2013 comd fertilizer_presentation

TRANSCRIPT

Global Fertilizer Market OutlookScotiabank Commodities Outlook Conference

Toronto, January 2013

Dr. Peter HarrissonConsultant, Fertilizers

: +44 207 903 2249: [email protected]

: www.crugroup.com

2

Presentation overview

Introduction to N, P & K markets

How do agricultural market interact with fertilizer markets?

Fertilizer affordability in India

Supply side response to high prices

Points to watch across N, P & K

Nutrient outlook in summary

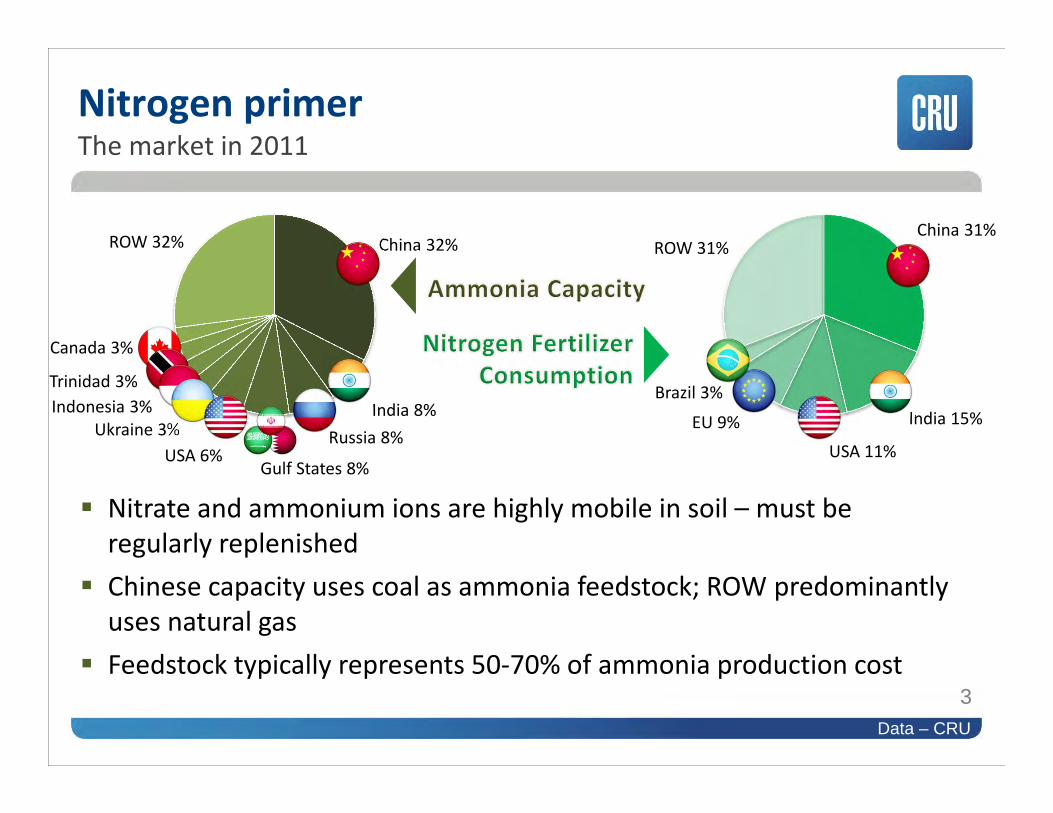

Nitrate and ammonium ions are highly mobile in soil – must be regularly replenished

Chinese capacity uses coal as ammonia feedstock; ROW predominantly uses natural gas

Feedstock typically represents 50‐70% of ammonia production cost

Nitrogen primerThe market in 2011

3

China 32%

India 8%

USA 6%Russia 8%

Indonesia 3%Ukraine 3%

Trinidad 3%

Canada 3%

Gulf States 8%

ROW 32% ROW 31%China 31%

India 15%

USA 11%EU 9%

Brazil 3%

Data – CRU

75% of identified phosphate rock reserves are in Morocco (IFDC 2011 estimate)

Producers may be vertically integrated or purchase phosphate rock and/or phosphoric acid

China and USA are largely self‐sufficient, India is major importer

Phosphate primerThe market in 2011

4

China 33%

USA 14%Morocco 15%Russia 5%

Tunisia 4%

Brazil 3%

China 30%

India 16%

USA 10%Brazil 9%

Saudi Arabia 3%

ROW 24% ROW 35%

Data – CRU

Cereals require less K than N & P, some crops like sugar cane and oil palm require high K

Little overlap between areas of high production and areas of high demand Canpotex and BPC handle 60‐70% of seaborne trade

Potash primerThe market in 2011

5

Canada 35%

Russia 17%Belarus 11%

USA 16%

Brazil 15%

China 19%

Germany 7%

Israel 6%

China 6%

Jordan 4%

India 8%EU 11%

Indonesia &Malaysia 9%

ROW 14%ROW 22%

Data – CRU

6million tonnes nutrient

0

5

10

15

20

N P K

0

5

10

15

20

N P K

0

5

10

15

20

N P K

0

5

10

15

20

N P K

0

10

20

30

40

50

N P K

Brazil

USA

Europe

India

China

China28%

India16%

USA12%

EU10%

Brazil6%

ROW28%

Total fertilizer demand by region

Fertilizer demand by region>70% fertilizer consumption is in China, India, USA, Europe and Brazil

