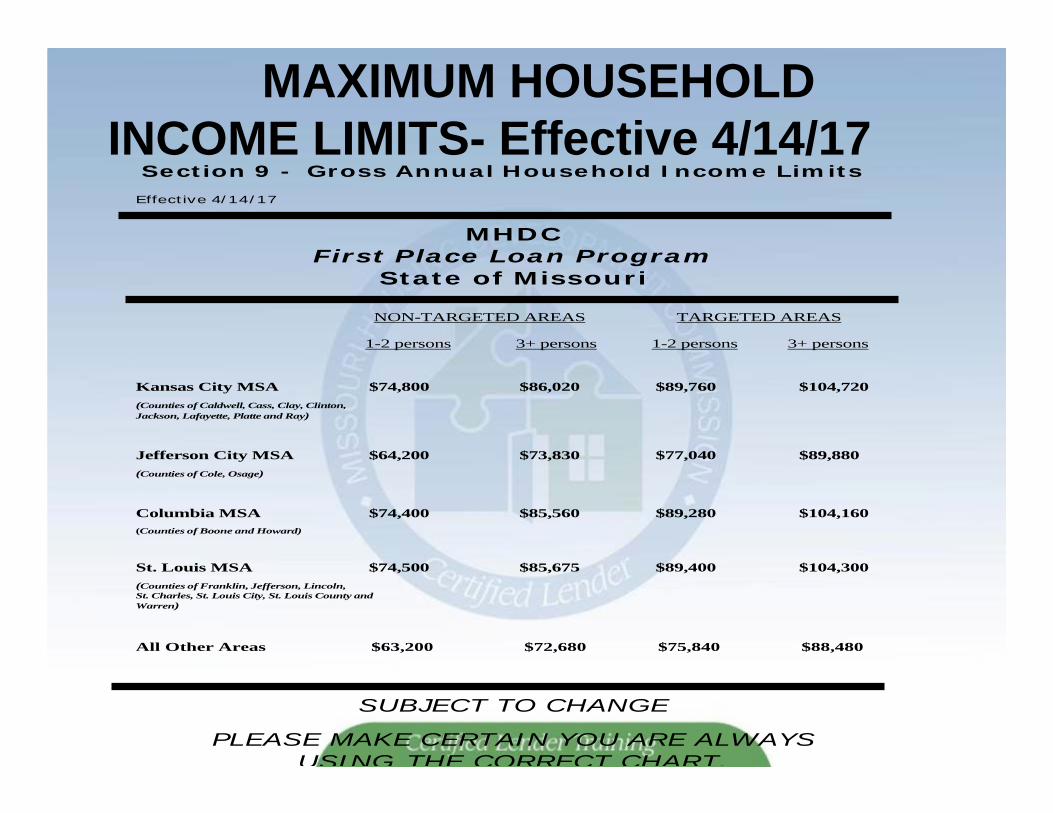

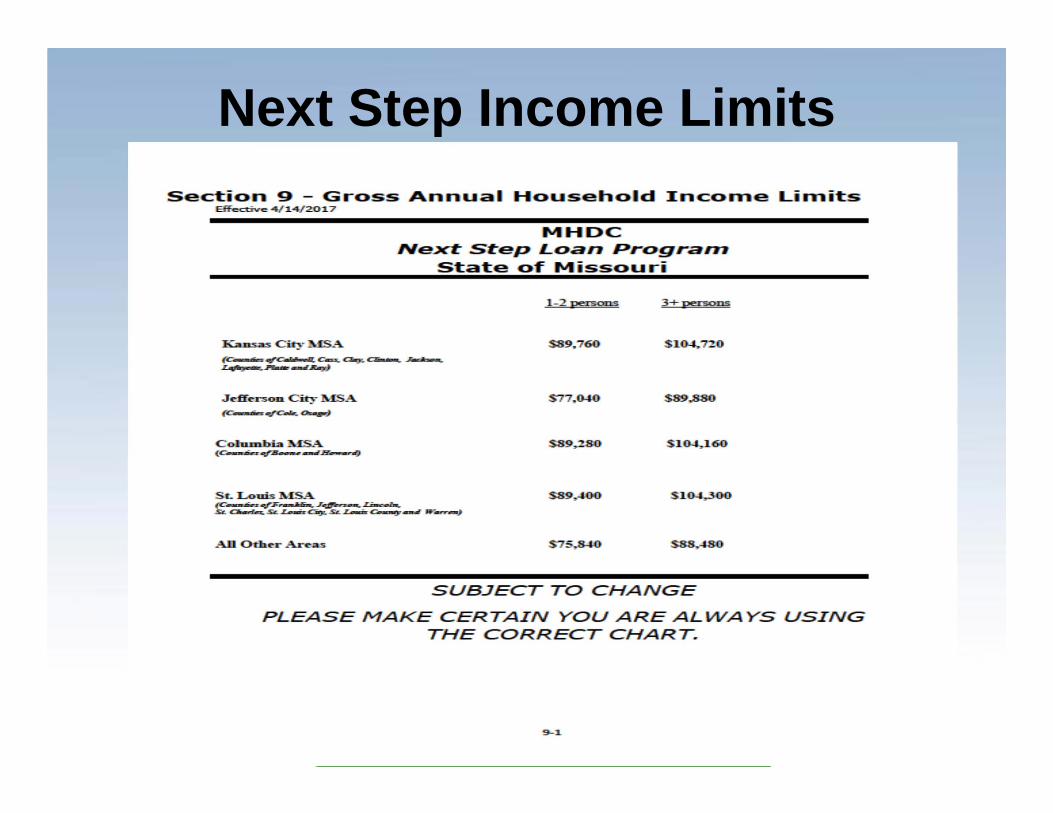

MAXIMUM HOUSEHOLDINCOME LIMITS- Effective 4/14/17

Section 9 - Gross Annual Household Income Limits Effective 4/14/17

MHDC First Place Loan Program

State of Missouri NON-TARGETED AREAS TARGETED AREAS

1-2 persons 3+ persons 1-2 persons 3+ persons

Kansas City MSA $74,800 $86,020 $89,760 $104,720 (Counties of Caldwell, Cass, Clay, Clinton, Jackson, Lafayette, Platte and Ray)

Jefferson City MSA $64,200 $73,830 $77,040 $89,880 (Counties of Cole, Osage)

Columbia MSA $74,400 $85,560 $89,280 $104,160 (Counties of Boone and Howard)

St. Louis MSA $74,500 $85,675 $89,400 $104,300 (Counties of Franklin, Jefferson, Lincoln, St. Charles, St. Louis City, St. Louis County and Warren)

All Other Areas $63,200 $72,680 $75,840 $88,480

SUBJECT TO CHANGE

PLEASE MAKE CERTAIN YOU ARE ALWAYS USING THE CORRECT CHART.

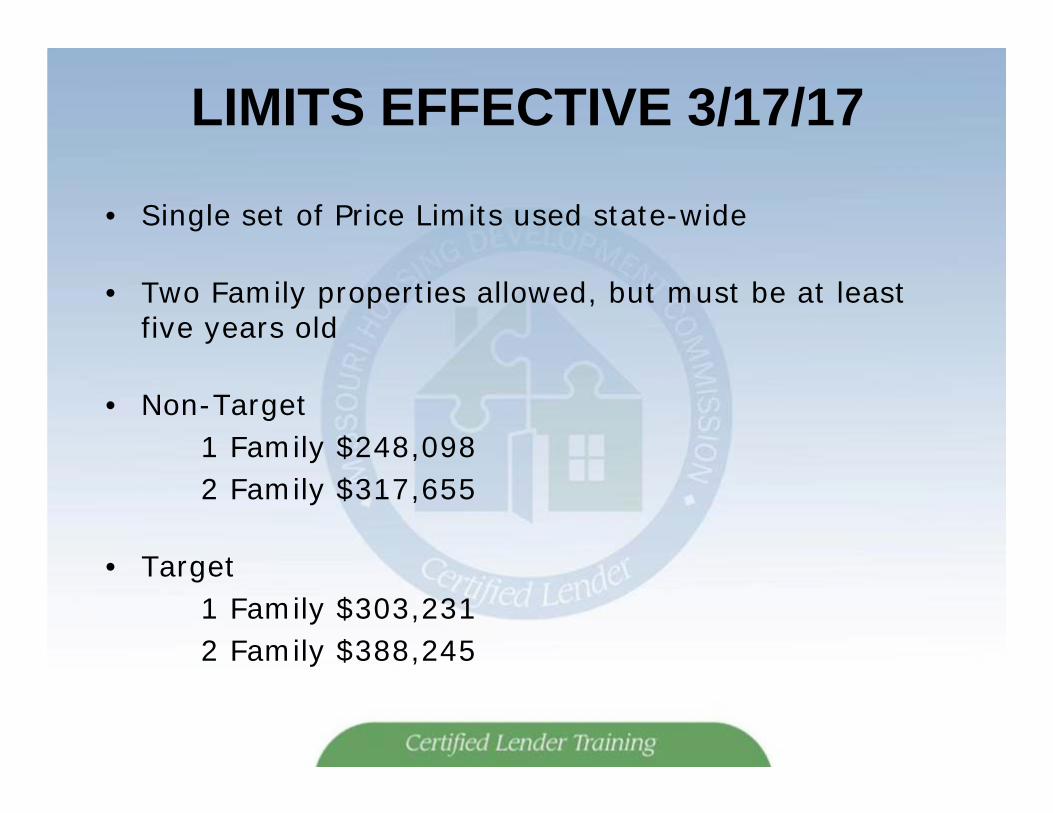

LIMITS EFFECTIVE 3/17/17

• Single set of Price Limits used state-wide

• Two Family properties allowed, but must be at least five years old

• Non-Target 1 Family $248,0982 Family $317,655

• Target 1 Family $303,2312 Family $388,245

2018 Single Family Programs

First Place MRB

• CAL• NON CAL

MCC

• Stand Alone• Next Step CAL•Next Step NON CAL

Next Step TBA

• CAL• NON CAL

MORTGAGE REVENUEBONDS (MRB)

Are a type of mortgage loan where the costof borrowing is partially subsidized by themortgage revenue bond & are generallydesigned to lower the cost ofhomeownership for low to moderateincome borrowers

The program offers first-time homebuyers30 year fixed mortgages at or below-market rates

Due to the nature of these loans, IRS rules apply

These loans have to be closed andpurchased by the master servicer usuallywithin 60 days

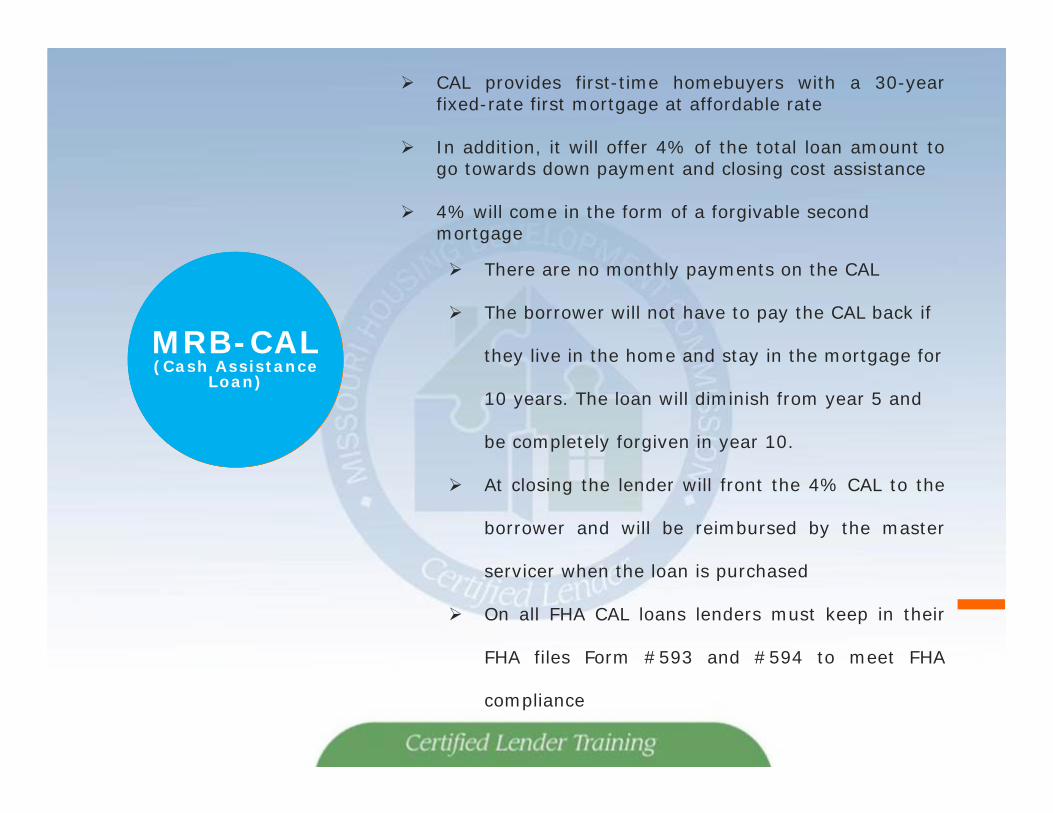

MRB-CAL(Cash Assistance

Loan)

CAL provides first-time homebuyers with a 30-yearfixed-rate first mortgage at affordable rate

In addition, it will offer 4% of the total loan amount togo towards down payment and closing cost assistance

4% will come in the form of a forgivable second mortgage

There are no monthly payments on the CAL

The borrower will not have to pay the CAL back if

they live in the home and stay in the mortgage for

10 years. The loan will diminish from year 5 and

be completely forgiven in year 10.

At closing the lender will front the 4% CAL to the

borrower and will be reimbursed by the master

servicer when the loan is purchased

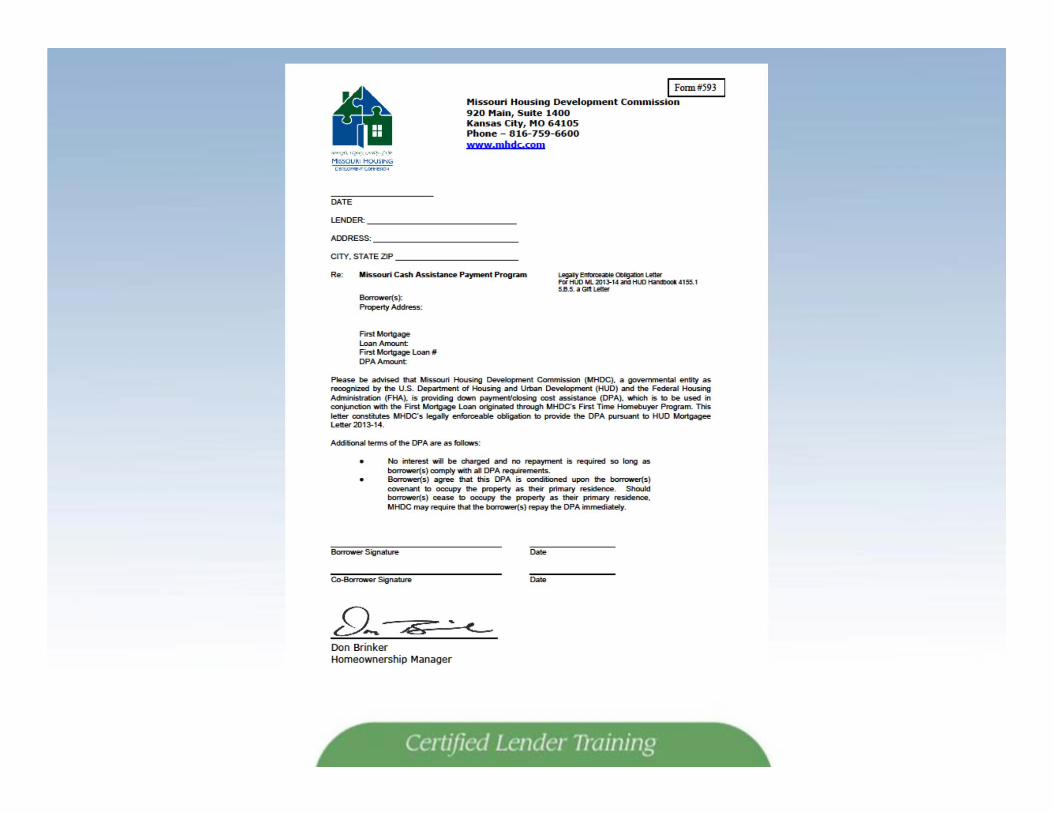

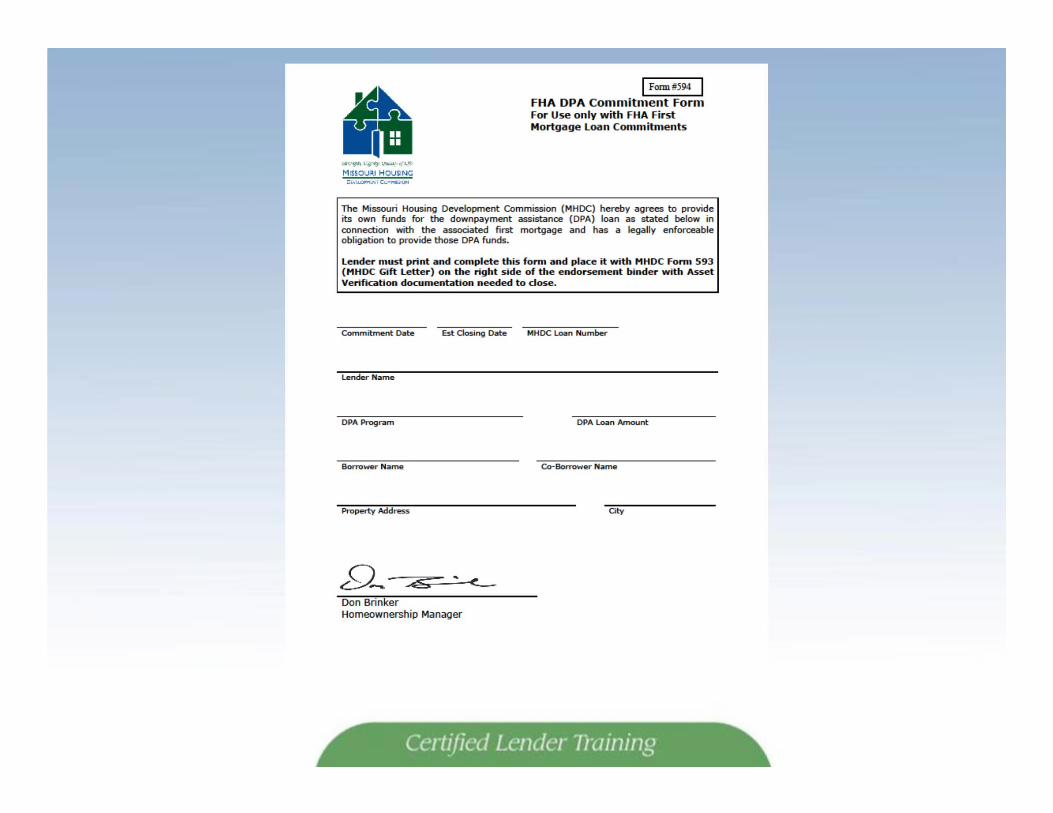

On all FHA CAL loans lenders must keep in their

FHA files Form #593 and #594 to meet FHA

compliance

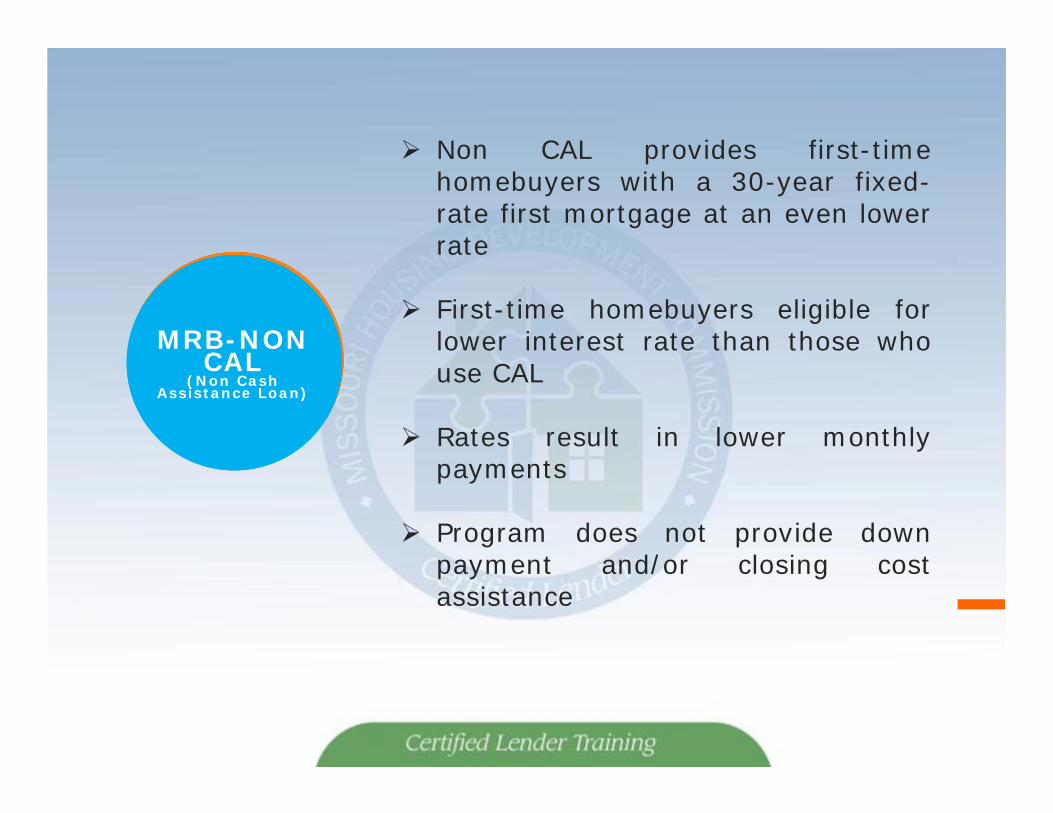

MRB-NON CAL

(Non Cash Assistance Loan)

Non CAL provides first-timehomebuyers with a 30-year fixed-rate first mortgage at an even lowerrate

First-time homebuyers eligible forlower interest rate than those whouse CAL

Rates result in lower monthlypayments

Program does not provide downpayment and/or closing costassistance

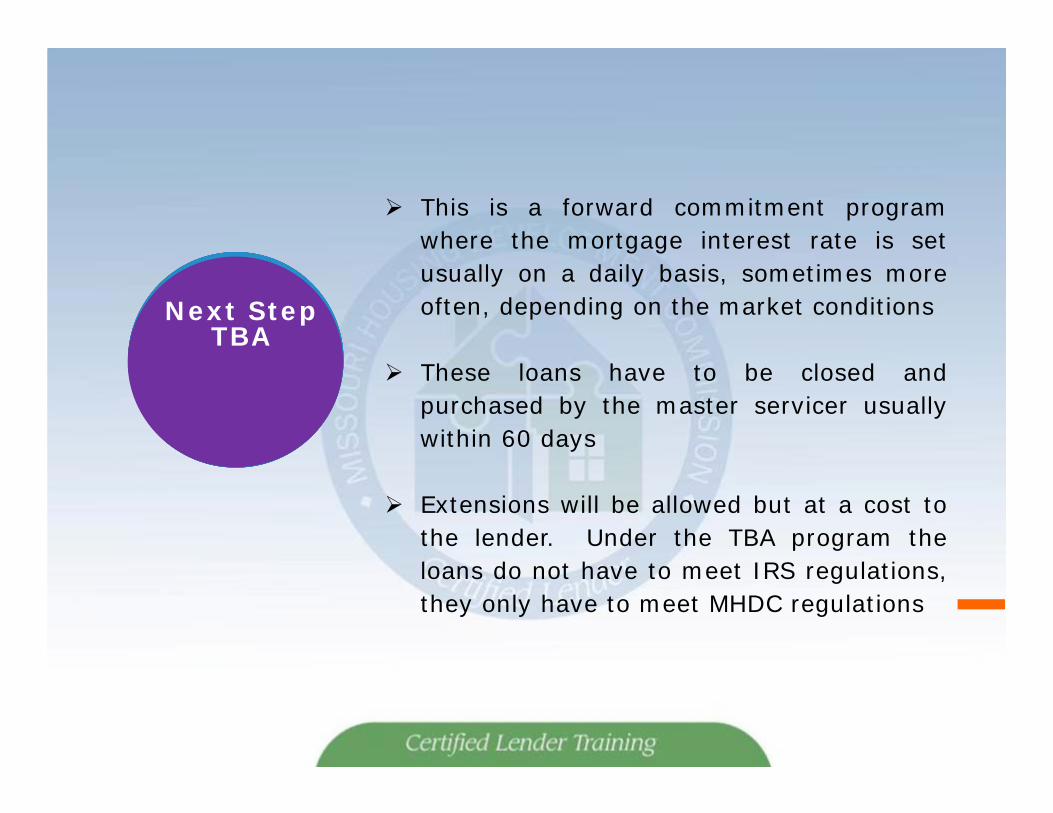

Next StepTBA

This is a forward commitment programwhere the mortgage interest rate is setusually on a daily basis, sometimes moreoften, depending on the market conditions

These loans have to be closed andpurchased by the master servicer usuallywithin 60 days

Extensions will be allowed but at a cost tothe lender. Under the TBA program theloans do not have to meet IRS regulations,they only have to meet MHDC regulations

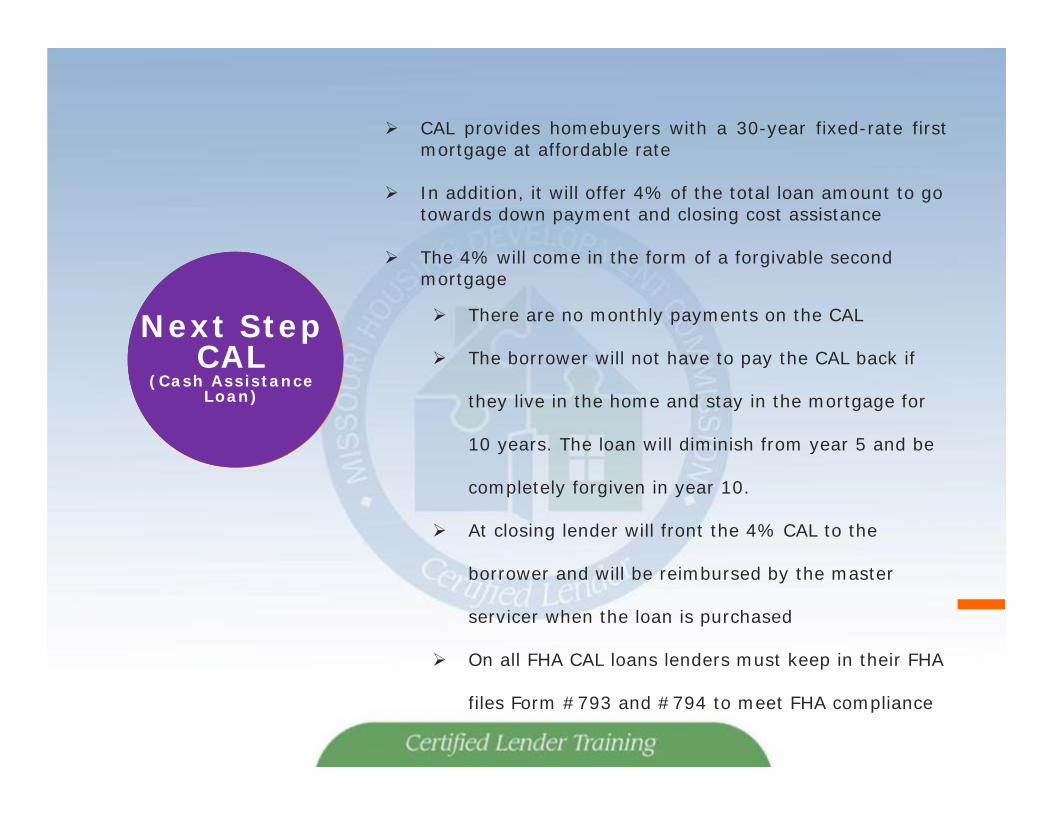

Next StepCAL

(Cash Assistance Loan)

CAL provides homebuyers with a 30-year fixed-rate firstmortgage at affordable rate

In addition, it will offer 4% of the total loan amount to go towards down payment and closing cost assistance

The 4% will come in the form of a forgivable second mortgage

There are no monthly payments on the CAL

The borrower will not have to pay the CAL back if

they live in the home and stay in the mortgage for

10 years. The loan will diminish from year 5 and be

completely forgiven in year 10.

At closing lender will front the 4% CAL to the

borrower and will be reimbursed by the master

servicer when the loan is purchased

On all FHA CAL loans lenders must keep in their FHA

files Form #793 and #794 to meet FHA compliance

Next StepNon CAL

(Non Cash Assistance Loan)

Non CAL provides homebuyers with a30-year fixed-rate first mortgage atan even lower rate

Homebuyers eligible for lower interestrate than those who use CAL

Rates result in lower monthly payments

Program does not provide downpayment and/or closing costassistance

Next Step Income Limits

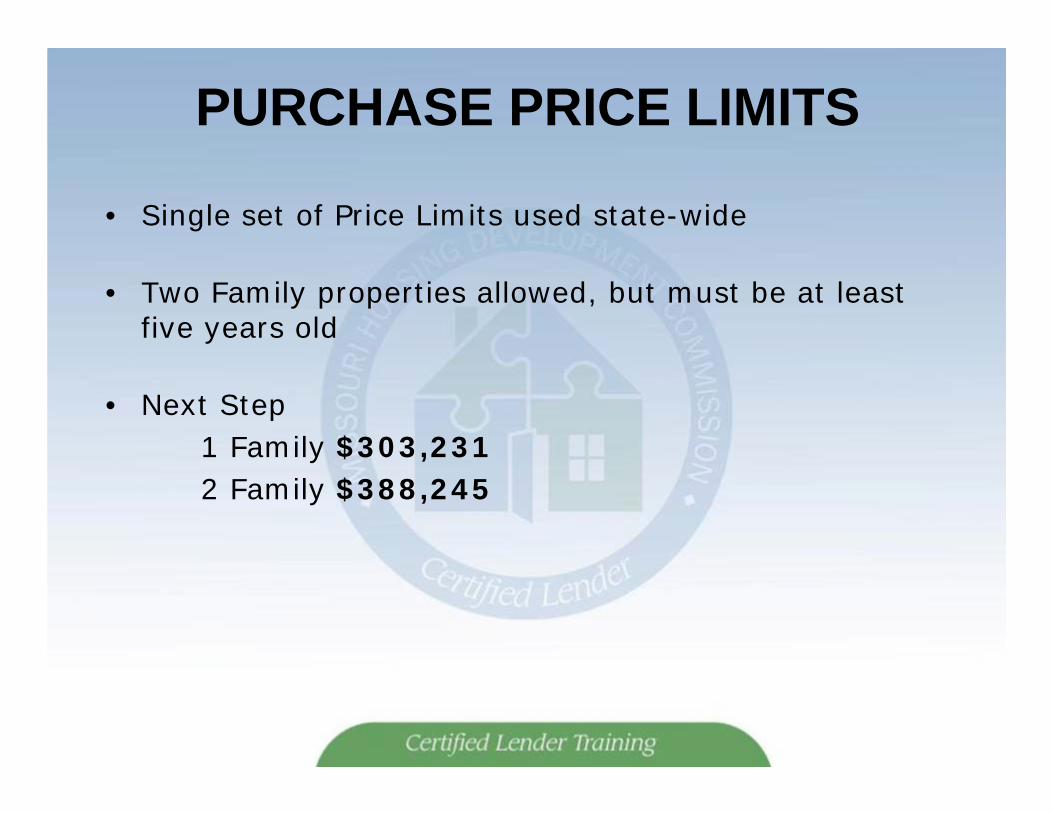

PURCHASE PRICE LIMITS

• Single set of Price Limits used state-wide

• Two Family properties allowed, but must be at least five years old

• Next Step 1 Family $303,2312 Family $388,245

Program Objectives

• The Next Step Program allows Missouri citizens the opportunity to continue their quest for homeownership.

• Next Step will enable non-first time homebuyers who lack sufficient equity or funds for downpayment to purchase their new home.

• The Next Step Program will provide incentives for home buyers to move into “Opportunity Areas” throughout Missouri.

Program Need• Some homeowners lack equity and need downpayment

assistance to purchase their next home.• Some homeowners become renters as a result. • The Next Step Program benefits Missouri borrowers in

several ways:• Bridges the gap between lack of equity and

downpayment needed to purchase their next home.• Allow first time buyers who fall outside the income limits

for the First Place Program to achieve homeownership.• Encourage qualified borrowers to move into

“Opportunity Areas” with downpayment and closing cost assistance.

Funding Next Step

• Funding for this program will be provided by the sale of the MBS in the TBA market or by the sale of taxable bonds.

• Mortgage interest rates will be set based on the TBA market.

• The interest rates will be adjusted on a daily basis as needed.

Opportunity Areas• “Opportunity Areas” will be determined by census tracts. • “Opportunity Area” census tracts were determined by the

following criteria:• Metro Areas

• Seventy percent (70%) or higher have some college education

• poverty rate is 5 percent or lower• Census tract median income is $50K - $120K

• Rural Areas• Fifty percent (50%) or higher have some college

education• poverty rate is 10 percent or lower• Census tract median income is $40K -120K

–

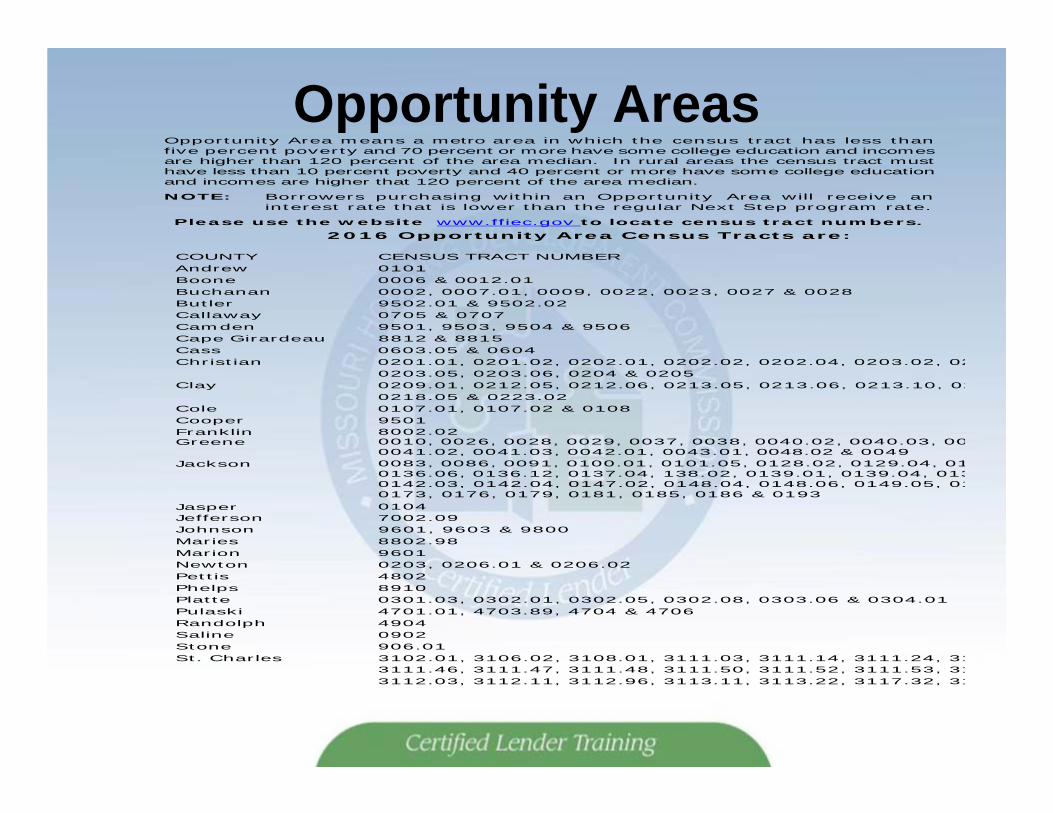

Opportunity AreasOpportunity Area means a metro area in which the census tract has less than five percent poverty and 70 percent or more have some college education and incomes are higher than 120 percent of the area median. In rural areas the census tract must have less than 10 percent poverty and 40 percent or more have some college education and incomes are higher that 120 percent of the area median.

NOTE: Borrowers purchasing within an Opportunity Area will receive an interest rate that is lower than the regular Next Step program rate.

