2015 annual report and 2016–2018 business plan

TRANSCRIPT

2015 Annual Report and 2016–2018 Business Plan

Table of Contents4 HIGHLIGHTS MESSAGES6 CHAIR

8 CEO

10 REGISTRAR

REPORTING12 BY THE NUMBERS

18 INSURANCE PROGRAM

20 OBJECTIVES: LOOKING BACK AND LOOKING AHEAD 2015 ACHIEVEMENTS AND GOALS FOR 2016-2018

FINANCIALS29 MANAGEMENT DISCUSSION

AND ANALYSIS

32 AUDITOR’S REPORT

33 STATEMENT OF FINANCIAL POSITION

34 STATEMENT OF OPERATIONS AND CUMULATIVE OPERATIONS AND INSURANCE PROGRAM FUND BALANCES

34 STATEMENT OF CASH FLOWS

35 NOTES TO FINANCIAL STATEMENTS

BUSINESS PLAN FINANCIALS42 SUMMARY FINANCIALS

(FISCAL 2016 –2018)

GOVERNANCE44 ORGANIZATIONAL STRUCTURE

44 BOARD OF DIRECTORS

46 COMMITTEES

47 MANAGEMENT

49 PURPOSE, MISSION AND VALUES

50 MANDATE

BACK CONTACT INFO

l 3

HighlightsIMPROVING COMPLAINTS PROCESS AND COMPLIANCERECO conducted widespread consultation in 2015 with a view to making real and significant changes to how we protect the public and operate as a regulator. Changes include:

» Taking a more progressive approach to discipline where appropriate and focusing on educating registrants about common errors to reduce their frequency;

» Piloting a new review process for registrant advertisements before they go public; we expect it will increase professionalism and compliance as this is rolled out fully in 2016;

» Making greater use of dispute resolution, which has proven to be an effective, more informal way of resolving issues;

» Improving our communication in a variety of ways — about and during the complaints process, and directly with registrants through: e-blasts; newsletters; webinars; trade shows; and meeting with registered professionals, board and associations.

TALKING TO CONSUMERSConsumer outreach included:

» Annual consumer awareness survey, which found 35% of consumers are aware of RECO, up from 32% in 2014.

» Interacting with about 7,000 people at 8 consumer shows.

» Consumer awareness campaigns in the spring and the fall:

– 1 consumer survey to find out Ontarians’ biggest concerns about buying or selling a home at different life stages;

– Weekly Ask Joe column in the Toronto Star that educates consumers about buying and selling a home and RECO’s support materials and consumer protection mandate;

– More than 28,000 visits to 3 new audience-specific web guides geared towards first-time home buyers, move-up buyers and downsizers;

– RECO messages being seen 2.9 million times through social media channels, with more than 24,000 engagements (likes, clicks, shares, comments, mentions or re-tweets on our content);

– More than 69 positive media hits, seen about 11.8 million times by Ontarians, during RECO’s fall Financial Literacy campaign;

– Increased followers on social media channels to 8,998 on Facebook (14% increase over 2014) and 4,809 on Twitter (34% increase over 2014).

RECO also responded to 13 media requests about new rules concerning offer handling (Bill 55, the Stronger Protection for Ontario Consumers Act, 2013). There were nearly 100 media hits in print, broadcast and online news outlets about the important consumer protection element of the new legislation. These media opportunities allowed us to continue to increase awareness of RECO in the marketplace and to educate the public about these consumer protection measures.

Registrant consultation and outreach in 2015 » Phone interviews, e-discussion groups and a questionnaire

» Regular registrant survey (conducted every two years)

» A new approach to area meetings of local boards where we sought feedback from participants on proposed changes

» Attendance at 54 industry events and presentations to industry professionals in 26 cities

» 3 For the Record newsletters, 4 Registrar’s Bulletins

RECO 2015 Annual Report and 2016–2018 Business Plan l 2015

Reconciliation (358)

Routine (555)

Courtesy (129)

Complaint-based (21)

Total Number of Inspections (1,063)

No Action Required (52%)

Administrative Actions (39.5%)Including being given a warning, taking an educational course, taking corrective action, or taking part in RECO dispute resolution.

Escalated Actions (8.5%)Required more serious regulatory action, including: appearing before a disciplinary committee; having their licence suspended or revoked by the Registrar; being charged under the Provincial Offences Act.

Actions for Complaints Closed

COMPLAINTS » Complaints closed in 2015 — 1,579

65% of complaints are from consumers 35% are from registrants

REGISTRATION RENEWALS » 92% done online vs 80% in 2014

RECO continues to expand online services to provide faster service to registrants

EDUCATIONThe online Mandatory Continuing Education (MCE)program completed its first full cycle in 2015.

» 23,455 registrants completed the online MCE program in its entirety (i.e., not a hybrid of old and new program)

» 89.7% of registration renewals were processed based on the online program

» 26,326 registrants completed at least one course

» 73,109 courses in total were completed

RECO surveyed registrants about their experience with the online MCE program. Of the 8,297 people who responded, 94% indicated the content was interesting and easy to follow and 94% indicated the courses themselves were easy to navigate and understand. We have worked to address suggestions made by users, which has improved the survey results since 2013.

Before becoming registered as a salesperson, applicants must complete an approved registration education program that provides them with the fundamentals of trading in real estate and the rules they must follow. In 2015, RECO continued work on a new approach for registration education that will enable aspiring registrants to be more practice-ready when they enter the profession. During the year, RECO gathered information from Canadian colleges and universities, education providers, OREA and other Canadian regulatory bodies. With this information, RECO was able to further refine its strategy for implementation. In 2016, RECO will accept proposals from possible education providers who will assist with the design, development and delivery of the new program. The selected provider will work towards a launch in 2019. In a future phase, RECO will allow additional education providers to provide registration education, allowing learners to choose how they prefer to learn.

OUTREACH AND RESPONSEComplaints, Compliance & Discipline Department responded to 33,934 inquiries:

Phone17,872

Email 16,013

Fax/Mail 49

INSPECTIONSRegistrants were surveyed in 2015 about the inspections process and the findings indicated a high level of satisfaction:

» 100% were very satisfied or satisfied with the professionalism of the RECO inspector;

» 99.1% were very satisfied or satisfied with the knowledge demonstrated by the RECO inspector; and,

» 97.2% were very satisfied or satisfied, overall, with RECO’s inspection process.

l 5 HIGHLIGHTS

On behalf of the Board of Directors, I am pleased to present the Real Estate Council of Ontario’s Annual Report for the 2015 fiscal year.

I have had the privilege of being Chair of RECO during a time of tremendous change in the profession, and this Annual Report describes how RECO is responding to the challenges and opportunities that arose in 2015 and moving forward with initiatives to ensure excellence in the delivery of regulatory services.

The sector continues to grow: registrants now number more than 73,000, and they are serving a strong Ontario housing market that continues to be robust, particularly in the Greater Toronto Area.

That’s why it is vital that we at RECO not just keep up with the times, but be a leader in consumer protection among regulators. To that end, 2015 was a year of consultation and action at RECO.

We reached out to consumers and registrants in unprecedented fashion.

Our consumer awareness campaign generated significant public attention: media outlets distributed our messages to millions of Ontarians and our social media channels enjoyed significant growth, which means that we are reaching more and more consumers each year. Staff also set up booths at eight consumer shows in 2015 and talked to more than 7,000 members of the public about RECO and its role in educating and protecting consumers.

“...registrants now number more than 73,000, and they are serving a strong

Ontario housing market that continues to be robust, particularly in the

Greater Toronto Area”

Jody Lavoie

RECO 2015 Annual Report and 2016–2018 Business Plan l 2015

Chair’s MessageWe also consulted widely with registrants in an effort to renew our relationship and gain mutual understanding about the regulated real estate sector. In addition to our regular registrant survey, we consulted widely with industry representatives of all levels of experience and expertise about their view of RECO’s role in the sector and our responsibilities concerning registrants.

The results were informative.

