2016 whistler institutional investor conference

TRANSCRIPT

2016 Whistler Institutional Investor ConferenceJanuary 21, 2016

Forward Looking Information

Both these slides and the accompanying oral presentations contain certain forward-looking statements within the meaning of the United States PrivateSecurities Litigation Reform Act of 1995 and forward-looking information within the meaning of the Securities Act (Ontario). Forward-looking statementsinvolve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Teck to bematerially different from any future results, performance or achievements expressed or implied by the forward-looking statements. These forward-lookingstatements include statements relating to the long-life our assets, estimated profit and estimated EBITDA, our expectation regarding market supply anddemand in the commodities we produce, our statement that we are in a strong financial position, our expected year-end cash balance, 2016 totalspending reduction expectations, capital and operating cost savings, our level of liquidity, statements regarding our credit rating, the availability of orcredit facilities and other sources of liquidity, reserve and resource life estimates, 2015 production and cost guidance, 2015 capital expenditure guidance,our statements that we have a strong growth pipeline, potential benefits of LNG use in haul trucks, all projections for Project Corridor, statementsregarding the production and economic expectations for the Fort Hills project, including but not limited to operating and sustaining cost projections,sustaining capital projection, free cash flow projections, estimated netback, operating margin, Alberta oil royalty, net margin, Teck’s share of go-forwardcapex, mine life, Fort Hills capital cost projections, transportation capacity and our ability to secure transport for our Fort Hills production, andmanagement’s expectations with respect to production, demand and outlook in the markets for coal, copper, zinc and energy.

These forward-looking statements involve numerous assumptions, risks and uncertainties and actual results may vary materially, which are described inTeck’s public filings available on SEDAR (www.sedar.com) and EDGAR (www.sec.gov). In addition, the forward-looking statements in these slides andaccompanying oral presentation are also based on assumptions, including, but not limited to, regarding general business and economic conditions, thesupply and demand for, deliveries of, and the level and volatility of prices of, zinc, copper and coal and other primary metals and minerals as well as oil,and related products, the timing of the receipt of regulatory and governmental approvals for our development projects and other operations, our costs ofproduction and production and productivity levels, as well as those of our competitors, power prices, continuing availability of water and power resourcesfor our operations, market competition, the accuracy of our reserve estimates (including with respect to size, grade and recoverability) and the geological,operational and price assumptions on which these are based, conditions in financial markets, the future financial performance of the company, our abilityto attract and retain skilled staff, our ability to procure equipment and operating supplies, positive results from the studies on our expansion projects, ourcoal and other product inventories, our ability to secure adequate transportation for our products, our ability to obtain permits for our operations andexpansions, our ongoing relations with our employees and business partners and joint venturers. Management’s expectations of mine life are based onthe current planned production rates and assume that all resources described in this presentation are developed. Certain forward-looking statements arebased on assumptions regarding the price for Fort Hills product and the expenses for the project, as disclosed in the slides. Assumptions regardingliquidity are based on the assumption that Teck’s current credit facilities remain fully available. Assumptions regarding our liquidity are also based oncurrent foreign exchange rates and assume that Teck’s 2015 guidance for production, costs and capital expenditures are met. Assumptions regardingFort Hills also include the assumption that project development and funding proceed as planned. Assumptions regarding our potential reserve andresource life assume that all resources are upgraded to reserves and that all reserves and resources could be mined. The foregoing list of assumptionsis not exhaustive. Assumptions regarding the Corridor project include that the transaction closes as planned and that the project is built and operated inaccordance with the conceptual preliminary design from a preliminary economic assessment.

2

Forward Looking Information

Factors that may cause actual results to vary materially include, but are not limited to, changes in commodity and power prices, changes in marketdemand for our products, changes in interest and currency exchange rates, acts of foreign governments and the outcome of legal proceedings,inaccurate geological and metallurgical assumptions (including with respect to the size, grade and recoverability of mineral reserves and resources),unanticipated operational difficulties (including failure of plant, equipment or processes to operate in accordance with specifications or expectations, costescalation, unavailability of materials and equipment, government action or delays in the receipt of government approvals, industrial disturbances orother job action, adverse weather conditions and unanticipated events related to health, safety and environmental matters), union labour disputes,political risk, social unrest, failure of customers or counterparties to perform their contractual obligations, changes in our credit ratings, unanticipatedincreases in costs to construct our development projects, difficulty in obtaining permits, inability to address concerns regarding permits of environmentalimpact assessments, and changes or further deterioration in general economic conditions. We will not achieve the maximum mine lives of our projects,or be able to mine all reserves at our projects, if we do not obtain relevant permits for our operations. Our Fort Hills project is not controlled by us andconstruction and production schedules may be adjusted by our partners. The Corridor project will be jointly owned. The effect of the price of oil onoperating costs will be affected by the exchange rate between Canadian and U.S. dollars.

Statements concerning future production costs or volumes are based on numerous assumptions of management regarding operating matters and onassumptions that demand for products develops as anticipated, that customers and other counterparties perform their contractual obligations, thatoperating and capital plans will not be disrupted by issues such as mechanical failure, unavailability of parts and supplies, labour disturbances,interruption in transportation or utilities, adverse weather conditions, and that there are no material unanticipated variations in the cost of energy orsupplies.

We assume no obligation to update forward-looking statements except as required under securities laws. Further information concerning assumptions,risks and uncertainties associated with these forward-looking statements and our business can be found in our Annual Information Form for the yearended December 31, 2014, filed under our profile on SEDAR (www.sedar.com) and on EDGAR (www.sec.gov) under cover of Form 40-F.

3

Agenda

Teck Overview & Strategy

Commodity Market Observations

Teck Update

4

Long-Term Strategy

Diversification to expand opportunity set

Long life assets

Low half of the cost curve

Appropriate scale

Low risk jurisdictions

5

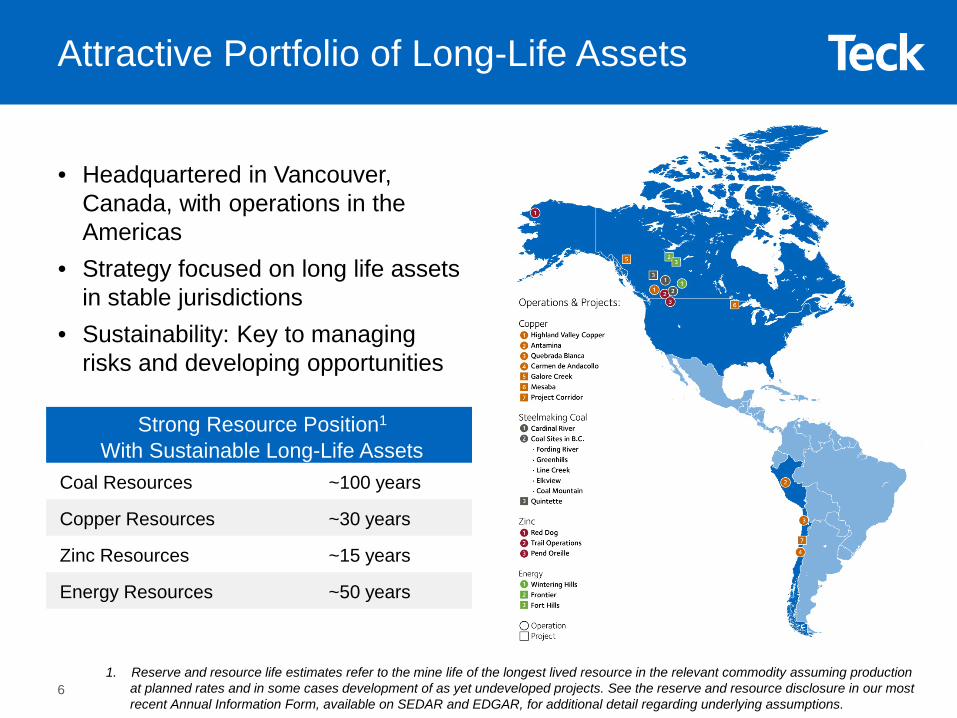

• Headquartered in Vancouver, Canada, with operations in the Americas

• Strategy focused on long life assets in stable jurisdictions

• Sustainability: Key to managing risks and developing opportunities

Strong Resource Position1

With Sustainable Long-Life AssetsCoal Resources ~100 years

Copper Resources ~30 years

Zinc Resources ~15 years

Energy Resources ~50 years

Attractive Portfolio of Long-Life Assets

1. Reserve and resource life estimates refer to the mine life of the longest lived resource in the relevant commodity assuming production at planned rates and in some cases development of as yet undeveloped projects. See the reserve and resource disclosure in our most recent Annual Information Form, available on SEDAR and EDGAR, for additional detail regarding underlying assumptions.

6

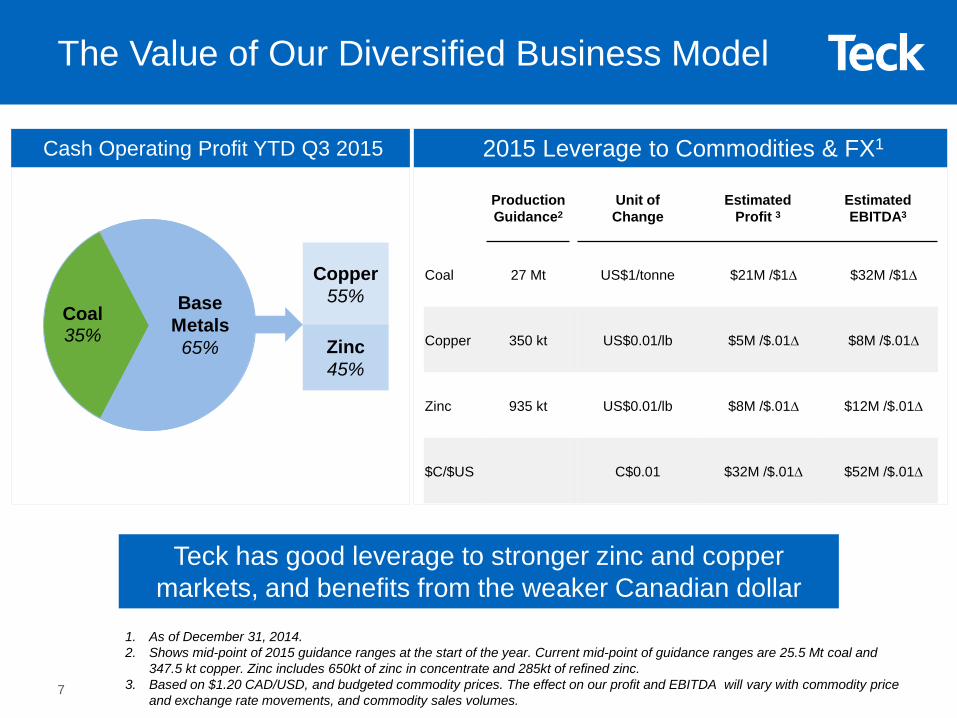

Coal35%

Copper 55%

Zinc45%

Teck has good leverage to stronger zinc and copper markets, and benefits from the weaker Canadian dollar

The Value of Our Diversified Business Model

Cash Operating Profit YTD Q3 2015

Production Guidance2

Unit of Change

Estimated Profit 3

EstimatedEBITDA3

Coal 27 Mt US$1/tonne $21M /$1∆ $32M /$1∆

Copper 350 kt US$0.01/lb $5M /$.01∆ $8M /$.01∆

Zinc 935 kt US$0.01/lb $8M /$.01∆ $12M /$.01∆

$C/$US C$0.01 $32M /$.01∆ $52M /$.01∆

2015 Leverage to Commodities & FX1

1. As of December 31, 2014.2. Shows mid-point of 2015 guidance ranges at the start of the year. Current mid-point of guidance ranges are 25.5 Mt coal and

347.5 kt copper. Zinc includes 650kt of zinc in concentrate and 285kt of refined zinc.3. Based on $1.20 CAD/USD, and budgeted commodity prices. The effect on our profit and EBITDA will vary with commodity price

and exchange rate movements, and commodity sales volumes.

Base Metals

65%

7

Agenda

Teck Overview & Strategy

Commodity Market Observations

Teck Update

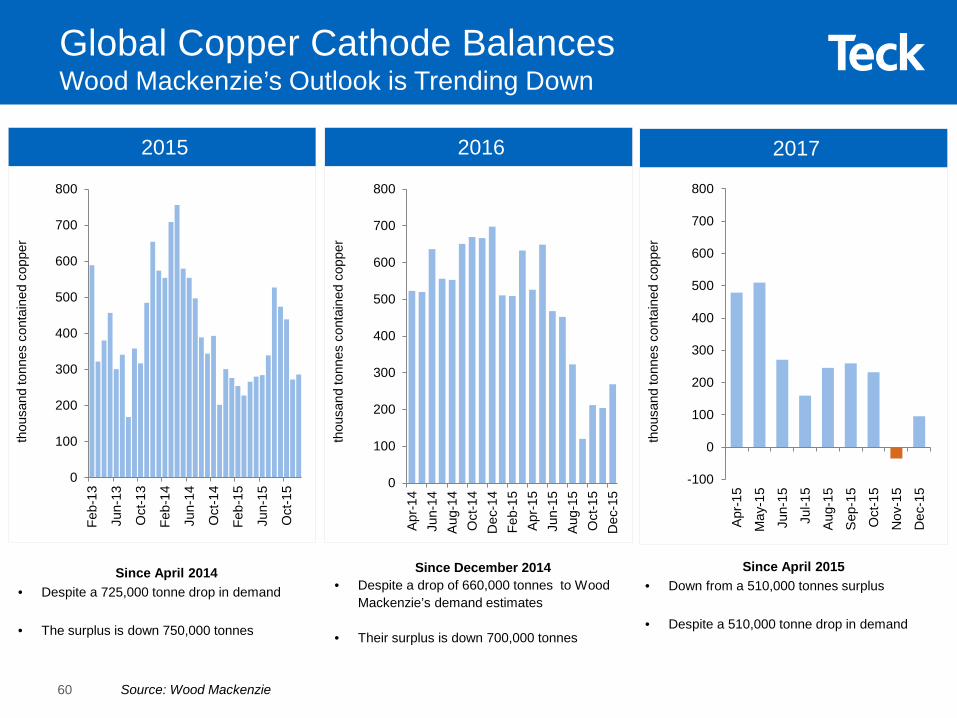

8

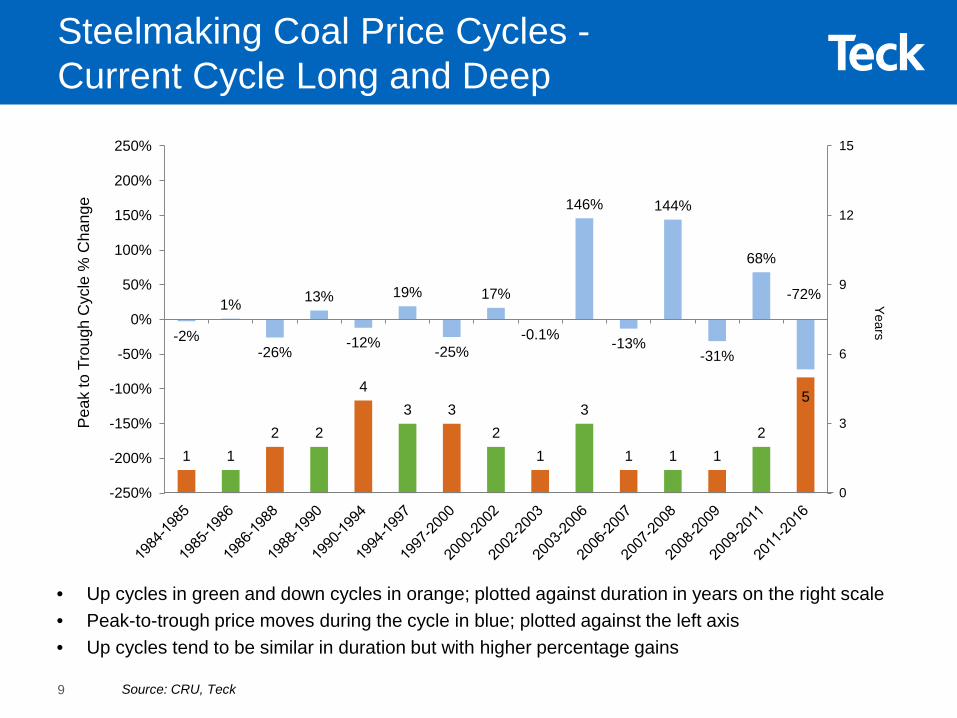

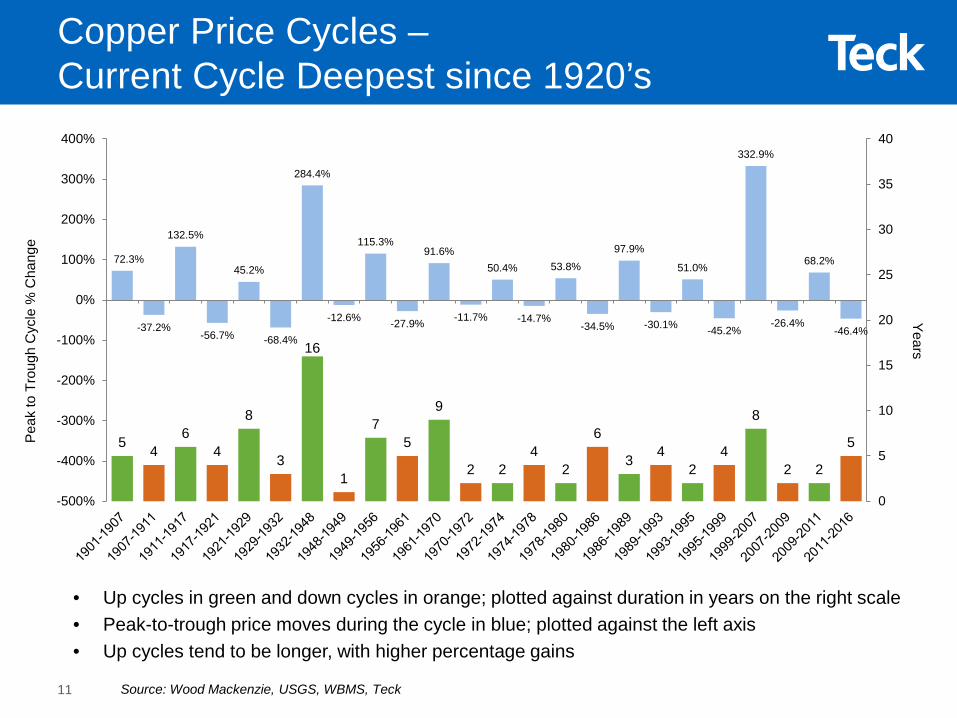

• Up cycles in green and down cycles in orange; plotted against duration in years on the right scale• Peak-to-trough price moves during the cycle in blue; plotted against the left axis• Up cycles tend to be similar in duration but with higher percentage gains

Source: CRU, Teck

Steelmaking Coal Price Cycles -Current Cycle Long and Deep

-2%

1%

-26%

13%

-12%

19%

-25%

17%

-0.1%

146%

-13%

144%

-31%

68%

-72%

1 12 2

43 3

21

3

1 1 12

5

0

3

6

9

12

15

-250%

-200%

-150%

-100%

-50%

0%

50%

100%

150%

200%

250%

Pea

k to

Tro

ugh

Cyc

le %

Cha

nge

Years

9

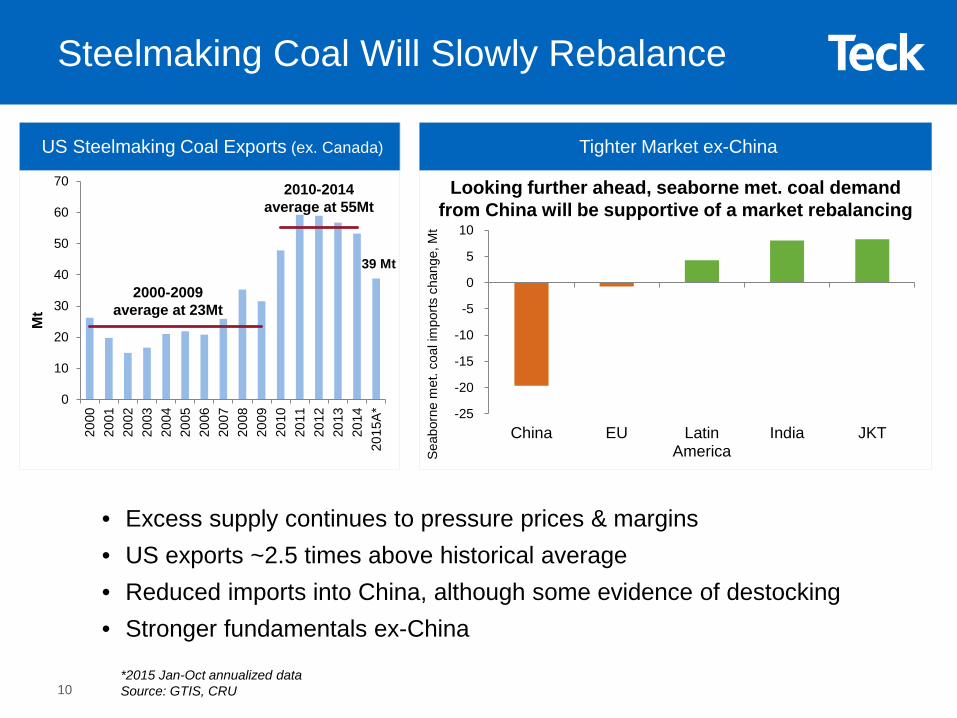

Steelmaking Coal Will Slowly Rebalance

• Excess supply continues to pressure prices & margins• US exports ~2.5 times above historical average• Reduced imports into China, although some evidence of destocking• Stronger fundamentals ex-China