Please use the website www.ffiec.gov to locate census tract numbers. 2016 Opportunity Area Census Tracts are:

COUNTY CENSUS TRACT NUMBER Andrew 0101 Boone 0006 & 0012.01 Buchanan 0002, 0007.01, 0009, 0022, 0023, 0027 & 0028 Butler 9502.01 & 9502.02 Callaway 0705 & 0707 Camden 9501, 9503, 9504 & 9506 Cape Girardeau 8812 & 8815 Cass 0603.05 & 0604 Christian 0201.01, 0201.02, 0202.01, 0202.02, 0202.04, 0203.02, 02 0203.05, 0203.06, 0204 & 0205 Clay 0209.01, 0212.05, 0212.06, 0213.05, 0213.06, 0213.10, 02 0218.05 & 0223.02 Cole 0107.01, 0107.02 & 0108 Cooper 9501 Franklin 8002.02 Greene 0010, 0026, 0028, 0029, 0037, 0038, 0040.02, 0040.03, 00

0041.02, 0041.03, 0042.01, 0043.01, 0048.02 & 0049 Jackson 0083, 0086, 0091, 0100.01, 0101.05, 0128.02, 0129.04, 01

0136.06, 0136.12, 0137.04, 138.02, 0139.01, 0139.04, 0130142.03, 0142.04, 0147.02, 0148.04, 0148.06, 0149.05, 010173, 0176, 0179, 0181, 0185, 0186 & 0193

Jasper 0104 Jefferson 7002.09 Johnson 9601, 9603 & 9800 Maries 8802.98 Marion 9601 Newton 0203, 0206.01 & 0206.02 Pettis 4802 Phelps 8910 Platte 0301.03, 0302.01, 0302.05, 0302.08, 0303.06 & 0304.01 Pulaski 4701.01, 4703.89, 4704 & 4706 Randolph 4904 Saline 0902 Stone 906.01 St. Charles 3102.01, 3106.02, 3108.01, 3111.03, 3111.14, 3111.24, 31 3111.46, 3111.47, 3111.48, 3111.50, 3111.52, 3111.53, 31 3112.03, 3112.11, 3112.96, 3113.11, 3113.22, 3117.32, 31

Interest Rates• There will be eight different interest rates in the Next Step

Program for example:– CAL Government– NON CAL Government – CAL Conventional – Non CAL Conventional – OA CAL Government– OA NON CAL Government – OA CAL Conventional – OA Non CAL Conventional

• These rates could change on a daily basis or sometimes twice a day. So make sure you are always using the correct rate.

Next Step • If a borrower lives in their current home and wants to

buy another home using the Next Step program, this will be allowed, however the following must be met:– The borrower must live in the new home as their

primary residence– The rental income from the old home must be

counted against the borrower for MHDC income qualifying, whether the borrower has rented the home or not

– Of course you will also have to follow your credit underwriting guidelines as well

Reservation Procedures for Next Step Program

• MHDC will announce interest rates by 9:00 am central time every business day excluding holidays and activate the reservation system so that reservations may be made. Reservations for the Next Step program can only be reserved from 9:00am to 5:00 pm central time Monday - Friday.

• Loans may not be canceled to re-reserve for a lower interest rate. Loans that are cancelled must wait sixty (60) days before re-reserving.

Reservation Expiration Dates

• If the lender determines that the loan will not be closed and purchased prior to reservation expiration, it is the responsibility of the lender to request an extension for that loan. Loans not extended prior to reservation expiration may be subject to mark-to-market fees.

• There will be two different extension fees:– A 15 day extension at .125% of the loan amount.– A 30 day extension at .25% of the loan amount.

• These fees will be netted out of your loan purchase by the master servicer. MHDC will only allow one extension before the loan closes.

MORTGAGE CREDIT

CERTIFICATE (MCC)

A certificate provided by MHDC to theborrower that directly converts a portionof the mortgage interest paid by theborrower into a non-refundable federal taxcredit

Mortgage credit certificates can only beissued by MHDC through certified lenders,and are typically available only to low- ormoderate- income buyers. MCC’s have tomeet IRS/MHDC regulations

These certificates are designed to helpfirst-time homebuyers qualify for a homeloan by reducing their tax liabilities belowwhat they would otherwise have to pay

MORTGAGE CREDIT

CERTIFICATE (MCC)

MCC will not be reissued

Therefore, if a borrower refinances theirhome they will lose their MCC

MCC’s are assigned to the borrower andthe mortgage on the home, so if theyrefinance or sell their home the MCC willbecome null and void

MCC are non assumable and nontransferrable

If the borrower fails to occupy their homeas their principal residence the MCC willbecome null and void

FOR MORTGAGE LOANS INVOLVING MCCS, CONVENTIONAL UNDERWRITING STANDARDS FOR HOUSING EXPENSE AND DEBT RATIOS MAY BE MODIFIED TO RECOGNIZE THE BENEFIT OF THE MCC FROM THE FEDERAL INCOME TAX CREDIT.

THE SECONDARY MORTGAGE MARKET AND THE MORTGAGE INSURANCE INDUSTRY HAVE ESTABLISHED UNDERWRITING POLICIES FOR LOANS INVOLVING MCCS. THESE ARE AVAILABLE SEPARATELY AS POLICY STATEMENTS FROM THE MORTGAGE LENDING INDUSTRY, BUT GENERALLY ALLOW THE CREDIT AVAILABLE UNDER THE MCC TO BE TREATED AS AN ADJUSTMENT TO THE MONTHLY LOAN PAYMENT AMOUNT.

MORTGAGE CREDIT

CERTIFICATE (MCC)

MORTGAGE CREDIT CERTIFICATE

MCC

TAX CREDIT VS TAX

DEDUCTION

Entitles taxpayers to subtract from theadjusted gross income before federalincome taxes are computed.Therefore, with a deduction, only apercentage of the amount deducted isrealized in savings.

TAX DEDUCTION

Entitles taxpayers to subtract theamount from their total federalincome tax liability, receiving a dollarfor dollar savings.

TAX CREDIT

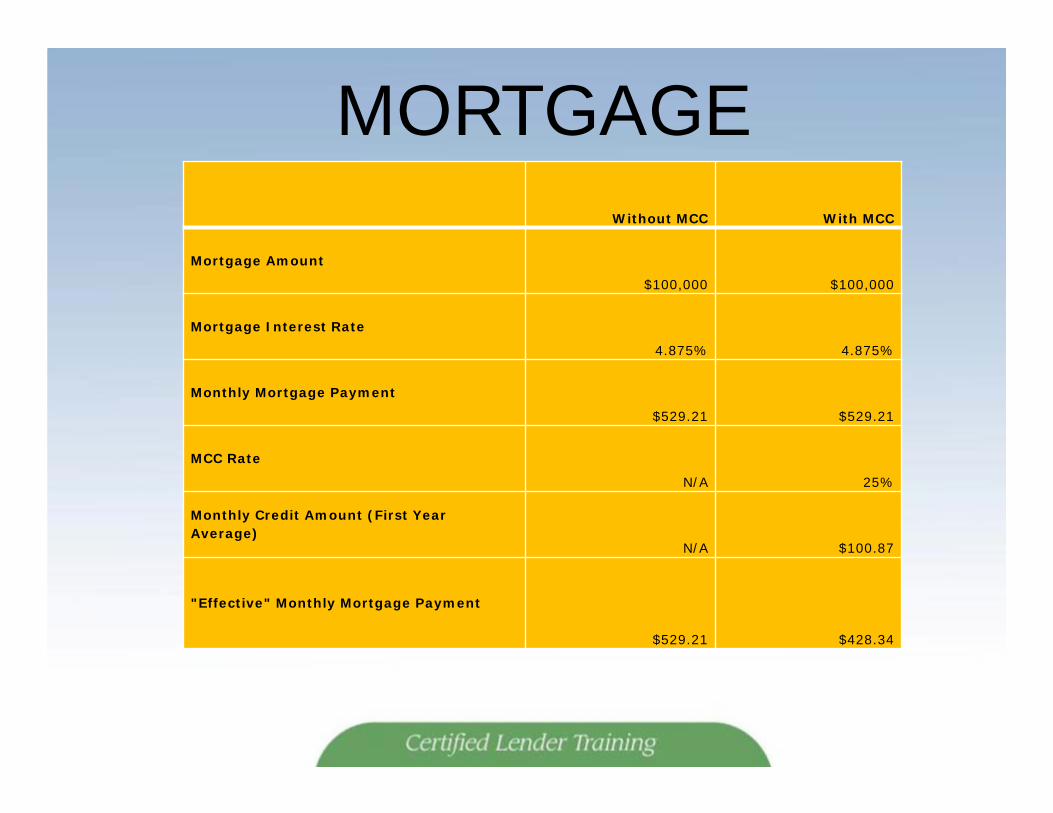

Without MCC With MCC

Mortgage Amount

$100,000 $100,000

Mortgage Interest Rate

4.875% 4.875%

Monthly Mortgage Payment

$529.21 $529.21

MCC Rate

N/A 25%

Monthly Credit Amount (First Year Average)

N/A $100.87

"Effective" Monthly Mortgage Payment

$529.21 $428.34

MORTGAGE

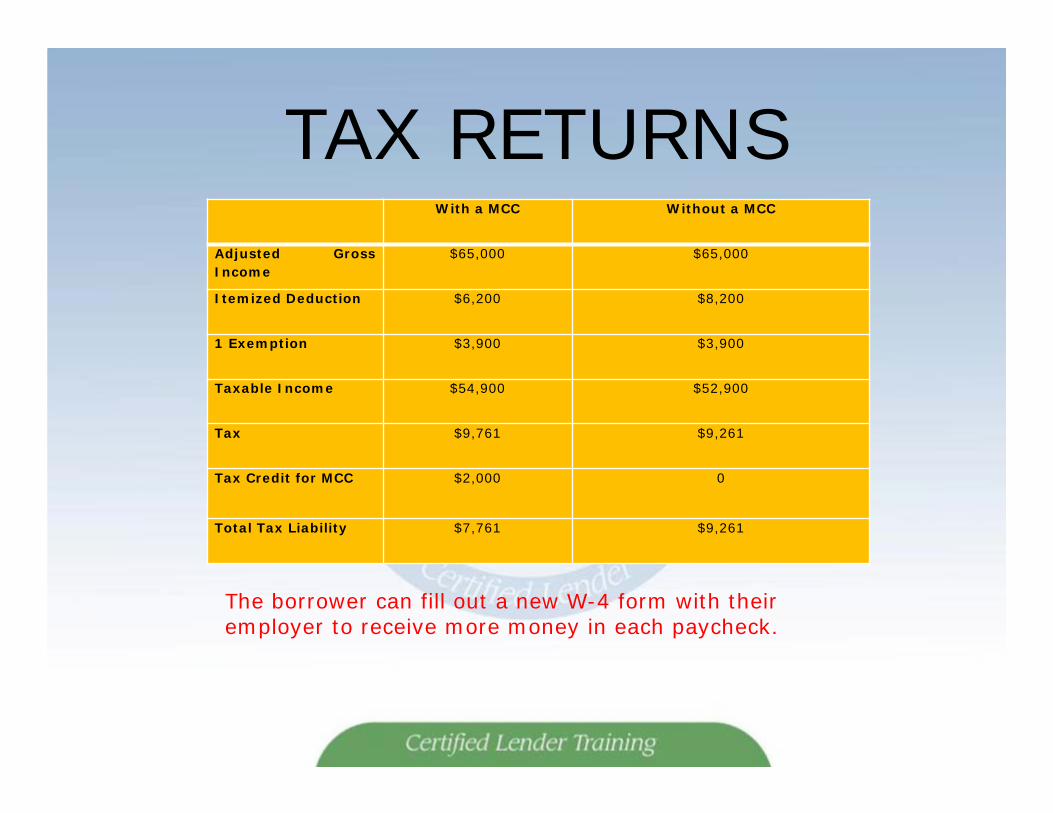

With a MCC Without a MCC

Adjusted GrossIncome

$65,000 $65,000

Itemized Deduction $6,200 $8,200

1 Exemption $3,900 $3,900

Taxable Income $54,900 $52,900

Tax $9,761 $9,261

Tax Credit for MCC $2,000 0

Total Tax Liability $7,761 $9,261

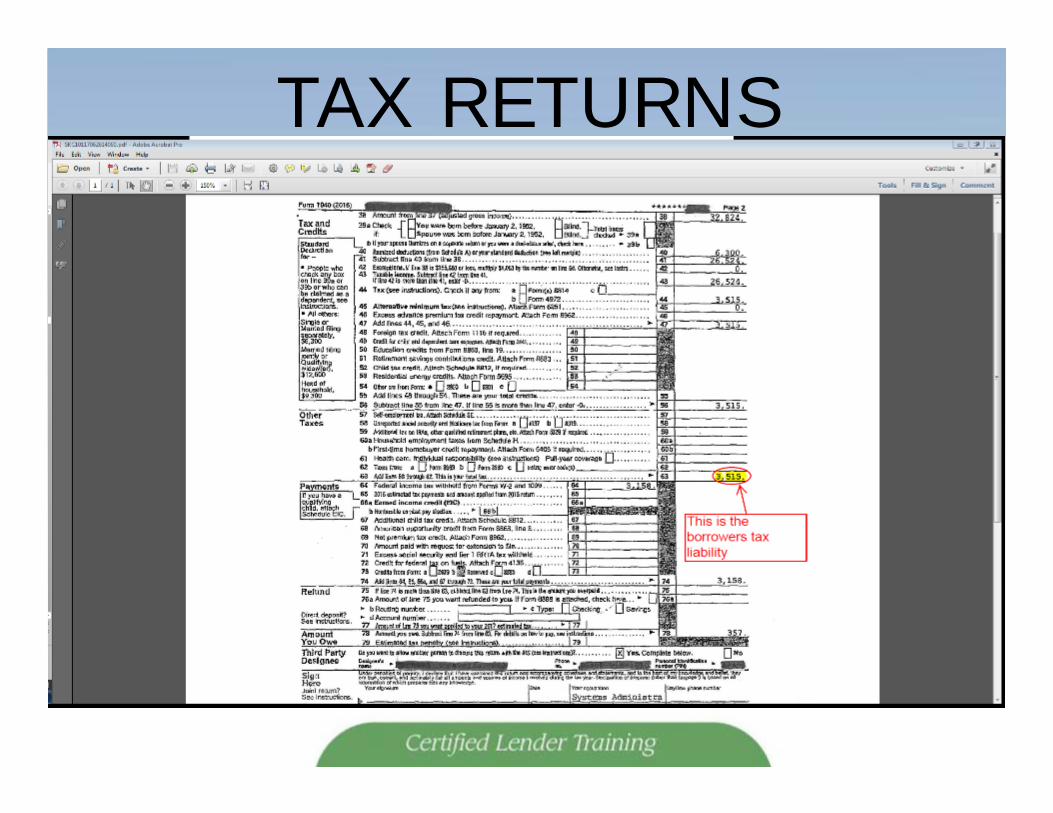

TAX RETURNS

The borrower can fill out a new W-4 form with their employer to receive more money in each paycheck.

TAX RETURNS

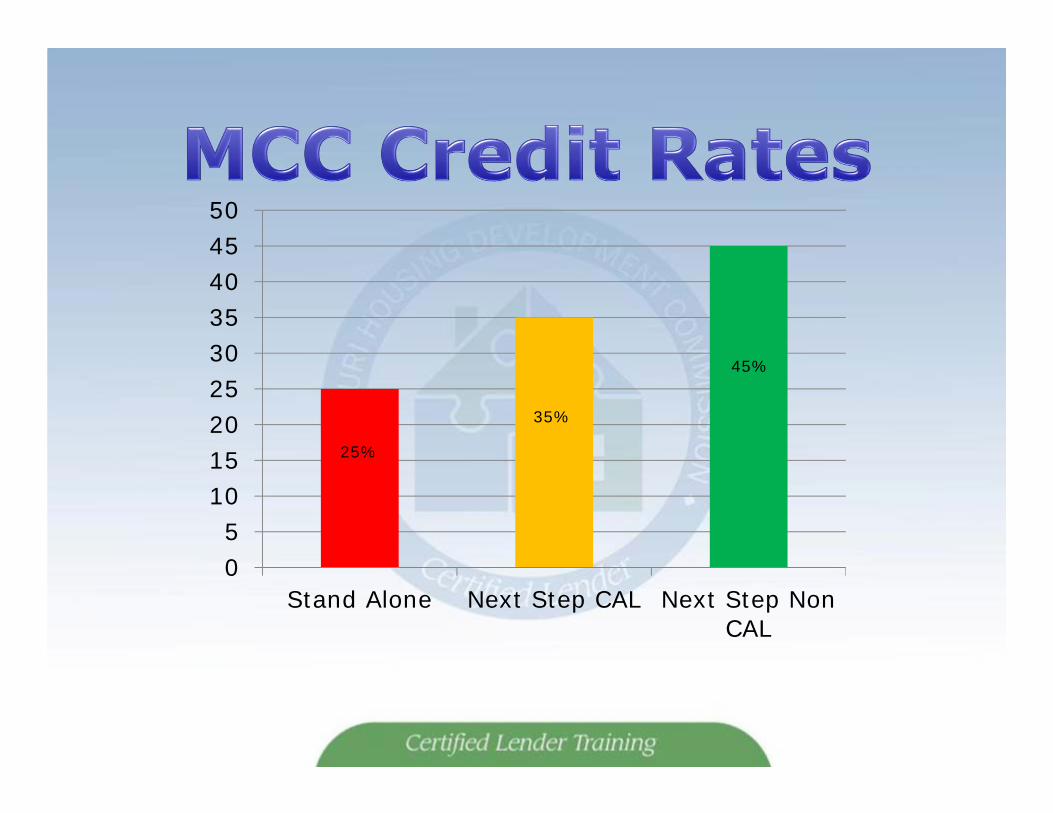

05

101520253035404550

Stand Alone Next Step CAL Next Step NonCAL

35%

45%

25%

MCCStand Alone

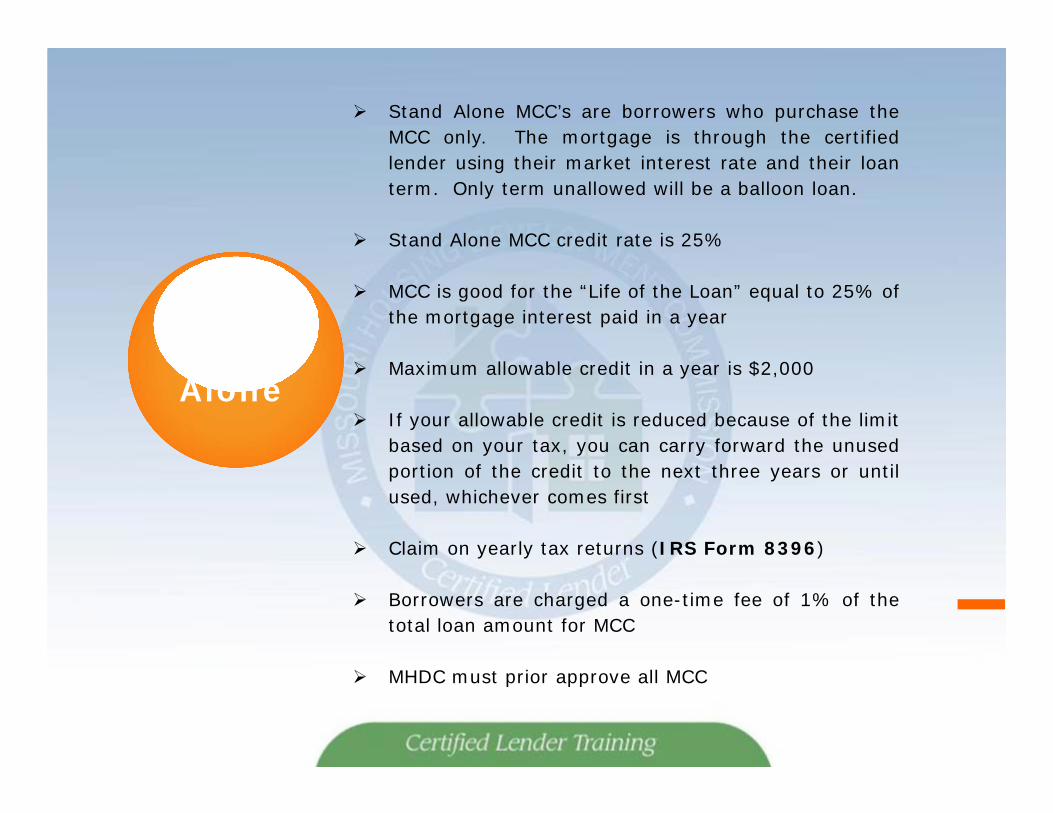

Stand Alone MCC’s are borrowers who purchase theMCC only. The mortgage is through the certifiedlender using their market interest rate and their loanterm. Only term unallowed will be a balloon loan.

Stand Alone MCC credit rate is 25%

MCC is good for the “Life of the Loan” equal to 25% ofthe mortgage interest paid in a year

Maximum allowable credit in a year is $2,000

If your allowable credit is reduced because of the limitbased on your tax, you can carry forward the unusedportion of the credit to the next three years or untilused, whichever comes first

Claim on yearly tax returns (IRS Form 8396)

Borrowers are charged a one-time fee of 1% of thetotal loan amount for MCC

MHDC must prior approve all MCC

MCC-Next Step

CAL(Cash Assistance

Loan)

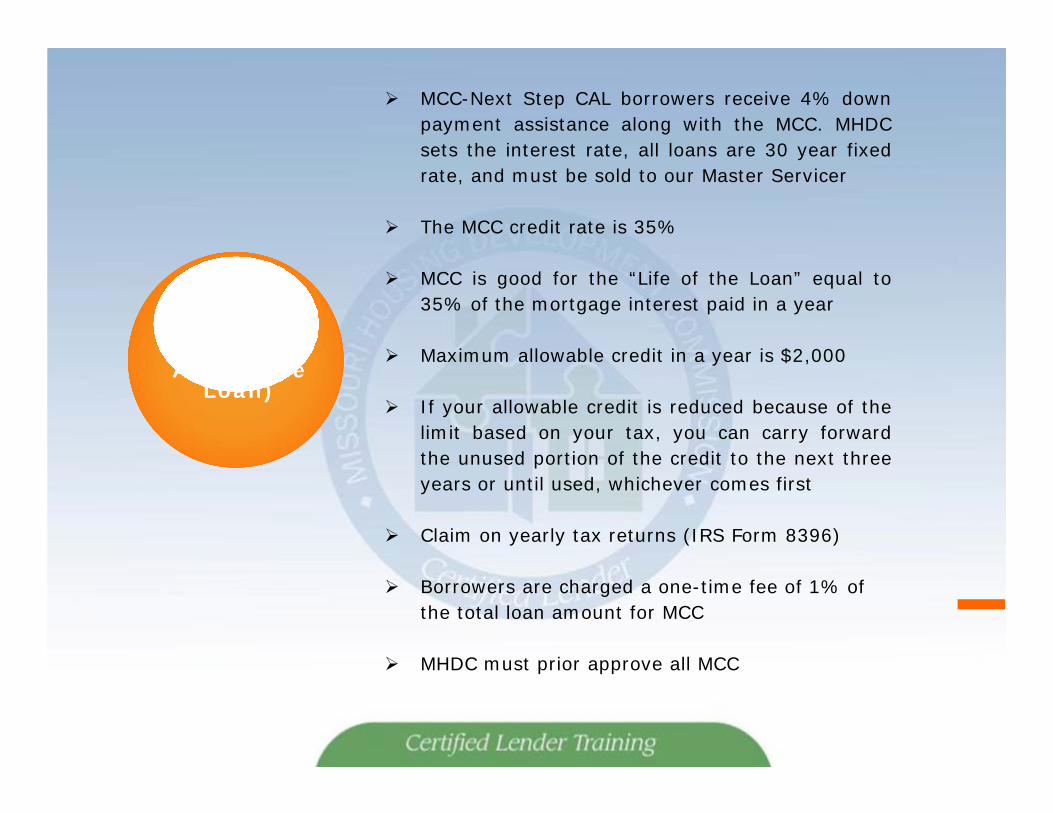

MCC-Next Step CAL borrowers receive 4% downpayment assistance along with the MCC. MHDCsets the interest rate, all loans are 30 year fixedrate, and must be sold to our Master Servicer

The MCC credit rate is 35%

MCC is good for the “Life of the Loan” equal to35% of the mortgage interest paid in a year

Maximum allowable credit in a year is $2,000

If your allowable credit is reduced because of thelimit based on your tax, you can carry forwardthe unused portion of the credit to the next threeyears or until used, whichever comes first

Claim on yearly tax returns (IRS Form 8396)

Borrowers are charged a one-time fee of 1% of the total loan amount for MCC

MHDC must prior approve all MCC

MCC-Next Step

Non CAL(Non Cash

Assistance Loan)

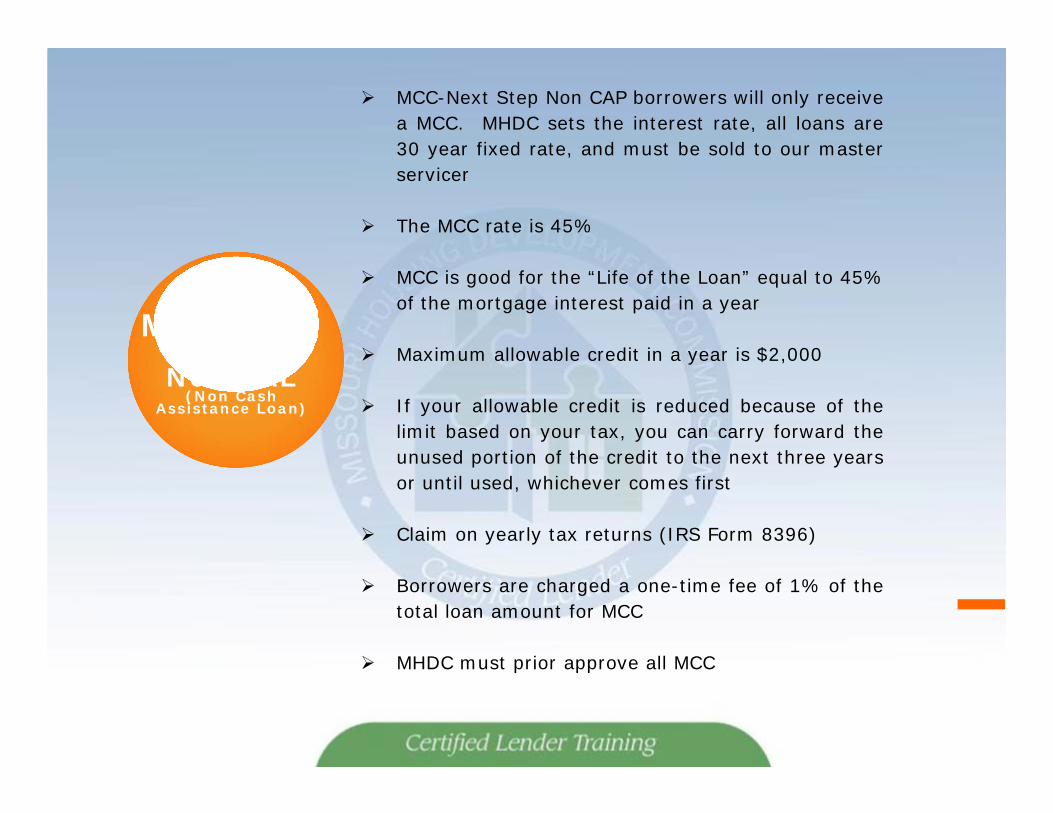

MCC-Next Step Non CAP borrowers will only receivea MCC. MHDC sets the interest rate, all loans are30 year fixed rate, and must be sold to our masterservicer

The MCC rate is 45%

MCC is good for the “Life of the Loan” equal to 45%of the mortgage interest paid in a year

Maximum allowable credit in a year is $2,000

If your allowable credit is reduced because of thelimit based on your tax, you can carry forward theunused portion of the credit to the next three yearsor until used, whichever comes first

Claim on yearly tax returns (IRS Form 8396)

Borrowers are charged a one-time fee of 1% of thetotal loan amount for MCC

MHDC must prior approve all MCC

RESERVATIONS OF FUNDS

• Must have signed application from applicant who hasentered into a fully-executed real estate contractbefore making a reservation

• Must have made preliminary determination thatapplicant qualifies per the financial institutionsguidelines for the mortgage loan

RESERVATIONS OF FUNDS

• To reserve funds, must use Lender On-Line (LOL), theMHDC on-line reservation system

• Funds reserved on individual basis by means of afirst-come, first-serve reservation system

• As soon as confirmation received, loan may close. Ifusing the MCC program you must submit yourapplication package to MHDC after reservation andbefore closing

LENDER ONLINE

Using the MHDC Online system to make a reservation

UTILIZING LENDER ONLINE• Must have access code issued by their administrator

• MHDC will not provide access codes to individuals

• Access the system online at www.mhdc.com/lenders

• Opening screen appears as sign-on field

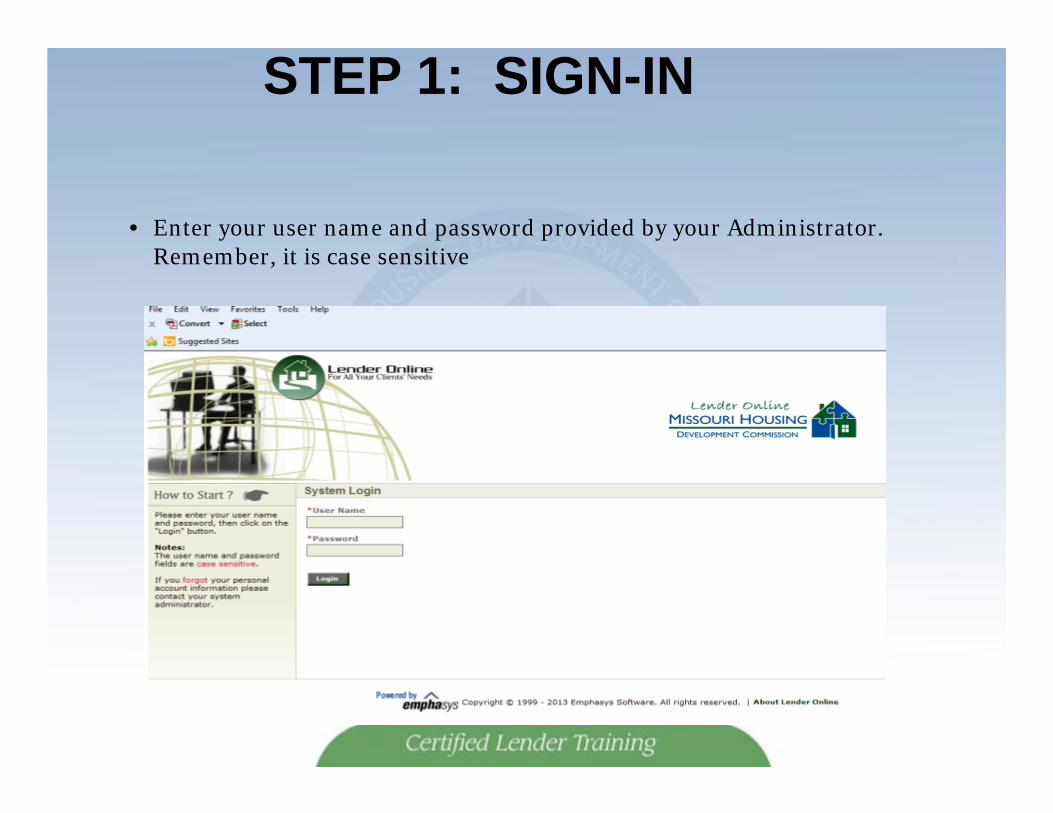

STEP 1: SIGN-IN

• Enter your user name and password provided by your Administrator. Remember, it is case sensitive

STEP 1: SIGN-IN

• Once logged on, the banner screen opens; displays important announcements for lenders (new income limits, new forms, etc.)