Registrants recognize RECO’s role in enforcing the Code of Ethics and real estate regulations and in protecting consumers. And, registrants also understand that being part of a regulated profession is of value because it builds consumer confidence and trust in the sector.

The consultation also told us where RECO could improve, and so we responded with actions and commitments on a number of fronts.

We know we need to consult more and communicate better with the sector. We need to be clearer when we are explaining the rules, and we have to make changes to the complaints process, particularly for advertising complaints. Some of this work was piloted in 2015 with the intent to continue along this path in 2016.

We also devoted a lot of time in 2015 to improved customer service through the modernization of our operations. Our commitment to electronic service delivery is paying dividends with quicker renewals of registration and insurance.

Work continued on a new, back-end data system to better serve registrants, and it is on track for a 2016 launch. This new system, called RECOserv, will speed up administrative processes and provide a wider array of information and services for registrants to access online. The fact that RECOserv offers a single repository of information means better service, too.

On the education front, there is much work being undertaken in continuing and registration education.

In 2015, we saw the full phase-in of the new Mandatory Continuing Education program to good reviews. A new update course was introduced, and new electives will be developed regularly to keep the content fresh and topical.

We also set out a new path for registration education and in 2016 will continue developing a new model that will prepare prospective registrants for an ever-evolving marketplace.

Another fundamental change in 2015 was our approach to the complaints process. RECO is taking a more educational approach to common discipline issues so that registrants can better understand how to avoid them in the future.

We are also committed to making more use of dispute resolution, a process that allows all parties to the complaint to be more involved in the outcome. It has become an increasingly important way to resolve a complaint.

And, we piloted a new advertising review process that allows brokers of record to submit advertisements for review before they are made public. RECO believes this will greatly increase advertising compliance in the sector.

In short, 2015 was a busy year filled with insights and accomplishments. I would like to thank RECO staff for their tremendous efforts this year. Their embrace of new and innovative ways of doing business bodes well for the future of the sector.

I would also like to thank the Board of Directors for their hard work and support in 2015. It has been an honour to serve as Chair, and I am looking forward to a successful 2016 as we build on the many achievements of 2015.

“...registrants now number more than 73,000, and they are serving a strong

Ontario housing market that continues to be robust, particularly in the

Greater Toronto Area”

l 7 MESSAGES CHAIR

As I look back on 2015, I am struck by how much RECO has accomplished in the last year. It has been a time of positive change.

We have focused our efforts on being an effective regulator, striving for excellence in our delivery of regulatory services to protect consumers and enhancing confidence in the real estate profession.

This mandate means we must ensure that registrants have the education and tools to operate within the rules, and we must respond appropriately to improper behaviour. Moreover, we must continue to travel along a path of reflection and action, always seeking ways to do things better.

Connecting with consumers is one of the ways we determine if we are on the right track as a regulator.

Every year, we gauge their knowledge of RECO and the sector and how we can do a better job of educating them about buying and selling a home or resolving their complaints. This past year was no exception.

RECO staff made their presence known at a number of consumer shows in 2015, talking face-to-face with first-time homebuyers, new or expecting parents, and — new this year — boomers who may be interested in downsizing as their children leave.

RECO also enjoyed strong media coverage during the year. Our weekly Ask Joe column in the Toronto Star, featuring our Registrar Joseph Richer, continues to receive good response, and our public campaign during Financial Literacy Month reached impressive numbers of consumers through our media efforts.

With the proclamation of the Ontario Government’s Bill 55, the Stronger Protection for Ontario Consumers Act, 2013, RECO spoke with print, broadcast and online media outlets about the legislation’s impact on consumers and the real estate industry.

Kate Murray

RECO 2015 Annual Report and 2016–2018 Business Plan l 2015

CEO’s MessageOur social media numbers continue to rise. We are reaching more and more consumers on Facebook and Twitter, delivering information to increase their knowledge about buying and selling and the benefits of working with a registered real estate professional.

On the industry side, RECO reached out to registrants in unprecedented fashion in 2015.

Along with the biennial registrant survey, RECO consulted widely with industry representatives about the RECO-registrant relationship. The reason for this is simple: RECO and the real estate sector need to work together better to ensure consumers are given the best possible service and advice.

We learned much from our consultations. Registrants told us they recognize RECO’s role in enforcing the Code of Ethics and real estate regulations and in protecting consumers. They also understand that being part of a regulated profession is of great value because that affiliation increases consumer confidence and trust in the industry.

Our consultation with the industry also told us we needed to make some changes in the way we operate so that we continue to improve as a regulator.

So, in 2015, we committed to making improvements in four key areas.

First, we are increasing our consultation and communications with the sector. Registrants will be kept better informed by more webinars and improved newsletters and e-blasts.

“We are reaching more and more consumers on Facebook and Twitter, delivering information to increase their knowledge about buying and selling and the benefits of working with a registered real estate professional”

Second, RECO is committed to improving its customer service. Staff are receiving more training and are being given new and better tools to interact more effectively with registrants and consumers. We are committed to increasing our electronic delivery of services, speeding up administrative tasks like registration and insurance renewals. And, we are preparing a consumer toolkit for registrants to use to educate their clients about buying and selling and the benefits of working with a registered real estate professional.

Third, we will help registrants be more compliant with the rules by taking an educational approach to discipline and communicating more clearly what is expected of them and how they can avoid common discipline issues. Of course, when the discipline matter is serious, we will use the tools we have at our disposal to address the issue and protect consumers.

And fourth, we are making changes to RECO’s complaints process.

In 2015, we piloted a new procedure in which brokers of record can check with RECO to see if an advertisement is compliant before it goes public. We believe that when this approach is fully rolled out in 2016, it will greatly reduce the number of complaints about advertising.

We are updating the complaints information on our website to make the process and outcomes more clear. We are committed to more communication to all parties to the complaint, so that even if the process takes some time, they will be informed of progress along the way.

We also plan to make more use of dispute resolution, which has proven to be an effective, more informal way of resolving issues.

All in all, 2015 has been a busy year of consultation, reflection and positive change, and I would like to thank RECO staff for their creativity and hard work. I would also like to thank the Board of Directors for their support and leadership.

I am looking forward to moving ahead with the priorities that we’ve identified. And, I am committed to keeping in touch with consumers and registrants to ensure we are able to adapt to our changing environment, continually improve and be a leader among regulators.

l 9 MESSAGES CEO

Being part of a regulated profession comes with rights and responsibilities. A well-regulated real estate sector enjoys increased public confidence and trust, and that is a positive consequence for both real estate professionals and the clients they serve.

A regulated profession also demands accountability, and that means each of us — RECO and registrants — taking responsibility to do the best we can in a sector that is experiencing extraordinary growth year after year.

Our consultation with registrants in 2015 tells us they recognize the value in being part of a regulated profession. So, we continue to work with the sector to raise the bar and to increase everyone’s accountability, including RECO’s.

In that spirit, RECO made a lot of important changes to its operations in 2015.

We put in place a new progressive approach to complaints that focuses on educating registrants about common, minor errors so that they don’t make them again. We piloted a new review process for advertisements before they go public, and we expect this will greatly improve advertising compliance in 2016 as we deploy the new process across the sector.

RECO also completed the first cycle of the online Mandatory Continuing Education program. As the transition from the original program to the new program is now complete, all registrants from now on will fulfill their continuing education requirements through RECO’s online program.

Though feedback has been positive and registrants tell us they like the program, we will continue to enhance it based on registrant needs and feedback. In 2015, we introduced a new update course, added two new electives and started planning new, topical content for future electives that will help registrants better serve their clients.

Joseph Richer

RECO 2015 Annual Report and 2016–2018 Business Plan l 2015

Registrar’s Message

“...we examined our operations, asked tough but important questions,

listened to what people had to say, and acted on what we heard”

This model of education is a good balance for registrants because it gives them greater control over their personal and professional development while ensuring they are given robust instruction in the fundamentals of trading in real estate, particularly as it relates to RECO’s mandate of consumer protection.

Looking ahead to 2016, RECO has a number of important projects planned that will raise the bar on service delivery to both registrants and consumers.

