2018 financial results of bank pekao sdc165124-2a28-4ab6-84c8-5aa301f6a354... · finance management...

TRANSCRIPT

2018 Financial results of Bank Pekao S.A Successful execution of our strategic ambitions in 2018

Warsaw, 26th of February 2019

2

Key achievements in 2018

Detailed financial performance in 4Q’18 and 2018

2019 business and financial outlook

Business growth and development

Appendix

1

2

3

4

5

3

Successful execution of our strategic ambitions in 2018

Double-digit RoE in 2018 (10.2%) achieved for a first time since 2014

+10% commercial revenue growth outpacing ca. 2x growth in deployed balance sheet in 2018

Exceeded milestone of +400K new current accounts, powered by a world-class digital platform: PeoPay

150bps improvement in Cost/Income ratio supported by ongoing digital transformation

Strong commercial and operational momentum into 2019 to deliver on our 2020 strategic goals

+11% net profit growth delivering on our ambition and promise, to reach ca. PLN 2.3bn net profit

Achievements Appendix Financial results Outlook Business development

4

Best Corporate Bank in Poland 2018 2nd time in a row

Key achievements in 2018 Double-digit recurring net profit growth delivered in 2018, highest earnings growth since 2011

+11% growth in recurring earnings fulfilling our ambitions for 2018

Robust volume growth in all strategic segments supported by strong

net interest income

+16% earnings increase in Q4(1) driven by another quarter with a strong

‘positive jaws’ effect in revenues and costs

Business development built on global recognition in all key areas

2 061

2 287

2017 2018

2 475

414

+11.0%

Recurring net profit generation

m PLN

The gain on re-measurement to fair value of previously held shares of PPIM & Xelion

Key levers of growth and achievements

World’s most innovative product

Best Private Bank in Poland 2018 4th time in a row

(1) Pro-forma, 2017 figures include results of Pekao Investment Management S.A. and Xelion under a full consolidation method

Achievements Appendix Financial results Outlook Business development

5

1) In units; 2) MID and large corporate ; 3) Share in total number of granted cash loans 4) Incl. the effect of the reduction of own branches by 34; 5) Retail segment

Key achievements in 2018 Successful execution on all commercial levers of our strategy

Key dimensions

Smart

growth

Digital

Acquisition

Business

efficiency

Expanding in most

profitable products &

maximizing cross-sell

potential

Building outstanding

digital experience

Accelerating

to record levels

Unlocking

full potential

of our distribution

New current accounts1, ths.

Mobile banking active Clients, ths. eop

Loans digital sales share3

Consumer loans volume, bn PLN, eop

New SME & Mid Clients

Mid Corporate total assets, bn PLN,eop

Revenue / Client in corporate2, ths. PLN

Number of branches4, eop

KPIs Commercial levers

406 274

1 614 1 239

12.3 10.7

15.3 13.5

135 119

1 263 938

30% 21%

825 851

126 100

+48% Product redesign and value

proposition

Product offer, organisation set-up

and expertise

Pro-active distribution and new

pricing tools

Portfolio-allocation, roll-out of

product offer and expertise

Cross-sell, actions on pricing and

capital allocation

Investment in digital tools

Customer digitalisation; risk and

pricing tools

Focus on profitability of branches

and geo-locations

Product offer, sales force training and

process automatization

2018 2017

+35%

+13%

+14%

+15%

+9pts

-26

+26%

+30%

Revenue / Sales FTE (indexed)5, ths.PLN

Achievements Appendix Financial results Outlook Business development

6

Lending growth and client acquisition Key achievements Digital and innovation

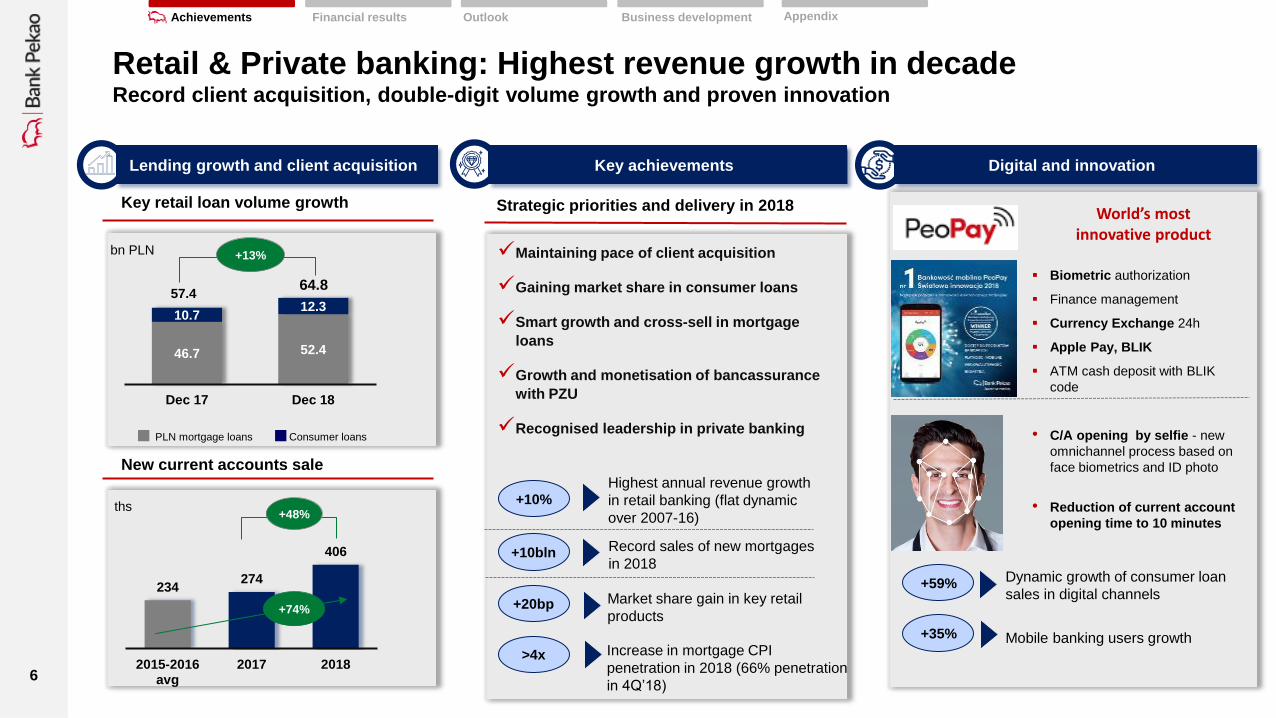

Retail & Private banking: Highest revenue growth in decade Record client acquisition, double-digit volume growth and proven innovation

Key retail loan volume growth

New current accounts sale

46.7 52.4

10.7 12.3

Dec 17 Dec 18

+13%

PLN mortgage loans Consumer loans

57.4 64.8

234 274

406

2015-2016avg

2017 2018

+48%

World’s most innovative product

• C/A opening by selfie - new

omnichannel process based on

face biometrics and ID photo

• Reduction of current account

opening time to 10 minutes

Biometric authorization

Finance management

Currency Exchange 24h

Apple Pay, BLIK

ATM cash deposit with BLIK

code

+74%

bn PLN

Strategic priorities and delivery in 2018

ths

Achievements Appendix Financial results Outlook Business development

Record sales of new mortgages

in 2018 +10bln

+20bp

+10%

Highest annual revenue growth

in retail banking (flat dynamic

over 2007-16)

Market share gain in key retail

products

>4x Increase in mortgage CPI

penetration in 2018 (66% penetration

in 4Q’18)

Maintaining pace of client acquisition

Gaining market share in consumer loans

Smart growth and cross-sell in mortgage

loans

Growth and monetisation of bancassurance

with PZU

Recognised leadership in private banking

+59% Dynamic growth of consumer loan

sales in digital channels

+35% Mobile banking users growth

7

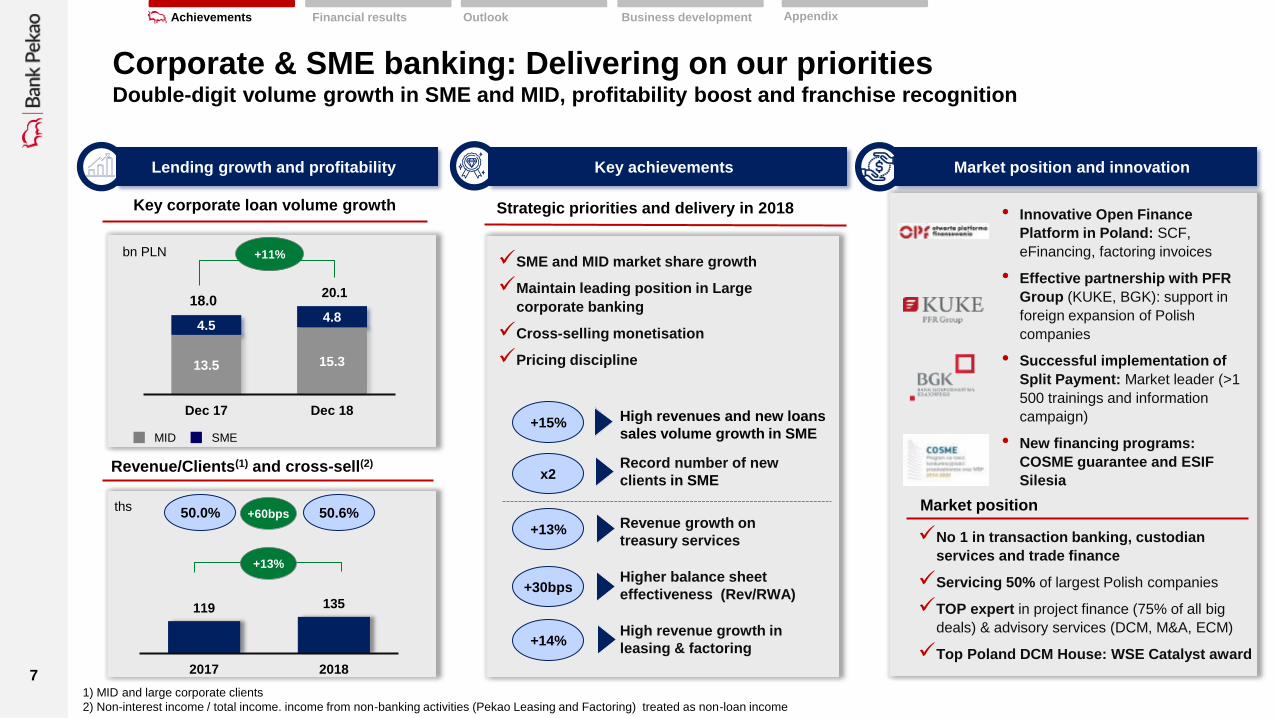

Lending growth and profitability Key achievements

Key corporate loan volume growth

Revenue/Clients(1) and cross-sell(2)

+11%

+13%

+15%

Corporate & SME banking: Delivering on our priorities Double-digit volume growth in SME and MID, profitability boost and franchise recognition

13.5 15.3

4.5 4.8

Dec 17 Dec 18

MID SME

SME and MID market share growth

Maintain leading position in Large

corporate banking

Cross-selling monetisation

Pricing discipline

x2

• Innovative Open Finance

Platform in Poland: SCF,

eFinancing, factoring invoices

• Effective partnership with PFR

Group (KUKE, BGK): support in

foreign expansion of Polish

companies

• Successful implementation of

Split Payment: Market leader (>1

500 trainings and information

campaign)

• New financing programs:

COSME guarantee and ESIF

Silesia

High revenues and new loans

sales volume growth in SME

Record number of new

clients in SME

Revenue growth on

treasury services

+14%

+30bps Higher balance sheet

effectiveness (Rev/RWA)

High revenue growth in

leasing & factoring

No 1 in transaction banking, custodian

services and trade finance

Servicing 50% of largest Polish companies

TOP expert in project finance (75% of all big

deals) & advisory services (DCM, M&A, ECM)

Top Poland DCM House: WSE Catalyst award

Market position

18.0 20.1

bn PLN

Achievements Appendix Financial results Outlook Business development

Market position and innovation

Strategic priorities and delivery in 2018

119 135

2017 2018

+13%

50.6% 50.0% +60bps

1) MID and large corporate clients

2) Non-interest income / total income. income from non-banking activities (Pekao Leasing and Factoring) treated as non-loan income

ths

8

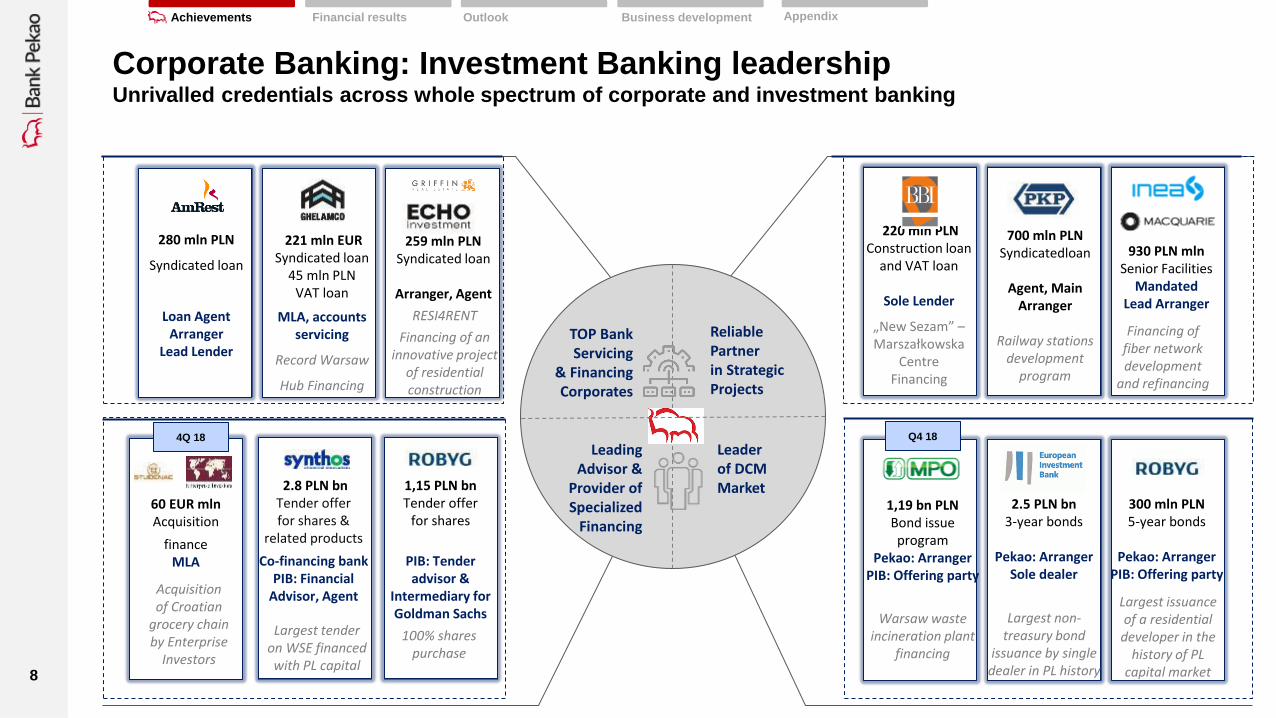

Corporate Banking: Investment Banking leadership Unrivalled credentials across whole spectrum of corporate and investment banking

TOP Bank Servicing

& Financing Corporates

Leading Advisor &

Provider of Specialized

Financing

Reliable Partner in Strategic Projects

Leader of DCM Market 2.8 PLN bn

Tender offer for shares &

related products

Co-financing bank PIB: Financial

Advisor, Agent

1,15 PLN bn Tender offer

for shares

PIB: Tender advisor &

Intermediary for Goldman Sachs

280 mln PLN

Syndicated loan

Loan Agent Arranger

Lead Lender

259 mln PLN Syndicated loan

Arranger, Agent

Largest tender on WSE financed with PL capital

100% shares purchase

60 EUR mln Acquisition

finance MLA

Acquisition of Croatian

grocery chain by Enterprise

Investors

RESI4RENT

Financing of an innovative project

of residential construction

221 mln EUR Syndicated loan

45 mln PLN VAT loan

MLA, accounts servicing

Record Warsaw

Hub Financing

220 mln PLN Construction loan

and VAT loan

Sole Lender

„New Sezam” –Marszałkowska

Centre Financing

700 mln PLN Syndicatedloan

Agent, Main

Arranger

Railway stations development

program

1,19 bn PLN Bond issue program

Pekao: Arranger PIB: Offering party

Warsaw waste incineration plant

financing

300 mln PLN 5-year bonds

Pekao: Arranger

PIB: Offering party

Largest issuance of a residential

developer in the history of PL

capital market

2.5 PLN bn 3-year bonds

Pekao: Arranger

Sole dealer

Largest non-treasury bond

issuance by single dealer in PL history

Q4 18 4Q 18

Financing of fiber network development

and refinancing

930 PLN mln Senior Facilities

Mandated Lead Arranger

Achievements Appendix Financial results Outlook Business development

9

Strategic partnerships in key areas Five partnerships already underway

Key

str

ate

gic

par

tne

rsh

ips

in 2

01

8

Key f

oc

us a

rea

s h

igh

ly c

orr

ela

ted

wit

h S

trate

gy 2

02

0 t

arg

ets

Acquisition

of Customers

& new business

models

Digital transformation

and innovations

Value added services

for Customers

Digital Journeys Programme supporting the digital transformation of the Polish society and small and

medium business

Joint efforts towards digital education and promotion of digital and cloud solutions among individual

and business Customers

Providing access to selected best-in-class digital and cloud solutions for the bank

