2015 01 infra_reit_website_s11

TRANSCRIPT

InfraREIT, Inc.January 29, 2015

Forward Looking Statements

These presentations contain “forward-looking statements” about the business, financial performance, contracts, leases and prospects of

InfraREIT, L.L.C. and, following the merger of InfraREIT, L.L.C. with and into InfraREIT, Inc., InfraREIT, Inc. (the “Company”). Words such

as “could,” “will,” “may,” “assume,” “forecast,” “position,” “predict,” “strategy,” “expect,” “intend,” “plan,” “estimate,” “anticipate,” “believe,”

“project,” “budget,” “potential” or “continue” and similar expressions are used to identify forward-looking statements, although not all

forward-looking statements contain such identifying words. These forward-looking statements are based on management’s current

expectations and assumptions about future events and are based on currently available information as to the outcome and timing of future

events. The Company’s actual results, performance or achievements could differ materially from those expressed or implied by such

statements. The Company’s capabilities or performance, stockholder value as well as any other statements that are not historical facts in

this presentation are forward-looking statements that involve certain risks and uncertainties, many of which are difficult to predict and

beyond the Company’s control. Factors that could cause actual results to differ materially from the results contemplated by such forward-

looking statements include, without limitation, risks that the projects the Company expects will not materialize for a variety of reasons,

including as a result of reductions in oil and gas drilling and related activity in the Permian Basin due to lower oil and gas prices relative to

our current expectations; the Company’s ability to acquire T&D assets on terms that are accretive to stockholders; the Company’s current

reliance on its tenant for all of the Company’s revenues and, as a result, the Company’s dependency on its tenant’s solvency and

financial and operating performance; defaults on or non-renewal or early termination of leases by the Company’s tenant; risks related to

future lease negotiations; changes in the regulated rates the tenants of the Company’s assets may charge their customers; the

completion of the Company’s capital expenditure projects on time and on budget; competitive conditions for the development and

acquisition of T&D assets; insufficient cash available to meet distribution requirements; the price and availability of debt and equity

financing; increased interest rates; changes in the availability and cost of capital; the Company’s level of indebtedness or debt service

obligations; changes in governmental policies or regulations with respect to the Company’s permitted capital structure, acquisitions and

dispositions of assets, recovery of investments and the Company’s authorized rate of return; weather conditions and other natural

phenomenal the effects of existing and future tax and other laws and governmental regulations; the Company’s failure to qualify or

maintain its status as a REIT; availability of qualified personnel; the termination of the Company’s management agreement or

development agreement or the loss of the services of the Company’s manager or the loss of access to the development function of the

Company’s developer; the effects of future litigation; changes in the tax laws applicable to REITs; adverse economic developments in the

electric power industry; changes in general business and economic conditions, particularly in Texas; and certain factors discussed

elsewhere in the Company’s prospectus. When considering forward-looking statements, you should keep in mind the risk factors and

other cautionary statements described under the heading “Risk Factors” included in the Company’s prospectus. Should one or more of

these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those

indicated. This presentation speaks only as of the date hereof, and the Company disclaims any obligation to update or revise any

forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

2

Introduction to InfraREIT

High-growth company focused on owning electric transmission & distribution

(T&D) infrastructure assets in the U.S., with an emphasis on the Texas market

and the Southwest

Unique opportunity to invest in a rapidly expanding, dividend-focused business

Significant growth opportunities in our current service territories that we expect

will facilitate the double-digit growth in Cash Available for Distribution,

complemented by a robust pipeline of development projects and potential

acquisition opportunities

Experienced management team

Closely aligned with Hunt, our development partner and long-term investor 3

Attractive Asset

Portfolio

Stable Cash Flow

Strong Track

Record

Constructive

Regulatory

Environment

Efficient Structure

High-Growth

Opportunities

~$1.1 bn in regulated electric T&D assets (rate base)

