2013 consolidated audit report on official development ... - coa…€¦ · coa commission on audit...

TRANSCRIPT

2013

Consolidated Audit Report on

Official Development Assistance Programs and Projects

TABLE OF CONTENTS Page 1.0 INTRODUCTION Legal Basis 1 Scope and Content 3 Methodology 5 2.0 HIGHLIGHTS OF THE REPORT 6 3.0 STATUS OF ODA-FUNDED PROJECTS Outstanding Balances 10 Availments 15 Repayments 17 Commitments 21 Undrawn Commitments 29 Debt Service Expenditures 34 4.0 AUDIT OBSERVATIONS AND RECOMMENDATIONS 43 4.1 Agency- specific Observations and Recommendations 4.1.1 Department of Agriculture (DA) 44 4.1.2 Department of Agrarian Reform (DAR) 52 4.1.3 Development Bank of the Philippines (DBP) 57 4.1.4 Department of Environment and Natural Resources (DENR) 60 4.1.5 Department of Energy (DOE) 65 4.1.6 Department of Public Works and Highways (DPWH) 68 4.1.7 Department of Social Welfare and Development (DSWD) 72 4.1.8 National Irrigation Administration (NIA) 80 4.1.9 Department of Transportation and Communications (DOTC) 87 4.1.10 Other Agencies’ finding 90 4.2 Common Audit Observations 92 4.3 General Audit Recommendations 93 4.4 Status of Implementation of Prior Years’ Audit Recommendations 95 5.0 CHART I Sources and Utilization 4 II Programs and Projects Status 6 III Loan Availments, Repayment and Balances by Type of Creditor 7 IV

Loan Cumulative Net Commitments, Availments and Undrawn Balances by Type of Creditor

8

V Changes on Loan Outstanding Balance 10 VI Outstanding Balance by Creditor Type 10 VII Outstanding Balance by Creditor (Details) 11 VIII Number of Loans Outstanding Balance by Sector 12

IX Cumulative Availments by Sector 15 X Commitments by Type of Creditor 22 XI Cumulative Commitments, Cancellation and Net Commitments by

Sector 24

XII Cumulative Commitments, Cancellation and Net Commitments by Implementing Agency

25

XIII Undrawn Balance by Sector 28 XIV Debt Service Expenditures 30 XV Principal Repayment by Type of Creditor and Type of Loans 35 XVI Comparative Interest Payment 37 XVII Commitment Fees by Creditor Type anf Loan Type 39 XVIII Status of Implementation of Prior Years’ Audit Recommendations 95 6.0 TABLES I Status and Breakdown of Loans 3 II Debt Service Expenditures by Creditors 8 III Debt Service Expenditures by Sector 8 IV Commitment Fees by Type of Creditor and Type of Loans 9 V Highest Five Outstanding Balance by Sector 12 VI Outstanding Balance by Implementing Agency 14 VII

VIII Current Year Availments by Creditor Comparative Repayment

15 16

IX Current and Cumulative Repayments by Creditor 17 X Current and Cumulative Repayments by Implementing Agency 19 XI List of New ODA Loans 20 XII Cancelled Commitments for 2013 21 XIII Cumulative Commitments, Cancellation and Net Loan Commitment

by Creditor 22

XIV Cumulative Commitments, Cancellation and Net Commitments by Implementing Agency

25

XV Net Commitments, Cumulative Availments and Undrawn Balance by Creditor

27

XVI Net Commitments, Cumulative Availments and Undrawn Balance by Sector and Implementing Agency

29

XVII Debt Service Expenditures by Creditor 31 XVIII Debt Service Expenditures Paid by BTr 32 XIX Debt Service Expenditures Paid by GOCCs 34 XX Debt Service Expenditures Paid by BTr for the Implementing

Agencies Account 35

XXI Interests by Type of Creditor and Loans 37 XXII Interests on Loans Paid by BTr 38 XXIII Interests on Loans Paid by GOCCs 38 XXIV Commitment Fees by Implementing Agency 40 XXV Commitment Fees by Implementing Agency and Project 40 XXVI DA - Project Status and Loan Summary Profile 45 XXVII DA - List of Projects with Audit Observations 45 XXVIII DAR - Project Status and Loan Summary Profile 53

XXIX DAR - List of Projects with Audit Observations 53 XXX DBP - Project Status and Loan Summary Profile 58 XXXI DBP - List of Projects with Audit Observations 58 XXXII DENR - Project Status and Loan Summary Profile 61 XXXIII DENR - List of Projects with Audit Observations 61 XXXIV DOE - Project Status and Loan Summary Profile 66 XXXV DPWH - Project Status and Loan Summary Profile 69 XXXVI DPWH - List of Projects with Audit Observations 69 XXXVII DSWD - Project Status and Loan Summary Profile 73 XXXVIII DSWD - List of Projects with Audit Observations 73 XXXIX NIA - Project Status and Loan Summary Profile 81 XXXX NIA - List of Projects with Audit Observations 81 XXXXI DOTC - Project Status and Loan Summary Profile 88 XXXXII DOTC - List of Projects with Audit Observations 88 XXXXIII Status of Implementation of Prior Years’ Audit Recommendations 95

2WHSMP Second Women’s Health and Safe Motherhood Project 4 Ps Pantawid Pamilyang Pilipino ProgramABC Approved Budget of the ContractACIR Assistant Commissioner of Internal RevenueACT Area Coordinating TeamADB Asian Development BankAGDB Authorized Government Depository BankALCO Asset Liability Committee ANF Air Navigation Facilities Modernization ProjectAO Accountable OfficerAOM Audit Observation MemorandumAPL Adaptable Program LoanAPP Annual Procurement PlanAPR Annual Procurement RequestARBs Agrarian Reform BeneficiariesARCP II Agrarian Reform Communities Project IIARE Acknowledgment Receipt of EquipmentARIIP Agno River Integrated Irrigation Project ARISP II Agrarian Reform Infrastructure Support Project, Phase II ARISP III Agrarian Reform Infrastructure Support Project, Phase III BAC Bids and Awards CommitteeBACC Board of Audit and Compliance CommitteeBAC/TWG Bids and Awards Committee /Technical Working GroupBFP Bureau of Fire ProtectionBIHC Bureau of International Health CooperationBIR Bureau of Internal RevenueBOC Bureau of CustomsBOE Bureau of Equipment BPIP Banaoang Pump Irrigation Project BRS Bank Reconciliation StatementBSMPC Barangay Sub-Project Management CommitteeBSP Banko Sentral ng PilipinasBSAARP Bacolod-Silay Airport Access Road ProjectBTr Bureau of the TreasuryCAAP Civil Aviation Authority of the PhilippinesCAF Contract Approval FormCBIM Community-Based Infrastructure ManualCBPM Community Based Procurement ManualCCA Certificate of Completion and AcceptanceCCT Conditional Cash TransferCEXIM The Export-Import Bank of ChinaCFA Implementation Management Agreement CFL Compact Fluorescent LampsCHARMP

Cordillera Highland Agricultural Resource Management Project CHI-I China National Construction and Agriculture Machinery ICIP Construction In ProgressCNAA Collective Negotiation AgreementCNMEG China National Machinery and Equipment Corp. GroupCOA Commission on AuditCOS Contract of ServiceCSF Container Service Fee CY Calendar YearDA Department of AgricultureDAC Deputy Area CoordinatorDAR Department of Agrarian ReformDBM Department of Budget and Management DBP Development Bank of the Philippines

LIST OF ACRONYMS

LIST OF ACRONYMS

DENR Department of Environment and Natural ResourcesDepEd Department of EducationDIADP Davao International Airport Development ProjectDILG Department of Interior and Local GovernmentDMAD Debt Monitoring and Analysis Division DOE Department of EnergyDOF Department of FinanceDOH Department of HealthDOTC Department of Transportation and CommunicationsDPWH Department of Public Works and HighwaysDSI Design Science IncorporatedDSWD Department of Social Welfare and DevelopmentDTI Department of Trade and IndustryDVs Disbursement VouchersECGD Export Credit Guarantee Department - Deutsche BankEGF Efficient Government FundEIB European Investment BankEME Extraordinary and Miscellaneous expensesEMF Environmental Monitoring FundEVAT Expanded Value Added Tax FAD Financial Accounting DepartmentFAPs Foreign Assisted ProjectsFAPsO Foreign-Assisted Project Office (FAPsO)FB Farmers BeneficiariesFEF front-end feeFFIs Foreign Funding Institutions FIMAS Finance & Management ServiceFIU Field Implementing UnitFIR Final Inspection ReportFLI Foreign Lending InstitutionFMIS Financial Management Information SystemFMR Financial Monitoring ReportFMSM Finance Management Sub-ManualFOREX Foreign Exchange FS Financial StatementFMO Fund Management OfficeFO Field OfficeFXRC Foreign Exchange Risk CoverFXRCF Foreign Exchange Risk Cover FeeGAA General Appropriations ActGAAM Government Accounting and Auditing Manual GCF Green Climate FundGEF Global Environment FacilityGFI Government Financing InstitutionsGMA Greater Maritime AccessGOP Government of the Philippines GOCCs Government Owned and Controlled CorporationsGPA Good Practice AwardsGPPB Government Procurement Policy BoardGSD General Services DivisionGSIS Government Service Insurance SystemHCAAP Help for Catubig Agricultural Advancement ProjectHH HouseholdHREA Head Revenue Executive AssistantHSDP Health Sector Development Project IAs Implementing AgenciesIARCDSP Italian Assistance to the Agrarian Reform Community

Development Support Program

LIST OF ACRONYMS

IBRD International Bank for Reconstruction and DevelopmentICS Inventory Custodian SlipIFAD International Fund for Agricultural DevelopmentIMA Implementation Management Agreement IMOs Irrigation Management OfficesIRPEP Irrigated Rice Production Enhancement ProgrammeIRR Implementing Rules and RegulationsIT Information TechnologyJBIC Japan Bank for International CooperationJICA Japan International Cooperation AgencyJEV Journal Entry VoucherJEXIM Export-Import Bank of Japan JRMP Jalaur River Multipurpose ProjectKC-AF KALAHI CIDSS - Additional FinancingKALAHI-CIDSS Kapit-Bisig Laban sa Kahirapan-Comprehensive and KFAED Kuwait Fund for Arab Economic DevelopmentKFW Kreditanstalt für WiederaufbauLADP Laguindingan Airport Development ProjectLAMP 2 Second Land Administration and Management ProjectLBP Landbank of the PhilippinesLBP-TOD Landbank of the Philippines-Treasury Operations Dept.LCCA Local Currency Current AccountLGUs Local Government UnitsMBURD Mega Bridges for Urban and Rural DevelopmentMCCT Modified Conditional Cash TransferMCT Municipal Coordinating TeamMDS Modified Disbursement SystemMICTSI Mindanao International Container Terminal Services, Inc.MIDSAAD Mindanao Sustainable Agrarian and Agriculture Development

ProjectMNGAS Manuals on the New Government Accounting SystemMOA Memorandum of AgreementMOOE Maintenance and Other Operating ExpensesMRDP Mindanao Rural Development ProgramMIRP Mindanao Road Improvement ProjectMWSS Manila Water and Sewerage SystemNCA Notice of Cash AllocationNCAA Non-Cash Availment AuthorityNCIP National Commission on Indegenous PeoplesNCISP Non-intrusive Container Inspection ProjectND Notice of DisbursementNEDA National Economic Development Authority NG National Government NGAs National Government AgenciesNGAS New Government Accounting SystemNGDAD National Government Debt Accounting Division NGOs Non-Governmental OrganizationsNGOs/POs Non-Governmental Organizations/Peoples' OrganizationNGP National Greening ProgramNHTO National Household Targeting Office NHTS-PR

National Household Targeting System for Poverty ReductionNIA National Irrigation Administration NIA-BPIP National Irrigation Administration - Banaoang Pump Irrigation

Project NIA-RIO National Irrigation Administration-Regional Irrigation OfficeNIADP New Iloilo Airport Development Project

LIST OF ACRONYMS

NLRC North Luzon Railway CorporationNPC National Power CorporationNPSBE National Program Support to Basic Education NPSENRMP National Program Support for Environment and Natural

Resources Management Program NOA Notice of AwardNPSTAR National Program Support for Tax Administration Reform NRIMP 2 National Roads Improvement and Management Project 2NRM Natural Resource ManagementOCM Overhead, Contingencies and MiscellaneousODA Official Development AssistanceOECF Overseas Economic Cooperation FundOGCC Office of the Government Corporate CounselOPEC Organization of the Petroleum Exporting CountriesORs Official ResceiptsOTC Over the CounterPAMANA PAyapa at MAsaganang PamayaNAnPAR Property Acknowledgement ReceiptPAS Philippine Accounting StandardsPBG Performance Based GrantPC Property CustodianPD Presidential DecreePDCI PHILJA Development Center IncorporatedPDS Philippine Dealing SystemPFRS Philippine Financial Reporting StandardsPPE Property Plant and EquipmentPEEP Philippine Energy Efficiency ProjectPEZA Philippine Economic Zone AuthorityPHIC Philippine Health Insurance CorporationPI Public InfrastructurePIA PHIVIDEC Industrial AuthorityPICE Philippine Institute of Civil EngineersPIDP Participatory Irrigation Development ProjectPIM Project Implementation Manual PLGU Provincial Local Government UnitPMIS Property Management Information SystemPMO Project Monitoring OfficePMST Project Management Support TeamPMU Project Monitoring UnitPHILJA Philippine Judicial AcademyPNOC Philippine National Oil CorporationPNR Philippine National RailwaysPO Purchase OrderPOW Program of WorkPPE Property, Plant and Equipment PPELC Property, Plant and Equipment Ledger CardPRDP Philippine Rural Development ProjectPS Procurement ServicePSO Project Support OfficePTC PHILJA Training Center PUV pool unit valuePWS Portable Water SystemPWU Provincial Women's UnionRA Republic ActRFO Regional Field OfficeRIGP Regional Infrastructure for Growth ProjectRITO Regional Information Technology Officer

