2014 economic summit presentation

DESCRIPTION

ÂTRANSCRIPT

Florida Realtors® 2014 Real Estate and Economic Summit

Doing Business in Florida’s Growing Markets

Sponsored by

Metro Market Trends, Inc.

MMT Info, Inc.

Who We Are

Metro Market Trends

(MMT Info) is a real

estate information and

technology company.

Acquire, Amend and

Append real estate data

for the entire state of

Florida and parts of

Alabama

Database of all properties

within our coverage area

Software Developers

Who Uses Our Data

Real Estate Brokerages

Realtors®

MLS Organizations

Appraisers

Banks/Lending

Institutions

Associations

Builders/Developers

County

Financial Services

Retail

Services

Title Companies

Insurance Industry

Why People Use Our Data

Locate Comparable Sales

Generate Custom Area Market Statistics

Develop a Target Marketing List

Track Pre-Foreclosures

Software Product History

REARS PIRS

Text

SearchNet

Text

Product

Progression

SalesNet TaxNet

SearchNet

MMTINFO.COM

800-239-1668

CLARK LA BLOND

THANK YOU FOR THIS

OPPORTUNITY

Florida Realtors® 2014 Real Estate and Economic Summit

Doing Business in Florida’s Growing Markets

Sponsored by

Florida Realtors® 2014 Real Estate and Economic Summit

Doing Business in Florida’s Growing Markets

Sponsored by

Housing and Mortgage Market

Update

Florida Realtors 2014 Economic Summit

Orlando, FL

December 10, 2013

Frank E. Nothaft

Chief Economist

18

The Emerging Purchase Market

Home sales up in U.S., driven by high affordability Up about 10%-12% in 2013, project 5%-6% gain in 2014 Most (not all) markets have high buyer affordability If 30-year FRMs rise to 5% by year-end 2014, most markets remain ‘affordable’

Lending shift to purchase-money dominated market Increase in home sales and prices drive growth in purchase-money FRM rate rise, ‘burnout’, substantially reduce refinance originations

Who’s buying homes? Return of the trade-up and first-time home-buyer Household formations and demographics will drive demand

First timers less likely to be young couples First timers more likely to be African-American or Latino

18

Office of the Chief Economist

18

Office of the Chief Economist

19

Low Interest Rates & Lower Home Prices Have

Increased Homebuyer Affordability

Office of the Chief Economist

19

Sources: National Association of Realtors Composite Housing Affordability Index – (% of median priced

home affordable on median income with conventional mortgage and 20% down), seasonally adjusted;

Freddie Mac Primary Mortgage Market Survey® and November 2013 Outlook.

3

5

7

9

11

13

15

17

19

50

75

100

125

150

175

200

1971

19

73

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

2007

20

09

20

11

20

13

Index Percent

NAR Affordability

Index (left scale)

30-Year Fixed

Mortgage Rate (right scale)

Index = 100 means

median income buys

median priced home

Forecast

Office of the Chief Economist

20

Unemployment Rate Has Declined to 6.7% in Florida

(7.3% in U.S.)

3

4

5

6

7

8

9

10

11

12

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

Florida

United States

Unemployment Rate (Percent)

Forecast

Sources: U.S. Department of Labor, Federal Reserve (Central Tendency projection midpoint of

Federal Reserve Governors and Reserve Bank presidents as of September 2013 for fourth

quarter of 2013, 2014, 2015 and 2016; other quarters obtained through linear interpolation).