Data – CRU

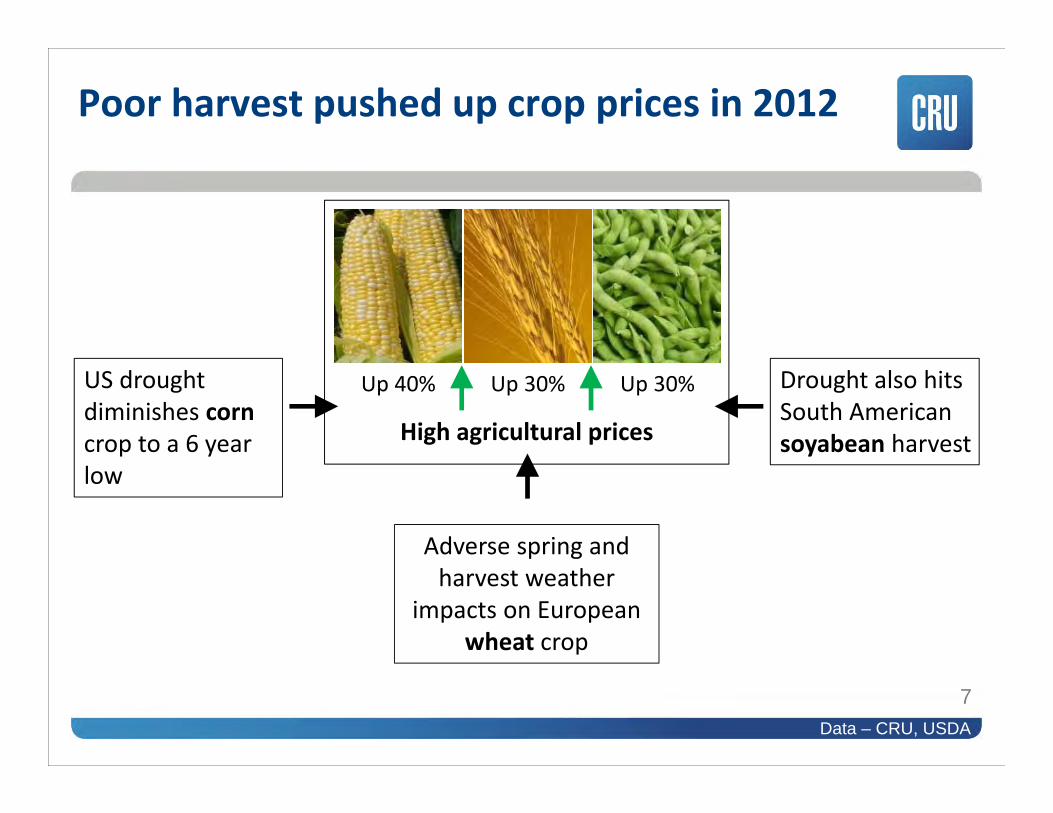

Poor harvest pushed up crop prices in 2012

7

US drought diminishes corn crop to a 6 year low

Drought also hits South American soyabean harvest

Adverse spring and harvest weather

impacts on European wheat crop

High agricultural prices

Up 40% Up 30% Up 30%

Data – CRU, USDA

8

United States2012 defined by drought

At the peak 80% of USA abnormally dry with >60% in drought

0

20

40

60

80

100

%

US drought area

Data – USDA

9

What is the impact on 2013? High corn plantings to trigger high application, particularly for N Increased crop areas expected to outweigh nutrient build up in soil

APPARENT DEMANDH1 2012 vs. H1 2011

Urea/Ammonia -2%

DAP -7%

MOP -28%

United States2012 defined by drought

01020304050607080

May Jun Jul Aug Sep Oct

%

Corn crop rating (% Good-Excellent)