LIST OF ACRONYMS

RMG Resource Management GroupROP Republic of the PhilippinesRPCI Report of Physical Count of InventoriesRPCPPE Report on the Physical Count of Property, Plant and

Equipment RPMT Regional Project Monitoring Team RPMO Regional Project Management OfficeRO Regional OfficeRORO Roll-On Roll-Off ROW Right of WayRSB Reinforced Steel barsRSMI Report of Supplies and Materials IssuedRTLA Retail Term Loan AgreementRuMEPP Rural Micro-Enterprise Promotion ProgrammeSADP I Selected Airports Development Project, Phase ISARO Special Allotment Release OrderSBGFC Small Business Guarantee and Finance CorporationSBP School Building ProjectsSC Supreme CourtSCs Stock CardsSCHARMP Second Cordillera Highland Agricultural Resource

Management ProjectSFD Saudi Fund for DevelopmentSL Subsidiary Ledger SLCs Supplies Ledger CardsSMEDSP Small & Medium Enterprise Development Support ProjectSMEFP Small Medium Enterprise Financing ProgrammeSOE Statement of ExpendituresSPs Sub-ProjectsSPCR Sub-Project Completion ReportSPSP Social Protection Support ProjectSPISP Southern Philippines Irrigation Sector ProjectSPU Supply and Property UnitSRRFPDP Social Reform Related Feeder Ports Development Projects SWDRP Social Welfare and Development Reform ProjectTADP Third Airports Development Project TCT Transfer Certificate of TitleTELOF Telecommunications Office TESDA Technical Education and Skills Development AuthorityTESDP Technical Education and Skill Development ProjectTSP Technical Service ProviderUCPB United Coconut Planters BankUSD US DollarsVAT Value Added Tax WB World Bank WFP Work and Financial Plan

1.0 INTRODUCTION

1

CONSOLIDATED AUDIT REPORT ON OFFICIAL DEVELOPMENT ASSISTANCE

FOR THE CALENDAR YEAR 2013

1.0 INTRODUCTION

1.1 Legal Basis

Official Development Assistance is governed by Republic Act (R.A.) No. 8182, as amended by R.A. No. 8555, approved on June 11, 1996, entitled:

The law was issued to facilitate the absorption and optimize the utilization of ODA

resources. It also excluded ODA loans from foreign debt limit of US$10 billion or its equivalent in other foreign currencies as set under Presidential Decree (P.D.) No. 1939, the law amending R.A No. 4860. The ODA loan continued to be the favored source of financing for the priority development projects of the country due to its lower interest rate and longer maturity periods compared to other foreign loans.

Section 2 of the subject law defines ODA as a loan or a loan and grant which

meets all of the following criteria:

a. It must be administered with the objective of promoting sustainable social and economic development and welfare of the Philippines;

b. It must be contracted with governments of foreign countries with whom the

Philippines has diplomatic, trade relations or bilateral agreements or which are members of the United Nations, their agencies and international or multilateral lending institutions;

c. There are no available comparable financial instruments in the capital market;

and

d. It must contain a grant element of at least twenty-five percent (25%). Grant element is the reduction enjoyed by the borrower whenever the debt service payments which shall include both principal and interest and expressed at their present values discounted at ten percent (10%) are less than the face value of the loan or loan and grant. The grant element of a loan or loan and grant is computed at the ratio of (i) the difference between the face value of the loan or loan and grant and the debt service payments to (ii) the face value of the loan or the loan and grant.

“An Act Excluding the Official Development Assistance (ODA) from the Foreign Debt Limit in order to Facilitate the Absorption and Optimize the Utilization of ODA Resources, Amending for the Purpose Paragraph 1, Section 2 of R.A. No. 4860, as amended”.

2

The main law on public debt is R.A. No. 4860, issued on August 8, 1966 entitled:

Under Section 1 of the above Act, the President of the Philippines is authorized, in behalf of the Republic of the Philippines, to contract such loans, credits and indebtedness with foreign governments, agencies or instrumentalities of such foreign governments, foreign financial institutions, or other international organizations, with whom, or belonging to countries with which, the Philippines has diplomatic relations, as may be necessary and upon such terms and conditions as may be agreed upon, to enable the Government of the Republic of the Philippines (ROP) to finance, either directly or through any government office, agency or instrumentality or any government-owned or controlled corporations, industrial, agricultural or other economic development purposes or projects authorized by law. It is also provided in this section that the authority of the President of the Philippines shall include the power to issue, for the purposes herein before stated, bonds for sale in the international markets the income from which shall be fully tax-exempt in the Philippines.

Section 2 provides that the total amount of loans, credits and indebtedness,

excluding interests, which the President is authorized to incur shall not exceed US$1 billion or its equivalent in other foreign currencies at the exchange rate prevailing at the time the loans, credits and indebtedness are incurred, provided that the total loans, credit and indebtedness incurred shall not exceed US$250 million or its equivalent in other currencies in the fiscal year of the approval of the Act, and US$250 million or its equivalent in other currencies every fiscal year thereafter.

Regarding the guarantee extended by the National Government (NG) to the

Government Owned and Controlled Corporations (GOCCs), the 1987 Philippine Constitution provides under Section 20, Article VII, that the President may contract or guarantee foreign loans on behalf of the Philippines with the prior concurrence of the Monetary Board, and subject to such limitations as may be provided by law. The Monetary Board shall, within thirty days from the end of every quarter of the calendar year, submit to the Congress a complete report of its decision on applications for loans to be contracted or guaranteed by the Government or government-owned and controlled corporations which would have the effect of increasing the foreign debt, and containing other matters as may be provided by law. This provision is likewise reiterated under Section 3 of RA No. 4860 which states that the President of the ROP is likewise authorized, in behalf of the ROP, to guarantee, upon such terms and conditions as may be agreed upon, foreign loans extended directly to, or bonds for sale in international markets issued by, corporations owned or controlled by the Government of the Philippines for industrial, agricultural or other economic development purposes or projects authorized by law.

“ An Act Authorizing the President of the Philippines to Obtain such Foreign Loans and Credits, or to Incur such Foreign Indebtedness, as may be Necessary to Finance Approved Economic Development Purposes or Projects, and to Guarantee, in behalf of the Republic of the Philippines, Foreign Loans Obtained or Bonds Issued by Corporations Owned or Controlled by the Government of the Philippines for Economic Development Purposes including those Incurred for Purposes of Re-lending to the Private Sector, Appropriating the Necessary Funds Therefor, and for Other Purposes”.

3

Another legal basis for public debt is PD No. 1939. This was issued on June 27,

1984 amending R.A. No. 4860 by increasing foreign debt limit to an amount not exceeding US$10 billion or its equivalent in other foreign currencies at the exchange rate prevailing at the time the loans, credits or indebtedness are incurred at terms of payment of not less than ten years except those contracted in the interest of national security and rehabilitation resulting from natural calamities. It amended the last paragraph of Section 3 of R.A. 4860 which state that the total amount of loans, credits or indebtedness incurred, and the proceeds of bonds, securities or other evidences floated or issued, which may be guaranteed by the President shall not be more than US$7.5 billion or its equivalent in other foreign currencies at the exchange rate prevailing at the time the guarantee is made excluding interests and other normal banking charges imposed or charged by the International Bank for Reconstruction and Development (IBRD), the Asian Development Bank (ADB) and other similar international financial institutions.

1.2 Scope and Content

The scope and content of the report are as follows:

1.2.1 The data on 406 ODA loans contracted and guaranteed by the National Government (NG) from January 1, 1995, as provided in Section 7 of R.A. No. 8182, up to December 31, 2013 are featured in this report.

There are two types of ODA loans: project loan and program loan. Project loans are foreign loans obtained to finance specific projects. Program loans are multi-purpose foreign loans not used to finance specific projects, but are conditioned on basic changes in economic, monetary or fiscal policies, among others. The loans comprise of 56 program loans and 350 project loans with cumulative net commitment amounting to P477.394 billion (US$10.753 billion) and P840.433 billion (US$18.929 billion) respectively. Table I shows the status and breakdown of these loans.

1.2.2 The loans were obtained from multilateral, bilateral and commercial creditors and utilized in five sectors: Infrastructure (Infra); Social Reform and Community Development (SRCD); Industry, Trade and Tourism (ITT); Agriculture, Agrarian

Program Project Total USD PHP5 50 55 5.588 248.0674 9 13 2.714 120.511

47 285 332 21.374 948.974- 6 6 0.006 0.275

56 350 406 29.682 1317.827USD 10.753 18.929 29.682PHP 477.394 840.433

Table I – Status and Breakdown of Loans

Cumulative Net Commitment

(in billion)

Cumulative Net Commitment

(in billion)StatusBreakdown

Active

1317.827

NewClosedCancelledTotal

4

Reform and Natural Resource (AARNR); and Governance and Institutions Development (GID). The graphical presentation of sources and utilization is shown in Chart 1.

Chart 1 – Sources and Utilization

1.2.3 The sources of the data in this report are the following:

a) Status Report on NG Direct and Guaranteed Loans – shows the details of foreign loans by loan account number, creditor and implementing agency with summary on the type of loans and creditors. This report is prepared by the Debt Monitoring and Analysis Division (DMAD), Bureau of the Treasury (BTr).

b) List of ODA loans signed during the year – the list is sourced from the

Department of Finance (DOF) and National Economic Development Authority (NEDA).

c) Summary of Debt Service Expenditures - Foreign – debt service pertaining to

payments made by the NG on Principal, Interests, Commitment Fees and Other Charges for the Direct and Relent Loans prepared by the National Government Debt Accounting Division (NGDAD), BTr

d) Actual Debt Service, ODA - Funded Projects – debt service pertaining to

payments made directly by the GOCCs for the NG Guaranteed loans prepared by concerned GOCCs.

1.2.4 Consolidated Audit Observations and Recommendations as of December 31, 2013

based on the audited reports submitted by the auditors of the implementing agencies concerned.

This report does not include Foreign-Assisted Projects (FAPs) funded from

ODA grants.

Sources (Creditor Type) Sources

(Creditor Type)

5

1.3 Methodology

The Commission on Audit (COA) maintains a database on ODA loans which is updated annually based on the Status Report on NG Direct and Guaranteed Loans submitted by the BTr. The data on the Status Report were validated from the DMAD, BTr and implementing agencies. The status of projects and loans were solicited from the agencies and respective auditors and verified from the NEDA Portfolio Review Report.

Based on updated data file, schedules were prepared for ODA loans by creditor,

sector and implementing agency with data on commitments, availments, repayments and outstanding and undrawn balances per loan account and project. The sectoral classifications of loans/projects used were based on NEDA reports. Data in tables, charts and narrative reports were taken from the reports.

All balances were translated to the local currency equivalent using the BSP

weighted average rate at reporting date which was published on the first working day of the ensuing year. Third currency balances are first converted to US Dollars (USD) then translated to Philippine Peso (PhP) using the exchange rate at reporting date.

In compliance with Section 8 (b) of R.A. No. 8182, as amended which mandated

the COA to conduct an audit of each ongoing and completed projects and submit report to Congress, the Auditors of National Government Agencies (NGAs), GOCCs and Local Government Units (LGUs) concerned, prepared and submitted to the National Government Sector (NGS) the audit observations and recommendations for consolidation. The consolidated audit observations and recommendations were grouped into audit issues related to Budget, Procurement, Financial Performance, Physical Performance, Project Sustainability and Other Issues.

2.0 HIGHLIGHTS OF THE REPORT

6

2.0 HIGHLIGHTS OF THE REPORT

The NG had contracted 406 ODA loans (excluding 7 cancelled loans) financing 336 programs and projects of the Government with net loan commitments of P1.318 trillion (US$29.68 billion) as of December 31, 2013. Of these programs and projects, 253 had been completed, 63 are on-going, and 12 have not yet started while 8 has been cancelled.

In 2013, 13 new loans were

contracted with net loan commitments of P120.51 billion (US$2.71 billion), 88.83 percent of these amounting to P107.06 billion (US$2.41 billion) remain undrawn, with no commitment fee paid by the NG.

Chart II – Programs and Projects Status

2.1 Loan Balances and Distribution

2.1.1 Outstanding Balances– P696.79 billion (US$15.69 billion)

As of December 31, 2013, out of 406 ODA loans, 328 had an outstanding balance amounting to P696.79 billion (US$15.69 billion) payable to three types of creditors, namely: Bilateral, Multilateral and Commercial.

2.1.2 Availments – P1.03 trillion (US$23.30 billion)

Total cumulative availments as of December 31, 2013 amounted to P1.03

trillion (US$23.30 million) while the current availments summed up to P36.40 billion (US$819.88 million).

