€¦ · · 2015-05-28chemicals, and it software ... kurkumbh (daud) talawade software park ......

TRANSCRIPT

SME Cluster Series 2015: PunePublished in India by Dun & Bradstreet Information Services India Pvt Ltd.

Registered Office ICC Chambers, Saki Vihar Road,Powai, Mumbai - 400072.CIN: U74140MH1997PTC107813Tel: +91 22 6676 5555, 2857 4190 / 92 / 94Fax: +91 22 2857 2060Email: [email protected]: www.dnb.co.in

New Delhi Office1st Floor, Administrative Building,Block ‘E’, NSIC - Technical Services Center,Okhla Industrial Estate Phase - III,New Delhi - 110020.Tel: +91 11 41497900/01Fax: +91 11 41497902

Kolkata Office166B, S. P. Mukherjee Road,Merlin Links, Unit 3E, 3rd Floor,Kolkata - 700026.Tel: +91 33 24650204Fax: +91 33 24650205

Chennai OfficeNew No: 28, Old No: 195,1st Floor, North Usman Road,T. Nagar, Chennai - 600017.Tel: 91 44 28142265/75, 42897602Fax: +91 44 28142285

Ahmedabad Office801 – 8th Floor, Shapath V,Opp. Karnavati Club, S. G. HighwayAhmedabad - 380054.Tel: +91 79 66168058/59

Bengaluru OfficeNo. 7/2 Gajanana Towers,1st Floor, Annaswamy Mudaliar Street, Opp. Ulsoor Lake,Bengaluru - 560042.Tel: +91 80 42503500Fax: +91 80 43503540

Hyderabad Office504, 5th Floor,Babukhan’s Millennium Centre,6-3-1099/1100, Somajiguda,Hyderabad - 500082.Tel: +91 40 66624102, 66514102Fax: +91 40 66619358

Director Pawan Bindal

Research and Analysis Naina Acharya, Seema Nair, Dipshikha Biswas, Sudhir Rewale

Sales Head Jayesh Bahadur

Sales Team Nittin Maheshwari, Sandeep Parakkal, Vini Batheja, Sunena Jain, Sarita Sharma, Tanya Bedi, Apoorwa Tyagi, Aloka Chatterjea, Rakesh Goyal, Rashmi Shetty, Sindhu R

Operations Team Nadeem Kazi, Ankur Singh, Sumit Sakhrani, Rajesh Gupta, Parmeshwar More

Design Team Tushar Awate, Shilpa Chandolikar, Aditya Salvi

All rights reservedThis publication is copyright and all rights are reserved. Apart from any fair dealing for the purpose of private study, research, criti-cism or review as permitted under the Copyright Act, no part may be reproduced by any process without written permission. Enquiries should be addressed to the publishers. Although every effort has been made in compiling and checking the information given in this publication to ensure that it is accurate, the authors, the publishers and their servants or agents shall not be held responsible for the continued accuracy of the information or for any errors, negligence or otherwise howsoever or for any consequence arising therefrom.

SME Cluster Series 2015: Pune

ISBN 978-93-82060-63-5

ContentsExecutive Summary ................................................................................. I

Research Methodology ...........................................................................III

Pune Cluster Overview ...................................................................... 1 - 7

Industry Overview

Auto Components ...................................................................... 11 - 16

IT-ITeS ..................................................................................... 21 - 24

Pune Cluster Insights ...................................................................... 27 - 35

I

Dun & Bradstreet India launches “SME Cluster Series 2015: Pune”, dedicated exclusively for the small and medium enterprises of the country. This report focuses on SMEs from the Pune region and offers insights in terms of their business perspective, financing requirements & preferences, challenges and outlook among others.

Some of the key findings from the study include:

• A considerable 37% of the SMEs believe that given the current economic environment, an entrepreneur in Pune can expect an ROI (return on Investment) of between 10-20% per annum over the next couple of years.

• About 45% of the respondents consider the business environment for starting and running a successful business for the micro, small and medium business in Pune to be moderate.

• Public sector banks and private banks emerged as the most preferred options to fund a new business, with 26% and 24% of the respondents indicating the same, respectively. A mere 4% of the respondents preferred venture capital as a means of sourcing funds to start a new business.

• Nearly 31% of the companies rated ‘Documentation process to obtain finance’ as ‘Difficult’ and at the same time a significant 30% of the respondents rated ‘Ease in procuring finance’ as ‘Difficult’.

• A majority (54%) of the SMEs rated ‘roadways & highways connectivity’ in Pune as ‘Easy’.

• High level of competition was cited as a major challenge by about 16% of respondents. Slow pace of implementation and lower demand were some of the other challenges cited by the SMEs in Pune.

The SME segment is expected to emerge as one of the key growth engines for the Indian economy. In its endeavor to aid the growth, Dun & Bradstreet India will continue to keep track of the developments in the SME segment. We hope that this study will be a reliable and useful source of reference to the SMEs. We look forward to your comments and suggestions.

Arun SinghSenior EconomistDun & Bradstreet India

Executive Summary

III

Objective of the ReportThe objective of “SME Cluster Series 2015: Pune” is to develop a one-point reference document, which will highlight the business perspective, financing requirements and preferences, outlook on growth prospects and various other parameters for SMEs operating in the Pune cluster. The report aims to provide insights that will facilitate enterprises to take informed decisions.

Methodology1. Desk Research A detailed review of relevant literature for the Pune cluster was conducted at this stage. 2. Questionnaire Development An in-depth desk research was conducted to develop a comprehensive questionnaire for the purpose

of primary survey with the objective to capture and analyze the trends and challenges of companies operating across various sectors in the Pune cluster.

3. Survey For the purpose of the survey, the companies were selected from internal Dun & Bradstreet database

and other authentic sources such as cluster and/or sectoral associations.

4. Eligibility criteria Companies with a total income of less than ` 1,000 mn as on FY14 were selected for the purpose

of survey. Companies involved in exclusive trading activities were excluded.

5. Collation of Information The data and information was collated from both, primary and secondary sources such as through

survey and authentic information as available in the public domain.

6. Analysis of data The information collected was scrutinized and analyzed to explore the cluster dynamics.

7. Report Writing The outcome of the project including the key analysis and results were written in the form of the

current report.