Tighter Market ex-ChinaUS Steelmaking Coal Exports (ex. Canada)

*2015 Jan-Oct annualized data Source: GTIS, CRU

-25

-20

-15

-10

-5

0

5

10

China EU LatinAmerica

India JKTSe

abor

nem

et. c

oal i

mpo

rts c

hang

e, M

t

Looking further ahead, seaborne met. coal demand from China will be supportive of a market rebalancing

39 Mt

0

10

20

30

40

50

60

70

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

A*

Mt

2000-2009average at 23Mt

2010-2014average at 55Mt

10

• Up cycles in green and down cycles in orange; plotted against duration in years on the right scale• Peak-to-trough price moves during the cycle in blue; plotted against the left axis• Up cycles tend to be longer, with higher percentage gains

Copper Price Cycles –Current Cycle Deepest since 1920’s

72.3%

-37.2%

132.5%

-56.7%

45.2%

-68.4%

284.4%

-12.6%

115.3%

-27.9%

91.6%

-11.7%

50.4%

-14.7%

53.8%

-34.5%

97.9%

-30.1%

51.0%

-45.2%

332.9%

-26.4%

68.2%

-46.4%

5 46

4

8

3

16

1

75

9

2 24

2

6

3 42

4

8

2 2

5

0

5

10

15

20

25

30

35

40

-500%

-400%

-300%

-200%

-100%

0%

100%

200%

300%

400%

YearsP

eak

to T

roug

h C

ycle

% C

hang

e

Source: Wood Mackenzie, USGS, WBMS, Teck11

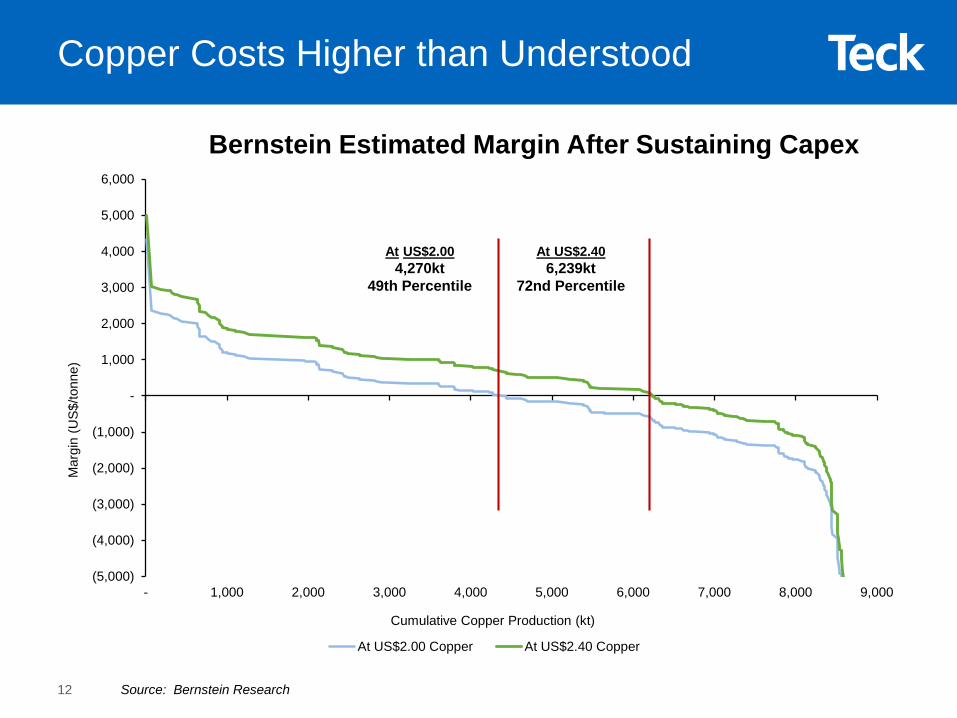

Copper Costs Higher than Understood

Source: Bernstein Research

Bernstein Estimated Margin After Sustaining Capex

(5,000)

(4,000)

(3,000)

(2,000)

(1,000)

-

1,000

2,000

3,000

4,000

5,000

6,000

- 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000

Mar

gin

(US$

/tonn

e)

Cumulative Copper Production (kt)

At US$2.00 Copper At US$2.40 Copper

At US$2.40 6,239kt

72nd Percentile

At US$2.004,270kt

49th Percentile

12

• Up cycles in green and down cycles in orange; plotted against duration in years on the right scale• Peak-to-trough price moves during the cycle in blue; plotted against the left axis• Up cycles tend to be longer, with higher percentage gains

Zinc Price Cycles –Current Cycle Longest Since 1920’s

YearsP

eak

to T

roug

h C

ycle

% C

hang

e

Source: Wood Mackenzie, USGS, WBMS, Teck

50%

-25%

50%

-26%

168%

-49%

12%

-40%

42%

-10%

8%

-55%

125%

-29%

193%

-10%

48%

-41%

26%

-24%

26%

-11%

25%

-7%

188%

-20%

44%

-14%

26%

-22%

116%

-36%

11%

-21%

21%

-8%

26%

-20%

9%

-31%

311%

-51%

36%

-32%

5

2

4

2 23

1 12

5

1

3

5

1

10

12

32 2 2

1

5

2

7

3 3

12 2

32

1 12

1 1 12 2

43

45

0

5

10

15

20

25

-500%

-400%

-300%

-200%

-100%

0%

100%

200%

300%

400%

1901

-190

619

06-1

908

1908

-191

219

12-1

914

1914

-191

619

16-1

919

1919

-192

019

20-1

921

1921

-192

319

23-1

928

1928

-192

919

29-1

932

1932

-193

719

37-1

938

1938

-194

819

48-1

949

1949

-195

119

51-1

954

1954

-195

619

56-1

958

1958

-196

019

60-1

961

1961

-196

619

66-1

968

1968

-197

519

75-1

978

1978

-198

119

81-1

982

1982

-198

420

00-2

002

1986

-198

919

89-1

991

1991

-199

219

92-1

993

1993

-199

519

95-1

996

1996

-199

719

97-1

998

1998

-200

020

00-2

002

2002

-200

620

06-2

009

2009

-201

120

11-2

016

13

$0

$100

$200

$300

$400

$500

$600

Spot Annual

Spot TCs vs. Realized Annual TCs

LME Zinc Stocks – Since Dec 2012

Zinc Market Poised for Change

• Supply situation fundamentally unchanged

• Growth in zinc demand expected to outpace supply

• Recent decline in demand growth caused inventory drawdown to slow

• Terminal markets absorbing unreported stock flows

4005006007008009001,0001,1001,200

50¢

60¢

70¢

80¢

90¢

100¢

110¢

120¢

Stocks Price

US

¢/lb

thou

sand

tonn

es

plotted to Jan. 12, 2015

US$

/dm

t

plotted to December 2015

Source: Teck, CRU14

Agenda

Teck Overview & Strategy

Commodity Market Observations

Teck Update

15

Responding to Difficult Market Conditions

• Further cost reductions achieved & focus on resetting our cost base− Gross profit1 up 5% in steelmaking coal

• ~C$1B in cash generated via two precious metal streaming agreements

• Strong financial position, with a cash balance2 of ~$1.8B− Exceeds the ~$1.5B of remaining Fort Hills capex− Expect to achieve year-end cash balance of ~$1.8B3

• Further capital and operating cost reductions announced

1. Before depreciation and amortization.2. As at October 21, 2015.3. As at October 21, 2015, and assuming commodity prices as of that date, C$/US$ exchange rate of 1.33 ,Teck’s 2015

guidance for production, costs and capital expenditures, existing US$ debt levels and no unusual transactions.16

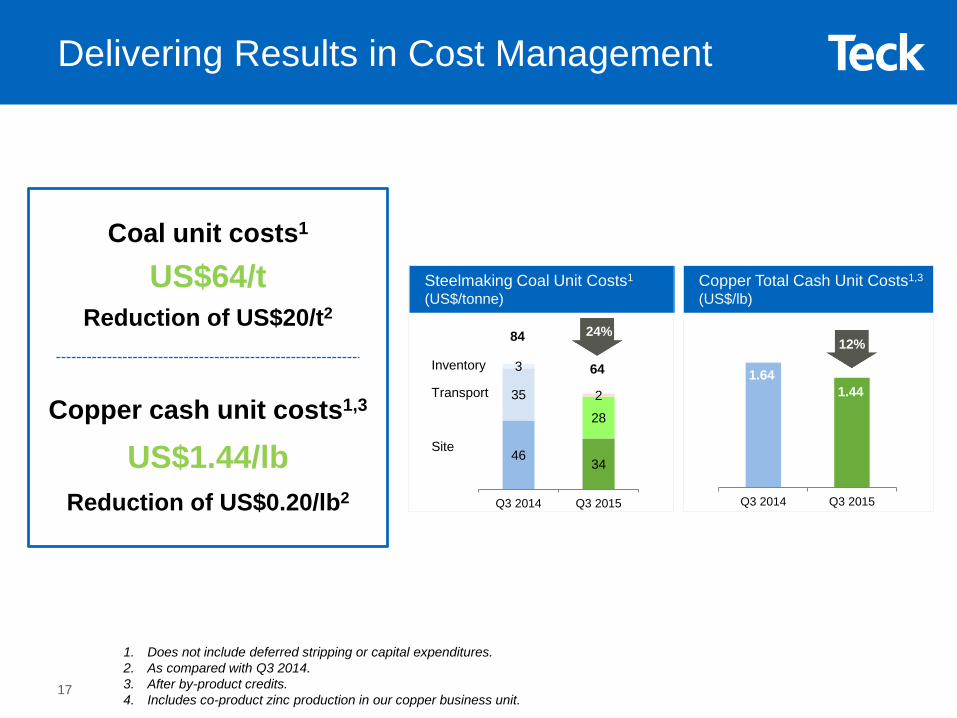

4634

35

28

3

2

Q3 2014 Q3 2015

Delivering Results in Cost Management

1. Does not include deferred stripping or capital expenditures. 2. As compared with Q3 2014. 3. After by-product credits.4. Includes co-product zinc production in our copper business unit.

24%

Steelmaking Coal Unit Costs1

(US$/tonne)

64

84

Site

Transport

Inventory

Q3 2014 Q3 2015

1.641.44

Copper Total Cash Unit Costs1,3

(US$/lb)

xx%12%

Coal unit costs1

US$64/tReduction of US$20/t2

Copper cash unit costs1,3

US$1.44/lbReduction of US$0.20/lb2

17

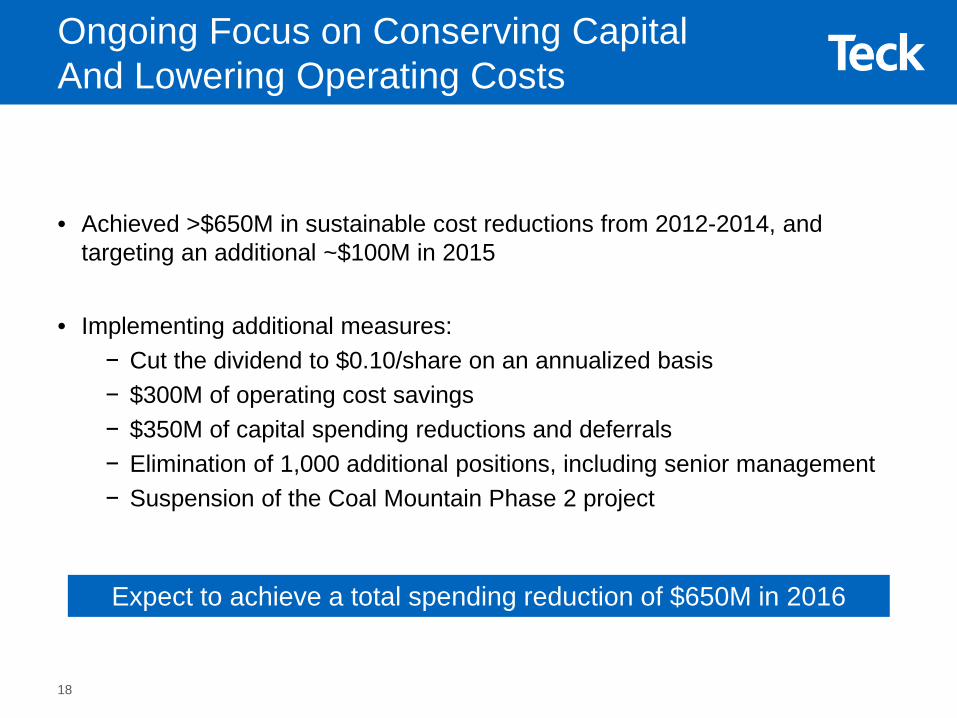

Ongoing Focus on Conserving Capital And Lowering Operating Costs

• Achieved >$650M in sustainable cost reductions from 2012-2014, and targeting an additional ~$100M in 2015

• Implementing additional measures:− Cut the dividend to $0.10/share on an annualized basis− $300M of operating cost savings− $350M of capital spending reductions and deferrals− Elimination of 1,000 additional positions, including senior management− Suspension of the Coal Mountain Phase 2 project

Expect to achieve a total spending reduction of $650M in 2016

18

$0

$250

$500

$750

$1,000

$1,250

$1,500

$1,750

$2,000

$2,250

$2,500

$2,750

$3,000

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

US$

M

191. As at October 21, 2015.2. Assumes current commodity prices, C$/US$ exchange rate of 1.31 ,Teck’s 2015 guidance for production, costs and capital

expenditures., existing US$ debt levels and no unusual transactions

Strong Financial Position1

• ~$1B in cash generated via two precious metal streaming agreements

• Current cash balance1 of ~$1.8B− Exceeds the ~$1.5B of remaining Fort Hills capex

• No debt due until 2017• Opportunities to further strengthen liquidity

2017Q1: US$300MQ3: US$300M

Expect to achieve year-end cash balance of ~$1.8B2

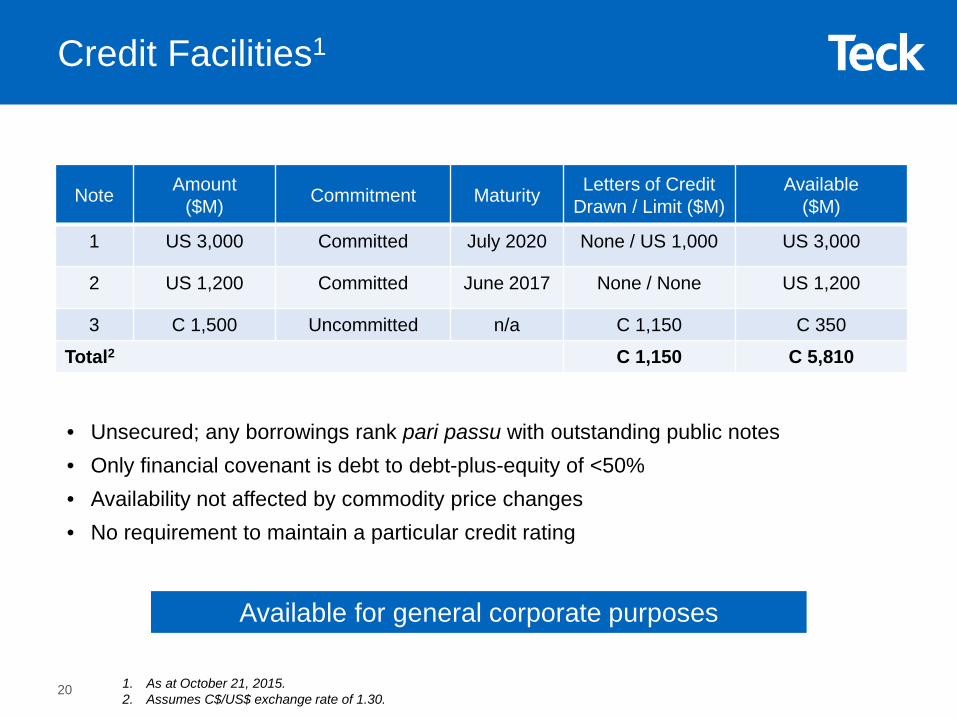

Credit Facilities1

Note Amount ($M) Commitment Maturity Letters of Credit

Drawn / Limit ($M)Available

($M)

1 US 3,000 Committed July 2020 None / US 1,000 US 3,000

2 US 1,200 Committed June 2017 None / None US 1,200

3 C 1,500 Uncommitted n/a C 1,150 C 350

Total2 C 1,150 C 5,810

• Unsecured; any borrowings rank pari passu with outstanding public notes• Only financial covenant is debt to debt-plus-equity of <50% • Availability not affected by commodity price changes• No requirement to maintain a particular credit rating

Available for general corporate purposes

1. As at October 21, 2015.2. Assumes C$/US$ exchange rate of 1.30.

20

Positioned to Weather The Market Downturn & Emerge Stronger and More Diversified

Attractive portfolio of long-life assets & resources

Good leverage to base metals markets

Attractive positions on commodity cost curves & focus on resetting our cost base

<20 months from start of commissioning at Fort Hills

Strong cash balance, ample credit facilities & opportunities to further strengthen liquidity

21

Additional Information

• In 2011, we launched our formal sustainability strategy

• Organized around 6 focus areas representing our most material sustainability challenges and opportunities

• Set short-term (2015) and long-term (2030) goals and vision for each area

• On track to achieve all of our 2015 goals

Our Sustainability Strategy

24

Received the PDAC 2014 Environmental and Social Responsibility Award

Best 50 Corporate Citizens in Canada 2015

On the Dow Jones Sustainability World Index six years in a row

One of top 100 most sustainable companies in the world and one of Canada’s most sustainable companies

Top 50 Socially Responsible Corporations in Canada

Received the Globe Foundation Environment Award in 2014

25

External Recognition

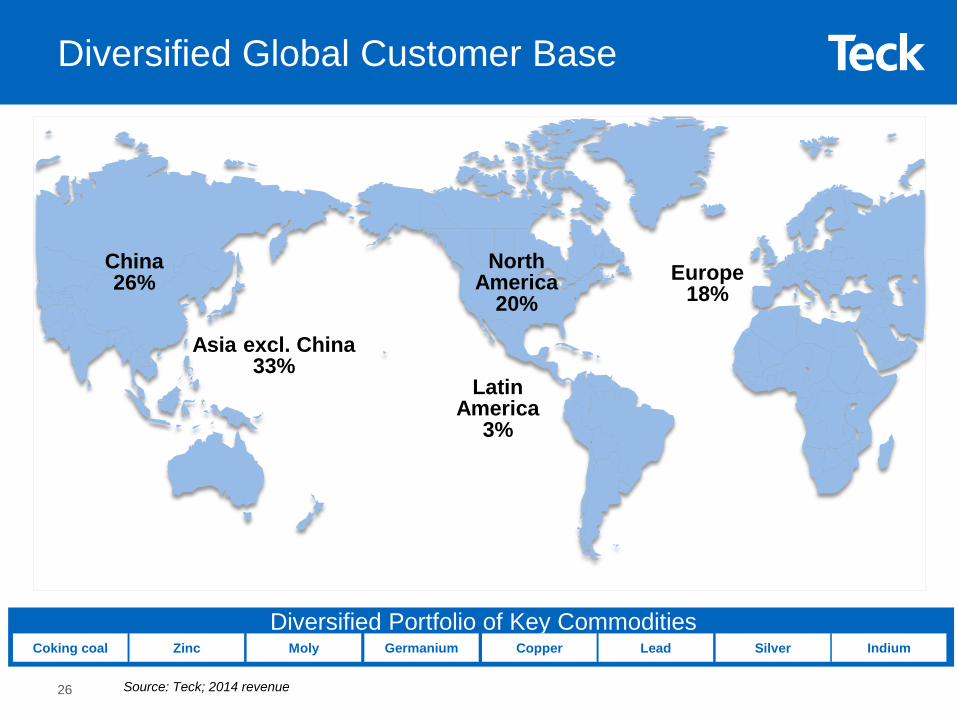

Diversified Portfolio of Key Commodities

NorthAmerica

20%Europe

18%

LatinAmerica

3%

China26%

Asia excl. China33%

26

Diversified Global Customer Base

Coking coal CopperZinc LeadMoly SilverGermanium Indium

Source: Teck; 2014 revenue

Actual 2014 Current 2015 GuidanceSteelmaking Coal

Coal production 26.7 Mt 25-26 MtCoal site costs C$54 /t1

Coal transportation costs C$38 /tCombined coal costs C$92 /t C$83-86 /tCombined coal costs US$84 ~US$64-66 /t2

CopperCopper production 333 kt 345-350 ktCopper cash unit costs3 US$1.65 /lb US$1.45-1.55 /lb

ZincZinc in concentrate production4 660 kt 635-665 ktRefined zinc production 277 kt 280–290 kt

Production & Site Cost Guidance

1. Including inventory adjustments.2. At $1.30 CAD/USD.3. Net of by-product credits.4. Including co-product zinc production from our copper business unit.