In terms of sectoral distribution, the Social Reform and Community

Development is the major recipient of this year’s loan availments amounting to P23.55 billion (US$530.42 million) or 64.69 percent, followed by Infrastructure – P8.21 billion (US$185.00 million) or 21.25 percent, Agriculture - Natural Resources and Agrarian Reform – P3.99 billion (US$89.82 million) or 10.96 percent, Industry, Trade and Tourism – P0.55 billion (US$12.40 million) or 1.51 percent, and Governance and Institutions Development – P0.99 billion (US$2.23 million) or 0.27 percent.

Among the implementing agencies, the NGAs availed a total of P747.24

billion (US$16.83 billion), while the GOCCs and LGUs got P276.94 billion (US$6.24 billion) and P9.84 billion (US$0.22 billion), respectively.

2.1.3 Repayments – P337.23 billion (US$7.60 billion)

Cumulative repayments of P337.23 billion (US$7.60 billion) or 33.61

percent of the total availments were made to the following creditors: Bilateral – P152.45 billion (US$3.43 billion) or 45.21 percent, Multilateral – P142.80 billion (US$3.22 billion) or 42.35 percent and Commercial – P41.98 billion (US$0.95 billion) or 12.45 percent.

7

Shown below are the loan cumulative Availments, Repayments and outstading balances as of December 31, 2013, summarized as to type of creditor.

Chart III - Loan Availments, Repayment & Balances by Type of Creditor

(in billion peso)

2.2 Commitments – P1.47 trillion (US$33.14 billion)

The cumulative loan commitments as of December 31, 2013 totaled P1.47 trillion or US$33.14 billion. The cumulative cancellation of commitments reached P153.36 billion (US$3.45 billion) or 10.42 percent of the cumulative commitments.

The net loan commitments of P1.32 trillion (US$29.68 billion) were sourced

from the following creditors: Bilateral – P639.16 billion (US$14.40 billion), Multilateral – P593.77 billion (US$13.37 billion) and Commercial – P84.89 billion (US$1.91 billion).

For the current year, 13 new loans were contracted from five creditors. While five loan accounts with On the other hand, P2.56 billion or US$57.72 million from five loan accounts were cancelled representing unused/undisbursed balances of loan accounts.

2.3 Undrawn Commitments – P283.81 billion (US$6.39 billion)

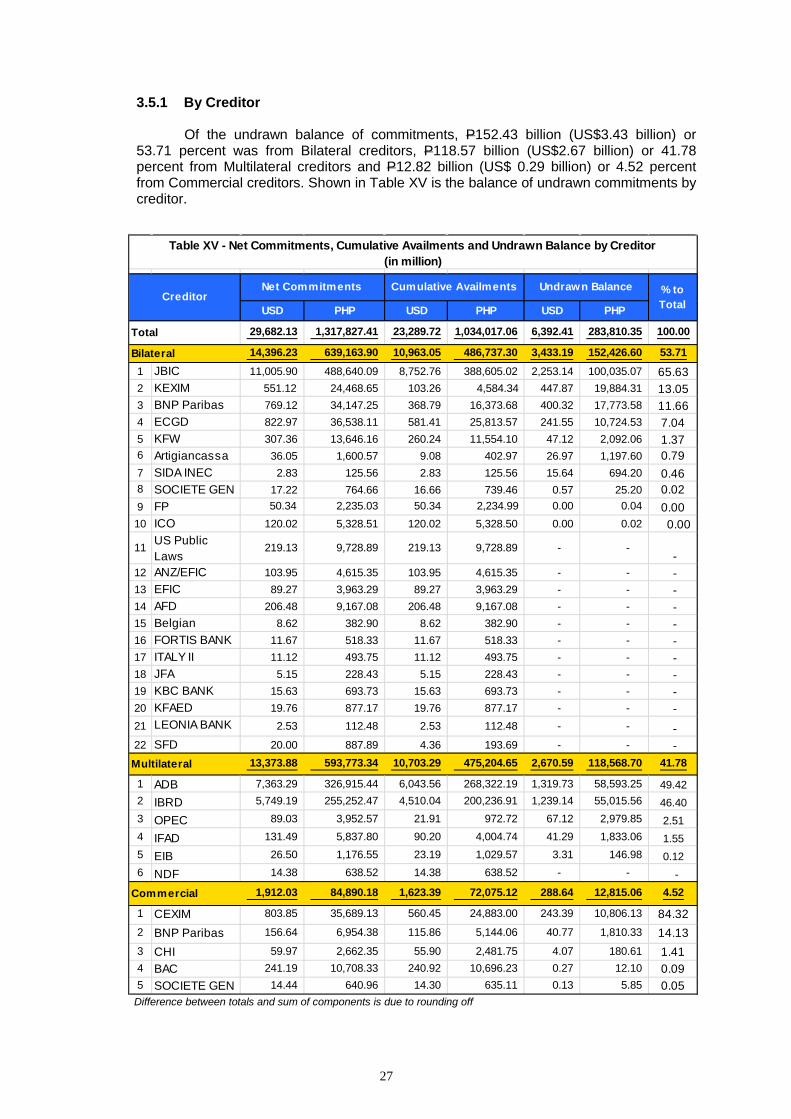

For the year, the undrawn balances of commitments of P283.81 billion (US$6.39 billion) represent 21.54 percent of the net loan commitments, of which, P152.43 billion (US$3.43 billion) or 53.71 percent is from Bilateral creditors, P118.57 billion (US$2.67 billion) or 41.78 percent from Multilateral creditors and P12.82 billion (US$0.29 billion) or 4.52 percent from Commercial creditors.

Creditor Type Cumulative Availments

Cumulative Repayment

Outstanding Balance

Commercial 72.08 41.98 30.10 Multilateral 475.20 142.80 332.40 Bilateral 486.74 152.45 334.29 Total 1,034.02 337.23 696.79 % to Cumulative availments 100.00% 32.61% 67.39%

8

Shown Chart IV are the loan cumulative net Commitments, Availments and

Repayments, as well as its balances as of December 31, 2013, summarized as to type of creditor.

Chart IV - Loan Cumulative Net Commitments, Availments

and Undrawn Balances by Type of Creditor (in billion peso)

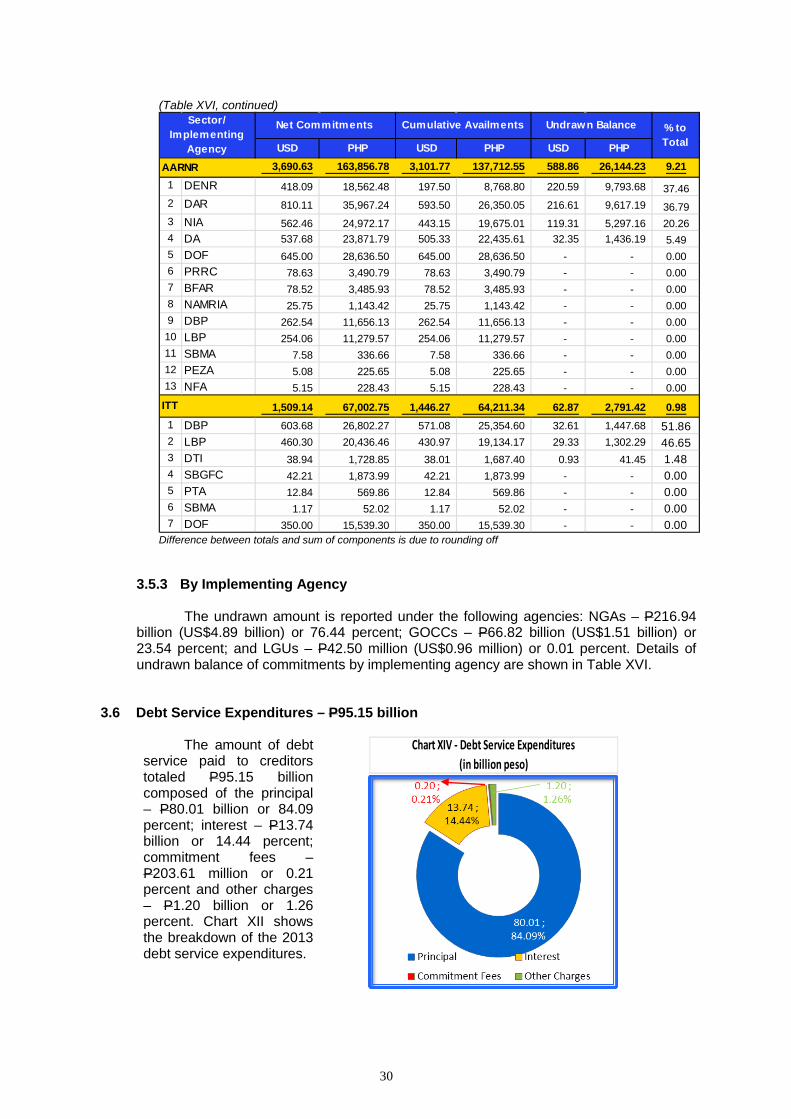

2.4 Debt Service Expenditures– P61.58 billion

During the year, the total debt service paid to creditors amounted to P95,149.04 billion, broken down as follows: Principal – P80.01 billion or 84.09 percent, Interest – P13.74 billion or 14.44 percent, Commitment Fees – P0.20 billion or 0.21 percent and Other charges – P1.20 billion or 1.26 percent as shown in Table II below.

Principal Interest Commit- ment Fees

Other Charges Total % to Total

1 Bilateral 24,786.01 6,138.86 172.63 751.04 31,848.54 33.472 Multilateral 48,098.16 6,734.65 28.00 386.16 55,246.98 58.063 Commercial 7,122.33 867.30 2.97 60.93 8,053.52 8.46

80,006.50 13,740.81 203.61 1,198.13 95,149.04 100.00

84.09 14.44 0.21 1.26 100.00

Table II- Debt Service Expenditures by Creditor Type(in million peso)

Creditor Type

TotalPercentage to total

Creditor Type Net Commitments

Cumulative Availments

Undrawn Balance

Commercial 84.89 72.08 12.81 Multilateral 593.77 475.20 118.57 Bilateral 639.17 486.74 152.43 Total 1,317.83 1,034.02 283.81 % to Net Commitments 100.00% 78.46% 21.54%

9

The breakdown of debt service expenditures by Sector is shown in Table III.

Commitment fees paid during the year for the undrawn balance amounted to P203.61 million or 0.07 percent of the total undrawn balance of commitments of P283.81 billion. Presented in Table IV are the types of loans with the amount of commitment fees paid to each type of creditor.

2.5 Audit Observations and Recommendations

The audit observations and recommendations which are significant and common among implementing agencies were summarized while iissues/observations particular to an agency are separately presented as agency-specific and both are grouped into audit issues related to Budget, Procurement, Financial Performance, Physical Performance, Project Sustainability and Other Issues.

Principal Interest Commit-

ments Fees

Other Charges Total % to Total

1 Infra. 35,735.97 6,584.22 163.36 981.38 43,464.92 45.682 GID 27,440.68 2,614.60 0.60 29.75 30,085.63 31.623 AARNR 8,374.40 1,675.36 13.65 85.91 10,149.31 10.674 SRCD 3,961.54 2,030.75 16.99 14.16 6,023.44 6.335 ITT 4,493.91 835.88 9.01 86.93 5,425.74 5.70

80,006.50 13,740.81 203.61 1,198.13 95,149.04 100.00

84.09 14.44 0.21 1.26 100.00

Total

Table III- Debt Service Expenditures by Sector(in million peso)

Sector

Percentage to total

NG Direct NG Relent

NG-Guaranteed Total % to Total

1 Bilateral 137.68 - 34.95 172.63 84.792 Multilateral 18.62 - 9.38 28.00 13.753 Commercial 2.97 - - 2.97 1.46

159.27 - 44.33 203.61 100.00

78.23 0.00 21.77 100.00

Creditor Type

TotalPercentage to total

Table IV- Commitment Fees Paid per Creditor Type and Type of Loans(in million pesos)

3.0 STATUS OF ODA –FUNDED

PROGRAMS AND PROJECTS

10

3.0 STATUS OF ODA-FUNDED PROJECTS

3.1 Outstanding Balance – P696.79 billion (US$15.69 billion)

As of December 31, 2013, the ODA loans has an outstanding balance of P696.79 billion (US$15.69 billion) which is lower by P46.20 billion (US$2.39 billion) compared with last year’s balance of P742.99 billion (US$18.09 billion). The decrease was caused by the adjustments, revaluation of foreign currency, and current year transactions (availments and repayments). The details are shown in Chart V:

3.1.1 By Type of Creditor The outstanding balance of ODA loans is payable to the following creditors: Bilateral – P 334.29 billion (US$7.53 billion) or 47.98 percent, Multilateral – P332.40 billion (US$7.49 billion) or 47.70 percent and Commercial – P30.10 billion (US$0.68 billion) or 4.32 percent. Chart VI presents the outstanding balance of ODA loans by creditor type as of December 31, 2013.

Of the outstanding ODA liabilities to bilateral creditors, the amount of P282.02 billion (US$6.35 billion) or 84.37 percent is payable to Japan Bank for International Cooperation (JBIC). For multilateral creditors, the liabilities to ADB and IBRD reached P168.22 billion (US$3.79 billion) or 50.61 percent and P159.46 billion (US$3.59 billion) or 47.97 percent, respectively. The breakdown are shown in the graphical presentations in the next page.