Research Methodology

PUNECLUSTER OVERVIEW

2

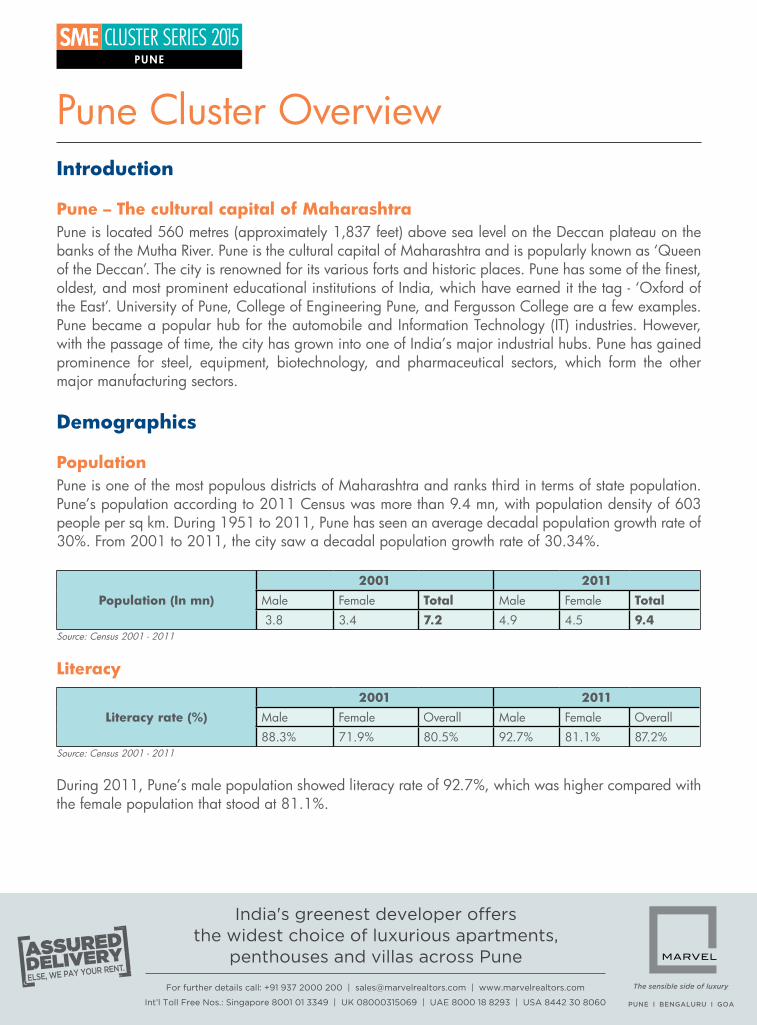

Pune Cluster OverviewIntroduction

Pune – The cultural capital of MaharashtraPune is located 560 metres (approximately 1,837 feet) above sea level on the Deccan plateau on the banks of the Mutha River. Pune is the cultural capital of Maharashtra and is popularly known as ‘Queen of the Deccan’. The city is renowned for its various forts and historic places. Pune has some of the finest, oldest, and most prominent educational institutions of India, which have earned it the tag - ‘Oxford of the East’. University of Pune, College of Engineering Pune, and Fergusson College are a few examples. Pune became a popular hub for the automobile and Information Technology (IT) industries. However, with the passage of time, the city has grown into one of India’s major industrial hubs. Pune has gained prominence for steel, equipment, biotechnology, and pharmaceutical sectors, which form the other major manufacturing sectors.

Demographics

PopulationPune is one of the most populous districts of Maharashtra and ranks third in terms of state population. Pune’s population according to 2011 Census was more than 9.4 mn, with population density of 603 people per sq km. During 1951 to 2011, Pune has seen an average decadal population growth rate of 30%. From 2001 to 2011, the city saw a decadal population growth rate of 30.34%.

Population (In mn)2001 2011

Male Female Total Male Female Total 3.8 3.4 7.2 4.9 4.5 9.4

Source: Census 2001 - 2011

Literacy

Literacy rate (%)2001 2011

Male Female Overall Male Female Overall

88.3% 71.9% 80.5% 92.7% 81.1% 87.2%Source: Census 2001 - 2011

During 2011, Pune’s male population showed literacy rate of 92.7%, which was higher compared with the female population that stood at 81.1%.

3

Pune Cluster Overview

Economic ScenarioDuring FY14, Pune district contributed 51% of the total GDDP (at current prices) of the Pune division (Pune district, Satara district, Sangli district, Solapur district, and Kolhapur district are parts of the Pune division). Gross District Domestic Product (GDDP) (at current prices) of the Pune division grew by 12.7% y-o-y to ` 3,380.52 bn in FY14 and its NDDP grew by 12.9% y-o-y. Pune’s per capita Net District Domestic Product (NDDP) grew by 11.5% y-o-y.

Gross/Net District Domestic Product And Per Capita Net District Income

GDDP (` Bn) NDDP (` Bn) Per Capita NDDP (`)

FY13 FY14 FY13 FY14 FY13 FY14Pune Division 2,999.00 3,380.52 2,699.53 3,047.41 1,147 1,279

GSDP (` Bn) NSDP (` Bn) Per Capita NSDP (`) FY13 FY14 FY13 FY14 FY13 FY14Maharashtra 13,222.22 15,101.32 11,952.09 13,651.49 1,039 1,171

Source: Directorate of Economics and Statistics ‘Economic Survey of Maharashtra 2014-15’

Industrial ScenarioPune is home to many prominent industries of India. Companies situated in Pune are into manufacturing of auto components, locomotives, agro-based products, electronic consumer durables, pharmaceuticals, chemicals, and IT software among others.

Large-scale companies present in PunePhillips India Bajaj Auto

Kirloskar Cummins Mahindra and Mahindra

Tata Electric And Locomotive Company Mercedes Benz India Ltd

Alfa Laval SKF Bearings

Weikfield India Kirloskar Pneumatics

Industrial Areas in Pune

Pimpri Chinchwad Bhigwan

Malegaon Pandare

Chakan Phase 1 Indapur

Chakan Phase 3 Kharadi Knowledge Park

Chakan Phase 4 Pune InfoTech Park (Hinjewadi Phase-I)

Jejuri & Addl. Jejuri Pune InfoTech Park (Hinjewadi Phase-II)

Ranjangaon (GC) Pune InfoTech Park (Hinjewadi Phase-III)

Kurkumbh (Daud) Talawade Software Park

Baramati (GC)Source: Maharashtra - Investment Regions, MIDC

4

Special Economic ZonesThere are numerous large IT and ITeS companies in Pune. Some of the big names include Infosys Ltd, Wipro Ltd, and Syntel International Ltd. The presence of these big IT names in Pune makes the IT and ITeS sectors one of the most prominent sectors in the district. As of December 2014, Pune had 36 approved SEZs, which formed 29% of the 124 approved SEZs in Maharashtra.

Infrastructure

Infrastructure highlights of Pune district

MSRDC built the ‘Mumbai-Pune Express Way’ (MPEW) in FY02, which reduced the physical distance between Pune and Mumbai substantially

MSRDC has completed various integrated road development programs in the Pune district (particularly in the Pune and Baramati talukas)

MSRDC has undertaken the expansion project of MPEW to improve road connectivity between Mumbai-Pune

Public passenger commuting is the major mode of transport in Pune. The Maharashtra State Road Transport Corporation (MSRTC) and Pune Mahanagar Parivahan Mahamandal Ltd (PMPML) are the major public transport service providers in Pune. As on March 31st 2014, the domestic air passenger traffic and air cargo traffic at the Pune airport was 3.5 mn and 21,135 tonnes. Further, Pune has the second highest domestic air passenger and air cargo traffic in Maharashtra.