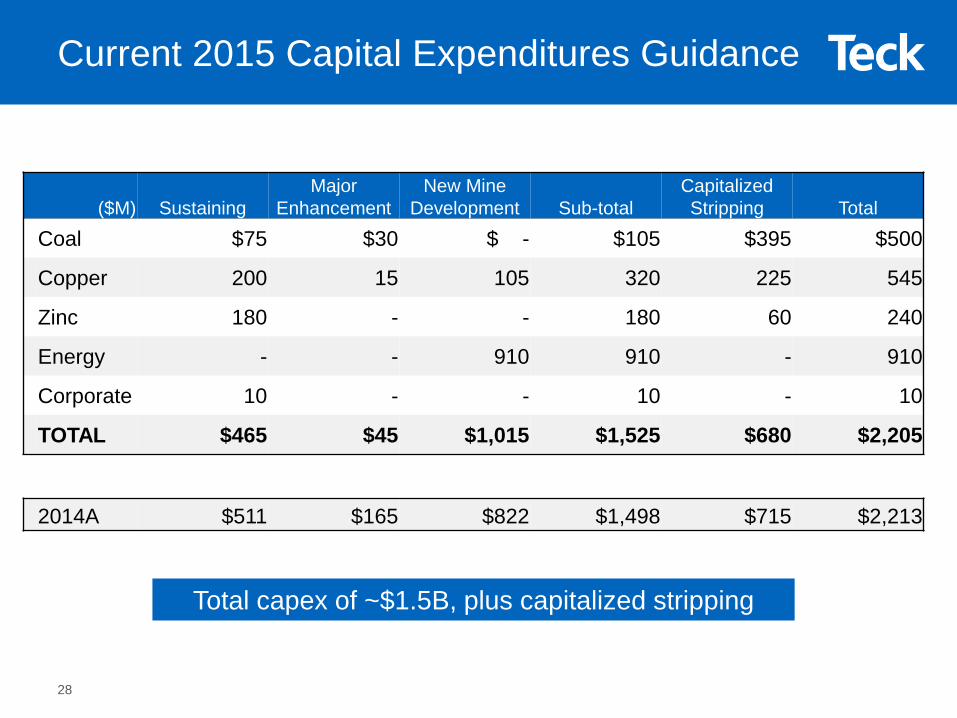

27

($M) SustainingMajor

EnhancementNew Mine

Development Sub-totalCapitalized Stripping Total

Coal $75 $30 $ - $105 $395 $500

Copper 200 15 105 320 225 545

Zinc 180 - - 180 60 240

Energy - - 910 910 - 910

Corporate 10 - - 10 - 10

TOTAL $465 $45 $1,015 $1,525 $680 $2,205

Total capex of ~$1.5B, plus capitalized stripping

2014A $511 $165 $822 $1,498 $715 $2,213

Current 2015 Capital Expenditures Guidance

28

Credit Ratings

S&P Moody’s Fitch DBRS

BBB Baa2 BBB BBB

BBB- Baa3 BBB- BBB (low)

BB+ Ba1 negative

BB+negative

BB (high)negative

BBnegative Ba2 BB BB

BB- Ba3 BB- BB (low)

Inve

stm

ent

Gra

deN

on-In

vest

men

t G

rade

Supported by:• Diversified business model• Low risk jurisdictions• Low cost assets• Conservative financial policies• Significant cost reductions• Capital discipline• Achieving production guidance• Production curtailments in coal• Dividend cut• Streaming transactions

Constrained by:• Debt-to-EBITDA metric, due to weak prices

Ratings reflect the current economic environment

As at January 15, 2016.29

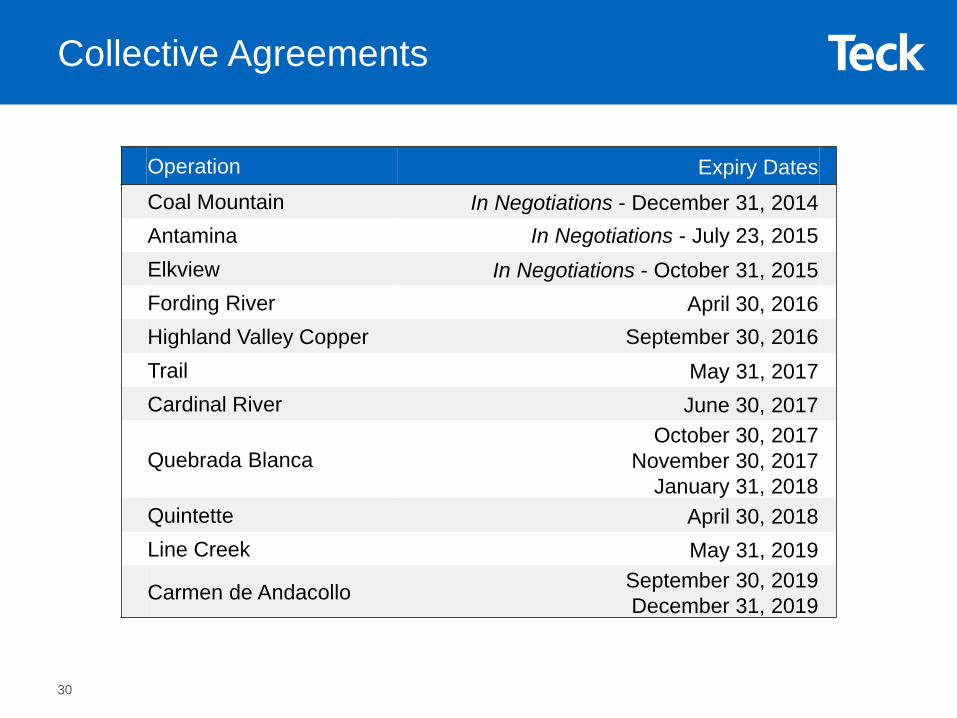

Operation Expiry DatesCoal Mountain In Negotiations - December 31, 2014Antamina In Negotiations - July 23, 2015Elkview In Negotiations - October 31, 2015Fording River April 30, 2016Highland Valley Copper September 30, 2016Trail May 31, 2017Cardinal River June 30, 2017

Quebrada BlancaOctober 30, 2017

November 30, 2017January 31, 2018

Quintette April 30, 2018Line Creek May 31, 2019

Carmen de Andacollo September 30, 2019December 31, 2019

Collective Agreements

30

$0

$10

$20

$30

$40

$50

$60

$70

80

100

120

140

160

180

200

220

240

260

Bloomberg Commodity Price Index (Left Axis) Teck (Right Axis)

Teck Stock Price vs. Bloomberg Commodity Price Index (2000-present)

Commodity Prices Impact Stock Price

Plotted to January 12, 2016

31

Steelmaking CoalBusiness Unit & Markets

70

80

90

100

110

120

130

140

150

$ / t

onne AUS$

Stronger US dollar favours producers outside of the US

Source: Argus, Bank of Canada

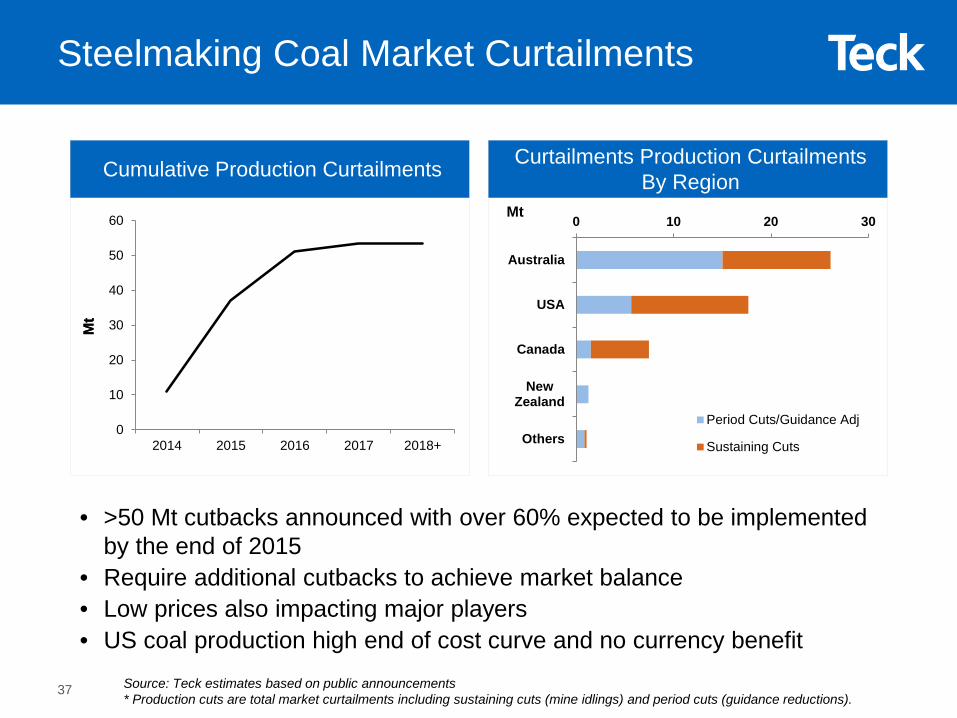

• >50 Mt cutbacks announced with over 60% expected to be implemented by the end of 2015

• Require additional cutbacks to achieve market balance

• US coal production high end of cost curve and no currency benefit

Coal Prices By CurrencyArgus FOB Australia

CDN$

US$

Met Coal Market Slowly Rebalancing; FX Assisting Producers Outside USA

plotted to January 11, 2016

33

0

3

6

9

12

15

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11A

pr-1

1Ju

l-11

Oct

-11

Jan-

12A

pr-1

2Ju

l-12

Oct

-12

Jan-

13A

pr-1

3Ju

l-13

Oct

-13

Jan-

14A

pr-1

4Ju

l-14

Oct

-14

Jan-

15A

pr-1

5Ju

l-15

Oct

-15

45 55 65 75

China

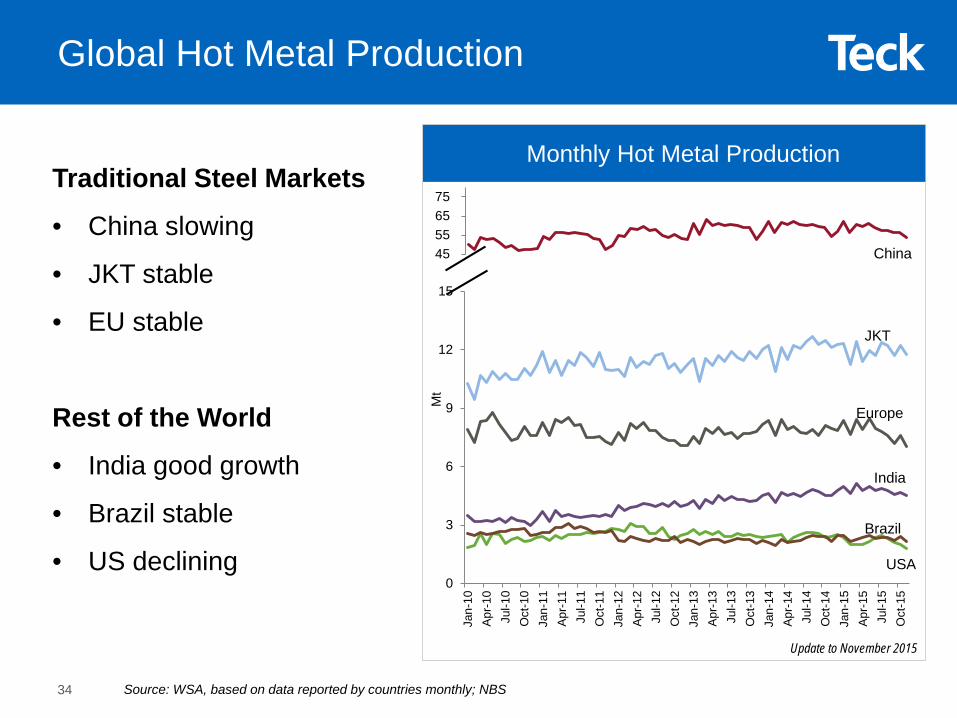

Traditional Steel Markets

• China slowing

• JKT stable

• EU stable

Rest of the World

• India good growth

• Brazil stable

• US declining

Monthly Hot Metal Production

Source: WSA, based on data reported by countries monthly; NBS

Mt

Update to November 2015

Global Hot Metal Production

JKT

India

Europe

USA

Brazil

34

Source: WSA, NBS, Wood Mackenzie, CRU1. Europe includes 12 countries.

Crude steel production to grow at ~1% CAGR between 2014 and 2020

Ex-China seaborne demand for steelmaking coal is forecasted to increase

by >2% CAGR in the same period

Crude Steel Production 2014-2020Crude Steel Production (Mt) 2014 2015 Nov YTD

annualized

Global* 1,647 (+1.2% YoY) 1,606 (-2.5% YoY)

China 823 (+0.9% YoY) 805 (-2.2% YoY)

Global, ex-China* 825 (+1.5% YoY) 801 (-2.8% YoY)

JKT 205 (+3% YoY) 197 (-3.9% YoY)

Europe 208 (+1.3% YoY) 203 (-2.3% YoY)

India 83 (+2.3% YoY) 90 (+7.8% YoY)

* Global production includes production only for the countries which report on monthly basis

Crude Steel Production Continues to Grow

35

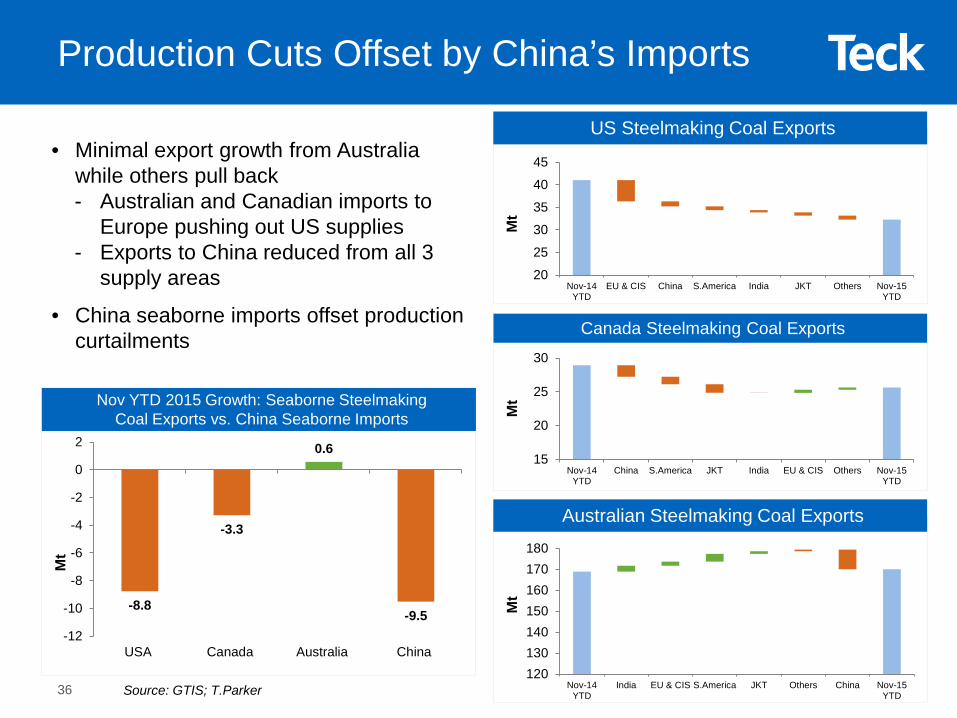

• Minimal export growth from Australia while others pull back- Australian and Canadian imports to

Europe pushing out US supplies- Exports to China reduced from all 3

supply areas

• China seaborne imports offset production curtailments

US Steelmaking Coal Exports

Australian Steelmaking Coal Exports

Nov YTD 2015 Growth: Seaborne Steelmaking Coal Exports vs. China Seaborne Imports

Source: GTIS; T.Parker

Production Cuts Offset by China’s Imports

Canada Steelmaking Coal Exports

20

25

30

35

40

45

Nov-14YTD

EU & CIS China S.America India JKT Others Nov-15YTD

Mt

120130140150160170180

Nov-14YTD

India EU & CIS S.America JKT Others China Nov-15YTD

Mt

15

20

25

30

Nov-14YTD

China S.America JKT India EU & CIS Others Nov-15YTD

Mt

-8.8

-3.3

0.6

-9.5-12

-10

-8

-6

-4

-2

0

2

USA Canada Australia China

Mt

36

Source: Teck estimates based on public announcements* Production cuts are total market curtailments including sustaining cuts (mine idlings) and period cuts (guidance reductions).

Curtailments Production Curtailments By RegionCumulative Production Curtailments

• >50 Mt cutbacks announced with over 60% expected to be implemented by the end of 2015

• Require additional cutbacks to achieve market balance• Low prices also impacting major players• US coal production high end of cost curve and no currency benefit

Steelmaking Coal Market Curtailments

0

10

20

30

40

50

60

2014 2015 2016 2017 2018+

Mt

Mt

0 10 20 30

Australia

USA

Canada

NewZealand

OthersPeriod Cuts/Guidance Adj

Sustaining Cuts

Mt

37

Relocation to China’s coastline facilitates access to seaborne raw materials

Sources: NBS, CISA

Chinese Steel Industry Moving to the Coast

38

Xinjiang

Tibet

Qinghai

Sichuan

Inner Mongolia

Henan

Shanxi

GuangxiGuandong

Fujian

Zhejiang

Jiangsu

Shandong

Laioning

Jilin

Heilongjiang

GuizhouHunan

Hubei

Jiangxi

Anhui

ShaanxiGansu

Ningxia

Qinghai

Sichuan

Yunnan

Beijing

Hebei

WISCO Fangchenggang Project• Major infrastructure in place. WISCO Fangchenggang Steel

Company established in Sep to wholly manage the project.• Cold roll line scheduled to be commissioned in H1 2015. Other

lines are scheduled to start successively within the year.• Blast furnaces (BFs) in the originally approved plan. Billet

rolling line only at this time. No timeline for BFs currently.• Targeting 5 Mt steel products in 2016 and 10 Mt in 2017.

Baosteel Zhanjiang Project• Coke ovens for BF #1 commissioned in July 2015. • BF #1 commissioning scheduled for September 2015

Ningde Steel Base• Proposed but no progress yet.

Ansteel Baiyunquan Project• Phase 1 (~ 5.4 Mt pig iron, 5.2 Mt crude

steel and 5 Mt steel products) in 2013.• Phase 2 (5.4 Mt BF) planned but no

progress yet.

Capital Steel Caofeidian Project• Planned 20 Mtpa steel capacity. • Phase 1 (10 Mt) completed in 2010.• Phase 2, planned with the investment of ~

US$7 billion, is kicked off soon in late Aug and scheduled to be completed by 2018. Capacity: hot metal 8.9Mt, crude steel 9.4Mt, steel products 9.0Mt.

Shandong Steel Rizhao Project• Planned 21.35 Mt crude steel. • Phase 1 (8.5 Mt) approved in Feb 2013• Construction started in Sep 2014 and

scheduled to commission by the end of 2016.