11

Chart VII – Outstanding Balance by Creditor (Details)

Bilateral Creditors

Multilateral Creditors

The amount due to commercial

creditors are mostly for CEXIM – P17.59 billion (US$396.25 million) or 58.45 percent, Bank of Austria Creditanstalt – P7.18 billion (US$161.77 million) or 23.86 percent and Raiffeissen Zentralbank Osterreich Aktiengeselschaft – P1.77 billion (US$39.84 million) or 5.88 percent, among others. The breakdown is shown in Chart VII.

Commercial Creditors

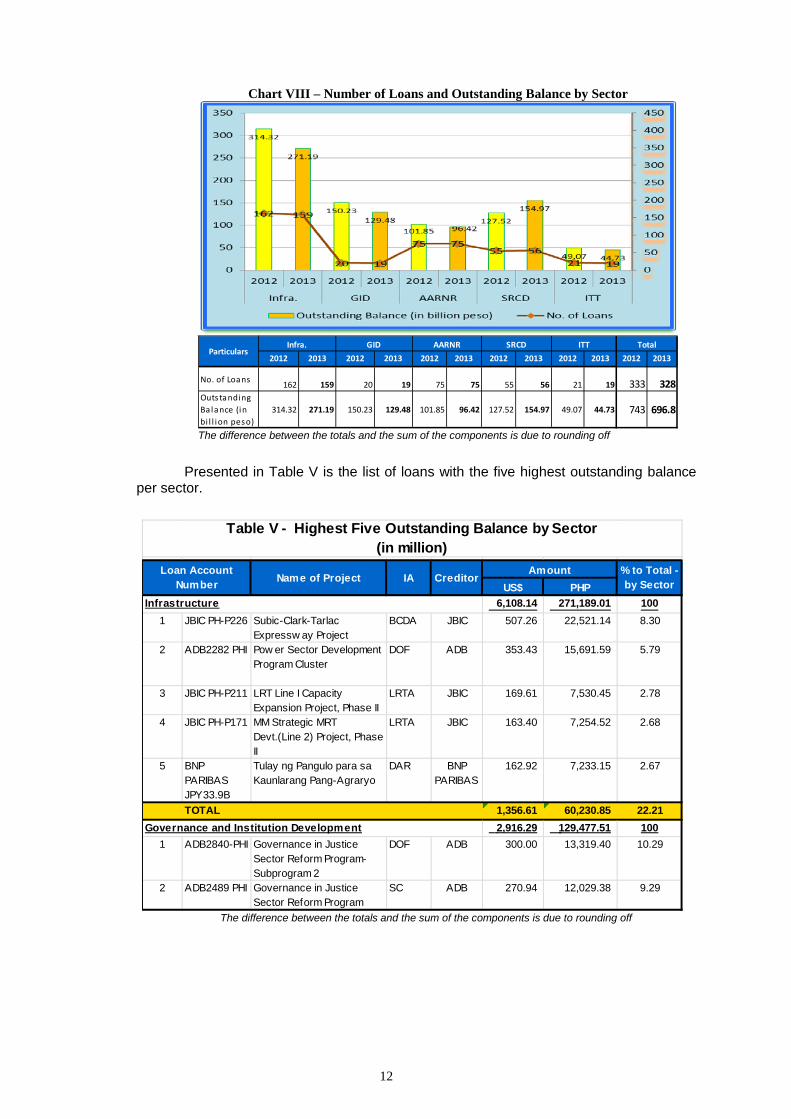

3.1.2 By Sector

Of the 406 loans, only 328 had an outstanding balance of P696.79 billion (US$15.69 billion) which is shared by the five sectors. Comparative figures are shown in Chart VIII.

12

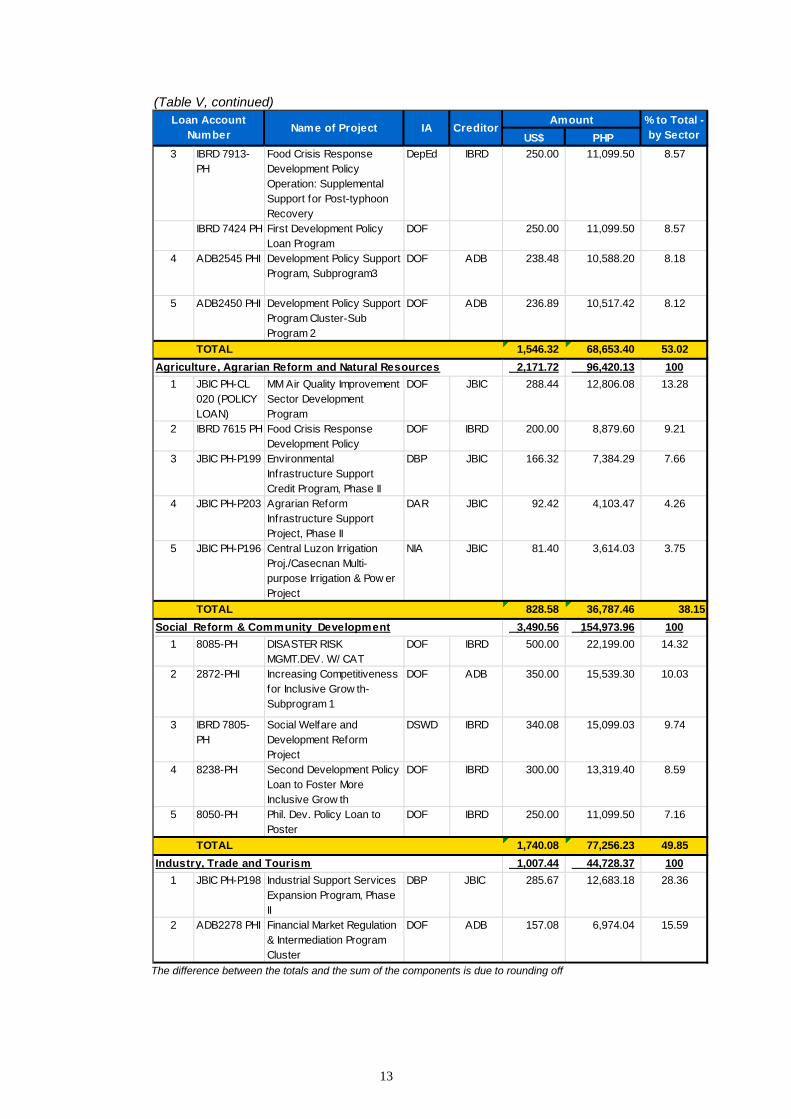

Presented in Table V is the list of loans with the five highest outstanding balance

per sector.

US$ PHP 6,108.14 271,189.01 100

1 JBIC PH-P226 Subic-Clark-Tarlac Expressw ay Project

BCDA JBIC 507.26 22,521.14 8.30

2 ADB2282 PHI Pow er Sector Development Program Cluster

DOF ADB 353.43 15,691.59 5.79

3 JBIC PH-P211 LRT Line I Capacity Expansion Project, Phase II

LRTA JBIC 169.61 7,530.45 2.78

4 JBIC PH-P171 MM Strategic MRT Devt.(Line 2) Project, Phase II

LRTA JBIC 163.40 7,254.52 2.68

5 BNP PARIBAS JPY33.9B

Tulay ng Pangulo para sa Kaunlarang Pang-Agraryo

DAR BNP PARIBAS

162.92 7,233.15 2.67

TOTAL 1,356.61 60,230.85 22.212,916.29 129,477.51 100

1 ADB2840-PHI Governance in Justice Sector Reform Program- Subprogram 2

DOF ADB 300.00 13,319.40 10.29

2 ADB2489 PHI Governance in Justice Sector Reform Program

SC ADB 270.94 12,029.38 9.29

Infrastructure

Governance and Institution Development

Table V - Highest Five Outstanding Balance by Sector(in million)

Loan Account Number Name of Project IA Creditor

Amount % to Total - by Sector

The difference between the totals and the sum of the components is due to rounding off

Chart VIII – Number of Loans and Outstanding Balance by Sector

2012 2013 2012 2013 2012 2013 2012 2013 2012 2013 2012 2013

No. of Loans 162 159 20 19 75 75 55 56 21 19 333 328Outstanding Ba lance (in bi l l ion peso)

314.32 271.19 150.23 129.48 101.85 96.42 127.52 154.97 49.07 44.73 743 696.8

TotalITTParticulars

Infra. GID AARNR SRCD

The difference between the totals and the sum of the components is due to rounding off

13

(Table V, continued)

US$ PHP 3 IBRD 7913-

PHFood Crisis Response Development Policy Operation: Supplemental Support for Post-typhoon Recovery

DepEd IBRD 250.00 11,099.50 8.57

IBRD 7424 PH First Development Policy Loan Program

DOF 250.00 11,099.50 8.57

4 ADB2545 PHI Development Policy Support Program, Subprogram3

DOF ADB 238.48 10,588.20 8.18

5 ADB2450 PHI Development Policy Support Program Cluster-Sub Program 2

DOF ADB 236.89 10,517.42 8.12

TOTAL 1,546.32 68,653.40 53.022,171.72 96,420.13 100

1 JBIC PH-CL 020 (POLICY LOAN)

MM Air Quality Improvement Sector Development Program

DOF JBIC 288.44 12,806.08 13.28

2 IBRD 7615 PH Food Crisis Response Development Policy

DOF IBRD 200.00 8,879.60 9.21

3 JBIC PH-P199 Environmental Infrastructure Support Credit Program, Phase II

DBP JBIC 166.32 7,384.29 7.66

4 JBIC PH-P203 Agrarian Reform Infrastructure Support Project, Phase II

DAR JBIC 92.42 4,103.47 4.26

5 JBIC PH-P196 Central Luzon Irrigation Proj./Casecnan Multi-purpose Irrigation & Pow er Project

NIA JBIC 81.40 3,614.03 3.75

TOTAL 828.58 36,787.46 38.153,490.56 154,973.96 100

1 8085-PH DISASTER RISK MGMT.DEV. W/ CAT

DOF IBRD 500.00 22,199.00 14.32

2 2872-PHI Increasing Competitiveness for Inclusive Grow th- Subprogram 1

DOF ADB 350.00 15,539.30 10.03

3 IBRD 7805-PH

Social Welfare and Development Reform Project

DSWD IBRD 340.08 15,099.03 9.74

4 8238-PH Second Development Policy Loan to Foster More Inclusive Grow th

DOF IBRD 300.00 13,319.40 8.59

5 8050-PH Phil. Dev. Policy Loan to Poster

DOF IBRD 250.00 11,099.50 7.16

TOTAL 1,740.08 77,256.23 49.851,007.44 44,728.37 100

1 JBIC PH-P198 Industrial Support Services Expansion Program, Phase II

DBP JBIC 285.67 12,683.18 28.36

2 ADB2278 PHI Financial Market Regulation & Intermediation Program Cluster

DOF ADB 157.08 6,974.04 15.59

Agriculture, Agrarian Reform and Natural Resources

Social Reform & Community Development

Industry, Trade and Tourism

Loan Account Number Name of Project IA Creditor

Amount % to Total - by Sector

The difference between the totals and the sum of the components is due to rounding off

14

(Table V, continued)

US$ PHP 3 JBIC PH-P189 Domestic Shipping

Modernization Program, Phase II

DBP JBIC 135.14 5,999.84 13.41

4 ADB2199 PHI Microfinance Development Program

DOF ADB 119.15 5,289.80 11.83

5 JBIC PH-P157 Metro Cebu Dev. Proj. III (Cebu South Reclamation)

LBP JBIC 68.38 3,036.08 6.79

TOTAL 765.42 33,982.93 75.98

Loan Account Number Name of Project IA Creditor

Amount % to Total - by Sector

The difference between the totals and the sum of the components is due to rounding off 3.1.3 By Implementing Agency

Of the outstanding liabilities, the amount of P523.49 billion (US$11.79 billion) or

75.13 percent was availed by the NGAs while P168.79 billion (US$3.80 billion) or 24.22 percent was for the account of the GOCCs. The balance of P4.51 billion (US$0.10 billion) or 0.65 percent is for the LGUs. Shown below is the total loan outstanding balance with the number of NG direct and relent loans and NG guaranteed loans.

US$ PHP

NGAs 230 0 230 11,790.81 523,488.20 75.13GOCCs 30 62 92 3,801.70 168,787.77 24.22LGUs 6 0 6 101.65 4,513.01 0.65 Total 266 62 328 15,694.16 696,788.98 100

% to Total

Implementing Agency

NG Direct and Relent

loans

NG Guaranteed

Total No. of Loans

Amount(in million)

The difference between the totals and the sum of the components is due to rounding off

Out of the total outstanding balance for NGAs, the amount of P236.24 billion

(US$5.32 billion) or 45.13 percent belongs to DOF, representing program loans for NGAs fund requirements. The DPWH also got P109.38 billion (US$2.46 billion) or 20.90 percent for the different government infrastructure projects such as construction and improvement of roads, bridges and highways, flood control projects and restoration/ rehabilitation of waterways, among others. The DepEd had P34.61 billion (US$0.78 billion) or 6.61 percent for projects implemented to support basic education.

