2015 06 15 eu refining roundtable_iea

TRANSCRIPT

Fifth Meeting of the EU Refining ForumBrussels, 15 June 2015

International Energy Agency

Recent Developments in EU Refining and in the Supply and Trade of Petroleum Products

© OECD/IEA 2014

© OECD/IEA 2012 © OECD/IEA 2014

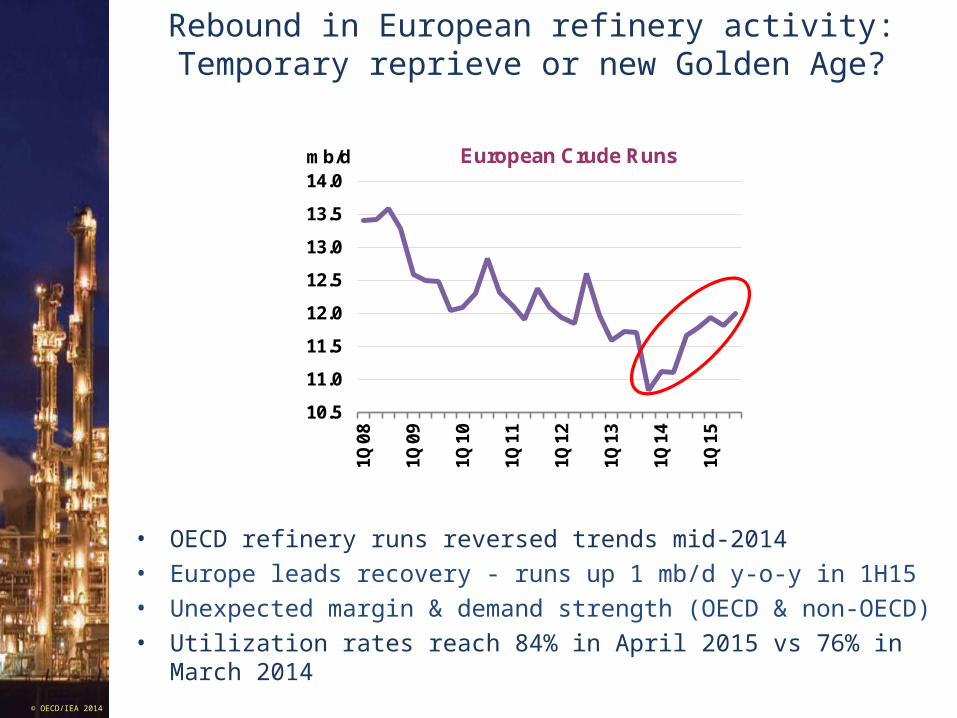

Rebound in European refinery activity:Temporary reprieve or new Golden Age?

• OECD refinery runs reversed trends mid-2014 • Europe leads recovery - runs up 1 mb/d y-o-y in 1H15• Unexpected margin & demand strength (OECD & non-OECD) • Utilization rates reach 84% in April 2015 vs 76% in March 2014

10.5

11.0

11.5

12.0

12.5

13.0

13.5

14.0

1Q08

1Q09

1Q10

1Q11

1Q12

1Q13

1Q14

1Q15

mb/d European Crude Runs

© OECD/IEA 2012 © OECD/IEA 2014

Lingering threat of over-capacity

• New capacity of 6.4 mb/d by 2020• Led by non-OECD Asia, Middle East• Scaled back since oil price drop

– Chinese projects stalling, new closures

• New product bypassing refining system• Surplus capacity still seen up to 5 mb/d in 2020, from 6-yr low

~3 mb/d in 2014

-1 000

- 500

0

500

1 000

1 500

2 000

2014 2015 2016 2017 2018 2019 2020

kb/d

OECD Americas

OECD Europe

OECD Asia Oceania

China

Other Asia

Middle East

Other non-OECD

Total Net

Global crude distillation capacity additions

© OECD/IEA 2012 © OECD/IEA 2014

EU as “sick man” of refining industry

• Falling regional demand

• High energy & labour costs

• Ageing, fragmented industry

– Only one European refinery > 400 kb/d (Shell Pernis)

