2015 09-22 advanced long term care planning

TRANSCRIPT

Thrive. Grow. Achieve.

Advanced Long Term Care (LTC) Planning for Medium and Large Size Estates

David Hillelsohn – The Haslett Management Group

September 22, 2015

How will you prepare for long term care? Help protect your lifestyle and assets

What are YOUR retirement goals?

o Financial security

o More time with family

o Travel

o A second home

o Leaving a legacy

How will you get there?

3

Could it happen to me? It could happen to anyone, at any time. Many people think only the elderly need long term care, but the reality is that accidents and illnesses can happen to anyone, at any time, and they often occur without warning. While people may recognize long term care costs as a significant risk to their standard of living, many don’t have a plan. Planning for long term care is critical …

Do you know someone who has needed Long Term Care? Yes No

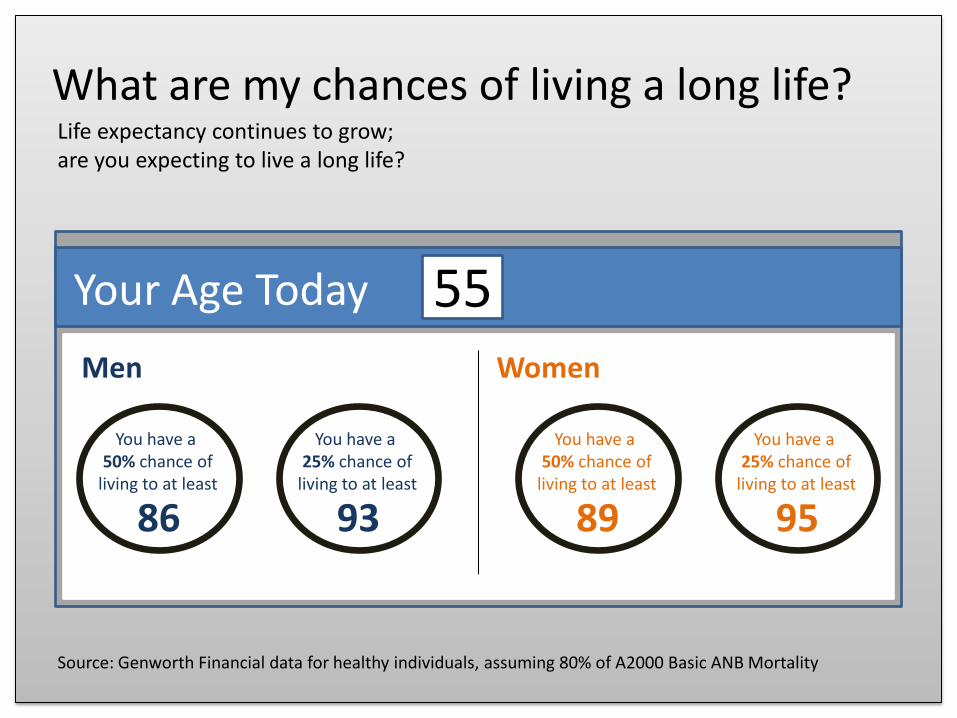

What are my chances of living a long life? Life expectancy continues to grow; are you expecting to live a long life?

55 Your Age Today Men Women

You have a 50% chance of

living to at least

You have a 25% chance of

living to at least

You have a 50% chance of

living to at least

You have a 25% chance of

living to at least

86 93 89 95

Source: Genworth Financial data for healthy individuals, assuming 80% of A2000 Basic ANB Mortality

Primary Retirement Concerns

Source: AgeWave/Harris Interactive Survey, 2010

45% 38%

17%

Medical expensesnot covered by

insurance

Outliving savings,lack of social

security and pension

Lack of personalsavings

When you think about your financial security during retirement, which of the following are you most worried about?

How will I handle unexpected medical expenses?

Will I have enough income to sustain my lifestyle in the future?