40%

45%

50%

55%

60%

65%

70%

0100200300400500600700800900

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Milli

on to

nnes

Total Coastal Coastal %

We Are a Leading Steelmaking Coal Supplier To Steel Producers Worldwide

NorthAmerica

~5%Europe~15%China

~25%

High quality, consistency, reliability, long-term supply

Asia excl. China~50%

Source: Teck; 2014

LatinAmerica

~5%

Proactively realigning sales with changing market39

0

50

100

150

200

250

300

350

Q1

2010

Q2

2010

Q3

2010

Q4

2010

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

US$

/ to

nne

Teck Realized Price (US$) Benchmark Price

Discount to the benchmark price is a function of:

1. Product mix: >90% hard coking coal

2. Direction of quarterly benchmark prices and spot prices- Q4 2015 benchmark for

premium products is US$89/t

Historical Average Realized Prices

Average Realized Price in Steelmaking Coal

Average realized price discount: ~8-9%Average realized % of benchmark: 91-92% (range: 88%-96%)

96%

88%

93%

94%92% YTD

91%

40

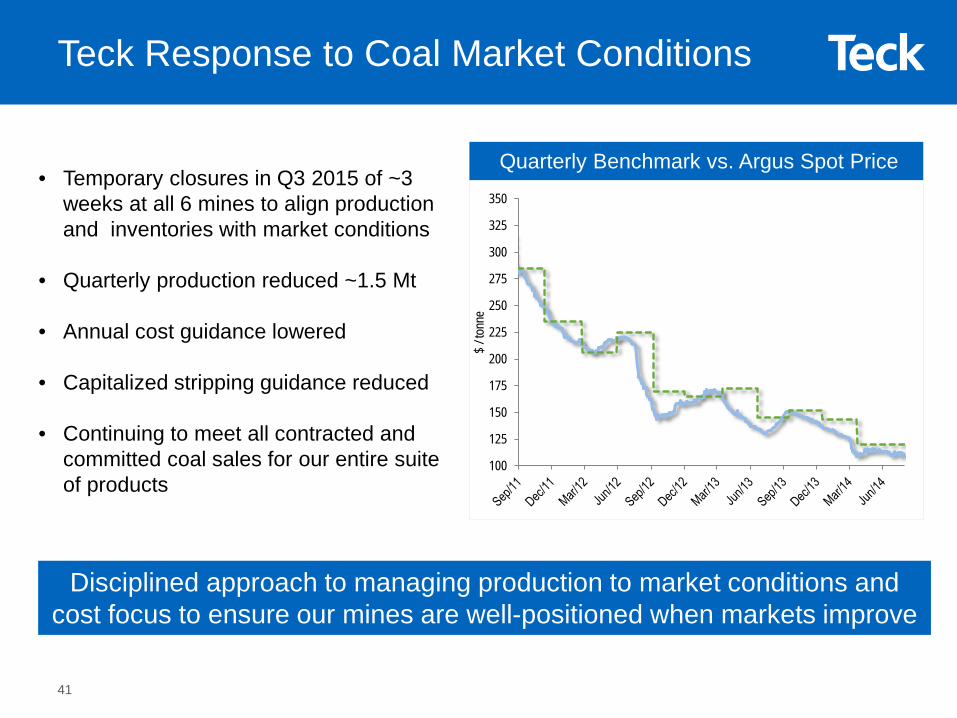

• Temporary closures in Q3 2015 of ~3 weeks at all 6 mines to align production and inventories with market conditions

• Quarterly production reduced ~1.5 Mt

• Annual cost guidance lowered

• Capitalized stripping guidance reduced

• Continuing to meet all contracted and committed coal sales for our entire suite of products

Disciplined approach to managing production to market conditions andcost focus to ensure our mines are well-positioned when markets improve

Teck Response to Coal Market Conditions

Quarterly Benchmark vs. Argus Spot Price

100

125

150

175

200

225

250

275

300

325

350

$ / to

nne

41

0

20

40

60

80

100

120

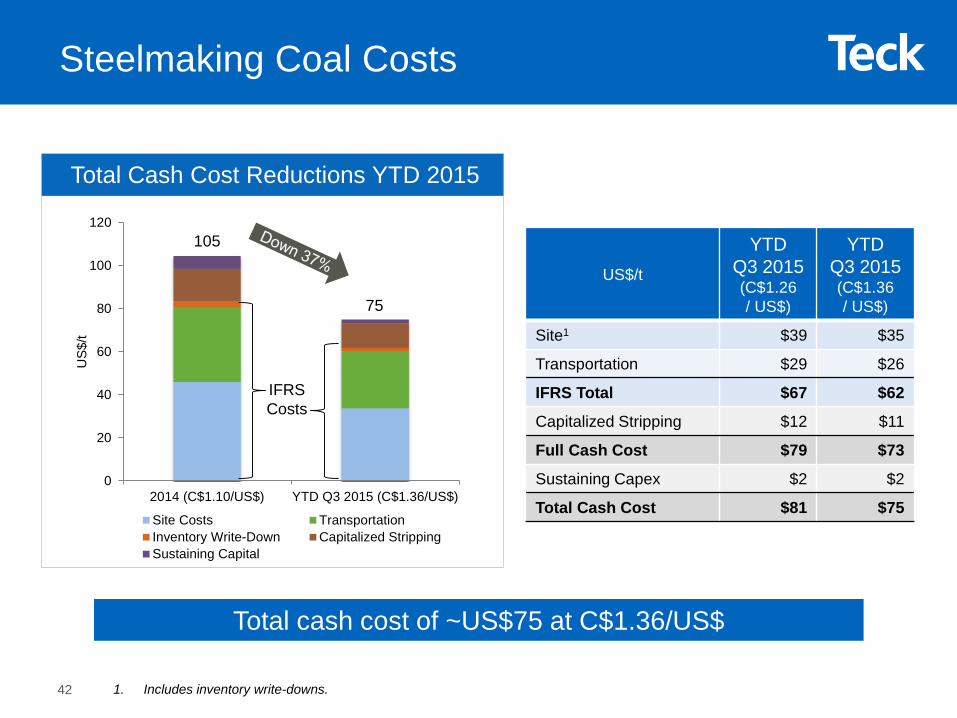

2014 (C$1.10/US$) YTD Q3 2015 (C$1.36/US$)

US$

/t

Site Costs TransportationInventory Write-Down Capitalized StrippingSustaining Capital

105

75

Total cash cost of ~US$75 at C$1.36/US$

Total Cash Cost Reductions YTD 2015

a

42

US$/t

YTD Q3 2015(C$1.26/ US$)

YTD Q3 2015(C$1.36/ US$)

Site1 $39 $35

Transportation $29 $26

IFRS Total $67 $62

Capitalized Stripping $12 $11

Full Cash Cost $79 $73

Sustaining Capex $2 $2

Total Cash Cost $81 $75

1. Includes inventory write-downs.

IFRS Costs

Steelmaking Coal Costs

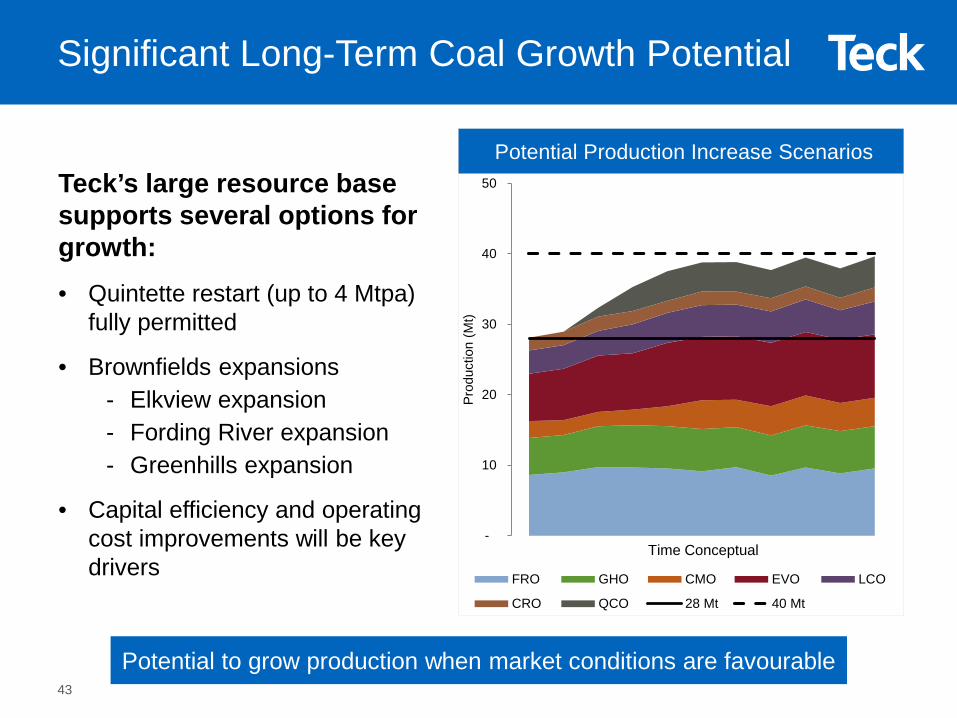

Significant Long-Term Coal Growth Potential

Potential Production Increase ScenariosTeck’s large resource base supports several options for growth:• Quintette restart (up to 4 Mtpa)

fully permitted

• Brownfields expansions- Elkview expansion - Fording River expansion- Greenhills expansion

• Capital efficiency and operating cost improvements will be key drivers

-

10

20

30

40

50

Prod

uctio

n (M

t)

FRO GHO CMO EVO LCO

CRO QCO 28 Mt 40 Mt

Time Conceptual

Potential to grow production when market conditions are favourable43

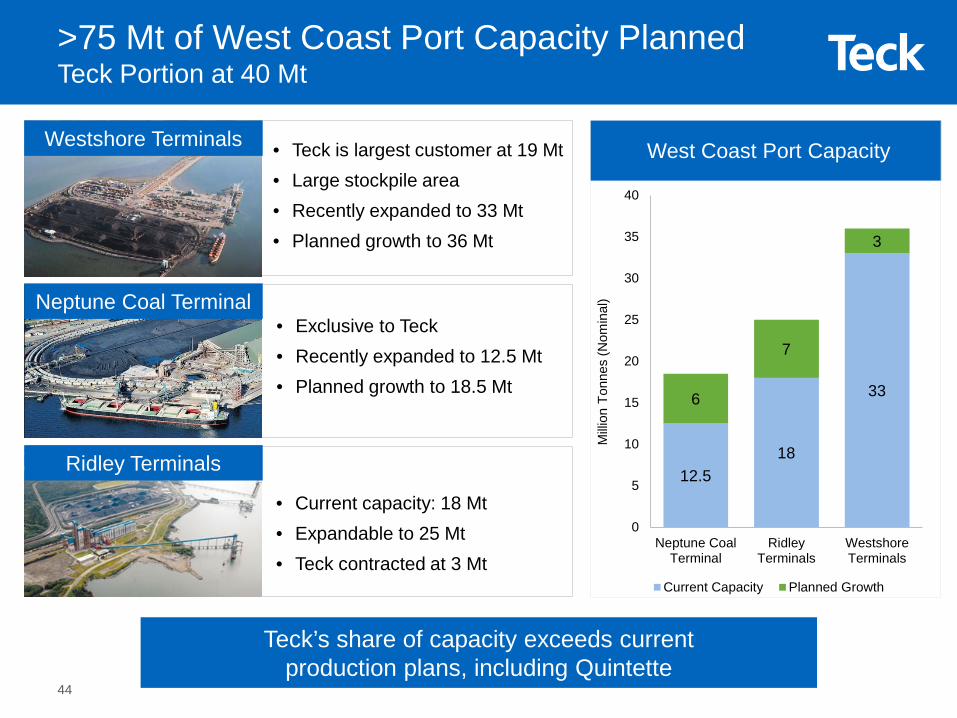

>75 Mt of West Coast Port Capacity PlannedTeck Portion at 40 Mt

• Exclusive to Teck • Recently expanded to 12.5 Mt • Planned growth to 18.5 Mt

Westshore Terminals

Neptune Coal Terminal

Ridley Terminals

West Coast Port Capacity

• Current capacity: 18 Mt• Expandable to 25 Mt• Teck contracted at 3 Mt

• Teck is largest customer at 19 Mt• Large stockpile area• Recently expanded to 33 Mt• Planned growth to 36 Mt

Milli

on T

onne

s (N

omin

al)

Teck’s share of capacity exceeds current production plans, including Quintette

12.518

336

7

3

0

5

10

15

20

25

30

35

40

Neptune CoalTerminal

RidleyTerminals

WestshoreTerminals

Current Capacity Planned Growth

44

0%

20%

40%

60%

80%

100%

CO2 NOx Particulate SOxDiesel Natural Gas

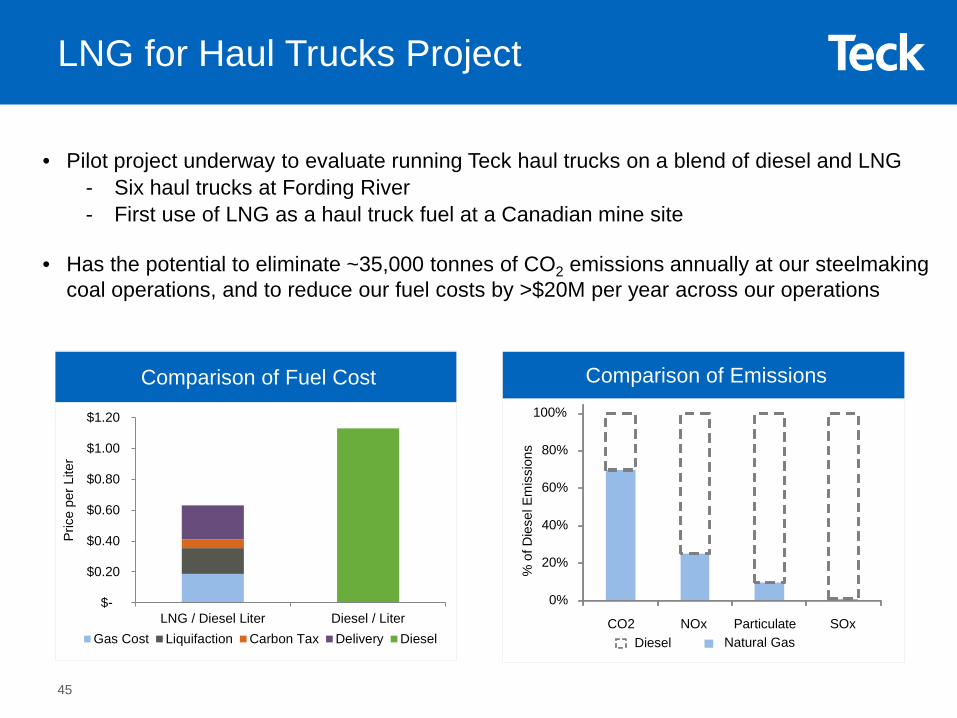

LNG for Haul Trucks Project

• Pilot project underway to evaluate running Teck haul trucks on a blend of diesel and LNG- Six haul trucks at Fording River- First use of LNG as a haul truck fuel at a Canadian mine site

• Has the potential to eliminate ~35,000 tonnes of CO2 emissions annually at our steelmaking coal operations, and to reduce our fuel costs by >$20M per year across our operations

Comparison of Fuel Cost

$-

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

LNG / Diesel Liter Diesel / LiterGas Cost Liquifaction Carbon Tax Delivery Diesel

Pric

e pe

r Lite

r

Comparison of Emissions

% o

f Die

sel E

mis

sion

s

45

• Around the world, and especially in China, blast furnaces are getting larger and increasing PCI rates

• Coke requirements for stable blast furnace operation are becoming increasingly higher

• Teck coals with high hot and cold strength are ideally suited to ensure stable blast furnace operation

• Produce some of the highest hot strengths in the world50 60 70 80 90 100

South Africa

Japan (Sorachl)

Japan(Yubarl)

U.S.A.Canada OtherTeck HCCAustraliaJapanSouth Africa

Australia(hard coking)and Canada

U.S.A.

Australia(soft coking)

10

20

30

40

50

60

70

80

Drum Strength Dl 30 (%)

CSR

Teck HCC

46

Coking Coal Strength

High Quality Hard Coking Coal

Copper Business Unit & Markets

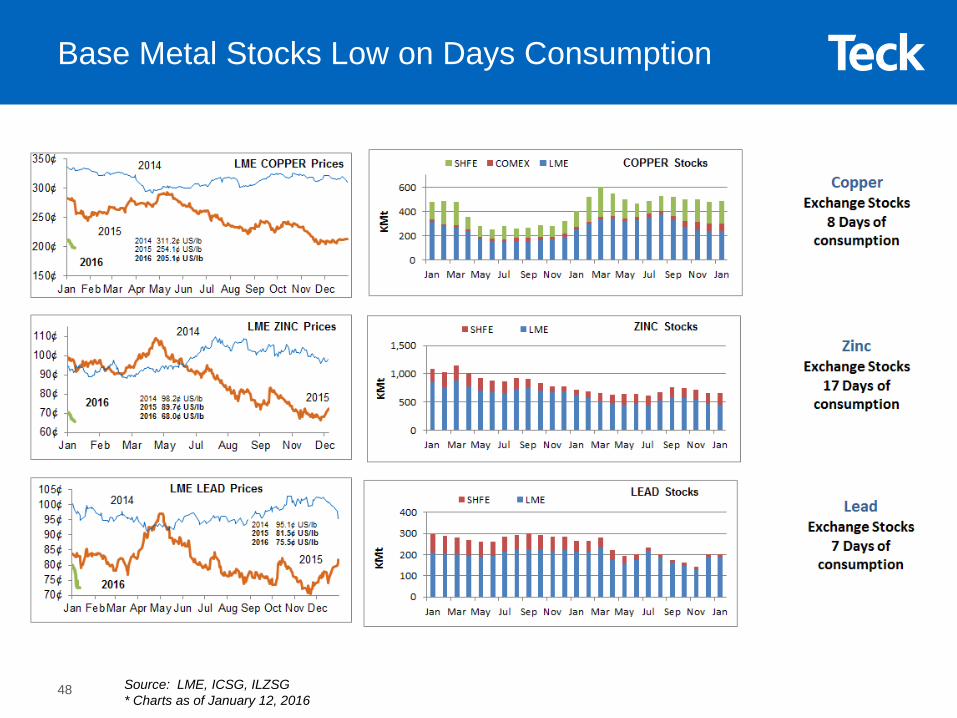

Base Metal Stocks Low on Days Consumption

Source: LME, ICSG, ILZSG* Charts as of January 12, 2016

48

0

200

400

600

800

1000

1200

1400

0¢

50¢

100¢

150¢

200¢

250¢

300¢

350¢

400¢

450¢

500¢

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

LME Stocks Comex SHFE Price

Historic Copper Metal Prices & StocksU

S¢/lb

thou

sand

tonn

es

plotted to Jan. 12, 2016

Daily Copper Prices & Stocks

Source: LME, ICSG, ILZSG49

16,000

16,500

17,000

17,500

18,000

18,500

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep

-15

Oct

-15

Nov

-15

Dec

-15

5% Disruption net of ProjectsMarket Adjustment2017 Adjusted

15,000

15,500

16,000

16,500

17,000

17,500

Feb-

13

Jun-

13

Oct

-13

Feb-

14

Jun-

14

Oct

-14

Feb-

15

Jun-

15

Oct

-15

2015 AdjustedMarket Adjustment5% Disruption

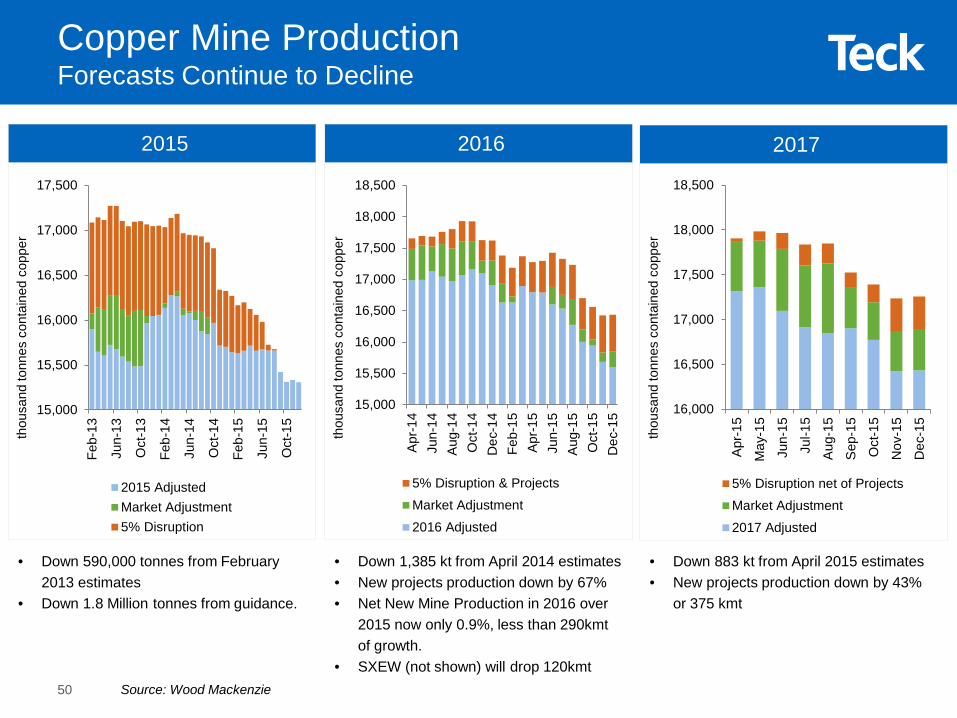

• Down 590,000 tonnes from February 2013 estimates

• Down 1.8 Million tonnes from guidance.