2011 2012 5-yr ave

Data –CRU, USDA

10

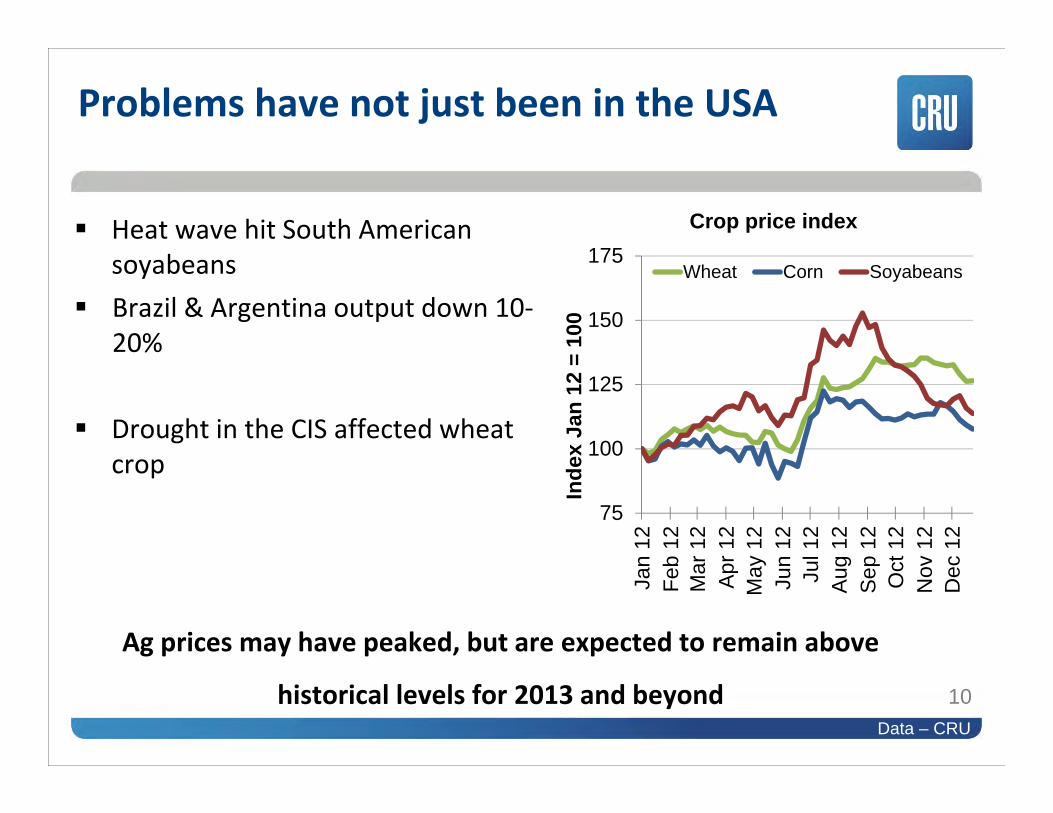

Heat wave hit South American soyabeans

Brazil & Argentina output down 10‐20%

Drought in the CIS affected wheat crop

Ag prices may have peaked, but are expected to remain above

historical levels for 2013 and beyond

Problems have not just been in the USA

75

100

125

150

175

Jan

12Fe

b 12

Mar

12

Apr

12

May

12

Jun

12Ju

l 12

Aug

12

Sep

12

Oct

12

Nov

12

Dec

12

Inde

x Ja

n 12

= 1

00

Crop price index

Wheat Corn Soyabeans

Data – CRU

50

100

150

200

250

300

350

400

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Jan

2006

= 1

00

Fertilizer Affordability Indices

Index of Crop Prices Index of Fertilizer Prices

Correlation 80%

2003-06 “normal” but balances tightening & prices trending up

Markets move to a new “normal”

Drought in the Americas

Fertilizer prices follow crop pricesHave crop and fertilizer markets moved to a new “normal”?

11Data – CRU

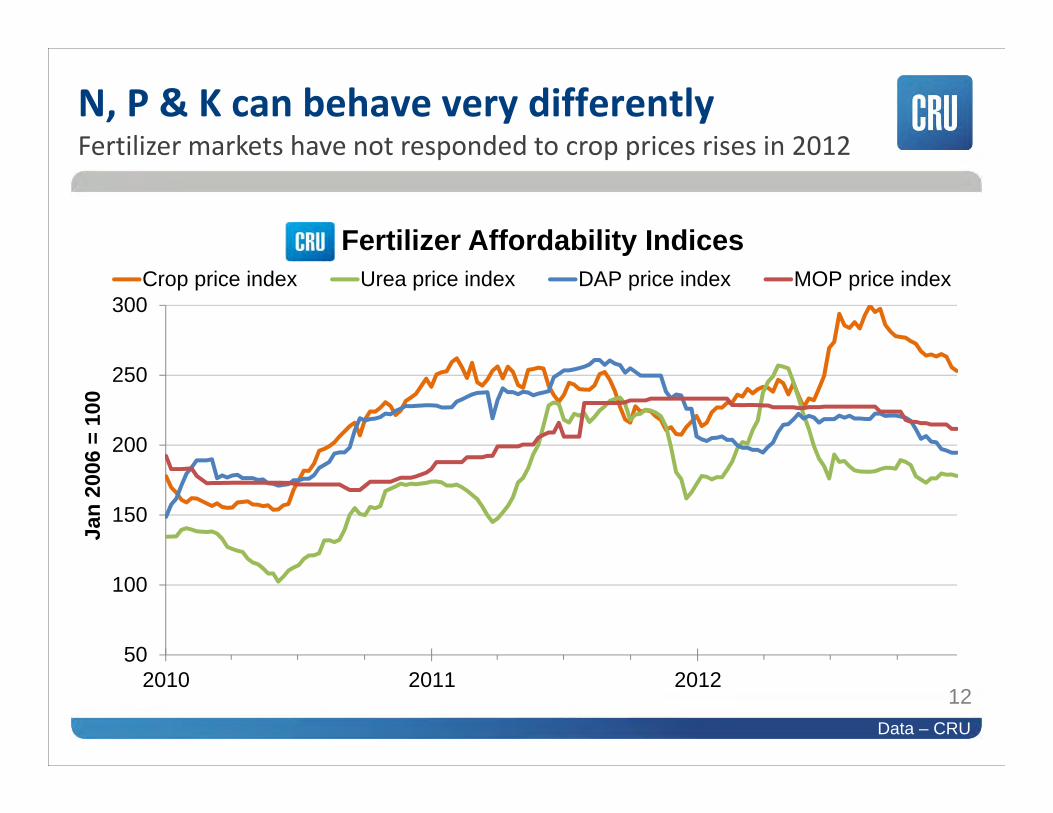

50

100

150

200

250

300

2010 2011 2012

Jan

2006

= 1

00

Fertilizer Affordability IndicesCrop price index Urea price index DAP price index MOP price index

12

N, P & K can behave very differentlyFertilizer markets have not responded to crop prices rises in 2012