Potential opportunities in PunePune has numerous prominent industries and educational institutions, which open up huge opportunities in the city across the wide range of industries present in the city. Prominent Industries • IT/ITeS

• Automobile industry

• Agricultural resources and agro-based industry

Products and services with high potential in Pune’s MSME Sector

• Dairy based products

• Automobile components

• Bio-coal briquettes from agro-waste

• General purpose machine shop

• Herbal and ayurvedic products

• Agro-processing export-oriented units

• Cold storage unit

• Starch from Jowar

• Solar cell

• Computer software/BPO/IT related productsSource: Brief industrial profile of Pune district, Ministry of MSME

5

Pune Cluster Overview

Major challenges hindering MSME growth in Pune 1. Loan availability 2. Improper infrastructure facilities3. Lack of proper marketing and promotional activities 4. Recovery of amounts due from customers

Policies and Schemes for MSMEsThe Government of Maharashtra continues its thrust on developing the MSME sector in the state. The Maharashtra Government recently announced that it has decided to come up with a dedicated industrial policy to provide the MSMEs with all the necessary incentives and facilities to set up their businesses in the state. The state is also working towards reducing the number of approvals required for setting up a business in Maharashtra.

As of December 2014, there were 211,403 MSME units functioning in Maharashtra with investments of ` 506.37 billion and 26.9 lakh employment. Among the various districts, at 83,033 MSMEs, Pune accounted for the single largest share of 39.3% in the total number of MSME units in the state; it also had the largest share of 34.9% in MSME employment in the state (as of December 2014).

State-specific Schemes & Policies

Package Scheme of IncentivesIn order to encourage the dispersal of industries to the industrially less developed areas, the Government of Maharashtra has been giving a package of incentives for new/expansion units located in such regions. Under the scheme, during 2014-15 (upto December), an amount of ̀ 17.62 billion was disbursed as an incentive to eligible MSMEs, large scale industries and mega projects.

Maharashtra Industrial Policy 2013The Industrial Policy 2013 focuses on the following1. Increased focus on less developed regions of the state to bring them on par with mainstream industrial

development2. Customized package of incentives for Ultra Mega and Mega Industrial Investment3. Holistic approach to MSME development4. Initiatives to encourage employment-intensive industries5. Path-breaking initiatives for investor facilitation and ease of doing business6. Optimal utilization of land for industrial development7. Strengthening of industrial infrastructure8. Assistance of unviable sick units for easy exit and to viable sick units for revival9. Incentives to bring about sustainable industrial development

6

Policy Targets• To achieve manufacturing sector growth rate of 12-13% p.a.• To achieve manufacturing sector share of 28% of state GDP• To create new jobs for 2 million persons• To attract investment of ` 5 lakh crore

Strategies to achieve the above objectives also involve greater thrust on MSME development, including developing skilled manpower; renewed focused on MSME; offering additional incentives to employment-intensive Mega units, and considering agro processing as a thrust sector.

Maharashtra Industrial Development Corporation (MIDC)As on 31st March 2014, about 90% developed plots are allotted to entrepreneurs. As of the same period, Pune had 9,754 industrial units in MIDC, with investment of ` 518.44 billion and providing employment to 4.21 lakh people.

Maharashtra Small Scale Industries Development Corporation (MSSIDC)The MSSIDC assists entrepreneurs for the development of small scale industries. During 2013-14, the turnover of MSSIDC stood at ` 1.68 billion.

Maharashtra State Khadi and Village Industries Board (MSKVIB)The main functions of the MSKVIB are to organise, develop and expand activities of Khadi and Village Industries (KVI) in the state. During 2013-14, financial assistance of ` 22.36 crore in the form of subsidy was given to KVI units.

Highlights of Schemes and Policies for MSMEs in India

Industrial Cluster Development ProgrammeAs an important strategy to enhance the productivity and competitiveness of MSMEs, the Government has announced scheme for development of potential clusters to facilitate deployment of available resources for effective implementation and more sustainable results in the medium to long term.

Micro Small Enterprises - Cluster Development Programme (MSE-CDP)The Government modified the MSE-CDP scheme for micro & small enterprises in February 2010. Under this scheme, the Government gives financial support as grant-in-aid to establish Common Facilities Centre and infrastructure development to enhance the productivity & competitiveness of the clusters.

Industrial Infrastructure Upgradation SchemeThe scheme aims at enhancing the competitiveness of industries by providing quality infrastructure through PPP in selected functional clusters.

7

Pune Cluster Overview

Recent Initiatives of the Government for MSMEsUnion Budget 2015-16:

• Allocation of ` 53 billion for micro-irrigation, watershed development and the ‘Pradhan Mantri Krishi Sinchai Yojana’

• Creation of a Trade Receivables discounting System (TReDS), an electronic platform to enable financing of trade receivables of MSMEs

• Allocation of ` 200 billion for Micro Units Development Refinance Agency (MUDRA) Bank for refinancing all Micro-finance Institutions lending to SMEs through a Pradhan Mantri Mudra Yojana, and creation of credit guarantee corpus of ` 30 billion

• Proposal to set up Self-Employment and Talent Utilisation (SETU), a techno-financial, incubation and facilitation programme to support all aspects of start-up business. An amount of ` 10 billion would be set aside as initial amount in NITI Aayog.

Other recent initiatives• A National Industrial Corridor Authority, with its headquarters in Pune, is being set up to coordinate

the development of the industrial corridors, with smart cities linked to transport connectivity, which will be the cornerstone of the strategy to drive India’s growth in manufacturing and urbanization. In the Union Budget 2014-15, an initial corpus of ` one billion was announced for this purpose.

INDUSTRY OVERVIEWAUTO COMPONENTS

IT-ITES

AUTO COMPONENTS

12

Auto ComponentsThe Indian auto components industry is one of the fastest growing industries in the country. It has grown at a CAGR of 14% during the last six years ended 2012-13. The industry has a distinct global competitive advantage in terms of cost and quality and this has aided in its transformation from a local supplier to a global auto parts supplier catering to some of the big names in the global automobile industry. The cost advantage stems from the cost-competitiveness in raw material and labour, while its established manufacturing base is a compelling attraction for global Original Equipment Manufacturers (OEMs) to outsource components from India. The industry is transforming itself from a low-volume highly fragmented industry into a competitive industry backed by competitive strengths, technology and transition up the value chain.