• Down 1,385 kt from April 2014 estimates• New projects production down by 67% • Net New Mine Production in 2016 over

2015 now only 0.9%, less than 290kmt of growth.

• SXEW (not shown) will drop 120kmt

Copper Mine Production Forecasts Continue to Decline

Source: Wood Mackenzie

thou

sand

tonn

es c

onta

ined

cop

per

2015 2016

15,000

15,500

16,000

16,500

17,000

17,500

18,000

18,500

Apr

-14

Jun-

14A

ug-1

4O

ct-1

4D

ec-1

4Fe

b-15

Apr

-15

Jun-

15A

ug-1

5O

ct-1

5D

ec-1

5

5% Disruption & ProjectsMarket Adjustment2016 Adjusted

2017

• Down 883 kt from April 2015 estimates • New projects production down by 43%

or 375 kmt

thou

sand

tonn

es c

onta

ined

cop

per

thou

sand

tonn

es c

onta

ined

cop

per

50

(300)

(250)

(200)

(150)

(100)

(50)

0

Thou

s. M

t-950

-859

-776-851

-945

-584

-839

-973

-831

-968

-1,015-1,200

-1,000

-800

-600

-400

-200

02005 2006 2007 2008 2009 2010 2011 2012 2013 2014

2015YTD

Thou

sand

tonn

esDisruptions Continue in Copper

Significant Copper Concentrate Disruptions Breakdown of Disruptions including SXEW

plotted to December 2015

plotted to December 2015

Source: Teck, CRU51

0¢

10¢

20¢

30¢

40¢

50¢

60¢

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Standard Spot High Grade Spot Realised TC/RC

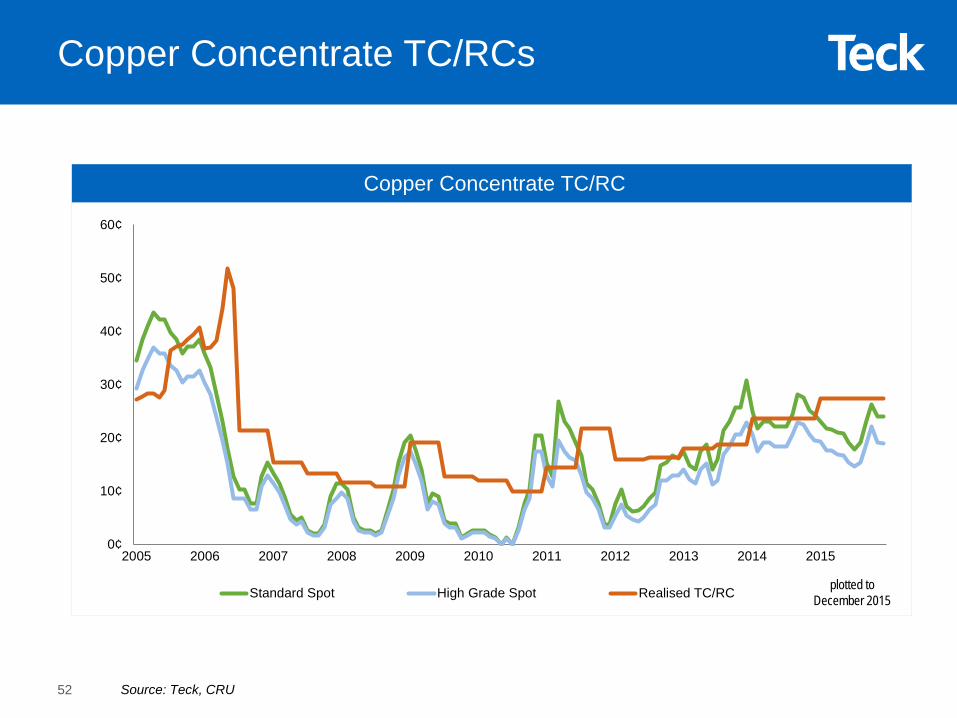

Copper Concentrate TC/RCs

Copper Concentrate TC/RC

plotted to December 2015

Source: Teck, CRU52

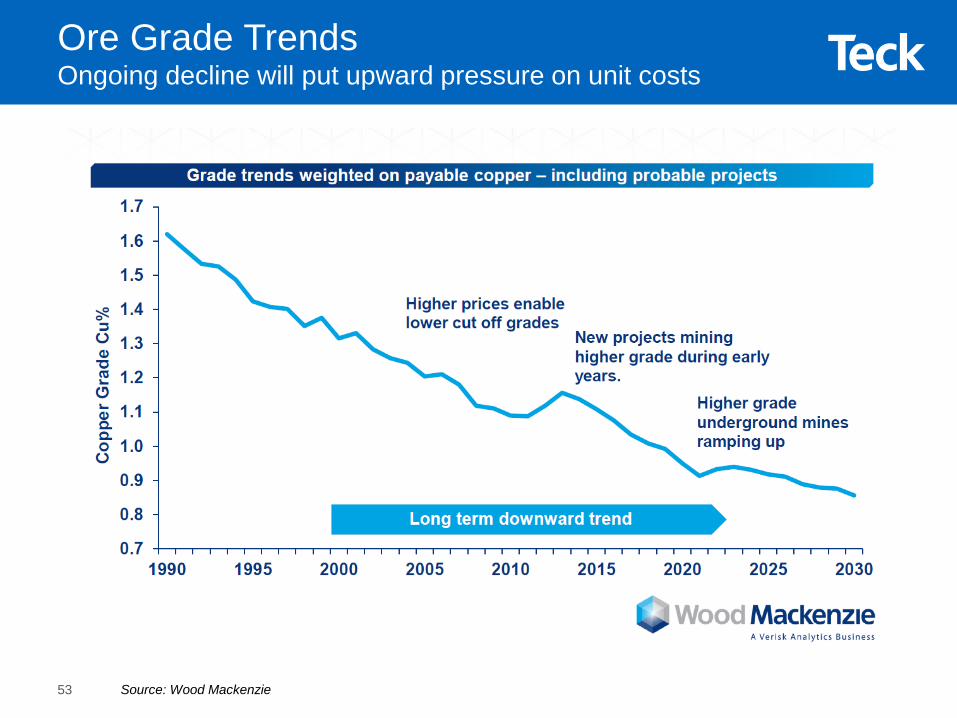

Ore Grade TrendsOngoing decline will put upward pressure on unit costs

Source: Wood Mackenzie53

Margin Compression at Its Lowest PointWorse than During the Global Financial Crisis

Source: Wood Mackenzie54

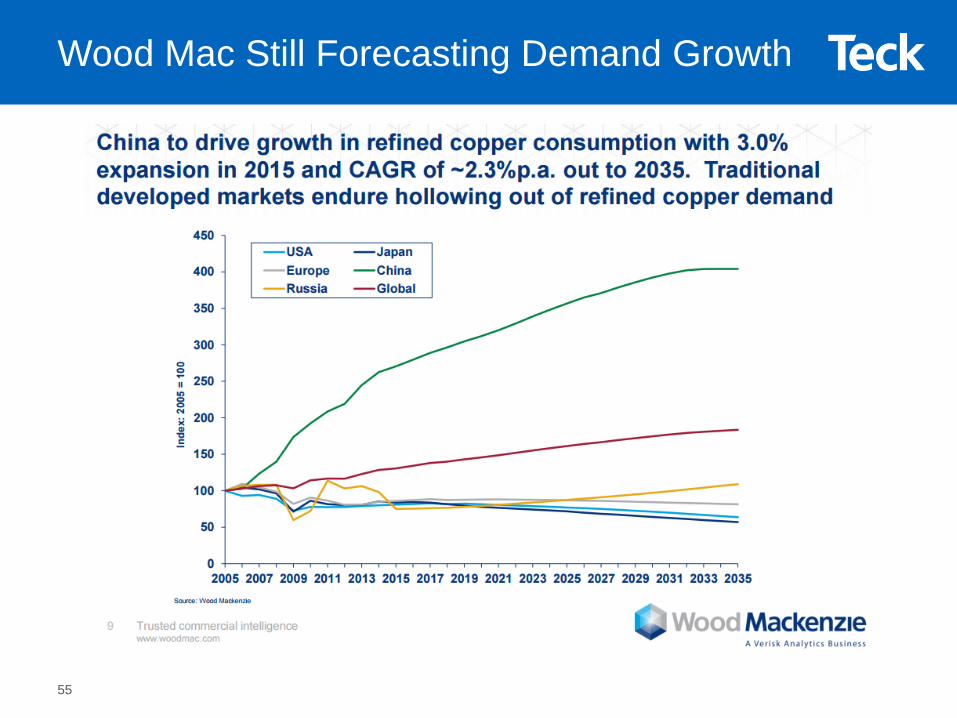

Wood Mac Still Forecasting Demand Growth

55

0100200300400500600700800900

1,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Cathode Concs Scrap Blister/Semis

000’

s to

nnes

(con

tent

)

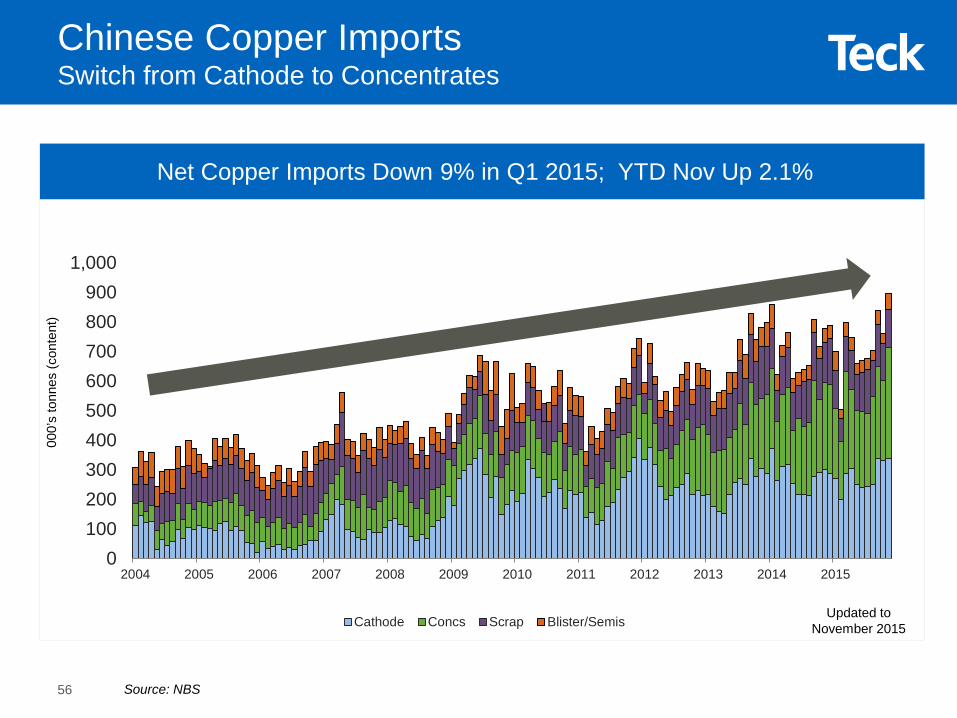

Net Copper Imports Down 9% in Q1 2015; YTD Nov Up 2.1%

Source: NBS

Chinese Copper Imports Switch from Cathode to Concentrates

Updated to November 2015

56

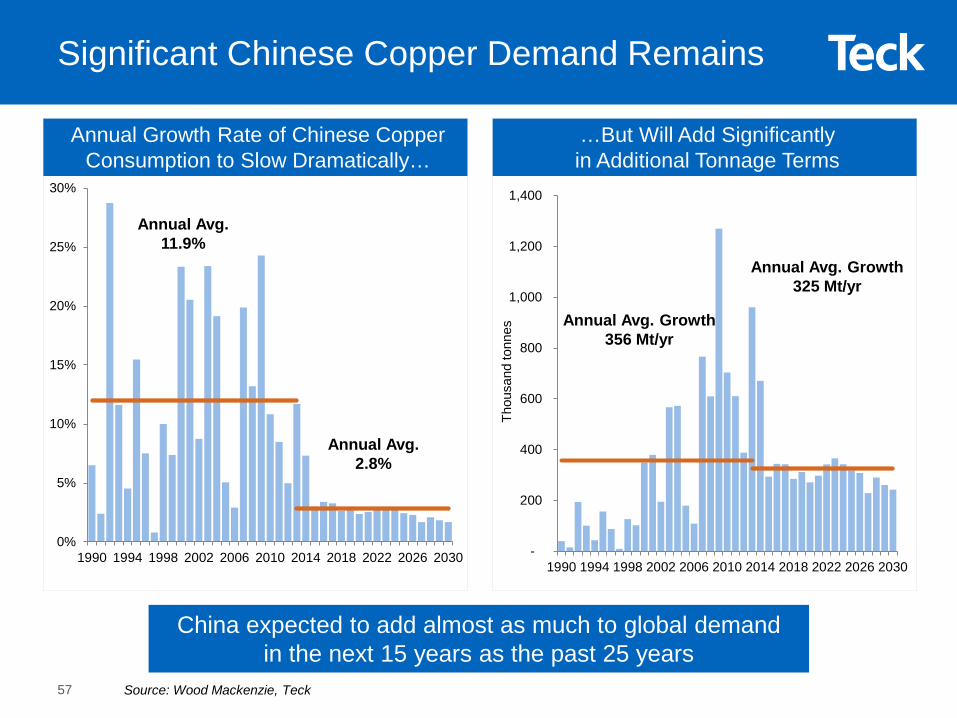

Significant Chinese Copper Demand Remains

…But Will Add Significantly in Additional Tonnage Terms

Annual Growth Rate of Chinese Copper Consumption to Slow Dramatically…

China expected to add almost as much to global demand in the next 15 years as the past 25 years

Source: Wood Mackenzie, Teck

-

200

400

600

800

1,000

1,200

1,400

1990 1994 1998 2002 2006 2010 2014 2018 2022 2026 2030

0%

5%

10%

15%

20%

25%

30%

1990 1994 1998 2002 2006 2010 2014 2018 2022 2026 2030

Annual Avg. 11.9%

Annual Avg. 2.8%

Annual Avg. Growth356 Mt/yr

Annual Avg. Growth325 Mt/yr

Thou

sand

tonn

es

57

0

500

1,000

1,500

2,000

2,500

2010 2011 2012 2013 2014 2015

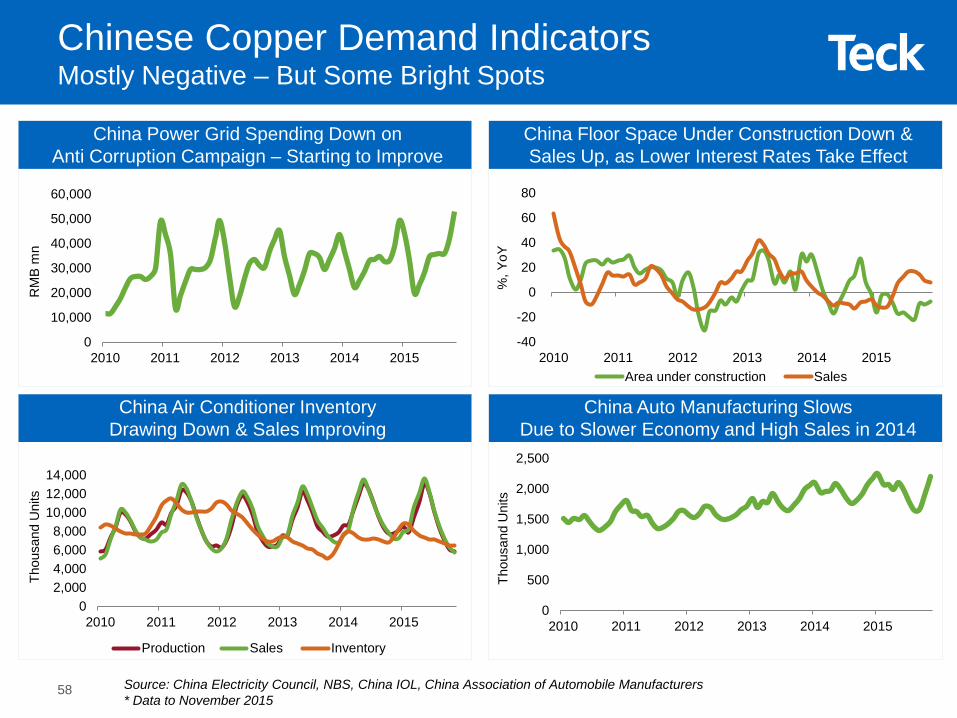

China Power Grid Spending Down on Anti Corruption Campaign – Starting to Improve

China Floor Space Under Construction Down & Sales Up, as Lower Interest Rates Take Effect

Source: China Electricity Council, NBS, China IOL, China Association of Automobile Manufacturers* Data to November 2015

China Air Conditioner Inventory Drawing Down & Sales Improving

China Auto Manufacturing SlowsDue to Slower Economy and High Sales in 2014

Thou

sand

Uni

ts

02,0004,0006,0008,000

10,00012,00014,000

2010 2011 2012 2013 2014 2015

Production Sales Inventory

Thou

sand

Uni

ts

%, Y

oY

-40

-20

0

20

40

60

80

2010 2011 2012 2013 2014 2015Area under construction Sales

0

10,000

20,000

30,000

40,000

50,000

60,000

2010 2011 2012 2013 2014 2015

RM

B m

nChinese Copper Demand IndicatorsMostly Negative – But Some Bright Spots

58

Copper Scrap Supply vs. LME Price

Copper Scrap Supply

Source: Wood Mackenzie

Copper scrap supply is strongly correlated with price

10%11%12%13%14%15%16%17%18%19%20%21%22%23%24%25%26%

$-

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Copper Price (USD/lb) Scrap as a % Consumption

59

-100

0

100

200

300

400

500

600

700

800

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep

-15

Oct

-15

Nov

-15

Dec

-15

0

100

200

300

400

500

600

700

800

Feb-

13

Jun-

13

Oct

-13

Feb-

14

Jun-

14

Oct

-14

Feb-

15

Jun-

15

Oct

-15

Since April 2014• Despite a 725,000 tonne drop in demand

• The surplus is down 750,000 tonnes

Source: Wood Mackenzie

thou

sand

tonn

es c

onta

ined

cop

per

2015 2016

0

100

200

300

400

500

600

700

800

Apr

-14

Jun-

14A

ug-1

4O

ct-1

4D

ec-1

4Fe

b-15

Apr

-15

Jun-

15A

ug-1

5O

ct-1

5D

ec-1

5

2017

thou

sand

tonn

es c

onta

ined

cop

per

thou

sand

tonn

es c

onta

ined

cop

per

Global Copper Cathode BalancesWood Mackenzie’s Outlook is Trending Down

Since December 2014• Despite a drop of 660,000 tonnes to Wood

Mackenzie’s demand estimates

• Their surplus is down 700,000 tonnes

Since April 2015• Down from a 510,000 tonnes surplus

• Despite a 510,000 tonne drop in demand

60

0

100

200

300

400

500

600

700

800

900

Global Refined Copper BalancesWood Mackenzie’s Outlook is Trending Down

‘000

s to

nnes

cop

per

Surplus only 0.9% of Global Demand

0

100

200

300

400

500

600

700

800

900

Jan-

13M

ar-1

3M

ay-1

3Ju

l-13

Sep

-13

Nov

-13

Jan-

14M

ar-1

4M

ay-1

4Ju

l-14

Sep

-14

Nov

-14

Jan-

15M

ar-1

5M

ay-1

5Ju

l-15

Sep

-15

Nov

-15

Wood Mackenzie 2015F Refined Surplus Wood Mackenzie 2016F Refined Surplus

Surplus only 2% of Global Demand

‘000

s to

nnes

cop

per

Source: Wood Mackenzie61

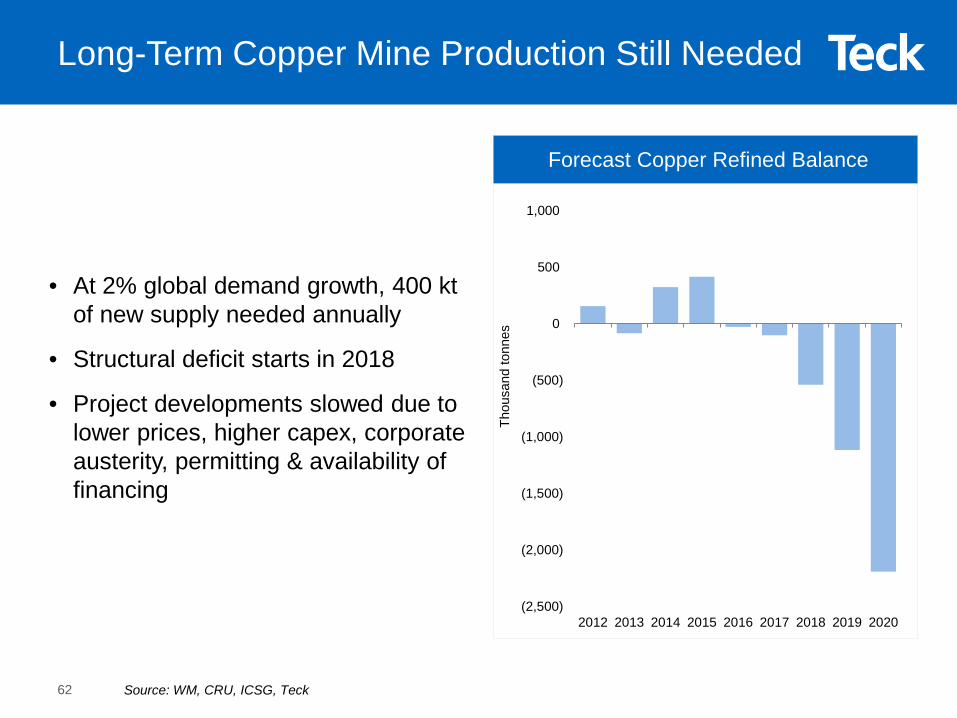

• At 2% global demand growth, 400 ktof new supply needed annually

• Structural deficit starts in 2018

• Project developments slowed due to lower prices, higher capex, corporate austerity, permitting & availability of financing