Nov-Dec 1982

10.8% Oct 2009

10.1%

FOMC

Midpoint

– Recession Year

Office of the

Chief

Economist

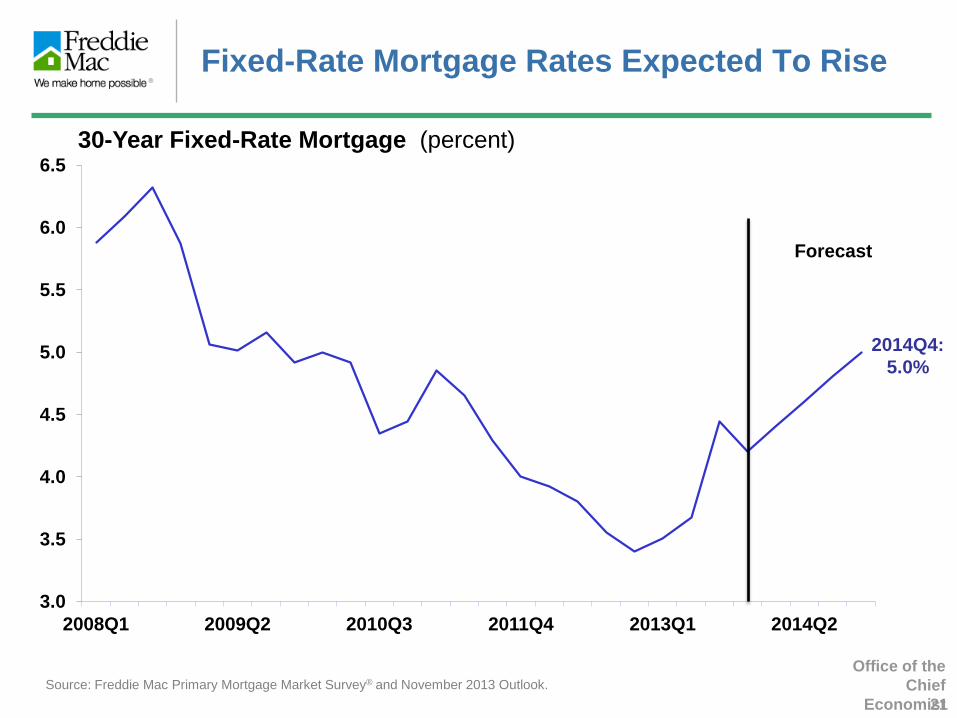

Fixed-Rate Mortgage Rates Expected To Rise

21

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

2008Q1 2009Q2 2010Q3 2011Q4 2013Q1 2014Q2

30-Year Fixed-Rate Mortgage (percent)

2014Q4:

5.0%

Source: Freddie Mac Primary Mortgage Market Survey® and November 2013 Outlook.

Forecast

Most Metro Areas Remain Affordable If Interest

Rates Rise to 5 percent

Office of the Chief Economist 22

Source: Moody’s Analytics (2013Q2 median family income), National Association of Realtors (2013Q2 median price),

Freddie Mac, American Housing Survey. Calculations assume a family earning the median income purchases the

median price home with a 10% down payment and a 30-year fixed-rate mortgage of 5%. Affordability is calculated by

requiring that principal, interest, taxes, and insurance not exceed 28% of gross monthly income. We estimate annual

taxes and homeowner’s Insurance based on the American Housing Survey to be 1.68% of the purchase price and

private mortgage insurance to be 0.5% per annum.

Affordable Not Affordable

At 5% Rate:

Office of the Chief Economist

23

10

20

30

40

50

60

70

80

2,500

3,500

4,500

5,500

6,500

7,500

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

U.S. Existing Home Sales (Thousands) Florida Existing Home Sales (Thousands)

Peak-to-2013Q3

Florida down 18%

U.S. down 26%

Source: National Association of Realtors® (US), Florida Realtors® (NSA SF Houses )

Florida Sales Up About 17%; U.S. Sales Up 13%

(2013 Q3 vs. 2012 Q3)

United States

Florida

Forecast

Inventories of Homes-For-Sale Are Near Lows

24

3

4

5

6

7

8

9

10

11

12

13

3

4

5

6

7

8

9

10

11

12

13

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Months Supply of Homes for Sale

Sources: National Association of Realtors, Bureau of Census, National Bureau of Economic Research

New Homes

Existing Homes

– Recession

Office of the Chief Economist

Days on Market Have Fallen for All Price Classes

0 20 40 60 80 100 120 140 160 180 200

Less than $50K

$50-100K

$100-150K

$150-200K

$200-250K

$250-300K

$300-400K

$400-600K

$600-1000K

$1000K+

Oct-13 Oct-12

Office of the Chief Economist Source: Florida Association of Realtors®.

Florida: Median Days on Market by Sale Price, October 2013 Florida: 46 Days

(vs. 63 days in October 2012)

25

Days

26

Vacant Housing Oversupply is Least in 10 Years

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Excess for-Rent Inventory

Excess for-Sale Inventory

Source: Freddie Mac calculations using U.S. Census Bureau data. Negative values reflect undersupply. The under/oversupply of vacant housing was estimated based on the average vacancy rate from 1994Q1 to 2003Q4.

Excess Vacant Homes (Numbers in Millions)

2003 2004 2005 2006 2007 2008 2009 2010 2000 2001 2002 2011 2012

0.2

2013

Office of the Chief Economist

Office of the Chief Economist

27

Florida House Prices Up 24% From Trough,

(still 36% Below 2006 Peak)

80

90

100

110

120

130

140

150

160

170

180

190

200

210

220

230

Jan 2000 Jan 2001 Jan 2002 Jan 2003 Jan 2004 Jan 2005 Jan 2006 Jan 2007 Jan 2008 Jan 2009 Jan 2010 Jan 2011 Jan 2012 Jan 2013

Source: Freddie Mac House Price Index

Florida

Freddie Mac House Price Index (December 2000=100)

