2014 results investor presentation - nedbank results investor presentation ... aug 13 feb 14 aug 14...

TRANSCRIPT

NEDBANK GROUP LIMITED

2014 RESULTSINVESTOR PRESENTATION

for year ended 31 December 2014

2

3,22,6

1,8 1,5

0

2

4

6

Aug 13 Feb 14 Aug 14 Feb 15

Nedbank 2014 GDP growth forecast

Growth currently slow in SA, but longer term opportunities in both SA & rest of Africa

Rest of Africa growing off a low base(IMF GDP growth forecasts, %)

SA GDP expectations revised downward

Global & local economy remains volatile, uncertain, complex & ambiguous

Source: Nedbank Group Economic Unit, IMF

2,21,5

2,1 2,5

5,2 4,8 4,9 5,2

0

2

4

6

13 14 15 16SA Sub Saharan Africa

Lower oil & commodity prices to play out

Volatility has increased

0

200

400

600

800

00 02 04 06 08 10 12 14

All Commodities IndexNonfood Agriculturals Price Index ($)Oil per barrel ($ indexed)

0

50

100

150

200

Jan 12 Jul 12 Jan 13 Jul 13 Jan 14 Jul 14 Jan 15

SA Banks indexJSE All Share indexNigerian Banks index

3

Wholesale credit growth ahead of retail, but lower inflation to benefit consumersWholesale credit growth ahead of retail (%)

Source: Nedbank Group Economic Unit

Consumers remain under pressure

Low inflation & interest rates lower for longer

-10

0

10

20

30

40

00 02 04 06 08 10 12 14

Households

Companies

SA Capex investment muted

0

250

500

750

93 95 97 99 01 03 05 07 09 11 13

Public sector

Private sector

CPI & Prime (%)

-10

-5

0

5

10

15

20

00 02 04 06 08 10 12 14

Consumer spending: Q-o-q changePersonal Disposable Income: Q-o-q change

-1

2

5

8

11

14

17

07 08 09 10 11 12 13 14 15 16 17

CPI (%)

Prime (%) Forecast

+25bps Nov ‘15

4

FOCUS ON SHAREHOLDER VALUE CREATION

5

9 83

1

10 7

53

11 7

21

13 1

43

14 3

95

2010 2011 2012 2013 2014

Continued focus on drivers of shareholder value creation

480 60

5 752 89

5

1 02

8

2010 2011 2012 2013 2014

13,4

15,3

16,417,2 17,2

14,2

13,0 13,1 13,0 13,5

2010 2011 2012 2013 2014

ROE (excl GW) Cost of equity

NAV per share(cents)

ROE & Cost of Equity (%)

Full-year dividend per share(cents)

NAV ROE > COE

9,5%

EP

Dividends

14,9%

Underpinned by solid CET1, surplus liquidity & high coverage

6

No fee increases, selected reductions & personal loans slowdown

Impacted NIR growth by ~3,5% in 2014

Well positioned to continue growing our transactional franchise

2014 a milestone year

Leadership & Board changes

Seamless Group Exco transition enabled by good succession planning & depth of leadership

Board appointments & scheduled retirements

Pan African Banking Network

Invested R6,3bn in the rest of Africa:

c20% shareholding in ETI (Ecobank)

