2015 energy & sustainability priorities and predictions

TRANSCRIPT

2015 ENERGY & SUSTAINABILITY PRIORITIES AND PREDICTIONS

Presenters:Indigo Teiwes, Business Solutions Director, and Erik Makinson, Product Director, Waste both with Ecova

January 29, 2015

Survey Summary

Who: 500 Energy, Sustainability, Facilities and Finance Professionals

What: The Ecova 2015 Energy & Sustainability Predictions Report conducted by Ecova

When: November & December 2014

http://more.ecova.com/2015-Energy-Sustainability-Predictions

Agenda

Big Themes & Findings

Energy & Sustainability Program Drivers

2015 Top Priorities

Inside Water and Waste

Wrap Up

Q & A

Big Themes and Findings

Program Drivers

Broader national trend of growth in demand for electric

Shale boom (largely offset by traditional gas declines)

Storage

Volatility

Ecova’s 2014 Energy Market Highlights

Energy Price Expectations

2010 2011 2012 2013 2014 2015

Retail Price of Electricity in Commercial Sector

10.19 10.23 10.09 10.29 10.69 10.88

Natural Gas Price Commercial Sector 9.45 8.90 8.11 8.08 8.99 9.05

EIA Retail Commercial Price Data (U.S. Average)

Survey Results Ecova Projections

Relatively flat in 2015

− Higher NG reserves and production

− Lower natural gas supply costs

− Increasing distribution costs

− Electric prices more closely tied to NG (coal plant capacity being replaced with gas-fired generation)

Energy Price Implications

Communication is essential

– Communicate with all company stakeholders early and often in order to mitigate budget risk

– Expectations for energy prices vary greatly across energy manager’s and accounting/finance

• Impacts on budgeting and forecasting

Be prepared with a long-term energy strategy

– Nationally, energy prices may flatten in 2015, this won’t last for long

– Wholesale electricity prices will become even more strongly correlated to gas

• Higher potential for energy price volatility in the coming years

Resource Trends

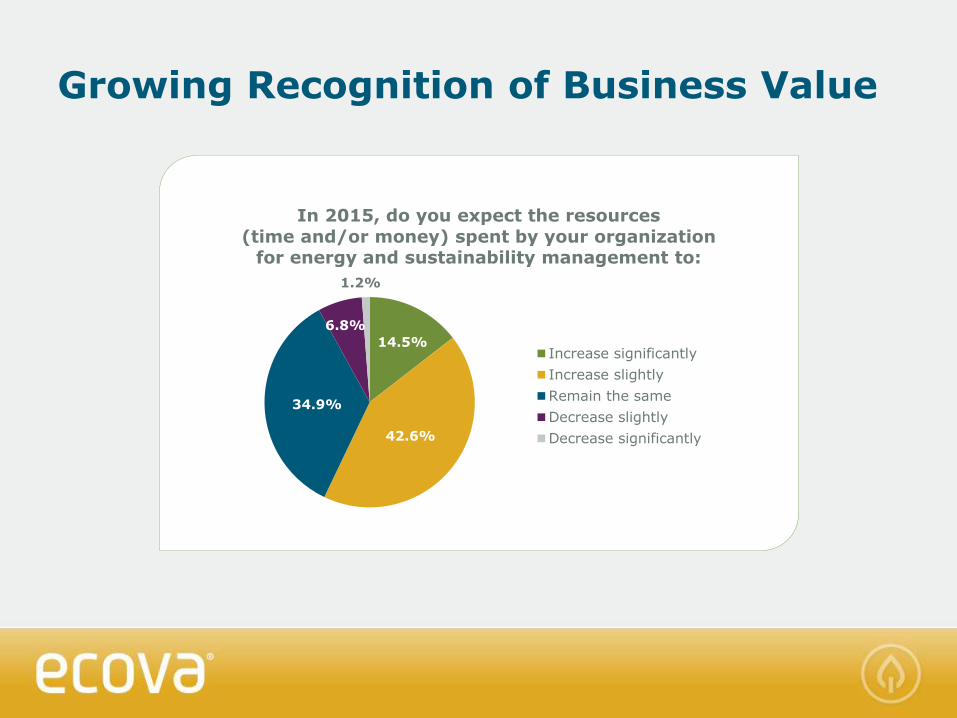

Growing Recognition of Business Value

14.5%

42.6%

34.9%

6.8%

1.2%

In 2015, do you expect the resources

(time and/or money) spent by your organization for energy and sustainability management to:

Increase significantly

Increase slightly

Remain the same

Decrease slightly

Decrease significantly

It Takes a Village

Growing stakeholder diversity in energy & sustainability programming

12.9%

13.4%

14.4%

16.4%

21.1%

3.7%

17.9%

What is your primary role/job function?

Finance / Accounting

Corporate

Sustainability

Energy management

Facility management

Energy procurement

Other (please specify)

Your Peers Rate Top Priorities for 2015

48.2%

52.3%

55.3%

Implement no cost, low cost efficiency efforts was

the top priority for leveraging energy data in 2015.

Implement no cost, low cost efficiency efforts

Support strategic energy and sustainability management plans/programs

Identify and implement capital expenditures to support energy efficiency projects

Lighting Leads (or LEDs?)