36%

Down

24%

Up

Hardest Hit Areas Lead Price Recovery

Office of the Chief Economist

28

Source: Freddie Mac House Price Index

Code

Metro

Trough-to-

Current

Green

Miami

Orlando

Tampa

29%

28%

24%

Yellow

Jacksonville

Pensacola

Tallahassee

17%

14%

11%

Red Sebring 8%

≥ 20%

< 10% 10 to 20 %

House-Price Growth

(Jan 2012 to Sept 2013)

Office of the Chief Economist

29

$434 $525 $575 $661 $768

$772

$1,225 $925

$459 $192

$294

$380

$350

$280

$240

$0

$500

$1,000

$1,500

$2,000

$2,500

2011 2012 2013 2014 2015

FHA & VA Conventional Refi Conventional Purchase

$1,500

$2,130

$1,850

$1,400

$1,200

(13)% (44)%

Refinances Are Still High,

Purchase-Money Increasing

Single-Family Mortgage Originations ($ Billions)

Sources: Freddie Mac’s August Economic Outlook, HUD, VA

Note: Forecast does not indicate Freddie Mac’s business prospects or expected

results and may change without notice

Lowest

Level

Since

2000

Office of the Chief Economist Sources: National Association of Realtors®

January – June 2013

About 80% of U.S. Buyers Are Owner-Occupants

Buyer Type

• 36% of owner-occupant

buyers were first-time buyers

• 87% of owner-occupant

buyers use a mortgage

• First-timers almost always

use mortgage financing

• Investors generally buy “all

cash”

30

Office of the Chief Economist

Desire to Own a Home Remains

Top Reason to Buy

Source: National Association of Realtors®, “Profile of Home Buyers and Sellers:

Reasons to Buy”, February 18, 2013

Primary Reason for Purchasing a Home

First-time Homebuyers Repeat Buyers

1. Desire to own a home of my own (60%) 1. Desire for a larger home (16%)

2. Affordability of homes (11%) 2. Job-related relocation or move (13%)

3. Change in family situation (9%) 3. Desire to own a home of my own (11%)

31

Office of the Chief Economist

First Timers are Younger, More Likely to be

Minority, and Have Smaller Down Payments

CharacteristicRepeat

Buyers

First-Time

Buyers

Age <= 35 years 23% 68%

Black or Hispanic 14% 23%

Median Household Income $93,000 $62,000

FHA or VA or RHS/RD1

28% 48%

Median Current LTV 82% 92%

Married % 59% 48%

Source: 2011 American Housing Survey (Owner-occupied, moved 2010 or 2011).

Median Household Income from NAR-Profile of Home Buyers and Sellers 2012.

Percent of Buyers using mortgage finance. 1

32

Where to Get More Information Look for regular updates to our economic forecast, commentary and data at

www.FreddieMac.com/news/finance

Contact us at [email protected]

Opinions, estimates, forecasts and other views contained in this document are those of Freddie Mac's Office of

the Chief Economist, do not necessarily represent the views of Freddie Mac or its management, should not be

construed as indicating Freddie Mac's business prospects or expected results, and are subject to change without

notice. Although the Office of the Chief Economist attempts to provide reliable, useful information, it does not

guarantee that the information is accurate, current or suitable for any particular purpose.

Information from this document may be used with proper attribution. Alteration of this document is prohibited.

© 2013 by Freddie Mac.

Florida Realtors® 2014 Real Estate and Economic Summit

Doing Business in Florida’s Growing Markets

Sponsored by

An Economic Forecast in Uncertain Times

Orlando, FL December 10th, 2013

U.S. Forecast

A Cloud of Uncertainty Hangs Over the Economy

Health Care Reform Impact on labor market

Dodd-Frank Financial Regulatory

Reform Impact on credit flows

Fiscal Cliff

Sequester, shutdown/debt Ceiling…

Monetary Policy

U.S. Forecast

A recent paper has created an index that quantifies economic

policy uncertainty and analyzes its economic impact:

Measuring Economic Policy Uncertainty

By Scott R. Baker Nicholas Bloom, and Steven J. Davis

U.S. Forecast

The index has three components:

1. Newspaper coverage of policy-related economic uncertainty.

2. Number of federal tax code provisions

set to expire in future years

3. Disagreement among economic forecasters

(Survey of Professional Forecasters)

U.S. Forecast

The economic impact of economic policy uncertainty

Statistical analysis in the paper show that

higher policy uncertainty causes:

1. Lower private investment

2. Lower industrial production 3. Much lower employment

Economic Policy Uncertainty Index

U.S. Forecast

161514131211100908070605040302010099

145.0

140.0

135.0

130.0

125.0

Total Nonfarm Payroll Employment(Millions)

Total Nonfarm Employment

U.S. Forecast

U.S. Forecast

161514131211100908070605040302010099

10.0

9.0

8.0

7.0

6.0

5.0

4.0

3.0

Civilian Unemployment Rate(%)