Data – CRU

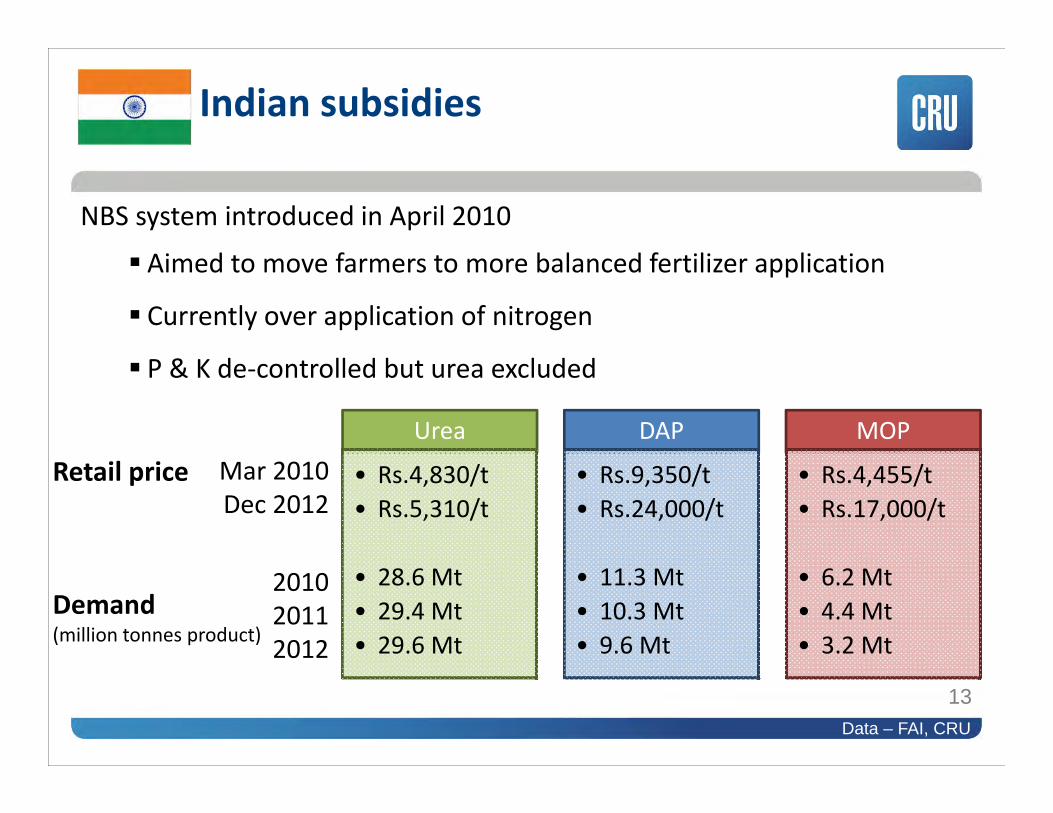

13

NBS system introduced in April 2010

Aimed to move farmers to more balanced fertilizer application

Currently over application of nitrogen

P & K de‐controlled but urea excluded

Urea

• Rs.4,830/t• Rs.5,310/t

• 28.6 Mt• 29.4 Mt• 29.6 Mt

DAP

• Rs.9,350/t• Rs.24,000/t

• 11.3 Mt• 10.3 Mt• 9.6 Mt

MOP

• Rs.4,455/t• Rs.17,000/t

• 6.2 Mt• 4.4 Mt• 3.2 Mt

201020112012

Mar 2010Dec 2012

Retail price

Demand(million tonnes product)

Indian subsidies

Data – FAI, CRU

14

What are the solutions? Lower import prices Higher or rebalanced government

subsidy Stronger Rupee

How much does the Indian farmer pay?What is the future for the subsidy regime?

What are the problems? P & K unaffordable in relation to N Farmers pushed towards buying

