2017 q2 pulse tooling update - oesa.org · pdf file85% 90% 95% 100% 2017 q2 capacity...

TRANSCRIPT

1

2017 Q2 Pulse Tooling UpdateMay 2017

2

Survey Overview

Harbour Results’ 2017 Q2 survey covered a quick update on the tooling industry current state. It covered an additional dive into key components of shops’ financial statements.

Survey population includes a total of 61 respondents, split 72% mold and 28% die.

3

TOOLING BAROMETER

4

Respondent Demographics

• Question: Please identify your Revenue for 2016• Question: Please identify your company’s geographic location

Location

32%

68%

4% of respondents from outside NA

21% 21%

26%

13%

18%

0%

5%

10%

15%

20%

25%

30%

<$5M $5-$10M $10-$20M $20-$40M >$40M

Revenue Range

28%

72%

Shop Type

Die Mold

5

Shops’ Utilizations Leveling Out or Slowing in Q2

• Question: Current capacity utilization for design/machining/assembly

91%89%

87%

81%

85%88% 89%

83%

87%84%

77%79% 79%

76%

67%

76%77% 76%

81%83%

60%

65%

70%

75%

80%

85%

90%

95%

100%

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

2016Q2

2016Q3

2016Q4

2017Q1

2017Q2

Capacity Utilization By Shop Type

Die Mold

81%78%

80%

90%

95%

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

2017 Q2 Capacity Utilization

6

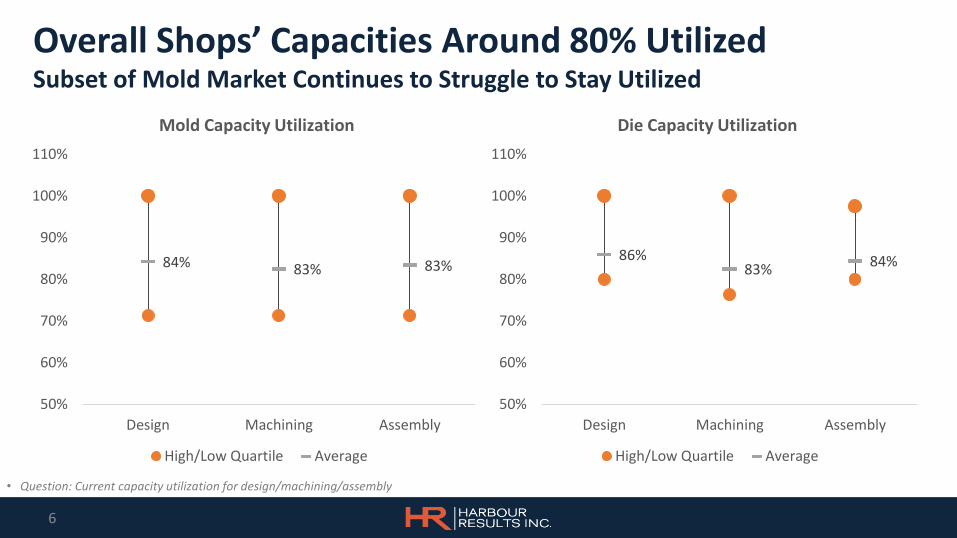

Overall Shops’ Capacities Around 80% UtilizedSubset of Mold Market Continues to Struggle to Stay Utilized

• Question: Current capacity utilization for design/machining/assembly

84% 83% 83%

50%

60%

70%

80%

90%

100%

110%

Design Machining Assembly

Mold Capacity Utilization

High/Low Quartile Average

86%83%

84%

50%

60%

70%

80%

90%

100%

110%

Design Machining Assembly

Die Capacity Utilization

High/Low Quartile Average

7

US Shops Having Harder Time Staying Full

• Source: AMBA

75%

71%74%

82%

77%

50%

60%

70%

80%

90%

100%

<$2.5M $2.5M-$5M $5M-$10M $10M-$20M >$20M

US Mold Capacity Utilization

Lower Quartile Upper Quartile Average

25% of shops fall under the red markers in utilization

8

Mold and Die Showing Very Similar P&L Statements

75% 78%

16%15%

9% 7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Mold Die

Profit and Loss Summary

EBIT

SG&A

COGS

24% 26%

29% 29%

16% 16%

6%7%

75%78%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Mold Die

Manufacturing Costs

Depreciation

Subcontracting

Direct Labor

Materials

9

Future Booked Business Drops from First Quarter

• Question: What is your shop’s tooling revenue (2016); Quarterly Booked Business

28%

21%

7%

2%

19%

9%

4%4%

0%

5%

10%

15%

20%

25%

30%

2017 Q3 2017 Q4 2018 Q1 2018 Q2

Mold and Die Booked Business(as of Q2 2017)

Die Mold

Average Booked BusinessMold: 36%Die: 57%

22%

14%

5%3%

0%

5%

10%

15%

20%

25%

2017 Q3 2017 Q4 2018 Q1 2018 Q2

Quarterly Booked Business(as of Q2 2017)

The average shop has 44% of their revenue

booked, down over 20% from first quarter 2017.