Transmission assets currently comprise ~75% of rate base

100% of revenue driven by regulated asset base

REIT revenue governed by multi-year leases

Increased rate base from $60 mm in 2009 to ~$1.1 bn in 2014

Successfully developed 300 miles and 4 substations of CREZ

transmission system

Closed acquisitions and completed rate case under REIT structure

Constructive T&D regulatory framework in Texas

Texas regulation supportive of REIT structure

Ability to do interim rate filings minimizes regulatory lag

REIT structure enables structurally advantaged cash generation

Hunt is highly aligned with shareholders

Footprint Projects expected to enable >10% CAD / share CAGR through

2018

Robust pipeline of ROFO projects, other T&D projects from Hunt and 3rd

party acquisitions

Target CAD / share CAGR of 10% - 15% through 2018

Investment Highlights

4

Hunt Consolidated: A Proven Energy Developer

Founded in 1934, the Hunt Oil Company and Hunt Consolidated (a diversified

holding company managed by the Ray L. Hunt family) are actively engaged in

energy and infrastructure businesses throughout the world

Hunt has a long history of entrepreneurial activity and a successful track record

in developing and constructing large complex projects, such as the Texas CREZ

project

Hunt has successfully partnered with large multinationals, international partners,

and governments, and has a presence in 14 countries around the world

5

Strategic Sponsor with Long-Term Alignment

Pro-forma for the offering, Hunt will own approximately 27.1%(1) of the

Company (common stock and operating units)

Lock-up agreements in respect of common stock and operating units

Incentive distribution feature in the management agreement

Hunt is required to offer specific development projects (ROFO Projects)

to InfraREIT

6

Hunt intends for InfraREIT to be the primary owner of Hunt’s future T&D

development projects

Through its ownership and its agreements as manager (Hunt

Manager) and developer (Hunt Developer), Hunt is highly aligned

with InfraREIT shareholders

(1) Assumes $23 IPO price. See “Principal Stockholders” in the prospectus.

Attractive Asset Profile

7

Dallas

Austin

San Antonio

Houston

El Paso

Amarillo

Texas

StantonCeleste

Brady

McAllen

Railroad DC Tie

Service Territory

Panhandle Transmission

Railroad DC Tie

PanhandleTransmission

~75% of our rate base

~ 620 miles

Transmission

Operations Center

Railroad DC Tie with

Mexico (300 MW)

Distribution ~25% of our rate base

~10,500 miles

Over 50,000 electric

delivery points

Constructive Regulatory Environment

8

2014 Rate Case Settlement: 9.7% allowed ROE and 55% debt / 45% equity

ERCOT

Texas has its own electrical grid managed by the Electric

Reliability Council of Texas (ERCOT)

Electric utilities are subject to regulation by the Public Utility

Commission of Texas (PUCT)

Transmission revenue requirement can be updated through

a rate case or an interim Transmission Cost of Service

(TCOS) filing (twice per year)

