2015 bswift benefits studymarketing.bswift.com/acton/attachment/5166/f-00c1/1/-/-/-/-/2015...the...

TRANSCRIPT

2015 bswift Benefits StudyThe tech-enabled evolution (not revolution)from paternalism to consumerism

JUNE 2015

Published by:

2 0 1 5 B S W I F T B E N E F I T S S T U DY

2

BackgroundMany pundits within the health insurance and benefits world have been talking

about a “revolution” in benefits. Most notably, they’ve been predicting rapid

employer adoption of private exchanges on the premise of presenting employers

with a radically new and different value proposition.

Rich Gallun, CEO, bswift, sees the situation differently: “The trends in the

employer market speak to an ‘evolution’—a journey that has been occurring

incrementally over the past 15 years—away from paternalism and toward

consumerism.” Taking a close look at what a private exchange offers employers,

Gallun notes: “The culmination of years of iterative technology development has

made it possible for employees to take ownership of their benefits, particularly

during the annual shopping and enrollment period, but also all year round

through deeper engagement with available health care tools and resources.”

Laurel Pickering, President and CEO of the Northeast Business Group on Health,

expands on two initiatives in which large employers are investing to reduce costs

and improve the quality of their health benefits programs: “First is offering High

Deductible Health Plans (HDHPs). Today, employers are implementing these

plans much more rapidly. Second, as a continuation of the consumer choice

logic that began with HDHPs, private exchanges have captured the attention

of benefits administrators over the past year. Private exchanges with defined

contribution allow employees to spend and save their benefits dollars as they

choose. While today private exchanges are primarily a vehicle for consumer

choice and administrative outsourcing, their future rests on their ability to

engage and support consumers in health spending and health choices.”

The 2015 bswift Benefits Study shows modest early adoption rates for private

exchanges for active employees (5% of employers with more than 500

employees, as of early 2015) and questions the adoption numbers reported by

many studies and the media, given the absence of a standardized definition of

the term “private exchange.” To help employers understand the trends “on the

ground” for 2015 and 2016, the focus of this study is on the practical initiatives

in which employers are investing today to reduce benefits costs while engaging

employees in a more consumer-centric, retail experience. The ultimate goal is

that employees could truly manage their own health and benefits investment.

This year’s report provides further evidence of an overall “megatrend” toward

consumerism by way of a sustained increase in the use of the following

initiatives: 1) employee self-service (online enrollment); 2) wellness incentives

and outcomes-based wellness programs; and 3) defined contribution with more

plan choices (especially HDHPs) and benefits options for employees.

Key FindingsEmployers push for more employee “skin in the game” for wellness: 40%

of large employers with wellness incentives

now offer annual incentives of $500 or

more, up from 29% in 2013. After many

years of gradually introducing wellness

program incentives and evaluating their

potential, employers are now using

significant incentives to encourage

employees to improve their health.

Biometrics continue to grow in usage by employers: The use of biometric tests

has grown to 49% of large employers

with wellness programs, and completion

of biometric tests continues to be one of

the top incentivized activities — by 67%

of those large employers with wellness

incentives.

Smoking cessation programs, social fitness and nutrition challenges make huge gains: For large employers with

wellness programs, the offer of smoking

cessation programs jumped from 52%

in 2014 to 71% in 2015, and social

challenges increased from 26% to 34%.

Employers are continuing to expand their

commitment to wellness programs and

expand avenues for employees to engage

in health improvement.

Premium discounts and surcharges remain top incentives; contributions to HSAs and HRAs are growing as use of cash incentives decreases. The most common type of incentive for

large employers is premium discounts/

surcharges, used by 61% of respondents

that offer wellness incentives. From 2014

to 2015, cash and gift cards declined

from 56% to 45% of large employers,

and HSA/HRA contributions increased

from 17% to 22%, demonstrating

employer interest in tax-advantaged

payment mechanisms.

2 0 1 5 B S W I F T B E N E F I T S S T U DY

3

The study was conducted in January and February 2015 among 500 benefits

decision makers at organizations that offer health benefits. Respondents were

required to be employed at organizations with 50 or more employees and

to have responsibility in HR/benefits/insurance, designing benefits plans and

selecting benefits carriers.

The respondents were divided into two groups: large employers with more

than 500 benefits-eligible employees and small employers with 50 to 500

benefits-eligible employees. This study focuses first on data collected from large

employers; key findings for employers with 50 to 500 employees appear at the

end of the study.

Companies Remain Committed to Workplace Wellness2014 marked another year of steady progress for workplace wellness programs.

Although some academics continue to question the efficacy of wellness

programs, the employer community remains committed to workplace wellness

and to putting more employee “skin in the game.” Inspired by positive results

from their own implementations as well as those of their peers, 85% of large

employers continue to invest in wellness programs, with significant upticks in

the use and dollar amount of wellness incentives and also in the deployment of

“social” wellness initiatives such as fitness challenges.

Increasing numbers of employers are also realizing the positive impact that

health and wellness programs can have on both presenteeism and corporate

culture. One need only scroll through the pages of the latest Fortune 100 Best

Companies to Work For list to recognize that workplace wellness programs

are part of the framework that defines leading companies. And employees

are responding: In a related Fortune survey, employees evaluate current and

prospective employers based on their commitment to health initiatives.

Wellness initiatives continue to be an integral component of employee benefits

offerings, with many CEOs and HR leaders believing that these programs are

among their most valuable contributions to their employees. Brad Wolfsen,

Senior Vice President, bswift, notes: “In short, workplace wellness has become

part of the fabric of American business culture.”

Key Findings (continued)

Adoption rates for private exchanges are more modest than have been widely publicized and predicted: 5% of large employers

reported that they currently have a

private exchange in 2015, and of those

that do not, 6% are considering a private

exchange for 2016.