Post the economic global crisis in 2008, the industry experienced rapid growth. However, in 2011-12, the industry faced a slowdown which led to reduction in turnover in FY14. The auto component industry however used the slowdown as an opportunity to develop internal capabilities to meet the evolving needs of customers. The industry has been constantly exploring adjacent markets such as aerospace, defence and railways to leverage better prospects.

Indian Auto Components industryThe annual turnover of the Indian auto component industry stood at ̀ 2,117 bn during FY14, registering a decline of 2% as compared to the previous year owing to high interest rates, high capital costs, fluctuating exchange rates and decline of investment in manufacturing.

Annual turnover of auto component industry

Source: Annual Report of Automotive Component Manufacturers Association of India (ACMA) FY14

13

Industry Overview: Auto Components

Several factors have enabled this transformation of the Indian auto components industry. The government’s role has been in the form of initiatives and incentives, additional subsidies and formation of various clusters as also economic liberalisation. The gradual increase witnessed in the per capita income in India has led to leading aspirations and greater demand for automobiles, which in turn has boosted the demand for auto components. In addition, the entry of various foreign players in the Indian market led to companies adopting innovative marketing strategies to fend competition. The competitive intensity led to the improvement in the end products.

Industry StructureThe Indian auto components industry can be broadly classified into the organised sector and the unorganized sector. There is a clear demarcation with respect to products in these two sectors. The organized sector caters to high value-added precision engineering products and accounts for around three fourth of the total production. The unorganised sector caters to the lower value-added segments. The organized players cater to the original equipment (vehicle) manufacturers, while the unorganized sector largely caters to the aftermarket. There are around 600 players in the organized sector accounting for around 70% of the industry’s total revenues.

In the organised sector, some of the major auto component manufacturers include Bosch Ltd, Bharat Forge Ltd, Brakes India Ltd, Bosch Chassis Systems India Ltd, Sona Koyo Steering Systems Ltd, Automotive Axles Ltd, Sundram Fasteners Ltd, Wheels India Ltd, Jay Bharat Maruti Ltd, Motherson Sumi Systems Ltd, Subros Ltd, Pricol Ltd and Amtek Auto Ltd, among others.

Industry ClassificationThe auto components industry in India can be classified based on different parameters. These include product range and size and location.

Product RangeThe Indian auto components industry offers a comprehensive product range, consisting of approximately 20,000 components required for vehicle manufacturing. The entire product range is grouped into seven categories. Engine parts and drive transmission and steering parts are the two main product categories, contributing to 50% of the Indian auto component industry in FY14.

14

Product Range- Share of Products in FY14 (%)

Source: ACMA

Based on their class and size of their location, companies in the Indian auto component industry can be classified as Tier I, Tier II and Tier III firms.

Tier I Tier II Tier III• Comprises large firms• Almost all the companies are

capable to manufacture multiple auto components, equipped with high-end technology and large number of OEM

• Most companies have high-end research and development centres to carry out new innovation

• High IT penetration in these areas which can reduce their operaional expense as most of the machines are automatic.

• Comprises medium sized firms• Comparatively less access to latest

technology• Mostly multiple component

manufacturers and have comparatively better operational efficiency

• Medium penetration of IT which are mostly fragmented

• Comprises of smaller, single-auto component manufacturing firms, largely unorganised players

• Comparatively less access to latest technology and generally use traditional technology

• Mostly single component manufacturers and no operational efficiency

• Low level of IT penetration and hence use traditional method of manufacturing

Exports and Imports ScenarioLow labour costs, availability of skilled labour and high quality consciousness among Indian vendors have supported the growth of auto component exports from India.

15

Industry Overview: Auto Components

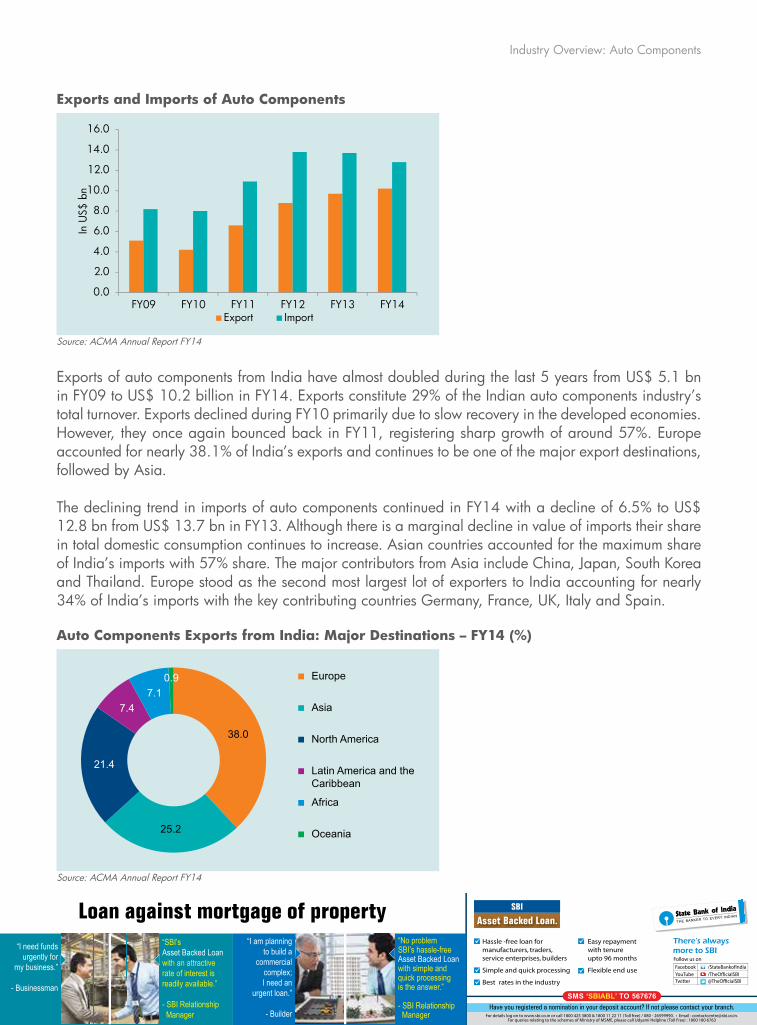

Exports and Imports of Auto Components

Source: ACMA Annual Report FY14

Exports of auto components from India have almost doubled during the last 5 years from US$ 5.1 bn in FY09 to US$ 10.2 billion in FY14. Exports constitute 29% of the Indian auto components industry’s total turnover. Exports declined during FY10 primarily due to slow recovery in the developed economies. However, they once again bounced back in FY11, registering sharp growth of around 57%. Europe accounted for nearly 38.1% of India’s exports and continues to be one of the major export destinations, followed by Asia.