For one, we are adopting a multi-departmental approach to address our most important regulatory issues around consumer protection so that we have a comprehensive strategy on managing those issues.

Advertising will be a key focus in 2016, with our Complaints, Compliance & Discipline department working in concert with the Inspections and Education departments to ensure a high level of compliance for registrants.

RECO will also continue to develop a new approach to handling complaints. Our staff and resources will be better deployed to achieve faster response times and effective outcomes. We will make even greater use of dispute resolution – a process that is valued because it involves all parties in a discussion aimed at settling issues.

We will continue to promote the new advertisement review process to raise professionalism by supporting compliance, which in turn may reduce complaints in this, our top category of complaint. And, we will use our new powers provided through the Stronger Protection for Ontario Consumers Act, 2013, to heighten transparency in the offer process. In 2015, RECO had 28 inquiries and one contravention of the Act since its proclamation on July 1, 2015.

Another goal is to ensure that the punishment fits the crime. Where appropriate, first-time offenders should be treated less harshly than repeat offenders, and RECO will use its resources to educate first and then step up its disciplinary actions when required. Of course, serious matters will still see the full force of the law brought to bear when it is appropriate.

The way we communicate with consumers and registrants is another area where we are looking to improve. It’s important that the information and decisions we deliver demonstrate consistency in approach and are easily understood.

And finally, RECO is committed to expanding electronic delivery of service. For registrants, that means quicker online renewals of registration or insurance. For consumers, that means easy access to a comprehensive hub of information about buying, selling and working with a registered real estate professional. For RECO, that means we reduce the amount of paper we use and lower our operational costs.

The coming months will build on our work in 2015, a year in which we examined our operations, asked tough but important questions, listened to what people had to say, and acted on what we heard.

We have made strides in raising the bar on professionalism and we will continue to promote leading practices so that consumers are protected and registrants are well equipped to meet the needs of their clients.

I am looking forward to 2016, anticipating that it will be another year of accomplishment as we work with registrants, boards and associations to ensure consumers are given the best possible advice and service in the real estate sector.

l 11 MESSAGES REGISTRAR

RECO is committed to protecting the public interest and enhancing consumer confidence in the real estate profession. We work to fulfill this goal through the day-to-day regulation of Ontario’s more than 73,000 real estate registrants.

The Ontario government sets the rules that real estate salespersons, brokers and brokerages must follow. RECO enforces that law – called the Real Estate and Business Brokers Act, 2002 (REBBA 2002) — and its associated regulations on behalf of the government.

RECO protects the public interest by:

» enforcing the standards to obtain and maintain registration as a brokerage, broker or salesperson;

» establishing minimum education requirements for registration, articling, broker, and continuing education;

» conducting routine inspections of brokerage offices to ensure legal compliance and to educate Brokers of Record;

» addressing inquiries, concerns and complaints about the conduct of registrants and taking appropriate action to protect the public interest;

» establishing and administering insurance requirements, which include consumer deposit protection; and,

» being the source of consumer protection education and information for real estate transactions.

By the Numbers

RECO 2015 Annual Report and 2016–2018 Business Plan l 2015

Salespersons45,235

Brokers12,231

Provisional salespersons

11,489

Brokerages3,450

Branch offices1,346

10,000 50,000

Total Registrants by Category (73,751)as at December 31, 2015

1993 1997 2002 2006 2010 2014 2015 (Jan to Dec)

Number of Registrants by year

0

40,000

20,000

60,000

80,000

Renewals(27,689)

Tranfers(8,983)

New (6,541)

Terminations(4,524)

Reinstatements(4,065)

Revisions(3,875)

Category changes(652)

5,000 30,000

Total Registrant Transaction by Type (56,329)as at December 31, 2015

REGISTRATIONRECO enforces the standards to obtain and maintain registration as a brokerage, broker or salesperson.

RECO’s Registrar determines who is eligible to become registered to trade in real estate in Ontario based on legal and regulatory requirements.

RECO’s registration department processes:

» new registrations of businesses, brokers and salespersons;

» renewals;

» reinstatements;

» broker and salesperson transfers and terminations; and,

» name and category changes.

RECO is moving from paper-based to online processing for all types of registration services. This has resulted in a dramatic decrease in the amount of time needed to renew a registration and a dramatic increase in the number of people renewing online.

For online terminations and transfers, the completed transaction can now be done in minutes instead of days, as had previously been the case.

Other online services are increasing in popularity as well and RECO will continue to invest in technological enhancements to provide more efficient service to registrants.

2014

Online Renewals

2015

0

25,000

Paper-based5,472 19,880 2,088 22,176

Online Paper-based Online

l 13REPORTING BY THE NUMBERS

EDUCATIONRECO establishes minimum education requirements for registration, articling, broker, and continuing education. RECO promotes ongoing education and competent, knowledgeable and professional service.

Registration education:

Before becoming registered as a salesperson, applicants must successfully complete an approved education program that provides them with the fundamentals of trading in real estate and the rules they must follow.

In 2015, RECO continued work on a new approach for registration education that will enable aspiring registrants to be more practice-ready when they enter the profession.

In 2016, RECO will accept proposals from possible education providers who will assist with the design, development and delivery of the new program. The selected provider will work towards a launch in 2019. In a future phase, RECO will allow additional education providers to provide registration education, allowing learners to choose how they prefer to learn.

Mandatory continuing education:

RECO completed the first cycle of the online Mandatory Continuing Education program in 2015. The program focuses on the topics that are most important to salespersons and brokers: how to operate a business under the law (REBBA 2002); consumer protection; and, current industry issues.

As the transition from the original program to the new program is now complete, all registrants will fulfill their continuing education requirements through online instruction.

RECO will continue to expand the number of topics in the continuing education curriculum that are relevant to a registrant’s business, with up to three new electives each year. A new mandatory update course was launched in August 2015.

RECO surveyed registrants about their experience with the online program. Of the 8,297 people who responded, 94% indicated the content was interesting and easy to follow and 94% indicated the courses themselves were easy to navigate and understand. We have worked to address suggestions made by users, which has improved the survey results since 2013. RECO will continue to listen to feedback and is committed to enhancing the program.

Number of registrants who completed entire new MCE program (not a ‘hybrid’ combination of old and new)

23,455Percentage of registration renewals that were processed based on the new MCE program versus a ‘hybrid’ of old and new program

89.7%Number of registrants who completed at least one course

26,326Number of courses completed

73,109RECO 2015 Annual Report and 2016–2018 Business Plan l 2015

INSPECTIONSRECO conducts routine inspections of brokerage offices to ensure legal compliance and to educate brokers.

RECO conducts inspections of brokerages to make sure that they are following the rules and regulations and protecting the interests of consumers and other registrants. This one-on-one contact provides opportunities to educate brokers of record about maintaining current and accurate records.

RECO inspections fall into four categories:

» Random routine visits to established brokerages;

» Courtesy inspections with new brokerages to help them ensure that their businesses are in compliance with regulatory requirements;

» Inspections generated by complaints; and,

» Inspections requested by RECO for a brokerage to submit trust account reconciliation statements.

Inspectors are trained to provide accurate information and to answer registrant questions. During brokerage inspection visits, inspectors examine records such as trust account records, trade contracts and trade record sheets.

In 2015, RECO asked brokerages involved in an inspection to answer a survey about their experience. The feedback was used to help RECO assess and continually improve our inspection processes and services. RECO will continue the survey in 2016.

Reconciliation (358)

Routine (555)

Courtesy (129)

Complaint-based (21)

Total Number of Inspections (1,063)

COMPLAINTSRECO addresses inquiries, concerns and complaints about the conduct of registrants and takes appropriate action to protect the public interest.

Registrants must follow the law when conducting their business. The law aims to protect consumers when they complete real estate transactions and helps ensure public confidence in Ontario’s real estate profession.

Most complaints received by RECO do not involve serious or malicious misconduct; many are a result of registrants making errors in completing paperwork or exercising poor judgment. The Registrar determines what action, if any, is appropriate, depending on the facts identified during the processing of the complaint.