Initial 36,4% shareholding in Banco Unico

Integrated Corporate & Investment Bank

Improve client service

Unlock future revenue growth opportunities

Optimisation Initiatives

Strategic Choices

Various cost optimisation initiatives across the Nedbank & Old Mutual Group

7

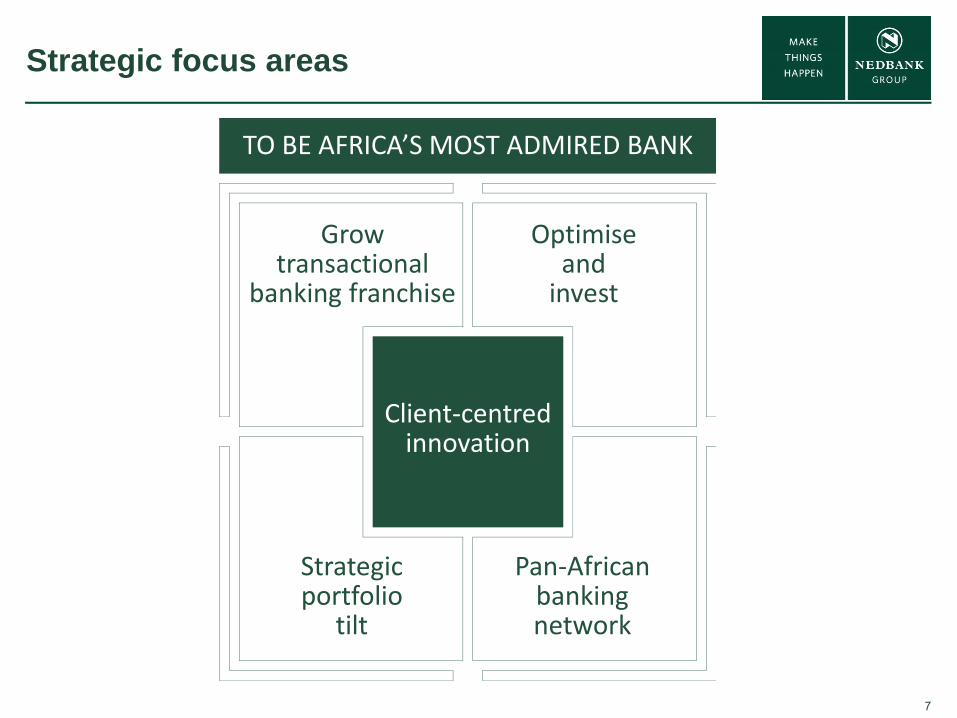

Strategic focus areas

TO BE AFRICA’S MOST ADMIRED BANK

Client‐centred innovation

Grow transactional

banking franchise

Optimiseandinvest

Strategic portfolio

tilt

Pan‐African banking network

8

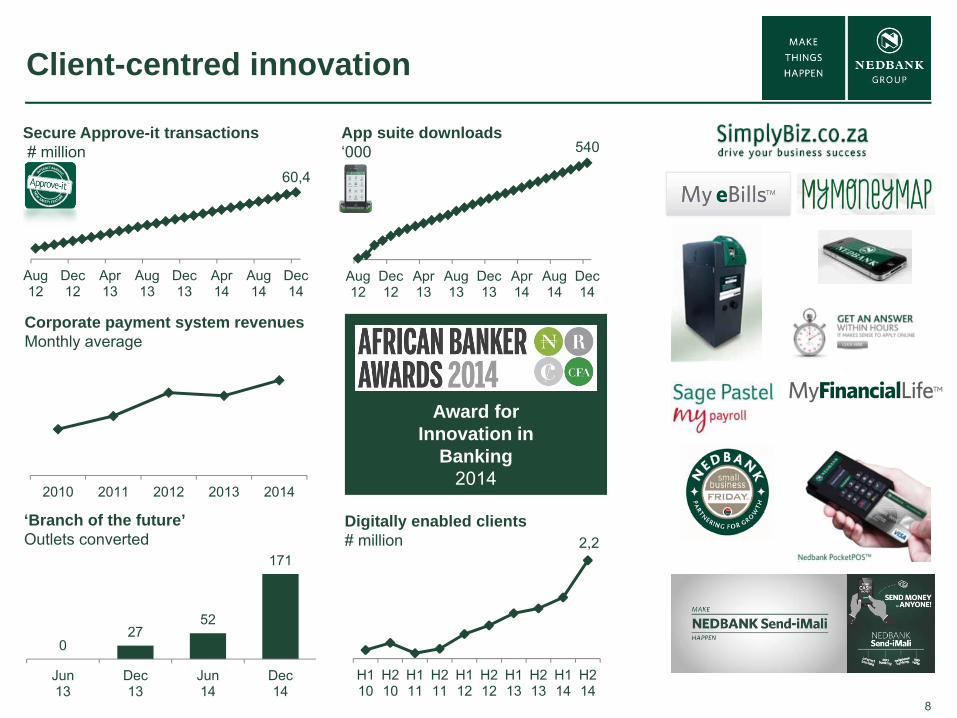

Client-centred innovation

Aug12

Dec12

Apr13

Aug13

Dec13

Apr14

Aug14

Dec14

App suite downloads‘000

Secure Approve-it transactions# million

Digitally enabled clients# million

Award for Innovation in

Banking2014

Corporate payment system revenuesMonthly average

‘Branch of the future’Outlets converted

H110

H210

H111

H211

H112

H212

H113

H213

H114

H214

Aug12

Dec12

Apr13

Aug13

Dec13

Apr14

Aug14

Dec14

2010 2011 2012 2013 2014

2,2

540

60,4

027

52

171

Jun13

Dec13

Jun14

Dec14

9

11,0% 11,0%

16,6%

12,4% 11,8%

4,9%

2009 2010 2011 2012 2013 2014

PL volume decrease & credit life pricing0% fee increases & selected fee reductionsNIR

Grow transactional banking franchise Following double digit NIR growth since 2009, strategic choices impacted 2014, but stronger growth in H2

NIR growth (%)

(0,6)

10,2

2,94,8

(3,5)

9,4

1,3

5,3

1,3

H1 2014 H2 2014NIR Commission & feesInsurance TradingOther NIR

160,3

8,4%

10

647 717 831

2 636 2 971 3 227

3 577 3 837

3 905

1 102 1 126

857

2012 2013 2014

5 566 6 152 6 675

328 271

213

2012 2013 2014

Grow transactional banking franchise Client & NIR growth in retail influenced by risk appetite & pricing choices

1 Single product clients2 Adjusted for MFC client migration3 Total growth excluding personal loans. 2014 Includes the impact of selected fee reductions (R40m) & no price increases (R195m)

#000 Rm

Card