On the part of the GOCCs, DBP has an outstanding balance of P42.51 billion

(US$0.96 billion) or 25.18 percent while the other implementing agencies with more than 10 percent share on the total GOCCs outstanding balance are LRTA, LBP and BCDA.

For the LGUs, only two implementing agencies shared in the total outstanding

balance, with P3.57 billion (US$80.42 million) or 79.12 percent for the account of ARMM while the amount of P0.94 billion (US$21.23 million) or 20.88 percent was attributed to the Provincial Gov’t. of Lanao Del Norte.

3.2 Availments – P1.03 trillion (US$23.29 billion)

As of December 31, 2013, cumulative availments reached P1.03 trillion (US$23.29 billion)

or equivalent to 70.28 percent of the total net commitments as presented in Chart III. Of these, P36.40 billion (US$0.82 billion) or 3.52 percent constitute availments during the year.

Table VI – Outstanding Balance by Implementing Agency (in million)

15

3.2.1 By Creditor Of the cumulative availments, Bilateral creditors provided the biggest amount of

P486.74 billion (US$10.96 billion) or 47.07 percent, of which P388.61 billion (US$8.75 billion) or 79.84 percent came from JBIC. Loans availed from multilateral creditors totaled P475.20 billion (US$10.70 billion) or 45.96 percent mostly coming from ADB – P268.32 billion (US$6.04 billion) or 56.46 percent and IBRD – P200.24 billion (US$4.51 billion) or 42.14 percent. Availments from Commercial creditors summed up to P72.08 billion (US$1.62 billion) or 6.97 percent. The graphical presentation is shown in Chart III while details by creditor is presented in Table XV.

The current

availments of P36.40 billion (US$819.88 million) are broken down as follows: Bilateral– P7.66 billion (US$172.48 million) or 21.04 percent, Multilateral – P27.83 billion (US$626.88 million) or 76.46 percent and Commercial – P0.91 billion (US$20.52 million) or 20.52 percent. Breakdown of current loan availments by creditor is shown in Table VII.

3.2.2 By Sector

Cumulative availments of P1.03 trillion were shared by the following sectors: Infrastructure – P481.14 billion (US$10.84 billion) or 46.53 percent, Governance and Institution Development – P175.89 billion (US$3.96 billion) or 17.01 percent, Social Reform and Community Development – P175.06 billion (US$3.94 billion) or 16.93 percent, Agriculture, Natural Resources and Agrarian Reform – P137.71 billion (US$3.10 billion) or 13.32 percent and Industry, Trade and Tourism – P64.21 billion (US$1.45 billion) or 6.21 percent. Table XVI shows the breakdown of availments.

Under the Infrastructure sector, the

DPWH availed P172.01 billion (US$6.54 billion) which accounted for 35.75 percent of the cumulative availments for the implementation of different projects.

Current year availments were

distributed to: SRCD – P23.55 billion (US$530.42 million) or 64.69 percent, , Infra. – P8.21 billion (US$185.00 million) or 22.56 percent, AARNR – P3.99 billion (US$89.82 million) or 10.96 percent, ITT – P0.55 billion (US$12.40 million) or 1.51 percent, and GID – P0.01 billion (US$2.23 million) or 0.27 percent.

Chart IX – Cumulative Availments by Sector (in billion pesos)

Difference between totals and sum of components is due to rounding off

USD PHP

Total Availments 819.88 36,401.08 100.00

Bilateral 172.48 7,657.81 21.041 JBIC 120.35 5,343.44 69.782 ECGD 28.42 1,261.95 16.483 ICO 10.25 455.29 5.954 SOCIETE GEN 9.08 402.97 5.265 KFW 4.06 180.45 2.366 SFD 0.27 11.96 0.167 AFD 0.04 1.75 0.02

Multilateral 626.88 27,832.15 76.46

1 IBRD 501.37 22,259.98 79.982 ADB 122.61 5,443.47 19.563 IFAD 2.04 90.69 0.334 OPEC 0.86 38.00 21.06

Commercial 20.52 911.12 2.50

1 BAC 20.16 894.84 98.212 CEXIM 0.25 11.16 1.223 BNP Paribas 0.12 5.12 0.56

% to Total

Table VII - Current Year Availments by Creditor(in million)

CY AvailmentsCreditor

16

3.2.3 By Implementing Agency

The NGAs cumulative availments reached P747.24 billion (US$16.83 billion) or 72.27 percent, GOCCs – P276.94 billion (US$6.24 billion) or 26.78 percent and LGUs – P9.84 billion (US$0.22 billion) or 0.95 percent. The DOF got the highest availment of P316.10 billion (US$7.12 billion) or 30.57 percent of the total cumulative availments for its program loans such as Development Policy Support Program, Local Government Financing and Budget Reform Program, Health Sector Development Program, Power Sector Development Program and Banking Sector Reform Program, among others. Details are shown in Table XIV.

The current year availments by implementing agency is as follows: a. NGAs – P32.65 billion (US$735.29 million) or 89.68 percent; b. GOCCs – P3.26 billion (US$73.45 million) or 8.96 percent; and c. LGUs – P0.49 billion (US$11.14 million) or 1.36 percent. During the year, the DOF received P13.32 billion (US$0.30 billion) or 40.80

percent for the project Second Development Policy Loan to Foster More Inclusive Growth while the DSWD received P8.38billion (US$0.19 billion) or 25.68 percent for Social Welfare and Development Reform, Social Protection Support and KALAHI-CIDSS project.

The DBP received P1.87 billion (US$42.21 million) or 57.46 percent of the current

availments for GOCCs on the following projects: Environmental Development Project – P1.13 billion (US$25.46 million), Logistics Infrastructure Development Project – P0.48 billion (US$10.84 million), Credit for Better HealthCare - P0.26 billion (US$5.90 million) and Rural Power Project – P0.35 million (US$0.01 million). The amount of P0.77 billion (US$17.40 million) or 23.69 percent will be used by LBP for Agricultural Credit Support Project, Support for Strategic Local Development & Investment Project and Metro Manila Waste Water Management Project.

For LGUs, the amount of P0.49 billion (US$11.14 million) or one percent of current

year availments was received by ARMM as additional financing for ARMM Soial Fund Project and ARMM Social Fund for Peace & Development Project.

3.3 Repayments – P337.23 billion (US$7.60 billion)

As of December 31, 2013, cumulative repayments reached P337.23 billion (US$7.60

billion), which is equivalent to 32.61 percent of the total availments or an increase of 6.34 percent compared with 2012. Comparative figures are presented in Table VIII. Of this amount, P76.95 billion (US$1.73 billion) or 22.82 percent covered repayment during the year.

3.3.1 By Creditor

Cumulative repayments of P337.23 billion (US$7.60 billion) were made to the

following: Bilateral creditors – P152.45 billion (US$3.43 billion) or 45.21 percent,

Table VIII – Comparative Repayment

2013 2012Cumulative Availments 1,034.02 1,007.80 26.22 Cumulative Repayments 337.23 264.81 72.42 Repayment rate (%) 32.61 26.28 6.34

ParticularsAmount

(in billion) Increase/ (decrease)

Difference between totals and sum of components is due to rounding

17

Multilateral creditors – P142.80 billion (US$3.22 billion) or 42.35 percent and Commercial creditors – P41.98 billion (US$0.95 billion) or 12.45 percent.

The JBIC is the recipient of P106.58 billion (US$ 2.40 billion) or 69.91 percent of

the cumulative repayments among bilateral creditors, followed by KEXIM with P24.35 billion (US$0.55 billion) or 15.97 percent. For the multilateral creditors, ADB and IBRD received P100.10 billion (US$2.25 billion) or 70.10 percent and P40.78 billion (US$0.92 billion) or 28.56 percent, respectively.

Current year’s repayments of P76.95 billion (US$1.73 billion) were made to the

following creditors: Bilateral – P22.50 billion (US$0.51 billion) or 29.25 percent; Multilateral – P47.16 billion (US$ 1.01 billion) or 61.30 percent and Commercial – P7.28 billion (US$0.16 billion) or 9.46 percent.

The details of repayments by creditor are shown below.

Table IX – Current and Cumulative Repayments by Creditor (in million)

USD PHP USD PHP

Total Repayment 1,733.08 76,945.32 7,595.57 337,228.08 100.00

Bilateral 506.87 22,504.05 3,433.70 152,449.61 45.211 JBIC 357.79 15,885.00 2,400.59 106,581.55 69.912 KEXIM 58.24 2,585.94 548.48 24,351.56 15.973 KFAED 10.52 466.86 93.44 4,148.49 2.724 ITALY II 6.63 294.44 85.95 3,816.07 2.505 US Public Laws 10.35 459.57 77.65 3,447.57 2.266 KFW 7.42 329.38 73.80 3,276.77 2.157 ECGD 37.24 1,653.31 46.27 2,054.21 1.358 AFD 6.95 308.61 27.97 1,241.90 0.819 ICO 2.45 108.84 14.81 657.39 0.43

10 ANZ/EFIC 1.87 83.22 14.18 629.41 0.4111 FORTIS BANK 1.26 55.85 13.47 597.92 0.3912 Belgian 0.86 38.40 9.51 422.35 0.2813 JFA 1.11 49.37 9.45 419.69 0.2814 FP 1.25 55.50 4.38 194.24 0.1315 EFIC 1.67 73.95 3.33 147.89 0.1016 SFD 1.00 44.39 3.00 133.18 0.0917 LEONIA BANK - - 2.83 125.56 0.0818 SIDA INEC - - 2.53 112.48 0.0719 Artigiancassa 0.26 11.42 2.06 91.37 0.06

Multilateral 1,062.29 47,163.72 3,216.43 142,802.89 42.35

1 ADB 923.85 41,016.98 2,254.67 100,102.78 70.102 IBRD 132.94 5,902.40 918.46 40,777.99 28.563 NDF 2.37 105.08 19.38 860.59 0.604 OPEC 1.16 51.54 13.68 607.30 0.435 IFAD 1.69 74.96 9.22 409.55 0.296 EIB 0.29 12.77 1.01 44.70 0.03

Commercial 163.92 7,277.55 945.44 41,975.58 12.45

1 CEXIM 103.60 4,599.78 164.21 7,290.42 17.372 Banco 1.35 59.81 155.91 6,921.89 16.49

% to Total

Cumulative RepaymentCreditor

Current Repayment

18

(Table IX, continued)

USD PHP USD PHP3 ERSTE (Austria) - - 122.18 5,424.50 12.924 CHI 20.13 893.87 102.46 4,548.99 10.845 BAC 15.72 697.89 79.15 3,514.12 8.376 ING Bank N.V. - - 52.13 2,314.51 5.517 FP 6.52 289.65 51.21 2,273.66 5.428 SOCIETE GEN - - 33.74 1,498.06 3.579 Banco Bilbao Vizcaya 1.10 49.02 30.23 1,342.08 3.20

10 NDF - - 27.40 1,216.72 2.9011 Bancaja - - 25.75 1,143.42 2.7212 FORTIS BANK - - 24.91 1,106.08 2.6413 ANZ/EFIC 7.15 317.56 14.30 635.11 1.5114 EFIC - - 14.08 625.02 1.4915 RZOA 2.01 89.22 14.07 624.54 1.4916 ECGD 4.35 192.97 13.92 617.83 1.4717 ICO - - 7.01 311.42 0.7418 Bank of America - - 6.19 274.99 0.6619 Credit Com'l de 0.92 40.75 5.45 242.06 0.5820 EDC 1.04 46.26 1.04 46.26 0.1121 Credit Agricole 0.02 0.78 0.09 3.89 0.01

% to Total

Cumulative RepaymentCreditor

Current Repayment

3.3.2 By Sector

Repayment were applied to the following sectors: Infrastructure – P209.95 billion (US$4.73 billion) or 62.26 percent; Governance and Institutions Development – P46.41 billion (US$1.05 billion) or 13.76 percent; Agriculture, Natural Resources and Agrarian Reform – P41.30 billion (US$0.93 billion) or 12.24 percent; Social Reform and Community Development – P20.08 billion (US4 0.45 billion) or 5.95 percent; and Industry, Trade and Tourism – P19.48 billion (US$ 0.44 billion) or 5.78 percent.

