2017 long-term capital market expectations · 2017 long-term capital market expectations “we’ve...

TRANSCRIPT

2017LONG-TERMCAPITAL MARKETEXPECTATIONS

“We’ve increased our forecast for developed-market

equities in view of an improving growth outlook and

moderate inflation expectations.”

1. Franklin Templeton Solutions is a global investment management group dedicated to multi-strategy solutions and is comprised of individuals representing various registered investment advisory entity subsidiaries of Franklin Resources, Inc., a global investment organization operating as Franklin Templeton Investments.

About Franklin Templeton Solutions

Franklin Templeton Solutions (FT Solutions)1 is a team of multi-asset and alternative investment

experts embedded within the global integrated platform of Franklin Templeton—a trusted partner

in asset management with clients in more than 170 countries. Our FT Solutions team has been

dedicated to managing multi-asset portfolios for over 20 years covering both traditional multi-asset

strategies and alternative strategies.

In addition to retail investors around the world, our FT Solutions team serves a variety of client

types in the institutional arena, ranging from sovereign wealth funds to public and private pension

plans. The hallmark of our approach is a disciplined discussion process—with an 80 plus-member

global investment forum—that manages assets of over US$40 billion (as of December 31, 2016).

BROOKS RITCHEY

Senior Vice President,

Director of Investment Solutions

CHANDRA SEETHAMRAJU, MBA, PH.D.

Vice President,

Director of Systematic Modeling

TOM NELSON, CFA, CAIA

Senior Vice President,

Director of Investment Solutions

Contents

THE WORLD FROM OUR PERSPECTIVE 2

OUR STRONGEST CONVICTIONS “FOR” 4

OUR STRONGEST CONVICTIONS “AGAINST” 10

OUR CAPITAL MARKET EXPECTATIONS 12

OUR METHODOLOGY AND MODELS 14

APPENDIX: INDEXES AND PROXIES USED 18

2017 Long-Term Capital Market ExpectationsFor Financial Professional Use Only. Not For Public Distribution.

Not FDIC Insured | May Lose Value | No Bank Guarantee

1

See appendix for methodology and models used.

We believe the global growth outlook is

improving, supported by fiscal stimulus around

the world, the pro-growth policies of the incoming

US administration and stabilized growth in China.

We also see inflation hovering in the moderate

zone for the next five to 10 years.

After our annual review of the data and themes driving capital markets—

current valuation measures, historical risk premiums, economic growth

and inflation prospects—we’re pleased to report on our 2017 Capital

Market Expectations.

Our Strongest Convictions:

For Against

Global Stocks Global Government Bonds

Swedish Krona Swiss Franc

Japanese Equity

US Infrastructure

February 2017

2017 Long-Term Capital Market Expectations For Financial Professional Use Only. Not For Public Distribution.

Global Growth. Significant

Uncertainty.

We believe the global growth outlook

is improving, supported by fiscal

stimulus around the world, pro-growth

policies of the incoming US

administration and stabilized growth

in China.

Stimulus fiscal policies finally arrived

center stage in 2016 as easy

monetary policies around the world

lost their effectiveness. For example:

• Japan announced a ¥28 trillion

stimulus package in August 2016.

• Donald Trump, president of the

United States, seems certain to

introduce significant fiscal stimulus

via a combination of tax cuts and

infrastructure spending.

• European Union (EU) countries are

still bound by Maastricht deficit and

debt limits, but given the anti-EU

populist movement in Europe, it’s

hard to rule out fiscal stimulus

completely.

The new US administration seems

likely to bring in fiscal stimulus and

de-regulation, which could be another

boost for growth. We expect the

financial, energy and health care

sectors (which combined account for

more than a third of the US economy)

to benefit the most.

China’s economic slowdown appears

to have reached its bottom in 2016.

The year-over-year Producer Price

Index finally nudged into positive

territory after almost four years of

negative results. The Manufacturing

Purchasing Managers’ Index also

tipped over 50, which should help to

keep the positive momentum.2 The

current strong dollar trend is also a

boost for the yuan and Chinese

exporters. It’s still too early to predict

the outcome of structural reforms in

China, but the country appears to be

making good progress on moving to a

consumer-driven economy from an

export-oriented economy, which we

also see as a big plus for global

growth.

Although we’re becoming more

confident about global growth, we

need to acknowledge that there are

significant uncertainties down the

road. For example:

• Current populist movements could

potentially create strong headwinds

in struggling European economies.

Based on the outcomes of the Brexit

vote and the recent Italian

referendum, the integrity of the EU

seems likely to face additional

challenges ahead before it

stabilizes—if it can stabilize.

• In the United States, markets seem

to be pricing in Trump’s ambitious

plans. Whether his administration

can deliver meaningful change to

the economy is still unknown, but

markets will be disappointed if

results fall short of expectations.

• China appears to have navigated

through another difficult trough,

however the country’s debt problem

has not been solved and appears to

be getting worse.

Finally, we believe aging population—

in China and in developed markets

overall—is a powerful demographic

factor that may depress global

growth. Given the current anti-

globalization and anti-trade

sentiments, it’ll be even harder to

mitigate the impact of these long-term

changes.

Moderate Inflation Ahead

In 2015 and early 2016, deflation

fears topped the list of risks to the

global economy. That concern has

diminished since commodity prices

stabilized. Inflation expectations

around the world started to notch

upward in the middle of 2016, well

before Trump’s victory. We believe

inflation will normalize faster in the

United States than the rest of the

world. However, long-term structural

2

2. Source: Bloomberg.

THE WORLD FROM OUR PERSPECTIVE

2017 Long-Term Capital Market ExpectationsFor Financial Professional Use Only. Not For Public Distribution.

factors such as aging populations and

the savings glut should keep inflation

in the moderate zone for the next five

to 10 years.

Currently, US Personal Consumption

Expenditure Core (PCE Core), a price

inflation measure that the US Federal

Reserve (Fed) emphasizes, is at

1.7% year-over-year.3 Trump’s fiscal

stimulus plan could create jobs and

increase aggregate demand in the

short term, which may bring PCE

Core back to the Fed’s target of 2%

within the next two years.

Although we believe that most of the

potential new US policies are

inflationary, if the rest of world does

not follow suit—given the openness of

our global economy—we do not

expect the US inflation rate to differ

significantly from those in the rest of

the world. Japan and Europe are

experiencing an aging population

trend, which we believe suppresses

aggregate demand and growth

potential. Negative interest rates still

exist in Japan and some European

countries. On top of that, the current

account surplus of major exporters

such as Germany, China and Japan

is now back to 2006–2008 levels and

therefore, the excessive supply of

capital is still a depressing factor for

interest rates and inflation. See chart

to the right.

Developed-Market Equities

Look Attractive, but

Developed-Market Bonds

Are Shaky

We’ve increased our forecast for

developed-market equities in view of

an improving growth outlook and

moderate inflation expectations.

Emerging-market equities are less

attractive this year primarily because

they recovered in 2016 and today’s

valuations are therefore less

attractive. On top of that, a rising

interest-rate cycle in the United

States could make emerging markets

vulnerable to significant capital

outflows.

After more than a 30-year run-up,

developed-market bond markets were

poised to sell off in the middle of

2016, even before the US election.

Since then, markets seem convinced

that the rising-rate cycle in US

Treasuries is likely to accelerate

regardless of negative interest rates

in Japan or quantitative easing (QE)

in Europe. Given the current low

yields and high durations, the

expected returns of developed-market

bonds are even lower than our last

year’s forecast.