Strengthening the leading position on the Polish market trough wider access to global investors

Joint approach to selected high value transactions on Polish market

Identification and support for global M&A opportunities for Polish companies

Joining the world leading and innovative blockchain network of over 150 banks

Streamlining the international settlements and operations minimizing friction in the cross-border

payments and strengthening compliance and security of operations

Education and

development of the

society

Addressing the 4th industrial revolution challenges through education and innovative solutions

Education programme AI Schools & Academy for kids and youths providing AI classes in 1500

schools in Poland and enabling participants to test the new skills in real life

Providing the small and medium business with an opportunity to leverage the digital economy

through the state-of-art AI based advanced analytics solutions - Pekao Navigator

Supporting building the awareness of an important social problem - anti-cancer prophylaxis

Comprehensive care about the well-being of the Employees and Customers both in terms of finance

and health

Achievements Appendix Financial results Outlook Business development

10

Investor Day London Rep. Office Opening London CEO Summit Warsaw European Financial Congress Sopot

Awards and events Recognition by market and industry experts

Corporate Bank

EFMA-Accenture Distribution & Marketing Innovation Awards 2018

PeoPay: the most innovative 2018 project

Retail & Private

Newsweek: #1 most customer -friendly mortgage bank in Poland

TOP EMPLOYER 2018/2019 8th time in a row

World’s Best Private Banks 2018 4th time in a row

WSE RESPECT Index Pekao among socially responsible companies 3rd time in a row

Bank Pekao SA infoline once again the best in Poland

Pekao TFI: 1st in the Customer Laurel contest 2019 in the "Investment Fund Companies" category for

Best Corporate Bank in Poland 2018 2nd time in a row

The Best Investment Bank in Poland 2018 2nd time in a row

Best Investment Bank

Best Sub-Custodian in Poland 2018 6th time in a row

Aw

ard

s

Eve

nts

Business Inspirator 2018 - „Innovations”

Pekao Connect – Innowacja 2018

Forbes: #2 Best bank for business customers (#11 in 2017)

WEF Davos

Achievements Appendix Financial results Outlook Business development

11

2017 (ΔY/Y) (1) 2018 (ΔY/Y) Strategic path to 2020

Growth

Loan growth +7% +6% +7-8% (CAGR 2017-20)

Commercial

revenues +4% +10% +10% (CAGR 2017-20)

Efficiency

Cost dynamics +1.6% +2.3% (2) Cost dynamic below CPI inflation

C/I (excl. BFG) 45.3%(3) 43.8% (2) < 40%

Risk CoR 40bps (3) 38bps (3) Up to ~50bps

Profitability ROE 9.2% 10.2% 12.5% (flat interest rates)

(1) Pro-forma, 2017 figures include results of Pekao Investment Management S.A. and Xelion under a full consolidation method and exclude one-off gain on re-measurement to fair value of previously held shares of PPIM

& Xelion

(2) Excluding the cost of voluntary retirement programme of PLN 50m in 1H18

(3) Excluding the impact of the sale of NPLs in 2017 and 2018

Value for investors We are on a clear path to achieve our strategic financials targets in 2020

Key dimensions

Key financial achievements in 2018 Tangible progress achieved on our key financial KPIs

Achievements Appendix Financial results Outlook Business development

12

Key achievements in 2018

Detailed financial performance in 4Q’18 and 2018

2019 business and financial outlook

Business growth and development

Appendix

1

2

3

4

5

13

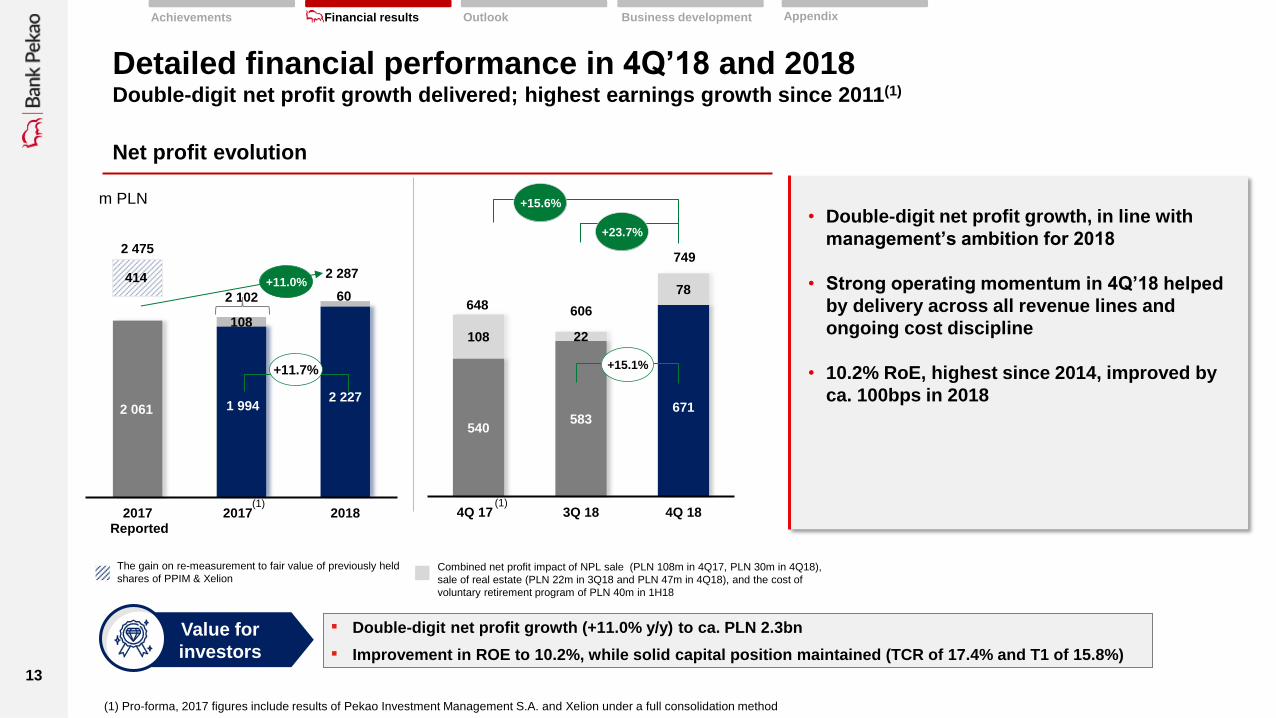

Detailed financial performance in 4Q’18 and 2018 Double-digit net profit growth delivered; highest earnings growth since 2011(1)

• Double-digit net profit growth, in line with

management’s ambition for 2018

• Strong operating momentum in 4Q’18 helped

by delivery across all revenue lines and

ongoing cost discipline

• 10.2% RoE, highest since 2014, improved by

ca. 100bps in 2018

2 061 1 994 2 227

60

108

2017 Reported

2017 2018

2 287

+11.7%

2 475

414 +11.0%

2 102

(1)

Net profit evolution

m PLN

540 583

671

108 22

78

4Q 17 3Q 18 4Q 18

749

648 606

+23.7%

+15.6%

(1)

+15.1%

▪ Double-digit net profit growth (+11.0% y/y) to ca. PLN 2.3bn

▪ Improvement in ROE to 10.2%, while solid capital position maintained (TCR of 17.4% and T1 of 15.8%)

Value for

investors

The gain on re-measurement to fair value of previously held

shares of PPIM & Xelion Combined net profit impact of NPL sale (PLN 108m in 4Q17, PLN 30m in 4Q18),

sale of real estate (PLN 22m in 3Q18 and PLN 47m in 4Q18), and the cost of

voluntary retirement program of PLN 40m in 1H18

(1) Pro-forma, 2017 figures include results of Pekao Investment Management S.A. and Xelion under a full consolidation method

Achievements Appendix Financial results Outlook Business development

14

Detailed financial performance in 4Q’18 and 2018 Record high gross operating profit due to revenue growth and cost discipline

Gross operating profit Operating income

Operating costs

m PLN

• 2018 gross operating profit at PLN 4.4bn, +8.9 y/y on a comparable

basis, thanks to strong income generation and ongoing cost discipline

• Strong 4Q’18 momentum on the back of +7.5% y/y operating income

increase and fall in costs by 1.9% y/y

• Underlying C/I ratio improved by 150bps to 43.8% in 2018, despite

ongoing investment initiatives in digital and operational transformation

7 325

7 757

2017 2018

+5.9%

(1)

864

843 848

4Q 17 3Q 18 4Q 18

-1.9%

+0.5%

(1)

3 319 3 394

50

2017 2018

+3.8% +2.3%

(1)

1 901 1 933

2 044

4Q 17 3Q 18 4Q 18

+7.5%

+5.7%

(1)

1 037 1 089

1 196

4Q 17 3Q 18 4Q 18

+15.3%

+9.8%

(1)

m PLN

m PLN

1) Pro-forma, 2017 figures include results of Pekao Investment Management S.A. and Xelion under a full consolidation method

2) Excluding impact of the cost of voluntary retirement program of PLN 50m in 1H18

4 006 4 313

50

2017 2018

+8.9%

4 006 4 363

(1)

+7.7%

XX% Dynamic excluding impact of the cost of voluntary retirement program of PLN 50m in 1H18

The cost of voluntary retirement program of PLN 50m in 1H18

Appendix Outlook Business development Achievements Financial results

(2)

15

• Continued strong growth

momentum in all businesses

on the back of robust net

interest income and resilience

across fee & commission lines

• Commercial revenue growth

of 10% y/y significantly

outpacing balance sheet growth

7 102 7 457

222

301

2017 2018

7 325

+5.9%

(1)

Detailed financial performance in 4Q’18 and 2018 Acceleration of income generation in 4Q’18; Strong commercial activity across all businesses

Operating income

Other income Core income

1 836 1 877

1 933

65

56

111

4Q 17 3Q 18 4Q 18

1 901

1 933

2 044

+7.5%

7 757

+5.7%

m PLN

1) Pro forma, 2017 figures include results of Pekao Investment Management S.A. and Xelion under a full consolidation method

Strong revenue dynamics

across commercial activity

10%

15%

8%

10%

-7%

Retail &

Private

SME

Corporate

Total

Commercial

2018 ΔY/Y%

ALM and

Others

Effect of obligatory reserves

and lower bond yields

2) Proceeds from NPL sales reported under credit provision line in 2018

(1)

Appendix Outlook Business development Achievements Financial results

(2)

16

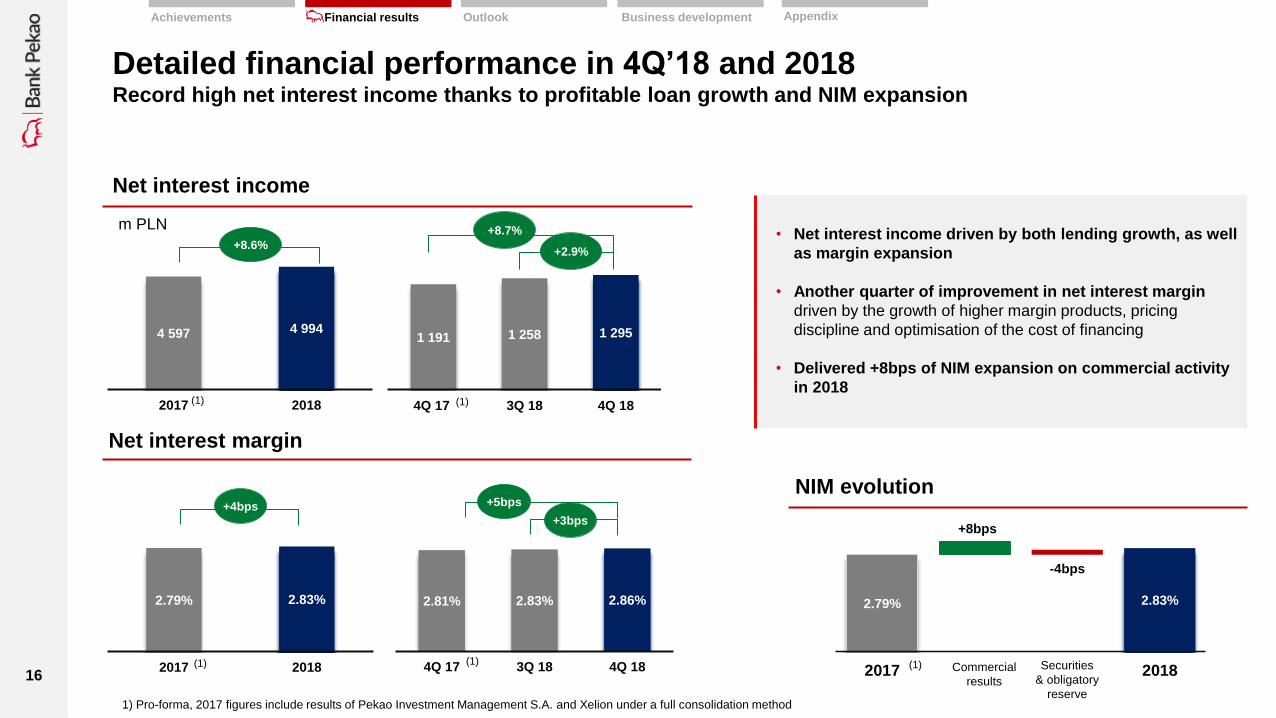

Detailed financial performance in 4Q’18 and 2018 Record high net interest income thanks to profitable loan growth and NIM expansion

Net interest margin

• Net interest income driven by both lending growth, as well

as margin expansion

• Another quarter of improvement in net interest margin

driven by the growth of higher margin products, pricing

discipline and optimisation of the cost of financing

• Delivered +8bps of NIM expansion on commercial activity

in 2018

2.79% 2.83%

2017 2018

+4bps

(1)

4 597 4 994

2017 2018

+8.6%

(1)

2.81% 2.83% 2.86%

4Q 17 3Q 18 4Q 18

+3bps

(1)

m PLN

+5bps

1 191 1 258 1 295

4Q 17 3Q 18 4Q 18

+8.7%

+2.9%

(1)

Net interest income

1) Pro-forma, 2017 figures include results of Pekao Investment Management S.A. and Xelion under a full consolidation method

2.79% 2.83%

+8bps

-4bps

2017 2018Commercial

results

Securities

& obligatory

reserve

NIM evolution

(1)

Appendix Outlook Business development Achievements Financial results

17

Detailed financial performance in 4Q’18 and 2018 Loan origination concentrated on most profitable segments

• Total lending growth of 6% y/y

• Targeted lending activity with 12.8% y/y

increase in key retail lending and 4.4%

lending growth deployed in core corporate

• 20bps of market share gains in key retail

lending through 2018

• Growth in corporate loan portfolio focused

on most profitable segments, with 12.6% y/y

loan volume expansion in mid-market

corporate sector

6 748 6 121 6 131

57 408 63 190 64 784

Dec 17 Sep 18 Dec 18

64 157

69 311 70 915

+12.8%

13 999 13 509 12 727

58 719 60 215 61 299

Dec 17 Sep 18 Dec 18

72 717 73 724 74 027

+4.4%

Corporates (Core corporate)

Other corporate loans (Public sector)

Key retail loans (PLN mortgage, consumer loans)

Other retail loans

+10.5%

+2.3%

+1.8%

+0.4%

Retail loans(1) Corporate loans(2)

1) Gross loans

2) Gross loans, corporate and SME including leasing and factoring, excl. BSB and reverse repo transactions

Appendix Outlook Business development Achievements Financial results

18

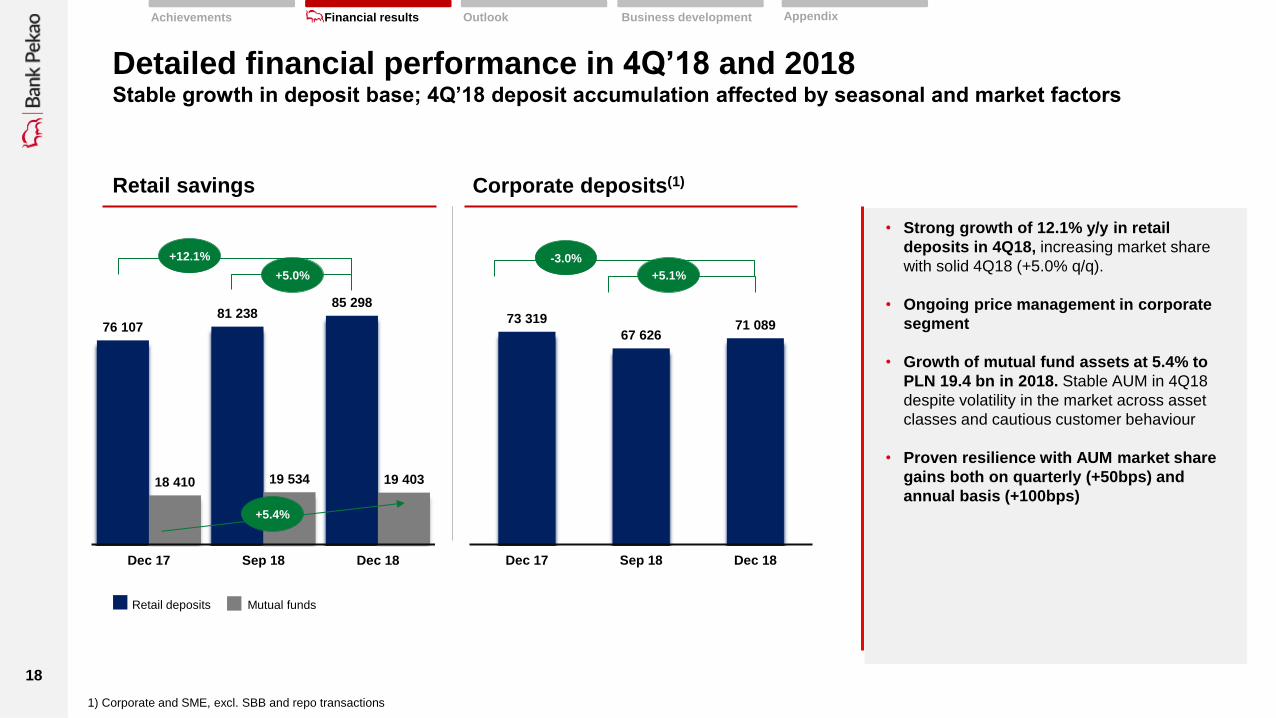

Detailed financial performance in 4Q’18 and 2018 Stable growth in deposit base; 4Q’18 deposit accumulation affected by seasonal and market factors

• Strong growth of 12.1% y/y in retail

deposits in 4Q18, increasing market share

with solid 4Q18 (+5.0% q/q).