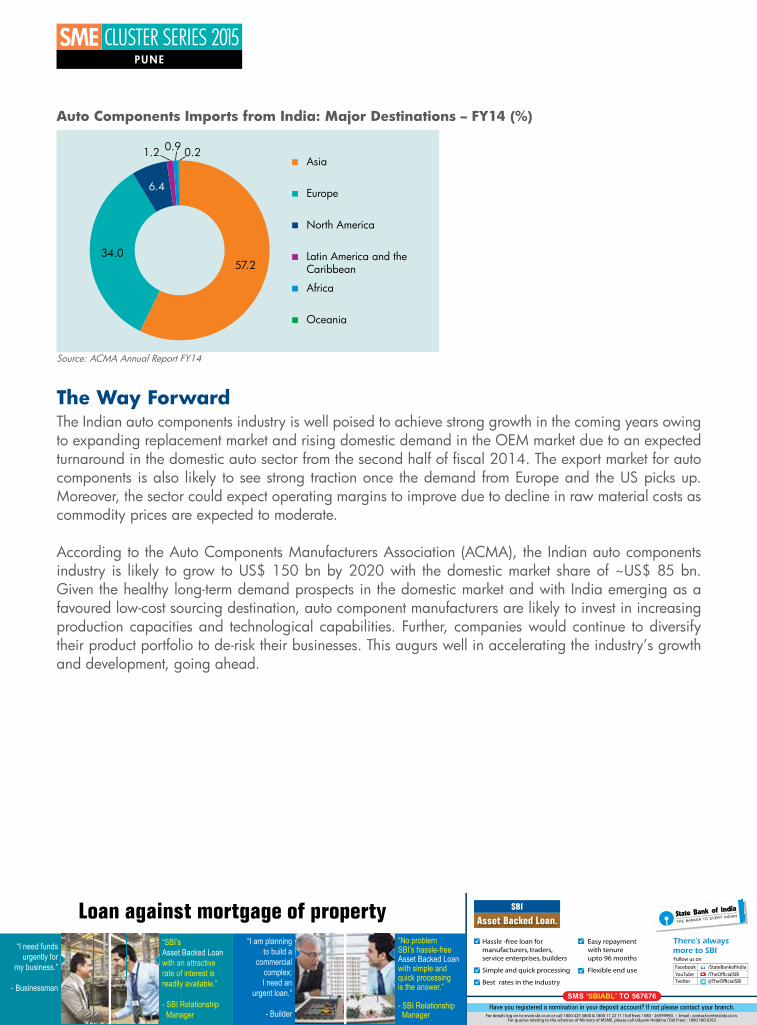

The declining trend in imports of auto components continued in FY14 with a decline of 6.5% to US$ 12.8 bn from US$ 13.7 bn in FY13. Although there is a marginal decline in value of imports their share in total domestic consumption continues to increase. Asian countries accounted for the maximum share of India’s imports with 57% share. The major contributors from Asia include China, Japan, South Korea and Thailand. Europe stood as the second most largest lot of exporters to India accounting for nearly 34% of India’s imports with the key contributing countries Germany, France, UK, Italy and Spain.

Auto Components Exports from India: Major Destinations – FY14 (%)

Source: ACMA Annual Report FY14

16

Auto Components Imports from India: Major Destinations – FY14 (%)

Source: ACMA Annual Report FY14

The Way ForwardThe Indian auto components industry is well poised to achieve strong growth in the coming years owing to expanding replacement market and rising domestic demand in the OEM market due to an expected turnaround in the domestic auto sector from the second half of fiscal 2014. The export market for auto components is also likely to see strong traction once the demand from Europe and the US picks up. Moreover, the sector could expect operating margins to improve due to decline in raw material costs as commodity prices are expected to moderate.

According to the Auto Components Manufacturers Association (ACMA), the Indian auto components industry is likely to grow to US$ 150 bn by 2020 with the domestic market share of ~US$ 85 bn. Given the healthy long-term demand prospects in the domestic market and with India emerging as a favoured low-cost sourcing destination, auto component manufacturers are likely to invest in increasing production capacities and technological capabilities. Further, companies would continue to diversify their product portfolio to de-risk their businesses. This augurs well in accelerating the industry’s growth and development, going ahead.

IT-ITES

22

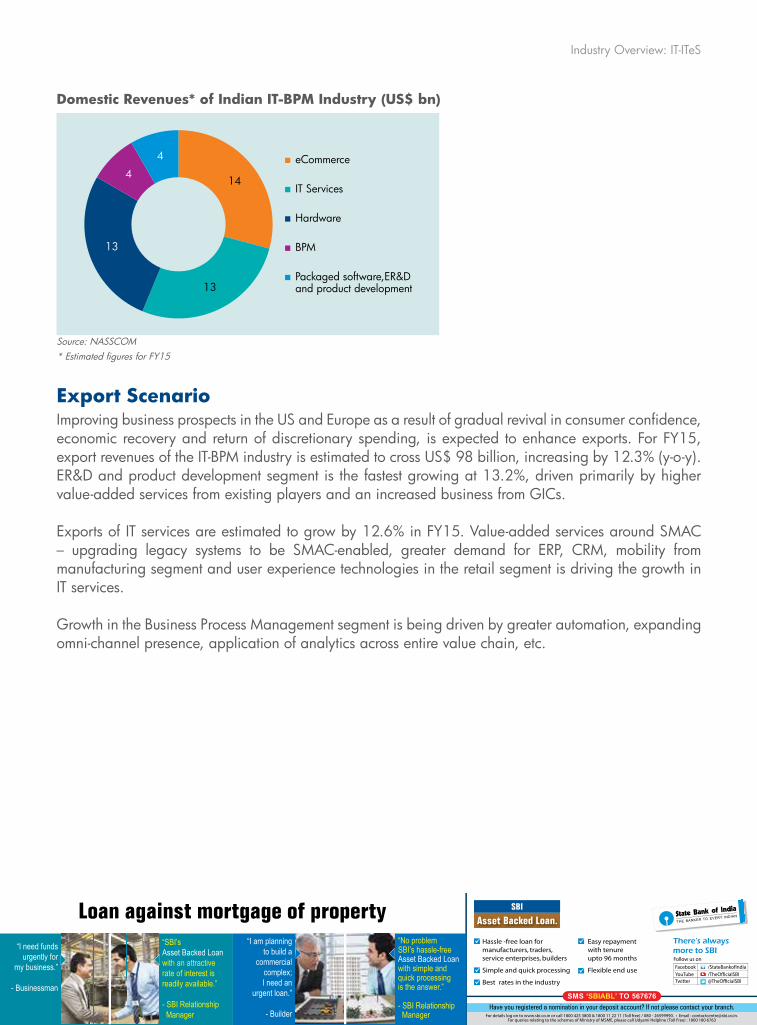

The Indian Information Technology (IT) and IT enabled services (ITeS) sectors have emerged as the growth engines of the Indian economy over the past decade. The sectors contribute substantially to India’s exports and GDP growth and generate massive urban employment. The IT-BPM industry’s relative share in India’s GDP stands at 9.5%. Large integrated players, including Indian and global IT service providers that have established their presence in India, dominate the industry. According to NASSCOM estimates, the Indian IT-BPM (Business Process Management) industry is estimated to account for US$ 146 billion during FY15, representing a growth of 13% over FY14. The industry is estimated to provide direct employment to nearly 3.5 million people and indirectly employs over 10 million people. Moreover, India’s market share in the global sourcing market increased from 52% in 2012 to 55% in 2014.