Consensus Economics (10Y) Breakeven Rate (5Y5Y)

United States 2.2% 1.9%

Canada 2.0% 1.5%

Eurozone 1.9% 1.2%

United Kingdom 2.0% 3.0%

Japan 1.3% 0.6%

Australia 2.5% 1.9%

3

Source: Consensus Forecasts, October 2016; Bloomberg, November 2016. There is no assurance that any forecast will be realized.

Long-Term Inflation Forecasts

3. Source: Bloomberg.

Long-term

structural

factors such

as aging

populations

and the

savings glut

should keep

inflation in the

moderate

zone for the

next five to 10

years.”

“

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Billions USD

Source: Bloomberg, International Monetary Fund (IMF), as of 12/31/16. Past performance does not guarantee future results.

Export-Driven Economies Nearing 2006–2008 Current Account Surplus Levels

Current Account Balance of Germany + Japan + China1998–2016

2017 Long-Term Capital Market Expectations For Financial Professional Use Only. Not For Public Distribution.

7.8%7.5%

8.7%

9.4%

0.3%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

GlobalEquity

Developed-MarketEquity

Emerging-MarketEquity

GlobalSmall-Cap

Equity

GlobalDeveloped

Gov't Bonds

Expected Return

4

We believe global stocks have greater

performance potential than other

asset classes in anticipation of

stimulus fiscal policy and a moderate

inflation environment in the next five

to 10 years.

As we expected at the beginning of

2016, markets recovered from the

initial volatility and ended the year in

positive territory. The MSCI World

Index was up 8.16%, and the SPX

Index was up 11.93%. Markets

showed significant resilience given

that two so-called “black-swan” events

occurred during the year: Brexit and

Trump’s election. We believe stocks

can benefit more from the expected

fiscal stimulus of the new Republican

regime in the United States. A

combination of tax cuts, deficit

spending, deregulation and foreign

cash repatriation could have a broad

boost effect on the economy. At the

same time, we believe the structural

problems in Europe and Japan will

keep global inflation moderate.

Although the US dollar (USD) and the

US 10-year yield moved up

significantly after the election, we

expect both markets to slow down in

2017, and the rate hike cycle will still

be a moderate one.

From a valuation perspective, price-

to-earnings (P/E) ratios are currently

below their long-term average, which

is favorable for long-term global stock

return potential.

Our average annual return

expectation for global equities is fairly

close to the historical average.

Overall, we expect global equities to

return 7.8% annually over the seven-

year period, with developed markets

returning 7.5%, emerging markets

8.7% and global small caps 9.4%. By

comparison, we expect global

government bonds to return less than

1%.

OUR STRONGEST CONVICTIONS “FOR”

Global Stocks Could Benefit from Improved Growth and Moderate

Inflation Outlook

Source: Thomson Reuters, Institutional Broker’s Estimate System (I/B/E/S), MSCI, as of 10/31/16. Past performance does not guarantee future results.

0

5

10

15

20

25

30

35

1988 1992 1996 2000 2004 2008 2012 2016

P/E Ratio

Average

P/E Ratios Favor Long-Term Global Equity Return Potential

MSCI All Country World Index P/E Ratio1988–2016

We Expect Global Equities to Outperform Many Other Asset Classes

Comparison of Expected Annualized Returns of Major Stock Indexes

vs. Global Government BondsAs of November 30, 2016

Projected Annualized Returns, January 1, 2017–December 31, 2023

Source: FT Solutions. See appendix on page 18 for representative indexes for each asset class. Opinions and beliefs expressed are those of FT Solutions and are subject to change without notice. There is no assurance that any forecast or projection will be realized.

2017 Long-Term Capital Market ExpectationsFor Financial Professional Use Only. Not For Public Distribution.

We are bullish on the Swedish krona

(SEK) from three different

perspectives:

• valuation

• growth prospects

• the expected monetary policy

environment

In our opinion, from a valuation

perspective, the SEK is the most

undervalued relative to other

developed-market currencies.

Sweden’s policy rate relative to its

growth trajectory is the most

displaced among developed markets:

While its policy rate is one of the most

negative, its nominal gross domestic

product (GDP) growth is one of the

most positive. The growth differential

between Sweden and the United

States has reached its widest point in

five years yet the Riksbank, the

Swedish central bank, maintains its

accommodative policy.

Unemployment has reached an eight-

year low, and the economic tendency

indicator (a survey of business and

consumer views of the economy)4

continues to trend higher. We expect

the positive trajectory for the Swedish

economy to continue.

The Riksbank remains committed to

its easy monetary policy, pledging not

to raise rates from its current negative

level until 2018 and offering to extend

its bond purchases in order to support

the economy. This policy has

effectively kept SEKUSD subdued.

Amid strengthening economic

fundamentals and rising house prices

in Sweden, however, it’s difficult to

see how negative policy rates could

continue. The IMF expects inflation in

Sweden to reach the central bank’s

target of 2% in 2018, leaving less

room for the central bank to maintain

its easy monetary policy.

We believe this policy is unlikely to

hold over the long term, especially if

inflation starts to pick up. The

Riksbank will need to begin its

tightening cycle, ultimately boosting

SEKUSD.

5

4. The Economic Tendency Indicator measures overall business and consumer sentiment. It is based on monthly business surveys in the manufacturing, construction, retail trade and private service sectors, as well as monthly consumer surveys. The indicator has a mean value of 100 and a standard deviation of 10. Values between 100 and 110 are equivalent to a stronger-than-normal economy, whereas values above 110 represent a much stronger-than-normal economy. Likewise, values between 90 and 100 show a weaker-than-normal economy and values below 90 are equivalent to a much weaker-than-normal economy.

Long Swedish Krona vs. US Dollar

Source: Bloomberg, National Institute of Economic Research (Sweden), as of 11/30/16. Past performance does not guarantee future results.

Sweden’s Economy Stronger than Normal

Sweden: Economic Tendency Indicator4

2010–2016

80

85

90

95

100

105

110

115

120

2010 2011 2012 2013 2014 2015 2016

Index above 110:

Economy is much

stronger than normal

Index below 90:

Economy is much

weaker than normal

Economic Tendency Indicator

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

2010 2011 2012 2013 2014 2015 2016

Unemployment Rate

Sweden’s Unemployment Rate at Eight-Year Low

Sweden: Unemployment Rate2010–2016

Source: Bloomberg, National Institute of Economic Research (Sweden), as of 12/31/16. Past performance does not guarantee future results.

2017 Long-Term Capital Market Expectations For Financial Professional Use Only. Not For Public Distribution.6

5. Source: Bloomberg.

6. Source: Organisation for Economic Co-operation and Development (OECD) Economic Outlook, Volume 16, Issue 2.

An improved growth outlook, high

profit margins and attractive

valuations all support Japanese

equity.

An ultra-loose monetary policy—

massive QE and negative interest

rates—combined with three stimulus

fiscal budgets in 2016 alone have

finally resulted in a positive impact on

growth. Real GDP increased at an

annualized rate of 1.6% in the first

three quarters of 2016.5

Exports were very resilient given

significant yen appreciation. After

declining in the first half of 2016,

exports rebounded sharply in the third

quarter.6 After the US election, the

Source: Bloomberg, as of 11/30/16. Past performance does not guarantee future results.

Japanese Profit Margins Near 20-Year High

TOPIX Profit Margins1996–2016

Source: Bloomberg, as of 11/30/16. Past performance does not guarantee future results.