Distribution rates typically updated through a rate case

State government and regulators focused on further

enabling the growth of the Texas economy by providing

reliable and inexpensive electric service

REIT structure approved by the PUCT

Proven Results & Track Record

9

0

250

500

750

1,000

Rate Base $ millions

2009 2014-Q3

$60 mm

$1,100 mm

25%

75%

Distribution Transmission

The CREZ Project, capital expenditures and acquisitions have enabled us to

significantly grow our business, with a heavy focus on Transmission

2014 Rate Base

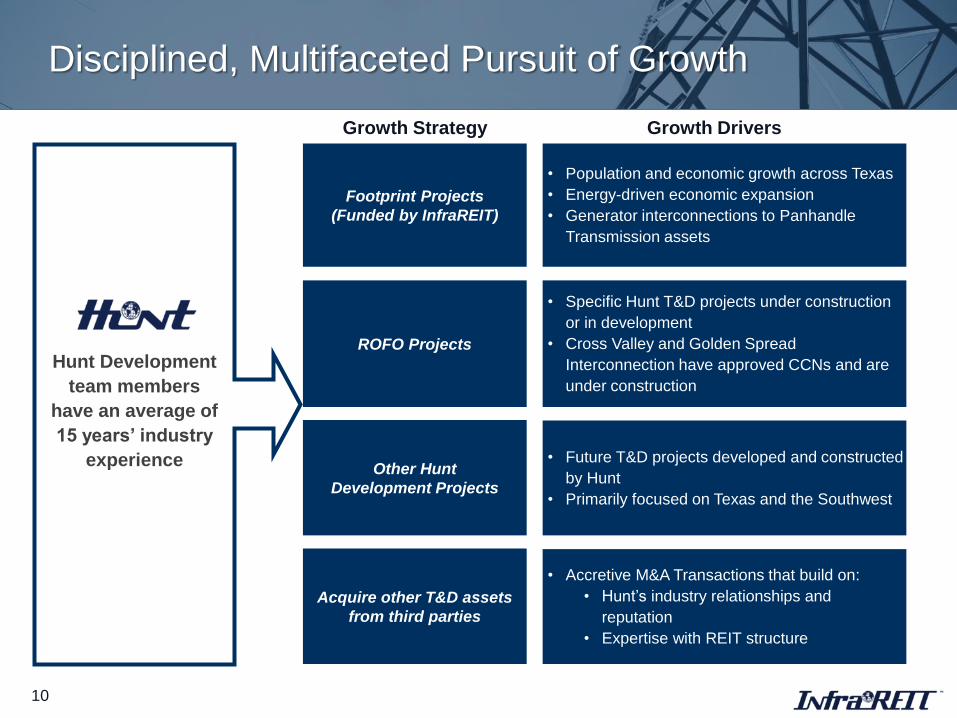

Disciplined, Multifaceted Pursuit of Growth

10

Footprint Projects

(Funded by InfraREIT)

Hunt Development

team members

have an average of

15 years’ industry

experience

ROFO Projects

Growth Strategy Growth Drivers

• Population and economic growth across Texas

• Energy-driven economic expansion

• Generator interconnections to Panhandle

Transmission assets

• Specific Hunt T&D projects under construction

or in development

• Cross Valley and Golden Spread

Interconnection have approved CCNs and are

under construction

• Accretive M&A Transactions that build on:

• Hunt’s industry relationships and

reputation

• Expertise with REIT structure

• Future T&D projects developed and constructed

by Hunt

• Primarily focused on Texas and the Southwest

Other Hunt

Development Projects

Acquire other T&D assets

from third parties

Renewable Energy Development and Interconnection in the Panhandle

and South Plains (CREZ Project)