urea over DAP & MOP Reduced P & K application not

sustainable in the medium term

Urea DAP MOPIndia CFR

(December 2012) $400/t $580/t $490/t

Price to farmer(December 2012) $100/t $400/t $300/t

Data – CRU Fertilizer Week

50

52

54

56

58

60

2011 2012 2013 2014 2015

million tonn

es DAP

Existing China Saudi Arabia Morocco

15

150

160

170

180

190

200

210

220

230

2011 2012 2013 2014 2015

million tonn

es urea

Existing China MENA ROW

50

55

60

65

70

75

80

85

90

2011 2012 2013 2014 2015

million tonn

es KCl

Existing Canada Russia ROW

26%additional

capacity by 2015

53%share of new capacity in

Canada

MOPDAPUrea

28%additional

capacity by 2015

57%share of new capacity in

China

9%additional

capacity by 2015

Morocco

No net capacity

gain outside China, Saudi

Arabia & Morocco

Supply side response to high pricesCapacity addition greatest in N & K

Data – CRU

16

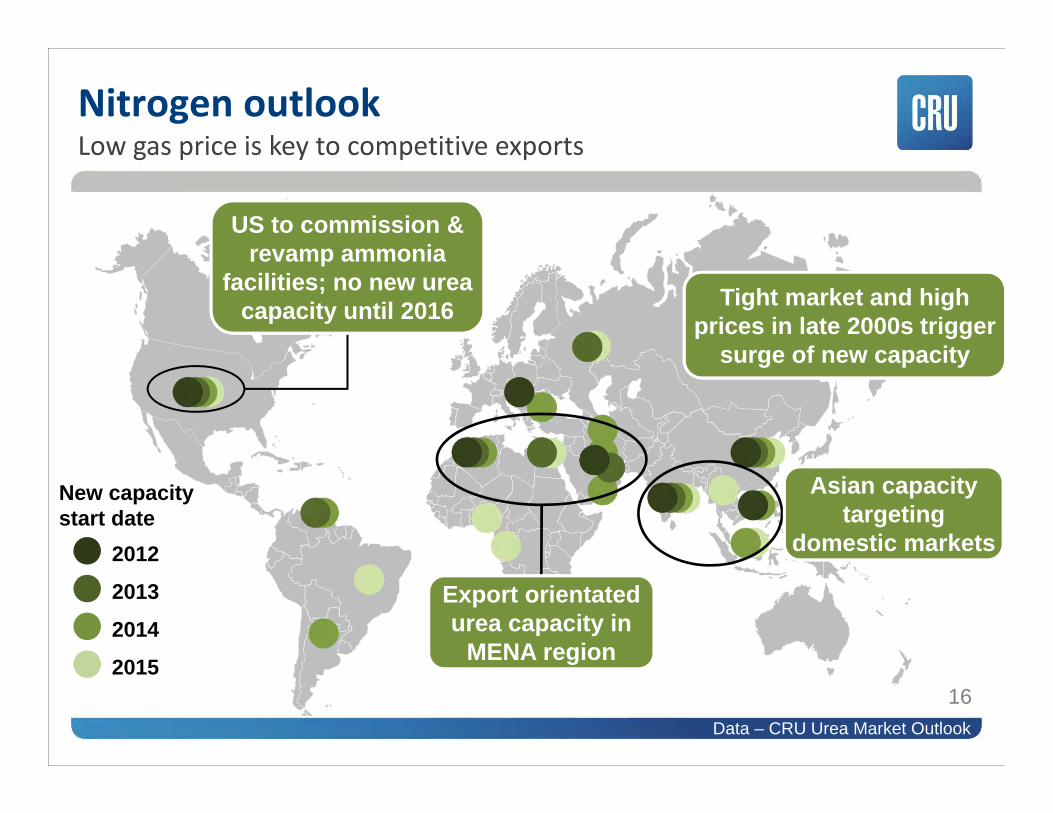

Nitrogen outlookLow gas price is key to competitive exports

2012

2013

2014

2015

Tight market and high prices in late 2000s trigger

surge of new capacity

US to commission & revamp ammonia

facilities; no new urea capacity until 2016

Export orientated urea capacity in

MENA region

Asian capacity targeting

domestic markets

New capacity start date

Data – CRU Urea Market Outlook

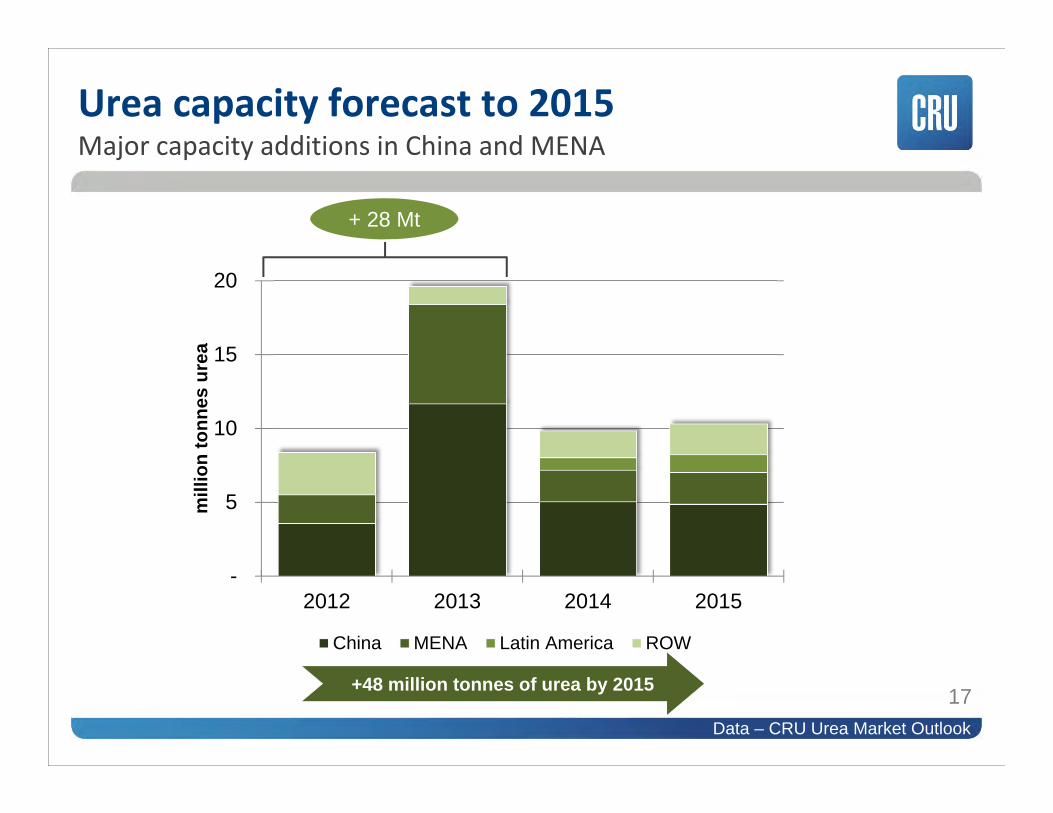

-

5

10

15

20

2012 2013 2014 2015

mill

ion

tonn

es u

rea

China MENA Latin America ROW

17+48 million tonnes of urea by 2015

+ 28 Mt

Urea capacity forecast to 2015Major capacity additions in China and MENA

Data – CRU Urea Market Outlook

18

List of Potential New ProjectsUS Import Dependence

15.8 Mtof major N fertilizers

importedin 2011

OCI / Iowa Fertilizer Company (IFCo) (2015)Summit’s Texas Clean Energy Project (TCEP) (2015)Ohio Valley Resources (OVR) (2016)CHS Inc (2017)JV between IFFCO, KIT, and a Canadian partner (2017)Dyno Nobel / Incitec Pivot (2018)

Rentech Nitrogen (2013)PCS (2014)CF Industries (2015)Yara (2016)

+ expansions and re‐starts

5.5 Mturea

US shale gas Can the US move towards Nitrogen self‐sufficiency?