Japanese Valuations Nearer to Historic Lows

TOPIX P/E Ratio2012–2016

-8%

-6%

-4%

-2%

0%

2%

4%

6%

1996 2001 2006 2011 2016

Profit Margin

10

15

20

25

30

35

2012 2013 2014 2015 2016

P/E Ratio

It’s Time to Go Long on Japanese Equity

2017 Long-Term Capital Market ExpectationsFor Financial Professional Use Only. Not For Public Distribution. 7

An improved growth outlook, high profit margins and

attractive valuations all support Japanese equity.”“

Source: Calculations by FT Solutions using data sourced from Bloomberg. See appendix on page 18 for representative indexes for each asset class. Opinions and beliefs expressed are those of FT Solutions and are subject to change without notice. There is no assurance that any forecast or projection will be realized.

7.5% 7.3%

8.1%

6.9% 6.8%

9.6%

8.3% 8.3%

0%

2%

4%

6%

8%

10%

12%

Developed-MarketEquity

United States Canada Europe ex UnitedKingdom

United Kingdom Japan Pacific ex Japan Australia

Expected Return

Among Developed-Market Equities, Japan Offers the Greatest Forward-Looking Opportunity

Comparison of Expected Annualized Returns of Various Developed-Market EquitiesAs of November 30, 2016

Projected Annualized Returns, January 1, 2017–December 31, 2023

yen reversed its appreciation trend.

Given the US rising rate cycle, we

expect there is room for additional

depreciation, which could be a further

boost for Japanese exports.

We believe private consumption is

another driver for potential growth

because of an increasing labor

shortage and subsequent potential

wage growth.

The profitability of Japanese firms is

very favorable. The profit margin of

the Tokyo Stock Price Index (TOPIX)

is at a 20-year high. At the same time,

valuations are attractive. The P/E

ratio is around 19, which is very low

compared to its own history.

2017 Long-Term Capital Market Expectations For Financial Professional Use Only. Not For Public Distribution.8

Public and private spending in US

infrastructure had already been

trending upward before the election.

Combined with strong interest in

revamping infrastructure on the part of

the new administration, we believe

this should bode well for investment

returns in this category.

On the public side, the Department of

Transportation’s FY 2017 budget

request is US$98.1 billion, up

significantly from the FY 2016 request

of US$72.4 billion (the enacted budget

ended up being US$76.0 billion). FY

2017 includes some major expansions

of the budget—extra spending

initiatives on pipeline safety, clean

energy transport, advanced

metropolitan planning, cybersecurity

US Infrastructure Will Benefit from the Coming Fiscal Stimulus

Source: Bloomberg, MSCI as of 11/30/16. Past performance does not guarantee future results.

Source: Bloomberg, MSCI, as of 11/30/16. Past performance does not guarantee future results.

Profit Margins for US Infrastructure Higher than Broad US Equities

Profit Margins: MSCI US Infrastructure vs. MSCI US Equity2012–2016

2012 2013 2014 2015 2016

10

12

14

16

18

20

22

US Infrastructure US Equity

P/E Ratio

0%

2%

4%

6%

8%

10%

12%

2012 2013 2014 2015 2016

MSCI US Infrastructure MSCI US Equity

Profit Margin

US Infrastructure Valuations Favorable Compared with Broad US Equities

P/E: MSCI US Infrastructure vs. MSCI US Equity2012–2016

2017 Long-Term Capital Market ExpectationsFor Financial Professional Use Only. Not For Public Distribution. 9

7. Source: US Department of Transportation, Transforming Communities in the 21st Century: Budget Highlights, Fiscal Year 2017.

and others.7 Election campaign

proposals included a US$1 trillion

dollar spending plan to update

infrastructure over the coming

decade. These plans will kick off new

projects and will require buy-in from

private financing, creating many

opportunities for investment in the

asset class.

While additional public expenditures

should boost infrastructure, on the

private side valuations and corporate

fundamentals also appear to bode

well for the asset class. Valuations

are looking more favorable for the

asset class than US equities, and

corporate profit margins are now

higher than broad US equities. (See

charts in this section.)

Infrastructure, as a real asset, also

demonstrates inflation-linked pricing

power. As we expect US inflation and

GDP to increase, we also expect

asset classes like US infrastructure to

protect against erosion in purchasing

power and to offer favorable risk-

adjusted returns compared to other

equity sectors less linked to the real

economy.

Infrastructure, as a real asset, demonstrates

inflation-linked pricing power.”

7.3%

7.9%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

US Equity US Infrastructure

Expected Return

Source: FT Solutions. See appendix on page 18 for representative indexes for each asset class. Opinions and beliefs expressed are those of FT Solutions and are subject to change without notice. There is no assurance that any forecast or projection will be realized.

We Expect Many Opportunities to Arise in US Infrastructure

Comparison of Expected Annualized Returns of US Equity vs. US InfrastructureAs of November 30, 2016

Projected Annualized Returns, January 1, 2017–December 31, 2023

“

2017 Long-Term Capital Market Expectations For Financial Professional Use Only. Not For Public Distribution.10

In spite of a brief improvement after the

US election, developed-market

government bond yields remain at very

low levels relative to the last 30 years—

largely as a result of QE and zero-

interest-rate policies around the world.

Given the improved growth outlook and

stabilized commodity prices, fears of

deflation appear to be diminishing:

Inflation is looming in the United States

and in the eurozone, and it is gradually

nearing the European Central Bank’s

2% target. We expect moderate

inflation to return and interest rates to

normalize in the next three to five

years. We believe the rising interest

rates will offset the already thin carry

benefit from yields.

We maintain our base-case expectation

of a gradual normalization of rates in

the United States. Although the pace of

rising rates in the United States might

be faster under Trump’s regime than

the market may otherwise have

expected, we think that given the

situation in Europe, Japan and China,

this is still a gradual shift. We live in a

more integrated world today than 30

years ago and the relative size of

different economies has changed. Even

if the new Republican regime can

deliver the expected stimulus, the

domestic policy changes in the United

States may not be as powerful as might

have occurred 30 years ago.

Overall, given the low starting yields,

our models suggest that the seven-year

expectations for developed-market

government bond returns are well

below what we’ve observed in history.

OUR STRONGEST CONVICTIONS “AGAINST”

Developed-Market Government Bonds: The Pain Shows No End

in Sight

0%

2%

4%

6%

8%

10%

12%

1984 1988 1992 1996 2000 2004 2008 2012 2016

World Government Bond Index

Yield to Maturity

Average since 1984

0.8%

1.5%

0.8%0.6%

0.9%

0.1%

2.4% 2.6%

5.6%5.8%

0%

1%

2%

3%

4%

5%

6%

7%

Expected Return

Developed Government Bonds Likely to Underperform

Comparison of Expected Annualized Returns of Developed Market

Bonds vs. Other Bond TypesAs of November 30, 2016

Projected Annualized Returns, January 1, 2017–December 31, 2023

Yields Remain at Historic Lows

World Government Bond Index Yield to Maturity1984–2016

Source: Calculations by FT Solutions using data sourced from Bloomberg. See appendix on page 18 for representative indexes for each asset class. Opinions and beliefs expressed are those of FT Solutions and are subject to change without notice. There is no assurance that any forecast or projection will be realized.

Source: Bloomberg, as of 11/30/16. Past performance does not guarantee future results.