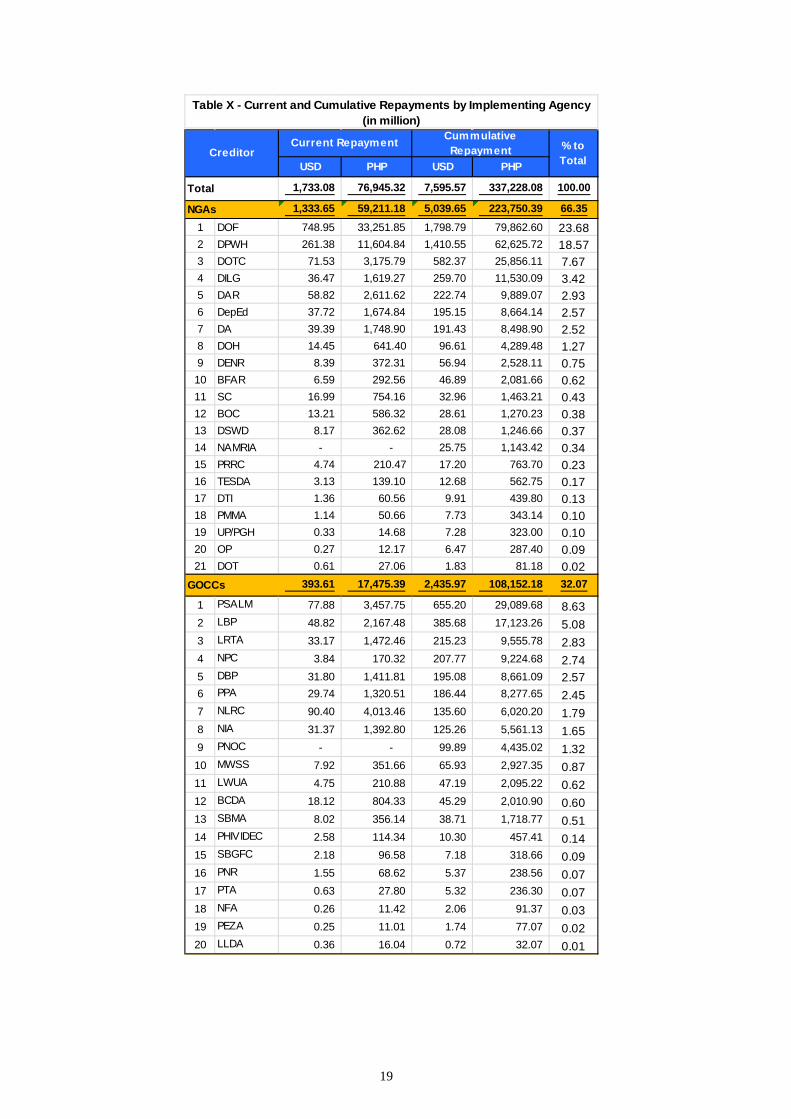

3.3.3 By implementing Agency

Cumulative repayments made for NGAs totaled P223.75 billion (US$5.04 billion) or 66.35 percent while for GOCCs the amount is P108.15 billion (US$2.44 billion) or 32.07 percent and for LGUs it is P5.33 billion (US$0.12 billion) or 1.58 percent. For the DOF account, P79.86 billion (US$ 1.80 billion) representing 23.68 percent of the cumulative repayment was paid while for DPWH, the amount is P62.63 billion (US$1.41 billion) or 18.57 percent.

Current year repayments of P44.03 billion (US$1.07 billion) were made for the

following implementing agencies: NGAs – P59.21 billion (US$1.33 billion) or 76.95 percent; GOCCs – P17.48 billion (US$ 0.39 billion) or 22.71 percent and LGUs – P258.75 million (US$5.83 million) or 0.34 percent.

The current and cumulative repayments by implementing agency is presented in

Table X.

19

Table X - Current and Cumulative Repayments by Implementing Agency(in million)

USD PHP USD PHP

Total 1,733.08 76,945.32 7,595.57 337,228.08 100.00

NGAs 1,333.65 59,211.18 5,039.65 223,750.39 66.351 DOF 748.95 33,251.85 1,798.79 79,862.60 23.682 DPWH 261.38 11,604.84 1,410.55 62,625.72 18.573 DOTC 71.53 3,175.79 582.37 25,856.11 7.674 DILG 36.47 1,619.27 259.70 11,530.09 3.425 DAR 58.82 2,611.62 222.74 9,889.07 2.936 DepEd 37.72 1,674.84 195.15 8,664.14 2.577 DA 39.39 1,748.90 191.43 8,498.90 2.528 DOH 14.45 641.40 96.61 4,289.48 1.279 DENR 8.39 372.31 56.94 2,528.11 0.7510 BFAR 6.59 292.56 46.89 2,081.66 0.6211 SC 16.99 754.16 32.96 1,463.21 0.4312 BOC 13.21 586.32 28.61 1,270.23 0.3813 DSWD 8.17 362.62 28.08 1,246.66 0.3714 NAMRIA - - 25.75 1,143.42 0.3415 PRRC 4.74 210.47 17.20 763.70 0.2316 TESDA 3.13 139.10 12.68 562.75 0.1717 DTI 1.36 60.56 9.91 439.80 0.1318 PMMA 1.14 50.66 7.73 343.14 0.1019 UP/PGH 0.33 14.68 7.28 323.00 0.1020 OP 0.27 12.17 6.47 287.40 0.0921 DOT 0.61 27.06 1.83 81.18 0.02

GOCCs 393.61 17,475.39 2,435.97 108,152.18 32.07

1 PSALM 77.88 3,457.75 655.20 29,089.68 8.632 LBP 48.82 2,167.48 385.68 17,123.26 5.083 LRTA 33.17 1,472.46 215.23 9,555.78 2.834 NPC 3.84 170.32 207.77 9,224.68 2.745 DBP 31.80 1,411.81 195.08 8,661.09 2.576 PPA 29.74 1,320.51 186.44 8,277.65 2.457 NLRC 90.40 4,013.46 135.60 6,020.20 1.798 NIA 31.37 1,392.80 125.26 5,561.13 1.659 PNOC - - 99.89 4,435.02 1.3210 MWSS 7.92 351.66 65.93 2,927.35 0.8711 LWUA 4.75 210.88 47.19 2,095.22 0.6212 BCDA 18.12 804.33 45.29 2,010.90 0.6013 SBMA 8.02 356.14 38.71 1,718.77 0.5114 PHIVIDEC 2.58 114.34 10.30 457.41 0.1415 SBGFC 2.18 96.58 7.18 318.66 0.0916 PNR 1.55 68.62 5.37 238.56 0.0717 PTA 0.63 27.80 5.32 236.30 0.0718 NFA 0.26 11.42 2.06 91.37 0.0319 PEZA 0.25 11.01 1.74 77.07 0.0220 LLDA 0.36 16.04 0.72 32.07 0.01

% to Total

Cummulative RepaymentCreditor

Current Repayment

20

(Table X, continued)

USD PHP USD PHP

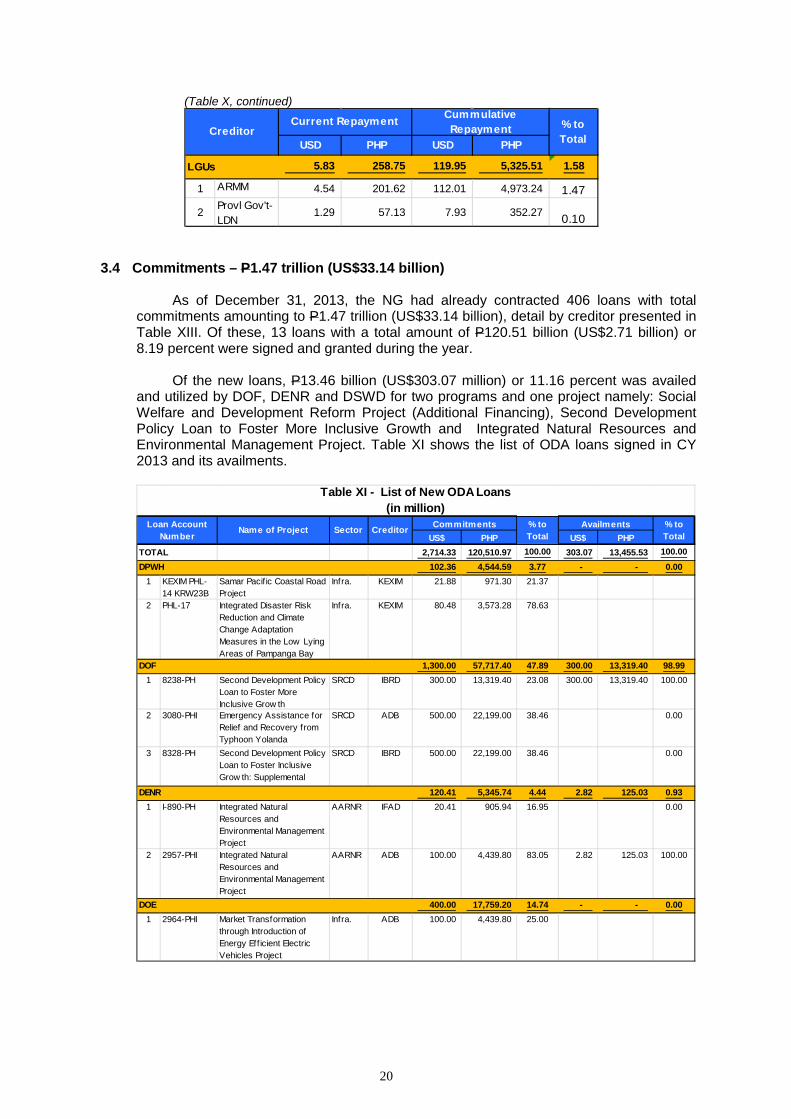

LGUs 5.83 258.75 119.95 5,325.51 1.58

1 ARMM 4.54 201.62 112.01 4,973.24 1.47

2 Provl Gov't-LDN

1.29 57.13 7.93 352.27 0.10

% to Total

Cummulative RepaymentCreditor

Current Repayment

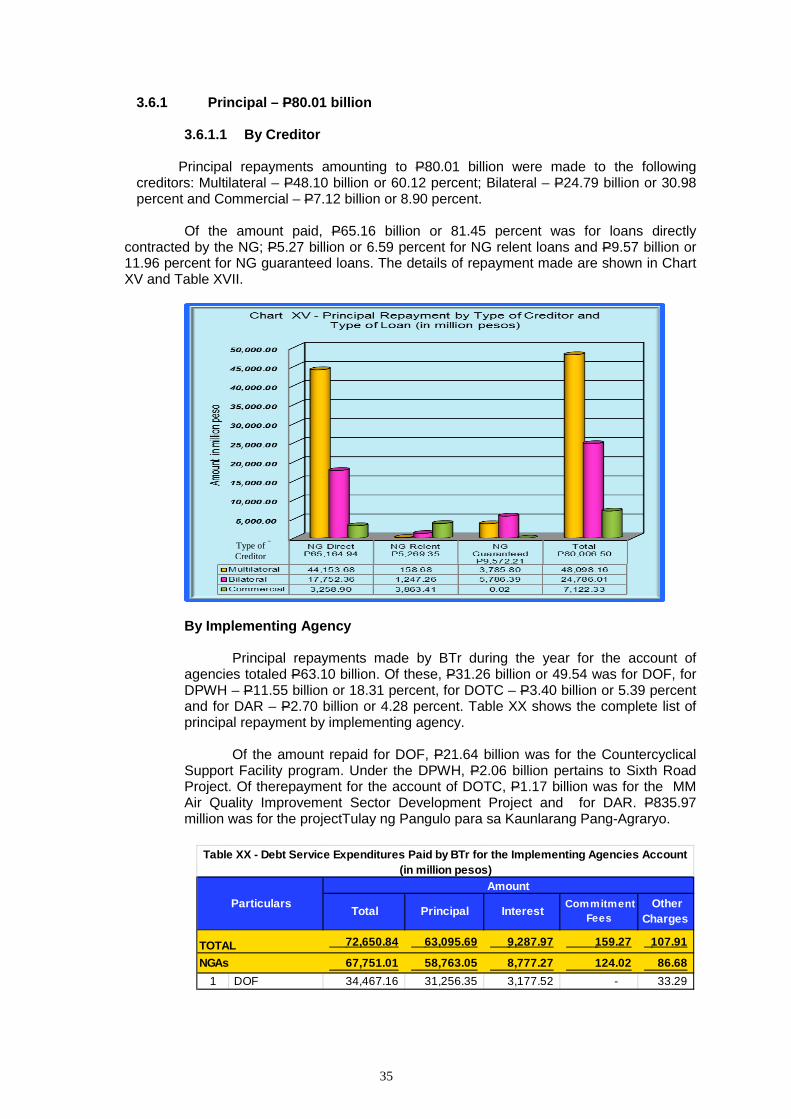

3.4 Commitments – P1.47 trillion (US$33.14 billion)

As of December 31, 2013, the NG had already contracted 406 loans with total commitments amounting to P1.47 trillion (US$33.14 billion), detail by creditor presented in Table XIII. Of these, 13 loans with a total amount of P120.51 billion (US$2.71 billion) or 8.19 percent were signed and granted during the year.

Of the new loans, P13.46 billion (US$303.07 million) or 11.16 percent was availed

and utilized by DOF, DENR and DSWD for two programs and one project namely: Social Welfare and Development Reform Project (Additional Financing), Second Development Policy Loan to Foster More Inclusive Growth and Integrated Natural Resources and Environmental Management Project. Table XI shows the list of ODA loans signed in CY 2013 and its availments.