In some cases, no action is taken by RECO because the complaint is withdrawn by the complainant or the Registrar dismisses the complaint because there is no cause for action or the complaint does not fall under RECO’s authority to act. In other cases, potential actions include the following:

» The Registrar may issue a written warning indicating that if the conduct that led to the complaint continues, further action may be taken;

» The Registrar may require a registrant to take education courses;

» The Registrar may attempt to mediate or resolve the complaint;

» The Registrar may apply voluntary conditions to a registration, with the registrant’s consent;

» The Registrar has the power to order an immediate temporary suspension of a registration where he or she believes it is in the public interest;

» The Registrar may issue a Notice of Proposal to revoke, suspend, refuse to renew, or apply conditions to a registration if a registrant is in contravention of REBBA 2002 and its regulations;

» Matters involving alleged breaches of the Code of Ethics may be referred for a Discipline Committee hearing; and,

» Offences related to REBBA 2002 and its regulations (other than the Code of Ethics) can result in charges laid under the Provincial Offences Act.

l 15REPORTING BY THE NUMBERS

No Action Required (52%)No independent evidence to support a contravention of REBBA 2002No independent evidence to support a contravention of REBBA 2002 and no jurisdiction for any secondary issues raisedNo cooperation from complainant for further information/documents needed to make an informed decision

Administrative Actions (39.5%)WarningWarning and course Warning and requirement to take actionWarning, course and requirement to take action Mediation

Escalated Actions (8.5%)Discipline hearingRegistrar’s proposalReferred to POA prosecution

Actions for Complaints Closed

Misrepresentation (10%)

Advertising (14%)

Conscientious competent services(6%)

Disclousures (3%)

Competing/ multiple offers (3%)

Interference (3%)

Presentation of offers (3%)

Other (58%)

Top Complaint Areas as at December 31, 2015

Complaint trends

RECO monitors complaint trends so that it can focus its education for both consumers and salespersons on areas of specific concern. This year, there was a 21% increase in the number of complaints that were opened. This can be partially attributed to RECO’s ongoing efforts to increase consumer awareness, as well as increasing media coverage of a “hot” housing market that has experienced supply and demand challenges.

RECO opened 2,160 complaints in 2015, compared to 1,780 in 2014— a 21% increase.

Consumers accounted for 65% of the complaints filed, while 35% were from registrants.

RECO also closed 1,579 complaints in 2015, compared to 1,376 in 2014.

RECO 2015 Annual Report and 2016–2018 Business Plan l 2015

123 Individual charges laid37 Prosecutions 31 Convictions

$161,200 Total fines $15,000 Total restitution payment ordered

36 months Total probation sentenced

INVESTIGATIONSRECO investigates alleged violations of the law (Real Estate and Business Brokers Act, 2002 and its associated regulations).

From January 1, 2015 to December 31st, 2015, RECO opened 157 investigations and closed 142.

The Provincial Offences Act governs how charges are processed and prosecuted in the Ontario courts. Individuals found guilty of offences are subject to fines up to $50,000 and a potential prison term of two years. Corporations found guilty of offences are subject to fines up to $250,000. Courts also have the power to order convicted persons to pay compensation and make restitution.

A listing of convictions for 2015 can be found in the Regulatory Digest at www.reco.on.ca.

Investigations Related To Mortgage Fraud

Mortgage fraud continues to be a concern. During 2015, RECO opened 19 investigations and closed 17 investigations related to allegations of mortgage fraud.

RECO addresses mortgage fraud through:

» education;

» collaboration with organizations concerned about mortgage fraud;

» investigative activities to ensure compliance; and,

» legal/statutory activities to impose disciplinary action on registrants proven to have participated in mortgage fraud.

Any registrant or applicant proven to have knowingly participated in mortgage fraud faces losing their registration or having registration refused. It should be noted that some registrants alleged to have participated in mortgage fraud voluntarily terminate their registration.

Administrative Regulatory Actions

In 2015, the Registrar took administrative regulatory action, such as issuing warnings and/or requiring educational courses, in 601 cases. In addition, 152 cases were referred to RECO dispute resolution.

Registrar’s Proposals

The Registrar’s authority to issue a proposal to refuse, revoke or refuse to renew registration is a critical component of RECO’s enforcement activities. It is the most severe action RECO takes and is reserved for the most serious circumstances.

The Registrar has the authority to issue a proposal in situations where the applicant cannot reasonably be expected to conduct business in a financially responsible way, or where past conduct gives reasonable grounds for the Registrar to believe that the applicant will not conduct business with integrity, honesty, and in accordance with the law.

In 2015, the Registrar issued 20 proposals to refuse or revoke registration; in addition, 21 proposals to revoke registration were issued due to non-payment of insurance premiums. This compares to five proposals to refuse or revoke registration, one to apply conditions and 21 proposals for non-payment of insurance in 2014.

A listing of refused and revoked registrations can be found in the Regulatory Digest at www.reco.on.ca.All registrants may be searched using the Real Estate Professional Search feature on the homepage, www.reco.on.ca.

DISCIPLINE AND APPEALS HEARINGSRECO’s Discipline and Appeals Committees are statutory tribunals subject to the Statutory Powers Procedures Act. Complaints involving alleged breaches of the Code of Ethics may be referred to the Discipline Committee for a hearing. If the panel makes a determination that a registrant has failed to comply with the Code of Ethics, it may order the registrant to take educational courses, pay a fine of up to $25,000, and/or impose costs. Either the registrant or RECO has a right to appeal the discipline decision within 30 days of issuance. Discipline and Appeals decisions are public information and always accessible to the public. A full list of Decisions is posted on RECO’s website at www.reco.on.ca.

Pre-hearings: 45Discipline hearings: 33 (total)

– Contested/contested in part: 1 – Order by the Chair (hearing waived): 32

Appeals Hearings: 3

AMENDMENTS TO THE ACTOn July 1, 2015, new rules took effect in Ontario that require brokerages to retain copies of offers. The law, which amends the legislation governing real estate in Ontario (REBBA 2002), also established an inquiry process to confirm the number of offers.

l 17REPORTING BY THE NUMBERS

Insurance ProgramProtection for Consumers — Protection for Registrants

RECO’s Insurance program was introduced on September 1, 2000 to provide protection to both consumers and registrants. All registrants are required to participate in RECO’s Insurance program which consists of three valuable insurance coverages:

» Consumer Deposit insurance protects consumers for loss of deposits caused by fraud, misappropriation of funds or insolvency by a registrant.

» Errors and Omissions coverage provides protection for registrants in the event that errors & omissions committed in the course of their professional services lead to claims made against them.

» Commission Protection coverage protects registrants from loss of commission caused by fraud, misappropriation of funds or insolvency of a brokerage.

CLAIMS STATISTICS AND TRENDSConsumer Deposit Insurance PolicyFrom inception of the program on September 1, 2000 to August 31, 2015, there have been 59 occurrences under the Consumer Deposit coverage. Payment of claims (settlements and expenses) under this coverage is estimated to reach $3,801,577.

Commission Protection Insurance PolicyFrom inception of the program on September 1, 2000 to August 31, 2015, there have been 121 occurrences under the Commission Protection coverage. Payment of claims (settlements and expenses) under this coverage is estimated to reach $4,483,368.

Errors and Omissions Insurance PolicyFrom inception of the program on September 1, 2000 to August 31, 2015, there have been 11,984 claims reported. The estimated total cost of claims settlements and expenses under this coverage is estimated to reach $118,326,837*.

* this figure does not include any provision for the insurer’s internal administrative expenses or further development on claims not yet finalized or reported.