2017 Long-Term Capital Market ExpectationsFor Financial Professional Use Only. Not For Public Distribution.

7.9%

2.5%

-8.7%

8.4%

-20.1%

19.6% 18.3%

33.2%

-20.5%

-30%

-20%

-10%

0%

10%

20%

30%

40%

GBP EUR AUD CAD NZD JPY NOK SEK CHF

Expected Change vs. USD

0%

-4%

2%

-1% -1%

-4%

2%

-1%

-9%-10%

-8%

-6%

-4%

-2%

0%

2%

4%

GBP EUR AUD CAD NZD JPY NOK SEK CHF

Expected Change vs. USD

11

All three components of the long-term

currency expectations model are

bearish for the Swiss franc (CHF),

including valuation, carry and real

interest-rate parity.

From a valuation perspective, the

Swiss franc continues to be the most

overvalued relative to other

developed-market currencies.

Conventional wisdom says that the

Swiss franc is a safe haven currency.

Recent uncertainties in Europe—the

debt crisis, the Greek bailout, Brexit

and populist uprisings across the

continent—have combined to rattle

confidence in the eurozone and drive

investors to perceived havens

including the Swiss franc. This

overbought environment has the

potential to reverse with the recent

sentiment shift and prospects of

global growth and reflation in the

United States and Europe.

Carry is the second component of the

model and takes into account the

difference in rates between two

respective countries. The theory is

that assets with higher yields tend to

appreciate relative to assets offering

lower yields. We expect policy in

Switzerland to remain

accommodative and the

government’s bond yield curve to

remain depressed relative to the US

yield curve. The Swiss franc is likely

to remain a funding currency relative

to the US dollar and other developed

currencies and therefore we expect

the CHF will likely weaken relative to

the USD.

The prospect of global reflation,

driven in part by the proposed policies

in the United States, may buoy yields

and inflation in the United States. The

IMF expects long-term inflation in

Switzerland to remain subdued,

further allowing the Swiss central

bank to maintain negative rates.

Swiss inflation is only expected to

reach 1% in 2021, substantially below

the central bank’s 2% target. This

inflation and policy difference will put

pressure on the Swiss franc versus

the US dollar. Real interest-rate parity

takes into account differences in

expected inflation between countries.

Because of the expected inflation

differential, this component of the

model forecasts depreciation of the

Swiss franc versus the US dollar in

the long term.

The Swiss franc continues to be the

most overvalued relative to other

developed-market currencies.”“

Short Swiss Franc vs. US Dollar

Source: Bloomberg, FT Solutions. Opinions and beliefs expressed are those of FT Solutions and are subject to change without notice. There is no assurance that any forecast or projection will be realized.

Thumbs Up Swedish Krona; Thumbs Down Swiss FrancLong-Term Expected Change vs. USD Based on Purchasing Power

Parity (PPP) ModelAs of November 30, 2016

Projected January 1, 2017–December 31, 2023

Long-Term Expected Change vs. USD Based on Real Interest-Rate

Parity ModelAs of November 30, 2016

Projected January 1, 2017–December 31, 2023

2017 Long-Term Capital Market Expectations For Financial Professional Use Only. Not For Public Distribution.12

OUR CAPITAL MARKET EXPECTATIONS

Expected Return Source: Franklin Templeton Solutions. Past performance does not guarantee future results. There is no assurance any forecast or projection will be realized. See appendix on page 18 for representative indexes for each asset class.

As of November 30, 2016

Seven-Year Annualized Return Capital Market Expectations (in Local

Terms), Projected January 1, 2017–December 31, 2023

*Data not available for full 20-year period. Returns calculated using data since inception of

the representative index, beginning 12/31/98.

Traditional Beta: Equity

Seven-Year Capital

Market Expectations

20-Year Annualized

Return

Global Equity 7.8% 6.8%

Developed-Market Equity 7.5% 6.8%

United States 7.3% 8.3%

Canada 8.1% 9.0%

Europe ex UK 6.9% 7.6%

United Kingdom 6.8% 6.4%

Japan 9.6% 1.1%

Pacific ex Japan 8.3% 5.4%

Australia 8.3% 8.6%

Specialty Equity

Global Natural Resources 8.3% 7.3%

Global Gold Miners 3.1% 0.1%

US Listed Infrastructure 7.9% 2.2%*

Global Real Estate Investment

Trusts (REITs)5.9% 9.8%

Seven-Year Capital

Market Expectations

20-Year Annualized

Return

Emerging-Market (EM) Equity 8.7% 8.9%

EM Europe, Middle East, Africa

(EMEA)8.3% 5.1%

EM Latin America 8.8% 12.1%

EM Asia 8.8% 3.5%

Global Small-Cap Equity 9.4% 7.9%

US Small Cap 9.2% 8.5%

As of November 30, 2016

Seven-Year Annualized Return Capital Market Expectations (in Local

Terms), Projected January 1, 2017–December 31, 2023

Traditional Beta: Fixed Income

Seven-Year Capital

Market Expectations

20-Year Annualized

Return

Global Developed-Market

Government0.3% 4.6%

US Government 1.3% 4.9%

Canadian Government 0.5% 5.7%

Europe ex UK Government 0.4% 4.7%

UK Government 0.1% 6.7%

Japanese Government -0.7% 2.6%

Australian Government 1.7% 6.6%

Global Corporate High Yield 4.0% 6.7%

US High-Yield USD 4.3% 7.2%

Pan-European EUR 2.4% 5.9%*

Pan-European GBP 3.9% 11.0%*

Seven-Year Capital

Market Expectations

20-Year Annualized

Return

Global Investment-Grade Credit 3.0% 5.1%

Issued in USD 2.7% 5.8%

Issued in GBP 2.1% 5.8%*

Issued in JPY 0.4% 1.1%*

Issued in EUR 1.7% 4.9%*

Issued in CAD 2.1% 5.7%*

Issued in AUD 3.3% 6.6%*

EM Debt Composite (36% Hard,

39% Local, 25% EM Corp)3.7% 8.6%

EM Debt–Government (Hard) 4.2% 10.1%

EM Debt–Government (Local) 6.3% 8.5%*

EM Corporate (Hard) 2.9% 6.6%*

Other Fixed Income

Inflation-Linked Bonds 0.7% 5.9%*

US Securitized 1.5% 5.2%

US Mortgage-Backed Securities 1.5% 5.2%

*Data not available for full 20-year period. Returns calculated using data since inception of

the representative index, beginning 1/31/99.

*Data not available for full 20-year period. Returns calculated using data since inception of the representative indexes: Global Corp IG Credit GBP beginning 12/31/99; Global Corp IG Credit JPY beginning 7/31/00; Global Corp IG Credit EUR beginning 7/31/98; Global Corp IG Credit CAD beginning 10/31/02; Global Corp IG Credit AUD beginning 6/30/04; EM Debt Government (Local) beginning 12/31/02; EM Debt Government (Hard) beginning 1/31/03; Inflation-Linked Bonds beginning 1/31/02.

2017 Long-Term Capital Market ExpectationsFor Financial Professional Use Only. Not For Public Distribution. 13

Expected Return Source: Franklin Templeton Solutions. Past performance does not guarantee future results. There is no assurance any forecast or projection will be realized. See appendix on page 18 for representative indexes for each asset class.