• At this screen:– New Reservation – Availability of Funds – Pre-Qualifications– Loan Status– Reports

• Level of access approved by your administrator will dictate which tabs you may access

STEP 2: To enter new reservation, click on “New Reservation” tab

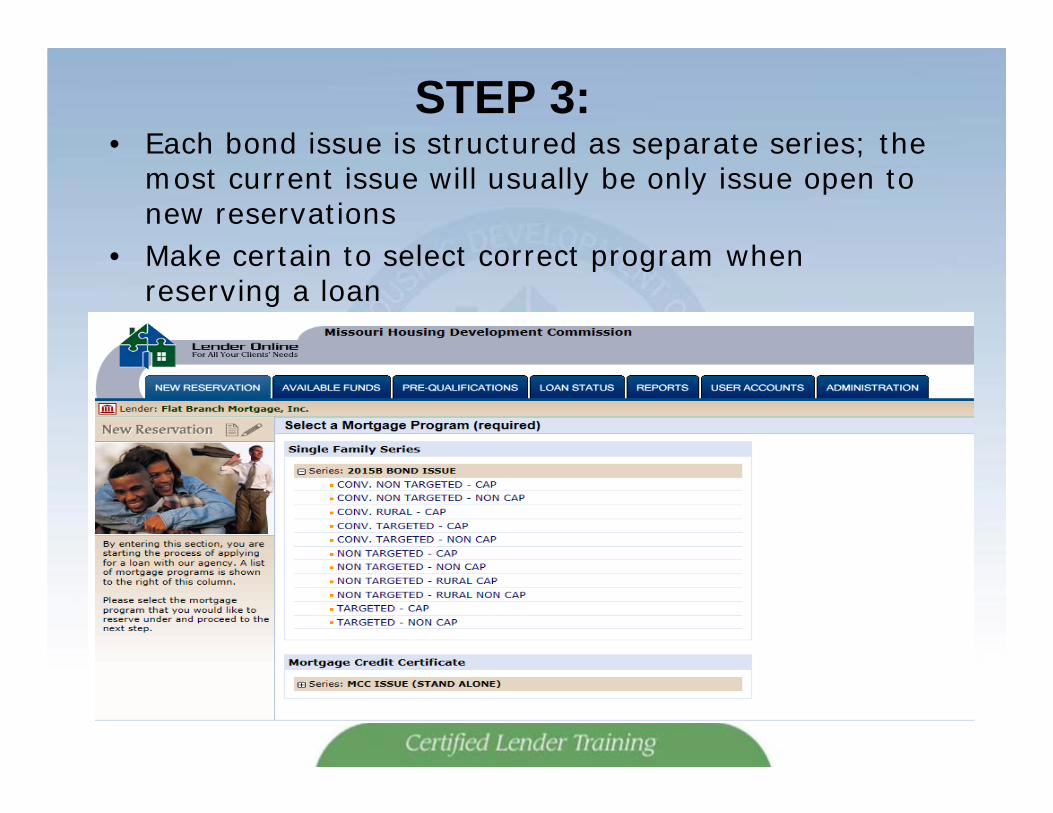

STEP 3: • Each bond issue is structured as separate series; the

most current issue will usually be only issue open to new reservations

• Make certain to select correct program when reserving a loan

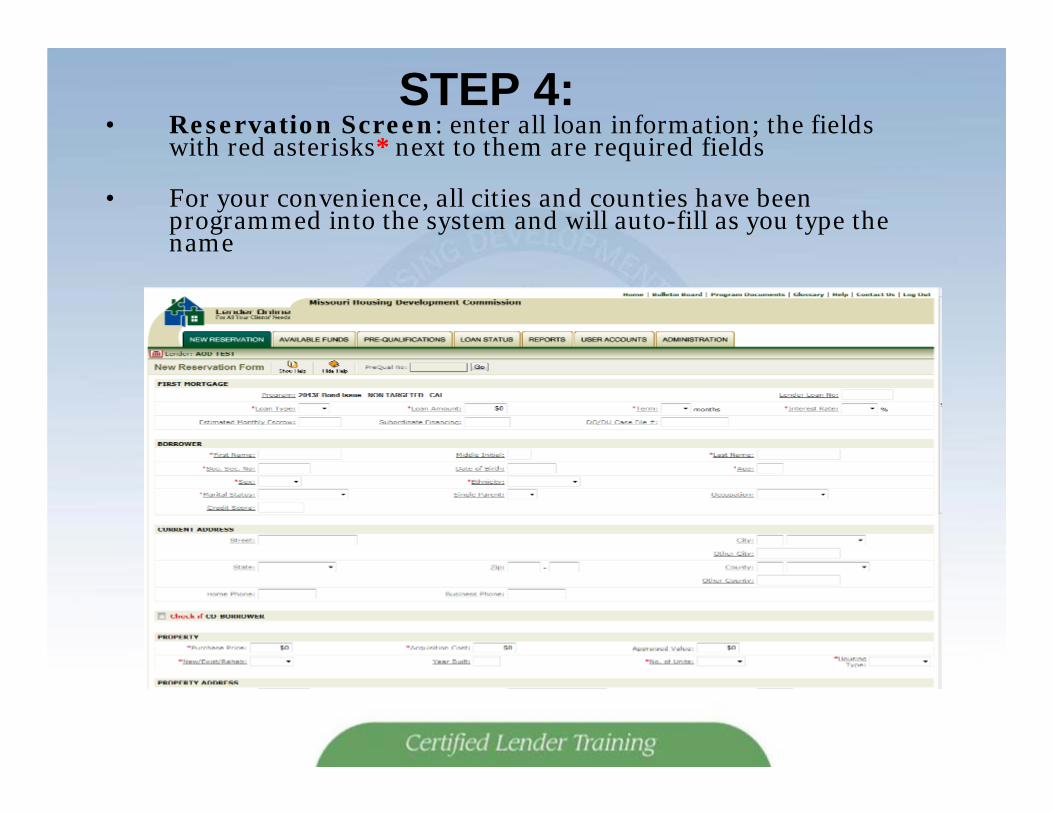

STEP 4: • Reservation Screen: enter all loan information; the fields

with red asterisks* next to them are required fields

• For your convenience, all cities and counties have been programmed into the system and will auto-fill as you type the name

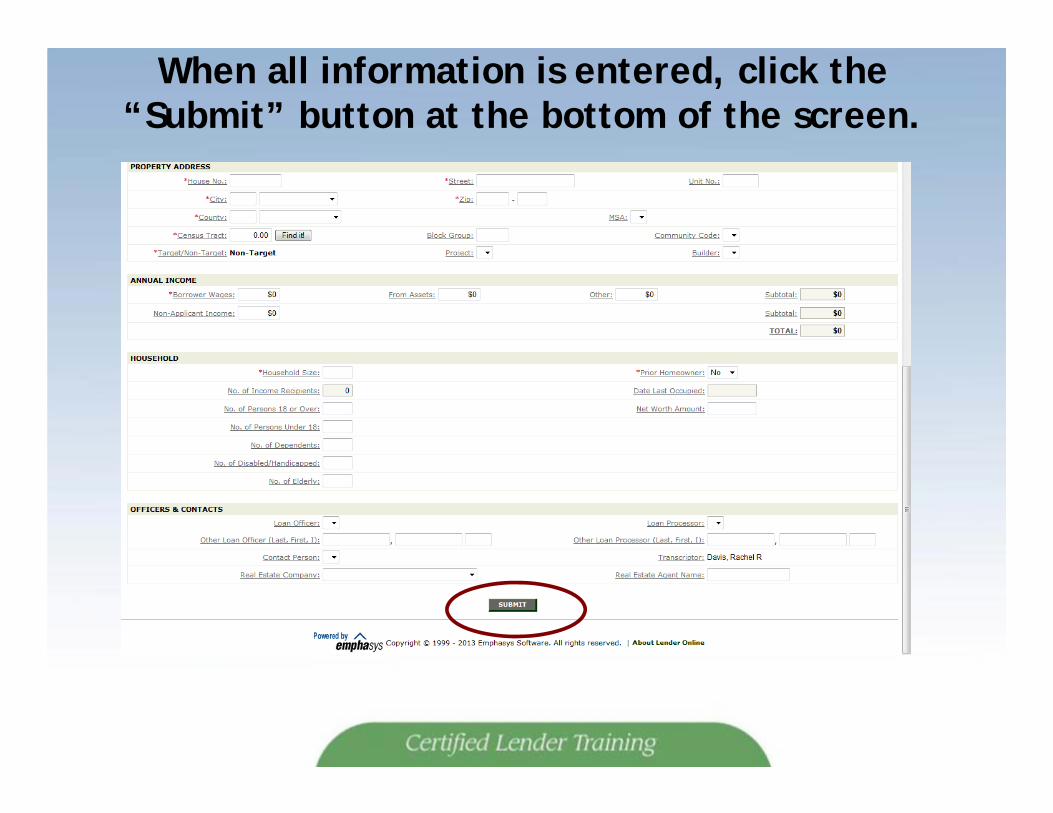

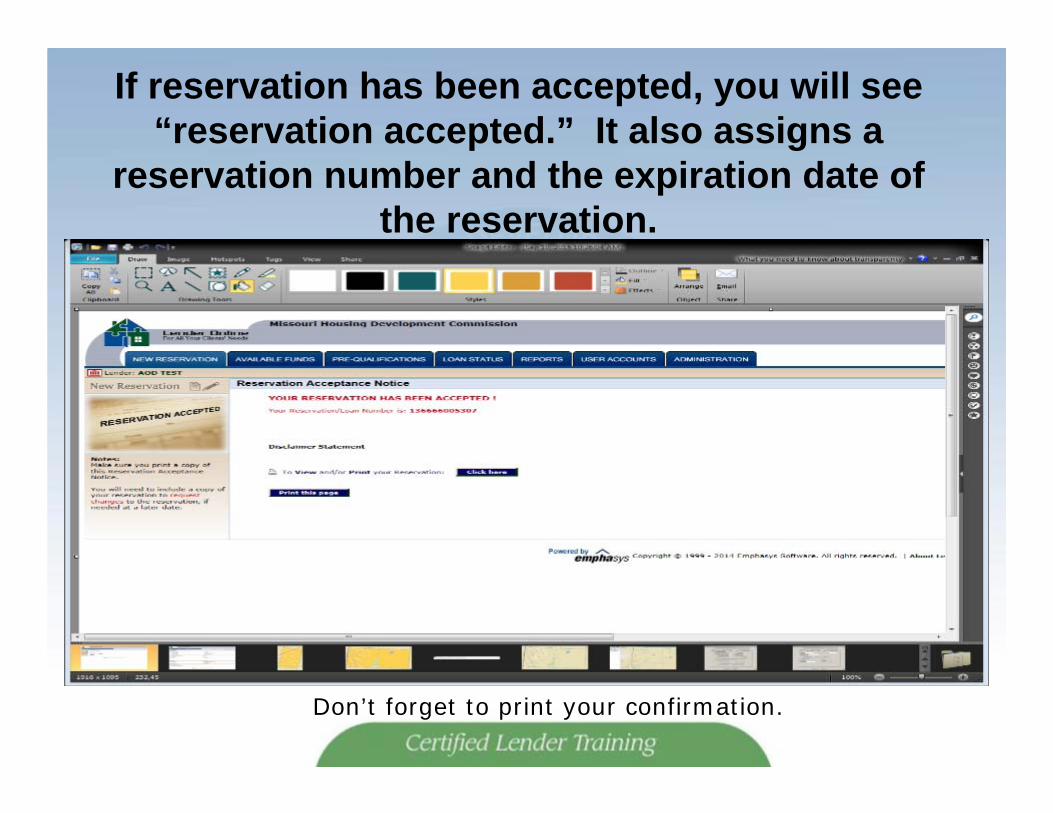

When all information is entered, click the “Submit” button at the bottom of the screen.

If reservation has been accepted, you will see “reservation accepted.” It also assigns a

reservation number and the expiration date of the reservation.

Don’t forget to print your confirmation.

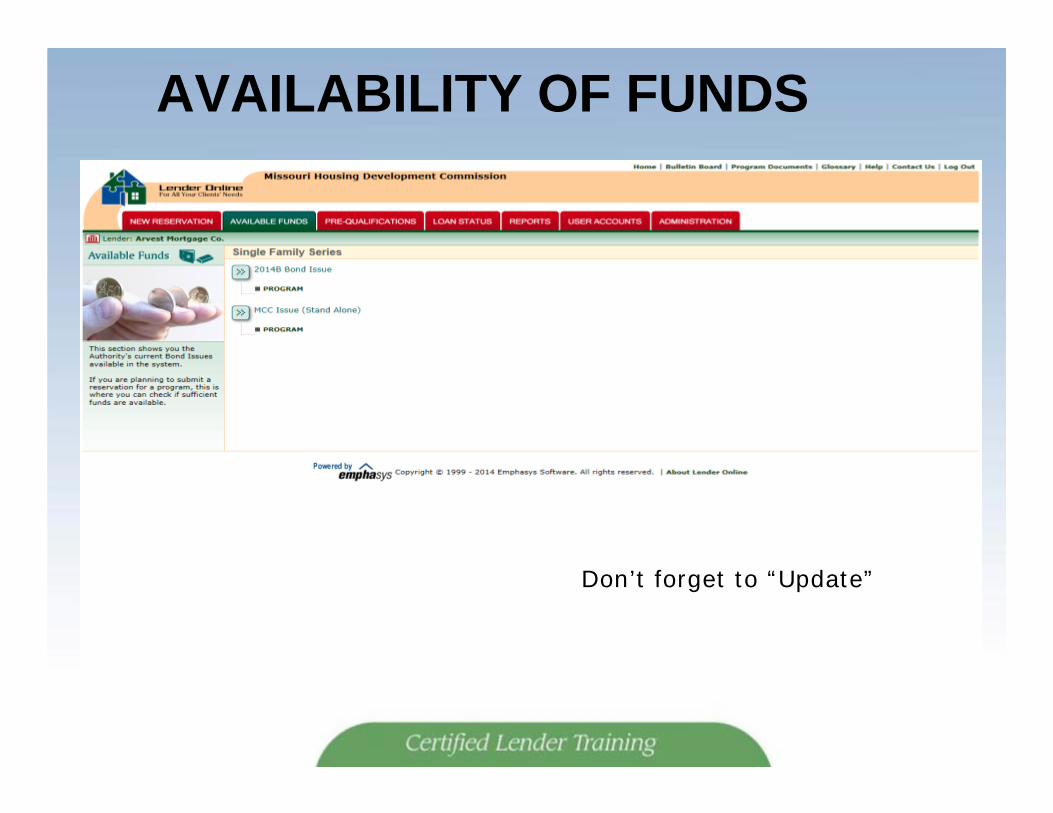

AVAILABILITY OF FUNDS

Don’t forget to “Update”

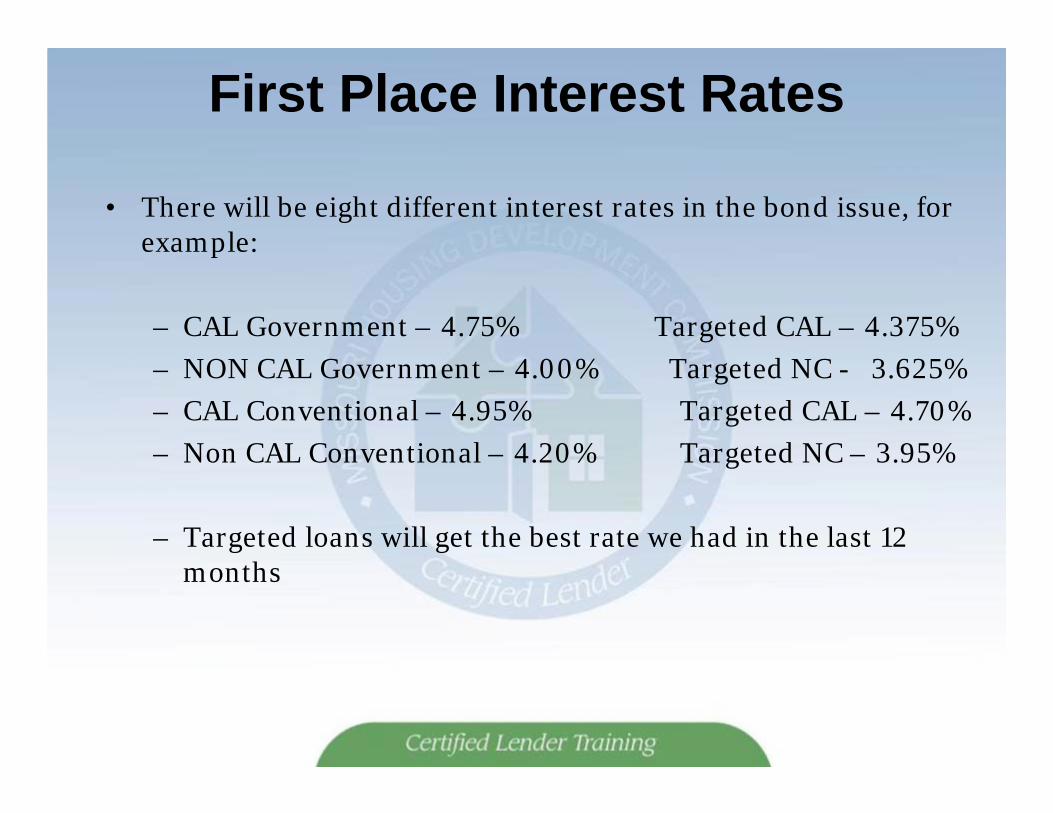

First Place Interest Rates

• There will be eight different interest rates in the bond issue, for example:

– CAL Government – 4.75% Targeted CAL – 4.375%– NON CAL Government – 4.00% Targeted NC - 3.625%– CAL Conventional – 4.95% Targeted CAL – 4.70%– Non CAL Conventional – 4.20% Targeted NC – 3.95%

– Targeted loans will get the best rate we had in the last 12 months

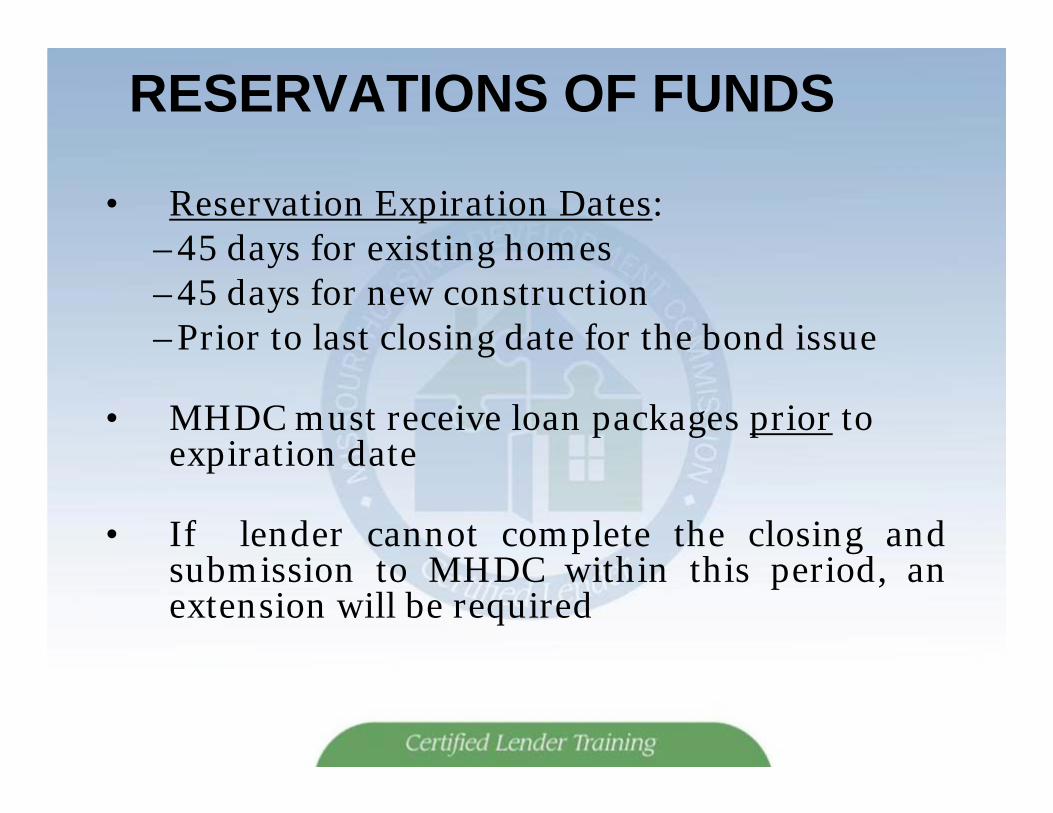

RESERVATIONS OF FUNDS

• Reservation Expiration Dates:–45 days for existing homes–45 days for new construction–Prior to last closing date for the bond issue

• MHDC must receive loan packages prior to expiration date

• If lender cannot complete the closing andsubmission to MHDC within this period, anextension will be required

RESERVATIONS OF FUNDS

• If reservation expires and MHDC has not received request for extension, the reservation will be automatically canceled

• Lenders are required to notify MHDC immediately of any changes

• Approved reservations may not change property address orbe transferred to another participating lender

VERY IMPORTANT

• If you reserve wrong type of funds and they are not availablewhen the loan is closed and shipped, we cannot guarantee thatwe will be able to approve the loan

• If you make a mistake, and find it after you have yourconfirmation, you cannot correct the mistake from the websiteyou must contact MHDC for a correction

CHANGES TO A RESERVATION• To alert MHDC of change: click “Contact Us” at the top of

screen and send email describing the error, and indicate correction being requested

• We will attempt to correct the error, and notify you by return email if we were successful

• Your confirmation number will not change

NOTE: A change of property will require a new reservation.

CHANGES TO A RESERVATION

• Return to the website in the next few hours and view “Loan Status”

• This will confirm your reservation has been corrected

• Print a copy of the screen for a record of the change

Forms on

Lender Online

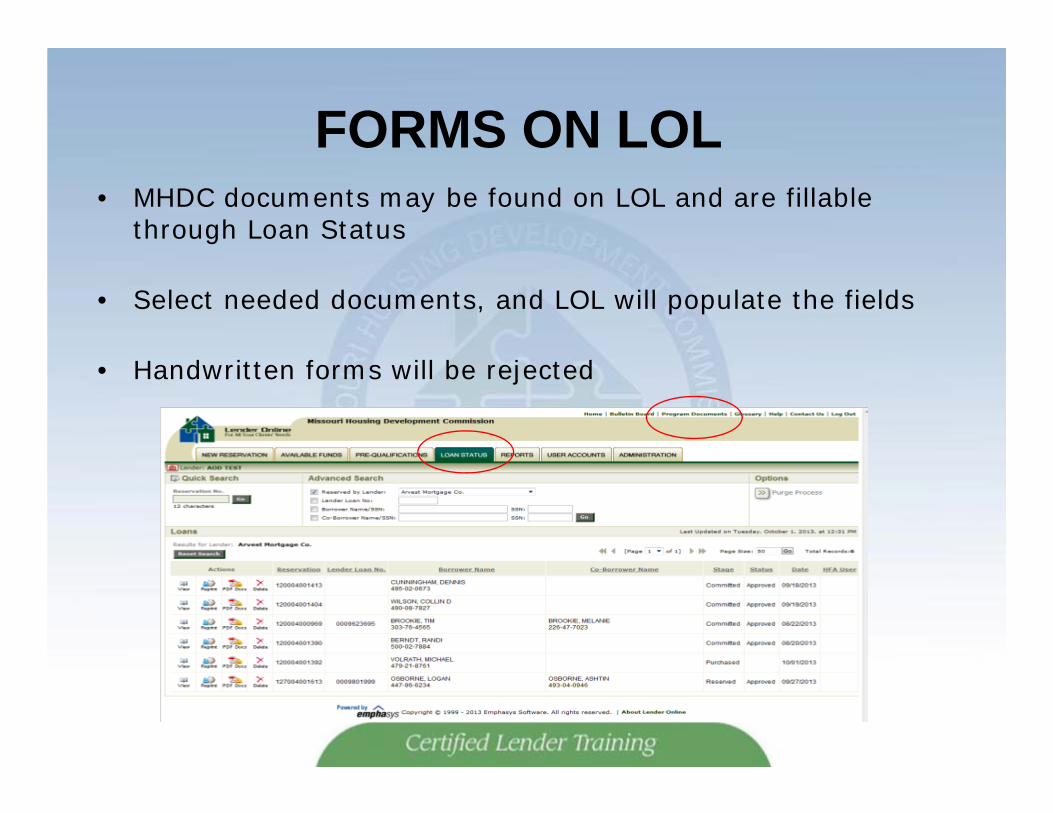

FORMS ON LOL• MHDC documents may be found on LOL and are fillable

through Loan Status

• Select needed documents, and LOL will populate the fields

• Handwritten forms will be rejected

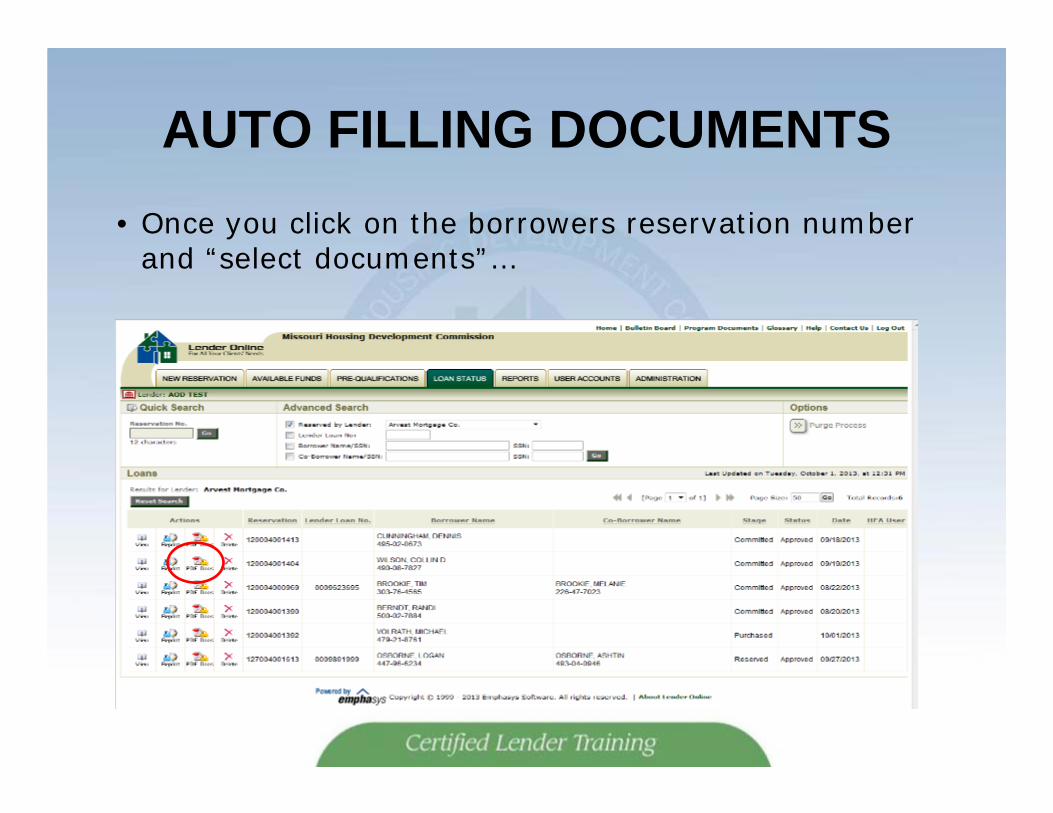

AUTO FILLING DOCUMENTS• Once you click on the borrowers reservation number

and “select documents”…

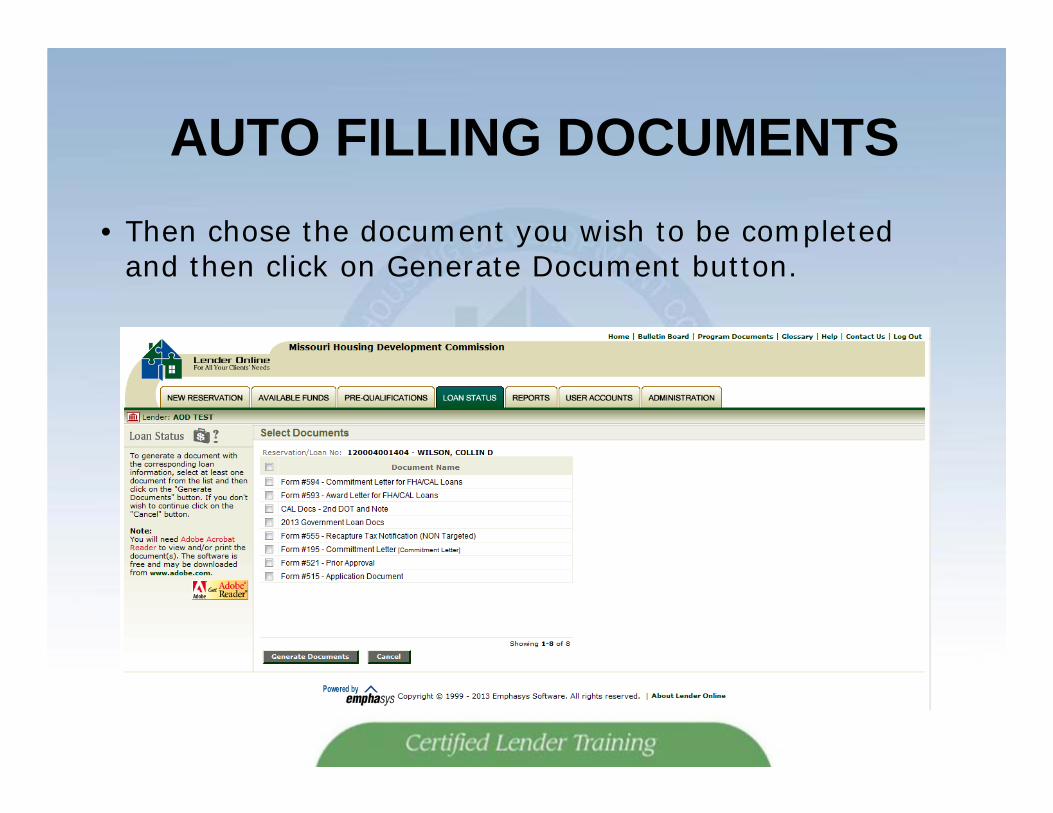

AUTO FILLING DOCUMENTS• Then chose the document you wish to be completed

and then click on Generate Document button.

AUTO FILLING DOCUMENTS

• Remember, this will not complete the entire form.Only the information you entered in at the reservationstage will be entered in the appropriate fields

• You must go through the documents and fill in anyblank fields that were not filled in automatically

• This is also a good time to check to make sure all thedata is accurate and make corrections wherenecessary

REMEMBER TO …• Cancel your own reservations in LOL

• Modify/extend your reservation by emailing any staff member in the homeownership department

• Documents are only accessible through LOL

• Files containing forms not printed from the websitewill be rejected

PLEASE REMEMBER THESEIMPORTANT RULES:

• An expiring reservation will only be extended if the lender has approved the loan

• Loans that have not been approved after 45 days will be cancelled

• To extend a reservation, from LOL, click “contact us”and email any person in the Homeownershipdepartment

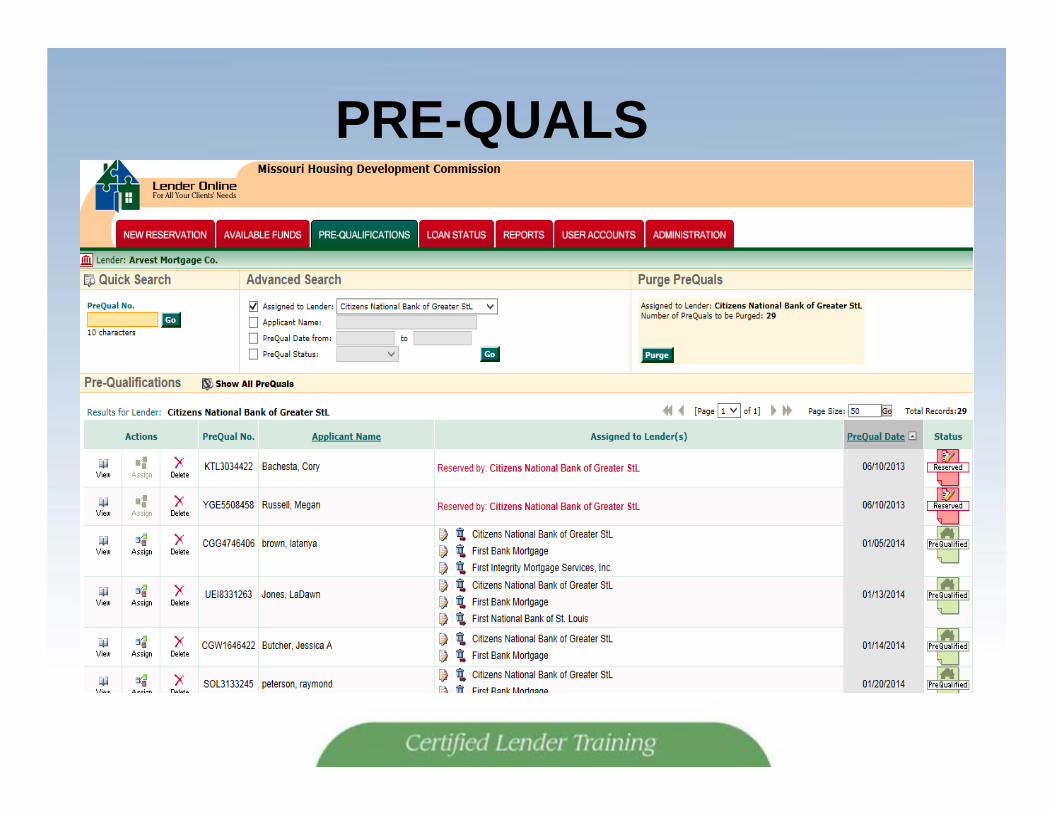

PRE-QUALS• Potential borrowers have an option of pre-qualifying

for the program through our website• This will only pre-qualify them for our program only

(i.e., income, purchase price, FTHB). They will still have to qualify for a mortgage

• Once the borrowers fill out the pre-qual information they will have the option to send it electronically to a maximum of three lenders

• Each lender’s branch office that is listed on our website could receive pre-qual from a borrower

• Each branch should have a contact person and that is who will get the pre-qual notification by email

PRE-QUALS• Once you receive the email notification from the

borrower you will go into LOL and click on your pre-qual tab and find the borrower and click the view button to retrieve their information

• This is basically a sophisticated referral system for you the lender

• Once you have contacted the borrower and have made a determination of whether or not they qualify for a mortgage using the program then you should go back into the system and either remove them from your pipeline or reserve them right from the pre-qual screen

• This is what the screen will look like:

PRE-QUALS

LOAN OFFICER TIP:Taking a Loan Application

• Have MHDC application forms signed

• Be certain to question who will live in the home

• Ask about all forms of income-Child Support, Social Security, etc.

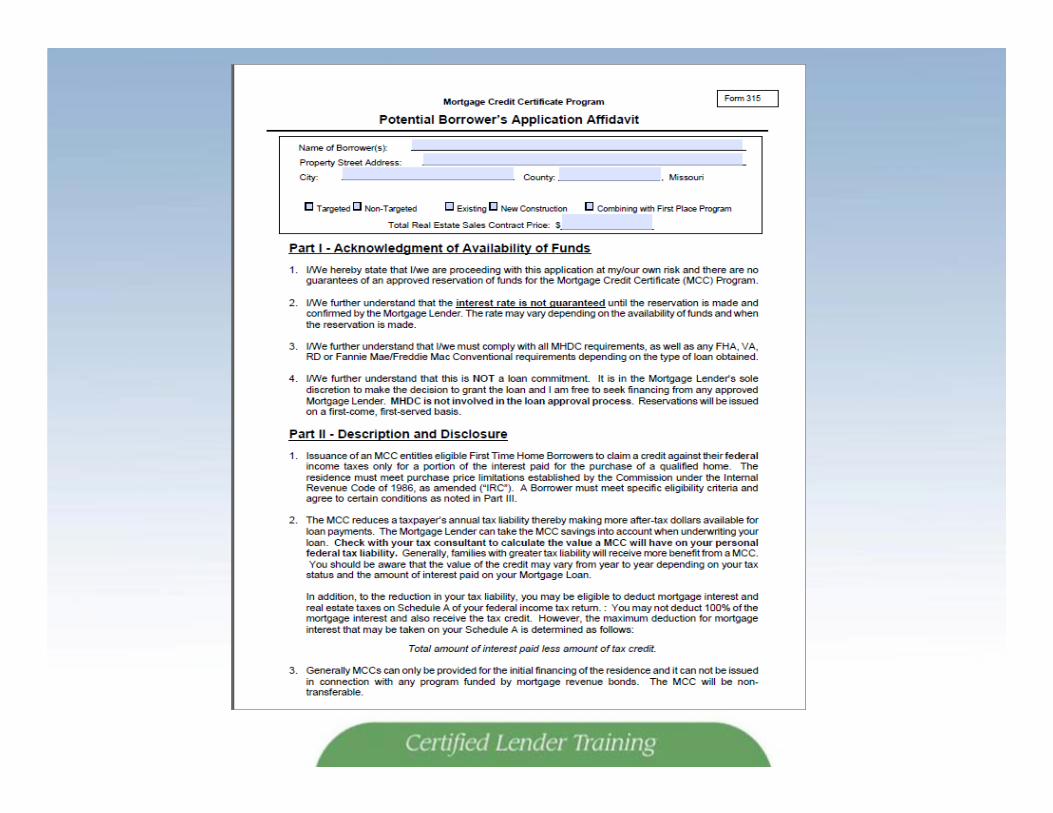

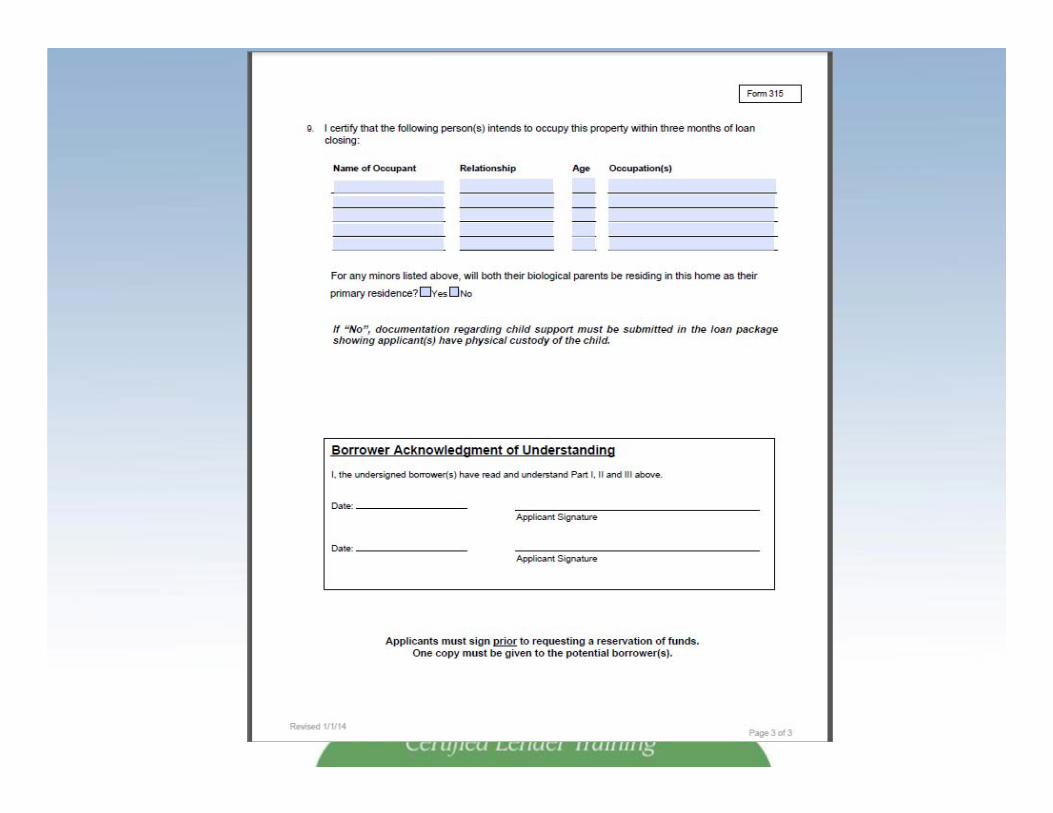

FORMS TO BE SIGNED AT APPLICATION:

• Form #515(MRB)/#315(MCC)/#715(Next Step) (application affidavit). This document will have to be signed at loan application for all loans

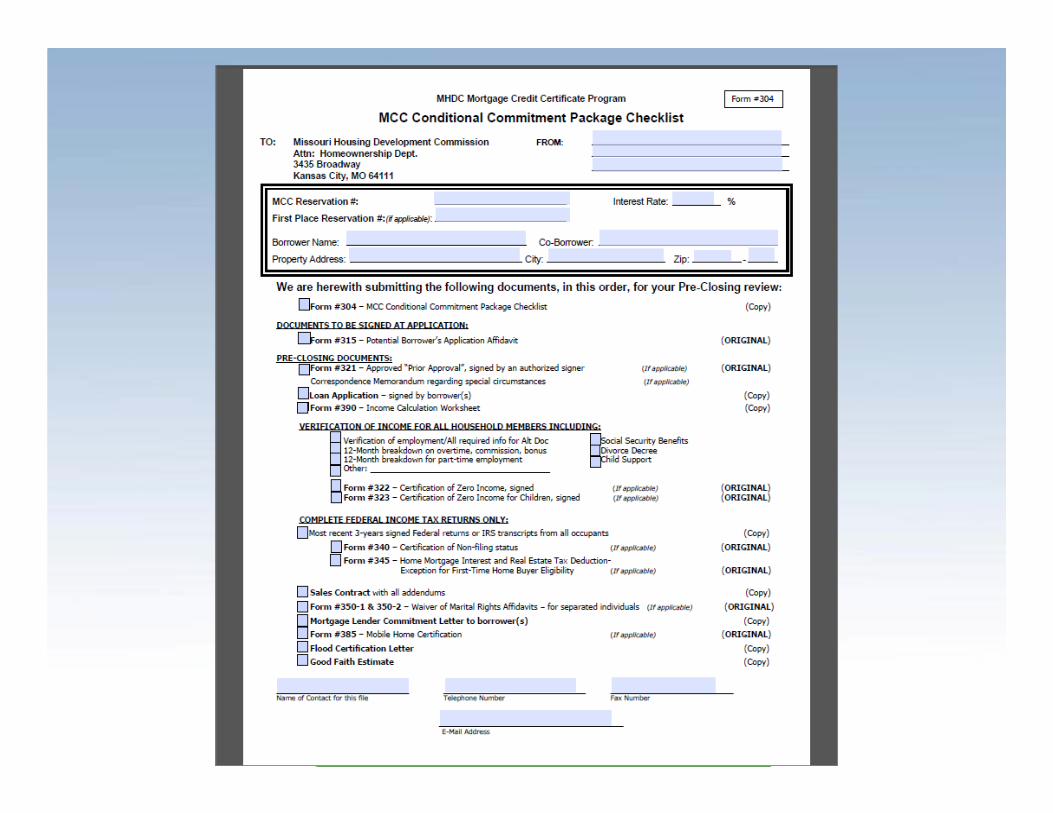

MCC Process

• Once the reservation has been submitted, the certifiedlender must then send the conditional submissionpackage to MHDC for review