Unemployment Rate

U.S. Forecast

Lost housing wealth

Weak labor market recovery

Have weighed on consumers

“Mini age of austerity”

U.S. Household Wealth

(Trillions of $)

2005 2006 2007 2008 2009

Q1* 2013 Q2

Total Assets 71.3 78.6 79.5 66.6 62.8 88.4

Financial

Assets 42.9 49.0 51.4 42.2 39.6 61.9

Home Equity 13.2 12.8 10.3 7.0 6.1 9.3

Net Worth 59.1 65.1 65.1 52.4 48.7 74.8

U.S. Economic Outlook

2013

Q1

2013

Q2

2013

Q3

2013

Q4 2013 2014

GDP

% Change, Annual Rate 1.1 2.5 3.0 1.6 1.8 2.3

Consumer Price Index

% Change, Annual Rate 0.2 0.0 2.6 1.2 1.5 1.8

Consumer Sentiment 76.4 79.8 80.1 74.6 80.1 83.1

Consumption

% Change, Annual Rate 2.3 1.8 1.5 2.0 1.9 2.5

Florida Housing Market

Housing market recovery continues to unfold Prices have gained traction Can the momentum be maintained?

The role of the investor

Housing finance still problematic

Florida Forecast

1615141312111009080706050403020100

300.0

250.0

200.0

150.0

100.0

50.0

0.0

9%

8%

7%

6%

5%

4%

3%

Florida Housing Starts(thousands)

Total Private Housing Starts30 year Mortgage Rates

Florida Housing Market

Investors are back in Florida residential real estate

Evidenced by high share of cash transactions Private equity & hedge funds

Is this a good thing or a bad thing?

Florida Housing Market

Housing Finance Unsustainably high share of cash transactions Mortgage availability has been restricted by

Dodd Frank Capital Standards Underwriting Standards Limited Private Securitization Demise of Mortgage Brokering Shell shock

Florida Forecast

In 2010 the economic recovery began

• Real GSP growth 0.3% that year

• In 2011 the economy limped further along

• .9% Real GSP growth

In 2012 we expect 2.4% growth

Job growth limped alongside the economy, but only starting late in 2010.

Florida Forecast

Economic growth doesn’t gain significant altitude until 2015

Real GSP growth: 2013 = 2.6% 2014 = 2.7% 2015 = 3.3%

Florida Forecast

1615141312111009080706050403020100

10%

5%

0%

-5%

-10%

Florida Real Gross State Product(% change year ago)

Florida Forecast

1615141312111009080706050403020100

14.0%

12.0%

10.0%

8.0%

6.0%

4.0%

2.0%

Florida & U.S. Unemployment Rate(%)

FL Unemployment RateU.S. Unemployment Rate

Florida Forecast

1615141312111009080706050403020100

8200.0

8000.0

7800.0

7600.0

7400.0

7200.0

7000.0

6800.0

Florida Employment(Thousands)

Wage & Salary Employment

Florida Forecast

1615141312111009080706050403020100

1250.0

1200.0

1150.0

1100.0

1050.0

1000.0

950.0

900.0

850.0

Florida Professional & Business Services Employment

(Thousands)

Florida Forecast

1615141312111009080706050403020100

700.0

600.0

500.0

400.0

300.0

Florida Construction Employment(Thousands)

Florida Forecast

1615141312111009080706050403020100

160.0

150.0

140.0

130.0

120.0

110.0

Florida Federal Government Employment

(Thousands)

Florida Forecast

1615141312111009080706050403020100

1050.0

1000.0

950.0

900.0

850.0

Florida State & Local Government Employment

(Thousands)

Florida Forecast

1615141312111009080706050403020100

1100.0

1050.0

1000.0

950.0

900.0

850.0

800.0

Florida Leisure & Hospitality Employment

(Thousands)

Florida Forecast

1615141312111009080706050403020100

190.0

180.0

170.0

160.0

150.0

140.0

130.0

120.0

Florida Information Employment(Thousands)

Florida Forecast

1615141312111009080706050403020100

560.0

540.0

520.0

500.0

480.0

460.0

Florida Financial Activities Employment

(Thousands)