As of November 30, 2016

Seven-Year Annualized Return Capital Market Expectations (in USD),

Projected January 1, 2017–December 31, 2023

Traditional Beta: Commodities

Seven-Year Capital

Market Expectations

20-Year Annualized

Return

Commodities 4.0% 1.4%

Oil 6.2% 4.7%

Gold 1.1% 5.2%

Precious Metal 8.9% 5.5%

Agriculture 7.5% -1.4%

As of December 31, 2016

Seven-Year Forecasts Capital Market Expectations, December 31, 2023

Traditional Beta: Currency

Seven-Year Capital

Market Expectations

Spot

as of 12/31/16

FX Rate

USD CAD 1.34 1.34

EUR USD 1.01 1.05

GBP USD 1.25 1.23

USD JPY 114.69 116.96

AUD USD 0.73 0.72

As of November 30, 2016

Seven-Year Annualized Return Capital Market Expectations (in USD),

Projected January 1, 2017–December 31, 2023

Alternatives

As of November 30, 2016

Seven-Year Annualized Return Capital Market Expectations (in Local

Terms), Projected January 1, 2017–December 31, 2023

Economic

Seven-Year Capital

Market Expectations

Policy Rate

as of 12/31/16

Cash Expected Return

USD Cash 2.2% 0.5%

CAD Cash 2.1% 0.5%

EUR Cash 1.4% 0.0%

GBP Cash 1.9% 0.3%

JPY Cash 0.5% 0.1%

AUD Cash 2.8% 1.5%

*Risk premia strategy (and sub-strategy) historic composite returns are simulated based on third-party data we pull from Bloomberg and aggregate using a proprietary methodology. See “Risks of Assumptions for Risk Premia and Other Alternatives” on page 17 for important information about risk premia composite calculation methodology.

**US Private Equity return calculated through 6/30/16.

Seven-Year Capital

Market Expectations

20-Year Annualized

Return

Alternatives

FT Solutions Risk Premia

Composite*3.2% 7.6%

US Private Equity 9.3% 13.9%**

Hedge Fund 6.0% 7.5%

2017 Long-Term Capital Market Expectations For Financial Professional Use Only. Not For Public Distribution.14

This period coincides with the

average length of a US business

cycle, as defined by the National

Bureau of Economic Research. Since

1945, there have been 11 US

business cycles with an average

duration of 69.5 months. The

timeframe also historically

corresponds to the average duration

of aggregate fixed income indexes

that we use.

Our long-term return expectations are

driven by current valuations, analyst

expectations, expected growth rates

and expected economic

environments. We use inputs and

model techniques specific to each

asset class within a process that

blends quantitative analysis with

fundamental research. The process

includes using the residual income

model (a form of the dividend

discount model) as well as

regressions on economic scenarios

for equity expectations and stressing

the yield curve for fixed income

expectations.

We base our CMEs more on forward-

looking assumptions rather than a

long-term historical average return for

an asset class. Using forward-looking

returns is an important distinction

since past performance should not

necessarily be an indication of future

returns, especially in times of

changing macroeconomic

environments. We build our return

expectations using informed forward

estimates of fundamentals and

economic regimes over the next five

to 10 years rather than simply relying

on historical performance.

OUR METHODOLOGY AND MODELS

This section provides an overview of the methodology and models we use to develop

long-term capital market expectations (CMEs) for various asset classes, including equities,

fixed income, commodities and alternatives. In total our 2017 CMEs cover 66 asset

classes including 19 in equity, 25 in fixed income, seven in commodities, five within

currency and four in the alternative beta and alpha spaces. In terms of economic

expectations, we deliver six expectations of regional three-month cash returns.

Our CMEs are intended to provide annualized seven-year return expectations. However,

the time horizon can be generalized to the next five to 10 years, and we update our

models annually.

Our long-term

return

expectations

are driven by

current

valuations,

analyst

expectations,

expected

growth rates

and expected

economic

environments.”

“

2017 Long-Term Capital Market ExpectationsFor Financial Professional Use Only. Not For Public Distribution. 15

Risks of Assumptions for Equity Return ExpectationsThe residual income model relies on the theory that a company’s equity value is equal to the sum of its current book value and its expected future cash flows. Actual equity returns may deviate from the expected returns if the theory does not hold or if realized return on equity differs substantially from the analyst estimates used in the modeling. Unforeseen macroeconomic shocks (such as strong shocks to inflation or GDP) or major changes in the structure of the equity markets could also cause actual returns to differ from the expected returns. In addition, actual returns may deviate from expected returns if one or more of the forecast components comprising the building blocks model turn out to be different from actual dividend yields, EPS growth or P/E expansion.

Risks of Assumptions for Specialty Equity Return ExpectationsActual returns may differ from the expected returns for specialty equity if our forward-looking assumptions of the relationships between asset classes differ from reality.

We build our

return

expectations

using

informed

forward

estimates of

fundamentals

and economic

regimes over

the next five

to 10 years

rather than

simply relying

on historical

performance.”

“Traditional Equities

We use several models for our equity

return expectations. The benefit of

using several different models is that

we take into account both the

absolute and relative forecasts (as in

the residual income model). To

develop our 2017 CMEs within

traditional equities, we used the

“residual income” model and the

“building blocks” model.

Residual Income Model

The residual income model uses the

relationship between price-to-book

(P/B) ratios, historical return of equity

(ROE), and forward-looking (one-year

and two-year) ROE to determine

expected returns. A higher forward

ROE tends to contribute to a higher

return expectation. A lower P/B ratio

typically indicates a higher return

expectation. In addition, we found that

comparing expected returns relative

to their own histories provides

insightful information. The percentile

of current expected return in relation

to historical expectations indicates

major bullishness or bearishness

relative to history. Our analysis shows

that rank-adjusted results provide

strong guidance in forecasting

returns.

Building Blocks Model

The building blocks model forecasts

returns by summing three forecasts:

1. Dividend yield sourced from

Bloomberg analyst estimates

2. Earnings-per-share (EPS) growth

rates, which are the average of

bottom-up analyst forecasts from

the I/B/E/S and top-down long-

term GDP and inflation forecasts

3. P/E expansion, which assumes

that P/E will converge to its long-

term average.

Specialty Equities

To develop our expectations for

specialty equities, we use regression

models. The models identify relevant

equity and commodity factors that

drive the expected returns for each

asset class. Based on the historic

betas and alphas we construct

forward-looking views that determine

our expectations. We believe that

within the specialty equity category,

the returns in natural resources, gold

miners, listed infrastructure and real

estate investment trusts (REITs)

should be in line with traditional equity

indexes. With regard to gold miners,

we also consider the gold price to be

a factor in the model. For

infrastructure, oil prices are a relevant

explanatory factor. Therefore, main

inputs to our specialty equity long-

term return models is the relationship

between those factors and the asset

class indexes.

2017 Long-Term Capital Market Expectations For Financial Professional Use Only. Not For Public Distribution.16

Risks of Assumptions for Fixed Income Return ExpectationsActual fixed income returns may deviate from the expected returns if the actual shift in the yield curve over seven years deviates substantially from the types of shifts and stresses applied to the yield curve in the model. Unforeseen macroeconomic shocks or major changes in the market structure or term structure could also cause actual returns to differ from expected returns.

Risks of Assumptions for CommoditiesActual returns may differ from the expected returns if the spot return and roll yield deviate from realized values.

Risks of Assumptions for Currency ExpectationsLong-term currency expectations depend on the accuracy of the theories (purchasing power parity, interest-rate differential and real interest-rate parity) and on the long-term projections for yields and inflation rates. If reality deviates from the theory, or if realized yields and inflation rates differ significantly from the projections, we may see that actual currency rates differ from the expected rates.

Fixed Income

Yield Curve Shift Model

The main input to our fixed income

return expectation is our yield curve

shift (YCS) model. Principal

component analysis (PCA) of

historical data has shown that the

expected returns for bonds are mainly

driven by current yield level and

parallel shift scenarios. Given a

parallel shift scenario, the YCS model

assumes current yield curve will shift

gradually to the target over seven

years. The model also involves

stressing the yield curve on a monthly

basis using a random walk approach.