• This requires all documentation on the check sheet(form #304)

• The documents must be submitted in the order thatis on the check sheet

Conditional Commitment

• Once MHDC reviews the conditional commitmentpackage, it will either send a deficiency letter to thelender or a conditional commitment

• Conditional commitment (form #394) will be emailedto the lender

• Once the lender receives the form #394 they can nowclose the loan

• If any major changes happen between conditionalcommitment and closing, the lender should notifyMHDC immediately in order to keep the MCCcommitment

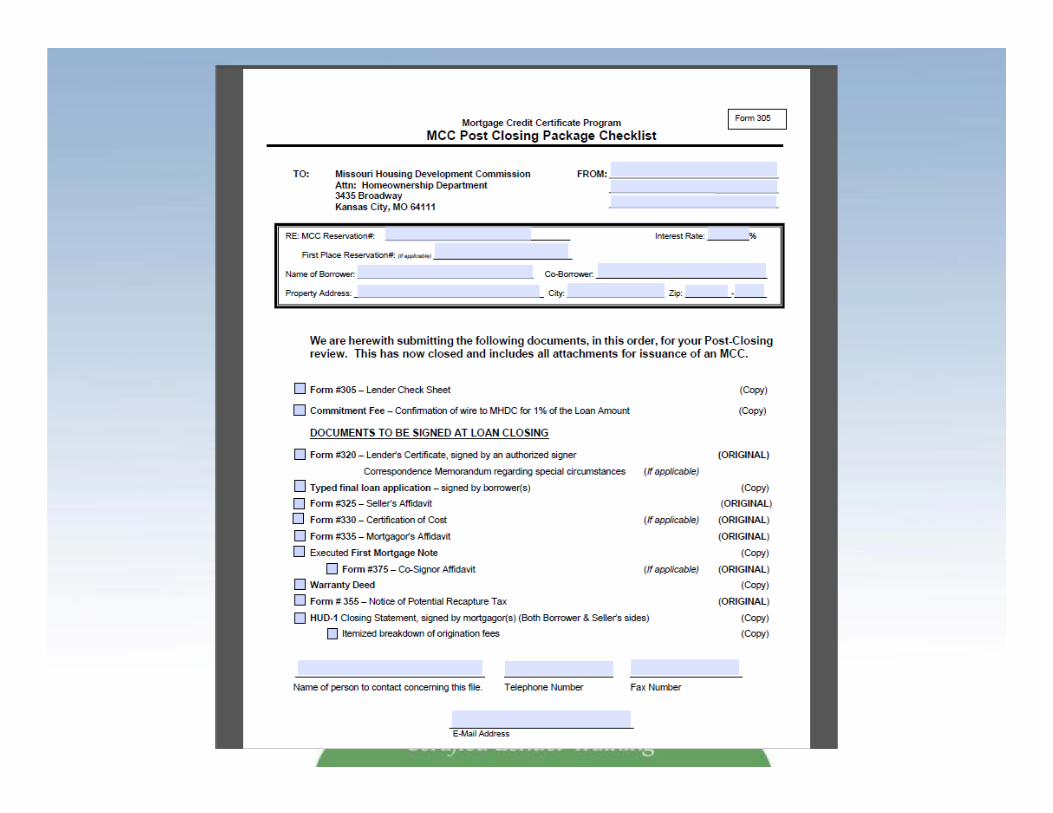

MCC Final Submission Package• After the loan has closed the lender should submit to

MHDC the final loan package• Documents should be sent in the order of the check

sheet (form #305)• Lenders are to wire the MCC fee (1% of the total loan

amount) to MHDC

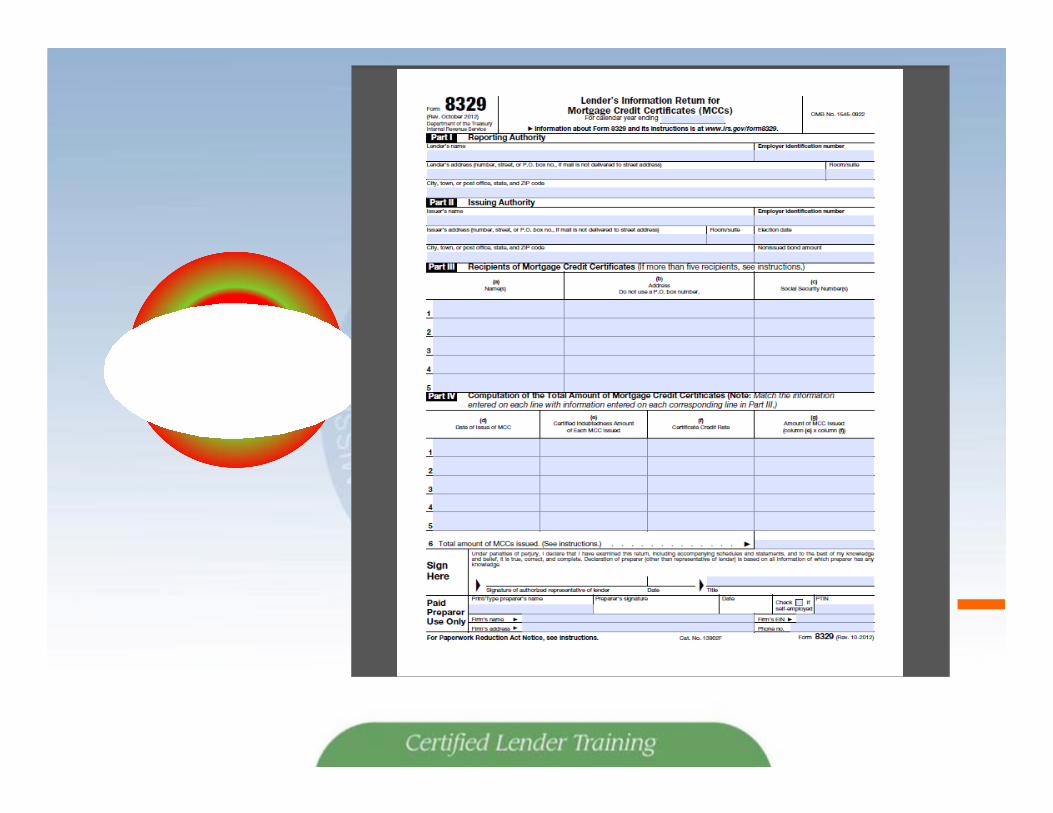

MCC Annual Reporting

• At the end of every year MHDC will send each lender a report of the MCC’s that were issued to each borrower for that calendar year

• Each lender that had their borrower use the MCC program will have to report to the IRS the list of borrowers who received the MCC

• Lender will do this by filing IRS form 8329

IRS(ANNUAL

REPORTING)

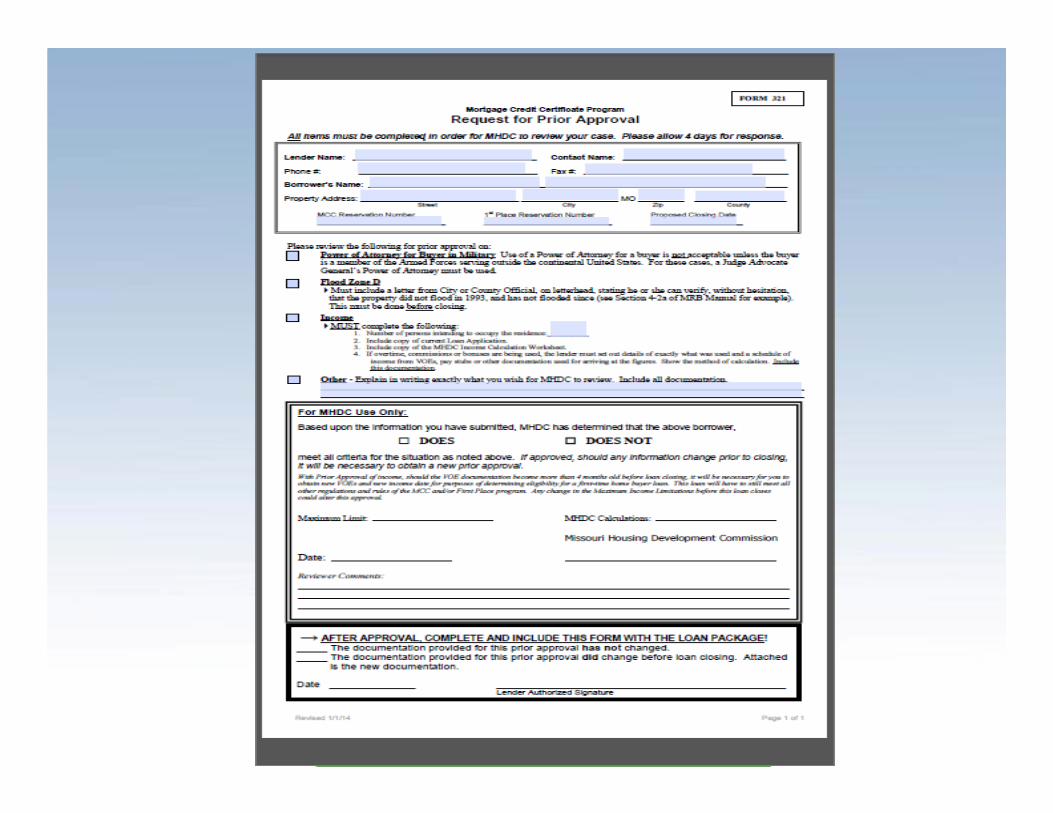

ITEMS REQUIRING PRIOR APPROVAL:1. Flood Zone D (non-mapped area)2. Power of Attorney for Active Duty Military borrowers3. Escrows for repairs

A lender may, and should, submit any unusual item to MHDC for prior approval if uncertain of the acceptability of the item.

• Income close to maximum

• Tax returns

USES OF POWERS OF ATTORNEY• Active duty military personnel currently stationed

outside the continental United States may present a JAG Power of Attorney in lieu of mailing documents to the buyer

• This must come from the office of the Judge AdvocateGeneral

ESCROWING FOR REPAIRS

• MHDC documents state that all funds that have been dispersed-escrows should be used rarely, if at all

• Any item escrowed must be weatherrelated or be a foreclosed or REO property

• The title company must escrow 1.5 times the bid

BUYERS PAYING FOR REPAIRS

• Buyer may not pay more for the property than the appraised value

• Therefore, if the appraised value and the sales price are the same, the buyer may not pay for any repairs

• If repairs cannot be completed prior to closing dueto weather conditions, prior approval of escrow forrepairs is required

CALCULATING BORROWER INCOME

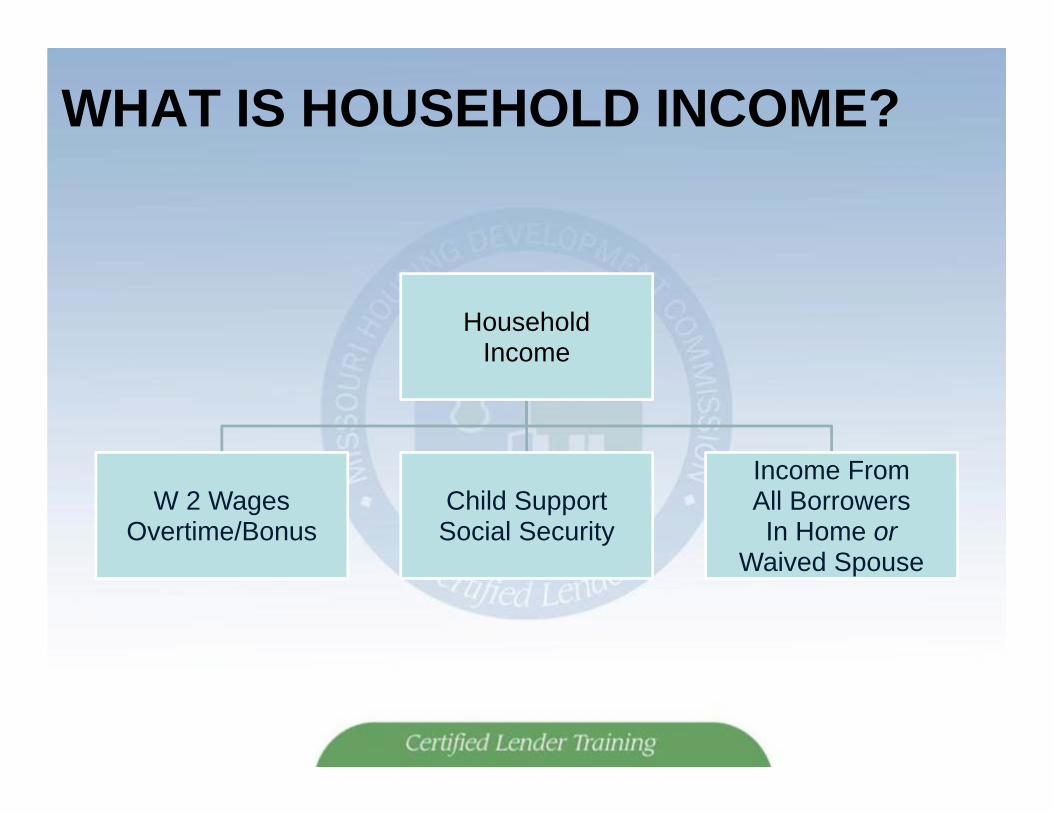

WHAT IS HOUSEHOLD INCOME?

HouseholdIncome

W 2 WagesOvertime/Bonus

Child SupportSocial Security

Income From All Borrowers In Home or

Waived Spouse

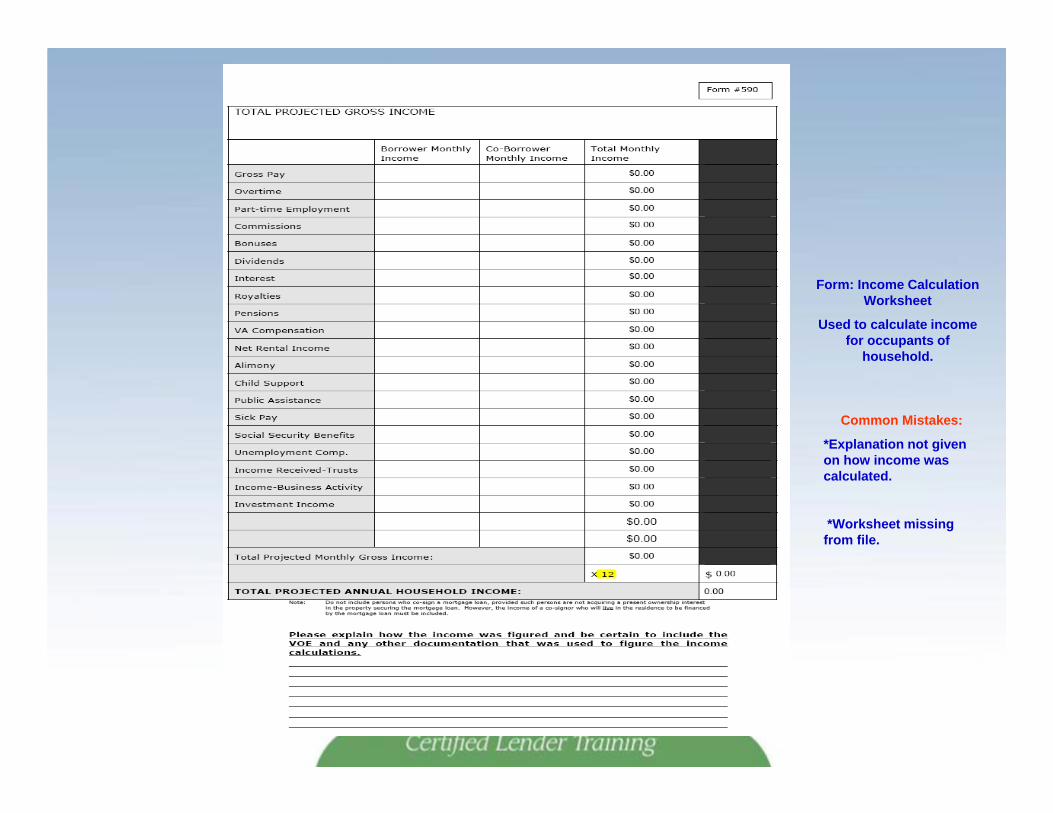

Form: Income Calculation Worksheet

Used to calculate income for occupants of

household.

Common Mistakes:

*Explanation not given on how income was calculated.

*Worksheet missing from file.

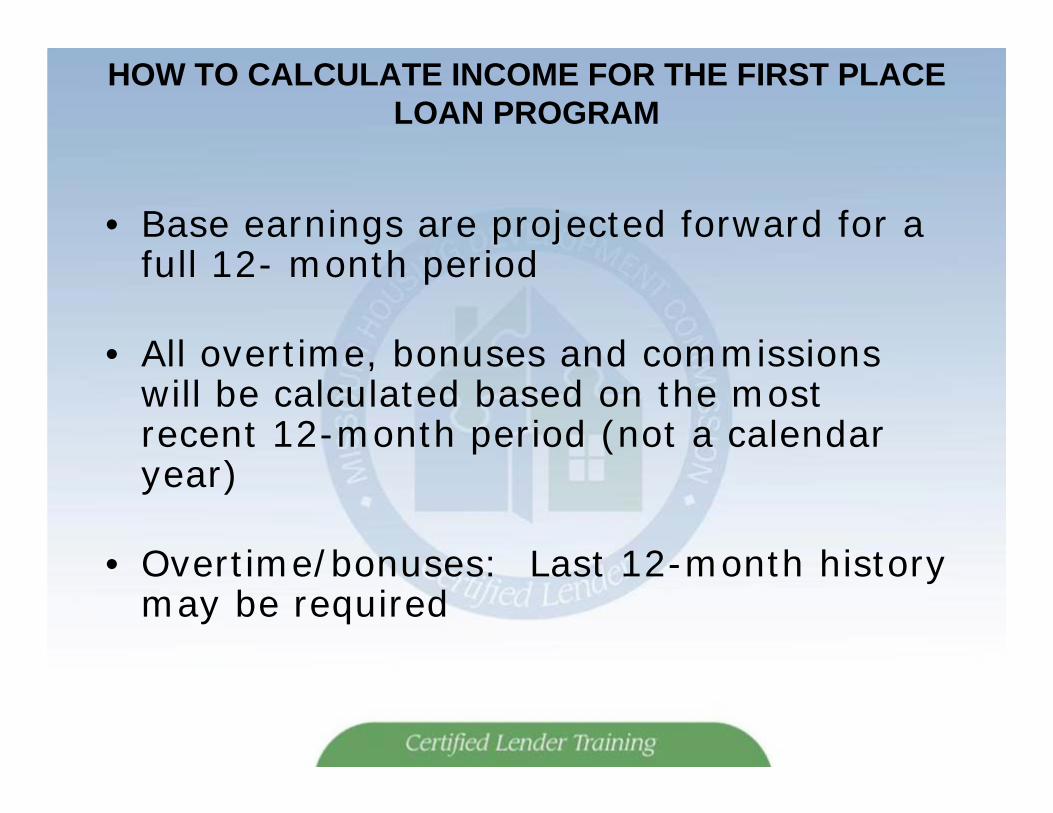

HOW TO CALCULATE INCOME FOR THE FIRST PLACE LOAN PROGRAM

• Base earnings are projected forward for a full 12- month period

• All overtime, bonuses and commissions will be calculated based on the most recent 12-month period (not a calendar year)

• Overtime/bonuses: Last 12-month historymay be required

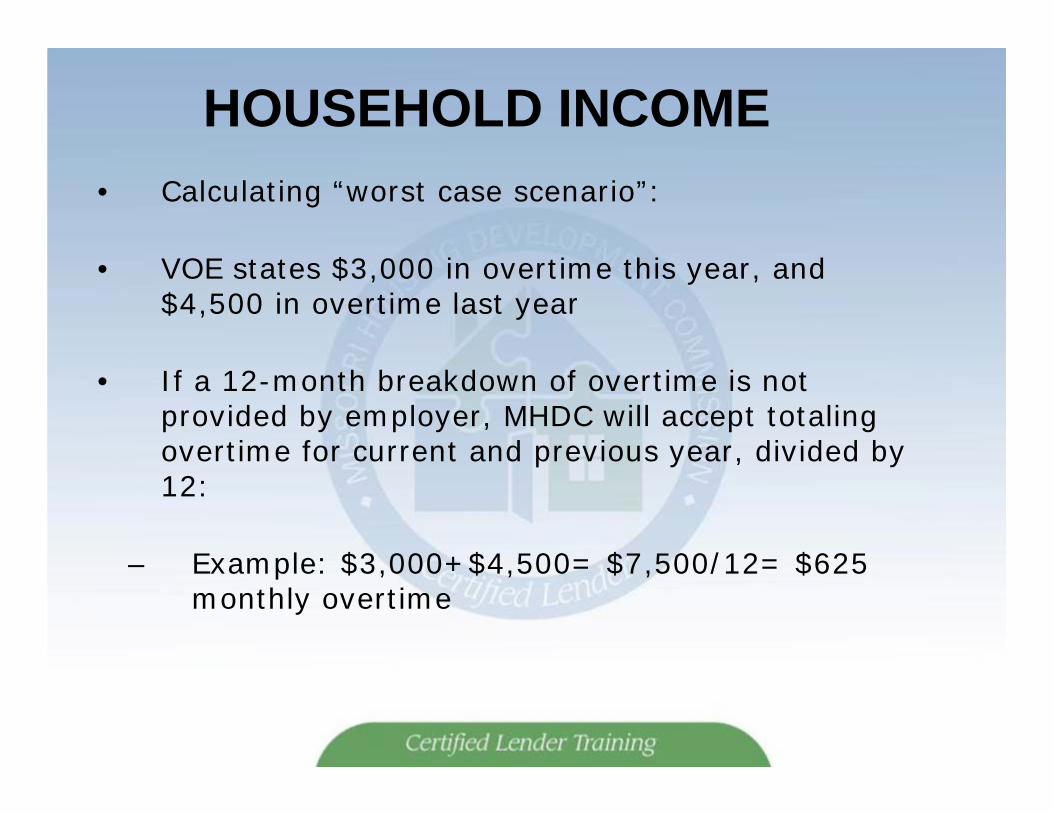

HOUSEHOLD INCOME• Calculating “worst case scenario”:

• VOE states $3,000 in overtime this year, and $4,500 in overtime last year

• If a 12-month breakdown of overtime is not provided by employer, MHDC will accept totaling overtime for current and previous year, divided by 12:

– Example: $3,000+$4,500= $7,500/12= $625 monthly overtime

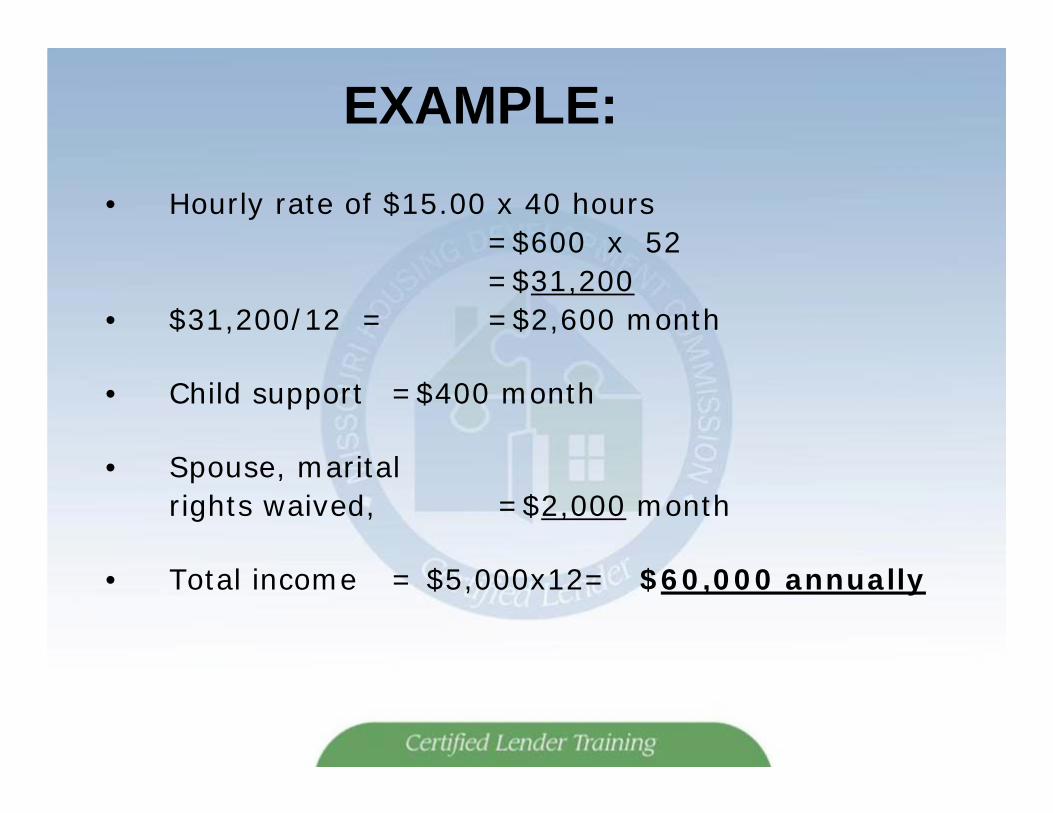

EXAMPLE:• Hourly rate of $15.00 x 40 hours

=$600 x 52 =$31,200

• $31,200/12 = =$2,600 month

• Child support =$400 month

• Spouse, marital rights waived, =$2,000 month

• Total income = $5,000x12= $60,000 annually

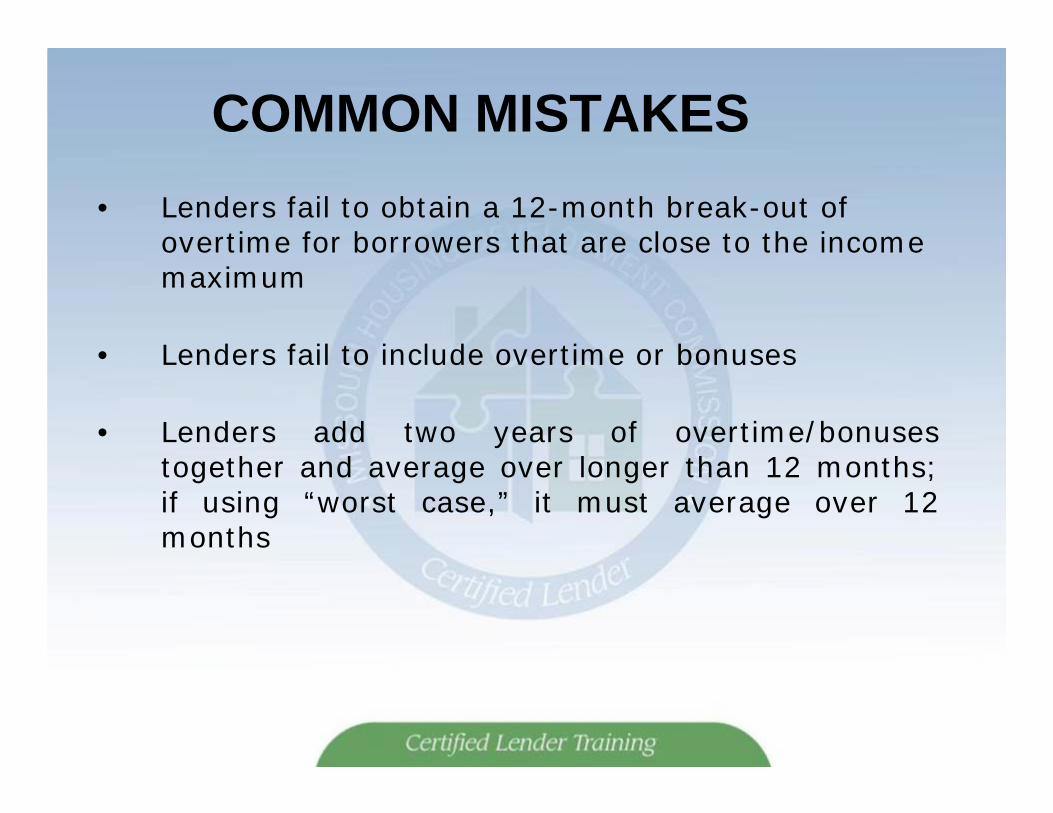

COMMON MISTAKES• Lenders fail to obtain a 12-month break-out of

overtime for borrowers that are close to the income maximum

• Lenders fail to include overtime or bonuses

• Lenders add two years of overtime/bonusestogether and average over longer than 12 months;if using “worst case,” it must average over 12months

VERIFICATION OF EMPLOYMENT• Alternative documentation is acceptable, but must

follow MHDC guidelines

• VOE must not be over four months old on the day of closing

• MHDC will accept The Work Number for Everyone, but requires full version/YTD totals

• Remember, MHDC uses the last 12 months ofincome for OT, bonuses and commission. Lendermust obtain a breakdown of overtime, commissions,etc. if necessary

OTHER FORMS OF INCOME

• Self-employment

• Child support

• Seasonal

• Unemployment

• Interest Income

DIFFERENCE IN CALCULATION FOR SELF-EMPLOYED PERSON

• Income listed on line 12 (net earnings) of the 1040 is used

• MHDC does not average income over several tax years

• Deductions are allowed, but all depreciation must be straight-line (Schedule C)

• Be certain to include the borrowers’ portionof retained earnings for partnerships and S-corporations

SEASONAL/IRREGULAR INCOME• Use the exact amount received in the previous 12-

month period

• If on the job less than 12-months, divide totalincome by months worked, then project forward toobtain 12-month income figure

• Example:$17,653/8 =$2,206.62 monthly, $2,206.62 x 12 =$26,479.50 annually

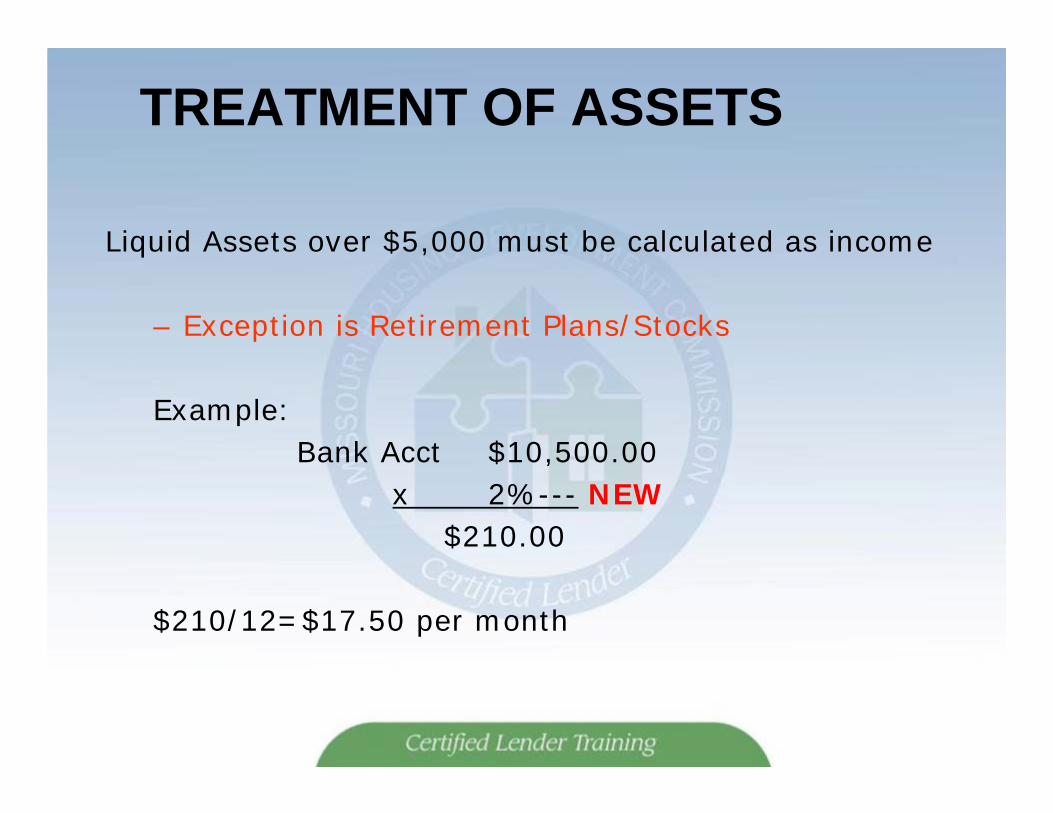

TREATMENT OF ASSETS

Liquid Assets over $5,000 must be calculated as income

– Exception is Retirement Plans/Stocks

Example:Bank Acct $10,500.00

x 2%--- NEW$210.00

$210/12=$17.50 per month

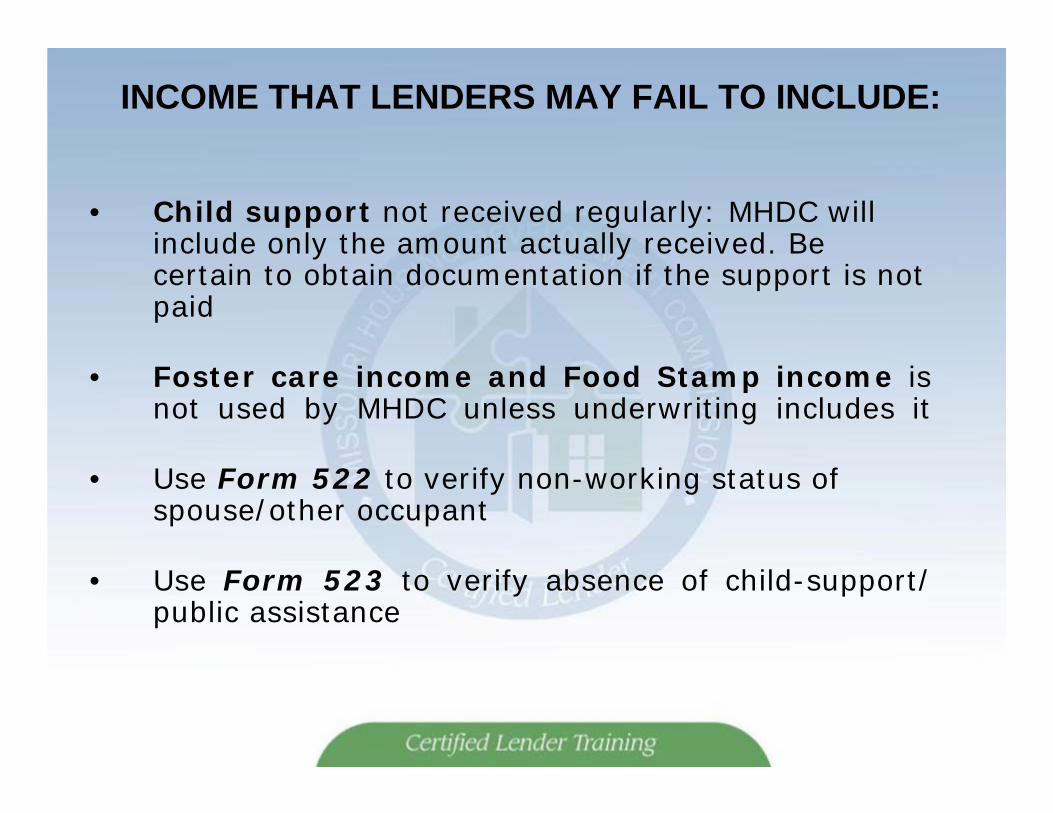

INCOME THAT LENDERS MAY FAIL TO INCLUDE:

• Child support not received regularly: MHDC will include only the amount actually received. Be certain to obtain documentation if the support is not paid

• Foster care income and Food Stamp income isnot used by MHDC unless underwriting includes it

• Use Form 522 to verify non-working status of spouse/other occupant

• Use Form 523 to verify absence of child-support/public assistance

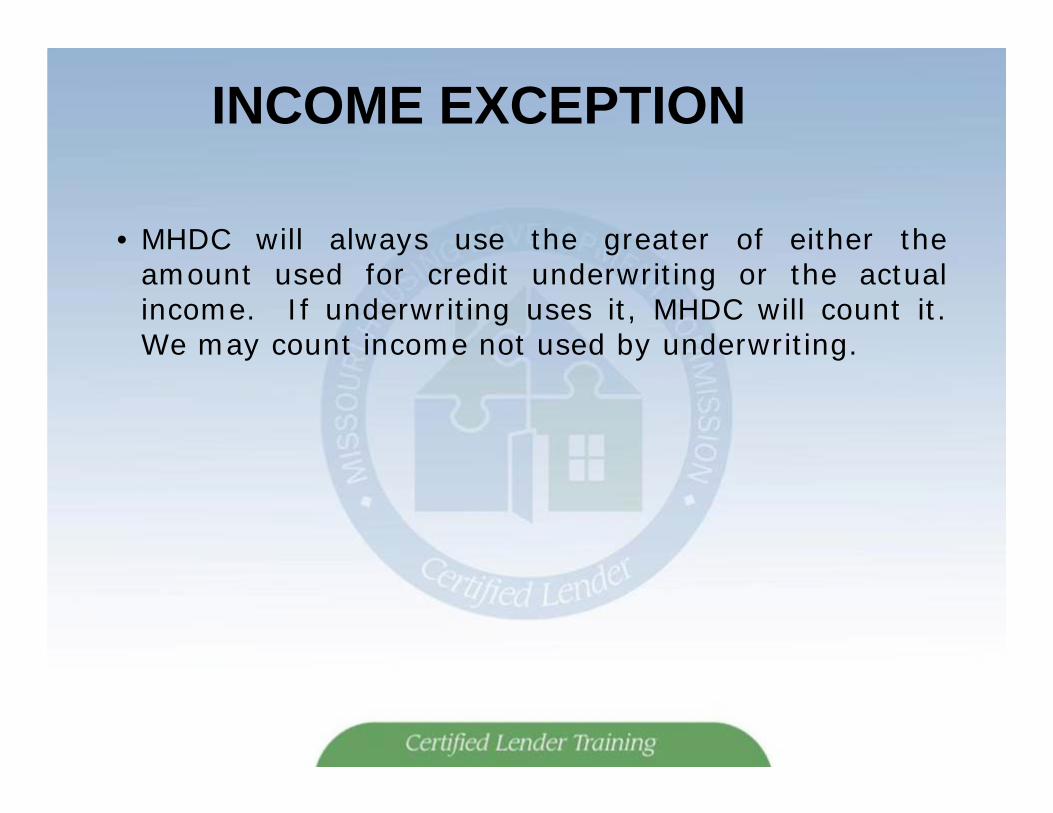

INCOME EXCEPTION

• MHDC will always use the greater of either theamount used for credit underwriting or the actualincome. If underwriting uses it, MHDC will count it.We may count income not used by underwriting.