Connects high-potential renewables zones to the North and Central Texas

load pockets

ERCOT reports 6,266 MW of new capacity in the Panhandle that has

signed generation interconnection requests

The GSEC Interconnection (ROFO Project) connects to Panhandle

Transmission Lines

Economic Expansion in West Texas

Investment required to ensure reliability and meet identified customer

requirements

Midland County population grew by 30.6% between 2000-2013 and is

projected to grow by 16.4% between 2013-2023

Regional electricity usage has grown rapidly; significant unmet needs

Economic and Population Growth in South Texas

Sharyland’s McAllen service area and Railroad DC Tie benefit from strong

population growth in the Rio Grande Valley and expanding economic

activity on both sides of the Texas and Mexico border

Track record and relationships in South Texas contributed to Cross Valley

Transmission Line (ROFO Project) opportunity

Economic Drivers of Footprint Growth

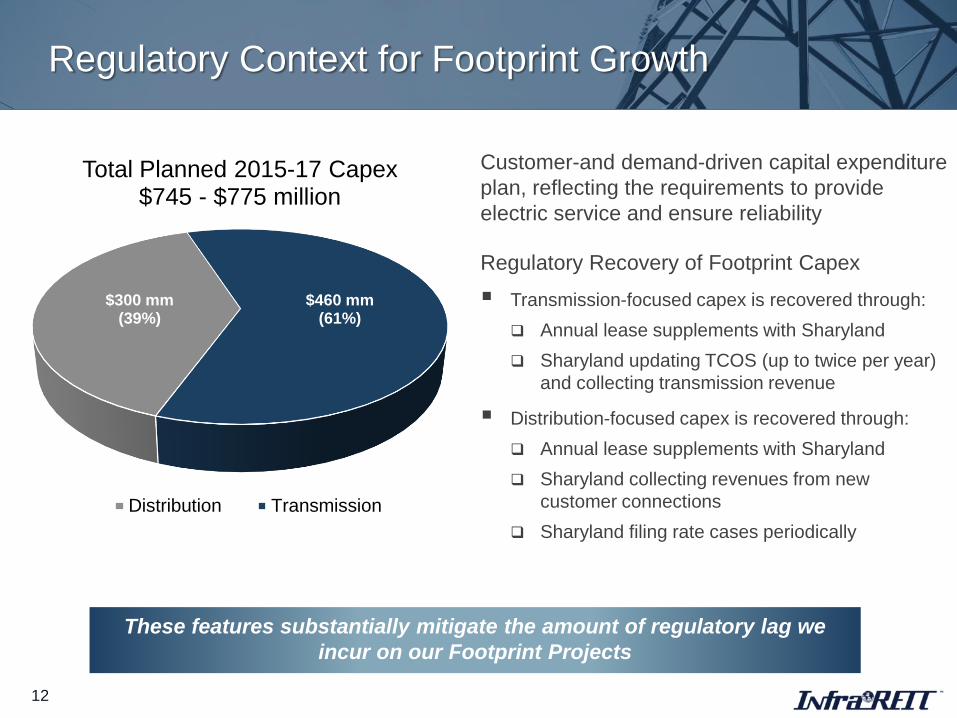

11 Source: ERCOT, US Census Bureau, Texas State Data Center

Customer-and demand-driven capital expenditure

plan, reflecting the requirements to provide

electric service and ensure reliability

Regulatory Recovery of Footprint Capex

Transmission-focused capex is recovered through:

Annual lease supplements with Sharyland

Sharyland updating TCOS (up to twice per year)

and collecting transmission revenue

Distribution-focused capex is recovered through:

Annual lease supplements with Sharyland

Sharyland collecting revenues from new

customer connections

Sharyland filing rate cases periodically

Regulatory Context for Footprint Growth

12

These features substantially mitigate the amount of regulatory lag we

incur on our Footprint Projects

$300 mm(39%)

$460 mm(61%)

Total Planned 2015-17 Capex$745 - $775 million

Distribution Transmission

Robust Pipeline of Development Projects

13

NV

CA

OK

TX

AZNM

MEXICO

Additional U.S. –

Mexico DC Ties

Additional South Texas

Transmission / Generation

Interconnections

Import capacity from

New Mexico and

Arizona to California

PJM and MISO

interconnection

ERCOT

Southeast Loop

Transmission

Line

South Plains

Reinforcement

NM

TX

AZ

NV

CA

M E X I C O

ROFO

Project

Estimated

Project CostExpected

Completion Status

Cross

Valley Line $160-$185mm 2016

Under

construction

GSEC Inter-

connection$100-$120mm 2016

Under

construction

Southline $700-$800mm --Draft EIS

Published

Verde $60-$80mm --In

development

Southline

Transmission

Project

Verde Transmission

Project

Cross Valley

Transmission Line

Golden Spread

Electric Coop

(GSEC)