Energy Management Systems

Real-time data

Increased insights

Remote control

Industry Highlights

– Retail leading the way: reduced consumption and high utilization of EMS

– Restaurants have opportunity: energy intensive, 40% have made no investment to date

Nearly

50 percentof respondents

have energy and

building management

systems installed.

Energy’s Not the Only Game in Town …

Why Worry about Water?

Rising water rates and rate variability

Significance of water spend

Increased pressure on water rates

Savings opportunities in bill management and consumption reduction

New York is seeing some of the largest price increases since 2008.

Washington DC and Delaware are seeing steep price increases.

Water on the R ise

Rising Water Costs

Small Box = 8% CAGRC Stores = 8% CAGRCasual Dining = 8% CAGRQuick Serve = 7% CAGRBig Box = 7% CAGR

Since 2008, water rates have increased by approximately 30% across all industries.

Waste Costs Piling Up

110.0

112.0

114.0

116.0

118.0

120.0

122.0

124.0

126.0

128.0

130.0

Producer Price Index:Waste Collection & Remediation Services

(Seasonally Adjusted, Base Year December 2008)

Regulation On the Increase

Classic waste regulation

New trend: focus on waste focus

Regional and/or state

– City level (i.e. Seattle, WA)

– State level (i.e. AB341, CA’sMandatory Commercial Recycling Law)

Extended Producer Responsibility (EPR)

– ~25 states have e-waste laws

Most Effective Waste Strategies

2015 Waste Priorities

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

Support Zero

Waste strategy

(i.e. reporting

landfill diversion)

Auditing waste

hauler contracts

Optimizing service

levels (right-sizing)

Improve pricing

and terms in

procurement

events

In your current role, what are your top priorities

for leveraging your waste data in 2015? (Check all that apply)

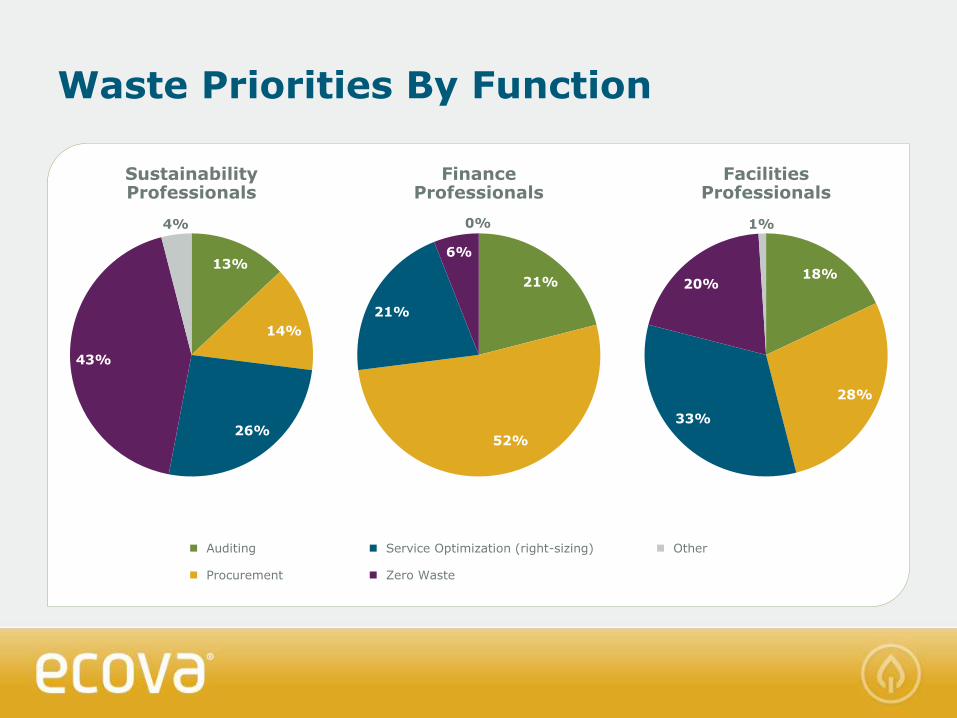

Waste Priorities By Function

Sustainability Professionals

Finance Professionals

Facilities Professionals

13%

14%

26%

43%

4%

21%

52%

21%

6%

0%

18%

28%

33%

20%

1%

Auditing Service Optimization (right-sizing) Other

Procurement Zero Waste

Benefits of Strategy Coordination

http://www.ecova.com/media/486976/24_hour_fitness_case_study.pdf

THE COMBINATION OF

PROCUREMENT AND RIGHT SIZING

WILL CONTRIBUTE TO AN ESTIMATED

SAVINGS BETWEEN 40% AND 50%

BY 2014.

Key Takeaways

Continued growth in drivers and investments

Integrated strategic plans

Diversity of stakeholders and perspectives and priorities

Communicate and plan appropriately for market price changes

Make the most out of managing waste

Upcoming Ecova Webinars

INSIDE ENERGY & SUSTAINABILITY SERIES

Watching your Waste: Deriving Value from a Foundation of Data – Thursday, February 19th at 11am PST

Quarterly Energy Market Watch – Thursday February 26th

at 11am PST

How to Make Your Utility Bill Data Work for You –Thursday, March 12th at 11am PST

Questions, comments, suggestions? [email protected]

Q&A

Thank you!