The results include expected returns

and the confidence intervals of the

expected returns for the fixed income

asset classes. Major inputs into the

model include:

1. Term structure (the shape of the

yield curve)

2. Yield volatilities

3. Market structures (weights for

different durations)

4. Expected shift scenarios

For corporate bonds and emerging-

market debt instruments, we assume

credit spreads will revert to their own

long-term averages over a seven-

year horizon. We estimate

corresponding default and recovery

rates based on the averages of their

long-term history.

Commodities

Spot Return and Roll Yield

We based our expected returns from

commodities on two sources: spot

return and roll yield. For spot return,

we apply an inflation-adjusted model

to forecast spot price. We first

calculate historical real commodity

prices given their historical inflation

rates, and forecast real commodity

price targets given the

macroeconomic outlook, then add

back the inflation expectation to get

the final target spot price. For roll

yield, we estimate historical roll yield

for each commodity and take the

long-term average for our forecasts.

Currency

We base our long-term foreign

exchange assumptions on equal-

weighting forecasts from three well-

documented theories: purchasing

power parity, interest-rate differential

and real interest-rate parity.

Purchasing Power Parity

Exchange rates should change to

create equilibrium ensuring that the

same set of goods will cost the same

if purchased with two different

currencies. Inputs include OECD

purchasing power parity and IMF

calculations.

Interest-Rate Differential

Currencies in countries with high

interest rates tend to appreciate

relative to currencies in countries with

lower interest rates. We use our own

forecast short-term cash rates for

given countries as inputs.

Real Interest-Rate Parity

Real interest-rate differential between

two countries drives the long-term

exchange rate between them. We use

our own forecasts for long-term

inflation for given countries.

2017 Long-Term Capital Market ExpectationsFor Financial Professional Use Only. Not For Public Distribution. 17

Risks of Assumptions for Risk Premia and Other AlternativesRisk premia strategy (and sub-strategy) historic composite returns are simulated based on third party data sourced from Bloomberg that we aggregate using a proprietary methodology. We divide the various strategies by type, rank them through a quantitative and qualitative process, and weight them by risk. Because these composites are determined based on our own assessments and calculations, these composites represent our own views and analysis and may vary from the methodologies and conclusions of others. Although we believe the composite data is accurate and reasonable, we cannot guarantee it, nor can we guarantee that implementation of any of the specific strategies would attain the performance or target of any composite mentioned in this paper. Actual performance of a specific strategy may differ substantially from the composite performance shown. All composite data is hypothetical and for illustrative purposes only. It does not represent the results of any actual portfolio or index. We created the composite data with the benefit of hindsight and knowledge of factors that could have positively affected the results. We have presented all composite and index data gross of fees and expenses. Fees and expenses would lower a managed portfolio’s returns.

Actual returns may differ from the expected returns if our efficiency assumptions or multi-factor models deviate from reality. For example, we have assumed a decreasing Sharpe ratio trend over the long term. Actual returns may not match expected returns if the Sharpe ratio instead increases or remains constant over the next seven years.

Risks of Assumptions for Economic ForecastsThe forward cash rate may deviate from the expected cash rate if the yield curve deviates substantially from the one that we applied in the model. Unforeseen macroeconomic shocks, changing government policies or major changes in the term structure would also cause the actual cash rate to differ from the expected cash rate.

Alternatives

We base our long-term forecasts for

alternatives on efficiency and

illiquidity premium assumptions. We

consider the historical trend of the

Sharpe ratio on risk premia and

hedge funds. We base all historical

data related to the risk premia

strategies on data from third parties

and do not represent the actual

performance of any portfolio or index.

Using the forward-looking Sharpe

ratio, cash rate and historical risk, we

construct our long-term risk premia

return expectations.

To determine our expectation for

private equity, we assumed an

illiquidity premium of 200 basis points,

which is generally in line with the

average of a sample of institutional

private market forecast assumptions.

For our hedge fund return

expectation, we combined our

efficiency assumption and multi-factor

models to forecast long run returns

that determine a seven-year CME for

hedge funds.

Economic Forecasts

We collected GDP and inflation rates

from multiple sources, including the

World Bank, OECD, IMF and other

third parties. Our portfolio managers

also make their own forecasts. Our

final forecasts comprise all the

external and internal forecasts. To

determine the short-term (three-

month) cash rate, we build out a

forward rate model and use the

Taylor rule based cash forecast

model. We include the current

government bond yield curve, current

inflation and GDP, long-term GDP

and inflation expectations as inputs.

2017 Long-Term Capital Market Expectations For Financial Professional Use Only. Not For Public Distribution.18

APPENDIX: INDEXES AND PROXIES USED

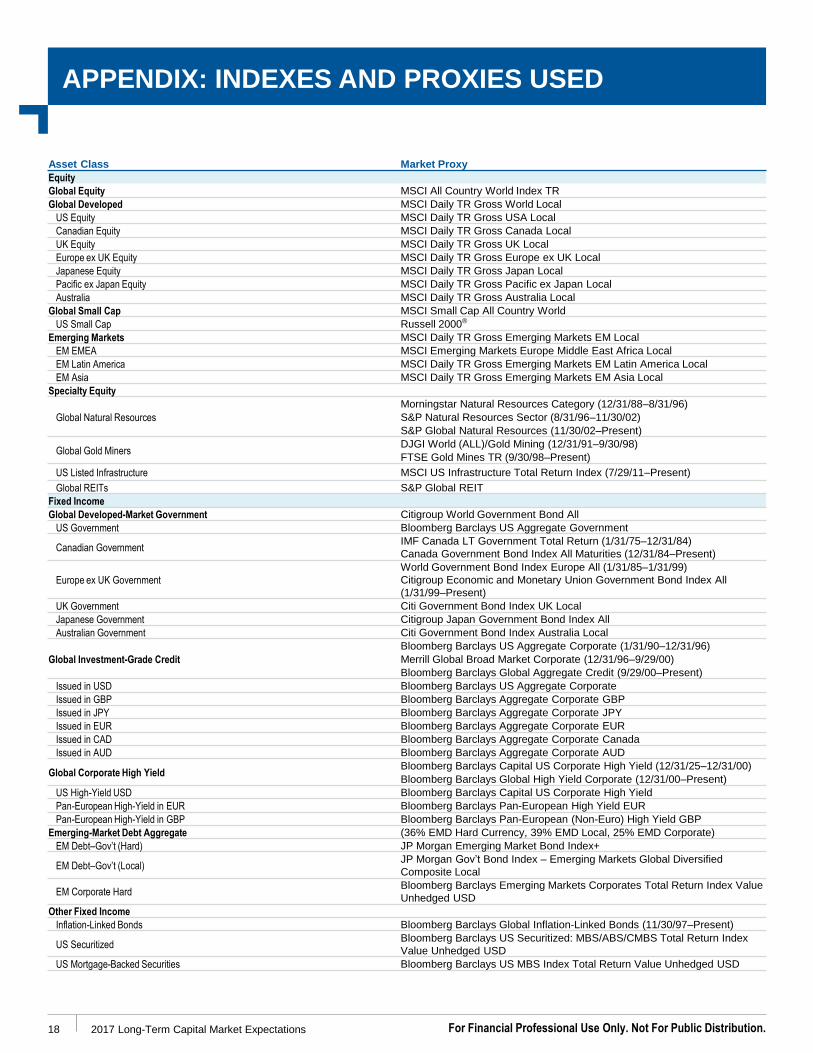

Asset Class Market Proxy

Equity

Global Equity MSCI All Country World Index TR

Global Developed MSCI Daily TR Gross World Local

US Equity MSCI Daily TR Gross USA Local

Canadian Equity MSCI Daily TR Gross Canada Local

UK Equity MSCI Daily TR Gross UK Local

Europe ex UK Equity MSCI Daily TR Gross Europe ex UK Local

Japanese Equity MSCI Daily TR Gross Japan Local

Pacific ex Japan Equity MSCI Daily TR Gross Pacific ex Japan Local

Australia MSCI Daily TR Gross Australia Local

Global Small Cap MSCI Small Cap All Country World

US Small Cap Russell 2000®

Emerging Markets MSCI Daily TR Gross Emerging Markets EM Local

EM EMEA MSCI Emerging Markets Europe Middle East Africa Local

EM Latin America MSCI Daily TR Gross Emerging Markets EM Latin America Local

EM Asia MSCI Daily TR Gross Emerging Markets EM Asia Local

Specialty Equity

Global Natural Resources

Morningstar Natural Resources Category (12/31/88–8/31/96)