Key statistical highlights include:

» The majority of activity in the program arises out of claims under the Errors and Omissions insurance coverage;

» A total of 11,984 claims have been reported — of which 1,248 remain open. The program has therefore managed, and closed, a total of 10,736 claims on behalf of registrants to date;

» Residential claims outnumber commercial claims by a margin of 5:1 (including vacant land and agricultural as commercial, otherwise the ratio is closer to 7:1);

» Urban claims outnumber rural claims by a margin of 8:1;

» The number of claims involving transactions which exceed $250,000 in value comprise approximately 58% of all claims reported, versus 57% in the previous year; and,

» There were 1,009 claims reported in the 12-months ended August 31, 2015, compared with 979 claims reported during the same 12-month period one year earlier.

RECO 2015 Annual Report and 2016–2018 Business Plan l 2015

Commercial* (1,919)

Residential (9,856)

Unknown and Other (209)

Claims by Transaction Type Commercial vs. Residential

*includes Vacant (393) and Agriculture (82)

$150,000-$250,000 (2,361)

$0-$150,000 (2,660)

$250,000-$500,000 (3,780)

$1,000,000 and up (1,077)

$500,000-$1,000,000 (2,106)

Claims by Value of Transaction

Top 5 Causes of Loss — Urban

Financial/ Mortgage

1,800

200

Miscommunication/ Non-Disclosure

1,698 973956 599

IncompleteSale

Foundations Structural

594

Top 5 Causes of Loss — Residential

IncompleteSale

Septic/ Environmental

1,800

200

Miscommunication/ Non-Disclosure

1,5761,041

827 645

Foundations Structural642

Top 5 Causes of Loss — Rural

Septic/Environmental

Foundations

300

50

Miscommunication/ Non-Disclosure

239203

17895

Well/Water Structural69

Top 5 Causes of Loss — Commercial

IncompleteSale

Tax (incl HST/GST)

Leasing/Income

400

50

Miscommunication/ Non-Disclosure

360 202 159157

Deposit146

l 19REPORTING INSURANCE PROGRAM

ObjectivesCONSUMER PRIORITIESThe public at large and more specifically the consumers of real estate services expect the marketplace to be safe, secure and free of behaviour and activity that would jeopardize their interests. For RECO, consumer protection is paramount and is the primary reason for having a regulated industry. RECO appreciates the critical role it must play to:

» educate and inform consumers about the marketplace and the value of a regulated industry;

» protect consumers’ interests and concerns;

» assure consumers that strong disciplinary mechanisms are in place where standards are not met; and,

» enhance consumers’ perception of the profession of real estate. RECO works with Consumer Protection Ontario to fulfill this role.

RECO’s consumer priorities will include:

Increase public awareness of RECO, its role and the value of working with registrants2015 ANNUAL REPORT BUSINESS PLAN 2016–2018

» Consumer survey shows awareness of RECO up to 35% from 32% in 2014

» Consumer survey in December, 2016 to gauge awareness level of RECO

» Had face-to-face interactions with 7,000 consumers at baby, bridal and boomer consumer shows

» Participate in more consumer shows for increased face-to-face interactions with Ontarians

» Conducted consumer awareness campaigns in the spring and fall, resulting in RECO messages being seen 2.9 million times through social media channels, with more than 24,000 engagements (likes, clicks, shares, comments, mentions or re-tweets on our content)

» Continue to engage with consumers through earned, paid, and social media

» Create toolkit of consumer education materials designed for registrants to share with their clients in print or on-line

» Built new website with improved readability and navigation, and emphasis on information for buyers and sellers

» Continue to update and improve website to reinforce it as a go-to spot for real estate protection information

» Media coverage of RECO’s fall campaign generated more than 69 positive media hits about consumer protection, seen about 11.8 million times by Ontarians

» Continue our consumer campaigns on consumer protection

RECO 2015 Annual Report and 2016–2018 Business Plan l 2015

Be the source of consumer protection education and information for real estate transactions2015 ANNUAL REPORT BUSINESS PLAN 2016–2018

» Created customized web pages for Financial Literacy Month, targeting three audiences: first-time buyers, up-sizers and down-sizers (these line up with our target consumer show audiences: brides, expecting parents and boomers); recorded 28,000 visits to these new guides

» Enhance educational content on website

» Produced regular Regulatory Digest so consumers and registrants could see summary of all RECO regulatory action in one place

» Continue to produce Regulatory Digest

» Disseminated 8000 copies of our consumer brochure, Reconnect; as well as 4000 copies of Home Buying and Selling brochure

» Disseminate at least 10,000 copies of Reconnect

» Produced weekly Ask Joe column in the Toronto Star providing consumer protection advice to home buyers and sellers

» Continue to use Toronto Star’s Ask Joe column to help educate consumers and make them aware of benefits of working with a regulated real estate professional

» Increased followers on social media channels to 8,998 on Facebook (14% increase over 2014) and 4,809 on Twitter (34% increase over 2014)

» Grow Facebook and Twitter following and increase engagements from 2015. Explore Instagram as potential new vehicle

» Participated in 100 media stories about new consumer protection rules concerning offer handling

» Continue to respond to media inquiries concerning consumer protection measures and other developments in the sector

Improve service quality and relationships with consumers2015 ANNUAL REPORT BUSINESS PLAN 2016–2018

» Adopted broader approach to improving internal processes to enhance consumer service and consumer confidence. Metrics set in 2015 will serve as baseline for coming years

» Continue to look at improving processes and evaluate success based on established benchmarks

» The Business Process RECOnfiguration — RECOserv — continues to evolve; once fully operational, it will provide a significant leap forward in file management and will simplify and speed up the RECO experience for both registrants and consumers

» RECOserv promises a one-stop portal for information on all areas of RECO’s governance. Its target for operational release is fall 2016. The streamlining of processes will permit goal setting for numerous functions, including timeframes for completing work on files

» Due to consistent annual increases in inquiry, complaint and investigation volumes, in 2015 our average complaint/investigation processing times rose from 90 days to 130 days. We expect that RECOserv and other initiatives in CCD will progressively lower the processing times of complaints and inquiries

» With the combination of RECOserv, internal initiatives and additional staffing, we expect to see progressive improvement in 2016 in online service experiences and available data; even greater gains in the years to come as planned changes become part of the process

» RECO’s new website launched in 2015; changes simplify the RECO experience for all audiences, making it easier to file complaints, search discipline decisions and process registration issues while being a comprehensive source of information

» Technical and content improvements to RECO’s website will offer consumers an enhanced access portal filled with helpful information

» RECO will publish its Service Standards on its website and will develop additional service standards after RECOserv is fully implemented and enhanced reporting is available

l 21REPORTING OBJECTIVES

REGISTRANT PRIORITIESAt the heart of a trusted and confident marketplace lie the qualifications, standards and professionalism of each and every registrant. For RECO, it is important that registrants be part of advancing regulatory goals and ensuring a fair, safe and informed real estate marketplace. RECO has a critical role to play by:

» improving the profession through enhanced education and training;

» ensuring education is directly tied to improved consumer protection;

» increasing registrant engagement in the process of enhancing standards and professionalism; and,

» establishing greater mutual respect for each other’s roles and contributions to the industry, profession and to consumer protection.