FEDERAL INCOME TAX RETURNS

• All adults expected to reside in the property must submit copies of the last three years of federal tax returns

• Do not submit state tax returns

• Federal income tax returns may not be amendedafter the date of application to comply with the first-time homebuyer requirement

FEDERAL INCOME TAX RETURNS• If the loan closes after April 15, prior years’ tax

return will be required

• Form 8453 is not acceptable

• Print-outs from the IRS or IRS Transcripts are acceptable. MHDC only needs either the transcripts or the actual 1040 returns. Please do not send both

• Applicants who were not required to file mustcomplete a Non-Filing Status form #540

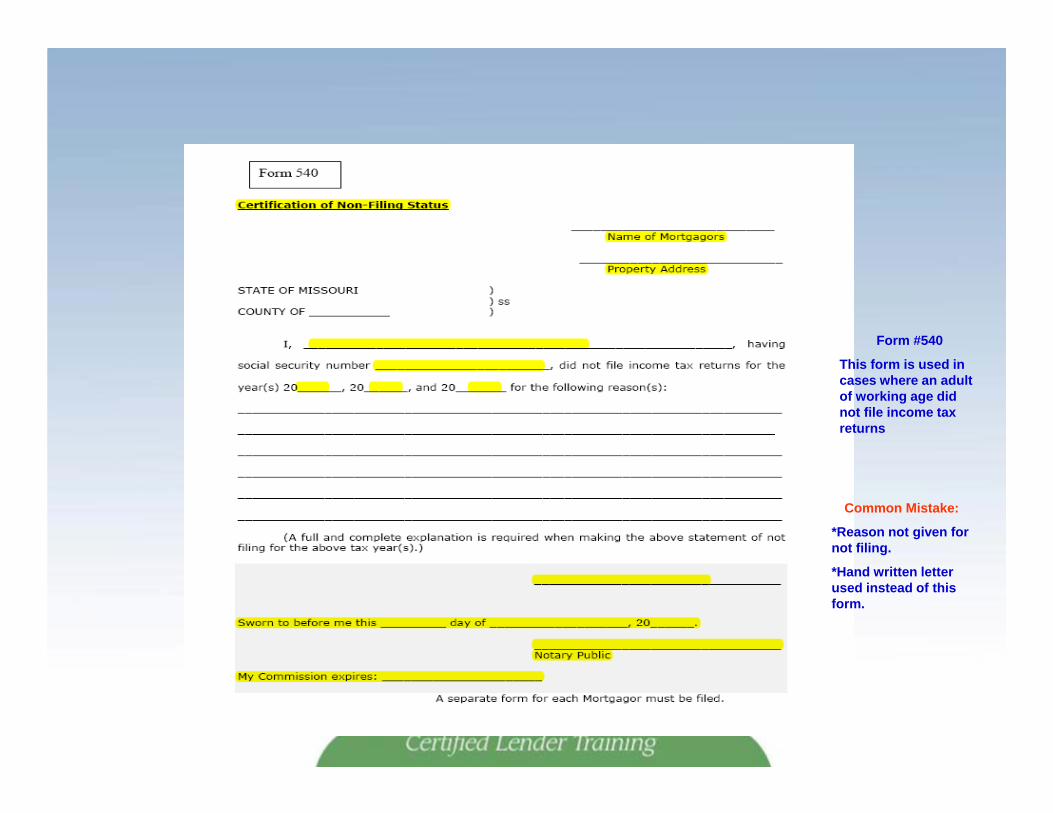

Form #540

This form is used in cases where an adult of working age did not file income tax returns

Common Mistake:

*Reason not given for not filing.

*Hand written letter used instead of this form.

PROCESSOR & UNDERWITER TIP• When reviewing tax returns, pay attention to the

borrowers present and past marital status. If a taxdeduction was taken for real estate or mortgageinterest by any borrower or occupant within the pastthree years, the loan is not eligible for purchase byMHDC.

• Watch the homeowner status of non-borrowingoccupants, they cannot have owned a home, even ifit is free and clear

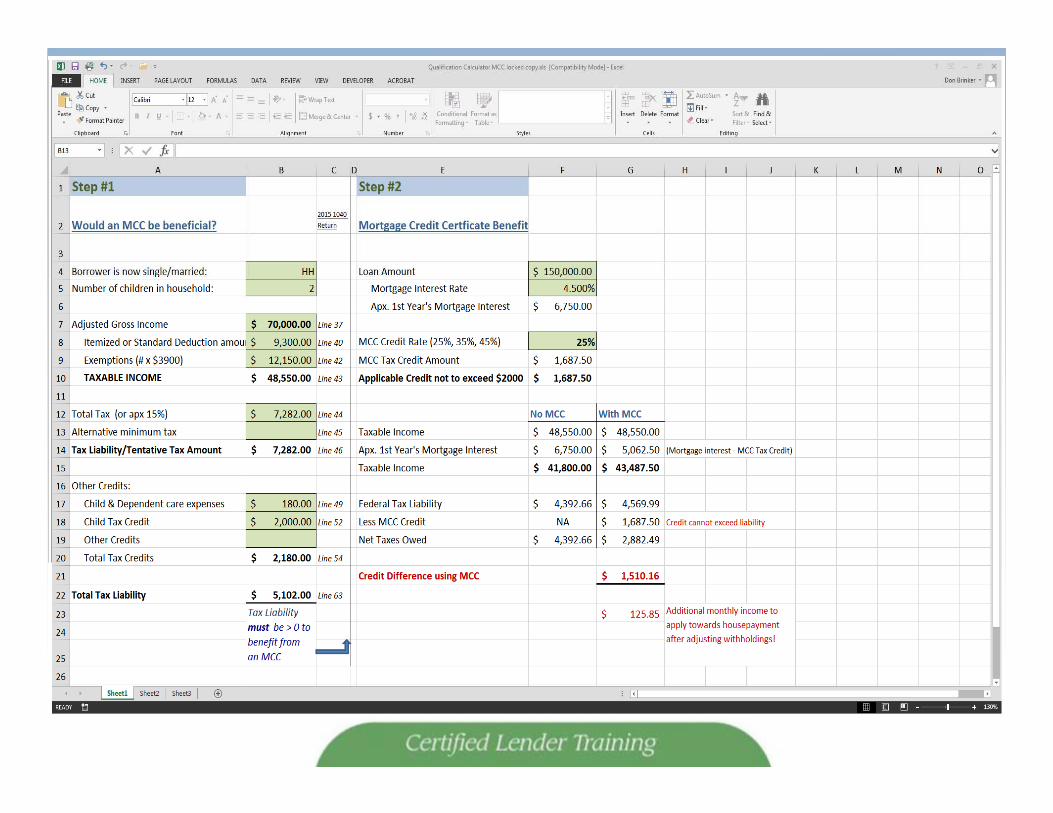

• Review the tax liability from previous years to makecertain that the MCC will benefit the borrower

OTHER PERSONS OCCUPYING THE PROPERTY

• MHDC requires that all information verified for all borrowers occupying property, even if not taking title or executing note

• This includes income and tax returns to verify first time buyer status, etc.

• Enter additional adults name and co-signer name (ifapplicable) on the Lender Certificate

REAL-ESTATE CONTRACT• Provide a copy of the real estate contract with all

addendums

• Be certain any adjustments to sales price are included

• Both buyer and seller must have executed and dated the contract

• The home may not have a purchase price higher than the appraised value

• Do not submit the reservation until you have a FINALcontract

RESIDENCE ELIGIBILITY REQUIREMENTS

• The types of properties eligible for First Place program are as follows:

– single family detached– row house– town house– Duplex– 1/2 duplex– condo– manufactured homes on permanent foundations;

peered/ skirted units are not eligible

OWNER OCCUPANCY REQUIREMENTS

• Mortgagors must occupy the residence within 60 days of loan closing and continue to occupy as long as the loan exists

• Mortgagors may not rent the property as long as the MHDC loan exists

PERSONS WHO ARE SEPARATED• Any applicant who is separated is still considered a

married person

• If the applicant and their spouse have been separated for more than 12 months, then each must sign the MHDC Marital Waiver Affidavits, (Form #550-1 and #550-2) stating they will not be residing together

• This also applies for spouses that are incarcerated

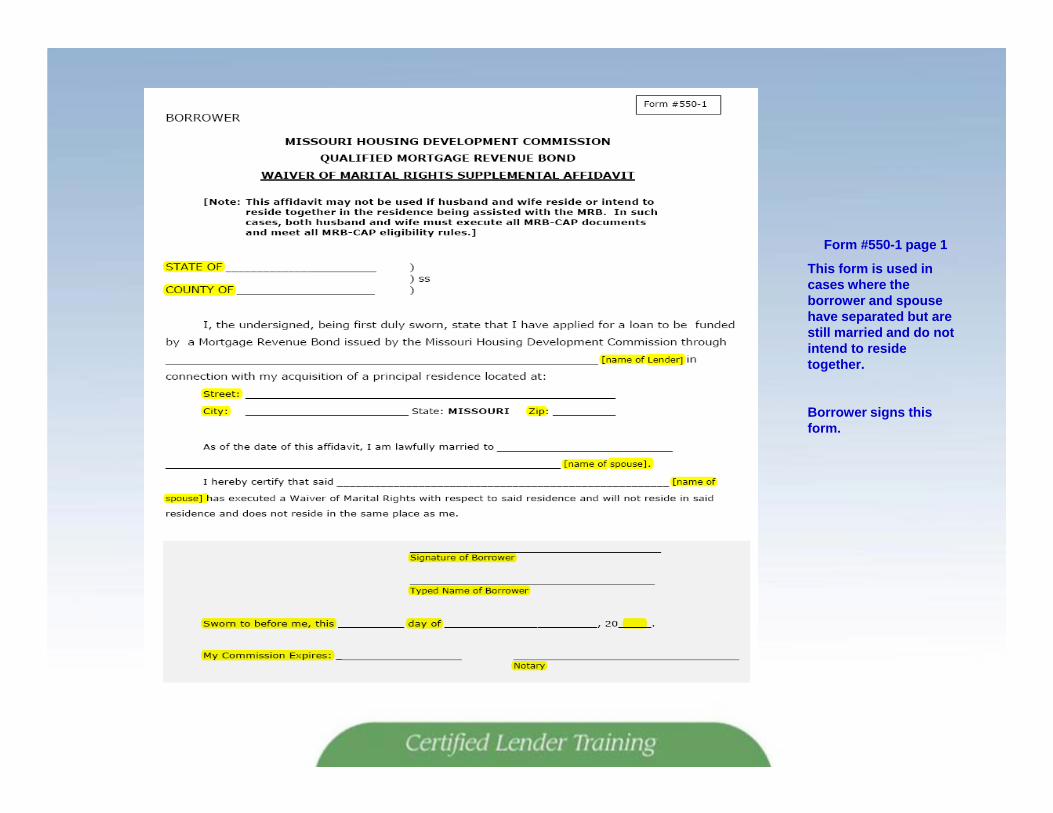

Form #550-1 page 1

This form is used in cases where the borrower and spouse have separated but are still married and do not intend to reside together.

Borrower signs this form.

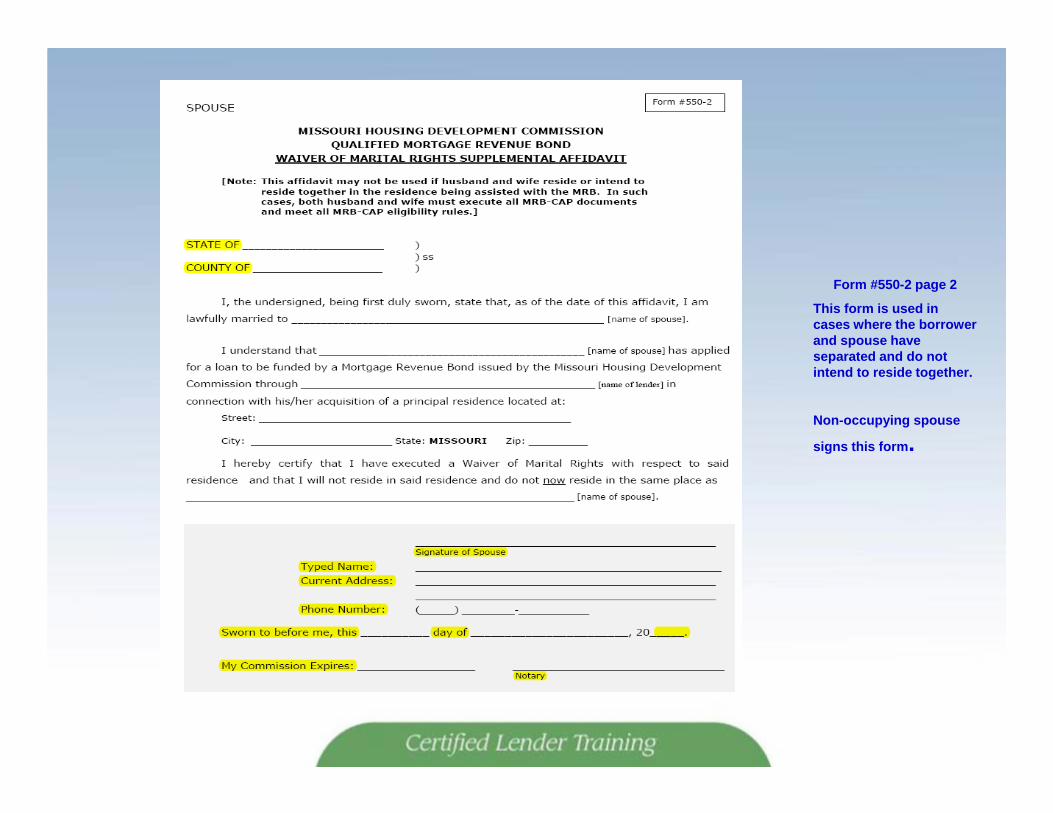

Form #550-2 page 2

This form is used in cases where the borrower and spouse have separated and do not intend to reside together.

Non-occupying spouse

signs this form.

PERSONS WHO ARE SEPARATED

• If an applicant who is currently separated from theirspouse owned a home with that spouse within the lastthree years, the applicant may not use First Place orMCC programs

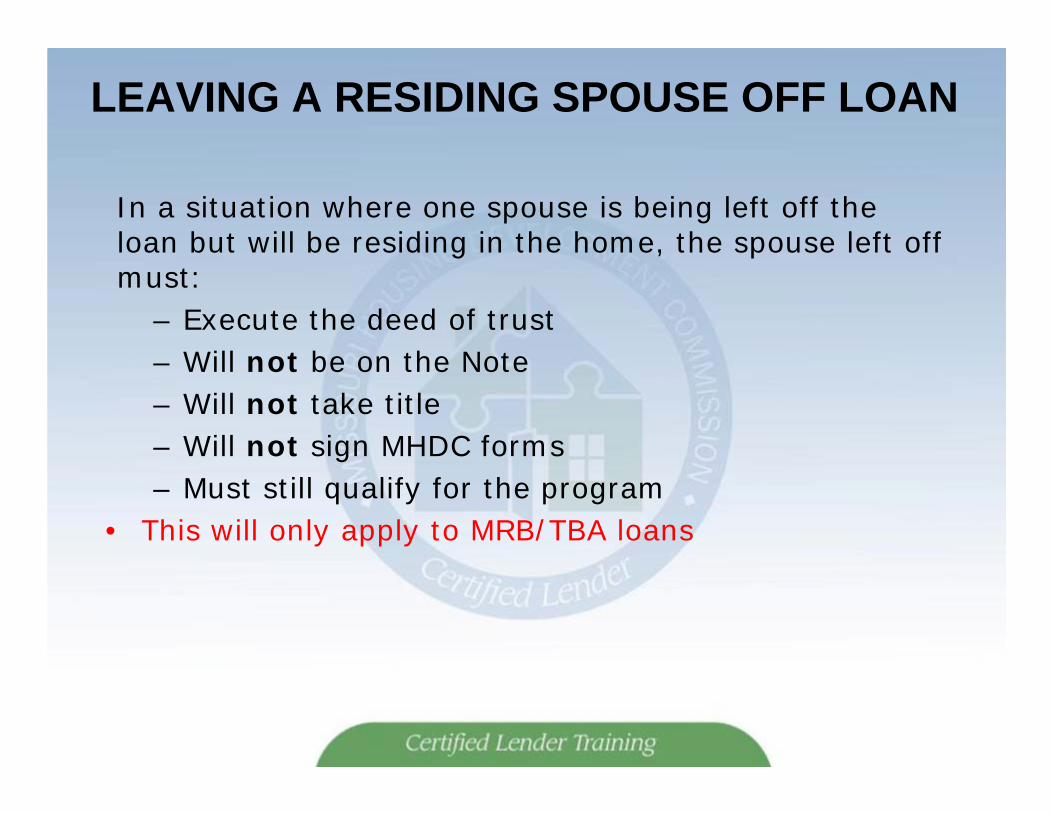

LEAVING A RESIDING SPOUSE OFF LOAN

In a situation where one spouse is being left off the loan but will be residing in the home, the spouse left off must:

– Execute the deed of trust– Will not be on the Note– Will not take title– Will not sign MHDC forms– Must still qualify for the program

• This will only apply to MRB/TBA loans

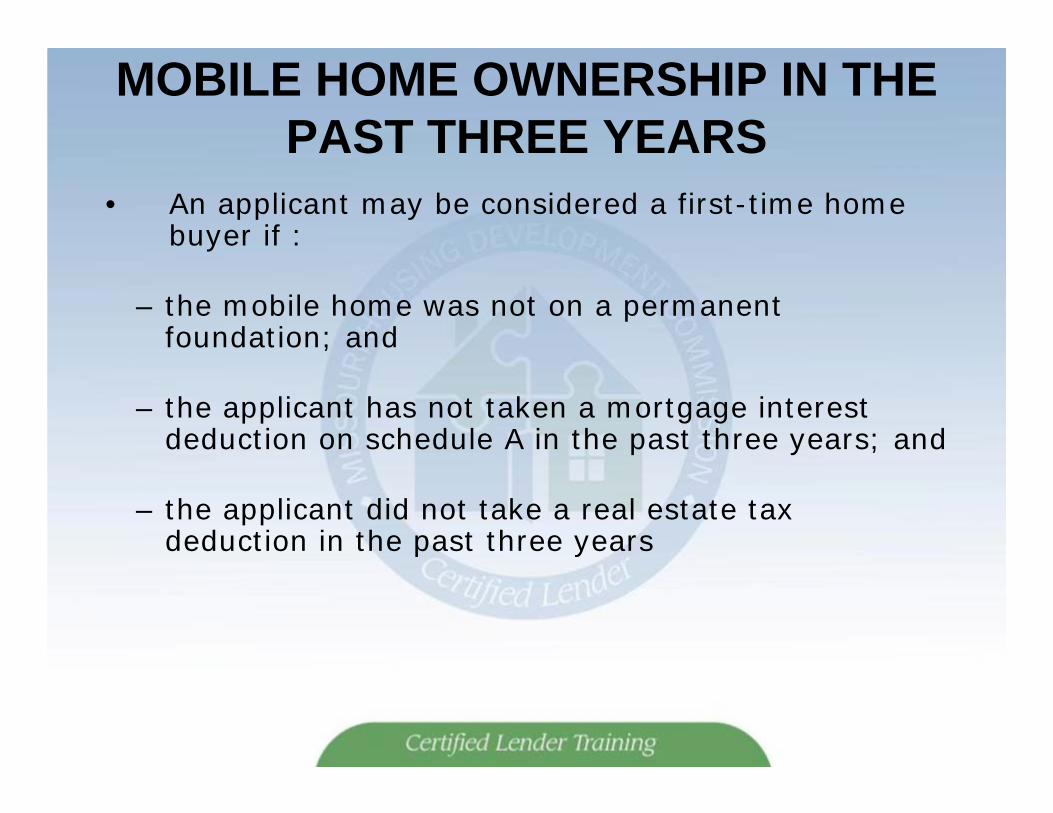

MOBILE HOME OWNERSHIP IN THE PAST THREE YEARS

• An applicant may be considered a first-time home buyer if :

– the mobile home was not on a permanent foundation; and

– the applicant has not taken a mortgage interest deduction on schedule A in the past three years; and

– the applicant did not take a real estate tax deduction in the past three years

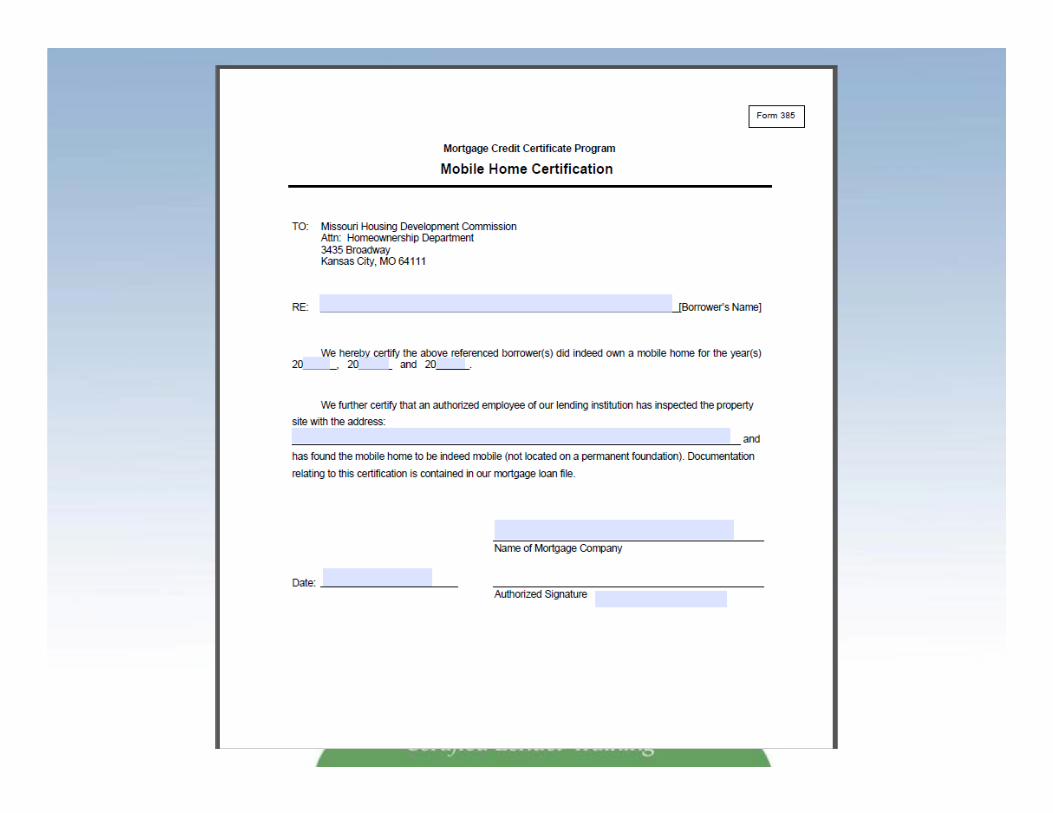

MOBILE HOME OWNERSHIP IN THE PAST 3 YEARS

• If the applicant qualifies as a first-time home buyer, the lender must certify that the mobile home is indeed mobile

• A representative from the mortgage company must verify the mobility of the mobile home

• This may be accomplished by completing MobileHome Certification-form #385

CLOSING DOCUMENTS

• After the loan closes the lender is to upload to MHDC and the master servicer a closing package with all necessary forms

CHECKLISTCORRESPONDENCE/PRIOR APPROVALS

• Supporting information should be included following the Lender’s Certificate

• This will include letters of explanation, prior approvalsetc.

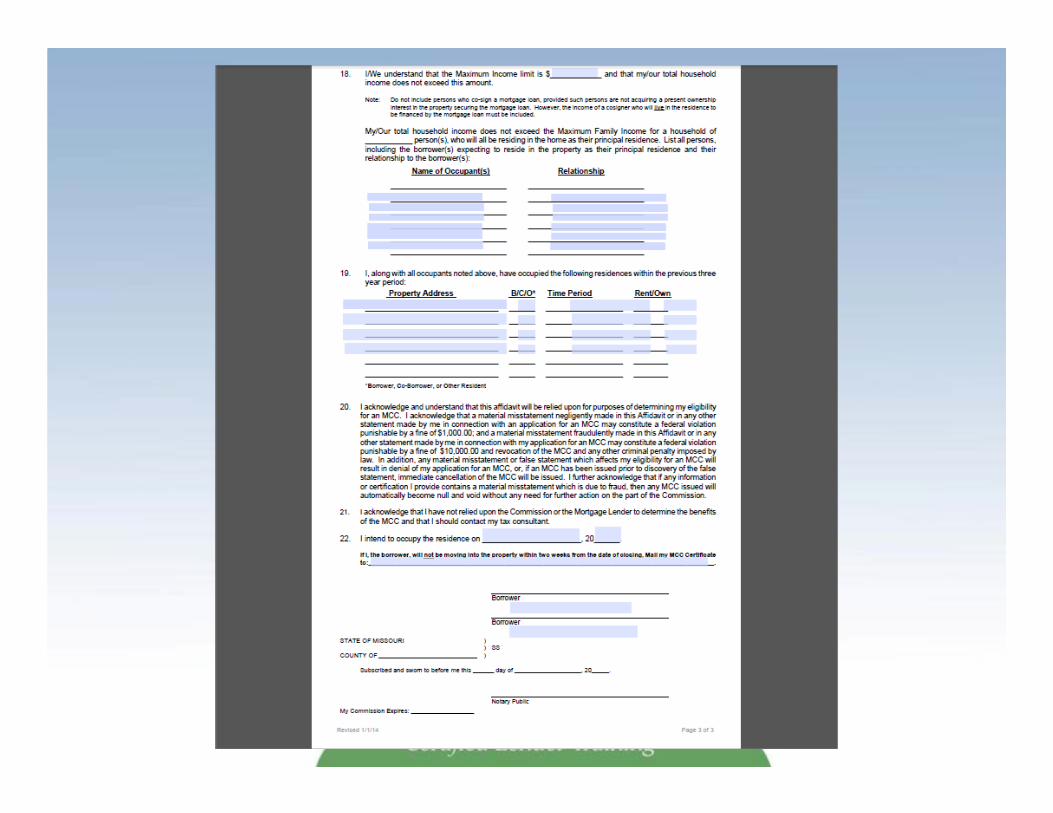

TOTAL NUMBER IN THE HOUSEHOLD

TOTAL NUMBER IN THE HOUSEHOLD

• This means the total number of persons who will be occupying the property as their full-time principal residence

• Lender will initially determine household size from Residential Loan Application, and use the household size to determine maximum income allowable

• At time of closing, borrower will execute aMortgagor’s Affidavit stating the number ofpersons who will occupy the home, and theircombined incomes

TOTAL NUMBER IN HOUSEHOLD

• A dependent may be counted if the parents are divorced and per the divorce decree each parent has custody 50 percent of the time

• Foster children are NOT counted as members of the household

• An unborn child may not be included as a dependent

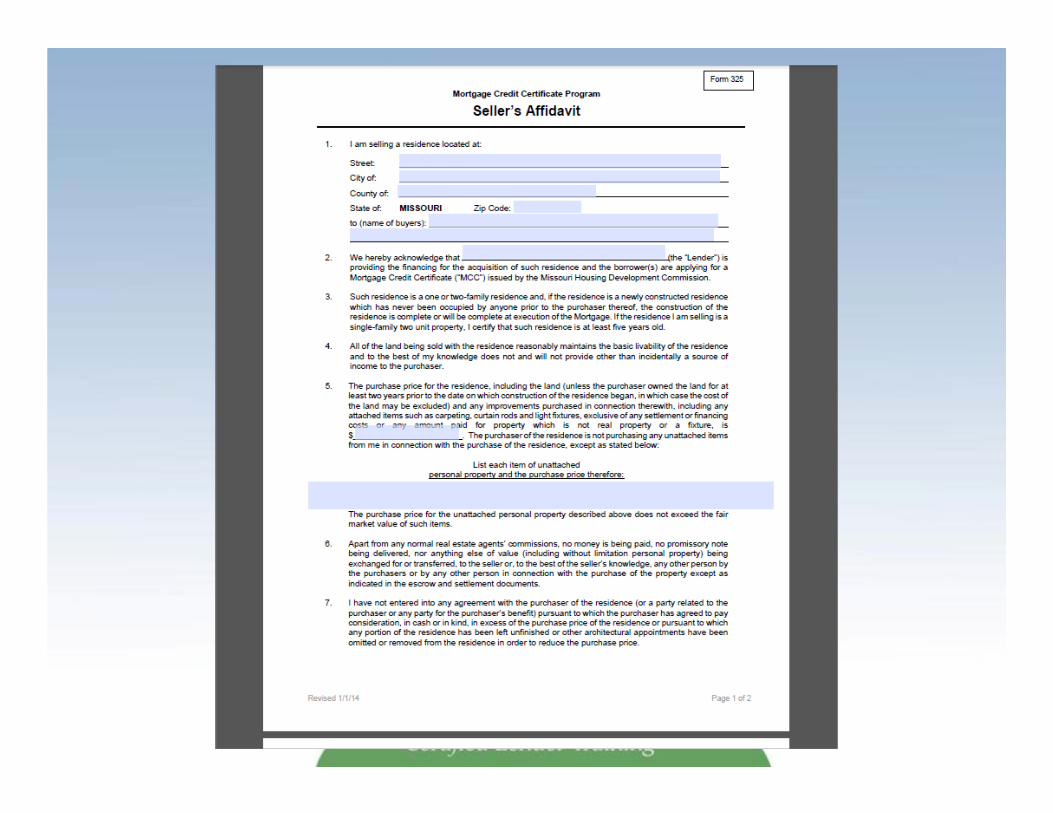

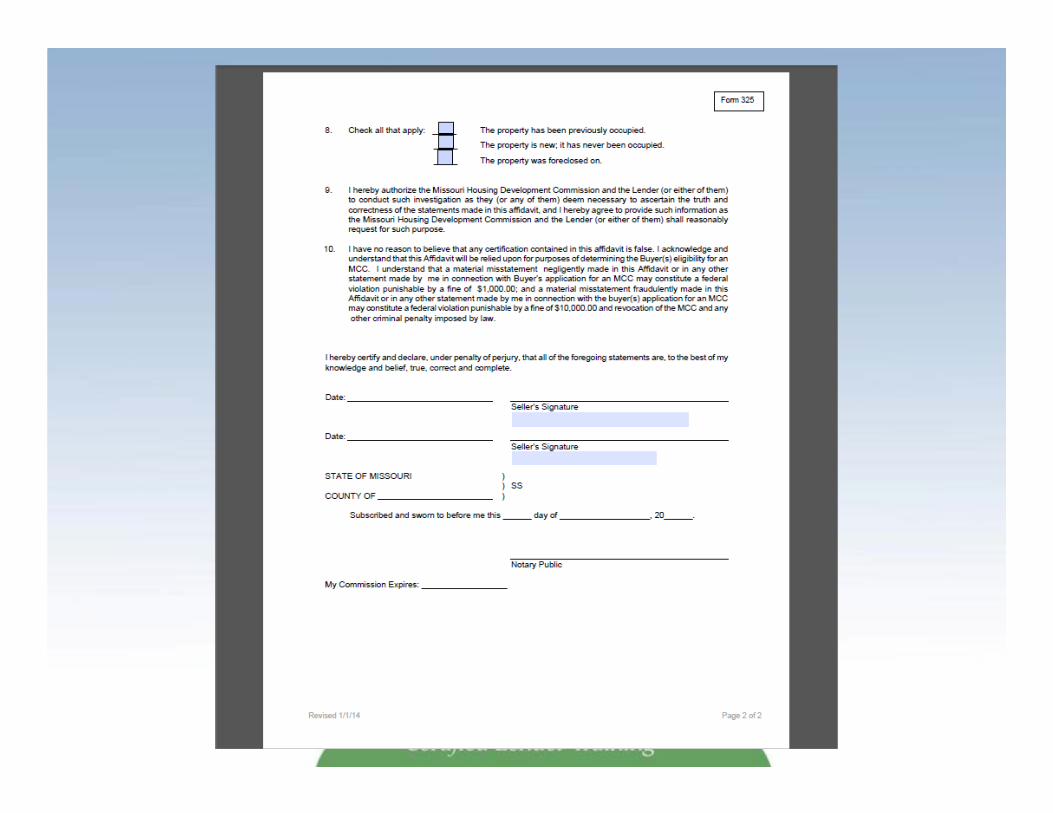

FORM #325/525Sellers Affidavit

• Verifies address, buyers name, sellers name, lender, sales price, etc.