3.0 million t/y N capacity added by 2015; 4.0 million t/y by 2017

Data – CRU Urea Market Outlook

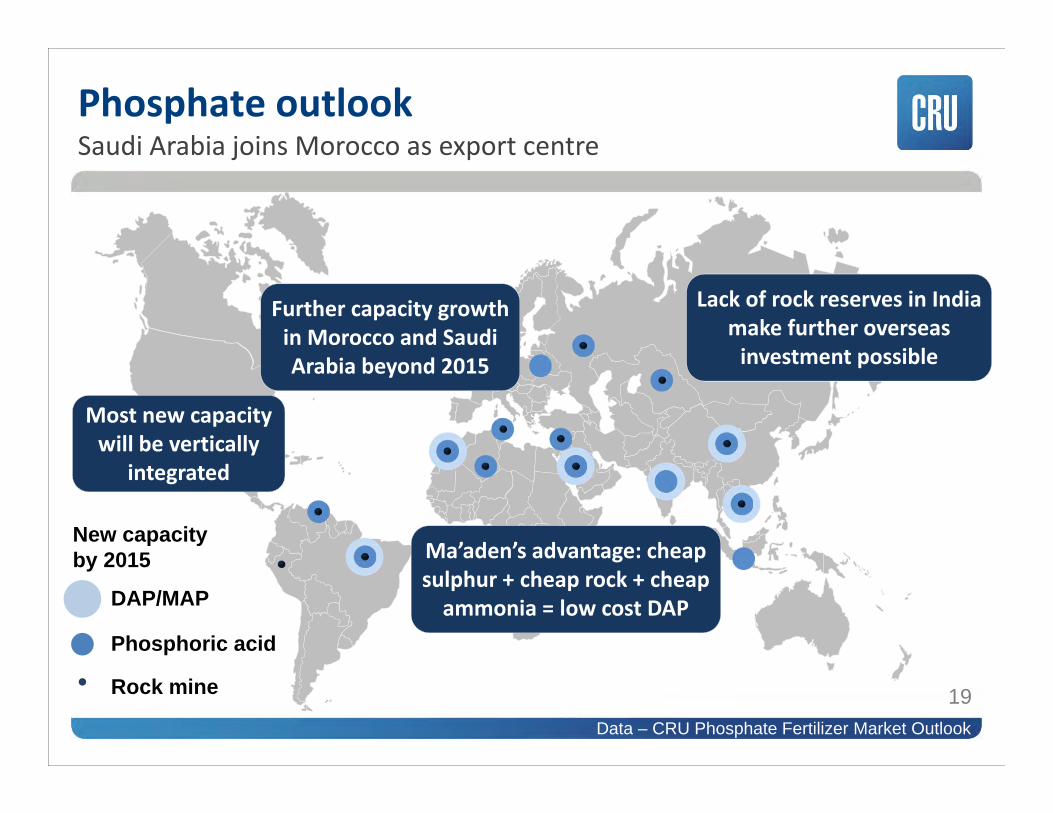

19

DAP/MAP

Phosphoric acid

Rock mine

New capacity by 2015

Phosphate outlookSaudi Arabia joins Morocco as export centre

Most new capacity will be vertically

integrated

Further capacity growth in Morocco and Saudi Arabia beyond 2015

Lack of rock reserves in India make further overseas investment possible

Ma’aden’s advantage: cheap sulphur + cheap rock + cheap ammonia = low cost DAP

Data – CRU Phosphate Fertilizer Market Outlook

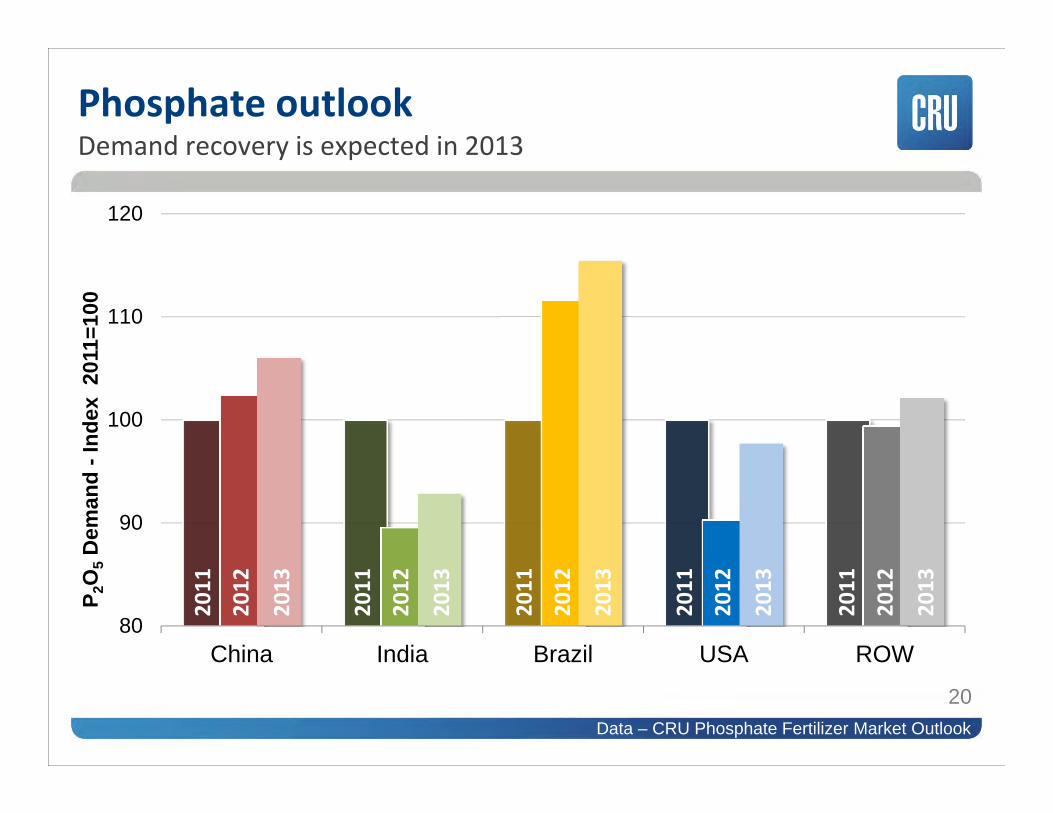

80

90

100

110

120

China India Brazil USA ROW

P 2O

5D

eman

d -I

ndex

201

1=10

0

20

Phosphate outlookDemand recovery is expected in 2013

2011

2012

2013

2011

2012

2013

2011

2012

2013

2011

2012

2013

2011

2012

2013

Data – CRU Phosphate Fertilizer Market Outlook

20

30

40

50

60

70

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

million tonn

es KCl

KCl deliveries

21

Potash outlookHigh prices have had a dampening effect on demand

no net growth

Data – CRU Potassium Chloride Market Outlook

22

Potash outlookHigh prices have had a dampening effect on demand

• Prices have fallen back which should aid demand

• China H1 2013 contract price down by $70/t to $400/t CFR

• Forecast is based on return to growth (agricultural requirements win out)

• Risk that prices will continue to depress growth e.g. India

20

30

40

50