• Ongoing price management in corporate

segment

• Growth of mutual fund assets at 5.4% to

PLN 19.4 bn in 2018. Stable AUM in 4Q18

despite volatility in the market across asset

classes and cautious customer behaviour

• Proven resilience with AUM market share

gains both on quarterly (+50bps) and

annual basis (+100bps)

76 107 81 238

85 298

18 410 19 534 19 403

Dec 17 Sep 18 Dec 18

73 319

67 626 71 089

Dec 17 Sep 18 Dec 18

Retail deposits Mutual funds

+12.1%

+5.0%

-3.0%

+5.1%

Retail savings Corporate deposits(1)

1) Corporate and SME, excl. SBB and repo transactions

+5.4%

Appendix Outlook Business development Achievements Financial results

19

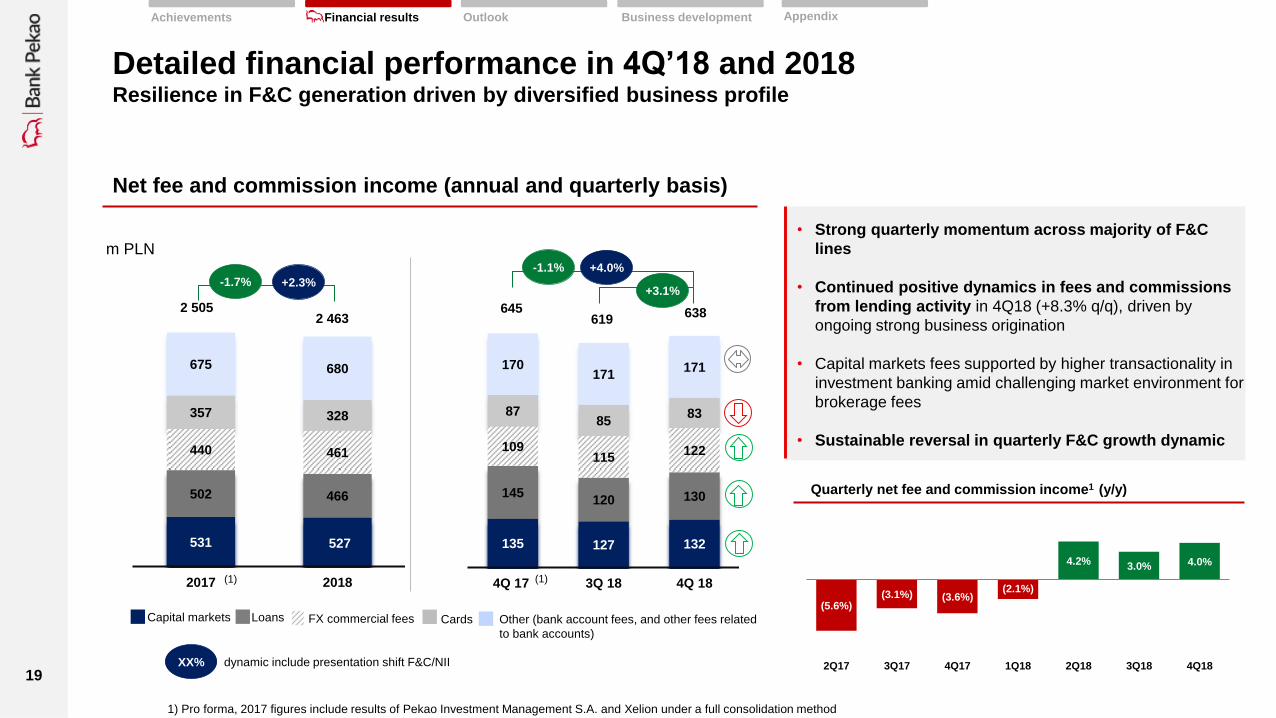

• Strong quarterly momentum across majority of F&C

lines

• Continued positive dynamics in fees and commissions

from lending activity in 4Q18 (+8.3% q/q), driven by

ongoing strong business origination

• Capital markets fees supported by higher transactionality in

investment banking amid challenging market environment for

brokerage fees

• Sustainable reversal in quarterly F&C growth dynamic

Detailed financial performance in 4Q’18 and 2018 Resilience in F&C generation driven by diversified business profile

Net fee and commission income (annual and quarterly basis)

2 505 2 463

645 619

638

Other (bank account fees, and other fees related

to bank accounts)

FX commercial fees Loans Capital markets Cards

m PLN

1) Pro forma, 2017 figures include results of Pekao Investment Management S.A. and Xelion under a full consolidation method

531 527

502 466

440 461

357 328

675 680

2017 2018(1)

-1.7%

135 127 132

145 120 130

109 115

122

87 85

83

170 171

171

4Q 17 3Q 18 4Q 18(1)

+4.0%

XX% dynamic include presentation shift F&C/NII

Quarterly net fee and commission income1 (y/y)

(5.6%) (3.1%) (3.6%)

(2.1%)

4.2% 3.0% 4.0%

2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18

+2.3%

-1.1%

+3.1%

Appendix Outlook Business development Achievements Financial results

20

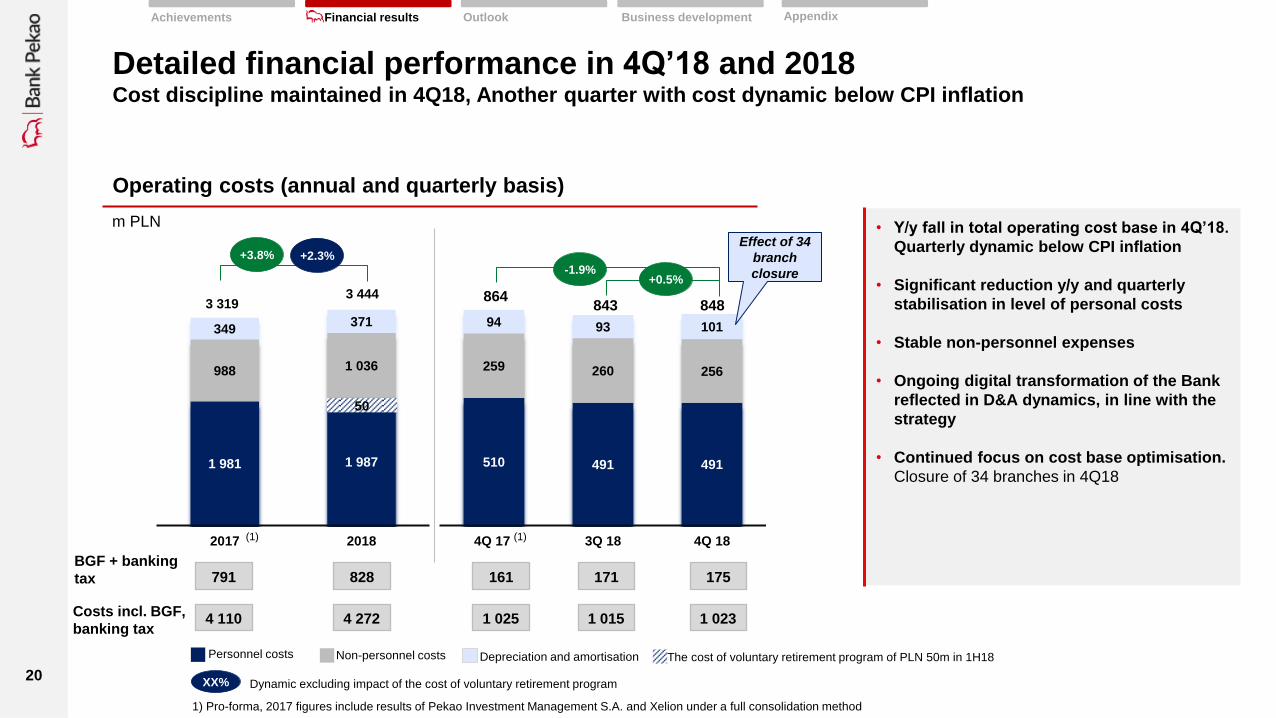

• Y/y fall in total operating cost base in 4Q’18.

Quarterly dynamic below CPI inflation

• Significant reduction y/y and quarterly

stabilisation in level of personal costs

• Stable non-personnel expenses

• Ongoing digital transformation of the Bank

reflected in D&A dynamics, in line with the

strategy

• Continued focus on cost base optimisation.

Closure of 34 branches in 4Q18

Detailed financial performance in 4Q’18 and 2018 Cost discipline maintained in 4Q18, Another quarter with cost dynamic below CPI inflation

Operating costs (annual and quarterly basis)

3 319 3 444

1 981 1 987

988 1 036

349 371

2017 2018

Non-personnel costs

Personnel costs

Depreciation and amortisation

510 491 491

259 260 256

94 93 101

4Q 17 3Q 18 4Q 18

-1.9%

(1)

864 843 848

+0.5%

BGF + banking

tax

Costs incl. BGF,

banking tax 4 110

791

4 272

828

1 025

161

1 015

171

1 023

175

+3.8%

m PLN

1) Pro-forma, 2017 figures include results of Pekao Investment Management S.A. and Xelion under a full consolidation method

+2.3%

XX% Dynamic excluding impact of the cost of voluntary retirement program

(1)

Effect of 34

branch

closure

The cost of voluntary retirement program of PLN 50m in 1H18

50

Appendix Outlook Business development Achievements Financial results

21

Detailed financial performance in 4Q’18 and 2018 Prudent risk control: Stable cost of risk and continually high asset quality

NPL ratio

Cost of risk (annual and quarterly basis)

• Annual and quarterly improvement in cost of

risk

• COR significantly below market

• Continually one of the highest NPL coverage

ratios in the Polish sector

• NPL ratio improving, helped by active risk

management (NPL sale)

NPL coverage ratio

5.5% 5.8% 5.4%

4Q 17 3Q 18 4Q 18

-2bps

Including IBNR, basket 1-2

67% 65% 66%

16% 14% 13%

4Q 17 3Q 18 4Q 18

83% 80% 79%

-40bps

Appendix Outlook Business development Achievements Financial results

1) restated, methodology unified for all periods. NPL ratio and coverage ratio included restricted interests, which was written off in June 2018

2) COR excluding sale of NPLs

(1) (1)

2017 2018

0.40% 0.38%

(2) (2)

0.46%

0.34% 0.33%

0.43% 0.35%

0.75%

0.63%

0.78% 0.73%

0.84%

4Q17 1Q18 2Q18 3Q18 4Q18

Bank Market

Source: Market – NBP; Bank – non-consolidated data consistent with NBP methodology

22

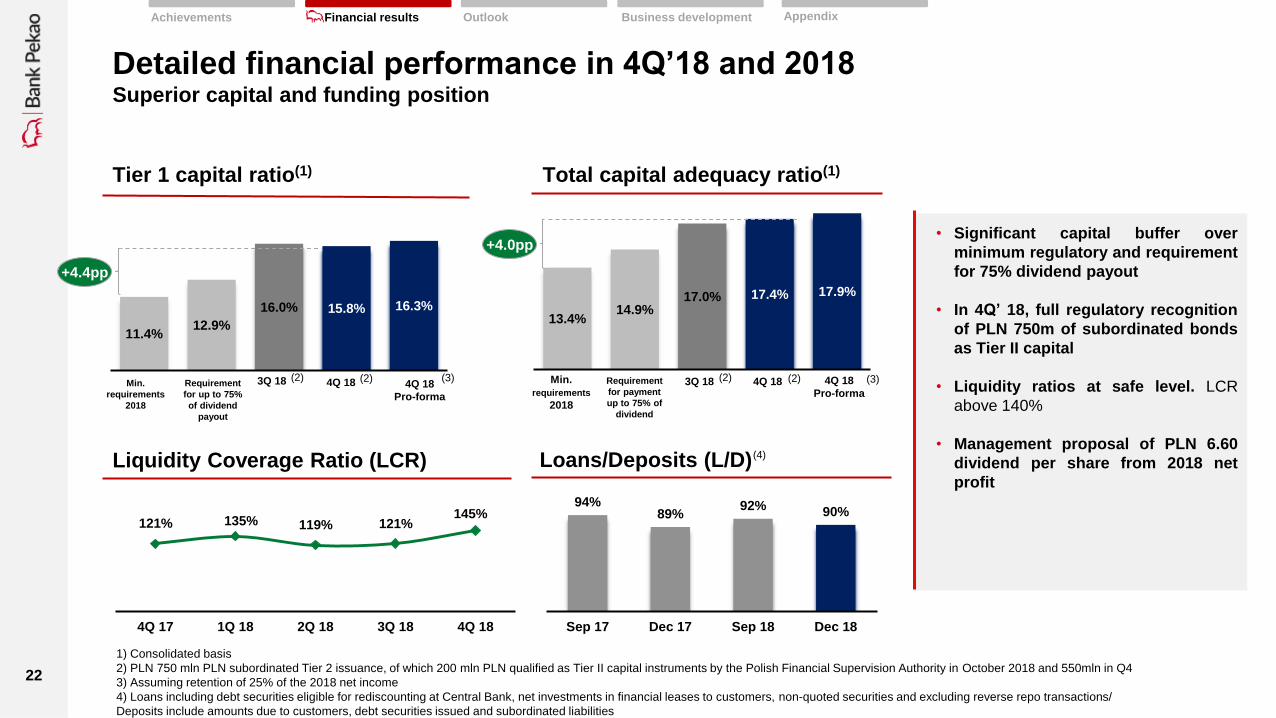

Detailed financial performance in 4Q’18 and 2018 Superior capital and funding position

Tier 1 capital ratio(1)

• Significant capital buffer over

minimum regulatory and requirement

for 75% dividend payout

• In 4Q’ 18, full regulatory recognition

of PLN 750m of subordinated bonds

as Tier II capital

• Liquidity ratios at safe level. LCR

above 140%

• Management proposal of PLN 6.60

dividend per share from 2018 net

profit

Total capital adequacy ratio(1)

Liquidity Coverage Ratio (LCR) Loans/Deposits (L/D)

94% 89%

92% 90%

Sep 17 Dec 17 Sep 18 Dec 18

121% 135% 119% 121% 145%

4Q 17 1Q 18 2Q 18 3Q 18 4Q 18

13.4% 14.9%

17.0% 17.4% 17.9%

Min.

requirements

2018

Requirement

for payment

up to 75% of

dividend

3Q 18 4Q 18

11.4% 12.9%

16.0% 15.8% 16.3%

Min.

requirements

2018

Requirement

for up to 75%

of dividend

payout

3Q 18 4Q 18

+4.4pp

+4.0pp

4Q 18

Pro-forma

4Q 18

Pro-forma

(3) (3)

1) Consolidated basis

2) PLN 750 mln PLN subordinated Tier 2 issuance, of which 200 mln PLN qualified as Tier II capital instruments by the Polish Financial Supervision Authority in October 2018 and 550mln in Q4

3) Assuming retention of 25% of the 2018 net income

4) Loans including debt securities eligible for rediscounting at Central Bank, net investments in financial leases to customers, non-quoted securities and excluding reverse repo transactions/

Deposits include amounts due to customers, debt securities issued and subordinated liabilities

(2) (2) (2) (2)

(4)

Appendix Outlook Business development Achievements Financial results

23

Key achievements in 2018

Detailed financial performance in 4Q’18 and 2018

2019 business and financial outlook

Business growth and development

Appendix

1

2

3

4

5

24

2019 Business and financial outlook Key strategic initiatives underway in 2019 driving commercial effectiveness

Appendix Business development Financial results Outlook Achievements

Credit process 2.0

Client Value Management Sales Force Effectiveness

What are we going to do?