2013-2016 Averages; Q2 2013 Forecast

Florida

Sector % Average Annual

Growth

Construction 7.3

Professional & Business Services 4.0

Trade, Transportation & Utilities 3.2

Education-Health Services 2.2

Leisure & Hospitality 2.0

Information 1.1

Manufacturing 0.9

Financial 0.7

State & Local Government 0.3

Federal Government -1.0

Region Population Growth

Average % Chg Rank

Florida 1.4 ---

Deltona 1.0 8

Gainesville 0.5 12

Jacksonville 1.4 4

Lakeland 1.0 9

Miami 1.3 5

Naples 2.2 1

Ocala 1.5 3

Orlando 2.1 2

Palm Bay 0.9 10

Pensacola 0.8 11

Tallahassee 1.0 7

Tampa 1.2 6

2013-2016 Averages; Q3 2013 Forecast

Region Employment Growth

Average % Chg Rank

Florida 2.0 ---

Deltona 1.6 7

Gainesville 1.3 10

Jacksonville 2.2 5

Lakeland 1.2 12

Miami 1.8 6

Naples 2.9 1

Ocala 2.4 3

Orlando 2.5 2

Palm Bay 1.6 8

Pensacola 1.3 9

Tallahassee 1.3 11

Tampa 2.3 4

2013-2016 Averages; Q3 2013 Forecast

Sean M. Snaith, Ph.D.

Director

Institute for Economic Competitiveness

(407) 823-1453

WWW.IEC.UCF.EDU

www.facebook.com/seansnaith

Twitter: @seansnaith

Thank you

Florida Realtors® 2014 Real Estate and Economic Summit

Doing Business in Florida’s Growing Markets

Sponsored by

Location And Consumer Behavior: Intersection For Economic Development

Grant Ian Thrall Ph.D. ,

Owner & Founder, Business Geography Advisors

Immediate Past President, American Real Estate Society

11/24/2013 6:54 AM

U.S. High-School Students Slip In Global Rankings

12/11/2013 [email protected] 69

http://online.wsj.com/news/articles/SB10001424052702304579404579234511824563116?mod=djemalertNEWS

The Blame For Education Failure

12/11/2013 [email protected] 71

http://www.gainesville.com/article/20131203/ARTICLES/131209908/1002/news?Title=99-6-of-local-teachers-rated-effective-or-higher

Solution: Treat Education Like A

Retail Business

• Grant Thrall, 2005, The Changing Demographics Of The Florida College Student, presentation to the Florida Association of Colleges and Universities, Sarasota FL. June.

• Grant Thrall and Noelle Mecoli, 2003, Spatial Analysis, Political Support, and Higher Education Funding, GeoSpatial Solutions 13(7): 44-47.

Available at http://www.IDOXYZ.com

Education is a private good •Excludable •Rival

Education Delivery Has Been Place Based Place Based Facilities Have A Trade Area Place Based & eAccess Serve Demographic Niches Education Has A Value Platform

Also see

Grant Thrall, 2002, Business Geography and New Real Estate Market Analysis,

Oxford University Press: New York and Oxford.

&

12/11/2013 [email protected] 73

Universities Have Trade Areas

74

Grant Thrall, Geographic Access To Florida Higher Education, Report to the Florida Board Of Governors. http://www.IDOXYZ.com

http://www.idoxyz.com/reprints/GeoSpatialSolutions/GSS-2003-July-Thrall-Mecoli.pdf

Know Your Customers Buckets

Lifestyle Segmentation Profiles aka Psychographics

75

ESRI Tapestry By Income

Geospatial analysts today partition individuals within

consuming groups by their Lifestyle Segmentation Profile (LSP) also known as Psychographics

http://www.esri.com/data/esri_data/tapestry

Percent Of 2003 First-Time Freshmen By LifeMode By University

12/11/2013 [email protected]

www.BusinessGeography.com 76

Segmenting education for successful value platforms www.dteia.com

Point Map Of UF L1 LSP Students’ UF Campus Residence Locations

12/11/2013 [email protected]

www.BusinessGeography.com 77

Distribution Of UF Student Increase By Psychographic Segment

Students of an LSP segment cluster by neighborhood

50% of UF students are L1 and L2 based upon permanent address

Student Scores Arrayed According To Grade And LSP

Reading Math

The value platform of schools is designed for one group. The further one is from the mean of the targeted group, the less likely will the student be a high performer and high achiever. This one value platform system wastes human capital and other resources.

Percent Of Households Within Three Lowest DTEIA™ Categories For Education Performance And Achievement

12/11/2013 [email protected] 80

XY Axis Theme – Percent Of Households With Lowest 3 DTEIA™ Scores Z Axis Extrusion - Count Of Households With Lowest 3 DTEIA™ Scores

12/11/2013 [email protected] 81

XY Axis Theme - Count Of High Achiever Households Z Axis Extrusion - % Of Households As High Achievers

12/11/2013 [email protected] 82

2010-2015 Population Change

12/11/2013 [email protected] 83

Based upon US Census Tract Level Forecasts, GeoSpatially Aggregated To 6x6 Square Mile Grids