60

70

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

million tonn

es KCl

KCl deliveries

no net growth

Data – CRU Potassium Chloride Market Outlook

23

50

60

70

80

90

2011 2012 2013 2014 2015

million tonn

es KCl

Existing Brownfield Greenfield

15% of additions are in greenfield

85% of additions are brownfield

Capacity forecast indicates extra 17million t/y capacity by 2015

Major greenfield projects are under construction with commissioning

after 2015

Potash outlookBrownfield capacity additions in the near term

Data – CRU Potassium Chloride Market Outlook

24

Cereals outlook is positive for N demandN : P/K ratios have risen amid volatile fertilizer prices

Major urea capacity additions in MENA & China High cost areas (e.g. Europe) to come under cost pressureGlobal operating rates projected to fall 86%75% Prices forecast to fall towards SRMC: Urea $350/t FOB Limited addition to ammonia capacity

Policy changes are a significant risk to the outlook China export tariffs Indian urea subsidy reform Indian embargo on Iranian exports

Nitrogen points to watch

25

Indian subsidy issues of major significance Largest global DAP importer Phosphoric acid contract to India agreed at $770/t CFR, down $85/t DAP price not yet agreed but recent spot sale at $535/t CFR India (Jan 2012) How far will demand recover in 2013?

Slower capacity growth than N & KOCP in powerful position – now joined by Ma’adenUS market supply stable but concerns over rock resources