• Must be executed by all persons having an ownership interest in property

• If executing the Warranty Deed, Form #525 must be executed

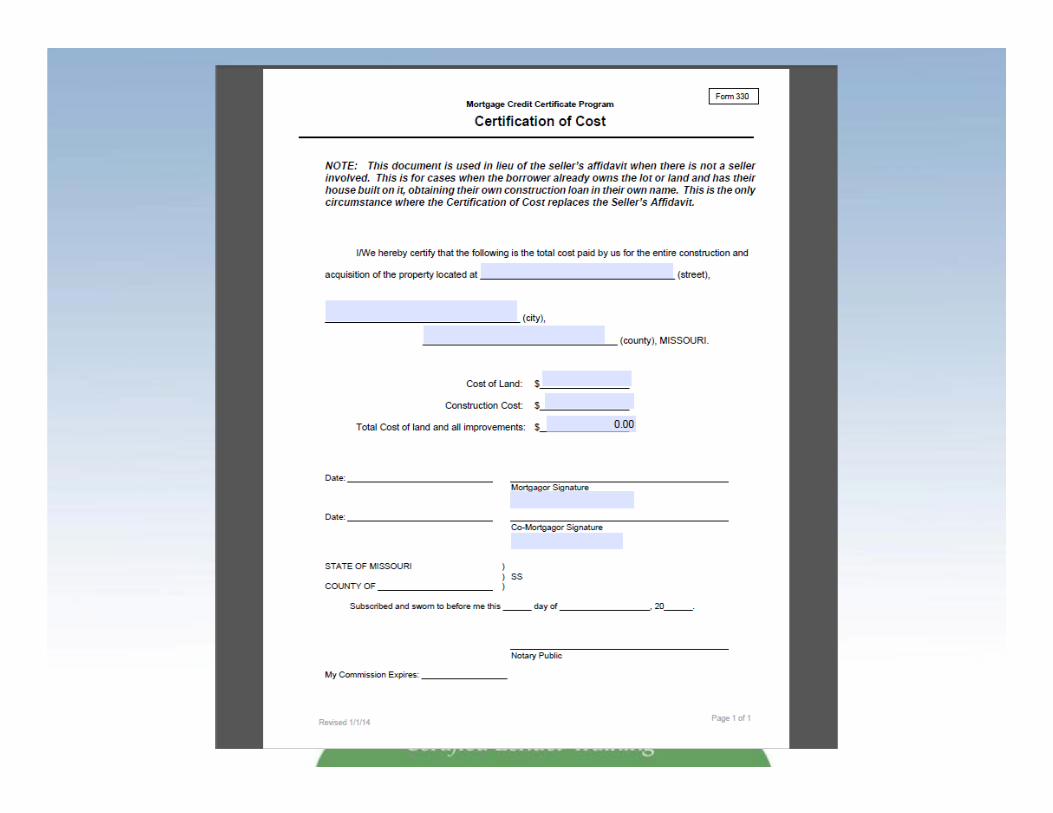

FORM #330Certification of Cost

• If a borrower constructed a home on a piece of land they owned, then applied for a First Place loan, there would not be a seller, so a Sellers Affidavit would not apply

• In these cases, the borrower would execute form #330

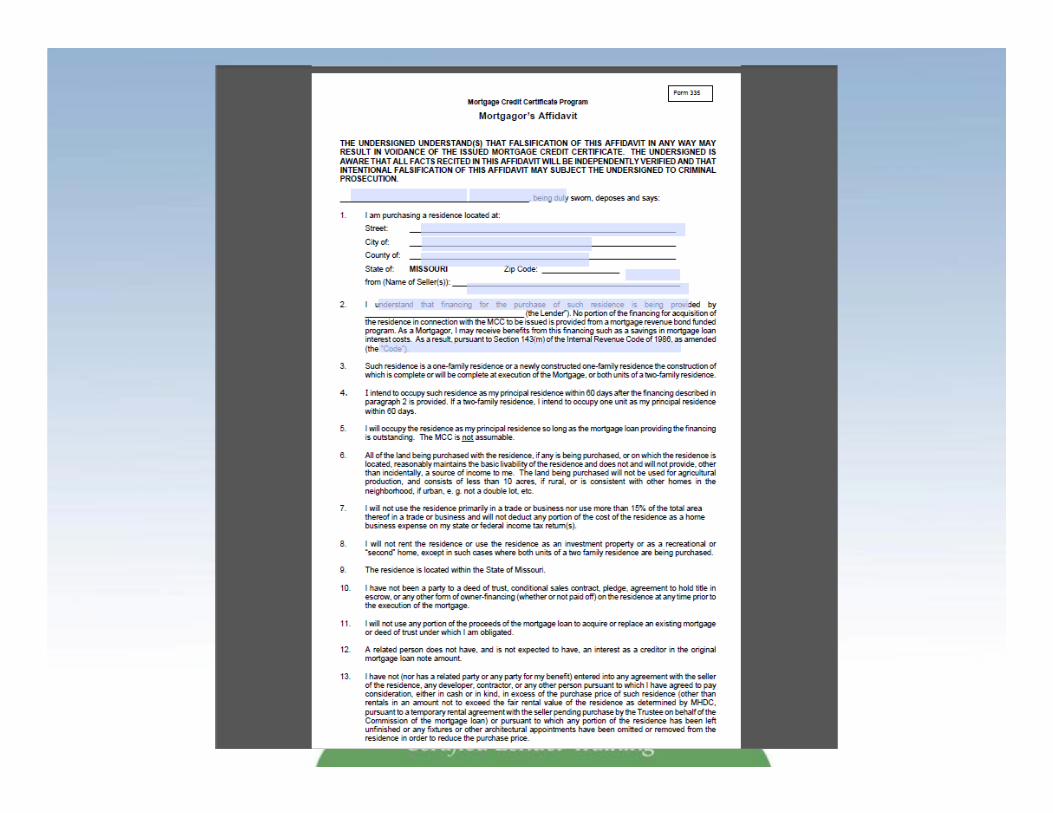

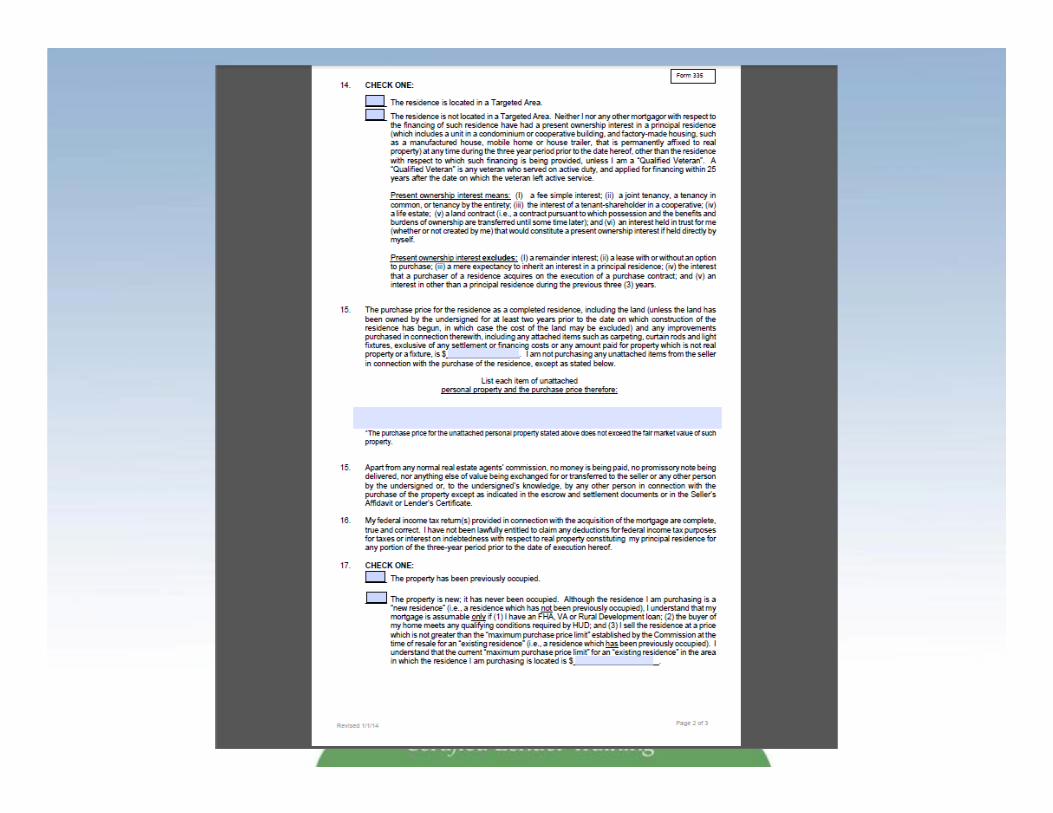

FORM #335Mortgagors Affidavit

• This form is signed by the borrower at the time ofclosing. By signing, the borrower states that allrepresentations made at application are true, that theincome verified is accurate, and who will occupy theproperty being purchased.

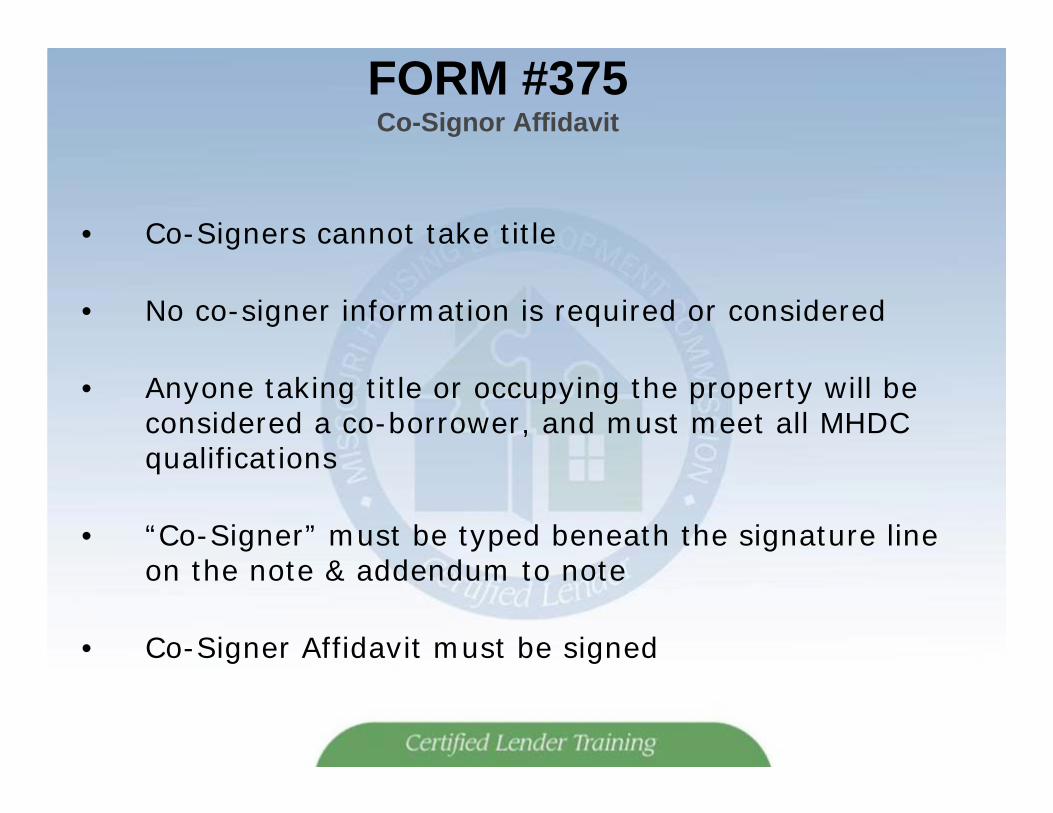

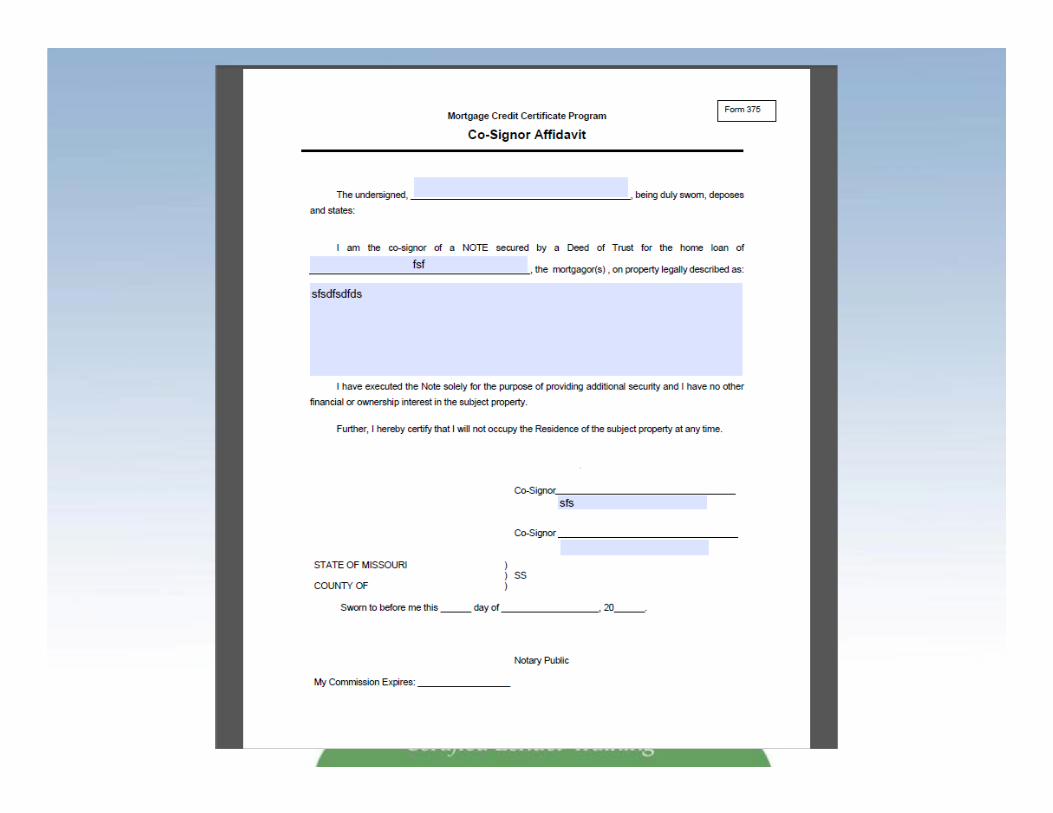

FORM #375Co-Signor Affidavit

• Co-Signers cannot take title

• No co-signer information is required or considered

• Anyone taking title or occupying the property will be considered a co-borrower, and must meet all MHDC qualifications

• “Co-Signer” must be typed beneath the signature line on the note & addendum to note

• Co-Signer Affidavit must be signed

WHAT HAPPENS WHEN THEHOUSE IS SOLD?

• Title to the home transfers as in any other transaction

• If the home is sold within the first nine years ofhomeownership, Recapture Tax may be triggered

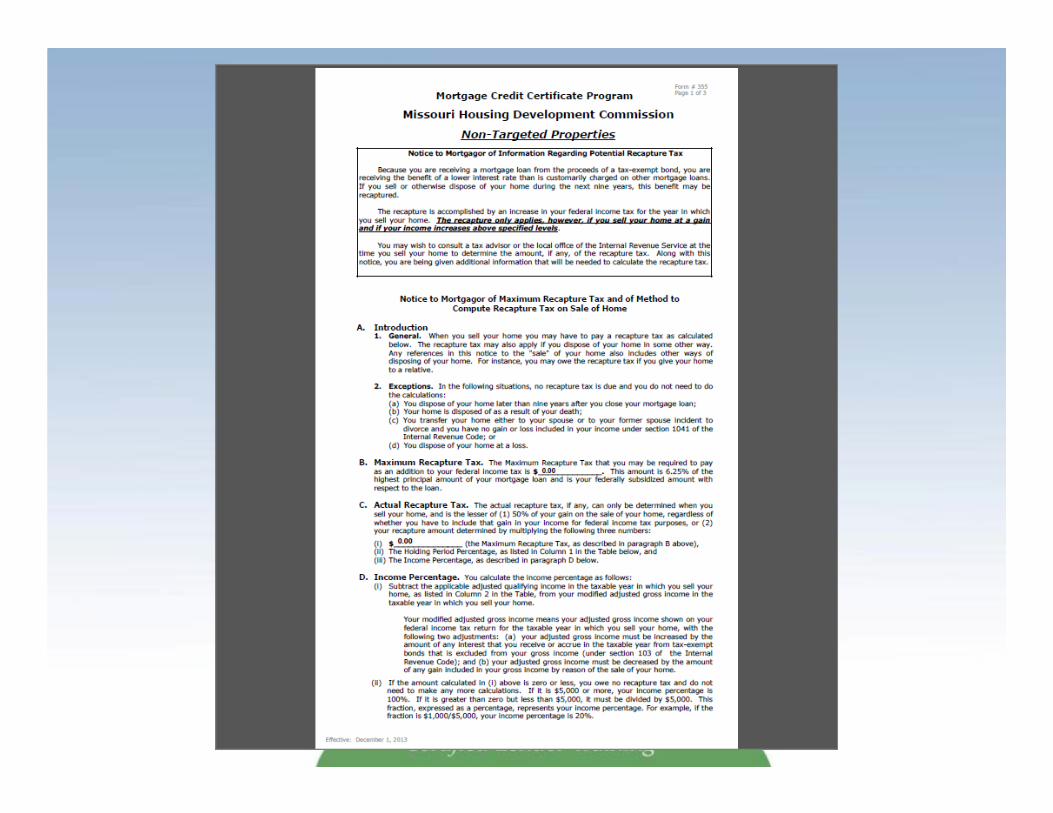

POTENTIAL RECAPTURE TAX

What is it, and how does it affect the borrower?

Potential Recapture Tax is not an issue on TBA loans

It only applies to MRB and MCC loans

RECAPTURE TAX HAS NOTHING TO DO WITH THE CAP FUNDS. Recapture tax applies to all MRB (CAP and NON CAP) and MCC loans.

WHAT IS RECAPTURE TAX?

• If a homebuyer sells his or her home in the first nine years of ownership AND

• If they make a profit AND

• If income is over maximum

– additional tax may be owed

HOW IS RECAPTURE TAX CALCULATED

• Uses IRS Form 8828 as a worksheet

• Calculated from time of purchase to time of sale

• Uses purchase price plus improvements as base price

• Deducts cost of sale

• Uses sales-year Adjusted Gross Income asdeterminant if Recapture Tax owed

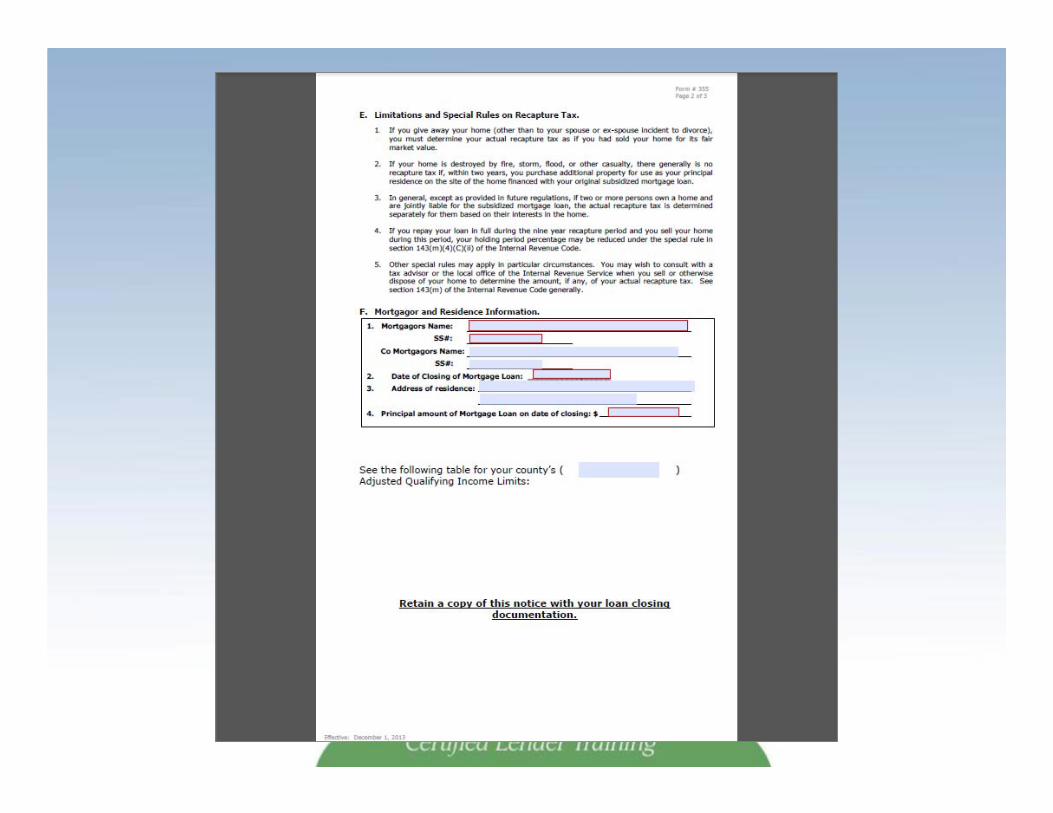

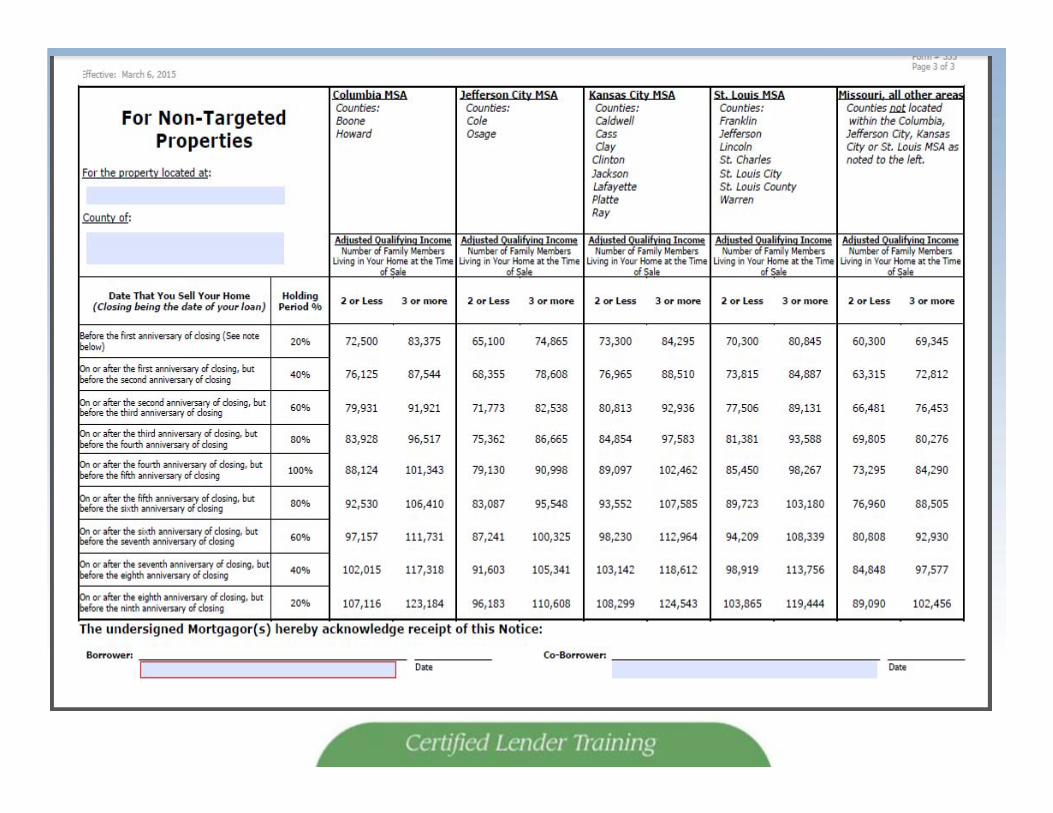

FORM #355Notice of Potential Recapture Tax

• This form describes to the borrower what the potential impact may be if the home is sold in the first nine years

• This form provides maximum incomes limits for use in calculating recapture tax

• These forms change annually; when HUD income limits change, the buyers must use the one they are provided at closing

SHOULD MY BUYER BY CONCERNED, PROBABLY NOT

• The average income for a First Place buyer is $49,000 annually

• The current Maximum Income is $63,200 or higher in some areas

• This means the average buyer is $14,200 undermaximum

• Household income would have to increase this much to reach today’s maximum

SHOULD THE BUYER BY CONCERNED, PROBABLY NOT

• Pay increases in the United States averaged less than 5% over the last 10 years

• The Maximum Income increases 5 percent automatically each year

• If your buyer qualifies for a First Place loan, it is extremely unlikely that household income will exceed the maximum income in the year of sale

THINGS TO CONSIDER:

• Borrower using CAL loan gets 4% assistance

• Borrower saves on interest rate while the home is owned

• Borrower has tax advantage while occupying his home

• Benefits of First Place program will usually outweigh the possibility of Recapture Tax

VERY IMPORTANT INFORMATION

• Convey to the buyer that they must retain this formuntil they sell their home. They will need to refer tothis chart if their home is sold in the first nine years ofownership

TARGETED CENSUS TRACTS: WHAT ARE THEY?

• FEDERALLY DESIGNATED AREAS

• Seventy-percent of households make less than 80 percent of area median income

• For an additional list of affected counties, and for maps of targeted areas, refer to the MHDC website, www.mhdc.com

• Check census tract on the internet at www.ffiec.gov

CLOSING DISCLOSURE STATEMENT

• Carefully review all fees to be sure they are allowed

• No junk fees are allowed

• Be certain the buyer is not receiving any of the 4% CAL funds (if used)

LENDER’S FEES AND CHARGES• Lender may charge the actual amount expended for

credit reports, work number, home inspections($400.00 max), pest inspections or treatments, flood letters, title examination and insurance, required title policy endorsements, mortgage insurance, attorney fees and filing/recording fees

• As of September 1, 2017, a $71.50 “Tax Service" fee must be collected on each first mortgage. The fee will be netted out by the master servicer upon purchase of the mortgage

LENDER’S FEES AND CHARGES• As of August 1, 2013, originating lenders may charge

an "Application/Processing" fee of up to $750 on eachfirst mortgage. If the fee is charged, the originatinglender must provide documentation to MHDC verifyingthat the fee was an "Application/Processing"fee. Only a joint "Application/Processing" fee isallowed, not a separate "Application" and/or"Processing" fee.

• Lenders may also charge a 1 percent origination feeto the buyer for First Place loans and .5% for NextStep loans.

PROHIBITED FEES

• The following may not be paid by the buyer:

– Document preparation fee, underwriting fee (except by a third party, then $300 maximum), commitment fee, discounts points, real estate sales commission, Federal Express/overnight delivery fees (unless agreed to in writing prior to closing)

FEES REGULATED BY MHDC

• Lenders may not charge discount points at closing on First Place/Next Step loans

• Lenders will be paid a 1.5% servicing release fee upon purchase of loan on First Place/Next Steps loans

COMMON MISTAKE

• Lenders pass-through a fee/charge from the realtor.Buyers may not pay any fees to the realtor. Lendersshould use every effort to ensure that fees to theseller are kept to a minimum.

• Lenders allow service providers (title companies etc)to charge more than the MHDC maximum fee allowed.Any amount over the MHDC maximum allowable feemust be refunded to the borrower before the loan willbe approved by MHDC.

NON U.S. CITIZENS• Each applicant, along with their spouses, must be a

U.S. citizen or a lawful resident alien

• Borrowers must occupy the property as their principal residence

• Borrowers must be eligible to work in the U.S.

• Borrowers and their spouses must have a valid socialsecurity number

• When the spouse of the borrower is not in the countrylegally, marital status may not be waived. Bothspouses must be legal U. S. residents

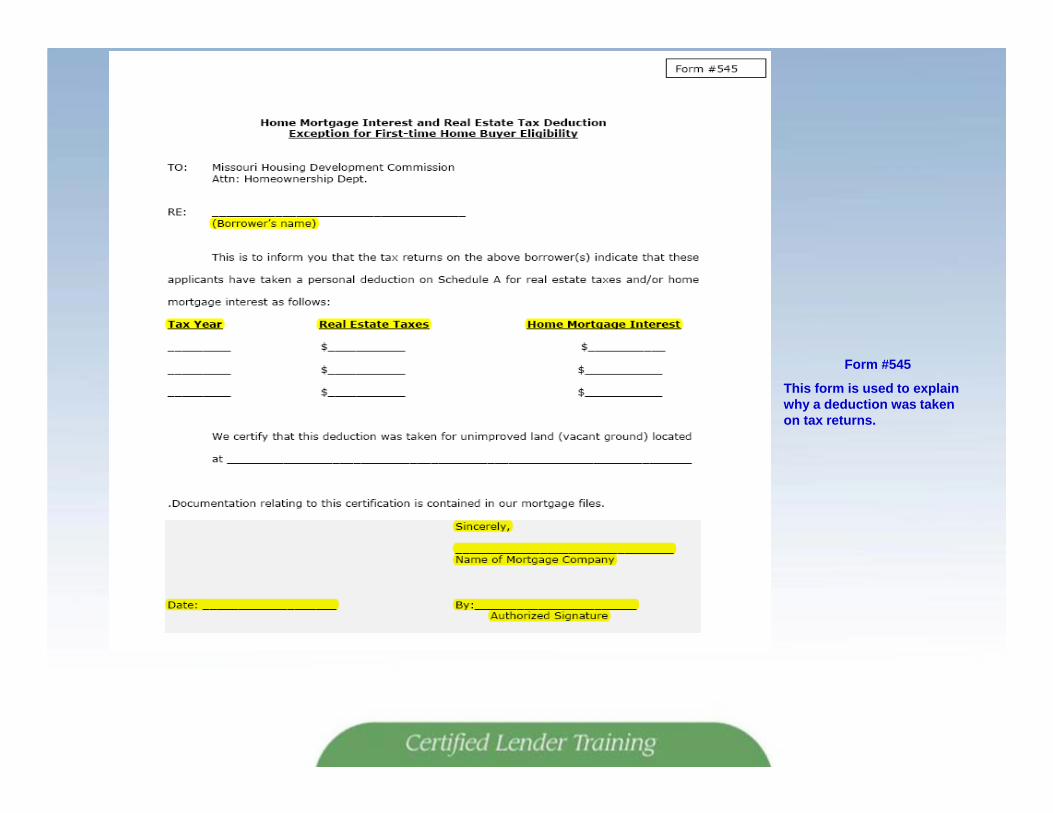

FORM #545The Home Mortgage Interest & Real Estate Tax Deduction Exemption

• If a buyer owned un-developed property, anddeducted the interest or real estate taxes on thatproperty on a Federal Income Tax return within thelast three years, Form #545 must be completed

Form #545

This form is used to explain why a deduction was taken on tax returns.

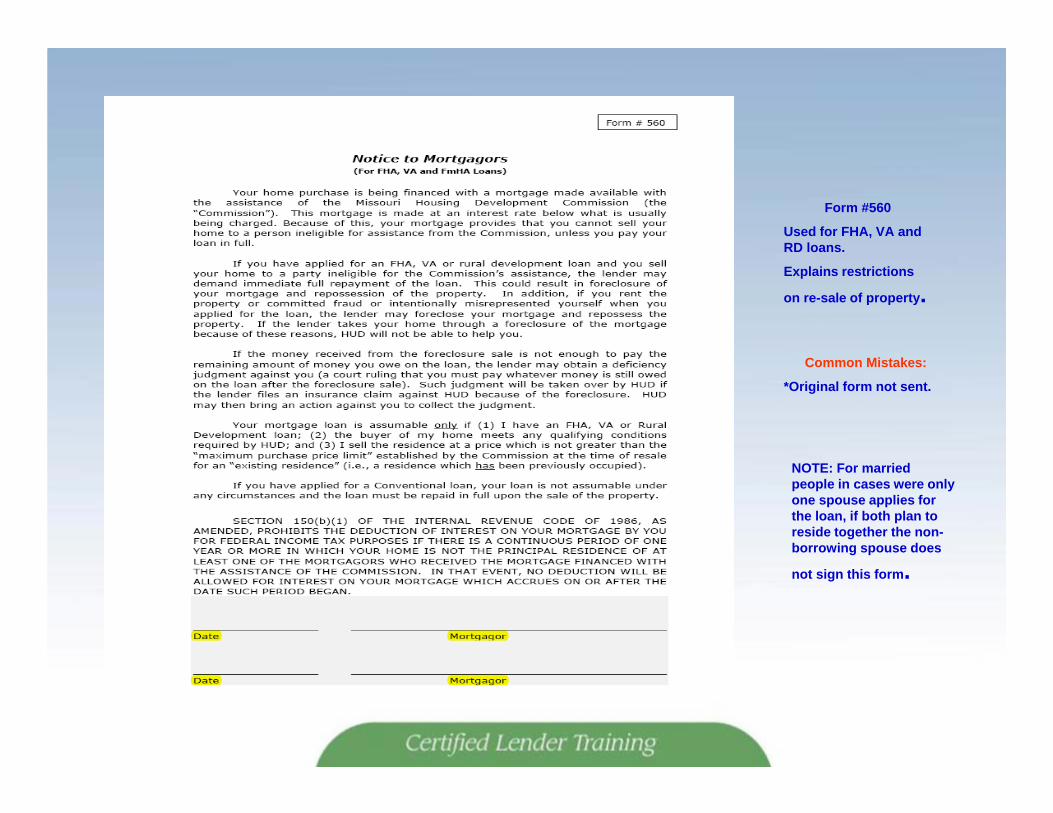

FORM #560Notice to Mortgagors

• Used only with FHA, VA, RD loans

• Explains restrictions on re-sale of property, renting property, etc. as they pertain to Government insured loans

• Not recorded with Deed of Trust

Form #560

Used for FHA, VA and RD loans.

Explains restrictions

on re-sale of property.

Common Mistakes:

*Original form not sent.

NOTE: For married people in cases were only one spouse applies for the loan, if both plan to reside together the non-borrowing spouse does

not sign this form.