Action For

• Treat education K-PhD as Retail

• Allow Florida to become innovators & entrepreneurial

12/11/2013 [email protected] 84

12/11/2013 [email protected] 85

Grant Ian Thrall Ph.D. American Real Estate Society, Immediate Past President Business Geography Advisors Manager Founder Owner 8703 SW 38th Ave., Gainesville, FL 32608 [email protected] t:352-331-0145 f:352-331-0166

| | |

Dr. Grant Ian Thrall served as elected President of the American Real Estate Society (2012-2013). ARES is a global association of real estate and land economics thought leaders. Members are university academics and high level influential practitioners. ARES is the world's largest and most prestigious publisher of real estate and land economics scholarly research. Thrall has served many of ARES' journals, including as co-editor for real estate information technology of Journal of Real Estate Literature, member of the editorial boards of Journal of Real Estate Research and Journal of Sustainable Real Estate. He has served fifteen years on the Board of Directors of the American Real Estate Society. He is on the academic board of the Appraisal Institute's Appraisal Journal. He is the only geographer to have served in these positions. Thrall has a Ph.D. in Geography and Economics, and an MA in Economics from The Ohio State University, and a BA in Business & Economics from California State University at Los Angeles. Grant Thrall has been one of the leading international contributors to the development of practice and scholarship of geospatial analysis for business - namely, "business geography" / "business location intelligence" particularly for the built environment. His book published by Oxford University Press, Business Geography and New Real Estate Market Analysis, is a synthesis of his pioneering scholarly contributions with foundations in his solid practitioner work of over a quarter century. The American Real Estate Society’s Journal of Real Estate Literature called his book “a paradigm shift” for real estate market analysis. The Wharton School of Business writes that Thrall’s book is “compelling” as it builds the bridge between urban economic and geographic sciences advancing real estate market analysis. George Mason University writes that Thrall’s book is one that every person in business needs to read. Dr. Thrall has written or edited over a dozen books, and over 150 professional articles. His ten volume Scientific Geography Series remains as the standard reference for academic scholarship and practitioner decisions on business location, and his book Land Use and Urban Form remains as the most comprehensive, while at the same time accessible, general theories of urban land use markets. Thrall is regularly quoted in the news media including an article on him in Florida Trend, and the Gainesville Sun Newspaper serving his adopted home of thirty years. Thrall receives the 2013 first annual "ARES/Marc-Louargand Award" for research written and presented by a practicing professional at the ARES Annual Meeting. Previously Thrall has been a recipient of the "ARES/Torto-Wheaton Prize for "Real Estate Market Analysis." He is recipient of the first Distinguished Scholar Award in Business Geography from the Association of American Geographers; the highest academic accolade in his geospatial field. He is elected founding Chair of the Business Geography Specialty Group of the Association of American Geographers. Dr. Thrall is Managing Director and Owner of www.BusinessGeography.com through which he has executed real estate market analysis for over $1B in sustainable infill development and redevelopment. He has been admitted as an expert in Federal and State Courts in the fields of real estate market analysis opining on location value, and Geographic Information Systems (GIS) technology opining on patents. Thrall has been an expert in over $100M in litigation. Dr. Thrall is co-founder of Direct Target Education Instruction Assessment - www.DTEIA.com. Thrall has two patents pending related to target education: 20080228747 Information System Providing Academic