Trans-actional

Secured

PersonalLoans

8 651 8 8206 888

6 423

+7,2%+9,0% 7 962

PersonalLoans1

Total Retail Client Base NIR

Retail exclPersonalLoans1

+10,5%+8,5%

Total

Total

+2,0%+8,7%

+9,2%3

+9,7%3

5 894

2

11

Grow transactional banking franchise Client-centred strategy driving growth in all segments

Total client base,# 000

Kid

s &

You

thE

ntry

Lev

el 1

Mid

dle

1, 2

Pro

fess

iona

l2S

mal

l Bus

ines

s

1 000944

3 6293 307

2013 2014

1 7361 662

79 87

215 224

20142013

1 ELB and Middle segment growth is negatively impacted by reduction in Personal Loans 2 Bases readjusted due to Professional’s migration to Consumer segments in Feb’14 of ~6kNote: Non-residential, Non-individual segment not shown

+6%

+10%

+4%

+10%

+4%

12

Optimise & Invest

Retail & Business Banking back office optimisation External cost optimisation review of

Shared Services SAP ERP implementation

- Live on 1 Jan 2015 (Procurement & Finance)

- HR module planned for Sept 2015 implementation

IT systems rationalisation- Decommissioned 18 core systems in

2014 - 74 since 2010 as we move from 250

to 60 Old Mutual SA Group (OMSA,

Nedbank & M&F) synergies on track for pre-tax run rate of R1bn in 2017

Optimise

Continued investment in the franchise Electronic & physical channels

- R1,7bn investment in ‘branch of the future’ to 2017

Regulatory requirements Rest of Africa expansion

- FlexCube rollout in Namibia Q1 2015- Investment in people & footprint

Invest

641906

2009 2014

Outlets (excl PL)

2009 2014

1816

3711+41%+104%

ATMs

13

Strategic portfolio tilt Average interest earning asset mix change

34,9 33,7 32,5 30,4

44,9 46,3 45,6 47,7

16,6 16,4 16,2 16,6

3,6 3,6 5,7 5,3

2011 2012 2013 2014

Retail WholesaleBusiness Banking Other

5,41%5,68% 5,81% 5,91%

1,82% 1,88% 1,89% 1,90%

3,29% 3,20% 3,24% 3,24%

3.48% 3.53% 3,57% 3,52%

2011 2012 2013 2014

Retail WholesaleBusiness Banking Group

Contribution to AIEA (%) Net interest margin (%)