At 14%, the domestic IT-BPM market, at US$ 48 billion in FY15, is estimated to grow faster than the exports market, driven largely due to the e-commerce market. IT services and software products are the next fast growing segments, growing at 10% and 12%, respectively.

Growth DriversGrowth in the IT services segment is being driven by SMAC-cloud enablement, custom developing application for mobile, and with the renewed focus on infrastructure projects, there has been an increased demand for SI and IT consulting. There has also been an increased demand for managed and data centre services from the Small and Medium Enterprise segment.

Growth in the software products segment is being driven by the rising demand for mobile app development, security software, system software, customer analytics products, among others.

Although there is growing demand for knowledge services (mainly analytics), the BPM segment remains a CIS-dominated segment. The BPM segment is witnessing continuous demand from sectors such as BFSI, telecom, healthcare, retail, etc.

IT-ITeS

23

Industry Overview: IT-ITeS

Domestic Revenues* of Indian IT-BPM Industry (US$ bn)

Source: NASSCOM* Estimated figures for FY15

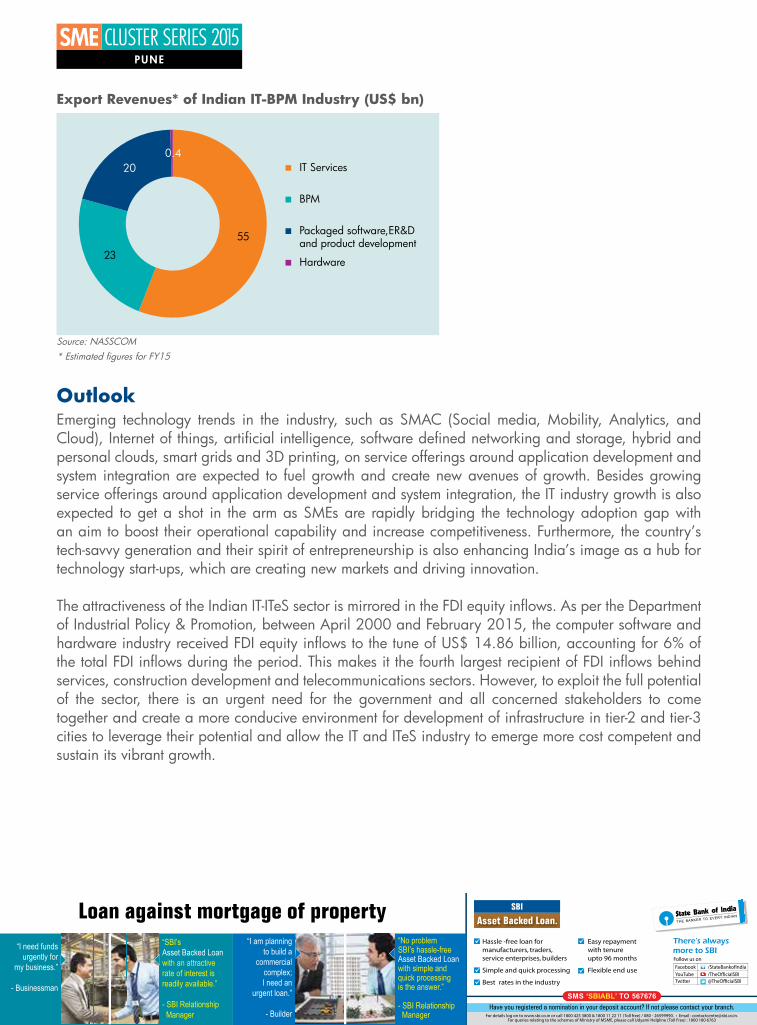

Export ScenarioImproving business prospects in the US and Europe as a result of gradual revival in consumer confidence, economic recovery and return of discretionary spending, is expected to enhance exports. For FY15, export revenues of the IT-BPM industry is estimated to cross US$ 98 billion, increasing by 12.3% (y-o-y). ER&D and product development segment is the fastest growing at 13.2%, driven primarily by higher value-added services from existing players and an increased business from GICs.

Exports of IT services are estimated to grow by 12.6% in FY15. Value-added services around SMAC – upgrading legacy systems to be SMAC-enabled, greater demand for ERP, CRM, mobility from manufacturing segment and user experience technologies in the retail segment is driving the growth in IT services.

Growth in the Business Process Management segment is being driven by greater automation, expanding omni-channel presence, application of analytics across entire value chain, etc.

24

Export Revenues* of Indian IT-BPM Industry (US$ bn)

Source: NASSCOM * Estimated figures for FY15

OutlookEmerging technology trends in the industry, such as SMAC (Social media, Mobility, Analytics, and Cloud), Internet of things, artificial intelligence, software defined networking and storage, hybrid and personal clouds, smart grids and 3D printing, on service offerings around application development and system integration are expected to fuel growth and create new avenues of growth. Besides growing service offerings around application development and system integration, the IT industry growth is also expected to get a shot in the arm as SMEs are rapidly bridging the technology adoption gap with an aim to boost their operational capability and increase competitiveness. Furthermore, the country’s tech-savvy generation and their spirit of entrepreneurship is also enhancing India’s image as a hub for technology start-ups, which are creating new markets and driving innovation.

The attractiveness of the Indian IT-ITeS sector is mirrored in the FDI equity inflows. As per the Department of Industrial Policy & Promotion, between April 2000 and February 2015, the computer software and hardware industry received FDI equity inflows to the tune of US$ 14.86 billion, accounting for 6% of the total FDI inflows during the period. This makes it the fourth largest recipient of FDI inflows behind services, construction development and telecommunications sectors. However, to exploit the full potential of the sector, there is an urgent need for the government and all concerned stakeholders to come together and create a more conducive environment for development of infrastructure in tier-2 and tier-3 cities to leverage their potential and allow the IT and ITeS industry to emerge more cost competent and sustain its vibrant growth.

PUNE CLUSTER INSIGHTS

28

IntroductionDun & Bradstreet conducted a primary study to capture and analyze the business trends of the small and medium enterprises (SMEs) operating in Pune. The survey aims to capture and highlight the SME trends in terms of revenue, financing, and policy initiatives required and major challenges faced by the small and medium enterprises (SMEs). The respondent mix comprised companies operating in the manufacturing, trading, and services industries.