S&P Natural Resources Sector (8/31/96–11/30/02)

S&P Global Natural Resources (11/30/02–Present)

Global Gold MinersDJGI World (ALL)/Gold Mining (12/31/91–9/30/98)

FTSE Gold Mines TR (9/30/98–Present)

US Listed Infrastructure MSCI US Infrastructure Total Return Index (7/29/11–Present)

Global REITs S&P Global REIT

Fixed Income

Global Developed-Market Government Citigroup World Government Bond All

US Government Bloomberg Barclays US Aggregate Government

Canadian GovernmentIMF Canada LT Government Total Return (1/31/75–12/31/84)

Canada Government Bond Index All Maturities (12/31/84–Present)

Europe ex UK Government

World Government Bond Index Europe All (1/31/85–1/31/99)

Citigroup Economic and Monetary Union Government Bond Index All

(1/31/99–Present)

UK Government Citi Government Bond Index UK Local

Japanese Government Citigroup Japan Government Bond Index All

Australian Government Citi Government Bond Index Australia Local

Global Investment-Grade Credit

Bloomberg Barclays US Aggregate Corporate (1/31/90–12/31/96)

Merrill Global Broad Market Corporate (12/31/96–9/29/00)

Bloomberg Barclays Global Aggregate Credit (9/29/00–Present)

Issued in USD Bloomberg Barclays US Aggregate Corporate

Issued in GBP Bloomberg Barclays Aggregate Corporate GBP

Issued in JPY Bloomberg Barclays Aggregate Corporate JPY

Issued in EUR Bloomberg Barclays Aggregate Corporate EUR

Issued in CAD Bloomberg Barclays Aggregate Corporate Canada

Issued in AUD Bloomberg Barclays Aggregate Corporate AUD

Global Corporate High YieldBloomberg Barclays Capital US Corporate High Yield (12/31/25–12/31/00)

Bloomberg Barclays Global High Yield Corporate (12/31/00–Present)

US High-Yield USD Bloomberg Barclays Capital US Corporate High Yield

Pan-European High-Yield in EUR Bloomberg Barclays Pan-European High Yield EUR

Pan-European High-Yield in GBP Bloomberg Barclays Pan-European (Non-Euro) High Yield GBP

Emerging-Market Debt Aggregate (36% EMD Hard Currency, 39% EMD Local, 25% EMD Corporate)

EM Debt–Gov’t (Hard) JP Morgan Emerging Market Bond Index+

EM Debt–Gov’t (Local)JP Morgan Gov’t Bond Index – Emerging Markets Global Diversified

Composite Local

EM Corporate HardBloomberg Barclays Emerging Markets Corporates Total Return Index Value

Unhedged USD

Other Fixed Income

Inflation-Linked Bonds Bloomberg Barclays Global Inflation-Linked Bonds (11/30/97–Present)

US SecuritizedBloomberg Barclays US Securitized: MBS/ABS/CMBS Total Return Index

Value Unhedged USD

US Mortgage-Backed Securities Bloomberg Barclays US MBS Index Total Return Value Unhedged USD

2017 Long-Term Capital Market ExpectationsFor Financial Professional Use Only. Not For Public Distribution. 19

*Risk premia strategy (and sub-strategy) historic composite returns are simulated based on third-party data we source from Bloomberg and aggregate using a proprietary methodology. See “Risks of Assumptions for Risk Premia and Other Alternatives” on page 17 for important information about risk premia composite calculation methodology.

MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

Important data provider notices and terms available at www.franklintempletondatasources.com.

Asset Class Market Proxy

Fixed Income (cont’d.)

Commodities

Oil (57% WTI + 43% Brent Oil)

Precious MetalGSCI Precious Metals Total Return (1/31/73–1/31/91)

Bloomberg Precious Metals Sub-Index Total Return (2/1/91–Present)

GoldS&P GSCI Gold Index (2/28/78–1/31/91)

Bloomberg Gold Sub-Index Total Return (2/1/91–Present)

Agriculture Bloomberg Agriculture Sub-Index Total Return

Alternatives

US Private EquityFT Solutions Proprietary Monthly Adjusted – Cambridge Associates

US Private Equity Index (1/31/86–6/30/16)

Risk Premia*

HFRI Fund of Fund Composite (12/31/89–11/30/97)

HFRX Global Hedge Fund Index (12/31/97–12/31/09)

FTS Systematic Beta Enhanced Composite (1/29/10–Present)

Hedge Fund HFRI Fund Weighted Composite Index

Cash

USD Encorr 90-Day T-Bill (12/31/74–1/31/97)

JPM Cash Index USD 3-Month (1/31/97–Present)

CAD Canada DEX 90-Day Bill (1/31/75–1/97)

JPM CAD Cash Index 3-Month (2/97–Present)

EUR

IMF Germany Deposit Rate (De-Annualized) (to 12/31/95)

Germany Cash Indexes – Libor Return 3-Month (1/31/96–1/31/99)

JPM Cash Index Euro Currency 3-Month (2/28/99–Present)

GBP JPM Cash Index GBP 3-Month

JPY JPM Cash Index JPY 3-Month

AUD Bloomberg AusBond Bank Index (3/31/87–1/31/97)

JP Morgan 3-Month AUD Cash Index (1/31/97–Present)

2017 Long-Term Capital Market Expectations For Financial Professional Use Only. Not For Public Distribution.20

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of

principal.

Stock prices fluctuate, sometimes rapidly and dramatically,

due to factors affecting individual companies, particular

industries or sectors, or general market conditions. Bond

prices generally move in the opposite direction of interest

rates. Thus, as the prices of bonds in an investment

portfolio adjust to a rise in interest rates, the value of the

portfolio may decline. Special risks are associated with

foreign investing, including currency fluctuations, economic

instability and political developments. Investments in

developing markets involve heightened risks related to the

same factors, in addition to those associated with their

relatively small size, lesser liquidity and lack of established

legal, political, business, and social frameworks to support

securities markets. Such investments could experience

significant price volatility in any given year. Derivatives,

including currency management strategies, involve costs

and can create economic leverage in a portfolio, which

may result in significant volatility and cause the portfolio to

participate in losses (as well as enable gains) on an

amount that exceeds the portfolio’s initial investment.

Because some risk premia strategy signals are built using

historical market events, the risk premia strategies can be

subject to model risk, whereby the strategies perform

differently than the model would expect for various

reasons, including but not limited to market and economic

conditions. In other words, the future performance and

correlations of risk premia strategies may differ, potentially

significantly, from historical performance and correlations.