Primary Retirement Concerns

Primary Retirement Concerns

Extended healthcare is a reality

1 Source: U.S. Department of Health and Human Services National Clearinghouse for Long Term Care Information website, May 2010 2 Source: Genworth Financial Claims Data, December 2009 3 Source: National Institute on Aging, National Institute of Health, 2/09

3.8 years 2

Average length of majority of long term care claims

4-7 years 3

Average life expectancy after Alzheimer's diagnosis after age 70 2 3

people 1

out of

People over 65 who will require long term care

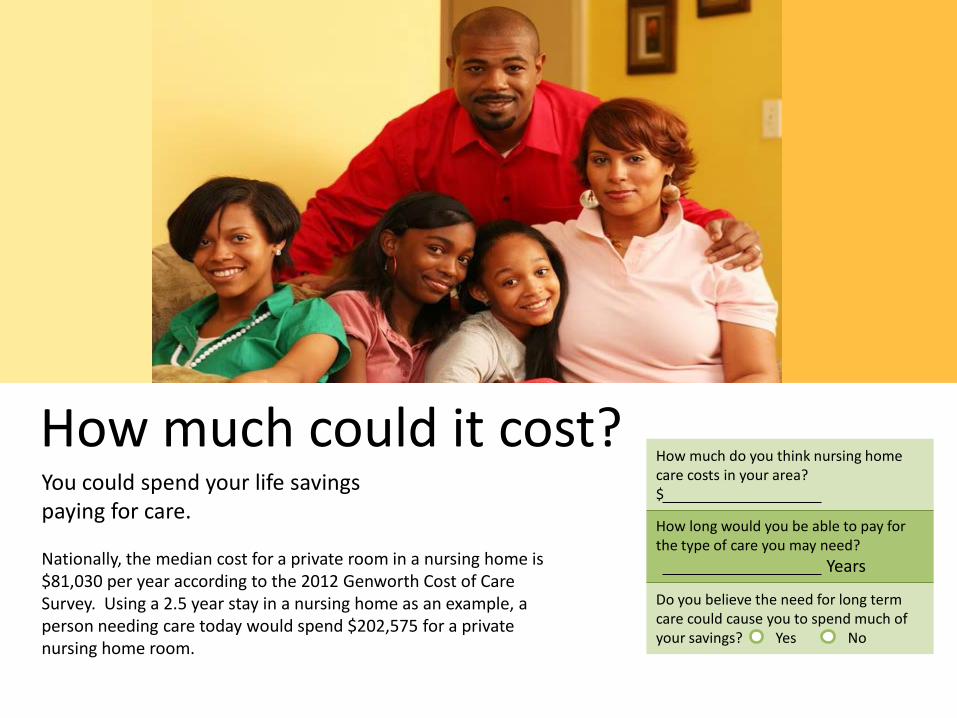

How much could it cost? You could spend your life savings paying for care.

Nationally, the median cost for a private room in a nursing home is $81,030 per year according to the 2012 Genworth Cost of Care Survey. Using a 2.5 year stay in a nursing home as an example, a person needing care today would spend $202,575 for a private nursing home room.

How much do you think nursing home care costs in your area? $

How long would you be able to pay for the type of care you may need? Years

Do you believe the need for long term care could cause you to spend much of your savings? Yes No

11

What are your options? There are many options to consider. Here are just a few.

Have you discussed Long Term Care issues with your spouse and/or family?

Spouse Yes No

Family Yes No

12

Option 1: Public Programs Generally, Medicare does not cover indefinite long term care, whether provided at home, in the community or in assisted living facilities. Nor was it designed to adequately cover “custodial care”; eating, bathing, dressing or using the restroom. What Medicare doesn’t cover is left for individuals to pay unless you have spent down to your states poverty level.

Option 3: Private/Family Support Of course, family and friends might care for you. Initially, this may seem like a good solution. However, ask yourself: Do I want to ask this of them? Will it change our relationship? Can I preserve family relationships?

Option 2: Self-Insure You might not realize it, but right now you’re self-insured, unless you’re otherwise covered. Without coverage, you have assumed the primary financial risk for the costs of long term care.