Queen of Deccan, Oxford of the East, and cultural capital of Maharashtra, Pune, is a city with a future that promises to be as interesting as its history. Pune is one of India’s industrial hubs known for its automobiles and IT industries, housing one of the largest concentrations of software technology companies in India. Steel equipment, biotechnology and pharmaceuticals are other manufacturing industries located in Pune.

Following are the key findings of the study:

Majority of the respondents operate in manufacturing sector and have income below ` 50 million The Pune cluster is largely a manufacturing cluster, with around 78% of the respondents in the manufacturing sector. Only around 10% of the respondents were operating in the service sector, while around 6% of the respondents were operating in the manufacturing and service sectors.

Break-up of companies (%)

Source: Dun & Bradstreet Research

The survey revealed that around 54% of the respondents earned income below ` 50 million in FY14, while around 27% of the respondents had income between ` 50 million and ` 500 million in FY14.

Pune Cluster Insights

29

Pune Cluster Insights

Income levels of SMEs in Pune (%)

Source: Dun & Bradstreet Research

The survey revealed that companies operating in the manufacturing and trading sectors majorly fell in the below ` 50 million income bracket. The pure trading companies and 56% of the manufacturing companies surveyed earned income below ` 50 million in FY14. In contrast, only 14% of the service companies surveyed had income below ` 50 million in FY14. In fact, 43% of the services companies earned income between ` 50 million and ` 500 million in FY14, and almost 29% of the companies earned income over ` 1 billion in FY14.

Business Environment

45% of the respondents consider the business environment to be ModerateThe survey tried to understand the overall business environment in the Pune cluster. When asked to rate the overall business environment in Pune, around 45% of the respondents rated the overall business environment in Pune as ‘Moderate’, while 28% of the respondents rated the business environment as ‘Difficult’.

The companies operating in the services sector found the business environment as difficult or moderate. Around 71% of the exclusive services companies rated the business environment as ‘Moderate’, while the percentage stood at 42% for exclusive manufacturing companies. Around 29% of the companies in the services sector rated the business environment as ‘Difficult’.

30

Business Environment in Pune (%)

Source: Dun & Bradstreet Research

Financing

Banks are considered the most ideal financing option for an entrepreneur in PuneThe survey tried to understand what SMEs considered as the most ideal option for sourcing funds for the entrepreneurs who are looking to venture into businesses. Banks emerged as the most preferred option for sourcing of funds, with a significant 70% of the respondents indicating this.

Around 26% of the respondents mentioned public sector banks as the ideal financing option, while 24% of the respondents mentioned private sector banks. Amongst the manufacturing companies, public sector banks were the most preferred, with 31% of the respondents indicating this. Around 16% of the respondents in the manufacturing sector also cited ‘own savings’ as among the preferred financing options. Among the surveyed SMEs in the services sector, private sector banks emerged as the most preferred financing option; 71% of the respondents mentioned private banks as the most preferred financing option.

Preferred financing option for entrepreneurs to start a new business (%)

Source: Dun & Bradstreet Research

31

Pune Cluster Insights

‘Documentation process to obtain finance’ rated as ‘Difficult’ by 31% of the respondentsIn terms of the degree of documentation process to obtain finance in Pune, nearly 31% of the companies rated ‘Documentation process to obtain finance’ as ‘Difficult’, while another 36% rated it as ‘Moderate’. At the same time, a significant 30% of the respondents rated ‘Ease in procuring finance’ as ‘Difficult’ while 39% of the surveyed companies rated it as ‘Moderate’.

Documentation process to obtain finance (%)

Source: Dun & Bradstreet Research

Ease in procuring finance (%)

Source: Dun & Bradstreet Research

32

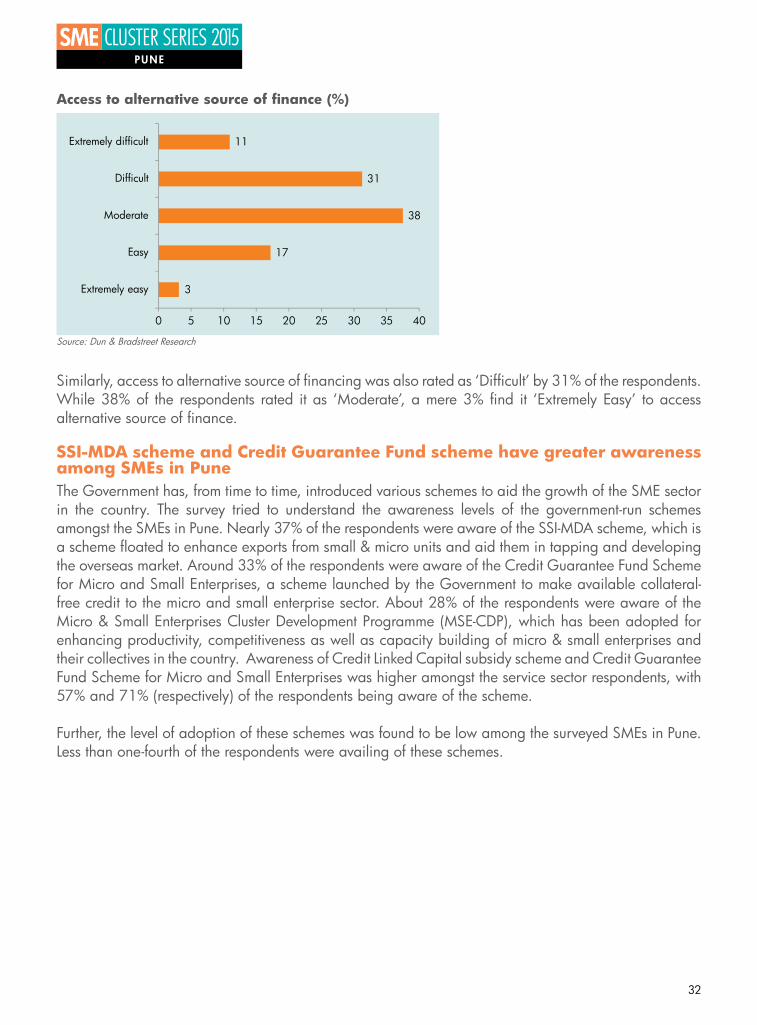

Access to alternative source of finance (%)

Source: Dun & Bradstreet Research

Similarly, access to alternative source of financing was also rated as ‘Difficult’ by 31% of the respondents. While 38% of the respondents rated it as ‘Moderate’, a mere 3% find it ‘Extremely Easy’ to access alternative source of finance.