Interconnection

Lubbock Power & Light

Interconnection

Under Construction Other ROFO Additional Development Opportunities

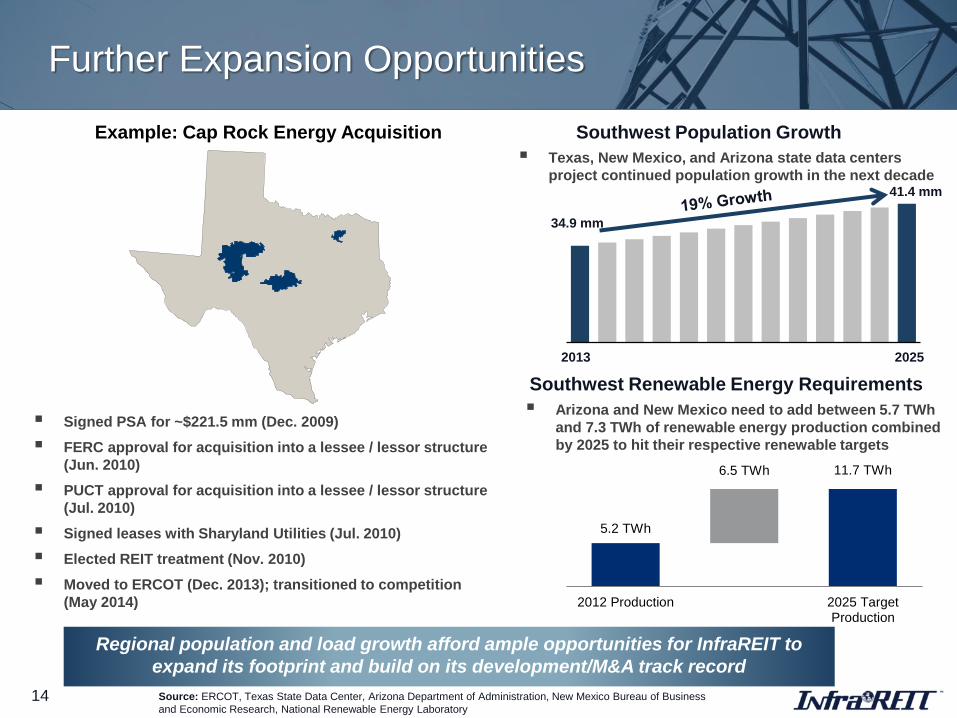

Further Expansion Opportunities

14

Southwest Renewable Energy Requirements

5.2 TWh

11.7 TWh6.5 TWh

2012 Production 2025 TargetProduction

Arizona and New Mexico need to add between 5.7 TWh

and 7.3 TWh of renewable energy production combined

by 2025 to hit their respective renewable targets

Southwest Population Growth

Regional population and load growth afford ample opportunities for InfraREIT to

expand its footprint and build on its development/M&A track record

Source: ERCOT, Texas State Data Center, Arizona Department of Administration, New Mexico Bureau of Business

and Economic Research, National Renewable Energy Laboratory

Example: Cap Rock Energy Acquisition

Signed PSA for ~$221.5 mm (Dec. 2009)

FERC approval for acquisition into a lessee / lessor structure

(Jun. 2010)

PUCT approval for acquisition into a lessee / lessor structure

(Jul. 2010)

Signed leases with Sharyland Utilities (Jul. 2010)

Elected REIT treatment (Nov. 2010)

Moved to ERCOT (Dec. 2013); transitioned to competition

(May 2014)

Texas, New Mexico, and Arizona state data centers

project continued population growth in the next decade

34.9 mm

41.4 mm

2013 2025

Board Structure

Management

Related Party

Transactions

Management

Agreement

9 total members, 6 independent

CEO, CFO and GC are officers of InfraREIT and Hunt Manager

Require majority approval by the independent board members

(i.e. ROFO Project acquisitions)

Hunt Manager responsible for day-to-day business and legal

activities of InfraREIT

Annual base fee equal to $10 million through March 31, 2015,

$13.1 million for April 1, 2015 through March 31, 2016, and

1.50% of total equity as of the previous year thereafter

Incentive fee equal to 20% of operating partnership distributions

per unit in excess of the Threshold Distribution Amount (120% of

initial distribution) payable quarterly

2015 distribution per unit: $0.225 quarterly

Threshold Distribution: $0.270 quarterly

Governance & Management

15

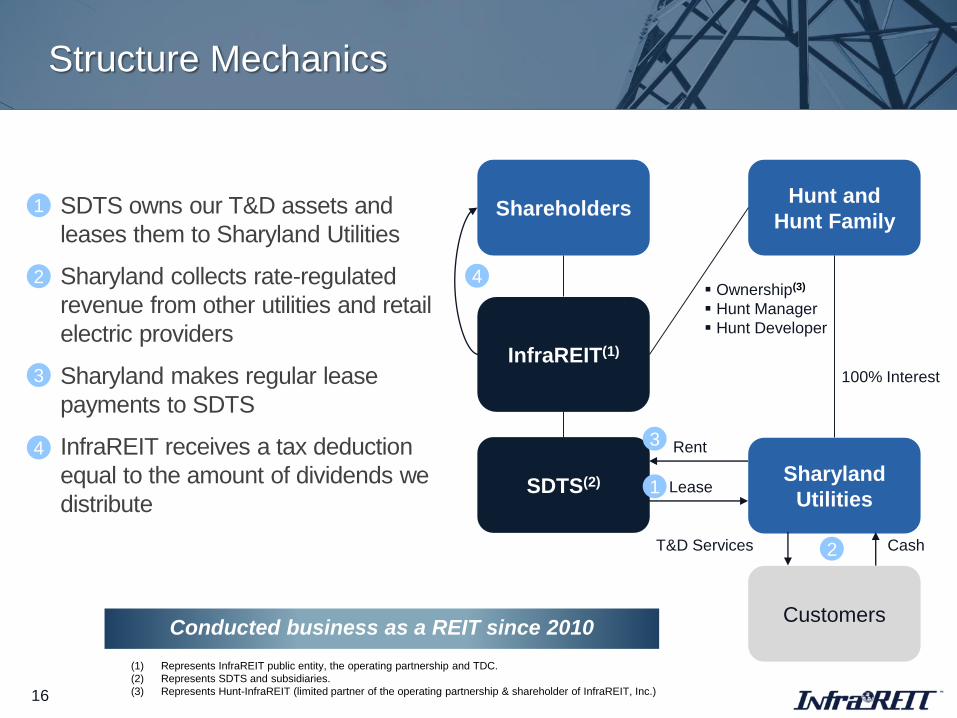

SDTS(2)