12/11/2013 [email protected] 86

Performance Indicators By Lifestyle Segmentation Profile And Related Methods; and 20080227077 Geographic Information System Providing Academic Performance Indicators And Related Methods. Previously, Thrall was co-founder of the nation's leading supplier of Internet backbone GIS ready fiber-optic pathway digital maps. Thrall has been a consultant with real estate advisory firms including PriceWaterhouseCoopers LLP, and Alvarez & Marsal LLC. In Gainesville Florida he has executed market analysis for many infill developments - Butler Plaza the largest power center in the US southeast - The Continuum - University Corners - O2BKids. He has published advisory research reports for Centers for Disease Control and Prevention, FannieMae, the Appraisal Institute, the Bill and Melinda Gates Foundation, Post Secondary Analytics, and the State University System of Florida Board of Governors for which he was primary author of Geographic Access Analysis of the State University System of Florida; Thrall's analysis contributed to the elevation of most of Florida's two-year community colleges to four-year state college status, including Santa Fe College in Gainesville FL. Dr. Grant Thrall was invited keynote speaker at the September 2013 International Council of Shopping Centers 2013 Research Conference in Philadelphia, and invited keynote speaker at the November 2013 Forum On Property Valuation In China, hosted by Xiamen University. Thrall was invited by Dr. Lawrence Yun to be a presenter on his panel at the November 10, 2012, National Association of Realtors® Conference and Expo in Orlando Florida (introduction, keynote address). He has been invited to give keynote addresses to University of Pennsylvania’s Wharton School of Business and Cal Berkeley’s Haas School of Business, the annual “Golledge Geography Lecture” at UC Santa Barbara, the annual “Burns Real Estate Lecture” in the Daniels College of Business at University of Denver, the Business College at University of Tulsa, Florida Association of Colleges and Universities, National Association of Real Estate Investment Managers, Senior Management of Publix Grocery, International Council Of Shopping Centers (North Florida); and invited plenary presentations to the Association of American Geographers, and the American Real Estate Society. He organized the Memphis Conference On Sustainable Real Estate. Dr. Thrall has been on the faculty, and held the ranks and titles ranging from Assistant through Full Professor, Distinguished Professor, and Endowed Chair of Excellence at universities including McMaster University in Canada, State University of New York at Buffalo, University of Memphis, San Diego State University, and University of Florida. He has held faculty appointments in Geography, Economics, Finance, and Real Estate; his faculty appointments have been in colleges of science, business, liberal arts, and social science. He presently holds positions as Fellow of the Homer Hoyt Institute in Palm Beach Florida; Fellow, David F. Miller (JC Penny) Center for Retailing Education & Research, Warrington College of Business Administration University of Florida. He holds faculty appointments as Visiting Professor at: Newman Department of Real Estate in the Zicklin School of Business of the Baruch College of Business City University of New York; REALTOR® University (Chicago); and Homburg University (Switzerland and Canada). He is a member of the leadership and review board of REALTOR® University, and the academic advisory board of the International Council of Shopping Centers. Dr. Thrall has chaired over 25 graduate student committees at MA and Ph.D. levels.

Dr. Thrall's most recent publications include "Review of Maptitude GIS For Real Estate Market Analysis"

GeoInformatics, 2013 issue 3. And his recent co-authored publications include "Location Efficiency and Mortgage

Default", Journal of Sustainable Real Estate which was cited in The Economist, NRDC, New Geography and HUD;

"Foreclosure Contagion and REO versus non-REO Sales," Winter 2012, International Real Estate Review. "A

General Model of Mortgage Failure Tipping Point with an Example from Southern California 2006-2007",

International Journal of Housing Markets and Analysis. 2013; 6(4):438-454.

Grant Thrall resides in Gainesville Florida where he has volunteered his expertise, advice and management of redevelopment of historic downtown Gainesville, a Tax Increment Community Redevelopment District. In appreciation, the Mayor and Gainesville City Commission declared two days as "Grant Thrall Days".