RECO’s registrant priorities will include:

Increase registrants’ understanding of RECO and its role2015 ANNUAL REPORT BUSINESS PLAN 2016–2018

» 2015 registrant survey shows a 71% satisfaction rate with RECO. Also, 82% use RECO as source of information about real estate rules and regulations

» Continue to educate registrants about compliance issues, and RECO’s consumer protection role via bulletins and articles. Conduct next biennial registrant survey in 2017

» Conducted registrant engagement research project to better understand how to raise registrants’ perceptions of being part of a regulated profession. Used findings as part of a “we asked, we heard you, we’re making changes” campaign

» Continue to make changes based on registrant engagement research, including improved communications for registrants

» Created two-part video on how to conduct business electronically

» Issue four videos during year, covering “how to” topics and messages about elevating professional conduct and customer service to exceed what the law requires

» Participated at 16 trade shows and interacted with 5,500 registrants. Delivered presentations at 38 registrant events

» Continue to participate in registrant trade shows and speaking opportunities

» Issued 40 e-blasts to registrants. With an average open rate of over 36%, RECO’s e-blasts were viewed almost 1.35 million times. Registrants also made over 130,000 clicks on the links included in the e-blasts

» Create a monthly e-blast newsletter to replace current approach of e-blasting ad hoc, for greater consistency and predictability

» Conduct three webinars with CEO and Registrar for Brockers of record and Executive Officers of local boards and associations

Enhance the knowledge and competence of real estate professionals2015 ANNUAL REPORT BUSINESS PLAN 2016–2018

» Introduced new residential and commercial update courses in continuing education program

» Introduce new elective courses for continuing education program with topics covering residential and commercial transactions, advertising compliance

» Decided how to proceed on registration education; decision based on extensive consultation through issuance of a white paper on registration education, surveys of other regulated sectors and surveys of multiple educational organizations

» Conduct competitive process to identify provider to develop and deliver new registration education program, incorporating leading adult learning methodologies and simulations; the new education program will move much of the existing articling curriculum (law and commercial) to the pre-registration program requirements ensuring all registrants entering the profession have a stronger knowledge base than is currently available through our current program

RECO 2015 Annual Report and 2016–2018 Business Plan l 2015

Improve service quality and relationships with registrants2015 ANNUAL REPORT BUSINESS PLAN 2016–2018

» 2015 registrant survey shows 71% satisfaction rate with RECO

» Using data from the registrant survey, carry on our program of continual improvement in all areas of our governance

» Changes to how we process renewal applications have greatly improved our processing times. In 2014, processing time for an individual renewal averaged 24 days; in 2015, the average time was just under 10 days

» Improvements to processing times will continue with the launch of RECOserv. By end of 2016, we expect all renewals will be done online; targeting eight business days for renewals applications to allow for internal checks and verifications. We expect this target will be dramatically reduced in subsequent years through internal automation; streamlining of processes will also allow us to set goals for other functions, including resolution of complaint files

» Introduced quality assurance surveys in 2015 for complaints (consumers and registrants) and inspections (registrants); will use results to guide us to provide quality service

» Inspections and complaints surveys will continue; these tools help measure the quality of our service levels and the impact of change we make, measured against our 2015 baseline. We want to substantially increase survey participation; we will act on survey results to make changes where necessary

» RECO’s inspectors completed over 700 site inspections in 2015; investigators completed a three-year high of 142 investigations

» With RECOserv and enhanced employee connectivity, we expect RECO’s inspectors will complete over 750 site inspections and 500 reconciliation inspections in 2016

» Changes and improvements to complaints handling process were a key focus in 2015:

– Piloted new process for industry-sourced advertising complaints that aims to promote registrant responsibility and professionalism; processed 19 in 2015;

– Compliance officers given greater discretion in their analysis of complaints; this includes increased consultation with parties to resolve complaint;

– Started to use early resolution; parties to this process report high levels of satisfaction and confidence that they are being heard and allowed to work toward a quicker settlement;

– Broadened net of eligible complaints for mediation or resolution between the parties, supported by RECO staff; 152 processed in 2015; this approach increases the satisfaction levels of the parties involved, as they have a say in the actual outcome. Also improves the overall turnaround times on complaints in the long term

» Changes and improvements to the complaints handling process will continue:

– as of January 2016, industry-sourced advertising complaints must be endorsed and filed exclusively by Brockers of record;

– Given the growing success of early resolution, RECO will continue to develop compliance officers’ resolution skillset and encourage adversarial parties to consider mediation as an alternative to litigation;

– Increased use of mediation — looking at ways to use this even more to settle disputes with a goal of tripling the number of 2015 resolutions, though we are limited by the willingness of the parties to achieve an agreeable resolution;

– Ongoing evolution of the complaints process will focus on fostering a compliance-first mindset with all registrants

» Introduced new residential and commercial update courses to Mandatory Continuing Education program

» Continue to develop MCE; development of the next update courses is underway, with emphasis on case studies featuring current topics and identifying challenges facing the industry

l 23REPORTING OBJECTIVES

STAKEHOLDER PRIORITIESRECO recognizes that in addition to consumers and registrants, there are many other important stakeholders who influence or are critical to the industry’s and RECO’s own success. These stakeholders include government, other provincial regulators and the three levels of organized real estate.

RECO must:

» work with government to enhance consumer protection;

» promote professionalism within the sector;

» look for opportunities to participate and contribute to industry-wide planning;

» build on the trusting relationships we have already formed; and,

» reach out to establish new relationships where, together, we can enhance professionalism and consumer confidence and be an example of excellence.

RECO’s stakeholder priorities will include:

Be proactive in supporting government and enhancing consumer protection2015 ANNUAL REPORT BUSINESS PLAN 2016–2018

» RECO educated registrants and consumers about new rules that took effect in Ontario on July 1, 2015; the rules, enforced by RECO, require brokerages to retain copies of offers and also established an inquiry process to confirm the number of offers

» Continue to work with the Ministry of Government and Consumer Services to ensure policy priorities are shared and mutually desirable goals are achieved

» At RECO’s request, the Ministry of Government and Consumer Services sought input on proposals to modernize insurance requirements under REBBA 2002 in March 2015; proposed changes are intended to streamline RECO’s administration of the insurance program and update terminology

» Work with the Ministry of Government and Consumer Services to modernize insurance requirements and improve consumer and registrant protection

» RECO volunteered to Chair the newly established Administrative Authorities Collaboration Council meetings

» Continue to participate in the Administrative Authorities Collaboration Council, as well as participating in the functional collaboration committee meetings

» RECO participated in government consumer protection initiatives

» Support government consumer protection initiatives

French language services2015 ANNUAL REPORT BUSINESS PLAN 2016–2018

» RECO’s current policy is to respond in French to all communications received in French. In 2015, RECO responded to seven inquiries in French

» RECO will continue to broaden its French-language offerings; RECO also provides basic information in French and other languages

» RECO began distributing the French versions of its Reconnect newsletter for consumers (newlyweds, expecting parents and boomers editions)

» In 2016, RECO will translate the most frequently visited and essential pages of its website (e.g. landing pages, complaint information) and continue to distribute the French version of its Reconnect newsletter for consumers

RECO 2015 Annual Report and 2016–2018 Business Plan l 2015

PEOPLE PRIORITIESRECO could not possibly deliver quality service without the dedication of talented and committed people. Throughout our organization, staff and management take pride in their work and strive to provide the highest levels of knowledge and efficiency possible to meet the needs of registrants and consumers. RECO has critical responsibilities as an employer:

» ensuring our people have a strong sense of pride and ownership in their work;

» connecting day-to-day activities to the longer term priorities and goals;

» unifying people in a strong team that contributes to measurable success; and,

» ensuring that RECO is an engaging and motivating place to work.

RECO’s people priorities will include:

Ensure a qualified, skilled, stable and sustainable workforce2015 ANNUAL REPORT BUSINESS PLAN 2016–2018

» Ongoing professional development for all staff related to their positions

» Continue to provide professional development opportunities for staff and regular performance feedback

» Annual performance reviews for all staff » Continue with annual performance reviews for all staff

» Introduced town hall meetings for all staff, with two being held in 2015 — an opportunity to provide input and learn about new initiatives

» Twice-yearly town hall meetings for all staff — an opportunity to provide input and learn about new initiatives

» Held 11 staff events » Hold regular staff events

» Launched Intranet site to support and encourage organization collaboration, corporate communication and knowledge management

» Further development of the internal Intranet site

» Conduct an employee engagement initiative through a third party, including an online survey of all staff, to determine the level of satisfaction and potential areas for improvement

Shape a culture of excellence throughout the organization2015 ANNUAL REPORT BUSINESS PLAN 2016–2018

» RECO set customer service standards » Continual assessment and improvement of customer service standards

» Business Process RECOnfiguration (RECOserv) workshops for all staff

» Business Process RECOnfiguration (RECOserv) training for staff as RECOserv rolls out in 2016

» Customer service training for all staff » Ongoing customer service training for all staff

» Accessibility for Ontarians with Disabilities Act (AODA) training for all staff

» Ongoing AODA training for all staff

» IT security training for all staff » Ongoing IT security training for all staff

l 25REPORTING OBJECTIVES

INTERNAL SYSTEMS PRIORITIESBalancing resource efficiency, effectiveness, quality, service excellence, and stakeholder accountability is a delicate act. Added pressures to “do more with less” have become the standard for most organizations. With that in mind, RECO will:

» continuously seek out ways to deliver more, more effectively, with higher quality and consistency; and,

» ensure that investments in technology enable RECO to stay ahead and deliver relevant, reliable tools that can advance the goals of increased efficiency, effectiveness and quality service.