Consumer choice and defined contribution are on the horizon: 17% of large employers are considering

defined contribution for 2016; of those

employers, the top initiative is to add

more health plan options in 2016.

Employee self-service continues to grow, but many employers are not taking full advantage of automation: The use of employee self-service for

enrollment continues to grow every

year; surprisingly, however, 25% of

large employers still do not offer online

enrollment options for new hires, and

18% do not provide automated alerts to

remind new hires of looming enrollment

deadlines.

The growing complexity of benefits takes a toll on HRIS/payroll vendors: The decline in market share for

HRIS/payroll vendors in the benefits

administration marketplace (from 60%

in 2013 to 45% in 2015) and the low

Net Promoter Scores (NPS) registered by

these vendors suggest that the demands

of benefits technology are escalating,

and these vendors are having difficulty

keeping up.

The 2015 bswift Benefits Study, commissioned by bswift and conducted by

Employee Benefit News, investigates trends in benefits technology, wellness

programs and defined contribution/private exchanges, comparing this year’s

numbers to those reported in 2013 and 2014.

2 0 1 5 B S W I F T B E N E F I T S S T U DY

4

Employers Push for Greater Employee “Skin in the Game”40% of large employers rate health cost savings as the primary objective for wellness programs (Figure 1). As a result, most employers (79% of large employers with wellness programs) seek to align employee

incentives with their own and shift from a paternalistic approach for health benefits to a more consumer-based

model that leverages the power of wellness incentives.

But some of these employers are voicing concern that the Affordable Care Act (ACA) regulations released

last year place restrictions on their efforts. The latest rules have certainly created a challenge for employers

that feature incentives for wellness programs, particularly those paying incentives to employees based on

health outcomes. “It’s not as easy to move to outcomes-based,” notes David Olsen, Director, Benefits, Lennox

International, referring to the impact of the ACA regulations. “We needed to come up with alternative

standards, ensure our plan documents incorporated wellness appropriately, provide extensive legal review

of the requirements and develop a robust communication strategy to ensure we communicated the

requirements of the program in a comprehensive and compliant manner.”

Despite these challenges, however, more employers have moved to outcomes-based programs (Figure 2). In

2015, 26% of large employers with wellness programs offer incentives for meeting or exceeding biometric

thresholds.

Michael Dermer, Senior Vice President and Chief Incentive Officer, Welltok, observes: “There has been

significant growth in the total incentives used by employers over the last five years. With that growth, there is

also the desire for more immediate-term ROI and the need to optimize the use of those dollars.”

1%

2%

2%

16%

37%

40%

1%

1%

6%

19%

33%

40%

Reduced employee absences

Increased employee productivity

Employee retention/satisfaction

Health outcomes

Employee engagement/participation

Health costsavings/avoidance

2015 2014

Figure 1—Key Performance Indicators (KPIs) for Wellness Programs, Large Employers What is the most important metric you use to evaluate the success of your wellness program?

>500 employees Base = Employers offering wellness programs Source: SourceMedia Research, 2014, 2015

2 0 1 5 B S W I F T B E N E F I T S S T U DY

5

Indeed, to help motivate employees to take charge of their health, employers are increasing the dollar

amount available for wellness incentives; 40% of employers now offer incentives of $500 or more, as

compared to 36% in 2014 and 29% in 2013 (Figure 3).

Premium discounts and surcharges continue to be the most frequently used incentive type (Figure 4). This year also saw a major shift toward funding Health Savings Accounts (HSAs) and Health Reimbursement

Arrangement (HRA) accounts (as opposed to cash rewards), as these consumer-directed accounts gain

greater market share. The employee and employer tax advantages of pre-tax HSA and HRA contributions

combined with HDHPs make account-based contributions better than cash for maximizing the value put in

the employee’s pocket.

40%

40%

>500 employees Base = Employers offering incentives for wellness programs Source: SourceMedia Research, 2013, 2014, 2015

15%

34%

51%

53%

74%

24%

62%

56%

65%

77%

26%

45%

53%

67%

72%

Meeting or exceedingbiometric thresholds

Wellnesseducation/classes

Tobacco use/tobacco non-use

Completion of biometric tests

Completion of HealthRisk Assessments (HRA)

2015 2014 2013

Figure 2—Incentivized Wellness Programs, Large EmployersFor which of the following wellness programs, if any, does your organization offer incentives (i.e., “carrots”) or disincentives (“sticks”)?

>500 employees Base = Employers offering incentives for wellness programs Source: SourceMedia Research, 2013, 2014, 2015

12%

10%

10%

33%

30%

26%

25%

24%

24%

26%

27%

33%

3%

9%

7%

2013

2014

2015

Less than $50 $50 to $249 $250 to $499 $500 to $1,000 More than $1,000

Figure 3—Investment in Wellness Incentives per Employee, Large Employers What is the annual dollar amount per employee for wellness incentives?

2 0 1 5 B S W I F T B E N E F I T S S T U DY

6

Employers Continue to Expand on Wellness Programs in the Workplace2015 saw a signifi cant increase in smoking cessation programs, up about 20 percentage points over last year’s

numbers, with 71% of employers offering these programs (compared to 52% in 2014). “Smoking cessation is a

relatively easy incentive to implement,” notes Gene Baker, Vice President, Total Rewards, Iron Mountain. “There

is universal agreement that tobacco is unhealthy, and smoking cessation programs are effectively the gateway

program for wellness.”

While the vast majority of employers (77%) rely on self-reported affi davits from employees, 23% now use

biometric tests to validate their employees’ tobacco-free status. As the cost of biometric tests decline and

available incentives increase, it makes sense that employers are adopting a “trust but verify” approach to

these incentives. This is consistent with the larger number of employers that now also leverage dependent

verifi cation programs (as discussed in the “Employee Self-Service” section below).