Structure Mechanics

16

SDTS owns our T&D assets and

leases them to Sharyland Utilities

Sharyland collects rate-regulated

revenue from other utilities and retail

electric providers

Sharyland makes regular lease

payments to SDTS

InfraREIT receives a tax deduction

equal to the amount of dividends we

distribute

1

2

3

4

Shareholders

InfraREIT(1)

Hunt and

Hunt Family

Sharyland

Utilities

Customers

T&D Services Cash

Lease

Rent

1

2

3

4 Ownership(3)

Hunt Manager

Hunt Developer

100% Interest

(1) Represents InfraREIT public entity, the operating partnership and TDC.

(2) Represents SDTS and subsidiaries.

(3) Represents Hunt-InfraREIT (limited partner of the operating partnership & shareholder of InfraREIT, Inc.)

Conducted business as a REIT since 2010

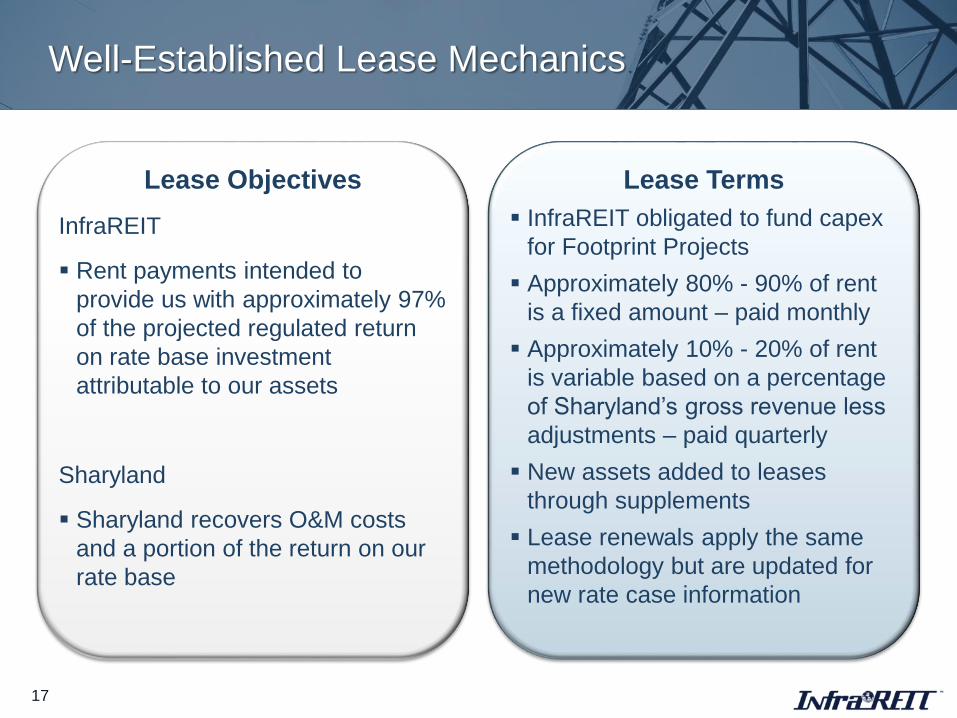

Well-Established Lease Mechanics

17

Lease Terms

InfraREIT obligated to fund capex

for Footprint Projects

Approximately 80% - 90% of rent

is a fixed amount – paid monthly

Approximately 10% - 20% of rent

is variable based on a percentage

of Sharyland’s gross revenue less

adjustments – paid quarterly

New assets added to leases

through supplements

Lease renewals apply the same

methodology but are updated for

new rate case information

Lease Objectives

InfraREIT

Rent payments intended to

provide us with approximately 97%

of the projected regulated return

on rate base investment

attributable to our assets

Sharyland

Sharyland recovers O&M costs

and a portion of the return on our

rate base

Building Our Income Statement

18

Lease Revenue

Less: Corporate SG&A

Less: Depreciation

Operating Income

Less: Interest Expense

Less: Income Tax Expense

Net Income

A

B

C

D

E

Approximately 97% of regulated return on rate base

(traditional utility model)