Prices turning upwards in 2013 if India turns round

Phosphate points to watch

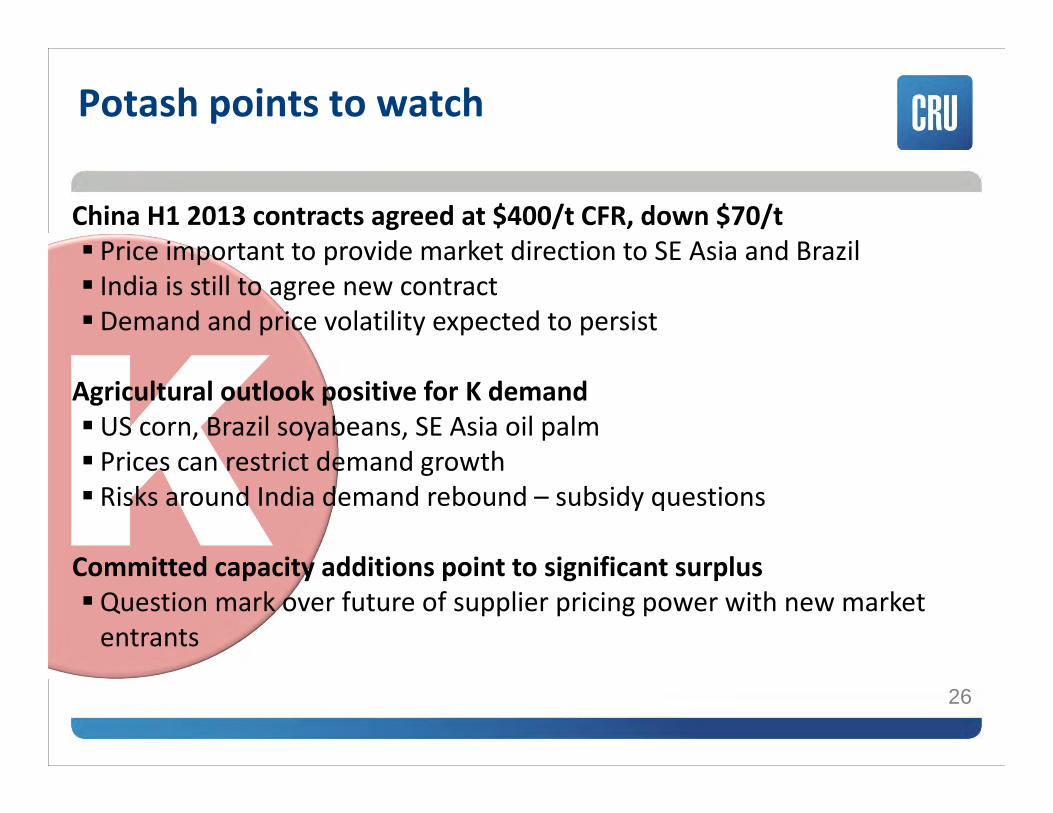

26

China H1 2013 contracts agreed at $400/t CFR, down $70/t Price important to provide market direction to SE Asia and Brazil India is still to agree new contract Demand and price volatility expected to persist

Agricultural outlook positive for K demandUS corn, Brazil soyabeans, SE Asia oil palm Prices can restrict demand growth Risks around India demand rebound – subsidy questions

Committed capacity additions point to significant surplusQuestion mark over future of supplier pricing power with new market entrants

Potash points to watch

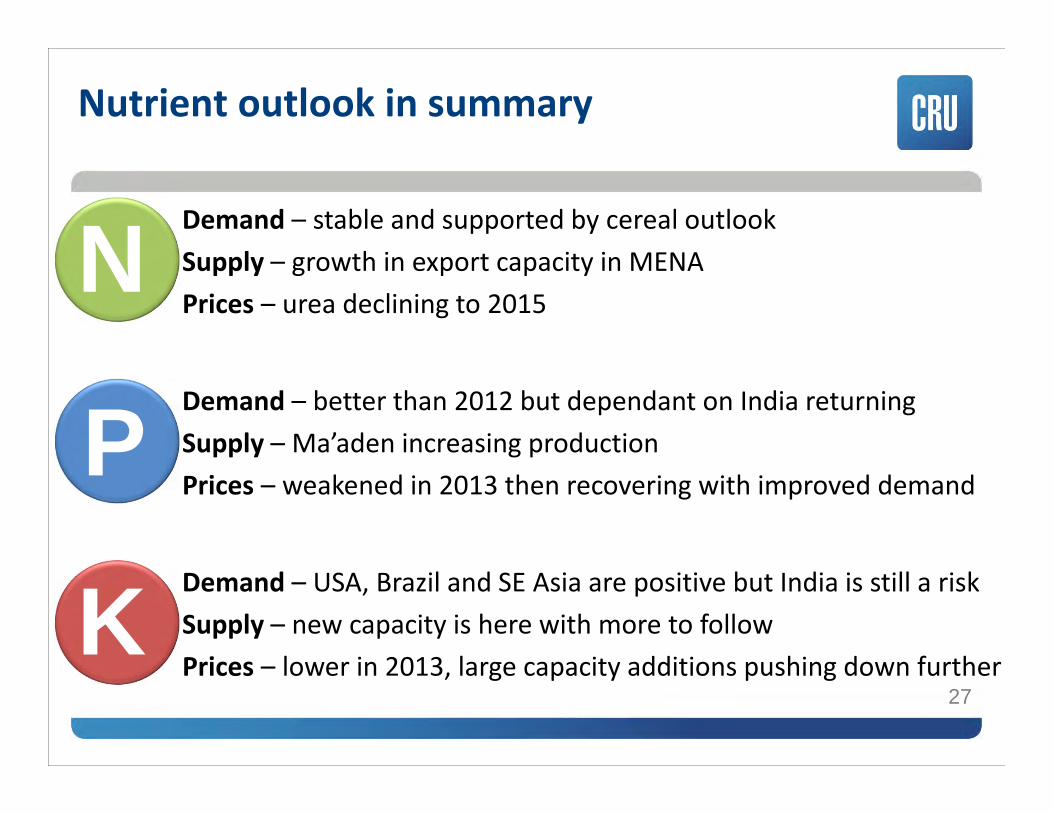

27

Demand – stable and supported by cereal outlookSupply – growth in export capacity in MENAPrices – urea declining to 2015

N

Demand – USA, Brazil and SE Asia are positive but India is still a riskSupply – new capacity is here with more to followPrices – lower in 2013, large capacity additions pushing down further

K

Demand – better than 2012 but dependant on India returningSupply – Ma’aden increasing productionPrices – weakened in 2013 then recovering with improved demand

P

Nutrient outlook in summary

28

MARKET OUTLOOK SERVICES Ammonia Urea Phosphate Rock Phosphate Fertilizer Potassium Chloride Sulphur Sulphuric Acid

Dr. Peter HarrissonConsultant, Fertilizers: +44 207 903 2249: [email protected]: www.crugroup.com

Thank you for your attention

COST SERVICES Nitrogen Fertilizers Potassium Chloride Phosphate Rock Phosphate Fertilizers

MULTI CLIENT SERVICES UAN Ammonium Nitrate Explosive grade ammonium nitrate Animal Feed Phosphates Potassium Sulphates/Nitrates