In tandem with the increase in clinical outcomes as the criterion by which to measure wellness program

success, employers’ use of biometric tests (specifi cally blood pressure, cholesterol and BMI) is also growing.

By developing health profi les of its employee population, employers can target areas of focus and track the

progress of their wellness programs over time.

“Capturing health data enables us to identify employee pockets to target for improvement, whether it is a particular

location or subsidiary. We also need to be able to show our leadership that we’re making strides in improving our

employees’ overall health,” states Keith Kolodgie, Director of Employee Benefi ts Services, MaineHealth.

>500 employees Base = Employers offering incentives for wellness programs Source: SourceMedia Research, 2013, 2014, 2015

Figure 4—Types of Wellness Incentives, Large EmployersWhat types of incentives or disincentives does your organization use?

Additional paid time off (e.g., vacation days)

Reduced co-pay/co-insurance

Eligible for richerplan and/or

lower deductible

Additional contributionsto a Health Savings

Account (HSA) orHealth Reimbursement

Arrangement (HRA)

Cash, gift cards or sweepstakes

Health insurancepremium discounts,

credits, surchagesor penalties

61%

64%

64%

45%

56%

48%

22%

17%

12%

8%

6%

4%5%

6%

2%2%

3%

2015 2014 2013

7%

2 0 1 5 B S W I F T B E N E F I T S S T U DY

7

The use of social challenges to support fitness and weight-loss initiatives is increasing, from 26% of employers

in 2014 to 34% in 2015. Making wellness a year-round program can have a favorable impact on employee

engagement rates and also serves to shift the workplace social dialogue to health and nutrition (Figure 5). “We are seeing employers use social challenges more often and for longer periods of time — their goals are to

make healthy behavior and wellbeing a workplace standard,” states Dr. Rajiv Kumar, Founder and CEO, ShapeUp.

This year reveals a marked recovery in wellness participation rates over last year. Nearly half of large companies

reported achieving participation rates over 50%. This represents a return to 2013 levels following the 2014 dip

to 39%, most likely the result of the distraction that ACA regulations wrought on employers last year.

The data shows that employee participation rates are impacted by the dollar amount of incentives. Only 12%

of employers offering annual incentives of less than $50 generate employee participation rates of higher than

50% (Figure 6). On the other hand, 67% of employers offering between $500 and $1,000 in incentives and

79% of employers offering more than $1,000 have participation rates of 50% or higher.

This demonstrates the power of incentives to drive employee participation in wellness programs.

While incentives go a long way toward motivating high levels of participation, the dollar amount of the

incentive alone does not guarantee high participation. No employer wants to be among the 21% of large

employers offering more than $1,000 in incentives and still suffering low participation rates (50% or less).

Program and incentive designs, in addition to effective employee communication, also matter.

1%

5%

33%

17%

29%

52%

52%

5%

13%

26%

41%

57%

52%

2%

16%

24%

34%

49%

58%

60%

67%

71%

Discounts on healthy food

Clinics and/or medical professionals/coaches at worksite

*Subsidized gym memberships

Biometric tests

*Lifestyle modification coaching(e.g., weight loss) online or via phone

Health Risk Assessments (HRA)

*Mental health/emotional wellnesscoaching online or via phone

Smoking cessation

2015 2014 2013

Fitness/weight loss challenges or activities

>500 employees Base = Employers offering wellness programs Source: SourceMedia Research, 2013, 2014, 2015*Data not available for all years

Figure 5—Employee Wellness Programs, Large Employers Which wellness programs or initiatives did/does your organization currently have in place for its employees?

2 0 1 5 B S W I F T B E N E F I T S S T U DY

8

Private Exchanges: Modest Start; No Common DefinitionConsulting firms Accenture and Oliver Wyman both predict that as many as 40 million individuals will enroll

in private exchanges by 2018, which could represent up to 33% of employees nationally. PwC estimates that

nearly half of all employers have either implemented or are considering using a private exchange for active

employees before 2018. Largely driven by expectations of higher revenue, sponsors of private exchanges—

looking to position messages about the value of consumer choice and the potential for cost savings—

are investing heavily. Every major insurer and national broker/consultant appears to have a

private exchange strategy.

The findings in the bswift Benefits Study show that the rate of private exchange adoption has been modest to

date, with some progress expected for 2016 (Figure 7). 5% of large employers self-reported that they are in

private exchanges as of 2015. Of those currently not offering a private exchange, an additional 6% of these

large employers are “considering” a private exchange for 2016 and possibly more in the years thereafter.

>500 employees Base = Employers offering incentives for wellness programs Source: SourceMedia Research, 2015

Less than 25% 26% to 50% 51% to 75% Greater than 75%

7%

4%

14%

30%

14%

24%

63% 25% 6% 6%

47% 16% 13%

35% 41% 11%

39% 28%

43% 36%

More than $1,000

$500 to $1,000

$250 to $499

$50 to $250

Less than $50

Figure 6—Participation Rates by Incentive Amount, Large EmployersIn 2015, what is the employee participation rate of your wellness program? (with breakouts by the annual dollar amount per employee for wellness incentives)

6%

77%

17%

Base = >500 employees Source: SourceMedia Research, 2015

67%

71%

Do you consideryour 2015 benefits program to be a private exchange?

Don’t know/not sure

5%Yes

No

Don’t know/not sure

Among those not offering a private exchange in 2015, are you consideringa private exchange for 2016?