Primarily management fee, public company costs and

professional fees at InfraREIT

PUCT-approved depreciation rates on our assets

InfraREIT consolidated interest expense

As a REIT, corporate taxes applied to net taxable income,

less deduction for dividends paid

A

B

C

D

E

Financing Strategy

19

Focus on Regulated

T&D Opportunities

Maintain Strong Balance Sheet

Grow Dividends

Sign long-term leases

that reflect regulated

rate structure

Minimize regulatory

lag with prudent rate

case / TCOS filings

80% - 85% long-term

CAD payout ratio

Construct Footprint

Projects

Acquire ROFO Projects

Acquire Other Hunt

Development Projects

Opportunistically

acquire other T&D

assets

Target consolidated credit metrics of 60% Debt / Capitalization and 12% FFO / Debt

Maintain 55% Debt / Capitalization at regulated subsidiary

Maintain significant liquidity to support capex plan and financial flexibility

Robust CAD & Dividend Growth Targets

20

Targeting a 10% - 15% CAGR of CAD /

share from 2015-18

Expect to achieve the lower half of

the range based on Footprint Projects

Ability to exceed the midpoint of the

range through accretive acquisitions

of Cross Valley Line and GSEC

Interconnection

Ability to achieve the top of the range

through the successful development

and acquisition of Southline, other

significant third-party acquisitions, or

additional Footprint Projects

Cash Available for Distribution (CAD) per Share(1)

$ millions

$1.07

0.002015E 2018E

($/S

ha

re)

(2)

10%+

15%

CAD/Share

CAGR

(1) See appendix for more detail on calculation of estimated CAD for 2015

(2) Based upon a total of 44,014,971 shares and 60,593,728 OP units outstanding after this offering and the reorganization.

Attractive Asset

Portfolio

Stable Cash Flow

Strong Track

Record

Constructive

Regulatory

Environment

Efficient Structure

High-Growth

Opportunities

~$1.1 bn in regulated electric T&D assets (rate base)

Transmission assets currently comprise ~75% of rate base

100% of revenue driven by regulated asset base

REIT revenue governed by multi-year leases

Increased rate base from $60 mm in 2009 to ~$1.1 bn in 2014

Successfully developed 300 miles and 4 substations of CREZ

transmission system

Closed acquisitions and completed rate case under REIT structure

Constructive T&D regulatory framework in Texas

Texas regulation supportive of REIT structure

Ability to do interim rate filings minimizes regulatory lag

REIT structure enables structurally advantaged cash generation

Hunt is highly aligned with shareholders

Footprint Projects expected to enable >10% CAD / share CAGR through

2018

Robust pipeline of ROFO projects, other T&D projects from Hunt and 3rd

party acquisitions

Target CAD / share CAGR of 10% - 15% through 2018

Investment Highlights

21

Appendix

22

Estimated Cash Available for Distribution

23

Estimated Cash Available for Distribution for the twelve months ending December 31, 2015 (1)

$ millions2015

Net Income Before Noncontrolling Interest 5.7

Add: Depreciation 40.0

Funds from Operations Before Noncontrolling Interest (2) 45.7

Add: Amortization of Deferred Financing Cost 3.1

Add: Non-cash consideration paid in Class A OP units 9.1

Add: Non-cash equity compensation 0.6

Less: Allowance for Funds Used During Construction – Equity (1.3)

Add (Less): Effect of Straight-line Rents 7.9

Less: Capital Expenditures to Maintain Net Assets (40.0)

Add: Reorganization expenses 39.6

Cash Available for Distribution 64.7

Less: Growth Capital Expenditures – Footprint (208.3)

Add: Financing Required to Fund Growth Capital Expenditures and Principal Amortization 208.3

Estimated Cash Available for Distribution After Investing and Financing Activities (CAD) 64.7

Average Shares Outstanding (mm of shares) 60.6

CAD / Share 1.07

CAD Payout Ratio 84.3%

Dividend / Share 0.90

(1) Estimates are for Footprint Projects only (no ROFO Projects are included). Estimated Cash Available for Distribution is based on numerous

assumptions and subject to the risks described in the prospectus. See “Distribution Policy” and “Risk Factors” in the prospectus.