SSI-MDA scheme and Credit Guarantee Fund scheme have greater awareness among SMEs in PuneThe Government has, from time to time, introduced various schemes to aid the growth of the SME sector in the country. The survey tried to understand the awareness levels of the government-run schemes amongst the SMEs in Pune. Nearly 37% of the respondents were aware of the SSI-MDA scheme, which is a scheme floated to enhance exports from small & micro units and aid them in tapping and developing the overseas market. Around 33% of the respondents were aware of the Credit Guarantee Fund Scheme for Micro and Small Enterprises, a scheme launched by the Government to make available collateral-free credit to the micro and small enterprise sector. About 28% of the respondents were aware of the Micro & Small Enterprises Cluster Development Programme (MSE-CDP), which has been adopted for enhancing productivity, competitiveness as well as capacity building of micro & small enterprises and their collectives in the country. Awareness of Credit Linked Capital subsidy scheme and Credit Guarantee Fund Scheme for Micro and Small Enterprises was higher amongst the service sector respondents, with 57% and 71% (respectively) of the respondents being aware of the scheme.

Further, the level of adoption of these schemes was found to be low among the surveyed SMEs in Pune. Less than one-fourth of the respondents were availing of these schemes.

33

Pune Cluster Insights

Awareness level of schemes amongst the SMEs in Pune (%)

Source: Dun & Bradstreet Research

Over 70% of respondents expect to earn an ROI upto 20% p.a. over the next two yearsReturn on investment (ROI) is a performance measure used to evaluate the efficiency of an investment. In the survey, Dun & Bradstreet attempted to understand the respondents’ expectations with respect to ROI over the next two years given the current economic climate and business environment. Around 37% of the respondents expect to earn an ROI between 10% and 20% per annum over the next two years, while around 34% of the respondents expect to earn an ROI of less than 10% per annum over the next two years. Around 9% of the respondents expect to earn an ROI of over 30% per annum over the next two years. Interestingly, around 29% of the respondents in the services sector expect to earn an ROI of over 30% per annum over the next two years.

Expectations on Return on Investment (%)

Source: Dun & Bradstreet Research

34

Challenges

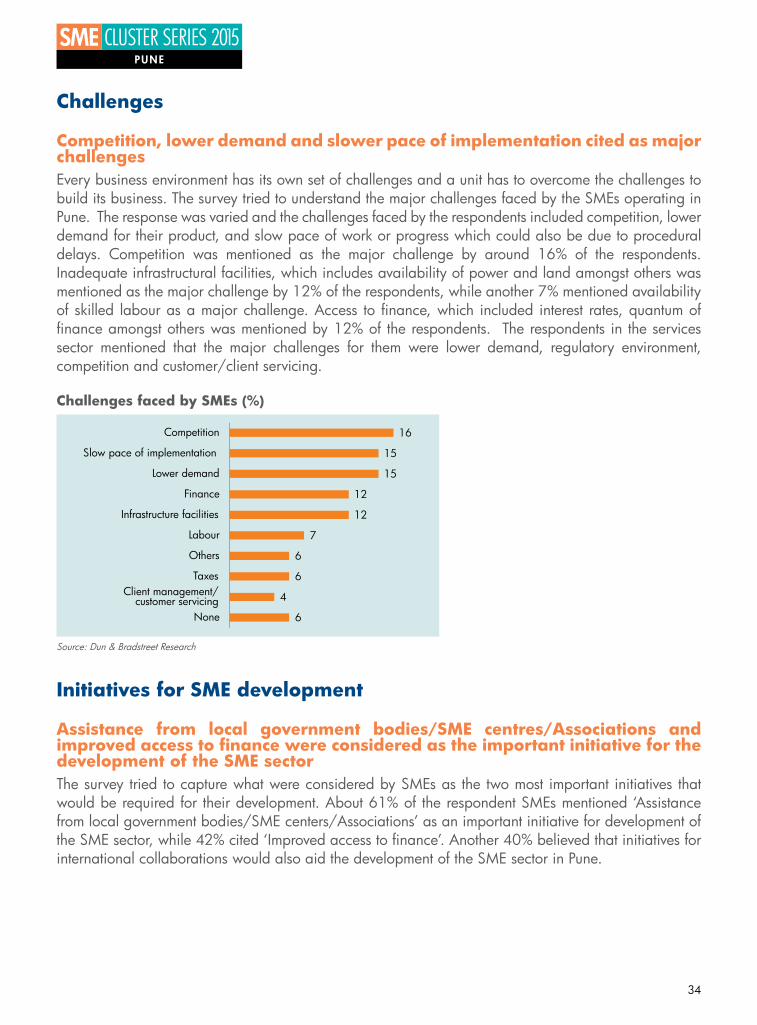

Competition, lower demand and slower pace of implementation cited as major challenges Every business environment has its own set of challenges and a unit has to overcome the challenges to build its business. The survey tried to understand the major challenges faced by the SMEs operating in Pune. The response was varied and the challenges faced by the respondents included competition, lower demand for their product, and slow pace of work or progress which could also be due to procedural delays. Competition was mentioned as the major challenge by around 16% of the respondents. Inadequate infrastructural facilities, which includes availability of power and land amongst others was mentioned as the major challenge by 12% of the respondents, while another 7% mentioned availability of skilled labour as a major challenge. Access to finance, which included interest rates, quantum of finance amongst others was mentioned by 12% of the respondents. The respondents in the services sector mentioned that the major challenges for them were lower demand, regulatory environment, competition and customer/client servicing.

Challenges faced by SMEs (%)

Source: Dun & Bradstreet Research

Initiatives for SME development

Assistance from local government bodies/SME centres/Associations and improved access to finance were considered as the important initiative for the development of the SME sector The survey tried to capture what were considered by SMEs as the two most important initiatives that would be required for their development. About 61% of the respondent SMEs mentioned ‘Assistance from local government bodies/SME centers/Associations’ as an important initiative for development of the SME sector, while 42% cited ‘Improved access to finance’. Another 40% believed that initiatives for international collaborations would also aid the development of the SME sector in Pune.

35

Pune Cluster Insights

Important Initiatives for development of SME sector (%)

Source: Dun & Bradstreet Research

Infrastructure Facilities

Access to infrastructure facilities is easier Connectivity to other clusters, states, markets through airways, roadways and waterways is one major deciding factor in the success of any cluster. Dun & Bradstreet in the survey tried to understand the respondents’ perspective in terms of Pune’s infrastructure connectivity. With regards to connectivity, in other words, access to ports and airports, around 37% of respondents mentioned that connectivity was relatively easier, while 34% mentioned it was moderate. More than half of the respondents believe that Pune has easier roadways & highway connectivity; the survey put this figure at 54%, while 28% mentioned that roadways & highways connectivity was moderate.

Infrastructure connectivity (%)

Source: Dun & Bradstreet Research