83%

11%

Figure 7—Private Exchanges 2015 Actual vs. 2016 Considering, Large Employers

2015 2016

2 0 1 5 B S W I F T B E N E F I T S S T U DY

9

Real confusion exists in the marketplace regarding the ambiguity (or variation) surrounding the definition of a

“private exchange.” According to Mike Smith, Director of Exchange Solutions, Lockton Benefit Group:

“Many people are confused by the various approaches to private exchanges. Some define a private exchange as

a vibrant marketplace of expanded plans and choices for employees, powered by decision support technology

and underlying defined contribution. Others say it’s a metallic structure of plans (platinum, gold, silver and

bronze) from competing carriers, underwritten on a fully insured basis. Still others say a private exchange is just

benefits administration on steroids and sometimes ‘free’ with the inclusion of voluntary benefits.”

Two components defining private exchanges seem universally held: first, expanding plan choice for

employees or “consumers”; and second, leveraging consumer-facing technology to help users make more

educated and personalized decisions. Michelle Dietz, Associate Vice President of Partner Integration, Unum,

puts it this way:

“We hear discussions about whether private exchanges are growing or whether they will survive long

term. While the terms ‘exchange’ or ‘marketplace’ might change, what will remain is the shift towards

technology-enabled benefits. Platforms help employers offer a wider set of benefits choices among the

employee population, fostering the personalization of benefits. Employers want to help employees make

selections, and they want to do it using a platform that offers some employer advantages too, such as ease of

administration and compliance reporting.”

“When asked if they are considering a private exchange for next year,” notes Don Garlitz, Senior Vice

President, bswift, “the majority of our clients would say ‘no.’ And many that say ‘yes’ are often just

adding more health plan options to their employee offering—especially an HDHP and sometimes also a

narrow network.”

The results of this year’s Benefits Study lead us to the view that a private exchange is a benefits offering that

presents multiple benefit and plan choices—with employees engaged as consumers, selecting plans that best

fit their individual needs, often with help from shopping and decision support tools. The health plan designs,

network arrangements, supplemental plan offerings and funding models may vary widely from employer to

employer, but the constant theme is a focus on tech-enabled, consumer choice and engagement.

Consumer Choice Is a Real Trend: Defined Contribution, Decision Support and Expanded Plan ChoicesThis study identifies three prevailing employer trends. First, the percentage of employers using defined

contribution for health and welfare benefits is increasing (Figure 8). The number currently utilizing a defined

contribution approach is small, but significantly more employers will be looking at it for 2016.

67%

71%

Figure 8—Defined Contribution, 2015 vs. 2016, Large EmployersIs your organization currently offering or considering a “defined contribution” approach for any of its health and welfare benefits for active employees?

Don’t know/not sure

Base = >500 employees Source: SourceMedia Research, 2015

10%

12%

77%

Offering for 2015 Considering for 2016

28%17%

55%

Yes

No

Don’t know/not sure

2 0 1 5 B S W I F T B E N E F I T S S T U DY

10

Second, one third (33%) of all large employers currently provide employees with decision support as part of

the shopping and enrollment process (Figure 9).

Third, a growing contingent of employers intends to introduce more plan choices, network options and carrier

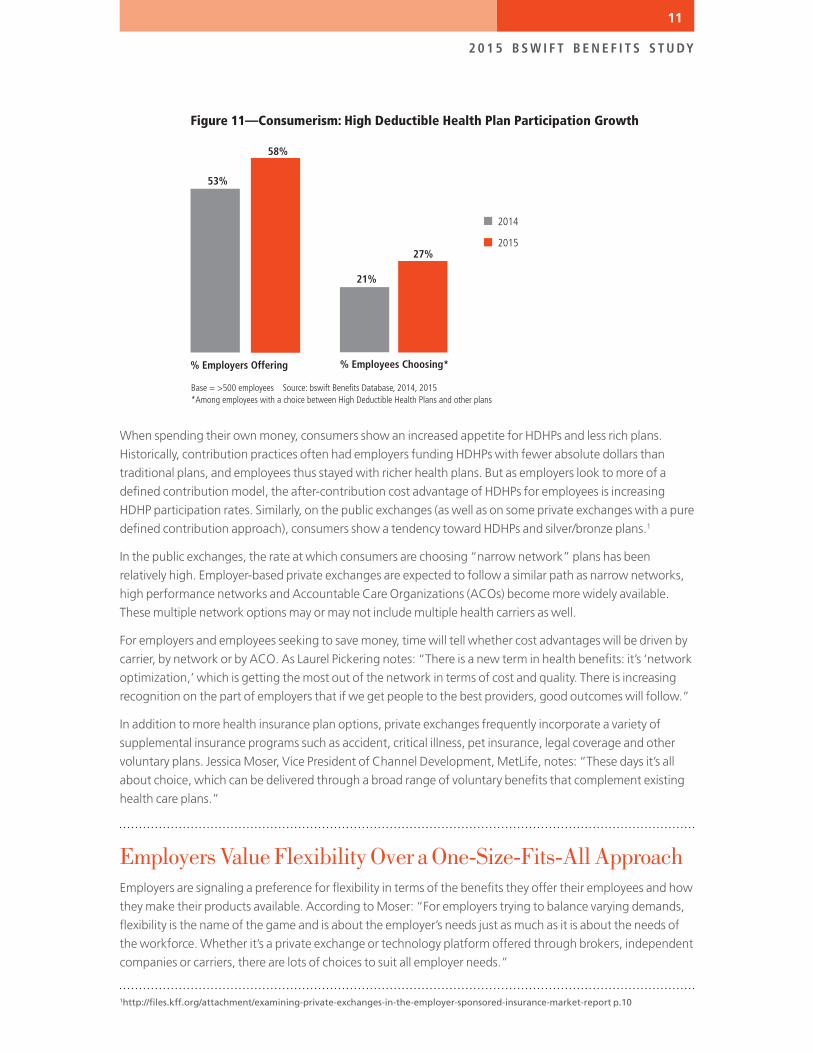

options (Figure 10). More employers are offering HDHPs to employees today (58% of large employers in 2015,

up from 53% in 2014, based on the bswift Benefits Database), and more employees are choosing these plans

(27% of employees with a choice of HDHPs and other plans in 2015, up from 21% in 2014) (Figure 11).