Option 4: Transfer the Risk Asset protection is essential to financial stability. No doubt you have already taken steps to ensure your financial well-being in the event of accidents. There are many approaches you can consider.

Option 5: All of the above By integrating public programs with private help and resources, you can develop a comprehensive plan to meet your needs.

Your options in risk transfer

Linked Benefits Products Reposition existing asset, exercise leverage and control

Traditional Long Term Care Insurance A percentage of your portfolio can pay premium

Business owners can deduct premiums

Transfer Risk

How to put your savings to work for you!?!

Male 55 LTC Funding Options

Genworth Financial Total Living Coverage Nationwide NLG-UL with LTC Rider – 15 Pay

Seeking monthly Long Term Care Benefit of $8,000 per month

Age 55 Single Premium $85,745 Total Premium $85,745

Age 55 Age 85 Premium $8,954 $8,954 Total Premium $8,954 $134,310

1 Assumes use of Flex Credit over the life of the policy and no Waiver of Premium

John Hancock Performance LTC

Age 55 Age 65 Age 75 Age 85 Annual Premium $1,426 $1,471 $1,463 $1,193 Total Premium $1,426 $14,753 $29,352 $44,900

For illustration purposes only. Values reflected are assumed to be accurate based upon carrier illustrations as of April 29, 2015. FOR AGENT USE ONLY

Potential Scenarios Scenario 1: Insured never needs Long-Term Care and passes away at age 85 Scenario 2: Client needs long-term care for 12 months beginning at age 80, and then passes away Scenario 3: Client receives 4-years of covered service beginning at age 80 before passing away

For illustration purposes only. Values reflected are assumed to be accurate based upon carrier illustrations as of April 29, 2015. FOR AGENT USE ONLY

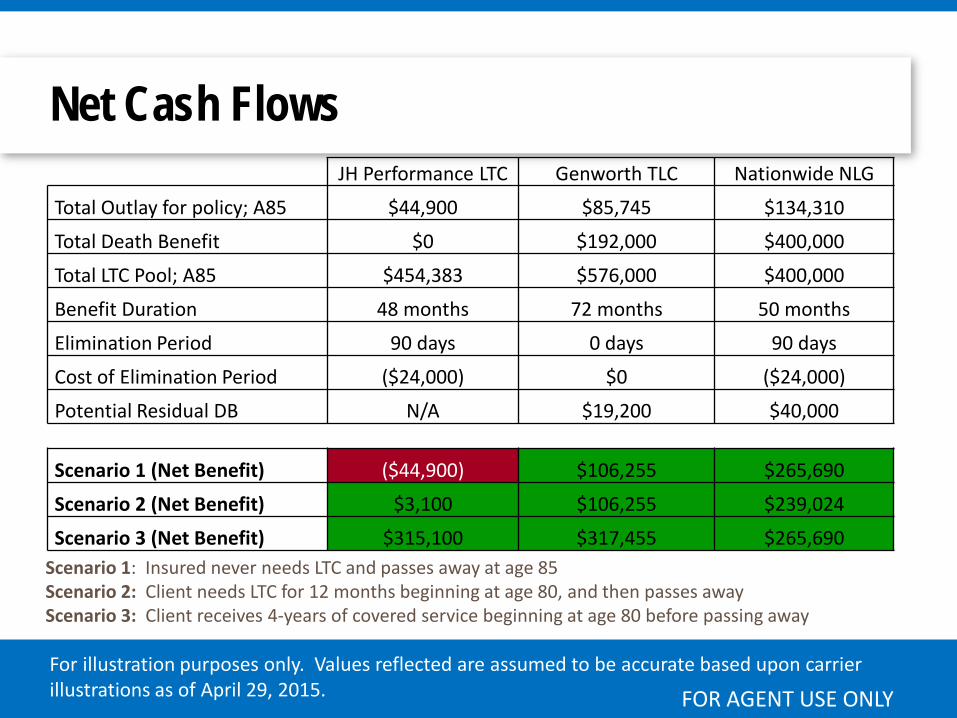

Net Cash Flows

Scenario 1: Insured never needs LTC and passes away at age 85 Scenario 2: Client needs LTC for 12 months beginning at age 80, and then passes away Scenario 3: Client receives 4-years of covered service beginning at age 80 before passing away