RECO’s internal systems priorities will include:

Ensure reliable systems and processes for core business2015 ANNUAL REPORT BUSINESS PLAN 2016–2018

» Significant progress made on the Business Process RECOnfiguration project, RECOserv; in 2015, RECO completed its requirements-gathering phase and the first two of five modules

» RECOserv rollout in Oct 2016; it will deliver a stable, modern and more capable system for RECO’s core business activities, including registrant information management and complaint case management

» Launch of Intranet site to support better corporate communication and knowledge management

» Increased development and use of Intranet site

» In 2015, three minor unplanned system outages to internal business systems; in all cases systems were restored within four hours of reported issue

» RECO’s performance target for business continuity in 2016: less than three failures and less than four hours to full resolution for any system outages

» In 2015, zero data security incidents at RECO » RECO’s performance target for safeguarding data in 2016: zero incidents

» Cyber security awareness training completed for all internal staff to help employees recognize and respond appropriately to real or potential cyber security threats

» Put in place improved intrusion prevention systems to safeguard RECO’s data from potential cyber security threats

» Launch of new, easier to use, version of the MyRECO certificate app

Embrace principles of continuous quality improvement throughout the organization2015 ANNUAL REPORT BUSINESS PLAN 2016–2018

» The main inquiry call centre kept average wait times to 24 seconds

» Goal for main inquiry call centre average wait times is within two minutes, in keeping with RECO’s service standards

» Introduced quality assurance surveys in 2015 for complaints (consumers and registrants) and inspections (registrants); will use results to guide us to provide quality service

» Continue to survey consumers and registrants about their experience with the complaints process; will survey registrants about inspections

» Continued to expand electronic service delivery in 2015 to improve service in a number of operational areas

» Continue to look at ways to improve service through the increased use of electronic service delivery

» Conduct an employee engagement survey and use the results to make quality improvements

RECO 2015 Annual Report and 2016–2018 Business Plan l 2015

FINANCIAL PRIORITIESThe Ministry, consumers and registrants expect the highest level of financial stewardship and accountability from RECO. Throughout our history we have been diligent in ensuring that our operational and governance systems and processes related to financial stewardship meet the highest standards possible and we have made great progress. It is important for RECO to:

» pay constant attention to the evolving needs and expectations of government;

» be disciplined and transparent in its dealings and relationships; and,

» make the most of financial resources.

RECO’s financial priorities will include:

Allocate funds responsibly to support strategic and operational priorities and ensure the long-term financial stability and endurance of the organization2015 ANNUAL REPORT BUSINESS PLAN 2016–2018

» Board of Directors held annual planning session in September; budget developed for 2016–2018 fiscal years based on identified strategic and operational priorities

» Board of Directors will hold its strategic planning session in the fall of 2016 to establish strategic goals in preparation for budget development for 2017–2019 fiscal years

Ensure accountability and transparency in the use of resources2015 ANNUAL REPORT BUSINESS PLAN 2016–2018

» Followed expense and procurement policies that are consistent with spirit and intent of government policies and practices

» RECO adheres to the expense and procurement policies that are consistent with the spirit and intent of government policies and practices

» Audited financial statements for fiscal 2015 are published in the Annual Report

» Budget for 2016 and financial plans for 2017 and 2018 are included in this report under section Business Plan Financials

l 27REPORTING OBJECTIVES

FinancialsMANAGEMENT DISCUSSION AND ANALYSISThis management discussion and analysis provides supplementary information for stakeholders and other readers of the financial statements of the Real Estate Council of Ontario (RECO). The analysis should be read in conjunction with the audited financial statements which follow.

In connection with its continuance under the Canada Not-for-Profit Corporations Act, RECO changed its fiscal year from April 1–March 31 to January 1–December 31. This has resulted in a 12-month fiscal period of January 1, 2015 to December 31, 2015 preceded by a 9-month fiscal period of April 1, 2014 to December 31, 2014.

Overview

RECO has two reporting categories: General Operations, and the Insurance Program. General operating receipts are derived primarily from registration fees required under the Real Estate and Business Brokers Act, 2002 (REBBA 2002): these are amortized to income over the two-year period of each registration. Operating revenue also includes payments under the Education Services Agreement with the Ontario Real Estate Association (OREA), where certain payments required under the agreement for the provision of the Pre-registration, Articling and Broker Educational Program are being recognized over the term of the agreement with payments based on annual enrolments being recognized in the current year. In August, 2013, RECO launched the RECO Mandatory Continuing Education (MCE) program for direct delivery to registrants of MCE requirements. Fees for RECO’s MCE program are recognized in the year received. Other sources of revenue include transfer fees, fines assessed by disciplinary panels, miscellaneous revenues, and interest, all of which are recognized in the current year.

Insurance Program receipts are required to be held in trust and segregated from general operating funds. Insurance payments include the premiums, the contribution to the premium stabilization fund, the contribution to the insurance administration fund plus the applicable taxes. Insurance receipts are amortized to income over the period of the insurance policy — September 1 to August 31. Other revenues include suspension fees and interest income, which are recognized in the year received.

RECO 2015 Annual Report and 2016–2018 Business Plan l 2015

MANAGEMENT OF CAPITALRECO defines its capital as its net assets for both the Operations Fund and the Insurance Program Funds.

For the Operations Fund, as a delegated administrative authority, RECO’s principal objective is to manage these assets in a manner that allows it to continue to meet the requirements of the administrative agreement with the Ministry of Government and Consumer Services, which includes a requirement to ensure it has adequate resources to comply with the agreement, REBBA 2002 and the Safety and Consumer Statutes Administration Act, 1996.

For the Insurance Program Funds, RECO’s principal objective is to continue to provide for insurance coverage for consumer deposits (protection of consumers), for errors and omissions insurance (protection of consumers and registrants), and for commission protection insurance (protection of registrants) at affordable rates for registrants. Net assets of the Insurance Program Funds are restricted for use in the Insurance Program.

l 29FINANCIALS MANAGEMENT DISCUSSION AND ANALYSIS

GENERAL OPERATIONSRevenues and ExpensesAs noted, the current fiscal period (2015) represents 12 months of activity whereas the previous fiscal period represented 9 months of activity. Under these circumstances, revenues and expenses show significant increases — 45% and 28% respectively.

12-months vs 9-months

2015 2014 Change %

$ $ $

Registration Fee Income 12,884,738 8,936,440 3,948,298 44

Education Revenues 2,881,521 1,885,256 996,265 53

Other income 1,275,405 913,727 361,678 40

Total revenues 17,041,664 11,735,423 5,306,241 45

Expenses 16,227,159 12,635,668 3,591,491 28

To provide more meaningful comparisons year over year, the schedule below describes what the results would have been had 2014 also reflected a 12-month period. In these circumstances, revenues would show an overall increase of $514,768 or 3% and expenses would show an overall decrease of $495,012 or 3%.

12-months vs 12-months

2015 2014 Change %

$ $ $

Registration Fee Income 12,884,738 12,711,006 173,732 1

Education Revenues 2,881,521 2,568,778 312,743 12

Other income 1,275,405 1,247,112 28,293 2

Total revenues 17,041,664 16,526,896 514,768 3

The increase in registration revenues is due to the increase in the number of registrants in the preceding and current year. The increase in education revenues results from higher enrolments in the pre-qualifying, articling and broker education courses delivered by OREA.