Florida Realtors® 2014 Real Estate and Economic Summit

Doing Business in Florida’s Growing Markets

Sponsored by

Dr. John Tuccillo

5,000

7,000

9,000

11,000

13,000

15,000

17,000

19,000

21,000

23,000

25,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013

2012

2011

2010

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013

2012

2011

2010

0

50

100

150

200

250

300

Ja

nu

ary

19

95

Ju

ly 1

99

5

Ja

nu

ary

19

96

Ju

ly 1

99

6

Ja

nu

ary

19

97

Ju

ly 1

99

7

Ja

nu

ary

19

98

Ju

ly 1

99

8

Ja

nu

ary

19

99

Ju

ly 1

99

9

Ja

nu

ary

20

00

Ju

ly 2

00

0

Ja

nu

ary

20

01

Ju

ly 2

00

1

Ja

nu

ary

20

02

Ju

ly 2

00

2

Ja

nu

ary

20

03

Ju

ly 2

00

3

Ja

nu

ary

20

04

Ju

ly 2

00

4

Ja

nu

ary

20

05

Ju

ly 2

00

5

Ja

nu

ary

20

06

Ju

ly 2

00

6

Ja

nu

ary

20

07

Ju

ly 2

00

7

Ja

nu

ary

20

08

Ju

ly 2

00

8

Ja

nu

ary

20

09

Ju

ly 2

00

9

Ja

nu

ary

20

10

Ju

ly 2

01

0

Ja

nu

ary

20

11

Ju

ly 2

011

Ja

nu

ary

20

12

Ju

ly 2

01

2

Ja

nu

ary

20

13

7,400,000

7,600,000

7,800,000

8,000,000

8,200,000

8,400,000

8,600,000

8,800,000

9,000,000 Ja

n 2

00

8

Ma

r 2

00

8

Ma

y 2

00

8

Ju

l 2

00

8

Se

p 2

00

8

Nov 2

00

8

Ja

n 2

00

9

Ma

r 2

00

9

Ma

y 2

00

9

Ju

l 2

00

9

Se

p 2

00

9

Nov 2

00

9

Ja

n 2

01

0

Ma

r 2

01

0

Ma

y 2

01

0

Ju

l 2

01

0

Se

p 2

01

0

No

v 2

01

0

Ja

n 2

011

Ma

r 2

011

Ma

y 2

011

Ju

l 2

011

Se

p 2

011

Nov 2

011

Ja

n 2

01

2

Ma

r 2

01

2

Ma

y 2

01

2

Ju

l 2

01

2

Se

p 2

01

2

Nov 2

01

2

Ja

n 2

01

3

Ma

r 2

01

3

Ma

y 2

01

3

Ju

l 2

01

3

Se

p 2

01

3

0%

10%

20%

30%

40%

50%

60%

Ja

n 2

00

8

Ma

r 2

00

8

Ma

y 2

00

8

Ju

l 2

00

8

Se

p 2

00

8

No

v 2

00

8

Ja

n 2

00

9

Ma

r 2

00

9

Ma

y 2

00

9

Ju

l 2

00

9

Se

p 2

00

9

No

v 2

00

9

Ja

n 2

01

0

Ma

r 2

01

0

Ma

y 2

01

0

Ju

l 2

01

0

Se

p 2

01

0

No

v 2

01

0

Ja

n 2

011

Ma

r 2

011

Ma

y 2

011

Ju

l 2

011

Se

p 2

011

No

v 2

011

Ja

n 2

01

2

Ma

r 2

01

2

Ma

y 2

01

2

Ju

l 2

01

2

Se

p 2

01

2

No

v 2

01

2

Ja

n 2

01

3

Ma

r 2

01

3

Ma

y 2

01

3

Ju

l 2

01

3

Se

p 2

01

3

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Ja

n 2

00

8

Ma

r 2

00

8

Ma

y 2

00

8

Ju

l 2

00

8

Se

p 2

00

8

No

v 2

00

8

Ja

n 2

00

9

Ma

r 2

00

9

Ma

y 2

00

9

Ju

l 2

00

9

Se

p 2

00

9

No

v 2

00

9

Ja

n 2

01

0

Ma

r 2

01

0

Ma

y 2

01

0

Ju

l 2

01

0

Se

p 2

01

0

No

v 2

01

0

Ja

n 2

011

Ma

r 2

011

Ma

y 2

011

Ju

l 2

011

Se

p 2

011

No

v 2

011

Ja

n 2

01

2

Ma

r 2

01

2

Ma

y 2

01

2

Ju

l 2

01

2

Se

p 2

01

2

No

v 2

01

2

Ja

n 2

01

3

Ma

r 2

01

3

Ma

y 2

01

3

Ju

l 2

01

3

Se

p 2

01

3

0

50,000

100,000

150,000

200,000

250,000 Ja

n 2

00

8

Ma

r 2

00

8

Ma

y 2

00

8

Ju

l 2

00

8

Se

p 2

00

8

No

v 2

00

8

Ja

n 2

00

9

Ma

r 2

00

9

Ma

y 2

00

9

Ju

l 2

00

9

Se

p 2

00

9

No

v 2

00

9

Ja

n 2

01

0

Ma

r 2

01

0

Ma

y 2

01

0

Ju

l 2

01

0

Se

p 2

01

0

No

v 2

01

0

Ja

n 2

011

Ma

r 2

011

Ma

y 2

011

Ju

l 2

011

Se

p 2

011

No

v 2

011

Ja

n 2

01

2

Ma

r 2

01

2

Ma

y 2

01

2

Ju

l 2

01

2

Se

p 2

01

2

No

v 2

01

2

Ja

n 2

01

3

Ma

r 2

01

3

Ma

y 2

01

3

Ju

l 2

01

3

Se

p 2

01

3

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000 Ja

n 2

00

8

Ma

r 2

00

8

Ma

y 2

00

8

Ju

l 2

00

8

Se

p 2

00

8

Nov 2

00

8

Ja

n 2

00

9

Ma

r 2

00

9

Ma

y 2

00

9

Ju

l 2

00

9

Se

p 2

00

9

Nov 2

00

9

Ja

n 2

01

0

Ma

r 2

01

0

Ma

y 2

01

0

Ju

l 2

01

0

Se

p 2

01

0

Nov 2

01

0

Ja

n 2

011

Ma

r 2

011

Ma

y 2

011

Ju

l 2

011

Se

p 2

011

Nov 2

011

Ja

n 2

01

2

Ma

r 2

01

2

Ma

y 2

01

2

Ju

l 2

01

2

Se

p 2

01

2

Nov 2

01

2

Ja

n 2

01

3

Ma

r 2

01

3

Ma

y 2

01

3

Ju

l 2

01

3

Se

p 2

01

3

The real estate market will continue to

grow

Residential sales up about 10 percent

Commercial market will continue modest

recovery

Values will rise at historical rates

Accessibility to finance will be the key

Florida Realtors® 2014 Real Estate and Economic Summit

Doing Business in Florida’s Growing Markets

Sponsored by