Identification of key Clients and prospects

Sales network operating model optimization

Streamlining key processes (Client planning, pricing,

Cooperation with Bank’s subsidiaries)

Providing modern and intelligent IT tools (sales support)

Intelligent growth supported by excellent understanding

of Client potential and needs

Unleashing sales potential of the network thanks to

digitization, automation and streamlining of processes

Effective pricing & optimal capital allocation

What are we going to do?

Optimization of retail branch network activities with

special focus on:

reorganizing operating model

equipping RM’s with necessary digital support tools

calibration of the incentives system

What do we want to achieve?

Building sustainable competitive advantage in terms of

retail branch network effectiveness and service quality

Ensuring consistency with market trends and evolving

Customer needs

CIB Retail

All

segments

What are we going to do?

Comprehensive review & optimization

Implementing cutting-edge IT tools

to achieve best-in-class Customer

experience

e2e process acceleration

Smart credit processes based on a

common system architecture

What do we want to achieve?

What do we want to achieve?

25

Omnichannel Platform – futher

development

C/A opening via „selfie” in PeoPay

New internet banking platforms

Pekao24 for individuals and micro

New functions in PeoPay (Mobile

authorization, GarminPay, P2P BLIK,

contacless cash withdrawals)

New simplified credit card offer with

additional benefits

New offer dedicated to private

banking clients

New services in the area of

knowledge and trainings for

microfirms

New internet banking platforms

PekaoBiznes24 for SME and

Corpo

Value added services for

Customers through

partnerships

Pekao Connect System -

Integrating Pekao and clients

accounting systems

Acquiring transformation

(process and product innovation)

Dedicated team of specialists

responsible for driving

innovations

Cooperation with partners on

banking unique value

proposition

Operational

Effectivness

Robotic process and

servicess automatisation

IT transformation

Franchise smart

optimiztion

Fit organisation

Pekao Innovation Lab

Transforming Bank Pekao to become leader in effectiveness

and digital champion delivering client value

Innovative

Environment

Corporate & SME Retail & Private

Relationship building & cross-sell

Value Added Services

Robotic Process Automation & Streamlining

Retail

CIB

SME

Back Office

Inn

ova

tio

n fo

cus

Customer experience & channel integration

2019 Business and financial outlook Key strategic initiatives underway in 2019 driving digital and operational transformation

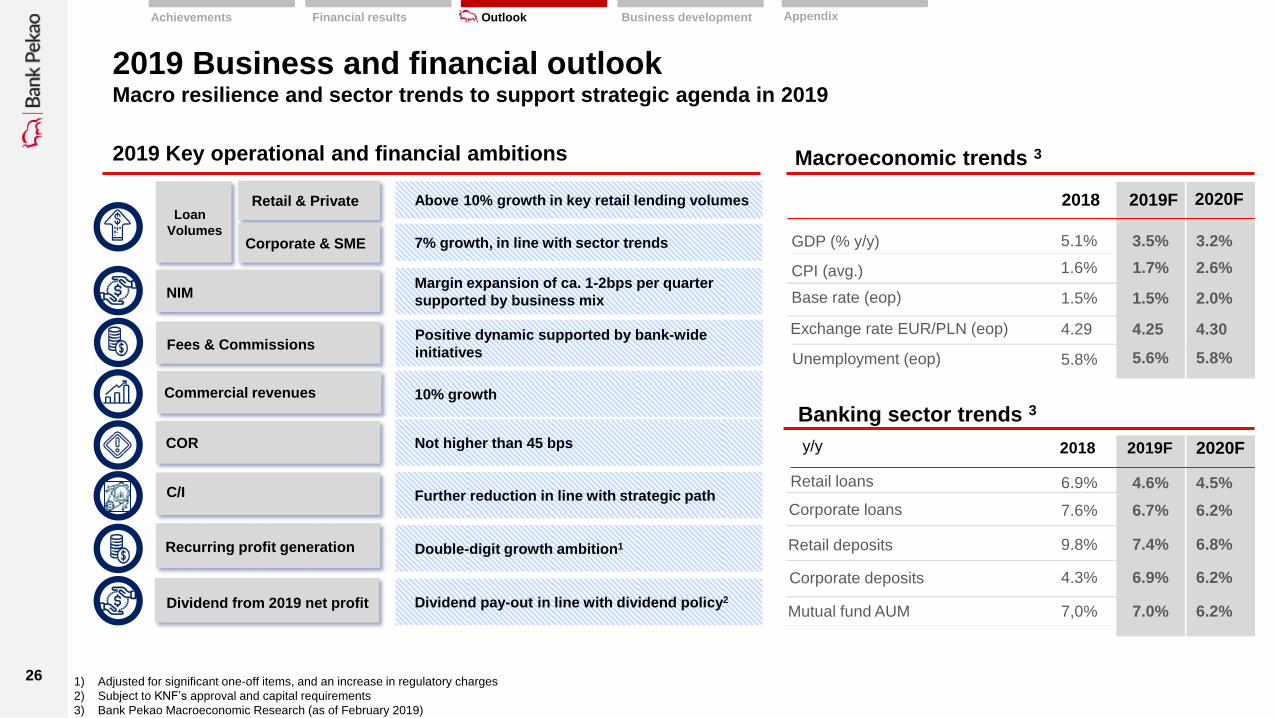

Appendix Business development Financial results Outlook Achievements

26

y/y

Banking sector trends 3

Macroeconomic trends 3 Net profit Net profit 2019 Key operational and financial ambitions

2018 2019F

GDP (% y/y) 5.1% 3.5%

CPI (avg.) 1.6% 1.7%

Base rate (eop) 1.5% 1.5%

2018 2019F

Retail loans 6.9% 4.6%

Retail deposits 9.8% 7.4%

Corporate deposits 4.3% 6.9%

Mutual fund AUM 7,0% 7.0%

Corporate loans 7.6% 6.7%

1) Adjusted for significant one-off items, and an increase in regulatory charges

2) Subject to KNF’s approval and capital requirements

3) Bank Pekao Macroeconomic Research (as of February 2019)

Exchange rate EUR/PLN (eop) 4.29 4.25

2020F

2020F

3.2%

2.6%

2.0%

4.30

4.5%

6.2%

6.8%

6.2%

6.2%

Retail & Private Above 10% growth in key retail lending volumes Loan

Volumes Corporate & SME

NIM

Commercial revenues

COR

C/I

Recurring profit generation

Dividend from 2019 net profit

7% growth, in line with sector trends

Margin expansion of ca. 1-2bps per quarter

supported by business mix

10% growth

Not higher than 45 bps

Further reduction in line with strategic path

Double-digit growth ambition1

Dividend pay-out in line with dividend policy2

Fees & Commissions Positive dynamic supported by bank-wide

initiatives Unemployment (eop) 5.8% 5.6% 5.8%

2019 Business and financial outlook Macro resilience and sector trends to support strategic agenda in 2019

Appendix Financial results Outlook Business development Achievements

27

Successful execution of our strategic ambitions in 2018

Double-digit RoE in 2018 (10.2%) achieved for a first time since 2014

+10% commercial revenue growth outpacing ca. 2x growth in deployed balance sheet in 2018

Exceeded milestone of +400K new current accounts, powered by a world-class digital platform: PeoPay

150bps improvement in Cost/Income ratio supported by ongoing digital transformation

Strong commercial and operational momentum into 2019 to deliver on our 2020 strategic goals

+11% net profit growth delivering on our ambition and promise, to reach ca. PLN 2.3bn net profit

Achievements Appendix Financial results Outlook Business development

28

Key achievements in 2018

Detailed financial performance in 4Q’18 and 2018

2019 business and financial outlook

Business growth and development

Appendix

1

2

3

4

5

29

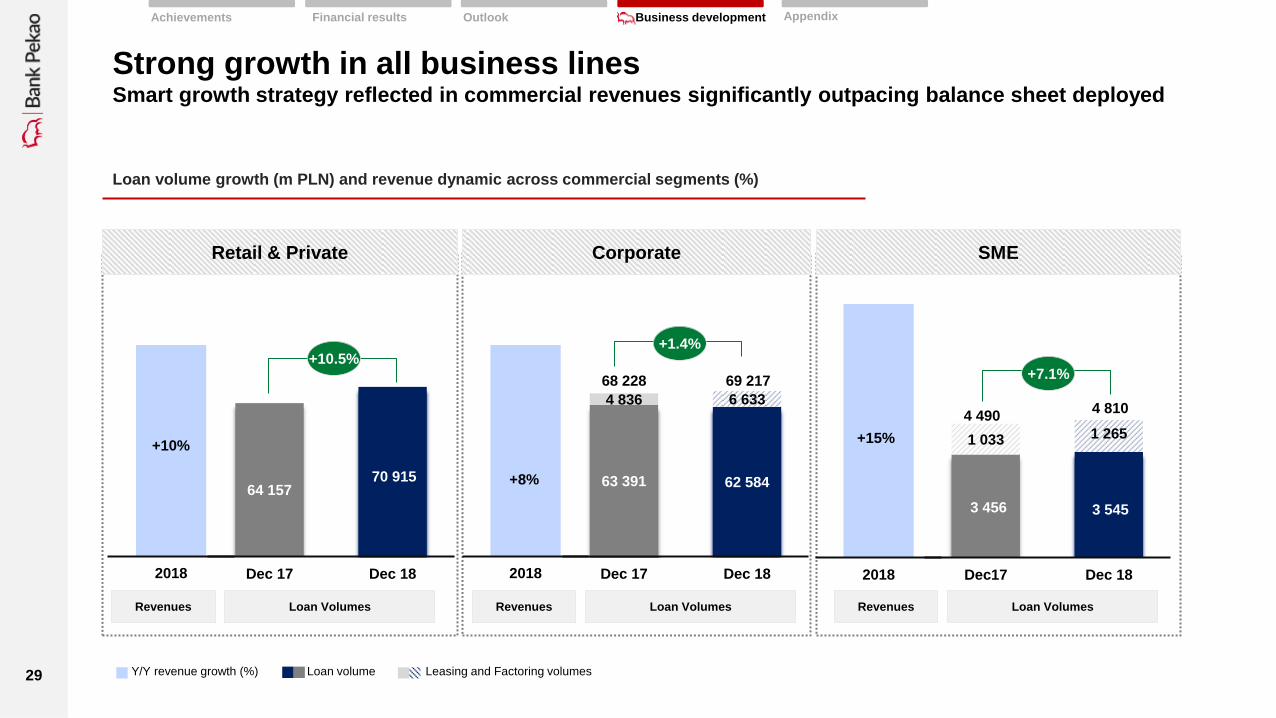

Strong growth in all business lines Smart growth strategy reflected in commercial revenues significantly outpacing balance sheet deployed

Loan volume growth (m PLN) and revenue dynamic across commercial segments (%)

64 157 70 915

Dec 17 Dec 182018

+10%

63 391 62 584

4 836 6 633

Dec 17 Dec 182018

+8%

3 456 3 545

1 033 1 265

Dec17 Dec 182018

+15%

4 490 4 810

Loan volume Leasing and Factoring volumes

+7.1%

+1.4% +10.5%

Corporate SME

Y/Y revenue growth (%)

68 228

Revenues Loan Volumes Revenues Loan Volumes Revenues Loan Volumes

69 217

Retail & Private

Appendix Financial results Outlook Business development Achievements

30

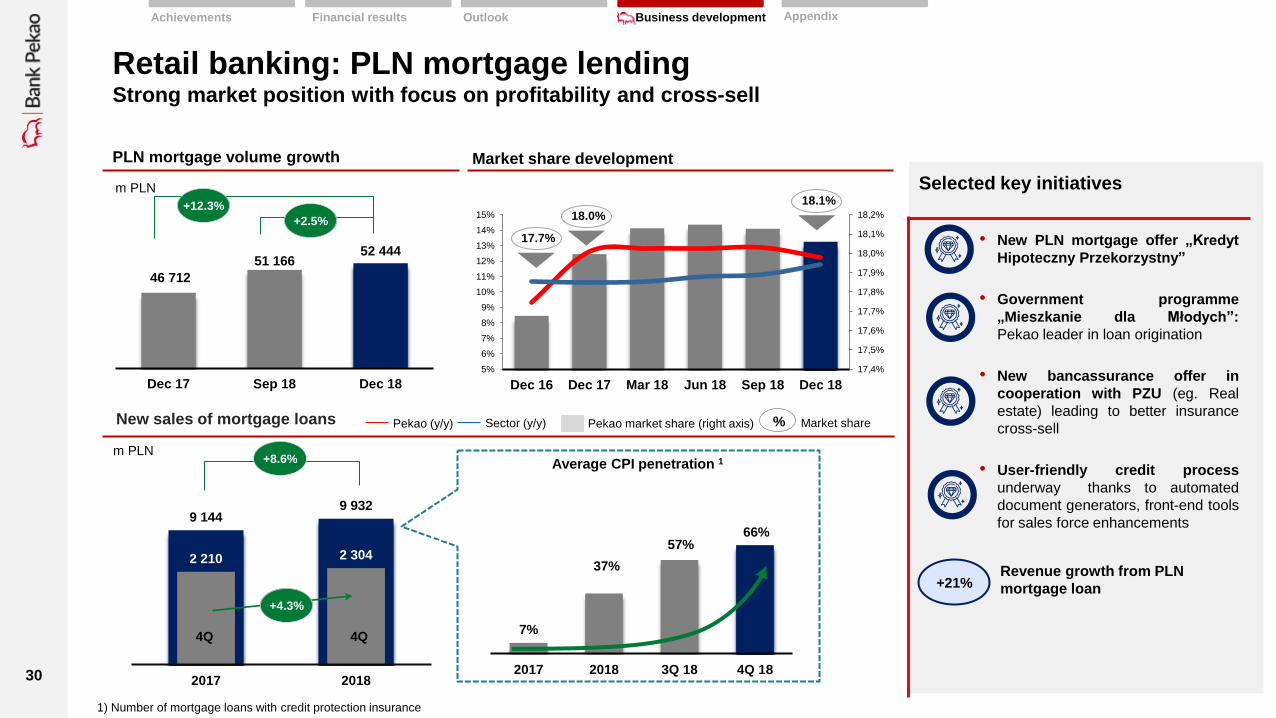

Retail banking: PLN mortgage lending Strong market position with focus on profitability and cross-sell

• New PLN mortgage offer „Kredyt

Hipoteczny Przekorzystny”

• Government programme

„Mieszkanie dla Młodych”:

Pekao leader in loan origination

• New bancassurance offer in

cooperation with PZU (eg. Real

estate) leading to better insurance

cross-sell

• User-friendly credit process

underway thanks to automated

document generators, front-end tools

for sales force enhancements

1) Number of mortgage loans with credit protection insurance

Selected key initiatives

+21% Revenue growth from PLN

mortgage loan

Appendix Financial results Outlook Business development Achievements

46 712

51 166 52 444

Dec 17 Sep 18 Dec 18

+2.5%

+12.3%

PLN mortgage volume growth

m PLN

Market share development

17,4%

17,5%

17,6%

17,7%

17,8%

17,9%

18,0%

18,1%

18,2%

5%

6%

7%

8%

9%

10%

11%

12%

13%

14%

15%

Dec 16 Dec 17 Mar 18 Jun 18 Sep 18 Dec 18

17.7%

18.1%

Pekao (y/y) Sector (y/y) Pekao market share (right axis) % Market share

18.0%

New sales of mortgage loans

m PLN +8.6%

7%

37%

57% 66%

2017 2018 3Q 18 4Q 18

Average CPI penetration 1

9 144 9 932

2 210 2 304

0

500

1 000

1 500

2 000

2 500

3 000

3 500

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

10 000

2017 2018

4Q 4Q

+4.3%

31

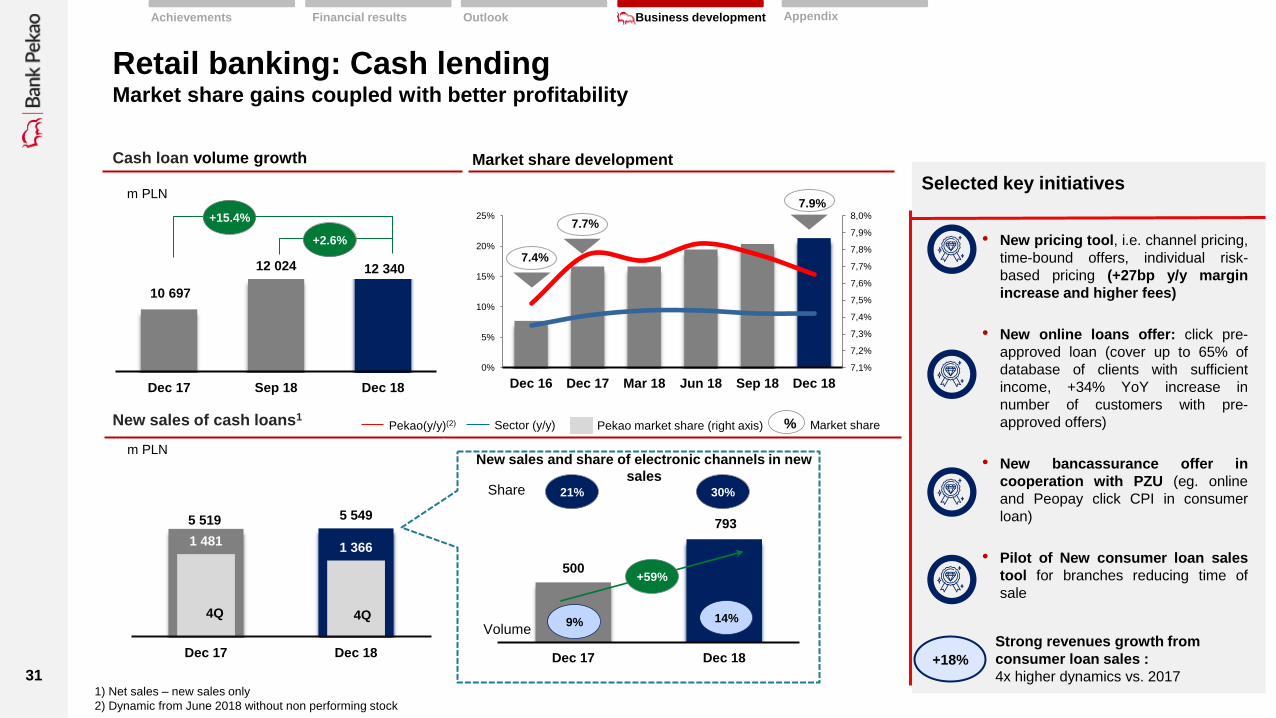

Retail banking: Cash lending Market share gains coupled with better profitability