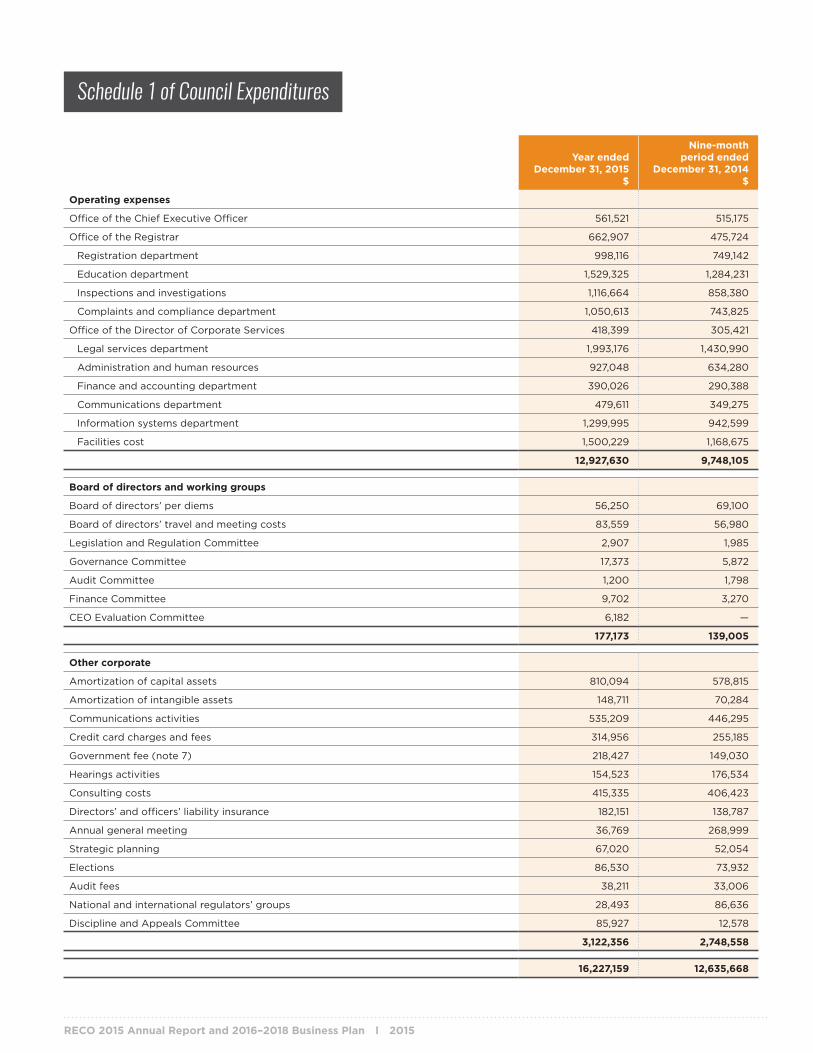

There are three main categories of expenses: operating departments and facilities; Board of Directors and committees; and other corporate expenses, which include communications activity, amortization of capital assets, external consulting, elections and other expenses. Operating expenses increased overall by 1%; Board and committees were 10% lower; and other corporate expenses were 16% lower. This is shown in the table below.

12-months vs 12-months

2015 2014 Change %

$ $ $

Departments and facilities 12,927,630 12,798,536 129,094 1

Board and committees 177,173 197,921 (20,748) (10)

Other corporate expense 3,122,356 3,725,714 (603,358) (16)

Total expenses 16,227,159 16,722,171 (495,012) (3)

Net Current AssetsNet current assets at December 31, 2015, which exclude deferred liabilities, were $20,636,413 compared to $19,684,083 at December 31, 2014.

Net Income and Accumulated Fund BalanceNet income for the 12-month period ended December 31, 2015 was $1,084,198 compared to a net loss of $684,964 for the 9-month period ended December 31, 2014. This net income increased the accumulated fund balance to $10,797,435 at December 31, 2015 from $9,713,237 at December 31, 2014.

RECO 2015 Annual Report and 2016–2018 Business Plan l 2015

INSURANCE PROGRAMRevenues and ExpensesAs with the Operations Fund, comparing revenues and expenses of a 12-month period to those of a 9-month period shows significant increases in revenues and expenses. Revenues show an increase of 40% and expenses show an increase of 38%.

12-months vs 9-months

2015 2014 Change %

$ $ $

Insurance premium 24,105,747 17,193,837 6,911,910 40

Premium stabilization 860,918 623,032 237,886 38

Insurance administration 924,512 657,492 267,020 41

Other income 118,065 126,521 (8,456) (7)

Total revenues 26,009,242 18,600,882 7,408,360 40

Expenses 25,153,185 18,192,051 6,961,134 38

To provide more meaningful comparisons year over year, the schedule below describes what the results would have been had 2014 also reflected a 12-month period. In these circumstances, revenues would show an overall increase of $1,390,624 or 6% and expenses would show an overall increase of $1,201,427or 5%.

12-months vs 12-months

2015 2014 Change %

$ $ $

Insurance premium 24,105,747 22,791,182 1,314,565 6

Premium stabilization 860,918 825,835 35,083 4

Insurance administration 924,512 871,246 53,266 6

Other income 118,065 130,356 (12,291) (9)

Total revenues 26,009,242 24,618,618 1,390,624 6

Expenses 25,153,185 23,951,758 1,201,427 5

The insurance premium, which accounts for most of the revenues and expenses, increased by 4%. A further 2% increase is due to the higher number of registrants year over year. The higher number of registrants subscribing to the program resulted in higher premium stabilization and insurance administration revenues. The reduction in other income is primarily lower suspension fees as more registrants paid by the due date and avoided the suspension process. On the expense side, the increase in premium expense of $1,314,565 was offset by reductions in costs to administer the program.

Net Income and Accumulated Fund BalanceAll premiums collected under the program are payable to the insurer. As a result, net income for the premium fund is virtually nil. Interest income is allocated 66% to the premium stabilization and 34% to the insurance administration funds. Insurance program operating expenses are charged to the Insurance Administration Fund. Net income for the premium stabilization fund was $1,057,312 for the 12-month period to December 31, 2015 compared to $623,032 for the 9-month period ended December 31, 2014. Net loss in the insurance administration fund was $4,861 for the 12-month period compared to $131,311 for the preceding 9-month period. At December 31, 2015, the accumulated fund balances were: $54,369 in the premium fund; $17,871,646 in the premium stabilization fund; and $500,714 in the insurance administration fund.

Net Current AssetsNet current assets, excluding deferred revenues and prepaid premiums, were $20,297,893 at December 31, 2015 compared to $19,030,058 at December 31, 2014.

l 31FINANCIALS MANAGEMENT DISCUSSION AND ANALYSIS

Auditor’s ReportMarch 24, 2016

INDEPENDENT AUDITOR’S REPORTTo the Registrants of Real Estate Council of Ontario

We have audited the accompanying financial statements of Real Estate Council of Ontario, which comprise the statement of financial position as at December 31, 2015 and the statements of operations and cumulative operations and insurance program fund balances and cash flows for the year then ended, and the related notes, which comprise a summary of significant accounting policies and other explanatory information.

Management’s responsibility for the financial statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with Canadian accounting standards for not-for-profit organizations, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements present fairly, in all material respects, the financial position of Real Estate Council of Ontario as at December 31, 2015 and the results of its operations and its cash flows for the year then ended in accordance with Canadian accounting standards for not-for-profit organizations.

Chartered Professional Accountants, Licensed Public Accountants

Toronto, Ontario

RECO 2015 Annual Report and 2016–2018 Business Plan l 2015

Statement of Financial Position

Operations Fund Insurance Program Funds TotalAs at December 31 2015 (unless noted) 2015 2014 2015 2014 2015 2014

Assets $ $ $ $ $ $

Current AssetsCash 1,043,955 789,343 442,027 256,146 1,485,982 1,045,489

Short-term investments (note 2) 20,329,969 19,180,047 20,006,542 18,960,137 40,336,511 38,140,184

Accounts receivable 573,783 477,611 89,536 95,557 663,319 573,168