Figure 9—Decision Support Tools, Large Employers As of January 2015, do you/will you offer decision support tools at the point of enrollment that help employees select health and/or other benefit plans?

Don’t know/not sure

Base = >500 employees Source: SourceMedia Research, 2015

Yes

No

Don’t know/not sure

33%

55% 12%

Figure 10—Expected Health Plan Changes, 2014 vs. 2015, Large EmployersWhich of the following health plan changes do you plan to make as a result of implementing a “defined contribution” approach?

50%

More health plan options

More carrier choices

More network options

Move from self-insuredto fully insured

Don't know/not sure

2015 2014

50%

40%

20%

10%

17%

6%

9%

6%

28%

38%

>500 employees Base = Employers offering or considering a defined contribution approach in 2016

Source: SourceMedia Research, 2014, 2015

2 0 1 5 B S W I F T B E N E F I T S S T U DY

11

When spending their own money, consumers show an increased appetite for HDHPs and less rich plans.

Historically, contribution practices often had employers funding HDHPs with fewer absolute dollars than

traditional plans, and employees thus stayed with richer health plans. But as employers look to more of a

defined contribution model, the after-contribution cost advantage of HDHPs for employees is increasing

HDHP participation rates. Similarly, on the public exchanges (as well as on some private exchanges with a pure

defined contribution approach), consumers show a tendency toward HDHPs and silver/bronze plans.1

In the public exchanges, the rate at which consumers are choosing “narrow network” plans has been

relatively high. Employer-based private exchanges are expected to follow a similar path as narrow networks,

high performance networks and Accountable Care Organizations (ACOs) become more widely available.

These multiple network options may or may not include multiple health carriers as well.

For employers and employees seeking to save money, time will tell whether cost advantages will be driven by

carrier, by network or by ACO. As Laurel Pickering notes: “There is a new term in health benefits: it’s ‘network

optimization,’ which is getting the most out of the network in terms of cost and quality. There is increasing

recognition on the part of employers that if we get people to the best providers, good outcomes will follow.”

In addition to more health insurance plan options, private exchanges frequently incorporate a variety of

supplemental insurance programs such as accident, critical illness, pet insurance, legal coverage and other

voluntary plans. Jessica Moser, Vice President of Channel Development, MetLife, notes: “These days it’s all

about choice, which can be delivered through a broad range of voluntary benefits that complement existing

health care plans.”

Employers Value Flexibility Over a One-Size-Fits-All ApproachEmployers are signaling a preference for flexibility in terms of the benefits they offer their employees and how

they make their products available. According to Moser: “For employers trying to balance varying demands,

flexibility is the name of the game and is about the employer’s needs just as much as it is about the needs of

the workforce. Whether it’s a private exchange or technology platform offered through brokers, independent

companies or carriers, there are lots of choices to suit all employer needs.”

2013

2014

2015

Don’t know/not sure

Base = >500 employees Source: bswift Benefits Database, 2014, 2015*Among employees with a choice between High Deductible Health Plans and other plans

Figure 11—Consumerism: High Deductible Health Plan Participation Growth

2014

2015

58%

53%

27%

21%

% Employers Offering % Employees Choosing*

1http://files.kff.org/attachment/examining-private-exchanges-in-the-employer-sponsored-insurance-market-report p.10

2 0 1 5 B S W I F T B E N E F I T S S T U DY

12

The confusion surrounding private exchanges and defined contribution has subsided a bit, with fewer

employers unsure about what defined contribution will mean for their organizations (Figure 10). The barrage

of attention from consultants and the media has helped educate employers on the practical realities of private

exchanges. From the experience of early adopters, a consensus seems to be emerging that “benefit

buy-down” (moving employees from traditionally richer health insurance plans to HDHPs or silver/bronze

plans) and “network optimization” offer quick hits for real savings.

Some of the early predictions about private exchanges do not appear to be on target as of 2015. Employers

are currently not “dumping” group coverage in favor of individual insurance arrangements; among other

factors, the tax advantages for group coverage appear to be too strong. Large employers are not running

immediately toward fully insured solutions; most (nearly 80%) expect to remain self-insured in 2016.

In summary, this study’s findings of modest private exchange penetration suggest that most employers are taking

an incremental approach to their benefits strategies in general, with a reluctance to throw away the longstanding

employer-customized commitments they have in place for wellness, disease management and other health

initiatives. States Garlitz from bswift: “A commitment to a more employee-centric and technology-enabled

program is clearly part of most employers’ employee benefits strategies.”

The Cadillac Tax as a Factor in PlanningMany pundits and consultants have pointed to the ACA’s “Cadillac tax” looming in 2018 as a reason for employers to

move to private exchanges, or at least to revisit the trajectory of their current employee benefits program. Given the

substantial tax that will be imposed on high-cost health plans beginning in 2018, 49% of large employers indicate

the tax as a factor in their 2016 benefits planning, but only 21% cite it as a major factor. The tax has clearly prompted

a subset of large employers to consider a private exchange; of those large employers considering a private exchange,

64% cite the “Cadillac tax” as a factor in their 2016 planning, with 32% describing it as a major factor (Figure 12).

As anticipated, the Cadillac tax is influencing more employers in their 2016 planning, compared to 2015. Employer

concern is likely to grow given that the tax is triggered by total plan cost and these costs continue to increase over

time. Although employers can pass along the tax burden to their employees, providing lower cost plan options

provides a way to minimize the impact on employees. To avoid the perception of a “benefit takeaway” associated

with eliminating high-cost plans, many employers will bring in lower cost options (including HDHPs and narrow

network plans) alongside the more expensive Cadillac plans, positioning consumer choice in a private exchange or

defined contribution arrangement as the solution.