US$ PHP US$ PHP TOTAL 2,714.33 120,510.97 100.00 303.07 13,455.53 100.00DPWH 102.36 4,544.59 3.77 - - 0.00

1 KEXIM PHL-14 KRW23B

Samar Pacif ic Coastal Road Project

Infra. KEXIM 21.88 971.30 21.37

2 PHL-17 Integrated Disaster Risk Reduction and Climate Change Adaptation Measures in the Low Lying Areas of Pampanga Bay

Infra. KEXIM 80.48 3,573.28 78.63

DOF 1,300.00 57,717.40 47.89 300.00 13,319.40 98.991 8238-PH Second Development Policy

Loan to Foster More Inclusive Grow th

SRCD IBRD 300.00 13,319.40 23.08 300.00 13,319.40 100.00

2 3080-PHI Emergency Assistance for Relief and Recovery from Typhoon Yolanda

SRCD ADB 500.00 22,199.00 38.46 0.00

3 8328-PH Second Development Policy Loan to Foster Inclusive Grow th: Supplemental

f

SRCD IBRD 500.00 22,199.00 38.46 0.00

DENR 120.41 5,345.74 4.44 2.82 125.03 0.931 I-890-PH Integrated Natural

Resources and Environmental Management Project

AARNR IFAD 20.41 905.94 16.95 0.00

2 2957-PHI Integrated Natural Resources and Environmental Management Project

AARNR ADB 100.00 4,439.80 83.05 2.82 125.03 100.00

DOE 400.00 17,759.20 14.74 - - 0.001 2964-PHI Market Transformation

through Introduction of Energy Eff icient Electric Vehicles Project

Infra. ADB 100.00 4,439.80 25.00

Availments % to Total

Table XI - List of New ODA Loans(in million)

% to Total

Loan Account Number

Name of Project Sector Creditor Commitments

21

(Table X, continued)

US$ PHP US$ PHP 2 8261-PHI Market Transformation Thru

Introduction of Energy Eff icient Electric Vehicles Project

Infra. ADB 300.00 13,319.40 75.00

DSWD 100.00 4,439.80 3.68 0.25 11.10 0.081 8218-PH Social Welfare and

Development Reform Project (Additional Financing)

SRCD IBRD 100.00 4,439.80 100.00 0.25 11.10 100.00

DOTC 691.57 30,704.24 25.48 - - 0.001 PH-P255 Capacity Enhancement of

Mass Transit Systems in Metro Manila Project

Infra. JBIC/JICA 411.07 18,250.55 59.44

2 PH-P256 New Bohol Airport Construction and Sustainable Environmet Protection Project

Infra. JBIC/JICA 102.47 4,549.56 14.82

3 PH-P257 Maritime Safety Capability Improvement Project for the Philippine Coast Guard

Infra. JBIC/JICA 178.03 7,904.13 25.74

Availments % to Total

% to Total

Loan Account Number

Name of Project Sector Creditor Commitments

The cumulative cancelled commitments as of December 31, 2013 reached P153.36 billion (US$3.45 billion) or 10.42 percent of the cumulative commitments of P1.47 trillion (US$33.14 billion).

During the year, cancellation of commitments amounting to P2.56 billion

(US$57.72 million) representing unused/undisbursed balances was made by the creditors of five loan accounts as shown in Table XII.

Of the amount cancelled, P1.27 billion (US$28.61 million) pertains to Multilateral

creditors while the balance of P1.29 billion (US$29.11 million) were for Bilateral creditors.

USD PHP

Total 57.72 2,562.67 Infrastructure 53.22 2,362.88

1 ADB2507 PHI Phil. Energy Eff iciency Project

DOE ADB 1.83 81.03

2 IBRD 7673 PH Rural Pow er Project (Additional Financing)

DBP IBRD 22.28 989.38

3 JBIC PH-P246 Post Ondoy and Pepeng Short Term Infrastructure Rehabilitation Project

DPWH JBIC 16.90 750.23

4 JBIC PH-P221 Help for Catubig Agr. Adv. Project, SI

NIA JBIC 12.21 542.25

Social Reform and Community Development 4.50 199.79 1 8035-PH Laguna Lake Development

AuthorityLLDA IBRD 4.50 199.79

Table XII - Cancelled Commitments for 2013(in million)

AmountLoan Account Number CreditorName of Project IA

22

3.4.1 By Creditor

Cumulative loan commitments as of December 31, 2013 amounted to P1.47 trillion or US$33.14 billion sourced from the following: Bilateral creditors – P724.89 billion (US$16.33 billion) or 49.27 percent, Multilateral creditors – P659.95 billion (US$ 14.86 billion) or 44.86 percent and Commercial creditors – P86.35 billion (US$1.94 billion) or 5.87 percent. The JBIC, a bilateral creditor, reported P555.64 billion (US$12.52 billion) or 37.78 percent of the total commitments while the ADB and IBRD, multilateral creditors, committed the amount of P361.92 billion (US$8.15 billion) or 24.60 percent and P285.58 billion (US$6.43 billion) or 19.41 percent, respectively.

Current year’s commitments or new loans totaling P120.51 billion (US$2.71 billion), as presented in Table XI, were sourced from Bilateral creditors – P35.25 billion (US$0.79 billion) and Multilateral creditors – P85.26 billion (US$1.92 billion).

The total net loan commitments by creditor are as follows: Bilateral – P639.16 billion (US$14.40 billion) or 48.50 percent, Multilateral – P593.77 billion (US$13.37 billion) or 45.06 percent and Commercial – P84.89 billion (US$1.91 billion) or 6.44 percent. Among the bilateral creditors, the JBIC had P488.64 billion (US$11.01 billion) accounting for 76.45 percent of the total bilateral net loan commitments. For multilateral creditors, the ADB and IBRD committed P326.92 billion (US$7.36 billion) or 55.06 percent and P255.25 billion (US$5.75 billion) or 42.99 percent, respectively. For commercial creditors, the CEXIM had the highest amount of P35.69 billion (US$0.80 billion) or 42.04 percent of the total commercial net commitments. Table XIII shows the complete list of foreign creditors and net loan commitments.

USD PHP USD PHP USD PHP

Total Net Commitments 33,136.33 1,471,186.56 3,454.19 153,359.15 29,682.13 1,317,827.41 100.00

Bilateral 16,327.10 724,890.52 1,930.87 85,726.62 14,396.23 639,163.90 48.501 JBIC 12,515.07 555,643.94 1,509.16 67,003.85 11,005.90 488,640.09 76.452 ECGD 822.97 36,538.11 - - 822.97 36,538.11 5.723 BNP Paribas 1,136.73 50,468.56 367.61 16,321.31 769.12 34,147.25 5.344 KEXIM 557.44 24,749.32 6.32 280.66 551.12 24,468.65 3.835 KFW 347.06 15,408.69 39.70 1,762.53 307.36 13,646.16 2.146 US Public Laws 220.00 9,767.56 0.87 38.67 219.13 9,728.89 1.527 AFD 206.48 9,167.08 - - 206.48 9,167.08 1.438 ICO 120.04 5,329.40 0.02 0.89 120.02 5,328.51 0.839 ANZ/EFIC 106.48 4,727.43 2.52 112.08 103.95 4,615.35 0.7210 EFIC 89.48 3,972.94 0.22 9.65 89.27 3,963.29 0.6211 FP 53.14 2,359.18 2.80 124.15 50.34 2,235.03 0.3512 Artigiancassa 36.05 1,600.57 - - 36.05 1,600.57 0.2513 SFD 20.00 887.89 - - 20.00 887.89 0.1414 KFAED 21.29 945.43 1.54 68.26 19.76 877.17 0.1415 SOCIETE GEN 17.22 764.66 - - 17.22 764.66 0.12

% to Total

Table XIII - Cumulative Commitments, Cancellation and Net Loan Commitment by Creditor(in million pesos)

Net Cumulative CommitmentsCreditor

Cumulative CommitmentsCumulative Cancellation

Chart X – Commitments by Creditor (in billion peso)

Difference between totals and sum of components is due to rounding off

23

(Table XIII, continued)

USD PHP USD PHP USD PHP16 KBC BANK 15.63 693.73 0.00 0.00 15.63 693.73 0.1117 FORTIS BANK 11.67 518.33 - - 11.67 518.33 0.0818 ITALY II 11.17 495.95 0.05 2.20 11.12 493.75 0.0819 Belgian 8.62 382.90 - - 8.62 382.90 0.0620 JFA 5.18 230.14 0.04 1.71 5.15 228.43 0.0421 SIDA INEC 2.84 126.23 0.01 0.66 2.83 125.56 0.0222 LEONIA BANK 2.53 112.48 0.00 0.00 2.53 112.48 0.02

Multilateral 14,864.30 659,945.13 1,490.42 66,171.79 13,373.88 593,773.34 45.06

1 ADB 8,151.68 361,918.17 788.39 35,002.73 7,363.29 326,915.44 55.06

2 IBRD 6,432.30 285,581.06 683.11 30,328.59 5,749.19 255,252.47 42.993 IFAD 140.66 6,244.84 9.17 407.04 131.49 5,837.80 0.984 OPEC 97.00 4,306.61 7.97 354.03 89.03 3,952.57 0.675 EIB 26.50 1,176.55 - - 26.50 1,176.55 0.206 NDF 16.17 717.92 1.79 79.40 14.38 638.52 0.11

Commercial 1,944.93 86,350.91 32.90 1,460.74 1,912.03 84,890.18 6.44

1 CEXIM 803.98 35,694.90 0.13 5.77 803.85 35,689.13 42.042 BAC 241.27 10,711.83 0.08 3.51 241.19 10,708.33 12.613 BNP Paribas 156.64 6,954.38 - - 156.64 6,954.38 8.194 ECGD 155.91 6,921.89 - - 155.91 6,921.89 8.155 EDC 124.44 5,524.89 2.26 100.38 122.18 5,424.50 6.396 CHI 59.97 2,662.35 - - 59.97 2,662.35 3.147 RZOA 53.75 2,386.46 - - 53.75 2,386.46 2.818 BBV 52.15 2,315.40 0.02 0.89 52.13 2,314.51 2.739 FP 38.65 1,716.11 2.49 110.60 36.16 1,605.50 1.89

10 Credit Com'l de France

49.64 2,203.88 15.90 705.81 33.74 1,498.06 1.76

11Credit Agricole Indosuez

27.43 1,217.94 0.03 1.22 27.40 1,216.72 1.43

12 Banco Santander 25.75 1,143.42 - - 25.75 1,143.42 1.35

13 ERSTE (Austria) 25.01 1,110.33 - - 25.01 1,110.33 1.3114 ANZ/EFIC 25.55 1,134.58 0.64 28.51 24.91 1,106.08 1.3015 ICO 21.62 959.99 - - 21.62 959.99 1.13

16 ING Bank N.V. 20.10 892.19 - - 20.10 892.19 1.05

17 SOCIETE GEN 14.44 640.96 - - 14.44 640.96 0.7618 EFIC 14.80 657.09 0.72 32.07 14.08 625.02 0.7419 FORTIS BANK 9.12 405.05 - - 9.12 405.05 0.48

20 Bancaja 7.01 311.42 - - 7.01 311.42 0.37

21 Bank of America 10.00 443.98 3.81 168.99 6.19 274.99 0.3222 NDF 7.70 341.86 6.82 302.98 0.88 38.89 0.05

% to Total

Net Cumulative CommitmentsCreditor

Cumulative CommitmentsCumulative Cancellation

Difference between totals and sum of components is due to rounding off

3.4.2 By Sector

Sectoral allocation of cumulative net commitments is as follows: Infrastructure –

P676.64 billion (US$15.24 billion) or 51.35 percent, Governance and Institutions Development – P176.12 billion (US$3.97 billion) or 13.36 percent, Agriculture, Natural Resources and Agrarian Reform – P163.86 billion (US$3.69 billion) or 12.43 percent, Social Reform and Community Development – P234.21 billion (US$5.28 billion) or 17.77 percent and Industry, Trade and Tourism – P67.00 billion (US$1.51 billion) or 5.08 percent. The breakdown of the amount by sector is shown in Chart XI.

24

Chart X - Cumulative Commitments, Cancellation and Net Commitments

Amount % to Total Amount % to Total Amount % to Total

Infra. 759.15 51.60 82.51 53.80 676.64 54.04GID 200.18 13.61 24.06 15.69 176.12 13.88AARNR 200.48 13.63 36.62 23.88 163.86 13.16SRCD 241.06 16.39 6.85 4.47 234.21 13.26ITT 70.32 4.78 3.32 2.16 67.00 5.67Total 1,471.19 100.00 153.36 100.00 1,317.83 100.00

% to Cumulative Commitments 100% 10% 90%

Type of CreditorCumulative Commitments Cumulative Cancellation Net Commitments

Difference between totals and sum of components is due to rounding off Cumulative cancellation of P153.36 billion (US$3.45 billion) or 10.00 percent of

cumulative commitments and distributed as follows: Infrastructure – P82.51 billion (US$1.86 billion) or 53.80 percent, Governance and Institutions Development – P24.06 billion (US$0.54 billion) or 15.69 percent, Agriculture, Natural Resources and Agrarian Reform – P36.62 billion (US$0.82 billion) or 23.88 percent, Social Reform and Community Development – P6.85 billion (US$0.15 billion) or 4.47 percent and Industry, Trade and Tourism – P3.32 billion (US$0.07 billion) or 2.16 percent.

3.4.3 By Implementing Agency

The cumulative commitments are shared by NGAs – P1.06 trillion (US$23.98 billion) or 72.38 percent; GOCCs – P395.68 billion (US$ 8.91 billion) or 26.90 percent and LGUs – P10.67 billion (US$ 0.24 billion) or 0.73 percent. Chart XII shows the distribution of cumulative commitments, cancellation and net commitments by implementing agency.