Forecast Copper Refined Balance

Long-Term Copper Mine Production Still Needed

Source: WM, CRU, ICSG, Teck

(2,500)

(2,000)

(1,500)

(1,000)

(500)

0

500

1,000

2012 2013 2014 2015 2016 2017 2018 2019 2020

Thou

sand

tonn

es

62

Building Partnerships: Corridor Project

Teck and Goldcorp have combined Relincho and El Morro projects and formed a 50/50 joint venture company

• Committed to building strong, mutually beneficial relationships with stakeholders and communities

Capital smart partnership • Shared capital, common infrastructure• Shared risk, shared rewards

Benefits of combining projects include:• Longer mine life• Lower cost, improved capital efficiency• Reduced environmental footprint• Enhanced community benefits• Greater returns over either standalone

project

63

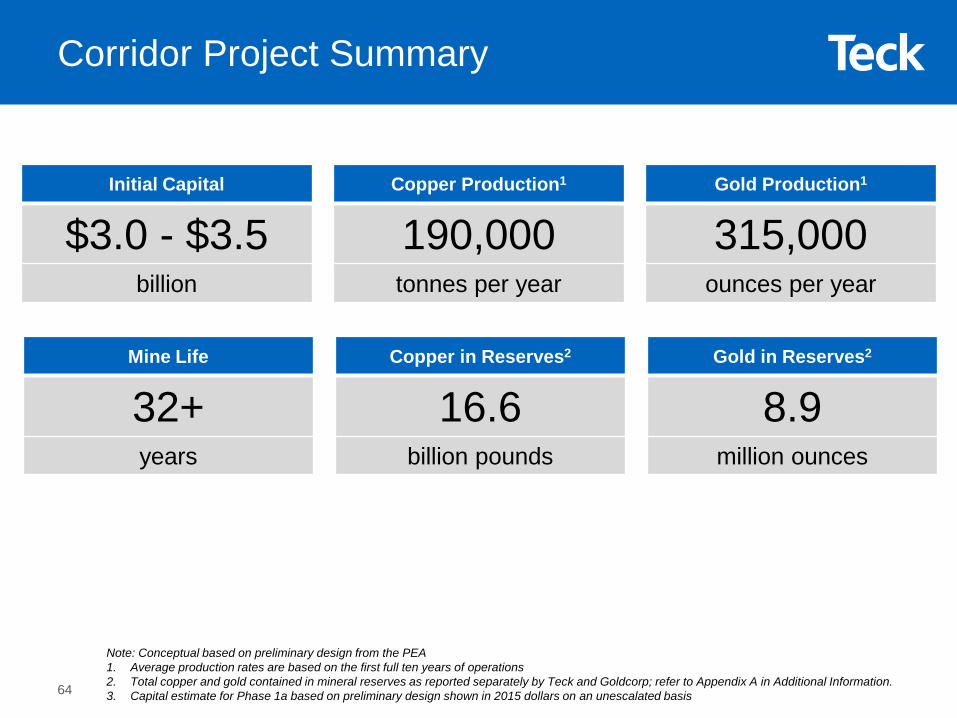

Corridor Project Summary

Initial Capital

$3.0 - $3.5billion

Copper Production1

190,000tonnes per year

Gold Production1

315,000ounces per year

Mine Life

32+years

Copper in Reserves2

16.6billion pounds

Gold in Reserves2

8.9million ounces

Note: Conceptual based on preliminary design from the PEA1. Average production rates are based on the first full ten years of operations2. Total copper and gold contained in mineral reserves as reported separately by Teck and Goldcorp; refer to Appendix A in Additional Information.3. Capital estimate for Phase 1a based on preliminary design shown in 2015 dollars on an unescalated basis64

Copper Development Projects in theAmericas

Corridor is one of the largest open pit copper development projects in the Americas on the basis of copper contained in Proven and Probable Reserves

-

5,000

10,000

15,000

20,000

25,000

Rad

omiro

Tom

ic

Cor

ridor

El A

rco

Que

brad

aB

lanc

a II

Que

llave

co

Agu

a R

ica

Rel

inch

o

El M

orro

Cas

ino

Sch

aft C

reek

Gal

ore

Cre

ek

Rio

Bla

nco

Cop

per E

quiv

alen

t in

Res

erve

s (M

lbs)

Copper-equivalent contained in Reserves (Mlbs)(North & South American Copper Projects)

Note: Copper equivalent reserves calculated using $3.25/lb Cu and $1,200/oz Au. Does not include copper resource projects that are currently in construction

Source: SNL Metals & Mining, Thomson One Analytics, and company disclosures.65

ZincBusiness Unit & Markets

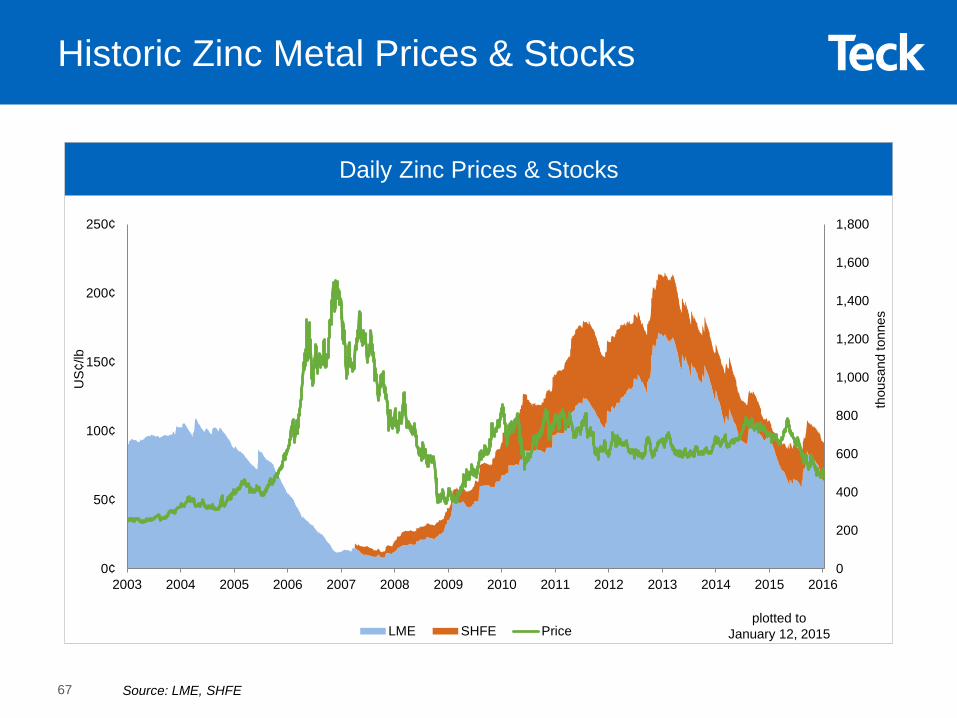

Historic Zinc Metal Prices & Stocks

Daily Zinc Prices & Stocks

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

0¢

50¢

100¢

150¢

200¢

250¢

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

LME SHFE Price

US¢

/lb

thou

sand

tonn

es

plotted to January 12, 2015

Source: LME, SHFE67

0

1,000

2,000

3,000

4,000

5,000

6,000

0

100

200

300

400

500

600

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013 2014 2015

Monthly Chinese Zinc Mine Production

LME Zinc Stocks

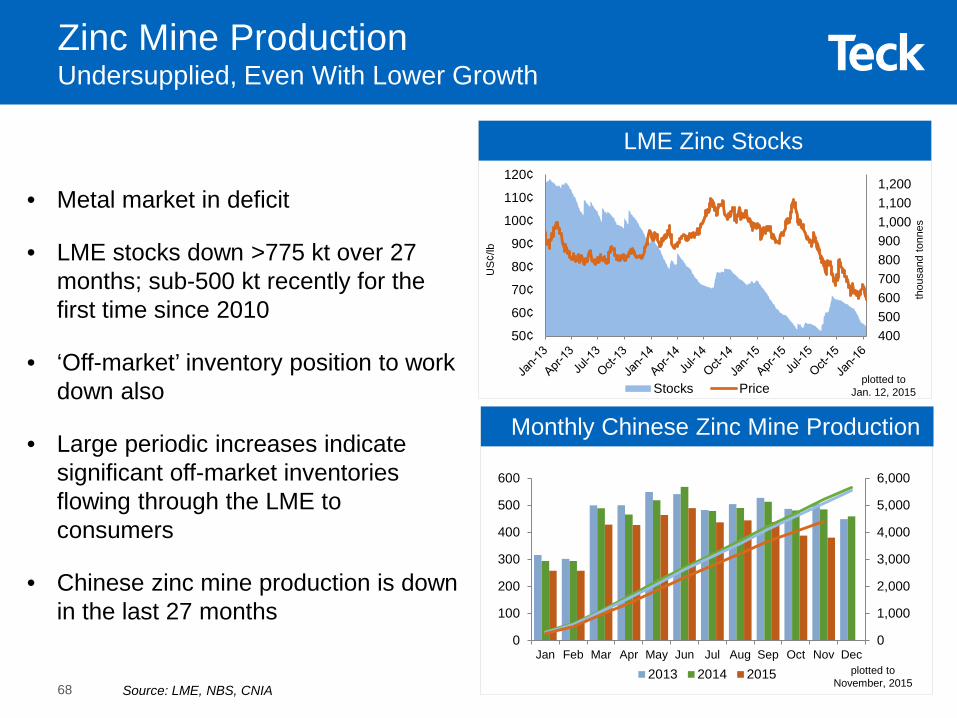

Zinc Mine ProductionUndersupplied, Even With Lower Growth

4005006007008009001,0001,1001,200

50¢

60¢

70¢

80¢

90¢

100¢

110¢

120¢

Stocks Priceplotted to

Jan. 12, 2015

plotted to November, 2015

• Metal market in deficit

• LME stocks down >775 kt over 27 months; sub-500 kt recently for the first time since 2010

• ‘Off-market’ inventory position to work down also

• Large periodic increases indicate significant off-market inventories flowing through the LME to consumers

• Chinese zinc mine production is down in the last 27 months

US

¢/lb

thou

sand

tonn

es

Source: LME, NBS, CNIA68

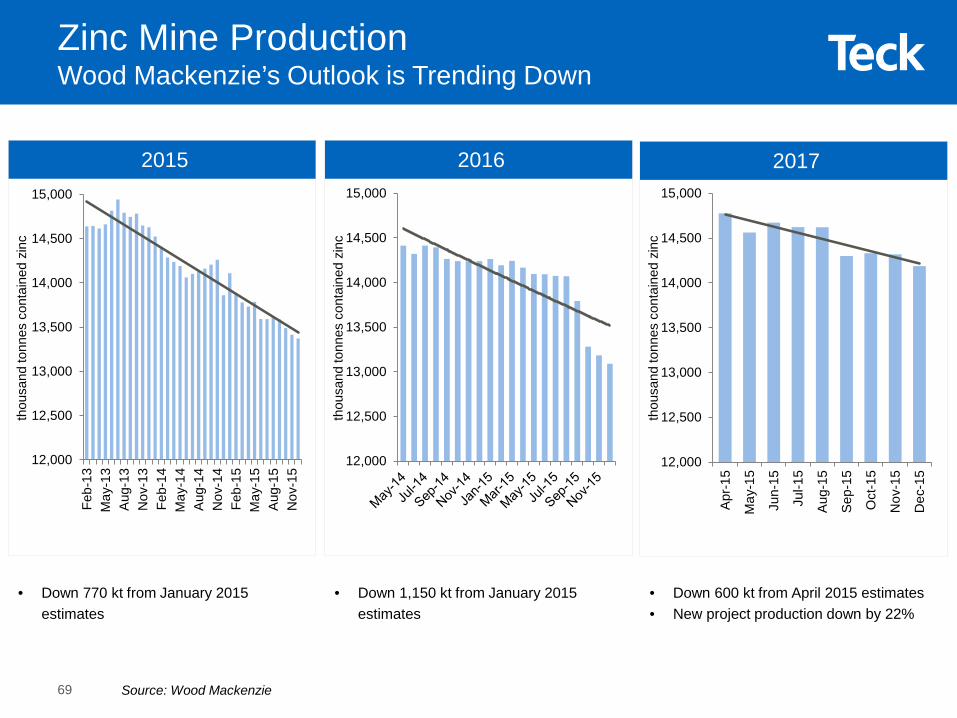

• Down 770 kt from January 2015 estimates

• Down 1,150 kt from January 2015 estimates

Zinc Mine Production Wood Mackenzie’s Outlook is Trending Down

thou

sand

tonn

es c

onta

ined

zin

c

2015 2016 2017

• Down 600 kt from April 2015 estimates • New project production down by 22%

thou

sand

tonn

es c

onta

ined

zin

c

thou

sand

tonn

es c

onta

ined

zin

c

12,000

12,500

13,000

13,500

14,000

14,500

15,000

Feb-

13M

ay-1

3A

ug-1

3N

ov-1

3Fe

b-14

May

-14

Aug

-14

Nov

-14

Feb-

15M

ay-1

5A

ug-1

5N

ov-1

5

12,000

12,500

13,000

13,500

14,000

14,500

15,000

12,000

12,500

13,000

13,500

14,000

14,500

15,000

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep

-15

Oct

-15

Nov

-15

Dec

-15

Source: Wood Mackenzie69

2014-2020 2014-2020

Significant Zinc Mine ReductionsLarge Short-Term Losses, More Long Term

-500

-400

-300

-200

-100

0

Cen

tury

Lish

een

Skor

pion

Red

Dog

Ros

eber

y

Brac

emac

-McL

eod

Rap

ura

Aguc

ha

Pom

orza

ny-O

lkus

z (in

cl B

ulk)

Jagu

ar

Mid

-Ten

ness

ee

Mae

Sod

Ende

avor

0

100

200

300

400

500

Gam

sber

gAn

tam

ina

Dug

ald

Riv

erM

cArth

ur R

iver

Bish

aG

ansu

Jin

hui

Kyzy

l-Tas

htyg

skoe

Shal

kiya

Res

tart

Sind

esar

Khu

rdAg

uas

Teni

das

Cha

ngba

Zaw

ar M

ines

El B

roca

lSa

ngui

kou

Car

ibou

Rea

ctiv

atio

nSa

n C

risto

bal

Pena

squi

to

Source: ICSG, Wood Mackenzie Teck, Company Reports70

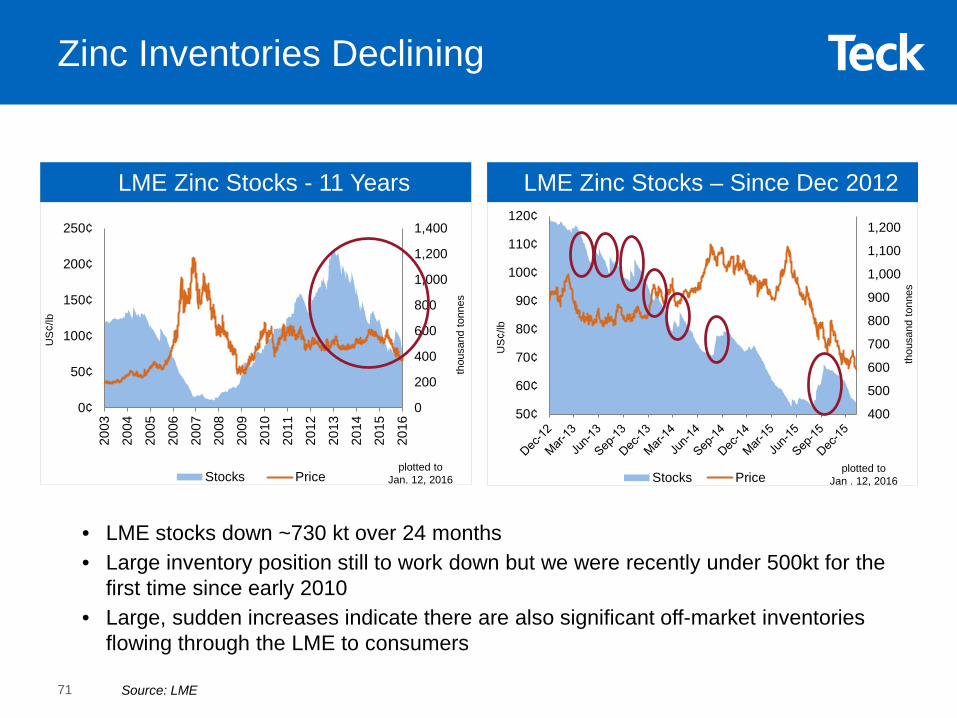

LME Zinc Stocks – Since Dec 2012LME Zinc Stocks - 11 Years

Zinc Inventories Declining

400

500

600

700

800

900

1,000

1,100

1,200

50¢

60¢

70¢

80¢

90¢

100¢

110¢

120¢

Stocks Price

0

200

400

600

800

1,000

1,200

1,400

0¢

50¢

100¢

150¢

200¢

250¢

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Stocks Price

US

¢/lb

thou

sand

tonn

esplotted to

Jan. 12, 2016

US

¢/lb

thou

sand

tonn

es

• LME stocks down ~730 kt over 24 months• Large inventory position still to work down but we were recently under 500kt for the

first time since early 2010• Large, sudden increases indicate there are also significant off-market inventories

flowing through the LME to consumers

plotted to Jan . 12, 2016

Source: LME71

• Down 259 kt from December 2014 estimates, taking the market from surplus into a deficit of 96 kt

• Down 442 kt from December 2014 estimates, taking the market further into deficit of 681 kt

thou

sand

tonn

es c

onta

ined

zin

c

2015 2016 2017

• Up 259 kt from April 2015 estimates • Wood Mackenzie expects 300 kt of

projects will come online in 2017 due to higher prices

thou

sand

tonn

es c

onta

ined

zin

c

thou

sand

tonn

es c

onta

ined

zin

c

(300)

(200)

(100)

0

100

200

300

400

Feb-

13M

ay-1

3A

ug-1

3N

ov-1

3Fe

b-14

May

-14

Aug

-14

Nov

-14

Feb-

15M

ay-1

5A

ug-1

5N

ov-1

5

(800)

(600)

(400)

(200)

0

200

400

May

-14

Jul-1

4

Sep

-14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sep

-15

Nov

-15 (500)

(400)

(300)

(200)

(100)