The number of overall employers considering Cadillac tax for 2016: 49% as factor, 21% as major factor

The number of overall employers considering Cadillac tax for 2015: 41% as factor, 12% as major factor

The number considering Cadillac tax for 2015, only looking at employers that are considering PIX: 46% as factor, 14% as major factor

The number considering Cadillac tax for 2015, only looking at employers that are considering PIX: 64% as factor, 32% as major factor

Figure 12—The Cadillac Tax as a Factor in Employee Benefits Planning

Major factor Minor factor

Base = >500 employees Source: SourceMedia Research, 2015

All employers

Employers considering private exchanges

All employers

Employers considering private exchanges

2016

2015

21% 28%

32% 32%

12% 29%

19% 31%

49%

64%

41%

50%

2 0 1 5 B S W I F T B E N E F I T S S T U DY

13

Figure 13—Employee Benefits Enrollment Methods, Large EmployersHow do your employees enroll in benefits (e.g., health, life, etc.) for each of the enrollment types?

Annual Open Enrollment

Life Event

New Hire

Online enrollmentfor all benefits without administrator involvement

Online enrollment for all benefits—but enrollments are verified/processed by a benefits administrator

Online enrollment for some benefits—other benefits are processed via manual or paper process

No online enrollment

Base = >500 employees Source: SourceMedia Research, 2015

32% 37% 14% 17%

16% 33% 14% 36%

26% 36% 13% 25%

The ACA and IRS Form 1095 CompliancePart of the value proposition of a private exchange is that technology can help employers meet burgeoning

compliance requirements, especially those associated with new ACA regulations. Whether or not they offer

health plans, employers with 50 or more full-time equivalents are required to prepare and distribute IRS Form

1095-C to all full-time employees and covered part-time employees, and self-insured large employers must

include more detailed coverage information than fully insured employers.

Not only must employers be prepared to demonstrate that coverage was affordable (based on the employee-

only cost for the lowest cost plan), but self-insured employers must also prove month-by-month coverage for

each individual, including dependents. The calculation of the lowest cost plan may be affected by employee

location/geography, employment classification and available wellness credits or surcharges, where only non-

tobacco credits are allowed in the formula (i.e., other wellness credits may not be used in the calculation of

the employee cost for the lowest cost plan).

Large employers indicate that the primary source of data necessary to complete these forms will come from

benefits administration systems (25%), carriers or TPAs (18%), payroll systems (18%), HRIS systems (16%) and

others—most frequently a broker or consultant or unknown/not sure (11%). Most payroll systems and many HRIS

platforms do not track the eligibility or dependent-coverage data required to complete the IRS forms. Therefore,

some employers that rely on payroll and HRIS systems to produce Form 1095 may be surprised to discover they

must pay to obtain necessary data from another source to complete the forms. Brokers and consultants may be

effective in helping support this work if they leverage a benefits administration system behind the scenes.

Employee Self-Service and AutomationEmployers continue their gradual move away from a reliance on paper-based processes as the way for

employees to enroll in benefits. The percentage of large firms without any online enrollment has declined in

the past year from 29% to 25% for New Hire Enrollment, from 41% to 36% for Life Event Enrollment and

from 20% to 17% for Annual Open Enrollment (Figure 13).

2 0 1 5 B S W I F T B E N E F I T S S T U DY

14

On the other hand, the contingent of employers relying 100% on employee self-service for enrollment has

not increased due to two factors. First, a pronounced—and growing—number of organizations are adding

a “verification” layer to their processes (especially for dependent verification). The percentage of firms using

online enrollment supplemented by a verification or administrative process increased from 34% to 37%

for Annual Open Enrollment and from 33% to 36% for New Hire Enrollment. Second, more employers are

seeking the involvement of administrators to help process certain benefits on a manual basis (speaking to the

increased complexity and selection of benefit offerings in 2015), with that percentage increasing from 9% to

13% for New Hire Enrollment and from 9% to 14% for Annual Open Enrollment.

Similarly, employers’ use of automated alerts to notify employees and/or administrators continues to grow—

from 21% in 2013 to 25% in 2015. However, a sizable percentage of large employers (18%) still do not

provide any automatic alerts to inform new hires or administrators of an important enrollment deadline

(Figure 14).

Despite widespread immersion in technology (approximately 90% of U.S. consumers own mobile phones

and/or have access to the Internet) and escalating expectations of employees, it is striking that, as of March

2015, 25% of large employers still do not offer online enrollment for new hires. Employee self-service for

benefits enrollment continues to increase, but there remains a surprisingly high volume of employers who are

not fully embracing or leveraging readily available technologies.

Benefits Technology: Increasing Complexity of Benefits Drives Market Shift to “Best-of-Breed” VendorsThe world of benefits—and, by association, benefits administration—is becoming more complex. Employers

must be agile enough to manage a changing environment composed of many moving parts, including ACA

compliance, HDHPs, wellness credits, spousal surcharges, defined contribution, mobile compatibility and

optimization, more benefit plan options, voluntary benefits and higher expectations from employees on the

benefits shopping experience, including decision support tools. In essence, the bar for industry-leading “ben

admin” has reached a new high.

Base = >500 employees Source: SourceMedia Research, 2013, 2014, 2015

Figure 14—New Hire Communication, Large Employers How are new hires alerted if their enrollment window is closing soon and their enrollment remains incomplete?