25

Of the cumulative cancelled commitments of P153.36 billion (US$3.45 billion), P1030.65 billion (US$2.27 billion) or 65.63 percent is for NGAs, P51.92 billion (US$1.17 billion) or 33.85 percent for GOCCs and P0.79 billion (US$0.02 billion) or 0.52 percent for LGUs.

Net loan commitments

at year end of P1.32 trillion is for the following: loans directly contracted by the NG – P964.18 billion (US$21.72 billion) or 73.16 percent, GOCCs – P343.76 billion (US$7.74 billion) or 26.09 percent and for LGUs – P9.88 billion (US$0.22 billion) or 0.75 percent..

For the NGAs, more than 50 percent of the amount is accounted under the

following agencies: DOF – P360.50 billion (US$8.12 billion) or 37.39 percent, DPWH – P240.77 billion (US$5.42 billion) or 24.97 percent, DOTC – P84.87 billion (US$1.91 billion) or 8.80 percent; and DAR – P52.83 billion (US$ 1.19 billion) or 5.48 percent. Under the GOCCs, P66.70 billion (US$1.50 billion) or 19.40 percent and P57.20 billion (US$1.29 billion) or 16.64 percent were reported by the DBP and LBP, respectively. The share for LGUs is only P9.88 billion (US$0.25 billion) or 0.75 percent of the total loan net commitments. Shown in Table XIV is the Net Loan Commitments by Implementing Agency.

(Table XIV, continued)

USD PHP USD PHP USD PHP

Total 33,136.33 1,471,186.56 3,454.19 153,359.15 29,682.13 1,317,827.41 100.00

NGAs 23,983.82 1,064,833.56 2,267.00 100,650.17 21,716.82 964,183.39 73.161 DOF 8,760.96 388,969.02 641.16 28,466.04 8,119.80 360,502.98 37.392 DPWH 5,751.57 255,358.03 328.47 14,583.23 5,423.10 240,774.80 24.973 DOTC 2,299.18 102,078.82 387.55 17,206.40 1,911.63 84,872.43 8.804 DAR 1,270.94 56,427.25 81.08 3,599.88 1,189.86 52,827.37 5.485 DSWD 1,064.12 47,244.98 2.57 114.32 1,061.55 47,130.66 4.896 DepEd 1,058.98 47,016.60 84.24 3,740.15 974.74 43,276.44 4.497 DA 768.12 34,103.10 202.43 8,987.56 565.69 25,115.54 2.608 DOE 431.10 19,139.98 1.83 81.03 429.28 19,058.95 1.989 DENR 836.86 37,154.82 418.77 18,592.33 418.09 18,562.48 1.9310 DILG 417.11 18,518.99 44.08 1,957.07 373.03 16,561.93 1.72

% to Total

Table XIV - Cumulative Commitments, Cancellation and Net Commitments by Implementing Agency(in million)

Cumulative Net CommitmentsImplementing

Agency

Cumulative Commitments

Cumulative Cancellation

Difference between totals and sum of components is due to rounding off

Chart XII - Cumulative Commitments, Cancellation and Net Commitments by Implementing Agency (in billion peso)

26

3.5 Undrawn Commitments – P283.81 billion (US$6.39 billion)

As of December 31, 2013, the undrawn balance of commitments reached P283.81 billion (US$6.39 billion) representing 21.54 percent of the total net commitments as shown in Chart IV.

USD PHP USD PHP USD PHP11 DOH 378.27 16,794.21 28.41 1,261.36 349.85 15,532.86 1.6112 SC 321.90 14,291.72 0.50 22.20 321.40 14,269.52 1.4813 BOC 198.22 8,800.55 0.13 5.77 198.09 8,794.78 0.9114 PRRC 90.63 4,023.58 12.00 532.79 78.63 3,490.79 0.3615 BFAR 90.57 4,021.15 12.05 535.22 78.52 3,485.93 0.3616 TESDA 71.24 3,162.91 13.14 583.29 58.10 2,579.61 0.2717 DTI 46.52 2,065.35 7.58 336.50 38.94 1,728.85 0.1818 BFP 28.21 1,252.45 - - 28.21 1,252.45 0.1319 NAMRIA 25.75 1,143.42 - - 25.75 1,143.42 0.1220 DOT 19.33 858.26 0.74 33.07 18.59 825.20 0.0921 PMMA 18.30 812.42 0.11 4.89 18.19 807.53 0.0822 UP/PGH 13.56 601.96 - - 13.56 601.96 0.0623 OP 11.39 505.61 0.16 7.09 11.23 498.51 0.0524 BIR 11.00 488.38 - - 11.00 488.38 0.05

GOCCs 8,912.13 395,680.75 1,169.37 51,917.74 7,742.76 343,763.00 26.09

1 DBP 1,602.74 71,158.62 100.45 4,459.87 1,502.29 66,698.75 19.402 LBP 1,410.92 62,642.11 122.50 5,438.93 1,288.42 57,203.18 16.643 NIA 868.16 38,544.54 52.31 2,322.37 815.85 36,222.16 10.544 LRTA 939.50 41,712.03 154.68 6,867.70 784.82 34,844.32 10.145 PSALM 1,063.98 47,238.79 328.54 14,586.35 735.45 32,652.44 9.506 BCDA 561.09 24,911.17 8.54 379.13 552.55 24,532.04 7.147 PPA 542.06 24,066.24 9.14 405.62 532.92 23,660.62 6.888 NLRC 400.00 17,759.20 - - 400.00 17,759.20 5.179 NPC 349.01 15,495.39 76.42 3,392.68 272.60 12,102.71 3.5210 MWSS 271.16 12,039.05 28.56 1,268.09 242.60 10,770.96 3.1311 SBMA 257.59 11,436.32 74.25 3,296.60 183.34 8,139.72 2.3712 LWUA 226.04 10,035.65 94.53 4,196.93 131.51 5,838.72 1.7013 PNOC 193.09 8,572.93 93.20 4,137.91 99.89 4,435.02 1.2914 PHIVIDEC 78.56 3,487.91 0.01 0.43 78.55 3,487.48 1.0115 PNR 46.88 2,081.52 0.01 0.25 46.88 2,081.27 0.6116 SBGFC 42.21 1,873.99 - - 42.21 1,873.99 0.5517 PTA 12.85 570.49 0.01 0.63 12.84 569.86 0.1718 LLDA 15.00 665.97 5.17 229.51 9.83 436.46 0.1319 NFA 5.18 230.14 0.04 1.71 5.15 228.43 0.0720 PEZA 26.10 1,158.70 21.02 933.05 5.08 225.65 0.07

LGUs 240.38 10,672.26 17.82 791.24 222.56 9,881.02 0.75

1 ARMM 199.24 8,846.02 5.85 259.69 193.39 8,586.33 86.90

2 Provl Gov't-LDN

41.13 1,826.24 11.97 531.55 29.16 1,294.69 13.10

% to Total

Cumulative Net CommitmentsImplementing

Agency

Cumulative Commitments

Cumulative Cancellation

Difference between totals and sum of components is due to rounding off

27

3.5.1 By Creditor

Of the undrawn balance of commitments, P152.43 billion (US$3.43 billion) or 53.71 percent was from Bilateral creditors, P118.57 billion (US$2.67 billion) or 41.78 percent from Multilateral creditors and P12.82 billion (US$ 0.29 billion) or 4.52 percent from Commercial creditors. Shown in Table XV is the balance of undrawn commitments by creditor.

USD PHP USD PHP USD PHP

Total 29,682.13 1,317,827.41 23,289.72 1,034,017.06 6,392.41 283,810.35 100.00

Bilateral 14,396.23 639,163.90 10,963.05 486,737.30 3,433.19 152,426.60 53.711 JBIC 11,005.90 488,640.09 8,752.76 388,605.02 2,253.14 100,035.07 65.632 KEXIM 551.12 24,468.65 103.26 4,584.34 447.87 19,884.31 13.053 BNP Paribas 769.12 34,147.25 368.79 16,373.68 400.32 17,773.58 11.664 ECGD 822.97 36,538.11 581.41 25,813.57 241.55 10,724.53 7.045 KFW 307.36 13,646.16 260.24 11,554.10 47.12 2,092.06 1.376 Artigiancassa 36.05 1,600.57 9.08 402.97 26.97 1,197.60 0.797 SIDA INEC 2.83 125.56 2.83 125.56 15.64 694.20 0.468 SOCIETE GEN 17.22 764.66 16.66 739.46 0.57 25.20 0.029 FP 50.34 2,235.03 50.34 2,234.99 0.00 0.04 0.0010 ICO 120.02 5,328.51 120.02 5,328.50 0.00 0.02 0.00

11 US Public Laws

219.13 9,728.89 219.13 9,728.89 - - -

12 ANZ/EFIC 103.95 4,615.35 103.95 4,615.35 - - - 13 EFIC 89.27 3,963.29 89.27 3,963.29 - - - 14 AFD 206.48 9,167.08 206.48 9,167.08 - - - 15 Belgian 8.62 382.90 8.62 382.90 - - - 16 FORTIS BANK 11.67 518.33 11.67 518.33 - - - 17 ITALY II 11.12 493.75 11.12 493.75 - - - 18 JFA 5.15 228.43 5.15 228.43 - - - 19 KBC BANK 15.63 693.73 15.63 693.73 - - - 20 KFAED 19.76 877.17 19.76 877.17 - - - 21 LEONIA BANK 2.53 112.48 2.53 112.48 - - - 22 SFD 20.00 887.89 4.36 193.69 - - - Multilateral 13,373.88 593,773.34 10,703.29 475,204.65 2,670.59 118,568.70 41.78

1 ADB 7,363.29 326,915.44 6,043.56 268,322.19 1,319.73 58,593.25 49.422 IBRD 5,749.19 255,252.47 4,510.04 200,236.91 1,239.14 55,015.56 46.403 OPEC 89.03 3,952.57 21.91 972.72 67.12 2,979.85 2.514 IFAD 131.49 5,837.80 90.20 4,004.74 41.29 1,833.06 1.555 EIB 26.50 1,176.55 23.19 1,029.57 3.31 146.98 0.126 NDF 14.38 638.52 14.38 638.52 - - -

Commercial 1,912.03 84,890.18 1,623.39 72,075.12 288.64 12,815.06 4.52

1 CEXIM 803.85 35,689.13 560.45 24,883.00 243.39 10,806.13 84.322 BNP Paribas 156.64 6,954.38 115.86 5,144.06 40.77 1,810.33 14.133 CHI 59.97 2,662.35 55.90 2,481.75 4.07 180.61 1.414 BAC 241.19 10,708.33 240.92 10,696.23 0.27 12.10 0.095 SOCIETE GEN 14.44 640.96 14.30 635.11 0.13 5.85 0.05

% to Total

Table XV - Net Commitments, Cumulative Availments and Undrawn Balance by Creditor(in million)

Undrawn BalanceCreditor

Net Commitments Cumulative Availments

Difference between totals and sum of components is due to rounding off

28

(Table XV, continued)

3.5.2 By Sector

The undrawn balance of commitments is shared by Infrastructure – P195.50 billion (US$4.40 billion) or 68.88 percent; Social Reform and Community Development – P59.15 billion (US$1.33 billion) or 20.84 percent; Agriculture, Agrarian Reform, Natural Resources and – P26.14 billion (US$0.59 billion) or 9.21 percent; Industry, Trade and Tourism – P2.79 billion (US$ 0.06 billion) or 0.98 percent and Governance and Institutions Development – P0.22 billion (US$5.04 million) or 0.08 percent. Chart XIII shows the undrawn balance of commitments by sector.

Presented in Table XVI is the details of net commitments, cumulative availments and undrawn balance of commitments by sector and by implementing agency.

USD PHP USD PHP USD PHP6 FP 36.16 1,605.50 36.16 1,605.47 0.00 0.03 0.00

7 ICO 21.62 959.99 21.62 959.98 0.00 0.02 0.00 8 RZOA 53.75 2,386.46 53.75 2,386.46 - - - 9 ERSTE 25.01 1,110.33 25.01 1,110.33 - - - 10 ECGD 155.91 6,921.89 155.91 6,921.89 - - - 11 EDC 122.18 5,424.50 122.18 5,424.50 - - - 12 ING Bank N.V. 20.10 892.19 20.10 892.19 - - -

13 Bancaja 7.01 311.42 7.01 311.42 - - -

14 FORTIS BANK 9.12 405.05 9.12 405.05 - - - 15 Banco Bilbao

Vizcaya 52.13 2,314.51 52.13 2,314.51 - - -

16 Credit Com'l de France

33.74 1,498.06 33.74 1,498.06 - - -

17 NDF 0.88 38.89 0.88 38.89 - - - 18 EFIC 14.08 625.02 14.08 625.02 - - - 19 ANZ/EFIC 24.91 1,106.08 24.91 1,106.08 - - - 20 Banco

Santander(SMCF-Spain)

25.75 1,143.42 25.75 1,143.42 - - -

21 Bank of America

6.19 274.99 6.19 274.99 - - -

22 Credit Agricole Indosuez

27.40 1,216.72 27.40 1,216.72 - - -

% to Total

Undrawn BalanceCreditor

Net Commitments Cumulative Availments

Difference between totals and sum of components is due to rounding off

Difference between totals and sum of components is due to

29

USD PHP USD PHP USD PHP

Total 29,682.13 1,317,827.41 23,289.72 1,034,017.06 6,392.41 283,810.35 100.00