1) Net sales – new sales only

2) Dynamic from June 2018 without non performing stock

• New pricing tool, i.e. channel pricing,

time-bound offers, individual risk-

based pricing (+27bp y/y margin

increase and higher fees)

• New online loans offer: click pre-

approved loan (cover up to 65% of

database of clients with sufficient

income, +34% YoY increase in

number of customers with pre-

approved offers)

• New bancassurance offer in

cooperation with PZU (eg. online

and Peopay click CPI in consumer

loan)

• Pilot of New consumer loan sales

tool for branches reducing time of

sale

+18%

Strong revenues growth from

consumer loan sales :

4x higher dynamics vs. 2017

Selected key initiatives

Appendix Financial results Outlook Business development Achievements

7,1%

7,2%

7,3%

7,4%

7,5%

7,6%

7,7%

7,8%

7,9%

8,0%

0%

5%

10%

15%

20%

25%

Dec 16 Dec 17 Mar 18 Jun 18 Sep 18 Dec 18

10 697

12 024 12 340

Dec 17 Sep 18 Dec 18

7.9%

7.4%

+15.4%

+2.6%

m PLN

Cash loan volume growth

7.7%

Market share development

4Q 4Q

500

793

Dec 17 Dec 18

21% 30% Share

New sales and share of electronic channels in new

sales

+59%

9% 14% Volume

5 519 5 549

1 481 1 366

0

500

1 000

1 500

2 000

2 500

3 000

3 500

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

10 000

Dec 17 Dec 18

m PLN

4Q 4Q

New sales of cash loans1 Pekao(y/y)(2) Sector (y/y) Pekao market share (right axis) % Market share

32

234 274

406

68 115

0

50

100

150

200

250

300

350

400

450

2015-2016 avg

2017 2018

10.4%

11.4%

Dec 17 Dec 18

Retail banking: Customer acquisition and investment management 400k acquisition target achieved; Resilience of asset management franchise in challenging market

Current Accounts: gross sale

ths

Mutual funds AUM1

+5.4%

Dec 17 Sep 18 Dec 18

18 410

19 403

+4.3%

2017 2018

1 523

1 590 • New Accounts Konto

Przekorzystne and Konto Świat

Premium with unique,

comprehensive offer

• Omnichannel C/A: Current account

in 10 minutes

• My First Fund: New attractive offer

for customers opening first mutual

fund (0 PLN upfront fee up to PLN

100k AUM)

• 4 new subscriptions of structured

products with full capital

protection

m PLN

m PLN

19 534

4Q 4Q

Investment products: net sale

Retail mutual funds market share (AUM)

+100bps

+74.0%

+12%

Good revenues growth

momentum from investment

products

+48.2%

1) Mutual funds managed by PPIM

Selected key initiatives

Appendix Financial results Outlook Business development Achievements

33

Selected key initiatives

119 135

2017 2018

2.9% 3.2%

2017 2018

Corporate banking: Consistent execution of strategy Strong focus on profitability and cross-selling potential

50.0% 50.6%

2017 2018

+30bps

Cross-sell(1)

1) Non-interest income / total income. income from non-banking activities (Pekao Leasing and Factoring) treated as non-loan income

2) In comparable terms (the same methodology of RWA calculation for both years)

3) Mid&Large

MID banking: Total assets

13 554 14 881 15 265

Dec 17 Sep 18 Dec 18

m PLN

Total revenue/RWA(2)

m PLN +60bps

Revenues per client (MID&large)

+13.8%

• 1st Innovative Open Finance

Platform in Poland: Managing SCF,

eFinancing, factoring invoices

• Kuke and Pekao cooperation: KUKE

guarantees support foreign expansion

of Polish companies thanks to access

financial instruments

• Split Payment: Nr 1 in the market (incl.

over 1,500 trainings and information

campaign)

• E-guarantee: Bank guarantees online

issued as an electronic document with

qualified electronic signature via

PekaoBiznes24 system

• 1st Municipal Investment Fund in

Poland: Pekao Samorząd Plus FIZ

+12.6%

+2.6%

ths PLN

Appendix Financial results Outlook Business development Achievements

34

SME banking: Growth momentum intact Strong client acquisition; sustainable asset growth

Loan sales

3 456 3 545

1 033 1 265

Dec 17 Dec 18

Loan volumes

Loans Leasing and Factoring

m PLN

+7%

m PLN

4 490 4 810

1 725 1 615

584 1 022

2017 2018

2 309 2 637

Loans Leasing and Factoring

+14%

x2

2017 2018

pcs

Clients acquisition1 Revenues per client

• 60 SME centres established ensuring client

proximity, servicing >50k SMEs

• Universal agreement for comprehensive offer in

transactional banking

• Hire of SME product specialists to support

cross-sell (treasury, leasing, factoring, EU

Funds)

• Unique solution for SME Companies: Loans

with the COSME guarantee. The guarantee line

signed directly with EFI for a record PLN 1.2bn

• ESIF Silesia Program: Preferential loans for

SME companies located in the Silesian Region

2017 2018

+19%

1) Clients with annual turnover above PLN 5m

PLN

Selected key initiatives

Appendix Financial results Outlook Business development Achievements

35

Digital Innovation Industry-leading initiatives supporting growth

Active clients of electronic banking1

ths PLN ths PLN

Payments in mobile banking PeoPay 2

Active clients of mobile banking1

2013 2014 2015 2016 2017 2018

2.6x

pcs.

1) Unique clients with min. 1 log-in within last 3 months

2) Transactions including HCE, Apple Pay, BLIK, QR

1 157

• Maximizing user experience thanks

to remote identity verification based

on face biometrics and ID photo

• Biometric authorization

• Finance management

• Currency Exchange 24h

• Online card managment

• Apple Pay, BLIK

• ATM cash deposit with BLIK code

1 981 1 998

2 185

Dec 17 Sep 18 Dec 18

+ 10%

938 1 179 1 263

Dec 17 Sep 18 Dec 18

+ 35%

• Testing new technologies

(biometrics, AI, machine learning)

• Hackathons, Service jams (i.e. new

branch format)

• Creating new services and products

concepts

Innovation Lab

World’s

most innovative product

Key achievements

Selected key initiatives

C/A opening by selfie

+99%

+94%

+88%

+30%

• growth in the number of daily

activations of PeoPay

• transfers realized via electronic

channels

• term deposits opened via electronic

channels

• Share of sales of consumer loan

PEX in electronic channels

Appendix Financial results Outlook Business development Achievements

36

Employer of the Best Talent Numerous initiatives supporting growth and development of our workforce

Streamlining recruitment processes

Nearly 4x YoY growth in # new hirings

Improving employees onboarding

Investing in managerial competences: Attracted

>80 new top professionals from PL and international

Establishing dedicated unit responsible for

innovations and cooperation with start-ups &

fintechs

Stimulating generational change

Roll-out of Voluntary retirement program

Improving competences

Increased engagement in professional

trainings (# trainees +162% YoY)

Boosting employer branding outlays to attract

professionals with strategic competences (Big Data,

Innovations, IT Developers, Sales)

Establishing strategic cooperation with Poland’s best

economics universities (SGH, WSE, Kozminski

University)

New summer internship program for talented

students of best PL and European universities

Effective employer branding

Simplifying management structure

Reducing number of director positions by 12%

YoY with total cost reduction by 10% YoY

2020 Strategy levers Strategic initiatives

"Top of mind"

banking

employer

Unique

development

opportunities

Attractive

remuneration

Organizational

culture

Market recognition: 8th time in a row

Appendix Financial results Outlook Business development Achievements

37

Key achievements in 2018

Detailed financial performance in 4Q’18 and 2018

2019 business and financial outlook

Business growth and development

Appendix

1

2

3

4

5

38

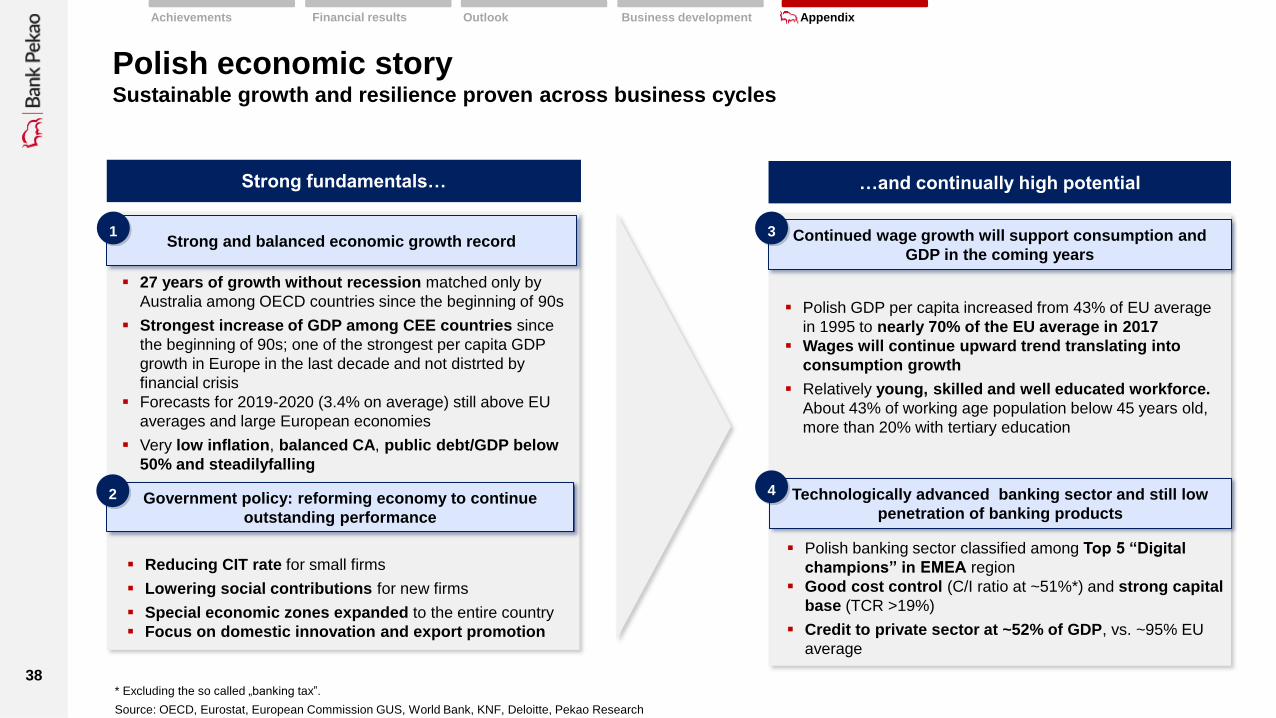

Polish economic story Sustainable growth and resilience proven across business cycles

* Excluding the so called „banking tax”.

Source: OECD, Eurostat, European Commission GUS, World Bank, KNF, Deloitte, Pekao Research

Strong fundamentals… …and continually high potential

Strong and balanced economic growth record

Government policy: reforming economy to continue

outstanding performance

Continued wage growth will support consumption and

GDP in the coming years

Technologically advanced banking sector and still low

penetration of banking products

27 years of growth without recession matched only by

Australia among OECD countries since the beginning of 90s

Strongest increase of GDP among CEE countries since

the beginning of 90s; one of the strongest per capita GDP

growth in Europe in the last decade and not distrted by

financial crisis

Forecasts for 2019-2020 (3.4% on average) still above EU

averages and large European economies

Very low inflation, balanced CA, public debt/GDP below

50% and steadilyfalling

Reducing CIT rate for small firms

Lowering social contributions for new firms

Special economic zones expanded to the entire country

Focus on domestic innovation and export promotion

Polish GDP per capita increased from 43% of EU average

in 1995 to nearly 70% of the EU average in 2017

Wages will continue upward trend translating into

consumption growth

Relatively young, skilled and well educated workforce.

About 43% of working age population below 45 years old,

more than 20% with tertiary education

Polish banking sector classified among Top 5 “Digital

champions” in EMEA region

Good cost control (C/I ratio at ~51%*) and strong capital

base (TCR >19%)

Credit to private sector at ~52% of GDP, vs. ~95% EU

average

1

2

3

4

Appendix Financial results Outlook Achievements Business development

39

2019 Outlook Solid growth of bank sector volumes despite less robust economic environment

Economic outlook Bank sector outlook

Pekao Research forecasts as of January 2019

(1) all non-housing loans (2) internal macroeconomic scenario, fixed exchange rates (3) deposits + retail customers assets in investment funds units (4) retail customers assets in investment funds units

2018 2019F 2020F

GDP, % 5.1 (F) 3.5 3.2

Private consumption, % y/y 4.5 (F) 3.8 3.5

Investments, % y/y 7.3 (F) 6.0 5.0

Unemployment, % eop 5.8 5.6 5.8

CPI, % avg 1,6 1.7 2.6

3M WIBOR, % eop 1.72 1.75 2.35

Reference rate, % eop 1,50 1.5 2.0

Exchange rate EUR, eop 4.29 4.25 4.30

Exchange rate USD, eop 3.74 3.79 3.74

Public sector balance, % GDP (0.6)(F) (0.9) (1.5)

2018 2019F 2020F (2)

Loans, % y/y 7.1 5.4 5.2

Retail, % y/y 6.9 4.6 4.5

Mortgage loans PLN 11.8 9.1 8.0

Consumer loans (1) 6.9 5.4 5.3

Corporate, % y/y 7.6 6.7 6.2

Savings (3) , % y/y 7.5 (F) 7.2 6.7

Deposits, % y/y 9.0 7.2 6.6

Retail, % y/y 9.8 7.4 6.8

Corporate, % y/y 4.3 6.9 6.2

Mutual Funds (4) , % y/y 7.0 7.0 n.a.