2015

2014

2013

25%

22%

21% 52%

56% 23%

57% 18%

26%

Auto alert Administrators monitor and notify No alerts or notifications

2 0 1 5 B S W I F T B E N E F I T S S T U DY

15

These new initiatives are positive developments for the market and for employees but are challenging to

execute well. They require fl exible and nimble benefi ts technology to enable a streamlined and seamless user

experience for both the employee and also the HR/benefi ts team.

What used to be considered “good enough” may not pass muster anymore; customers have higher

expectations. For years, HRIS/payroll vendors offering a “one-stop shop” approach with “integrated”

solutions encompassing everything from payroll to talent management to benefi ts have been making the

case that although their benefi ts solutions may not be “state-of-the-art,” they get the job done. As of 2015,

however, this argument appears to be losing ground, as the numbers in the study reveal.

Increasingly, the HRIS/payroll “one-stop shop” vendors are losing market share within the benefi ts technology

marketplace. From 2013 to 2015, HRIS/payroll’s market share of the overall benefi ts administration marketplace

for large employers declined from 60% to 45% and has been replaced by benefi ts technology specialists,

benefi ts outsourcing fi rms, benefi ts brokerage/consulting fi rms and private exchanges (Figure 15).

Even more striking is the difference in customer satisfaction between the HRIS/payroll “one-stop shops” and

at least some of the leading benefi ts technology companies. In this survey, respondents were asked to identify

their primary technology for managing enrollment and eligibility data for employee benefi ts and to rate,

on a scale of 0 to 10, the likelihood that they would recommend that vendor to a colleague, using the Net

Promoter Score (NPS) methodology.

In 2015, similar to 2014, the overall NPS for the HRIS/payroll vendors is worse than -50, and none of the

major players registered a positive NPS, which shows both that benefi ts are very complicated as well as the

deep dissatisfaction on the part of benefi ts leaders and managers with the benefi ts solutions that their HRIS/

payroll vendors offer. In contrast, there are some benefi ts solution vendors with an NPS greater than +20.

Considering that many view NPS as a leading indicator of growth, the future looks bright for leaders in the

benefi ts technology space.

Of note is that this NPS data is based solely on benefi ts technology and does not address HRIS/payroll vendors’

ability to deliver on the rest of their value proposition. When considering only their core HR and payroll

functions, some of these vendors may fare better in terms of their NPS scores.

Figure 15—HRIS/Payroll Market Share of Benefits Administration Market, Large Employers

2013 2014 2015

58%

57% 18%

Auto alert Administrators monitor and notify No alerts or notifications

45%

60%

Base = >1,000 employees Source: SourceMedia Research, 2013, 2014, 2015

2 0 1 5 B S W I F T B E N E F I T S S T U DY

16

Companies with 50 to 500 Employees: WellnessThis year’s study shows fewer small employers (defined for purposes of this study as those with 50 to 500

employees) investing in workplace wellness, with 63% offering wellness programs in 2015, down from

about 70% in 2014. The 63% of small employers is also significantly lower than the 85% of large employers

investing in wellness in 2015. This is likely due to three size-related reasons: smaller organizations have

limited resources for bearing the administrative burden of wellness, there is a predominance of fully insured

health solutions among small employers (64% are fully insured) and lower overall health/benefits budgets for

these employers mean there is less potential impact on their financial results.

Key findings include:

Employee engagement/participation is more important than cost savings in assessing wellness program

success. 33% of small employers reported employee engagement/participation as the top Key Performance

Indicator (KPI) of success for their wellness program, ahead of cost savings, which was the second ranked

KPI (at 26%). This reversal of order among the top two KPIs vis-à-vis the large employer segment may be

explained by the fact that more of these small employers are fully insured, thus putting more of the pressure

to reduce costs on the insurer rather than the employer, at least in the short term.

Incentives are primarily based on completion of HRAs and biometric tests, which is similar to the findings for

large employers. For those employers offering wellness incentives to employees, completion of health risk

assessments (HRAs) leads the pack at 67% (a jump up from 56% in 2014), followed closely by completion of

biometric tests at 63% (vs. 58% for the year before). Participation in wellness education or coaching comes in

third at 46%, down from its top spot at 73% for 2014 (Figure 16).

Figure 16—State of Incentivized Wellness Programs, Small vs. Large EmployersFor which of the following wellness programs, if any, does your organization offer incentives (i.e.,”carrots”) or disincentives (”sticks”)?

Completion of Health RiskAssessments (HRA)

Completion ofbiometric tests

Participation in/completionof wellness education

or coaching

Tobacco use/tobacco non-use

Meeting or exceedingbiometric thresholds(i.e., for cholesterol,

blood pressure)

50-500 employees >500 employees

67%

63%

72%

67%

26%

16%

45%

46%

34%

53%

Base = Employers offering incentives for wellness programs Source: SourceMedia Research, 2015

>500 employees 50-500 employees

2 0 1 5 B S W I F T B E N E F I T S S T U DY

17

Outcomes-based wellness programs are likely to grow in 2016. While only 16% of small employers use outcomes-

based wellness today (compared to 26% of large organizations), 30% are considering offering incentives/

disincentives for meeting or exceeding biometric thresholds for 2016 (compared to 18% of larger employers).

The amount invested in wellness incentives is similar between small and large employers. 38% of small

employers offer annual wellness incentives of greater than $500, which is comparable to that of large

employers (Figure 17).

Companies with 50 to 500 Employees: Defined Contribution and Private ExchangesSmall employers are embracing private exchanges and defined contribution more rapidly than large

employers, but the faster adoption rate has not been driven by concerns with the Cadillac tax.

Key findings include:

Defined contribution and private exchanges are gaining traction more rapidly for small employers than for

large employers. Currently, 20% of organizations with 50 to 500 employees use a defined contribution

approach to benefits (twice the rate of large employers), and 25% are considering offering it for 2016.