JH Performance LTC Genworth TLC Nationwide NLG

Total Outlay for policy; A85 $44,900 $85,745 $134,310 Total Death Benefit $0 $192,000 $400,000

Total LTC Pool; A85 $454,383 $576,000 $400,000

Benefit Duration 48 months 72 months 50 months

Elimination Period 90 days 0 days 90 days

Cost of Elimination Period ($24,000) $0 ($24,000)

Potential Residual DB N/A $19,200 $40,000

Scenario 1 (Net Benefit) ($44,900) $106,255 $265,690

Scenario 2 (Net Benefit) $3,100 $106,255 $239,024

Scenario 3 (Net Benefit) $315,100 $317,455 $265,690

For illustration purposes only. Values reflected are assumed to be accurate based upon carrier illustrations as of April 29, 2015. FOR AGENT USE ONLY

What’s the right approach?

Linked Benefits Products

Traditional Long Term Care Insurance

Protection of Principal

Interest Earning Pays the Premium

Partial Deductibility of Premium

Maximum protection for LTC

Transfer of Existing Assets

No Ongoing Premium Required

Availability of Assets to Transfer

Client willing to co-Insure the risk

You already protect your other assets

Health – Health Insurance

Family – Life Insurance

Car – Car Insurance

Home – Homeowners

Retirement Savings – ??

Why not help protect the retirement wealth that

you work your entire life to accumulate?

18

What should you do? Everyone’s needs are different.

Weighing all of the risks and costs is critical. It helps you determine the amount of protection you need in order to secure your assets and savings. Long term care insurance helps cover the costs of long term care. It doesn’t replace what families do; it builds on your existing infrastructure of support, so caregivers can provide better care for a longer period of time. In short, long term care insurance can help you maintain your lifestyle, protect your assets and savings, and give you the options necessary to receive quality care and services.

Key Tax Concepts – LTCi is Accident and Health

• Employer may deduct premium 100% for LTCi purchased for employees

• Business Owners may have income limits based upon Corporate Structure

• Employer can identify class of participants • Premium not treated as income for non-owner

employees • Reimbursement LTCi Benefits are received Income

Tax-Free • Employee Paid LTCi paid with after-tax dollars

The Haslett Management Group, Inc.

Not intended to be tax advice. Please consult a tax professional for details.

2015 LTCi Eligible Premium Limits

Age of Insured before the Close of the Year

Eligible Premium Limit

Age 40 or less $ 380 Ages 41 to 50 $ 710 Ages 51 to 60 $1,430 Ages 61 to 70 $3,800 Ages 70 & Over $4,750

The per-diem limitation under Section 7702B(d)(4) for periodic payments received under a qualified long term care insurance contract have been increased for 2015 to $330.

The Haslett Management Group, Inc. Not intended to be tax advice. Please consult a tax professional for details.

Key Tax Concepts •Eligible Premium Limits are counted towards

unreimbursed medical expenses

•A Health Savings Account (H.S.A.) can be used to help pay LTCi premiums up to the Eligible Premium Limit

•2% of greater owner’s of S-Corporations, LLC’s, and Partners in a Partnership can take a deduction for Corporate Paid LTC coverage up to the Eligible Premium Limit

•There is no Eligible Premium Limitation for C-Corporations and Non-Profit Organizations

The Haslett Management Group, Inc.

Not intended to be tax advice. Please consult a tax professional for details.