• Moderate slowdown expected in 2019

after highest GDP growth rate in

decade, achieved in 2018

• Household consumption remains

buoyant, while fixed investment

performance continues to be mixed

(strong public investment offset by soft

private investment activity)

• Slowing external demand is perceived

as the main risk to economic prospects

in Poland and may put pressure on

export. Import activity is still supported

by strong internal demand

• Bank volume growth in 2019 to

moderate in retail products whilst

corporate activity expected at broadly

similar growth dynamic

Financial results Outlook Business development Appendix Achievements

40

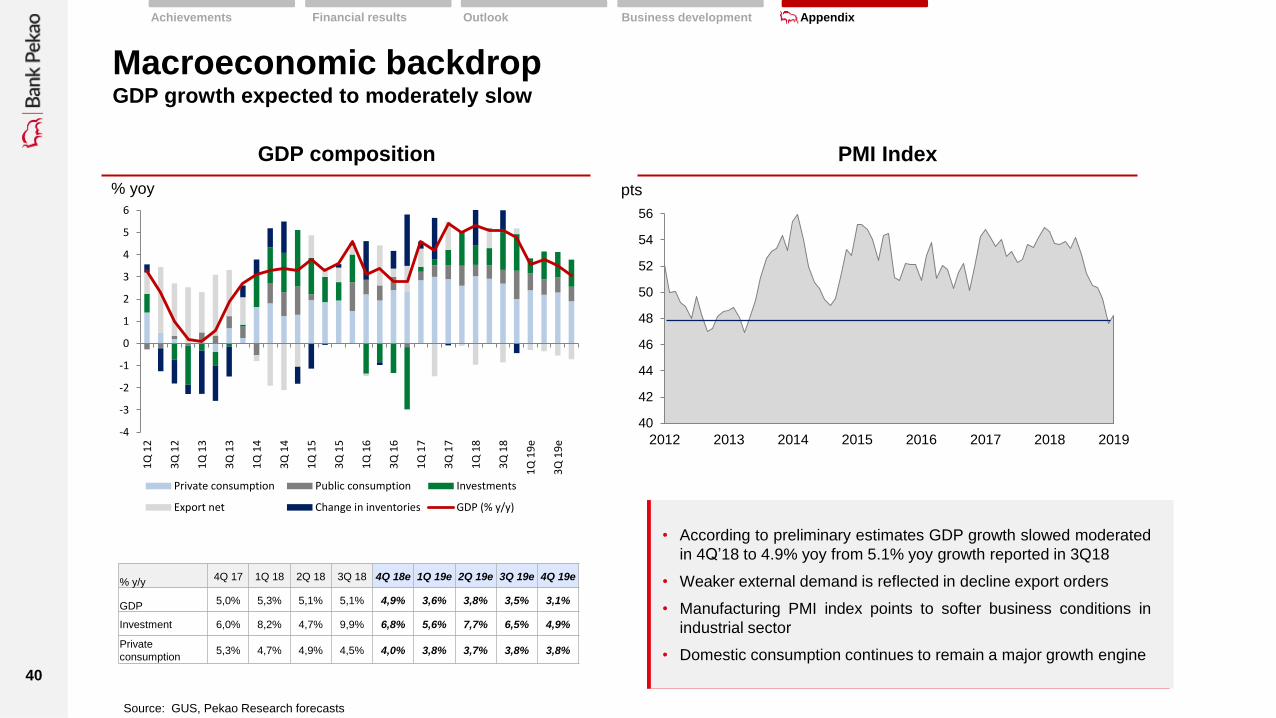

Macroeconomic backdrop GDP growth expected to moderately slow

GDP composition PMI Index

Source: GUS, Pekao Research forecasts

% yoy pts

• According to preliminary estimates GDP growth slowed moderated

in 4Q’18 to 4.9% yoy from 5.1% yoy growth reported in 3Q18

• Weaker external demand is reflected in decline export orders

• Manufacturing PMI index points to softer business conditions in

industrial sector

• Domestic consumption continues to remain a major growth engine

-4

-3

-2

-1

0

1

2

3

4

5

6

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

3Q

15

1Q

16

3Q

16

1Q

17

3Q

17

1Q

18

3Q

18

1Q

19

e

3Q

19

e

Private consumption Public consumption Investments

Export net Change in inventories GDP (% y/y)

% y/y 4Q 17 1Q 18 2Q 18 3Q 18 4Q 18e 1Q 19e 2Q 19e 3Q 19e 4Q 19e

GDP 5,0% 5,3% 5,1% 5,1% 4,9% 3,6% 3,8% 3,5% 3,1%

Investment 6,0% 8,2% 4,7% 9,9% 6,8% 5,6% 7,7% 6,5% 4,9%

Private

consumption 5,3% 4,7% 4,9% 4,5% 4,0% 3,8% 3,7% 3,8% 3,8%

40

42

44

46

48

50

52

54

56

2012 2013 2014 2015 2016 2017 2018 2019

Financial results Outlook Business development Appendix Achievements

41

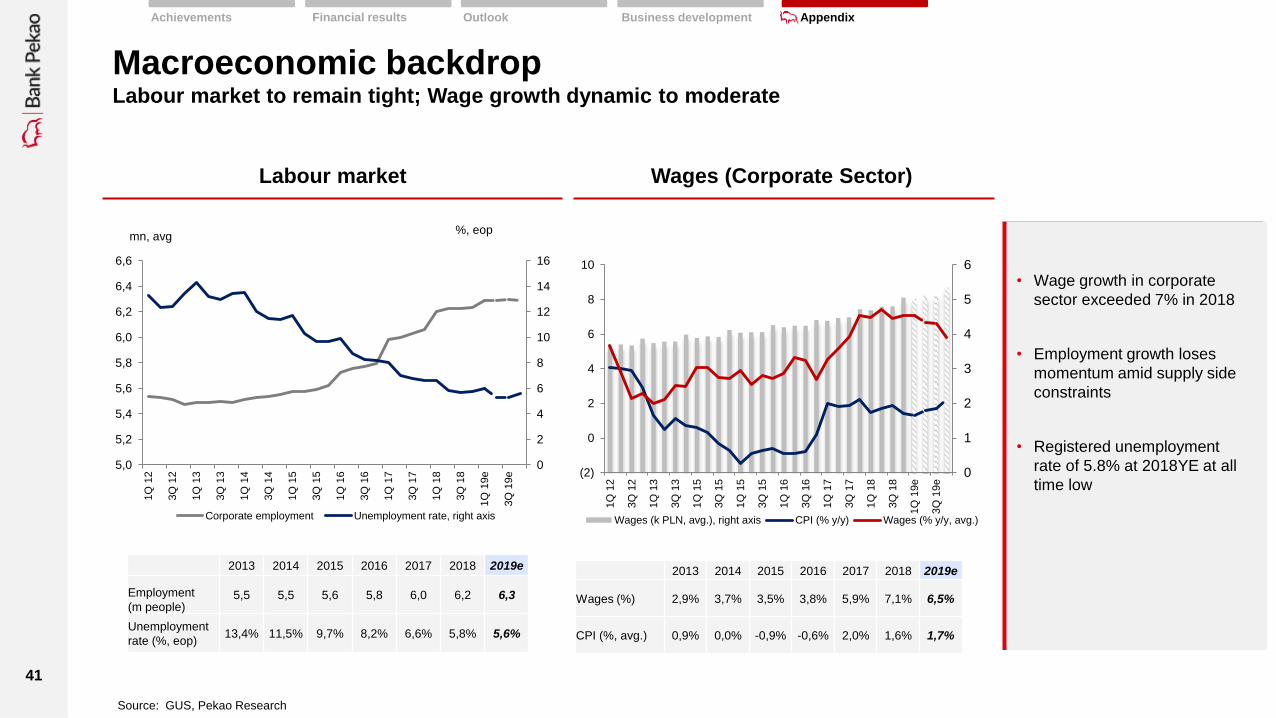

Macroeconomic backdrop Labour market to remain tight; Wage growth dynamic to moderate

Labour market Wages (Corporate Sector)

Source: GUS, Pekao Research

mn, avg %, eop

• Wage growth in corporate

sector exceeded 7% in 2018

• Employment growth loses

momentum amid supply side

constraints

• Registered unemployment

rate of 5.8% at 2018YE at all

time low

0

2

4

6

8

10

12

14

16

5,0

5,2

5,4

5,6

5,8

6,0

6,2

6,4

6,6

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

3Q

15

1Q

16

3Q

16

1Q

17

3Q

17

1Q

18

3Q

18

1Q

19e

3Q

19e

Corporate employment Unemployment rate, right axis

0

1

2

3

4

5

6

(2)

0

2

4

6

8

10

1Q

12

3Q

12

1Q

13

3Q

13

1Q

15

3Q

15

1Q

15

3Q

15

1Q

16

3Q

16

1Q

17

3Q

17

1Q

18

3Q

18

1Q

19e

3Q

19e

Wages (k PLN, avg.), right axis CPI (% y/y) Wages (% y/y, avg.)

2013 2014 2015 2016 2017 2018 2019e

Employment

(m people) 5,5 5,5 5,6 5,8 6,0 6,2 6,3

Unemployment

rate (%, eop) 13,4% 11,5% 9,7% 8,2% 6,6% 5,8% 5,6%

2013 2014 2015 2016 2017 2018 2019e

Wages (%) 2,9% 3,7% 3,5% 3,8% 5,9% 7,1% 6,5%

CPI (%, avg.) 0,9% 0,0% -0,9% -0,6% 2,0% 1,6% 1,7%

Financial results Outlook Business development Appendix Achievements

42

Macroeconomic backdrop CPI inflation running below NBP target; First rate hikes expected in 2020

Inflation, interest rates Government bond yields

Source: NBP, GUS, Pekao Research

Exchange rates

%

%

eop

Base rate

Feb 2019 -

1,50%

• NBP reference interest rate at 1.5%, lombard rate at 2.5% and

deposit rate at 0.5% in 4Q 2018

• CPI declined to 1.1% yoy at the end of 4Q 2018, still below

the NBP target of 2.5% after touching 2% level in 2018

• CPI is expected to run below the NBP target (2.5%) until 2020

and interest rate hikes by the Monetary Policy Council are not

expected in 2019. We factor 2 rates hikes of 25bps each in

2020

-2

-1

0

1

2

3

4

5

6

1Q

12

3Q

12

1Q

13

3Q

13

1Q

15

3Q

15

1Q

15

3Q

15

1Q

16

3Q

16

1Q

17

3Q

17

1Q

18

3Q

18

1Q

19e

3Q

19e

3M WIBOR (% eop) CPI (% y/y) Base rate NBP (%)

0

1

2

3

4

5

6

1Q

12

3Q

12

1Q

13

3Q

13

1Q

15

3Q

15

1Q

15

3Q

15

1Q

16

3Q

16

1Q

17

3Q

17

1Q

18

3Q

18

1Q

19e

3Q

19e

2Y 5Y 10Y

2,0

2,5

3,0

3,5

4,0

4,5

5,0

1Q

12

3Q

12

1Q

13

3Q

13

1Q

15

3Q

15

1Q

15

3Q

15

1Q

16

3Q

16

1Q

17

3Q

17

1Q

18

3Q

18

1Q

19e

3Q

19e

EUR/PLN USD/PLN CHF/PLN

Financial results Outlook Business development Appendix Achievements

43

Loans and advances to households and

institutional clients Deposits of households and institutional

clients

Macroeconomic backdrop Steady accelaration in household loans, strong inflow of deposits towards end of year

bl PLN bl PLN

* Households and non-profit institutions serving households

** Enterprises, non-bank financial institutions & public sector

Source: NBP

• Retail loans: strong growth

in core products throughout

the year (PLN mortgages

+11,8% y/y, consumer loans

+8,9% y/y at the end of

year)

• Corporate loans:

disappointing result in terms

of investment loans (-2,1%

y/y eop), but double-digit

growth achieved for

revolving credit

• Deposits: strong inflow in

households and enterprises

sectors towards end of the

year; high pace in general in

2018 shifted toward current

deposit

% y /y 2013 2014 2015 2016 2017 1Q 18 2Q 18 3Q 18 4Q 18

Households 4,5 5,5 6,6 5,2 1,8 3,3 4,8 5,3 6,9

Corporate 2,5 7,3 7,0 4,5 6,2 5,8 6,7 7,9 7,3

% y /y 2013 2014 2015 2016 2017 1Q 18 2Q 18 3Q 18 4Q 18

Households 6,5 9,2 9,4 9,5 4,1 4,7 6,4 7,8 9,8

Corporate 4,5 7,7 3,7 8,5 4,9 7,7 6,4 4,6 7,4

568 599 639 672 683 693 712 721 731

381 408

437 457 485 493 506 520 520

100

300

500

700

900

1100

1300

2013 2014 2015 2016 2017 1Q18 2Q18 3Q18 4Q18

Households* Corporate**

571 624 682 747 778 792 805 819 854

323 348

361 392 411 434 443 438 441

100

300

500

700

900

1100

1300

2013 2014 2015 2016 2017 1Q18 2Q18 3Q18 4Q18

Households* Corporate**

Financial results Outlook Business development Achievements Appendix

44

Bank loans and receivables to households*

Macroeconomic backdrop Further accelaration in household volumes in Q4’18, mixed for corporates

* Households and non-profit institutions serving households ** Enterprises, non-bank financial institutions & public sector; Source: NBP

2018 2013 2014 2015 2016 2017

% Ytd

Household deposits*

% Ytd

Bank loans and receivables to institutional clients**

% Ytd

Institutional client deposits**

% Ytd

-1%

0%

1%

2%

3%

4%

5%

6%

7%

XII' I II III IV V VI VII VIII IX X XI XII

-1%

1%

3%

5%

7%

9%

11%

XII' I II III IV V VI VII VIII IX X XI XII

-1%

1%

3%

5%

7%

9%

11%

XII' I II III IV V VI VII VIII IX X XI XII

-5%

0%

5%

10%

15%

XII' I II III IV V VI VII VIII IX X XI XII

Financial results Outlook Business development Appendix Achievements

45

Household non-performing loans* Corporate non-performing loans*

Main trends NPL statistics distorted by changes in methodology, but generally positive picture

Fom the beginning of 2018 data according to the changed methodology (impact of IFRS9 implementation).

* Share of non-performing loans in portfolio.

Source: NBP, KNF

2013 2014 2015 2016 2017 1Q 18 2Q 18 3Q 18 XI'18

Total 7,0% 6,5% 6,2% 6,0% 6,0% 6,5% 6,0% 5,9% 5,9%

Mortgage 3,1% 3,1% 2,8% 2,9% 2,8% 2,9% 2,6% 2,5% 2,5%

Consumer and other 12,8% 11,5% 11,2% 10,6% 10,6% 11,7% 10,9% 10,8% 10,7%

2013 2014 2015 2016 2017 1Q 18 2Q 18 3Q 18 XI'18

Total 11,9% 11,4% 10,4% 9,1% 8,3% 9,8% 9,0% 9,0% 8,9%

SME 13,0% 12,7% 12,2% 11,0% 10,0% 11,8% 11,3% 11,3% 11,4%

Large f irms 10,2% 9,5% 7,6% 6,4% 5,9% 7,1% 6,0% 6,1% 5,7%

0%

2%

4%

6%

8%

10%

12%

14%

16%

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

XI'18

Retail total Mortgage Consumer and other

4%

6%

8%

10%

12%

14%

16%

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

XI'1

8

Corporate total SME Large firms

• Households: one-off spike at

the beginning of the year due

to changes in methodology

(visible mainly in non-mortage

lending), declining trend

afterwards in both mortage and

other loans supported by NPL

sales in the sector

• Corporate sector: significant

increase at the beginning of

the year due to changes in

methodology; converged to

previous levels towards end of

2018 for large corporates but

remain elevated for SMEs

Financial results Outlook Business development Appendix Achievements

46

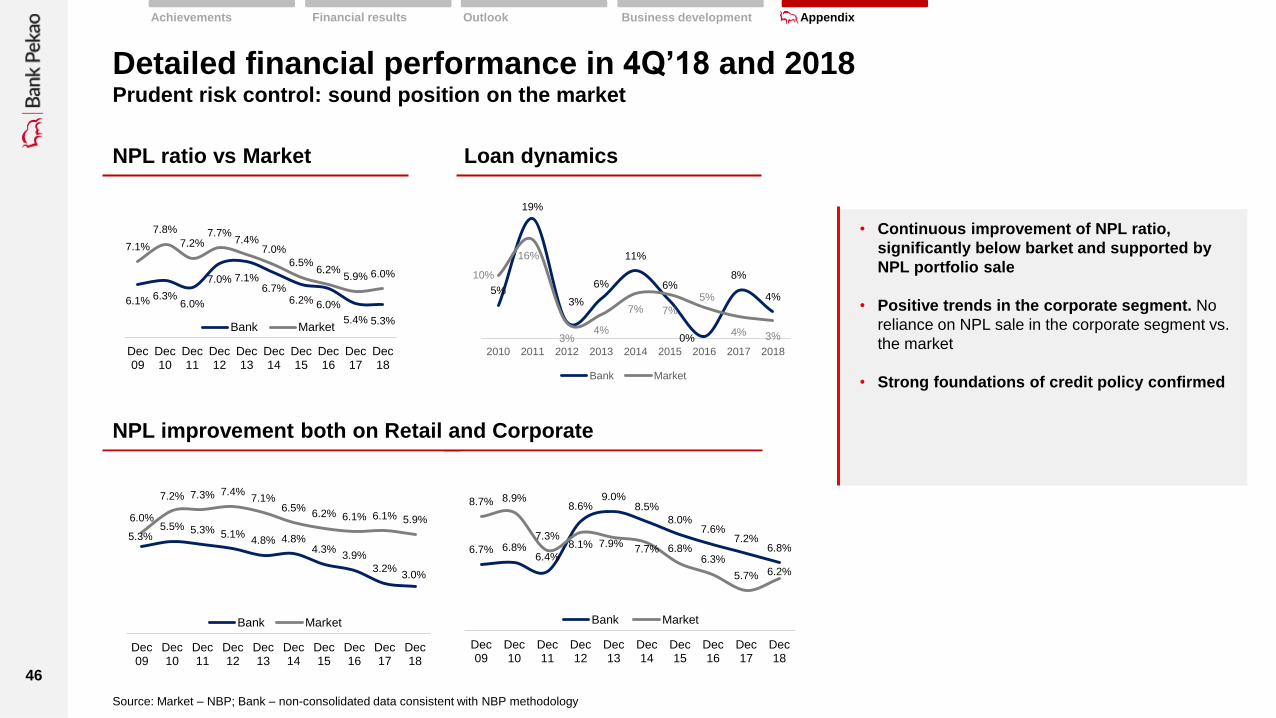

Detailed financial performance in 4Q’18 and 2018 Prudent risk control: sound position on the market