Approximately 12% of small employers view their 2015 benefits program as a private exchange (more than

twice the rate of large employers), and 10% are considering one for 2016.

Most small employers are likely to remain fully insured in 2016. For 2015, 64% of small employers are fully insured,

and 36% are self-insured. The survey responses suggest these numbers are likely to remain similar for 2016.

50-500 employees >500 employees

Figure 17—Investment in Wellness Incentives per Employee, Small vs. Large EmployersWhat is the annual dollar amount per employee for wellness incentives?

Less than $50

$50 to $249

$250 to $499

$500 to $1,000

More than $1,000

10%

14%

26%

26% 26%

24%

22%

33%

29%

7%

9%

Base = Employers offering incentives for wellness programs Source: SourceMedia Research, 2015

2 0 1 5 B S W I F T B E N E F I T S S T U DY

18

The Cadillac tax is less concerning to small employers. Only about 21% cite the ACA-related excise tax on

employer-provided health benefits as a factor in their benefits planning for 2016. At about half the rate

cited by larger organizations, this finding is intriguing given that small employers—at least those with more

than 50 employees or full-time equivalents—are equally exposed to the tax consequences. This lower level

of concern among small employers may reflect either a lack of awareness of the tax consequences or the

historical reality that, compared with larger employers and unions, these firms have been less likely to sponsor

very rich plan designs.

Companies with 50 to 500 Employees: Self-Service and AutomationWhen it comes to implementing employee self-service and automation for benefits enrollment and

administration, small employers have significant opportunities ahead of them.

Key findings include:

The majority of small companies do not have online enrollment for new hires. 63% of small employers—a

slight uptick from last year’s 61%—are without an online system for enrolling new hires in benefits. For

life events and annual open enrollment, the percentages without an online solution are 62% and 53%,

respectively. Additionally, very few small employers leverage new hire auto alerts (9%).

In regards to ACA compliance, small employers plan to use varied sources to calculate lowest cost health

plans. The primary source of information that small employers plan to use to verify the lowest cost health

plan for each employee is their payroll system (30%), followed by their carrier/TPA (20%) and then their

benefits administration system (18%). This statistic reflects the absence of benefits administration solutions

in this employer segment. Small employers with fully insured health plans, simple benefit programs and

basic eligibility data available on their payroll system or HRIS may be able to report on affordability without a

comprehensive benefits administration platform, but others may be challenged to determine and defend the

affordability of health plans for certain groups of employees.

Figure 18—State of Automation, Small vs. Large Employers

New hire employeeself-service without

administratorinvolvement

New hire auto alerts

Life event employeeself-service without

administratorinvolvement

Open enrollmentfor all benefits

withoutadministratorinvolvement

50-500 employees >500 employees

26%

7%

24%

9%

16%

5%

31%

7%

Base = All respondents Source: SourceMedia Research, 2015

2 0 1 5 B S W I F T B E N E F I T S S T U DY

19

ConclusionThe 2015 bswift Benefits Study findings provide evidence that we are in the midst of an evolution, rather than

a revolution, in employee benefits. Yes, the employee benefits world is trending toward “retail” and shifting

from a “paternalistic” approach to more of a “consumerist” approach, but the changes are incremental and

most employers are taking discrete steps at their own pace and on their own terms. Many employers are

essentially leveraging their existing programs while adding more choice and technology to their offerings.

The key “consumerism” trends highlighted in this study include steady, incremental increases in: a) employee

self-service and online enrollment; b) the use and amount of wellness incentives as well as the use of “social”

challenges and c) more plan choices for employees—such as health plan options like HDHPs and narrow

networks.

Despite the hyped predictions, the employer world is not moving en masse to radical new private exchange

models overnight. In fact, some might argue that the term “private exchange” is just a new name for a

modern employee shopping experience with a greater choice of plan offerings and with technology enabling

greater employee engagement with their health care all year round.

ACA has helped accelerate the ongoing evolution of employee benefits programs and given employers

both a reason and “cover” to introduce less rich health plan options and to further shift costs to employees.

ACA has also helped fuel the nation’s ongoing education on health care. Finally, ACA has added substantial

complexity to employers’ regulatory requirements; employers with large hourly and part-time populations

were impacted in 2014, but in 2015, all employers will need to learn more about their obligations in regards

to 6055/6056 reporting and 1095 forms.

“We expect that the next three years will bring continued movement toward consumerism,” notes Rich

Gallun, CEO, bswift. “If the tax code is eventually changed to remove the advantages of group health

coverage, things may change more quickly and radically. But in the meantime, there is steady progress in

leveraging technology to empower and educate consumers, to offer more choice and to create a more

consumerist world.”

MethodologyThe study was based on the results of an online survey fielded during January and February of 2015. In

total, SourceMedia surveyed 500 benefit decision makers at organizations that offer health benefits. The

sample was randomly drawn from subscribers of Employee Benefit News. The margin of error for the

total sample is +/-5.0% at the 95% confidence level.

About bswift

bswift, an Aetna subsidiary, offers software and services that streamline benefits, HR and payroll

administration for employers and exchanges nationwide. bswift’s state-of-the art, cloud-based technology,

outsourcing solutions and Springboard Marketplace exchange platform significantly reduce administrative

costs and time-consuming paperwork, making life easier for administrators and millions of consumers who

enroll in benefits with bswift. To learn more, please contact us at:

10 S. Riverside Plaza, Chicago, IL 60606 877.9.BSWIFT | [email protected] | www.bswift.com

About SourceMedia

SourceMedia Research (a unit of SourceMedia, publisher of Employee Benefit News) provides complete

custom B2B research solutions for strategists, marketers, agencies and others seeking in-depth insight

into select segments of the financial services industry. SourceMedia Research combines a strong technical

competency in market research with deep market knowledge and focus. www.sourcemedia.com