Plan Comparison Insurance Carrier Genworth Financial John Hancock LifeSecure Mutual of Omaha

A.M. Best Rating A - A + A - A+

Product Name PC Flex 3 Sponsored Group One for Many Secure Solution

Number Needed for Discount No Minimum 3 total participants 10 Total Applicants 5 Eligible Employee

participants

Voluntary Premium Discount

Available N/A 5% 3% 5%

Underwriting Offer Full Underwriting with List Bill

Full Underwriting with Premium

Discount

Simplified Issue with 10 total applicants to

include Actively at Work spouses; Rx and MIB to verify SI criteria and paystub

Full Underwriting with Premium Discount using Gender Based

Pricing

Eligible Employee Actively at Work to Age 75

Age 18 – 75 working 30 hrs/wk

Age 18 – 65 working 20 hrs/wk; Full

Underwriting to Age to Age 79

Age 18 – 79 working 30 hrs/wk

Enrollment Period Ongoing 180 Days 90 Days Max 60 Days

Final offer made by the Insurance Company upon receipt of required documentation to establish an Employer Sponsored Long Term Care program. Some product variations may apply based upon product selection and state of residence.

Plan Comparison Insurance

Carrier Genworth Financial John Hancock LifeSecure Mutual of Omaha

Program PC Flex 3 Sponsored Group (New) One for Many (2) Secure Solution

Monthly Premium Summary

Benefit Limit

$3,000/Month of Benefit up to $108,000 of Initial

Benefit

$3,000/Month of Benefit up to $108,000 of Initial

Benefit

$3,000/Month of Benefit up to $100,000 of Initial

Benefit

$3,000/Month of Benefit up to $109,500 of Initial

Benefit

Age 40 $66.35 / $85.71* n/a $37.17 $38.48 / $58.39*

Age 50 $73.67 / $103.04* n/a $49.42 $47.26 / $69.66*

Age 60 $89.27 / $115.10* n/a $79.33 $67.60 / $104.35*

Benefit Limit

$3,000/Month of Benefit up to $108,000 of Initial Benefit with Annual 3%

Compound Growth

$3,000/Month of Benefit up to $108,000 of Initial

Benefit with Annual CPI-Compound Growth

$3,000/Month of Benefit up to $100,000 of Initial Benefit with Annual 3%

Compound Growth

$3,000/Month of Benefit up to $109,500 of Initial Benefit with Annual 3%

Compound Growth

Age 40 $88.75 / $134.46* $86.38 $90.32 $81.20 / $125.89*

Age 50 $101.58 / $151.98* $107.54 $106.25 $97.11 / $154.65*

Age 60 $130.66 / $194.62* $144.56 $147.56 $124.72 / $204.11*

Premiums noted are for illustration purposes only using pricing as April 23, 2015 based upon situs state. Final Offer made by the Insurance Company and some state variations may apply. Consult the Outline of Coverage for coverage details. * Genworth and Mutual

of Omaha figures show Gender Specific pricing, Male / Female pricing shown above.

Need for Assistance is Universal

• Expanded health care delivery at time of crisis – Round-the-clock home health care – Aides who provide custodial care – Assisted living /nursing facility use – Continuing Care Retirement Communities

• Increased health care costs due to customized services – Round-the-clock home health care cost range: $120,000 - $300,000 per year – High-end facilities cost range: $100,000 - $250,000 per year The Haslett

Management Group, Inc.

Long Term Care Strategies for High Net Worth Clients

• Co-Insuring Aspects of LTCi Risk – Longer Waiting Periods – Inflation Component – Lump Sum Asset Allocation

• High-End delivery expectations on LTC services – Largest policy sold in Virginia with $800/day of benefit – Higher cost providers / more selective of types of providers

• Corporate Paid LTC with Return of Premium • 1035 Exchange of an appreciated asset into LTCi Plans • Establishing a fiduciary roadmap for the family • Protecting the ability to meet future financial obligations • Purchasing Long Term Care Insurance for family members

– Accident and Health Insurance is free from gift tax implications The Haslett

Management Group, Inc.