0

100

200

300

400

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep

-15

Oct

-15

Nov

-15

Dec

-15

Zinc Concentrate BalancesWood Mackenzie’s 2015 and 2015 Outlooks Trending Down

Source: Wood Mackenzie72

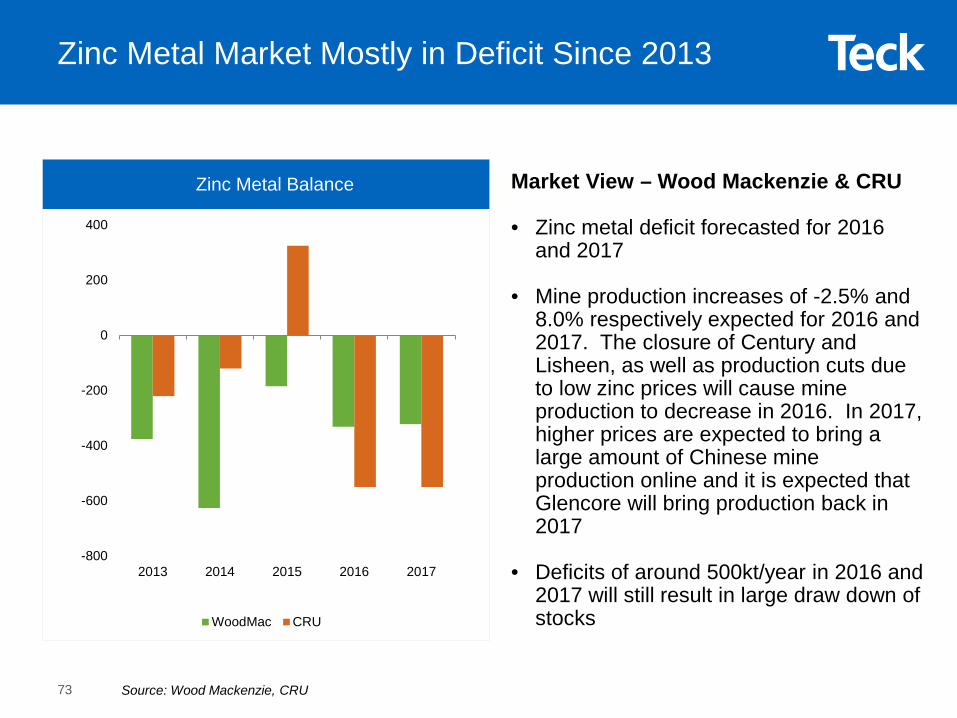

Zinc Metal Market Mostly in Deficit Since 2013

-800

-600

-400

-200

0

200

400

2013 2014 2015 2016 2017

WoodMac CRU

Market View – Wood Mackenzie & CRU

• Zinc metal deficit forecasted for 2016 and 2017

• Mine production increases of -2.5% and 8.0% respectively expected for 2016 and 2017. The closure of Century and Lisheen, as well as production cuts due to low zinc prices will cause mine production to decrease in 2016. In 2017, higher prices are expected to bring a large amount of Chinese mine production online and it is expected that Glencore will bring production back in 2017

• Deficits of around 500kt/year in 2016 and 2017 will still result in large draw down of stocks

Zinc Metal Balance

Source: Wood Mackenzie, CRU73

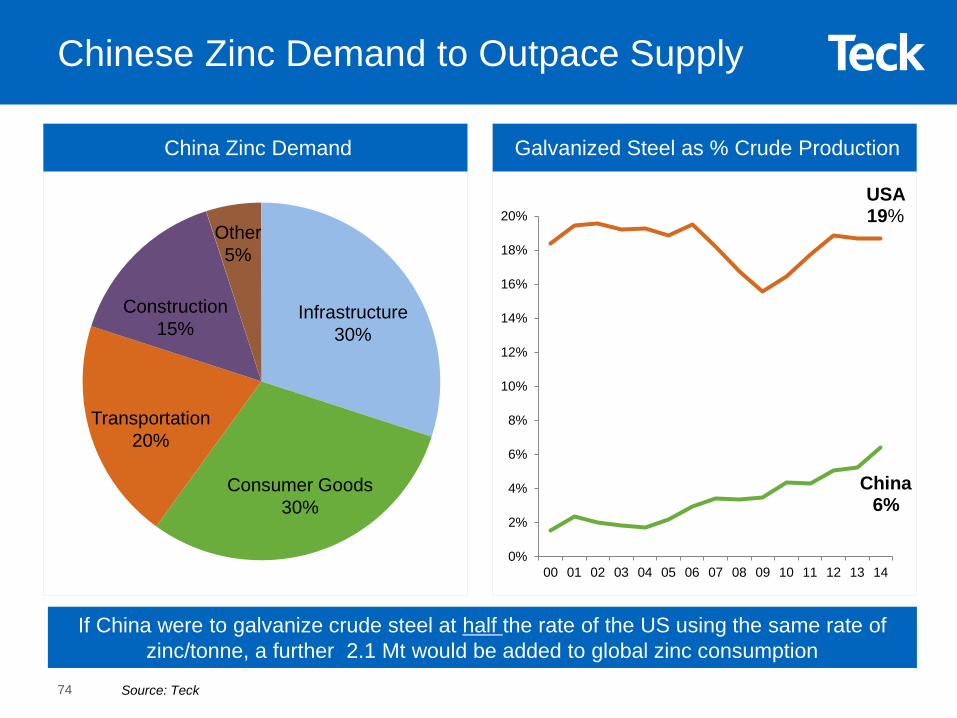

China6%

USA 19%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Galvanized Steel as % Crude ProductionChina Zinc Demand

Construction15%

Transportation 20%

Other 5%

Consumer Goods30%

Infrastructure30%

Chinese Zinc Demand to Outpace Supply

Source: Teck

If China were to galvanize crude steel at half the rate of the US using the same rate of zinc/tonne, a further 2.1 Mt would be added to global zinc consumption

74

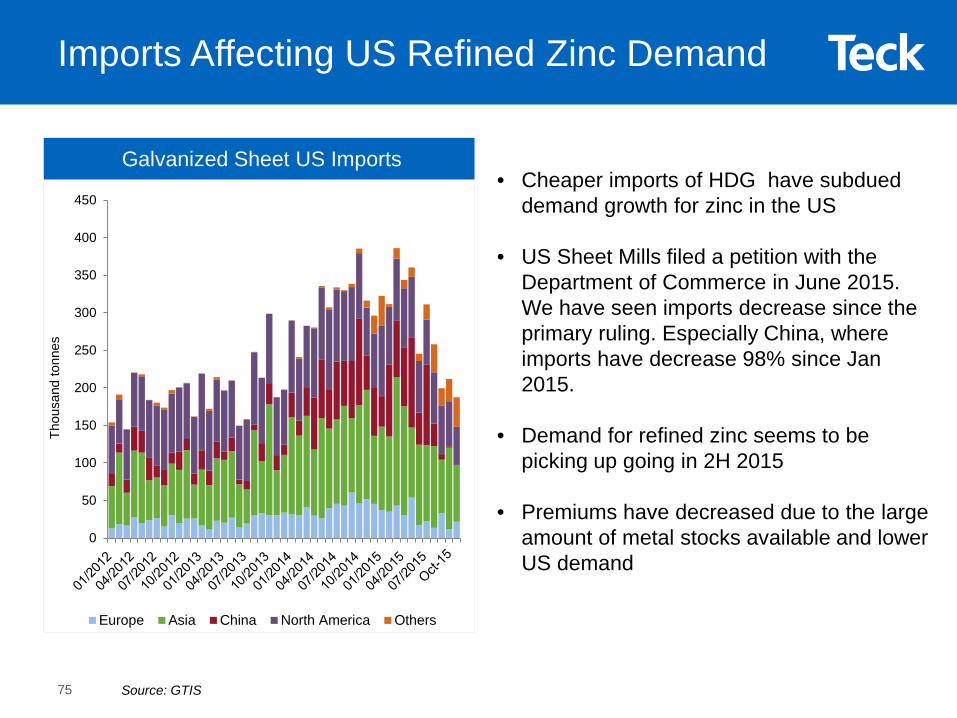

• Cheaper imports of HDG have subdued demand growth for zinc in the US

• US Sheet Mills filed a petition with the Department of Commerce in June 2015. We have seen imports decrease since the primary ruling. Especially China, where imports have decrease 98% since Jan 2015.

• Demand for refined zinc seems to be picking up going in 2H 2015

• Premiums have decreased due to the large amount of metal stocks available and lower US demand

0

50

100

150

200

250

300

350

400

450

Thou

sand

tonn

es

Europe Asia China North America Others

Galvanized Sheet US Imports

Imports Affecting US Refined Zinc Demand

Source: GTIS75

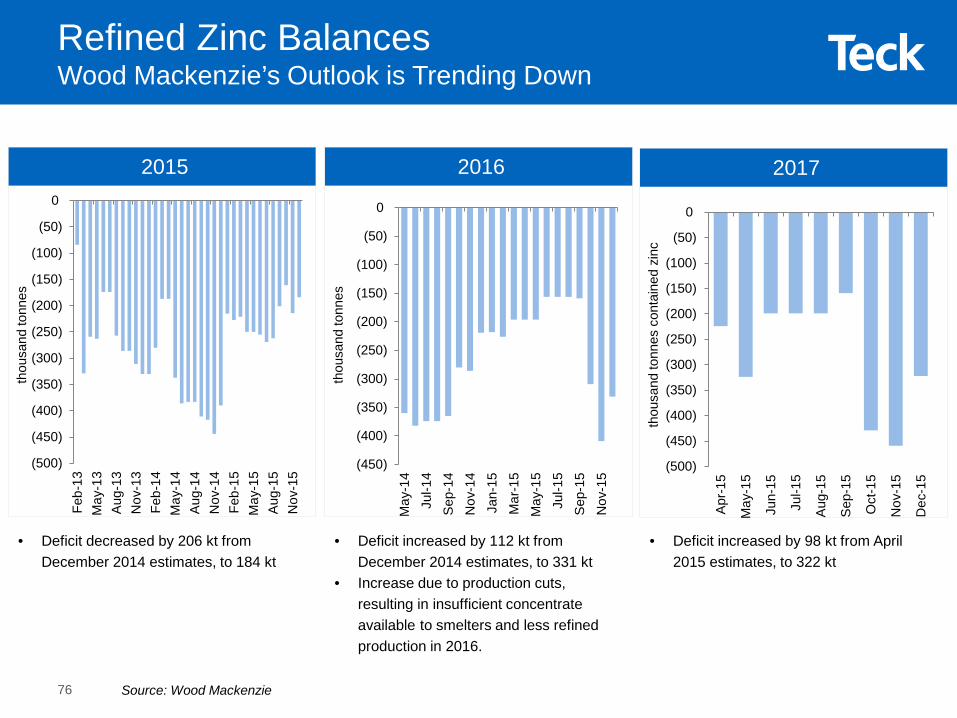

• Deficit decreased by 206 kt from December 2014 estimates, to 184 kt

• Deficit increased by 112 kt from December 2014 estimates, to 331 kt

• Increase due to production cuts, resulting in insufficient concentrate available to smelters and less refined production in 2016.

thou

sand

tonn

es

2015 2016 2017

• Deficit increased by 98 kt from April 2015 estimates, to 322 kt

thou

sand

tonn

es

thou

sand

tonn

es c

onta

ined

zin

c

Refined Zinc BalancesWood Mackenzie’s Outlook is Trending Down

(500)

(450)

(400)

(350)

(300)

(250)

(200)

(150)

(100)

(50)

0

Feb-

13M

ay-1

3A

ug-1

3N

ov-1

3Fe

b-14

May

-14

Aug

-14

Nov

-14

Feb-

15M

ay-1

5A

ug-1

5N

ov-1

5

(450)

(400)

(350)

(300)

(250)

(200)

(150)

(100)

(50)

0

May

-14

Jul-1

4S

ep-1

4N

ov-1

4Ja

n-15

Mar

-15

May

-15

Jul-1

5S

ep-1

5N

ov-1

5

(500)

(450)

(400)

(350)

(300)

(250)

(200)

(150)

(100)

(50)

0

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep

-15

Oct

-15

Nov

-15

Dec

-15

Source: Wood Mackenzie76

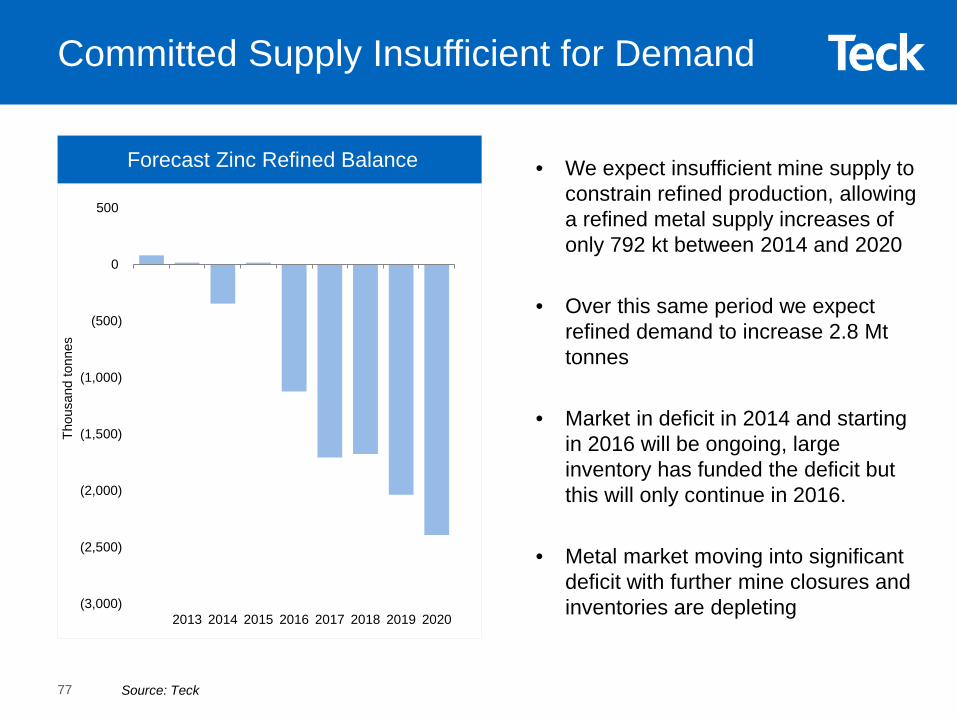

Committed Supply Insufficient for Demand

Forecast Zinc Refined Balance

Source: Teck

• We expect insufficient mine supply to constrain refined production, allowing a refined metal supply increases of only 792 kt between 2014 and 2020

• Over this same period we expect refined demand to increase 2.8 Mt tonnes

• Market in deficit in 2014 and starting in 2016 will be ongoing, large inventory has funded the deficit but this will only continue in 2016.

• Metal market moving into significant deficit with further mine closures and inventories are depleting(3,000)

(2,500)

(2,000)

(1,500)

(1,000)

(500)

0

500

2013 2014 2015 2016 2017 2018 2019 2020

Thou

sand

tonn

es

77

EnergyBusiness Unit & Markets

Building An Energy Business

Strategic diversification

Large truck & shovel mining projects

World-class resources

Long-life assets

Mining-friendly jurisdiction

Competitive margins

Minimizing execution risk

Tax effective

79

Mined bitumen is in Teck’s ‘sweet spot’

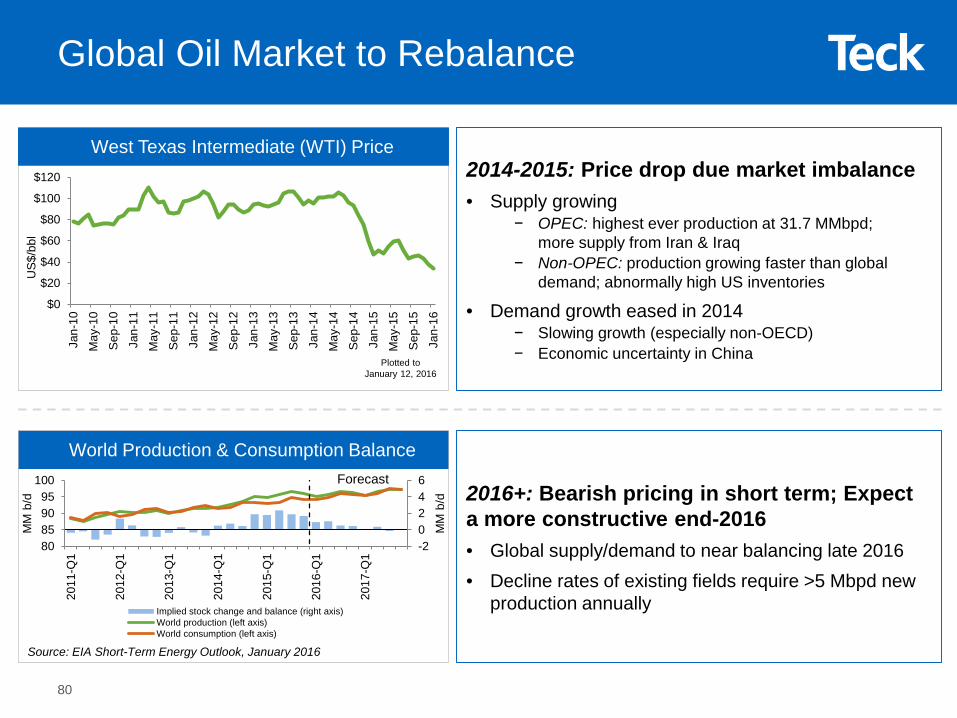

Global Oil Market to Rebalance

$0

$20

$40

$60

$80

$100

$120

Jan-

10

May

-10

Sep

-10

Jan-

11

May

-11

Sep

-11

Jan-

12

May

-12

Sep

-12

Jan-

13

May

-13

Sep

-13

Jan-

14

May

-14

Sep

-14

Jan-

15

May

-15

Sep

-15

Jan-

16

US

$/bb

l

Plotted toJanuary 12, 2016

Source: EIA Short-Term Energy Outlook, January 2016

2014-2015: Price drop due market imbalance• Supply growing

− OPEC: highest ever production at 31.7 MMbpd; more supply from Iran & Iraq

− Non-OPEC: production growing faster than global demand; abnormally high US inventories

• Demand growth eased in 2014− Slowing growth (especially non-OECD)− Economic uncertainty in China

2016+: Bearish pricing in short term; Expect a more constructive end-2016• Global supply/demand to near balancing late 2016• Decline rates of existing fields require >5 Mbpd new

production annually

West Texas Intermediate (WTI) Price

World Production & Consumption BalanceForecast

-20246

80859095

100

2011

-Q1

2012

-Q1

2013

-Q1

2014

-Q1

2015

-Q1

2016

-Q1

2017

-Q1

MM

b/d

MM

b/d

Implied stock change and balance (right axis)World production (left axis)World consumption (left axis)

80

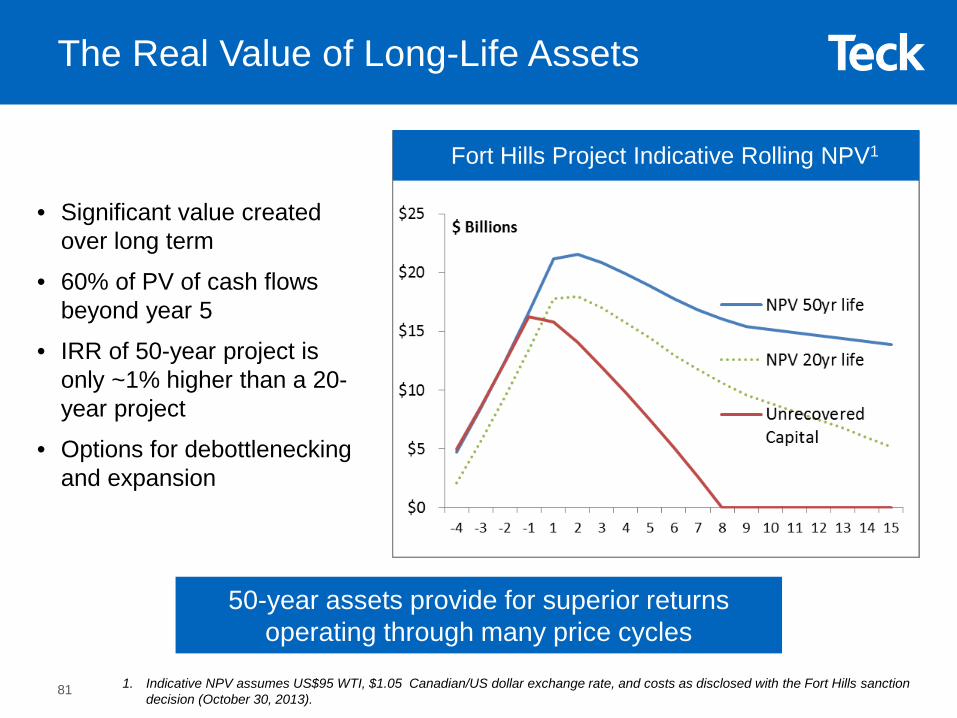

• Significant value created over long term

• 60% of PV of cash flows beyond year 5

• IRR of 50-year project is only ~1% higher than a 20-year project

• Options for debottlenecking and expansion

50-year assets provide for superior returns operating through many price cycles

The Real Value of Long-Life Assets

Fort Hills Project Indicative Rolling NPV1

1. Indicative NPV assumes US$95 WTI, $1.05 Canadian/US dollar exchange rate, and costs as disclosed with the Fort Hills sanction decision (October 30, 2013).