(2) For a discussion of Funds from Operations Before Noncontrolling Interest, see slide 26

Debt Obligations & Available Liquidity

24

Long-Term Debt (rate / maturity)

($ millions)

Outstanding

As of Sept. 30, 2014

TDC Senior Secured Notes

(8.50% / December 30, 2020)$ 20.3

SBC Senior Secured Notes

(6.47% / September 30, 2030)106.6

McAllen Senior Secured Notes

(7.25% / December 30, 2029)46.7

CREZ Term Loan Facility

(2.41%(1) / June 20, 2018)400.9

CREZ Senior Secured Fixed Rate Note

(5.04% / June 20, 2018)60.0

Total $ 634.5

Post-IPO Facilities

Liquidity Facilities

($ millions)

Total

Amount

Outstanding

Post-OfferingAvailable

InfraREIT Partners Revolver $ 75 $ 0 $ 75

SDTS Revolver 250 0 250

Total $ 325 $ 0 $ 325

(1) CREZ term loan accrues interest at LIBOR plus 2.25% for a period of three years, at which point the interest rate

will increase to LIBOR plus 2.50%.

Lease Summary

25

Leases

Lease

Expiration

Date

Total Electric

Plant

($ mm) (1)

Summary of Assets

CREZ Lease 12/31/2020 $644Substantially all of our Panhandle

transmission assets

S/B/C Lease 12/31/2015 290

Our T&D assets located in and around

Stanton, Brady and Celeste, Texas, other

than our 138 kV transmission loop

Other Leases (2) 12/31/2019 –

12/31/2022184

Our assets located in South Texas, including

our Railroad DC Tie, our transmission

operation centers in Amarillo, Texas; our 138

kV transmission line that loops around our

Stanton, Texas territory; and a small portion

of our Panhandle transmission assets

(1) Consists of electric plant, net for the applicable lease as of September 30, 2014.

(2) Includes McAllen Lease, Stanton Transmission Loop Lease and ERCOT Transmission Lease

Non-GAAP Legend

In this prospectus, we refer to “Funds from Operations,” which is a financial measure that is derived on the basis of

methodologies other than in accordance with U.S. GAAP. In this prospectus, when we use the phrase “before noncontrolling

interest” to modify net income or Funds from Operations, we are referring to the applicable amount of net income or Funds

from Operations, in each case before any reduction to such item as a result of the noncontrolling interest in our Operating

Partnership. The National Association of Real Estate Investment Trusts, or NAREIT, defines Funds from Operations as net

income (computed in accordance with GAAP), excluding gains and losses from sales of property (net) and impairments of

depreciated real estate, plus real estate depreciation and amortization (excluding amortization of deferred financing costs) and

after adjustments for unconsolidated partnerships and joint ventures. Applying the NAREIT definition to our financial

statements results in Funds from Operations representing net income before net income attributable to noncontrolling interest,

depreciation, impairment of assets and gain (loss) on sale of assets. Funds from Operations does not represent cash

generated from operations as defined by GAAP and it is not indicative of cash available to fund all cash needs, including

distributions.

Our management uses Funds from Operations before noncontrolling interest as an important supplemental measure of our

operating performance. We use this metric before noncontrolling interest as we feel it is important to evaluate our entire

consolidated business. This performance measure provides perspectives not immediately apparent from net income. We

consider Funds from Operations to be an important supplemental disclosure of operating performance for an equity REIT due

to their widespread acceptance and use among REITs. In addition, we believe that Funds from Operations is frequently used

by securities analysts, investors and other interested parties in the evaluation of REITs. We offer this measure to assist the

users of our financial statements in assessing our operating performance under GAAP, but this measure is non-GAAP

measures and should not be considered a measure of liquidity, alternatives to net income or indicators of any other

performance measure determined in accordance with GAAP, nor is it indicative of funds available to fund our cash needs,

including capital expenditures, make payments on our indebtedness or make distributions. However, our method of calculating

Funds from Operations may be different from methods used by other companies and, accordingly, may not be comparable to

similar measures as calculated by other companies that do not use the same definition or implementation guidelines or

interpret the standards differently from us. Investors should not rely on Funds from Operations as a substitute for any GAAP

measure, including net income, cash flows provided by operating activities or revenues.

26