– Vs. 10 in Asia, 8 in N. America, 5 in the Middle East

• Disadvantaged feedstock costs

• Heavy regulatory burden

© OECD/IEA 2012 © OECD/IEA 2014

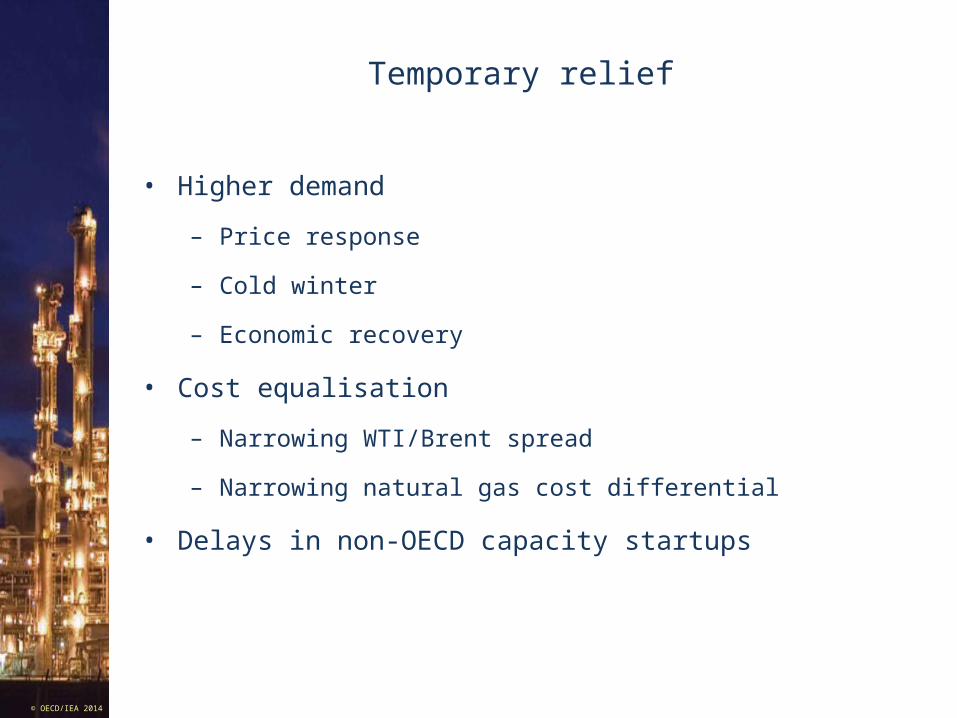

Temporary relief

• Higher demand

– Price response

– Cold winter

– Economic recovery

• Cost equalisation

– Narrowing WTI/Brent spread

– Narrowing natural gas cost differential

• Delays in non-OECD capacity startups

© OECD/IEA 2012 © OECD/IEA 2014

Price reset

• 60% drop in crude oil prices June 2014 - January 2015• From backwardation to contango• Slowing US LTO supplies, Atlantic surplus lift NYMEX WTI

more than Brent (WTI-Brent narrowed to $4/bbl)

40

50

60

70

80

90

100

110

120

Jan 14 Apr 14 Jul 14 Oct 14 Jan 15 Apr 15

$/bblCrude Futures

Front Month Close

NYMEX WTI ICE Brent

Source: ICE, NYMEX

© OECD/IEA 2012 © OECD/IEA 2014

Demand rebound

• First time annual demand growth > 2 mb/d since 2010

-1%

0%

1%

2%

3%

-1

0

1

2

3

1Q2011 1Q2013 1Q2015

mb/d Global y-on-y absolute growthTotal products growth rate

LPG Naphtha GasolineJetKero Diesel RFOOther Total (RHS)

© OECD/IEA 2012 © OECD/IEA 2014

Non-OECD startup delays

• 1.5 mb/d aggregated delays

• Saudi Arabia (Yanbu), UAE (Ruwais), India (Paradip), Brazil

(Abreu e Lima), Colombia (Cartagena expansion)

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

1Q13 3Q13 1Q14 3Q14 1Q15 3Q15

mb/d Global Crude ThroughputsAnnual Change

OECD Non-OECD

© OECD/IEA 2012 © OECD/IEA 2014

Non-OECD capacity fails to keep up with demand

• Global refinery crude intake estimated 1.4 mb/d higher for each of the first three quarters.