10

15.7%

11.9%

17.9%

12.2%

13.9%

9.3%

11.5%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2015 Q1 2015 Q2 2015 Q3 2015 Q4 2016 Q1 2016 Q2 2016 Q3 2016 Q4 2017 Q1 2017 Q2

Work On-Hold

Work On Hold Rises Back to Over 11%

The clearly cyclical nature of work on hold continues, as a significant number of shops (particularly on the mold side)

are experiencing delays

• Question: What percent of jobs that you have been awarded are currently on hold due to reasons outside of your control?

11

12.8% 10.7%0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Die Mold

Work On Hold by Shop Type - 2017 Q1

D3 Driving Significant Delays in Suppliers

• Question: What percent of jobs that you have been awarded are currently on hold due to reasons outside of your control?

While a significant number of shops are

experiencing “standard” levels of delays, there are a subset of die and

mold shops experiencing

significant (+20%) delays due to several

key programs

12

49%

51%56% 56%

62% 62% 62% 62% 62%68%

51%

44%

59% 59%

57% 57% 57%61% 61%

71%

25%

35%

45%

55%

65%

75%

85%

2014 Q4 2015 Q1 2015 Q2 2015 Q3 2015 Q4 2016 Q1 2016 Q2 2016 Q3 2016 Q4 2017 Q1

Progressive Payment Terms and AR Paid On Time

Percent Progressive Terms Percent of AR Paid On-Time

Payment Terms and Timing Peaked in First Quarter

• Question: Over the past three months, approximately what percent of your: new booked business includes progressive payment terms; accounts receivables were being paid within contract terms

13

56%

72% 72%68% 68%

73%79%

79%85%

80%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

2016Q2

2016Q3

2016Q4

2017Q1

2017Q2

General Business Outlook

Sentiment Positive Threshold

Sentiment Dips, Remains PositiveWith an increase in work on hold and decreases in

utilization, booked business and payment

terms, shops saw a slight decrease in optimism from

the first quarter.

• Question: Over the next three months, the general outlook for your business is:

While a small decrease occurred from the previous quarter, shops remain very optimistic.

Sentiment% of

Respondents

Pessimistic 0%

Somewhat pessimistic 3%

Neutral 14%

Somewhat Optimistic 44%

Very Optimistic 39%

14

PRIMARY AND SECONDARY SHOPS

15

Previous State of the Mold Supply Chain

16

Future State of the Mold Supply Chain

17

Current/Future State of the Die Supply Chain

18

Primary Shops Have Less Trouble Staying Full

87% 86% 87% 86%

76%81%

87%91% 90%

95%

78%80% 80%

76%

70%

78% 78%

75%

81%78%

60%

65%

70%

75%

80%

85%

90%

95%

100%

2015 Q1 2015 Q2 2015 Q3 2015 Q4 2016 Q1 2016 Q2 2016 Q3 2016 Q4 2017 Q1 2017 Q2

Capacity Utilization By Primary and Secondary Shops

Primary Secondary

• Question: Current capacity utilization for design/machining/assembly

19

Primary Shops More Vulnerable to Work On Hold

14%

22%

28%

20%

16%

11%

15%16%

10% 10%

16% 16%

11%

14% 14%

9%11%

0%

5%

10%

15%

20%

25%

30%

35%

2015 Q1 2015 Q2 2015 Q3 2015 Q4 2016 Q1 2016 Q2 2016 Q3 2016 Q4 2017 Q1 2017 Q2

Work On-Hold

Primary Work on Hold Secondary Work on Hold Level

• Question: What percent of jobs that you have been awarded are currently on hold due to reasons outside of your control?