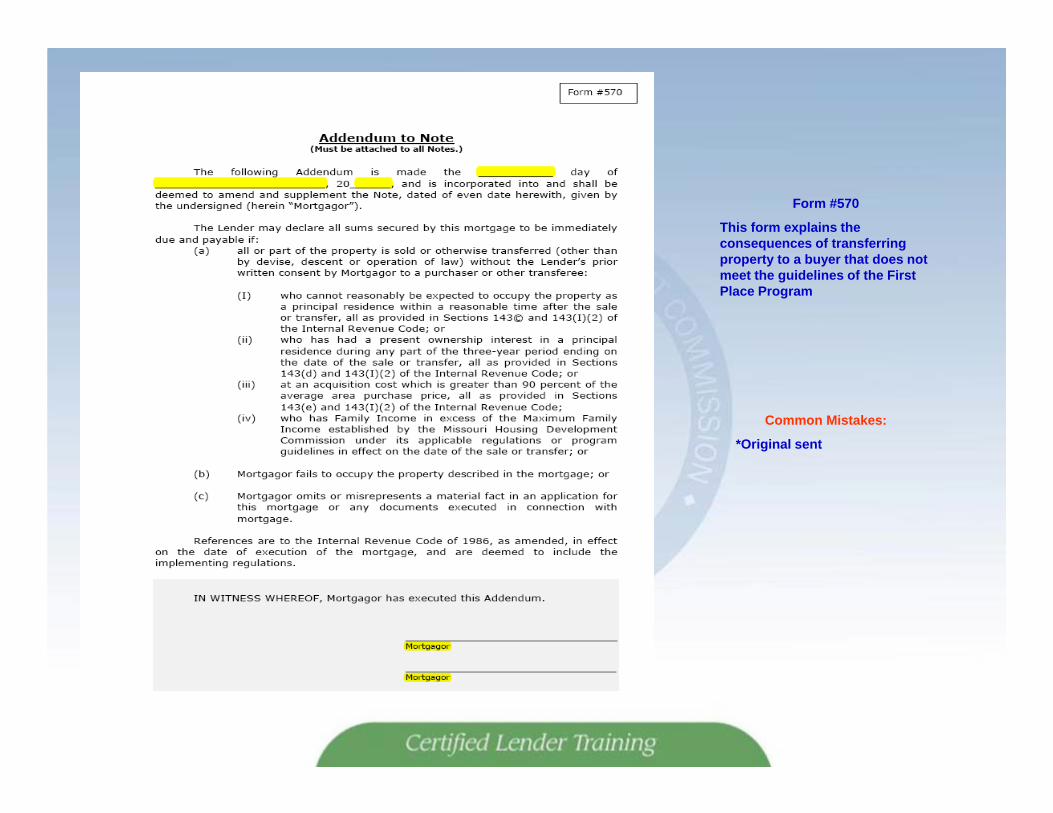

FORM #570Addendum to Note

• Attach to copy of the executed mortgage note

• Explains the consequences of transferring property to buyer that does not meet the guidelines of the First Place program

• Original goes to master servicer

Form #570

This form explains the consequences of transferring property to a buyer that does not meet the guidelines of the First Place Program

Common Mistakes:

*Original sent

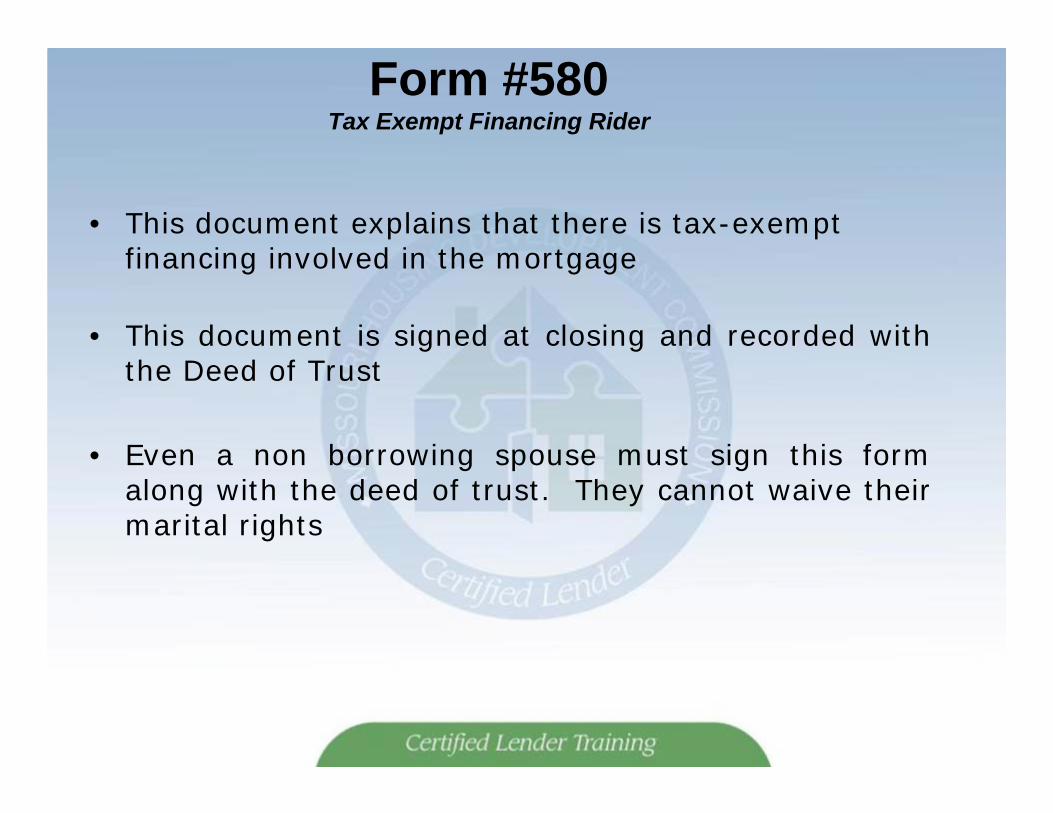

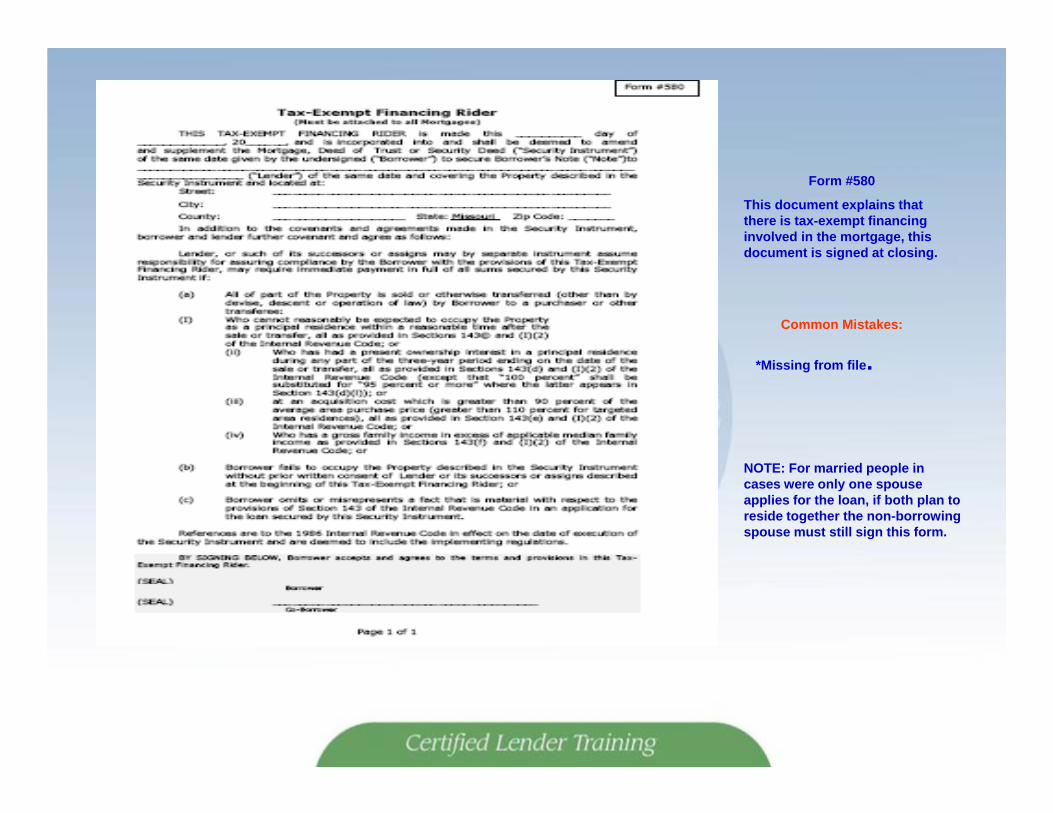

Form #580Tax Exempt Financing Rider

• This document explains that there is tax-exempt financing involved in the mortgage

• This document is signed at closing and recorded withthe Deed of Trust

• Even a non borrowing spouse must sign this formalong with the deed of trust. They cannot waive theirmarital rights

Form #580

This document explains that there is tax-exempt financing involved in the mortgage, this document is signed at closing.

Common Mistakes:

*Missing from file.

NOTE: For married people in cases were only one spouse applies for the loan, if both plan to reside together the non-borrowing spouse must still sign this form.

CLOSER TIPPRE-CLOSING CHECKLIST

PRE-CLOSING CHECKLIST

• Do I have tax-returns or equivalent for all occupants?

• Income for all borrowers verified?

• Is the title company familiar with MHDC rules?

• Are both income and acquisition cost within guidelines?

• Are all fees allowed?

• Flood Zone OK?

• Rate verified?

• Are all MHDC forms correctly completed?

THE LOAN CLOSES!

CLOSING LOANS AT THE TITLE COMPANY

• Be certain your instructions to the title company are explicit

• Let the title company know about the maximum closing fees allowed

• Don’t allow tax returns or other documents requiring review to be brought to closing

LOAN CLOSING

• Loan may not be subject to a “buy down” (only applies to First Place/Next Step)

• Mortgage must be in fee simple title

• Must be a first mortgage

• Must be underwritten and documented in accordance with prudent standards, and in compliance with applicable program guidelines (i.e., FHA, VA, FNMA, RD)

• Must be 30 year term, and have payments due on the first of each month. (only applies to First Place/Next Step)

SHIPPER TIP: THE LOAN IS CLOSED, NOW WHAT?

• CAREFULLY review forms for correct execution

• Review MHDC checklist (Form #505/#305 Lender Checklist) to ensure all required docs are sent with file

• Call MHDC with any questions before shipping

• Do not send a file knowing it is incomplete

SELLING LOANS TO MHDC

Submitting packages to MHDC and Master ServicerOnly applies to MRB/TBA loans

SALE OF FIRST PLACE LOANS

• Lenders may not retain servicing on First Place or the Next Step loans

• All First Place and Next Step loans are sold to MHDCs’ master servicer, ServiSolution’s

SUBMITTING FILES TO THE MASTER SERVICER

• Lenders are to submit a separate file to master servicer containing all required items

• All lenders must deliver packages eligible to be sold into the secondary market

• Any file must be eligible for sale to FHA, FNMA, RD or VA

• Lenders may use MERS

MASTER SERVICER• Each file will be reviewed for compliance with the

appropriate underwriting guidelines

• Files are not re-underwritten

• Master servicer will pay the lender when the loan is approved by both MHDC and master servicer

EDOCS ARE HERE!

• This will make the entire MHDC process paperless for all programs

• Next Step Program, this program will be less documentation.

• All loans must be uploaded through EDOCS.

What you need to utilize EDocs• You must have access to Lender Online (LOL) • You must have a username and password• You must have Adobe Reader• You must be able to scan documents

What Is EDocs?

• eDocs stands for Electronic Documents• eDocs is a way that lenders can submit their

compliance files to MHDC and the Master Servicer electronically using Lender Online (LOL)

• eDocs will eliminate paper files being sent to MHDC This will help reduce cost of shipping

• eDocs will also eliminate the need for originals and live signatures on MHDC documents. This should cut down on deficiencies on the file.

How to submit files

• Form #505 should be used as your guide to stacking order

• Prepare your package with all required forms and signatures

• Instead of mailing MHDC your package....

you can now simply scan your file and upload it onto Lender Online!

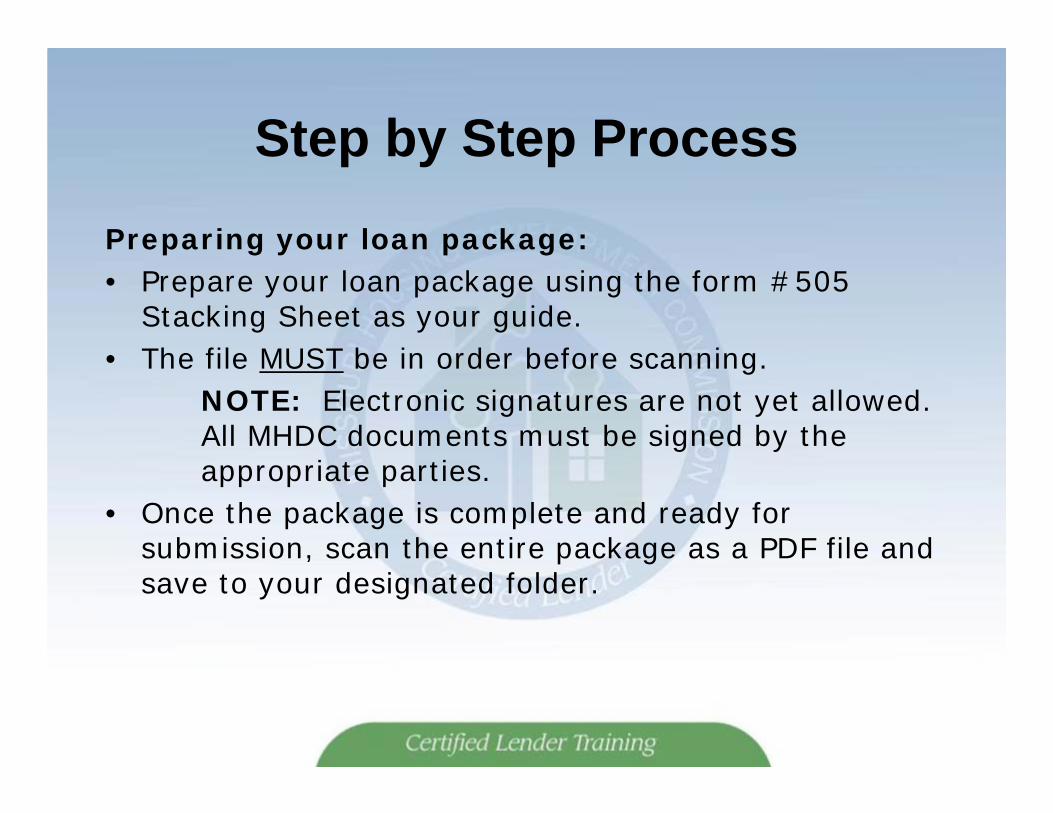

Step by Step Process

Preparing your loan package:• Prepare your loan package using the form #505

Stacking Sheet as your guide.• The file MUST be in order before scanning.

NOTE: Electronic signatures are not yet allowed. All MHDC documents must be signed by the appropriate parties.

• Once the package is complete and ready for submission, scan the entire package as a PDF file and save to your designated folder.

Step by Step Process

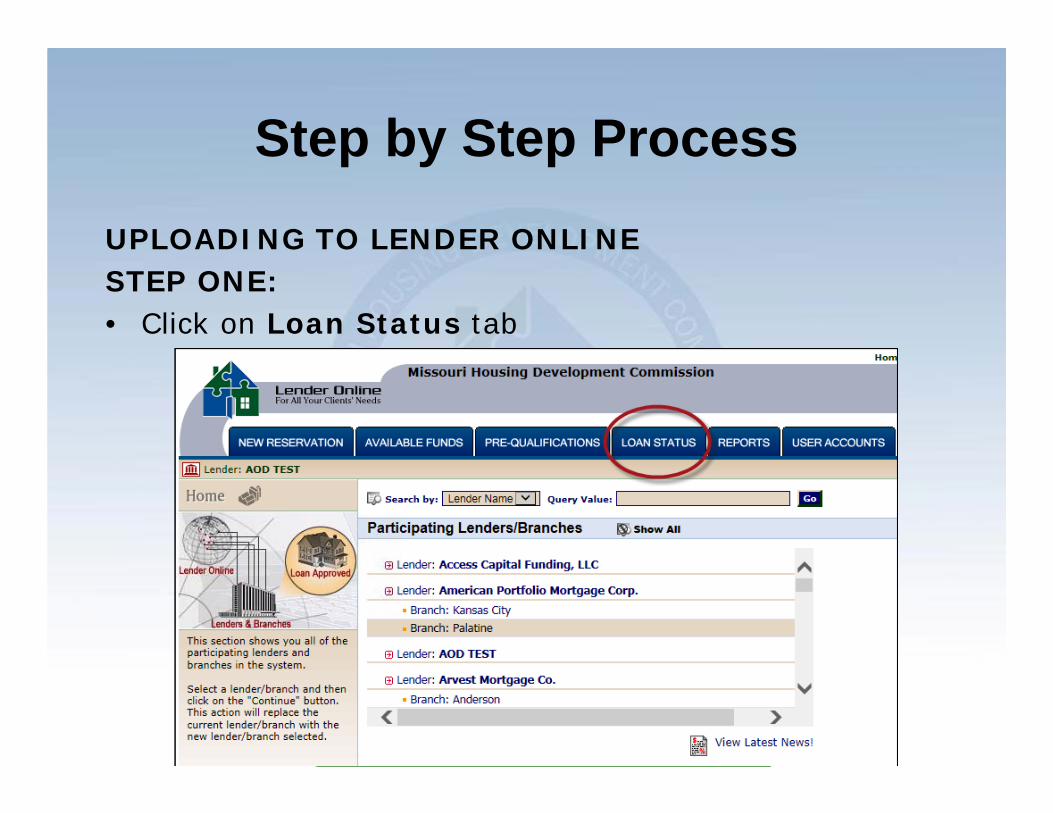

UPLOADING TO LENDER ONLINESTEP ONE:• Click on Loan Status tab

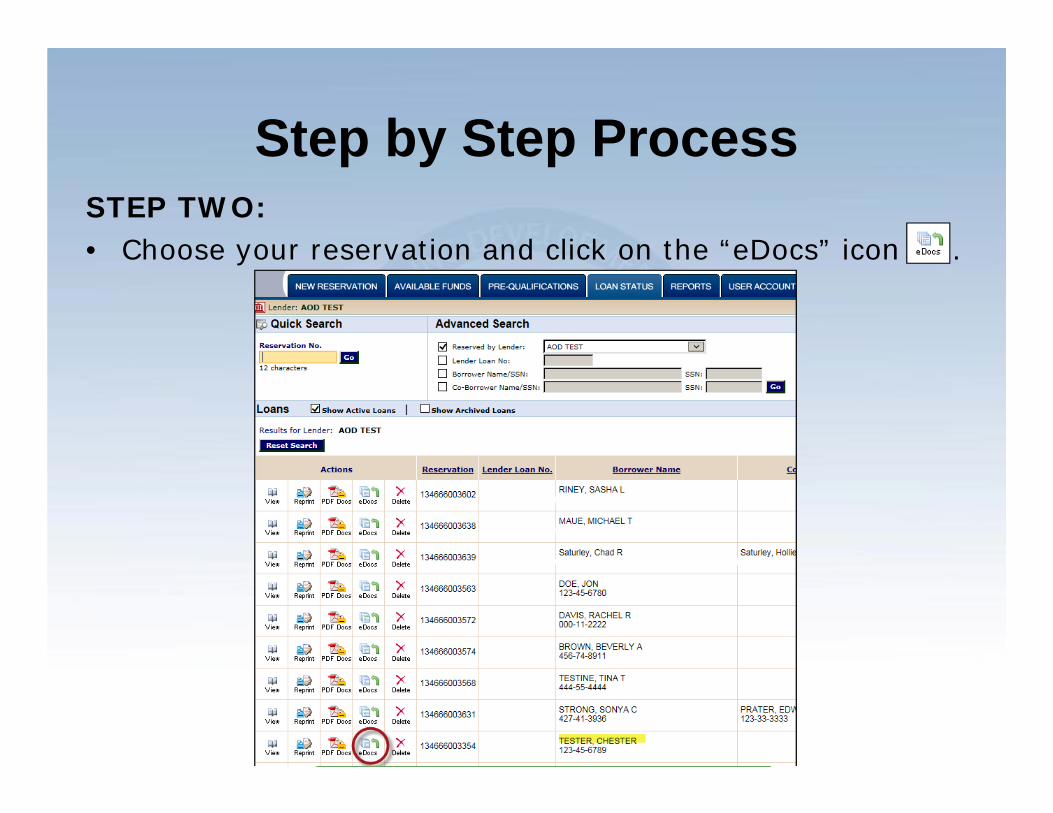

Step by Step ProcessSTEP TWO:• Choose your reservation and click on the “eDocs” icon .

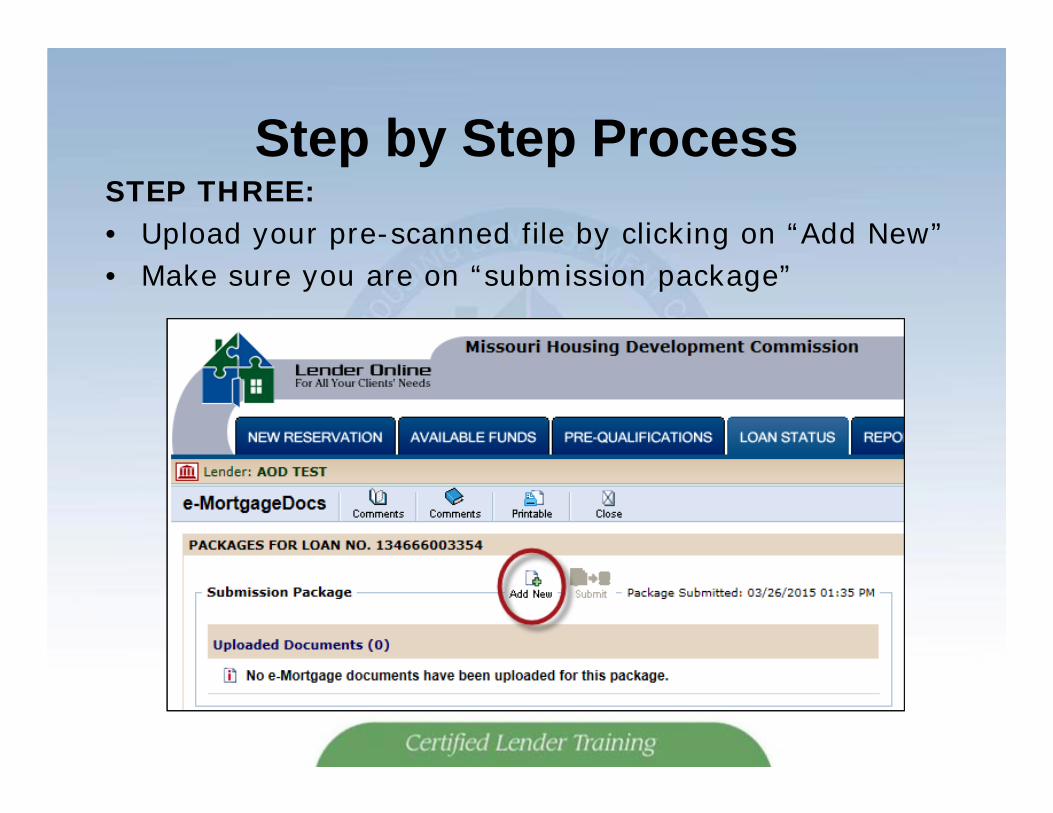

Step by Step ProcessSTEP THREE:• Upload your pre-scanned file by clicking on “Add New”• Make sure you are on “submission package”

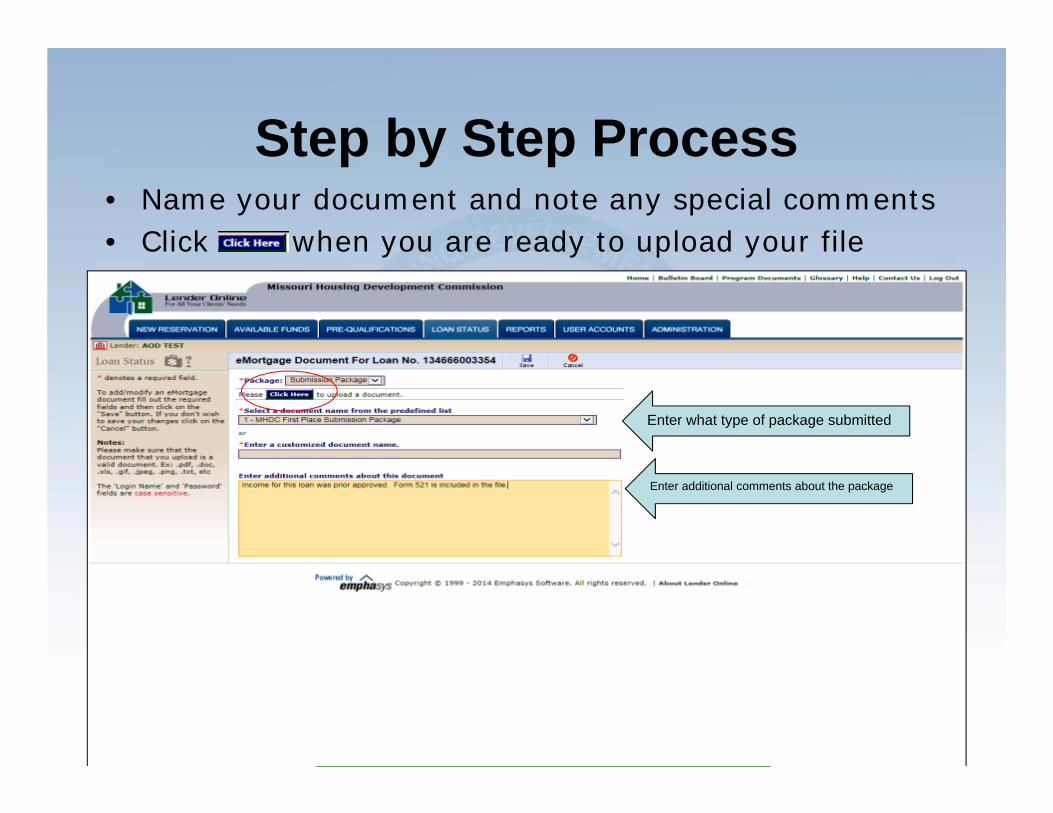

Step by Step Process• Name your document and note any special comments• Click when you are ready to upload your file

Enter what type of package submitted

Enter additional comments about the package

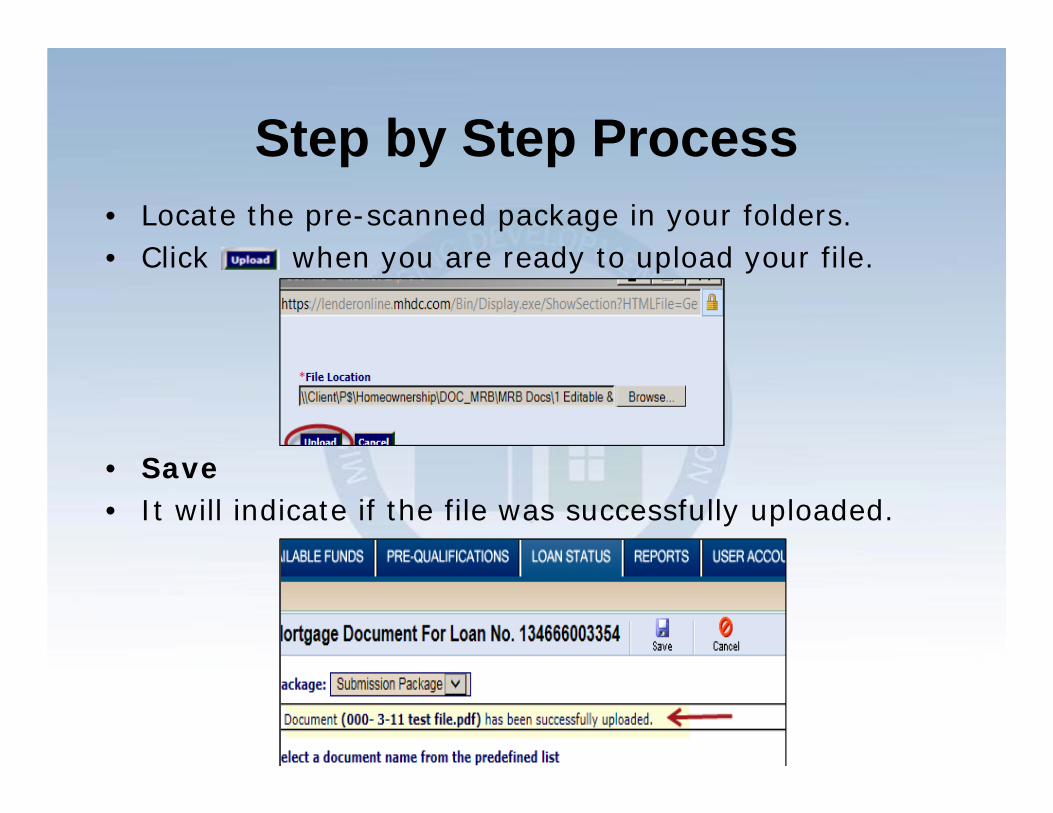

Step by Step Process• Locate the pre-scanned package in your folders.• Click when you are ready to upload your file.

• Save• It will indicate if the file was successfully uploaded.

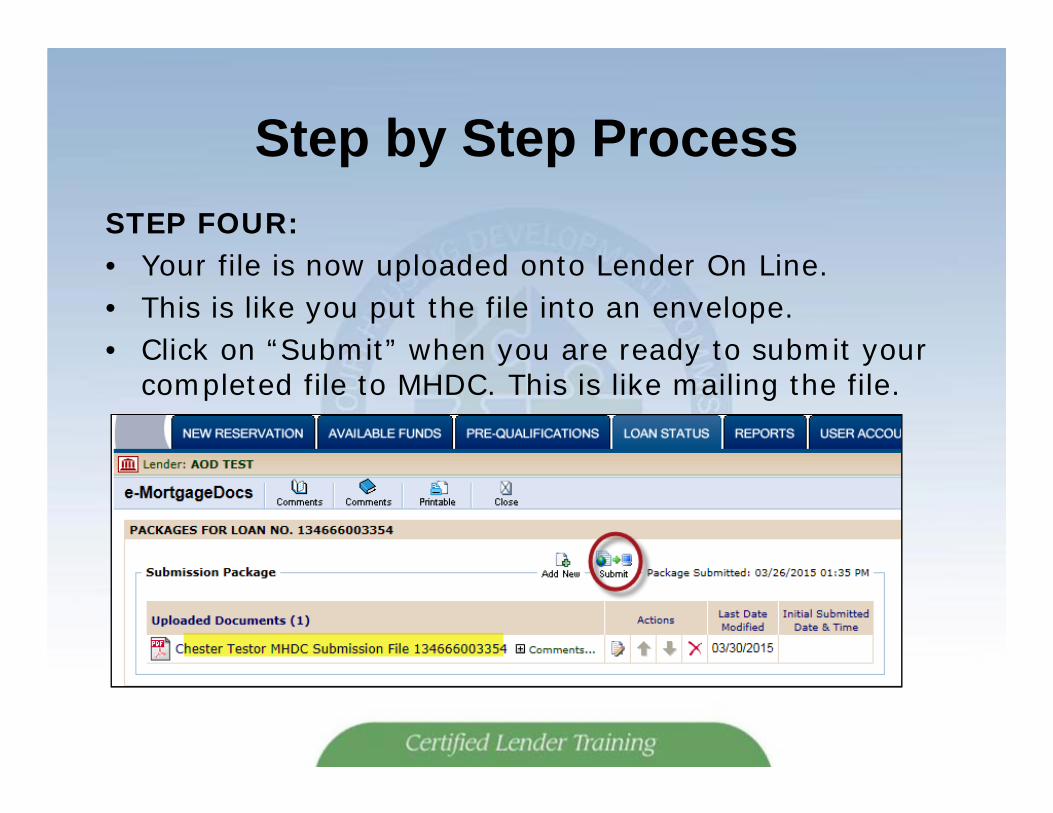

Step by Step ProcessSTEP FOUR:• Your file is now uploaded onto Lender On Line.• This is like you put the file into an envelope.• Click on “Submit” when you are ready to submit your

completed file to MHDC. This is like mailing the file.

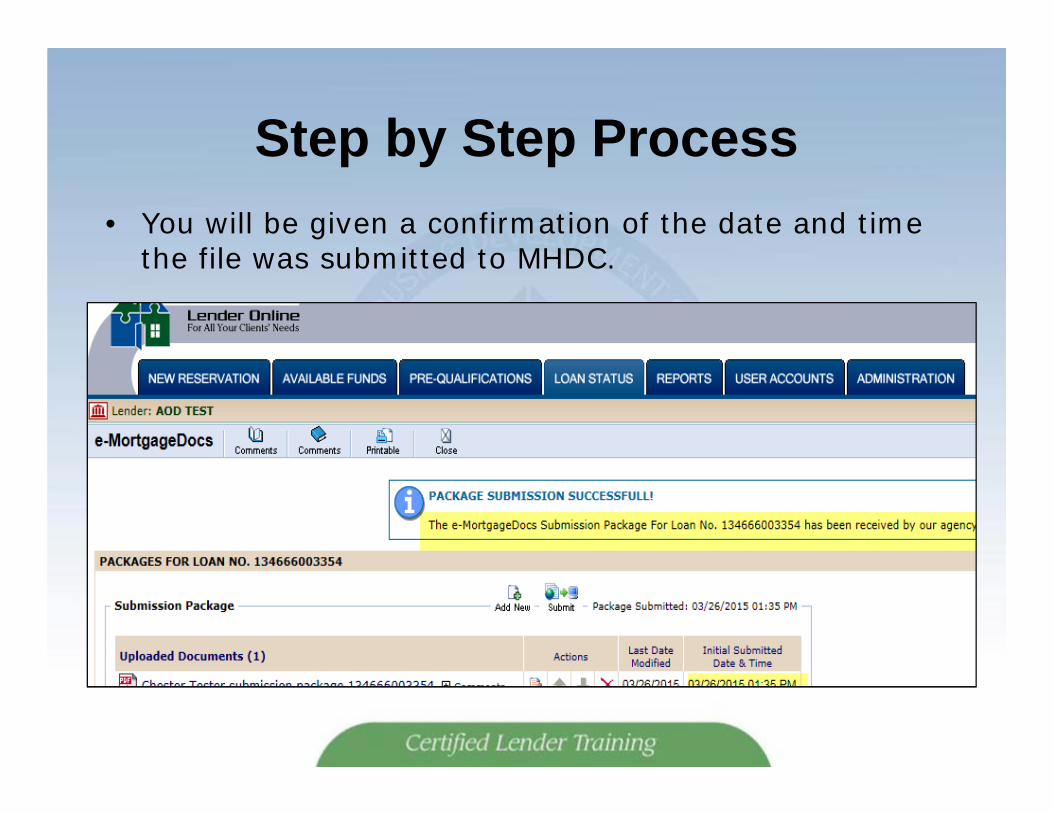

Step by Step Process• You will be given a confirmation of the date and time

the file was submitted to MHDC.

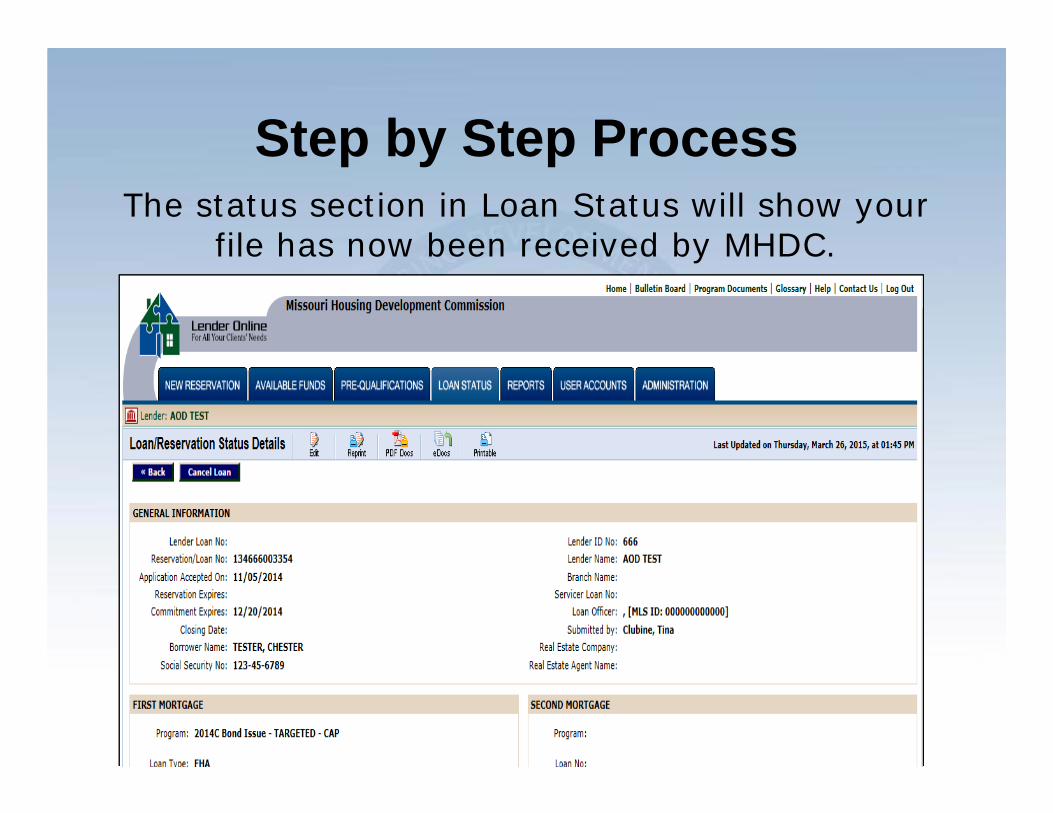

Step by Step ProcessThe status section in Loan Status will show your

file has now been received by MHDC.

Lender Online Status StagesHow do I know if it’s been approved?What are the different stages in LOL?

Lender Online Status Stages• Lenders are able to check the status of their files on Lender

Online under the Loan Status tab.