However, non-OECD refiners fail to meet demand as new refineries slow to start up – providing support to OECD and entire oil complex

While OECD – essentially Europe – was responsible for most of growth so far this year, non-OECD to take over in 3Q

- 0.5

0.0

0.5

1.0

1.5

2.0

2.5

1Q12 1Q13 1Q14 1Q15

mb/d Non-OECD Throughputs vs. DemandAnnual growth

Crude Runs Oil Product Demand

© OECD/IEA 2012 © OECD/IEA 2014

European refiners pick up the slack as runs grow faster than regional demand

• Demand up by 0.5 mbd in 1Q15 y-o-y, reversing earlier drops

• European throughputs fall faster than demand in 2014…

• …but rebound faster than demand in 2015

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

1Q09 1Q10 1Q11 1Q12 1Q13 1Q14 1Q15

mb/d Demand, crude runs change y-o-y

delta demand delta crude runs

© OECD/IEA 2012 © OECD/IEA 2014

European refinery margins pick up lifted by gasoline cracks

• NWE simple margins turned clearly positive in 2015, though

runs had increased already from mid-2014

• NWE cracking margins reach levels unseen since early 2012

-7.5-5.0-2.50.02.55.07.5

10.012.515.0

Jan 08 Jan 10 Jan 12 Jan 14

$/bbl Refining Margins North West Europe

Brent (Cracking) Brent (HS)

Urals (Cracking) Urals (HS)

© OECD/IEA 2012 © OECD/IEA 2014

2014-1H15 to be a low in surplus capacity

• Surplus global refining capacity hit 6-year low ~3 mb in 2014 as OECD refinery closures offset new non-OECD capacity

• Refinery margins gets significant boost from mid-year• New capacity puts system under renewed pressure from

2015 onward

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2006 2008 2010 2012 2014 2016 2018 2020

mb/d

Global surplus refinery capacity

© OECD/IEA 2012 © OECD/IEA 2014

Non-OECD accounts for 90% of refining capacity growth

• Non-OECD Asia adds 42% of total, or 2.7 mb/d of crude distillation capacity

• Middle East expands capacity by a further 1.7 mb/d, taking total capacity to 10.3 mb/d at the end of the decade

OECD10%

China24%

Other Asia18%

Middle East26%

Latin America8%

Others14%

© OECD/IEA 2012 © OECD/IEA 2014

More OECD closures in the cards

• Refinery utilisation up to 84% in April 2015• Total of 4.8 mb/d of capacity shut in OECD since 2008• Additional 450 kb/d announced in Asia Oceania through 2017• More shutdowns likely to be announced

• Total to cut 263 kbd of capacity (closure of La Mede, trims Lindsey capacity by 110 kbd)

0

200

400

600

800

1 000

1 200

1 400

2008 2010 2012 2014 2016

mb/d

Americas Europe Asia Oceania

50%

60%

70%

80%

90%

100%

2007 2009 2011 2013 2015 2017 2019

Americas Europe Asia Oceania

OECD refinery closures OECD refinery utilisation rates

© OECD/IEA 2012 © OECD/IEA 2014

Russia’s “pivot to Asia”

Rosneft supply deals with CNPC, Sinopec, Essar, PetroVietnam

-0.60 -0.40 -0.20 0.00 0.20 0.40

China

Oth Asia

Oth Eur

Mid East

L. America

OECD Am

Africa

OECD AO

OECD Eur

mb/d

FSU export growth, 2014-20

© OECD/IEA 2012 © OECD/IEA 2014

European middle-distillates imports stabilizeIncreasing volumes coming from US, India… and Middle East?

• European gasoil imports stabilizing ~ 47 mt/yr since 2013, jet imports are reaching 20 mt/yr

• Middle East OPEC is top jet fuel supplier• FSU ~ 1/2 of diesel imports, followed by U.S. (25-30%) and India (~10%)• Middle East to ship more middle distillates to Europe as new refineries

ramp up?

05

101520253035404550

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

other India OPEC US FSU

mt/year OECD Europe gasoil/diesel imports

02468

101214161820

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

other India OPEC US FSU

mt/year OECD Europe jet fuel imports

© OECD/IEA 2012 © OECD/IEA 2014

Trouble ahead?

• European demand strength expected to be short-lived– Opportunistic buying post-price drop may be losing steam– Weather wildcard– Efficiency gains– Mature, ageing market– Tepid economic growth

• Respite of non-OECD import demand also temporary– New capacity to be eventually brought on line– China shifts gears, lowers demand growth rate

• Longer-term climate policies dampen prospects for oil in fuel mix as fuel mix evolves

• Global product trade to loom larger in European supply