20

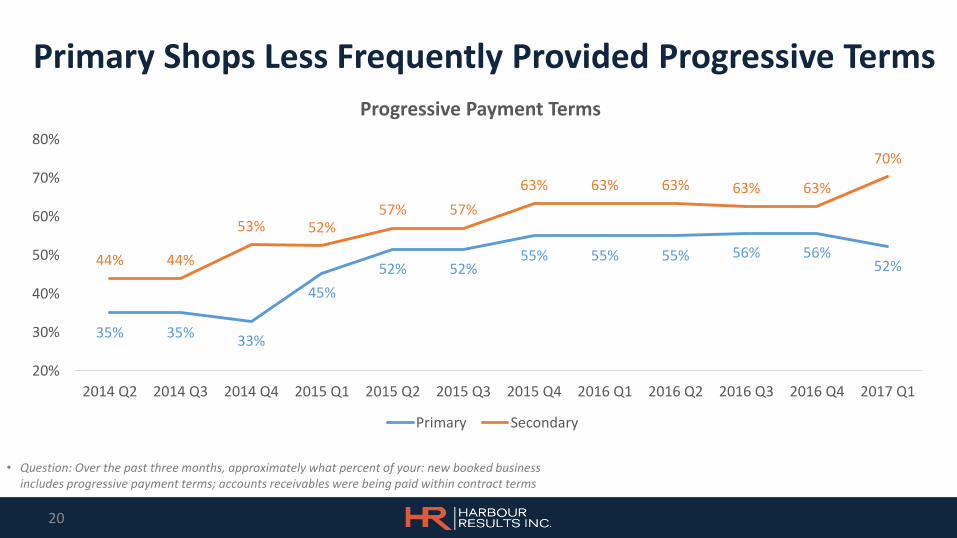

Primary Shops Less Frequently Provided Progressive Terms

• Question: Over the past three months, approximately what percent of your: new booked business includes progressive payment terms; accounts receivables were being paid within contract terms

35% 35%33%

45%

52% 52%55% 55% 55% 56% 56%

52%44% 44%

53% 52%57% 57%

63% 63% 63% 63% 63%

70%

20%

30%

40%

50%

60%

70%

80%

2014 Q2 2014 Q3 2014 Q4 2015 Q1 2015 Q2 2015 Q3 2015 Q4 2016 Q1 2016 Q2 2016 Q3 2016 Q4 2017 Q1

Progressive Payment Terms

Primary Secondary

21

Primary shops have to approach sales

differently than other tool shops. They have

to intentionally oversell their capacity

and outsource whatever they cannot handle, since they are more susceptible to delays/work holds.

Primary Shops Have to Oversell CapacityUse Outsourcing To Flex to Accommodate Work Delays/Holds

• Question: Current capacity utilization for design/machining/assembly

76.2% 81.4% 87.4% 90.5% 89.9% 95.4%

14.3%14.3%

14.3% 14.3% 15.0%15.0%28.2% 20.3%

16.3% 16.3% 11.3%14.8%

0%

20%

40%

60%

80%

100%

120%

140%

2016 Q1 2016 Q2 2016 Q3 2016 Q4 2017 Q1 2017 Q2

Primary Shop Utilization, Outsourcing and Work On Hold

Work On Hold

Outsourcing

Capacity Utilization

22

Primary Shops Leveraging SG&A For EBIT

76% 75%

7%17%

17%7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Primary Secondary

Profit and Loss Summary

COGS SG&A EBIT

24% 24%

28% 29%

19% 15%

4% 6%

76% 75%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Primary Secondary

Manufacturing Costs

Depreciation

Subcontracting

Direct Labor

Materials

23

What Are They (or Should They Be) Doing?Primary Shops Establishing strong tooling supply

base and supplier development to support them.

Focusing on becoming preferred suppliers for OEMs and large T1s and developing these relationships

Developing strategic sales plans to “feed the beast”

Capacity planning to avoid lulls

Driving efficiency in their shops and investing in capital

Secondary Shops Developing relationships with

primary shops as supply base shifts

Working to take advantage of advantageous stair steps of growth, working to drive bottom line

Pushing for advantageous payment terms

Sales planning to focus on filling walls with best-fit work with high margins

Developing niche

24

WHAT NEXT?

25

2017 Still Looks to be a Very Heavy Year for Tool Sourcing

33

42

35 34

17

33

13

0

10

20

30

40

50

2016 2017 2018 2019 2020 2021 2022

Annual OEM Launches by Type (w/o Facelift) - Tool Sourcing

New Entry Redesign

While New Entry and Redesigns showing a decrease in future years, the next 18-24 months still show strong opportunity for tool shops.

26

The Addition of Facelifts Level Out Work for Some Mold Shops

64 63 63 63

54

66

37

0

10

20

30

40

50

60

70

80

2016 2017 2018 2019 2020 2021 2022

Annual OEM Launches by Type - Tool Sourcing

New Entry Redesign Facelift

27

Summary Despite small dips in key indicators, sentiment remains at one

of highest points in last two years.

There continues to be a division between shops who are very busy and shops struggling to bring work in.

Overall averages for profitability relatively healthy, but the underlying variance strengthens the growing division.

Shops need to capitalize on the “good times”, and make sure they are prepared for the possibility of a dip.