100% 100% 100%100%

Note: Wholesale includes Nedbank Corporate & Nedbank Capital | Other represents the balance of AIEA

141 Client premium relative to prime with home loans excluding staff & re-advances

Strategic portfolio tilt Retail asset pay-outs & pricing

YoY %Rbn %

2,42 2,49 2,36 2,41 2,30 2,43

0,48 0,51 0,65 0,84 0,70 0,57

H1 H2 H1 H2 H1 H2

MFC(vehicles)

Home Loans

Personal Loans

Other

2012 2013

0,5 0,8 0,7 0,7 0,6 1,1 4,7 4,9 5,3 6,1 5,6

7,5

12,1 14,0 14,7

15,9 15,0 16,6

8,0 7,5 5,1

4,1 3,6

3,9 25,4 27,1

25,8 26,8 24,7

29,1

H1 H2 H1 H2 H1 H220142012 2013 2014

11,2 13,0 14,9 17,5 17,6 16,9

Asset payouts Book growth New business pricing1

12,1

1,0

(16,3)

15

Strategic portfolio tilt Judiciously growing new homeloans

2010 FY2014 FY

Average advances (Rbn)1

Defaulted Loans (%)1 Credit Loss Ratio (%)1

Vintages Vintages

1 Retail Home loan book excluding Retail Relationship Banking & Business Banking2 Based on Nedbank MMFTP, Liquidity & Balance Sheet Management charges, excluding endowment on ECAP3 Margin required for 06-08 profile to be EP neutral in 2010, assuming no drop-off due to higher price4 LTV based on original loan amount & valuation at point of registration

>10090-100

LTV Distribution (%)4 Dec ‘14Lending margin (%)2

~300bps higher margin required3

80-900-80

4422 26

1312

38

3739

347

272

Pre-06 06-08 09-14

14

62

168

36 38

Pre-06 06-08 09-14

1.51.2 1.2

1.51.0

1.9

Pre-06 06-08 09-14

7,2

14,7

3,45,1

7,5

2,6

Pre-06 06-08 09-14

2,22,5

1,0

0,1 0,1 0,2

Pre-06 06-08 09-14

Headline Earnings (Rm)1

Vintages

(111)

(748)

(45)

44 86 355

Pre-06 06-08 09-14

16

Strategic portfolio tilt CLR reflective of mix change & quality portfolio

136113 105 106

79

11889

59 5546

Group CLR (bps)

Group CLR excl. PLs (bps)

Impairment charge (Rm)

2010 2011 2012 2013 2014

Personal loans Homeloans Wholesale Other

6 188

4 506

Group credit loss ratio (bps)

17

26 7

65

23 2

10

19 2

73

17 8

48

15 8

46

2010 2011 2012 2013 2014

9,1%

5,6%

4,8%3,1%

1,6%1,3%

5,5%

3,0%2,5%

Retail Wholesale Nedbank Group

Strategic portfolio tilt Defaulted advances declining & coverage increasingDefaulted advances (Rm)Defaulted advances as % of book (%)

33,9% 37,7% 38,6% 42,3% 43,1%

5 523 5 7016 692

5 867 5 808

763 641866 888 941

2010 2011 2012 2013 2014

Total & specific coverage (%)

Write-offs (Rm)

Post write-off recoveries (Rm)

70,0%64,2%56,4%49,5%41,9%

Note: 2013 Total & specific coverage restated

(11,2%)

18

0%

5%

10%

15%

20%

Home Loans Personal Loans VAFMFC Card Retail TotalHL Back HL Front Prime

H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H22006 2007 2008 2009 2010 2011 2012 2013 2014

Strategic portfolio tilt Defaults reducing across all retail asset classes

2005

Defaults by asset class% of total advances

19

Pan-African banking network

A client-centred, risk-mitigated, capital-efficient, longer-term strategy

SADC & East Africa (A) Grow presence from 6 to 10 countries in the

medium-term Standardised operating model & IT system Banco Unico (Mozambique): acquired 36,4%

stake for R252m (with pathway to control) Coverage bankers in East & West Africa West & Central Africa (B) Acquired 20% equity stake in ETI for $493m

in October 2014 Ecobank strengthening its franchise

‒ Presence in 36 countries ‒ #1 in 6, top 3 in 14 countries‒ New Board, Chairman & CEO