NPL ratio vs Market

NPL improvement both on Retail and Corporate

• Continuous improvement of NPL ratio,

significantly below barket and supported by

NPL portfolio sale

• Positive trends in the corporate segment. No

reliance on NPL sale in the corporate segment vs.

the market

• Strong foundations of credit policy confirmed

Loan dynamics

5%

19%

3%

6%

11%

6%

0%

8%

4%

10%

16%

3% 4%

7% 7%

5%

4% 3% 0%

5%

10%

15%

20%

2010 2011 2012 2013 2014 2015 2016 2017 2018

Bank Market

Financial results Outlook Business development Appendix Achievements

6.7% 6.8% 6.4%

8.6% 9.0%

8.5%

8.0% 7.6%

7.2% 6.8%

8.7% 8.9%

7.3% 8.1% 7.9%

7.7% 6.8% 6.3%

5.7% 6.2%

Dec09

Dec10

Dec11

Dec12

Dec13

Dec14

Dec15

Dec16

Dec17

Dec18

Bank Market

5.3% 5.5% 5.3% 5.1%

4.8% 4.8% 4.3%

3.9%

3.2% 3.0%

6.0%

7.2% 7.3% 7.4% 7.1%

6.5% 6.2% 6.1% 6.1% 5.9%

Dec09

Dec10

Dec11

Dec12

Dec13

Dec14

Dec15

Dec16

Dec17

Dec18

Bank Market

6.1% 6.3% 6.0%

7.0% 7.1% 6.7%

6.2% 6.0%

5.4% 5.3%

7.1%

7.8%

7.2% 7.7%

7.4% 7.0%

6.5% 6.2%

5.9% 6.0%

Dec09

Dec10

Dec11

Dec12

Dec13

Dec14

Dec15

Dec16

Dec17

Dec18

Bank Market

Source: Market – NBP; Bank – non-consolidated data consistent with NBP methodology

47

Selected data

48

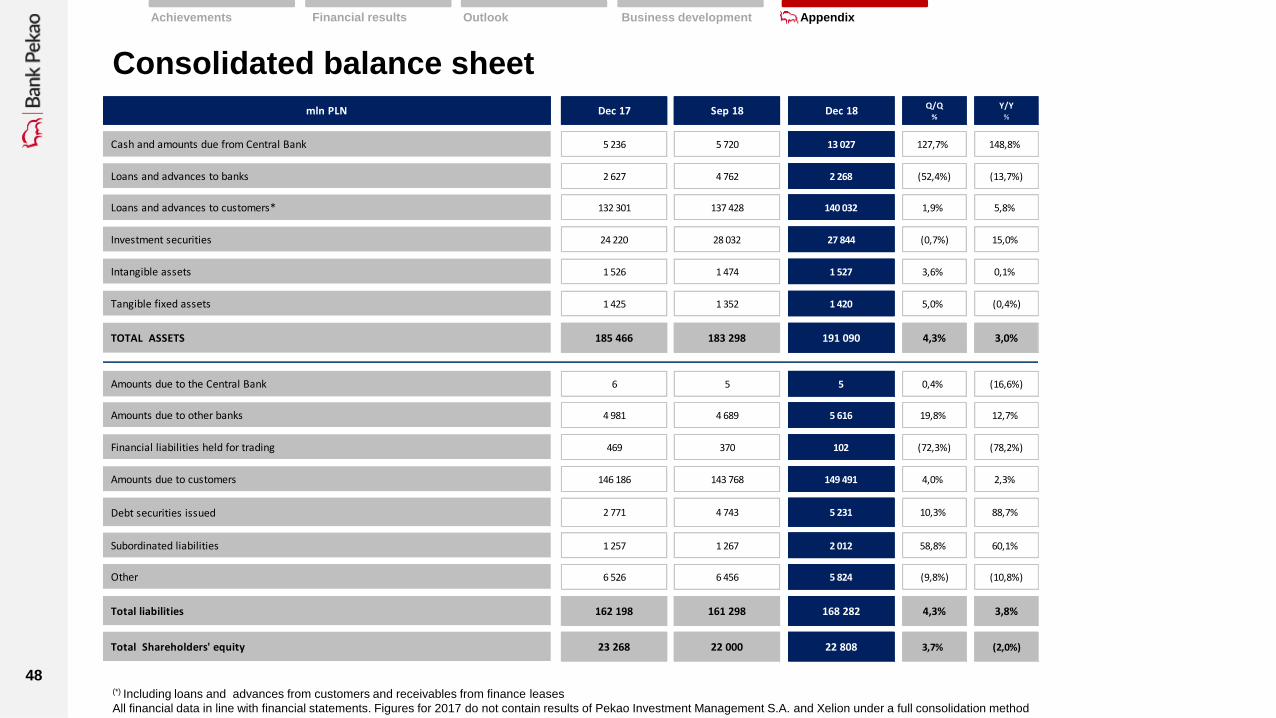

Consolidated balance sheet

(*) Including loans and advances from customers and receivables from finance leases

All financial data in line with financial statements. Figures for 2017 do not contain results of Pekao Investment Management S.A. and Xelion under a full consolidation method

Financial results Outlook Business development Appendix Achievements

mln PLN Dec 17 Sep 18 Dec 18 Q/Q%

Y/Y%

Cash and amounts due from Central Bank 5 236 5 720 13 027 127,7% 148,8%

Loans and advances to banks 2 627 4 762 2 268 (52,4%) (13,7%)

Loans and advances to customers* 132 301 137 428 140 032 1,9% 5,8%

Investment securities 24 220 28 032 27 844 (0,7%) 15,0%

Intangible assets 1 526 1 474 1 527 3,6% 0,1%

Tangible fixed assets 1 425 1 352 1 420 5,0% (0,4%)

TOTAL ASSETS 185 466 183 298 191 090 4,3% 3,0%

Amounts due to the Central Bank 6 5 5 0,4% (16,6%)

Amounts due to other banks 4 981 4 689 5 616 19,8% 12,7%

Financial liabilities held for trading 469 370 102 (72,3%) (78,2%)

Amounts due to customers 146 186 143 768 149 491 4,0% 2,3%

Debt securities issued 2 771 4 743 5 231 10,3% 88,7%

Subordinated liabilities 1 257 1 267 2 012 58,8% 60,1%

Other 6 526 6 456 5 824 (9,8%) (10,8%)

Total liabilities 162 198 161 298 168 282 4,3% 3,8%

Total Shareholders' equity 23 268 22 000 22 808 3,7% (2,0%)

49

Consolidated income statement

(1) NII and dividends and other income from equity investments. In 2018, in line with MSSF9, the bank reclassified some credit commissions and fees to net interest income

(2) Costs excl. guarantee funds charges

(3) In 2018 the bank changed methodology of presenting in P&L statement revenues from NPL sale reclassifying from net other income/expenses to provision

(4) Net profit attributable to equity holders of the Bank

NOTE: Data as reported

Financial results Outlook Business development Appendix Achievements

mln PLN 4Q 17 3Q 18 4Q 18 Q/Q % Y/Y % 12M 2017 12M 2018 Y/Y %

Net interest income (1) 1 198,1 1 258,2 1 294,9 2,9% 8,1% 4 652,7 5 014,2 7,8%

Net fee and commission 617,2 619,0 638,3 3,1% 3,4% 2 353,0 2 462,6 4,7%

Operating income 2 022,4 1 932,7 2 043,6 5,7% 1,0% 7 350,4 7 757,1 5,5%

Operating costs (2) (854,5) (843,3) (847,7) 0,5% (0,8%) (3 263,4) (3 444,4) 5,5%

OPERATING PROFIT 1 167,9 1 089,4 1 195,8 9,8% 2,4% 4 087,1 4 312,7 5,5%

Provisions (3) (152,8) (155,3) (104,9) (32,5%) (31,4%) (521,3) (511,0) (2,0%)

Guarantee funds charges (22,6) (30,5) (30,7) 0,5% 35,6% (269,0) (265,5) (1,3%)

Banking tax (138,8) (140,9) (144,2) 2,3% 3,9% (522,3) (562,0) 7,6%

PROFIT BEFORE INCOME TAX 1 253,8 793,3 976,8 23,1% (22,1%) 3 153,0 3 047,3 (3,4%)

Income tax (199,7) (186,9) (227,6) 21,7% 14,0% (677,3) (759,5) 12,1%

GROUP NET INCOME (4) 1 054,1 605,8 749,2 23,7% (28,9%) 2 475,1 2 287,2 (7,6%)

50

Consolidated income statement pro-forma

(1) NII and dividends and other income from equity investments; In 2018, in line with MSSF9, bank reclassified some credit commissions and fees to net interest income

(2) Costs excl. guarantee funds charges

(3) In 2018 the bank changed methodology of presenting in P&L statement revenues from NPL sale reclassifying from net other income/expenses to provision

(4) Net profit attributable to equity holders of the Bank

NOTE: Pro-forma, 2017 figures include results of Pekao Investment Management S.A. and Xelion under a full consolidation method

Financial results Outlook Business development Appendix Achievements

mln PLN 4Q 17 3Q 18 4Q 18 Q/Q % Y/Y % 12M 2017 12M 2018 Y/Y %

Net interest income (1) 1 191,0 1 258,2 1 294,9 2,9% 8,7% 4 616,9 5 014,2 8,6%

Net fee and commission 645,3 619,0 638,3 3,1% (1,1%) 2 505,0 2 462,6 (1,7%)

Operating income 1 901,0 1 932,7 2 043,6 5,7% 7,5% 7 324,5 7 757,1 5,9%

Operating costs (2) (863,8) (843,3) (847,7) 0,5% (1,9%) (3 319,0) (3 444,4) 3,8%

OPERATING PROFIT 1 037,1 1 089,4 1 195,8 9,8% 15,3% 4 005,5 4 312,7 7,7%

Provisions (3) (10,1) (155,3) (104,9) (32,5%) 935,0% (378,6) (511,0) 35,0%

Guarantee funds charges (22,6) (30,5) (30,7) 0,5% 35,6% (269,0) (265,5) (1,3%)

Banking tax (138,8) (140,9) (144,2) 2,3% 3,9% (522,3) (562,0) 7,6%

PROFIT BEFORE INCOME TAX 851,7 793,3 976,8 23,1% 14,7% 2 799,9 3 047,3 8,8%

Income tax (203,5) (186,9) (227,6) 21,7% 11,8% (697,1) (759,5) 9,0%

GROUP NET INCOME (4) 648,2 605,8 749,2 23,7% 15,6% 2 102,2 2 287,2 8,8%

51

Key performance indicators

NOTE: Data as reported

Financial results Outlook Business development Appendix Achievements

mln PLN 4Q 17 3Q 18 4Q 18Q/Q

net

Y/Y

net12M 2017 12M 2018

Y/Y

net

ROE (%) 18,6% 11,1% 13,4% 2,25 -5,24 11,0% 10,2% -0,85

ROA (%) 2,4% 1,3% 1,6% 0,29 -0,77 1,4% 1,3% -0,14

NIM (%) 2,8% 2,8% 2,9% 0,03 0,05 2,8% 2,8% 0,04

L/D (%) 88,5% 92,3% 89,5% -2,80 1,00 88,5% 89,5% 1,00

Cost/Income Ratio (%) 42,3% 43,6% 41,5% -2,10 -0,75 44,4% 44,4% 0,00

Cost of Risk (%) 0,45% 0,44% 0,39% -0,05 -0,06 0,40% 0,38% -0,02

TCR 17,1% 17,0% 17,4% 0,40 0,30 17,1% 17,4% 0,30

Tier 1 16,1% 16,0% 15,8% -0,20 -0,30 16,1% 15,8% -0,30

52

Selected data

(*) Number of accounts including pre-paid card accounts (**) Retail clients’ accounts (***) Pożyczka Ekspresowa (Express Loan)

Financial results Outlook Business development Appendix Achievements

Bank Dec 17 Sep 18 Dec 18 Q/Q % Y/Y %

Outlets 851 849 825 (2,8%) (3,1%)

ATM's 1 745 1 709 1 708 (0,1%) (2,1%)

Employees 15 316 14 674 14 569 (0,7%) (4,9%)

No of PLN current accounts (ths)* 5 669 5 876 5 949 1,2% 4,9%

No of mortgage loan accounts (ths)** 354 374 378 1,1% 6,7%

No of clients holding a consumer loan accounts (ths)*** 621 670 678 1,3% 9,2%

Number of individuals acitive users electronic banking Pekao24 (ths) 1 846 1 998 2 045 2,4% 10,8%

Number of individuals with an access to mobile banking (ths) 1 541 1 772 1 829 3,2% 18,7%

Group Dec 17 Sep 18 Dec 18 Q/Q % Y/Y %

Employees 17 339 16 906 16 714 (1,1%) (3,6%)

Number of MF accounts (ths) 762 736 723 (1,8%) (5,1%)

Number of Brokerage accounts (ths) 335 273 269 (1,5%) (19,6%)

53

Activity by segments

(1) Total net interest income, dividends and other income from equity investments

(2) Operating costs excluding guarantee funds charges

Nota: Income statement consistent with presentation version

Financial results Outlook Business development Appendix Achievements

2017 2018 Y/Y%

2017 2018 Y/Y%

2017 2018 Y/Y%

2017 2018 Y/Y%

2017 2018 Y/Y%

2017 2018 Y/Y%

Net interest income (1) 2 420,4 2 736,5 13,1% 40,6 38,7 (4,7%) 1 338,2 1 354,9 1,2% 160,8 180,1 12,0% 692,6 704,0 1,6% 4 653 5 014 7,8%

Non-interest income 1 285,8 1 420,3 10,5% 28,2 47,0 66,7% 834,5 1 019,0 22,1% 225,6 260,9 15,7% 323,6 (4,4) n.a. 2 698 2 743 1,7%

Operating income 3 706,2 4 156,7 12,2% 68,8 85,7 24,6% 2 172,7 2 373,9 9,3% 386,4 441,1 14,1% 1 016,2 699,6 (31,2%) 7 350,4 7 757,1 5,5%

Operating costs (2) (2 268,2) (2 384,6) 5,1% (53,7) (68,6) 27,6% (629,8) (671,4) 6,6% (317,3) (314,8) (0,8%) 5,8 (5,1) n.a. (3 263,4) (3 444,4) 5,5%

OPERATING PROFIT 1 438,0 1 772,1 23,2% 15,1 17,2 13,8% 1 542,9 1 702,5 10,3% 69,1 126,3 82,8% 1 022,0 694,5 (32,0%) 4 087,1 4 312,7 5,5%

Net write-downs/provision (196,3) (255,8) 30,3% (0,5) (0,1) (82,9%) (298,4) (234,2) (21,5%) (34,4) (32,3) (6,3%) 8,4 11,3 34,6% -521 -511 (2,0%)

Guarantee funds charges (155,7) (171,5) 10,2% (0,6) (0,6) (9,1%) (121,2) (153,3) 26,5% (7,6) (8,5) 12,2% 16,1 68,4 324,5% -269 -265 (1,3%)

Banking tax (522,3) (562,0) 7,6% -522 -562 7,6%

PROFIT BEFORE INCOME TAX 1 073,3 1 345,5 25,4% 13,8 14,5 5,5% 1 124,1 1 314,5 16,9% 27,0 85,5 216,3% 914,8 287,3 (68,6%) 3 153,0 3 047,3 (3,4%)

mln PLN

Retail Banking Private BankingCorporate&Investment

Banking

Assets&Liabilities

Management & OthersGroupSME Banking

54

Group net profit structure

(*) On December 11, 2017, the Bank acquired 51% of the stock in Pekao Investment Management S.A. and took control of this company. (**) On December 11, 2017, the Bank acquired 50% of the stock in Dom Inwestycyjny Xelion Sp. z o.o and took control of this company.