In addition, because the risk premia composites in this

paper are determined based on FT Solutions’ own

assessments and calculations, these composites represent

solely the views and analyses of FT Solutions and may

vary from the methodologies and conclusions of others.

Although FT Solutions believes that the composite data is

accurate and reasonable, there is no guarantee of such,

that implementation of any of the specific strategies would

attain the performance, or target of any composite

mentioned in this paper. Actual performance of a specific

strategy may differ substantially from the composite

performance shown.

Investing in the natural resources sector involves special

risks, including increased susceptibility to adverse

economic and regulatory developments affecting the

sector—prices of such securities can be volatile,

particularly over the short term. Some strategies, such as

hedge fund and private equity strategies, are available only

to pre-qualified investors, may be speculative and involve a

high degree of risk. An investor could lose all or a

substantial amount of his or her investment in such

strategies. Real estate securities involve special risks,

such as declines in the value of real estate and increased

susceptibility to adverse economic or regulatory

developments affecting the sector.

2017 Long-Term Capital Market ExpectationsFor Financial Professional Use Only. Not For Public Distribution. 21

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should

not be construed as individual investment advice or a

recommendation or solicitation to buy, sell or hold any security or

to adopt any investment strategy. It does not constitute legal or

tax advice.

The views expressed are those of the investment manager and

the comments, opinions and analyses are rendered as of

publication date and may change without notice. The information

provided in this material is not intended as a complete analysis of

every material fact regarding any country, region or market. All

investments involve risks, including possible loss of

principal.

Data from third party sources may have been used in the

preparation of this material and Franklin Templeton Investments

(“FTI”) has not independently verified, validated or audited such

data. FTI accepts no liability whatsoever for any loss arising from

use of this information and reliance upon the comments opinions

and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all

jurisdictions and are offered outside the U.S. by other FTI

affiliates and/or their distributors as local laws and regulation

permits. Please consult your own professional adviser for further

information on availability of products and services in your

jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One

Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL

BEN/342-5236, franklintempleton.com - Franklin Templeton

Distributors, Inc. is the principal distributor of Franklin Templeton

Investments’ U.S. registered products, which are available only in

jurisdictions where an offer or solicitation of such products is

permitted under applicable laws and regulation.

Australia: Issued by Franklin Templeton Investments Australia Limited

(ABN 87 006 972 247) (Australian Financial Services License Holder No.

225328), Level 19, 101 Collins Street, Melbourne, Victoria, 3000.

Austria/Germany: Issued by Franklin Templeton Investment Services

GmbH, Mainzer Landstraße 16, D-60325 Frankfurt am Main, Germany.

Authorized in Germany by IHK Frankfurt M., Reg. no. D-F-125-TMX1-08.

Canada: Issued by Franklin Templeton Investments Corp., 5000 Yonge

Street, Suite 900 Toronto, ON, M2N 0A7, Fax: (416) 364-1163, (800)

387-0830, www.franklintempleton.ca. In Canada, FT Solutions is part of

Fiduciary Trust Company of Canada, a wholly owned subsidiary of

Franklin Templeton Investments Corp. Dubai: Issued by Franklin

Templeton Investments (ME) Limited, authorized and regulated by the

Dubai Financial Services Authority. Dubai office: Franklin Templeton

Investments, The Gate, East Wing, Level 2, Dubai International Financial

Centre, P.O. Box 506613, Dubai, U.A.E., Tel.: +9714-4284100

Fax:+9714-4284140. France: Issued by Franklin Templeton France S.A.,

20 rue de la Paix, 75002 Paris, France. Hong Kong: Issued by Franklin

Templeton Investments (Asia) Limited, 17/F, Chater House, 8 Connaught

Road Central, Hong Kong. Italy: Issued by Franklin Templeton

International Services S.à.r.l. – Italian Branch, Corso Italia, 1 – Milan,

20122, Italy. Japan: Issued by Franklin Templeton Investments Japan

Limited. Korea: Issued by Franklin Templeton Investment Trust

Management Co., Ltd., 3rd fl., CCMM Building, 12 Youido-Dong,

Youngdungpo-Gu, Seoul, Korea 150-968. Luxembourg/Benelux: Issued

by Franklin Templeton International Services S.à r.l. – Supervised by the

Commission de Surveillance du Secteur Financier - 8A, rue Albert

Borschette, L-1246 Luxembourg - Tel: +352-46 66 67-1 - Fax: +352-46 66

76. Malaysia: Issued by Franklin Templeton Asset Management

(Malaysia) Sdn. Bhd. & Franklin Templeton GSC Asset Management Sdn.

Bhd. Poland: Issued by Templeton Asset Management (Poland) TFI S.A.,

Rondo ONZ 1; 00-124 Warsaw. Romania: Issued by the Bucharest

branch of Franklin Templeton Investment Management Limited, 78-80

Buzesti Street, Premium Point, 7th-8th Floor, 011017 Bucharest 1,

Romania. Registered with Romania Financial Supervisory Authority under

no. PJM01SFIM/400005/14.09.2009, authorized and regulated in the UK

by the Financial Conduct Authority. Singapore: Issued by Templeton

Asset Management Ltd. Registration No. (UEN) 199205211E. 7 Temasek

Boulevard, #38-03 Suntec Tower One, 038987, Singapore. Spain: Issued

by the branch of Franklin Templeton Investment Management,

Professional of the Financial Sector under the Supervision of CNMV, José

Ortega y Gasset 29, Madrid. South Africa: Issued by Franklin Templeton

Investments SA (PTY) Ltd which is an authorised Financial Services

Provider. Tel: +27 (21) 831 7400 Fax: +27 (21) 831 7422. Switzerland:

Issued by Franklin Templeton Switzerland Ltd, Stockerstrasse 38, CH-

8002 Zurich. UK: Issued by Franklin Templeton Investment Management

Limited (FTIML), registered office: Cannon Place, 78 Cannon Street,

London EC4N 6HL. Authorized and regulated in the United Kingdom by

the Financial Conduct Authority. Nordic regions: Issued by Franklin

Templeton Investment Management Limited (FTIML), Swedish Branch,

Blasieholmsgatan 5, SE-111 48 Stockholm, Sweden. Phone: +46 (0) 8

545 01230, Fax: +46 (0) 8 545 01239. FTIML is authorised and regulated

in the United Kingdom by the Financial Conduct Authority and is

authorized to conduct certain investment services in Denmark, in

Sweden, in Norway and in Finland. Offshore Americas: In the U.S., this

publication is made available only to financial intermediaries by

Templeton/Franklin Investment Services, 100 Fountain Parkway, St.

Petersburg, Florida 33716. Tel: (800) 239-3894 (USA Toll-Free), (877)

389-0076 (Canada Toll-Free), and Fax: (727) 299-8736. Investments are

not FDIC insured; may lose value; and are not bank guaranteed.

Distribution outside the U.S. may be made by Templeton Global Advisors

Limited or other sub-distributors, intermediaries, dealers or professional

investors that have been engaged by Templeton Global Advisors Limited

to distribute shares of Franklin Templeton funds in certain jurisdictions.

This is not an offer to sell or a solicitation of an offer to purchase

securities in any jurisdiction where it would be illegal to do so.

Franklin Templeton Distributors, Inc.

One Franklin Parkway

San Mateo, CA 94403-1906

(800) DIAL BEN® / 342-5236

franklintempleton.com

Copyright © 2017 Franklin Templeton Investments. All rights reserved. CME_PERWP_0217