70 Nedbank wholesale banking clients now bank with Ecobank

‘One bank’ experience for clients across 39 countries & >2 000 staffed outlets

20

Pan-Africa banking networkInvestment & financial performance

Invested to become c20% ETI & 36,6% Banco Unico shareholder

ETI investment (31 Dec 2014): Cost: R5,9bn Book value: R6,2bn Market value: R5,5bn

Entry price of less than 1,0x NAV Long-term strategic shareholding &

alliance

8

133

-10

10

30

50

70

90

110

130

150

2013 2014

Headline earnings (Rm)

Strategic Associate investmentsSADC & East Africa banking subsidiaries

165

224

0

50

100

150

200

250

300

2013 2014

Headline earnings (Rm)

21

0%

1%

2%

3%

4%

0%

100%

200%

2010 2011 2012 2013 2014South Africa Outside South AfricaLending Margin (RHS) CLR (RHS)

Pan-Africa banking networkExporting sector expertise

Deal activity in 24 countries across AfricaIB average loans & advancesNIM & CLR (%)

IET1 average loans & advances (Rbn)GOI (Rm)

Resource Finance average loans & advances (Rbn)GOI (Rm)

-

300

600

0%

100%

200%

2010 2011 2012 2013 2014South Africa Outside South AfricaRevenue (RHS)

-

400

800

0%

100%

200%

2010 2011 2012 2013 2014South Africa Outside South AfricaRevenue (RHS)

Note 1: IET – Infrastructure, Energy & Telecommunications

22

FINANCIAL PERFORMANCE & OUTLOOK

23

Key performance indicators

2014 2013

ROE (excl goodwill) 17,2% 17,2%

Diluted HEPS growth 13,0% 15,0%

Credit loss ratio 0,79% 1,06%

NIR : expense ratio 82,8% 86,4%

Efficiency ratio1 56,5% 55,1%

Common equity tier 1 CAR 11,6% 12,5%

Dividend per share (cents) 1 028 895

Note 1: Efficiency ratio includes associate income

24

8 670 8 670

11 470

9 8809 880

1 741

1 059

951 2 115

134 560

2013 NII Impairments NIR Expenses AssociateIncome

Direct tax &other

2014

Headline earnings growth drivers

Headline earnings (Rm)

14,0%

8,2% (19,0%) 4,9% 9,4% >100%

Excluding ETI +13,4%

25

69,782,6

2013 2014

Total Qualifying Statutory Liquid Assets & Cash Reserves

12,5

11,6

2,4 1,2

1,2

0,9

Dec2013

Generationof

reserves

Dividends Increasein RWA

Impact ofinvestments

Dec2014

Capital Only 2015

Balance sheet metrics remain sound

Common equity tier 1 ratio (%)

Liquidity & funding

R2,5bn Basel III compliant tier 2 capital subordinated debt issued R1,7bn old-style tier 2 capital subordinated

debt redeemed in 2014

Basel III target range: 10,5% -12,5%

Additional Tier 1 & Tier 2 capital

Qualifying statutory liquid assets (Rbn)

Min. 60% LCR exceeded from 1 January 2015

Ave. Q4 LT funding ratio: 25,4% (ahead of industry average)