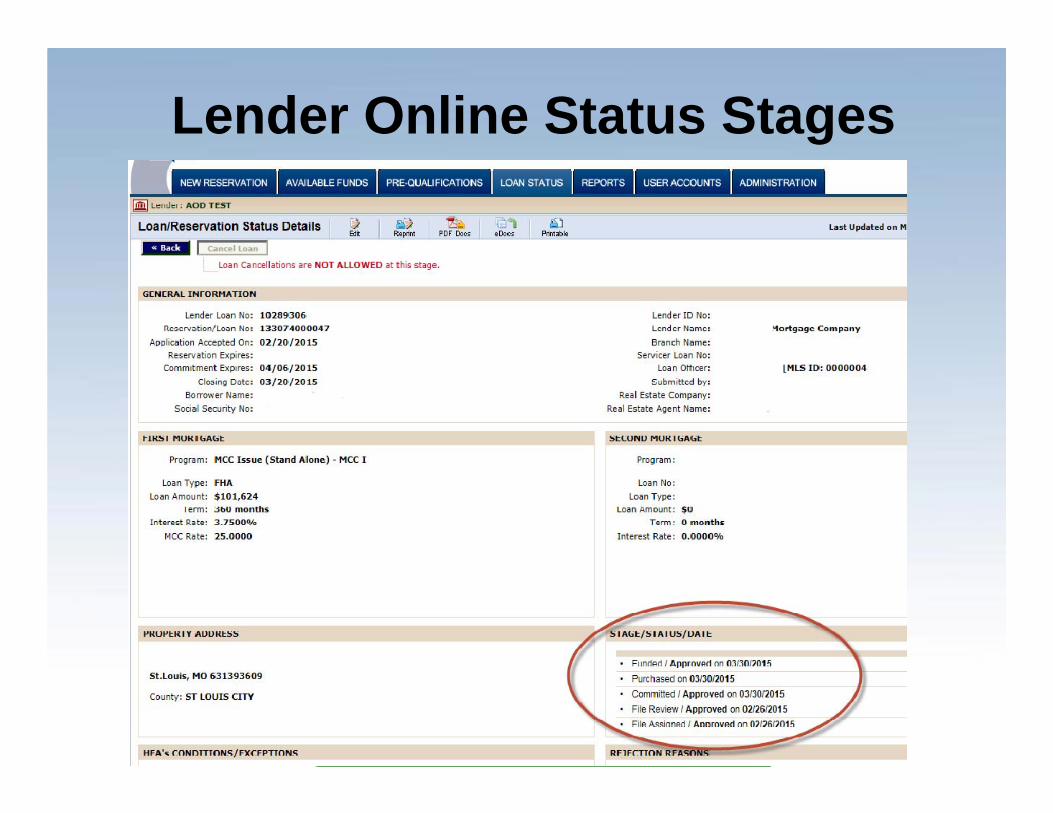

• There are seven stages to each reservation/loan:

1. Reserved – You have made your reservation2. File Rec’d – MHDC has received the file 3. File Assigned – The file has been checked out for review4. File Review – The file is in the process of being reviewed5. Committed – The file has been approved by MHDC6. Purchased – ServiSolutions has purchased the loan7. Funded –MHDC has pooled the loan

Lender Online Status Stages

Lender Online Status Stages

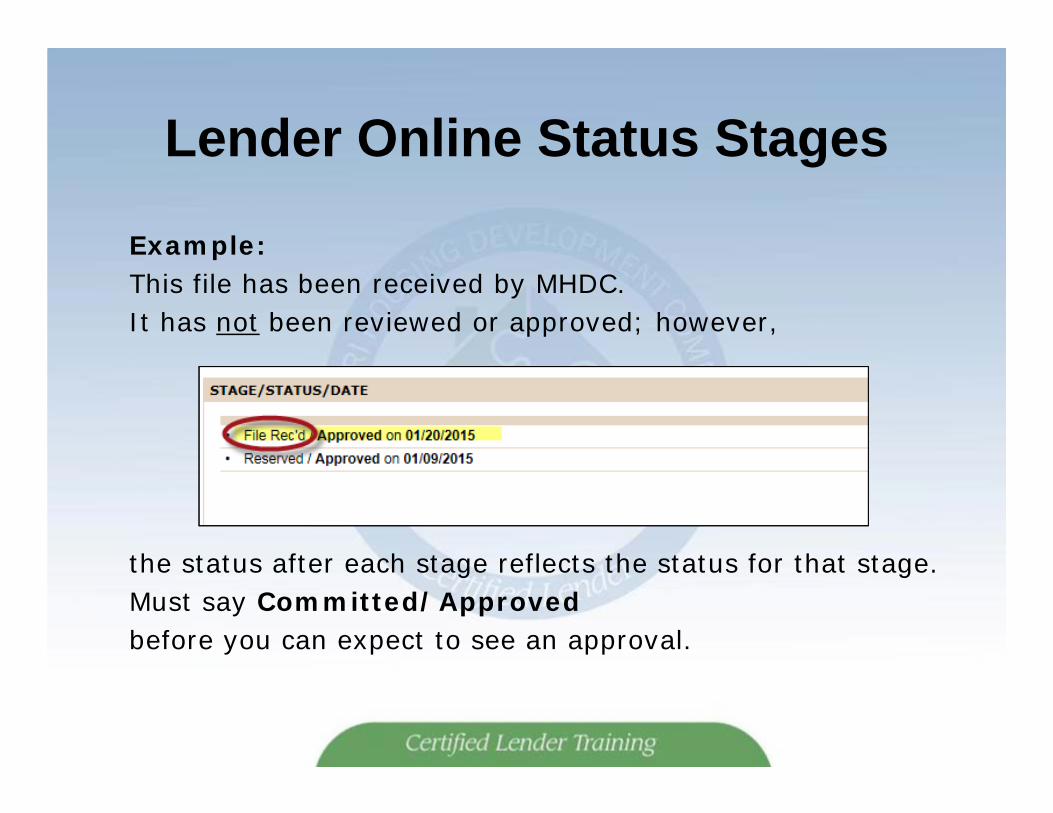

Example:This file has been received by MHDC.It has not been reviewed or approved; however,

the status after each stage reflects the status for that stage.Must say Committed/Approvedbefore you can expect to see an approval.

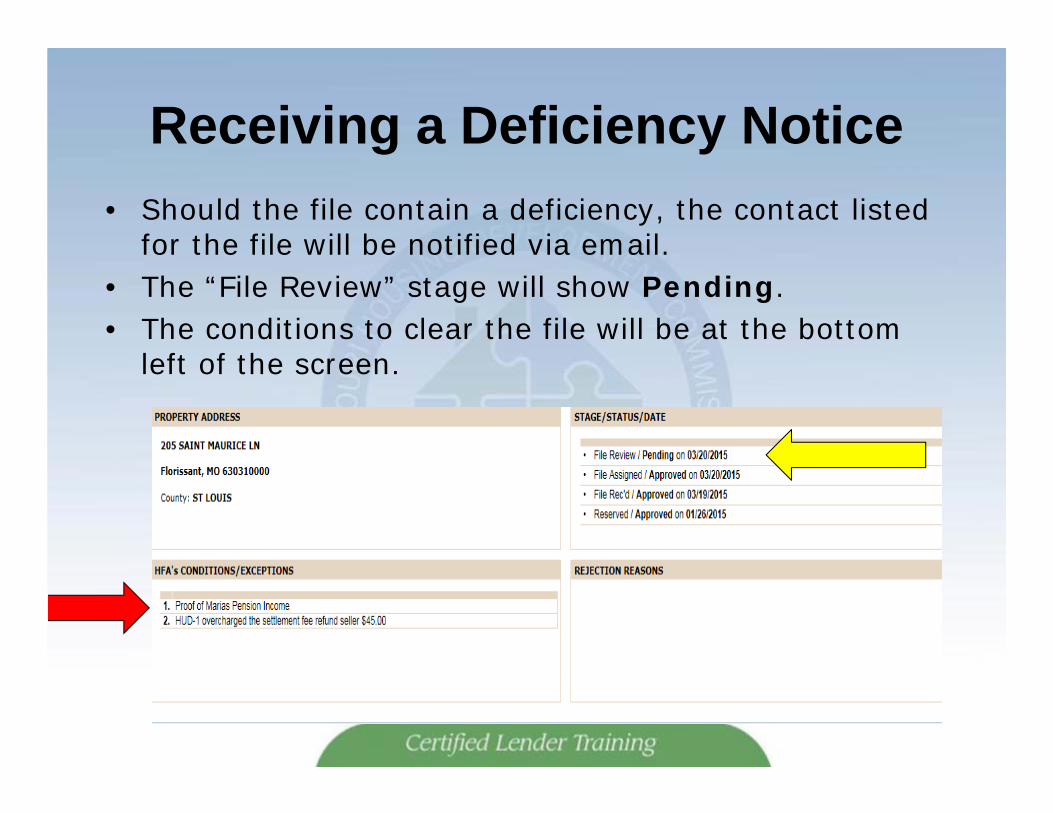

Receiving a Deficiency Notice• Should the file contain a deficiency, the contact listed

for the file will be notified via email.• The “File Review” stage will show Pending.• The conditions to clear the file will be at the bottom

left of the screen.

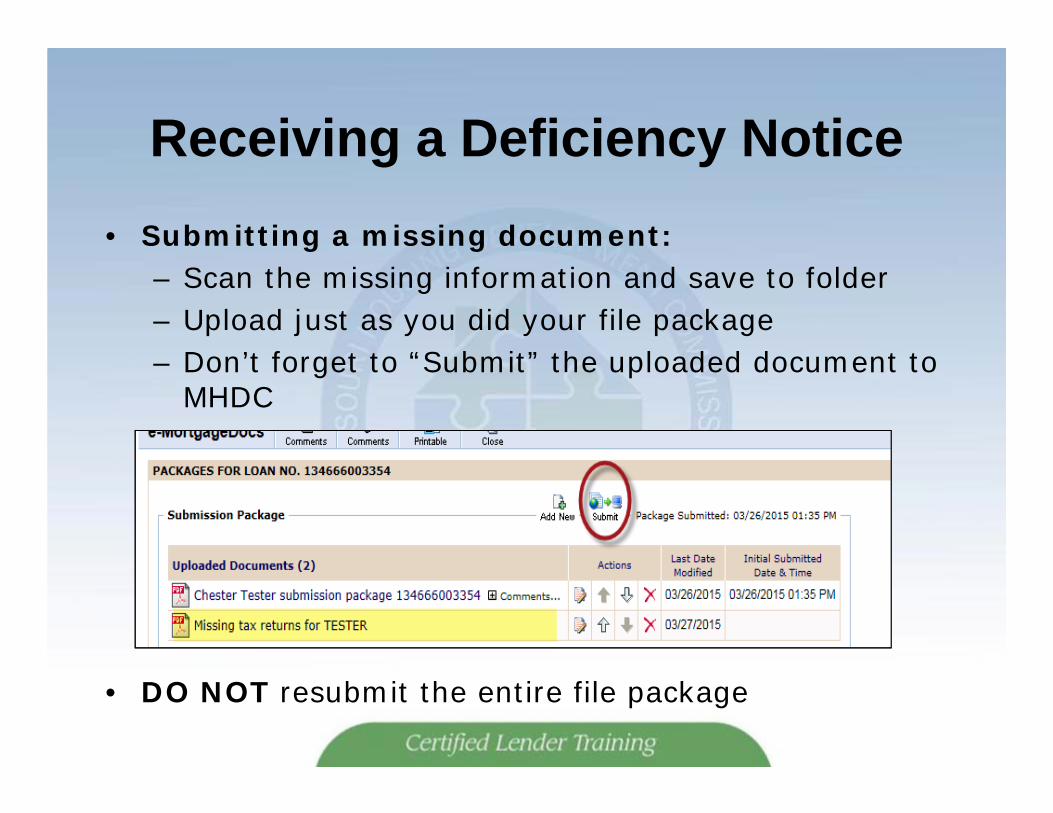

Receiving a Deficiency Notice• Submitting a missing document:

– Scan the missing information and save to folder– Upload just as you did your file package– Don’t forget to “Submit” the uploaded document to

MHDC

• DO NOT resubmit the entire file package

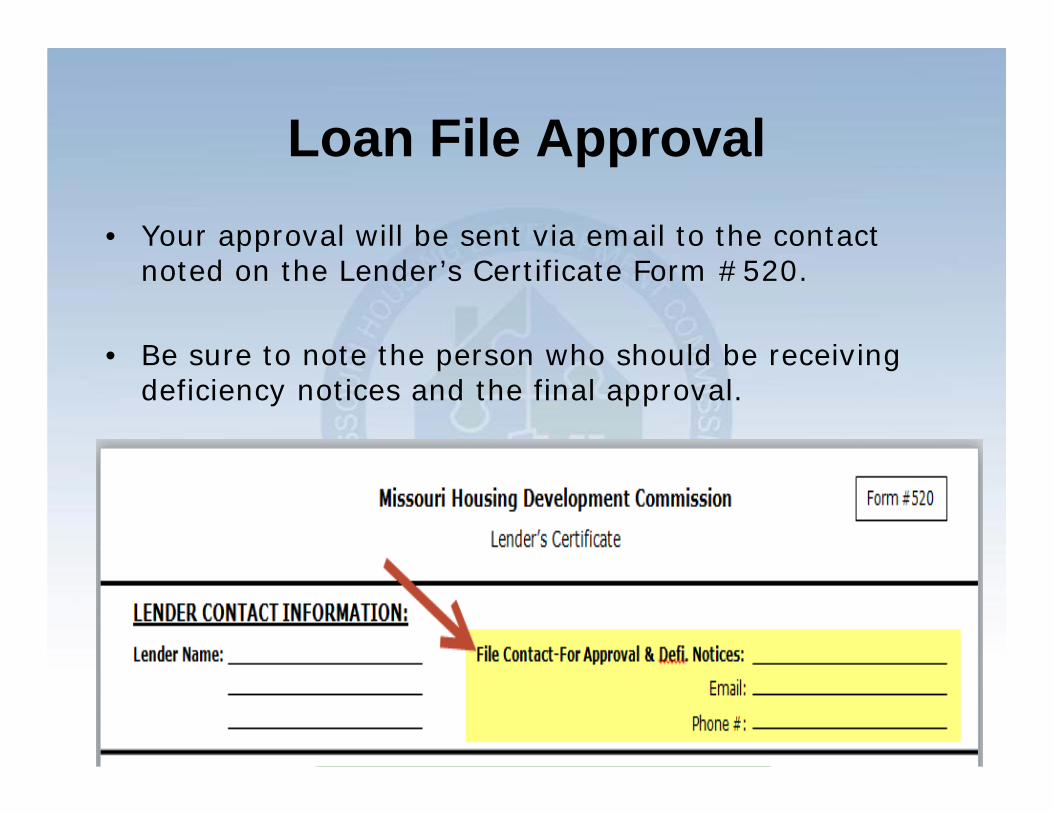

Loan File Approval• Your approval will be sent via email to the contact

noted on the Lender’s Certificate Form #520.

• Be sure to note the person who should be receiving deficiency notices and the final approval.

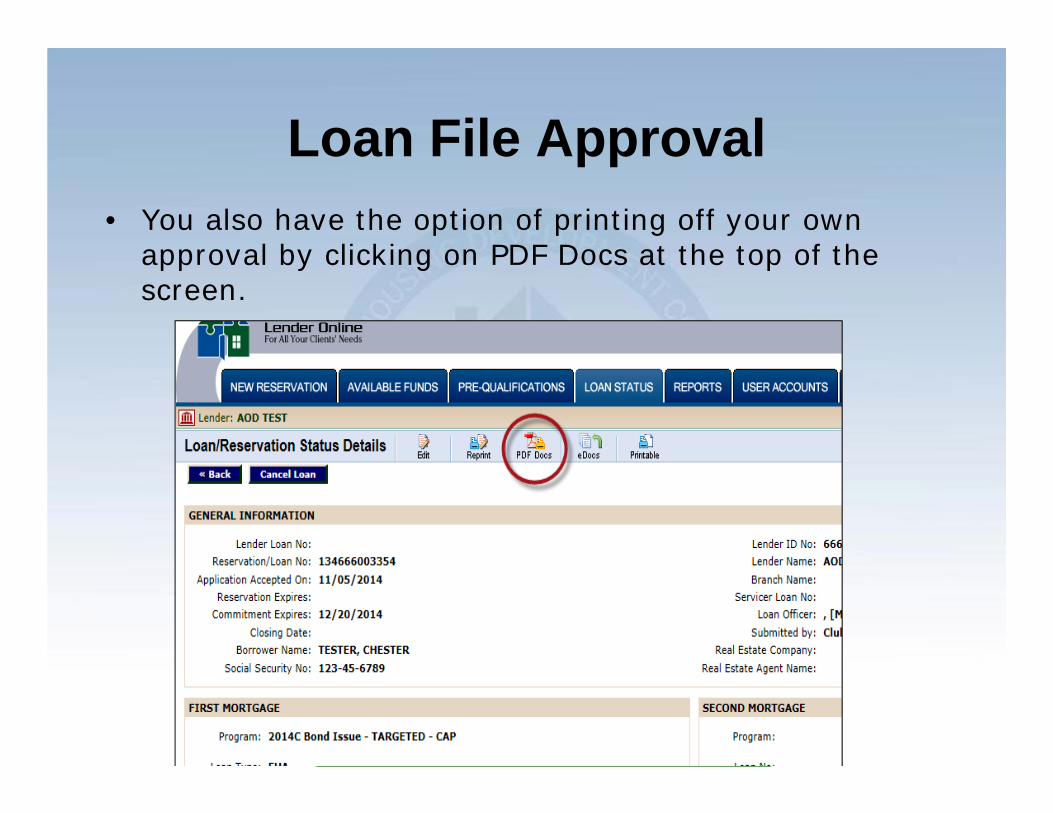

Loan File Approval• You also have the option of printing off your own

approval by clicking on PDF Docs at the top of the screen.

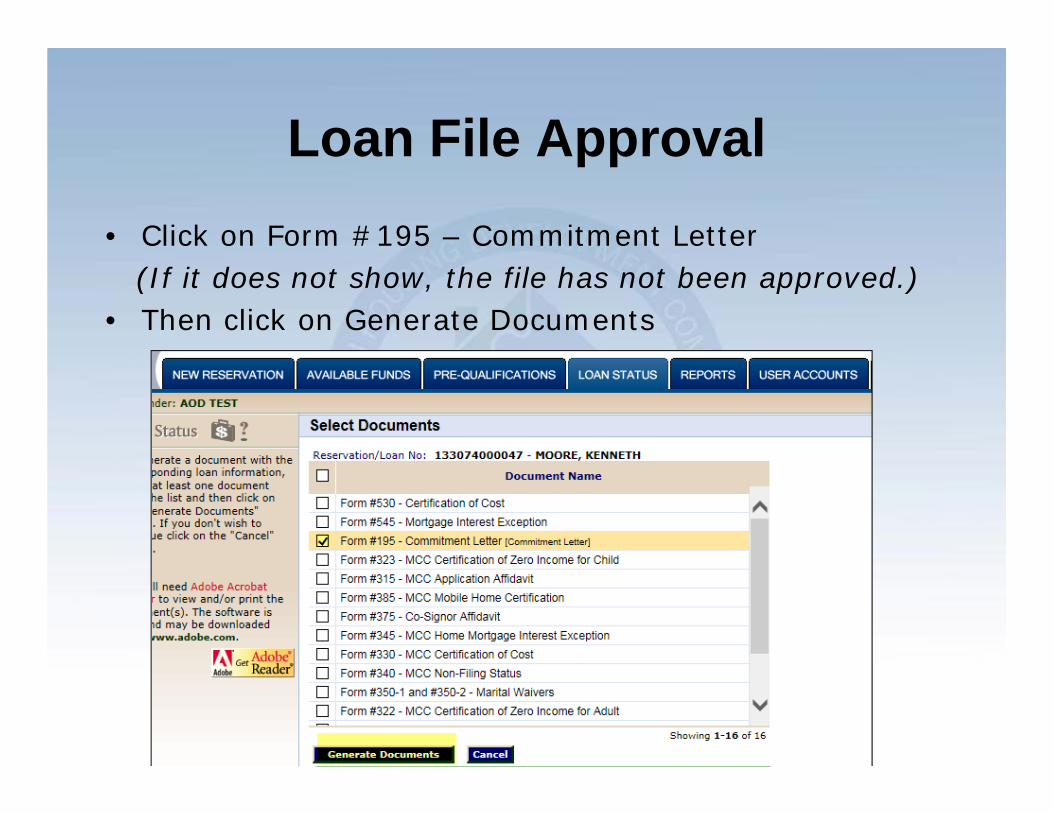

Loan File Approval• Click on Form #195 – Commitment Letter

(If it does not show, the file has not been approved.)• Then click on Generate Documents

Do’s and Don’t to RememberDO

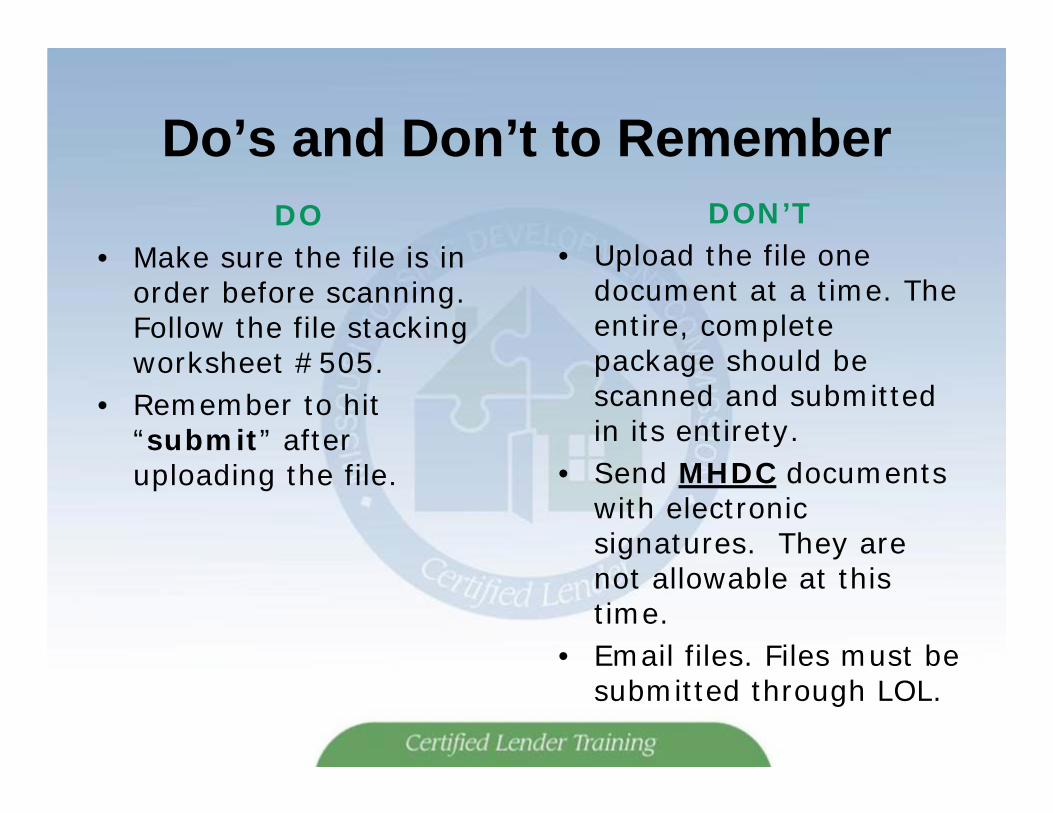

• Make sure the file is in order before scanning. Follow the file stacking worksheet #505.

• Remember to hit “submit” after uploading the file.

DON’T• Upload the file one

document at a time. The entire, complete package should be scanned and submitted in its entirety.

• Send MHDC documents with electronic signatures. They are not allowable at this time.

• Email files. Files must be submitted through LOL.

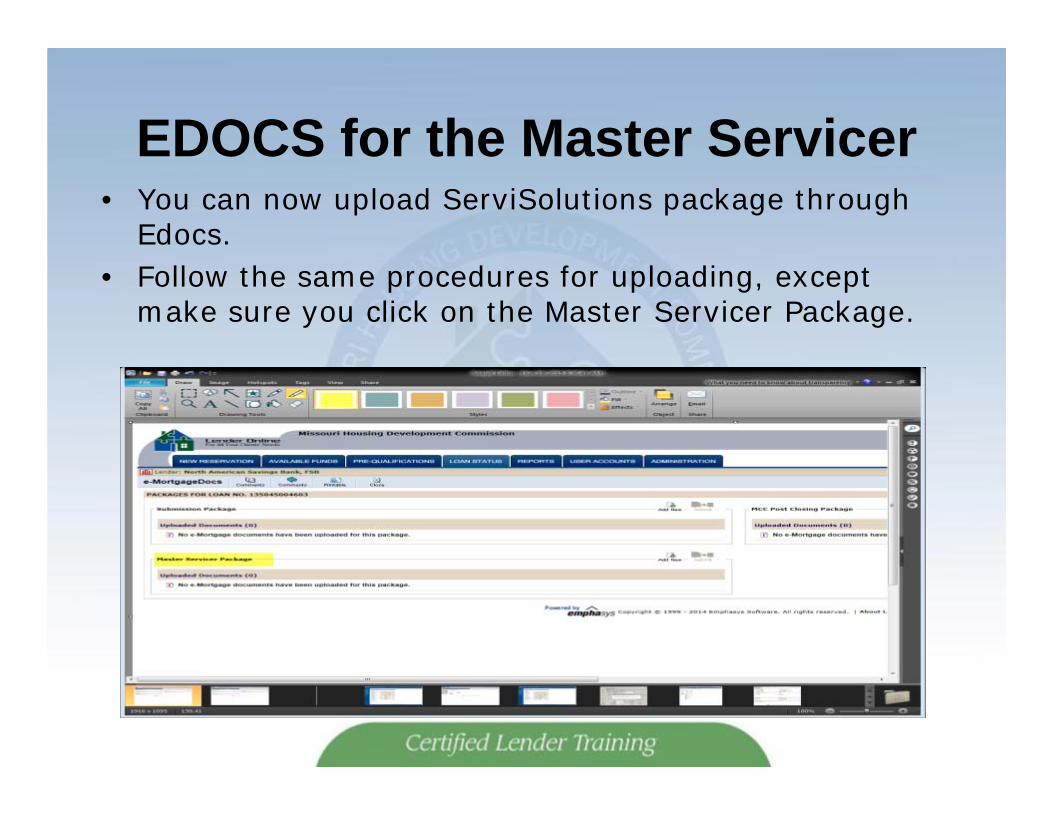

EDOCS for the Master Servicer• You can now upload ServiSolutions package through

Edocs. • Follow the same procedures for uploading, except

make sure you click on the Master Servicer Package.

FILE SUBMISSION

• All suspended files must be corrected within 30 days of notification to the lender

• Reservations for suspended files will be canceled after 30 days

• Lenders are responsible for tracking suspended files

AVOIDING PROBLEMS WITH APPROVALS AFTER CLOSING

• Review file before closing to be sure all information has been provided

• Use checklist to make sure that all information is sent to MHDC correctly & accurately

• Call with questions

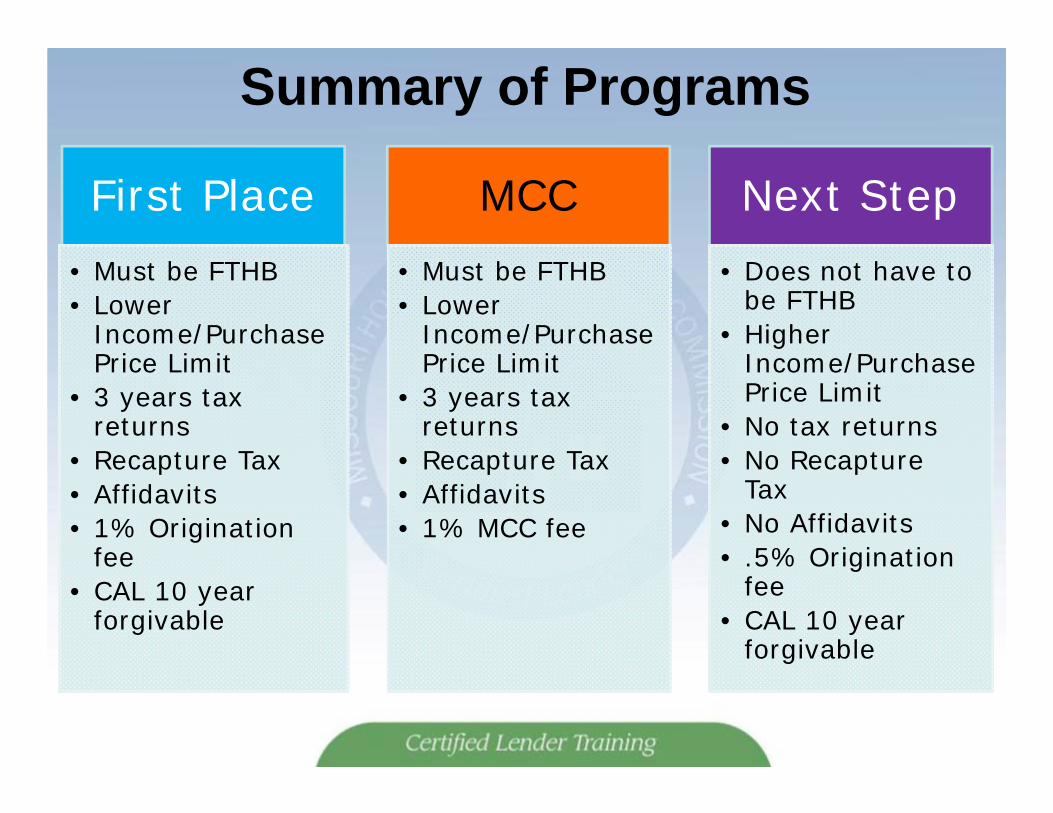

Summary of Programs

First Place• Must be FTHB• Lower

Income/Purchase Price Limit

• 3 years tax returns

• Recapture Tax• Affidavits • 1% Origination

fee• CAL 10 year

forgivable

MCC• Must be FTHB• Lower

Income/Purchase Price Limit

• 3 years tax returns

• Recapture Tax• Affidavits• 1% MCC fee

Next Step• Does not have to

be FTHB• Higher

Income/Purchase Price Limit

• No tax returns• No Recapture

Tax• No Affidavits• .5% Origination

fee• CAL 10 year

forgivable

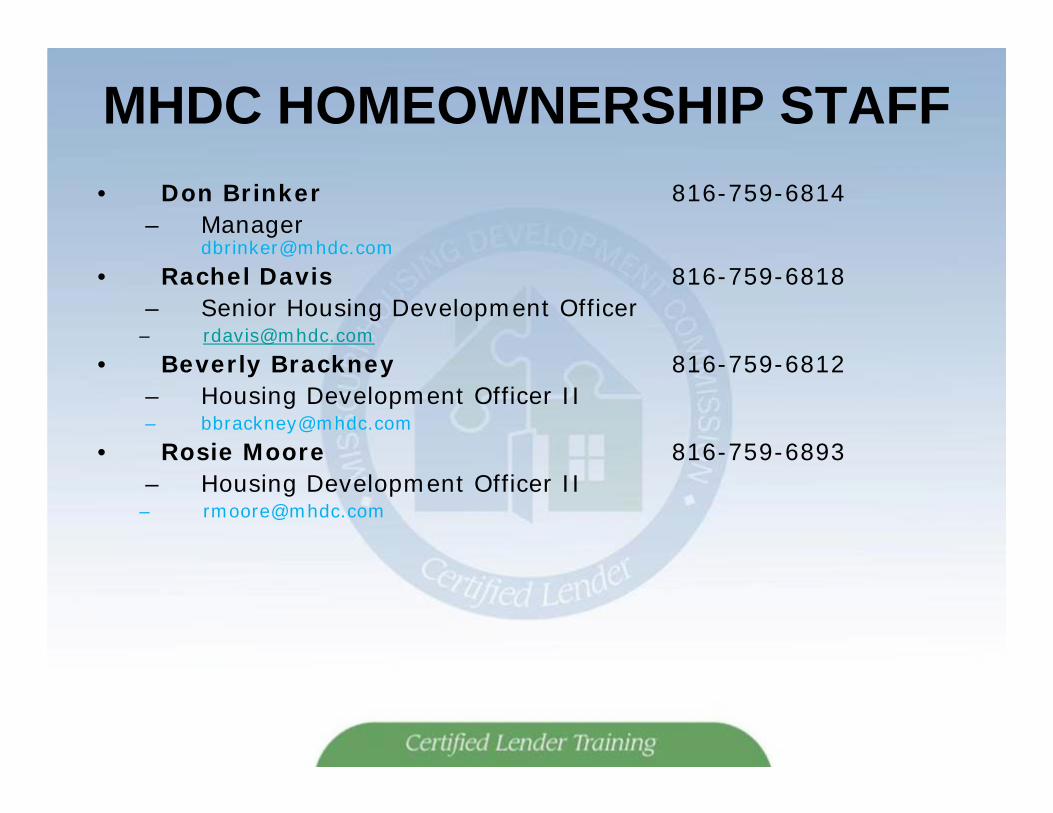

MHDC HOMEOWNERSHIP STAFF• Don Brinker 816-759-6814

• Rachel Davis 816-759-6818– Senior Housing Development Officer– [email protected]

• Beverly Brackney 816-759-6812– Housing Development Officer II– [email protected]

• Rosie Moore 816-759-6893– Housing Development Officer II– [email protected]

WEB SITE• www.mhdc.com

• Contains First Place manual and forms

• Lists upcoming training

• Lists participating lenders

• Lists income limits, sales price limits, target areas, etc.

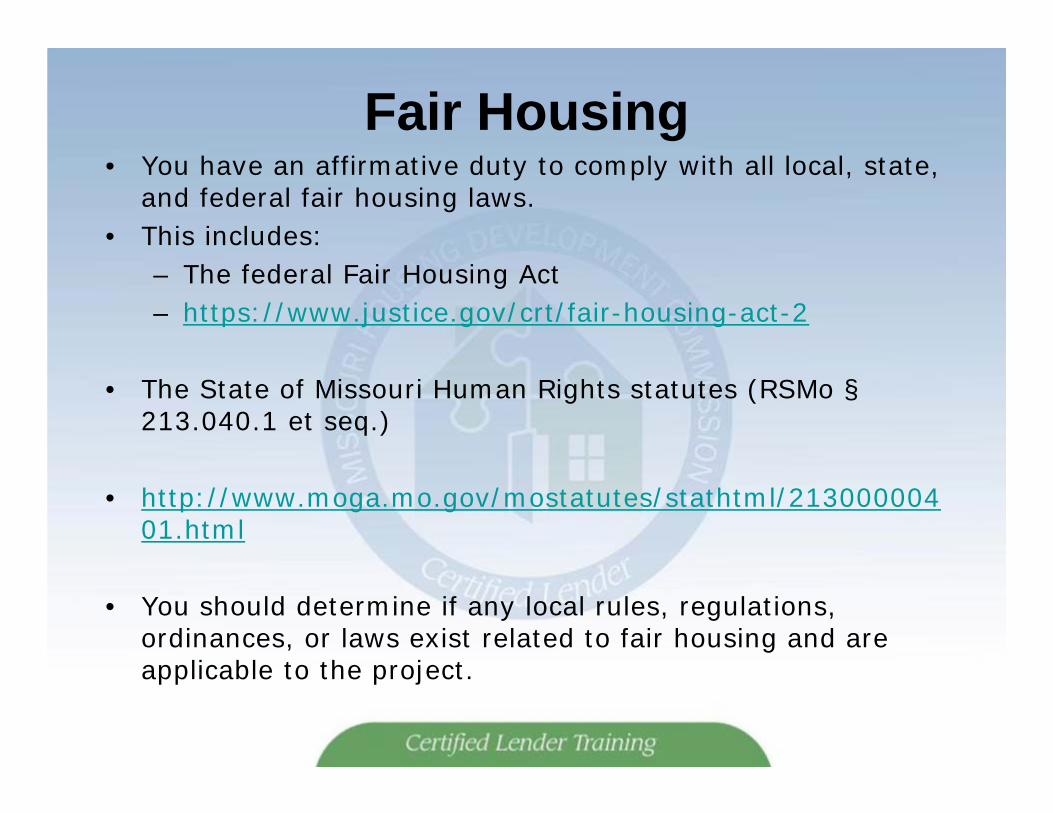

Fair Housing• You have an affirmative duty to comply with all local, state,

and federal fair housing laws.• This includes:

– The federal Fair Housing Act– https://www.justice.gov/crt/fair-housing-act-2

• The State of Missouri Human Rights statutes (RSMo §213.040.1 et seq.)

• http://www.moga.mo.gov/mostatutes/stathtml/21300000401.html

• You should determine if any local rules, regulations, ordinances, or laws exist related to fair housing and are applicable to the project.

Fair Housing• Additional information regarding compliance with fair housing may be located at the following:• The Department of Housing and Urban Development

– Website: https://portal.hud.gov/hudportal/HUD– Fair Housing and Equal Opportunity for All Brochure:

https://portal.hud.gov/hudportal/documents/huddoc?id=FHEO_Booklet_Eng.pdf– Fair Housing Poster:

https://portal.hud.gov/hudportal/documents/huddoc?id=Fair_Housing_Poster_Eng.pdf– Outreach Tools:

https://portal.hud.gov/hudportal/HUD?src=/program_offices/fair_housing_equal_opp/marketing– HUD Resources Page: https://portal.hud.gov/hudportal/HUD?src=/resources– YouTube Channel: https://www.youtube.com/user/HUDchannel

• *Please be aware that not all videos may have been posted by HUD.

• The Missouri Commission on Human Rights– Website: https://labor.mo.gov/mohumanrights– If there are any online trainings sites we can link them here

• National Association of Realtors– Website (Fair Housing Resources): http://www.realtoractioncenter.com/for-associations/fair-housing/

• American Bankers Association– Website (Fair Lending): http://www.aba.com/compliance/pages/fairlending.aspx

• Missouri Housing Development Commission– Website: http://mhdc.com/

• *Information and links are available by clicking on the Equal Housing Opportunity logo on the webpage.

Fair Housing• Questions regarding fair housing or your obligations may be directed to

the following organizations:• Kansas City Regional Office (HUD): • 400 State Avenue, Room 200• Kansas City, KS 66101-2406 • Phone: (913) 551-5462

• St. Louis Regional Office (HUD):• 1222 Spruce Street, Suite 3.203• St. Louis, MO 63103-2836• Phone: (314) 418-5400

• Missouri Commission on Human Rights• 3315 W. Truman Blvd., Rm 212• P.O. Box 1129• Jefferson City, MO 65102-1129• Phone: 573-751-3325• [email protected]

Fair Housing• While some resource locations have been provided

that assist in educating about the duty to comply with fair housing laws it is important that you consult with your legal counsel to ensure that you remain in compliance with fair housing laws at all times. MHDC does not represent or warranty that the resources provided are current or accurate, only that they represent information available from other government agencies or national associations who provide education or monitor compliance with fair housing laws. At no time does MHDC certify your compliance with fair housing laws, through this presentation of information or otherwise, and MHDC assumes no responsibility or liability for your failure to comply with any fair housing law.

THANK YOU for attending

MHDC LENDER TRAINING

THE END