Trust Implications

• Incidental Ownership in Traditional LTC policy – Few Companies Allow It – Carriers Allow Assignment of Benefit to a Provider – Requires Specific Trust Language to include Obligation to Pay LTC expenses

• Trust Ownership of Hybrid LTC Plans – Trust document must include wording permitting the trust to own life insurance – The Trust must have an insurable interest in the individual insured under the life insurance policy – The trust must have an insurable interest in the insured for purposes of health insurance – The trust must be obligated to pay the insured’s long term care expenses

• Insurable Interest – For Life Insurance, the policy-owner would suffer a financial loss if the insured died – For LTC Insurance, where the policy-owner has an obligation to pay the insured’s medical or long term care

expenses • Obligation to Pay Insured’s LTC Expenses

The LTC benefits under a hybrid Life/LTC plan must be paid either directly to the service provider or as a reimbursement to the owner for actual LTC expenses incurred1. If a trust owned a hybrid policy but the trustee was not permitted to pay the insured’s LTC expenses, the carrier would not be able to pay the claim without the trust violating its terms. To avoid such a result and ensure suitability of ownership, the carrier would require that the trustee have an obligation to pay the insured’s LTC expenses. 1 IRC §101(5)(1)(B) The Haslett

Management Group, Inc. Not intended to be legal advice. Please consult a legal professional for details.

Divorce and Pre-Nuptial Implications related to LTC

• Pre-Nuptial Agreements – Protection of existing assets and claims of maintenance should couple split – Cannot waive a spouse’s duty to provide support

• Includes food, shelter, and medical care – Medicaid does not recognize prenuptial agreements – Wealthy spouse should consider buying LTCi for the spouse with little property

• Traditional LTCi or Lump-Sum Hybrid – Note state variations do exist

• Divorce – Immediate need for LTCi protection – Typically more of a negotiation component without plan implementation

• If not court decreed, an amount equal to the age-based limit will not be considered a taxable gift

• Step-Family relationships create an additional consideration when planning for Long Term Health Care needs

• Establishing a fiduciary roadmap for the family

The Haslett Management Group, Inc.

Tax Law Implications for LTCi Pension Protection Act of 2006

•Effective 1/1/2010 for policies sold after 1996

•Prior to 1/1/2010, LTC Benefits and Charges From Annuity-LTC Are Taxable – Life-LTC products were previously given non-taxable status on QLTC benefits

•Key Changes – Qualified LTC riders under a non-tax qualified annuity contract will be treated as a separate

contract, thus withdrawals for QLTC benefits from these riders are considered tax free benefits

– Entire Annuity Linked Benefit contract requires 7.7% DAC Tax vs. 1.75% on Annuity only contracts

– LTC rider charges against the account value will be tax-free, although they reduce the client’s cost basis (but not below zero)

– Exchanges (including partial 1035s) made from a life insurance policy or annuity contract into a traditional LTC policy will not be subject to taxes on the accumulated gain in the prior contract

– Eligible retired public safety officer may use tax-free distributions from qualified plans to pay for QLTC coverage

The Haslett Management Group, Inc. Not intended to be tax advice. Please consult a tax professional for details.

Have you taken steps to help protect yourself against potential long term health care costs? Yes No

How would you prefer to pay for the costs of long term care?

Personal savings and assets

Insurance / Risk Sharing

Do you believe you could need care at some point in the future?

Yes No

It’s time to get started….

We can help you. Raffa Financial Services, Inc. is a comprehensive insurance and employee benefit brokerage and consulting firm located in Rockville, Maryland. The firm has a staff of twenty five (25) employees and producers with an average of 14 years of industry experience per staff member. Raffa Financial Services core competencies include the following services: • Employee Benefits Brokerage and Consulting • Executive Benefit and Business Continuation Planning • Retirement Plan Advisory Services • Individual Financial and Insurance Planning

We understand that our business is extremely personal, and we acknowledge that our services are most likely needed during the most difficult circumstances that our clients could possibly face. When our clients are sick or hurt, when someone is disabled, when a loved one is lost or when you face the uncertainty of retirement, our firm and our staff has to be there to provide knowledge, certainty, support and empathy. At Raffa, we know that our legacy is millions of dollars in insurance contacts that will support those who need help the most. We live, work and support our clients with this knowledge every day. Most importantly, we care.

Steven K. Heger, CLU, PPC President

(877) 403-2540

Jeyalene Baron Broker

(240) 403-2556