81

Fort Hills Is One of the Best Undeveloped Oil Sands Mining Leases

Ore grade is a function of the bitumen quantity in the deposit

TV:BIP is a ratio of the total volume of bitumen in place to the total volume of material required to be moved (like a strip ratio)

Strip Ratio vs. Ore Grade

Source: Teck

9.5

10

10.5

11

11.5

12

8910111213

Ore

Gra

de (w

t% b

itum

en)

TV:BIP

Fort Hills

Frontier

• >3 billion bbls of proven plus probable reserves of bitumen

- Production 180,000 barrels per day (bpd) of bitumen

- Teck’s share is significant at 36,000 bpd; equivalent to 13 million barrels per year (Mbpy)

• World-class resource- Average ore grade of 11.4%- Strip ratio of 1.5:1 and TV:BIP of 10.5

• Consistent production year-over-year through multiple decades

- Targeting first oil in Q4 2017- Expect 90% of planned production

capacity within 12 months

82

Minimizing Execution Risk In The Fort Hills Project

• Cost-driven schedule- “Cheaper rather than sooner”

• Disciplined engineering approach

• “Shovel Ready” • Global sourcing of engineering

and module fabrication• Balanced manpower profileSuncor has completed 4

projects of ~$20 billion over last 5 years, all at or under budget

Benefiting from Suncor’s operational and project development experience

83

• Focusing on productivity improvements- Reduced pressure on skilled labour and contractors

• Benefiting from availability of fabricators for major equipment

• Seeking project cost reductions- Exploring performance improvements with

contractors and suppliers- Building cost savings and improved productivity

expectations into current contract negotiations- Reviewing all indirect costs

Lower Oil Price Environment Provides Opportunities for the Fort Hills Project

“Major projects in construction such as Fort Hills…will move forward as planned and take full advantage of the current economic environment.

These are long-term growth projects that are expected to provide strong returns when they come online in late 2017.”

- Suncor, January 13, 2015

Enhanced ability to deliver on time and on budget84

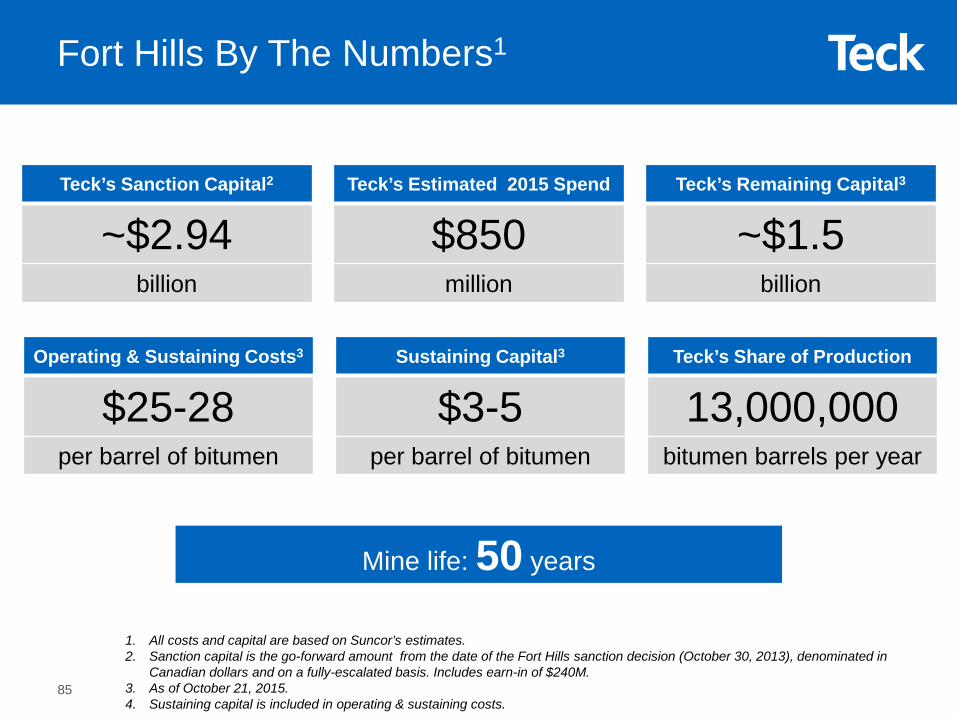

Teck’s Sanction Capital2

~$2.94billion

Teck’s Estimated 2015 Spend

$850million

Teck’s Remaining Capital3

~$1.5billion

Operating & Sustaining Costs3

$25-28per barrel of bitumen

Sustaining Capital3

$3-5per barrel of bitumen

Teck’s Share of Production

13,000,000bitumen barrels per year

1. All costs and capital are based on Suncor’s estimates.2. Sanction capital is the go-forward amount from the date of the Fort Hills sanction decision (October 30, 2013), denominated in

Canadian dollars and on a fully-escalated basis. Includes earn-in of $240M. 3. As of October 21, 2015.4. Sustaining capital is included in operating & sustaining costs.

Mine life: 50 years

Fort Hills By The Numbers1

85

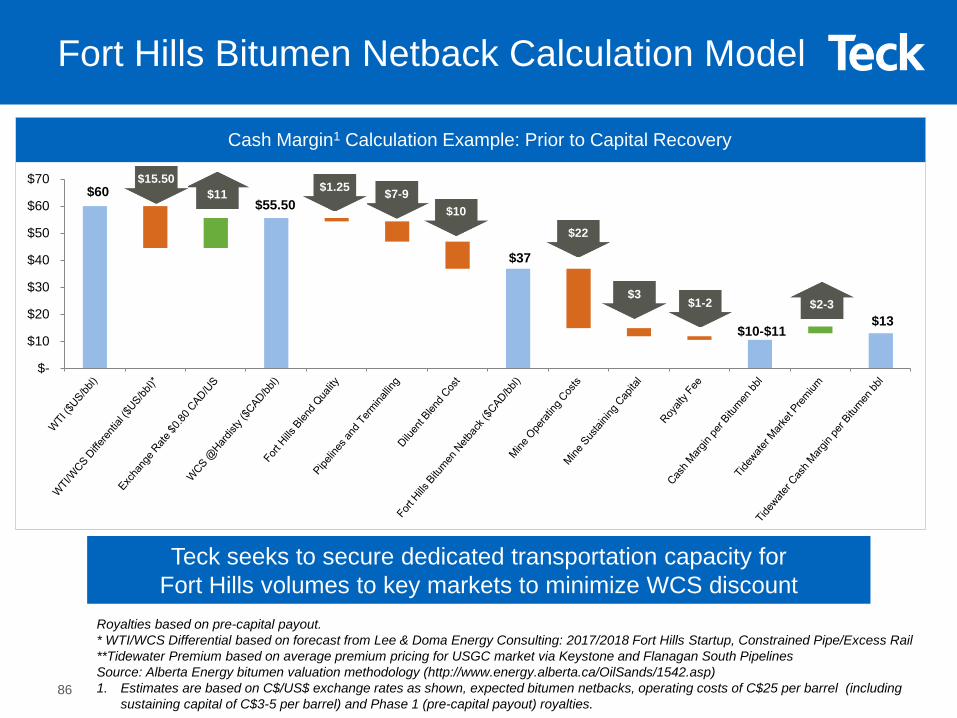

Royalties based on pre-capital payout. * WTI/WCS Differential based on forecast from Lee & Doma Energy Consulting: 2017/2018 Fort Hills Startup, Constrained Pipe/Excess Rail**Tidewater Premium based on average premium pricing for USGC market via Keystone and Flanagan South PipelinesSource: Alberta Energy bitumen valuation methodology (http://www.energy.alberta.ca/OilSands/1542.asp)1. Estimates are based on C$/US$ exchange rates as shown, expected bitumen netbacks, operating costs of C$25 per barrel (including

sustaining capital of C$3-5 per barrel) and Phase 1 (pre-capital payout) royalties.

Cash Margin1 Calculation Example: Prior to Capital Recovery

Teck seeks to secure dedicated transportation capacity for Fort Hills volumes to key markets to minimize WCS discount

Fort Hills Bitumen Netback Calculation Model

$60$55.50

$37

$10-$11 $13

$-

$10

$20

$30

$40

$50

$60

$70$11

$10

$15.50$7-9$1.25

$22

$3$1-2 $2-3

86

Source: Shorecan, Net Energy, Lee & Doma

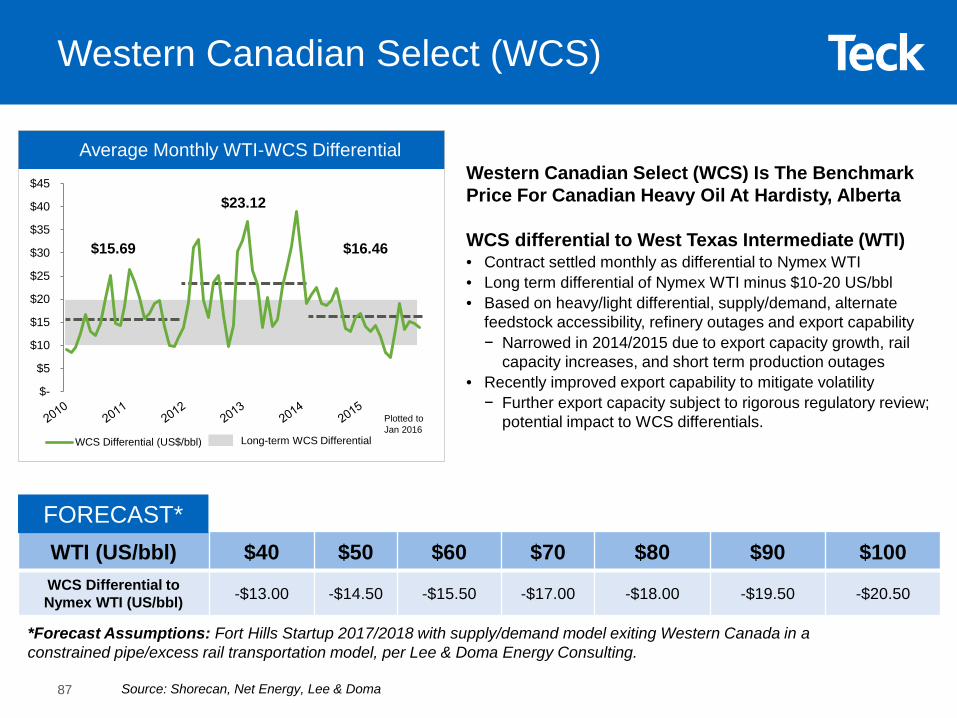

Western Canadian Select (WCS)

Average Monthly WTI-WCS DifferentialWestern Canadian Select (WCS) Is The Benchmark Price For Canadian Heavy Oil At Hardisty, Alberta

WCS differential to West Texas Intermediate (WTI) • Contract settled monthly as differential to Nymex WTI• Long term differential of Nymex WTI minus $10-20 US/bbl• Based on heavy/light differential, supply/demand, alternate

feedstock accessibility, refinery outages and export capability− Narrowed in 2014/2015 due to export capacity growth, rail

capacity increases, and short term production outages• Recently improved export capability to mitigate volatility− Further export capacity subject to rigorous regulatory review;

potential impact to WCS differentials.Plotted to Jan 2016

Long-term WCS Differential

$15.69

$23.12

$16.46

WTI (US/bbl) $40 $50 $60 $70 $80 $90 $100WCS Differential to Nymex WTI (US/bbl) -$13.00 -$14.50 -$15.50 -$17.00 -$18.00 -$19.50 -$20.50

*Forecast Assumptions: Fort Hills Startup 2017/2018 with supply/demand model exiting Western Canada in a constrained pipe/excess rail transportation model, per Lee & Doma Energy Consulting.

FORECAST*

$-

$5

$10

$15

$20

$25

$30

$35

$40

$45

WCS Differential (US$/bbl)

87

Source: Shorecan, Net Energy, Lee & Doma

Diluent (C5+) Pricing

Average Monthly WTI/Diluent (C5+) Differential

Diluent (C5+) at Edmonton, Alberta Is the benchmark contract for diluent supply for oil sands

Diluent differential to West Texas Intermediate (WTI)• Contract settled monthly as differential to Nymex WTI• Based on supply/demand, seasonal demand (high in winter, low

in summer), import outages• Long-term diluent (C5+) differential of Nymex WTI +/- $5 US/bbl

Diluent (“Pool” in Edmonton is a common stream of a variety of qualities• Diluent pool comprised of local and imported natural gas liquids

WTI (US/bbl) $40 $50 $60 $70 $80 $90 $100Diluent (C5+) Differentialto Nymex WTI (US/bbl) +$2.50 +$1.50 +$0.50 -$0.50 -$1.50 -$2.50 -$3.50

*Forecast Assumptions: Fort Hills Startup 2017/2018, using 2015 CAPP Western Canadian oil production forecast, Diluent (C5+) differentials per Lee & Doma Energy Consulting

FORECAST*

Long -term C5+ DiffPlotted to Jan 2016

($10)

($5)

$0

$5

$10

$15

$20

Jan-

10M

ay-1

0S

ep-1

0Ja

n-11

May

-11

Sep

-11

Jan-

12M

ay-1

2S

ep-1

2Ja

n-13

May

-13

Sep

-13

Jan-

14M

ay-1

4S

ep-1

4Ja

n-15

May

-15

Sep

-15

Jan-

16

US

/bbl

WTI/C5+ Diff

88

Diversified Market Access Strategy

Teck Marketing Plan for 50 kbpd Diluted Bitumen Blend

Cushing

Flanagan

Houston

Kitimat

HardistyEdmonton

Saint John

N.E. US

US Gulf Coast

Europe

Asia

TransCanada Energy East (Europe, Asia, US Gulf Coast, N.E. US)

Teck can enter long-term commitments

Enbridge Northern Gateway (Asia)

Keystone, Keystone XL (US Gulf Coast)Enbridge Flanagan South (US Gulf Coast)

Vancouver

TransMountain Pipeline (Asia)

Steele City

Asia

Europe

Asia

Superior

Sufficient Export Capacity In Place• Includes Pipeline And Rail Capability

• No shut in risk, but price risk likely

Targeting Long Term Market Access • US Gulf Coast And Deep Water Ports • Entered into commercial agreements:

• 425 kbbls Hardisty storage capacity• Pipeline capacity opportunities:

• Keystone/Keystone XL/Flanagan South to US Gulf

• TransMountain expansion to Vancouver• Energy East to East Coast

Non-committed barrels sold spot at Hardisty or nominated on common carriage pipeline

89

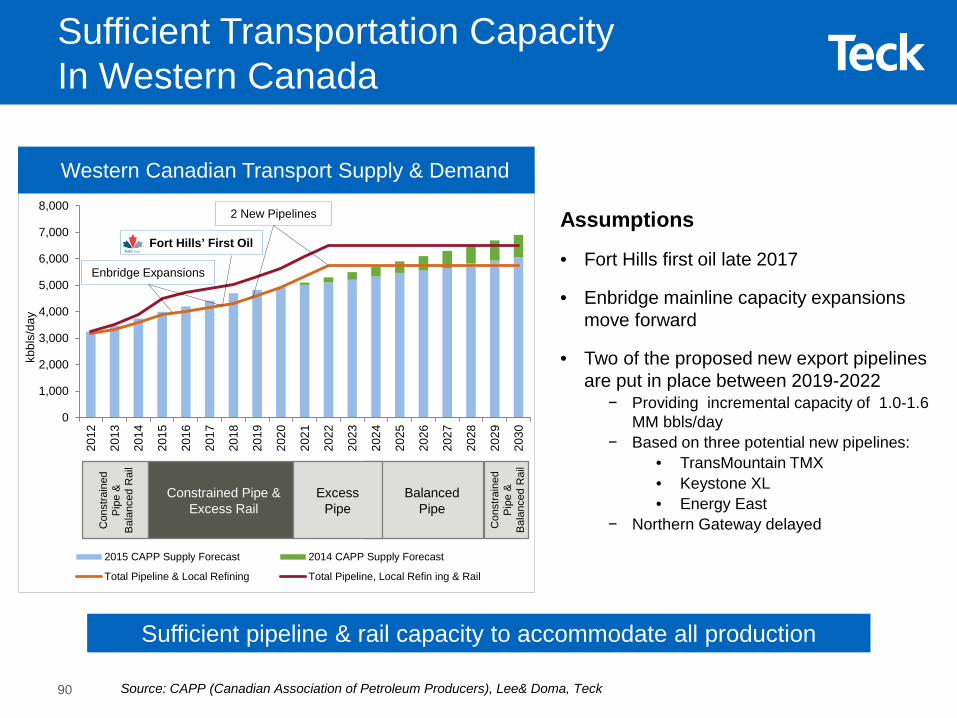

Sufficient Transportation Capacity In Western Canada

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

kbbl

s/da

y

2015 CAPP Supply Forecast 2014 CAPP Supply Forecast

Total Pipeline & Local Refining Total Pipeline, Local Refin ing & Rail

Con

stra

ined

P

ipe

&

Bal

ance

d R

ail

Constrained Pipe & Excess Rail

Excess Pipe

Balanced Pipe

2 New Pipelines

Enbridge Expansions

Western Canadian Transport Supply & Demand

Assumptions

• Fort Hills first oil late 2017

• Enbridge mainline capacity expansions move forward

• Two of the proposed new export pipelines are put in place between 2019-2022

− Providing incremental capacity of 1.0-1.6 MM bbls/day

− Based on three potential new pipelines:• TransMountain TMX• Keystone XL• Energy East

− Northern Gateway delayed

Source: CAPP (Canadian Association of Petroleum Producers), Lee& Doma, Teck

Sufficient pipeline & rail capacity to accommodate all production

Fort Hills’ First Oil

Con

stra

ined

P

ipe

&

Bal

ance

d R

ail

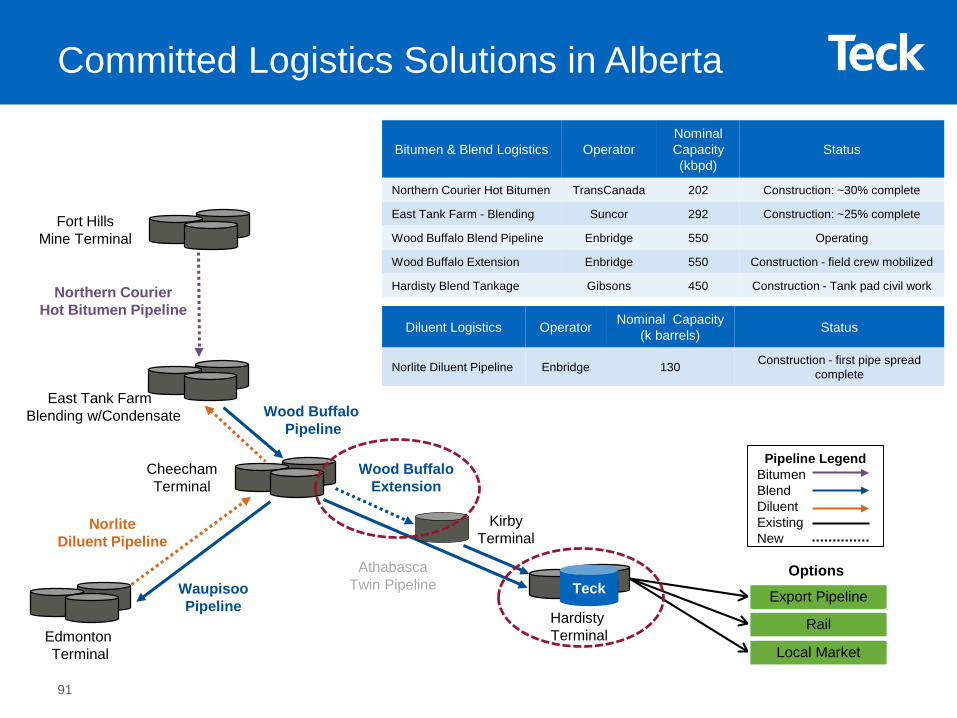

90

East Tank Farm Blending w/Condensate

Bitumen & Blend Logistics OperatorNominalCapacity(kbpd)

Status

Northern Courier Hot Bitumen TransCanada 202 Construction: ~30% complete

East Tank Farm - Blending Suncor 292 Construction: ~25% complete

Wood Buffalo Blend Pipeline Enbridge 550 Operating

Wood Buffalo Extension Enbridge 550 Construction - field crew mobilized

Hardisty Blend Tankage Gibsons 450 Construction - Tank pad civil work

Wood BuffaloExtension

NorliteDiluent Pipeline

Cheecham Terminal

Hardisty Terminal

Wood Buffalo Pipeline

AthabascaTwin PipelineWaupisoo

Pipeline

Edmonton Terminal

Fort HillsMine Terminal

Northern CourierHot Bitumen Pipeline

TeckOptions

Export Pipeline

Rail

Local Market

Pipeline LegendBitumenBlendDiluentExistingNew

Kirby Terminal

Diluent Logistics Operator Nominal Capacity (k barrels) Status

Norlite Diluent Pipeline Enbridge 130 Construction - first pipe spread complete

Committed Logistics Solutions in Alberta

91