R4,5bn senior unsecured debt issued

NSFR remains work in progress

26

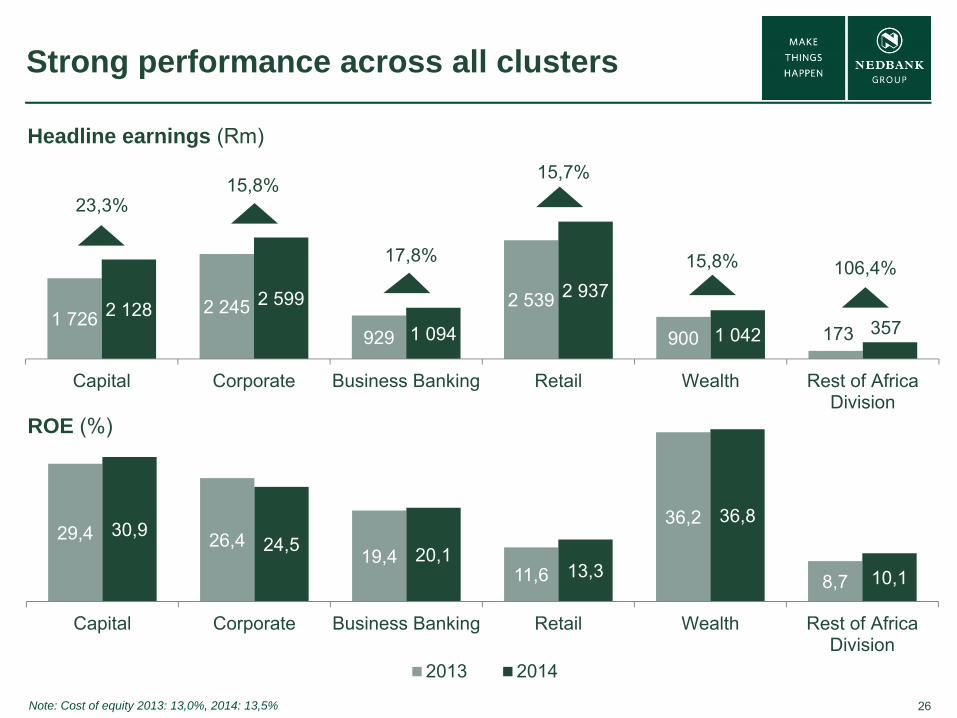

1 726 2 245929

2 539

900 1732 128 2 599

1 094

2 937

1 042 357

Capital Corporate Business Banking Retail Wealth Rest of AfricaDivision

29,4 26,419,4

11,6

36,2

8,7

30,924,5 20,1

13,3

36,8

10,1

Capital Corporate Business Banking Retail Wealth Rest of AfricaDivision

2013 2014

23,3%15,8%

17,8% 15,8%

Strong performance across all clusters

Headline earnings (Rm)

ROE (%)

106,4%

15,7%

Note: Cost of equity 2013: 13,0%, 2014: 13,5%

27

Nedbank Corporate & Investment Bank – powerful, scalable client facing wholesale business

Rationale for combined CIBCombines the respective strengths of Nedbank Capital & Corporate to build a market leading

franchise with a stronger client-centred focus

Combined headline earnings (Rm) ROE (%)

1 202 1 228 1 431 1 726 2 128

1 357 1 5711 817

2 2452 599

21,7%23,6% 23,7%

27,6% 27,0%

0%

5%

10%

15%

20%

25%

30%

0

1 000

2 000

3 000

4 000

5 000

6 000

2010 2011 2012 2013 2014

Capital Corporate ROE

2 559 2 7993 248

3 9714 727

Market leader in commercial property finance

Strong corporate bank & highly rated on levels of client service

Sector & product expertise in investment banking

Good growth opportunities in rest of Africa, infrastructure etc

Utilise power of combined CIB balance sheet to originate & lead larger deals

Leverage our strategic partners: Ecobank, Banco Único, Bank of China, CIBC

Positioning

28

Nedbank Retail & Business Banking – underlying business showing an improved performance & contributing to growth

Headline Earnings

PersonalLoans1

Card

Rm

413 432 624

MFC21 193 1 152 1 134

HomeLoans2 153 308 485

RRB

778 859 863

12,2 11,2 17,9

18,0 15,9 15,7

3,6 7,8 12,4

28,8 30,9 28,2

ROE%

Business Banking

161 222 323 7,9 11,4 15,1

944 929 1 094

2012 2013 2014

21,5 19,4 20,1

2012 2013 20141 Profitability relates to the advances book & excludes some transactional, deposit & insurance income derived from strong Personal Loans positioning in the market2 Excludes lending products in RRB