NOTE: Data as reported

Financial results Outlook Business development Appendix Achievements

mln PLN cumulativeGroup's share in

capital % 2017 2018 Y/Y %

Bank Pekao S.A. Banking - Poland 2 088,1 2 310,6 10,7%

Entities - consolidated under full method 79,8 188,6 136%

of which:

Pekao Leasing Sp. z o.o. Leasing 100% 34,8 47,6 36,8%

Centralny Dom Maklerski Pekao S.A. Brokerage 100% 33,1 24,8 (25,1%)

Pekao Bank Hipoteczny S.A. Mortgage Bank 100% 5,8 2,6 (55,2%)

Pekao PTE S.A. in liquidation Pension Fund 100% (3,1) 3,0

Pekao Faktoring Sp. z o.o. Factoring 100% 11,0 13,7 24,5%

Pekao Investment Banking S.A. Brokerage 100% 4,7 9,6 104,3%

Centrum Bankowości Bezpośredniej Sp. z o.o. Call Centre 100% 3,8 3,2 (15,8%)

Pekao Financial Services Sp. z o.o. Servicing MF/PF 66,5% 6,0 3,9 (35,0%)

Centrum Kart S.A. Cards 100% 0,8 0,3 (62,5%)

Pekao Fundusz Kapitałowy Sp. z o.o. in liquidation Business consulting 100% 0,4 0,4 0,0%

Pekao Property S.A. Real estate development 100% (24,5) (0,1) (99,6%)

FPB "MEDIA" Sp. z o.o. - indirect Real estate development 100% 0,9 (15,6) -1833%

Dom Inwestycyjny Xelion Sp. z o.o. Financial Advisory 100% 0,3 5,0

Pekao Investment Management S.A. Mutual Funds 100% 5,8 90,2

Entities - valued under the equity method 39,5 0,0 -100%

Pekao Investment Management S.A* Mutual Funds 36,9 ---

Dom Inwestycyjny Xelion Sp. z o.o. ** Financial Advisory 2,6 ---

Exclusions and consolidation adjustments 267,7 (212,0)

Group Net Profit (**) 2 475,1 2 287,2 (7,6%)

55

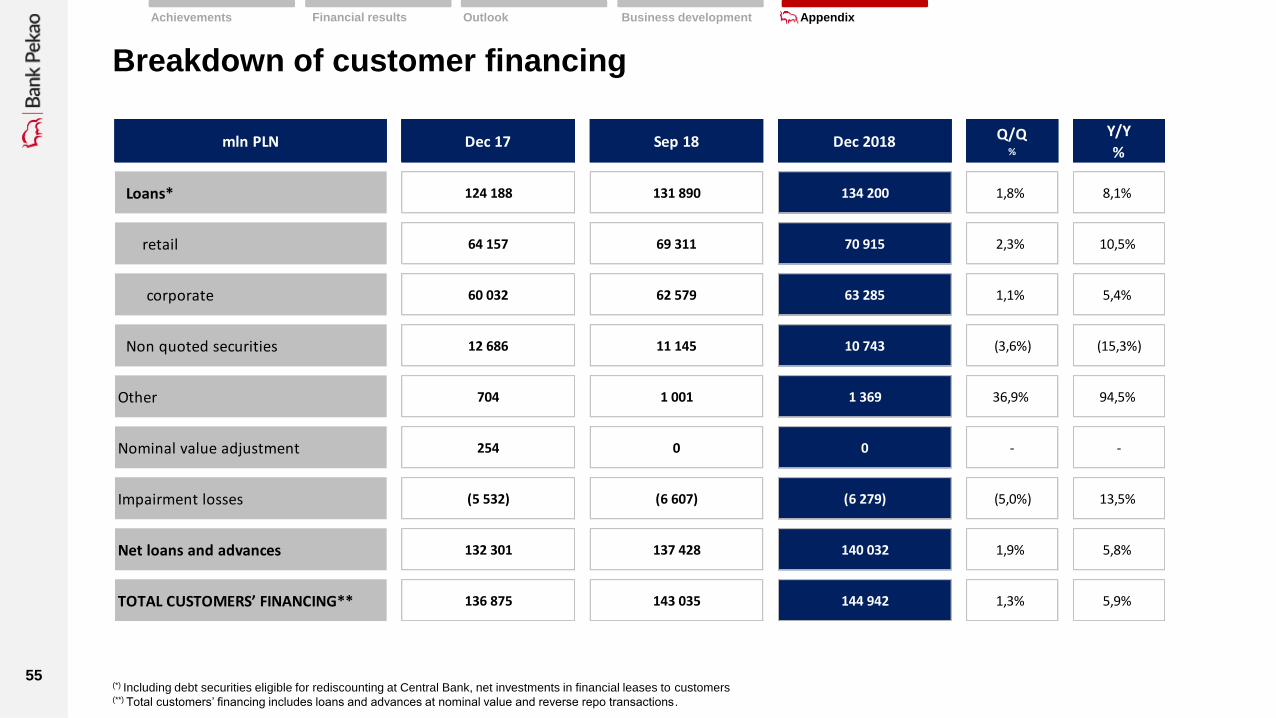

Breakdown of customer financing

(*) Including debt securities eligible for rediscounting at Central Bank, net investments in financial leases to customers (**) Total customers’ financing includes loans and advances at nominal value and reverse repo transactions.

Financial results Outlook Business development Appendix Achievements

mln PLN Dec 17 Sep 18 Dec 2018 Q/Q%

Y/Y

%

Loans* 124 188 131 890 134 200 1,8% 8,1%

retail 64 157 69 311 70 915 2,3% 10,5%

corporate 60 032 62 579 63 285 1,1% 5,4%

Non quoted securities 12 686 11 145 10 743 (3,6%) (15,3%)

Other 704 1 001 1 369 36,9% 94,5%

Nominal value adjustment 254 0 0 - -

Impairment losses (5 532) (6 607) (6 279) (5,0%) 13,5%

Net loans and advances 132 301 137 428 140 032 1,9% 5,8%

TOTAL CUSTOMERS’ FINANCING** 136 875 143 035 144 942 1,3% 5,9%

56

Financial results Outlook Business development Appendix Achievements

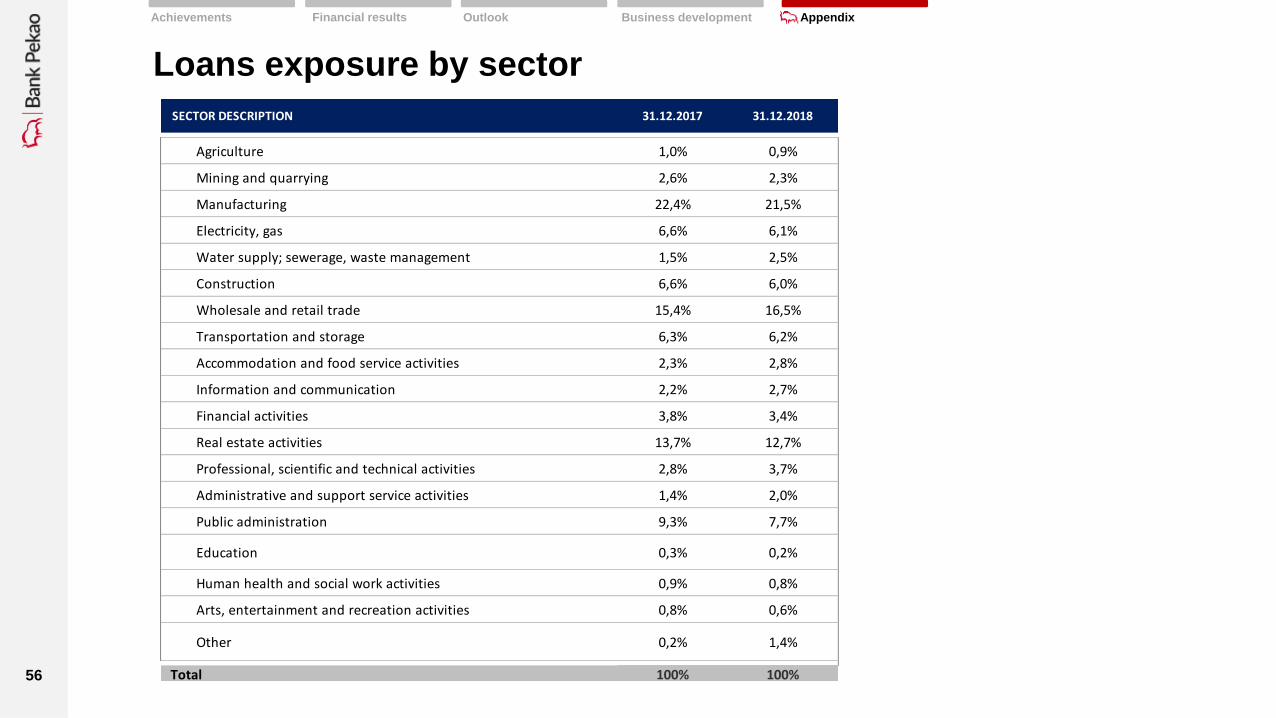

Loans exposure by sector

SECTOR DESCRIPTION 31.12.2017 31.12.2018

Agriculture 1,0% 0,9%

Mining and quarrying 2,6% 2,3%

Manufacturing 22,4% 21,5%

Electricity, gas 6,6% 6,1%

Water supply; sewerage, waste management 1,5% 2,5%

Construction 6,6% 6,0%

Wholesale and retail trade 15,4% 16,5%

Transportation and storage 6,3% 6,2%

Accommodation and food service activities 2,3% 2,8%

Information and communication 2,2% 2,7%

Financial activities 3,8% 3,4%

Real estate activities 13,7% 12,7%

Professional, scientific and technical activities 2,8% 3,7%

Administrative and support service activities 1,4% 2,0%

Public administration 9,3% 7,7%

Education 0,3% 0,2%

Human health and social work activities 0,9% 0,8%

Arts, entertainment and recreation activities 0,8% 0,6%

Other 0,2% 1,4%

Total 100% 100%

57

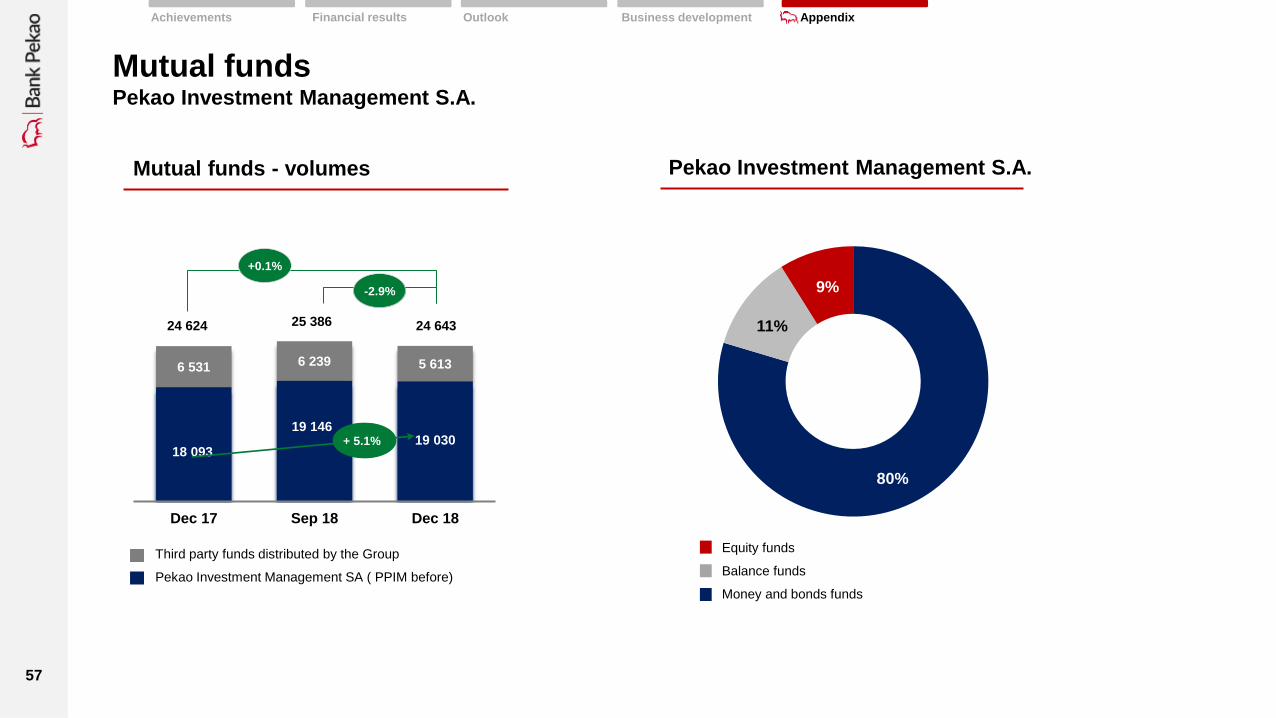

Mutual funds Pekao Investment Management S.A.

Mutual funds - volumes Pekao Investment Management S.A.

80%

11%

9%

Equity funds

Balance funds

Money and bonds funds

18 093

19 146 19 030

6 531 6 239 5 613

Dec 17 Sep 18 Dec 18

+ 5.1%

-2.9%

+0.1%

24 624 25 386 24 643

Pekao Investment Management SA ( PPIM before)

Third party funds distributed by the Group

Financial results Outlook Business development Appendix Achievements

58

Ratings of Bank Pekao S.A.

On October 17, 2018, Fitch Ratings has changed the following ratings of Bank Pekao S.A.: Long-term Issuer Default Rating (IDR) from "A-“ to "BBB+;„ Outlook on long-term IDR from “Negative” to “Stable”

Viability Rating (VR) from "a-" to "bbb+"; Other Bank’s ratings Fitch Ratings confirmed at the unchanged level.

(**) On October 12, 2018, S& P Global Ratings changed following ratings of Poland: Long-term in foreign currencies from "BBB +" to "A-„; Long-term in the national currency from "A-" to "A„; Outlook on the long-term domestic

and long-term ratings from “Positive” to “Stable”

(***) On October 15, 2018 S&P Global Ratings confirmed the Issuer Credit Rating of Bank Pekao S.A. and at the same time upgraded Bank’s RCR long-term

rating from "BBB+" to "A-". The short-term RCR was confirmed at the "A-2" level.

Financial results Outlook Business development Appendix Achievements

31.12.2018

FITCH RATINGS PEKAO POLAND

Long-term rating (IDR) BBB+ A-

Short-term rating F2 F2

Viability rating bbb+ -

Support rating 5 -

Outlook Stable Stable

S&P GLOBAL RATINGS PEKAO POLAND

Long-term rating BBB+ A-

Short-term rating A-2 A-2

Stand-alone bbb -

Outlook Stable Stable

MOODY'S INVESTORS SERVICE LTDPEKAO

(unsolicited rating)POLAND

Long-term foreign-currency deposit rating A2 A2

Short-term deposit rating Prime-1 Prime-1

BCA baa1 -

Long term counterparty credit risk A1(cr) -

Short term counterparty credit risk Prime-1(cr) -

Outlook Stable Stable

59

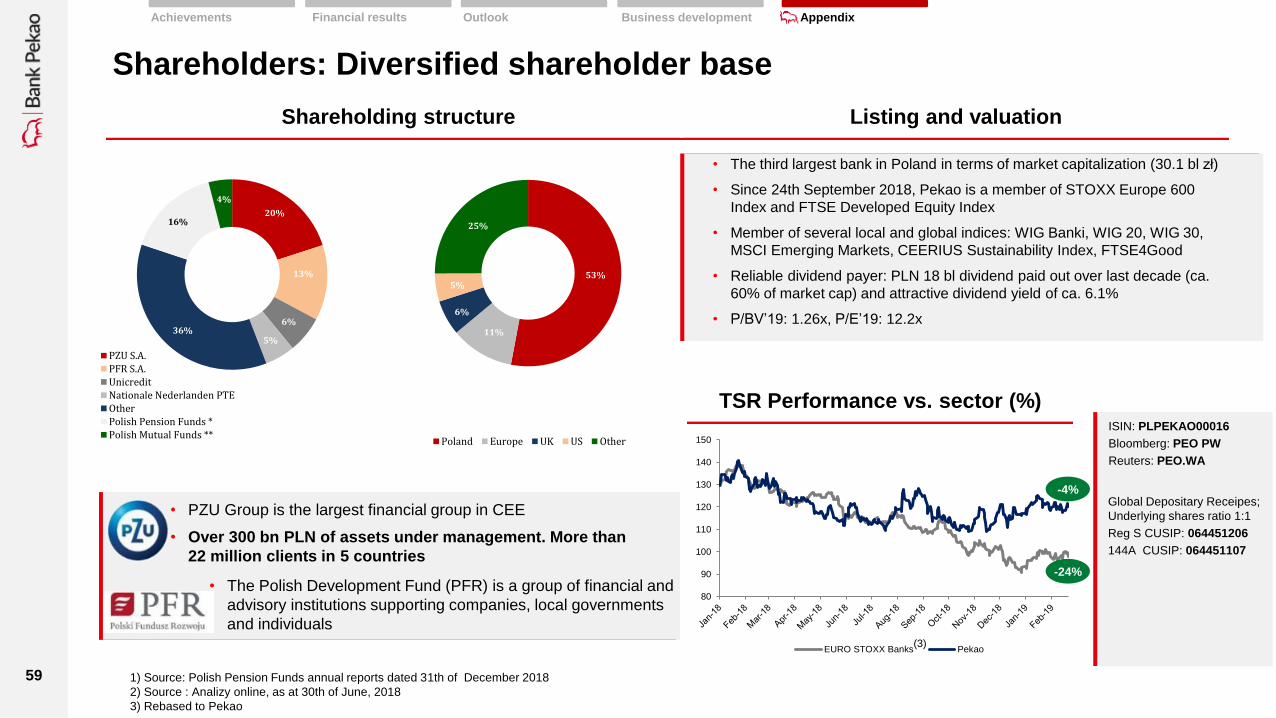

• The third largest bank in Poland in terms of market capitalization (30.1 bl zł)

• Since 24th September 2018, Pekao is a member of STOXX Europe 600

Index and FTSE Developed Equity Index