29

Nedbank Wealth – strong growth & momentum off a high base

Wealth Management – strong performance & growth

Record YoY HE growth Momentum in financial

planning Top quartile performance Single, integrated HNW

proposition >12,000 HNW clients

Asset Management – scale & momentum

Insurance – rebasing of traditional volumes

Top 3 Raging Bull company Unique Best of BreedTM

model Excellent fund performance

over time Investment in mobile, digital

& brand

Rebasing of traditional insurance product volumes

Strong growth in funeral & niche offerings

Innovation in mobile & digital Investment in single client-

centric system

Assets Under Management (Rbn)

2010 2011 2012 2013 2014InternationalLocal

212190

151

112103

0

100

200

300

400

500

600

0

500

1000

1500

2000

2500

3000

2010 2011 2012 2013 2014

+12%

Life EV & VNB (Rm)

Embedded valueValue of new business

(27%)

-2 000 000

3 000 000

8 000 000

13 000 000

18 000 000

23 000 000

2

5 000 002

10 000 002

15 000 002

20 000 002

25 000 002

30 000 002

2010 2011 2012 2013 2014LiabilitiesAdvances

Liabilities & Advances (Rbn)

+28%

+13%

30

2015 guidance

Advances to grow at mid-single digits

Margin below the 2014 levelNII

At the lower end of our target range of 80 – 120bps

Above mid-single digit growth (excluding fair-value adjustments)

Above mid-single digit growth

CLR

NIR

Expenses

Volatile economic environment

Forecast risk increased

Building our franchise for the long-term

Growth in DHEPS greater than growth in nominal GDPDHEPSgrowth

31

Medium-to-long-term targets

Metric 2014Medium-to-long-term

target 2015 outlook1

ROE (excl goodwill) 17,2% 5% above COE Below target

Diluted HEPS growth 13,0% ≥ CPI + GDP growth + 5% > CPI + GDP growth

Credit loss ratio 79bps 80 – 120 bps At the lower end of our target range

NIR : expenses 82,8% > 85% Below target

Efficiency ratio2 56,5% 50% - 53% Above target

CET 1 CARTier 1 CARTotal CAR

B III11,6%12,5%14,6%

Basel III basis:10,5% - 12,5%11,5% - 13,0%14,0% - 15,0%

Within target range

Dividend cover 2,07 1,75 to 2,25 times

1 2015 outlook based on current economic forecasts2 Efficiency ratio includes associate income & going forward this target will be reviewed in line with this change

32

Contact us

Nedbank Groupwww.nedbankgroup.co.zaNedbank Group LimitedTel: +27 (0) 11 294 4444Physical address 135 Rivonia RoadSandown 2196 South Africa

Download the Nedbank Investor Centre App from the Nedbank App Suite:

Nedbank Investor RelationsHead of Investor Relations Alfred Visagie Direct tel: +27 (0) 11 295 6249 Cell: +27 (0) 82 855 4692 Email: [email protected]

Investor Relations Consultant Penny Him Lok Direct tel: +27 (0)11 295 6549 Email: [email protected]

DisclaimerNedbank Group has acted in good faith and has made every reasonable effort to ensure the accuracy and completeness of the information contained in this document,including all information that may be defined as 'forward-looking statements' within the meaning of United States securities legislation.Forward-looking statements may be identified by words such as ‘believe’, 'anticipate', 'expect', 'plan', 'estimate', 'intend', 'project', 'target', 'predict' and 'hope'.Forward-looking statements are not statements of fact, but statements by the management of Nedbank Group based on its current estimates, projections, expectations,beliefs and assumptions regarding the group's future performance.No assurance can be given that forward-looking statements will prove to be correct and undue reliance should not be placed on such statements.The risks and uncertainties inherent in the forward-looking statements contained in this document include, but are not limited to: changes to IFRS and the interpretations,applications and practices subject thereto as they apply to past, present and future periods; domestic and international business and market conditions such as exchangerate and interest rate movements; changes in the domestic and international regulatory and legislative environments; changes to domestic and international operational,social, economic and political risks; and the effects of both current and future litigation.Nedbank Group does not undertake to update any forward-looking statements contained in this document and does not assume responsibility for any loss or damagewhatsoever and howsoever arising as a result of the reliance by any party thereon, including, but n limited to, loss of earnings, profits, or consequential loss or damage.†